Languages

Pages

Legal

1

2Q082Q08

2

Agenda

Global View

Usiminas

Investments

Mining & Logistics

Financials

Corporate Governance and Social Responsability

3

Agenda

Global View

Usiminas

Investments

Mining & Logistics

Financials

Corporate Governance and Social Responsability

4

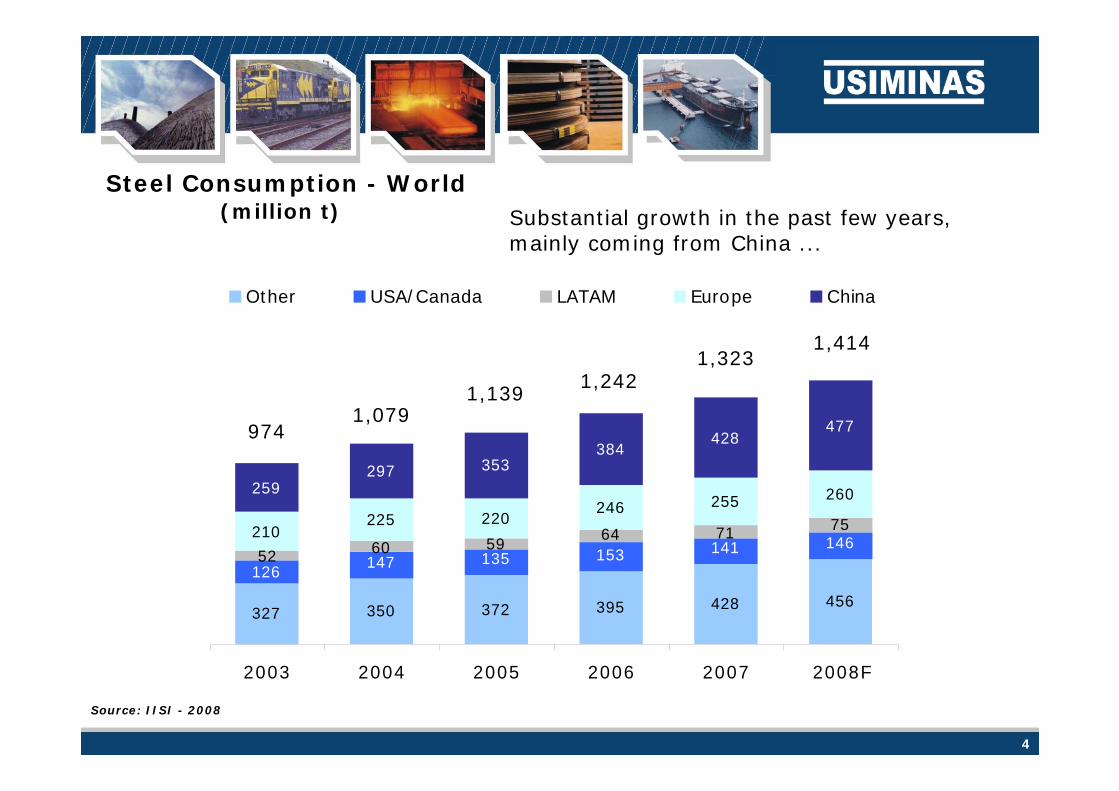

327 350 372 395 428 456

147 135 153 141 146210

225 220246 255 260259

297 353384

428477

126

757164596052

2003 2004 2005 2006 2007 2008F

Other USA/Canada LATAM Europe China

Steel Consumption - World(million t)

Source: IISI - 2008

Substantial growth in the past few years,mainly coming from China ...

