Languages

Pages

Legal

National & International Trade Outlook

Paul BinghamManaging Director, Global Commerce and TransportationIHS Global Insight

Cobb Galleria Center, Atlanta April 29, 2010

2010 GEORGIA LOGISTICS SUMMIT

Copyright © 2010 IHS Global Insight. All Rights Reserved.

2

Trade Demand Follows Recovery from Recession

• Trade demand recovery varies across a multi-speed world – Asia in the fast lane, Europe in the slow lane, and the U.S. in between

• Debt levels influence the speed and shape of the recovery by region and country, most visible now in Southern Europe

• Asia is increasing its role in generating global growth and this is evident in patterns of U.S. and world trade

• The long-term downward pressure on the dollar exchange rate remains, even as it appreciates against the euro in the near term

• Helps U.S. export competitiveness; dampens import demand

• Near-term U.S. trade recovery will moderate after inventories are rebuilt; long-term trade volumes still grow faster than the economy

Copyright © 2010 IHS Global Insight. All Rights Reserved.

3

-9

-6

-3

0

3

6

9

1974 1979 1984 1989 1994 1999 2004 2009 2014

Real GDP Industrial Production

(Percent change)

Trade volumes reflect goods production which is more volatile than the economy as a whole

Source: IHS Global Insight

Copyright © 2010 IHS Global Insight. All Rights Reserved.

4

-12

-8

-4

0

4

8

GDP PrivateConsumption

FixedInvestment

GovernmentConsumption

Exports

2009 2010 2011 2012

(Percent change in real value)

In World Economic Growth by Sector, Trade Fell the Most and Comes Back Strongest

Source: IHS Global Insight

Copyright © 2010 IHS Global Insight. All Rights Reserved.

5

-15

-10

-5

0

5

10

15

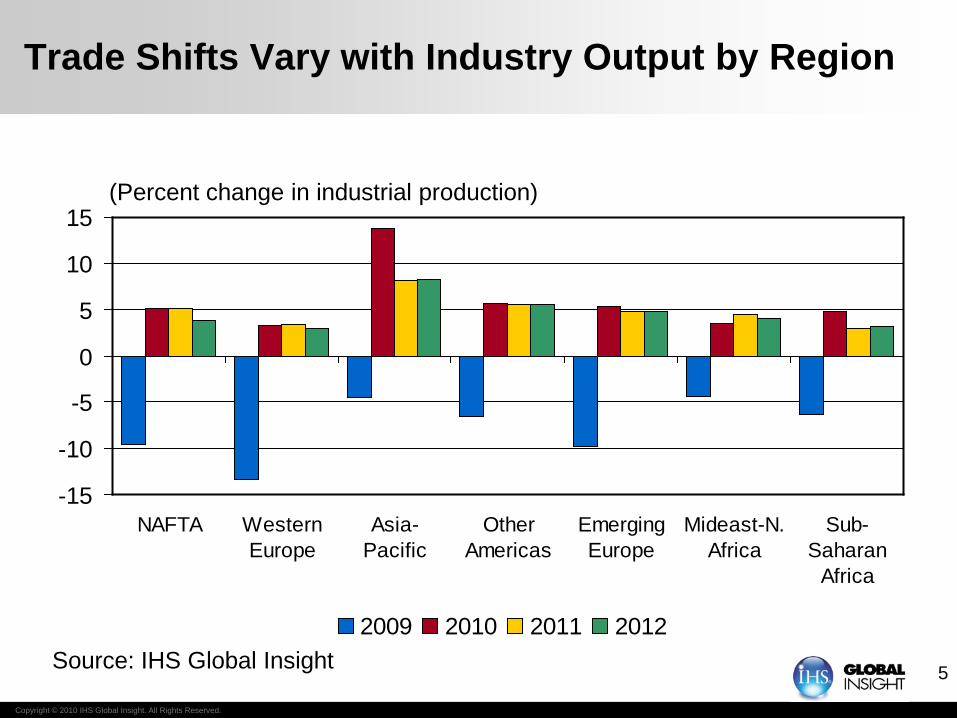

NAFTA WesternEurope

Asia-Pacific

OtherAmericas

EmergingEurope

Mideast-N.Africa

Sub-Saharan

Africa

2009 2010 2011 2012

(Percent change in industrial production)

Trade Shifts Vary with Industry Output by Region

Source: IHS Global Insight

Copyright © 2010 IHS Global Insight. All Rights Reserved.

