Languages

Pages

Legal

1

2012

Employee Benefit Plan Audit Conference

Basic Audit Workshop

Maryland Association of CPAsColumbia, Maryland

May 8, 2012

2

Discussion Leaders

Marcus AronMarilee P. Lau

3

Overviewand

Introduction

4

Workshop

• ERISA and Related Regulations• Planning, Supervision and Internal Control• Contributions and Participant Data• Benefit Payments, Claims and Benefit

Obligations• Investments and Investment Income• Audit Completion• Reporting and Disclosure Requirements• Party-in-interest, Prohibited Transactions

and Plan Tax Status

5

Workshop

• Interactive with participants• Basic Regulatory, Accounting,

Auditing and Reporting fundamentals • Participant questions, observations

and real life examples encouraged

6

Who Is Here?

• External Auditors• Internal Auditors• Plan Administrators/sponsors• Attorneys• Tax Professionals• Third Party Administrators• Regulators—IRS/DOL

7

Plan Auditors

• Regional Firm• Local Firm• Partners• Managers• Staff

8

Plan Audits

• How many plans does your firm audit?A.< 5B.<10C.<25D.<50E.<100

9

Types of Audits

• Defined Benefit Plans• Defined Contribution Plans401(k)/403(b)Profit SharingESOPS

• Health and Welfare Plans• Full Scope Audits11K filings

• Limited Scope Audits

10

ERISA and Related Regulations

Audit GuideChapter 1 and Appendix A

11

Learning ObjectivesUpon completion you should have an understanding of the following:• How a benefit plan is defined under

ERISA, GAAP and the IRS• The design and functioning of various

types of benefit plans• When an audit is required• The role of the various parties involved

in the operation of the benefit plan

12

ERISA

Employee Retirement Income Security Act (ERISA) of 1974

Governs operation, administration & annual reporting for pension & welfare plans

ERISA contains four Titles– General DOL responsibilities– Tax Law requirements– Specific jurisdiction and enforcement

procedures– Multiemployer plan matters

13

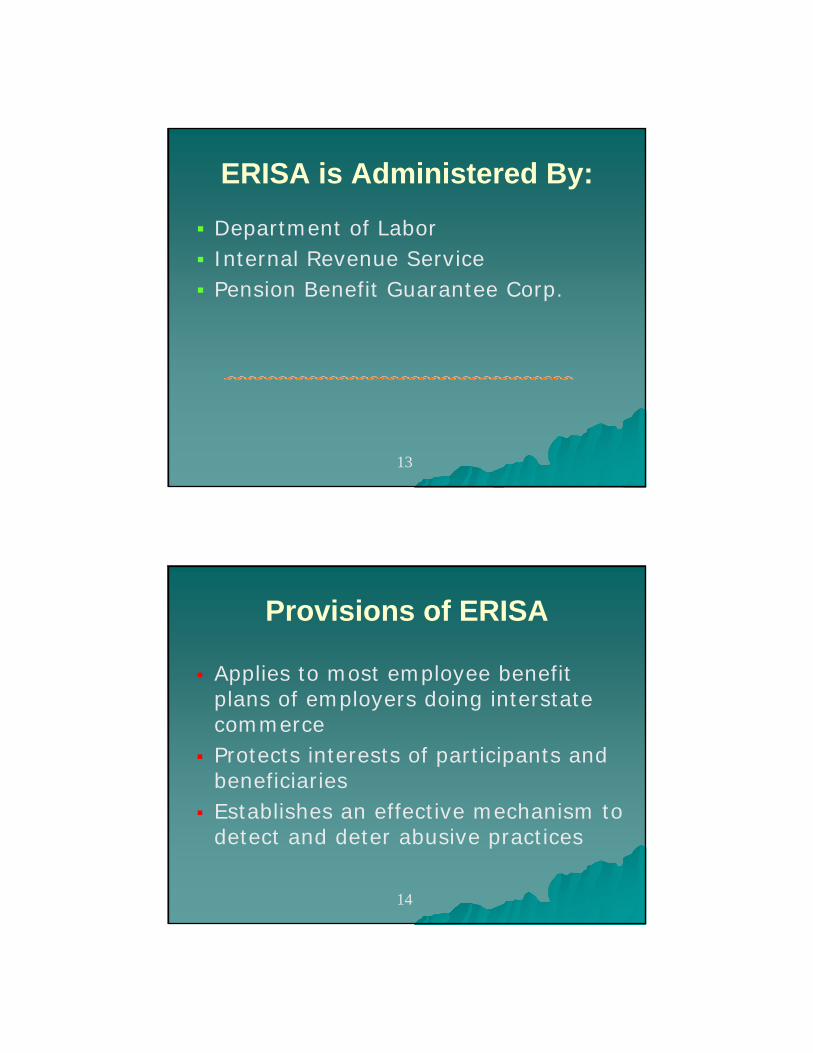

ERISA is Administered By:

Department of Labor Internal Revenue Service Pension Benefit Guarantee Corp.

14

Provisions of ERISA

Applies to most employee benefit plans of employers doing interstate commerce

Protects interests of participants and beneficiaries

Establishes an effective mechanism to detect and deter abusive practices

15

Types of Plans

Defined Benefit Retirement PlansDefined Contribution Retirement

PlansHealth and Welfare Plans

16

Defined Benefit Plans

Promises a future benefit that is stated in the plan document or can be calculated according to a formula provided in the plan document• Traditional Defined Benefit Plan• Cash Balance Plan

17

Defined Contribution Plans

Requires an individual account for each participant and provides benefits based on amounts contributed, investment experience, allocated expenses and allocated forfeitures• Profit sharing plan• Money purchase plan• Cash or deferred arrangement—401(k) • Tax Savings Annuity Plans—403(b)• Employee stock ownership plan—ESOP

18

Health and Welfare Plans

Covers• Medical, dental, vision• Short and Long term disability• Prescription drugs• HSA, FSA, Dependent Care• Vacations, Tuition, Legal

Can be a DB plan or a DC plan

19

General Reporting Requirements

• Requires annual reporting via the Form 5500

• Plans with 100 or more participants may require a financial statement audit

• Plans with under 100 may require a financial statement audit if certain, waiver conditions are not met

• Certain financial entities also file directly with the DOL

20

Plans Requiring a Financial Statement Audit

• ERISA section 103(a)(3)(A) contains audit requirement

• Plans filing the Form 5500 as a “large plan” generally require an audit

• Some exceptions to the audit requirement do exist

• Some small pension plans may be required to have an audit

21

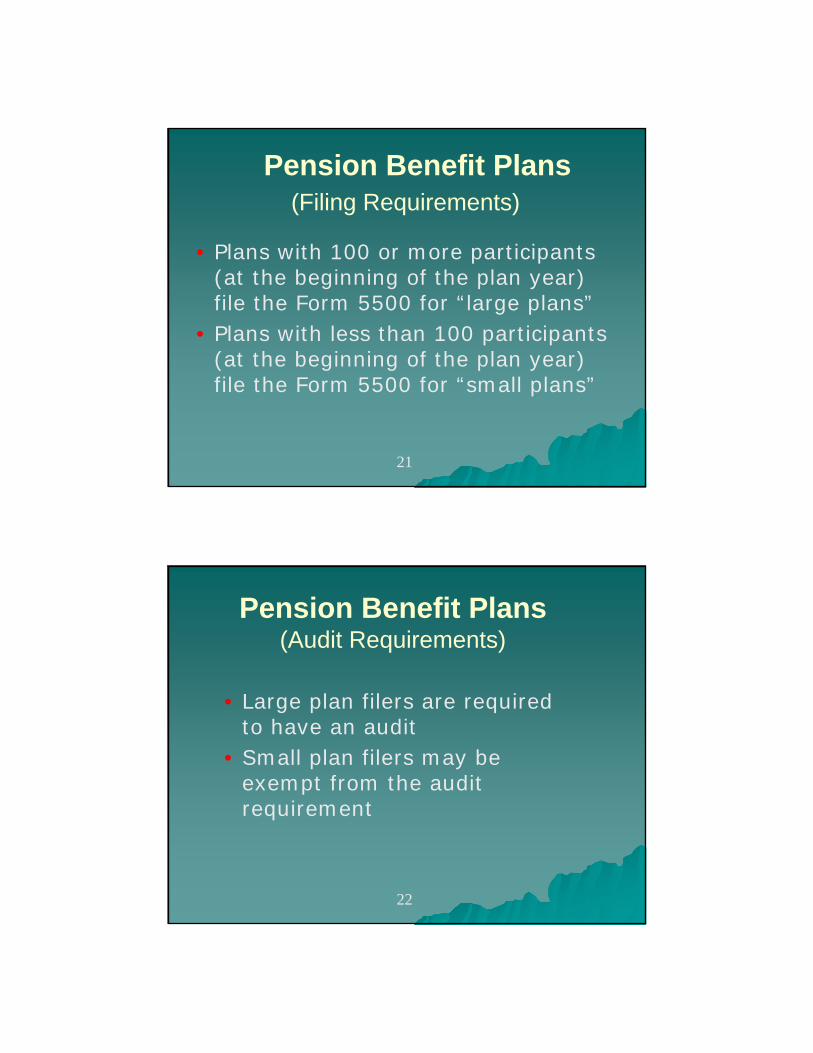

Pension Benefit Plans(Filing Requirements)

• Plans with 100 or more participants (at the beginning of the plan year) file the Form 5500 for “large plans”

• Plans with less than 100 participants (at the beginning of the plan year) file the Form 5500 for “small plans”

22

Pension Benefit Plans(Audit Requirements)

• Large plan filers are required to have an audit

• Small plan filers may be exempt from the audit requirement

23

Small Pension Plan Security Regulation

• Vulnerability of small plans to theft & fraud• Small plans hold over $500 billion in assets• Goals:

– Improve security of pension assets– Increase the accountability of those handling

assets– Encourage small employers to sponsor plans

• Effective for plan years beginning after April 17, 2001

• Rule adds disclosure & fidelity bonding requirements to certain small plans

24

What Does This Mean?