9741,079

1,1391,242

1,3231,414

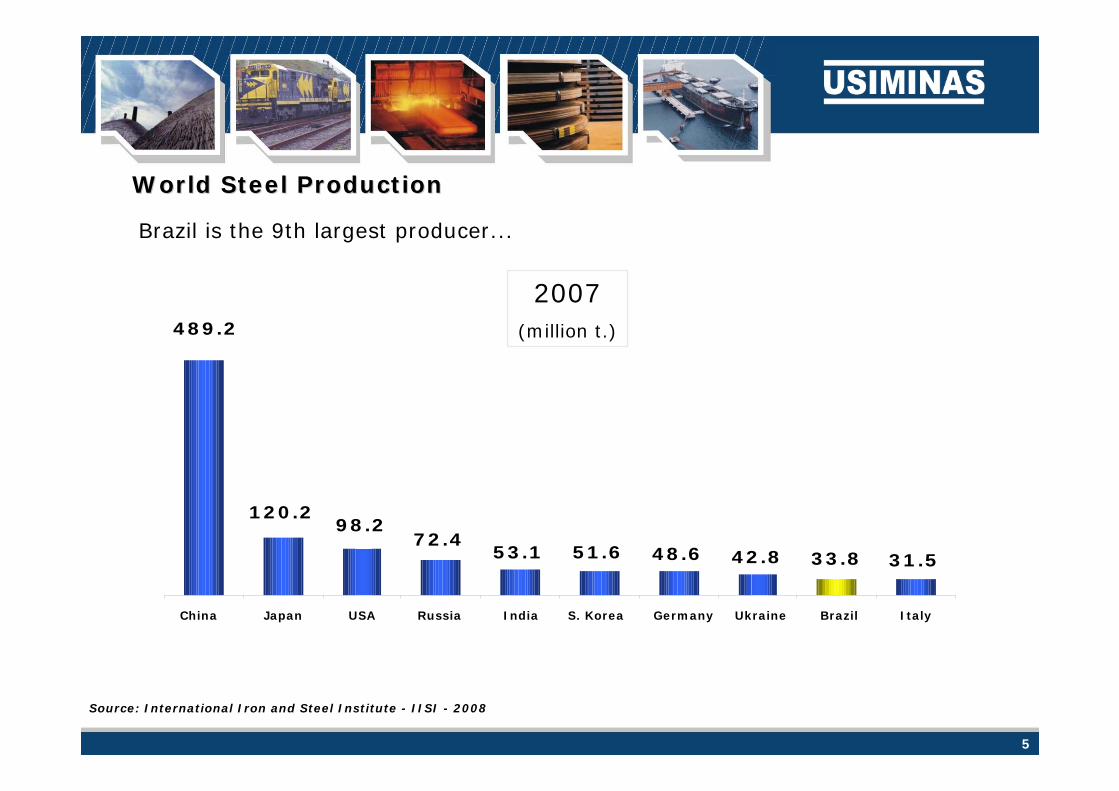

5

31.533.842.848.651.653.172.4

98.2120.2

489.2

World Steel ProductionWorld Steel Production

Brazil is the 9th largest producer...

Source: International Iron and Steel Institute - IISI - 2008

2007(million t.)

China Japan USA Russia India S. Korea Germany Ukraine Brazil Italy

6

416 449462 517 528 558 567 602 615 627 650 655

779

595

Brazil

Mexico India

Austra

lia CISUSA In

teg

China

South

Kor

ea (I

nteg

)Can

ada

Easte

rn E

urop

eW

ester

n Eur

ope

Japa

nUSA M

ini

Globa

l Ave

rage

Source: WSD, May 2008

Brazil has the lowest production cost in the world

Cost competitivenessCost competitiveness

Production Cost USD / ton(Slabs – May 2008)

7

Agenda

Global View

Usiminas

Investments

Mining & Logistics

Financials

Corporate Governance and Social Responsability

8

Usiminas System is the 36th largest producer in the world and 1st flat steel

producer in Latin America

Brazilian Steel ProductionBrazilian Steel Production

Top Brazilian Steel

Producers - 2007(33.8 million ton = Brazil’s crude

steel production)

Gerdau 21.5%

ArcelorMittal 30.3%

Usiminas 25.7%

Others6.7%

CSN 15.8%

Major Producers 2007(crude steel production - million t.)

