Languages

Pages

Legal

AN ANALYSIS OF THE VALUE CHAIN

OF QUINOA

Word count: 31.298

Korneel Merchiers Student number : 01205083

Promotor/ Supervisor: Prof. dr. Broos Maenhout

Commissioner: Drs. Thuzar Linn

Master’s Dissertation submitted to obtain the degree of:

Master of Science in Business Engineering: Operations Management

Academic year: 2016 - 2017

CONFIDENTIALITY AGREEMENT I declare that the content of this Master’s Dissertation may be consulted and/or reproduced, provided that the source is referenced. Name student : Korneel Merchiers Signature

I

Abstract

Agriculture plays an important role in less developed countries. People need agriculture to be

able to feed themselves and survive. Besides this, agriculture is also responsible for the em-

ployment and revenues of a lot of local populations in these countries. Often, the productivity

of agriculture in less developed countries does not live up to its full potential. Links and pro-

portions in the value chain are not optimal and are often fragmented. In such less developed

countries, farmers face the problem of having to sell their products at too low prices. On the

other hand, too high prices are set for consumers. When applied to Quinoa, it is clear that all

these facets occur. When farmers discovered that quinoa could be cultivated on less nutritious

fields, the production started to grow. The last couple of years, the production of quinoa is re-

ally booming. This resulted in the year 2013 being named as “The international year of quinoa”.

Although Peru and Bolivia are among the poorest nations in Latin-America, more than half of

the global supply of quinoa is actually coming from these countries. It was in the early 2000s

that Western nations discovered Quinoa. Since then, the demand has risen and so has the price.

Peru and Bolivia’s gross domestic product have only benefited from this. A question that often

comes to mind is “How long can Peru and Bolivia depend on quinoa as the agent of their pros-

perity?”. Quinoa-growing farmers could no longer afford to eat the crops themselves because

the price tripled but is now again decreasing. Domestic consumption has dropped and people

that migrated to cities in search of a better life are returning to their arid homeland to grow

quinoa to export. Furthermore, farmers and ranchers associations are starting up to influence

rural development policies. These are focused on associating small producers to face national

and international markets, supporting training and capacity building. Besides these, there are

of course independent farmers, processors, exporters, retail stores and other organizations who

have linkages with each other and thus influence the value chain.

The concrete problem of my thesis involves the analysis of the value chain of quinoa from a

less developed country like Peru to a developed country like Belgium (or Europe in general). In

the literature, both Peru and Bolivia are considered because, as a neighbouring country of Peru,

Bolivia is also an important producer of quinoa in the world, just like Peru. The objective is to

identify the different stages in the value chain as well as the different actors in each stage, de-

scribe the deficiencies occurring in the value chain and look for future possibilities to enhance

II

and upgrade the critical parts of the value chain. In such a way, the impact the actors have in

the value chain and on each other is estimated based on their constraints and margins. Fur-

thermore, the influence on the value that is created by them and the total and final value that

is delivered to the customer willing to buy quinoa is assessed. Our research is mainly based on

available literature and our own findings. Since Peruvian companies were not really willing to

share their production quantities and corresponding prices, averages and approximations were

taken to be able to provide an estimate for the country as a whole. This allowed us to come up

with a reliable value chain and some recommendations for the future of the quinoa industry in

Peru.

III

Acknowledgements

I would first like to thank my master’s dissertation supervisor, professor Maenhout, for his ap-

propriate assistance and guidance during the research and writing. I would also like to thank

Inge Overmeer, Agriculture Manager at Solid International, for helping me getting into contact

with organizations in Peru and providing me with significant information and data. Further-

more, I would like to acknowledge my aunt for helping me with Spanish translations and the

Peruvians that provided me with information. Finally, I want to express my gratefulness to my

parents and grandparents for supporting and encouraging me throughout the process of re-

searching and writing this thesis. This accomplishment would not have been possible without

each of the above.

Contents

I Literature 1

1 Quinoa 3

1.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

1.2 Social-Economic Context . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

1.2.1 Before 2000: Food Insecurity . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

1.2.2 Growth for the period 2000-2013 . . . . . . . . . . . . . . . . . . . . . . . . . . 5

1.2.3 Future . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

1.3 Characteristics of the International Quinoa Trade . . . . . . . . . . . . . . . . . . . . 10

2 Methods of Value Chain Analysis 15

2.1 Theory of Value Chain Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

2.1.1 Value Chain: Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

2.1.2 Creating Value in a Supply Chain Environment . . . . . . . . . . . . . . . . . 16

2.1.3 Importance of Value Chain Analysis . . . . . . . . . . . . . . . . . . . . . . . . 18

2.1.4 Global Value Chains . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

2.2 Methodology for Value Chain Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

2.3 Value Chains in Agriculture . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

2.3.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

2.3.2 Value Chain concepts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

2.3.3 Agricultural Value Chains and Food Security . . . . . . . . . . . . . . . . . . . 22

2.3.4 Value Chain Analysis to Achieve Nutrition Goals . . . . . . . . . . . . . . . . . 24

2.3.5 Global Value Chains in Agriculture . . . . . . . . . . . . . . . . . . . . . . . . . 25

2.4 Game Theory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

2.4.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27

2.4.2 Application of Game Theory in Agriculture . . . . . . . . . . . . . . . . . . . . 28

IV

CONTENTS V

2.5 Upgrading the Value Chain . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

2.5.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

2.5.2 "Future" Possibilities for Upgrading . . . . . . . . . . . . . . . . . . . . . . . . 33

II Case Study: Illustration 35

3 Examples of Value Chain Analysis 37

3.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

3.2 The Coffee Value Chain . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

3.2.1 Basic Coffee Supply Chain . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

3.2.2 Case Study: Coffee Value Chain from Nicaragua to Finland . . . . . . . . . . 39

3.3 The Cocoa Value Chain . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

III Case Study: An Analysis of the Value Chain of Quinoa 47

4 Socio-Economic Context 51

4.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

4.2 Population and Education . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

4.3 Participation in Economic Activity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

4.4 Social Impact by Outsiders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

4.5 Prospects for the Future . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

5 Characteristics of the Value Chain of Quinoa 57

5.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

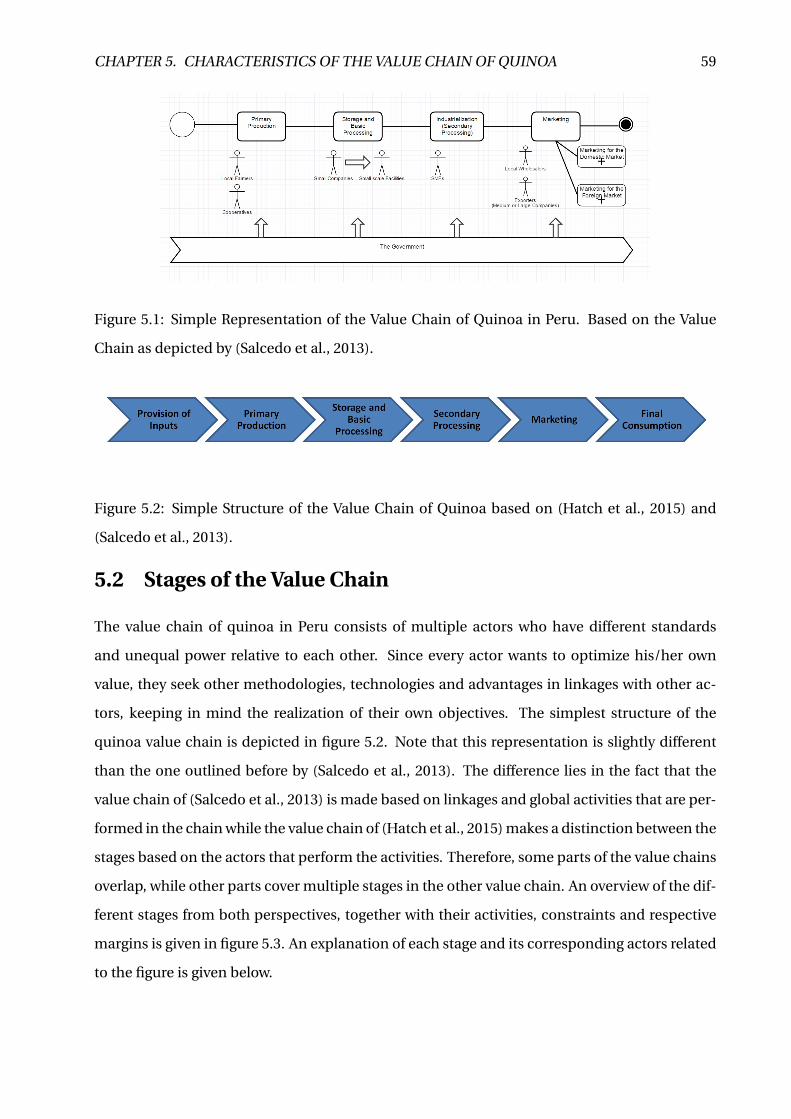

5.2 Stages of the Value Chain . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

5.2.1 Provision of Inputs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

5.2.2 Primary Production . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

5.2.3 Storage and Basic Processing . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

5.2.4 Industrialization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

5.2.5 Marketing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

5.2.6 Final Consumption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

5.3 Multi-Stage Actors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

5.3.1 COOPAIN . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

5.3.2 Vinculos Agricolas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

CONTENTS VI

5.3.3 De Guste Group SAC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

5.3.4 Avendaño Trading Company SAC . . . . . . . . . . . . . . . . . . . . . . . . . 70

5.3.5 Alisur SAC . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

5.3.6 The Government . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

5.3.7 Solid International - Solid Food Peru/Europe . . . . . . . . . . . . . . . . . . 71

5.4 Indirect Actors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 73

6 Analysis of the Value Chain of Quinoa 75

6.1 Assessing the Value . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

6.1.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

6.1.2 Qualitative Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

6.1.3 Quantitative Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 80

6.2 Upgrading the Value Chain of Quinoa . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

6.2.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

6.2.2 Improvement Guidelines . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

6.2.3 Challenges . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 86

6.2.4 Future Possibilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

7 Conclusion 91

Bibliography 93

Appendices 99

A Worldwide Production and Distribution of Quinoa 100

B Distribution and Production in Peru 101

C Export of Quinoa from Peru to Europe: Value and Quantity 103

D Example of a Value Chain: The Furniture Industry 105

E Participation of Nicaragua in Global Value Chains 107

F The Position of Peru and Bolivia 109

F.1 Human Development Index: Components and Trends . . . . . . . . . . . . . . . . . 109

F.1.1 Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 109

CONTENTS VII

F.1.2 Interpretation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 110

F.2 Poverty in Bolivia and Peru . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 111

F.2.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 111

F.2.2 Population Trends, Health Outcomes and Education Achievements . . . . . 111

F.2.3 Interpretation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112

F.3 National Income and Composition of Resources . . . . . . . . . . . . . . . . . . . . . 113

