Languages

Pages

Legal

CONFIDENTIALAFC Asia Frontier FundSeptember 2013

AFC Asia Frontier Fund May 2017

2

INTRODUCING ASIA FRONTIER CAPITAL

AFC Asia Frontier Fund

3

Proven Expertise In Frontier Markets• Asia Frontier Capital Limited was created in June 2013 through a Management Buy Out from Leopard Capital• The founder and CEO, Thomas Hugger, has more than 20 years experience in investing in Frontier Markets• Licensed by SFC Hong Kong for Type 4 (advising on securities) and Type 9 (asset management)

Asia Frontier Capital Offers Three Funds• AFC Asia Frontier Fund – Launched 30th March 2012• AFC Vietnam Fund – Launched 23rd December 2013• AFC Iraq Fund – Launched 26th June 2015

Attractive Equities Identified in Structured Investment Policy• Asia Frontier Capital has identified equities with good upside potential• The Fund has access to numerous primary and secondary research sources• A Structured Investment and Research process is being followed

AFC Asia Frontier Fund

INTRODUCING ASIA FRONTIER CAPITAL

Our Team

Thomas Hugger, CEO and Fund Manager, has spent 27 years inprivate banking and has been investing in Asian and AfricanFrontier Markets since 1993. He is the former Managing Partner,CFO & COO of Leopard Capital; and was previously a ManagingDirector and Head of Portfolio Management at LGT Bank in HongKong. Mr. Hugger was the founding shareholder of one of thelargest brokerage companies in Bangladesh. He is also a CertifiedFinancial Investment Analyst (CFIA) and Investment Adviser(Switzerland) and a Certified European Federation of FinancialAnalysts Societies (EFFAS) Financial Analyst.

Ahmed Tabaqchali, CIO of Iraq Investments, is an experienced capitalmarkets professional with over 22 years of experience in MENAmarkets as well as the US. He is currently a board member of the CreditBank of Iraq and former Executive Director of NBK Capital, theinvestment banking arm of the National Bank of Kuwait. Prior to theseroles Ahmed was Managing Director and Head of InternationalInstitutional Sales at WR Hambrecht + Co. This followed on from rolesas a Managing Director at KeyBanc Capital Markets and Director &Head of Capital Markets & Institutional Sales at Jefferies Int'l in London.Ahmed is an Iraqi as well as British national and holds a M.Sc. inMathematics from Oxford University in England, a B.Sc. (Hons, 1st class)in Mathematics from Victoria University and a B.Sc. in Mathematicsfrom Canterbury University in New Zealand.

Ruchir Desai, CFA, Senior Investment Analyst, is an MBA graduatein Finance from CUHK Business School at The Chinese University ofHong Kong and is also an alumnus of The Fuqua School of Businessat Duke University where he spent a semester during his MBAprogram. He is also a Chartered Financial Analyst (CFA) charterholder. Prior to being based in Hong Kong, Ruchir was based inMumbai where he spent two years as a Senior Analyst at HandsOnVentures LLC, a private equity group focused on investments in theBusiness Services industry. Prior to this role, he spent three yearsas a Research Analyst at Pioneer Investcorp Ltd, an institutionalbrokerage based in Mumbai.

Peter de Vries, Marketing Director, has over 25 years experience infinance of which 20 in Hong Kong. He is a former Director and SeniorRelationship Manager at Leopard Capital. Prior to that he was anExecutive Vice President at Upbest Financial Services where he wasinvolved with fund raising and deal structuring for real estateinvestment and development projects in Macau. Previously he workedas Executive Vice President at ViewTrade Securities in Hong Kong ashead of the business development for the Asia Pacific region. Mr. DeVries has also held the position of Assistant Vice President at MerrillLynch Asia Pacific. He holds an MBA in finance from Calstate Hayward,and a Masters of Science in Electrical Engineering from TwenteUniversity in the Netherlands. Mr. De Vries is fluent in Dutch, Englishand German.

Scott Osheroff, Regional Research Analyst, holds a Bachelor’sDegree in Business Administration with a Concentration in Financefrom Northeastern University. Prior to joining Asia Frontier Capital,Scott worked with Pathfinder Capital Management in SoutheastAsia and Mongolia. Prior to this role, Scott co-founded a publishingcompany whose principal asset, EmergingFrontiers.com, wasleveraged to provide investment coverage on public and privateinvestments in Asia’s frontier markets. He has spent the last twoyears between Mongolia and Cambodia, and currently resides inYangon, Myanmar.

Ms. Margaret Kwok, Accounting & Administration Executive, has over30 years of prior work experience in accounting, administration, andfinancial services at institutions such as Christfund Securities, PFCInternational, and Guoyuan Securities. She holds advanced levelcertificates in Accounting & Costing from London Chamber ofCommerce & Industry and a Certificate in Accountancy from KwaiChung Technical Institute. Margaret is fluent in Cantonese, Mandarinand English.

4AFC Asia Frontier Fund

OUR TEAM

Our Team

Thomas Hugger, CEO and Fund Manager,has spent 27 years in private banking and hasbeen investing in Asian and African FrontierMarkets since 1993. He is the formerManaging Partner, CFO & COO of LeopardCapital; and was previously a ManagingDirector and Head of Portfolio Managementat LGT Bank in Hong Kong. Mr. Hugger wasthe founding shareholder of one of thelargest brokerage companies in Bangladesh.He is also a Certified Financial InvestmentAnalyst (CFIA) and Investment Adviser(Switzerland) and a Certified EuropeanFederation of Financial Analysts Societies(EFFAS) Financial Analyst.

Lord Fraser of Corriegarth, Director.Andrew Fraser is a graduate of St John'sCollege, Oxford after which he held numerousposts in the financial sector both in the City ofLondon and elsewhere. He has previously heldpositions as; CEO of Baring Securities in theUK, Chairman of Equity Partners Ltd., aBangladesh investment bank, as well asChairman of Bridge Securities, a quoted Koreancompany, amongst other posts. At present heis a global investor based in London.

Dr. Marc Faber, is CEO, investment advisor

and fund manager of Marc Faber Limited. He

is the publisher of a widely read monthly

investment newsletter The Gloom, Boom

and Doom report which highlights global

investment opportunities. Dr. Faber is

respected around the world for his market

forecasts over the past three decades.

5AFC Asia Frontier Fund

SHAREHOLDERS OF ASIA FRONTIER CAPITAL LIMITED

6

WHY ASIAN FRONTIER MARKETS?

