Languages

Pages

Legal

U.S. employment situation: September 2013

Release date: October 22, 2013

July’s growth demonstrates the

resilience of the labor market

U.S. employment situation: July 2015 August 7, 2015

July 2015 employment summary

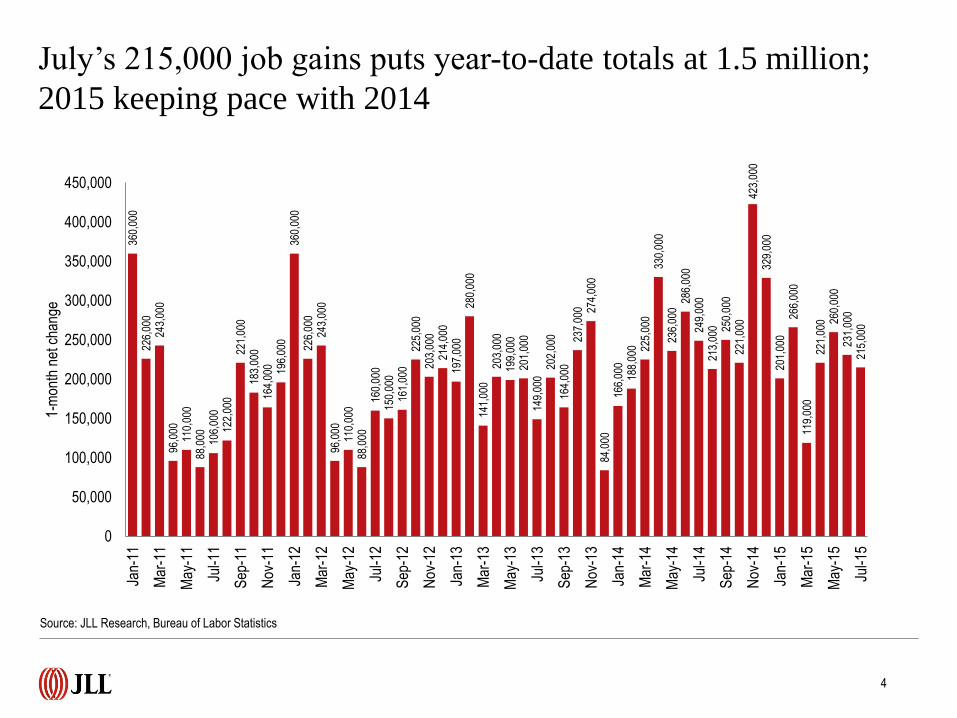

• After a bumpy beginning to 2015, the labor market continued its steady and upward trajectory with the addition of 215,000 net new jobs in

July. While slightly lower than the previous few months, year-to-date job creation now rests at 1.5 million and is in line with 2014.

• Unemployment remained unchanged at 5.3 percent, while unemployment for college graduates continues to hover between 2.5 and 2.7

percent, slightly less than half the national rate. However, labor force participation remains relatively flat across demographic segments,

particularly for high-school graduates.

• Sustained employment and a looming talent crunch in major markets becoming more apparent have enabled wages to grow even more

above the rate of inflation, in part due to the ongoing collapse in energy prices. Private-sector wages are up 2.1 percent year-on-year, while

those in professional and business services are growing even faster at 2.6 percent.

• Office-using industries contributed 59,000 jobs to May’s growth, much lower than the past two months. This more muted level of growth

was not limited to the office-using sectors: durable goods, which had previously been powering improvements in manufacturing, contracted

moderately in July.

