Languages

Pages

Legal

Becoming Global Billionaires from Mainland China:Theory and Evidence

Kezhou Xiao

Department of EconomicsLondon School of Economics and Political Science (LSE)

This paper has been presented at LSE Work-in-Progress (London); Fudan University(Shanghai); Peking University (Beijing); Xi’an Jiaotong University (Xi’an); AMES 2019,

Xiamen University (Xia’men).

June 24, 2019

Kezhou Xiao (LSE) Billionaires June 24, 2019 1 / 64

Introduction

贫穷不是社会主义。致富光荣。[Translation: Poverty is not

socialism. To get rich is glorious.]

邓小平[Deng Xiaoping]

The true pacemakers of socialism were not the intellectuals or agi-

tators who preach it but the Vanderbilts, Carnegies and Rockfellers.

p.134, Capitalism, Socialism, and Democracy, Schumpeter [1942]

Kezhou Xiao (LSE) Billionaires June 24, 2019 2 / 64

Outline of the Presentation

Empirical Motivation: The Increase in the Numbers of BillionaireEntrepreneurs from Mainland ChinaA China Puzzle from the perspective of “extractive” institutions.My Research Question: How to reconcile between the two?

A China Puzzle:Becoming Global Billionaires in a Seemingly Extractive Institution.

Kezhou Xiao (LSE) Billionaires June 24, 2019 3 / 64

Becoming Global Billionaries from Mainland China

Stylized facts on China’s Emerging Global Billionaires (2003-2017, TheWorld’s Billionaires, Forbes):

Fact 1: China witnessed the largest increase in absolute numbers ofglobal billionairesFact 2: While China experienced the largest gains in the share ofglobal billionaires, United State saw its share drop from almost half toless than 30%Fact 3: While China witnessed the largest increase in the number oftop 100 global billionaires, United State remained dominant inabsolute numbers for the top 100 league.

Channelling the Incentives by Deng’s Reformist StrategyTo get rich is glorious. - Deng Xiaoping.

Kezhou Xiao (LSE) Billionaires June 24, 2019 4 / 64

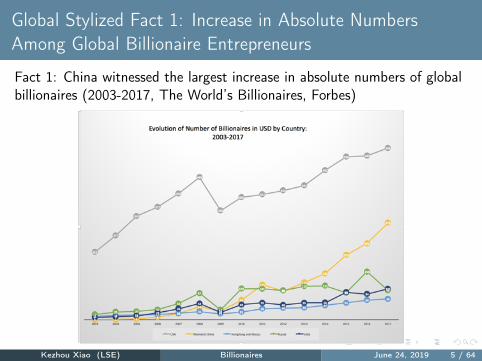

Global Stylized Fact 1: Increase in Absolute NumbersAmong Global Billionaire Entrepreneurs

Fact 1: China witnessed the largest increase in absolute numbers of globalbillionaires (2003-2017, The World’s Billionaires, Forbes)

Kezhou Xiao (LSE) Billionaires June 24, 2019 5 / 64

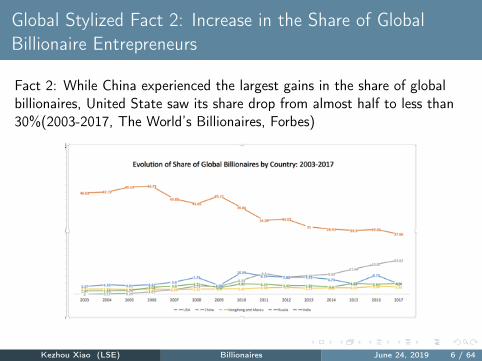

Global Stylized Fact 2: Increase in the Share of GlobalBillionaire Entrepreneurs

Fact 2: While China experienced the largest gains in the share of globalbillionaires, United State saw its share drop from almost half to less than30%(2003-2017, The World’s Billionaires, Forbes)

Kezhou Xiao (LSE) Billionaires June 24, 2019 6 / 64

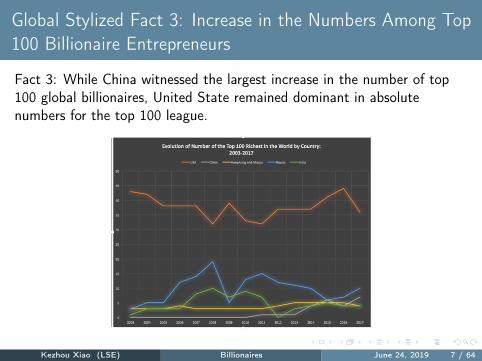

Global Stylized Fact 3: Increase in the Numbers Among Top100 Billionaire Entrepreneurs

Fact 3: While China witnessed the largest increase in the number of top100 global billionaires, United State remained dominant in absolutenumbers for the top 100 league.

Kezhou Xiao (LSE) Billionaires June 24, 2019 7 / 64

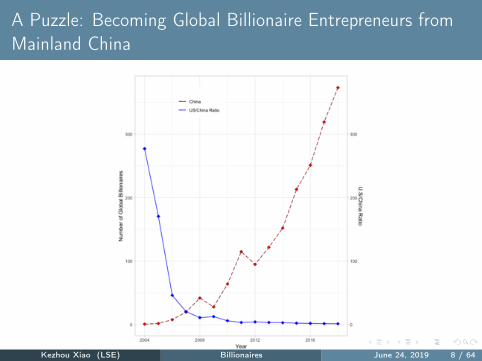

A Puzzle: Becoming Global Billionaire Entrepreneurs fromMainland China

Kezhou Xiao (LSE) Billionaires June 24, 2019 8 / 64

An Outline: Why is this Question So Important

Micro-agents of innovation and creative destruction [Schumpeter,1942]How do these entrepreneurs become global billionaires in a countryruled by a communist party?Evaluating latest theoretical framework: the problems with existingpolitical economy theories(a critique of Acemoglu and Robinson[2012])Construct a Unique Database: The World’s Billionaires, Forbes 2017& Hurun’s China Rich List, 2016, Orbis, company website, publiclyavailable info via a detailed codebook.Propose a Political Economy Framework in the spirit of Baumol [1990]Estimate an Empirical framework: A human equation approach

Kezhou Xiao (LSE) Billionaires June 24, 2019 9 / 64

The Grand Debate on China: Leading Academics versusLeading Self-made Billionaires

A China Puzzle: Becoming Global BillionairesHow to become global billionaires in a seemingly “extractive” institution?

Why nation fails: Extractive institutions cannot be compatible withsustained and innovation-based growth [Acemoglu and Robinson,2012]. Creative destruction should not be there at all!Self-made billionaire Jack Ma (Global Billionaire Ranking: 23, Forbes2017 Feb version, Net worth: 28.3 Billion USD), at Stanford Programon Regions of Innovation and Entrepreneurshiphttp://fsi.stanford.edu/news/jack_ma_ideas_and

_technology_can_change_the_world_20130506

Who is right? My take: Seek truth from facts. - Deng Xiaoping.