AFC Asia Frontier Fund

7AFC Asia Frontier Fund

WHY ASIAN FRONTIER MARKETS

AFC Asia FrontierFund Universe

Bangladesh

Cambodia

Iraq

Laos

Maldives

Mongolia

Myanmar

Pakistan

Papua New Guinea

Sri Lanka

Vietnam

8

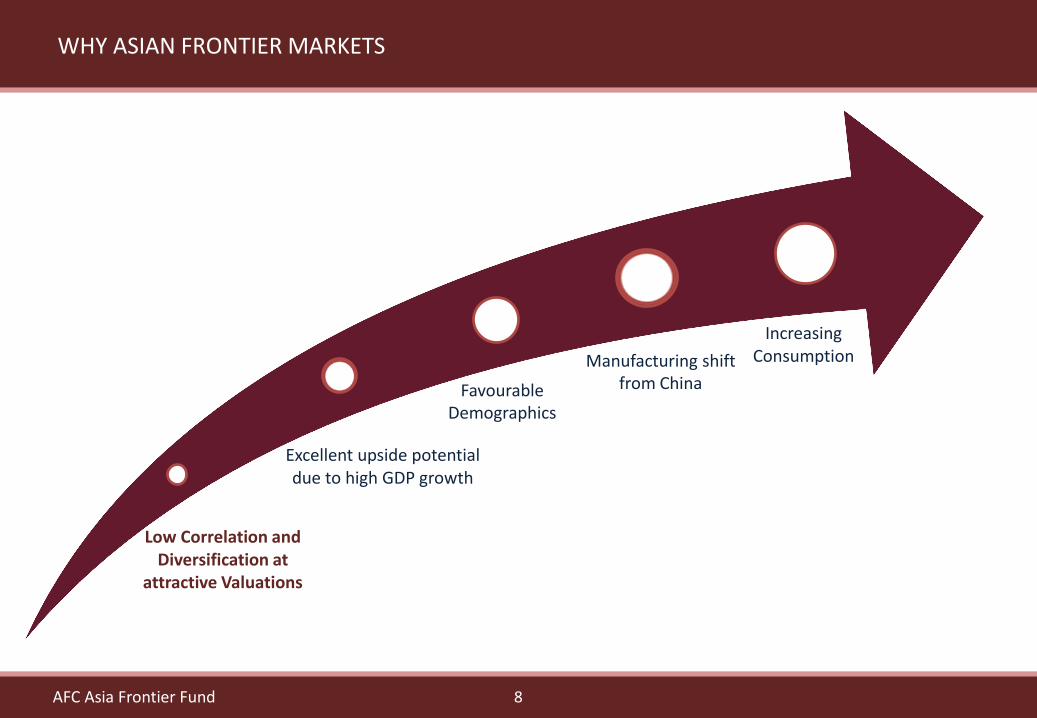

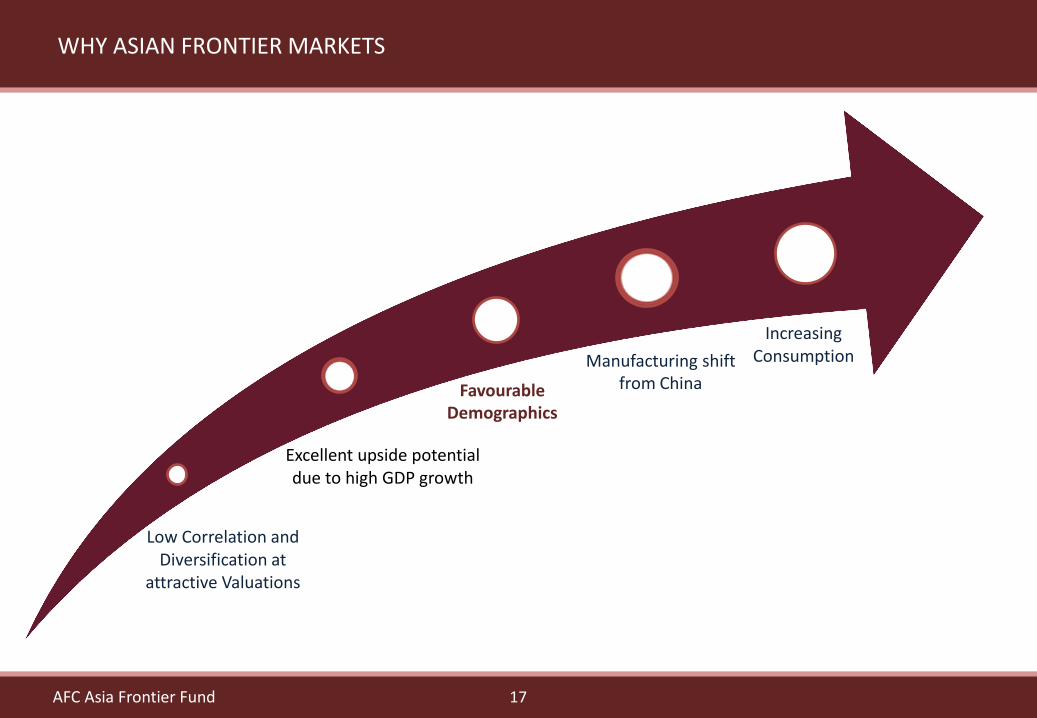

Excellent upside potential due to high GDP growth

Low Correlation and Diversification at

attractive Valuations

Increasing Consumption

Favourable Demographics

AFC Asia Frontier Fund

WHY ASIAN FRONTIER MARKETS

Manufacturing shift from China

9

Diversification has led to Low Correlations for the Fund with Global Markets

AFC Asia Frontier Fund

Source: Bloomberg, Asia Frontier Capital. Correlations based on Monthly Returns and Net Fund ReturnsAAFF – AFC Asia Frontier Fund

WHY ASIAN FRONTIER MARKETS

Correlation of AAFF with MSCI Indexes since Inception (30th March 2012)

Variable AAFFMSCI World

Index

MSCI Emerging Markets

Index

MSCI BRIC Index

MSCI Frontier Markets Index

MSCI World Index 0.33 1.00

MSCI Emerging Markets Index 0.30 0.75 1.00

MSCI BRIC Index 0.33 0.74 0.98 1.00

MSCI Frontier Markets Index 0.57 0.63 0.58 0.57 1.00

MSCI Frontier Markets Asia Index 0.79 0.43 0.35 0.35 0.62

10

Low Correlations for the Fund with Global Markets has led to excellent Risk-Return profile

AFC Asia Frontier Fund

*Returns of indexes are based on Net Total Return USD IndexesReturns of funds are net, after fees.

Annualised Volatility

Cumulative Returns*

AFC Asia Frontier Fund 9.01% 78.07%

MSCI World Index 10.87% 58.77%

MSCI Frontier Markets Index

11.60% 34.26%

MSCI Frontier Markets Asia Index

13.61% 42.04%

MSCI Emerging Market Index

15.26% 6.37%

MSCI BRIC Index 18.39% 4.04%

WHY ASIAN FRONTIER MARKETS

AFC Asia Frontier Fund USD A

MSCI World

MSCI Frontier Markets

MSCI Frontier Markets Asia

MSCI Emerging Markets MSCI Bric Index

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

6% 8% 10% 12% 14% 16% 18% 20%

Net

Re

turn

Annualised Volatility

Annualised Volatility vs. Fund Performance (Net) (Since Inception, March 2012)

11

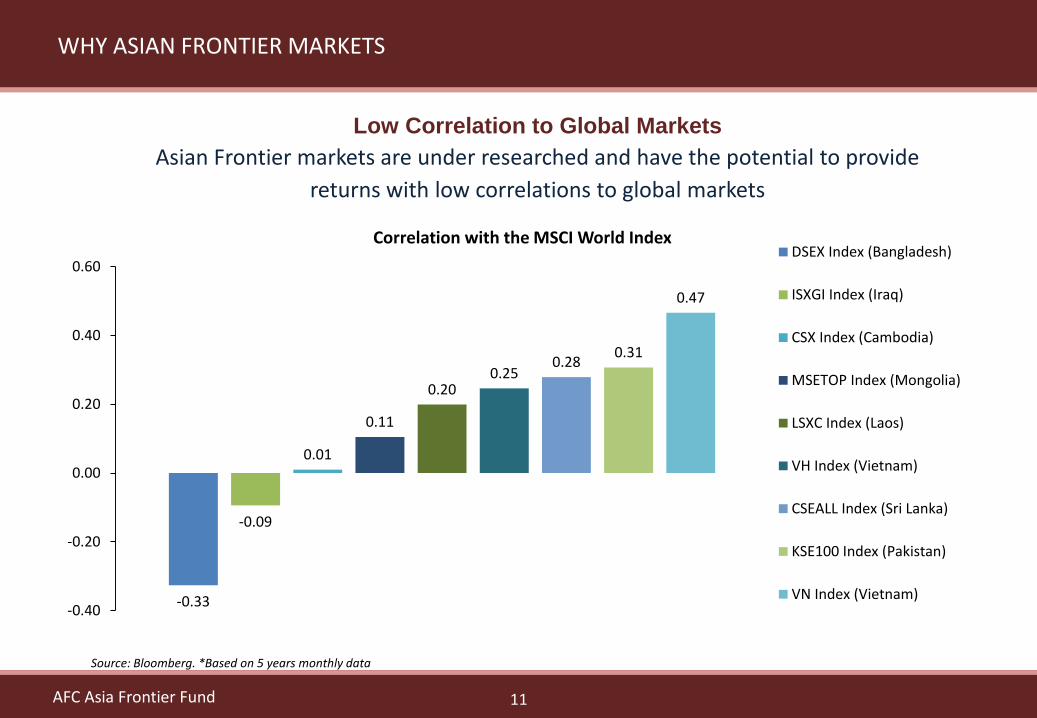

Low Correlation to Global Markets

Asian Frontier markets are under researched and have the potential to provide

returns with low correlations to global markets

AFC Asia Frontier Fund

WHY ASIAN FRONTIER MARKETS

Source: Bloomberg. *Based on 5 years monthly data

-0.33

-0.09

0.01

0.11

0.200.25

0.280.31

0.47

-0.40

-0.20

0.00

0.20

0.40

0.60

Correlation with the MSCI World IndexDSEX Index (Bangladesh)

ISXGI Index (Iraq)

CSX Index (Cambodia)

MSETOP Index (Mongolia)

LSXC Index (Laos)

VH Index (Vietnam)

CSEALL Index (Sri Lanka)

KSE100 Index (Pakistan)

VN Index (Vietnam)

12

Attractive Valuations

Asian Frontier markets offer attractive dividend yieldsand lower Price to Earnings and Price to Book ratiosrelative to emerging markets

Asian Frontier markets are valued attractively relativeto emerging Asian countries

AFC Asia Frontier Fund

Source: Bloomberg. P/E is based on Trailing 12 Months and P/B is latest reporting period.

WHY ASIAN FRONTIER MARKETS

Select Asian Frontier Index Valuations

Country Index P/E (x) P/B (x)Dividend Yield (%)

Pakistan KSE100 10.6 2.0 4.3

Laos LSXC 11.3 0.9 6.4

Sri Lanka CSEALL Share 12.0 1.3 3.1

Vietnam VNINDEX 15.6 2.2 2.9

Emerging Asia Index Valuations

Country Index P/E (x) P/B (x)Dividend Yield (%)

Thailand SET 16.5 1.9 3.1

Malaysia FBMKLCI 17.4 1.8 3.1India BSE SENSEX 21.8 2.8 1.3

Philippines PCOMP 21.8 2.5 1.6Indonesia JCI 23.3 2.5 1.9

Source: Bloomberg. P/E is based on Trailing 12 Months and P/B is latest reporting period.

13AFC Asia Frontier Fund

WHY ASIAN FRONTIER MARKETS

Low Market Cap/GDP relative to Emerging Markets Offers Value

Source: Bloomberg, Asia Frontier Capital

3% 6% 8%

19% 22%28%

32%39% 39% 40% 43%

69%74%

82% 83%

102%

0%

20%

40%

60%

80%

100%

120%

Market Cap. as % of GDP - Asian Frontier v/s Emerging Markets

14

Excellent upside potential due to high GDP growth

Low Correlation and Diversification at

attractive Valuations

Increasing Consumption

Favourable Demographics

AFC Asia Frontier Fund

WHY ASIAN FRONTIER MARKETS

Manufacturing shift from China

15

Healthy GDP Growth Outlook for AFC Frontier Universe

AFC Asia Frontier Fund

WHY ASIAN FRONTIER MARKETS

Source: IMF

7.77.2 6.8 6.7

6.25.3 5.2

4.7 4.6

3.1

1.4

5.4

0.0

2.0

4.0

6.0

8.0

10.0

Average GDP Growth Estimates (2017-2021)