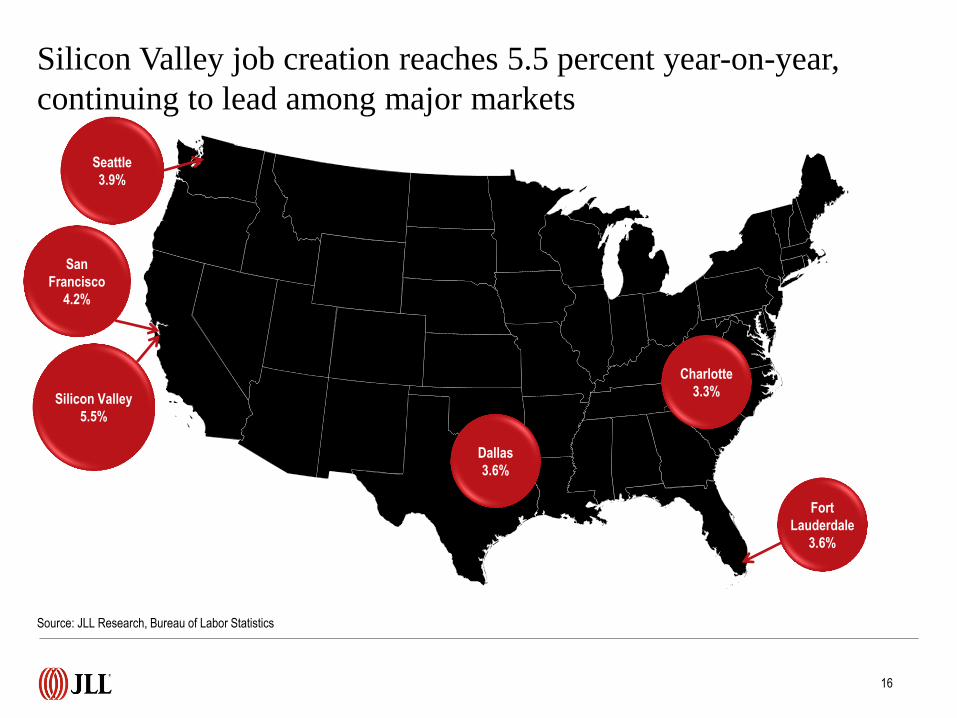

• At the market level, Silicon Valley saw 5.5-percent annual job growth, among the highest rates recorded for a JLL-tracked market this cycle.

Tech-heavy markets such as San Francisco and Seattle as well as the rapidly growing Sun Belt markets such as the Carolinas, South

Florida and Texas remain leaders, although Houston is beginning to see a sharp slowdown in employment growth to 1.9 percent, compared

to the nearly 4.0-percent growth just one year ago.

- Even slower-growth markets, particularly those in the Great Lakes, Midwest and Northeast, posted small but significant bumps in annual

growth rates.