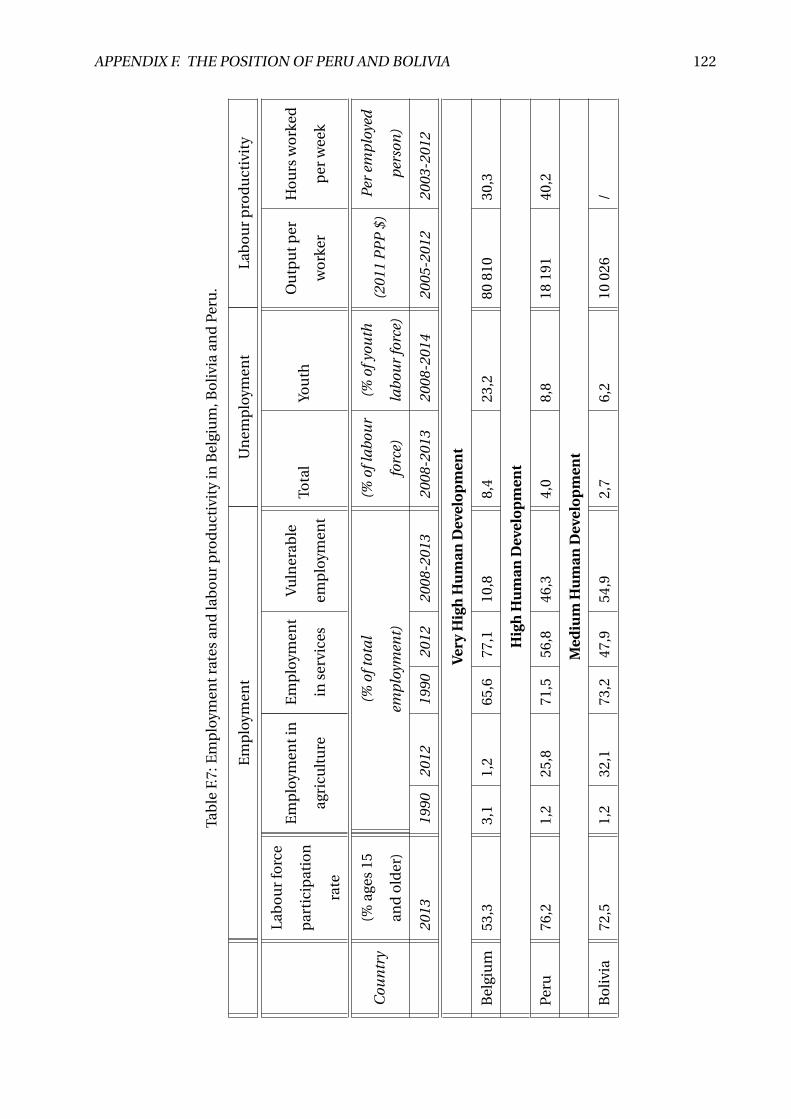

F.4 Employment Rates and Labour Productivity . . . . . . . . . . . . . . . . . . . . . . . 113

F.4.1 Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 113

F.4.2 Interpretation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 114

F.5 International Integration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 115

F.5.1 Definitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 115

F.5.2 Interpretation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 115

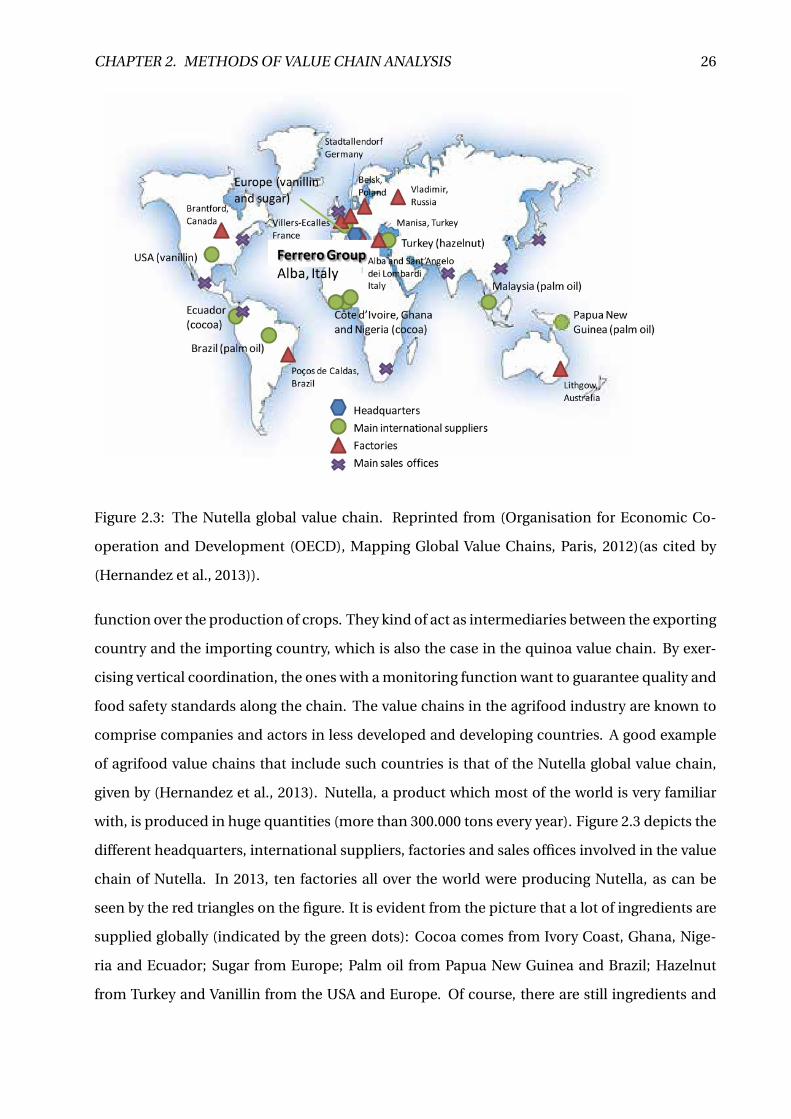

List of Tables

1.1 The evolution of export and production (in metric tons) and the associated prices

($/kg) in Peru. Reprinted from (Vinculos Agricolas, nd). . . . . . . . . . . . . . . . . 13

3.1 Consumer prices (€/kg) of conventional and Fair Trade coffee in Finland based on

purchases in one retail chain for the years 2006-2009. Copied from (Valkila et al.,

2010). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

4.1 Population and education in Peru: Region of Ayacucho and Lima. Copied from

(Censos nacionales de población y de vivienda, 2008). . . . . . . . . . . . . . . . . . 54

4.2 Participation in Economic Activity. Copied from (Censos nacionales de población

y de vivienda, 2008). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

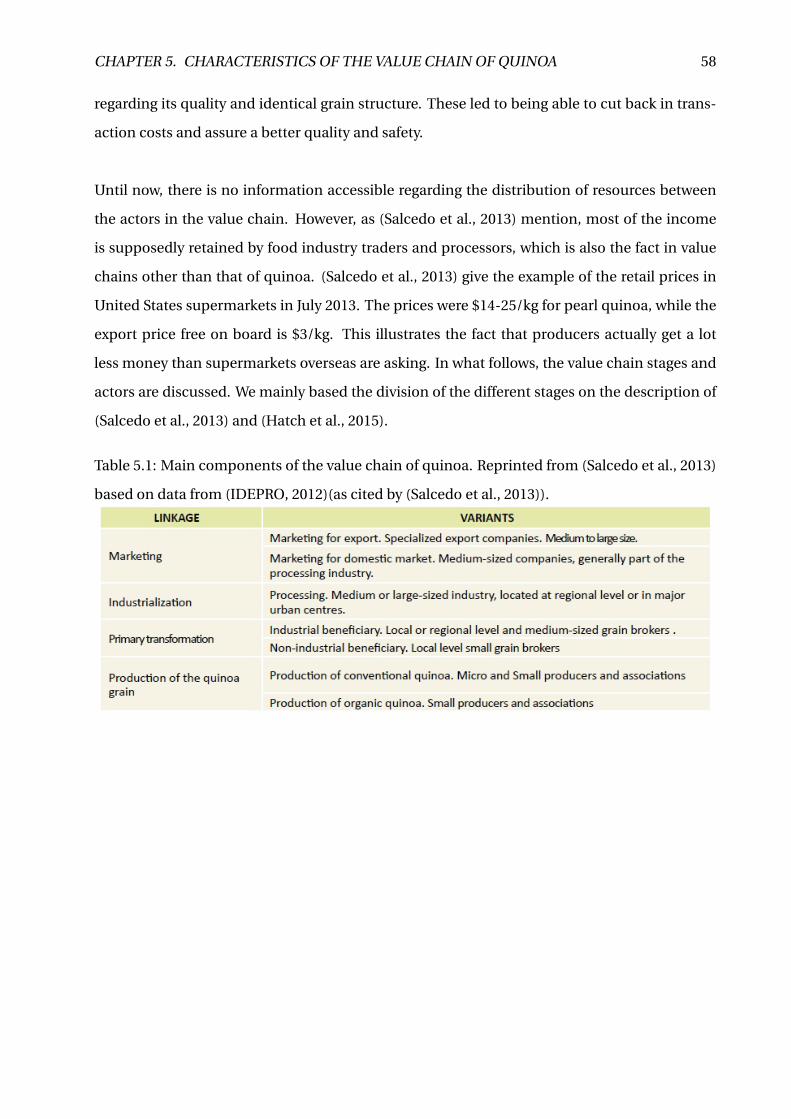

5.1 Main components of the value chain of quinoa. Reprinted from (Salcedo et al.,

2013) based on data from (IDEPRO, 2012)(as cited by (Salcedo et al., 2013)). . . . . 58

5.2 Harvested area, production and yield for different regions in Peru. Reprinted from

(Cenagro, 2012)(as cited by (Hatch et al., 2015)). . . . . . . . . . . . . . . . . . . . . . 63

5.3 The Net Export Volume (kg) and Price per kg ($/kg) for five exporters of quinoa in

Peru. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

6.1 The price for producers (Farm Price), for Peruvian consumers, for export, for in-

termediaries and for European consumers in $/kg for the period 2007-2016. Based

on an aggregation of data from (Vinculos Agricolas, nd), (Fallis, 2013), (Hatch

et al., 2015) and (Bio-Planet, nd). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

6.2 Margins for farmers, processors/exporters, intermediaries and wholesalers/retailers

in % for the period 2007-2016. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84

VIII

LIST OF TABLES IX

C.1 The Import Value and Quantity of Quinoa from Peru to Different European Coun-

tries for the period 2012 - 2016. Retrieved from (European Commission, nd). . . . . 104

F.1 Human Development Index and components for 2014. . . . . . . . . . . . . . . . . 117

F.2 Human Development Index for 1990-2014 and the average annual HDI growth

per country for this period. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 118