16

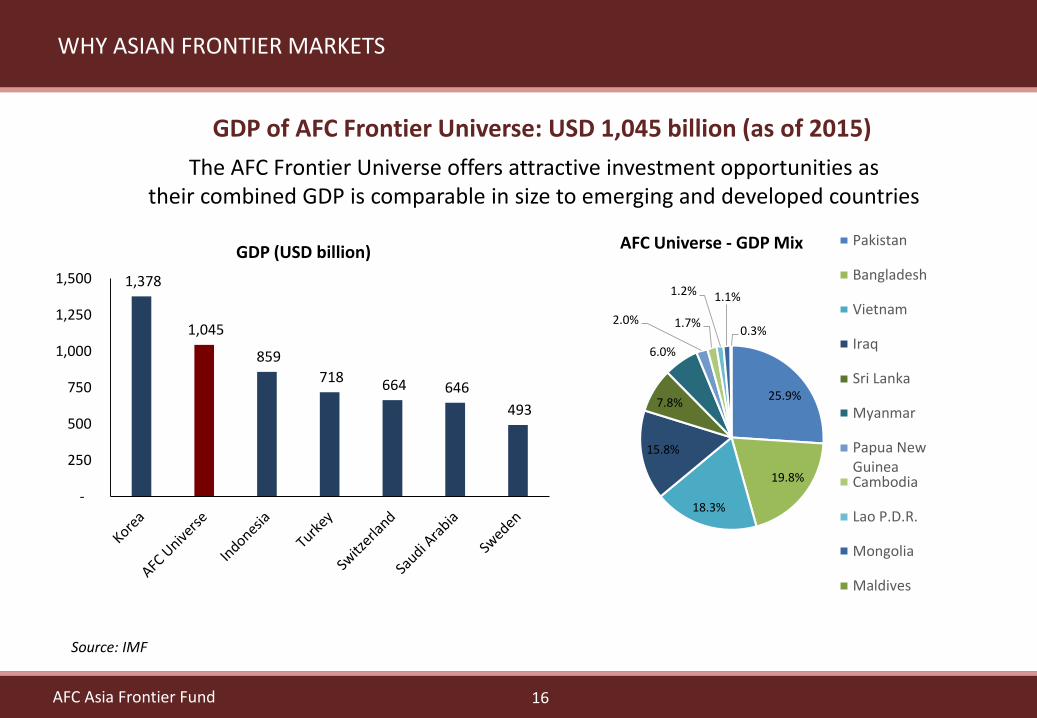

The AFC Frontier Universe offers attractive investment opportunities as their combined GDP is comparable in size to emerging and developed countries

AFC Asia Frontier Fund

WHY ASIAN FRONTIER MARKETS

Source: IMF

GDP of AFC Frontier Universe: USD 1,045 billion (as of 2015)

25.9%

19.8%

18.3%

15.8%

7.8%

6.0%

2.0% 1.7%

1.2% 1.1%

0.3%

AFC Universe - GDP Mix Pakistan

Bangladesh

Vietnam

Iraq

Sri Lanka

Myanmar

Papua NewGuineaCambodia

Lao P.D.R.

Mongolia

Maldives

1,378

1,045

859

718 664 646

493

-

250

500

750

1,000

1,250

1,500

GDP (USD billion)

17

Excellent upside potential due to high GDP growth

Low Correlation and Diversification at

attractive Valuations

Increasing Consumption

Favourable Demographics

AFC Asia Frontier Fund

WHY ASIAN FRONTIER MARKETS

Manufacturing shift from China

18AFC Asia Frontier Fund

WHY ASIAN FRONTIER MARKETS

The AFC Frontier Universe has a sizeable population which continues to grow and will support future GDP growth

AFC Frontier Universe Combined Population: 583 million (as of 2015)

Source: IMF

32.6%

27.4%

15.7%

8.9%

6.0%

3.6%2.7%

1.3% 1.2% 0.5% 0.1%

AFC Universe - Population Mix Pakistan

Bangladesh

Vietnam

Myanmar

Iraq

Sri Lanka

Cambodia

Papua NewGuineaLao P.D.R.

Mongolia

Maldives

1,373 1,293

583

337 322 255 204

-

250

500

750

1,000

1,250

1,500

China India AFCUniverse

EuroArea

UnitedStates

Indonesia Brazil

Population (millions)

19

Compared to Developed Markets, the AFC Frontier Universe has a much younger population growing at a faster rate: This supports future economic growth and consumption

AFC Asia Frontier Fund

WHY ASIAN FRONTIER MARKETS

Source: United Nations Population Division.

AFC Frontier Universe – A Young and Growing Population

AFC Frontier Universe is supported by huge young population Developed Markets are not getting younger. AFC Frontier Universe offer young and growing population

59%

39% 37%33%

28%

0%

20%

40%

60%

80%

AFCUniverse

NorthAmerica

NorthernEurope

WesternEurope

Japan

% of Population below age of 30

25

38 4044

471.5%

0.7%0.6%

0.2%

-0.2%-0.4%

0.0%

0.4%

0.8%

1.2%

1.6%

0

10

20

30

40

50

AFCUniverse

NorthAmerica

NorthernEurope

WesternEurope

Japan

Median Age and Population Growth

Median Age Population Growth

20AFC Asia Frontier Fund

Increasing urbanisation will support growth in the Consumer, Infrastructure and Financial sectors

WHY ASIAN FRONTIER MARKETS

The AFC Universe is Urbanising from a Low Base

Source: World Bank

38%

62%

AFC Universe

Urban Rural

80%

20%

OECD Members

Urban Rural

21

Excellent upside potential due to high GDP growth

Low Correlation and Diversification at

attractive Valuations

Increasing Consumption

Favourable Demographics

AFC Asia Frontier Fund

WHY ASIAN FRONTIER MARKETS

Manufacturing shift from China

22AFC Asia Frontier Fund

Asian Frontier countries presently have similar demographics to what China had in the 1990s. By 2020 Asian Frontier countries will continue to have a young population relative to China

WHY ASIAN FRONTIER MARKETS

The Shift from China

Source: United Nations Population Division

Median Age – China in 1990 v/s Asian Frontier countries at present have similar median ages

% of Population > Age 60 – China v/s Asian Frontier countries in 2020 - Asian Frontier countries’ younger population offer an

alternative to China

37

2522 22 24 26

2830

32

0

10

20

30

40

Median Age

17%16%

13%

10%

8% 8% 7% 7%

0%

4%

8%

12%

16%

20%

% of Population Aged > 60

23AFC Asia Frontier Fund

Combination of young workforce and low wages is attracting manufacturing activities to Asian frontier countries as wages in China increase and the workforce gets greater employment opportunities

WHY ASIAN FRONTIER MARKETS

The Shift from China

Source: China Statistical Bulletin, Wage Indicator Foundation, Bangladesh Garment Manufacturers & Exporters Association, General Statistics Office of Vietnam

*Rebased to 100 (2003). RMG: Ready Made Garments

Wages in Asian Frontier countries are amongst the lowest in the regionBangladesh and Vietnam are good examples of the shift of

manufacturing from China to neighboring countries

0

100

200

300

400

500

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Bangladesh RMG & Vietnam Export Growth*

Bangladesh Vietnam

65 6883

111 115133

150

223251 252

274298

0

75

150

225

300

375

Monthly Minimum Wage (USD)

24

Excellent upside potential due to high GDP growth

Low Correlation and Diversification at

attractive Valuations

Increasing Consumption

Favourable Demographics

AFC Asia Frontier Fund

WHY ASIAN FRONTIER MARKETS

Manufacturing shift from China

25AFC Asia Frontier Fund

Percentage of Durables in Private Consumption

AFC AsiaFrontier Fund

Universe

Per capita income USD PPP (2012)

Bangladesh $ 729

Cambodia $ 792

Iraq $ 3,918

Laos $ 1,017

Maldives $ 4,385

Mongolia $ 2,499

Myanmar -

Pakistan $ 1,217

PNG $ 1,625

Sri Lanka $ 2,699

Vietnam $ 1,372

WHY ASIAN FRONTIER MARKETS

26AFC Asia Frontier Fund

Consumption Expenditure is Increasing in Frontier Markets

0

1

2

3

4

5

6

7

8

9

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Household final consumption expenditure per capita growth (annual %)

BRICS Average Linear (BRICS Average)

-1

0

1

2

3

4

5

6

7

8

9

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Household final consumption expenditure per capita growth (annual %)

AFC Country Universe Average Linear (AFC Country Universe Average)

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Household final consumption expenditure per capita (USD - constant 2005) Bangladesh

Cambodia

Iraq

Lao PDR

Maldives

Mongolia

Myanmar

Pakistan

Papua NewGuineaSri Lanka

Vietnam

AFC Average

-2

-1

0

1

2

3

4

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Household final consumption expenditure per capita growth (annual %)

Developed Countries Linear (Developed Countries)

WHY ASIAN FRONTIER MARKETS

27AFC Asia Frontier Fund

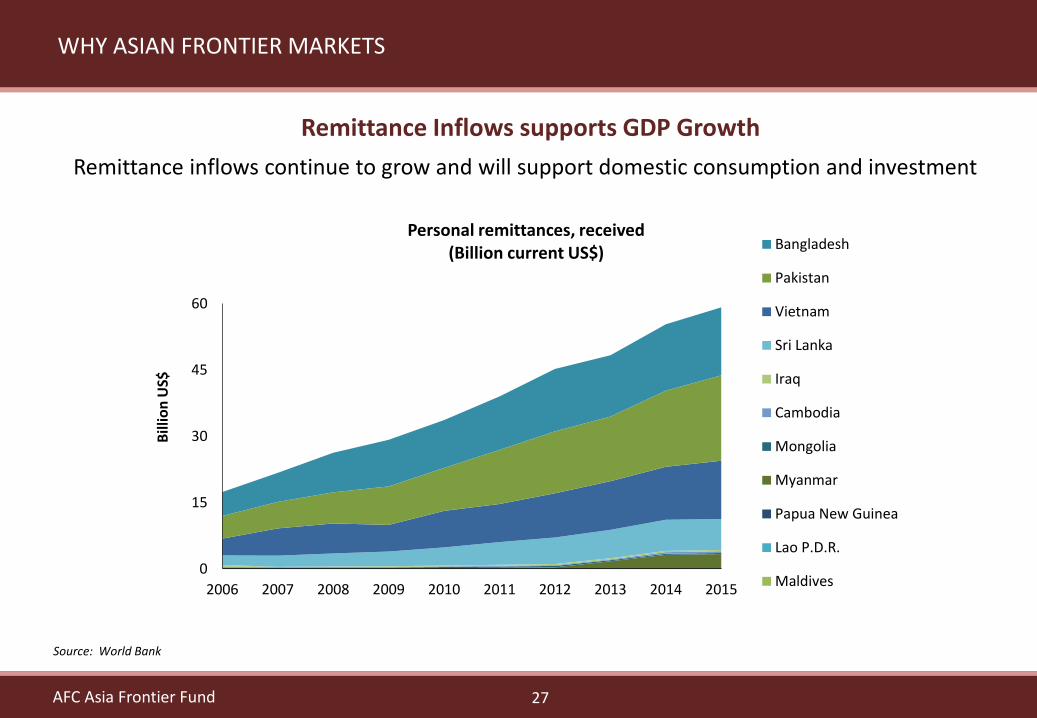

WHY ASIAN FRONTIER MARKETS

Remittance inflows continue to grow and will support domestic consumption and investment

Remittance Inflows supports GDP Growth

Source: World Bank

0

15

30

45

60

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Bill

ion

US$

Personal remittances, received (Billion current US$)

Bangladesh

Pakistan

Vietnam

Sri Lanka

Iraq

Cambodia

Mongolia

Myanmar

Papua New Guinea

Lao P.D.R.