Source: JLL Research, Bureau of Labor Statistics

July 2015 labor market at a glance

+215,000

1-month net change

+2,915,000

12-month net change

+782,000

10-year average annual growth

Source: JLL Research, Bureau of Labor Statistics

5.3%

Unemployment rate

-90bp

12-month change in unemployment

7.0%

10-year average unemployment

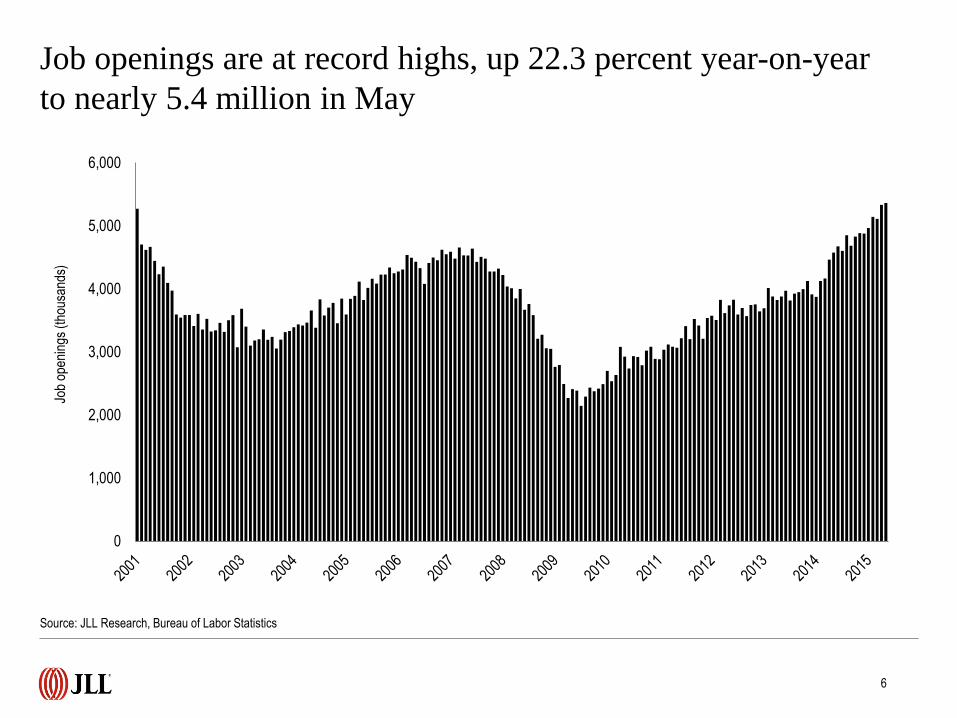

5,334,000

Job openings

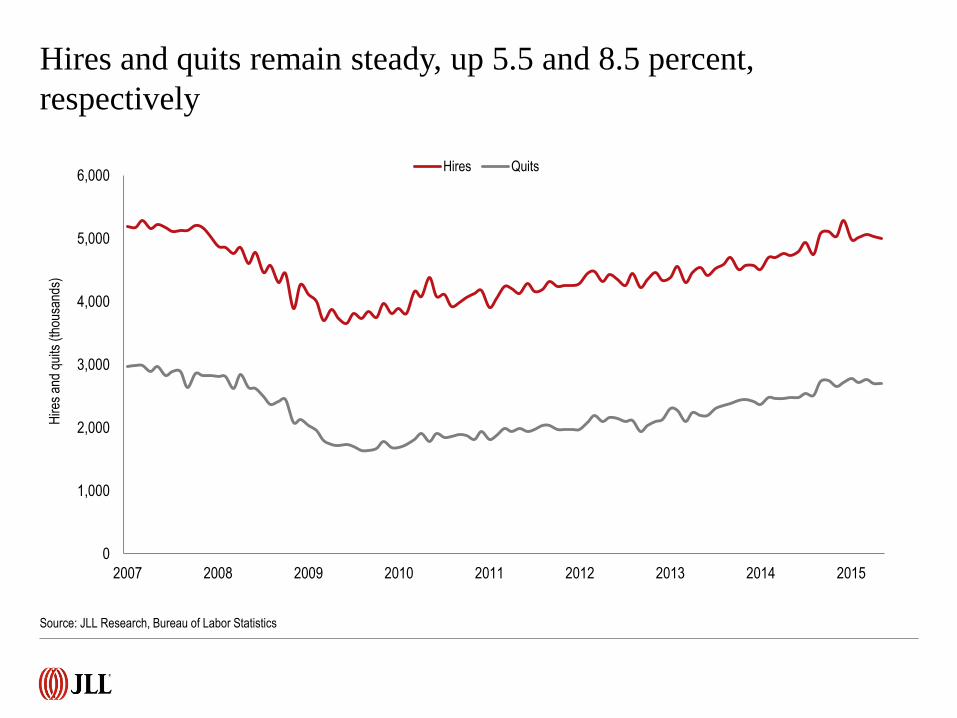

5,000,000

Hires

2,699,000

Quits

July’s 215,000 job gains puts year-to-date totals at 1.5 million;

2015 keeping pace with 2014 36

0,00

0 22

6,00

0 24

3,00

0 96

,000

11

0,00

0 88

,000

10

6,00

0 12

2,00

0 22

1,00

0 18

3,00

0 16

4,00

0 196,

000

360,

000

226,

000

243,

000

96,0

00

110,

000

88,0

00

160,

000

150,

000

161,

000

225,

000

203,

000

214,

000

197,

000

280,

000

141,

000

203,

000

199,

000

201,

000

149,

000

202,

000

164,

000

237,

000 27

4,00

0 84

,000

16

6,00

0 18

8,00

0 225,

000

330,

000

236,

000

286,

000

249,

000

213,

000 25

0,00

0 22

1,00

0 42

3,00

0 32

9,00

0 20

1,00

0 26

6,00

0 11

9,00

0 22

1,00

0 260,

000

231,

000

215,

000

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

Jan-

11

Mar

-11

May

-11

Jul-1

1

Sep

-11

Nov

-11

Jan-

12

Mar

-12

May

-12

Jul-1

2

Sep

-12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep

-13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep

-14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-1

5

1-m

onth

net

cha

nge

4

Source: JLL Research, Bureau of Labor Statistics

Unemployment stable at 5.3 percent as job growth matches

volatility in labor market

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

-1,000.0

-800.0

-600.0

-400.0

-200.0

0.0

200.0

400.0

600.0

Une

mpl

oym

ent r

ate

(%)

1-m

onth

net

cha

nge

(tho

usan

ds)

Monthly employment change Unemployment rate

Source: JLL Research, Bureau of Labor Statistics

5

Job openings are at record highs, up 22.3 percent year-on-year

to nearly 5.4 million in May

Source: JLL Research, Bureau of Labor Statistics

6

0

1,000

2,000

3,000

4,000

5,000

6,000

Job

open

ings

(th

ousa

nds)