6

Trade Recovery by Commodity is Not Uniform, as Stage of Recovery Varies By Industry Sector

• Manufacturing recovery best for Autos, Metals, Chemicals and Commodities

• Output won’t reach pre-recession levels for several years• High commodity prices challenge sectors that use them

• Strong recovery for Information, Technology and Communications, recovering to former levels and above

• Banking / Finance stabilizes in U.S. (2010) and Europe (2011), but recovery is affected by bad loans and de leveraging

• Commercial / consumer credit availability still constrained• Continued, though select, push for infrastructure supports

trade related to transportation, communications and utilities

• Construction and related trade faces disappointing markets

Copyright © 2010 IHS Global Insight. All Rights Reserved.

77

Global Merchandise Trade Recovers by Next Year

0

50

100

150

200

250

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Air Sea Land/Other

(Trillions of U.S. dollars)

Source: IHS Global Insight World Trade Service

Copyright © 2010 IHS Global Insight. All Rights Reserved.

8

The U.S. Recovery: Picking Up Steam

• Underlying 2010 U.S. GDP growth forecast near 3.0%

• Steep recoveries usually follow steep recessions, but recoveries after financial crises are usually slower

• Consumer spending growth faces the headwind of still-high unemployment, but spending is now the strongest in three years

• Business spending on equipment (and services) and inventory rebuilding are boosting growth, as seen in freight and trade

• Non-residential construction and state-and-local spending will be a drag on the recovery of the economy into 2011

• Housing construction will struggle to get off the bottom

• Excess capacity will restrain wage and price inflation

Copyright © 2010 IHS Global Insight. All Rights Reserved.

9

-8

-6

-4

-2

0

2

4

6

8

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 20123

4

5

6

7

8

9

10

11

Real GDP Growth (Left scale) Unemployment Rate (Right scale)

(Annual percent change) (Percent)

The U.S. Economic Recovery Advances

Source: IHS Global Insight

Copyright © 2010 IHS Global Insight. All Rights Reserved.

10

-10.0

-7.5

-5.0

-2.5

0.0

2.5

5.0

7.5

1990 1993 1996 1999 2002 2005 2008 2011 2014

U.S. Real GDP Industrial Production

(Percent change)

Industrial Production Outpaces Real GDP

Source: IHS Global Insight

Copyright © 2010 IHS Global Insight. All Rights Reserved.

11

Recovery Pace Varies by Business SizeCyclical Indicators Rising; Small Business Lagging

30

35

40

45

50

55

60

2007 2008 2009 201080828486889092949698100

ISM Manufacturing ISM Non-Manufacturing NFIB Small-Business

ISM Diffusion Indexes, 50 = breakeven NFIB Index,1986=100

Source: IHS Global Insight

Copyright © 2010 IHS Global Insight. All Rights Reserved.

12

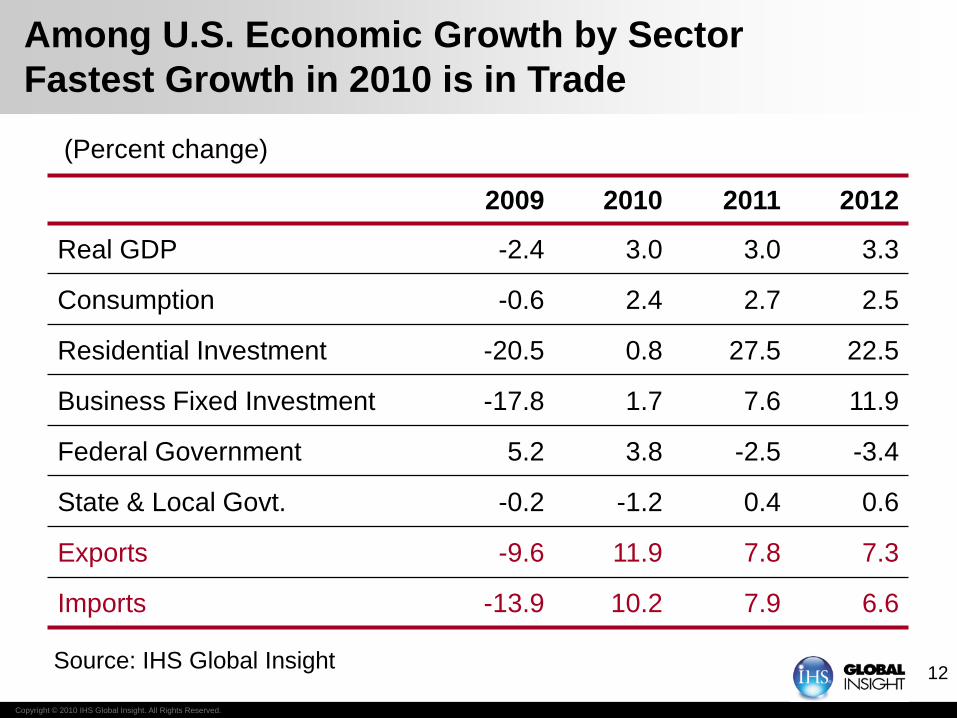

2009 2010 2011 2012

Real GDP -2.4 3.0 3.0 3.3

Consumption -0.6 2.4 2.7 2.5

Residential Investment -20.5 0.8 27.5 22.5

Business Fixed Investment -17.8 1.7 7.6 11.9

Federal Government 5.2 3.8 -2.5 -3.4

State & Local Govt. -0.2 -1.2 0.4 0.6

Exports -9.6 11.9 7.8 7.3

Imports -13.9 10.2 7.9 6.6

(Percent change)

