Languages

Pages

Legal

7/30/2019 About Banking Industry

http://slidepdf.com/reader/full/about-banking-industry 1/6

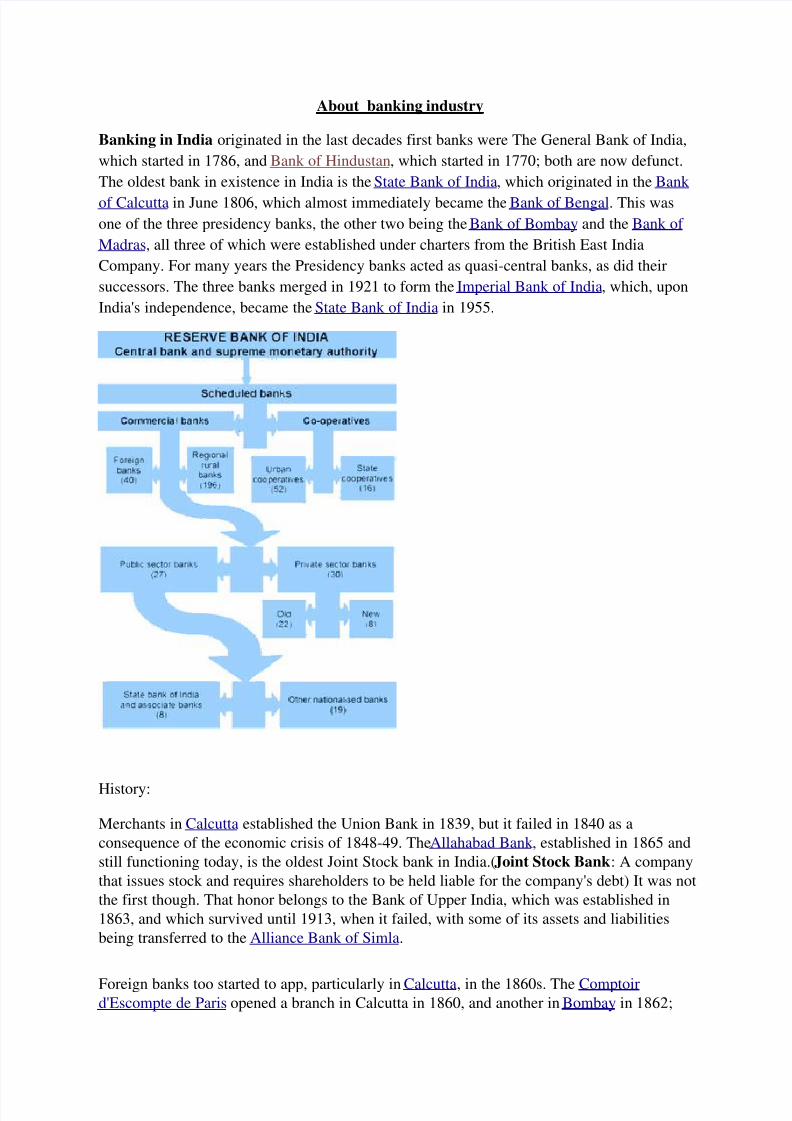

About banking industry

Banking in India originated in the last decades first banks were The General Bank of India,

which started in 1786, and Bank of Hindustan, which started in 1770; both are now defunct.

The oldest bank in existence in India is the State Bank of India, which originated in the Bank

of Calcutta in June 1806, which almost immediately became the Bank of Bengal. This was

one of the three presidency banks, the other two being the Bank of Bombay and the Bank of

Madras, all three of which were established under charters from the British East India

Company. For many years the Presidency banks acted as quasi-central banks, as did their

successors. The three banks merged in 1921 to form the Imperial Bank of India, which, upon

India's independence, became the State Bank of India in 1955.

History:

Merchants in Calcutta established the Union Bank in 1839, but it failed in 1840 as a

consequence of the economic crisis of 1848-49. TheAllahabad Bank , established in 1865 and

still functioning today, is the oldest Joint Stock bank in India.(Joint Stock Bank: A company

that issues stock and requires shareholders to be held liable for the company's debt) It was not

the first though. That honor belongs to the Bank of Upper India, which was established in

1863, and which survived until 1913, when it failed, with some of its assets and liabilities

being transferred to the Alliance Bank of Simla.

Foreign banks too started to app, particularly in Calcutta, in the 1860s. The Comptoird'Escompte de Paris opened a branch in Calcutta in 1860, and another in Bombay in 1862;

7/30/2019 About Banking Industry

http://slidepdf.com/reader/full/about-banking-industry 2/6

branches inMadras and Pondicherry, then a French colony, followed. HSBC established itself

in Bengal in 1869. Calcutta was the most active trading port in India, mainly due to the trade

of the British Empire, and so became a banking center.