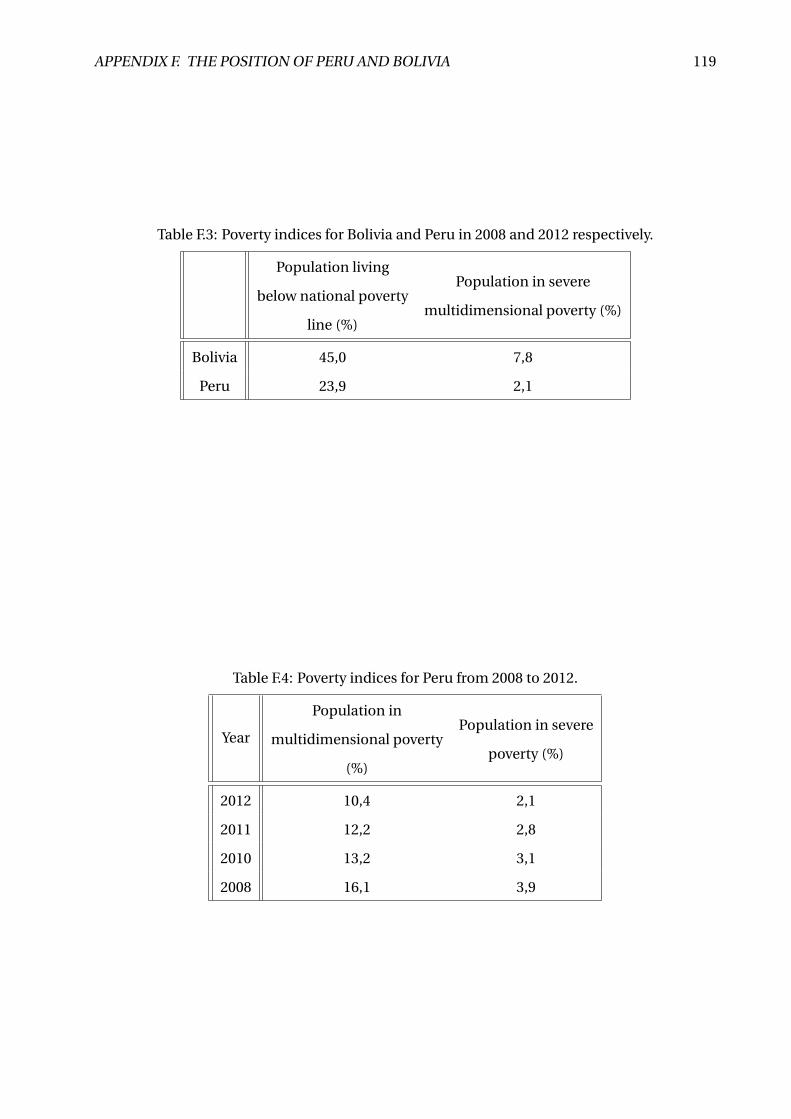

F.3 Poverty indices for Bolivia and Peru in 2008 and 2012 respectively. . . . . . . . . . . 119

F.4 Poverty indices for Peru from 2008 to 2012. . . . . . . . . . . . . . . . . . . . . . . . . 119

F.5 Population trends, mortality rates, literacy rate and secondary education rate for

Belgium, Peru and Bolivia. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 120

F.6 National income and composition of resources. . . . . . . . . . . . . . . . . . . . . . 121

F.7 Employment rates and labour productivity in Belgium, Bolivia and Peru. . . . . . . 122

F.8 International integration of Belgium, Peru and Bolivia. . . . . . . . . . . . . . . . . . 123

List of Figures

1.1 Cultivated Area (in ha) in Peru and Bolivia for the period 2000-2015. Based on an

aggregation of data from (Jacobsen, 2011); (Hatch et al., 2015); (Fallis, 2013) and

(Documento conjunto ALADI - FAO, 2014). Note that the cultivated area for Peru

in 2015 is an estimation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

1.2 Production (in tons) in Peru and Bolivia for the period 2000-2015. Based on an

aggregation of data from (Jacobsen, 2011); (Hatch et al., 2015); (Fallis, 2013) and

(Documento conjunto ALADI - FAO, 2014). . . . . . . . . . . . . . . . . . . . . . . . . 7

1.3 Yield (in ton/ha) in Peru and Bolivia for the period 2000-2015. Based on an ag-

gregation of data from (Jacobsen, 2011); (Hatch et al., 2015); (Fallis, 2013) and

(Documento conjunto ALADI - FAO, 2014). Note that the yield for Peru in 2015 is

based on the estimation of the cultivated area. . . . . . . . . . . . . . . . . . . . . . . 8

1.4 Production and export of quinoa in Bolivia and Peru. Based on an aggregation

of data from (Jacobsen, 2011); (Hatch et al., 2015); (Fallis, 2013) and (Documento

conjunto ALADI - FAO, 2014). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

1.5 Global world exports in quinoa (2012). Reprinted from (Comtrade and LAIA, nd)(as

cited by (Salcedo et al., 2013)). Note: LAIA = Latin American Integration Associa-

tion; UE = EU = European Union . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

1.6 Exports (tons) and the related export price ($/kg) of quinoa from Peru: 2000-2016.

Based on an aggregation of data from [LAIA](as cited by (Salcedo et al., 2013)) and

(Vinculos Agricolas, nd). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

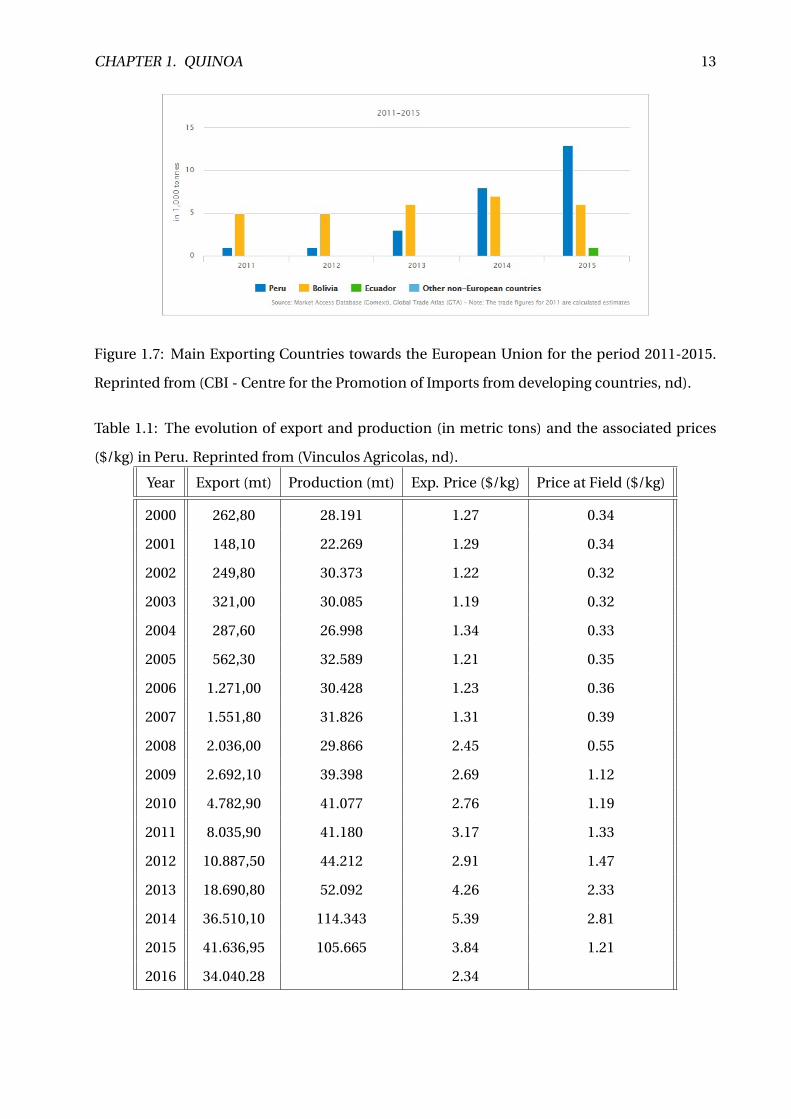

1.7 Main Exporting Countries towards the European Union for the period 2011-2015.

Reprinted from (CBI - Centre for the Promotion of Imports from developing coun-

tries, nd). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

2.1 The different stages in a supply chain. Reprinted from (Chopra and Meindl, 2016). 17

X

LIST OF FIGURES XI

2.2 A simplified representation of a food supply chain. Reprinted from (Hawkes and

Ruel, 2012). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

2.3 The Nutella global value chain. Reprinted from (Organisation for Economic Co-

operation and Development (OECD), Mapping Global Value Chains, Paris, 2012)(as

cited by (Hernandez et al., 2013)). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

3.1 The basic coffee supply chain. Reprinted from (Gilbert, 2008). . . . . . . . . . . . . 39

3.2 The marketing chain of coffee from Nicaragua to Finland. Reprinted from (Valkila

et al., 2010). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

3.3 The cocoa-chocolate supply chain. Reprinted from (Gilbert, 2008). . . . . . . . . . 45

5.1 Simple Representation of the Value Chain of Quinoa in Peru. Based on the Value

Chain as depicted by (Salcedo et al., 2013). . . . . . . . . . . . . . . . . . . . . . . . . 59

5.2 Simple Structure of the Value Chain of Quinoa based on (Hatch et al., 2015) and

(Salcedo et al., 2013). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

5.3 The value chain of quinoa as considered in our case study. . . . . . . . . . . . . . . 74

6.1 Gross Marketing Margins (in %) for the different stages in the value chain for the

period 2013-2016. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84

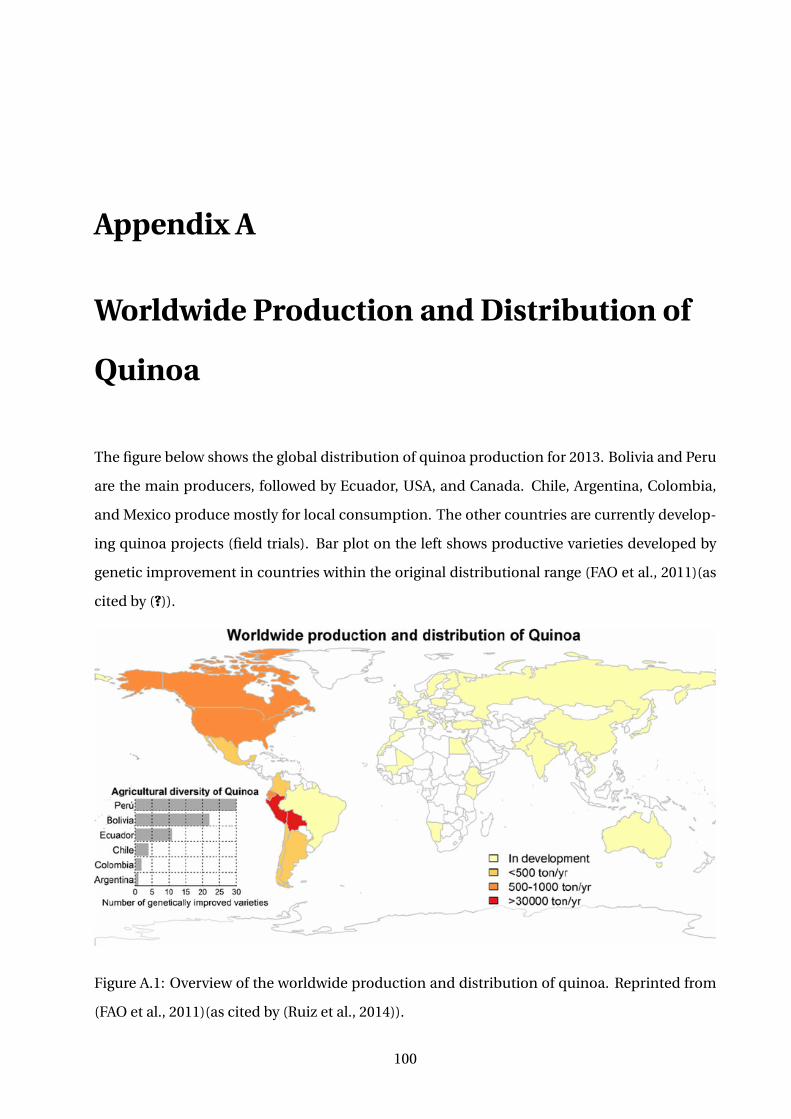

A.1 Overview of the worldwide production and distribution of quinoa. Reprinted

from (FAO et al., 2011)(as cited by (Ruiz et al., 2014)). . . . . . . . . . . . . . . . . . . 100