Kezhou Xiao (LSE) Billionaires June 24, 2019 10 / 64

The Grand Debate on China: Academics’ Sceptical Views

A China Puzzle: Becoming Global BillionairesHow to become global billionaires in a seemingly “extractive” institution?

...even though extractive institutions can generate some growth,

they will usually not generate sustained economic growth, and cer-

tainly not the type of growth that is accompanied by creative de-

struction. When both political and economic institutions are ex-

tractive, incentives will not be there for creative destruction and

technological change.

p.94, Why Nations Fail, Acemoglu and Robinson [2012]

Kezhou Xiao (LSE) Billionaires June 24, 2019 11 / 64

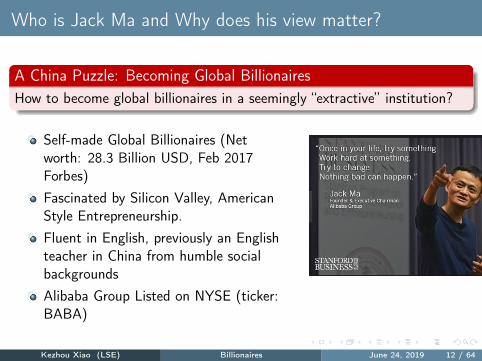

Who is Jack Ma and Why does his view matter?

A China Puzzle: Becoming Global BillionairesHow to become global billionaires in a seemingly “extractive” institution?

Self-made Global Billionaires (Networth: 28.3 Billion USD, Feb 2017Forbes)Fascinated by Silicon Valley, AmericanStyle Entrepreneurship.Fluent in English, previously an Englishteacher in China from humble socialbackgroundsAlibaba Group Listed on NYSE (ticker:BABA)

Kezhou Xiao (LSE) Billionaires June 24, 2019 12 / 64

Self-Made Billionaire Jack Ma’s Views

A China Puzzle: Becoming Global BillionairesHow to become global billionaires in a seemingly “extractive” institution?

...“change creates opportunities for ordinary people like you and

me”, noted Ma. The significant changes in China will offer young

people opportunities to shine as technology has leveled the playing

field.

...It is against this transformative context that Alibaba will continue

to stay true to its original mission — to make it easy to do business

anywhere in the world.

Transcript: Jack Ma’s speech at Stanford University on May

4, 2013, http: / / fsi .stanford .edu/ news/ jack _ma _ideas_and _technology _can _change _the _world _20130506

Kezhou Xiao (LSE) Billionaires June 24, 2019 13 / 64

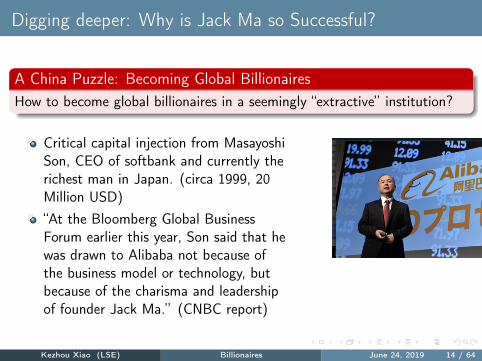

Digging deeper: Why is Jack Ma so Successful?

A China Puzzle: Becoming Global BillionairesHow to become global billionaires in a seemingly “extractive” institution?

Critical capital injection from MasayoshiSon, CEO of softbank and currently therichest man in Japan. (circa 1999, 20Million USD)“At the Bloomberg Global BusinessForum earlier this year, Son said that hewas drawn to Alibaba not because ofthe business model or technology, butbecause of the charisma and leadershipof founder Jack Ma.” (CNBC report)

Kezhou Xiao (LSE) Billionaires June 24, 2019 14 / 64

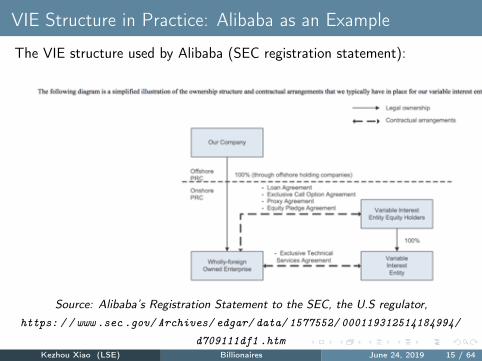

VIE Structure in Practice: Alibaba as an Example

The VIE structure used by Alibaba (SEC registration statement):

Source: Alibaba’s Registration Statement to the SEC, the U.S regulator,https: / / www .sec .gov/ Archives/ edgar/ data/ 1577552/ 000119312514184994/

d709111df1 .htmKezhou Xiao (LSE) Billionaires June 24, 2019 15 / 64

Playing Global Capitalism in a Communist Party-State: WhyOpen Economy Matters?

The Political Economy Solution for the Best Grassroot Enterpreneursin the Innovation Sector:The power of VIE structures: a marriage between indigenousentrepreneurship and global capital market!

Why VIE structures?Open up avenues for obtaining foreign financingBypassing tedious foreign operation and ownership regulations withinChinaAn ingenious financing vehicle to float outside China, mainly in the U.SBy listing on U.S markets, dual class stock (A and B type of stocks)can be issued. (e.g. Google/Alphabet, Facebook. etc all did it)!

Kezhou Xiao (LSE) Billionaires June 24, 2019 16 / 64

My Research Method: Following the Money and Inspectingthe Superstars

Research Question/Motivation at the Operational Level:Do global billionaires in China become rich via political connections (cronystate capitalism) or self-made in competitions (innovative capitalismcompeting in a global market)?

The research focus is to understand the impact of the social andpolitical background of these entrepreneurs on their first scoop of goldin the formative years and the choices of financing in later stages.Formative stage: How did they make their first scoop of gold?Financing/investment stage: How did they finance their investmentsto grow their enterprises to today’s level?

Kezhou Xiao (LSE) Billionaires June 24, 2019 17 / 64

The Grand Debate on China: My Contributions

A NEW Political Economy Model of Entrepreneurship in a GlobalEconomy in the spirt of Baumol [1990] (formalization of theframework)Compile a large database on an Emerging class of Global Billionnairesand Super Rich Entrepreneurs from China with a NEW conceputalframeworkSummary of their Companies, Entrepreneurship, and Social-politicalbackgrounds via a political economy of finance empirical equation à laBesley and Reynal-Querol [2011] (testing the framework)

My Position:Practise is the sole criteria for testing truth. - Deng Xiaoping.