20,2

20,5

22,8

22,9

26,5

28,6

32,8

33,8

34,5

116,4

8,735 - USIMINAS

10 - Wuhan

9 - US Steel

8 - Tangshan

7 - Jiangsu Shagang

6 - Tata Steel

5 - Baosteel

4 - Posco

3 - JFE

2 - Nippon Steel

1 - Arcelor Mittal

Source: IBS - 2008 and Metal Bulletin - 2008

9

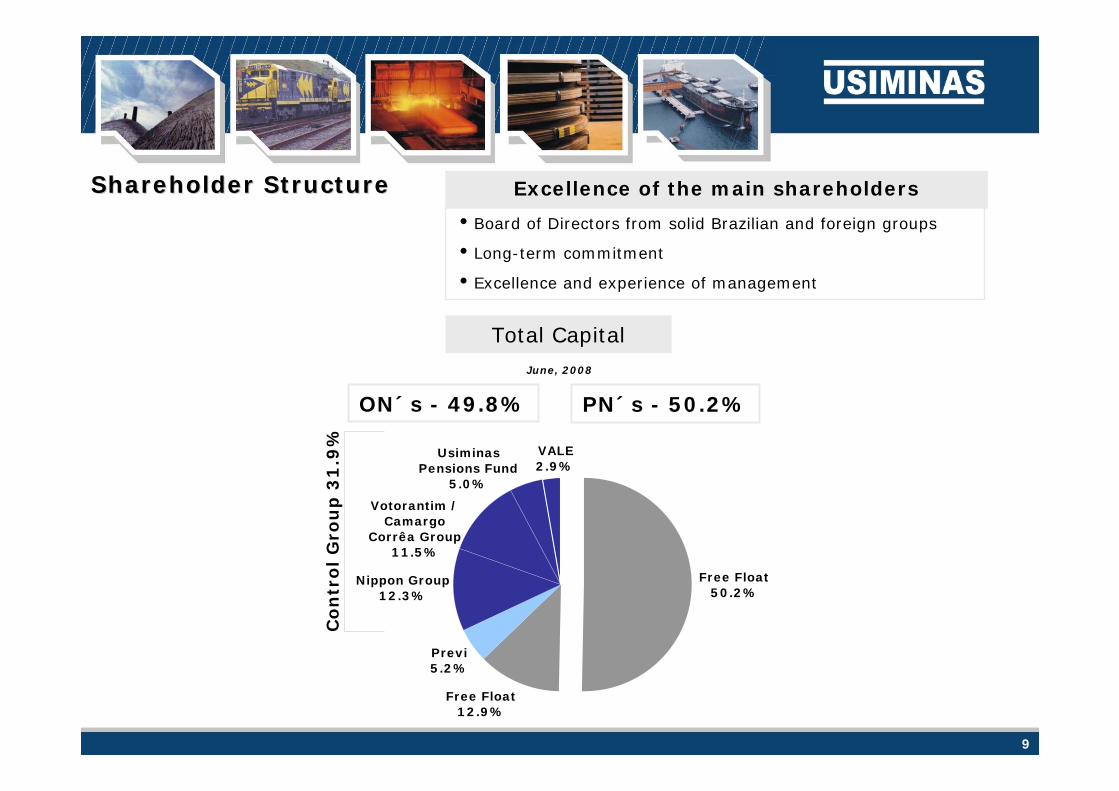

iBoard of Directors from solid Brazilian and foreign groups

iLong-term commitment

iExcellence and experience of management

Excellence of the main shareholdersShareholder StructureShareholder Structure

Free Float50.2%

Previ5.2%

Free Float12.9%

Votorantim / Camargo

Corrêa Group11.5%

Usiminas Pensions Fund

5.0%

VALE2.9%

Nippon Group12.3%

Co

ntr

ol

Gro

up

31

.9%

Total CapitalJune, 2008

PN´s - 50.2%ON´s - 49.8%

10

Usiminas is strategically locatedUsiminas is strategically locatedClose to major domestic marketsIron Ore Mine2 portsRailroad (MRS)

BrazilBrazil

(Minas Gerais)

(São Paulo) (Rio de Janeiro)

(Espírito Santo)

Praia MoleTerminal

IngáTerminal

CubatãoTerminal

São Paulo

BeloHorizonte

MRSJ. BonifJ. Bonifááciocio

PlantPlant

IntInt. C. CââmaramaraPlantPlant

Iron OreIron OreMinesMines

SantanaSantanaParaParaííso so PlantPlant

11

Operating Profit Margins %

High quality, value-added products (from slabs to coated products)