The first entirely Indian joint stock bank was the Oudh Commercial Bank, established in

1881 in Faizabad. It failed in 1958. The next was the Punjab National Bank , establishedin Lahore in 1895, which has survived to the present and is now one of the largest banks in

India.

Post independence :

The partition of India in 1947 adversely impacted the economies of Punjab and West Bengal,

paralyzing banking activities for months. India's independence marked the end of a regime of

theLaissez-faire for the Indian banking. The Government of India initiated measures to play

an active role in the economic life of the nation, and the Industrial Policy Resolution adopted

by the government in 1948 envisaged a mixed economy. This resulted into greaterinvolvement of the state in different segments of the economy including banking and finance.

The major steps to regulate banking included:

The Reserve Bank of India, India's central banking authority, was established in April

1935, but was nationalized on January 1, 1949 under the terms of the Reserve Bank of

India (Transfer to Public Ownership) Act, 1948 (RBI, 2005b).[1]

In 1949, the Banking Regulation Act was enacted which empowered the Reserve Bank of

India (RBI) "to regulate, control, and inspect the banks in India".

The Banking Regulation Act also provided that no new bank or branch of an existing

bank could be opened without a license from the RBI, and no two banks could havecommon directors.

Nationalization:

Despite the provisions, control and regulations of Reserve Bank of India, banks in India

except the State Bank of India or SBI, continued to be owned and operated by private

persons. By the 1960s, the Indian banking industry had become an important tool to facilitate

the development of the Indian economy. At the same time, it had emerged as a large

employer, and a debate had ensued about the nationalization of the banking industry. Indira

Gandhi, thenPrime Minister of India, expressed the intention of the Government of India in

the annual conference of the All India Congress Meeting in a paper entitled"Stray thoughts

on Bank Nationalisation." [2] The meeting received the paper with enthusiasm.

Thereafter, her move was swift and sudden. The Government of India issued an ordinance

('Banking Companies (Acquisition and Transfer of Undertakings) Ordinance, 1969'))

and nationalised the 14 largest commercial banks with effect from the midnight of July 19,

1969. These banks contained 85 percent of bank deposits in the country.[2] Jayaprakash

Narayan, a national leader of India, described the step as a "masterstroke of political

sagacity." Within two weeks of the issue of the ordinance, the Parliament passed the Banking

Companies (Acquisition and Transfer of Undertaking) Bill, and it receivedthepresidential approval on 9 August 1969.

7/30/2019 About Banking Industry

http://slidepdf.com/reader/full/about-banking-industry 3/6

A second dose of nationalization of 6 more commercial banks followed in 1980. The stated

reason for the nationalization was to give the government more control of credit delivery.

With the second dose of nationalization, the Government of India controlled around 91% of

the banking business of India. Later on, in the year 1993, the government merged New Bank

of India with Punjab National Bank . It was the only merger between nationalized banks and

resulted in the reduction of the number of nationalised banks from 20 to 19. After this, untilthe 1990s, the nationalised banks grew at a pace of around 4%, closer to the average growth

rate of the Indian economy.

Adopting of banking technology:

The IT revolution had a great impact in the Indian banking system. The use of computers had

led to introduction of online banking in India. The use of the modern innovation and

computerisation of the banking sector of India has increased many fold after the economic

liberalisation of 1991 as the country's banking sector has been exposed to the world's market.The Indian banks were finding it difficult to compete with the international banks in terms of

the customer service without the use of the information technology and computers.

The RBI in 1984 formed Committee on Mechanisation in the Banking Industry

(1984)[6] whose chairman was Dr C Rangarajan, Deputy Governor, Reserve Bank of India.

The major recommendations of this committee was introducing MICR[7] Technology in all

the banks in the metropolis in India.This provided use of standardized cheque forms and

encoders.

In 1988, the RBI set up Committee on Computerisation in Banks (1988)[8] headed by Dr.

C.R. Rangarajan which emphasized that settlement operation must be computerized in the

clearing houses of RBI in Bhubaneshwar, Guwahati, Jaipur, Patna andThiruvananthapuram.It further stated that there should be National Clearing of inter-city

cheques at Kolkata,Mumbai,Delhi,Chennai and MICR should be made Operational.It also

focused on computerisation of branches and increasing connectivity among branches through

computers.It also suggested modalities for implementing on-line banking.The committee

submitted its reports in 1989 and computerisation began form 1993 with the settlement

between IBA and bank employees' association.[9]

In 1994, Committee on Technology Issues relating to Payments System, Cheque Clearing and

Securities Settlement in the Banking Industry (1994)[10]was set up with chairman Shri WS

Saraf, Executive Director, Reserve Bank of India. It emphasized on Electronic Funds

Transfer (EFT) system, with the BANKNET communications network as its carrier. It alsosaid that MICR clearing should be set up in all branches of all banks with more than 100

branches.