B.1 Volume of quinoa production in metric tons for Peru in 2013 and 2014. Reprinted

from (Ministerio de Agricultura y Riego, 2014)(as cited by (Hatch et al., 2015)). . . . 101

B.2 Cultivated surface used for quinoa production in Peru in 2013 and 2014. Reprinted

from (Ministerio de Agricultura y Riego, 2014)(as cited by (Hatch et al., 2015)). . . . 102

D.1 The forestry, timber and furniture value chain. Reprinted from (Kaplinsky and

Morris, 2002). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106

E.1 Nicaragua: Curve of value added stages in the global apparel value chain. Reprinted

from (Frederick, 2010)(as cited by (Hernandez et al., 2013)). . . . . . . . . . . . . . . 108

Part I

Literature

1

2

Chapter 1

Quinoa

1.1 Introduction

(Composition and James, 2009) states that "quinoa is one of the seeds considered as pseudo-

cereals". According to (Composition and James, 2009), this crop was a valuable food for the

Incas and still remains a valuable food crop for people of the rural regions in the Andean of

Southern America: Ecuador, Peru, Bolivia, Colombia and Venezuela. Quinoa is native to these

regions and was already used more than 5000 years ago. Since the nutritional food quality of

quinoa grains is very good and the fact that there is the possibility to grow quinoa anywhere

between sea level and mountains that reach 4000m above sea level in harsh weather condi-

tions, the interest in quinoa has risen enormously in recent years. According to (Birbuet and

Machicado, 2008) scientists consider it the best food on the globe and highly appreciated by in-

ternational markets. That explains why it was declared to be the Perfect Food for Humanity by

UNESCO. The expansion has also led to other countries in the world like Kenya, India, Morocco,

Italy, Spain, the United States and Japan starting quinoa plantations (Parker-gibson, 2016). An

overview of the worldwide production and distribution of Quinoa is shown in appendix A.

1.2 Social-Economic Context

1.2.1 Before 2000: Food Insecurity

Latin-America can be seen as a region in which there was and still is a lot of poverty. Up to half

of the population was not able to provide themselves with adequate food. Therefore, the state

of food security was investigated. According to (Barraclough and Utting, 1987), this concept

3

CHAPTER 1. QUINOA 4

assures that the supply and distribution of food is competent in quality as well as in quantity

by meeting the nutritional needs of several different social groups. It ensures that market de-

mands are met without severe shortages or brutal shifts in prices.

Food security in Bolivia and Peru caused the rural population to be self-sufficient in several

products because they were getting more and more support from public investments in ex-

pertise, machinery and capacity to grow production. Efforts to assure Bolivia and Peru to be

partly independent on imports did not lead to the desired result as new facilities were used

at only a small fraction of their capacity. This caused the products in Bolivia and Peru to be

more expensive than imports and extra subsidies for the processing enterprises being neces-

sary. Therefore, dependency on food imports increased in the early 1980s, mainly in the cities,

while peasants still relied on their own production. This, together with the poor transporta-

tion possibilities available, left the food system pretty vulnerable. The poor industrial base of

the countries caused its food system to be even more reliant on imports and a self-governing

food system inaccessible. To solve this problem on the one hand, an effective food strategy

focussed on the agricultural sector in terms of agricultural investments and services as well as

on economic and social policies (e.g. trade, exchange rates, health, education, infrastructure,

etc.) should be installed. On the other hand, focus on the agricultural sector calls for enor-

mous shifts in power relationships and asks for small farmers to organize themselves in greater

democratic farmer associations. Such organizations are looking to provide farmers with several

services regarding marketing, processing, agro-industrial production, etc. but also designing

and executing policies and programs in order to improve the food security systems.

(Barraclough and Utting, 1987) insist that people that have to cope with food insecurity can

only improve their situation by organizing themselves in local farmer associations and force

their governments to imply food strategies that are nationally-oriented. In this respect, there

was a high need for farmers to cooperate and re-organize in associations to stimulate farmer’s

production and employment but also to be able to have an influence on political issues. They

should aim for "policies to generate more employment, better working conditions, improved

education and health services, and access to adequate food at prices they can afford" (Barr-

aclough and Utting, 1987). Besides this, they should also try to collaborate with other Latin

American countries having to cope with similar problems and these problems would persist

CHAPTER 1. QUINOA 5

if they did not try to change anything. With the establishment of the national quinoa growers

association (ANAPQUI) in 1983, the production for the international market had begun (Jacob-

sen, 2011).

According to (Janvry and Sadoulet, 2000), Latin American countries still had high rates of rural

poverty because of the highly unequal distribution of income, both between sectors and within

the rural sector, during the 1990s, despite relatively high income levels among developing coun-

tries and a lot of intentions to turn things around. Appendix F illustrates and interprets several

facts and figures regarding the poverty and development in Peru and Bolivia in recent years

as well as information about Belgium to show the significant differences between the coun-

tries. In the late 1990s, they were convinced that people leaving the countryside to go to urban

areas was something that could help the rural poverty. Thereby, (Janvry and Sadoulet, 2000) ex-

plained that an increase in the productivity of certain assets, which is affected by technological

changes, could help against the rural poverty in 2 manners: Directly because the technologi-

cal innovation will raise the welfare of poor farmers and indirectly through the influence that

technological change can have on the price of food for the consumers, on the employment and

wage rates in the agricultural but also other sectors and on foreign exchange contributions.

The best way to implement this technological change to reduce the poverty of farmers is by

initiatives that seek complementarity in interventions that are specified per region and by or-

ganizing in associations. An approach that is regionally-focused and involves local farmers is

necessary if technology is to be used to reduce poverty. And this is what farmers of quinoa

also opted to do: They wanted to implement the technological innovation in the production of

quinoa because they knew the value and important nutritional qualities of quinoa.

1.2.2 Growth for the period 2000-2013

Despite the exceptional characteristics that it always had, it was only since the beginning of the

21st century that the demand for quinoa started to grow enormously. This had several impor-

tant reasons:

1. According to (Dreibus, 2016)(as cited by (Parker-gibson, 2016)) the rising interest in ve-

gan, vegetarian and gluten-free diets played an important role. The world started to dis-

cover celiac disease which resulted in an increase in demand for grains without gluten

CHAPTER 1. QUINOA 6

(Birbuet and Machicado, 2008).

2. The accelerated increase of the demand of high-quality organic products and the growth

of the market of fair trade products (Birbuet and Machicado, 2008).

3. Several countries adopted the food efficiency programs that were supported by the Food

and Agriculture Organization of the United Nations (FAO) (Birbuet and Machicado, 2008).

4. People discovered that quinoa could be used as a source of food in areas that have to cope

with food insecurity (Ruiz et al., 2014)(as cited by (Parker-gibson, 2016)).

Issues

When looking specifically at Bolivia and Peru, although both countries’ production of quinoa

increased over the last 20 years because of an enlarged production area, they had a limited

capacity of quinoa production available in the beginning and were not able to fulfil the huge

increases in demand immediately. Figures 1.1, 1.2 and 1.3 show the enormous increase in culti-

vated area and production for the considered period. A reason for the continuous higher yield

in Peru than in Bolivia may be the social-economic gap that persists between the two countries,

as is discussed in chapter 4 and appendix F.

Figure 1.1: Cultivated Area (in ha) in Peru and Bolivia for the period 2000-2015. Based on an

aggregation of data from (Jacobsen, 2011); (Hatch et al., 2015); (Fallis, 2013) and (Documento

conjunto ALADI - FAO, 2014). Note that the cultivated area for Peru in 2015 is an estimation.

CHAPTER 1. QUINOA 7

Figure 1.2: Production (in tons) in Peru and Bolivia for the period 2000-2015. Based on an

aggregation of data from (Jacobsen, 2011); (Hatch et al., 2015); (Fallis, 2013) and (Documento

conjunto ALADI - FAO, 2014).

(Jacobsen, 2011) states that the main problem of the agricultural sector was situated at the grain

processing link of the chain, until the early 2000s. The yearly processing capacity of quinoa in

Bolivia was only one third of the actual production of quinoa for one year. This led to a big loss

of the product itself. Half of the bigger quinoa-producing companies of the sector in Bolivia,

who were responsible for four fifth of quinoa exports, agreed to implement a subversive tech-

nological change to try to overcome the deficits. The technological innovation played a crucial

role in the processing of quinoa and this was the fundamental basis for a development program

called the "Quinoa Alliance". This united the main quinoa-producing companies and producer

associations of the sector.

The government’s interest in quinoa as a commodity of priority to increase the income of the

country increased the importance of the production of quinoa even more according to (Jacob-

sen, 2011). The socio-economic circumstances were very bad (We would like to refer to Ap-

pendix F for a broad elaboration on the socio-economic conditions in Peru and Bolivia in recent

years) and together with the area increase in the first years of the 21st century, the yield had to

cope with an enormous decrease. Another problem caused by the area increase is the destruc-

tion of the vegetation cover leading to an acceleration of erosion [FAUTAPO, 2008](as cited by

(Jacobsen, 2011)). Although the drop in yield, the prices kept increasing leading to an expanded

CHAPTER 1. QUINOA 8

Figure 1.3: Yield (in ton/ha) in Peru and Bolivia for the period 2000-2015. Based on an aggrega-

tion of data from (Jacobsen, 2011); (Hatch et al., 2015); (Fallis, 2013) and (Documento conjunto

ALADI - FAO, 2014). Note that the yield for Peru in 2015 is based on the estimation of the culti-

vated area.

intensification with which quinoa was produced because farmers wanted to supply more to the

international markets (the export value had risen from $2.7 million in 1999 to $8.9million in

2006 [PNUD Bolivia, 2008](as cited by (Jacobsen, 2011)). The export of quinoa had increased

since the beginning of the new century, causing the domestic consumption to decrease. Figure

1.4 illustrates the absolute amounts of production and export for Bolivia and Peru. The differ-

ence between production and export is what is used for seeds, domestic consumption or other

uses. We can state that the domestic consumption decreased proportionally to the production,

mainly due to an increase in prices and therefore export. The figure also shows that Peru be-

came a largest exporter of quinoa, while this had always been Bolivia before 2014.

As stated by (Jacobsen, 2011), the production was in crisis because the yield decreased and

the price of quinoa tripled from 1999 to 2008, up to $2300/ton. The rising demands on the

world market and the growing commercial quinoa cultivation are leading to land degradation

caused by a much intensified production of quinoa whereas they should better adopt an ex-

tensive production to respond to the high prices (Bioversity International, 2007);[MDRyT, 2009]

and (Bosque, 2008)(as cited by (Jacobsen, 2011)).

CHAPTER 1. QUINOA 9

Figure 1.4: Production and export of quinoa in Bolivia and Peru. Based on an aggregation of

data from (Jacobsen, 2011); (Hatch et al., 2015); (Fallis, 2013) and (Documento conjunto ALADI

- FAO, 2014).

Possible Solutions

Since quinoa is a product that can be cultivated in several different agro-climatic conditions

in the Andes (Jacobsen, 2003)(as cited by (Jacobsen, 2011)), a production outside the region

would decrease the enormous pressure on the soil in vulnerable regions and bolster the market

worldwide and thereby benefit others in the world because of its huge market potential (Jacob-

sen, 2003)(as cited by(Jacobsen, 2011)).