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

Con

sum

er c

onfid

ence

inde

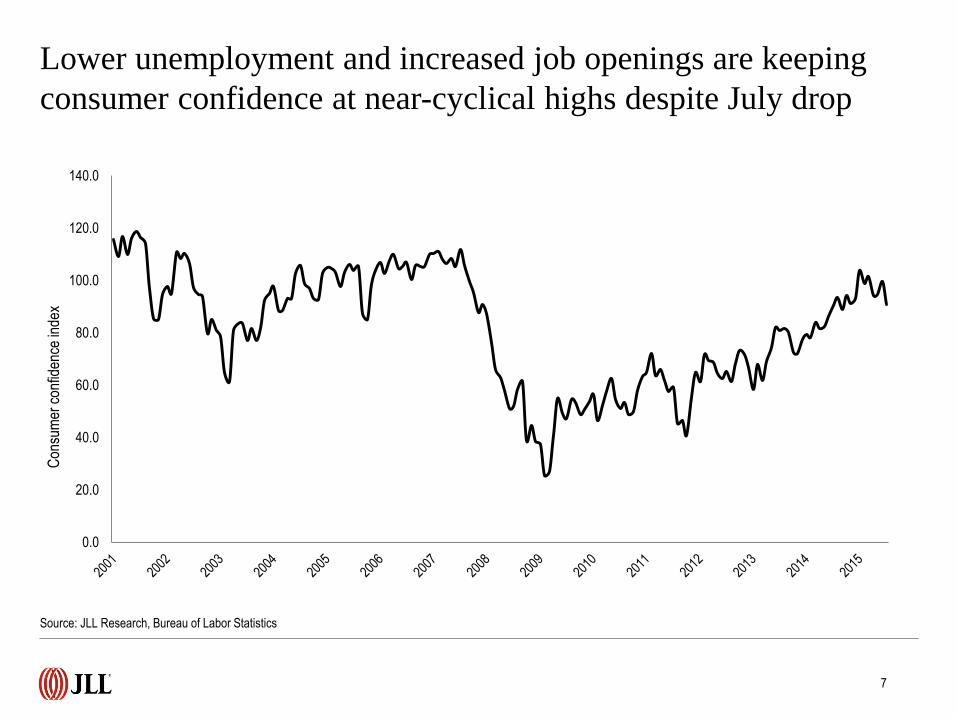

x Lower unemployment and increased job openings are keeping

consumer confidence at near-cyclical highs despite July drop

Source: JLL Research, Bureau of Labor Statistics

7

-8.9

-8.0

-4.0

-1.4

2.0

2.6

5.0

6.0

6.3

7.0

14.4

15.0

17.0

23.0

30.0

30.1

35.9

37.0

40.0

-20 -10 0 10 20 30 40 50

Temporary help services

Durable goods

Mining and logging

Motor vehicles and parts

Information

Utilities

Government

Construction

Wholesale trade

Other services

Transportation and warehousing

Manufacturing

Financial activities

Nondurable goods

Leisure and hospitality

Health care and social assistance

Retail trade

Education and health services

Professional and business services

1-month net change (thousands)

Monthly growth by industry more muted, with PBS, education,

health and retail growing at similar rates

Source: JLL Research, Bureau of Labor Statistics

8

PBS

Education and health

Retail trade

All other subsectors

Top three

subsectors

responsible for

52.6 percent of

monthly

growth.

A sharp uptick in non-durable goods pushed goods-producing

employment to its highest monthly gain in 2015 (+17,000)

-1,000.0

-800.0

-600.0

-400.0

-200.0

0.0

200.0

400.0

600.0

2008 2009 2010 2011 2012 2013 2014 2015

1-m

onth

net

cha

nge

(tho

usan

ds)

Goods-producing Service-providing

Source: JLL Research, Bureau of Labor Statistics

9

-64.0

11.6

39.5

53.0

62.0

62.0

80.0

84.4

97.0

125.3

145.5

156.0

159.0

231.0

321.7

436.0

526.6

572.0

666.0

-200 0 200 400 600 800

Mining and logging

Utilities

Motor vehicles and parts

Information

Nondurable goods

Government

Other services

Wholesale trade

Durable goods

Temporary help services

Transportation and warehousing

Financial activities

Manufacturing

Construction

Retail trade

Leisure and hospitality

Health care and social assistance

Education and health services

Professional and business services

12-month net change (thousands)

PBS

Education and health

Leisure and hospitality

Retail trade

Manufacturing

Financial activities

All other jobs

Mining and logging continues to see annual job losses due to

unstable oil prices; PBS leads with 666,000 new jobs created

Source: JLL Research, Bureau of Labor Statistics

10

Core subsectors added 76.2 percent

of all jobs over the past 12 months.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Une

mpl

oym

ent (

%)