Among the lowest cost producers in the world

Source: Integer Research

Cost competitivenessCost competitiveness

2005 2006 2Q 2007

43,040,8 39,4

35,233,4

0

10

20

30

40

50

China SteelTata SteelUsiminas

Novolipetsk CSN

37,134,6

28,7 28,2 27,5

0

10

20

30

40

50

MagnitogorskTata Steel

UsiminasNovolipetskCSN

40,037,5

31,7 30,9 29,9

0

10

20

30

40

50

JSW SteelCSN

Novolipetsk UsiminasEzz

12

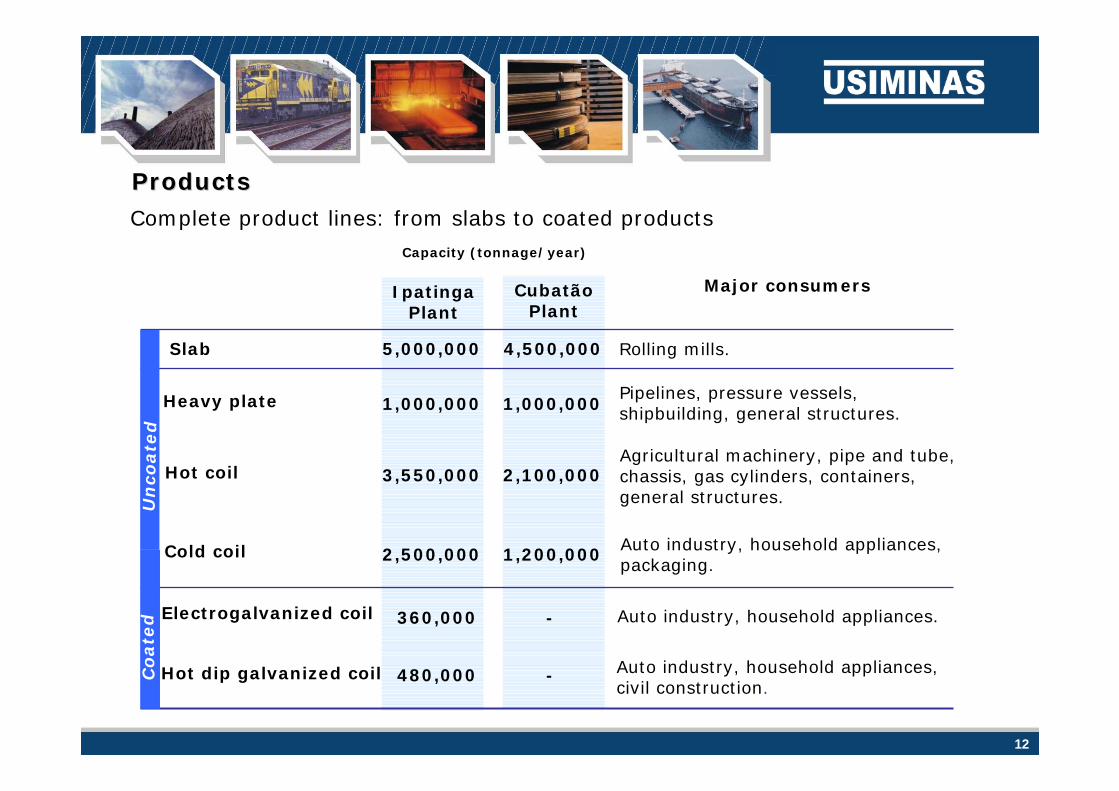

Major consumers

Heavy plate 1,000,000 1,000,000

Hot coil 3,550,000 2,100,000

Cold coil 2,500,000 1,200,000

-

-

Capacity (tonnage/year)

360,000

480,000

Slab 5,000,000 4,500,000

Electrogalvanized coil

Hot dip galvanized coil

Pipelines, pressure vessels,shipbuilding, general structures.

Agricultural machinery, pipe and tube,chassis, gas cylinders, containers,general structures.

Auto industry, household appliances, packaging.

Auto industry, household appliances.

Auto industry, household appliances,civil construction.

Rolling mills.

IpatingaPlant

CubatãoPlant

Products Products Complete product lines: from slabs to coated products

Un

coate

dC

oate

d

13

SalesSales

(million ton. )(million ton. )

Domestic market is a priority

As of June, 2008

84%

77%

67%

72% 69% 70%

67%

16%

23%

33%

28%31%30%

33%

2002 2003 2004 2005 2006 2007 1H08

7,722 7,7108,062

7,3487,945

Domestic Market Foreign Market

7,990

3,803

14

SalesSales

Domestic Market(Volume: 3.194 million t. - 1H08)

Combination of market leadershipand diversified customer base

reduces market risk

Spain14%

Argentina21%

USA14%

Indonesia2%

Bolivia3%

Mexico6%

Taiwan5%

South Korea7%

Chile11%

Germany6%

Others11%

Distributors23%

Autoparts18%

Auto Industry

13%

Civil Construction

6%

Household Appliances

2%

Industrial Equipment

9%

Elect-Equipment

4%

Packaging1%

Pipelines7%

Others10%

Small Diam. Tubes7%

International Market(Volume: 0.609 million t. - 1H08)

Diversified geographic sales

As of June, 2008

15

USIMINAS15%

Others17%

ArcelorMittal14%

CSN / Inal11%

Gerdau8%

Armco4%

Benafer4% Pires do Rio /

Cibraço4%

Tuper4%

Frefer4%

Tyco Metal4%

Zamprogna7%

Mangels4%

Steel Steel Distribution SectorDistribution Sector

Source: INDA - June, 2008

16

Market ShareMarket ShareDomestic Market (%) - 1H08Domestic Market (%) - 1H08Combination of market leadership and diversified customer base reduces market risk

* Flat Steel market: Usiminas System, CSN, Acesita and Arcelor Brasil.

49% Market share *

89%

29%

68%

66%

61%

10%

42%

47%

52%

60%

0,0% 20,0% 40,0% 60,0% 80,0% 100,0%

Distributors

Packaging

Civil Construction

Shipbuilding

Elect. Equipment

Household Appliances

Pipelines

Small Diam. Tubes

Autoparts

Auto Industry

TOTAL

OthersIpatinga and Cubatão Plants

48%

53%

40%

58%

39%

86%

33%

71%

100%

34%

12%

Flat Steel

As of June, 2008

17

BrazilBrazil’’s outlook - 2008s outlook - 2008

i Flat steel demand is expected to exceed 10%

Vehicle production may reach 3.400 million (Anfavea)

Industrial segment should outperform, growth to exceed 10%

Civil Construction growing activities

Source: IBS / Usiminas / Anfavea

8,576 8,90810,109

9,229 9,902

11,66912,922

2002 2003 2004 2005 2006 2007 2008E

+18%

1,793 1,8282,210

2,528 2,6112,973

3,400

2002 2003 2004 2005 2006 2007 2008E

+14%

Vehicle Production (1,000 vehicles)Flat Steel Demand (1,000 t.)

