Languages

Pages

Legal

日本の再生可能エネルギー特別措置法とプロジェクトファイナンス省令・告示とパブリックコメントに対する「考え方」及び各電力会社の「電力購入契約要綱」の発表を受けて、売電契約の内容とプロジェクト関連契約の注意点を検討する。

再生可能エネルギーセミナー「アジア・大洋州の主要地域における 新動向と課題」

国際協力銀行9階講堂(東京)2012年9月5日

弁護士 江口 直明東京事務所

22

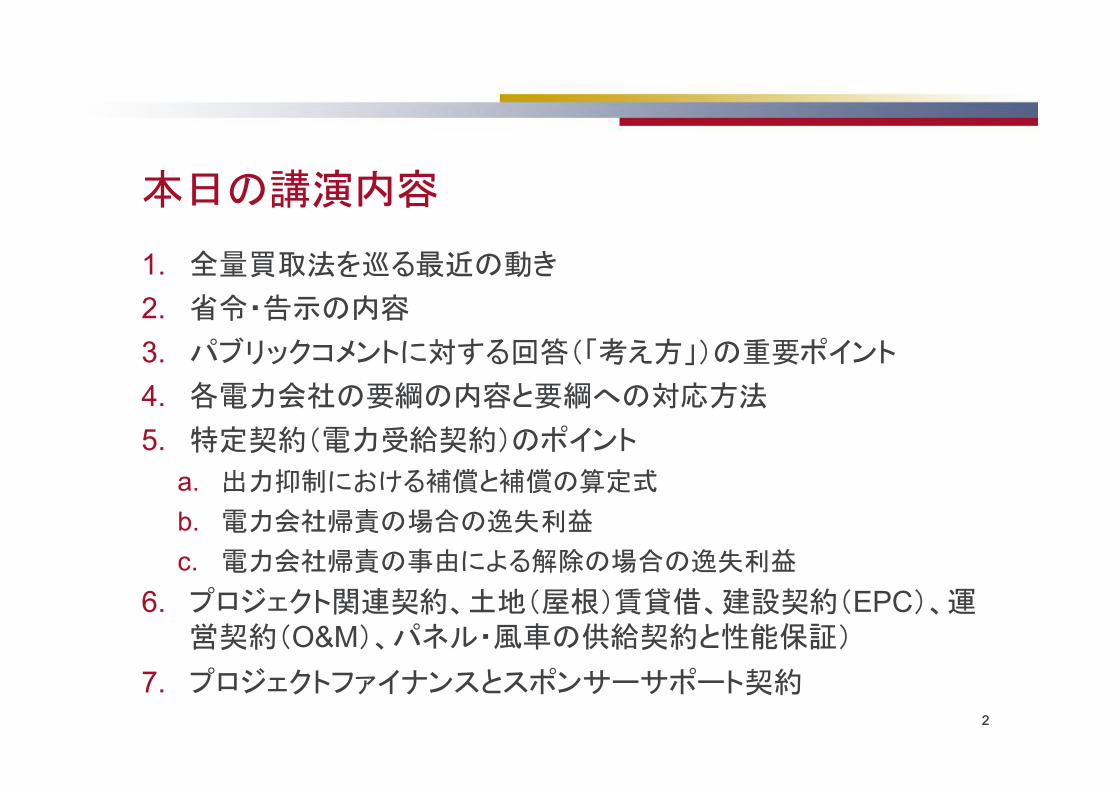

本日の講演内容

1. 全量買取法を巡る 近の動き

2. 省令・告示の内容

3. パブリックコメントに対する回答(「考え方」)の重要ポイント

4. 各電力会社の要綱の内容と要綱への対応方法

5. 特定契約(電力受給契約)のポイント

a. 出力抑制における補償と補償の算定式

b. 電力会社帰責の場合の逸失利益

c. 電力会社帰責の事由による解除の場合の逸失利益

6. プロジェクト関連契約、土地(屋根)賃貸借、建設契約(EPC)、運営契約(O&M)、パネル・風車の供給契約と性能保証)

7. プロジェクトファイナンスとスポンサーサポート契約

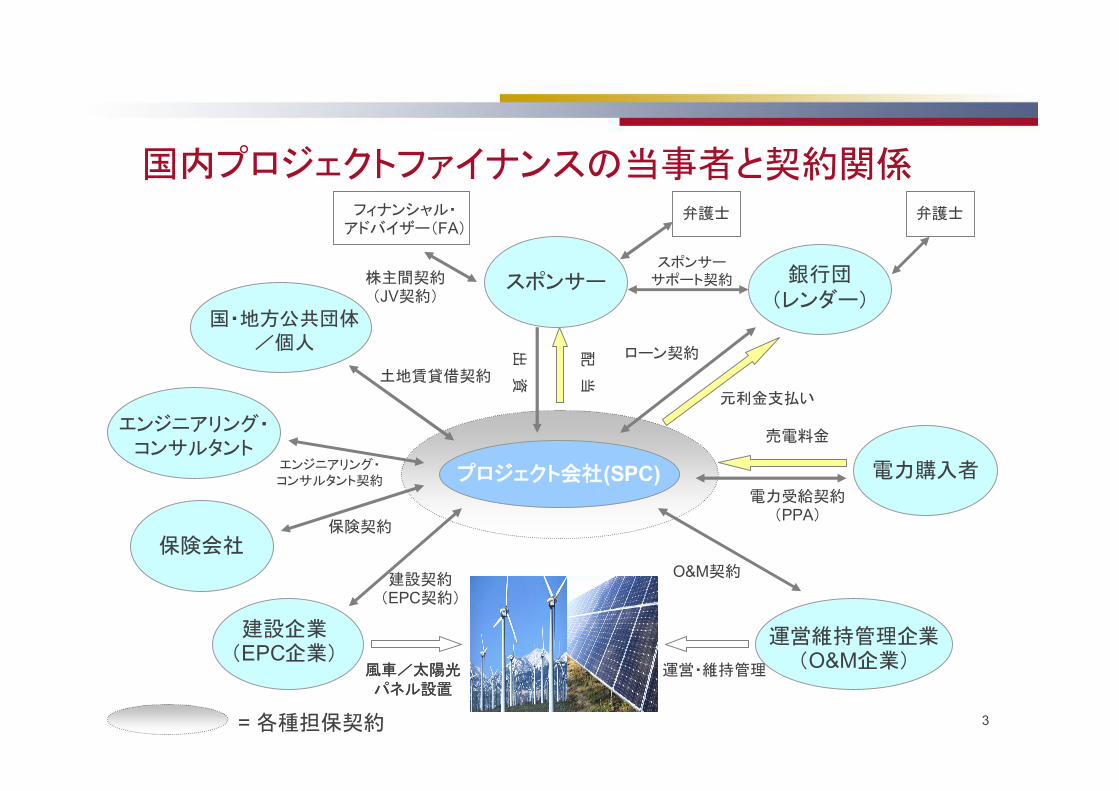

3

国・地方公共団体/個人

エンジニアリング・コンサルタント

保険会社

建設企業(EPC企業)

スポンサー

プロジェクト会社(SPC)

銀行団(レンダー)

電力購入者

運営維持管理企業(O&M企業)

= 各種担保契約

フィナンシャル・アドバイザー(FA)

弁護士

株主間契約(JV契約)

スポンサーサポート契約

土地賃貸借契約

出資

配当

元利金支払い

売電料金

電力受給契約(PPA)

O&M契約

エンジニアリング・コンサルタント契約

保険契約

建設契約(EPC契約)

風車/太陽光パネル設置

ローン契約

弁護士

風車/太陽光パネル設置

運営・維持管理

国内プロジェクトファイナンスの当事者と契約関係

4

全量買取法を巡る近の動き

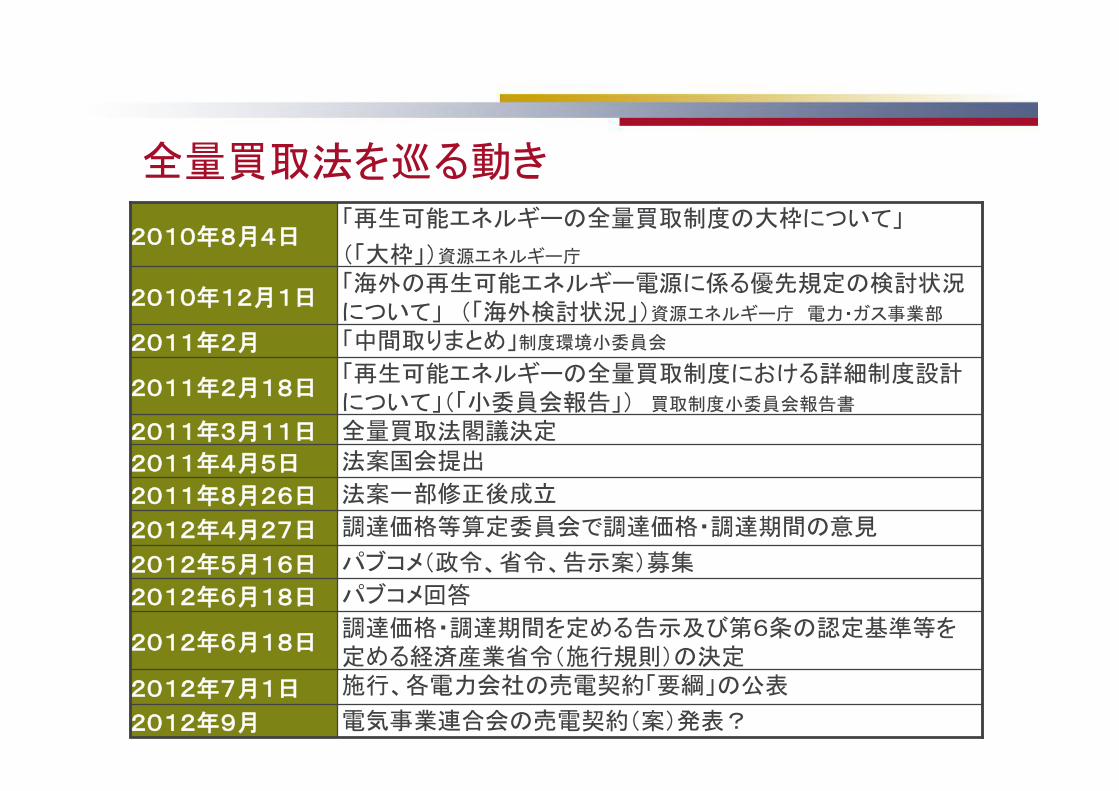

全量買取法を巡る動き

省令・告示の内容省令・告示の内容

電気事業連合会の売電契約(案)発表?2012年9月

施行、各電力会社の売電契約「要綱」の公表2012年7月1日

調達価格・調達期間を定める告示及び第6条の認定基準等を定める経済産業省令(施行規則)の決定

2012年6月18日

パブコメ回答2012年6月18日

パブコメ(政令、省令、告示案)募集2012年5月16日

調達価格等算定委員会で調達価格・調達期間の意見2012年4月27日

法案一部修正後成立2011年8月26日

法案国会提出2011年4月5日

全量買取法閣議決定2011年3月11日

「再生可能エネルギーの全量買取制度における詳細制度設計について」(「小委員会報告」) 買取制度小委員会報告書

2011年2月18日

「中間取りまとめ」制度環境小委員会2011年2月

「海外の再生可能エネルギー電源に係る優先規定の検討状況について」 (「海外検討状況」)資源エネルギー庁 電力・ガス事業部

2010年12月1日

「再生可能エネルギーの全量買取制度の大枠について」

(「大枠」)資源エネルギー庁2010年8月4日

6

省令・告示の内容

7

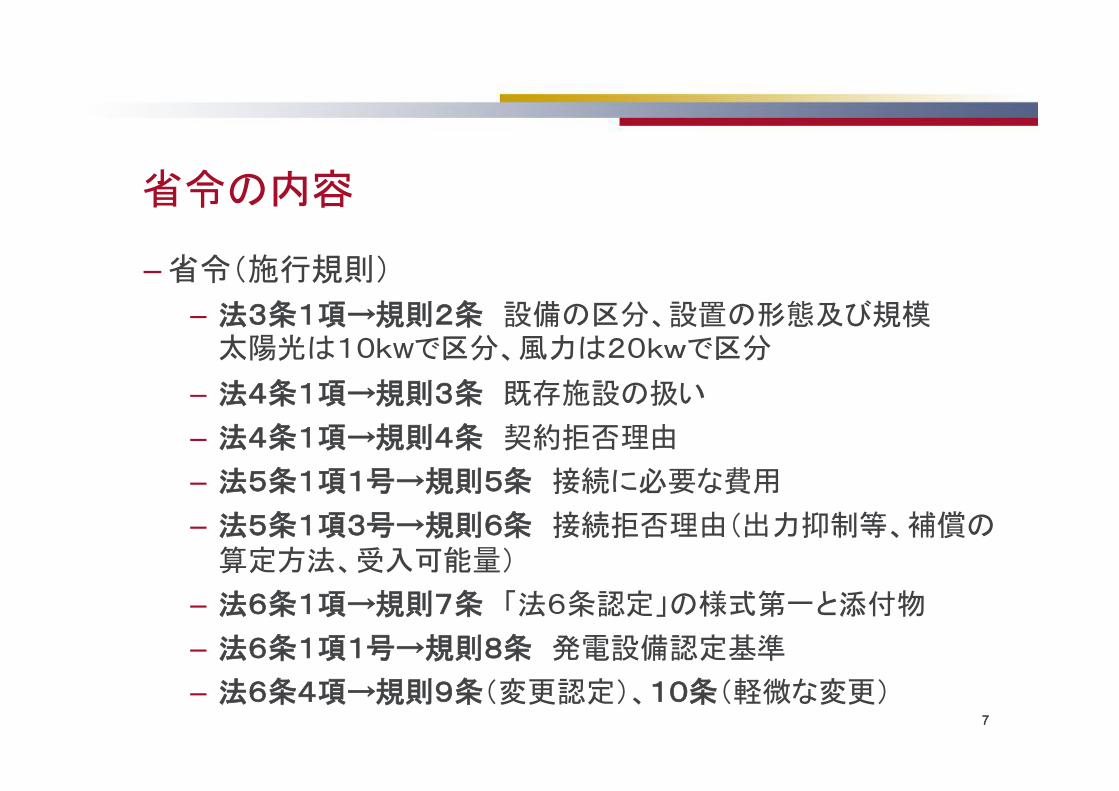

省令の内容

–省令(施行規則)

– 法3条1項→規則2条 設備の区分、設置の形態及び規模太陽光は10kwで区分、風力は20kwで区分

– 法4条1項→規則3条 既存施設の扱い

– 法4条1項→規則4条 契約拒否理由

– 法5条1項1号→規則5条 接続に必要な費用

– 法5条1項3号→規則6条 接続拒否理由(出力抑制等、補償の算定方法、受入可能量)

– 法6条1項→規則7条 「法6条認定」の様式第一と添付物

– 法6条1項1号→規則8条 発電設備認定基準

– 法6条4項→規則9条(変更認定)、10条(軽微な変更)7

8

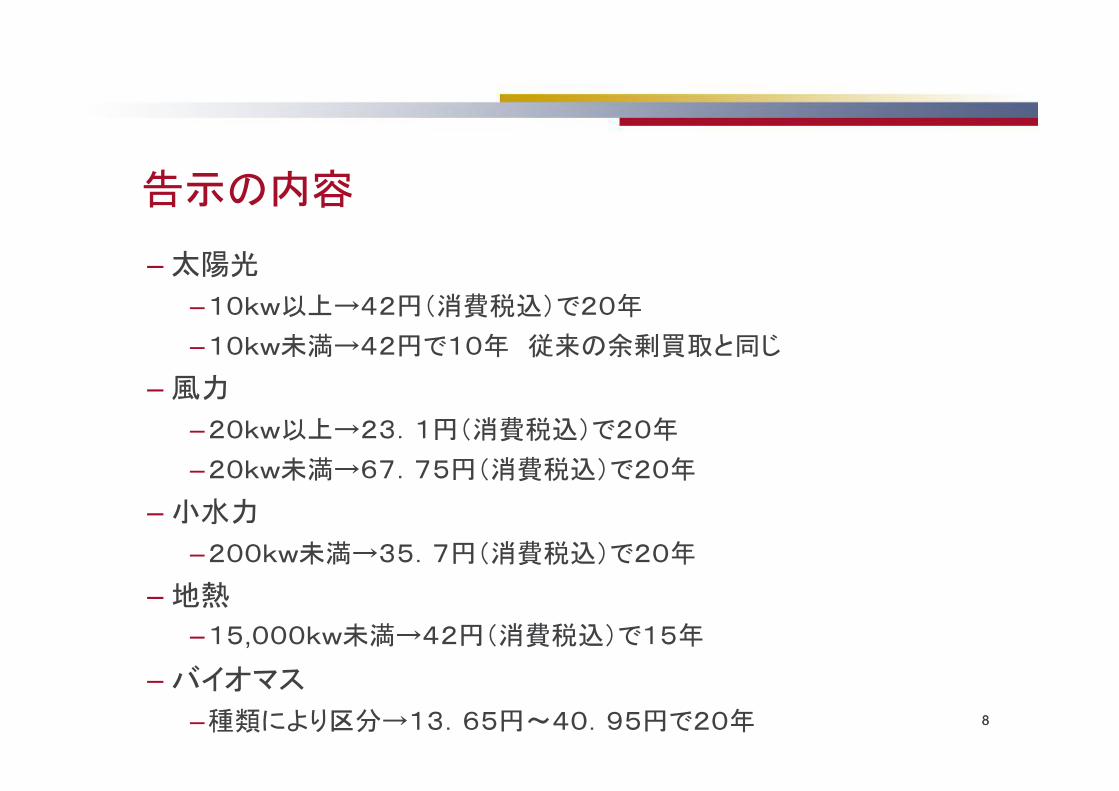

告示の内容

– 太陽光

–10kw以上→42円(消費税込)で20年

–10kw未満→42円で10年 従来の余剰買取と同じ

– 風力

–20kw以上→23.1円(消費税込)で20年

–20kw未満→67.75円(消費税込)で20年

– 小水力

–200kw未満→35.7円(消費税込)で20年

– 地熱

–15,000kw未満→42円(消費税込)で15年

– バイオマス

–種類により区分→13.65円~40.95円で20年 8

9

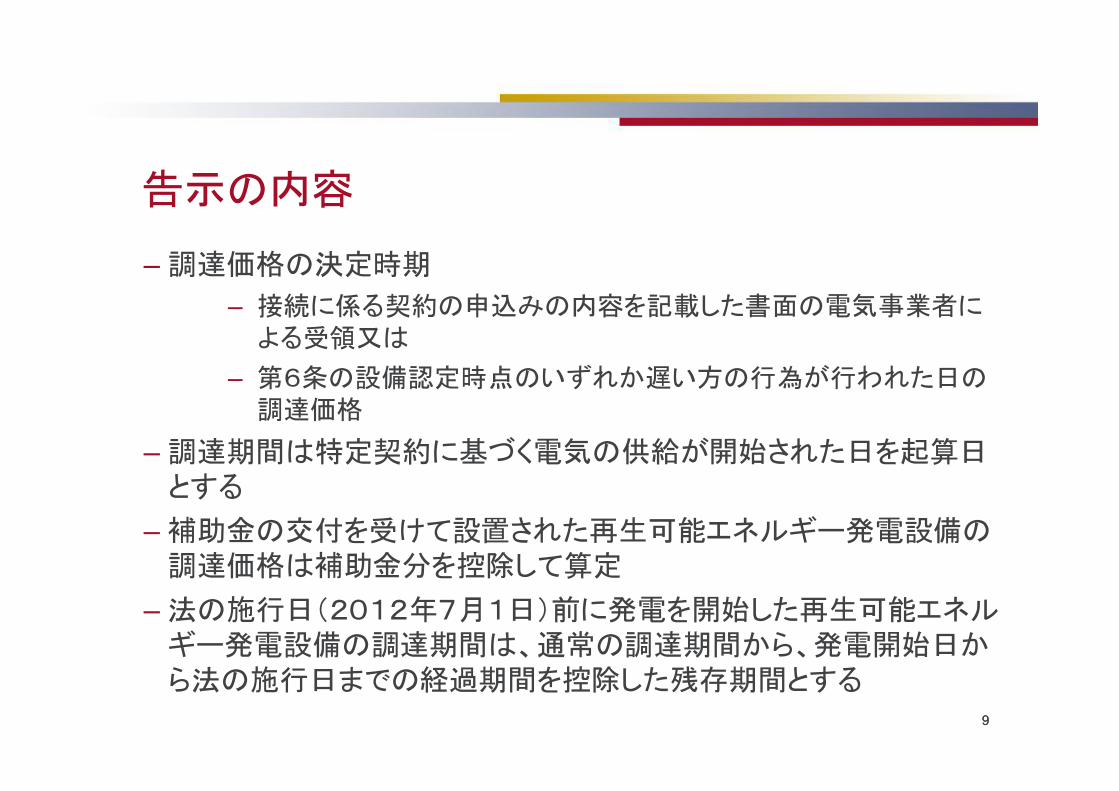

告示の内容

– 調達価格の決定時期

– 接続に係る契約の申込みの内容を記載した書面の電気事業者による受領又は

– 第6条の設備認定時点のいずれか遅い方の行為が行われた日の調達価格

– 調達期間は特定契約に基づく電気の供給が開始された日を起算日とする

– 補助金の交付を受けて設置された再生可能エネルギー発電設備の調達価格は補助金分を控除して算定

– 法の施行日(2012年7月1日)前に発電を開始した再生可能エネルギー発電設備の調達期間は、通常の調達期間から、発電開始日から法の施行日までの経過期間を控除した残存期間とする