Maldives

28AFC Asia Frontier Fund

Asian Frontier Consumer Stocks are undervalued and some companies have been catching up with Emerging Market valuations over the past year. This has helped generate alpha for the fund.

Asian Frontier Consumer Picks

Regional Comparisons

Source: Bloomberg. P/E based on Trailing 12 Month Earnings, P/B based on most recent reporting period.

Country Company P/E (x) P/B (x) Dividend Yield (%)

Vietnam Consumer Beverage Products 8.7 1.8 1.7

Vietnam Consumer Food Products 14.1 3.8 5.0

Mongolia Consumer Food Products 17.1 0.5 0.6

Bangladesh Shoe Retailer 18.7 5.3 2.0

Pakistan Automobile Manufacturer 22.6 2.6 0.6

Country Company P/E (x) P/B (x) Dividend Yield (%)

Thailand President Bakery 19.7 4.7 2.6

Philippines Universal Robina Corp 25.9 5.3 1.8

India Maruti Suzuki India 26.8 5.4 0.5

India Bata India 33.7 6.2 0.6

China Tsingtao Brewery 38.8 2.5 1.2

WHY ASIAN FRONTIER MARKETS

29

INVESTMENT STRATEGY

AFC Asia Frontier Fund

30

Top-down Approach

Value / Growth

Risk Mitigation

Cash

AFC Asia Frontier Fund

INVESTMENT STRATEGY

INVESTMENT STRATEGY – IDEA GENERATION PROCESS – COMBINATION OF BOTTOM UP-TOP DOWN

31AFC Asia Frontier Fund

Bottom-up stock shortlisting using tools

based on Valuation and Fundamental

parameters

Top-down stock shortlisting based on

economy and industry analysis

Access to Third Party Research (daily

updates, company specific research, industry research)

On the ground visits to countries. Conducted

269 management meeting over the past

15 months

Relationship with sell side analysts for views on company/industry

32AFC Asia Frontier Fund

•Historical trend of growth, margins and cash from operations

• Focus on trend in RoEs and dividend payout ratios.Historical Financial Statement

Analysis

•Well established brand

• Large distribution network

•High Market Share

•Economies of Scale

•Cost Structure

• Stable Management

Competitive Advantages

• Is company operating in an industry with favorable outlook

•Example 1: Shoes per capita in Bangladesh is significantly lower than emerging market peers

•Example 2: Upswing in infrastructure spending in Pakistan positive for cement companies

Industry Outlook & Opportunity

• Conduct both local and regional peer analysis by comparing valuation, fundamental and industry metrics

Peer Comparison Analysis

INVESTMENT STRATEGY – RESEARCH PROCESS

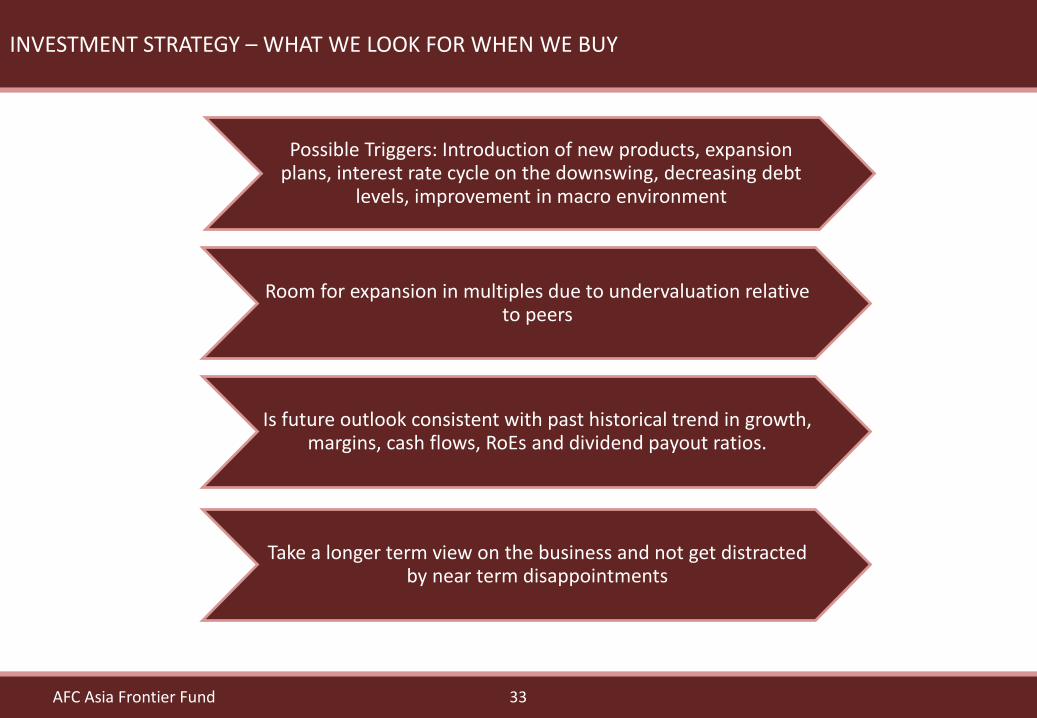

INVESTMENT STRATEGY – WHAT WE LOOK FOR WHEN WE BUY

33AFC Asia Frontier Fund

Possible Triggers: Introduction of new products, expansion plans, interest rate cycle on the downswing, decreasing debt

levels, improvement in macro environment

Room for expansion in multiples due to undervaluation relative to peers

Is future outlook consistent with past historical trend in growth, margins, cash flows, RoEs and dividend payout ratios.

Take a longer term view on the business and not get distracted by near term disappointments

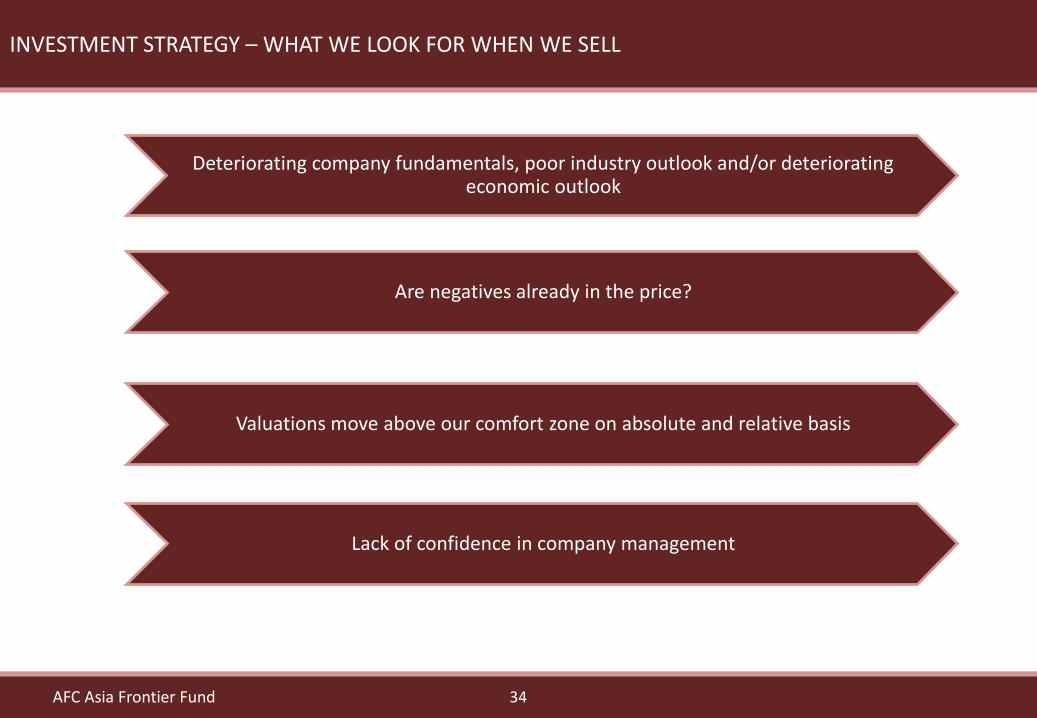

INVESTMENT STRATEGY – WHAT WE LOOK FOR WHEN WE SELL

34AFC Asia Frontier Fund

Deteriorating company fundamentals, poor industry outlook and/or deteriorating economic outlook

Are negatives already in the price?