As stated earlier, farmers are no longer consuming their own production of quinoa but partic-

ularly grow it to export because the price is too high to keep it. With the money they earn from

selling it, they can buy much more other products with a lower value. Figure 1.4 illustrates the

decrease in consumption of own production towards 2010 (pink dots). (Jacobsen, 2011) indi-

cates that the consumption of quinoa in Bolivia amounts to only 2kg per person per year and

the consumption of rice or pasta has risen to more than 25kg per person per year, whereas in

Peru, a person consumes more than 20kg per year.

1.2.3 Future

Right now, some believe quinoa has already lived up to its full potential in the highlands of

Peru and Bolivia. After the international year of quinoa, production (as can be seen on figure

CHAPTER 1. QUINOA 10

1.2, especially for Peru) as well as prices reached its peak in 2014. Producers could get up to

€6/kg for organic quinoa. Due to its flexibility and high potential, people started to cultivate

quinoa in the lowlands, in the north of Peru, along the coast, closer to bigger cities. Since the

yield realized in these parts of the country are a lot higher (4 000 kg/ha compared to 1 000

kg/ha in the highlands) thanks to better weather conditions and use of pesticides, the total

production started to increase enormously. Everywhere in the country new quinoa farmers

were popping up like daisies. Furthermore, the United States, Canada, European countries etc.

all started small plantations of quinoa to cultivate their own quinoa in order to reduce import

and transportation costs. These factors all led to a drop in price and loss of markets for the

Peruvian and Bolivian farmers.

1.3 Characteristics of the International Quinoa Trade

In this section, we will elaborate on the characteristics of the international trade of quinoa. The

main goal is to identify the actors of the value chain (e.g. importers and exporters) and give a

clear overview of the market access conditions and the essential elements of global supply and

demand for quinoa on which our case study can be based. Research for this section is mainly

based on (Salcedo et al., 2013)’s paper about "International Quinoa Trade".

As mentioned in earlier sections, the increase in the demand of quinoa can be explained by

several reasons. As the demand grew significantly, so did the international trade. Since the

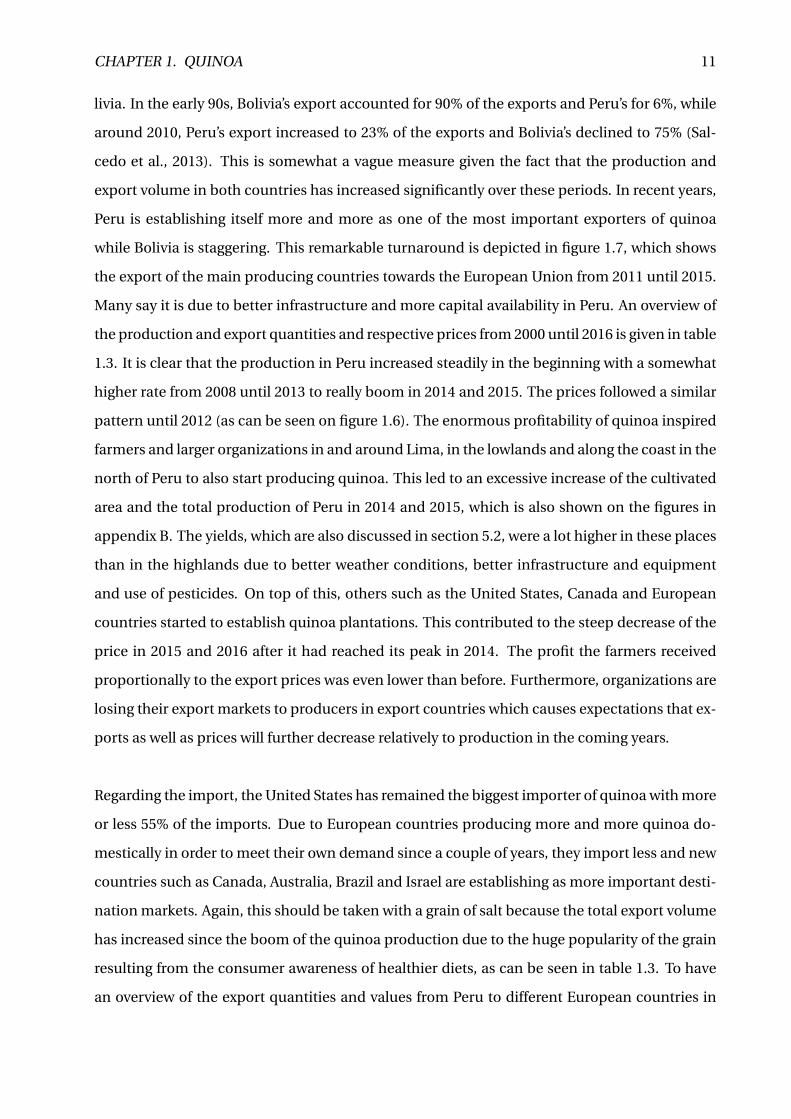

Latin-American countries (LAIA) account for more than 80% of the export of quinoa (as can be

seen on Figure 1.5), a tariff opening for quinoa was introduced by the World Customs Organiza-

tion according to (Salcedo et al., 2013). Most of the exports go to the United States and a decent

percentage to Canada. The other exports are mostly intended to go to Western Europe. Figure

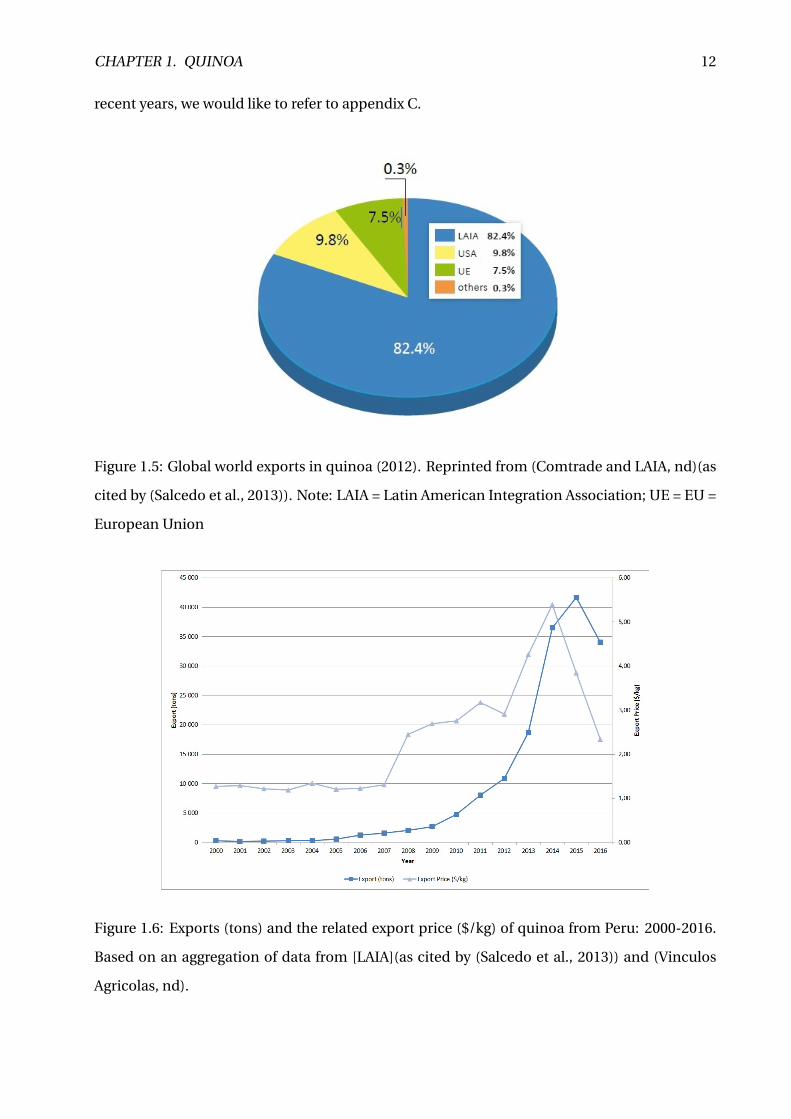

1.6 indicates the enormous growth in exports that Bolivia and Peru have witnessed. This figure

shows the amount of tons and the corresponding price at which the quinoa was exported dur-

ing the years from 1992 until 2012. The export increased more than 40 times from 600 tonnes

in 2002 to 37 000 tonnes in 2012, which corresponds to an annual growth rate of 22,8% (Salcedo

et al., 2013).

Also, the export of quinoa in Peru has increased proportionally to the export of quinoa in Bo-

CHAPTER 1. QUINOA 11

livia. In the early 90s, Bolivia’s export accounted for 90% of the exports and Peru’s for 6%, while

around 2010, Peru’s export increased to 23% of the exports and Bolivia’s declined to 75% (Sal-

cedo et al., 2013). This is somewhat a vague measure given the fact that the production and

export volume in both countries has increased significantly over these periods. In recent years,

Peru is establishing itself more and more as one of the most important exporters of quinoa

while Bolivia is staggering. This remarkable turnaround is depicted in figure 1.7, which shows

the export of the main producing countries towards the European Union from 2011 until 2015.

Many say it is due to better infrastructure and more capital availability in Peru. An overview of

the production and export quantities and respective prices from 2000 until 2016 is given in table

1.3. It is clear that the production in Peru increased steadily in the beginning with a somewhat

higher rate from 2008 until 2013 to really boom in 2014 and 2015. The prices followed a similar

pattern until 2012 (as can be seen on figure 1.6). The enormous profitability of quinoa inspired

farmers and larger organizations in and around Lima, in the lowlands and along the coast in the

north of Peru to also start producing quinoa. This led to an excessive increase of the cultivated

area and the total production of Peru in 2014 and 2015, which is also shown on the figures in

appendix B. The yields, which are also discussed in section 5.2, were a lot higher in these places

than in the highlands due to better weather conditions, better infrastructure and equipment

and use of pesticides. On top of this, others such as the United States, Canada and European

countries started to establish quinoa plantations. This contributed to the steep decrease of the

price in 2015 and 2016 after it had reached its peak in 2014. The profit the farmers received

proportionally to the export prices was even lower than before. Furthermore, organizations are

losing their export markets to producers in export countries which causes expectations that ex-

ports as well as prices will further decrease relatively to production in the coming years.

Regarding the import, the United States has remained the biggest importer of quinoa with more

or less 55% of the imports. Due to European countries producing more and more quinoa do-

mestically in order to meet their own demand since a couple of years, they import less and new

countries such as Canada, Australia, Brazil and Israel are establishing as more important desti-

nation markets. Again, this should be taken with a grain of salt because the total export volume

has increased since the boom of the quinoa production due to the huge popularity of the grain

resulting from the consumer awareness of healthier diets, as can be seen in table 1.3. To have

an overview of the export quantities and values from Peru to different European countries in

CHAPTER 1. QUINOA 12

recent years, we would like to refer to appendix C.

Figure 1.5: Global world exports in quinoa (2012). Reprinted from (Comtrade and LAIA, nd)(as

cited by (Salcedo et al., 2013)). Note: LAIA = Latin American Integration Association; UE = EU =

European Union

Figure 1.6: Exports (tons) and the related export price ($/kg) of quinoa from Peru: 2000-2016.