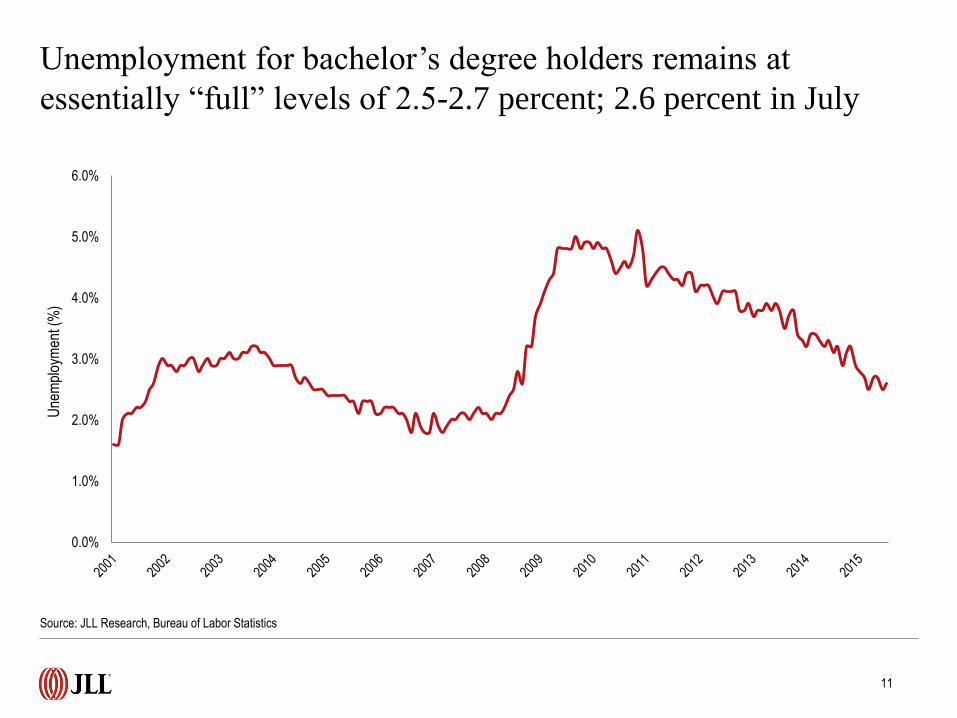

Unemployment for bachelor’s degree holders remains at

essentially “full” levels of 2.5-2.7 percent; 2.6 percent in July

Source: JLL Research, Bureau of Labor Statistics

11

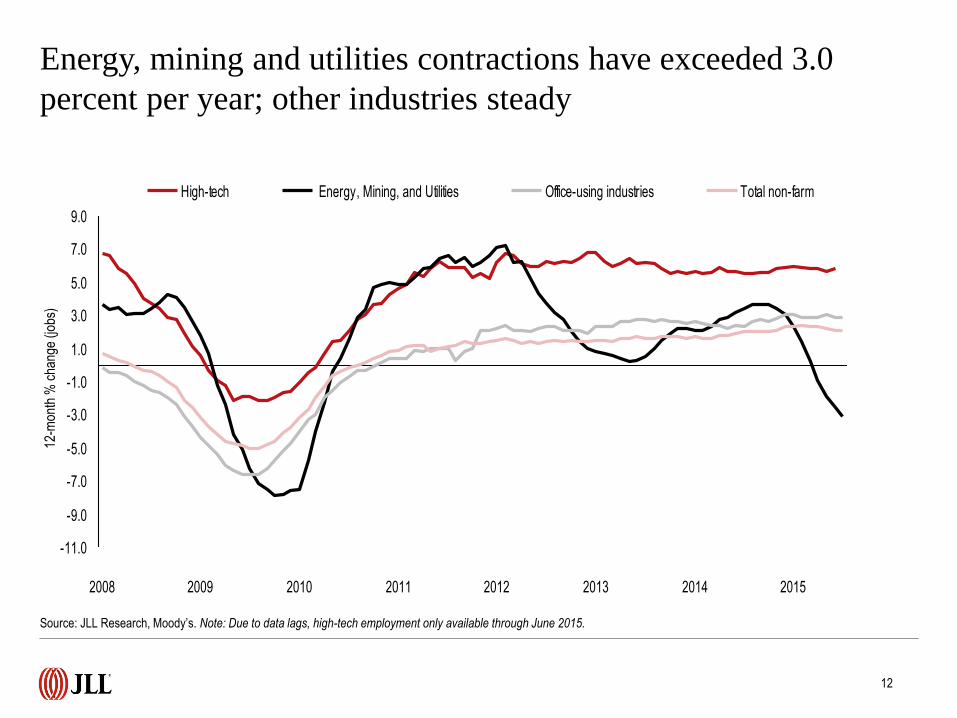

Energy, mining and utilities contractions have exceeded 3.0

percent per year; other industries steady

-11.0

-9.0

-7.0

-5.0

-3.0

-1.0

1.0

3.0

5.0

7.0

9.0

2008 2009 2010 2011 2012 2013 2014 2015

High-tech Energy, Mining, and Utilities Office-using industries Total non-farm

Source: JLL Research, Moody’s. Note: Due to data lags, high-tech employment only available through June 2015.

12

12-m

onth

% c

hang

e (jo

bs)

Tech job creation continues to hover slightly below 6.0 percent

due to sustained industry demand Year-on-year percent employment growth

Source: JLL Research, Bureau of Labor Statistics

13

Weekly claims over the course of 2015 have averaged just

285,000 and have remained relatively flat

Source: JLL Research, U.S. Department of Labor

14