• Only applies to pension plans with less than 100 Participants at the beginning of the year

• Includes a two part test• If the plan fails either part an audit

is required• The two tests are financial and

disclosure

25

Welfare Benefit Plans(Exemptions From Filing/Audit)

• Plans with less than 100 participants at beginning of the plan year, and–pay benefits solely from sponsor assets,

or–provide benefits through insurance

contracts, or– combination of two items above, and

forward any employee contributions within three months of receipt

26

Welfare Benefit Plans(Exemptions From Audit)

Plans with 100 or more participants at the beginning of the plan year, and

• benefits paid solely from sponsor assets• benefits provided exclusively through

insurance contracts• benefits paid partly from sponsor assets

and partly through insurance contracts

27

Cafeteria Arrangements

• Generally are not required to be audited unless they also provide welfare benefits

• PWBA Technical Release 92-1–Section 125 (Cafeteria) Plans may

not need an audit if assets are not held in trust

28

Direct Filing Entities (DFEs)• Entities required to file

–Master Trust Investment Accounts (MTIAs)

• Entities that may elect to file–Pooled Separate Accounts (PSAs)–Common Collective Trusts (CCTs)–103-12 Investment Entities (103-12IEs)–Group Insurance Arrangements (GIAs)

29

DFEs Electing Not to File• Affects how participating plans file

– If PSA or CCT does not file as DFE, plan may not use limited reporting on Schedule H

– If GIA does not file, each plan participating in GIA must make its own filing

– If 103-12 does not file, participating plans are not afforded limited reporting and plan audit relief

30

Helpful “Links”

• EBSA website– http://www.dol.gov/ebsa/

• FAQs about pensions plans and ERISA– http://www.dol.gov/ebsa/faqs/faq_compliance

_pension.html• FAQs on the Small Pension Plan Audit

Waiver Regulation– http://www.dol.gov/ebsa/faqs/faq_auditwaiver

.html

31

Helpful “Links”

• FAQs about Abandoned Plans–http://www.dol.gov/ebsa/faqs/faq-

abplanreg.html• FAQs about the DFVC Program

–http://www.dol.gov/ebsa/faqs/faq_DFVC.html

32

Common Audit Deficiencies

• Participant Data• Investments• Contributions• Benefit Payments• Related Party/Prohibited

Transactions• Reporting and Disclosures

33

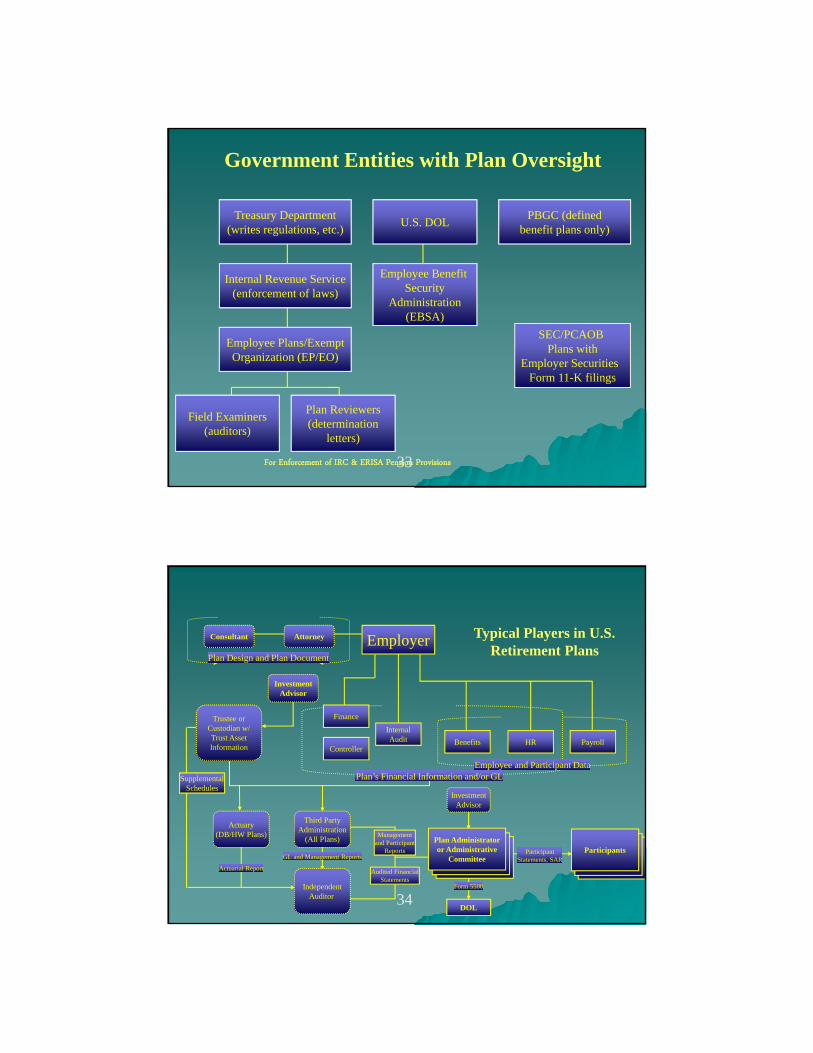

Government Entities with Plan Oversight

For Enforcement of IRC & ERISA Pension Provisions

Treasury Department(writes regulations, etc.)

Internal Revenue Service(enforcement of laws)

Employee Plans/ExemptOrganization (EP/EO)

U.S. DOL

Employee Benefit Security

Administration(EBSA)

Field Examiners(auditors)

Plan Reviewers(determination

letters)

SEC/PCAOB Plans with

Employer Securities Form 11-K filings

PBGC (definedbenefit plans only)

34

Typical Players in U.S. Retirement Plans

EmployerAttorneyConsultant

Plan Design and Plan Document

InvestmentAdvisor

Trustee orCustodian w/Trust AssetInformation

Finance

Controller

InternalAudit Benefits Payroll

Plan’s Financial Information and/or GL

IndependentAuditor

Actuary(DB/HW Plans)

Third PartyAdministration

(All Plans)

InvestmentAdvisor

Plan Administratoror Administrative

Committee

DOL

ParticipantsParticipantStatements, SAR

Form 5500

SupplementalSchedules

Actuarial Report

HR

GL and Management Reports

Managementand Participant

Reports

Audited FinancialStatements

Employee and Participant Data

35

Authoritative Literature• FASB Accounting Standards Codification

(FASB ASC)• Statements on Auditing Standards

(SAS-AU)• Audit & Accounting Guide for Employee

Benefit Plans• Audit Risk Alert for Employee Benefit

Plans Industry Developments• Employee Benefits Security

Administration (EBSA)• PCAOB/SEC

36

Review Questions

1.What is the difference between a defined benefit plan and a defined contribution plan?

2.Name three common types of defined contribution plans?

3.When would an audit generally be triggered for a DC plan?

37

Questions????

38

Planning, Risk Assessment and Internal Control

Audit Guide Chapters 5 and 6

39

Learning ObjectivesUpon completion you should have an understanding of the following:• Issues related to client acceptance• How to determine the scope of the audit• How to gain an understanding of a

plan’s internal controls• Assessing engagement fraud and overall

audit risk assessment• Development of a written audit program

40

Planning and Supervision

Determination of Audit Scope• Is this an ERISA covered

plan?• How many participants at

the beginning of plan year?• < than 100 participants - no

audit is necessary• Regulatory exemptions from

audit

41

Initial or First Year Audits• Predecessor Auditors

– AU 315 requirements• Communication• Review work papers

• Opening balances– What procedures need to be performed– Participant data

• Who are the Service Providers– Trustee– Record Keeper– Actuary

42

What Type of Audit to Perform?

Must apply all applicable GAAS procedures

Basis of Accounting—accrual or modified cash

Full Scope Audit– Must audit investment information

Limited Scope Audit– Investment information not audited– Investments certified by a qualified Trustee– DOL Regulation 2520.103-8

Form 5500 and Supplemental Schedules

43

Form 5500 Schedules

Required schedules for audit opinion• Schedule H• Schedule G• Supplemental schedules

– 4(a) Delinquent Participant Contributions– 4(i) Assets Held– 4(j) 5% Reportable Transactions

Other schedules• Schedules A, C, D and SB/MB

44

Professional Standards

• Professional Standards Relating to Audit Planning–First Standard of Field Work–Statements on Auditing Standards

• AU 311—Planning and Supervision• AU 380—Communications with those

charged with Governance– Needs to be done at the beginning of the

engagement

45

Engagement Letter• Engagement letter is part of your

required communication with the those charged with governance—AU 380–Name of Plan, financial

statements/schedules–Audit Scope –Timing of audit work–5500 preparation–Fees

• See example letter in the Audit Guide

46

Engagement LetterAdditional Matters

• Whether due to the complex or subjective nature of the subject matter, the audit may require the special skills and knowledge of a specialist (i.e. use of actuaries for DB and H&W plans or valuation professionals for investments)

• Non-attest services--assistance in drafting the Plan’s financial statements (including supplemental schedules) and related footnotes

47

Audit Risk

• Assess audit risk• Create an audit staffing plan• Create a written audit program• Audit procedures

–Nature–Timing–Extent

48

Internal Control

• Professional Standards• Standards of Field Work• Statements on Auditing Standards

–Numerous statements on the control environment• Such as: AU 314, AU 316, AU 318, AU

324, AU 325, AU 380 and PCAOB #5

49

GAAS Requirement

• Auditor must understand each of the five components of internal control sufficient to plan the audit–Obtain via tests of design AND–Determining whether they have been

placed in operation• Required for ALL audits even if

control risk is planned at maximum

50

Entity’s Internal Control Structure

• Obtain an understanding of:–Control environment–Risk assessment– Information and Communication–Control Activities–Monitoring

• Document the understanding of the internal control structure

51

Entity’s Internal Control Structure

• Assessing Control Risk–Occurrence or Existence–Rights and obligations –Completeness–Accuracy or Valuation and Allocation–Cut-off–Classification and Understandability

• Document Basis for Conclusions

52

Risk Assessment

• Internal and External Events• Change in Circumstances• Understanding How Management

Identifies Risks• Understanding Management’s

Assertions

53

Risk Assessment• SASs provide guidance concerning the

auditor’s assessment of risk of material misstatement whether caused by error or fraud in a financial statement audit

• Auditors need to design and perform audit procedures responsive to assessment of risks

• Requires an in-depth understanding of the entity including its internal control

54

Risk Assessment• A rigorous assessment of risks of

material misstatement is required• Evaluation of and testing of internal

controls at the entity level• If risks are identified during planning

meeting, the audit team should identify the controls related to the risks to determine what additional audit procedures will be performed to address the risks

55

Risk Assessment

• Consideration of management override will likely necessitate the performance of some substantive procedures

• Auditors can default to maximum control risk without documenting the basis for that assessment

56

Overview of AU 325Communicating Internal Control Related

Matters Identified in An Audit

• Defines the terms deficiency in internal control, significant deficiency and material weakness

• Provides guidance on evaluating the severity of deficiencies in internal control identified in an audit of financial statements

• Requires the auditor to communicate, in writing, to management and those charged with governance significant deficiencies and material weaknesses identified in an audit

57

Definitions

• A material weakness is a deficiency, or combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected on a timely basis.