Based on an aggregation of data from [LAIA](as cited by (Salcedo et al., 2013)) and (Vinculos

Agricolas, nd).

CHAPTER 1. QUINOA 13

Figure 1.7: Main Exporting Countries towards the European Union for the period 2011-2015.

Reprinted from (CBI - Centre for the Promotion of Imports from developing countries, nd).

Table 1.1: The evolution of export and production (in metric tons) and the associated prices

($/kg) in Peru. Reprinted from (Vinculos Agricolas, nd).

Year Export (mt) Production (mt) Exp. Price ($/kg) Price at Field ($/kg)

2000 262,80 28.191 1.27 0.34

2001 148,10 22.269 1.29 0.34

2002 249,80 30.373 1.22 0.32

2003 321,00 30.085 1.19 0.32

2004 287,60 26.998 1.34 0.33

2005 562,30 32.589 1.21 0.35

2006 1.271,00 30.428 1.23 0.36

2007 1.551,80 31.826 1.31 0.39

2008 2.036,00 29.866 2.45 0.55

2009 2.692,10 39.398 2.69 1.12

2010 4.782,90 41.077 2.76 1.19

2011 8.035,90 41.180 3.17 1.33

2012 10.887,50 44.212 2.91 1.47

2013 18.690,80 52.092 4.26 2.33

2014 36.510,10 114.343 5.39 2.81

2015 41.636,95 105.665 3.84 1.21

2016 34.040.28 2.34

Chapter 2

Methods of Value Chain Analysis

2.1 Theory of Value Chain Analysis

2.1.1 Value Chain: Definitions

(Kaplinsky and Morris, 2002) define the value chain as "the full range of activities which are

required to bring a product or service from conception through the different phases of produc-

tion, delivery to the final consumers and final disposal after use." A simple example is given in

appendix D, in which the value chain of the furniture industry is shortly described. The value

chains can be of a different type. Based on the idea of governance, (Gereffi and Korzeniewicz,

1994) (as cited by (Kaplinsky and Morris, 2002)) distinguish two types of value chains: Buyer-

driven chains and Producer-driven chains. Governance refers to the controlling and monitoring

of the implied rules and interactions between the different actors in the value chain by setting

parameters regarding products, processes and qualifications. It is important that these rules

and interactions carefully reflect the actors, activities, roles and functions and their relation-

ships with each other. When this governance role is played by a buyer at the top of the chain,

(Kaplinsky and Morris, 2002) categorize it as buyer-driven chains. Such chains are most present

in labour-intensive sectors such as the aforementioned furniture, but also clothing, electronics,

handicrafts etc. The second type, producer-driven chains, describe the governing role to be

played by the leading producer of the chain and are most likely to be present in capital- and

technology-intensive environments (e.g. software, heavy machinery, car industry, etc.). (Ger-

effi et al., 1999) (as cited by (Kaplinsky and Morris, 2002)) further state that the different kinds

of value chains are related with different kinds of production systems. (Kaplinsky and Morris,

15

CHAPTER 2. METHODS OF VALUE CHAIN ANALYSIS 16

2002) complement these findings by saying that value chains not only differ within and between

sectors, but also the international, national and local context is an important factor to take into

account.

According to (Donovan et al., 2015), there are several definitions of a value chain. In his paper

’Guides for Value Chain Development: A Comparative Review’, he distinguishes three defini-

tions of a value chain as follows:

1. A value chain can be interpreted based on the value adding activities that are performed

in every step from start to end product or service. In this definition, (Donovan et al.,

2015) emphasize that the development of the chain is focused on enhancing production

processes.

2. A second possibility to see a value chain is as a combination of actors that are linked to

each other by the activities they perform. (Donovan et al., 2015) report that the weakest

actors are mainly the core of the chain development.

3. Thirdly, (Donovan et al., 2015) state that a value chain can also be interpreted to fulfil the

market demand by regarding the value chain as a strategic network. These value chains

are developed over time as the goal is to form a decent value adding chain.

Obviously, these definitions are often interpreted in a combined matter. (Donovan et al., 2015)

also gives two possible definitions of value chain development, which he describes as "an ac-

tor/chain type that focuses on strengthening certain actors and improving relations between

smallholders and other actors in a chain; a business-environment type that focuses on improv-

ing the business environment in which chain actors operate." The goal of value chain devel-

opment is very diverse but mainly looks to enhance the chain by investigating the drawbacks

of actors and activities, looking at competitors and coming up with innovations to address the

drawbacks and improve the chain and process such that all actors benefit from it.

2.1.2 Creating Value in a Supply Chain Environment

The first thing (Hawkes and Ruel, 2012) stated is that a value chain starts with a supply chain:

(Chopra and Meindl, 2016) define a supply chain as "a system consisting of all parties involved,

directly or indirectly, in fulfilling a customer request. It includes manufacturers and suppliers,

CHAPTER 2. METHODS OF VALUE CHAIN ANALYSIS 17

transporters, warehouses, retailers and customers." The typical supply chain consists of differ-

ent stages, as shown on figure 2.1. The arrows indicate that each stage is connected through the

flow of products, services, information, money etc. Functions used to complete the requests of

customers include new product development, marketing, operations, distribution, finance and

customer service (Chopra and Meindl, 2016).

Figure 2.1: The different stages in a supply chain. Reprinted from (Chopra and Meindl, 2016).

The definition of a supply chain allows to say that a value chain involves all the processes and

the actors that play a significant role from the origin of a product to its clearance, as can be

seen on figure 2.2, on which I will focus more in section 2.3. A value chain can be described

as a supply chain where "value is added to the product through "value-adding" activities as it

passes through the chain. These activities create value for the value chain actors." (Hawkes and

Ruel, 2012). Value creation can be in terms of the economic value of the product itself, the eco-

nomic value that is created for the actors in the chain or the value that is added to the product

as it goes through the different steps in the chain (Hawkes and Ruel, 2012). On the other hand,

(Dixit, 2014) declares that value chains unfold around the needs of consumers and these are in

turn translated in the needs for the market. A drawback of this is that the needs for the market

are not directly embedded in agriculture policy frameworks. Well-working markets are easier

when you want to improve the productivity and production. According to (Dixit, 2014), a pol-

icy framework that is based on the value chain allows to observe the link between the different

actors of the value chain: and facilitates to identify the process or actor in the chain that should

CHAPTER 2. METHODS OF VALUE CHAIN ANALYSIS 18

be targeted for a potential value addition.

According to (Dixit, 2014), policy makers and international communities have recently been at-

tracted to global value chains. These value chains indicate a "production process that crosses

the border of the country where it is produced in order to create a decent end product. This in-

ternational environment for production and trade causes certain threats because it is not in line

with traditional trade and the mindset of investment policies" (Dixit, 2014). (Dixit, 2014) gives

the example of tariffs and other customs restrictions on trade that may not only harm foreign

supplies but also be a barrier to indigenous exports by levying fees and therefore increasing the

cost. Quinoa can be seen as a product that is part of such a global value chain since it is pro-

duced in Bolivia and Peru and exported to multiple markets across its borders. Global value

chains are described in more detail in section 2.1.4.

2.1.3 Importance of Value Chain Analysis

(Kaplinsky and Morris, 2002) mention the three main reasons why it is important to perform a

value chain analysis:

1. Competitiveness is extremely important due to the increased division of labour and the

global diffusion of the production components.

2. A detailed value chain analysis has the possibility to enhance the production processes

and thereby enter global markets.

3. A thorough understanding of the dynamic factors in the value chain facilitates entry in

the global markets and corresponding growth.

2.1.4 Global Value Chains

For their definition of global value chains, (Hernandez et al., 2013) start with a definition of a

value chain obtained from (Gereffi and Fernandez-Stark, 2016): "The full range of activities that

firms and workers do to bring a product from its conception to its end use and beyond." Accord-

ing to (Hernandez et al., 2013), this includes different activities such as the design, production,

marketing, distribution and support to the final consumer. Since these activities and actors are

not focused on one country and therefore located in several countries, the value chain is said to

CHAPTER 2. METHODS OF VALUE CHAIN ANALYSIS 19

be global.

It was in the beginning of the year 2000 that global value chains started to take off. This shows

similarities with the evolution of the quinoa grain. From the beginning of the new century, the

interest in quinoa rose enormously and started to expand beyond the borders of Bolivia and

Peru a couple of years later. (Hernandez et al., 2013) mention three factors responsible for the

raise of global value chains:

1. Production got more and more fragmented over several countries due to the increased

transport and infrastructure possibilities. Global value chains allow to portray the rela-

tionships of the fragmented activities and link them geographically.

2. Some countries are specialized in cultivating products that are used for production of

another good in a country that is specialized in the processing of the good. This good

may further be transferred to another country for consumption. (Hernandez et al., 2013)

state that countries are more and more specializing in processes and business functions

than in products, which leads to countries trying to position themselves in value chains.

Global value chains ease this transition process.

3. Global value chains establish networks of buyers and suppliers and allow to get a better

understanding of the controlling and monitoring structures. According to (Hernandez

et al., 2013), this is crucial to determine what influence policies have on actors and where

activities are performed.

These factors need to be taken into account in order to better understand how global value

chains operate and to be able to map a value chain like the one of quinoa. The value chain of

quinoa can be interpreted as being fragmented over producing and processing countries Peru

and Bolivia, where it is also consumed or from where it is transferred to other distributing and

consuming countries like the US, Canada, France, Spain, Germany, Australia etc. Networks of

producers, processors, exporters, wholesalers and retailers are established to deliver a quality

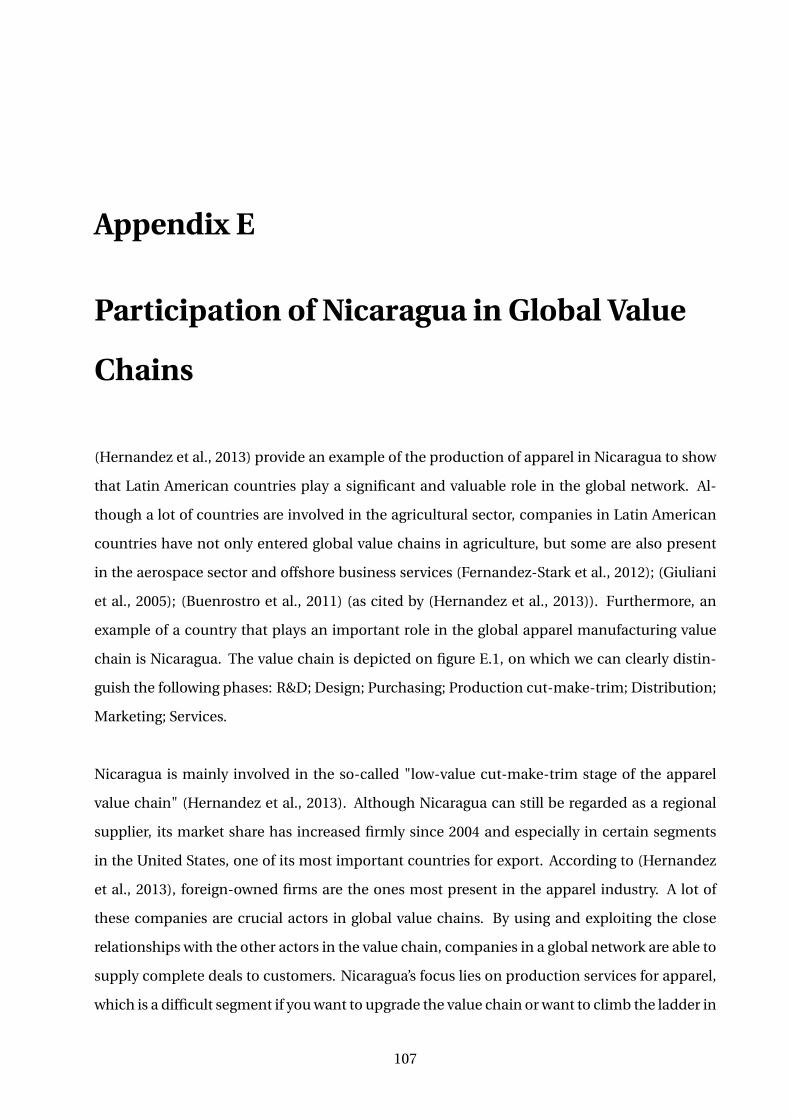

product to the customers. An example of a Latin-American country participating in global value

chains is given in appendix E.