9

10

パブリックコメントに対する回答(「考え方」)の重要ポイント

11

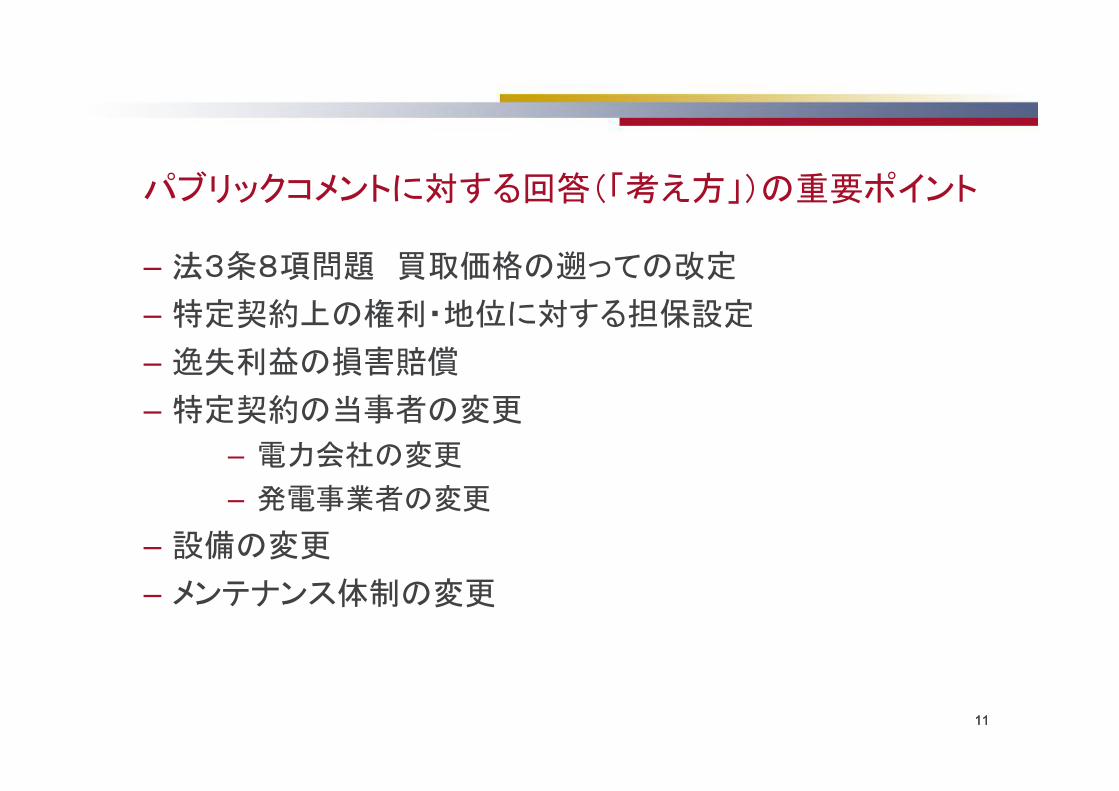

– 法3条8項問題 買取価格の遡っての改定

– 特定契約上の権利・地位に対する担保設定

– 逸失利益の損害賠償

– 特定契約の当事者の変更

– 電力会社の変更

– 発電事業者の変更

– 設備の変更

– メンテナンス体制の変更

11

パブリックコメントに対する回答(「考え方」)の重要ポイント

12

各電力会社の要綱の内容と要綱への対応方法

13

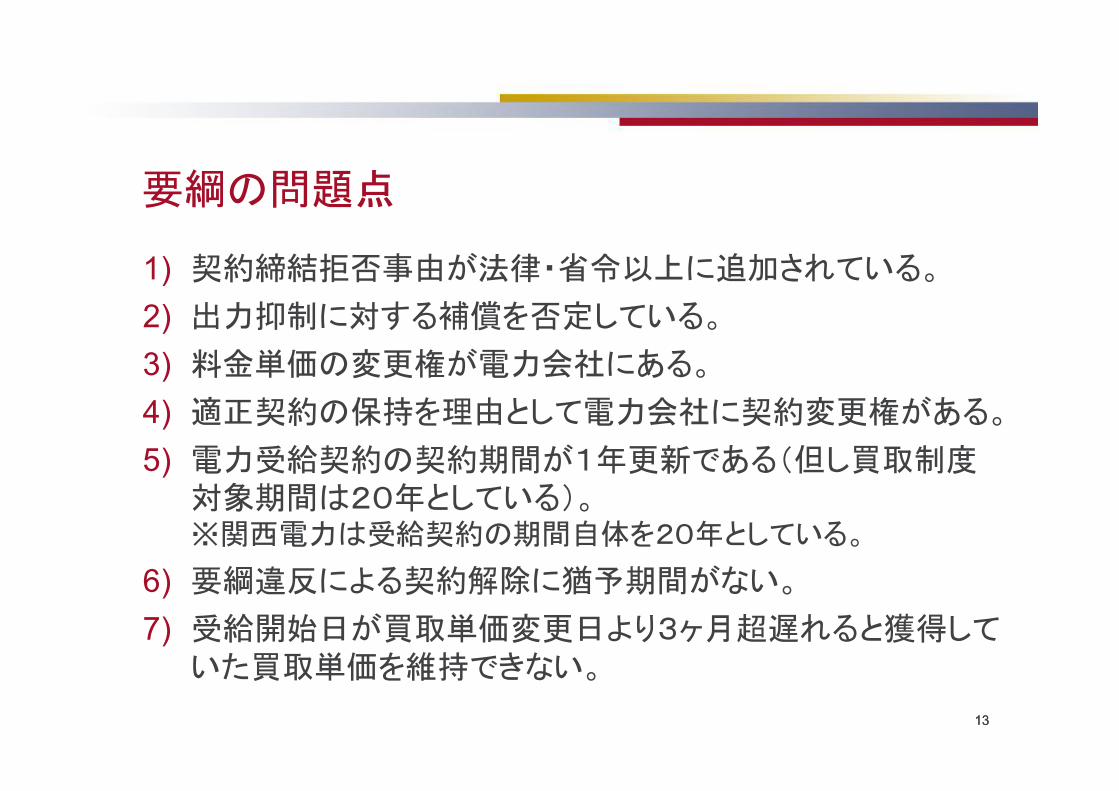

要綱の問題点

1) 契約締結拒否事由が法律・省令以上に追加されている。

2) 出力抑制に対する補償を否定している。

3) 料金単価の変更権が電力会社にある。

4) 適正契約の保持を理由として電力会社に契約変更権がある。

5) 電力受給契約の契約期間が1年更新である(但し買取制度対象期間は20年としている)。※関西電力は受給契約の期間自体を20年としている。

6) 要綱違反による契約解除に猶予期間がない。

7) 受給開始日が買取単価変更日より3ヶ月超遅れると獲得していた買取単価を維持できない。

13

14

特定契約(電力受給契約)のポイント

15

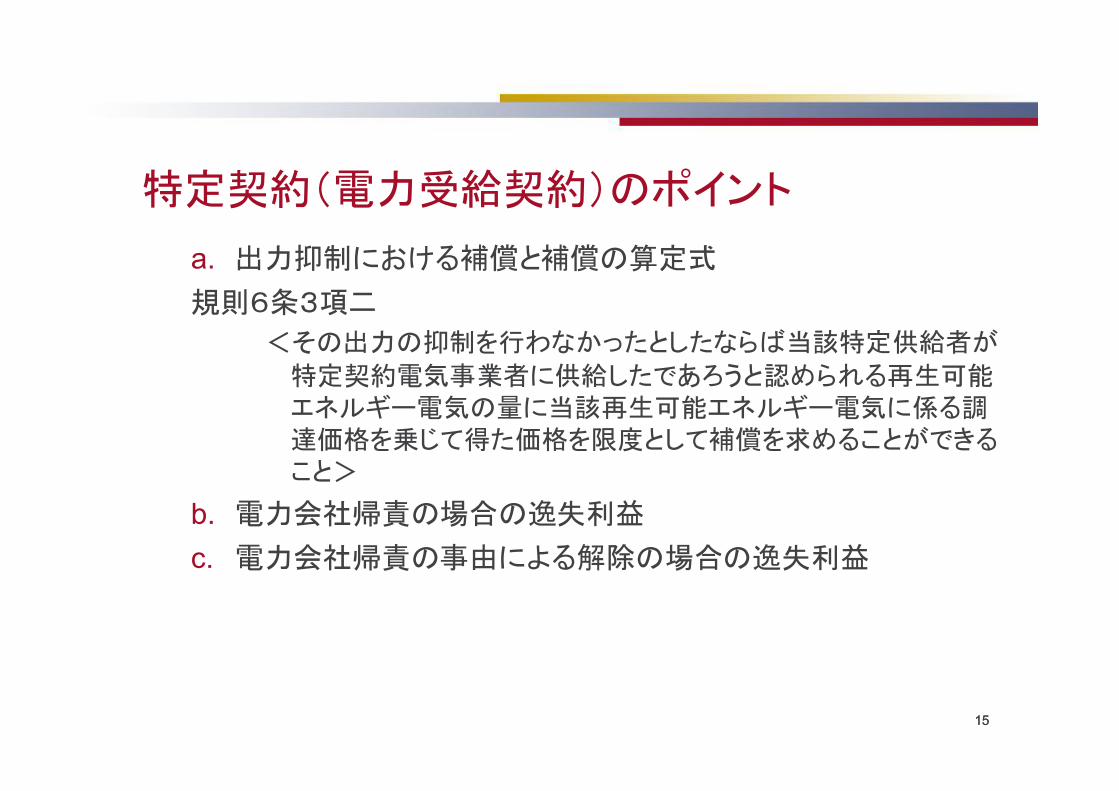

特定契約(電力受給契約)のポイント

a. 出力抑制における補償と補償の算定式

規則6条3項二

<その出力の抑制を行わなかったとしたならば当該特定供給者が

特定契約電気事業者に供給したであろうと認められる再生可能エネルギー電気の量に当該再生可能エネルギー電気に係る調達価格を乗じて得た価格を限度として補償を求めることができること>

b. 電力会社帰責の場合の逸失利益

c. 電力会社帰責の事由による解除の場合の逸失利益

15

16

プロジェクト関連契約

17

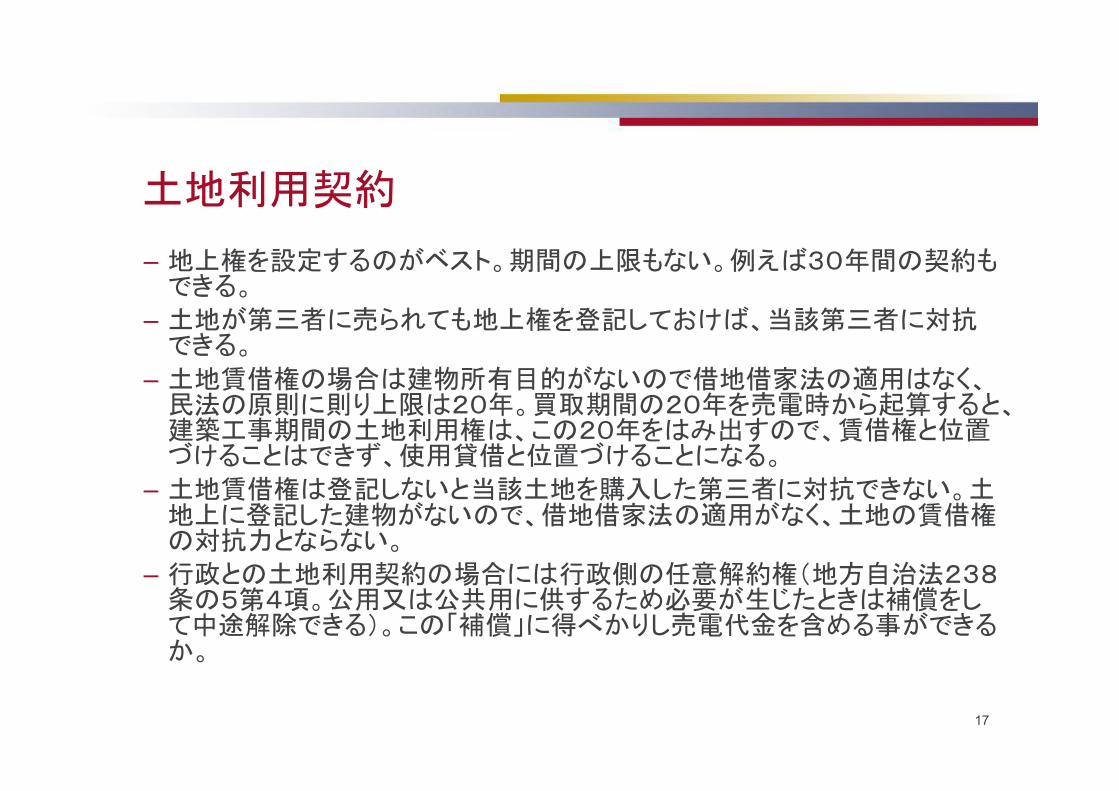

土地利用契約

– 地上権を設定するのがベスト。期間の上限もない。例えば30年間の契約もできる。

– 土地が第三者に売られても地上権を登記しておけば、当該第三者に対抗できる。

– 土地賃借権の場合は建物所有目的がないので借地借家法の適用はなく、民法の原則に則り上限は20年。買取期間の20年を売電時から起算すると、建築工事期間の土地利用権は、この20年をはみ出すので、賃借権と位置づけることはできず、使用貸借と位置づけることになる。

– 土地賃借権は登記しないと当該土地を購入した第三者に対抗できない。土地上に登記した建物がないので、借地借家法の適用がなく、土地の賃借権の対抗力とならない。

– 行政との土地利用契約の場合には行政側の任意解約権(地方自治法238条の5第4項。公用又は公共用に供するため必要が生じたときは補償をして中途解除できる)。この「補償」に得べかりし売電代金を含める事ができるか。

18

建設契約(EPC=Engineering, Procurement and Construction Agreement)– パネル調達又は風車の調達についても責任をとる一括契約か。

– パネル調達又は風車調達契約の相手方が別の当事者の場合、パネル又は風車の不具合をもともとの製品の瑕疵として製造者に請求するか、施工方法が悪かったとしてEPCに請求するか、どちらに主張すればいいか不明

確な場合が生じる。

– 工事が遅れて、電力受給契約が解除された場合、再度電力受給契約を結び直しても、結び直した時点の低い買取価格しか適用されないので、その価格で買取期間満了まで売電事業を行った場合に得べかりし利益をEPCに請求する必要がある。通常の予定損害賠償(LD=Liquidated Damages)では不足するかもしれない。

– 瑕疵担保は2年又は、故意過失があると10年。

– 性能保証は10年まで90%出力保証、10年超は80%出力保証。

19

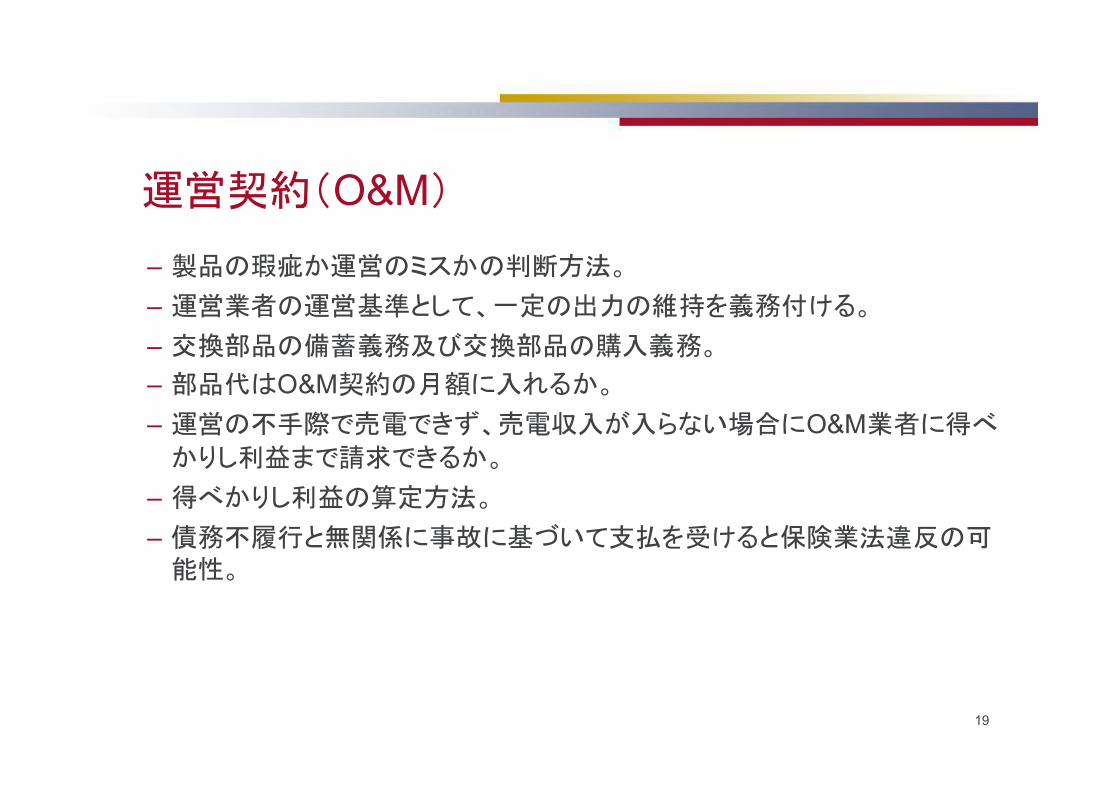

運営契約(O&M)

– 製品の瑕疵か運営のミスかの判断方法。

– 運営業者の運営基準として、一定の出力の維持を義務付ける。

– 交換部品の備蓄義務及び交換部品の購入義務。

– 部品代はO&M契約の月額に入れるか。

– 運営の不手際で売電できず、売電収入が入らない場合にO&M業者に得べ

かりし利益まで請求できるか。

– 得べかりし利益の算定方法。

– 債務不履行と無関係に事故に基づいて支払を受けると保険業法違反の可能性。

20

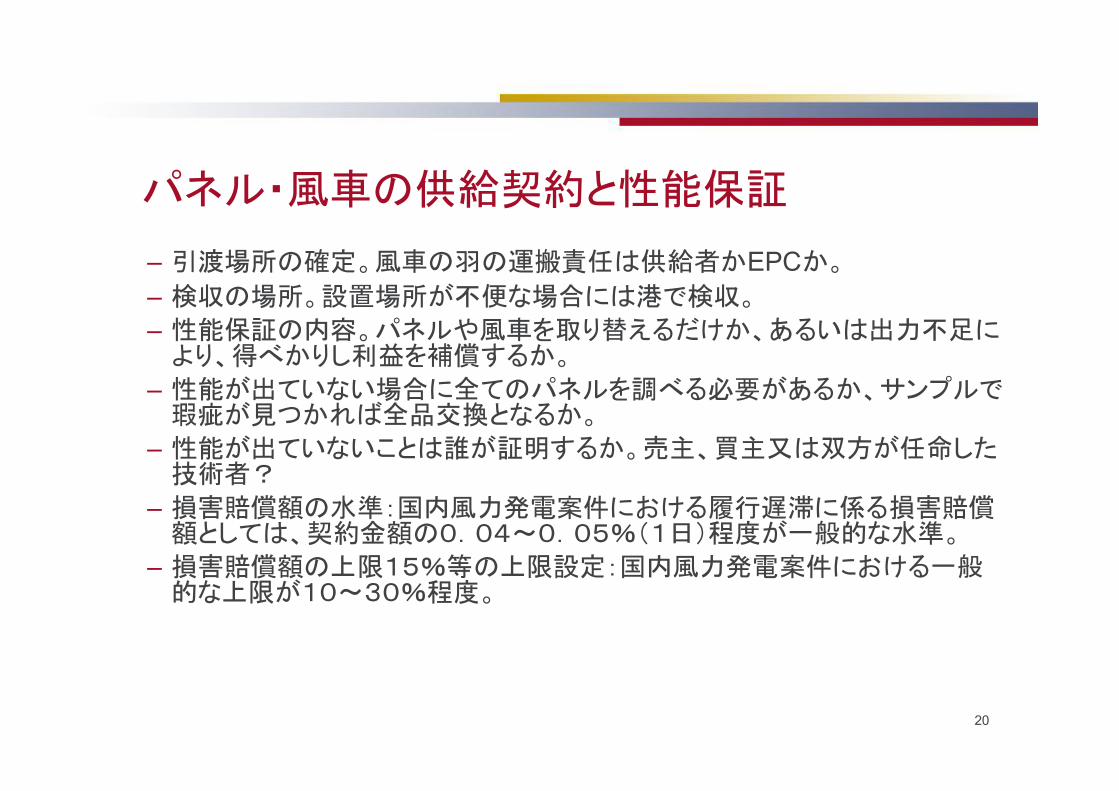

パネル・風車の供給契約と性能保証

– 引渡場所の確定。風車の羽の運搬責任は供給者かEPCか。

– 検収の場所。設置場所が不便な場合には港で検収。

– 性能保証の内容。パネルや風車を取り替えるだけか、あるいは出力不足により、得べかりし利益を補償するか。

– 性能が出ていない場合に全てのパネルを調べる必要があるか、サンプルで瑕疵が見つかれば全品交換となるか。

– 性能が出ていないことは誰が証明するか。売主、買主又は双方が任命した技術者?