• A significant deficient is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance.

58

Evaluating Deficiencies- Severity Evaluation

• Severity of deficiency depends on– Magnitude of the potential misstatement

resulting from the deficiency or deficiencies– Whether there is a reasonable possibility that

the entity’s controls will fail to prevent, or detect and correct a misstatement of an account balance of disclosure

• Does not depend on whether a misstatement actually occurred

59

Impact of Service Organizations on Plan’s Internal Control

• Who Has Control of the assets and participant accounts?

• Where are participant and investment records?–Bank– Insurance company– Investment Advisor–Recordkeeper

60

Service Organizations• SAS 70 superseded by two standards• SSAE No. 16, Reporting on Controls at a

Service Organization– Only contains guidance for service auditors– Three reports, SOC 1, SOC 2 and SOC 3– Effective for service auditor’s reports for periods

ending on or after June 15, 2011• Clarified SAS, Audit Considerations Related

to an Entity Using a Service Organization– Only for user auditors– Effective for audits of financial statements

for periods ending on or after December 15, 2012 (same as clarified standards)

61

SOC Reports

• SCO 1 Reports– Restricted use report– Type 1 or type 2– Purpose is for reports on controls for financial statement

audits• SCO 2 Reports

– Generally a restricted use report– Type 1 or type 2– Purpose is for reports on controls related to compliance

or operations• SCO 3 Reports

– General use report– Public Seal– Purpose is for reports on controls related to compliance

or operations

62

Service Organization Control Reports

SOC 1 Reports

• SSAE No. 16, Reporting on Controls at a Service Organization

• User auditors continue to use guidance in AU 324 until new guidance is effective

• Audit Tool “Documentation of Use of a Type 2 Service Auditor’s Report in an Employee Benefit Plan Financial Statement Audit”

63

SOC 1 Reports

• What is similar– Type 1 and Type 2 reports– Service auditor obtains the same level of evidence

and issues examination level opinion– Restricted to user entities that are customers of the

service organization and user auditors– Primarily an auditor to auditor communication– Provides user auditors with information about

controls at a service organization that are relevant to the user entities’ financial statements

64

Consideration of Fraud

• Requires the auditor to assess the risk of material misstatement due to fraud and provides categories of risk factors

• Document in the workpapers:–Risk factors–Response to those risk factors–Other considerations

65

Requirements for AU 316

• Description of Fraud–Characteristics

• Incentive or pressures• Opportunity• Rationalization or Attitude

–Misstatement• Fraudulent reporting• Misappropriation of assets

66

AU 316

• Importance of exercising professional skepticism

• Discussion among the engagement personnel regarding risks—brainstorming session

• Expanded inquiries regarding fraud among management and audit committees

67

AU 316

• Generally requires more substantive auditing procedures and documentation– Risk of management override– Analytical procedures

• Presumption that improper revenue recognition is a fraud risk

• Fraud risk for a benefit plan– Misappropriation of assets– Hard to value investments– Fraudulent payment of claims and benefits

68

Have You Ever Discovered Fraud in an Employee Benefit

Plan?

69

Questions????

70

Contributions and Participant Data

Audit GuideChapters 8 & 10

71

Learning Objectives

Upon completion you should:Be able to plan and perform appropriate audit procedures with respect to participant data and contributions

72

Contributions and Participant Data

Audit Objectives-Contributions–Whether the amounts received or due

the plan have been determined, recorded and disclosed in the plan’s financial statements in conformity with the plan document and GAAP

–Whether appropriate allowance has been made for uncollectible plan contributions receivable

73

Contributions and Participant Data

Audit Objectives for Participant Data and Allocations– Whether covered employees have been properly

recorded in eligibility records and contribution reports – Accurate participant data for eligible employees has

been supplied to the plan’s recordkeeper and, if applicable to the plan’s actuary.

– Whether net assets have been properly allocated to the individual participant’s account

– Whether the sum of all participant accounts reconciles with the total net assets available for plan benefits

74

Contributions

Defined Contribution Plan– 403(b) plans have additional contributions

• 15 years of service have an additional deferral limit• Allowable contributions for terminated employees for 5

years following severance

Defined Benefit PlansHealth and Welfare PlansTransfers and Merged Plans

75

Auditing ConsiderationsDefined Contribution Plan

Participant eligibility and data integrity Participant enrollment (including automatic

enrollment) Employee deferrals, after-tax and catch up

contributions– Remittance of employee contributions

Employer contributions and receivables– Matching and discretionary contributions– Remittance of employer contributions

76

DC Audit Procedures Obtain a schedule of contributions

received and receivable Reconcile contributions received from the

schedule to the plan’s payroll records, recordkeeper report and trustee report

Determine that employee contributions have been remitted timely to the trust

Obtain roll forward of the forfeiture account and determine whether forfeitures appropriately used based upon the plan document

Reconcile participant balances to trust assets

77

Eligibility Testwork

• Determine what participant data must be tested, by reviewing plan document

• Select a sample of employees from payroll and recordkeeper

• Agree census data to employee’s personnel file, recordkeeping detail and payroll register

• Verify that eligibility is in accordance with the plan document and that the proper eligible compensation has been used

78

DC Contribution Testwork

Test payroll data for a selected number of participants by agreeing to earnings records, time cards and authorization

Recalculate participant's deferral amount Recalculate matching contribution Determine that employee contributions have not

exceeded annual limits Recalculate income allocations for a sample of

participants Consider confirming investment elections and

salary deferral % directly with participants

79

Other Considerations

Rollovers from other qualified plans

Catch up contributionsRoth ContributionsUse of forfeitures

– Employer contributions– Pay administrative expense– Reallocate to participants

80

Rollover Contributions

Review plan document to determine that the rollover was made in accordance with the plan provisions

Test asset transfer from the former trustee (custodian) to the current trustee including verification of the participant-directed investments, if applicable

Review participant record keeping account to determine that the rollover amount is properly reflected

81

Catch Up Contributions

$5,500 limit for 2011 and 2012Participant must be making

contributions to the planAge 50 or older by the end of the

calendar year

82

Roth Contributions Plan document needs to be amended to

allow for Roth 401(k) contributions Contributions are subject to the same

limits as traditional contributions Changes in the law allow more

individual to contribute to the a Roth 401 (k)

There is no tax deduction for contributions to a Roth 401(k) as contributions are after tax

Income needs to be tracked separately

83

Defined Benefit Plan Contributions

Determine that contributions are consistent with the plan’s funding policy and are properly authorized

Review the amount contributed and, if applicable, determine that it meets the requirements of the funding standard

Determine if receivables are properly recorded

Review the Schedule SB/MB of the Form 5500 and reconcile if necessary

84

DB Participant Data Testwork

Complete similar procedures as for a defined contribution plan related to census data

Trace information from payroll records to the information provided to the plan’s actuary

Confirm information provided to the plan’s actuary for eligible compensation and census data

85

Health & Welfare Plans

Determine that the employer contributions are consistent with the plan’s funding policy. (Usually pay as you go)

Insure that all contributions are reported for the plan regardless if deposited to the trust

Review the contribution provisions of the plan document for employees and test compliance

86

HW Contributions Eligibility and contribution testwork

– Select a sample of employees from payroll and claims processor

– If a paper trail is not available, consider sending positive confirmations to a sample of participants

– Verify that eligibility is in accordance with the plan document

– Agree census data to employee’s personnel file, detail and payroll register

– Recalculate participant's contribution amount for benefits selected

– Test employer contributions to invoices (premiums and claims)

– Consider confirmations with service providers– Test contributions receivable– Verify payroll records are accurate

87

Merged Plans

Reconcile net assets available per the trustee to the recordkeeper immediately prior and subsequent to the merger

For Defined Contribution plans compare selected participant accounts immediately prior to and subsequent to the merger to determine that accounts were transferred properly

Test transfer of assets from the former trustee to the current trustee

For Defined Benefit plans test selected employee census data and

Review actuarial report to determine that the effect of the merger on benefit obligations is properly accounted for and disclosed

88

Benefit Paymentsand

Plan Obligations

Audit Guide Chapters 9 and 10

89

Learning Objectives

• Benefit Payments—As a result you should be able to plan and perform appropriate audit procedures with respect to benefit payments

• Benefit Obligations—As a result you should be able to plan and perform appropriate audit procedures with respect to plan benefit obligations

90

Benefit Payments

Audit Objectives–Payments are in accordance with plan

documents and other supporting documentation

–Whether the payments are made to or on behalf of persons entitled to them and only to such persons

–Whether transactions are recorded in the proper account, amount and period

91

Types of Distributions

Termination/cash-out/rollover– Participants can elect to take their account balance

when they terminate employment with the Company– Plan sponsors can force out balances for terminated

participants if the account balance is < $1,000 or force to an IRA if < $5000)

– Participants can take their balance in cash (which would be taxable) or roll the amount into another qualified plan such as an IRA or their new employer’s plan.

Retirement– Participants may take their account balance when they

reach retirement age

92

Types of Benefit Payments H&W benefit payments

–Claims paid directly to participants or paid directly to health care provider

Loans– Participants may borrow from their

account—amounts not subject to income tax if repaid

Hardship Withdrawal– If certain financial hardship provisions met,

can take a withdrawal while still employed but amount subject to income tax

93

Types of Benefit Payments In Service Withdrawal

– After attaining 59 1/2, participants can request a distribution from their account while still employed. Income tax will be triggered unless the amounts are rolled over into an IRA

QDRO (Qualified Domestic Relations Order)– A judgment, decree or order that creates or

recognizes an alternate payee’s (such as former spouse) right to receive all or a portion of a participant’s account balance or retirement benefit

94

VestingParticipant’s right to company contributions that have accrued in their individual account. “Cliff vesting” provides that company contributions

will be fully vested only after a specific amount of time and that employees who leave before this happens will not be entitled to any of the company contributions.