Valuations move above our comfort zone on absolute and relative basis

Lack of confidence in company management

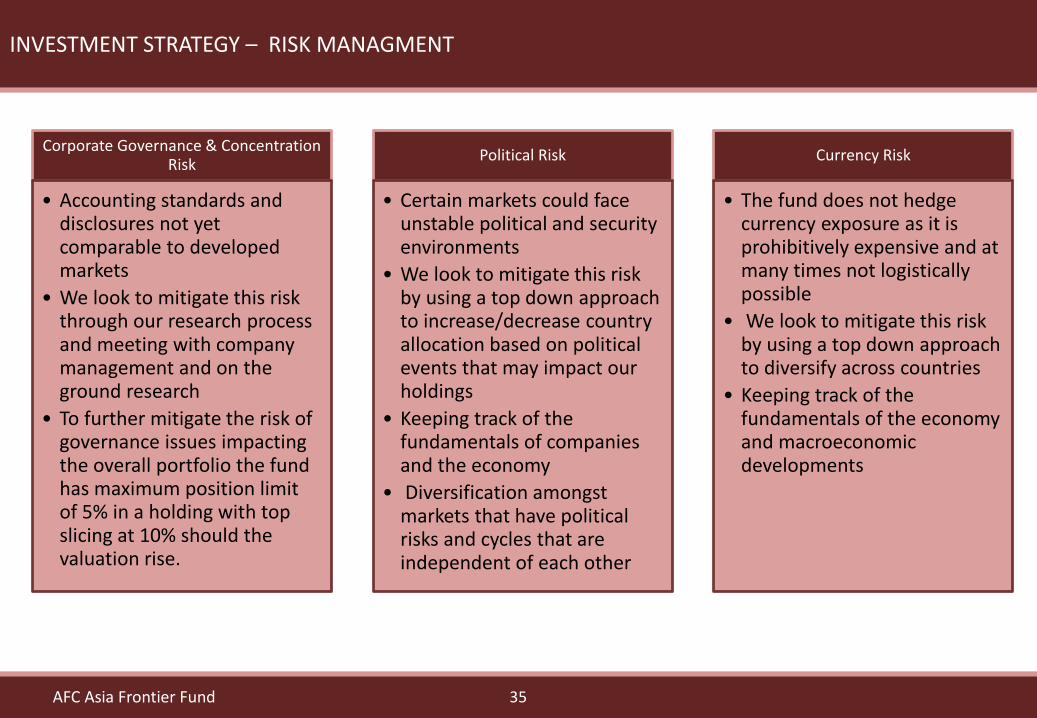

INVESTMENT STRATEGY – RISK MANAGMENT

35AFC Asia Frontier Fund

Corporate Governance & Concentration Risk

• Accounting standards and disclosures not yet comparable to developed markets

• We look to mitigate this risk through our research process and meeting with company management and on the ground research

• To further mitigate the risk of governance issues impacting the overall portfolio the fund has maximum position limit of 5% in a holding with top slicing at 10% should the valuation rise.

Political Risk

• Certain markets could face unstable political and security environments

• We look to mitigate this risk by using a top down approach to increase/decrease country allocation based on political events that may impact our holdings

• Keeping track of the fundamentals of companies and the economy

• Diversification amongst markets that have political risks and cycles that are independent of each other

Currency Risk

• The fund does not hedge currency exposure as it is prohibitively expensive and at many times not logistically possible

• We look to mitigate this risk by using a top down approach to diversify across countries

• Keeping track of the fundamentals of the economy and macroeconomic developments

INVESTMENT STRATEGY – TOP 10 HOLDINGS

36AFC Asia Frontier Fund

Current Top 10 HoldingsCompany Country Sector % of NAVBeximco

PharmaceuticalsBangladesh Healthcare 9.2%

AFC Iraq Fund Iraq Fund/ETF 3.6%

Searle Company Ltd. Pakistan Healthcare 3.5%

D.G. Khan Cement Pakistan Materials 2.6%

Pak Elektron Pakistan Consumer Discretionary 2.5%

Traphaco JSC Vietnam Healthcare 2.4%

Cotec Construction Vietnam Industrials 2.3%

Hai Duong Pump Vietnam Industrials 2.3%

Safaco Foodstuff Vietnam Consumer Staples 2.4%

Atlas Honda Pakistan Consumer Discretionary 2.0%

37

FUND INFORMATION

AFC Asia Frontier Fund

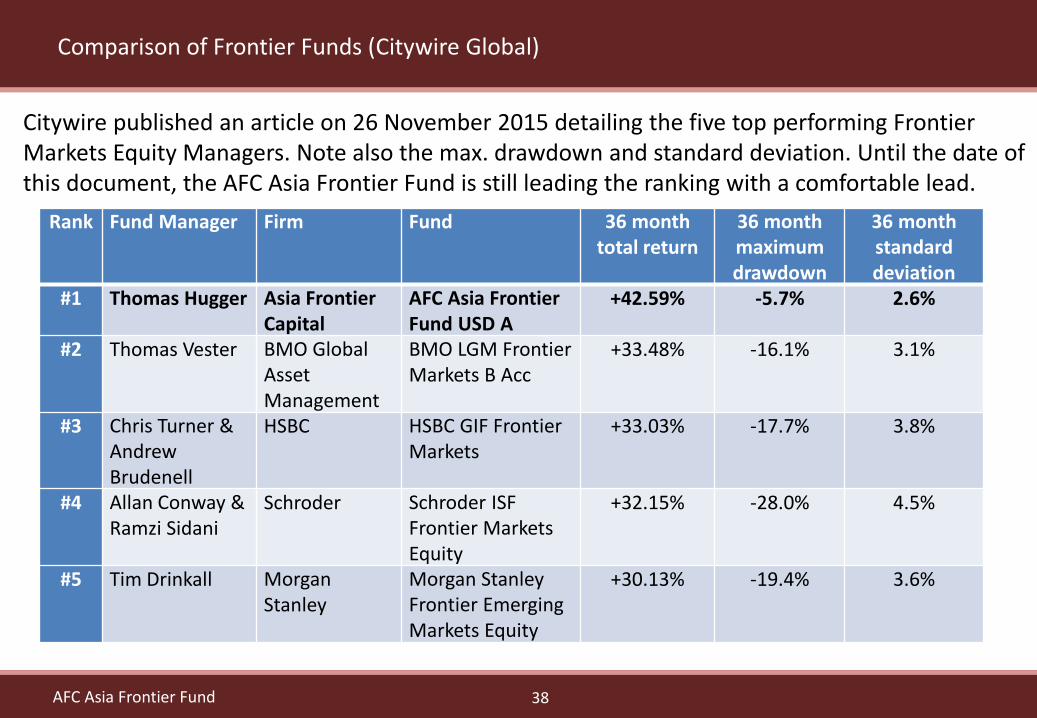

Comparison of Frontier Funds (Citywire Global)

38AFC Asia Frontier Fund

Rank Fund Manager Firm Fund 36 month total return

36 month maximumdrawdown

36 month standard deviation

#1 Thomas Hugger Asia Frontier Capital

AFC Asia Frontier Fund USD A

+42.59% -5.7% 2.6%

#2 Thomas Vester BMO Global Asset Management

BMO LGM Frontier Markets B Acc

+33.48% -16.1% 3.1%

#3 Chris Turner &Andrew Brudenell

HSBC HSBC GIF Frontier Markets

+33.03% -17.7% 3.8%

#4 Allan Conway & Ramzi Sidani

Schroder Schroder ISF Frontier Markets Equity

+32.15% -28.0% 4.5%

#5 Tim Drinkall Morgan Stanley

Morgan Stanley Frontier Emerging Markets Equity

+30.13% -19.4% 3.6%

Citywire published an article on 26 November 2015 detailing the five top performing Frontier Markets Equity Managers. Note also the max. drawdown and standard deviation. Until the date of this document, the AFC Asia Frontier Fund is still leading the ranking with a comfortable lead.

AWARDS

39AFC Asia Frontier Fund

40AFC Asia Frontier Fund

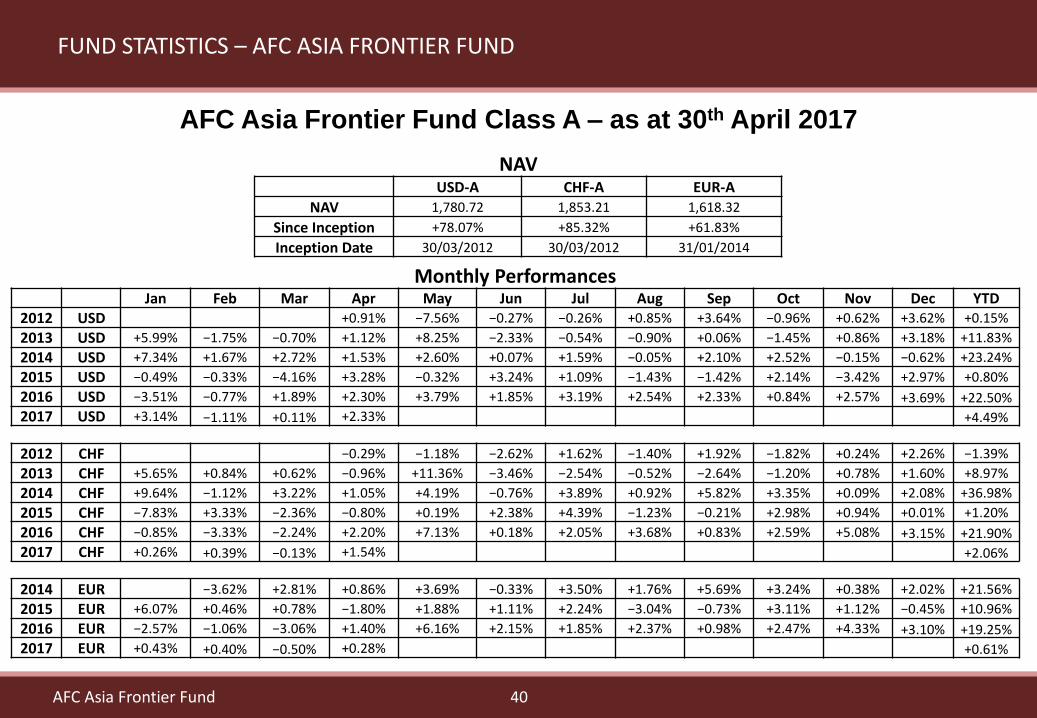

FUND STATISTICS – AFC ASIA FRONTIER FUND

NAVUSD-A CHF-A EUR-A

NAV 1,780.72 1,853.21 1,618.32

Since Inception +78.07% +85.32% +61.83%

Inception Date 30/03/2012 30/03/2012 31/01/2014

Monthly PerformancesJan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec YTD