Kezhou Xiao (LSE) Billionaires June 24, 2019 18 / 64

A Quick View of My Arguments and Results

This paper:(a) argues that the very existence of global billionaire entrepreneursfrom mainland China chairing some of the largest internet companiesin the world - Jack Ma (Alibaba), Pony Ma (Tencent), Robin Li(Baidu), William Ding (NetEase), Richard Liu (JD) and others -refutes Acemoglu and Robinson [2012](b) proposes a new political economy framework to study these globalbillionaire entrepreneurs in the spirit of Baumol [1990](c) estimates a human element equation à la Besley andReynal-Querol [2011] and find that (i) the politically unconnectedbillionaire entrepreneurs financed by foreign venture capitalists aremore likely to float their companies outside mainland China (mainly inHong Kong and the U.S), use offshore financing vehicles, and makeentries into the innovative sectors and (ii) the politically connectedglobal billionaire entrepreneurs, however, are strongly associated witha record of state-owned enterprise (SOE) restructuring.Kezhou Xiao (LSE) Billionaires June 24, 2019 19 / 64

Academic Literatures and My Research Project

My research project fits into many discussions in the literature:Political institutions and economic performance [Acemoglu andRobinson, 2012, Besley and Kudamatsu, 2008]The reward structure of entrepreneurs [Acemoglu, 1995, Baumolet al., 2007, Baumol, 1990]The role of political connections in resource misallocation, in particularfinancial resources [Faccio, 2006, Fisman, 2001, Rajan and Zingales,2003, Haber et al., 2008]Theories from financial economics [Myers, 1984, Holmström andTirole, 2001]The link between finance and economic growth [King and Levine,1993, Levine, 2005]Growing like China [Song et al., 2011]: My paper expands the insightsand findings by focusing on innovation!

Kezhou Xiao (LSE) Billionaires June 24, 2019 20 / 64

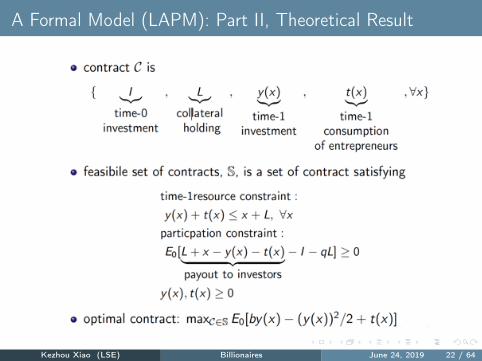

Formal Model: Part I

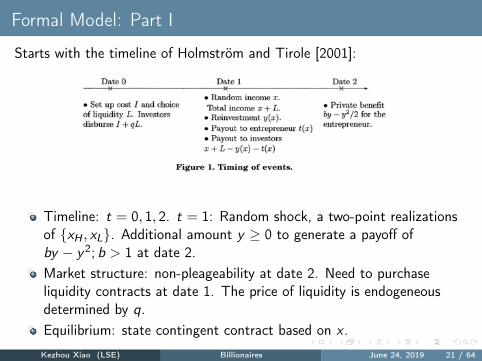

Starts with the timeline of Holmström and Tirole [2001]:

Timeline: t = 0, 1, 2. t = 1: Random shock, a two-point realizationsof {xH , xL}. Additional amount y ≥ 0 to generate a payoff ofby − y2; b > 1 at date 2.Market structure: non-pleageability at date 2. Need to purchaseliquidity contracts at date 1. The price of liquidity is endogeneousdetermined by q.Equilibrium: state contingent contract based on x .

Kezhou Xiao (LSE) Billionaires June 24, 2019 21 / 64

A Formal Model (LAPM): Part II, Theoretical Result

Kezhou Xiao (LSE) Billionaires June 24, 2019 22 / 64

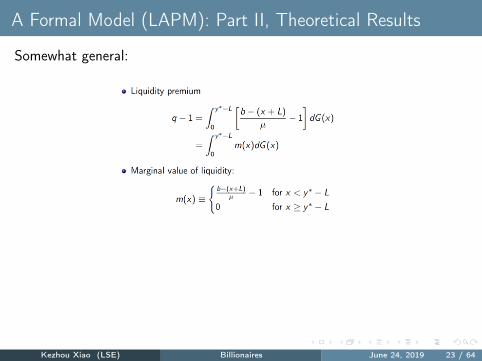

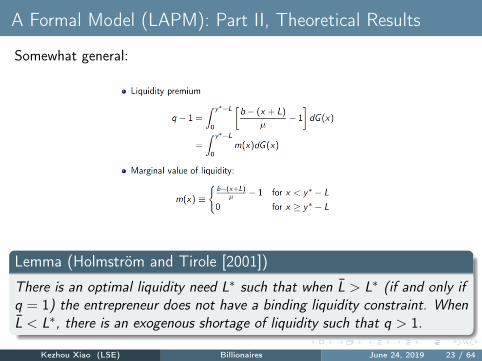

A Formal Model (LAPM): Part II, Theoretical Results

Somewhat general:

Lemma (Holmström and Tirole [2001])

There is an optimal liquidity need L∗ such that when L̄ > L∗ (if and only if

q = 1) the entrepreneur does not have a binding liquidity constraint. When

L̄ < L∗, there is an exogenous shortage of liquidity such that q > 1.

Kezhou Xiao (LSE) Billionaires June 24, 2019 23 / 64

A Formal Model (LAPM): Part II, Theoretical Results

Somewhat general:

Lemma (Holmström and Tirole [2001])

There is an optimal liquidity need L∗ such that when L̄ > L∗ (if and only if

q = 1) the entrepreneur does not have a binding liquidity constraint. When

L̄ < L∗, there is an exogenous shortage of liquidity such that q > 1.

Kezhou Xiao (LSE) Billionaires June 24, 2019 23 / 64

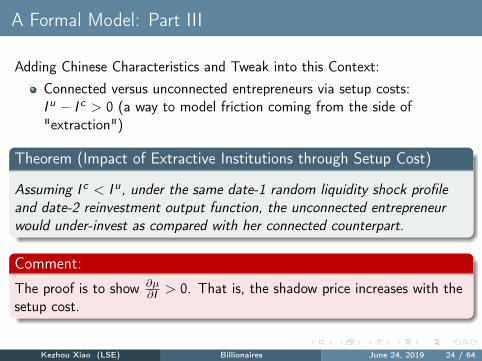

A Formal Model: Part III

Adding Chinese Characteristics and Tweak into this Context:Connected versus unconnected entrepreneurs via setup costs:I u − I c > 0 (a way to model friction coming from the side of"extraction")

Theorem (Impact of Extractive Institutions through Setup Cost)

Assuming I c < I u, under the same date-1 random liquidity shock profile

and date-2 reinvestment output function, the unconnected entrepreneur

would under-invest as compared with her connected counterpart.

Comment:

The proof is to show ∂µ∂I > 0. That is, the shadow price increases with the

setup cost.

Kezhou Xiao (LSE) Billionaires June 24, 2019 24 / 64

A Formal Model: Part IV

Adding Chinese Characteristics and Tweak into this Context:Assuming that all the agents in this economy try to solve itscontractual game with the state-owned banks acting in accordancewith an allocative policy in favor of the connected entrepreneurs.From this assumption and LAMP model, three possible outcomesemerge for the closed regime.In short, the grassroots suffer from both political economy andfinancial frictions.