In plans with “graduated vesting,” vesting occurs in specified increments.

Generally vesting is graduated and is for 5 years or less

Safe Harbor Plans—fully vested at time of contribution

95

Audit Procedures for Benefit Payments

Obtain a schedule of distributions, claim payments/premiums and withdrawals

Reconcile to trail balance and trustee statements

Consider analytical procedures

96

Audit ProceduresFrom the schedule of distributions and

withdrawals• Select a sample which includes all types of

benefit payments and perform the following– Examine benefit election form and support for

qualifying event (such as termination notice)– Determine that the participant was eligible for the

type of distribution (such as hire date and term date per the employees file)

– Determine proper amount was forfeited, if applicable– Recalculate the distribution based on plan provisions– Determine that the appropriate tax has been withheld– For a H&W plan determine that the claim is for

covered services and applicable deductibles/limits have been applied

97

Audit Procedures

Trace payment to cash disbursement/trust records Determine that employee has been removed from

payroll records and participant listings Agree distribution amount to participant’s statement Obtain check copy and agree signature to employee’s

HR file or send confirmation or examine wire transfer if done electronically

For hardship withdrawals—examine evidence supporting the need for hardship and determine if salary deferrals have be stopped

For death benefits—obtain death certificate For QDRO—obtain court order

98

Other Procedures

Evaluate procedures for determining continued eligibility for benefits

Evaluate procedures for investigating long outstanding benefit checks

Compare participant payments with individual account records

Payments made by third party administrators may require a SOC 1 Type 2 report

99

Heath & Welfare Plans Follow guidance in FASB ASC 965 Read relevant provisions of the plan document

and underlying contracts Review and test the accumulated eligibility

credits and total benefit obligations Test premiums paid to insurance companies

(Schedule A of Form 5500) Test the obligation for claims payable and

IBNR Test individual claims for eligibility, nature of

the claim and documentary support• Other Liabilities

– Excess Contributions– Payables to third parties

100

Participant Loan Procedures

Obtain a listing of participant loans from the recordkeeper or trustee/custodian

Listing should include date of loan, original amount of loan, interest rate, due date, payments and ending loan balance

Agree to trust report and financial statements

101

Participant Loan Procedures

Select a sample of new loans Agree original loan amount to loan agreement or other

authorization Agree year end balance to loan amortization schedule Verify that the loan amount did not exceed 50% of the

participant’s account balance or $50,000 (less any outstanding loans), whichever is less, when loan was granted

Verify that the loan amortization period does not exceed the number years as indicated in the plan document

Agree distribution to participant’s statement Agree loan repayment amount to payroll deduction

102

Participant Loan Procedures

Additionally Determine if loans are current at year end Determine how delinquent loans and loans for

terminated employees are handled Determine if “deemed distributions” are

accounted for appropriately (i.e. receivable or a distribution for GAAP purposes)

Determine that loans receivable are included on the “Schedule Assets Held” as an investment

103

Participant Loans

Loan in default—if participant is not making the specified repayments through payroll (may occur if participant terminates, leave of absence, etc.)

Loan may become a deemed distribution if participant defaults and does not pay back the loan.

104

Plan Benefit ObligationsAudit Procedures

Utilize procedures for auditing participant data Check the professional qualifications and

competence of the plan actuary—AU 336, Using the work of a Specialist

Understand the actuary’s work Inquire about the actuary’s objectivity and

independence Test reliability and completeness of census data Send confirmation to actuary regarding census

data used and independence

105

Health and Welfare Plans

Determine that IBNR and benefits payable has been appropriately calculated–Obtain lag reports–Review assumptions if done by third

party such as the claims processor Insure that premiums payable are

included in obligation not statement of changes

106

Questions????

107

Investments andRelated Income

Audit GuideChapter 7

108

Learning Objectives

As a result you should be able to understand the various types of investments in employee benefit plans and to plan and perform appropriate audit procedures with respect to investments and related income in employee benefit plans.

109

Full Scope Vs. Limited Scope

That’s Easy! –In a full scope audit you audit the

investments –In a limited scope audit you don’t

audit the investments–So what’s so difficult?

109

110

Limited Scope Definition Summary of DOL Regulations 2520.103

– Where an audit is required, the financial statements accompanying the annual Form 5500 must be in accordance with GAAP

– Provides for an exclusion from the audit of investments (valuation and existence) and plan-level investment activity, if qualifying institution holding the assets certifies to the accuracy and completeness of the information

Qualifying Institutions Bank or similar institution (e.g., a trust company) Insurance carrier Regulated and supervised and subject to periodic examination by a State or Federal agency

110

111

Limited Scope Definition

Summary of DOL Regulations 2520.103– Provides sample certification language to be used by the

certifying institution The XYZ Bank (Insurance Carrier) hereby certifies

that the foregoing statement furnished pursuant to 29 CFR 2520.103-5(c) is complete and accurate.

– Indicates that certification extends to “ordinary business records” of the certifying institution

– The certification must be signed by a person authorized to represent the insurance carrier or bank trust department

111

112

Why the Limited Scope Audit Made Sense in 1974

ERISA Regulations – Pre-ERISA environment: no protection for participants or for assets– ERISA designed to ensure that participants are protected and that the

assets exist and values are accurate Financial institutions

– Highly regulated organizations– ERISA required plan assets to be held in a trust or an insurance contract– Holding assets in a trustee’s vault (versus the plan administrator’s safe)

provided more safeguards over the assets and protected the existence– Trustee/custodians could provide a valuation independent of the plan

sponsor Fair Value of plan assets were commonly part of trustee or

custodian's “ordinary business records”– Plan investments had readily determinable market values– Plan & trust structures were less complex

SAS 70 Reports did not exist—financial institutions did not want each plan’s auditors coming in to review their internal controls

Negotiated between the DOL and the financial institutions

112

113

Professional GuidanceRegarding Investments

FASB ASC 820, Fair value Measurements and Disclosure

FASB ASC 960-325, Plan Accounting Defined Benefit Plans-Investments

FASB ASC 962-325, Plan Accounting Defined Contribution Plans-Investments

FASB ASC 965-325, Plan Accounting Health and Welfare Benefit Plans--Investments

113

114

Audit Objectives

Whether all investments are recorded and exist

Whether investments are owned by the plan, free of liens, etc.

Whether investment principal and income transactions are properly valued in conformity with GAAP

Whether investment information is properly presented and disclosed including leveling

Whether investment transactions are initiated in accordance with the established investment policies

Whether amounts are properly allocated114

115

Full Scope Audits

Assets held by a Third Party Are the investments recorded and do they

exist (Confirm in writing) Are assets owned by the plan Are assets reconciled to trustee

reports/recordkeeper/investment managers

Proper recording principal and income transactions

Proper presentation and disclosure of investment information–Does plan have hard to value investments–Does plan engage in securities lending

115

116

Full Scope Audits

Understand the plan’s investment strategy and valuation mythologies

Analyze changes in investments Determine existence and ownership

of assets Review and inquire:

–Plan minutes–Agreements for evidence of liens,

pledges and security interests–Investment manager reports

116

117

Investments Full Scope Audits

What Is Different From a Limited Scope Audit? Confirm existence directly with holder of assets

(more than one custodian may hold assets) Year-end market value testing and leveling Purchases and sales testing Investment income testing

– Interest & dividends– Realized gains and losses– Unrealized gains and losses

117

118

For All Audits

Review footnotes and schedules–Proper classification by type of

investment–Proper description for method of

determining fair value – Issuer of investment is correct

Review Schedules A & D of Form 5500–Determine if investments are with an

insurance company–Determine if investment is a DFE

118

119

Fair Value Measurements and Disclosures

Are Management's Responsibility

For all audits Management needs to:• Establish an accounting and financial reporting process

for determining the fair value measurements and disclosures

• Select appropriate valuation measurements• Identify and adequately support any significant

assumptions used• Prepare the valuation• Ensure that the presentation and disclosure of fair value

measurements are in accordance with GAAP

119

120

Common Types of Plan Investments

• Common stocks • Mutual funds

• Common/collective trusts • Unallocated Insurance contracts

• Pooled separate accounts • US Government Securities

• Corporate bonds • Master trusts – holding any or all of these investment types

120

121

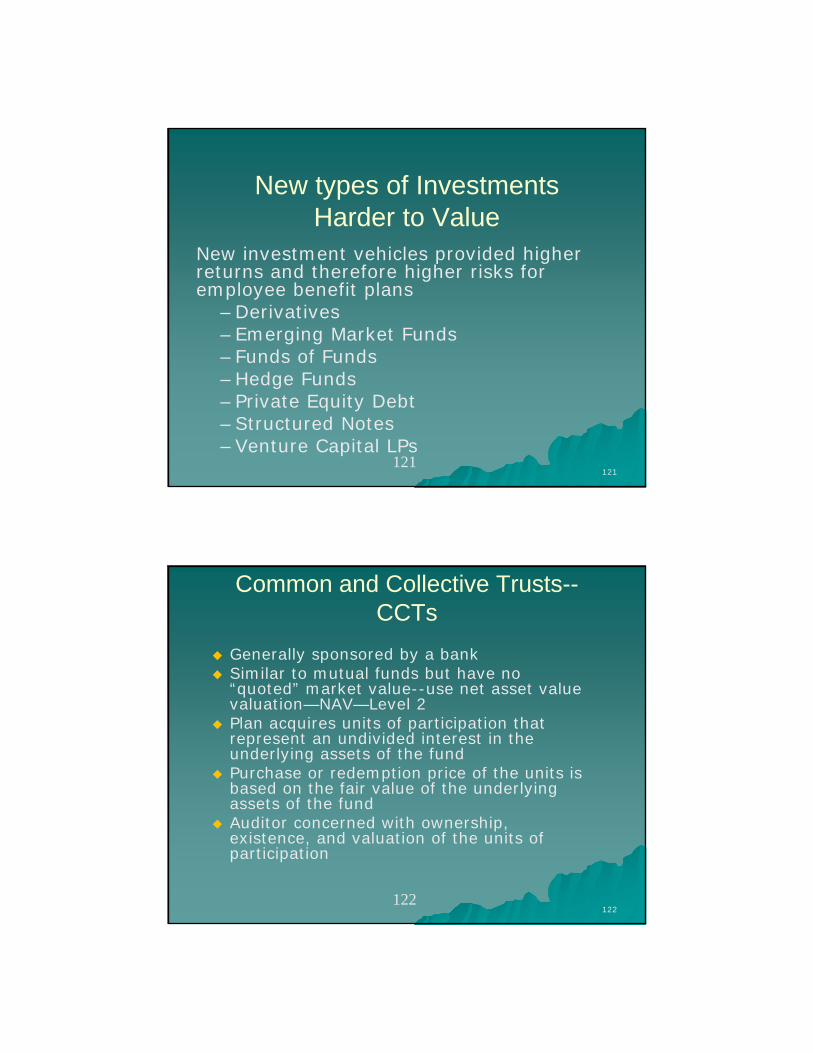

New investment vehicles provided higher returns and therefore higher risks for employee benefit plans