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000

600,000

650,000

700,000

Cla

ims

Initial claims 4-week moving average

0

1,000

2,000

3,000

4,000

5,000

6,000

2007 2008 2009 2010 2011 2012 2013 2014 2015

Hire

s an

d qu

its (

thou

sand

s)

Hires Quits

Hires and quits remain steady, up 5.5 and 8.5 percent,

respectively

Source: JLL Research, Bureau of Labor Statistics

Silicon Valley job creation reaches 5.5 percent year-on-year,

continuing to lead among major markets

Source: JLL Research, Bureau of Labor Statistics

16

Silicon Valley

5.5%

San

Francisco

4.2%

Fort

Lauderdale

3.6%

Seattle

3.9%

Dallas

3.6%

Charlotte

3.3%

Some East Coast and Midwestern markets are still growing

slower, but have seen a small bump of late

17

Source: JLL Research, Bureau of Labor Statistics

Hampton

Roads

1.3%

St. Louis

1.4%

Milwaukee

1.5%

Cleveland

1.7%

Philadelphia

1.1%

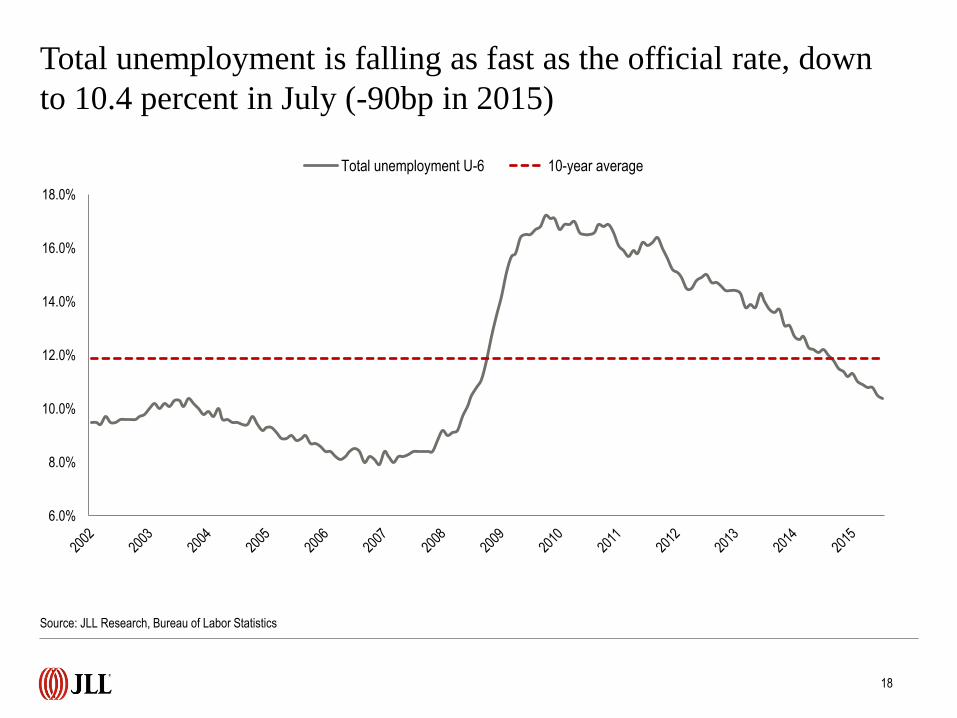

Total unemployment is falling as fast as the official rate, down

to 10.4 percent in July (-90bp in 2015)

