Languages

Pages

Legal

66

Accounting System and Financial Reporting of NGOs: Case Study of a BRAC’s Project

Munima Siddika1 and Mohammad Sarwar Jahan Rekabder2

Abstract: In the absence of specific accounting and financial reporting standards and

diverse interpretation of certain terms under the laws of the land, it has become a very

difficult task to follow a standardized procedure in generation and presentation of

accounting and financial information of NGOs. The practices followed by NGOs in

Bangladesh are varied and diverse and there by preparation of financial statements are

incomparable and difficult for uses to understand. The paper tries to demonstrate

financial reporting and accounting system of a BRAC’s project and provide a guideline

for constituting suitable financial reporting and accounting systems for NGOs. The

article elaborates on basis of preparation of financial statements and reporting

procedure and then followed by accounting systems of regional office and head office of

that project. The final part of the article discuses issues relating to financial report and

financial transparency of the project.

Keywords: BRAC, NGO, Accounting System, Financial Statements, Financial Report.

1 Munima Siddika, Lecturer, Faculty of Business and Economics, Daffodil International University, 102 Sukrabad, Mirpur Road, Dhaka-1207, Bangladesh.

2 Mohammad Sarwar Jahan Rekabder, Lecturer, Faculty of Business and Social Studies, State University of Bangladesh,

67

INTRODUCTION

NGOs have become major players in the field of international and national development.

Since the mid-1970s, the NGO sector in both developed and developing countries has

experienced exponential growth. From 1990 to 2000 total development aid disbursed by

international NGOs increased ten-fold. In 1992 international NGOs channeled over $7.6

billion of aid to developing countries. (Retrieved from: http://wbln0018.worldbank.org)

on 25th February, 2006. Bangladesh has largely failed to assist the poor or reduce poverty

because of limited resources and planning, while NGOs have grown dramatically, but it

ostensibly fails to fill this gap. There are more and bigger NGOs here than in any other

country of equivalent size. The Association of Development Agencies in Bangladesh

(ADAB) had a total membership of 886 NGOs/PVDOs (Private Voluntary Development

Organizations) in December 1997, of which 231 were central and 655 chapter (local)

members (ADAB, 1998). The ADAB Directory lists 1007 NGOs, including 376 non-

member NGOs. The NGO Affairs Bureau of the Government of Bangladesh (GOB),

which has to approve all foreign grants to NGOs working in Bangladesh, released grants

worth about $250 million US dollars in FY 1996-97 to 1,132 NGOs, of which 997 are

local and 135 are foreign (NGO Affairs Bureau, 1998). NGOs have mainly functioned to

service the needs of the landless, usually assisted by foreign donor funding as a

counterpoint to the state's efforts (Lewis, 1993). Besides all these advancement the field

of NGO, Financial Reporting process and application of accounting is disgraceful. NGOs

in Bangladesh have increasingly become subject to question and criticism from the

government, political parties, intellectuals and the public in genus for misuse of funds,

gender discrimination, and nepotism. Absence of proper guidelines in preparing financial

statements and reports makes it more complex. The government of Bangladesh doesn’t

have any unique rules for preparing the financial reports. BRAC is one of the largest

NGOs in Bangladesh. It has more than hundreds projects. BRAC maintains books of

accounts and other record on a program or project basis. And its reporting process is

transparent and one of the most structured system in Bangladesh. This report we will

discuss about the financial reporting and Accounting system of BRAC Education

Program (BEP). BEP begun experimentally in 1985, it is an independent education

68

program organized and managed by BRAC with the approval of NGO Bureau of the

Government of Bangladesh. The analysis and discussion of reporting systems of BRAC

Education Program will give guidance and support to other NGOs about the generation of

accounting systems and reporting procedure, and to maintain a transparent system of

utilizing grants.

2. LITERATURE REVIEW

International Accounting Standards (IAS) doesn’t have specific guidelines for NGOs.

Regarding applicability of Accounting Standards to NGOs, the Accounting Standards

Board (ASB) has given an opinion in September 1995. “The Institute will issue

Accounting Standards for use in the presentation of the general purpose financial

statements issued to the public by such commercial, industrial or business enterprises as

may be specified by the Institute from time to time and subject to the attest function of its

members” It is clear from the above that the Accounting Standards are applicable to

NGOs whose some, or more, of the activities are commercial or business in nature.