–Derivatives–Emerging Market Funds–Funds of Funds–Hedge Funds–Private Equity Debt–Structured Notes–Venture Capital LPs

New types of InvestmentsHarder to Value

121

122

Common and Collective Trusts--CCTs

Generally sponsored by a bank Similar to mutual funds but have no

“quoted” market value--use net asset value valuation—NAV—Level 2

Plan acquires units of participation that represent an undivided interest in the underlying assets of the fund

Purchase or redemption price of the units is based on the fair value of the underlying assets of the fund

Auditor concerned with ownership, existence, and valuation of the units of participation

122

123

CCTsAudit procedures

– Obtain and read copy of contract– Confirm directly with trustee the units of

participation held– Obtain a copy of most recent audited financial

statements of the fund– Obtain SOC-1 Type 2 Report

Issues—audited statements not as of the plan year end

Fair value presentation with adjustment to contract value for CCTs that are stable value funds

Must chose to select the use of NAV as a practical expedient for fair value

123

124

Contracts with Insurance Companies

Investment contracts vs. insurance contracts– In an insurance contract the risk is shifted to the

insurance company– Investment contracts reported at fair value except for

“fully benefit responsive” contracts of defined contribution plans which are reported at fair value with an adjustment to contract value

Deposit administration contracts (DA) Immediate participation guarantee

contracts (IPG)Separate and pooled separate contracts

124

125

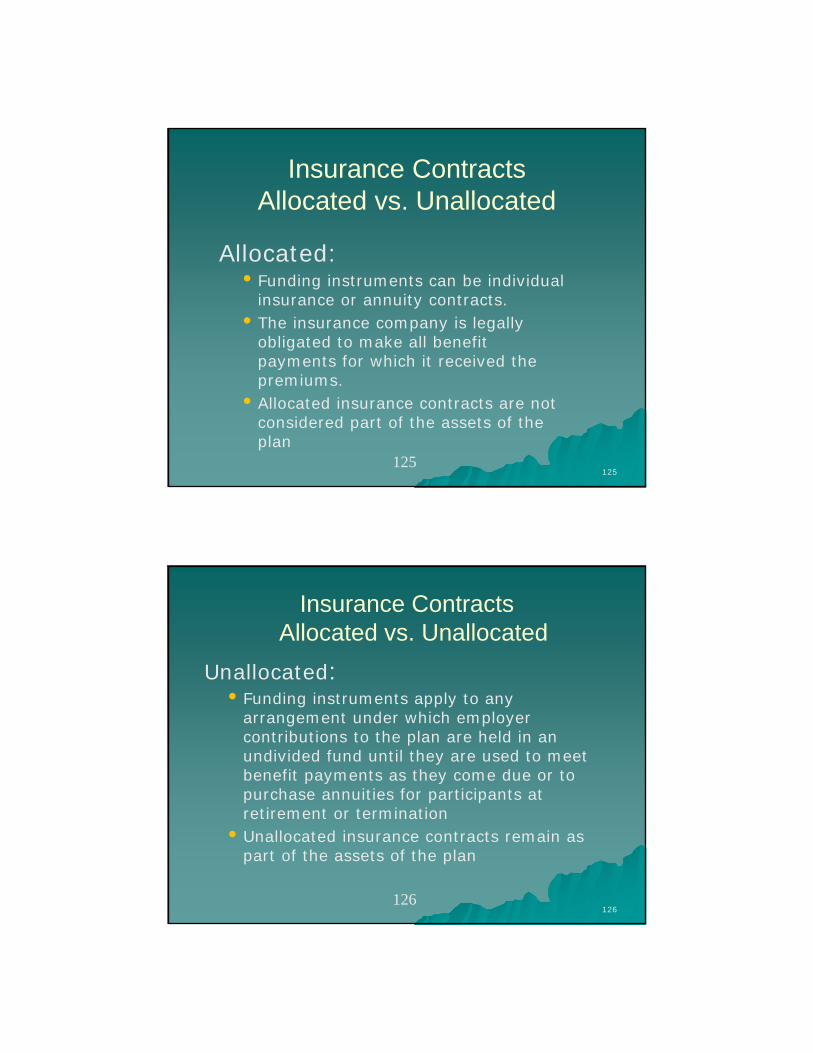

Insurance ContractsAllocated vs. Unallocated

Allocated:• Funding instruments can be individual

insurance or annuity contracts.• The insurance company is legally

obligated to make all benefit payments for which it received the premiums.

• Allocated insurance contracts are not considered part of the assets of the plan

125

126

Insurance ContractsAllocated vs. Unallocated

Unallocated:• Funding instruments apply to any

arrangement under which employer contributions to the plan are held in an undivided fund until they are used to meet benefit payments as they come due or to purchase annuities for participants at retirement or termination

• Unallocated insurance contracts remain as part of the assets of the plan

126

127

Audit Procedures for Insurance Contracts

Obtain and read copy of the contract Confirm contributions or premiums made to the

fund or account during the year Determine reasonableness of the interest rate Determine that the annuity purchases were made

on the basis of stipulated contract rates Obtain and review most recent audited financial

statements—many times no financial statements Obtain SOC 1 type 2 report Fair value may equal contract value

127

128

Pooled Separate Accounts—PSA’s

• Generally sponsored by an insurance company

• Several plans participate in PSA’s• Similar to mutual funds but have no “quoted”

value—use NAV—Level 2 investments• Assets of the separate account are assets of

the insurance company but are not commingled with the insurance company’s general assets

• Purpose is to allow flexibility in the investment of plan’ funds

128

129

PSA’s

Audit procedures—similar to CCT’s– Obtain and read copy of contract– Confirm directly with insurance company the

units of participation held– Obtain a copy of the most recent audited

financial statements of the account– Obtain SOC 1 type 2 report

Issues– Many times no audited financial statements– Audited statements are not as of the plan year

end– Use of NAV as practical expedient for fair

value

129

130

Master Trusts A combined account for companies that sponsor

more than one employee benefit plan A bank ordinarily serves as trustee, or

custodian, and may have discretionary control over the assets

Each plan has an interest in the assets of the trust and ownership is represented by a record of proportionate dollar interest, by units of participation, or specific identification

Master trusts are not required to be audited under ERISA, however appropriate audit procedures apply to individual plans with assets invested in a master trust

Apply the same auditing procedures that you would when auditing investments

130

131

Hard to Value Investments

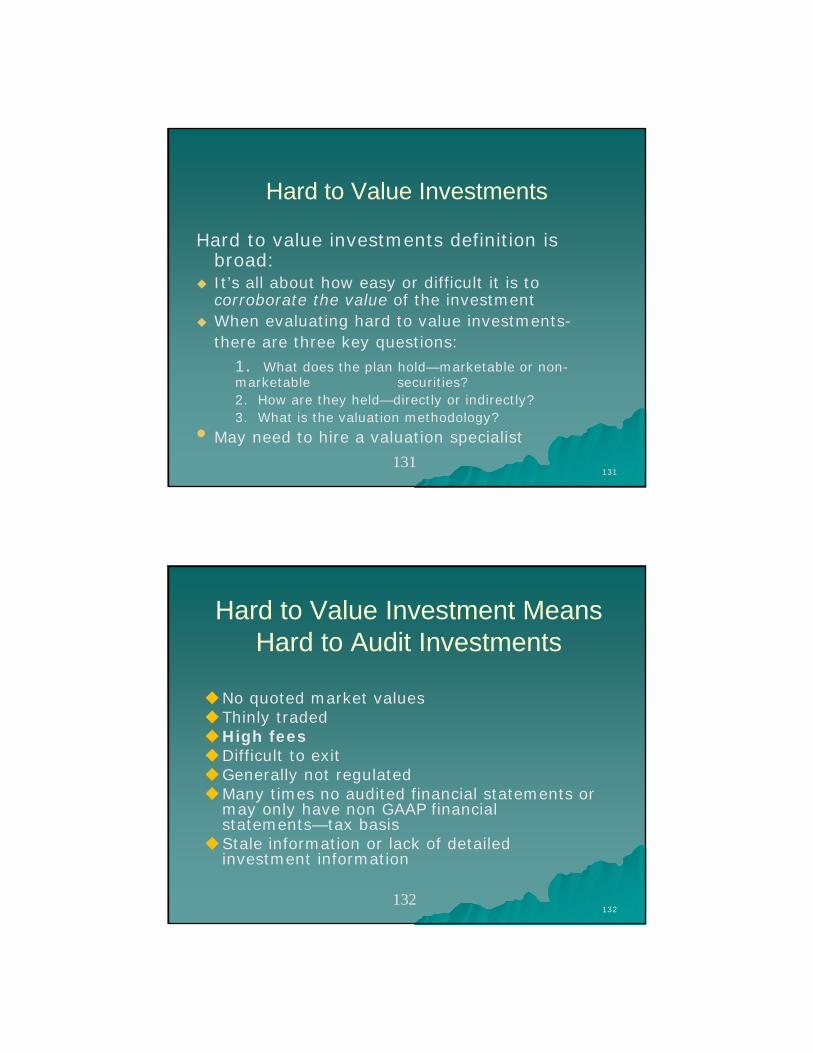

Hard to value investments definition is broad:

It’s all about how easy or difficult it is to corroborate the value of the investment

When evaluating hard to value investments-there are three key questions:

1. What does the plan hold—marketable or non-marketable securities?2. How are they held—directly or indirectly?3. What is the valuation methodology?