– 損害賠償額の水準:国内風力発電案件における履行遅滞に係る損害賠償額としては、契約金額の0.04~0.05%(1日)程度が一般的な水準。

– 損害賠償額の上限15%等の上限設定:国内風力発電案件における一般的な上限が10~30%程度。

21

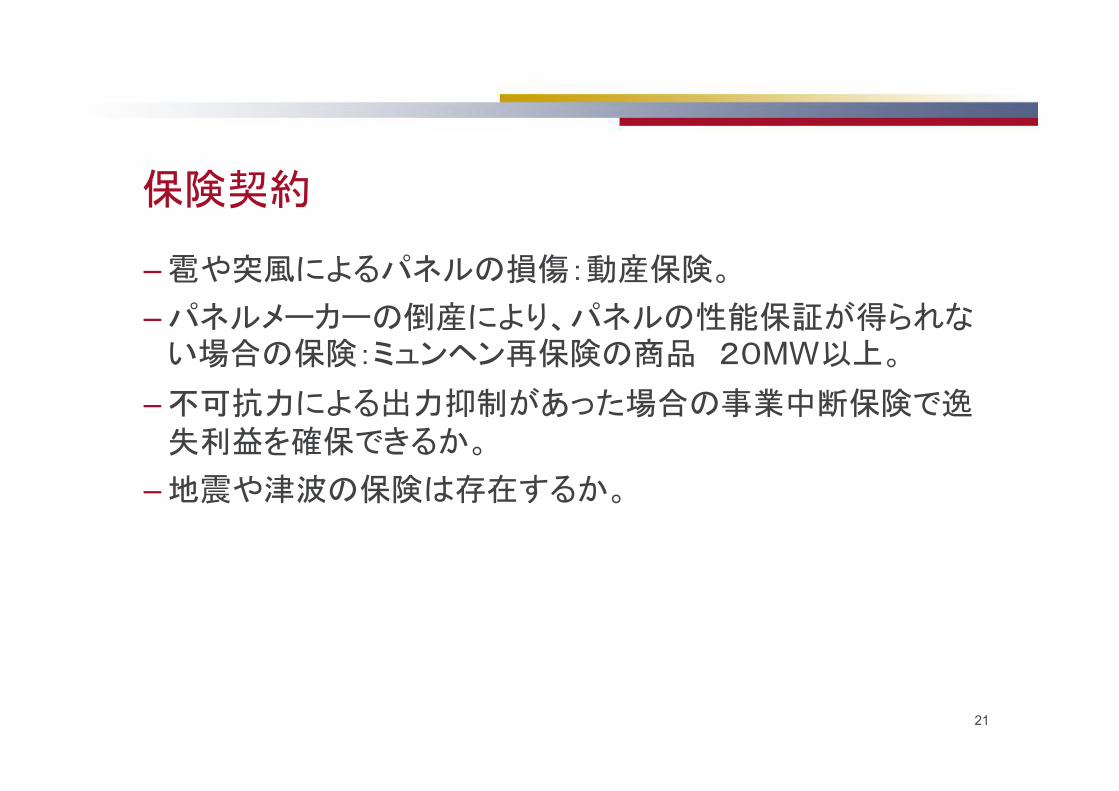

保険契約

–雹や突風によるパネルの損傷:動産保険。

–パネルメーカーの倒産により、パネルの性能保証が得られない場合の保険:ミュンヘン再保険の商品 20MW以上。

–不可抗力による出力抑制があった場合の事業中断保険で逸失利益を確保できるか。

–地震や津波の保険は存在するか。

22

屋根貸し契約

– 屋根部分だけの賃借権を登記できない不動産登記法の不備。

– 空間地上権という方法も考えられるが、登記実務なし。

– 屋根の所有者で賃貸人が建物を第三者に売却した場合、屋根貸しを受けている借主は当該第三者に対抗できず、当該第三者が太陽光パネルの撤去を求めた場合には対応せざるをえない。

– 上記のような不都合を回避するため、屋根の賃貸人を屋根貸し契約で縛り、屋根の賃貸人が第三者に建物を売却する場合には、必ず、既存の太陽光パネルの設置目的の屋根の賃貸借契約を引き継ぐように屋根の賃貸人を契約で縛る。

– 10kW未満の太陽光発電設備も束ねることにより全量買取制度の

対象となることが前提。パブコメ回答35頁122番。近接性の要件なし。

23

匿名組合ストラクチャーと税法

–グリーン投資減税の拡充:即時償却制度の創設

–10kW以上の太陽光及び1万kW以上の風力

–平成24年7月1日から平成25年3月31日までに認定発電設備を取得し、その取得の日から1年以内にその事業の用に供する場合に即時償却が認められる。合同会社に発電設備を保有させ、匿名組合出資をすることにより、即時償却のメリットを匿名組合員が享受することができる可能性が開けた

24

税務上の注意点

もっとも、匿名組合出資について常に導管性が認められるわけではない点には注意が必要である。

すなわち、組合員が「特定組合員(純粋にパッシブな投資家として組合事業に関与しない場合など)」に該当し、組合事業の 終的な損益の見込みが実質的に欠損となっていない場合において、当該組合事業に帰せられる損益が明らかに欠損とならないと見込まれるときは、組合損失の全額が当該組合の特定組合員である法人において損金不算入とされる可能性がある(租税特別措置法第67条の12第①号かっこ書、租税特別措置法施行令第39条の31第⑦号。いわゆる日本型レバレッジドリースによる節税スキーム封じのため平成17年税制改正により導入された税制)。

組合員の事業への関与度合は適切か、即時減価償却の効果がいわゆる日本型レバレッジドリースの場合の「人工的な損益の歪み」と解されないかなどといった観点から、当該メガソーラー事業がこれに該当し、税務上当初の匿名組合損失の損金性が否定されないかについて、さらに検討する必要がある。

また、これに加えて本件スキームが「過度の節税スキーム」として包括的な租税回避防止条項に基づき税務上否認されないかどうかも検討する必要がある。

25

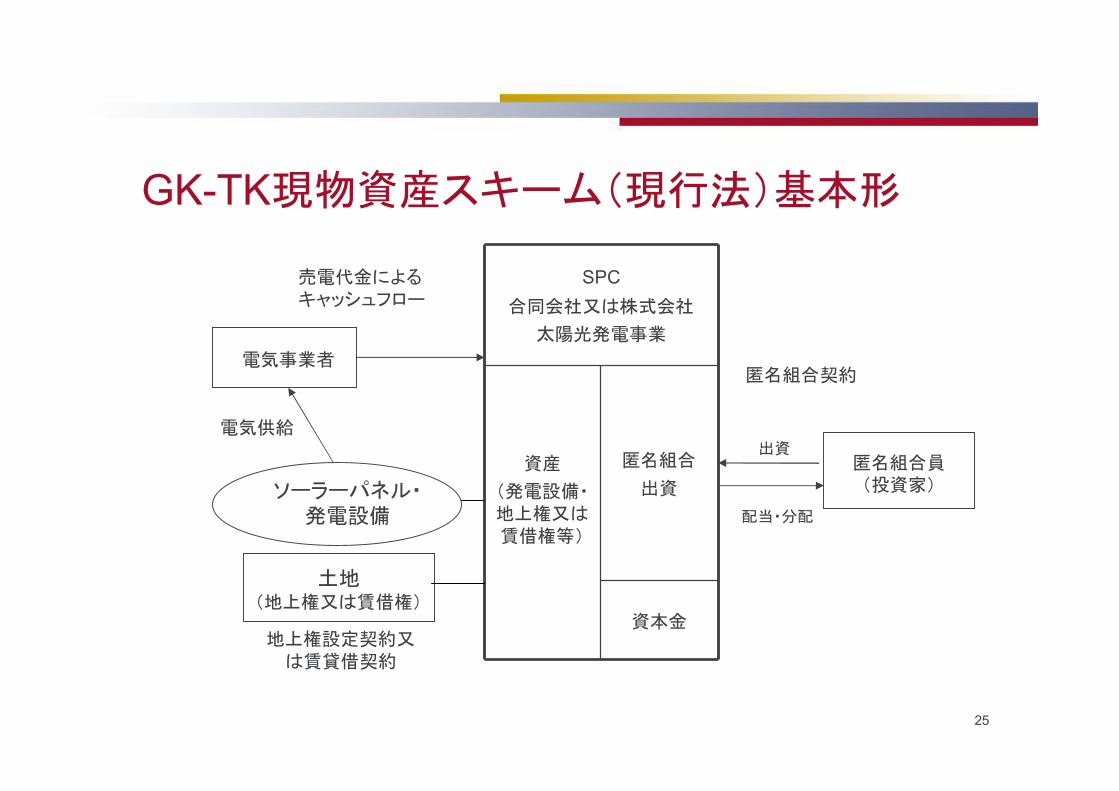

SPC合同会社又は株式会社

太陽光発電事業

資産

(発電設備・地上権又は賃借権等)

匿名組合

出資

資本金

匿名組合員(投資家)

土地(地上権又は賃借権)

ソーラーパネル・発電設備

GK-TK現物資産スキーム(現行法)基本形

匿名組合契約

配当・分配

地上権設定契約又は賃貸借契約

電気事業者

売電代金によるキャッシュフロー

出資電気供給

26

GK-TK現物資産スキーム(現行法)スキームの概要

– SPCであるX社は、本件土地について、土地の所有者と地上権設定契約又は賃貸

借契約を締結し、本件土地の地上権又は賃借権(借地権)を設定。

– X社は、投資家との間で、匿名組合契約(商法第535条)を締結。投資家から、匿名

組合出資を受ける。

– X社は、本件土地上に、太陽光発電パネル等の太陽光発電設備を新規に建設・保

有。本件発電設備の建設費用は匿名組合出資(及び借入金)で資金調達。

– 電気事業者との間で電力受給契約を締結し、当該電力受給契約に基づき本件発電設備により発電した電気を供給・売却。

– 本件発電設備は、太陽光発電パネル、パワーコンディショナー、変電設備、送電線設備その他の建物以外の設備。案件によっては、パワーコンディショナーの格納用等に付属の建物を新規に建築する場合がある。匿名組合出資は借地権の取得、地代・賃料等の費用及び建物の新築費用等に充てず、かかる費用は自己資本又は借入金により調達(匿名組合の出資金は不動産関係の費用にあてない)。

– X社は、本件発電事業により得られる収益を、匿名組合契約に基づき匿名組合員であるA社に分配。

27

不動産特定共同事業法との関係

– 問題点 不動産特定共同事業法(平成6年法律第77号)により、匿名組合契約型の契約(「不動産特定共同事業契約」)を締結し、投資家が事業者(営業者)の不動産取引のため出資を行い、当該事業者が投資家に不動産取引から生ずる収益・利益の分配を行う事業は「不動産特定共同事業」に該当。不動産特定共同事業を営む者は、主務大臣又は都道府県知事の許可が必要(法第3条第1項)。

– 「不動産取引」とは、「不動産の売買、交換又は賃貸借」をいう。

– 「不動産」とは、宅地建物取引業法の「宅地」又は「建物」をいう。本件発電設備のような太陽光パネルとその設備は、「宅地」又は「建物」のいずれにも該当しないため、同法の「不動産」にそもそも該当しない。

– 架空電線路用・保安通信設備用の柱と電気工作物である「太陽電池発電設備」は、建築基準法上、建築基準法施行令と平成23年9月30日付国土交通省告示第1002号により、建築基準法の対象となる工作物から除外。本件発電設備のような太陽光パネルとその設備は、原則として、建築基準法の適用除外。

– 本件土地と建物は同法の対象。法文上、「不動産取引」は「不動産の売買、交換又は賃貸借」をいう。土地の「地上権」の設定と、建物の新規の建築と保有は「不動産取引」の定義に該当しない。しかるに、国土交通省は、匿名組合の出資金をかかる不動産関連の費用に充てる行為は、同法の対象となり得るとの見解。

28

不動産特定共同事業法の問題点と結論

結論: 本件発電事業は不動産特定共同事業法の対象外であるとの解釈が可能。

– 本件発電設備のような太陽光パネルとその設備は、原則として、不動産特定共同事業法の「不動産」の定義である「宅地」又は「建物」のいずれにも該当しないことから、同法の対象外。

– 土地の地上権の設定、新規の建物の新築・保有は、同法の「不動産取引」の定義に該当しないが、国土交通省は、匿名組合出資をもってかかる不動産関係の費用に充てる場合は、不動産特定共同事業法の対象になり得るという見解。従って、スキーム上、投資家からの匿名組合の出資金を不動産関連の費用(本件土地の借地権の取得と付属建物の建築費用)に充てないことを想定。不動産関連の費用は、自己資本(株主資本)又は借入金により調達。

– 本件発電設備は、原則として、同法の「不動産」の定義(「宅地」又は「建物」)に該当せず、また、本件の匿名組合契約は不動産取引のために出資を行うものではないことから、 「不動産特定共同事業契約」に該当しない。

– 従って、本件発電事業は「不動産特定共同事業」の対象外であり、X社は同法の許

可を受ける必要はないと解釈することが可能。

29

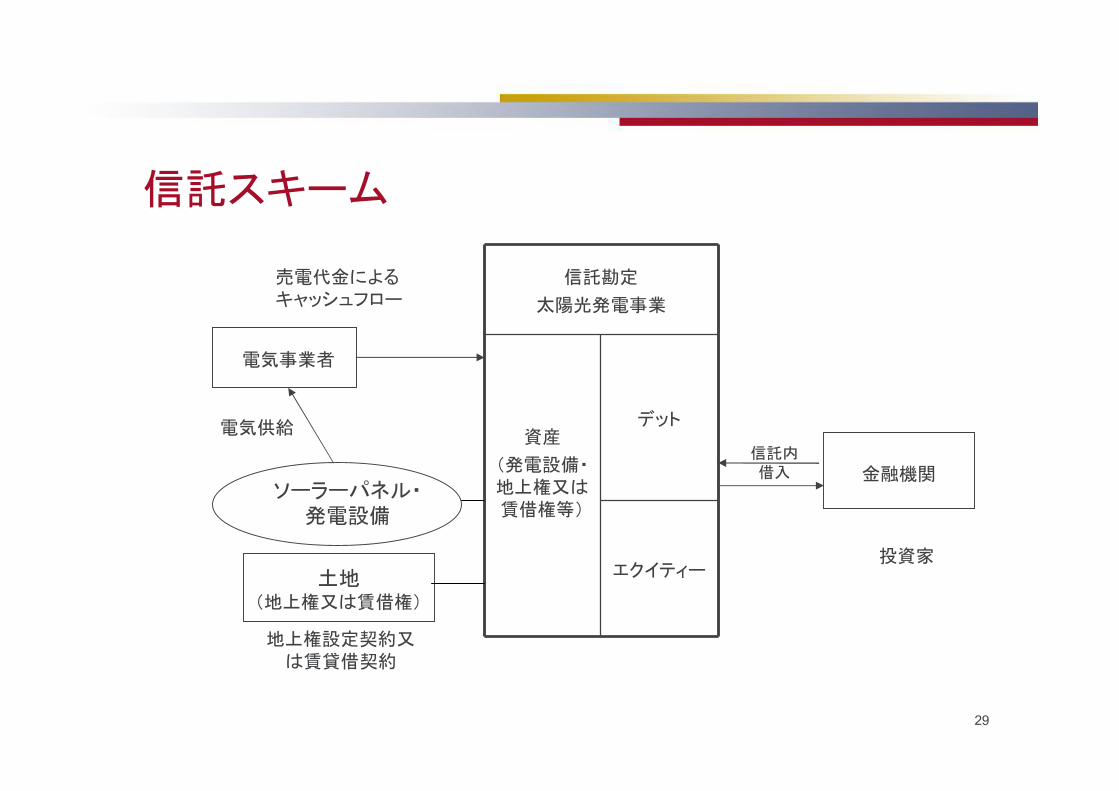

信託勘定

太陽光発電事業

資産

(発電設備・地上権又は賃借権等)

デット

エクイティー

金融機関

土地(地上権又は賃借権)

ソーラーパネル・発電設備

信託スキーム

投資家

地上権設定契約又は賃貸借契約

電気事業者

売電代金によるキャッシュフロー

信託内借入

電気供給

30

プロジェクトファイナンスとスポンサーサポート契約

31

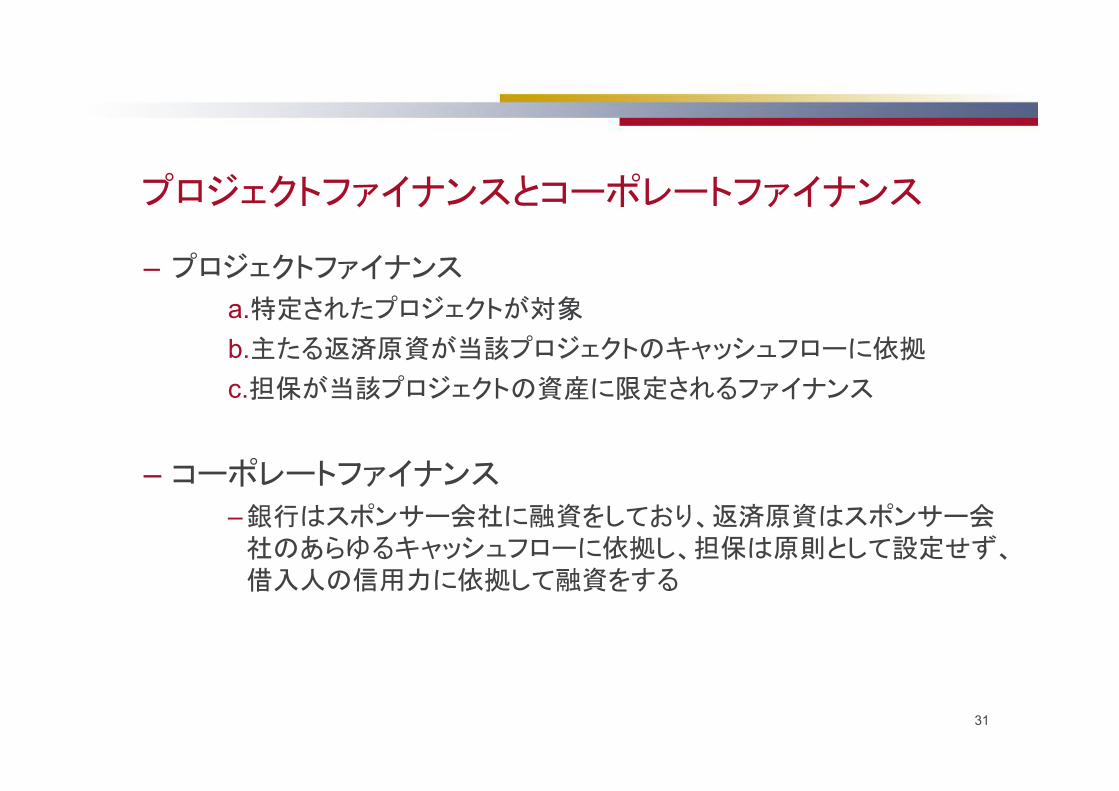

プロジェクトファイナンスとコーポレートファイナンス

– プロジェクトファイナンス

a.特定されたプロジェクトが対象

b.主たる返済原資が当該プロジェクトのキャッシュフローに依拠

c.担保が当該プロジェクトの資産に限定されるファイナンス

– コーポレートファイナンス

–銀行はスポンサー会社に融資をしており、返済原資はスポンサー会社のあらゆるキャッシュフローに依拠し、担保は原則として設定せず、借入人の信用力に依拠して融資をする

32

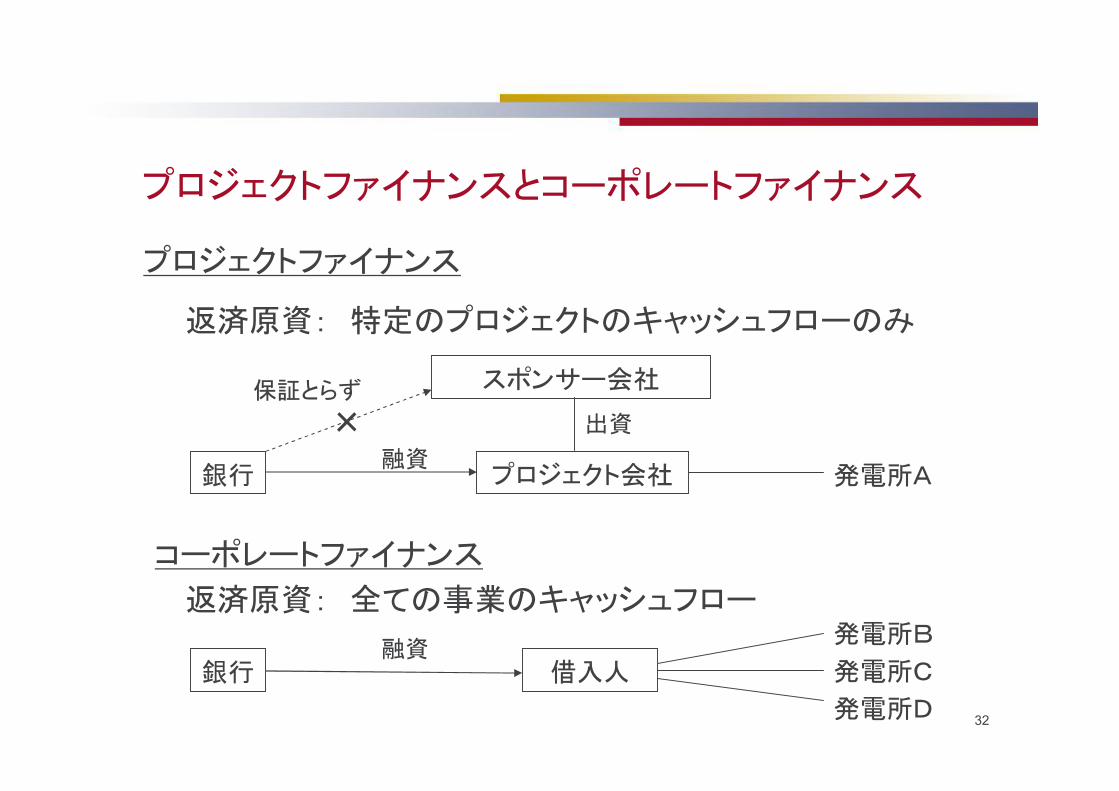

プロジェクトファイナンスとコーポレートファイナンス

プロジェクトファイナンス

返済原資: 特定のプロジェクトのキャッシュフローのみ

銀行

スポンサー会社

プロジェクト会社 発電所A

出資×保証とらず

融資

返済原資: 全ての事業のキャッシュフロー

銀行 借入人 発電所C融資

コーポレートファイナンス

発電所B

発電所D

33

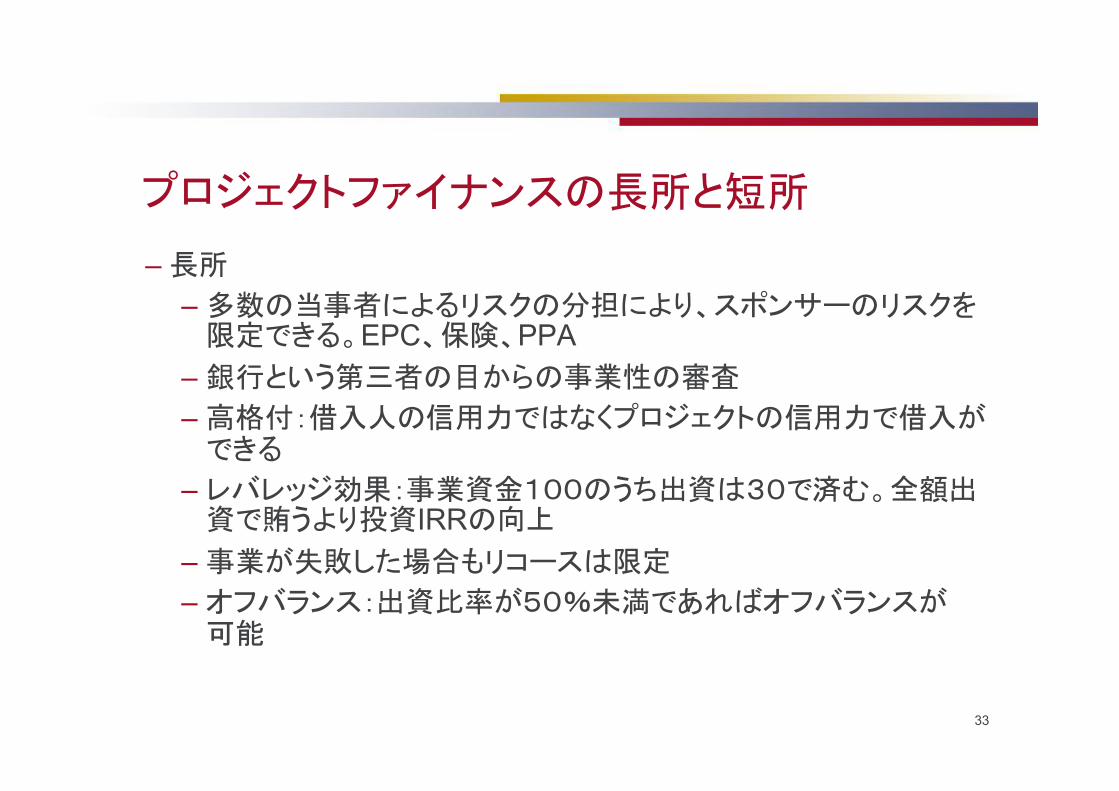

プロジェクトファイナンスの長所と短所

– 長所

– 多数の当事者によるリスクの分担により、スポンサーのリスクを限定できる。EPC、保険、PPA

– 銀行という第三者の目からの事業性の審査

– 高格付:借入人の信用力ではなくプロジェクトの信用力で借入ができる

– レバレッジ効果:事業資金100のうち出資は30で済む。全額出資で賄うより投資IRRの向上

– 事業が失敗した場合もリコースは限定

– オフバランス:出資比率が50%未満であればオフバランスが可能

34

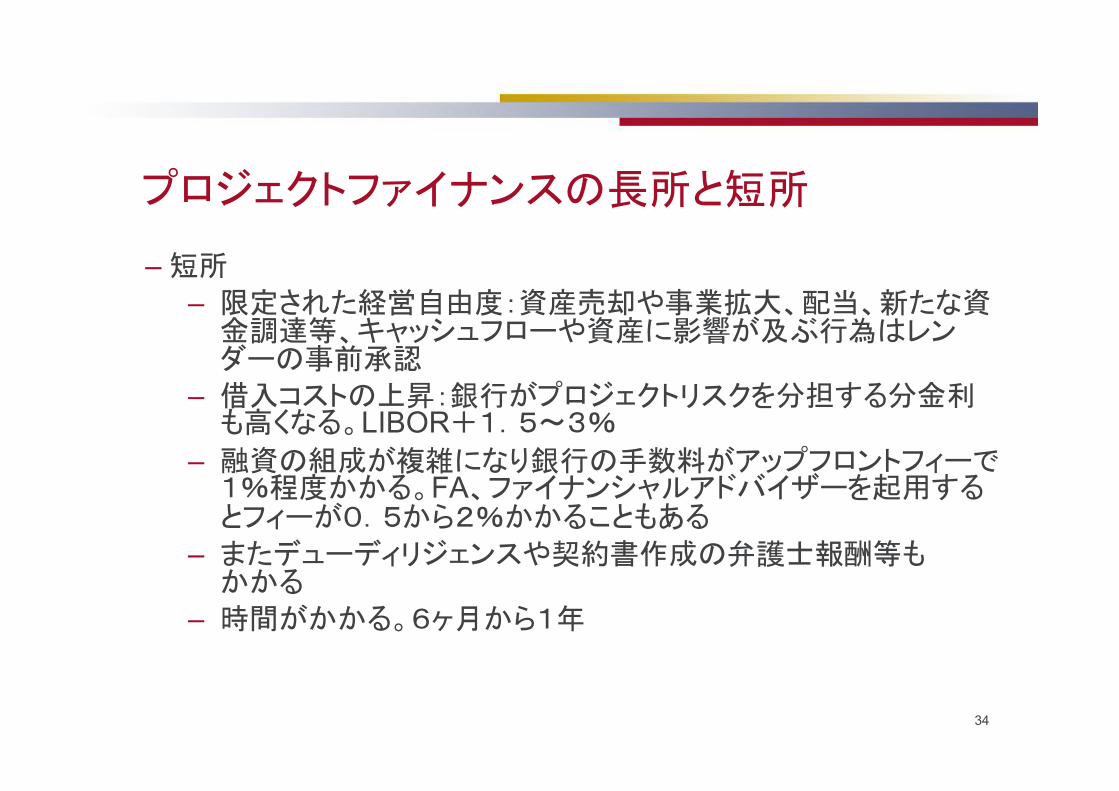

プロジェクトファイナンスの長所と短所

– 短所

– 限定された経営自由度:資産売却や事業拡大、配当、新たな資金調達等、キャッシュフローや資産に影響が及ぶ行為はレンダーの事前承認

– 借入コストの上昇:銀行がプロジェクトリスクを分担する分金利も高くなる。LIBOR+1.5~3%

– 融資の組成が複雑になり銀行の手数料がアップフロントフィーで1%程度かかる。FA、ファイナンシャルアドバイザーを起用するとフィーが0.5から2%かかることもある