However, it is very difficult to determine what the exact meaning of commercial is or

business activities with reference to NGOs. NGOs are not meant for earning profit out of

their activities. There are some NGO related laws and regulations in Bangladesh. While

registration is not mandatory for any NGOs, 2 types of legal frame work govern NGOs of

Bangladesh.

a. Laws for Incorporation Acts: There are four such Acts in Bangladesh: the Societies

Registration Act, 1861; the Trust ACT, 1882; Co-operative Societies Act, 1952

and the Companies Act of 1994.

b. Three laws and ordinances for regulation the relationship of such associations with

the Government: The Voluntary Social Welfare Agencies (Regulation and Control)

Ordinance, 1961; the Foreign Donation (Voluntary Activities) Regulation

Ordinance, 1982. This Forms the basis for registration with the NGO Affairs

Bureau (NGOAB); the Foreign Contribution (Regulation Ordinance 1982)

Government organization, The NGO affairs Bureau, has been carrying out NGOs

registration and processing of funds. NGO Bureau examines and evaluates reports

69

submitted by NGOs and the checking of their income and expenditure accounts. The

inspection and audit of accounts kept by NGOs are under section 4 and 5 of the Foreign

Donation (Voluntary Activities) Regulation Ordinance 1978. As per Bangladesh

Chartered Accountants Order 1973, the NGO Affairs Bureau will prepare a list of

Bangladesh Chartered Accountants for annual audit of NGO accountants. The NGOs

prepare their annual program report within three months of ending the financial year and

send copies to NGOAB’s Economic Relation Divisions, Concern Ministries, Concerned

Deputy Commissioner and Bangladesh Bank, the following information should be

incorporated with it: (a) project should be shown separately in the annual report. The

main theme of project based report should expenses against actual target achieved in

detail on the proposal, expenses against the Thana & Districts in the project should also

be shown clearly (b) full list of permanent or liquid assets with vehicles of the

organization (c) Sources of organizations own income & expenditure (d) Details of

organization’s foreign travels by its officers & employees (f) Details of organization’s

revolving loan fund investment described by sector (f) Details of fund for projects

implemented with fund generated through agreement with Government’s different

ministries and directors and other sources (g) Details of persons employed by the

organization (with monthly salaries of Taka 5,000 and above or one time Taka 10,000 or

above, their names, designation, qualifications, age, total salaries, allowance and length

of services with the organization) should be attached.

In preservation of foreign aid accounts NGO Bureau have guidelines for NGOs according

to The Foreign Donation (Voluntary Activities) Regulation Ordinance, 1982: (a) all

foreign funds or foreign Currency remitted but received in Bangladeshi Taka (Currency)

should be received through only one bank account by each NGO. (b) Bangladesh Bank

on receipt of six monthly foreign currency accounts received in July and January each

year from NGOs will send it to NGO Affairs Bureau and Economic Relations Division.

(c) All expense vouchers will be preserved for 5 years at head office of the NGO. At the

field level, they will preserve copy of expense vouchers at their office for 5 years. (d)

NGO will preserve books of accounts: (a) In the case of foreign aid material Form, FD-5

(b) In the case of foreign funds through double entry system Cash Book.

70

All documents maintained in (d) should be preserved on an annual basis-one from 1st July

to 31st December and the other 1st January to 30th June. The World Bank put emphasis on

the reporting practice of NGOs but the existing laws and regulations has minimal

emphasis on the reporting of the NGOs. It would be effective if there could be a simple

and single form of reporting for all NGOs and for all of their activities. But the activities

of the NGOs’ are too numerous and diverse and the legal interests of the government and

the public are too diverse to make this possible. BRAC has consistently maintained high

levels of transparency in all its operations; its extraordinary effort towards financial

transparency was recognized in 2005 when it won the CGAP (Consultative Group to

Group to Group to Assist the Poor). BRAC follows and prepare the financial reports on

the basis of GAAP and International Accounting Standards (IAS).

METHODOLOGY

As research approach case study is taken to make an empirical inquiry that investigates a

phenomenon within its real life context. Here the accounting system of BRAC Education

Program is described in a framework within an organizational environment. The events

are described in some detail with the main and subsidiary points highlighted. BRAC is a

gigantic organization it maintains and amasses lots of information. The accounting

system is identical in every outlet and for every project. The information was taken from

the Head office (BRAC Center) and from one Regional office (Dhaka Urban Samoli) by

interviewing the staff and management. The information used in this case study is both

primary (collected from field) and secondary (collected from annual report, progress

report, Code of conduct, statements, and written principles)

FINANCIAL ACCOUNTING SYSTEM OF BRAC EDUCATION SYSTEM:

BEP has some principles; these principles guide the Project behavior and help in the

development of policies and procedures for financial activities. The principles are:

stewardship or safekeeping of the project resources, accountability to explain how funds

71

are being used, transparency to ensure financial information is recorded accurately and

presented clearly; consistency is maintained over the years so that comparisons can be

made; non-deficit financing, it represents sufficient funding source, standard

documentation guides the system of maintaining financial records and documentation

according to internationally accepted accounting standards and principles. The

procedures and the implications of the accounting standards followed by BRAC

Education Program for reporting; are adopted depending on the expertise and resources

available; the volume and type of transactions; reporting requirements of managers; and

obligations to donors.