2012 USD +0.91% −7.56% −0.27% −0.26% +0.85% +3.64% −0.96% +0.62% +3.62% +0.15%

2013 USD +5.99% −1.75% −0.70% +1.12% +8.25% −2.33% −0.54% −0.90% +0.06% −1.45% +0.86% +3.18% +11.83%

2014 USD +7.34% +1.67% +2.72% +1.53% +2.60% +0.07% +1.59% −0.05% +2.10% +2.52% −0.15% −0.62% +23.24%

2015 USD −0.49% −0.33% −4.16% +3.28% −0.32% +3.24% +1.09% −1.43% −1.42% +2.14% −3.42% +2.97% +0.80%

2016 USD −3.51% −0.77% +1.89% +2.30% +3.79% +1.85% +3.19% +2.54% +2.33% +0.84% +2.57% +3.69% +22.50%

2017 USD +3.14% −1.11% +0.11% +2.33% +4.49%

2012 CHF −0.29% −1.18% −2.62% +1.62% −1.40% +1.92% −1.82% +0.24% +2.26% −1.39%

2013 CHF +5.65% +0.84% +0.62% −0.96% +11.36% −3.46% −2.54% −0.52% −2.64% −1.20% +0.78% +1.60% +8.97%

2014 CHF +9.64% −1.12% +3.22% +1.05% +4.19% −0.76% +3.89% +0.92% +5.82% +3.35% +0.09% +2.08% +36.98%

2015 CHF −7.83% +3.33% −2.36% −0.80% +0.19% +2.38% +4.39% −1.23% −0.21% +2.98% +0.94% +0.01% +1.20%

2016 CHF −0.85% −3.33% −2.24% +2.20% +7.13% +0.18% +2.05% +3.68% +0.83% +2.59% +5.08% +3.15% +21.90%

2017 CHF +0.26% +0.39% −0.13% +1.54% +2.06%

2014 EUR −3.62% +2.81% +0.86% +3.69% −0.33% +3.50% +1.76% +5.69% +3.24% +0.38% +2.02% +21.56%

2015 EUR +6.07% +0.46% +0.78% −1.80% +1.88% +1.11% +2.24% −3.04% −0.73% +3.11% +1.12% −0.45% +10.96%

2016 EUR −2.57% −1.06% −3.06% +1.40% +6.16% +2.15% +1.85% +2.37% +0.98% +2.47% +4.33% +3.10% +19.25%

2017 EUR +0.43% +0.40% −0.50% +0.28% +0.61%

AFC Asia Frontier Fund Class A – as at 30th April 2017

41AFC Asia Frontier Fund

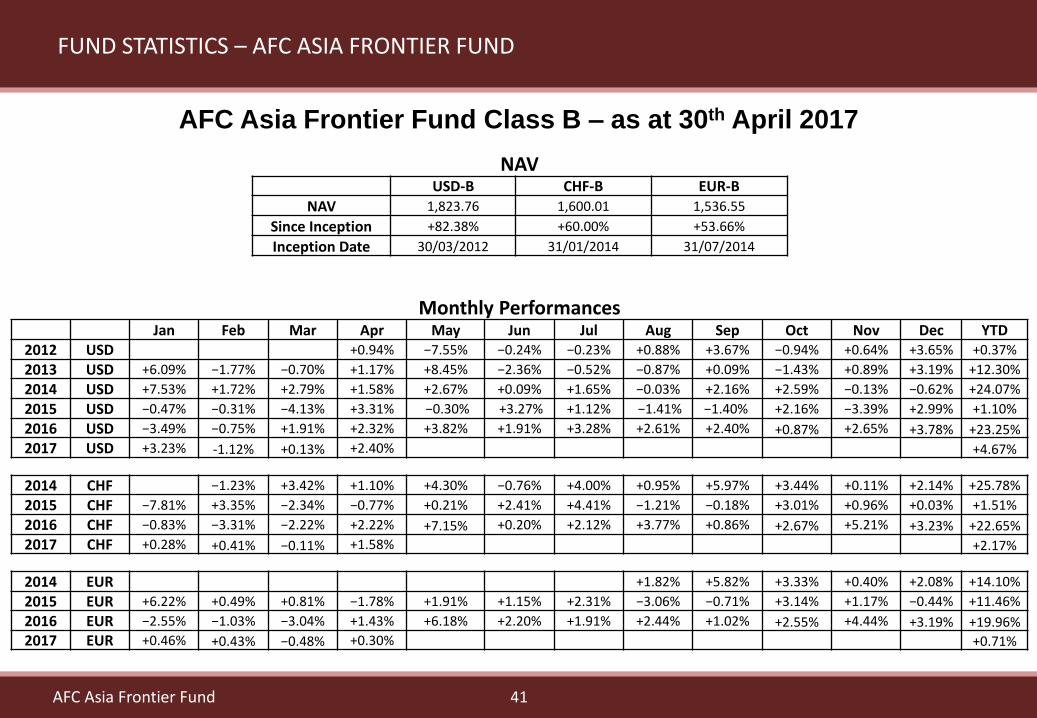

FUND STATISTICS – AFC ASIA FRONTIER FUND

Monthly PerformancesJan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec YTD

2012 USD +0.94% −7.55% −0.24% −0.23% +0.88% +3.67% −0.94% +0.64% +3.65% +0.37%

2013 USD +6.09% −1.77% −0.70% +1.17% +8.45% −2.36% −0.52% −0.87% +0.09% −1.43% +0.89% +3.19% +12.30%

2014 USD +7.53% +1.72% +2.79% +1.58% +2.67% +0.09% +1.65% −0.03% +2.16% +2.59% −0.13% −0.62% +24.07%

2015 USD −0.47% −0.31% −4.13% +3.31% −0.30% +3.27% +1.12% −1.41% −1.40% +2.16% −3.39% +2.99% +1.10%

2016 USD −3.49% −0.75% +1.91% +2.32% +3.82% +1.91% +3.28% +2.61% +2.40% +0.87% +2.65% +3.78% +23.25%

2017 USD +3.23% -1.12% +0.13% +2.40% +4.67%

2014 CHF −1.23% +3.42% +1.10% +4.30% −0.76% +4.00% +0.95% +5.97% +3.44% +0.11% +2.14% +25.78%

2015 CHF −7.81% +3.35% −2.34% −0.77% +0.21% +2.41% +4.41% −1.21% −0.18% +3.01% +0.96% +0.03% +1.51%

2016 CHF −0.83% −3.31% −2.22% +2.22% +7.15% +0.20% +2.12% +3.77% +0.86% +2.67% +5.21% +3.23% +22.65%

2017 CHF +0.28% +0.41% −0.11% +1.58% +2.17%

2014 EUR +1.82% +5.82% +3.33% +0.40% +2.08% +14.10%

2015 EUR +6.22% +0.49% +0.81% −1.78% +1.91% +1.15% +2.31% −3.06% −0.71% +3.14% +1.17% −0.44% +11.46%

2016 EUR −2.55% −1.03% −3.04% +1.43% +6.18% +2.20% +1.91% +2.44% +1.02% +2.55% +4.44% +3.19% +19.96%

2017 EUR +0.46% +0.43% −0.48% +0.30% +0.71%

NAVUSD-B CHF-B EUR-B

NAV 1,823.76 1,600.01 1,536.55

Since Inception +82.38% +60.00% +53.66%

Inception Date 30/03/2012 31/01/2014 31/07/2014

AFC Asia Frontier Fund Class B – as at 30th April 2017

42AFC Asia Frontier Fund

FUND STATISTICS – AFC ASIA FRONTIER FUND (NON – US)

NAVUSD-A CHF-A EUR-A

NAV 1,780.59 1,853.21 1,618.32

Since Inception +78.06% +85.32% +61.83%

Inception Date 30/03/12 30/03/12 31/01/14

AFC Asia Frontier Fund (non-US) Class A – as at 30th April 2017

Monthly PerformancesJan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec YTD