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Total unemployment U-6 10-year average

Source: JLL Research, Bureau of Labor Statistics

18

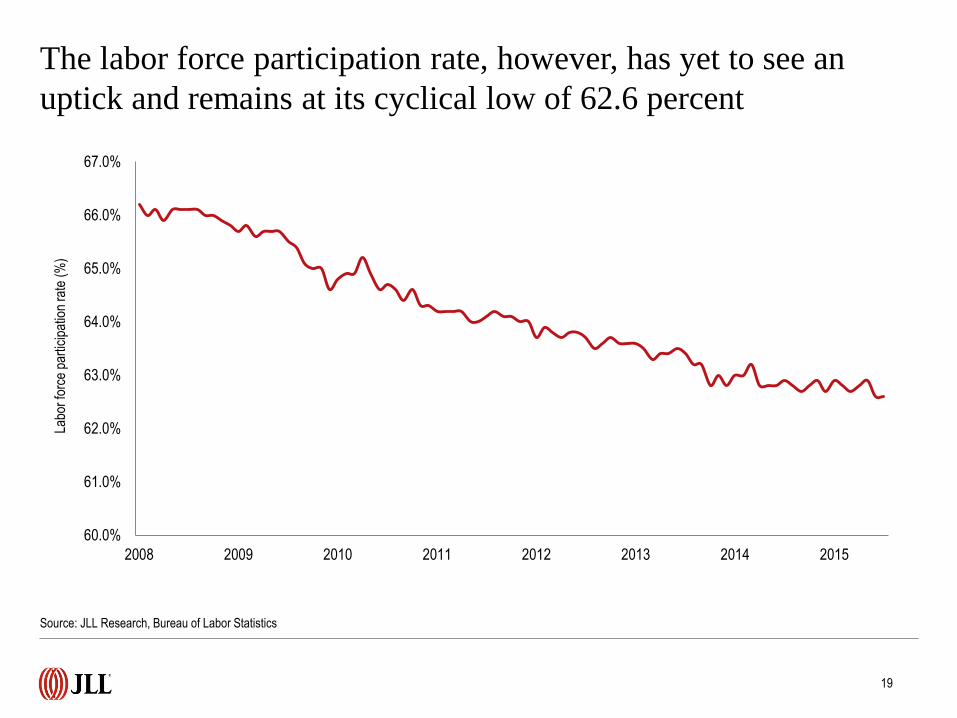

The labor force participation rate, however, has yet to see an

uptick and remains at its cyclical low of 62.6 percent

Source: JLL Research, Bureau of Labor Statistics

19

60.0%

61.0%

62.0%

63.0%

64.0%

65.0%

66.0%

67.0%

2008 2009 2010 2011 2012 2013 2014 2015

Labo

r fo

rce

part

icip

atio

n ra

te (

%)