Basis of Preparation of Financial Statements of BEP

According to the IAS-1, non-profit, government and other public sector enterprises

seeking to apply this standard may need to amend the description used for certain line

items in the financial statements and for the financial statements themselves. BRAC

prepare the BEP’s financial statements under the historical cost convention on a going

concern basis. BEP also follows the accrual basis of accounting or a modified form there

of key income and expenditure items. The head office or the main center records all

treasury, investment and management functions. The accounting records and financial

statements are maintained and presented in accordance with the principles of fund

accounting. Funds are established and maintained the under fund accounting principles.

Donors’ Grants

BRAC preserve and accumulate foreign grants according to Foreign Donations

(Voluntary Activities) Regulation Ordinance, 1978. At present three practices are widely

followed by NGOs in recognition of grants: Grants recognized as income, grants

recognized as liabilities and grants recognized as income only to the extent of the

expenditure incurred (Anand Pagaria, 2006). BEP recognize grants as income when

conditions on which they depend have been met. If the grants are specified for the

funding of specific project, then income is recognized equal to expenditure incurred on

the project or program. For donors’ grants which involve funding fixed assets, income is

recognized as the amount equivalent to depreciation expenses charged on the fixed assets

72

concerned. All donors’ grants received are initially recorded at fair value as liabilities in

the “Grants Received in Advance Account”. For grants utilized to purchase fixed assets

are transferred to deferred income accounts. Donors’ grants received in-kind through the

provision of gift and/ or services, are also recorded in fair value. Income reorganization

of such grants follows that of cash based donor and any expenditure yet to be funded but

for which funding has been agreed at the end of any specific period is recognized as grant

receivable.

Revenue Recognition

According to ISA-18, revenue should be measured at fair value of consideration received

or receivable. NGOs don’t have revenues like the normal business organizations, they

recognize grants as revenues. BRAC maintains a bank account for foreign donors

(According to: Foreign Donations Regulation Ordinance, 1978 (30) under sub-rule (4) of

rule 4) and revenue is recognized as the interest accrued and as per IAS-18, interest

revenue is recognized on a time-proportion basis using the effective interest rate. All

other incomes are recognized when the right to receive such income has been reasonably

determined and all conditions precedent is satisfied.

Matching of Expenses

BEP’s program related expenses arise from goods and services being distributed to

beneficiaries in accordance with the program related objectives and activities. Head

office’s program related expenses are allocated to the program at approximately 7% of

their costs, most of the time these allocations are made with the consent of the donors.

Assets

IAS-1 standards requires certain disclosures on the on the financial statements.

Enterprises need to present current and non-current assets and liabilities on the face of the

balance sheet as separate classifications considering nature of operation of the

enterprises. When an enterprise chooses not to make this classification, assets and

liabilities should be presented broadly in order of their liquidation value. As BEP is a

project of BRAC, it presents the balance sheet according to its operational nature, and it

73

doesn’t classify its assets and liabilities as current and non-current assets. According to

IAS-16 and IAS-1, the NGO states its’ fixed assets at cost less accumulated depreciation,

depreciation is provided for on a straight line basis over the estimates useful life. Like the

profitable business organization, accounts receivables are stated at nominal value and

stated net provision for irrecoverable amounts.

Provisions for Liabilities

BEP’s Provisions for liabilities are recognized when there is a present obligation as a

result of a past event and it is probable that an overflow of resources embodying

economic benefit will be required to settle the obligation and a reliable estimate of the

amount can be made. Provisions are reviewed at each balance sheet date and adjusted to

reflect the current best estimate. If the effect of time value of money is material, the

amount of a provision is the present value of the expenditure expected to be required to

settle the obligations.

Taxation

Under the income Tax Ordinance 1984 (Amended),in addition to its commercial

activities, BEP is also subject to taxation on income derived from its other non

commercial activities unless they are tax exempt. The tax charge is in respect of taxable

income arising from Deferred taxation is provided for using the liability method, on all

temporary differences at the balance sheet date between the tax bases of assets and

liabilities and their carrying amounts for financial reporting purpose. Deferred taxation

benefits are only recognized when their recognition is probable.

Impairment of Assets

IAS-36 addresses mainly accounting for impairment of goodwill, intangible assets and

property plant and equipment. The standard includes requirements for identifying an

impaired asset, its recoverable amount, recognizing or revising any resulting impairment

loss and disclosing information on impairment losses or reversal of impairment loss. At

each balance sheet date, BEP carried out a review, on the carrying amount of assets to

determine whether there is any indication of impairment. If any such indication exists,

74

impairment is measures by comparing the carrying values of the assets with their

recoverable amounts.