– またデューディリジェンスや契約書作成の弁護士報酬等もかかる

– 時間がかかる。6ヶ月から1年

35

プロジェクトリスクのシェアー

– 当該リスクを もうまくコントロールできるものが当該リスクを分担する

– 土地所有権又は利用権の確保については事業会社の責任

– プラントを期限内、予算内及び性能を達成して完工するリスクはEPCコントラクターが取る

– 自然災害による工事中断リスクは保険会社が取る

– プラントの運営に関するリスクはO&M事業者が取る

– リスクの種類は大きく分類して3つ

– 政治リスク・制度変更リスク

– 自然リスク

– 商業リスク

36

スポンサー・サポート契約

– プロジェクト・ファイナンスなので、借入金の債務保証をスポンサーがするものではない

– スポンサーは出資先の会社が健全に事業運営をすることを貸付人に約束するもの。スポンサー間は連帯債務ではない

– 劣後貸付、追加劣後貸付の義務履行の約束

– プロジェクト関連契約の義務履行の約束

– 表明保証(プロジェクト関連契約に関する許認可の保有、株式保有、)

– 誓約

– 借入人にプロジェクト関連契約を遵守させる

– プロジェクト完工日の実現

– 借入人の監督

– 人員派遣、技術支援

– 代替企業の選定と承継

– 劣後貸出債権の劣後性の維持

– 出資比率の維持

– 倒産スポンサーの株式買取義務

37

スポンサー・サポート契約 その2

– 借入人の誓約違反について、貸付人が被った損害賠償

– 次の事由により貸付人が被った損害賠償

– 売電債権の質権設定に対する電力会社の異議なき承諾が取れなかった場合

– 電力受給契約の契約上の地位譲渡予約に対する電力会社の承諾が取れなかった場合

– 予約完結権の行使に基づく契約上の地位の譲渡に際して、電力会社の承諾を取得できなかったこと

– 電力受給契約に関する借入人の表明保証に虚偽があった場合

– 予定されていた補助金が全部又は一部交付されないこと又は補助金の全部又は一部について返還を求められたこと

– 補助金適正化法で要求される担保権設定についての承認を受けていないこと、承認が取り消されたこと、当局から担保権設定に異議が出たこと

– 用地を工場財団に組み入れられなかったこと

– 電力会社から解列指令が出されたこと

– 電力受給契約が電力会社の責めに帰すべき事由により解除されたこと

– 騒音・低周波騒音・景観その他の重大な環境問題が生じた場合

– 用地の使用権限が制約され又は使用権限を失った場合

– 上記理由により返済不能額が生じた場合は、当該返済不能額を損害額とみなす

38

取扱案件①

– 風力発電案件

– 北海道幌延町

– 北海道さらきとまない

– 北海道響灘

– 青森六ヶ所村

– 愛媛県三崎町

– 秋田県八竜

– 石川県輪島

39

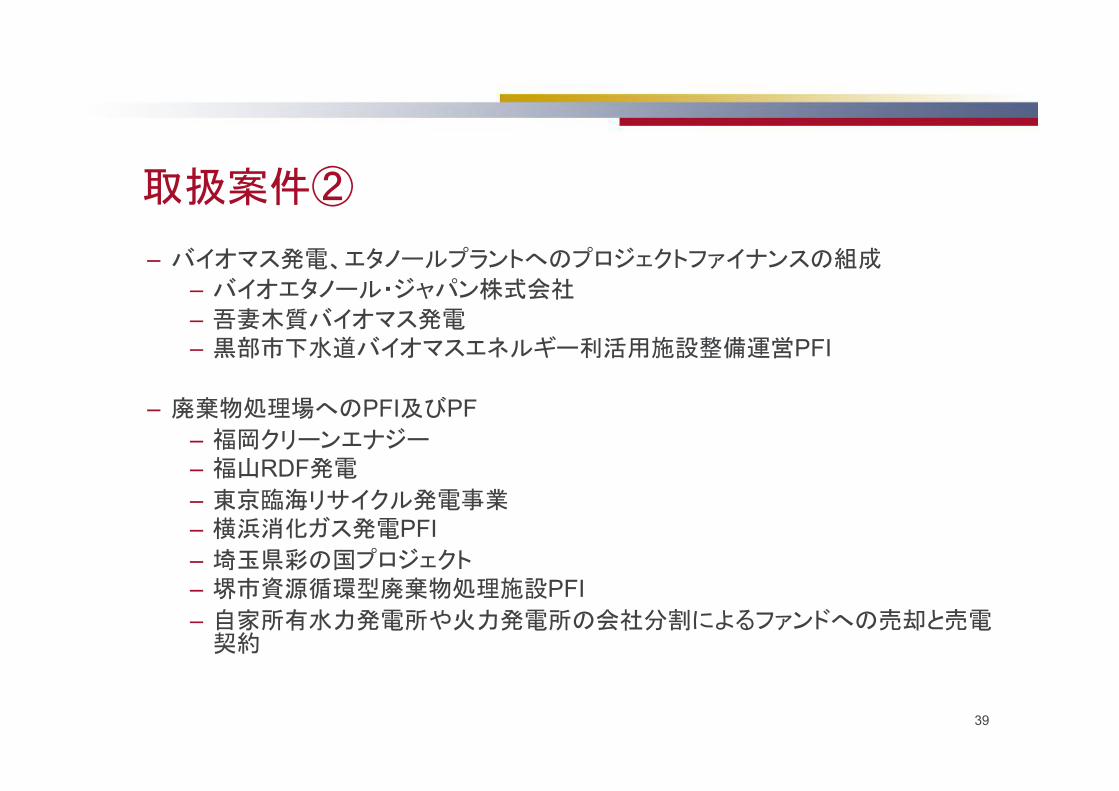

取扱案件②

– バイオマス発電、エタノールプラントへのプロジェクトファイナンスの組成

– バイオエタノール・ジャパン株式会社

– 吾妻木質バイオマス発電– 黒部市下水道バイオマスエネルギー利活用施設整備運営PFI

– 廃棄物処理場へのPFI及びPF– 福岡クリーンエナジー– 福山RDF発電

– 東京臨海リサイクル発電事業– 横浜消化ガス発電PFI– 埼玉県彩の国プロジェクト– 堺市資源循環型廃棄物処理施設PFI– 自家所有水力発電所や火力発電所の会社分割によるファンドへの売却と売電契約

40

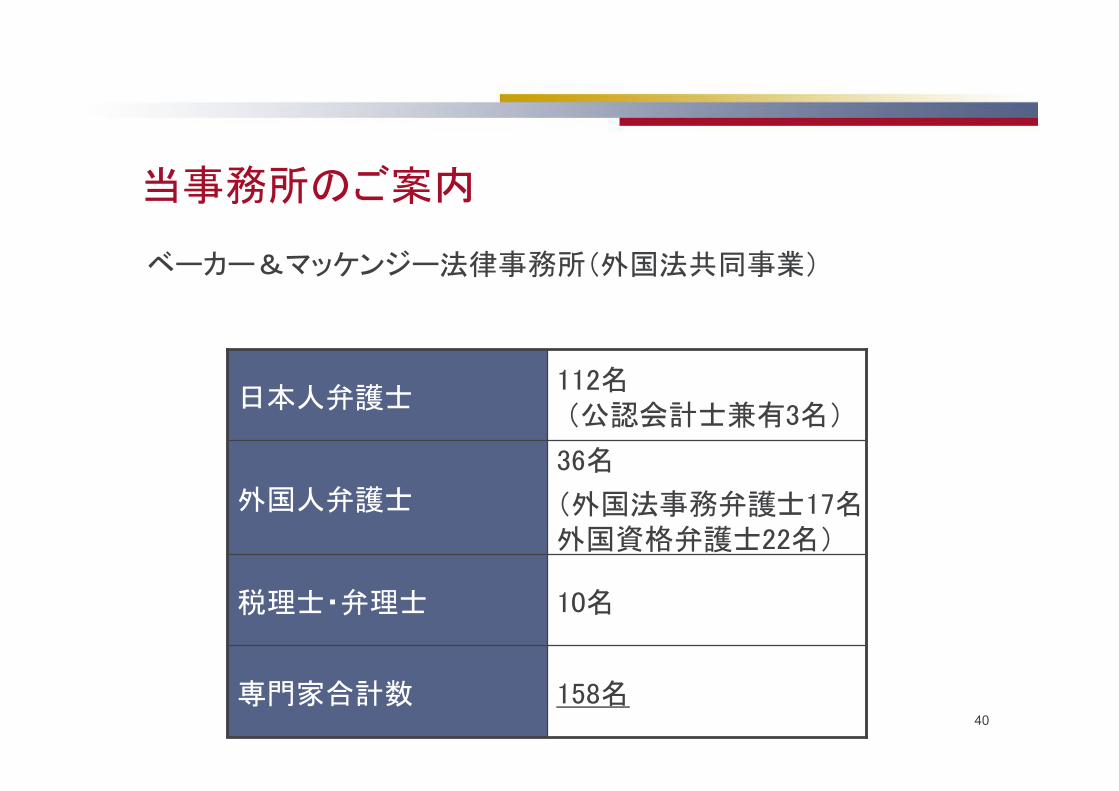

当事務所のご案内

ベーカー&マッケンジー法律事務所(外国法共同事業)

158名専門家合計数

10名税理士・弁理士

36名

(外国法事務弁護士17名外国資格弁護士22名)

外国人弁護士

112名(公認会計士兼有3名)

日本人弁護士

41

41©2012江口

直明/Naoaki Eguchi

アゼルバイジャンバクー

アラブ首長国連邦アブダビ

イギリスロンドン

イタリアミラノローマ

ウクライナキエフ

エジプトカイロ

オーストリアウィーン

オランダアムステルダム

カザフスタンアルマティ

トルコ

イスタンブールバーレーン

マナマハンガリー

ブダペストフランス

パリベルギー

アントワープブリュッセル

ポーランドワルシャワ

南アフリカ

ヨハネスブルグ

モロッコ

カサブランカルクセンブルクロシア

サンクトペテルブルグモスクワ

北米、 ラテンアメリカ

インドネシアジャカルタ

オーストラリアシドニーメルボルン

シンガポールタイ

バンコク台湾

台北中国

上海北京香港

日本東京

フィリピンマニラ

ベトナムハノイホーチミン

マレーシアクアラルンプール

アメリカサンフランシスコシカゴダラスニューヨークパロアルトヒューストンマイアミワシントン D.C.

アルゼンチンフアレスブエノス・アイレス

カナダトロント

コロンビアボゴタ

チリサンティアゴ

メキシコグアダラハラティフアナメキシコ・シティモンテレイ

ブラジルサン・パウロブラジリアポルト・アレグレリオ・デ・ジャネイロ

ベネズエラカラカスバレンシア

ベーカー&マッケンジー法律事務所のご案内71オフィス(44ヶ国)

カタール

ドーハ

サウジアラビア

リヤド

スイス

ジュネーブ

チューリッヒスウェーデン

ストックホルムスペイン

バルセロナマドリッド

トルコイスタンブール

チェコプラハ

ドイツデュッセルドルフフランクフルトベルリンミュンヘン

アジア・パシフィックヨーロッパ、中東、アフリカ

ご清聴ありがとうございました。

© 2012 Baker & McKenzie. All rights reserved.Baker & McKenzie International is a Swiss Verein with member law firms around the world. In accordance with the common terminology used in professional service organizations, reference to a “partner” means a person who is a partner, or equivalent, in such a law firm. Similarly, reference to an “office” means an office of any such law firm.

ベーカー&マッケンジー法律事務所(外国法共同事業)

弁護士 江口 直明電話[email protected]

Australia’s Renewable Energy MarketAn introduction to legal and policy trends, opportunities and issues for investment

Renewable Energy Seminar: Latest Trends and Issues in the Asia Pacific Region

JBIC, TokyoSeptember 5, 2012

Paul CurnowSydney

44

Outline

1. Renewable energy in Australia2. Market snapshot3. The Renewable Energy Target4. Additional policies

a. Carbon Pricing Mechanismb. Clean Energy Finance Corporationc. Australian Renewable Energy Agency