+11%

+14%

18

Investments & TechnologyInvestments & Technology

Commitment to the best technology

Partnership with Nippon Steel assures access to state-of-the-art technologyin steel production, including high value-added products

6th Technology Transfer Agreement with Nippon Steel, valid until 2009

425 received patents, of which 23 are international

150 researchers

Usiminas sells US$ 2 for each US$ 1of acquired technology.

19

Agenda

Global View

Usiminas

Investments

Mining & Logistics

Financials

Corporate Governance and Social Responsability

20

Production capacity5 million tons/yr

Start of works1st Half 2009

Start up 2.5 million t/yr in 20112.5 million t/yr in 2012

Coke plant2.0 million t/yr

Power plant250 MW

TOTALTOTAL Investments Investments: US$ 5.7: US$ 5.7 billion billion * ** Does not include investment in thermoelectric powerplant of approximately US$ 400 million

NewNew Slab Plant Slab Plant (Santana do Para (Santana do Paraííso)so)

21

LINE VOLUMEthsd tons

START UPFORECAST

PROJECT AMOUNT

UNIGAL II(Galvanized) 550 1st Half 2011 US$ 460 million

Heavy Plates 500 2nd Half 2010 US$ 500 million

Hot Rolled Coils 150 1st Half 2011 US$ 130 million

Other US$ 1.0 billion

Total Investments

Technology updating, cost savings and environmental control, with highlight for Coke

Plant 3 (+750kt/yr) and thermolectric powerplant (60 MW) in 2008

US$ 2.1 billion

Investments to serve “high value-added markets”

Investments

Intendente CIntendente Cââmaramara Plant (Ipatinga) Plant (Ipatinga)

22

LINE VOLUMEthsd tons

START UPFORECAST PROJECT VALUE

Hot Strip Mill 2,300 / 4,800 1st Half 2011 US$ 1.0 billion

BF1 Revamping 3.5 thsd/day => 4.5 thsd/day Concluded US$ 170 million

Continuous Casting Machine +350 / ano Concluded US$ 140 million

Other US$ 1.1 billion

Total Investments

Technology updating, cost savings and environmental control

US$ 2.4 billion

JosJoséé Bonif Bonifááciocio Plant (Cubat Plant (Cubatãão)o)

Investments

23

Plant / Equip CAPACITYtons

PROJECT VALUE

Concentration Plant 16 million US$ 650 million

Pellet Plant 7 million US$ 750 million

Mining Equip. - US$ 90 million

Railroad conection - US$ 60 million

Others - US$ 20 million

Acquisition 1,4 billion US$ 1,9 billion

Total Investments US$ 3.47 billion

MiningMining

Investments

24

Usiminas 2013Usiminas 2013Technical configurationTechnical configuration of the of the plants after plants after the theinvestment programinvestment program

Current After Current After

Slabs 5.00 5.00 4.50 4.80 ( 1)

Hvy Plate 1.00 1.50 1.00 1.00

Hot Strip 3.60 3.80 2.10 4.40 / 6.10 ( 2 )

Cold Strip 2.50 2.50 1.20 1.20

EG 0.36 0.36 - -

HDG 0.48 1.03 - -

Intendente Câmara Plant

million tons

José Bonifácio Plant Santana do Paraíso

New Plant

-

-

5.00

-

-

-

Source: Usiminas

(1) Concluded - May/2008(2) Additional expansion - up to 6.10 million tons/year

25

Agenda

Global View

Usiminas

Investments

Mining & Logistics

Financials

Corporate Governance and Social Responsability

26

J. Mendes is the last sizeable mining asset available in the Quadrilátero Ferrífero,a major iron ore province in Brazil

The acquired company is comprised of four mining sites with total expectedresources of 2.7 to 3.0 Bt and expected reserves of 1.1 to 1.8 Bt

Expected mine useful life of at least 25 years

Expected iron content between 46 and 48%

Current production level at roughly 5 MMt/year

J. Mendes brief overviewJ. Mendes brief overview

Somisa Global/Camargos J Mendes Pau de Vinho

27

0

10

20

30

2008 2009 2010 2011 2012 2013 2014

Pellet Feed

Sinter Feed

Lump

Mining AssetsMining Assets

Source: Usiminas

5.2 5.88.8 9.0

10.5

27.729.2

13.0

2.2

14.0

28

Mining AssetsMining Assets

AlthoughAlthough Ipatinga and Santana do Para Ipatinga and Santana do Paraííso doso do not have not havelogistics accesslogistics access to to be supplied by its be supplied by its mines mines on on ““SerraSerraAzulAzul””, Usiminas, Usiminas will have will have the the benefit benefit of of full full ““hedgehedge””against ironagainst iron ore ore price fluctuations price fluctuations