CHAPTER 2. METHODS OF VALUE CHAIN ANALYSIS 20

2.2 Methodology for Value Chain Analysis

As mentioned earlier, (Kaplinsky and Morris, 2002) stated that value chains differ within and

between sectors. Thereby, the context in which they operate alters too. (Kaplinsky and Morris,

2002) ranked several issues and factors to focus on when analyzing a supply chain: A first and

far most important step is the understanding of the market. To be able to conduct a secure

value chain analysis, (Kaplinsky and Morris, 2002) outlined the following key aspects and steps

of value chain analysis:

1. The way a chain is looked at determines which relations and actions are to be the key

processes, functions, roles etc.

2. Mapping value chains is a second important consideration. This involves the determina-

tion of constraint, the selection of appropriate variables and the assignment of numbers

and values to the respective variables for each actor or step in the value chain. In the case

of quinoa in Peru and Bolivia, the main variables of importance are the produced, trans-

ported and exported quantities and corresponding prices. This is on which the case study

will focus.

3. Since more and more systems use the ’pull-principle’, the characteristics of the final stages

should get primary attention and should be clearly defined in order to recognize critical

factors such as a clear segmentation of the market, definition of critical success factors

(e.g. low cost, quality, differentiation etc.) and the rapid changing environment.

4. The way producers approach end markets, benchmarking the efficiency, controlling, mon-

itoring and upgrading value chains (Kaplinsky and Morris, 2002).

Not all but most of these aspects should be considered and utilized in a value chain analysis.

When we want to expand this analysis to broader horizons such as new international markets

like the one of quinoa, a global value chain analysis should be applied, like explained in section

2.1.4 above.

CHAPTER 2. METHODS OF VALUE CHAIN ANALYSIS 21

2.3 Value Chains in Agriculture

2.3.1 Introduction

As stated before, a lot of people in Southern American countries suffer from hunger and food

insecurity. (Hawkes and Ruel, 2012) indicate that these people are denied easy access to such

foods due to a limited availability, economic constraints, lack of knowledge and information,

and related lack of demand for nutritious foods. In their paper, they assume that agriculture

could partly solve this problem by providing aid to people that are at risk and by enhancing

the availability, affordability, acceptability and quality of the nutritious foods such as quinoa.

Installing development programs focused on the agricultural production and consumption by

small farmers is not sufficient to improve the nutrition. All what happens between production

and consumption has to be mapped. According to (Hawkes and Ruel, 2012), this can be done

by adopting several concepts, analysis and approaches regarding the value chain. The analy-

sis is concentrated on identifying the actors and its relationships and on the activities that are

performed throughout the value chain. Figure 2.2 clearly illustrates the different activities and

corresponding actors that are needed to achieve and enhance the concepts of food availability,

food affordability, food acceptability and food quality. There are also several alternative ap-

proaches to agricultural development that are used to encourage poor groups of people to be

part of more modern value chains. These approaches want to increase the return to the farmers

as a means of improving processes, products, functions, volume and coordination (Hawkes and

Ruel, 2012).

2.3.2 Value Chain concepts

Value chain concepts have the potential to influence both the supply and the demand of nu-

tritious foods such as quinoa. The analysis gives an indication of the availability, the price and

the quality of the foods together with the interference of the government. (Hawkes and Ruel,

2012) give an example of value chain analysis where it is used to identify the type of value that

products need to supply to enhance the demand and the acceptability of that product as well as

determining whether extra nutritional value changes the value perception and the willingness

to pay for consumers.

CHAPTER 2. METHODS OF VALUE CHAIN ANALYSIS 22

Figure 2.2: A simplified representation of a food supply chain. Reprinted from (Hawkes and

Ruel, 2012).

(Hawkes and Ruel, 2012) write that when the nutrition goals are clearly stated and solution-

oriented, the convenience of value chain concepts allows to accomplish the goals more easily.

In section 2.3.4, their view on how to apply value chain concepts to achieve nutrition goals is

illustrated.

2.3.3 Agricultural Value Chains and Food Security

Value chain analysis that is focused on achieving nutrition goals as mentioned in section 2.3.4

is very closely related to the agricultural value chain and the associated food security and there-

fore also to the value chain of quinoa. The concept of food insecurity is something Bolivia and

Peru already have to cope with since a long time, although not to the same extent recently. It

can be seen as the base, from which it all started, of the quinoa production. Since there was

CHAPTER 2. METHODS OF VALUE CHAIN ANALYSIS 23

and is food insecurity in Bolivia and Peru, people look for new products and strategies, mainly

situated in the agricultural sector, to overcome the problems. (Dixit, 2014) states that a value

chain perspective on the agricultural sector delivers guidelines to address certain constraints

and restrictions related to the development of the agricultural sector and the realisation of food

security objectives. Due to the increasing globalization and the increased acquisition and dis-

tribution channels, research of the value chains is becoming more important in agriculture.

Although (Dixit, 2014) argues that this is why agricultural value chains are more buyer-driven

instead of producer-driven, the value chain of quinoa is also producer-driven because the pro-

duction process is influenced by "foreign value that is added in domestic agricultural produc-

tion and exports" (Dixit, 2014).

(Dixit, 2014) states that a value chain-based policy framework can facilitate food security con-

siderations. He mentions ’food availability on the national market’, ’food accessibility for peo-

ple’ and ’food utilisation’ as the core aspects of assuring food security. The first aspect, food

availability, is in line with improving the agricultural productivity because a better productivity

assists its availability. Secondly, access to food is said to be the most important factor because it

supports people’s security. Food utilisation mainly focuses on achieving nutrition goals. (Dixit,

2014) is convinced that a policy framework would improve the whole value chain by imple-

menting extra investments for production systems and infrastructure for the market and for

distribution. This will in turn lead to an agricultural sector that is flexible and able to handle

possible issues in the future. According to (Dixit, 2014), a policy framework with multilateral

trade rules, installed under the World Trade Organisation (WTO), enhances the performance of

actions to achieve food security goals for example by decreasing tariffs and other barriers. First

of all, multilateral rules would restrict the extent to which the government subsidises farmers

who are considered to have a negative impact. Secondly, a reduction in tariffs and trade trans-

action costs would improve the access and utilisation factors of food security and therefore also

the value chain. Thirdly, (Dixit, 2014) states that the WTO would also like to provide predictable

access to supply and therefore retain its reliable source of food supply. It would install limits on

export for a certain product to prevent a shortage for this product. A last thing that WTO would

like to inaugurate are the multilateral rules on food safety and quality standards because they

are crucial for a good working value chain.

CHAPTER 2. METHODS OF VALUE CHAIN ANALYSIS 24

We can conclude that "upstream and downstream markets are the main avenues of value addi-

tion" (Dixit, 2014) in agriculture. (Dixit, 2014) states that markets are the drivers for outside ac-

tors to join the value chain. He is convinced that a value chain-based framework can empower

the authorities to acknowledge markets’ influence when there are more connections with the

private sector and when the agricultural value chains’ importance keeps increasing. This will

lead to governmental involvement in some of the activities in order to assist production and

productivity and create better functioning markets. This will further lead to an increasing and

growing agricultural sector that is supported by the government. When we look at quinoa in

this respect, the government is indeed trying to provide support for poor farmers, but larger

farmers and processors are still too often reaping the benefits away from the small farmers by

abusing their power towards the government or exporters.

2.3.4 Value Chain Analysis to Achieve Nutrition Goals

When looking more specifically to value chain analysis in the agricultural sector, the most com-

mon and important objective is related to nutrition goals. In this respect, (Hawkes and Ruel,

2012) investigate whether value chain concepts can help to achieve nutritional goals. They state

that adopting concepts of the value chain has the possibility to enhance the supply and demand

of nutritious foods, especially for the poor people. "Value chain concepts enable the potential

of assessing the availability, the price and the nutrient quality of foods in specific communities.

Thereby they indicate what an influence public interventions and policies have on the integra-

tion in the value chain." (Hawkes and Ruel, 2012). Since they embody the different steps in the

chain and recognize that the coordination among the actors enhances the ability of the sector

to create value, they are able to provide a framework for coordinating actions and actors and

for identifying and engaging the sectors that need to be involved. And this is very relevant to

the agricultural sector. Therefore, (Hawkes and Ruel, 2012) give a detailed overview of steps to

follow in order to achieve nutritional goals:

1. Starting from a clearly-stated and outcome-oriented nutrition goal is important.

2. Define the nutrition problem and identify the gaps in food and nutrients by targeting one

or more food value chains.

3. First create economic value for value chain actors. This will in turn lead to an increase in

value for nutrition. This is illustrated below.

CHAPTER 2. METHODS OF VALUE CHAIN ANALYSIS 25

4. It is important to search for comprehensive solutions that are adapted to the context.

"The search for solutions should take the whole value chain, including different sectors

and actors at different scales, into account, but the application of solutions should be

tailored to circumstance" (Hawkes and Ruel, 2012).

5. Focus on improving the coordination of the actors within the chain by intervening where

necessary and developing alliances between the actors involved.

6. Look for solutions that both add value for nutrition as well as for actors of the value chain.

7. Add value for consumers by offering new attributes and add value for producers by allow-

ing them to produce more or supply a larger market.

8. Aim attention at meeting, increasing and creating demand.

9. Develop a policy environment which gives incentives to the actors in the chain to value

nutrition.

An example of a project with explicit nutrition goals and related activities according to (Hawkes

and Ruel, 2012) is the "Enhancing of the bean value chain in Uganda". This is very similar to

the projects involving quinoa in Peru and Bolivia because it’s a project focused on improving

the production, marketing and consumption of beans in order to improve the living conditions

of the people. "In a value-chain framework, actions included research into increasing yields,

improving nutrient quality after harvest, understanding consumers’ preferences and demand,

increasing their awareness of the nutritional and health benefits of beans, and promoting bean

consumption" (Mazur et al., 2011)(as cited by (Hawkes and Ruel, 2012)).

2.3.5 Global Value Chains in Agriculture

Global value chains are not restricted to products or services in a manufacturing industry. (Her-

nandez et al., 2013) state that agriculture can be linked to the value chains of the downstream

activities, the so called "agrifood business". According to (Hernandez et al., 2013), it is becom-

ing more and more a trend to structure these downstream activities in global value chains.