5. Investing in Australia

45

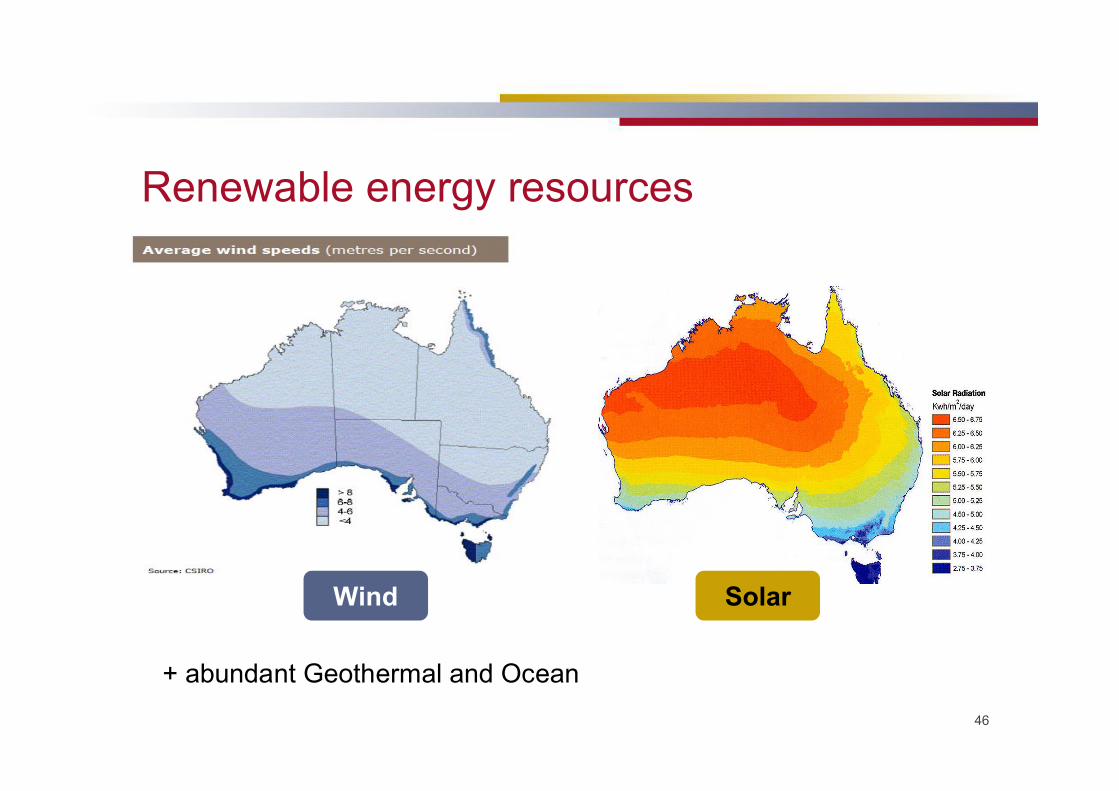

Renewable energy in Australia

46

Renewable energy resources

+ abundant Geothermal and Ocean

Wind Solar

47

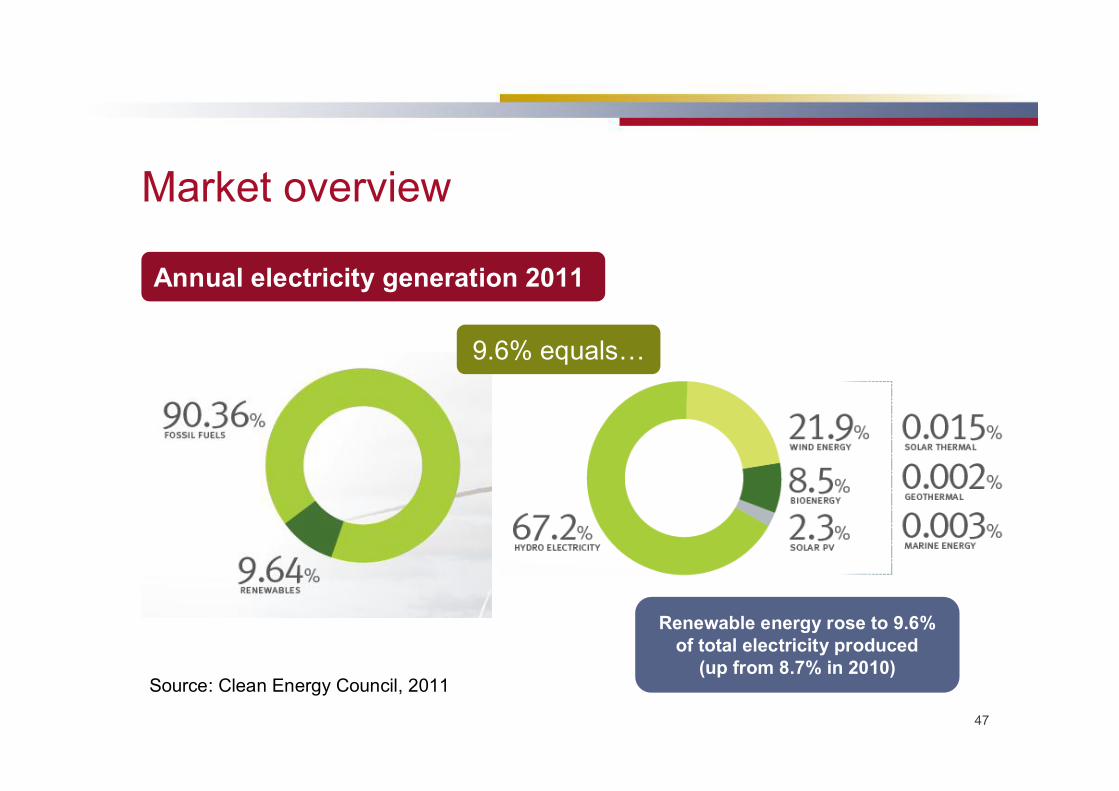

Market overview

Annual electricity generation 2011

Renewable energy rose to 9.6% of total electricity produced

(up from 8.7% in 2010)Source: Clean Energy Council, 2011

9.6% equals…

48

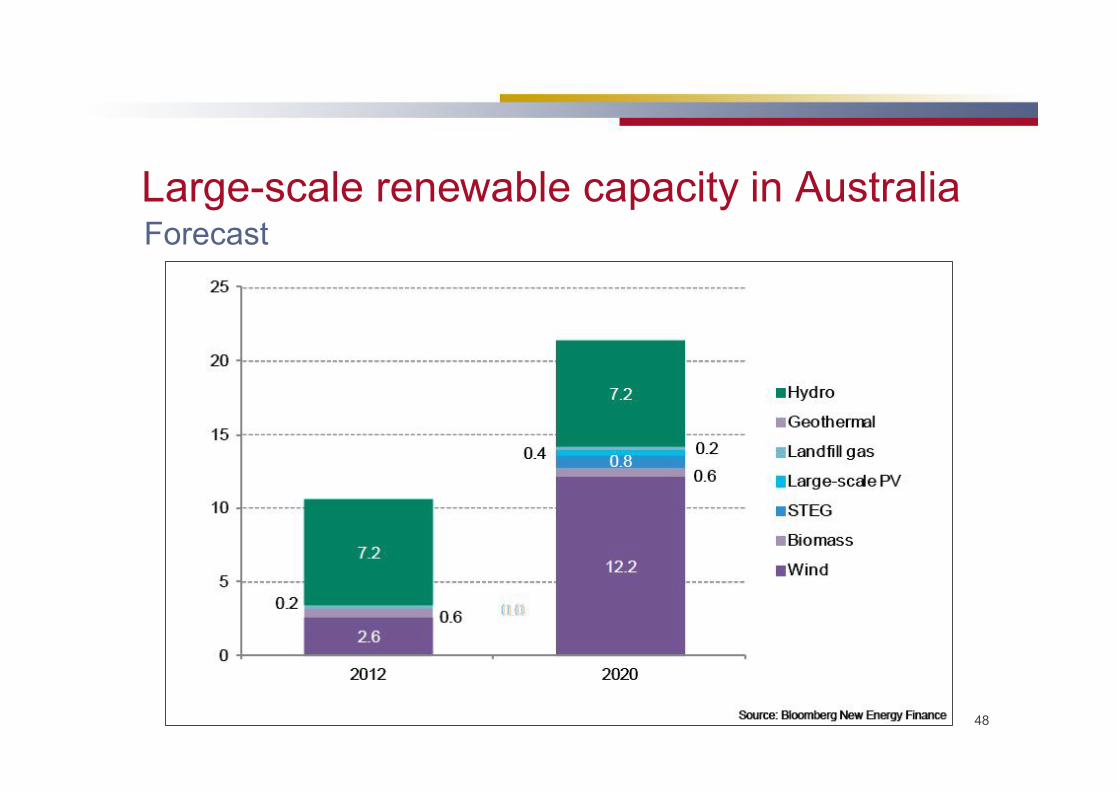

ForecastLarge-scale renewable capacity in Australia

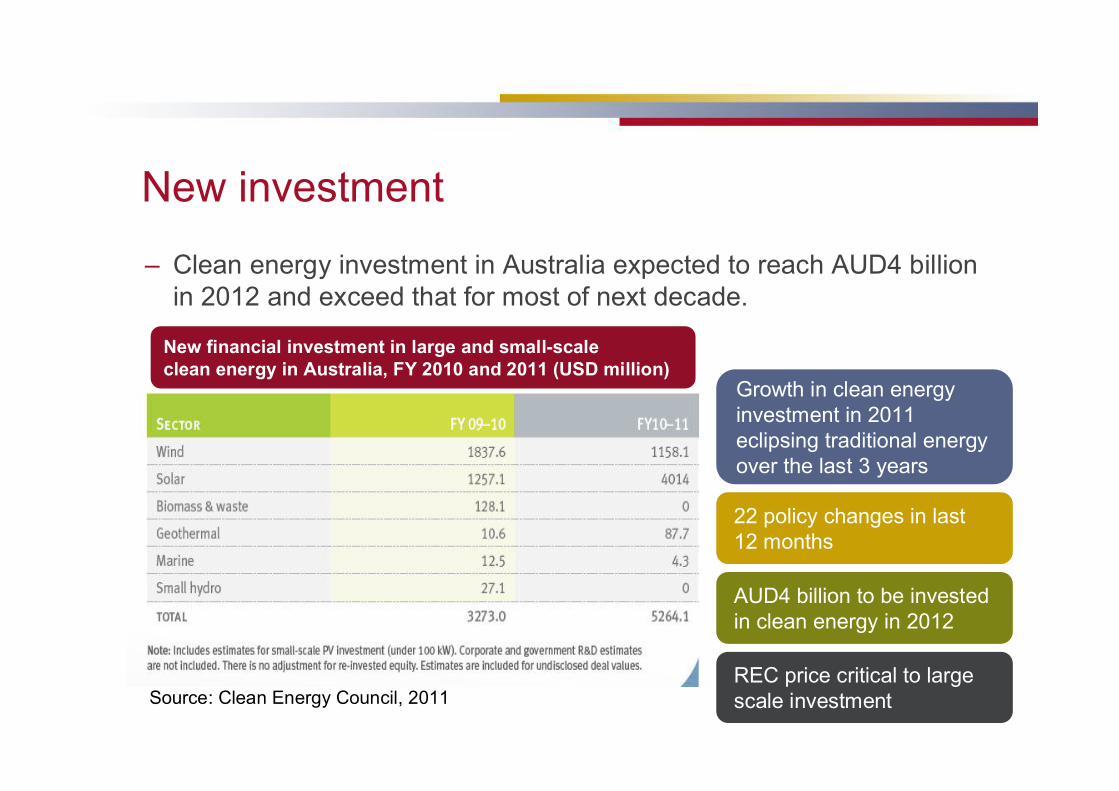

New investment

– Clean energy investment in Australia expected to reach AUD4 billion in 2012 and exceed that for most of next decade.

Source: Clean Energy Council, 2011

New financial investment in large and small-scale clean energy in Australia, FY 2010 and 2011 (USD million)

REC price critical to large scale investment

AUD4 billion to be invested in clean energy in 2012

22 policy changes in last 12 months

Growth in clean energy investment in 2011 eclipsing traditional energy over the last 3 years

50

AU

D m

illions

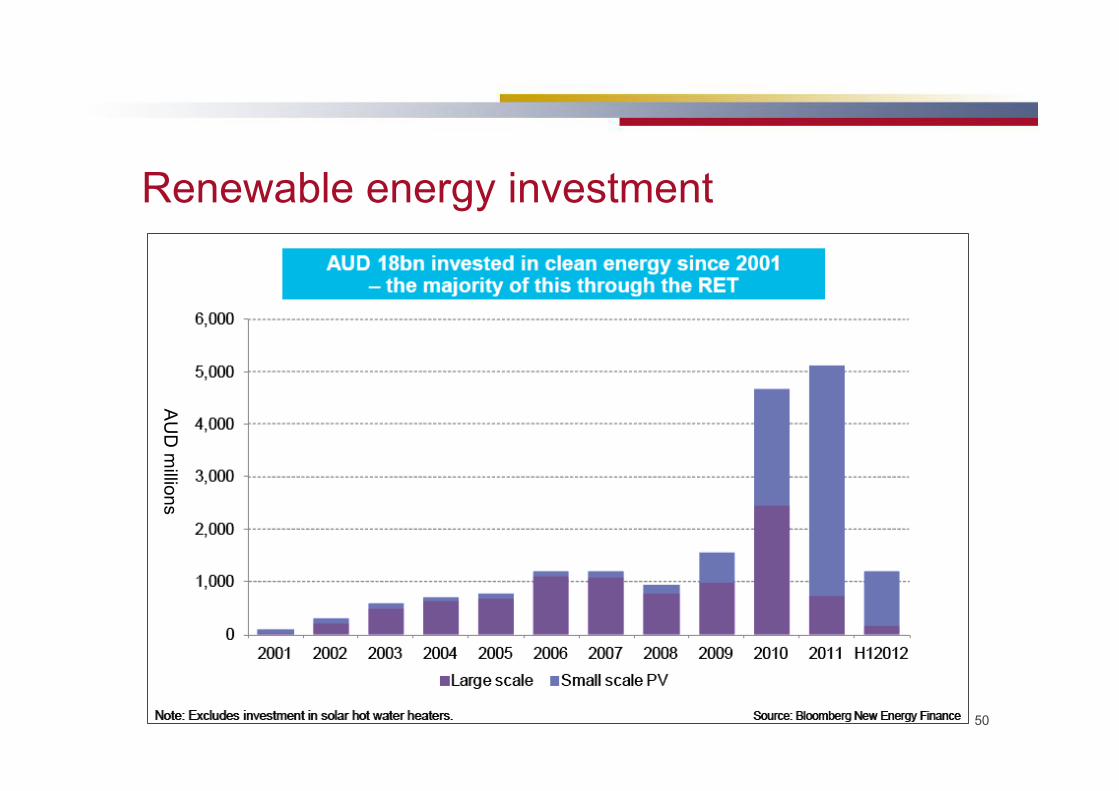

Renewable energy investment

51

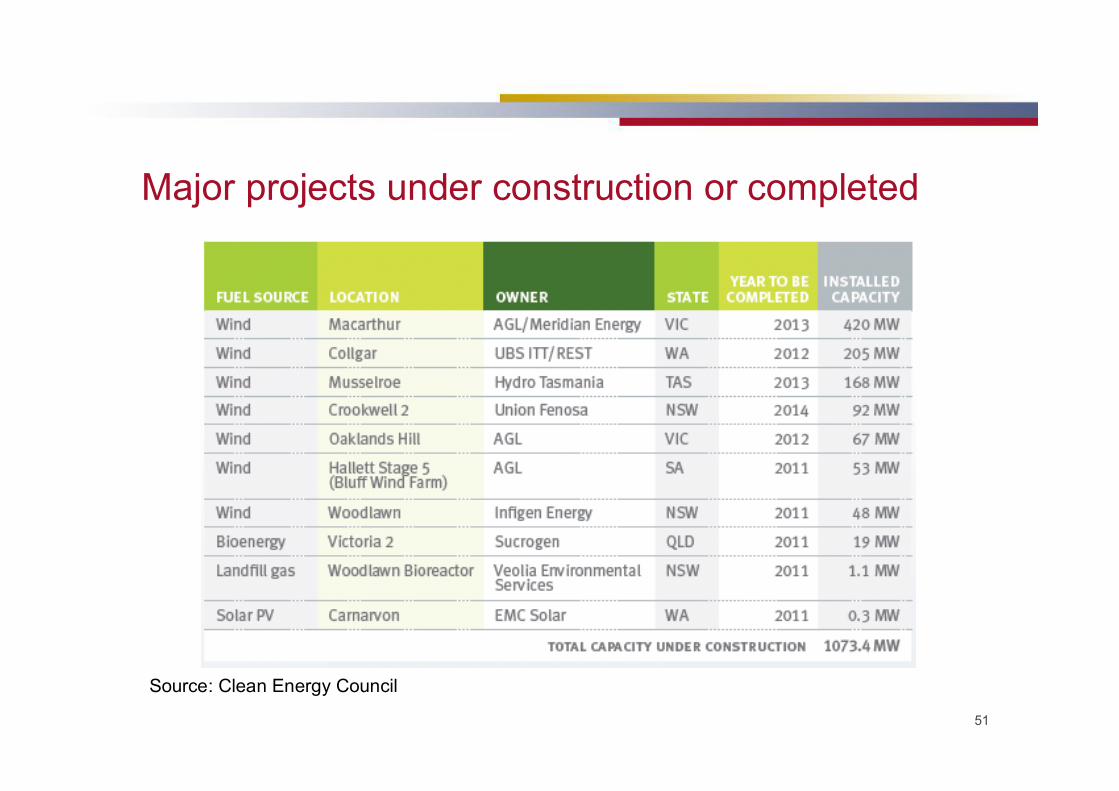

Major projects under construction or completed

Source: Clean Energy Council

52

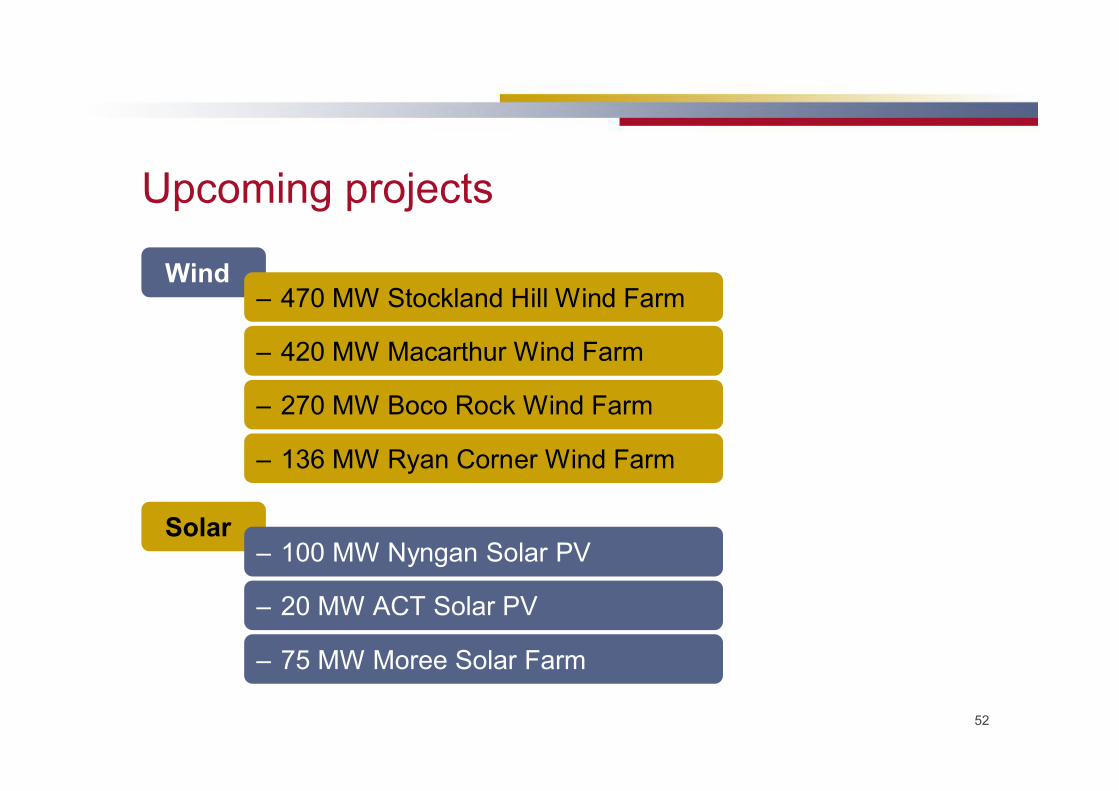

Upcoming projects

Wind

Solar

– 470 MW Stockland Hill Wind Farm

– 420 MW Macarthur Wind Farm

– 270 MW Boco Rock Wind Farm

– 136 MW Ryan Corner Wind Farm

– 100 MW Nyngan Solar PV

– 20 MW ACT Solar PV

– 75 MW Moree Solar Farm

53

Renewable energy target

54

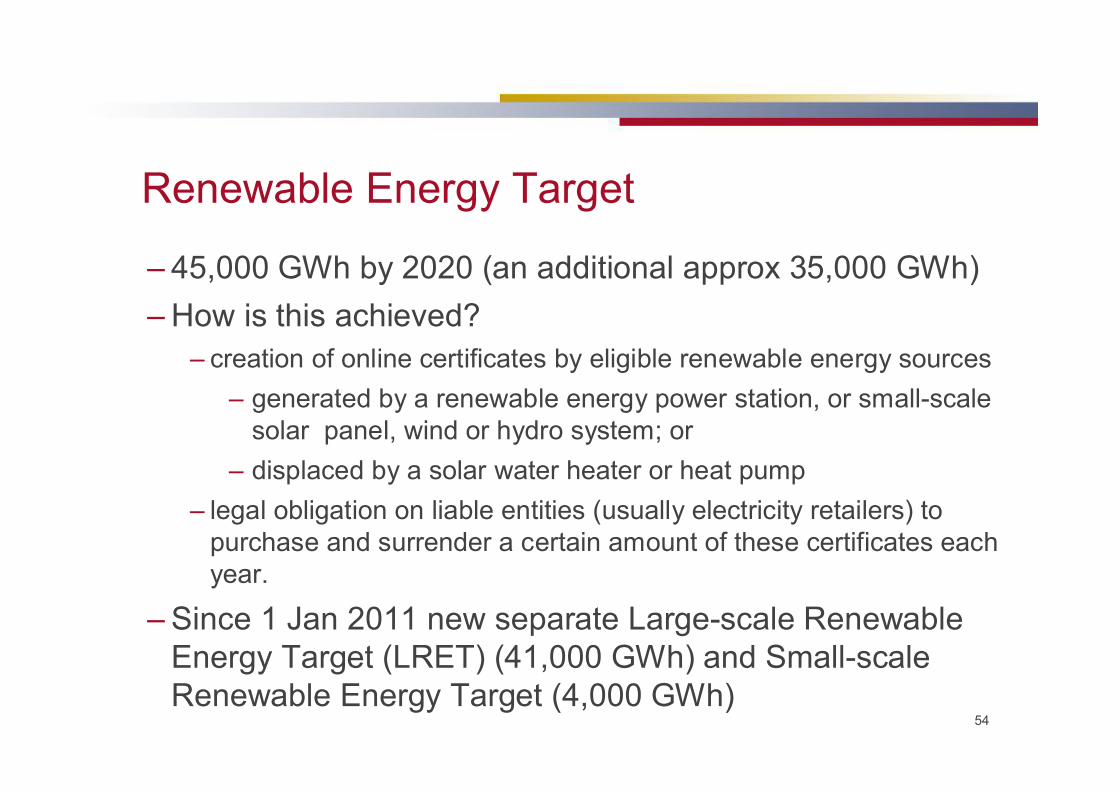

Renewable Energy Target

– 45,000 GWh by 2020 (an additional approx 35,000 GWh)– How is this achieved?

– creation of online certificates by eligible renewable energy sources– generated by a renewable energy power station, or small-scale

solar panel, wind or hydro system; or– displaced by a solar water heater or heat pump

– legal obligation on liable entities (usually electricity retailers) to purchase and surrender a certain amount of these certificates each year.

– Since 1 Jan 2011 new separate Large-scale Renewable Energy Target (LRET) (41,000 GWh) and Small-scale Renewable Energy Target (4,000 GWh)

55

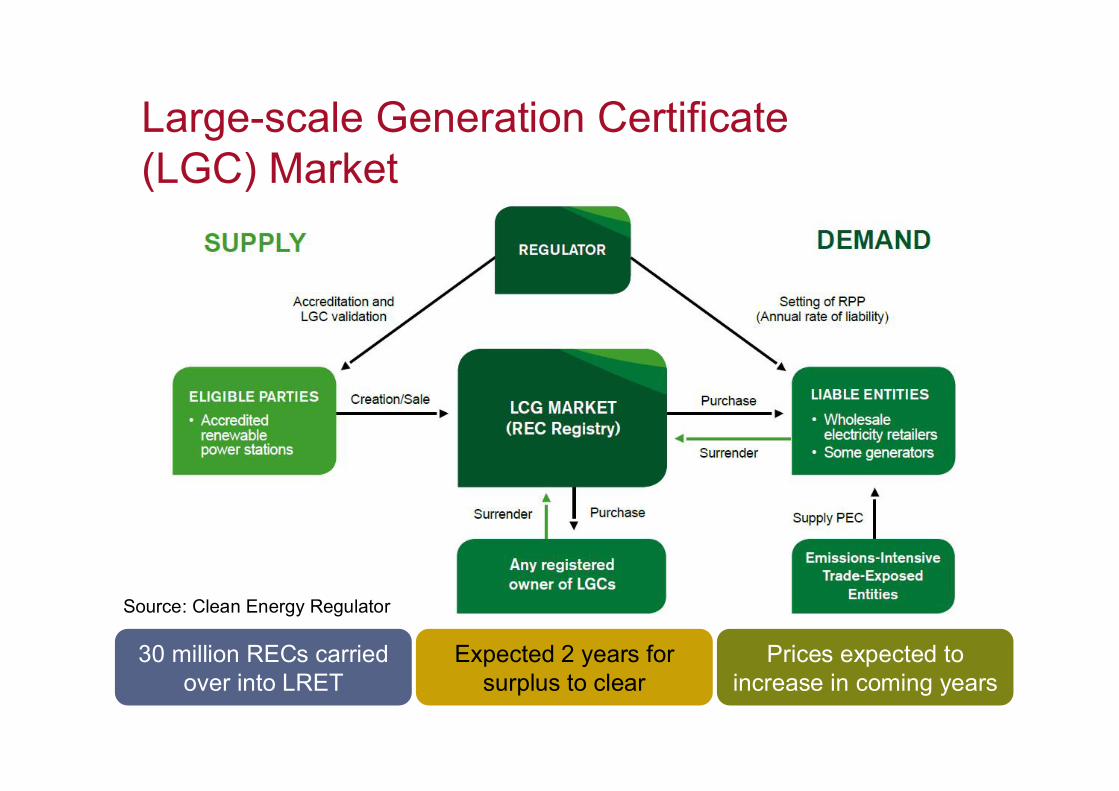

Large-scale Generation Certificate (LGC) Market

30 million RECs carried over into LRET

Expected 2 years for surplus to clear

Prices expected to increase in coming years

Source: Clean Energy Regulator

56

Projected supply-demand growth in LRET

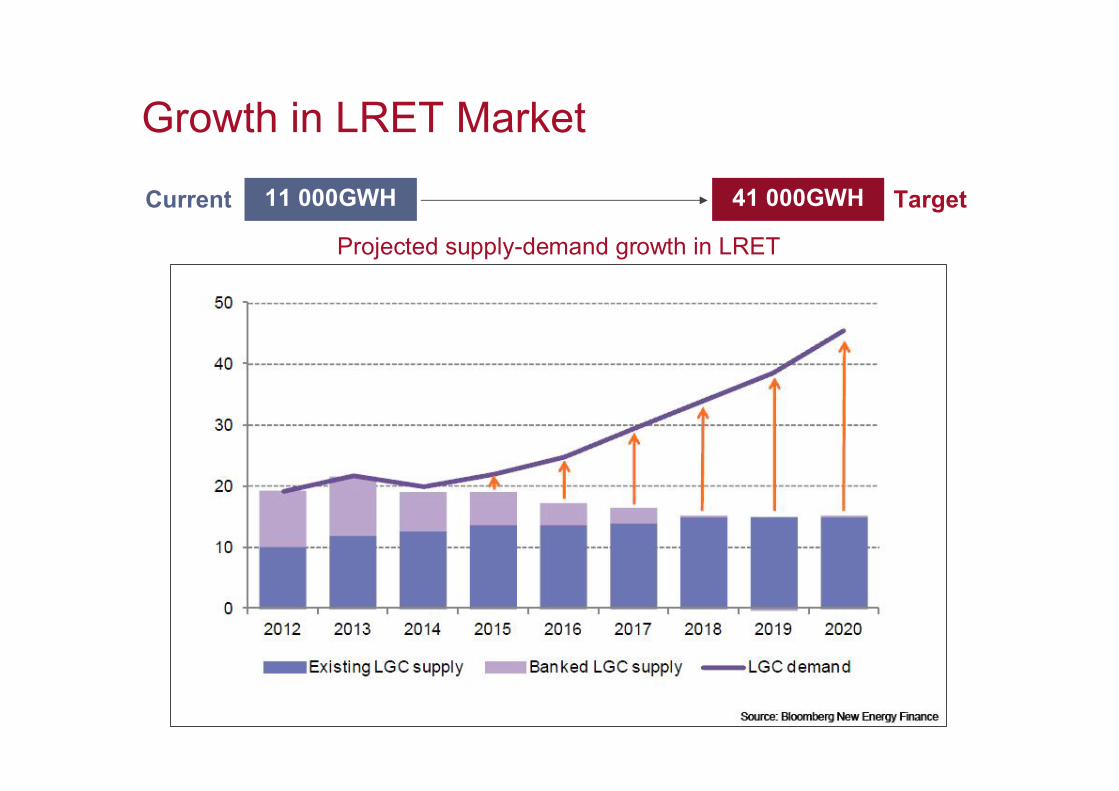

11 000GWH 41 000GWHCurrent Target

Growth in LRET Market

57

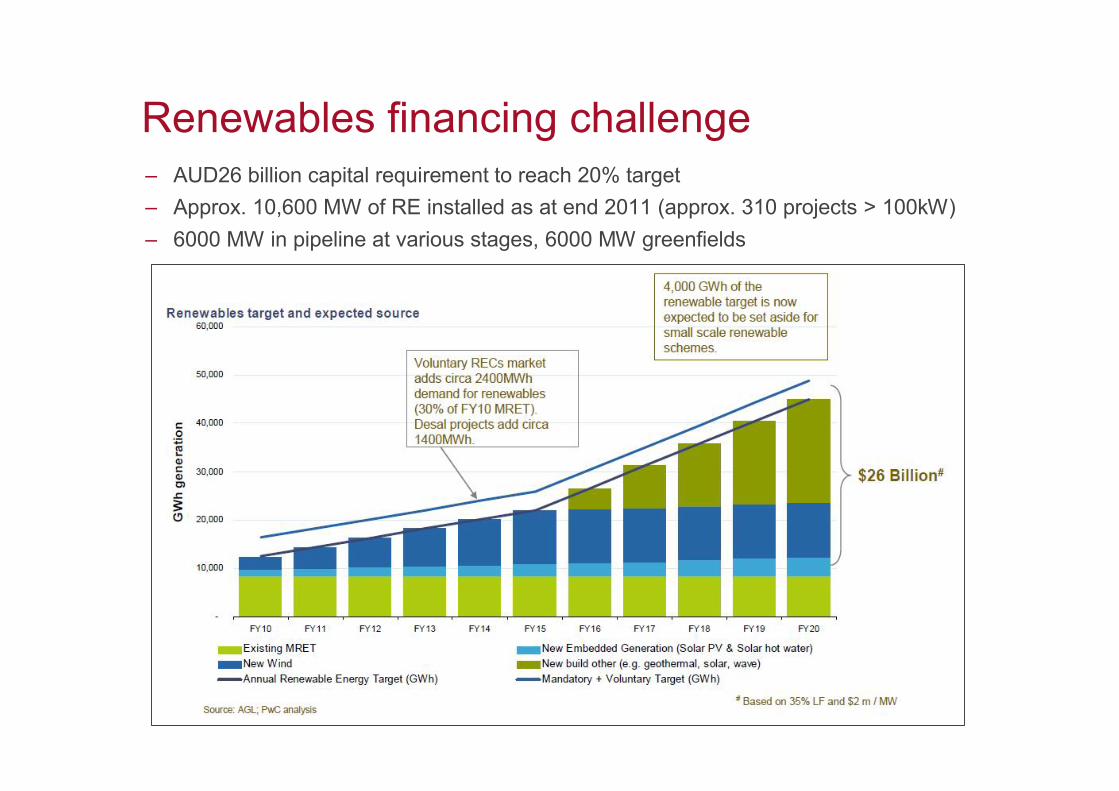

Renewables financing challenge– AUD26 billion capital requirement to reach 20% target– Approx. 10,600 MW of RE installed as at end 2011 (approx. 310 projects > 100kW)– 6000 MW in pipeline at various stages, 6000 MW greenfields