Committee for proposing Legislation On Electronic Funds Transfer and other Electronic

Payments (1995)[11] emphasized on EFT system. Electronic banking refers to DOING

BANKING by using technologies like computers, internet and networking,MICR,EFT so as

to increase efficiency, quick service,productivity and transparency in the transaction.

Apart from the above mentioned innovations the banks have been selling the third party

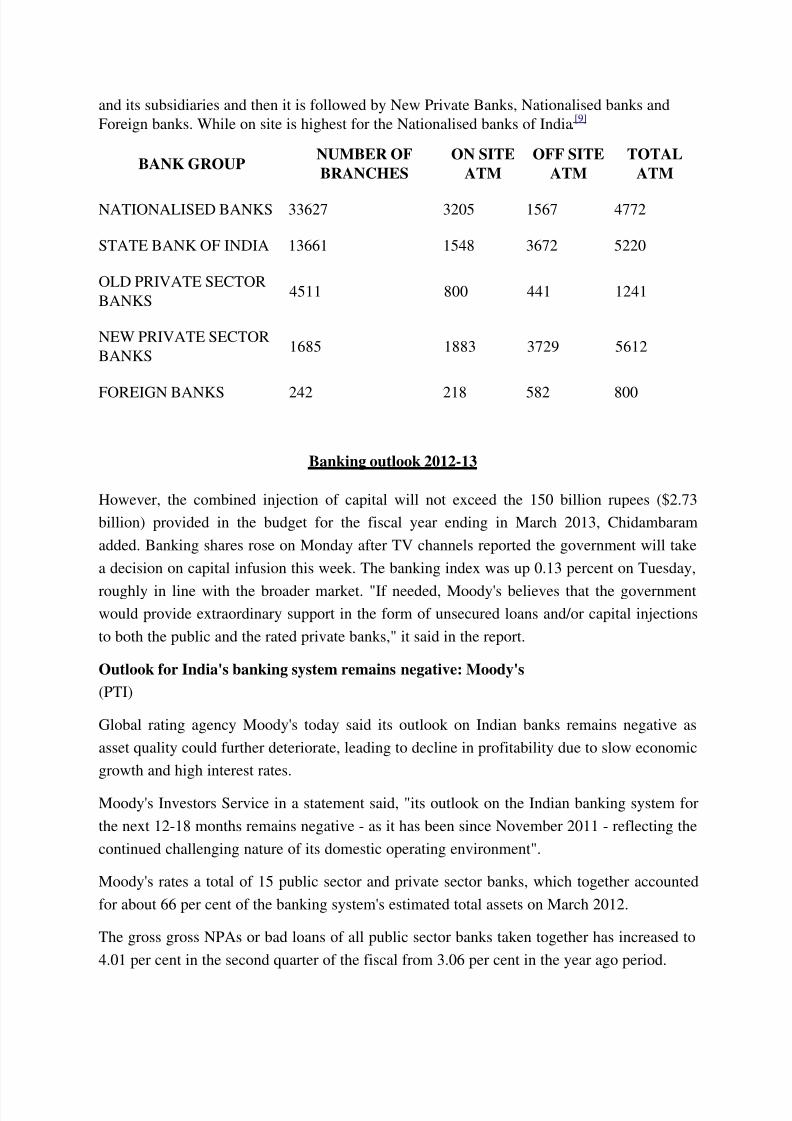

products like Mutual Funds, insurances to its clients.Total numbers of ATMs installed in

India by various banks as on end March 2005 is 17,642.[12] The New Private Sector Banks in

India is having the largest numbers of ATMs which is fol off site ATM is highest for the SBI

7/30/2019 About Banking Industry

http://slidepdf.com/reader/full/about-banking-industry 4/6

and its subsidiaries and then it is followed by New Private Banks, Nationalised banks and

Foreign banks. While on site is highest for the Nationalised banks of India.[9]

BANK GROUPNUMBER OF

BRANCHES

ON SITE

ATM

OFF SITE

ATM

TOTAL

ATM

NATIONALISED BANKS 33627 3205 1567 4772

STATE BANK OF INDIA 13661 1548 3672 5220

OLD PRIVATE SECTOR

BANKS4511 800 441 1241

NEW PRIVATE SECTOR

BANKS1685 1883 3729 5612

FOREIGN BANKS 242 218 582 800

Banking outlook 2012-13

However, the combined injection of capital will not exceed the 150 billion rupees ($2.73

billion) provided in the budget for the fiscal year ending in March 2013, Chidambaram

added. Banking shares rose on Monday after TV channels reported the government will take

a decision on capital infusion this week. The banking index was up 0.13 percent on Tuesday,

roughly in line with the broader market. "If needed, Moody's believes that the governmentwould provide extraordinary support in the form of unsecured loans and/or capital injections

to both the public and the rated private banks," it said in the report.