These global value chains are said to be managed by processors and retailers who are part of

the chain. (Hernandez et al., 2013) mention supermarkets as an example of retailers who are

part of the chain and have contracts with importers as well as exporters to exert a monitoring

CHAPTER 2. METHODS OF VALUE CHAIN ANALYSIS 26

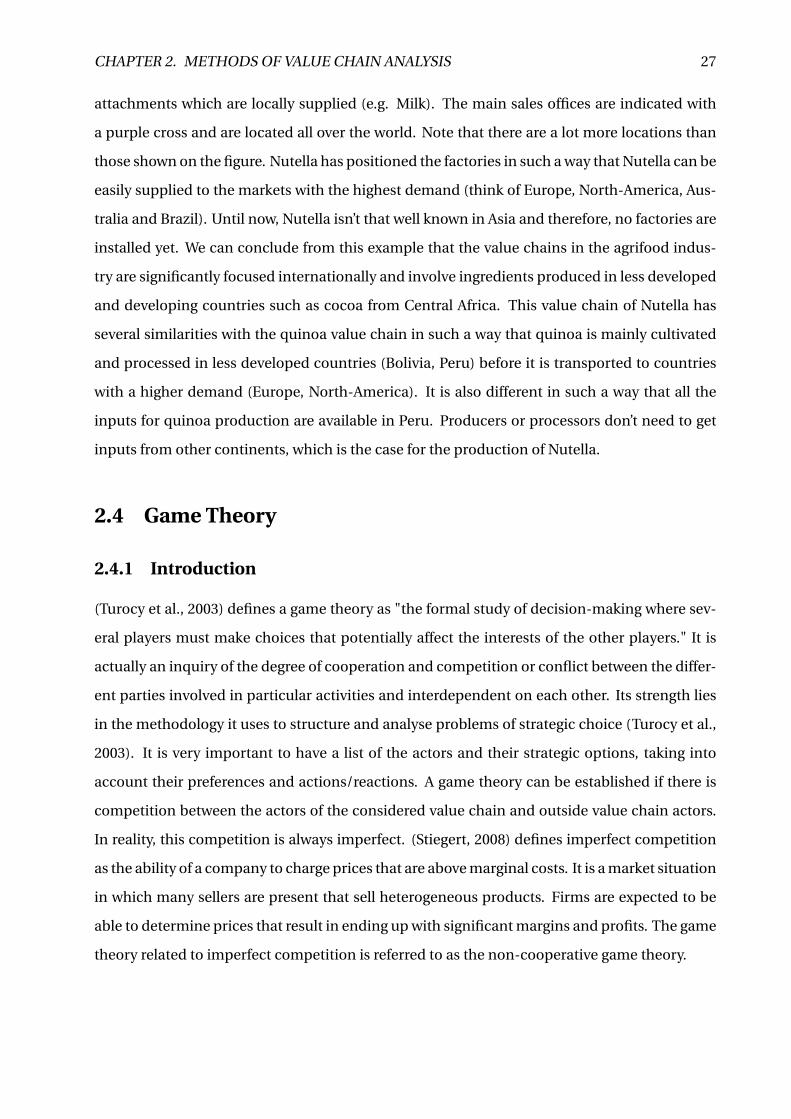

Figure 2.3: The Nutella global value chain. Reprinted from (Organisation for Economic Co-

operation and Development (OECD), Mapping Global Value Chains, Paris, 2012)(as cited by

(Hernandez et al., 2013)).

function over the production of crops. They kind of act as intermediaries between the exporting

country and the importing country, which is also the case in the quinoa value chain. By exer-

cising vertical coordination, the ones with a monitoring function want to guarantee quality and

food safety standards along the chain. The value chains in the agrifood industry are known to

comprise companies and actors in less developed and developing countries. A good example

of agrifood value chains that include such countries is that of the Nutella global value chain,

given by (Hernandez et al., 2013). Nutella, a product which most of the world is very familiar

with, is produced in huge quantities (more than 300.000 tons every year). Figure 2.3 depicts the

different headquarters, international suppliers, factories and sales offices involved in the value

chain of Nutella. In 2013, ten factories all over the world were producing Nutella, as can be

seen by the red triangles on the figure. It is evident from the picture that a lot of ingredients are

supplied globally (indicated by the green dots): Cocoa comes from Ivory Coast, Ghana, Nige-

ria and Ecuador; Sugar from Europe; Palm oil from Papua New Guinea and Brazil; Hazelnut

from Turkey and Vanillin from the USA and Europe. Of course, there are still ingredients and

CHAPTER 2. METHODS OF VALUE CHAIN ANALYSIS 27

attachments which are locally supplied (e.g. Milk). The main sales offices are indicated with

a purple cross and are located all over the world. Note that there are a lot more locations than

those shown on the figure. Nutella has positioned the factories in such a way that Nutella can be

easily supplied to the markets with the highest demand (think of Europe, North-America, Aus-

tralia and Brazil). Until now, Nutella isn’t that well known in Asia and therefore, no factories are

installed yet. We can conclude from this example that the value chains in the agrifood indus-

try are significantly focused internationally and involve ingredients produced in less developed

and developing countries such as cocoa from Central Africa. This value chain of Nutella has

several similarities with the quinoa value chain in such a way that quinoa is mainly cultivated

and processed in less developed countries (Bolivia, Peru) before it is transported to countries

with a higher demand (Europe, North-America). It is also different in such a way that all the

inputs for quinoa production are available in Peru. Producers or processors don’t need to get

inputs from other continents, which is the case for the production of Nutella.

2.4 Game Theory

2.4.1 Introduction

(Turocy et al., 2003) defines a game theory as "the formal study of decision-making where sev-

eral players must make choices that potentially affect the interests of the other players." It is

actually an inquiry of the degree of cooperation and competition or conflict between the differ-

ent parties involved in particular activities and interdependent on each other. Its strength lies

in the methodology it uses to structure and analyse problems of strategic choice (Turocy et al.,

2003). It is very important to have a list of the actors and their strategic options, taking into

account their preferences and actions/reactions. A game theory can be established if there is

competition between the actors of the considered value chain and outside value chain actors.

In reality, this competition is always imperfect. (Stiegert, 2008) defines imperfect competition

as the ability of a company to charge prices that are above marginal costs. It is a market situation

in which many sellers are present that sell heterogeneous products. Firms are expected to be

able to determine prices that result in ending up with significant margins and profits. The game

theory related to imperfect competition is referred to as the non-cooperative game theory.

CHAPTER 2. METHODS OF VALUE CHAIN ANALYSIS 28

2.4.2 Application of Game Theory in Agriculture

Since agriculture has to cope with a time lag between investment and pay-off (it can take up to

a year or more from seed to harvest and sale), price-taking principles and unexpected weather

conditions etc., uncertainly is said to be omnipresent in agriculture. Game theory models that

address the uncertainty and decision-making processes in agriculture need to be investigated:

On the one hand, this concerns long-term decisions regarding the location, the type of farm-

ing, the size of the farm, purchase or rental of land, materials and machines to invest in and

timing of investment, human capital and other resources (Agrawal and Heady, 1968). On the

other hand, short-term decisions need to be made such as when to sell, how long to store, the

kind of manure and the amount, whether other techniques are more useful etc. (Agrawal and

Heady, 1968). Another important factor that enforces uncertainty is of course the lack of knowl-

edge about the decisions and moves of competitors. (Agrawal and Heady, 1968) give some game

theories that can be applied in agriculture but they refer to the late 60s and are somewhat out-

dated. (Sexton et al., 1994) also examined game theories in agricultural markets and stated

that agricultural products are expensive to transport because they are bulky and perishable.

Therefore, the markets for raw agricultural products are actually geographical markets where

imperfect competition will certainly occur. It is said to be present in the international trade

of multiple agricultural products because trading agencies, the government and other author-

ities intervene in import and export to get control of the situation. According to (Sexton et al.,

1994), uncertainty or lack of information that causes asymmetries between the actors is an im-

portant source of strategic behaviour. As stated earlier and again confirmed by (Sexton et al.,

1994), informational asymmetries are omnipresent in agricultural markets. An example given

by (Sexton et al., 1994) mentions that processors may have more information regarding markets

overseas than farmers which gives them incentives to misuse these advantages. On the other

hand, farmers may have informational advantages regarding the characteristics and quality of

their crops.

The models established by (Sexton et al., 1994) include Principal-Agent Models, Auctions and

Collective Bargaining. All of these are more or less present in the quinoa industry. Collective

Bargaining is a method commonly used by the associations of farmers in order to negotiate

better prices with exporters etc. Auctions are sporadically present in the quinoa industry. They

can be used to boost the quinoa price enormously, although this can have a lot of negative

CHAPTER 2. METHODS OF VALUE CHAIN ANALYSIS 29

effects in the long term.

Principal-Agent Models

(Sexton et al., 1994) define Principal-Agent Models as models in which the principal is the entity

who hires the agent to perform some task. The principal may be a farmer who is looking for a

marketing firm to act as an agent and sell the farmer’s products. The agent may have an infor-

mational advantage in this case, as he is better informed about market conditions etc. Another

example is a processor who acts as a principal and is looking for a farmer to cultivate speci-

fied products. In this case, the farmers have an informational advantage because they have the

knowledge about productions costs and quality etc. This is not restricted to farmers and pro-

cessors but can also be applied in other parts of the value chain (e.g. An exporter can act as the

principal while retailing firms as the agents or vice versa). (Sexton et al., 1994) make a distinc-

tion between three models based on the information asymmetries between the actors. These

models are:

1. Moral hazard models: Models in which actions taken by the agents are executed without

the principal knowing or seeing it. It may be most relevant in agriculture when the proces-

sor acts as the principal and the farmer as the agent. This allows farmers to influence the

quality of products and reap more benefits for example. It is the processor’s responsibility

to be totally informed by means of contracts and financial terms.

2. Adverse selection models: Models in which the agents have secret knowledge which they

don’t want to share with the principal, already from before getting in contact. These mod-

els may result in the elimination of products of higher quality because of the inability to

recognize and reward quality and may lead to overage of low-quality products. Thereby, it

also provides motives for the government to intervene with certain quality standards and

certifications.

3. Vertical control: This kind of model includes contracts in which upstream entities (e.g.

Farmer) restrict the behaviour of downstream entities (e.g. Processor or exporter). These

contracts involve exclusive sales arrangements, fees, fixed quantities, bundling of goods,

etc. It is the goal of the farmer to select contractual tools appropriately in order to maxi-

mize his/her profit and propose them to the processors. These models can be found quite

often in the food retailing part of agriculture.

CHAPTER 2. METHODS OF VALUE CHAIN ANALYSIS 30

Auctions

Auctions are mainly used in case prices are fluctuating constantly, when fixed prices don’t work

accordingly (e.g. fish, eggs, fruits and vegetables) or when quality of a good is variable (e.g.

livestock, wool, used equipment). In order to thrive on a continuous basis and establish value,

many actors on both the selling side and the buying side are needed to facilitate the move-

ment towards a competitive market price that reflects true value. (Sexton et al., 1994) states

that monopoly’s (one supplier) and monopsony’s (one buyer) can also be favourable with re-

gard to auctions (e.g. governments can act as a monopolist for oil and mineral exploitations

but can also act as a monopsonist for public services and construction projects because they

are the one providing the capital to build these projects). The main reason for monopolists and

monopsonists to use auctions is asymmetry of information (Sexton et al., 1994). Since a mo-

nopolist is the only provider of a particular product, he is able to set take-it-or-leave-it prices

to maximize his own value when buyers know the value of the product. The other way around

counts for monopsonists.