Kezhou Xiao (LSE) Billionaires June 24, 2019 25 / 64

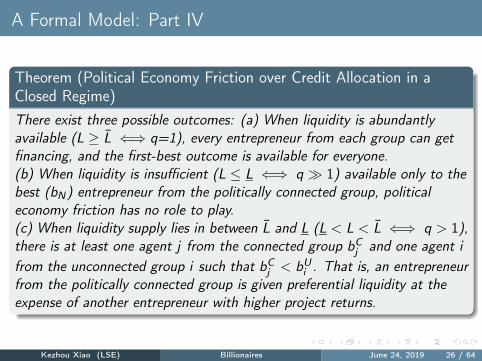

A Formal Model: Part IV

Theorem (Political Economy Friction over Credit Allocation in aClosed Regime)There exist three possible outcomes: (a) When liquidity is abundantly

available (L ≥ L̄ ⇐⇒ q=1), every entrepreneur from each group can get

financing, and the first-best outcome is available for everyone.

(b) When liquidity is insufficient (L ≤ L ⇐⇒ q ≫ 1) available only to the

best (bN) entrepreneur from the politically connected group, political

economy friction has no role to play.

(c) When liquidity supply lies in between L̄ and L (L < L < L̄ ⇐⇒ q > 1),

there is at least one agent j from the connected group bCj

and one agent i

from the unconnected group i such that bCj< bU

i. That is, an entrepreneur

from the politically connected group is given preferential liquidity at the

expense of another entrepreneur with higher project returns.

Kezhou Xiao (LSE) Billionaires June 24, 2019 26 / 64

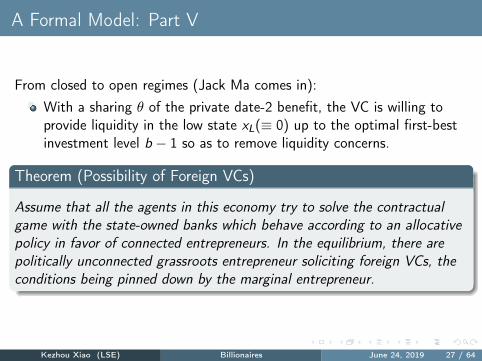

A Formal Model: Part V

From closed to open regimes (Jack Ma comes in):With a sharing θ of the private date-2 benefit, the VC is willing toprovide liquidity in the low state xL(≡ 0) up to the optimal first-bestinvestment level b − 1 so as to remove liquidity concerns.

Theorem (Possibility of Foreign VCs)

Assume that all the agents in this economy try to solve the contractual

game with the state-owned banks which behave according to an allocative

policy in favor of connected entrepreneurs. In the equilibrium, there are

politically unconnected grassroots entrepreneur soliciting foreign VCs, the

conditions being pinned down by the marginal entrepreneur.

Kezhou Xiao (LSE) Billionaires June 24, 2019 27 / 64

A Formal Model: Part V

From closed to open regimes (Jack Ma comes in):With a sharing θ of the private date-2 benefit, the VC is willing toprovide liquidity in the low state xL(≡ 0) up to the optimal first-bestinvestment level b − 1 so as to remove liquidity concerns.

Theorem (Possibility of Foreign VCs)

Assume that all the agents in this economy try to solve the contractual

game with the state-owned banks which behave according to an allocative

policy in favor of connected entrepreneurs. In the equilibrium, there are

politically unconnected grassroots entrepreneur soliciting foreign VCs, the

conditions being pinned down by the marginal entrepreneur.

Kezhou Xiao (LSE) Billionaires June 24, 2019 27 / 64

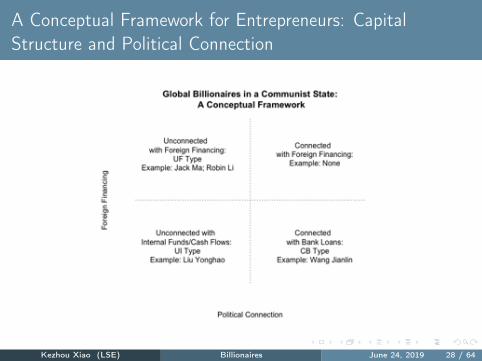

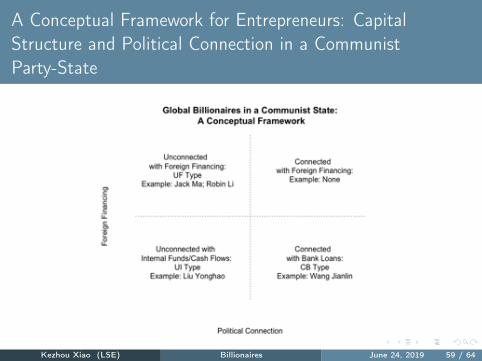

A Conceptual Framework for Entrepreneurs: CapitalStructure and Political Connection

Kezhou Xiao (LSE) Billionaires June 24, 2019 28 / 64

A Conceptual Framework for Billionaire Entrepreneurs:Political Connections and Capital Structure

Three Testing Hypothesis:H-1: The politically connected billionaire entrepreneurs are less likelyto solicit outside funding with their access to state-owned banks andless concerned about risk of expropriation. This type corresponds,more or less, to unproductive entrepreneurship (labelled as CB-type).H-2: The politically unconnected grassroots billionaires withoutsufficient degrees of foreign exposures are capable of financingthemselves via bootstrapping (E firms á la Song et al. [2011]). Thistype coincides with productive entrepreneurship (labelled as UI-type).H-3: The politically unconnected with some degrees of foreignexposures have a higher tendency of being financed by foreign VCsthrough an offshore entity so as to overcome liquidity need andattenuate political economy frictions. This type refers to destructiveentrepreneurship (labelled as UF-type).

Kezhou Xiao (LSE) Billionaires June 24, 2019 29 / 64

Orbis Database: Company Information

Orbis is the world’s mostpowerful comparable dataresource on private companiesNBER training manual:www.nber.org/data/

international-finance/

Sebnem.pdf

LSE Library accessEnglish Website:https://www.bvdinfo.com/

en-gb/our-products/data/

international/orbis

Kezhou Xiao (LSE) Billionaires June 24, 2019 30 / 64

Who is Hurun (胡润))?

Rupert Hoogewerf: British Businessmanand Publisher. Previously: worked atAndersen.Hurun (His Chinese name, character: 胡润) China Rich List, established in 1999.Chinese and Japanese, B.A, Durham,UK, 1993. Alumni of Eton. Diploma inRenmin University, Beijing, onMandarin.Along China Rich List: Also HurunPhilanthropy List and Art List.

Kezhou Xiao (LSE) Billionaires June 24, 2019 31 / 64

China’s Super Rich Class: Hurun 2016 China Rich List

2,056 Individuals.Approx: 300 Million USD threshold (2B RMB)Exclude: Hong Kong and MacauEnglish Website: http://www.hurun.net/EN/Home/Index

Started in 1999

Kezhou Xiao (LSE) Billionaires June 24, 2019 32 / 64

My Codebook: Hurun 2016 China Rich List and Forbes 2017

2,056 Individuals on Hurun China Rich List, 2016 and Forbes, 2017the World’s Billionaires (319).Company Info, Listing Info, Location, Industry, etc (company websiteresearch)Financing Decisions and Capital Structure: Foreign Financing throughventure capitalist? Offshore Vehicles? (Orbis, Global CompanyResearch Database)Social and Political Backgrounds: bios/interviews (public informationresearch)

Grand Quest:Are they rich via political connections (crony state capitalism) or self-madein competitions (innovative capitalism competing in a global market)?