Mining29.2 MM t/yr

J. Bonifácio Plant10.3 MM t/yr

Dom. Mkt. Sales2.2 MM t/yr

Exports16.7 MM t/yr

Supply

IntendIntend. C. Cââmaramara Plant Plant8.0 MM t/8.0 MM t/yryr

Santana do ParaSantana do Paraíísoso8.0 MM t/8.0 MM t/yryr

JosJoséé Bonf Bonfáácio Plantcio Plant2.0 MM t/2.0 MM t/yryr

Hedge Hedge

Source: Usiminas

29

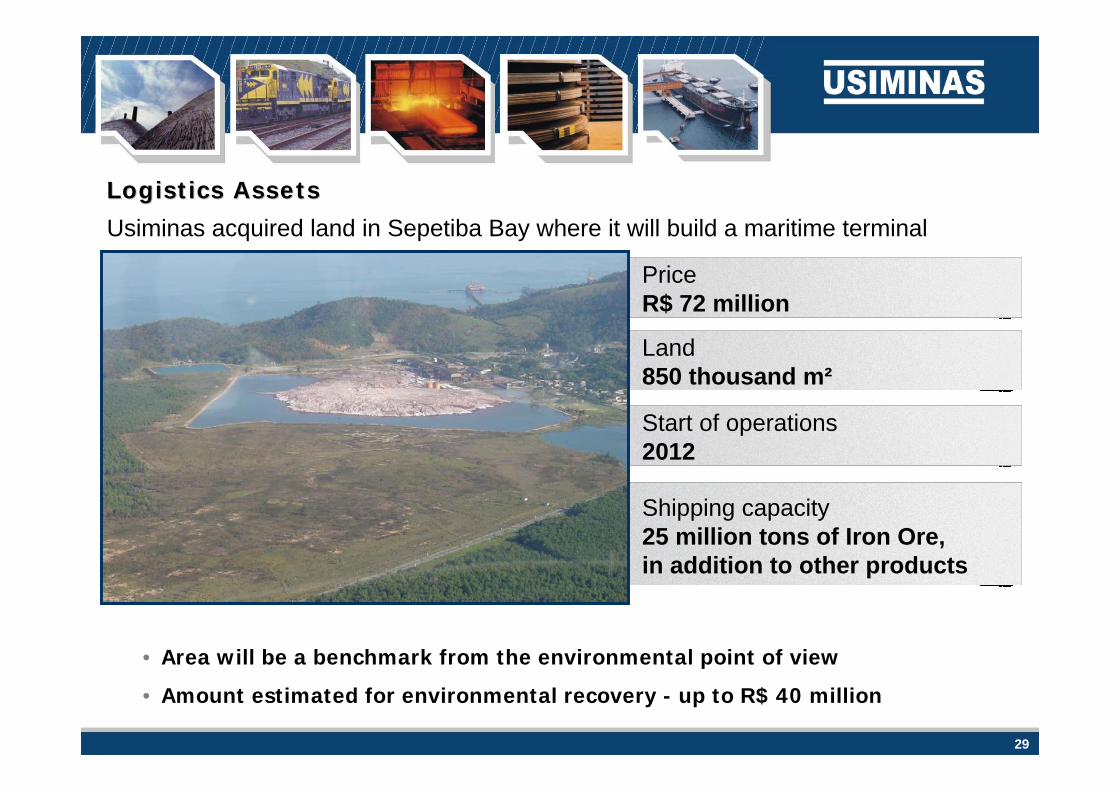

Start of operations 2012

Logistics AssetsLogistics Assets

• Area will be a benchmark from the environmental point of view

• Amount estimated for environmental recovery - up to R$ 40 million

PriceR$ 72 million

Land850 thousand m²

Shipping capacity25 million tons of Iron Ore, in addition to other products

Usiminas acquired land in Sepetiba Bay where it will build a maritime terminal

30

Agenda

Global View

Usiminas

Investments

Mining & Logistics

Financials

Corporate Governance and Social Responsability

31

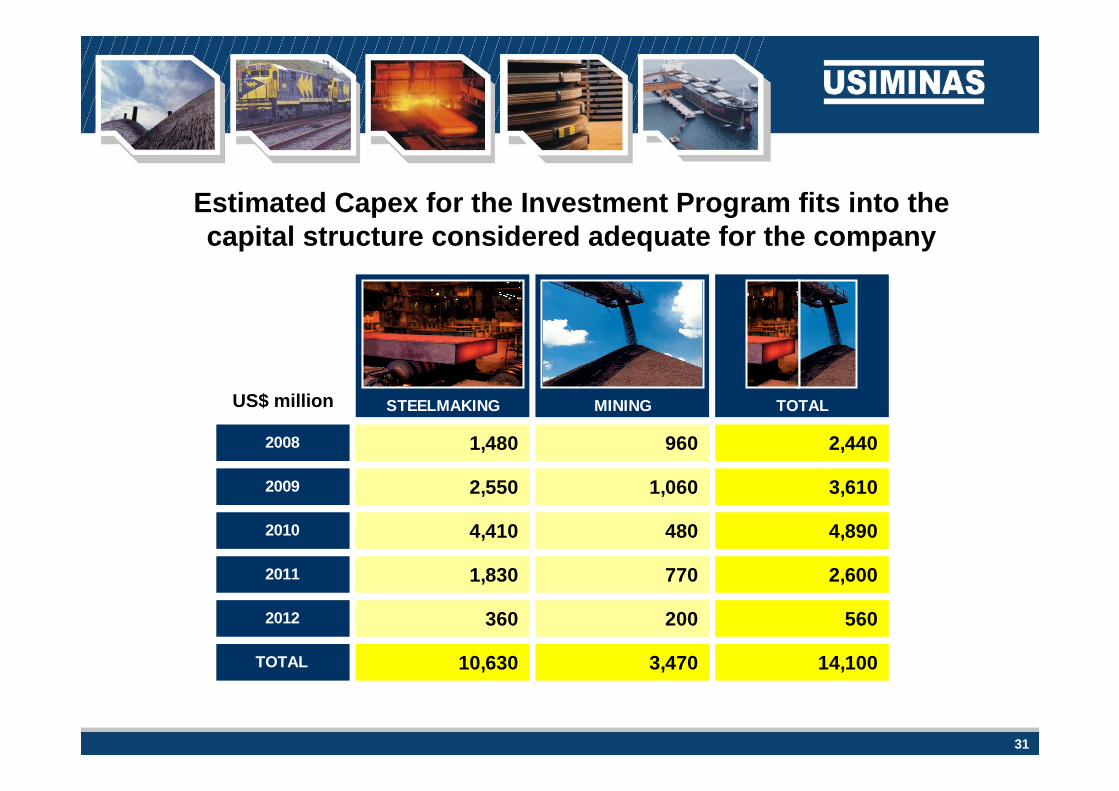

STEELMAKING MINING TOTAL

2008 1,480 960 2,440

2009 2,550 1,060 3,610

2010 4,410 480 4,890

2011 1,830 770 2,600

2012 360 200 560

TOTAL 10,630 3,470 14,100

Estimated Capex for the Investment Program fits into thecapital structure considered adequate for the company

US$ million

32

530734 657 831 999

1,9222,269

2,010

2,581

1.1811.602

31%35% 32% 35% 35%

46%42%

35% 36% 35% 37%

19991,81

20001,83

20012,35

20022,92

20033,07

20042,93

20052,44

20062,18

20071,95

1H071,75

1H081,74

Ebitda Ebitda Margin

AVG.R$/US$

ConsolidatedConsolidated Ebitda Ebitda

Investment return and market conditions have allowed consistent cash generation

US$ Million

As of June, 2008

33

83

2,841

238 434 358 284 473 460138 216 9

40986

Cash 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019on

Debt has an adequate maturity profile

SwapCDI5%

Long83%

US$ 2,659 M

Short17%

US$ 529 M

Foreign65%

Local35%

TERM CURRENCY

“Stand by Facility” - US$ 300 million

Note: Principal Values

US$ Million

Consolidated Debt MaturityConsolidated Debt Maturity

As of June, 2008

34

346(537)