Financial Instruments

According to IAS-32, BEP recognize and disclosure financial instruments in the balance

sheet when the NGO become a party to the contractual provisions of the instrument.

Receivables are carried at anticipated realizable values. Unlike the profitable organization

bad debts are written off when identified and an estimate is made, based on all

outstanding amounts of the balance sheet. BEP state the payables at cost which is the fair

value of the consideration to be paid in the future for goods and services received. Cash

and cash equivalents for the purpose of the statement of cash flows comprise cash and

bank balance, included in cash and bank balances, which are received through donors’

grants

ACCOUNTING SYSTEMS OF THE REGIONAL OFFICE

Traditionally, Accounting records fall into two main categories: Supporting Documents

and Books of Account. BEP keep files of the following original documents to support

every transaction taking place: Receipt or voucher for money received, receipt or voucher

for money paid out, invoices, certified and stamped as paid, paying-in vouchers for

money paid into the bank, bank statements, journal vouchers for adjustments and non-

cash transactions. BEP maintains several books of accounts as part of a full bookkeeping

system: General/Nominal Ledger, Journal or Day Book, Wages book, Assets Register

and Bank Reconciliations statements. The management information system of BEP

collects data from 565 area office then these are integrated under 139 regional offices and

then send it to head office for analysis. The accounting system of these regional offices is

well organized and supported by computer aided accounting software but we will discuss

the systems manually.

75

Charts of Accounts

The first step taken by BRAC is to choose an accounting software package which is clear

and concise and easy to operate and maintain the NGO accounting. The second step of

BRAC was to clarify purpose of organization and reflect that in a clear and concise chart

of accounts. It is important that a chart of accounts reflect all the major functions and

project operation of the organization in a concise and systematic manner (retrieved from:

http://www.global.net.pg/atprojects/manage.htm, retrieved on February 23, 2007). BRAC

has more than hundreds projects, it prepares charts of accounts and code them for

computer aided soft ware. The coding of the account head represents the specific project,

regional office, and lastly the respective income, expenditure, liabilities or assets.

Cash Book

Regional office maintains separate cash books according to IAS-7 for different area

office under it. The area office maintains petty cash books for the recording of cash. The

area office conveys all its accounts (mainly expenditure) at the end of the month to the

regional office. The regional office then prepare separate cash book for every area office.

The opening balances of these cash book represent the cash on hand of the area office.

All expenditure and revenue recorded in the cash book are supported by vouchers.

Ledger Book

The format and procedure of preparing the ledger is same as the normal business

organization. Different transactions of account heads are accumulated here. After

recording the transaction of the last date of the month, balance is drowned. As it is a

computerized system, data is typically entered into the system only once. Once the entry

has been approved by the user, the software includes the information in all reports in

which the relevant account number appears

Receipt and Expenditure Statement

The receipts and expenditure statement is one kind of trial balance which is prepared by

regional office, which include the balances of the ledger. In computer aided accounting

76

system the receipt and expenditure statement is automatically prepared when ledger is

prepared.

Head Office Current Account Breakup Statement

The regional office maintains and transfers a ledger account to HO it includes

transactions like Motorcycle loan, Bonus Provisions, Gratuity Provisions, Provident

Fund, Insurance provisions for the employees. The regional office also transfers a

Motorcycle Loan Schedule as motorcycle is considered as assets.

ACCOUNTING SYSTEMS of THE HEAD OFFICE

The head office transactions are same like the regional office. Most of the transactions

are recorded at cash and the accounts are automatically posted to Receipts and

Expenditure statement under different heads. Head office maintains two sets of ledger

accounts other then the normal account heads. These are “Field Area Current Account

breakup” to record transaction with the regional office and Head Office Current Account

Break up to maintain correlation with the Regional Offices’ breakups. It provides a

provision to reconcile and find out the accounts in transit.