Kezhou Xiao (LSE) Billionaires June 24, 2019 33 / 64

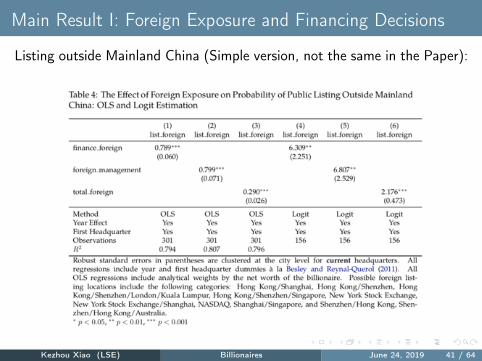

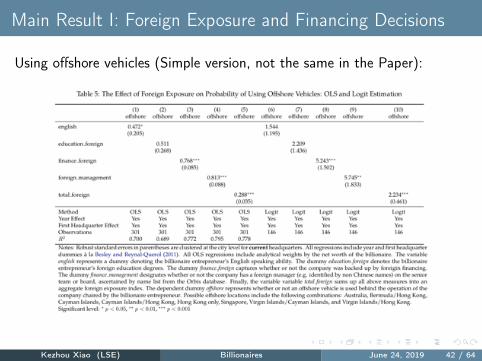

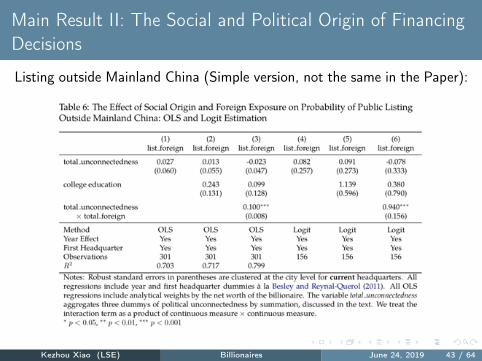

Key Dependent Variable: Financing Decisions D

Listing outside mainland China. Possible foreign listing locationsinclude the following categories: Hong Kong/Shanghai, HongKong/Shenzhen, Hong Kong/Shenzhen/London/Kuala Lumpur, HongKong/Shenzhen/Singapore, New York Stock Exchange, New YorkStock Exchange/Shanghai, NASDAQ, Shanghai/Singapore,Shenzhen/Hong Kong, and Shenzhen/Hong Kong/Australia.Using offshore vehicles. Possible offshore locations include thefollowing combinations: Australia, Bermuda/Hong Kong, CaymanIslands, Cayman Islands/Hong Kong, Hong Kong only, Singapore,Virgin Islands/Cayman Islands, and Virgin Islands/Hong Kong.An incidence of state-owned enterprise (SOE) restructuringAn entry of Technology, Media, and Telecom (TMT) industry

Kezhou Xiao (LSE) Billionaires June 24, 2019 34 / 64

Key Independent Variable: Foreign Element F

English speaking dummy.Foreign education dummy.An incidence of foreign financing dummy. Backed by foreign VCs- critical factor.An occurance of non-Chinese names in senior management orboardTotal_foreign: aggregate all four measures above. Max: 4. Min: 0.

Kezhou Xiao (LSE) Billionaires June 24, 2019 35 / 64

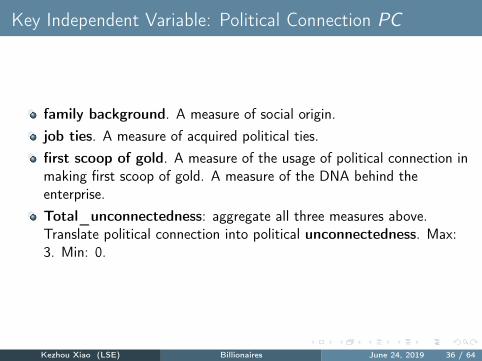

Key Independent Variable: Political Connection PC

family background. A measure of social origin.job ties. A measure of acquired political ties.first scoop of gold. A measure of the usage of political connection inmaking first scoop of gold. A measure of the DNA behind theenterprise.Total_unconnectedness: aggregate all three measures above.Translate political connection into political unconnectedness. Max:3. Min: 0.

Kezhou Xiao (LSE) Billionaires June 24, 2019 36 / 64

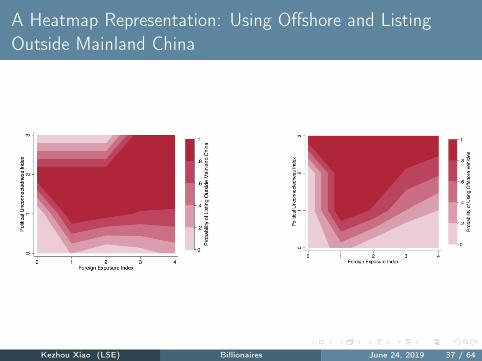

A Heatmap Representation: Using Offshore and ListingOutside Mainland China

Kezhou Xiao (LSE) Billionaires June 24, 2019 37 / 64

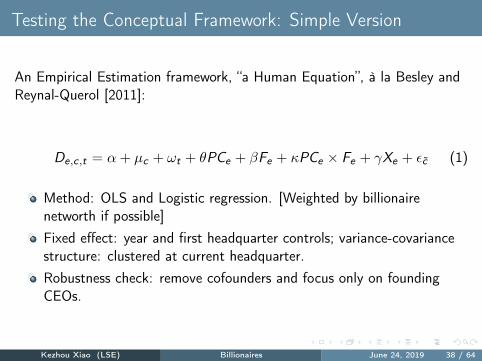

Testing the Conceptual Framework: Simple Version

An Empirical Estimation framework, “a Human Equation”, à la Besley andReynal-Querol [2011]:

De,c,t = α+ µc + ωt + θPCe + βFe + κPCe × Fe + γXe + 'c̃ (1)

Method: OLS and Logistic regression. [Weighted by billionairenetworth if possible]Fixed effect: year and first headquarter controls; variance-covariancestructure: clustered at current headquarter.Robustness check: remove cofounders and focus only on foundingCEOs.