355860

1,317

2,3342,491 0,1-0,20,20,40,72,3

3,1

0

1.000

2.000

3.000

4.000

20023,53

20032,89

20042,65

20052,34

20062,14

20071,77

1H081,59

Net Debt Net Debt / Ebitda

R$/US$

Total Net DebtTotal Net Debt

And have made it possible to considerably reduce debtUS$ Million

As of June, 2008

35

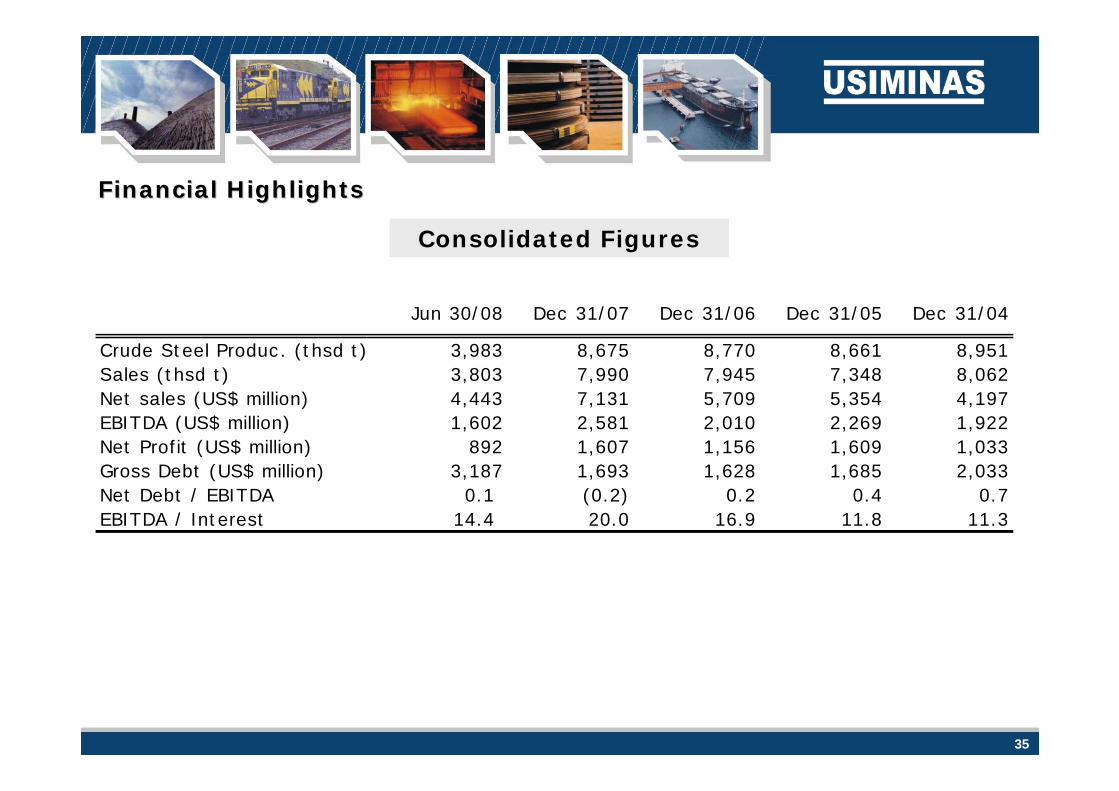

Consolidated Figures

Financial HighlightsFinancial Highlights

Jun 30/08 Dec 31/07 Dec 31/06 Dec 31/05 Dec 31/04

Crude Steel Produc. (thsd t) 3,983 8,675 8,770 8,661 8,951Sales (thsd t) 3,803 7,990 7,945 7,348 8,062Net sales (US$ million) 4,443 7,131 5,709 5,354 4,197EBITDA (US$ million) 1,602 2,581 2,010 2,269 1,922Net Profit (US$ million) 892 1,607 1,156 1,609 1,033Gross Debt (US$ million) 3,187 1,693 1,628 1,685 2,033Net Debt / EBITDA 0.1 (0.2) 0.2 0.4 0.7EBITDA / Interest 14.4 20.0 16.9 11.8 11.3

36

Agenda

Global View

Usiminas

Investments

Mining & Logistics

Financials

Corporate Governance and Social Responsability

37

Investments in Social ResponsibilityInvestments in Social Responsibility

Environmental Protection

Community

- More than R$ 2 billion invested in Ipatinga and Cubatão plantssince 1992.

- Usiminas and Cosipa were the 2nd and 3rd steel companies in theworld to be certified with ISO 14001.

- Fresh water recirculation rate above 93%.

- Green belt in Ipatinga area is 10 times aboverecommended level (World Health Organization).

- More than R$ 139 million invested in cultural activities in thelast fifteen years (tax incentives), involving 3 thousandartists and 200 thousand spectators.

- Construction of its 2nd hospital, one of three in Brazilaccredited by ONA (National Accreditation Organization),through USIMINAS Foundation, which is self sustaining. Bothhospitals provide healthcare to a region with 600 thousandinhabitants.

- Investment in education through São Francisco Xavier School,maintained by USIMINAS foundation, teaching more than 3thousand children and young people.

- The city of Ipatinga holds a “high standard of humandevelopment”, as defined by the UN - United Nations.

38

www.usiminas.com.br/ri

Investor Relations:Bruno Seno Fusaro (Head of IR) Matheus Perdigão Rosa Luciana Valadares dos [email protected] [email protected] [email protected].: + 55-31-3499-8772 Tel.: + 55-31-3499-8056 Tel.: + 55-31-3499-8619Fax: + 55-31-3499-9357

Gilson Rodrigues Bentes Diogo Dias Gonçalves Cosipa (São Paulo Office) [email protected] [email protected] Tel.: + 55-31-3499-8710 Tel.: + 55-11-5070-8980

Declarations relative to business perspectives of the Company, operating andfinancial results and projections, and references to the growth of the Company,constitute mere forecasts and were based on Management’s expectations inrelation to future performance. These expectations are highly dependent onmarket behavior, of Brazil’s economic situation, on the industry and oninternational markets, and are therefore subject to change.

ADRLevel I

Top Related