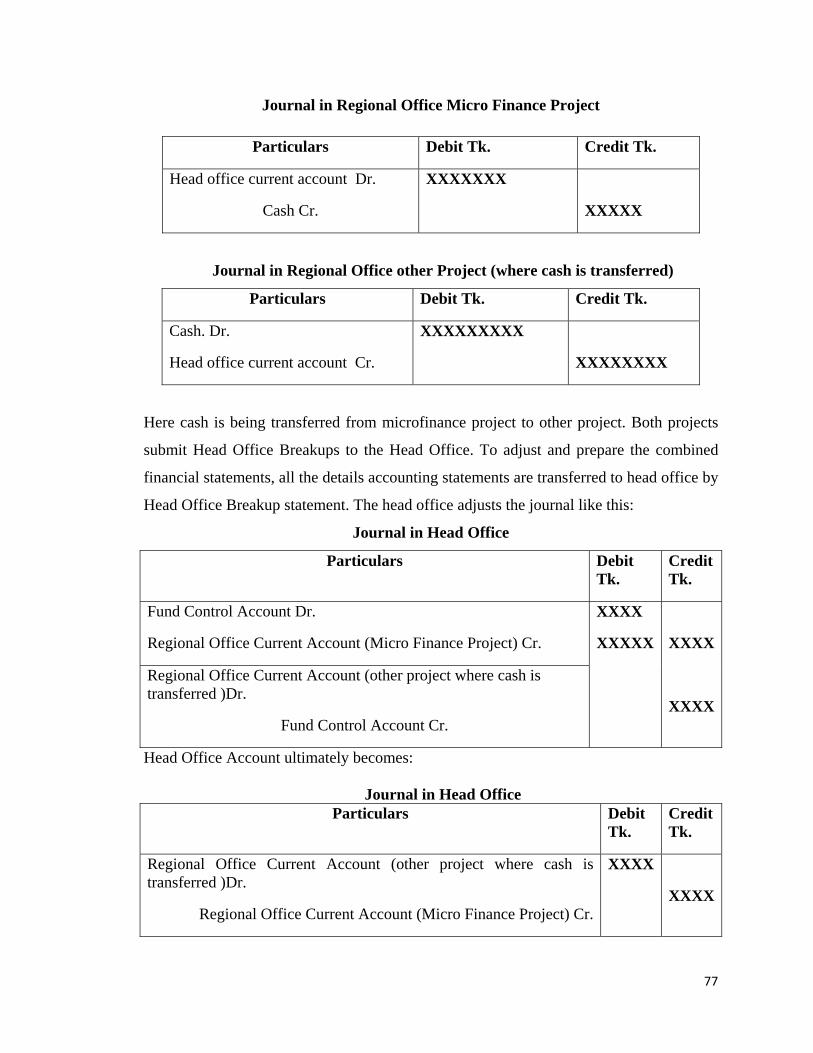

Fund Control

The income generating micro finance project transfer money to all projects and at the end

of every month and the money transferred is adjusted with Head Office Current Account

and it is done to avoid cash payment from the HO. The transactions are made by passing

journal entries “Fund Control Account” and it is shown on the Head Office Current

Account Break up Statement. In the field or regional office when micro finance project

transfer money to other project, then the journal is passed like this:

77

Journal in Regional Office Micro Finance Project

Particulars Debit Tk. Credit Tk.

Head office current account Dr.

Cash Cr.

XXXXXXX

XXXXX

Journal in Regional Office other Project (where cash is transferred)

Particulars Debit Tk. Credit Tk.

Cash. Dr.

Head office current account Cr.

XXXXXXXXX

XXXXXXXX

Here cash is being transferred from microfinance project to other project. Both projects

submit Head Office Breakups to the Head Office. To adjust and prepare the combined

financial statements, all the details accounting statements are transferred to head office by

Head Office Breakup statement. The head office adjusts the journal like this:

Journal in Head Office

Particulars Debit Tk.

Credit Tk.

Fund Control Account Dr.

Regional Office Current Account (Micro Finance Project) Cr.

XXXX

XXXXX

XXXX

XXXX

Regional Office Current Account (other project where cash is transferred )Dr.

Fund Control Account Cr.

Head Office Account ultimately becomes:

Journal in Head Office Particulars Debit

Tk. Credit Tk.

Regional Office Current Account (other project where cash is transferred )Dr.

Regional Office Current Account (Micro Finance Project) Cr.

XXXX

XXXX

78

The detailed accounts accumulated under Receipt and Expenditure Statement and Head

Office Current Account Breakup Statement prepared in the Regional Offices are monthly

transferred to the Head Office. The accounting information collected by auto taker (a

computer supported device) is then automatically posted to ledger account maintained by

the head office. Then finally management prepares the financial statements, which

includes Balance Sheet, the Statement of Receipts and Payments, Statement of Changes

in Net Assets and Statement of Cash Flows.

7. REPORTING OF BEP

BRAC submit audit reports for all projects, along with FD-4 certified by the auditors, to

the NGO Affair Bureau and to Prime Minister’s Office.

7.1 Reporting for the BOAD

BEP’s reporting for the Board is done quarterly (or as required). This reporting includes a

Balance Sheet and a Statement of Receipts and Payments. This entail accounting for all

funds (i.e.: including USD funds). A uniform and consistent format is used for reporting

to the Board. This is also the report that is provided to auditors and used in the annual

report.

7.2 Reporting to the Management

BEP’s prepares management reports monthly, at the end of every quarter or as required.

There are different kinds of reports used by managers of BEP to take decisions: the

Budget Compared to Actual Performance Report, the narrative progress Report

(represents the achievements and impact of the project on the beneficiaries), the internal

financial report (prepared for 18 months to analysis cost, expenditure and their change),

quarterly cash flow projections report (to analysis exchange gains and fund deficits),

monitoring report (prepared by the monitoring team of 14members for every unit of the

NGO, which lists 20 issues need to be followed up).