Kezhou Xiao (LSE) Billionaires June 24, 2019 38 / 64

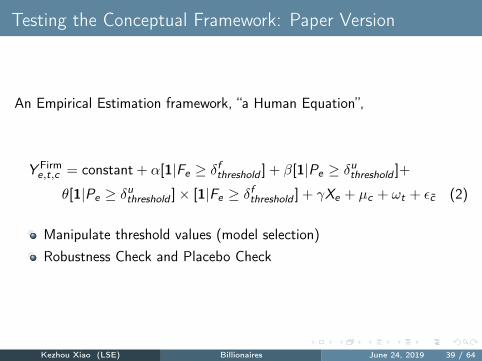

Testing the Conceptual Framework: Paper Version

An Empirical Estimation framework, “a Human Equation”,

Y Firme,t,c = constant + α[1|Fe ≥ δf

threshold] + β[1|Pe ≥ δu

threshold]+

θ[1|Pe ≥ δuthreshold

]× [1|Fe ≥ δfthreshold

] + γXe + µc + ωt + 'c̃ (2)

Manipulate threshold values (model selection)Robustness Check and Placebo Check

Kezhou Xiao (LSE) Billionaires June 24, 2019 39 / 64

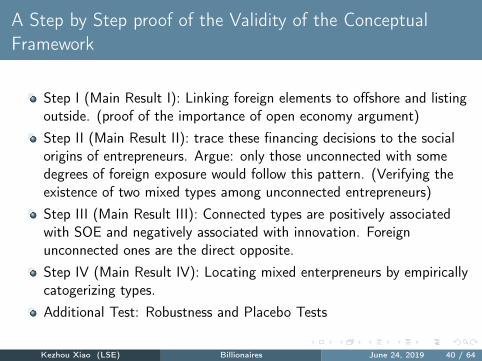

A Step by Step proof of the Validity of the ConceptualFramework

Step I (Main Result I): Linking foreign elements to offshore and listingoutside. (proof of the importance of open economy argument)Step II (Main Result II): trace these financing decisions to the socialorigins of entrepreneurs. Argue: only those unconnected with somedegrees of foreign exposure would follow this pattern. (Verifying theexistence of two mixed types among unconnected entrepreneurs)Step III (Main Result III): Connected types are positively associatedwith SOE and negatively associated with innovation. Foreignunconnected ones are the direct opposite.Step IV (Main Result IV): Locating mixed enterpreneurs by empiricallycatogerizing types.Additional Test: Robustness and Placebo Tests

Kezhou Xiao (LSE) Billionaires June 24, 2019 40 / 64

Main Result I: Foreign Exposure and Financing Decisions

Listing outside Mainland China (Simple version, not the same in the Paper):

Kezhou Xiao (LSE) Billionaires June 24, 2019 41 / 64

Main Result I: Foreign Exposure and Financing Decisions

Using offshore vehicles (Simple version, not the same in the Paper):

Kezhou Xiao (LSE) Billionaires June 24, 2019 42 / 64

Main Result II: The Social and Political Origin of FinancingDecisions

Listing outside Mainland China (Simple version, not the same in the Paper):

Kezhou Xiao (LSE) Billionaires June 24, 2019 43 / 64

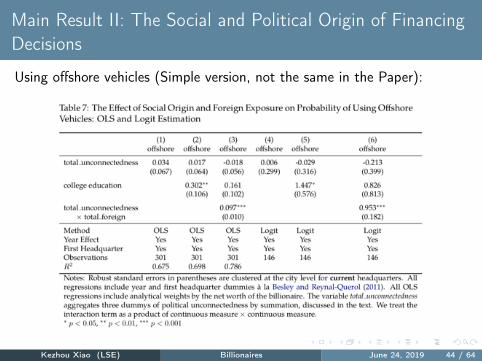

Main Result II: The Social and Political Origin of FinancingDecisions

Using offshore vehicles (Simple version, not the same in the Paper):

Kezhou Xiao (LSE) Billionaires June 24, 2019 44 / 64

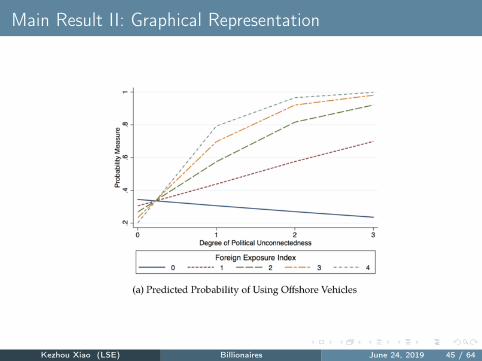

Main Result II: Graphical Representation

Kezhou Xiao (LSE) Billionaires June 24, 2019 45 / 64

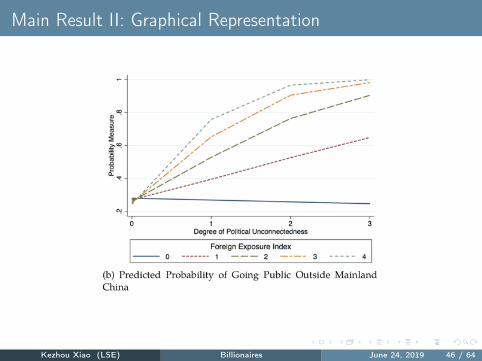

Main Result II: Graphical Representation

Kezhou Xiao (LSE) Billionaires June 24, 2019 46 / 64

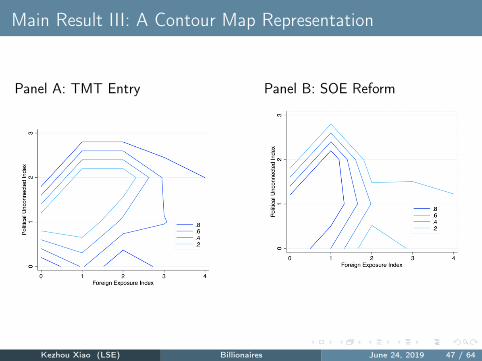

Main Result III: A Contour Map Representation

Panel A: TMT Entry Panel B: SOE Reform

Kezhou Xiao (LSE) Billionaires June 24, 2019 47 / 64

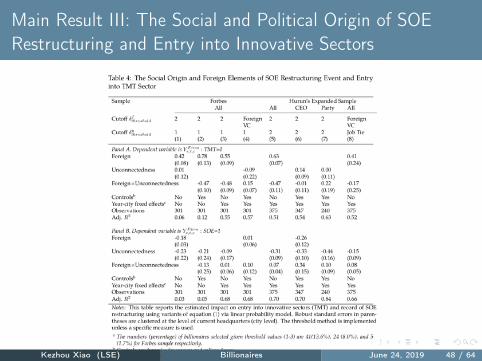

Main Result III: The Social and Political Origin of SOERestructuring and Entry into Innovative Sectors