Among U.S. Economic Growth by Sector Fastest Growth in 2010 is in Trade

Source: IHS Global Insight

Copyright © 2010 IHS Global Insight. All Rights Reserved.

13

-6-4

-20

24

68

10

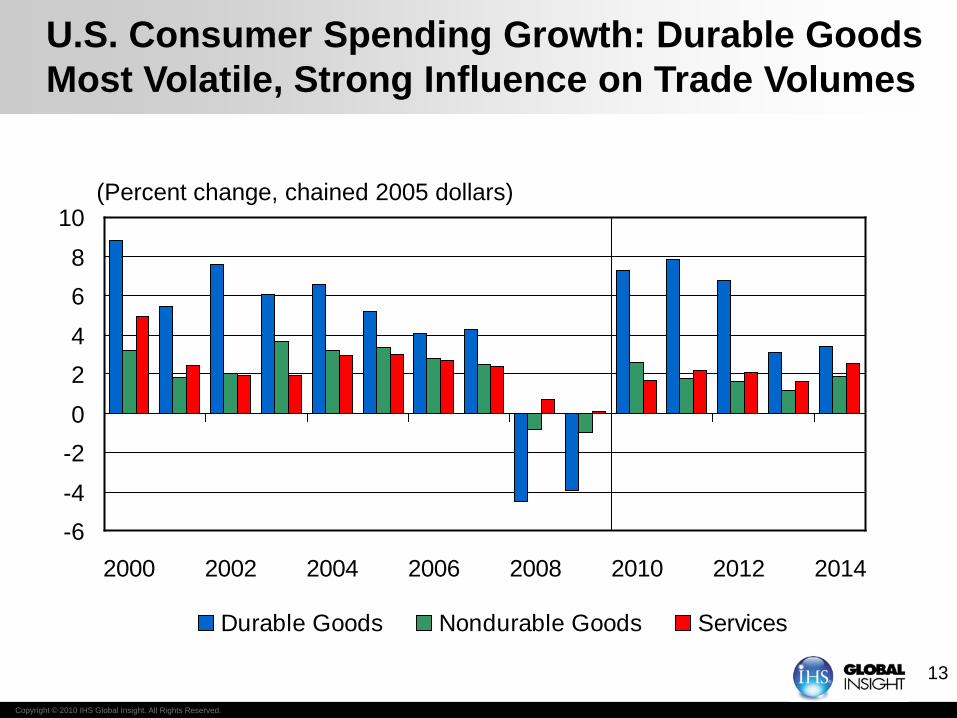

2000 2002 2004 2006 2008 2010 2012 2014

Durable Goods Nondurable Goods Services

(Percent change, chained 2005 dollars)

U.S. Consumer Spending Growth: Durable Goods Most Volatile, Strong Influence on Trade Volumes

Copyright © 2010 IHS Global Insight. All Rights Reserved.

14

(Percent change annualized rate, volumes)

Inventory Cycle Boosts U.S. Exports and Imports

-40

-30

-20

-10

0

10

20

30

2007 2008 2009 2010 2011 2012

Real U.S. Exports Real U.S. ImportsSource: IHS Global Insight

Copyright © 2010 IHS Global Insight. All Rights Reserved.

15

-8

-6

-4

-2

0

2

4

6

2008 2009 2010 2011 2012

GDP Final Sales

(Annualized real rate of growth in U.S., Q/Q, percent)

U.S. Inventory Cycle Led to the Q4 Growth Spurt

Source: IHS Global Insight

Copyright © 2010 IHS Global Insight. All Rights Reserved.

16

Recession Impacts on Logistics

Trade recession led to underutilized U.S. logistics system capacity across seaports, airports, terminals, railroads, trucking, warehousing and labor. Providers reduced deployed capacity where they could.

Consequences:

• Trade recovery faces capacity bottlenecks; vessel and air cargo capacity not back to pre-recession levels, despite size of idled equipment fleet.

• Freight captured by truck from intermodal rail during recession likely to shift back again, as rates and relative costs of trucking increase

• Still-improving intermodal rail service continues to capture line-haul long-distance trucking, reducing trucking average length of haul.

• Continued evolution of trade gateways from shipper demands and carriers optimizing operations and services

Top Related