7.3 Reporting for donors

79

Donors have their own reporting requirements and specifications and an NGO should

attempt to meet these as much as possible. Conversely, if donors are amenable, a generic

format may be agreeable. Donor reports are submitted no more than one month after the

close of the accounting period being reported upon. A donor tracking schedule is set up to

monitor due dates and for work planning purposes.

8. FINDINGS AND RECOMMENDATIONS:

The accounting system of BRAC Education Program is well planned and contemporary

and it is highly eulogize by the donors. It assists the internal control, cash control, internal

auditing process, budget formulation and execution, facilities or property management,

financial operations and analysis, grants management and information resources

management. But there are some weaknesses in this financial Accounting system. Like:

1. The project grassroots links are not efficient enough so the generation of

information in that level is weak and some times not supported by documents

2. The filed based development expertise some times fails to develop innovative

measures to support modern financial Management

3. The project doesn’t give more emphasis on long-term commitment and

sustainability; which could assist the progress and accountability of the project.

4. The cost effectiveness of the project is not used uniformly in every outlets

5. For generation of accounting information and reporting the project authority don’t

have modern process oriented approach and they failed to increase institutional

capacity.

In order to make the project accounting process modern some recommendations could be

considered: The project could hire more expertise and modern management technique; it

could be more participative and transparent; the information could be modernized by use

of internal network and of process oriented approach and value based management

approach could make the accounting process efficient. BRAC Education Program is one

of the largest projects in Bangladesh which is financed by the foreign donors; the

80

accounting system of this project is well organized and transparent. The processes of

presenting the financial statements are unique and very systematic. BEP after all these

limitations; could give the other NGOs some guidelines for preparing and installing

accounting systems, making assumptions about accounting principles and lastly but not

the list to prepare and present financial statements and submit financial reports.

8. REFERENCES

Ananda Pagaria. CA. 2006. NGO’s-Accounting and Legal Intricacies, The Chartered Accountant, June

2006: 1716-1723.

ADAB. (1998). Directory of PVD0s1NGD0s in Bangladesh (Ready Reference). Dhaka: ADAB.

Ahmad Mokbul Morshed. 2005. “The State, Laws and Non-Governmental Organizations (NGOs) in

Bangladesh”. International Journal of Not-for-Profit Law. Vol. 3. Issue. 3

BBS. (1998). Statistical Pocketbook of Bangladesh. Dhaka: BBS

Bird, P., Morgan-Jones, P. (1981), Financial Reporting by Charities, Institute of Chartered Accountants

in England and Wales, London.

Charities Aid Foundation (CAF) (1989), Charity Trends 11th Edition, Charities Aid Foundation,

Tonbridge

Ebdon, R. (1995). "NGO Expansion and The Fight to Reach The Poor: Gender Implications of NGO

Scaling-up in Bangladesh". IDS Bulletin. Vol. 26. No. 3. pp. 4955.

Hashemi, S. M. 1995. "NGO Accountability in Bangladesh: Beneficiaries, Donors and State" in Edwards,

M. and Hulme, D. (eds.) Non-governmental Organizations: Performance and Accountability Beyond the

Magic Bullet. London: Earthscan Publications.

http://www.ngoregnet.org/contact_us.asp

http://www.aidsalliance.org/sw17688.asp#nav-tools#nav-tools

81

http://www.oneworldtrust.org/?display=ngoinitiatives&text=1

http://www.gdrc.org/ngo/financial-mgmt.html

http://www.ngomanager.org/dcd/Topsites/

Lewis, D. J. 1993. "NGO-Government Interaction in Bangladesh" in Farrington, J. and Lewis, D. J.

(eds.) Non-Governmental Organizations’ and the State in Asia: Rethinking Roles in Sustainable

Agricultural Development. London: Routledge.

Montgomery, R. et al. (1996). "Credit for The Poor in Bangladesh: The BRAC Rural Development

Programme and the Government Thana Resource Development and Employment Programme" in

Hulme, D. and Mosley, P. (eds.) (1996). Finance Against Poverty. Vol. 2. London: Routledge.

NGO Affairs Bureau. 1998. Flow of Foreign Grant Fund Through NGO Affairs Bureau at a Glance.

Dhaka: NGO Affairs Bureau, PM's Office/GOB.

Report of the NAB for the Prime Minister. "There are several complaints of irregularity and corruption

against the NGOs", Bhorer Kagoj. 29 July, 1992 (Daily Newspaper in Bangla).

Reza, H. (1992). "Main report, NGO: New Challenge for the State and Government", Kagoj. 31 August,

1992 (Weekly Magazine in Bangla).