Kezhou Xiao (LSE) Billionaires June 24, 2019 48 / 64

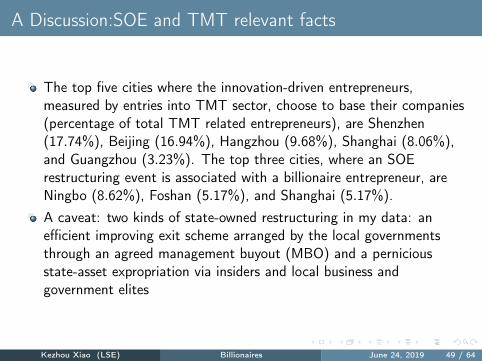

A Discussion:SOE and TMT relevant facts

The top five cities where the innovation-driven entrepreneurs,measured by entries into TMT sector, choose to base their companies(percentage of total TMT related entrepreneurs), are Shenzhen(17.74%), Beijing (16.94%), Hangzhou (9.68%), Shanghai (8.06%),and Guangzhou (3.23%). The top three cities, where an SOErestructuring event is associated with a billionaire entrepreneur, areNingbo (8.62%), Foshan (5.17%), and Shanghai (5.17%).A caveat: two kinds of state-owned restructuring in my data: anefficient improving exit scheme arranged by the local governmentsthrough an agreed management buyout (MBO) and a perniciousstate-asset expropriation via insiders and local business andgovernment elites

Kezhou Xiao (LSE) Billionaires June 24, 2019 49 / 64

Joseph Schumpeter, C. Wright Mills and William Baumol

That is one of the errors in Schumpeter’s idea of the ‘gale of

innovations’: he systemmatically confuses technological gain with

financial manipulation.

p.96, the Power Elite, Mills [1956/2000]

More important for the discussion here, Schumpeter’s list of en-

trepreneurial activities can usefully be expanded to include such

items as innovation in rent-seeking procedures . . .

Entrepreneurship: Productive, Unproductive, and Destructive,

Baumol [1990]

Kezhou Xiao (LSE) Billionaires June 24, 2019 50 / 64

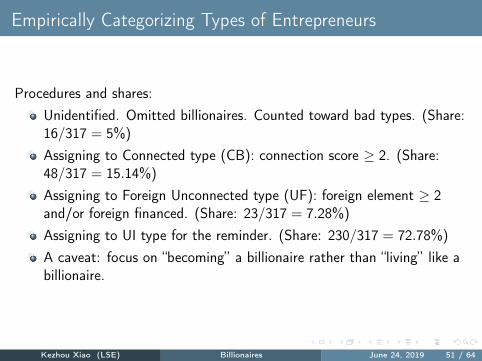

Empirically Categorizing Types of Entrepreneurs

Procedures and shares:Unidentified. Omitted billionaires. Counted toward bad types. (Share:16/317 = 5%)Assigning to Connected type (CB): connection score ≥ 2. (Share:48/317 = 15.14%)Assigning to Foreign Unconnected type (UF): foreign element ≥ 2and/or foreign financed. (Share: 23/317 = 7.28%)Assigning to UI type for the reminder. (Share: 230/317 = 72.78%)A caveat: focus on “becoming” a billionaire rather than “living” like abillionaire.

Kezhou Xiao (LSE) Billionaires June 24, 2019 51 / 64

Locating Mixed Entrepreneurship in a CommunistParty-State

Kezhou Xiao (LSE) Billionaires June 24, 2019 52 / 64

Robustness Check

A distributional test (K-S test).A check on the impact of party organA permutation and non-parametric test.

Kezhou Xiao (LSE) Billionaires June 24, 2019 53 / 64

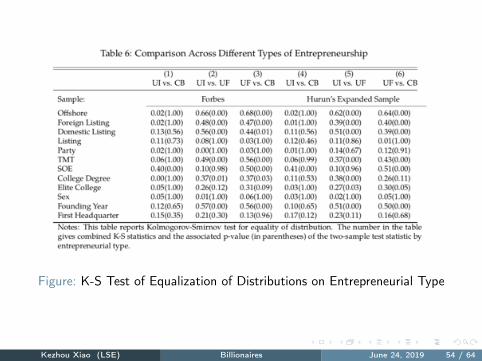

Figure: K-S Test of Equalization of Distributions on Entrepreneurial Type

Kezhou Xiao (LSE) Billionaires June 24, 2019 54 / 64

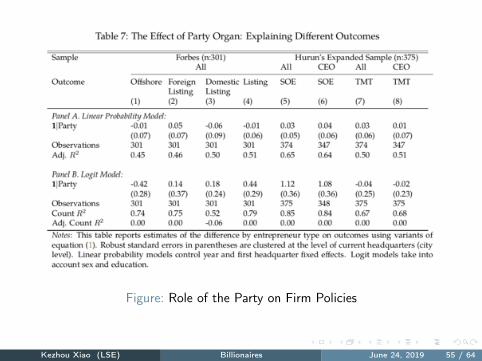

Figure: Role of the Party on Firm Policies

Kezhou Xiao (LSE) Billionaires June 24, 2019 55 / 64

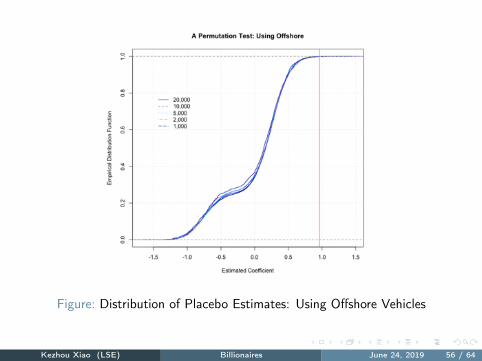

Figure: Distribution of Placebo Estimates: Using Offshore Vehicles

Kezhou Xiao (LSE) Billionaires June 24, 2019 56 / 64

The Limitations of Extractive/Inclusive InstitutionsArgument

A penetrating critique/stab on Acemoglu and Robinson [2012]:Institutions do matter. But these are NOT everything. Institutionsshape incentive structures in which human agents dance, play, andsuffer.Theories of human agency without institutions, on the other hand, aretautological. (Smart, you get rich; stupid, you suck.)The only way to get out of this is have a bridge, the sociologicalimagination, between human agency and institutional framework,highlighting the significance of “creative response” [Schumpeter, 1947]within existing institutions.My paper exemplifies such an attempt: despite inefficient institutionsand financial undevelopment, Jack Ma and others are capable ofpresenting multiple creative responses and make themselves billionairesin this century. (the essence of entrepreneurship)

Kezhou Xiao (LSE) Billionaires June 24, 2019 57 / 64

Three Short Personal Biographies in the Making of aBillionaire History: A Sociological Imagination via OurConceptual Framework

The sociological imagination enables us to grasp history and biog-

raphy and the relation between the two within society. That is its

task and its promise.

p.6, the Sociological Imagination, Mills [1959/2000]

Kezhou Xiao (LSE) Billionaires June 24, 2019 58 / 64

A Conceptual Framework for Entrepreneurs: CapitalStructure and Political Connection in a CommunistParty-State

Kezhou Xiao (LSE) Billionaires June 24, 2019 59 / 64

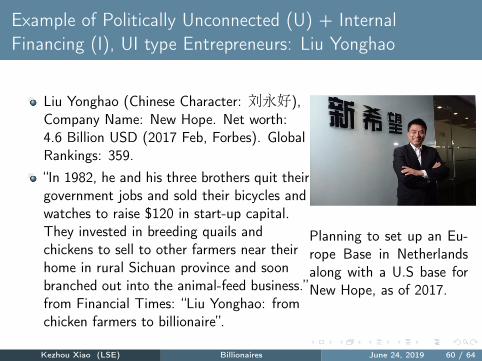

Example of Politically Unconnected (U) + InternalFinancing (I), UI type Entrepreneurs: Liu Yonghao

Liu Yonghao (Chinese Character: 刘永好),Company Name: New Hope. Net worth:4.6 Billion USD (2017 Feb, Forbes). GlobalRankings: 359.“In 1982, he and his three brothers quit theirgovernment jobs and sold their bicycles andwatches to raise $120 in start-up capital.They invested in breeding quails andchickens to sell to other farmers near theirhome in rural Sichuan province and soonbranched out into the animal-feed business.”from Financial Times: “Liu Yonghao: fromchicken farmers to billionaire”.