58

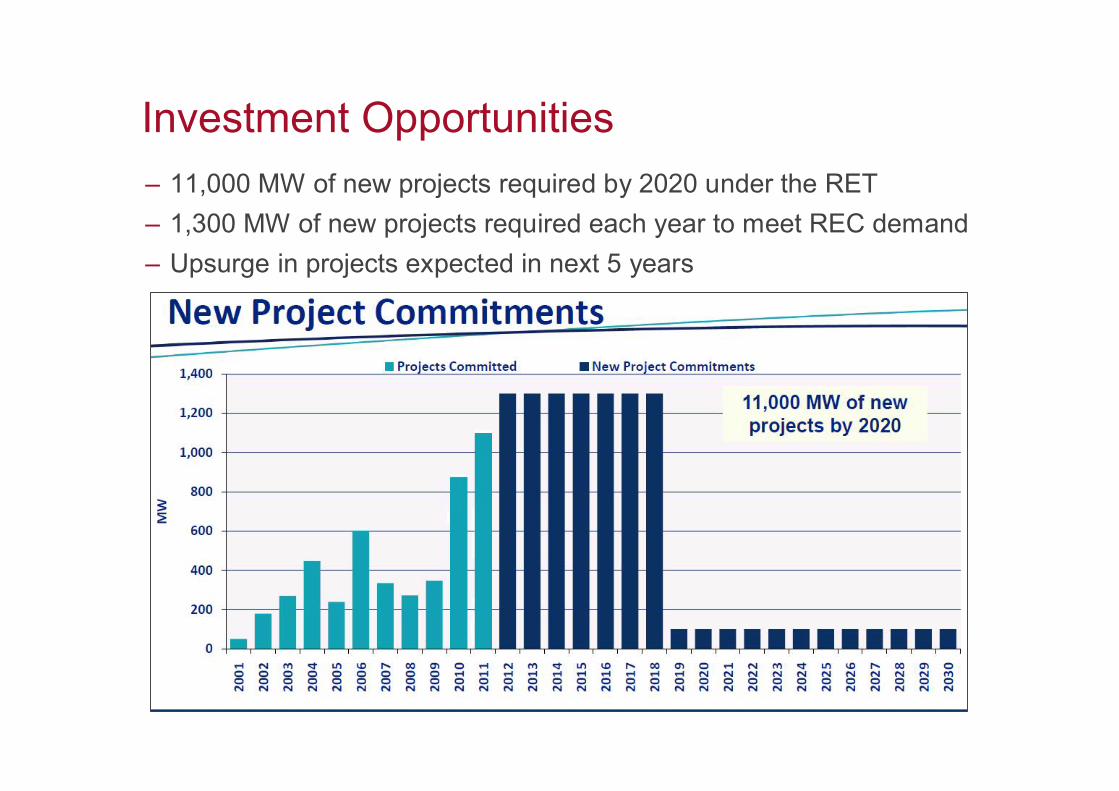

Investment Opportunities– 11,000 MW of new projects required by 2020 under the RET– 1,300 MW of new projects required each year to meet REC demand– Upsurge in projects expected in next 5 years

59

Additional policies

60

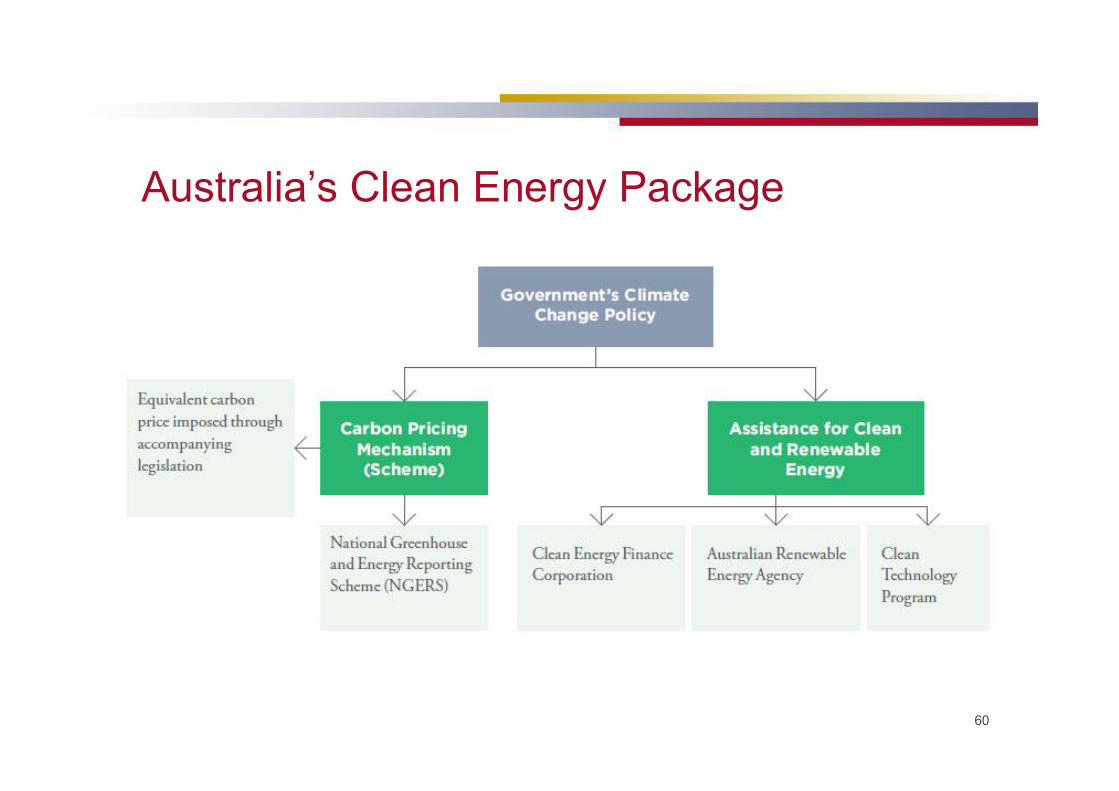

Australia’s Clean Energy Package

61

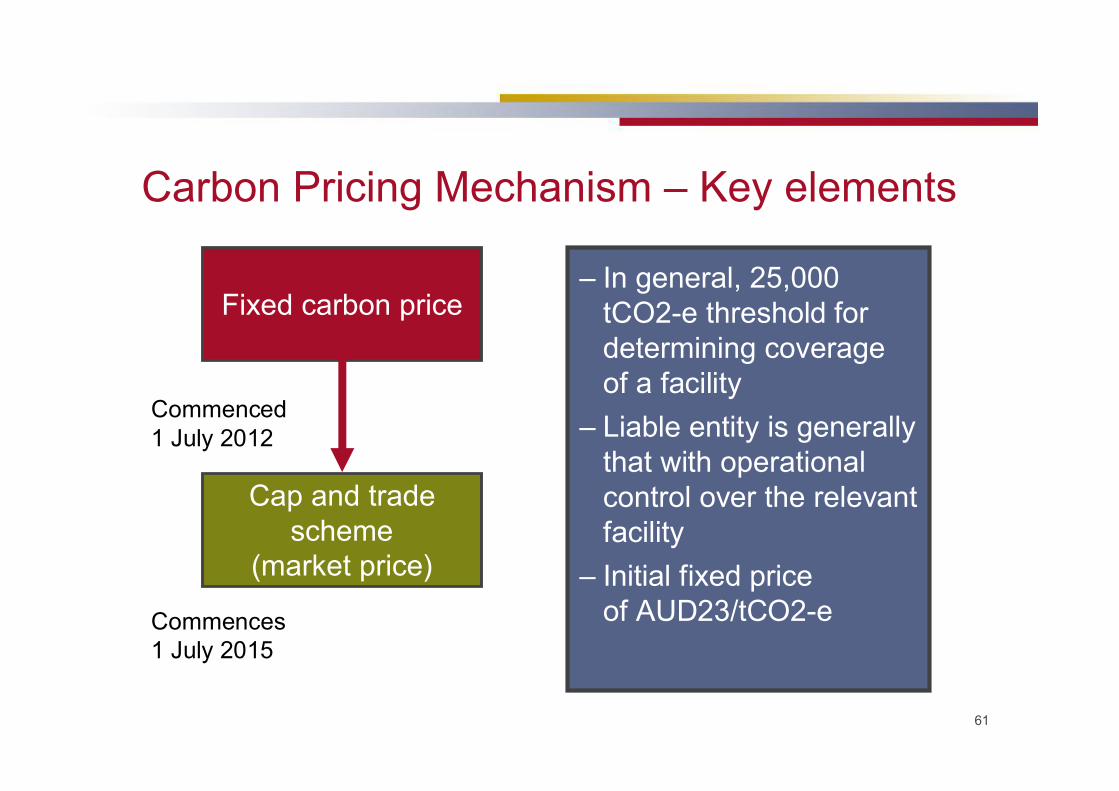

Carbon Pricing Mechanism – Key elements

– In general, 25,000 tCO2-e threshold for determining coverage of a facility

– Liable entity is generally that with operational control over the relevant facility

– Initial fixed price of AUD23/tCO2-e

Fixed carbon price

Cap and trade scheme

(market price)

Commenced1 July 2012

Commences 1 July 2015

62

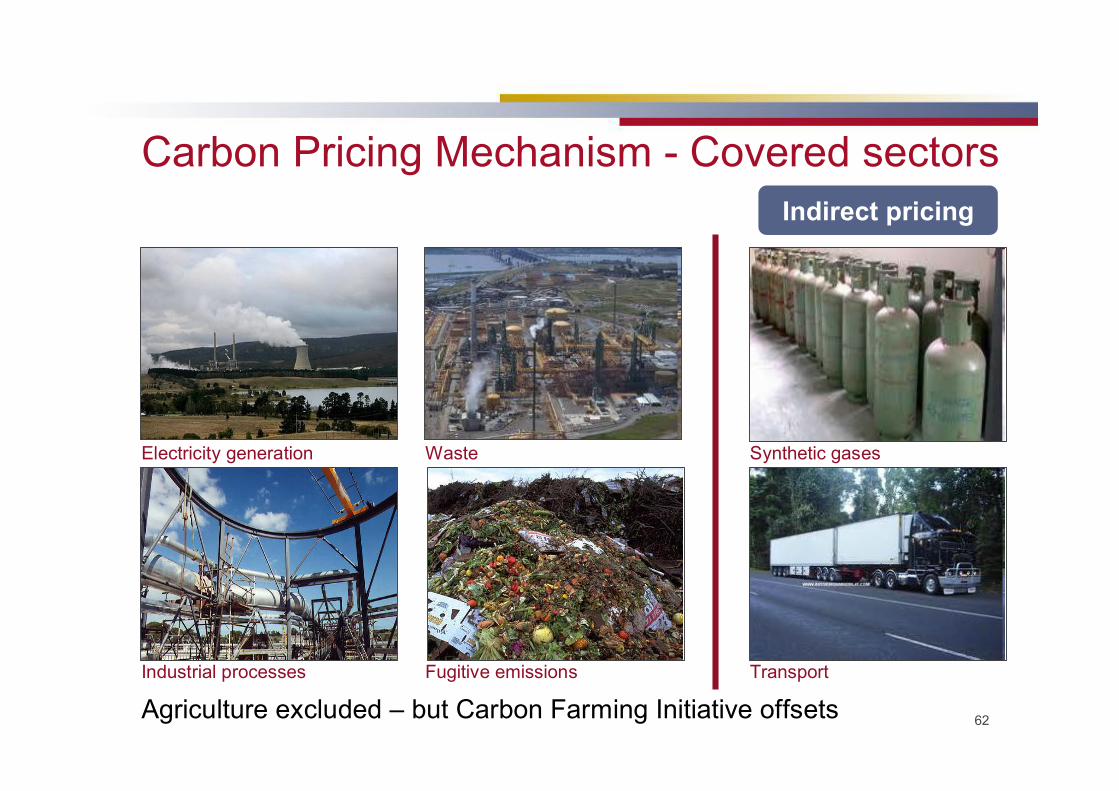

Carbon Pricing Mechanism - Covered sectors

Synthetic gases

Transport

Agriculture excluded – but Carbon Farming Initiative offsets

Electricity generation Waste

Industrial processes Fugitive emissions

Indirect pricing

63

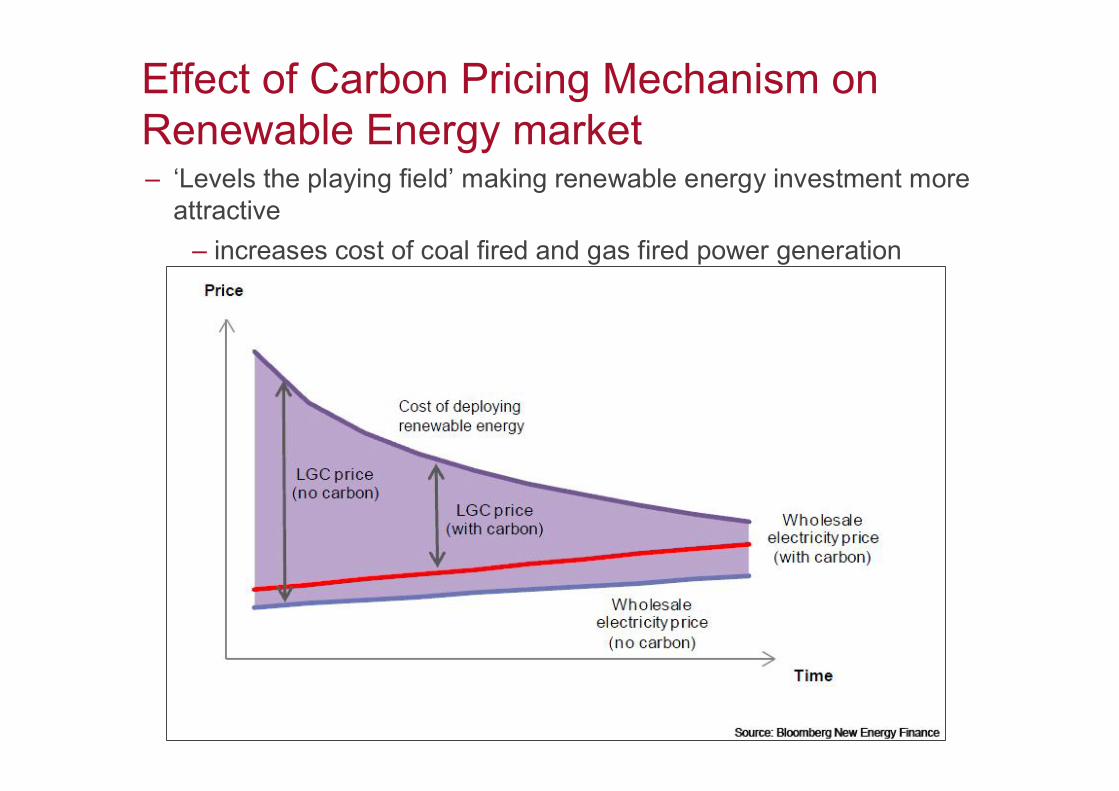

Effect of Carbon Pricing Mechanism on Renewable Energy market– ‘Levels the playing field’ making renewable energy investment more

attractive– increases cost of coal fired and gas fired power generation

64

Clean Energy Finance Corporation (CEFC)

– The CEFC was announced under the Clean Energy Future Package

– Established to encourage private investment and overcome market barriers to commercialising clean energy technologies

– It will:– have AUD10 billion in available funding over five years, with at

least half earmarked for renewable energy projects– operate through providing loans, loan guarantees and equity

investments along side private investors in renewable energy projects

– commence operations from 1 July 2013

65

Australian Renewable Energy Agency (ARENA)

– ARENA, also an independent statutory body, responsible for managing existing AUD3.2 billion worth of government funding

– Responsible for overseeing delivery and implementing direct government funding for renewable energy projects, including:– AUD100 million Renewable Energy Venture Capital Fund– AUD40 million Emerging Renewables Program

– The Solar Flagships program, Australian Solar Institute and the Australia Centre for Renewable Energy will come under ARENA control.

66

Investing in Australia

67

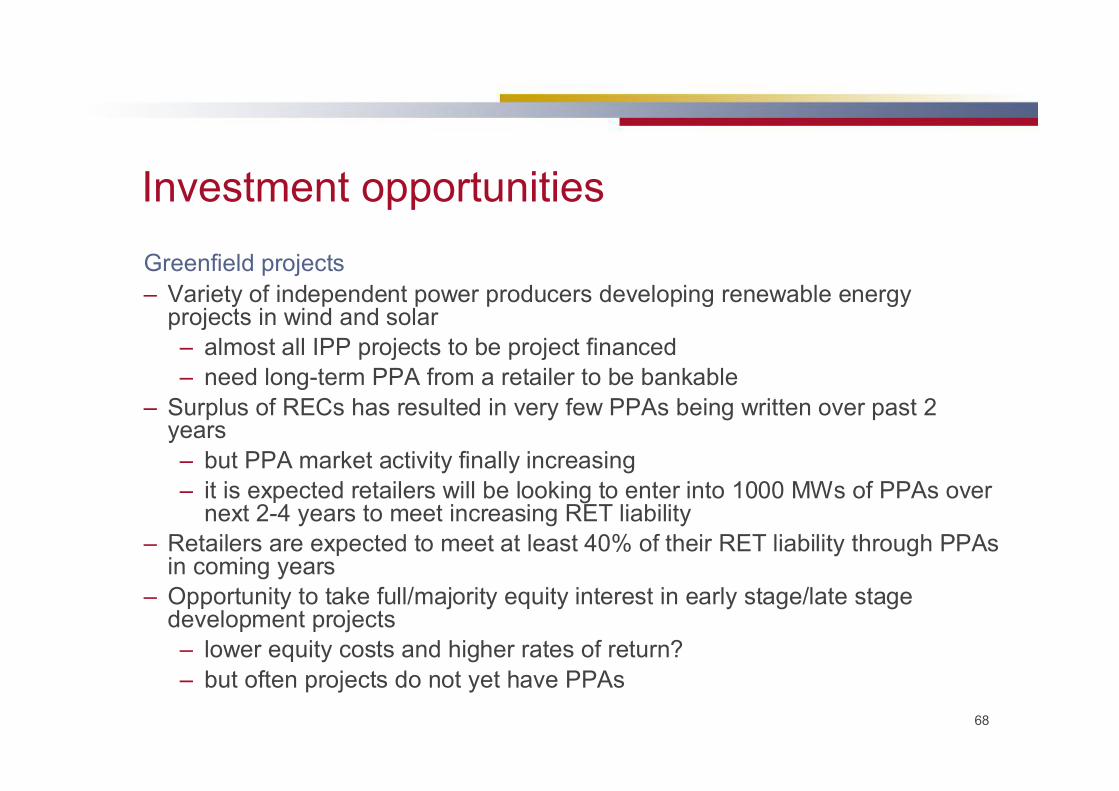

Investment opportunities

Projects developed by Retailers– Market dominated by three major retailers: Origin, AGL & TruEnergy– Typically favouring Build Transfer Operate model

– most projects that have reached financial closure in last 2 years have been developed by retailers

– crowded out independent developers and – with oversupply of RECs – no need for Retailers to enter into long term PPAs

– Opportunity to take full/majority equity interest in an operating asset with stable rate of return

– but is rate of return high enough?– retailers charge upfront premium

68

Investment opportunitiesGreenfield projects– Variety of independent power producers developing renewable energy

projects in wind and solar– almost all IPP projects to be project financed– need long-term PPA from a retailer to be bankable

– Surplus of RECs has resulted in very few PPAs being written over past 2 years– but PPA market activity finally increasing – it is expected retailers will be looking to enter into 1000 MWs of PPAs over

next 2-4 years to meet increasing RET liability– Retailers are expected to meet at least 40% of their RET liability through PPAs

in coming years– Opportunity to take full/majority equity interest in early stage/late stage

development projects– lower equity costs and higher rates of return?– but often projects do not yet have PPAs