2012 USD +0.90% −7.56% −0.27% −0.26% +0.85% +3.64% −0.96% +0.61% +3.62% +0.14%

2013 USD +5.99% −1.75% −0.70% +1.12% +8.25% −2.33% −0.54% −0.90% +0.06% −1.45% +0.86% +3.18% +11.83%

2014 USD +7.34% +1.67% +2.72% +1.53% +2.60% +0.07% +1.59% −0.05% +2.10% +2.52% −0.15% −0.62% +23.24%

2015 USD −0.49% −0.34% −4.15% +3.28% −0.32% +3.24% +1.09% −1.43% −1.42% +2.14% −3.42% +2.96% +0.79%

2016 USD −3.51% −0.77% +1.89% +2.30% +3.80% +1.85% +3.19% +2.54% +2.33% +0.84% +2.57% +3.69% +22.51%

2017 USD +3.14% −1.11% +0.11% +2.33% +4.49%

2012 CHF −0.29% −1.18% −2.62% +1.62% −1.40% +1.92% −1.82% +0.24% +2.26% −1.39%

2013 CHF +5.65% +0.84% +0.62% −0.96% +11.36% −3.46% −2.54% −0.52% −2.64% −1.20% +0.78% +1.60% +8.97%

2014 CHF +9.64% −1.12% +3.22% +1.05% +4.19% −0.76% +3.89% +0.92% +5.82% +3.35% +0.09% +2.08% +36.98%

2015 CHF −7.83% +3.33% −2.36% −0.80% +0.19% +2.38% +4.39% −1.23% −0.21% +2.98% +0.94% +0.01% +1.20%

2016 CHF −0.85% −3.33% −2.24% +2.20% +7.13% +0.18% +2.05% +3.68% +0.83% +2.59% +5.08% +3.15% +21.90%

2017 CHF +0.26% +0.39% −0.13% +1.54% +2.06%

2014 EUR −3.62% +2.81% +0.86% +3.69% −0.33% +3.50% +1.76% +5.69% +3.24% +0.38% +2.02% +21.56%

2015 EUR +6.07% +0.46% +0.78% −1.80% +1.88% +1.11% +2.24% −3.04% −0.73% +3.11% +1.12% −0.45% +10.96%

2016 EUR −2.57% −1.06% −3.06% +1.40% +6.16% +2.15% +1.85% +2.37% +0.98% +2.47% +4.33% +3.10% +19.25%

2017 EUR +0.43% +0.40% −0.50% +0.28% +0.61%

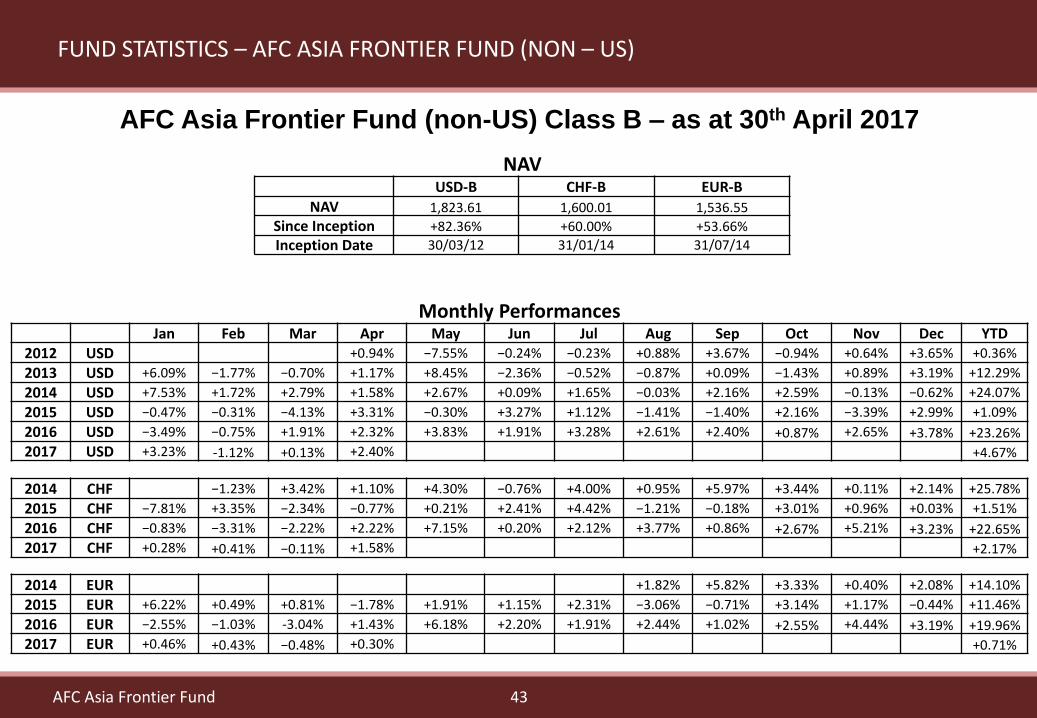

43AFC Asia Frontier Fund

NAVUSD-B CHF-B EUR-B

NAV 1,823.61 1,600.01 1,536.55

Since Inception +82.36% +60.00% +53.66%

Inception Date 30/03/12 31/01/14 31/07/14

FUND STATISTICS – AFC ASIA FRONTIER FUND (NON – US)

AFC Asia Frontier Fund (non-US) Class B – as at 30th April 2017

Monthly PerformancesJan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec YTD

2012 USD +0.94% −7.55% −0.24% −0.23% +0.88% +3.67% −0.94% +0.64% +3.65% +0.36%

2013 USD +6.09% −1.77% −0.70% +1.17% +8.45% −2.36% −0.52% −0.87% +0.09% −1.43% +0.89% +3.19% +12.29%

2014 USD +7.53% +1.72% +2.79% +1.58% +2.67% +0.09% +1.65% −0.03% +2.16% +2.59% −0.13% −0.62% +24.07%

2015 USD −0.47% −0.31% −4.13% +3.31% −0.30% +3.27% +1.12% −1.41% −1.40% +2.16% −3.39% +2.99% +1.09%

2016 USD −3.49% −0.75% +1.91% +2.32% +3.83% +1.91% +3.28% +2.61% +2.40% +0.87% +2.65% +3.78% +23.26%

2017 USD +3.23% -1.12% +0.13% +2.40% +4.67%

2014 CHF −1.23% +3.42% +1.10% +4.30% −0.76% +4.00% +0.95% +5.97% +3.44% +0.11% +2.14% +25.78%

2015 CHF −7.81% +3.35% −2.34% −0.77% +0.21% +2.41% +4.42% −1.21% −0.18% +3.01% +0.96% +0.03% +1.51%

2016 CHF −0.83% −3.31% −2.22% +2.22% +7.15% +0.20% +2.12% +3.77% +0.86% +2.67% +5.21% +3.23% +22.65%

2017 CHF +0.28% +0.41% −0.11% +1.58% +2.17%

2014 EUR +1.82% +5.82% +3.33% +0.40% +2.08% +14.10%

2015 EUR +6.22% +0.49% +0.81% −1.78% +1.91% +1.15% +2.31% −3.06% −0.71% +3.14% +1.17% −0.44% +11.46%

2016 EUR −2.55% −1.03% -3.04% +1.43% +6.18% +2.20% +1.91% +2.44% +1.02% +2.55% +4.44% +3.19% +19.96%

2017 EUR +0.46% +0.43% −0.48% +0.30% +0.71%

44AFC Asia Frontier Fund

FUND STATISTICS

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800M

ar 1

2A

pr

12

May

12

Jun

12

Jul 1

2A

ug

12

Sep

12

Oct

12

No

v 1

2D

ec 1

2Ja

n 1

3Fe

b 1

3M

ar 1

3A

pr

13

May

13

Jun

13

Jul 1

3A

ug

13

Sep

13

Oct

13

No

v 1

3D

ec 1

3Ja

n 1

4Fe

b 1

4M

ar 1

4A

pr

14

May

14

Jun

14

Jul 1

4A

ug

14

Sep

14

Oct

14

No

v 1

4D

ec 1

4Ja

n 1

5Fe

b 1

5M

ar 1

5A

pr

15

May

15

Jun

15

Jul 1

5A

ug

15

Sep

15

Oct

15

No

v 1

5D

ec 1

5Ja

n 1

6Fe

b 1

6M

ar 1

6A

pr

16

May

16

Jun

16

Jul 1

6A

ug

16

Sep

16

Oct

16

No

v 1

6D

ec 1

6Ja

n 1

7Fe

b 1

7M

ar 1

7A

pr

17

Fund Performance - USD Class A (Net)

MSCI Frontier Markets Asia Net Total Return USD Index AFC Asia Frontier Fund (after fees)

45AFC Asia Frontier Fund

FUND STATISTICS

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

2,000

2,100

2,200

2,300M

ar 1

2A

pr

12

May

12

Jun

12

Jul 1

2A

ug

12

Sep

12

Oct

12

No

v 1

2D

ec 1

2Ja

n 1

3Fe

b 1

3M

ar 1

3A

pr

13

May

13

Jun

13

Jul 1

3A

ug

13

Sep

13

Oct

13

No

v 1

3D

ec 1

3Ja

n 1

4Fe

b 1

4M

ar 1

4A

pr

14

May

14

Jun

14

Jul 1

4A

ug

14

Sep

14

Oct

14

No

v 1

4D

ec 1

4Ja

n 1

5Fe

b 1

5M

ar 1

5A

pr

15

May

15

Jun

15

Jul 1

5A

ug

15

Sep

15

Oct

15

No

v 1

5D

ec 1

5Ja

n 1

6Fe

b 1

6M

ar 1

6A

pr

16

May

16

Jun

16

Jul 1

6A

ug

16

Sep

16

Oct

16

No

v 1

6D

ec 1

6Ja

n 1

7Fe

b 1

7M

ar 1

7A

pr

17

Fund Performance – USD Class A (Gross)

MSCI Frontier Markets Asia Net Total Return USD Index AFC Asia Frontier Fund (Gross)

46AFC Asia Frontier Fund

Growth in Fund Size and Number of Clients

FUND STATISTICS

0

20

40

60

80

100

120

140

-

5,000

10,000

15,000

20,000

25,000Fe

b 1

2

Ap

r 1

2

Jun

12

Au

g 1

2

Oct

12

Dec

12

Feb

13

Ap

r 1

3

Jun

13

Au

g 1

3

Oct

13

Dec

13

Feb

14

Ap

r 1

4

Jun

14

Au

g 1

4

Oct

14

Dec

14

Feb

15

Ap

r 1

5

Jun

15

Au

g 1

5

Oct

15

Dec

15

Feb

16

Ap

r 1

6

Jun

16

Au

g 1

6

Oct

16

Dec

16

Feb

17

Ap

r 1

7

Nu

mb

er

of

Clie

nts

Fun

d S

ize

(U

S$'0

00

)

Private Clients (Right Axis) Institutional Clients (Right Axis) Fund Size (US$'000) (Left Axis)

47AFC Asia Frontier Fund

COUNTRY ALLOCATION

26.1%24.7%

17.8%

12.6%

4.0% 3.6% 2.8%1.6% 1.1% 0.3%

5.4%

0%

5%

10%

15%

20%

25%

30%

Country Allocation – 30th April 2017

48AFC Asia Frontier Fund

SECTOR ALLOCATION

18.2%

15.1% 14.5%

11.9% 11.5%10.6%

4.4%3.6%

2.1%1.4% 1.3%

5.4%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Sector Allocation – 30th April 2017

49

Investment Manager: Asia Frontier Capital Ltd., Cayman Islands

Investment Advisor: Asia Frontier Investments Ltd., Hong Kong

Fund Base Currencies: USD, EUR, CHF

Subscription Frequency: Monthly, 5 business days before end of month

Redemption: Monthly:

- 90 days prior notice for class A shares

- 180 days prior notice for class B shares

Management Fee: 1.8% p.a. of NAV for class A shares

1.5% p.a. of NAV for class B shares

Performance Fee: 10% NAV appreciation above 3 month USD-LIBOR +2% and high water mark for class A shares

8% NAV appreciation above 3 month USD-LIBOR +2% and high water mark for class B shares