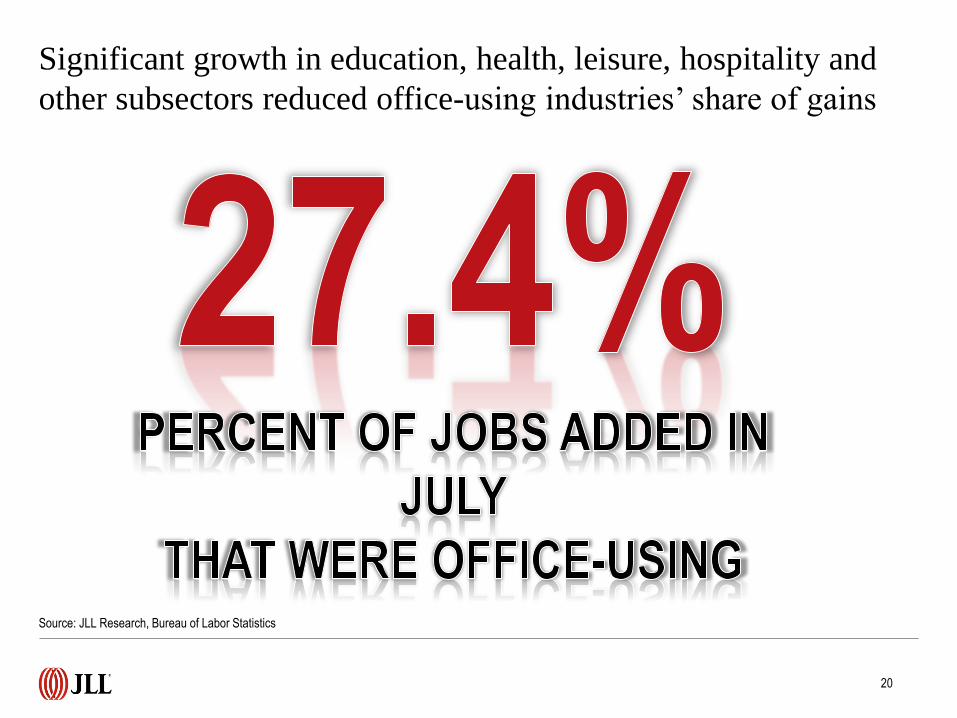

Significant growth in education, health, leisure, hospitality and

other subsectors reduced office-using industries’ share of gains

Source: JLL Research, Bureau of Labor Statistics

20

PBS’ slowdown to 40,000 new jobs was likely a monthly

aberration; financial activities steady at 17,000 new jobs

-300

-250

-200

-150

-100

-50

0

50

100

150

200

2009 2010 2011 2012 2013 2014 2015

Information Professional and business services Financial activities

Source: JLL Research, Bureau of Labor Statistics

21

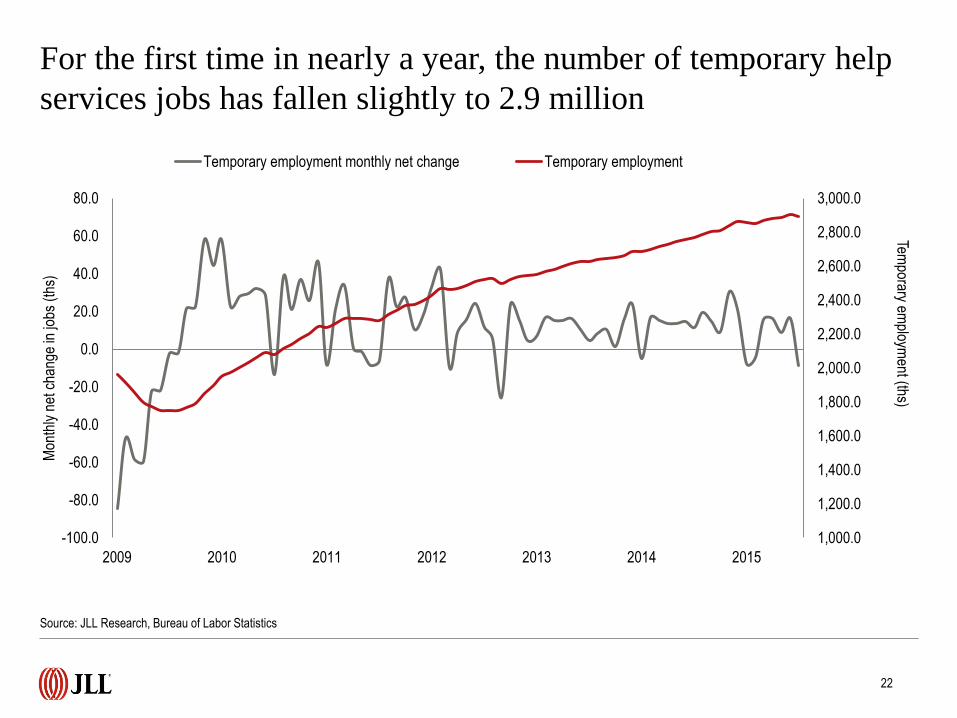

For the first time in nearly a year, the number of temporary help

services jobs has fallen slightly to 2.9 million

1,000.0

1,200.0

1,400.0

1,600.0

1,800.0

2,000.0

2,200.0

2,400.0

2,600.0

2,800.0

3,000.0

-100.0

-80.0

-60.0

-40.0

-20.0

0.0

20.0

40.0

60.0

80.0

2009 2010 2011 2012 2013 2014 2015

Mon

thly

net

cha

nge

in jo

bs (

ths)

Temporary employment monthly net change Temporary employment

Temporary em

ployment (ths)

Source: JLL Research, Bureau of Labor Statistics

22

©2015 Jones Lang LaSalle Research IP, Inc. All rights reserved. All information contained herein is from sources deemed reliable; however, no representation or warranty is made to the accuracy thereof.

For more information, please contact:

Ben Breslau

Managing Director - Americas Research

John Sikaitis

Managing Director - Office and Local Markets Research

Phil Ryan

Research Analyst – Office and Economy Research

Or, find more employment, business and real estate

research at jll.com.

>>> Click here to check it out.

Top Related