Outlook for India's banking system remains negative: Moody's

(PTI)

Global rating agency Moody's today said its outlook on Indian banks remains negative as

asset quality could further deteriorate, leading to decline in profitability due to slow economic

growth and high interest rates.

Moody's Investors Service in a statement said, "its outlook on the Indian banking system for

the next 12-18 months remains negative - as it has been since November 2011 - reflecting the

continued challenging nature of its domestic operating environment".

Moody's rates a total of 15 public sector and private sector banks, which together accounted

for about 66 per cent of the banking system's estimated total assets on March 2012.

The gross gross NPAs or bad loans of all public sector banks taken together has increased to

4.01 per cent in the second quarter of the fiscal from 3.06 per cent in the year ago period.

7/30/2019 About Banking Industry

http://slidepdf.com/reader/full/about-banking-industry 5/6

As per the agency, banks' average standalone credit strength is D+, or ba1 on the long-term

rating scale, whereas their average foreign currency long-term deposit rating is Baa3, which

is investment grade.

Major challenges

The banking industry in India is undergoing a major transformation due to changes in

economic condition and continuous deregulation. These multiple changes happening one

after other has a ripple effect on a bank trying to graduate from completely regulated sellers

market to completed deregulated customers market.

Deregulation:

This continuous deregulation has made the banking market extremely competitive

with greater autonomy, operational flexibility, and decontrolled interest rate and liberalized

norms for foreign exchange. The deregulation of the industry coupled with decontrol in

interest rates has led to entry of a number of players in the banking industry. At the same

time reduced corporate credit off thanks to sluggish economy has resulted in large number

of competitors battling for the same pie.

New rules:

As a result, the market place has been redefined with new rules of the game. Banks

are transforming to universal banking, adding new channels with lucrative pricing and

freebees to offer. Natural fall out of this new players, new channels squeezed spreads,

demanding customers better service, marketing skills heightened competition, new rules of

the game pressure on efficiency missed opportunities. Need for new orientation diffused

customer loyalty. Bank has led to a series of innovative product offerings catering to various

customer segments, specifically retail credit.

Efficiency:

This in turn has made it necessary to look for efficiencies in the business. Bank need

to access low cost funds and simultaneously improve the efficiency. The banks are facing

pricing pressure, squeeze on spread and have to give thrust on retail assets.

Diffused customer loyalty:

This will definitely impact customer preferences, as they are bound to react to the

value added offerings. Customers have become demanding and the loyalties are diffused.

These are multiple choices; the wallet share is reduced per bank with demand on flexibility

and customization. Given the relatively low switching costs; customer retention calls forcustomized service and hassle free, flawless service delivery.

7/30/2019 About Banking Industry

http://slidepdf.com/reader/full/about-banking-industry 6/6

Misaligned mindset:

These changes are creating challenges, as employees are made to adapt to changing

conditions. There is resistance to change from employees and the seller market mindset is

yet to be changed coupled with fear of uncertainty and control orientation. Acceptance of

technology in but the utilization is not maximized.

Competency gap:

Placing the right skill at the right place will determine success. The competency gap

needs to be addressed simultaneously otherwise there will be missed opportunities. The

focus of people will be doing work but not providing solutions, on escalating problems

rather than solving them and on disposing customers instead of using the opportunity to

cross sell.

STRATEGIC OPTIONS WITH BANKS TO COPE WITH THE CHALLENGES:

Leading players in the industry have embarked on a series of strategic and tactical

initiatives to sustain leadership. The major initiatives include:

a) Investing in state of the start of the art technology as the back bone of to ensure

reliable service delivery.

b) Leveraging the branch network and sales structure to mobilize low cost current and

savings deposits.

c) Making aggressive forays in the retail advances segments of home and personal loans.

d) Implementing organization wide initiatives involving people, process and technology to

reduce the fixed costs and the cost per transaction.

e) Focusing on fee based income to compensate foe squeezed spread.

f) Innovating products to capture customer ‘mind share’ to begin with and later the

wallet share.

g) Improving the asset quality as Basel II norms.