69

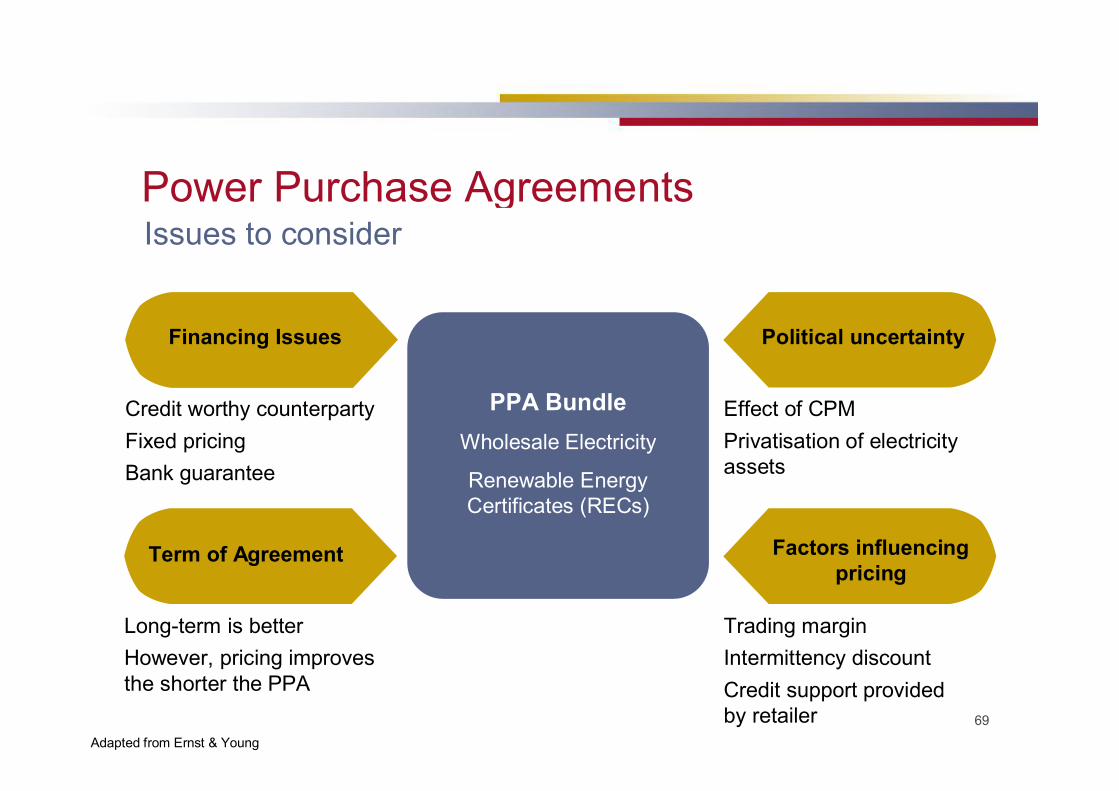

Power Purchase AgreementsIssues to consider

PPA BundleWholesale Electricity

Renewable Energy Certificates (RECs)

Financing Issues

Term of Agreement

Political uncertainty

Factors influencing pricing

Credit worthy counterpartyFixed pricingBank guarantee

Effect of CPMPrivatisation of electricity assets

Long-term is betterHowever, pricing improves the shorter the PPA

Trading marginIntermittency discountCredit support provided by retailer

Adapted from Ernst & Young

70

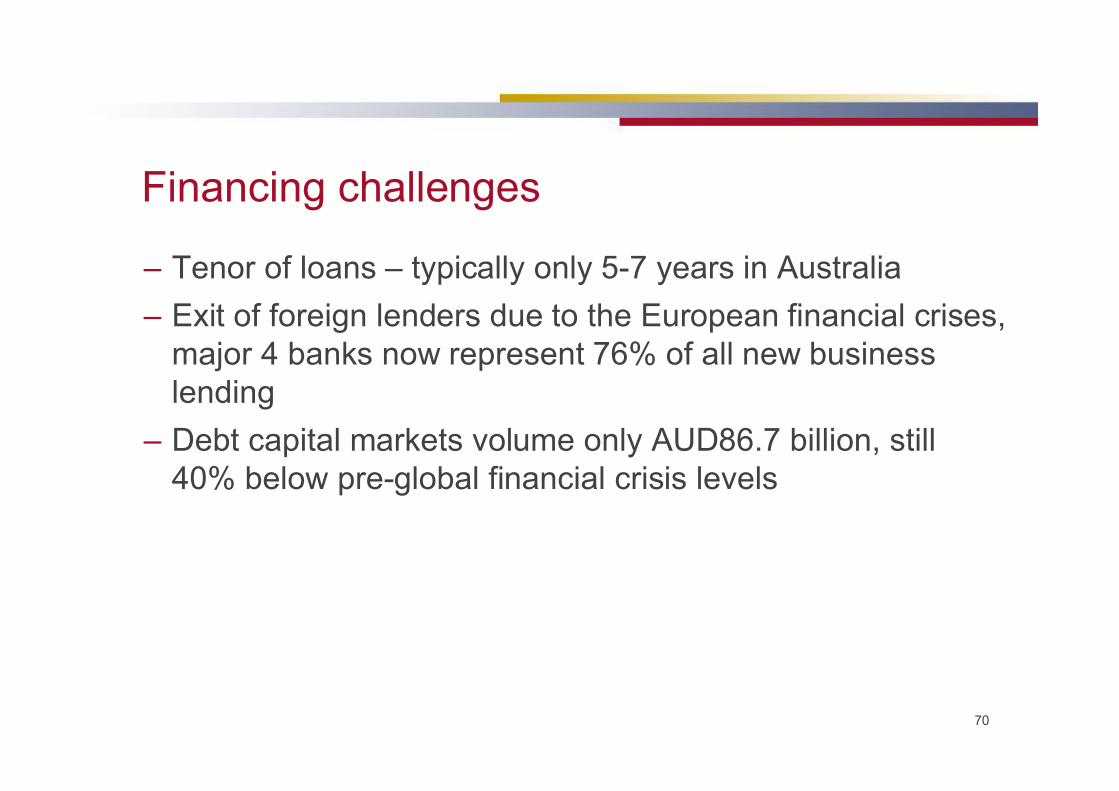

Financing challenges

– Tenor of loans – typically only 5-7 years in Australia– Exit of foreign lenders due to the European financial crises,

major 4 banks now represent 76% of all new business lending

– Debt capital markets volume only AUD86.7 billion, still 40% below pre-global financial crisis levels

71

Foreign Investment Review Board (FIRB)

– Australia is open to foreign investment - some investment requires notification and/or approval

– FIRB governs foreign investment proposals in Australia– Advice should be sought on whether FIRB approval required

to investProposals requiring notification

– Acquisitions of substantial interests in existing Australian businesses with total gross assets greater than AUD244 million

– State-owned investors

Thank you

© 2012 Baker & McKenzie. All rights reserved.Baker & McKenzie International is a Swiss Verein with member law firms around the world. In accordance with the common terminology used in professional service organizations, reference to a “partner” means a person who is a partner, or equivalent, in such a law firm. Similarly, reference to an “office” means an office of any such law firm.

Renewable Energy Market Update - Thailand

Renewable Energy Seminar: Latest Trends and Issues in the Asia Pacific Region

JBIC, TokyoSeptember 5, 2012

Vit VatanayothinBangkok

Regulatory developments and market opportunities

74

Outline

1. Regulatory and market developmentsa. Backgroundb. Current market statusc. Feed-in tariff

2. Investment opportunities3. Key market and investment issues

75

Regulatory and market developments

76

Background– Renewable energy under SPP and VSPP regulations -

power plants using:

as sources of power generation.

Wind

Solar

Hydro

Biogas

Biomass

77

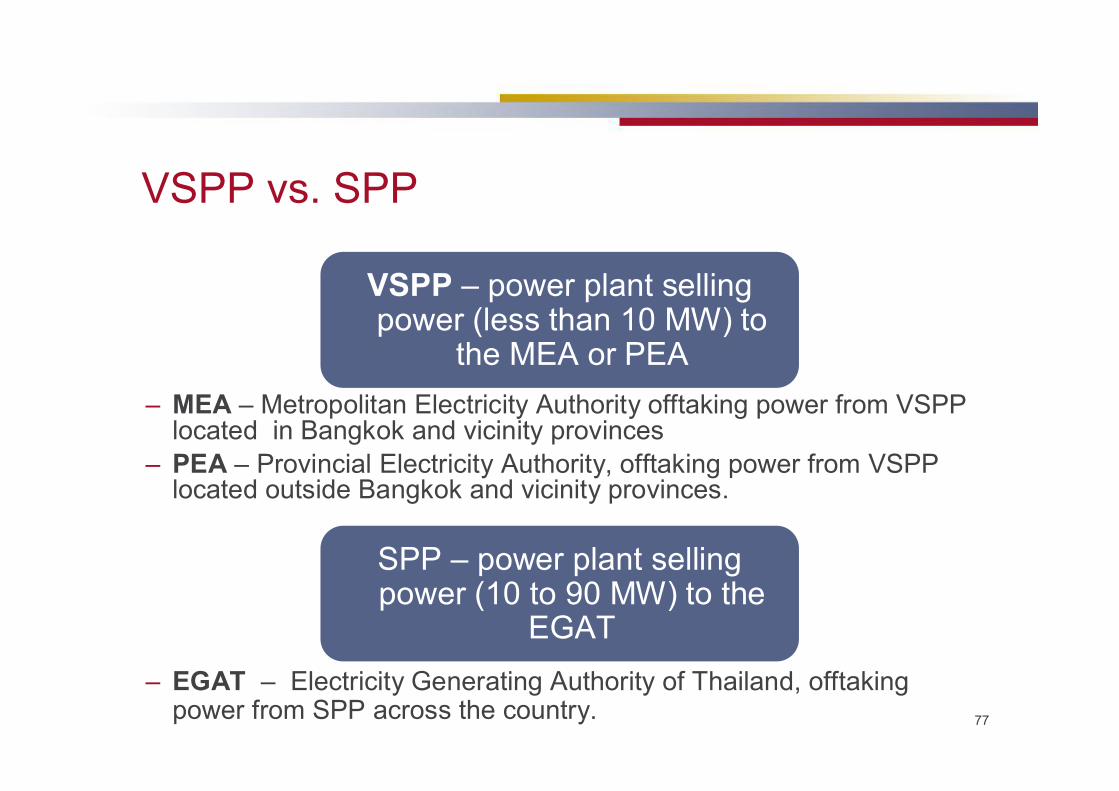

VSPP vs. SPP

– EGAT – Electricity Generating Authority of Thailand, offtaking power from SPP across the country.

VSPP – power plant selling power (less than 10 MW) to

the MEA or PEA

SPP – power plant selling power (10 to 90 MW) to the

EGAT

– MEA – Metropolitan Electricity Authority offtaking power from VSPP located in Bangkok and vicinity provinces

– PEA – Provincial Electricity Authority, offtaking power from VSPP located outside Bangkok and vicinity provinces.

78

– 20-year alternative energy development plan (PDP 2010 Revision No. 3) (2010-2030) announced by Ministry of Energy̶ by 2030, renewable energy ≈14% (6% this year) of total

generation ̶ capacity of ≈55,000 MW̶ steady revenue stream over life of PPA (renewable every

5 years)

Why renewable energy projects?

79

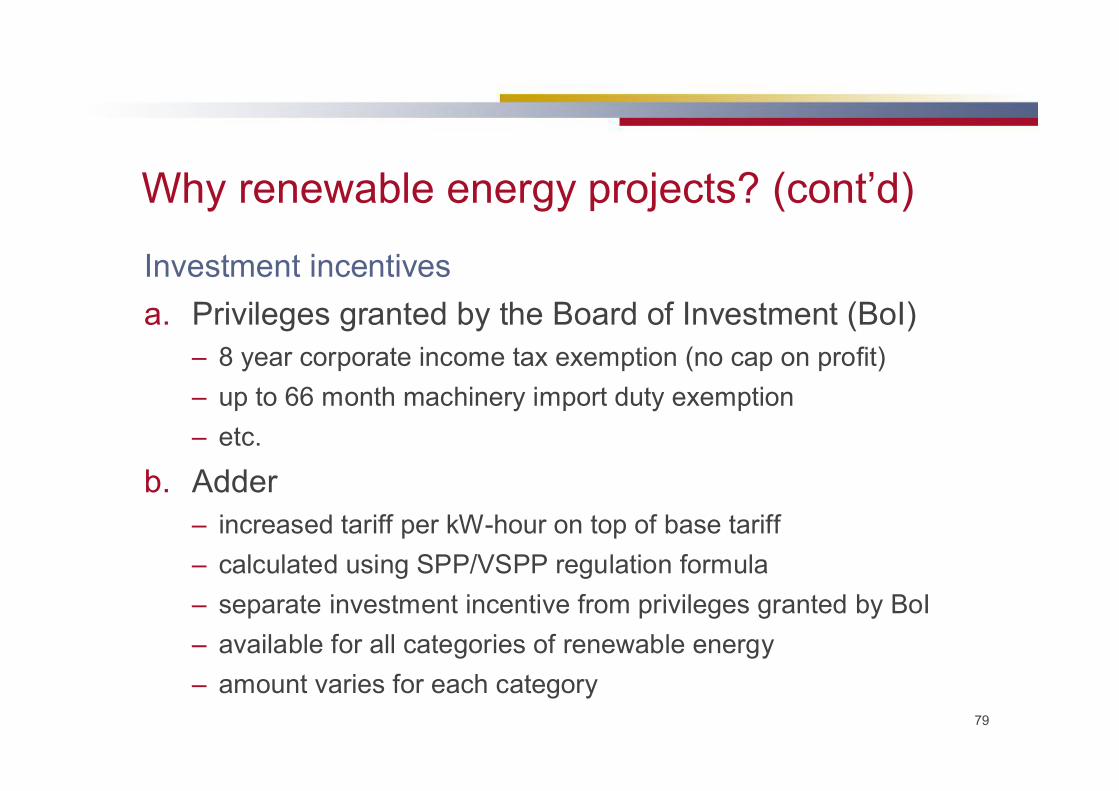

Investment incentivesa. Privileges granted by the Board of Investment (BoI)

– 8 year corporate income tax exemption (no cap on profit)– up to 66 month machinery import duty exemption– etc.

b. Adder– increased tariff per kW-hour on top of base tariff– calculated using SPP/VSPP regulation formula– separate investment incentive from privileges granted by BoI– available for all categories of renewable energy– amount varies for each category

Why renewable energy projects? (cont’d)

80

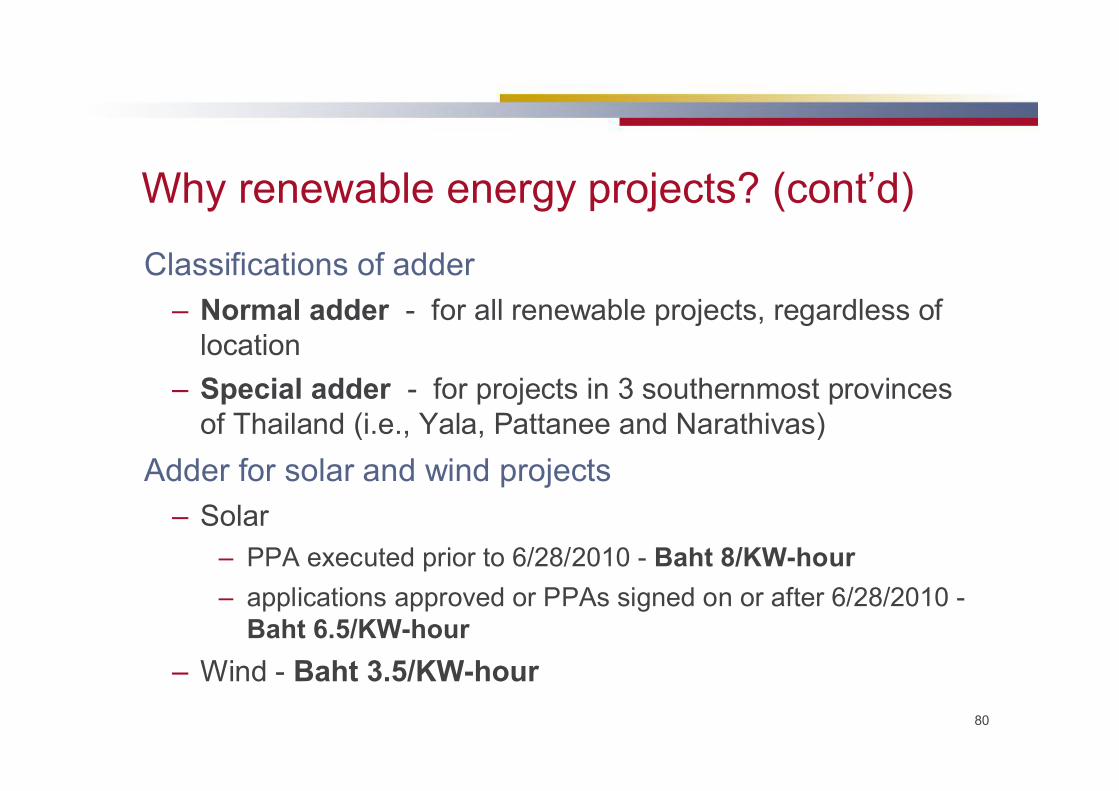

Classifications of adder– Normal adder - for all renewable projects, regardless of

location– Special adder - for projects in 3 southernmost provinces

of Thailand (i.e., Yala, Pattanee and Narathivas)Adder for solar and wind projects

– Solar – PPA executed prior to 6/28/2010 - Baht 8/KW-hour– applications approved or PPAs signed on or after 6/28/2010 -

Baht 6.5/KW-hour– Wind - Baht 3.5/KW-hour

Why renewable energy projects? (cont’d)

81

– Adder availability period– Wind and solar projects : 10 years from COD– Other projects : 7 years from COD

Why renewable energy projects? (cont’d)

Fuel

Previous Adder(Baht/ kWh)

Present Adder(Baht/ kWh)

Special Adder

for the 3 Southernmost

Provinces (Baht/kWh)

Total Adder

for the 3 Southernmost

Provinces (Baht/kWh)

Special Adder for Projects

Replacing PEA Diesel Power

Plants (Baht/kWh)

Total Adder for Projects

Replacing PEA Diesel Power Plants (Baht/

kWh)

Termfrom COD

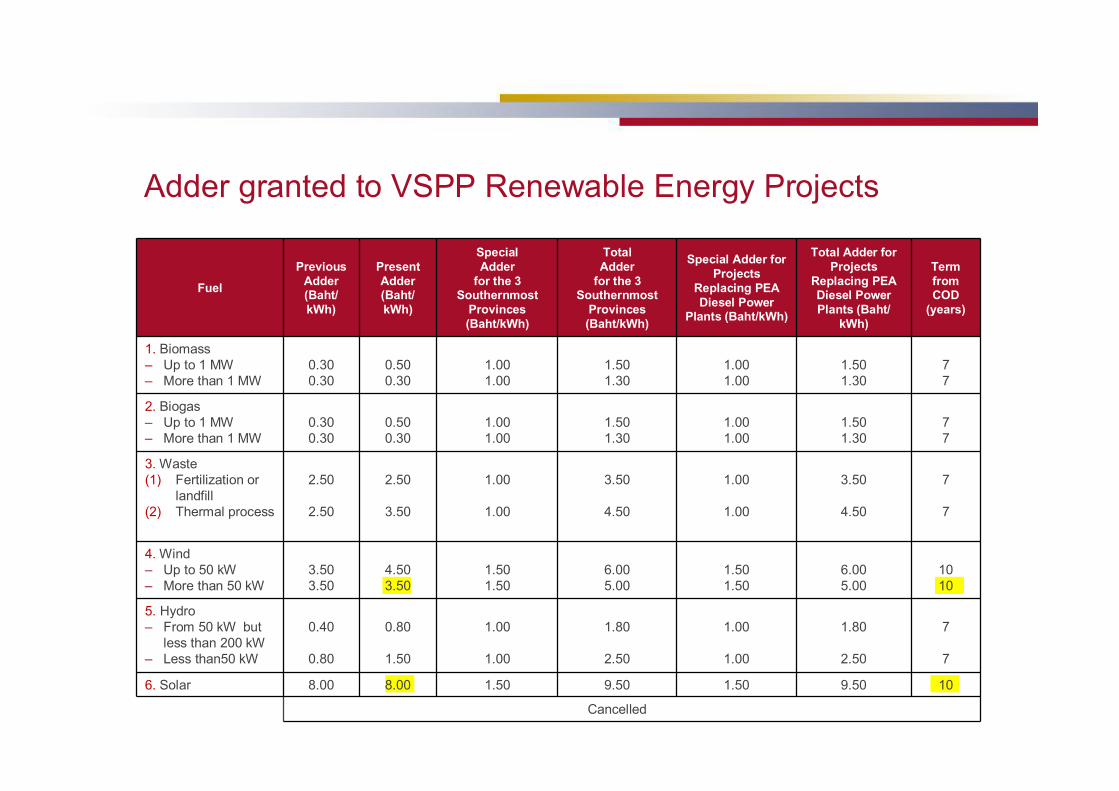

(years)

1. Biomass– Up to 1 MW– More than 1 MW

0.300.30

0.500.30

1.001.00

1.501.30

1.001.00

1.501.30

77

2. Biogas– Up to 1 MW– More than 1 MW

0.300.30

0.500.30

1.001.00

1.501.30

1.001.00

1.501.30

77

3. Waste(1) Fertilization or

landfill(2) Thermal process

2.50

2.50

2.50

3.50

1.00

1.00

3.50

4.50

1.00

1.00

3.50

4.50

7

7

4. Wind– Up to 50 kW– More than 50 kW

3.503.50

4.503.50

1.501.50

6.005.00

1.501.50

6.005.00

1010

5. Hydro– From 50 kW but

less than 200 kW– Less than50 kW

0.40

0.80

0.80

1.50

1.00

1.00

1.80

2.50

1.00

1.00

1.80

2.50

7

7

6. Solar 8.00 8.00 1.50 9.50 1.50 9.50 10

Cancelled

Adder granted to VSPP Renewable Energy Projects

83

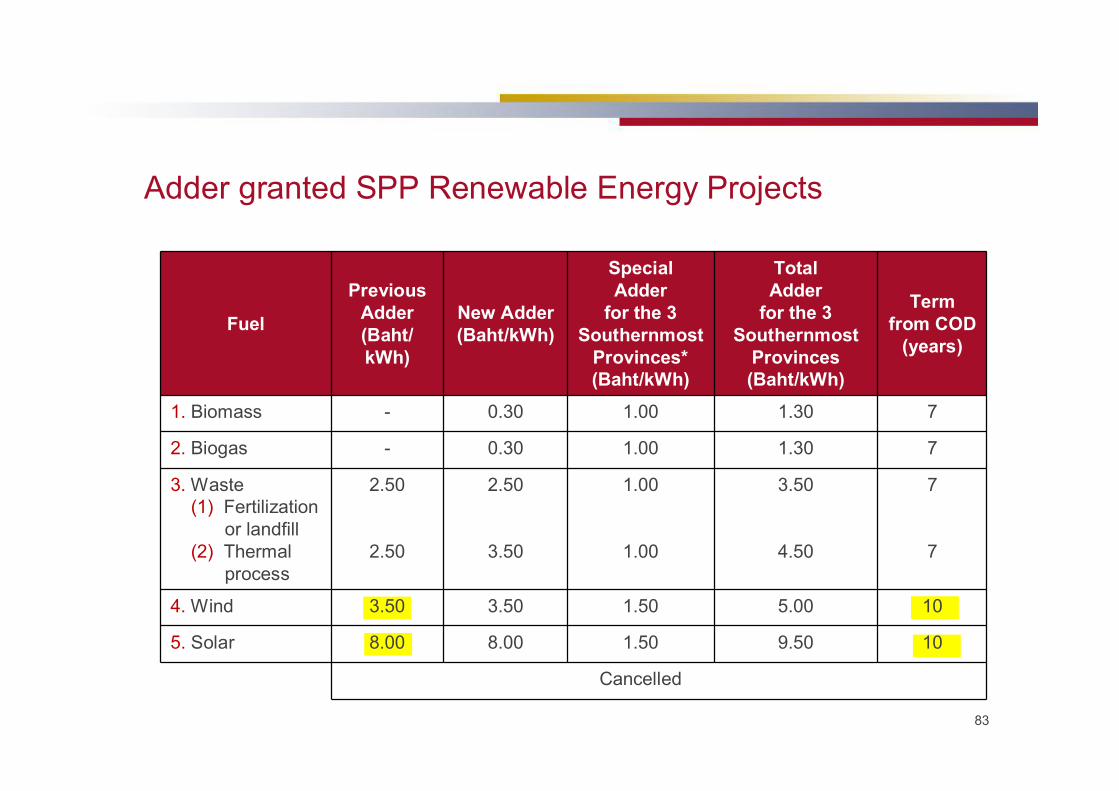

Adder granted SPP Renewable Energy Projects

Fuel

Previous Adder(Baht/kWh)