• May need to hire a valuation specialist

131

132

Hard to Value Investment MeansHard to Audit Investments

No quoted market valuesThinly tradedHigh feesDifficult to exitGenerally not regulatedMany times no audited financial statements or

may only have non GAAP financial statements—tax basis

Stale information or lack of detailed investment information

132

133

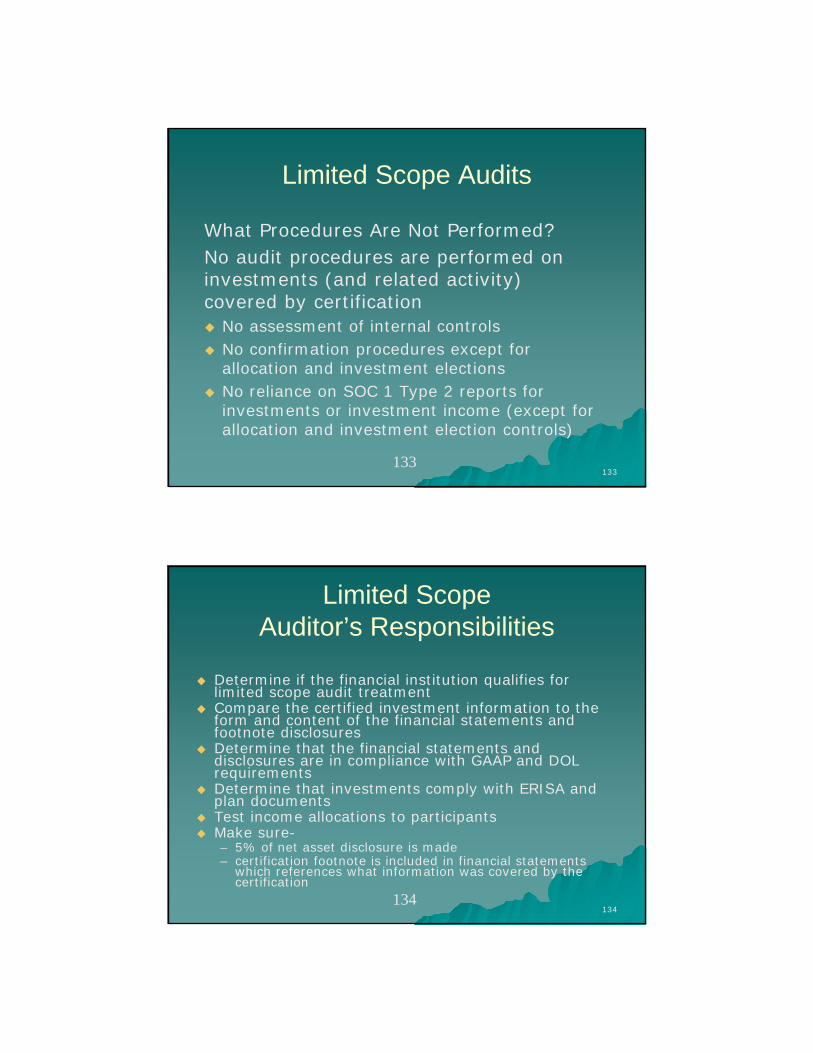

Limited Scope Audits

What Procedures Are Not Performed?No audit procedures are performed on investments (and related activity) covered by certification No assessment of internal controls No confirmation procedures except for

allocation and investment elections No reliance on SOC 1 Type 2 reports for

investments or investment income (except for allocation and investment election controls)

133

134

Limited Scope Auditor’s Responsibilities

Determine if the financial institution qualifies for limited scope audit treatment

Compare the certified investment information to the form and content of the financial statements and footnote disclosures

Determine that the financial statements and disclosures are in compliance with GAAP and DOL requirements

Determine that investments comply with ERISA and plan documents

Test income allocations to participants Make sure-

– 5% of net asset disclosure is made– certification footnote is included in financial statements

which references what information was covered by the certification

134

135

Limited Scope Auditor’s Responsibilities

Proper presentation and disclosure– Inquire if plan’s certified investments are valued at

fair value as of the end of the plan year – Inquire as to the mythology for valuing plan

investments to determine if footnote disclosures are complete and accurate

– Inquire if plan investments include securities lending

135

136

Limited Scope Auditor’s Responsibilities

Participant Income Allocation Testing Tested in limited scope audit as allocations are

not certified Consider using investment returns for month or

quarter Some firms testing only allocations of interest

and dividends Cannot solely rely on a SOC 1 Type 2 Report

– A SOC 1 Type 2 Report can be used to reduce testing but need to document reliance on such report

136

137

Impact of ASU 820Limited Scope Audits

ASU 820 Fair Value Measurements-requires a better understanding of the custodial pricing processes– Requires communication with the trustee or

custodian to determine pricing methodologies used in order to facilitate disclosure of Level 1, 2 & 3 pricing inputs

– Requires an understanding of the nature of the investment, whether it is a partnership interest, an illiquid security, etc.

•137137

138

Hard To Value Investments in a Limited Scope Audit

Obtain an understanding as to the methodology for determining the fair value of the investments

Inquire of the plan sponsor if the value stated in the trust statements is based on values as of the financial statement date

If the certification does not cover the hard to value investments then full scope audit procedures will need to be performed for those investments or modify report per AG ¶ 7.77

Inquire as to securities lending arrangements

138

139

Limited Scope vs. Full Scope

Audit Procedures Limited Scope Full Scope

Confirm assets directly with custodian X

Agree the certified investment information to the Plan’s financial statement

X

Year-end market value testing and leveling X

Investment Transaction Testing X

Test investment income allocation to participants X X

Determine that the Plan’s financial statement and disclosures are in compliance with GAAP

X X

139

140

A-1 Retirement and Investment Services

The information provided on the enclosed reports is a summary of the financial activity for MRM 401(k) Plan for the plan year ended December 31, 2009. Life Savings Insurance Company certifies that the forgoing statement furnished pursuant to 29 CFR 2520.103-5(c) is complete and accurate in accordance with its business records.

Vice PresidentAccount Management ServicesA-1 Retirement and Investment Services

140

141

Issues with Certifications

Not certified as to fair value Fair value not certified as of the plan’s year

end Regulations only require certification to be

based upon the ordinary books and records of the trustee or custodian—No mention of “fair value”

Regulations require investments to be reported on Form 5500 at fair value regardless of what is certified

Limited scope may not be appropriate

141

142

"Ordinary Business Records"

DOL Regulations require:"…such information as is contained within the ordinary business records of the bank, trust company, or similar institution and is needed by the plan administrator to comply with the requirements of section…“

“Ordinary business records” may be best-available values, which may or may not be fair value!

142

143

Limited Scope Audit Issues

Indicators that there may be additional information required– Cost equals fair value for certain investments– Fair value for certain investments have not

changed for several years– Description of investments on the Schedule of

Assets is inconsistent with footnote for investments

– Certain investments are not included in the certification

143

144

Limited ScopeAuditor’s Responsibilities

If something unusual comes to your attention –bring matter to the attention of the plan management

If material discrepancies noted, plan management should investigate and consider:– Requesting trustee/custodian to correct and either

recertify or amend the certification– If information is excluded, the plan administrator is

responsible for proper valuation and reporting– Engage the auditor to perform full-scope audit and/or

full-scope procedures, as appropriate See Audit Guide ¶ 7.75

144

145

Investment information Not Prepared in Conformity With GAAP and DOL

Regulations

If plan administrator is unable to determine the fair value of alternative investments, the financial statements may not be in accordance with GAAP and DOL Requirements:– Auditors report would have to be modified

Add emphasis of matter paragraph to auditors' report for a limited scope engagement which would discuss the effects of not applying adequate valuation procedures

The auditor cannot perform valuation procedures for the plan in order to determine the fair value of alternative investments without impairing the auditors independence

145

146

Questions????

147

Commitments, Contingencies,

Administrative Expenses and Completion Procedures

Audit Guide Chapter 12

148

Learning Objectives

As a result you should be able to plan and perform appropriate audit procedures with respect to commitments and contingencies, administrative expenses and audit completion procedures for a defined contribution plan and defined benefit plan

149

Professional Standards

AU 337, Inquiry of a Client’s Lawyer Concerning Litigation, Claims and Assessments

AU 333, Client Representations FASB ASC 440 and 450, Commitments and

Contingencies AU 316, Consideration of Fraud in a Financial

Statement audit AU 339, Audit Documentation AU 380, Communication with Those Charged with

Governance AU 325, Communicating Internal Control Related

Matters Identified in an Audit FASB ASC 855, Subsequent Events

150

Commitments and Contingencies

Audit Procedures Discuss possible issues with plan sponsor or

third party administrator Review meeting minutes for contingent

liabilities Review plan sponsor’s financial statements Analyze legal expenses for contingencies or

prohibited transactions Obtain a client representation letter Inquire concerning any investigations by

regulatory authorities Send inquiry letter to plan’s ERISA counsel

151

Legal Letters

When management has consulted legal counsel regarding plan matters

Sent near the end of field work or an updated letter may be required

Should be sent to ERISA counsel Inquire regarding litigation, claims or assessments

and plan qualification issues Obtain audit inquiry letter from in-house counsel, if

applicable If no consultation include a statement in management

representation letter Legal letter inquiry should include example language

in Audit Guide

152

Administrative Expenses

Audit Objectives– Expenses in accordance with plan agreement– Properly classified and recorded

Audit Procedures– Are expenses properly authorized– Expenses in accordance with service contracts– Fees comply with service provider agreements