Salamon, L. M. and Anheier, H. K. (1997). "Toward a Common Definition" in Salamon, L. M. and

Anheler, H. K. (eds.). Defining The Nonprofit Sector A Crossnational Analysis. Manchester: Manchester

University Press.

Task-Force Report. (1992). Report of the Task-Forces on Bangladesh Development Strategies for the

1990s: Managing the Development Process. Vol. I & 2, Dhaka: University Press Limited.

White, S. (1999). "NGOs, Civil Society, and the State in Bangladesh: The Politics of Representing The

Poor". Development and Change. Vol. 30. pp. 307-326.

82

Wood, G. D. (1997). "States Without Citizens: The Problem of the Franchise State" in Edwards, M. and

Hulme, D. (eds.). NGOs, States and Donors: Too Close for Comfort? London: Macmillan

World Bank. (1996). the World Bank's Partnership with Nongovernmental Organizations. Washington

D. C: Participation and NGO Group, Poverty and Social Policy Department/the World Bank.

List of Government Ordinances/Rules/Working Procedures: (i) The Foreign Donations (Voluntary

Activities) Regulation Ordinance 1978: Ordinance No. XLVI of 1978.

(ii) The Foreign Donations (Voluntary Activities) Regulation Rules, 1978: No. S.R.O. 329-1/78.

(iii) The Foreign Contributions (Regulation) Ordinance, 1982. Ordinance No. XXXI of 1982.

(iv) Working Procedure of Foreign assisted Bangladeshi Non-Government Voluntary Organization

(NGOs) A Circular: 22.43.3.1.0.46.93-478, dated. 27-07-1993.

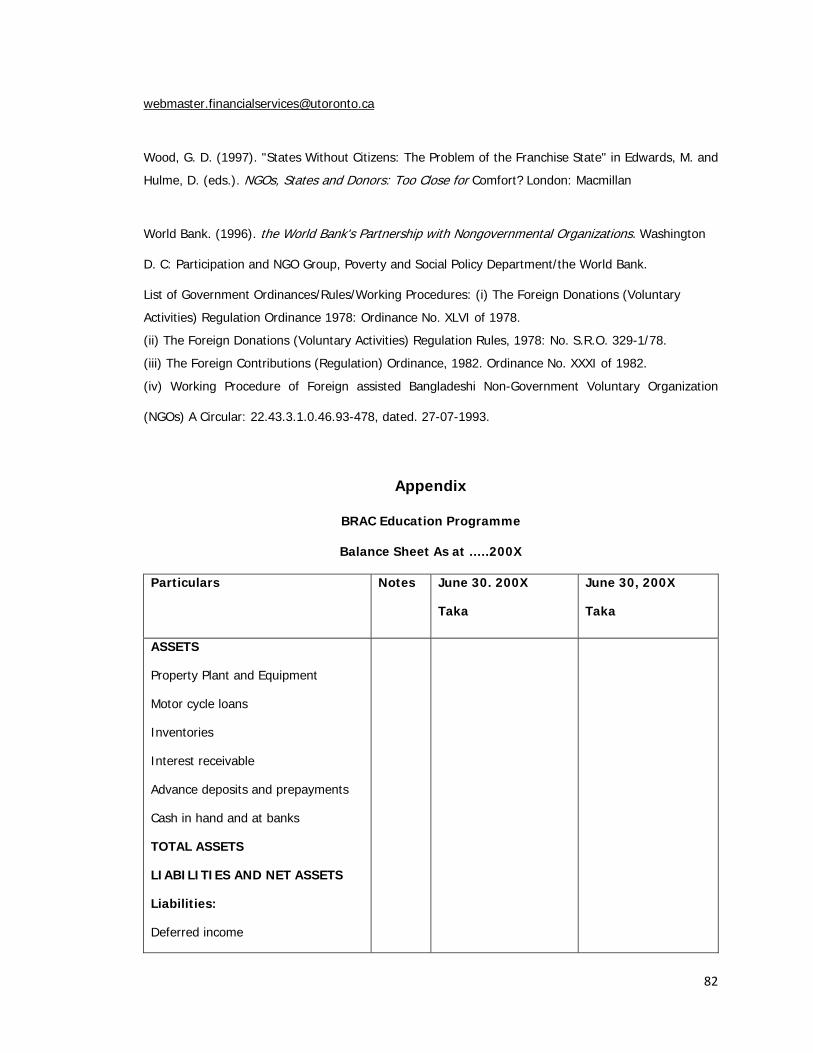

Appendix

BRAC Education Programme

Balance Sheet As at …..200X

Particulars Notes June 30. 200X

Taka

June 30, 200X

Taka

ASSETS

Property Plant and Equipment

Motor cycle loans

Inventories

Interest receivable

Advance deposits and prepayments

Cash in hand and at banks

TOTAL ASSETS

LIABILITIES AND NET ASSETS

Liabilities:

Deferred income

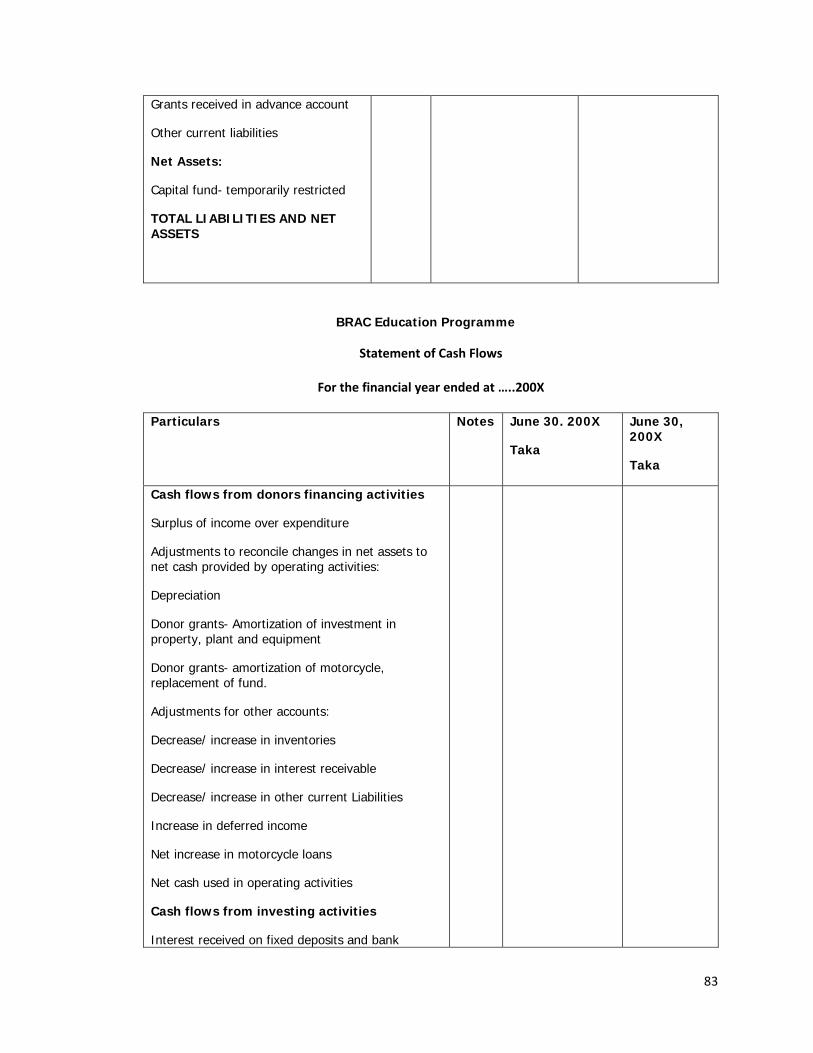

83

Grants received in advance account

Other current liabilities

Net Assets:

Capital fund- temporarily restricted

TOTAL LIABILITIES AND NET ASSETS

BRAC Education Programme

Statement of Cash Flows

For the financial year ended at …..200X

Particulars Notes June 30. 200X

Taka

June 30, 200X

Taka

Cash flows from donors financing activities

Surplus of income over expenditure

Adjustments to reconcile changes in net assets to net cash provided by operating activities:

Depreciation

Donor grants- Amortization of investment in property, plant and equipment

Donor grants- amortization of motorcycle, replacement of fund.

Adjustments for other accounts:

Decrease/ increase in inventories

Decrease/ increase in interest receivable

Decrease/ increase in other current Liabilities

Increase in deferred income

Net increase in motorcycle loans

Net cash used in operating activities

Cash flows from investing activities

Interest received on fixed deposits and bank

84

accounts

Less- purchase of property plant and equipment

Net cash used in investing activities

Cash flows from donors financing activities

Grants received during the year:

BRAC’s contribution

Less- Grants utilized during the year

Net increase in cash and cash equivalents

Cash and cash equivalents, begging of the year

cash and cash equivalents, end of the year.

BRAC Education Programme

Statement of Income and Expenditure

For the financial year ended at …..200X

Particulars Notes June 30. 200X

Taka

June 30, 200X

Taka

INCOME

Donor grants

Bank interest income

EXPENDITURE

Surplus of income over expenditure for the year

BRAC Education Programme

Statement of changes in Net Assets

For the financial year ended at …..200X

Particulars Notes Capital fund (temporarily restricted)

85

Taka

At July 1, 200X

Net surplus for the year

At June 30, 200X

Net surplus for the year

At June 30, 2006

Top Related