Initial Minimum Investment: USD/EUR/CHF 50,000 for US Investors

USD/EUR/CHF 25,000 for non-US Investors

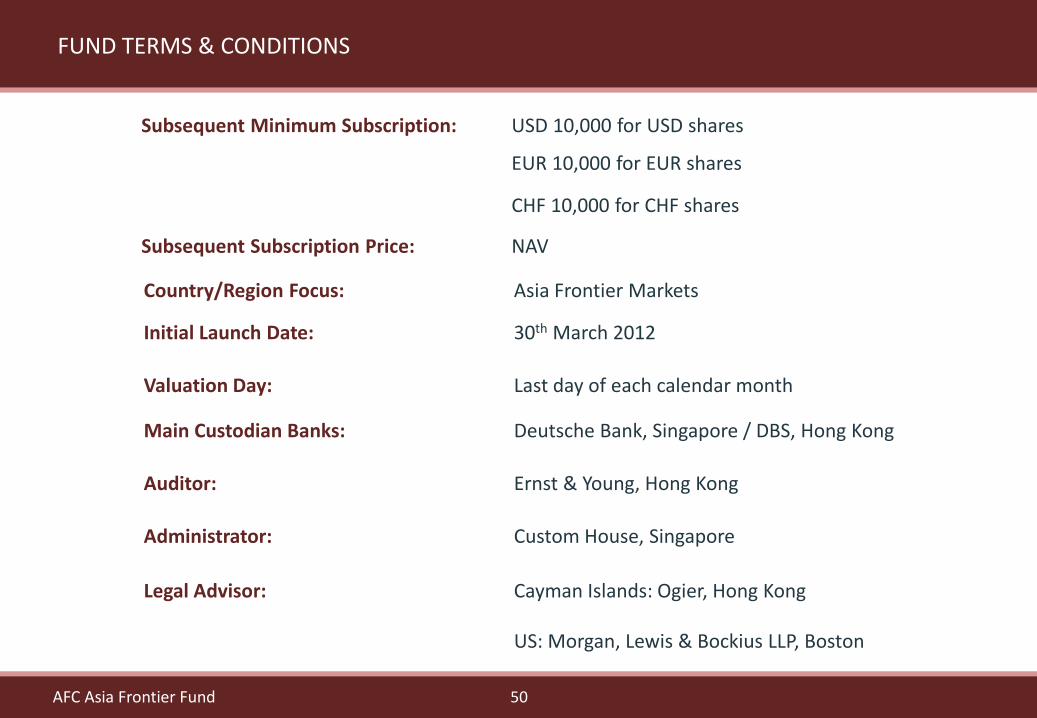

FUND TERMS & CONDITIONS

AFC Asia Frontier Fund

50

Subsequent Minimum Subscription: USD 10,000 for USD shares

EUR 10,000 for EUR shares

CHF 10,000 for CHF shares

Subsequent Subscription Price: NAV

Country/Region Focus: Asia Frontier Markets

Initial Launch Date: 30th March 2012

Valuation Day: Last day of each calendar month

Main Custodian Banks: Deutsche Bank, Singapore / DBS, Hong Kong

Auditor: Ernst & Young, Hong Kong

Administrator: Custom House, Singapore

Legal Advisor: Cayman Islands: Ogier, Hong Kong

US: Morgan, Lewis & Bockius LLP, Boston

AFC Asia Frontier Fund

FUND TERMS & CONDITIONS

51

ASIA FRONTIER CAPITAL LTD.Thomas Hugger, CEO and Fund Manager, Hong KongEmail: [email protected]: +852 3904 1015, Fax: +852 3904 1017

Peter de Vries, Marketing Director, Hong KongEmail: [email protected]: +852 3904 1079, Fax: +852 3904 1017

Website: www.asiafrontiercapital.com

Registered Office: c/o Intertrust Cayman Islands, 190 Elgin Avenue, George TownGrand Cayman KY1-9007, Cayman Islands

Hong Kong Office:Asia Frontier Investments Limited905, 9th Floor, Loon Kee Building, 267-275 Des Voeux Road Central, Hong Kong

AFC Asia Frontier Fund

CONTACT INFORMATION

Asia Frontier Investments Limited is licensed by SFC Hong Kong for Type 4 (advising on securities) and Type 9 (asset management)

*The representative of the Fund in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Sharesin Switzerland must exclusively be made to qualified investors. The place of performance and jurisdiction for Shares in the Funddistributed in Switzerland are at the registered office of the Representative.

This Presentation is presented solely for purposes of discussion to assist prospective investors in determining whether they have a preliminary interest in the investment opportunity described herein. Under no

circumstances is it to be used or considered as an offer to sell, or a solicitation of an offer to buy, any security or other interest in AFC Asia Frontier Fund, AFC Umbrella Fund or any other fund related thereto (the

“Fund”). Offers and sales of interests in the Fund will not be registered under the laws of any jurisdiction and will be made solely to qualified investors under all applicable laws. Potential investors must read the entire

Offering Memorandum delivered by the Fund and the disclosure in this Subscription Agreement. Nothing contained herein shall be deemed to be binding against, or to create any obligations or commitment on the

part of, any potential investor or the Asia Frontier Capital (the “Fund Sponsors”). The Fund Sponsors reserve the right, in their sole and absolute discretion with or without notice, to alter the terms or conditions of this

Presentation and the Fund and/or to alter or terminate the potential investment opportunity described herein. Potential investors are not to construe this Presentation as investment, legal or tax advice. Prior to

making any potential investment, potential investors should consult with their own legal, investment, accounting, regulatory, tax and other advisors to determine the consequences of the potential investment

opportunity described herein and to arrive at an independent evaluation of such potential investment opportunity.

By accepting this Presentation, the recipient agrees not to copy, distribute, discuss or otherwise disclose this Presentation or the contents hereof (including the potential investment opportunity described) or any

other related information provided by the Fund Sponsors or by its agents to any person other than employees of recipient evaluating this potential investment opportunity on recipient’s behalf without the prior written

consent of the Fund Sponsors.

While the information contained herein has been obtained from various sources which the Fund Sponsors believe, but does not guarantee, to be reliable, the Fund Sponsors do not represent that it is accurate or

complete and it should not be relied upon as such. No person has been authorized to give any information or make any representation or warranty regarding the subject matter hereof, either express or implied, and,

if given or made in this Presentation, in other materials or verbally, such information, representation or warranty cannot and should not be relied upon nor is any representation or warranty made as to the accuracy,

content, suitability or completeness of the information, analysis or conclusions or any information furnished in connection herewith contained in this Presentation and it is not to be relied upon as a substitute for

independent review of the underlying documents, available due diligence information and such other information as prospective investors may deem appropriate or prudent to review. The Fund Sponsors, their

agents, their respective affiliates, and each of their respective shareholders, members, officers, directors, managers, employees, counsel, advisors, consultants and agents (“Representatives”), expressly disclaim any

and all liability for express or implied representations or warranties that may be contained in, or for omissions from or inaccuracies in, this Presentation or any other oral or written communication transmitted or made

available to a prospective investor or its Representatives. Without limiting the generality of the foregoing, nothing contained herein is or shall be relied upon as a promise or representation as to any matter, including,

without limitation, the future performance of the potential investment opportunity described herein. None of the Fund Sponsors, their agents, or their respective Representatives is under any obligation to correct any

inaccuracies or omissions in this Presentation. Each prospective investor will have the sole responsibility for verifying the accuracy of all information furnished in this Presentation and in any other due diligence

information furnished to a prospective investor, and each prospective investor shall have the sole responsibility for determining the value of the potential investment based on assumptions said prospective investor

believes to be reasonable. There shall be no recourse against the Fund Sponsors or any of their Representatives in the event of any errors or omissions in the information furnished, the methodology used, the

calculations of values or conclusions. Without limiting the generality of the foregoing, any historical information or information based on past performance included herein is for informational purposes only, has

inherent limitations and is not intended to be a representation, warranty or guarantee of future performance. All of the information presented herein is subject to change without notice. Actual returns to potential

investors may be lower than the figures shown herein. Projected performance data shown constitutes “forward-looking information” which is based on numerous assumptions and is speculative in nature. Actual

results may vary significantly from the values and rates of return projected herein. There can no assurance that the Fund will realize its rate of return objectives or return of investors’ capital. Potential investors should

have the financial ability and willingness to accept the risks (including without limitation the risk of loss and lack of liquidity) characteristic of investments in entities such as the Fund.

AN INVESTMENT IN THE FUND WILL NOT BE APPROPRIATE FOR ALL INVESTORS. INTERESTS IN THE FUND WILL INVOLVE A HIGH DEGREE OF RISK AND ARE INTENDED FOR SALE ONLY TO

SOPHISTICATED INVESTORS WHO ARE CAPABLE OF UNDERSTANDING AND ASSUMING THE RISKS INVOLVED. INVESTORS MAY LOSE ALL OR SUBSTANTIALLY ALL OF THEIR INVESTMENT.

THE INTERESTS IN THE FUND HAVE NOT BEEN REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED (THE “SECURITIES ACT”), OR THE APPLICABLE SECURITIES LAWS OF ANY

US. STATE OR ANY NON-U.S. JURISDICTION, AND ARE BEING OFFERED AND SOLD IN RELIANCE ON EXEMPTIONS FROM THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND ANY

SUCH APPLICABLE LAWS. INTERESTS IN THE FUND HAVE NOT BEEN APPROVED OR DISAPPROVED BY THE US. SECURITIES AND EXCHANGE COMMISSION OR BY THE SECURITIES REGULATORY

AUTHORITY OF ANY STATE OR ANY OTHER RELEVANT JURISDICTION, NOR HAS ANY OTHER AUTHORITY OR COMMISSION PASSED UPON THE ACCURACY OR ADEQUACY OF THIS MEMORANDUM.

ANY REPRESENTATION TO THE CONTRARY IS UNLAWFUL.

*The representative of the Fund in Switzerland is Hugo Fund Services SA, 6 Cours de Rive, 1204 Geneva. The distribution of Shares in Switzerland must exclusively be made to qualified investors. The place of

performance and jurisdiction for Shares in the Fund distributed in Switzerland are at the registered office of the Representative.

** The Fund is registered for sale to investors in Japan, Switzerland (qualified investors), Hong Kong & UK (professional investors), Singapore (accredited investors) and USA (accredited investors and qualified

purchasers).

** By accessing information contained herein, users are deemed to be representing and warranting that they are either a Hong Kong Professional Investor or are observing the applicable laws and regulations of their

relevant jurisdictions.

52AFC Asia Frontier Fund

DISCLAIMER

Top Related