Hot button for DOL

153

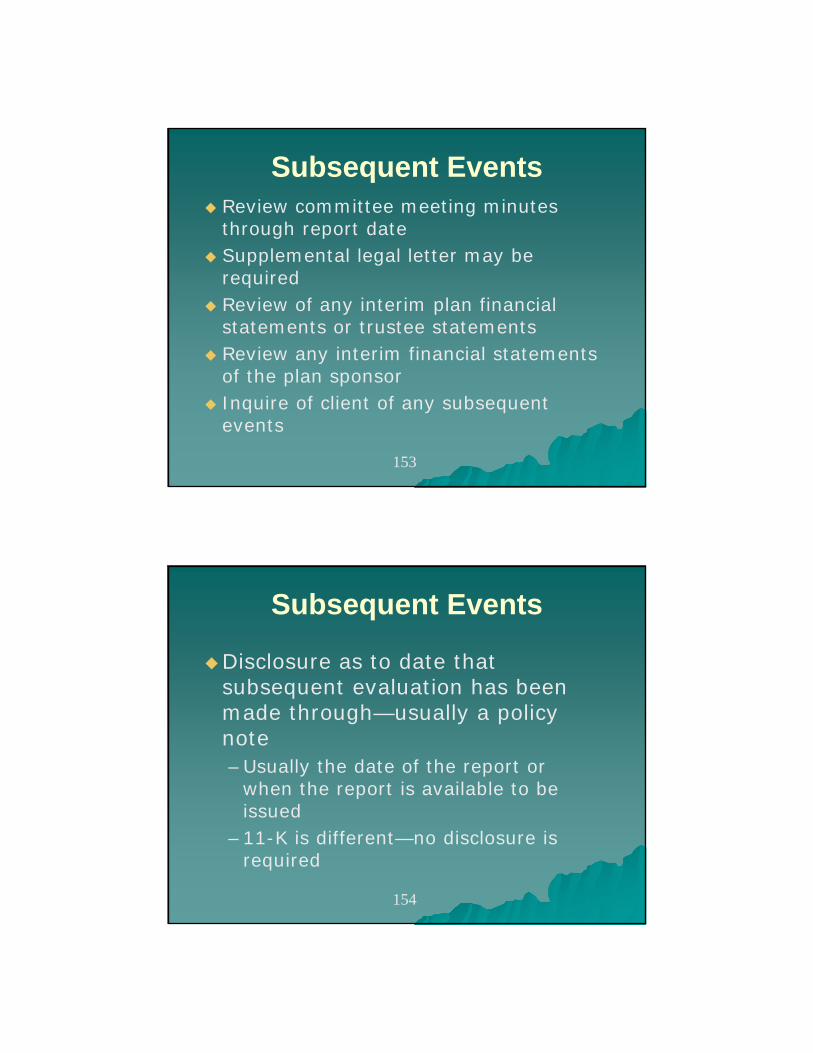

Subsequent Events Review committee meeting minutes

through report date Supplemental legal letter may be

required Review of any interim plan financial

statements or trustee statements Review any interim financial statements

of the plan sponsor Inquire of client of any subsequent

events

154

Subsequent Events

Disclosure as to date that subsequent evaluation has been made through—usually a policy note–Usually the date of the report or

when the report is available to be issued

–11-K is different—no disclosure is required

155

Types of Subsequent Events

Recognized Subsequent Events--Type 1

Nonrecognized Subsequent Events--Type 2

Examples– Mergers– Termination– Spin-offs– Changes in service providers– Plan amendments

156

Specific Plan Representations

Plan amendments Intentions to merge or terminate the plan Omissions from participant data Acceptance of actuarial assumptions Whether the plan is qualified under the IRC Existence of related party and party-in-

interest transactions Investments valued at fair value Timely deposits of employee deferrals Compliance testing

157

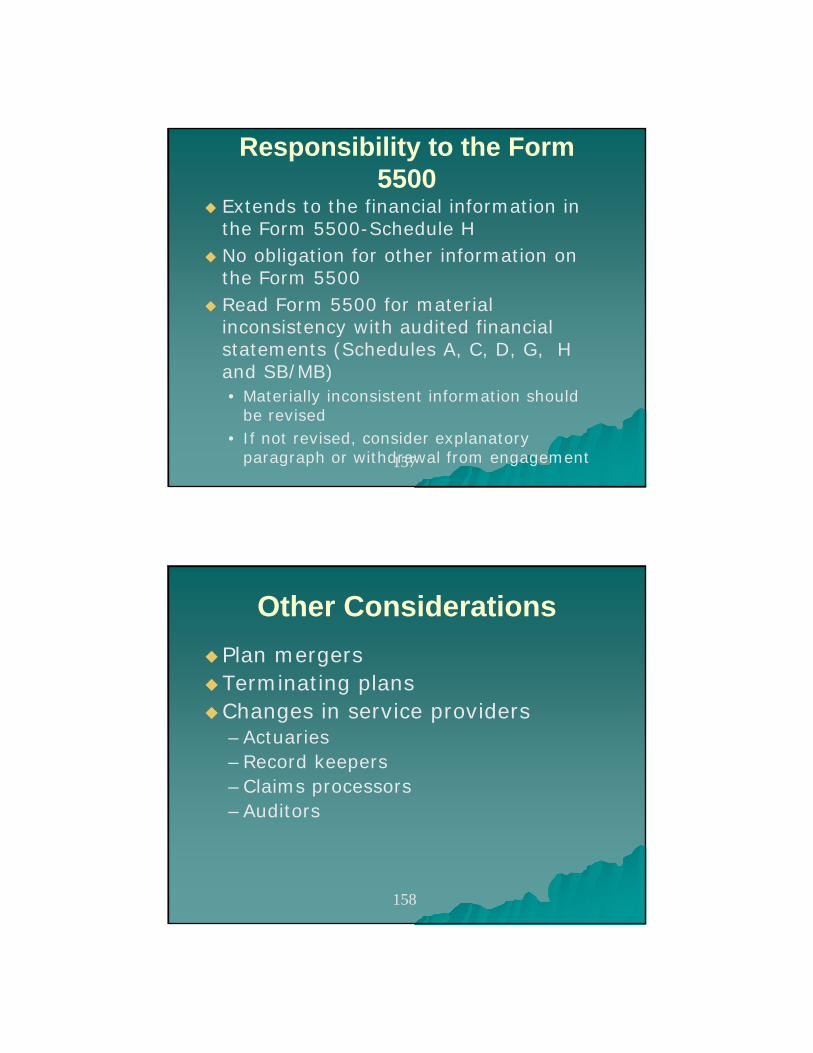

Responsibility to the Form 5500

Extends to the financial information in the Form 5500-Schedule H

No obligation for other information on the Form 5500

Read Form 5500 for material inconsistency with audited financial statements (Schedules A, C, D, G, H and SB/MB)• Materially inconsistent information should

be revised• If not revised, consider explanatory

paragraph or withdrawal from engagement

158

Other Considerations

Plan mergersTerminating plansChanges in service providers

–Actuaries–Record keepers–Claims processors–Auditors

159

Communications with those Charged with Governance

AU 380 (SAS 114) requires communication regarding The auditors responsibility under GAAS An overview of the planned scope and timing

of the audit Significant findings from the audit such as

– Uncorrected misstatements– Risks of fraud identified– Judgments as to quality of the plans accounting

principles– Significant difficulties encounter during the audit– Disagreements with management, if any

160

Internal Control Related Matters

AU 325 (SAS 115), Communicating Internal Control Related Matters Identified in an Audit–Must be a written communication–Should be made not later than 60

days following the report release date

–Communicate significant deficiencies and material weaknesses

161

Review Questions

1.What types of things must be communicated to those charged with governance?

2.What procedures should be performed for administrative expenses which are deemed to be immaterial?

3.What are the new requirements for subsequent event disclosures?

162

Questions????

163

Audit GuideChapters 2, 3 and 13Appendix D & E

Reporting and Disclosure Requirements

164

Learning Objectives

As a result you should be able tounderstand the financial statement reporting and disclosure requirements with respect to benefit plans and thereporting required for the Form 5500.

165

Reporting and Disclosure Requirements

Authoritative LiteratureRequired Financial StatementsFinancial Statement Disclosure

RequirementsERISA and DOL Reporting

Requirements

166

Authoritative Literature and Other Tools

FASB ACC 960, 962 and 965AICPA Audit Guide—current editionAICPA Audit Risk Alert—current

editionTrends and TechniquesAICPA Disclosure GuidesEFAST-2 Form 5500 filings

167

Supplementary and Other Information

SAS No. 118, Other Information in Documents Containing Audited Financial Statements

SAS 119, Supplementary Information in Relation to the Financial Statements as a Whole

SAS 120 No. 120, Required Supplementary Information

168

SAS 118 Addresses auditor’s responsibility in relation to

other information in documents containing audited f/s and the auditor’s report there on

Auditor’s opinion on the f/s does not cover other information, and the auditor has no responsibility for determining whether such information is properly stated (absent a separate requirement)

Auditor required to read the other information for material inconsistencies between the audited financial statements and other information

169

SAS 119 Addresses the auditor’s responsibility when

engaged to report on whether “supplementary information” is fairly stated, in all material respects, in relation to the f/s as a whole

Information presented outside basic f/s excluding required information

Does not apply to DOL schedules In order to opine on whether information is

fairly stated in relation to the f/s as a whole– Auditor to determine if certain conditions are met– Auditor to perform certain procedures (using the

same materiality level as used during the f/s audit)

170

SAS 119 Applicability Full Scope Audit—generally engaged to

report on whether the supplementary information is fairly presented in relation to the basic financial statements (SAS 119)– Revised paragraph about supplemental

schedules in the auditor’s report—see audit guide

No changes to the Form 11-k auditor’s report when filing with the SEC under the PCAOB standards—two sets of standards

171

Applicability of SAS 118 ERISA limited scope engagements

– Disclaimer being issued on the basic financial statements—therefore precluded from expressing an “in relation to” opinion on the supplementary information

– Because the DOL requires the supplementary information to be presented with the financial statements, those schedules would be considered other information in documents containing audited financial statements

– Since likely not engaged to issue an opinion Auditor still required to follow SAS 118 See revisions in the Risk Alert

172

Defined Benefit Pension Plans

Statement of Net Assets Available for Plan Benefits

Statement of Changes in Net Assets Available for Plan Benefits

Information regarding the actuarial present value of accumulated plan benefits

Information regarding year-to-year change in accumulated plan benefits

173

Defined Benefit Health and Welfare Plans

Statement of Net Assets Available for Plan Benefits

Statement of Changes in Net Assets Available for Plan Benefits

Information regarding the plan’s benefit obligations

Information regarding year-to-year change in the plan’s benefit obligations

174

Defined Contribution Pension Plans and Health and Welfare

Plans

Statement of Net Assets Available for Plan Benefits

Statement of Changes in Net Assets Available for Plan Benefits

175

Disclosure Requirements

Plan’s accounting policies, including a description of methods and significant assumptions used to determine the fair value of investments

A brief general description of the plan agreement, including its contribution, vesting and allocation provisions, disposition of forfeitures and benefit provisions the year

Significant plan amendments adopted during the year and the effect of such amendments on net assets if significant either Individually or in the aggregate.