Planning to set up an Eu-rope Base in Netherlandsalong with a U.S base forNew Hope, as of 2017.

Kezhou Xiao (LSE) Billionaires June 24, 2019 60 / 64

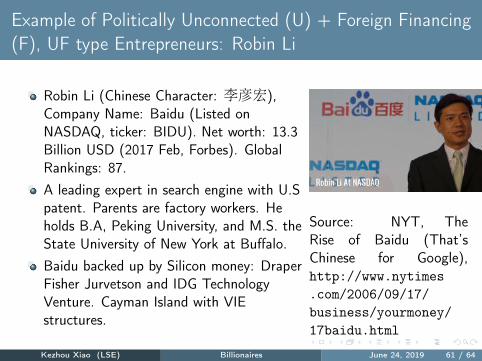

Example of Politically Unconnected (U) + Foreign Financing(F), UF type Entrepreneurs: Robin Li

Robin Li (Chinese Character: 李彦宏),Company Name: Baidu (Listed onNASDAQ, ticker: BIDU). Net worth: 13.3Billion USD (2017 Feb, Forbes). GlobalRankings: 87.A leading expert in search engine with U.Spatent. Parents are factory workers. Heholds B.A, Peking University, and M.S. theState University of New York at Buffalo.Baidu backed up by Silicon money: DraperFisher Jurvetson and IDG TechnologyVenture. Cayman Island with VIEstructures.

Source: NYT, TheRise of Baidu (That’sChinese for Google),http://www.nytimes

.com/2006/09/17/

business/yourmoney/

17baidu.html

Kezhou Xiao (LSE) Billionaires June 24, 2019 61 / 64

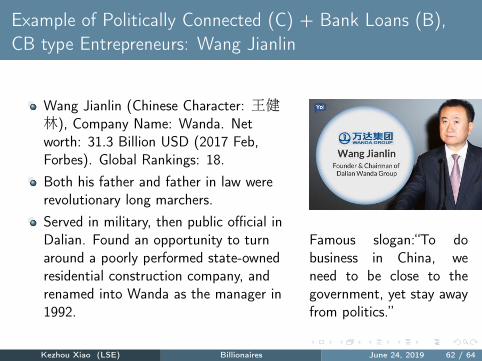

Example of Politically Connected (C) + Bank Loans (B),CB type Entrepreneurs: Wang Jianlin

Wang Jianlin (Chinese Character: 王健林), Company Name: Wanda. Networth: 31.3 Billion USD (2017 Feb,Forbes). Global Rankings: 18.Both his father and father in law wererevolutionary long marchers.Served in military, then public official inDalian. Found an opportunity to turnaround a poorly performed state-ownedresidential construction company, andrenamed into Wanda as the manager in1992.

Famous slogan:“To dobusiness in China, weneed to be close to thegovernment, yet stay awayfrom politics.”

Kezhou Xiao (LSE) Billionaires June 24, 2019 62 / 64

Conclusions

Men make their own history, but they do not make it as they

please; they do not make it under self-selected circumstances, but

under circumstances existing already, given and transmitted from

the past. The tradition of all dead generations weighs like a night-

mare on the brains of the living.

The Eighteenth Brumaire of Louis Bonaparte. Karl Marx, 1852

This paper makes several contributions to the literature:The first ever systematic analysis of rising global billionaireentrepreneurs from a Communist Party-State. Both theoretical andempirical.Demonstrate the need to consider mixed entrepreneurship within theChinese context.Showcase the importance of foreign financing channel for attenuatingpolitical economy and financial frictions.

Kezhou Xiao (LSE) Billionaires June 24, 2019 63 / 64

Questions!

Kezhou Xiao (LSE) Billionaires June 24, 2019 64 / 64

D. Acemoglu. Reward structures and the allocation of talent. European

Economic Review, 39(1):17–33, 1995.

D. Acemoglu and J. Robinson. Why nations fail: The origins of power,

prosperity, and poverty. Crown Business, 2012.

W. J. Baumol. Entrepreneurship: Productive, unproductive, anddestructive. Journal of Political Economy, 98(5 Part 1):893–921, 1990.

W. J. Baumol, R. E. Litan, and C. J. Schramm. Good capitalism, badcapitalism, and the economics of growth and prosperity. 2007.

T. Besley and M. Kudamatsu. Making autocracy work. Institutions and

economic performance, edited by Helpman Elhanan, pages 452–510,2008.

T. Besley and M. Reynal-Querol. Do democracies select more educatedleaders? American political science review, 105(03):552–566, 2011.

M. Faccio. Politically connected firms. The American economic review, 96(1):369–386, 2006.

R. Fisman. Estimating the value of political connections. The American

economic review, 91(4):1095–1102, 2001.Kezhou Xiao (LSE) Billionaires June 24, 2019 64 / 64

S. H. Haber, D. C. North, and B. R. Weingast. Political institutions and

financial development. Stanford University Press, 2008.B. Holmström and J. Tirole. Lapm: A liquidity-based asset pricing model.

the Journal of Finance, 56(5):1837–1867, 2001.R. G. King and R. Levine. Finance and growth: Schumpeter might be

right. The quarterly journal of economics, 108(3):717–737, 1993.R. Levine. Finance and growth: theory and evidence. Handbook of

economic growth, 1:865–934, 2005.C. W. Mills. The power elite, volume 20. Oxford University Press,

1956/2000.C. W. Mills. The sociological imagination. Oxford University Press,

1959/2000.S. C. Myers. The capital structure puzzle. The journal of finance, 39(3):

574–592, 1984.R. Rajan and L. Zingales. Saving capitalism from the capitalists, volume

2121. New York: Crown Business, 2003.J. A. Schumpeter. Capitalism, socialism and democracy. Harper &

Brothers, 1942.Kezhou Xiao (LSE) Billionaires June 24, 2019 64 / 64

J. A. Schumpeter. The creative response in economic history. The journal

of economic history, 7(2):149–159, 1947.Z. Song, K. Storesletten, and F. Zilibotti. Growing like china. The

American Economic Review, 101(1):196–233, 2011.

Kezhou Xiao (LSE) Billionaires June 24, 2019 64 / 64