New Adder(Baht/kWh)

Special Adder

for the 3 Southernmost

Provinces* (Baht/kWh)

Total Adder

for the 3 Southernmost

Provinces (Baht/kWh)

Termfrom COD

(years)

1. Biomass - 0.30 1.00 1.30 7

2. Biogas - 0.30 1.00 1.30 7

3. Waste(1) Fertilization

or landfill(2) Thermal

process

2.50

2.50

2.50

3.50

1.00

1.00

3.50

4.50

7

7

4. Wind 3.50 3.50 1.50 5.00 10

5. Solar 8.00 8.00 1.50 9.50 10

Cancelled

84

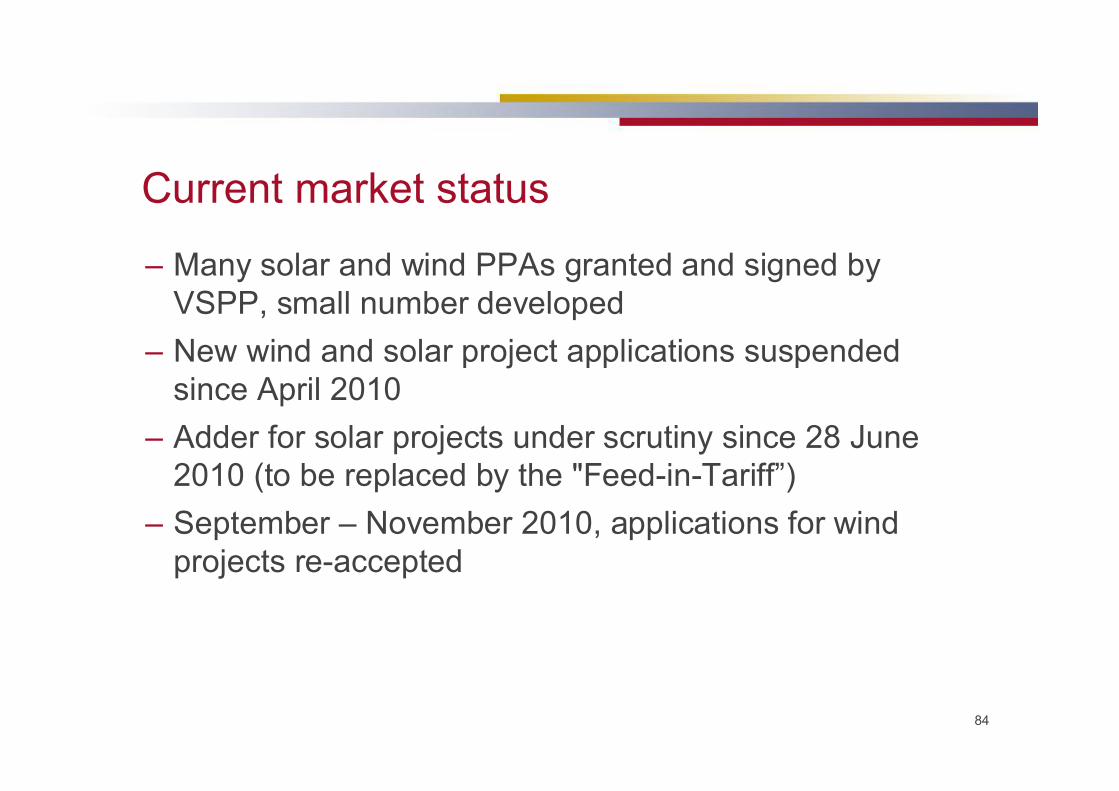

– Many solar and wind PPAs granted and signed by VSPP, small number developed

– New wind and solar project applications suspended since April 2010

– Adder for solar projects under scrutiny since 28 June 2010 (to be replaced by the "Feed-in-Tariff”)

– September – November 2010, applications for wind projects re-accepted

Current market status

85

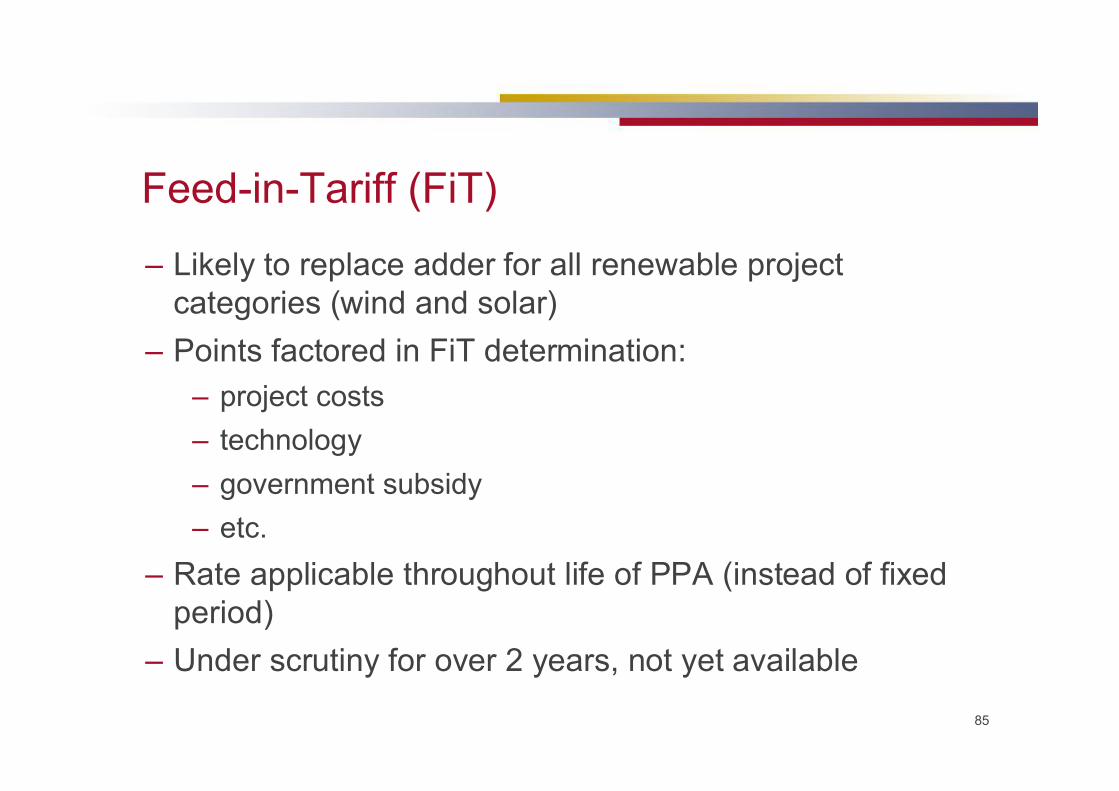

– Likely to replace adder for all renewable project categories (wind and solar)

– Points factored in FiT determination:– project costs – technology– government subsidy– etc.

– Rate applicable throughout life of PPA (instead of fixed period)

– Under scrutiny for over 2 years, not yet available

Feed-in-Tariff (FiT)

101

Investment opportunities

86

Investment opportunities

– Renewable energy not restricted business under Thai Foreign Business Act

– SPV carrying out renewable energy business can have a foreign majority-owned shareholding or 100% foreign owned structure

– Land can be acquired if the SPV has obtained BoI privileges

87

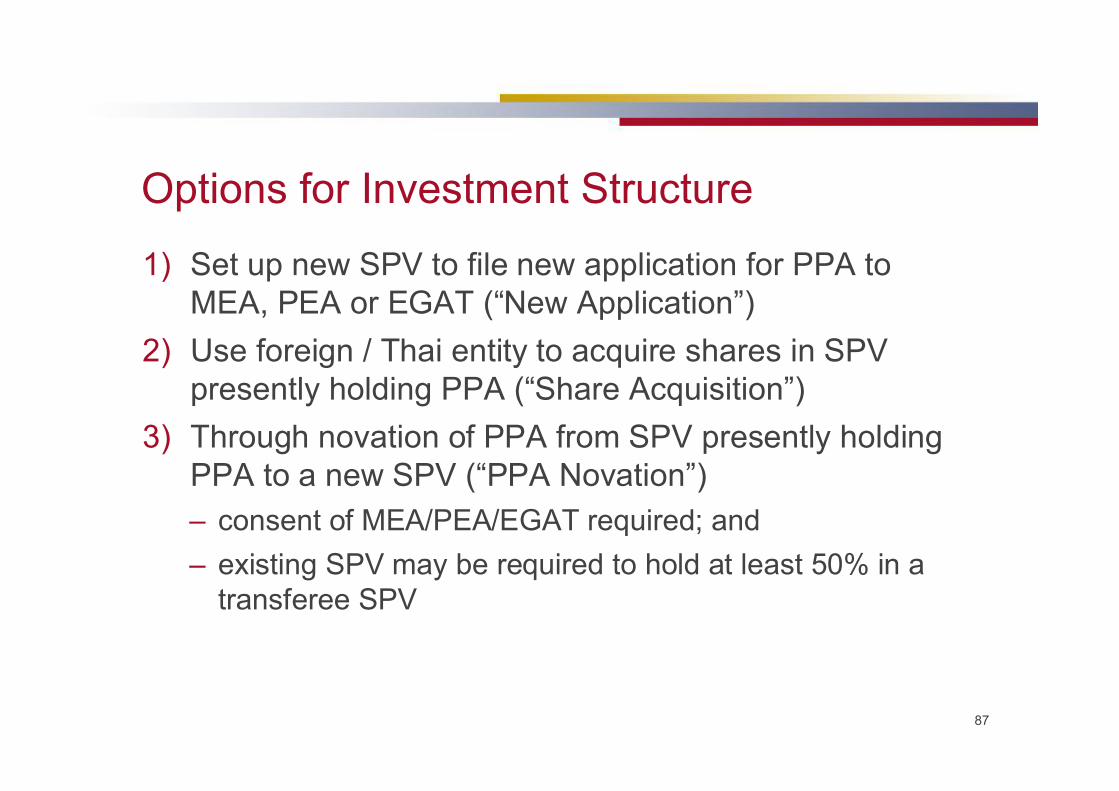

1) Set up new SPV to file new application for PPA to MEA, PEA or EGAT (“New Application”)

2) Use foreign / Thai entity to acquire shares in SPV presently holding PPA (“Share Acquisition”)

3) Through novation of PPA from SPV presently holding PPA to a new SPV (“PPA Novation”)– consent of MEA/PEA/EGAT required; and– existing SPV may be required to hold at least 50% in a

transferee SPV

Options for Investment Structure

88

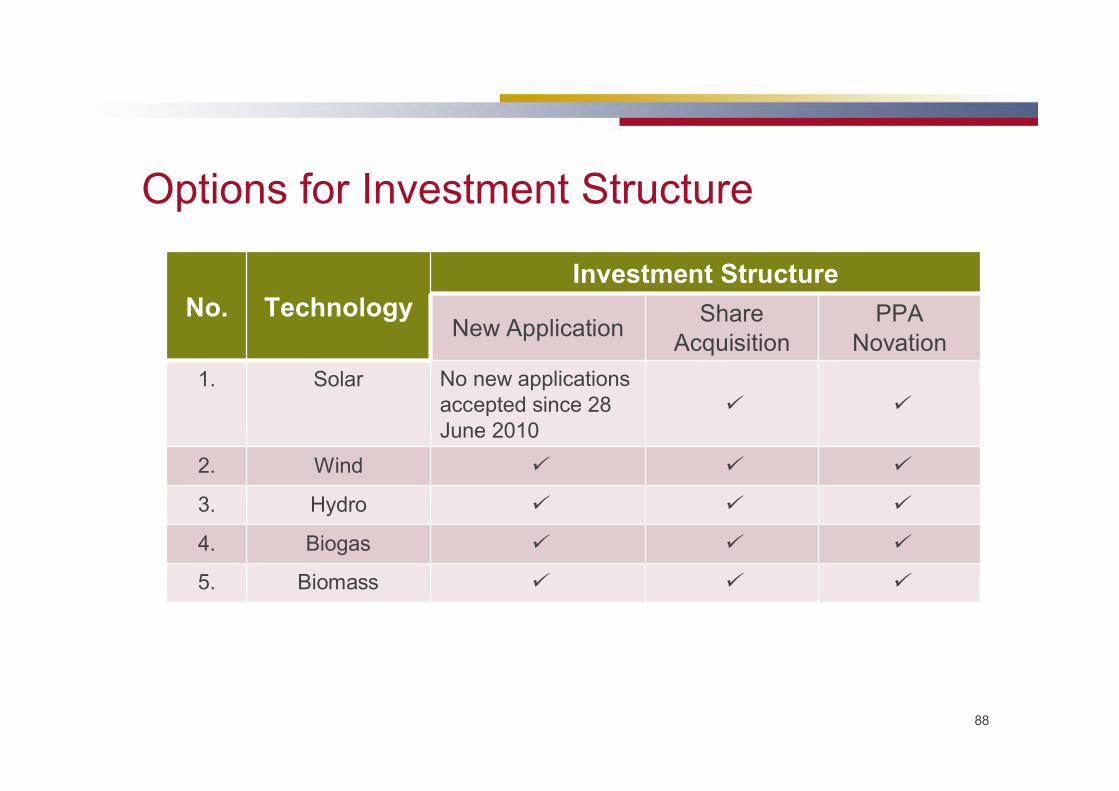

Options for Investment Structure

No. TechnologyInvestment Structure

New Application Share Acquisition

PPA Novation

1. Solar No new applications accepted since 28 June 2010

ü ü

2. Wind ü ü ü

3. Hydro ü ü ü

4. Biogas ü ü ü

5. Biomass ü ü ü

89

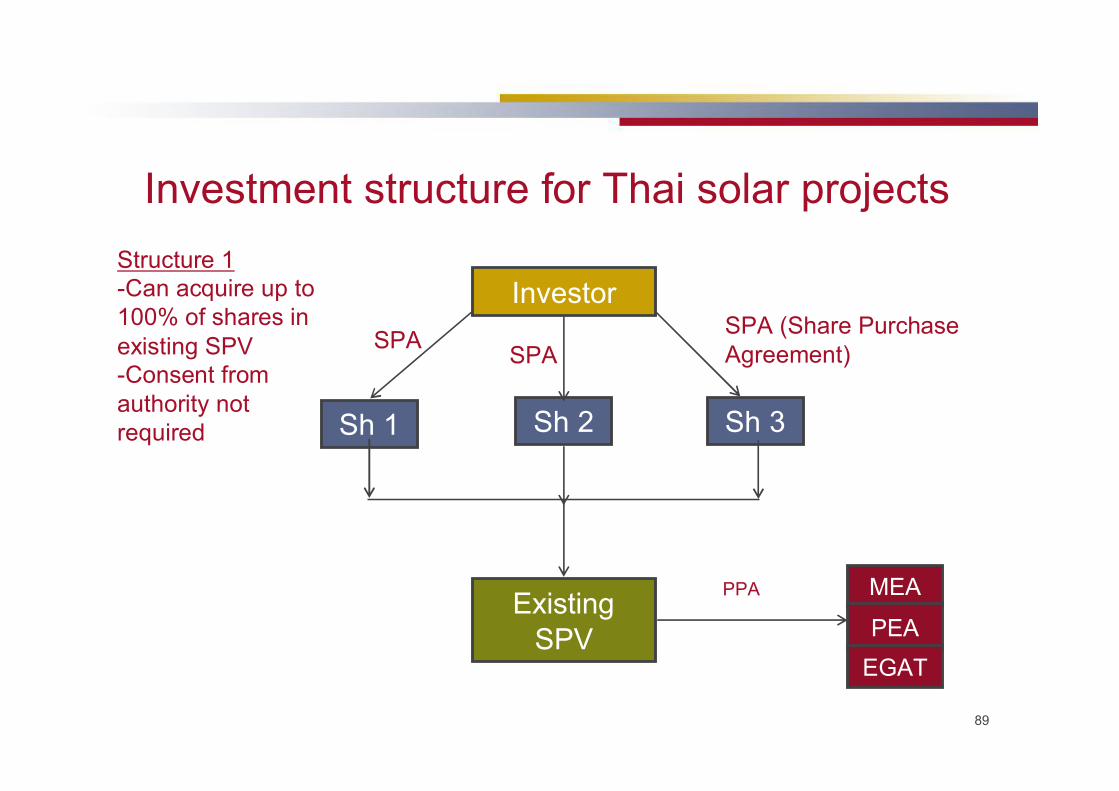

Investment structure for Thai solar projectsStructure 1-Can acquire up to 100% of shares in existing SPV-Consent from authority not required

Investor

Sh 1 Sh 2 Sh 3

Existing SPV

MEA

PEAEGAT

SPA SPASPA (Share Purchase Agreement)

PPA

90

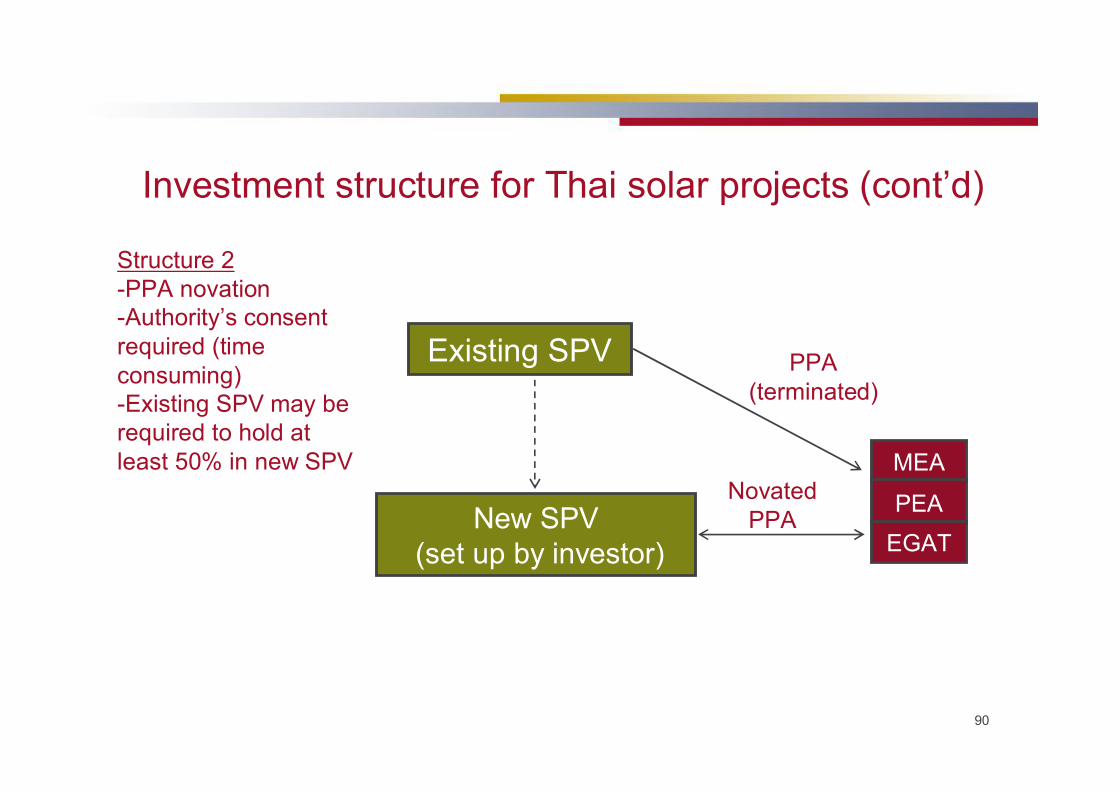

Structure 2-PPA novation -Authority’s consent required (time consuming)-Existing SPV may be required to hold at least 50% in new SPV

Existing SPV

New SPV(set up by investor)

PPA (terminated)

Novated PPA

Investment structure for Thai solar projects (cont’d)

MEA

PEAEGAT

101

Key market and investment issues

91

Key market and investment issuesBiogas– Relatively small project (max. 2 MW), but facing the same

difficulties as larger renewable projects doBiomass– Extremely difficult to find and secure reliable (both quality

and quantity) feedstock suppliers from local sources for steady power generation

– Feedstock suppliers are poor local farmers– Professional contracted farming may be a solution

92

– Only Irrigation Department may build and operate a dam– Permission to use, build and operate dam hydro power

facilities may fall within Private-Public Participation Act (PPA Act)

– final approval from cabinet (time consuming and unpredictable process)

Hydro

93

– Each PPA normally granted under SPP program (exceeding 10 MW)

– Most good wind speed areas - north eastern and southern parts of Thailand

– Increased costs - difficult to find target with good project site close to the grid (delivery point)

– Commercial operation date under PPA may be too short for project development and completion

Wind

94

– Good areas for wind farm mostly in government controlled areas

– e.g. reserved forest area controlled by Forestry Department, Treasury Department, etc.

– Permission to use reserved area land for wind farm project may fall within PPA Act

– final approval from cabinet (time consuming and unpredictable process)

Wind (cont’d)

95

– Scheduled commercial operation date under each PPA may be too short for project development and completion

– SPV holding PPA may also carry out other business– Legal due diligence is a key to investment decision

Wind (cont’d)

96

– Each PPA normally granted under VSPP program (up to 10 MW)

– Aggregate MW under several PPAs may be too small for investment size

– Difficult to find target with good project site close to the grid (delivery point)

– SPV holding PPA may also carry out other business– Commercial operation date under each PPA may be too

short for project development and completion– Legal due diligence is key to investment decision

Solar

97

Q & A

Thank you

© 2012 Baker & McKenzie. All rights reserved.Baker & McKenzie International is a Swiss Verein with member law firms around the world. In accordance with the common terminology used in professional service organizations, reference to a “partner” means a person who is a partner, or equivalent, in such a law firm. Similarly, reference to an “office” means an office of any such law firm.

Top Related