176

Disclosure Requirements Policy regarding the purchase of insurance contracts

that have been excluded from plan assets and the related income

Federal income status of the plan if a favorable determination letter has not been obtained or maintained. (ERISA plans require disclosure whether or not a tax ruling or determination letter has been obtained)

Investments that represent 5% or more of total net assets as of the end of the year

For ESOP plans, investments pledged to secure debt of the plan as well as a description of the provisions regarding the release of such investments

177

Disclosure Requirements

Participant-directed investment programs—amounts relating to these programs can be disclosed as a separate line item on the face of the financial statements

Amounts allocated to accounts of persons who have elected to withdraw from the plan but have not yet been paid as of year end

Significant related-party transactions Significant subsequent events—need date

included in footnotes

178

Disclosure Requirements-DB Plan

If the amendments were adopted after the date of the accumulated benefit information, and accordingly their effect was not included in the calculation, this fact should be stated

Significant assumptions used in determining the actuarial present value of accumulated plan benefits or benefit obligations, including any significant changes in the method or assumptions during the year.

179

Disclosure Requirements-DB Plan The funding policy and any changes in the

policy during the year. Disclose their funded status with respect to

any applicable minimum funding requirements and whether those requirements have been met.

If a minimum funding waiver has been granted or is pending by the IRS or if a rehabilitation program has been established, that fact should be disclosed

A brief description of the benefit priority and PBGC coverage in the event of plan termination

180

ERISA and DOL Reporting Requirements

Comparative Statement of Net Assets Available for Plan Benefits

Description of accounting principles Variances from GAAP Differences between financial

statements and Form 5500 Supplemental schedules Additional information attached to the

Form 5500

181

Form 5500 Reporting Supplemental Schedules—(All part of Schedule G except Schedules 4a, 4i and 4j)Schedule G Part I “Schedule of Loans or Fixed

Income Obligations in Default or Classified as Uncollectible”

Part II “Schedule of Leases in Default or Classified as Uncollectible”

Part III “Nonexempt Transaction”

182

Supplementary Schedules

“Schedule H, line 4a-Schedule of Delinquent Participant Contributions” (include participant loans)

“Schedule H, line 4i-Schedule of Assets (Held at End of the Year)”

“Schedule H, line 4i-Schedule of Assets (Acquired and Disposed of Within the Plan Year)” (schedule rarely required)

“Schedule H, line 4j-Schedule of Reportable Transactions”– For participant directed transactions this schedule is

not required

183

Example Financial Statements and Footnote

Disclosures

Audit GuideAppendix D, E, and F

184

Review Questions

1. List some specific disclosures for defined benefit plans?

2. Which statements are required to be comparative for a DC plan and for a DB plan?

3. Would your answer be different if beginning of the year valuation was performed for a DB plan?

185

Questions????

186

Party-in-Interest Transactions, Prohibited Transactions, and Plan Tax Status

Audit Guide Chapters 11 & 12

187

Learning Objectives

Upon completion of you should have an understanding of the following:• Who is a party-in-interest• How to identify a party-in-interest and a

prohibited transaction• What audit procedures to perform and

impact on the auditor’s report• Auditor’s responsibility related to Plan

tax status

188

Generally Accepted Auditing Standards

• Auditor’s cannot be expected to provide assurance that all related party transactions will be discovered

• Auditor’s need to be aware of the possible existence of material related party transactions as well as potential party-in-interest transactions that could impact the financial statements

189

Professional Standards

Related Party Transactions• FASB ASC 850, Related Party

Disclosures• AU 54, Illegal Acts by Clients

Prohibited Transactions• AU 317, Illegal Acts by Clients• FASB ASC 450, Accounting for

Contingencies• AU 316, Consideration of Fraud in a

Financial Statement Audit

190

Party In Interest Transactions

ERISA Section 3(14)• Fiduciaries or employees of the plan• Person providing services to the plan• Employer whose employees are

covered by the plan• Person who owns 50% or more of

such an employer or relatives of such persons

191

FASB ASC 850 - Related Party Disclosures

• Related parties are also Parties-in-Interest

• Related party transactions may not necessarily involve accounting recognition

• Related party transactions do not necessarily violate ERISA

192

ERISA section 406(a)

Forbids certain transactions between the plan and parties in interest• Sale, exchange or lease of property• Loan or other extension of credit (includes untimely

deposits to the trust of employee salary deferrals)• Furnishing of goods, services or facilities• Transfer of plan assets for the benefit of a party-in-

interest• Acquisition of employer securities or real property in

violation of the 10 percent limitationNot having a written service agreement with a service provider could be a prohibited transaction

193

Party In Interest Transactions

Impact the following audit areas:• Planning and performing the audit to

identify all material party-in-interest transactions

• Required disclosures• Possible report modifications if a

prohibited transaction has occurred

194

Related Party and Party in Interest Transactions

Existence of Related Parties and Parties in Interest• Evaluate the plan sponsor’s procedures for identifying, accounting

and reporting such transactions• Request names of related parties and parties-in-interest• Review transactions with such parties• Review prior year work papers containing transactions or inquire

of predecessor auditors• Review regulatory filings • Inquiries of plan management regarding any related party or

party-in-interest transactions• Review agreements with service providers

195

Identifying Party-In-Interest Transactions

• Provide audit staff with names of related parties• Review committee minutes• Review correspondence with regulatory agencies• Review invoices from legal council• Look for large, unusual transactions or

nonrecurring transactions• Review conflict of interest statements obtained

from plan management• Review transactions with the plan’s major service

providers, investees, etc.

196

Audit Implications for PTs• Obtain an understanding of the transaction

– How it occurred– Sufficiency of other information

• Inquire of management at a level above those involved

• Consult plan’s ERISA counsel or other specialists• Apply similar procedures as for related party

transactions or illegal acts• Test reasonableness of amounts being disclosed• Auditor has a responsibility to deal with all

prohibited transactions regardless of materiality

197

Prohibited Transactions

Reporting Implications• Financial impact of fines, penalties and receivables

for money being paid back to the plan• Adequacy of financial statement disclosures and

supplemental schedule • Contingencies may also need to be disclosed• Consider the implications of the prohibited

transaction in relation to other aspects of the audit• Prohibited transactions must be disclosed on

Schedule G, Part III of the Form 5500• Financial statement materiality does not apply to

supplemental schedules

198

Late Deposits

• Not reported on Schedule G• Late deposits recorded on Line 4a of

the Form 5500• Reported on Supplemental Schedule

199

Audit Implications for Prohibited Transactions

• AU 317, requires the auditor to be alert to prohibited transactions

• AU 316, requires the auditor to assess and document the risk of material misstatement

• Auditor has the responsibility to deal with all prohibited transactions, regardless of quantitative materiality

200

DOL’s Voluntary Correction Program

• Eligible for immediate relief from payment of certain excise taxed imposed by IRS

• Not required to report the corrected transaction as nonexempt on supplemental schedules of Form 5500

• Full compliance with the program will result in the DOL’s issuance of a “No Action Letter” and no imposition of penalties on the plan sponsor

• Disclosure is necessary if VFC has not yet been approved—consult plan’s legal counsel

201

Prohibited Transactions

• Proper disclosure not made:– If material, express a qualified or

adverse opinion on the supplemental schedules

– If not material, modify report on the supplemental schedules by disclosing the transaction

– If disclosure is not made, consider withdrawing from the engagement

202

Prohibited Transactions

Audit implications of prohibited transactions:• Reliability of management’s

representations• Impact on specific control procedures• Assure that appropriate plan management

is adequately informed of prohibited transactions

• Include in SAS 114 and 115 letters

203

Plan’s Tax Status• Plan financial statements generally do

not have accrued income taxes or a provision for income tax as qualified plans are granted special tax status

• Audit Objectives– Is the trust qualified under the Internal Revenue

Code– Is plan operating in compliance with the plan

document– Do any transactions impact plan qualification– Recording of asserted or unasserted claims– UBIT—impact of FASB ASC 740-10 (Fin 48)

204

Plan’s Tax Status

Audit Procedures• Review IRS determination letter

– 403(b) plans do not have a determination letter program yet

• Review current and subsequent plan amendments

• Inquire about plan’s operations or changes which may impact tax status including compliance testing

• Review results of other audit work for impact on tax status

205

Required Disclosures

• FASB Interpretation No. 48 Accounting for Uncertainty in Income Taxes– Required for all plans as of December 31,

2009– Main provisions require

Income taxes paid by the entityManagement’s determination of the taxable status

of the entity All tax positions need to be considered

• Disclosures– Whether an uncertainty exists or not– Open tax years

206

Required Compliance Testing

• Minimum coverage test• Minimum participation tests• Average deferral limits—not required for

403(b) plans• Average contribution percentage limits• Annual additions limitation• Top heavy test• Exclusive benefit rule• Diversification of certain employer security

holdings

207

Other Areas for Audit Emphasis

Plan Design Plan Amendments Operational Issues Eligibility testing Contributions testing Distributions testing Use of forfeitures and vesting test work Income and expense allocation test

work

208

What if Operational Issues?

Audit Procedures• Have client quantify the error as to dollar

impact on financial statements• Determine if the amount is material to the

financial statements and/or if disclosure is required

• Include in management representation letter how and when the error will be corrected

• Consider inclusion in SAS 114/115 letters• Depending on the nature and magnitude of

the error modification of the report may be necessary

209

Review Questions

1.What is the materiality threshold for reporting a prohibited transaction?

2.What responsibility does the auditor have for the discrimination testing?

3.Are the auditors a related party and/or a party in interest?

210

Questions????

Top Related