Languages

Pages

Legal

2021Annual Teaching Plans

ACCOUNTING FET

OS1001362

ii

It is illegal to photocopy any pages from this book without the written permission of the copyright holder

Shuter & Shooter Publishers (Pty) LtdShuters House, 110 CB Downes Road, Pietermaritzburg 3201, South Africa

PO Box 61, Mkondeni 3212, South Africa

Copyright © Shuter & Shooter Publishers (Pty) Ltd 2021

OS1001362 (TM2001445)

All rights reserved.No part of this publication may be reproduced, stored in or introduced into a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without prior written permission from the publisher. Any person who commits any unauthorized act

in relation to this publication may be liable to criminal prosecution and civil claims for damages.

iiiINTRODUCTION

INTRODUCTION

Shuter & Shooter is committed to serving the educational needs of

a changing South Africa.

• We develop and publish educational material.• We provide supplementary professional services in the education sector.• We off er superior customer service and distribution.

Shuter & Shooter is proud to be 100% South African, 100% black-owned and a Level 1 BBBEE company. Please support more local publishers like Shuter & Shooter.

iv INTRODUCTION

Our products include:• Textbooks

• Teacher Guides

• Workbooks

• Study Guides

• Core Readers

• Graded Readers

• Phonics Reading Schemes

• TVET Materials

• Dictionaries

• Atlases

• Wall Charts

• Educational Toys and Puzzles

• Reference Books

• E-Books

• Digital Learning Resources

We are also proud to be an accredited training provider, registered with the ETDP SETA and SACE.

vINTRODUCTION

Why choose our books?• Fully CAPS compliant

• Lots of activities and exercises

• Relevant examples throughout the books

• Simple language, written at the level of the learner

• Easy to plan lessons

• Planning and Tracking Booklets help to make teaching easier

Advantages of using our books• Improves learners’ results

• Assess progress easily

• Reduce the administrative burden

• Helps save planning and preparation time

• Follows the CAPS precisely, making teaching easier

• Most of our titles are also available as e-Books

vi CONTENTS

CONTENTS

Grade 10 ..............................................................................................1

Term 1 ................................................................................................................................... 2

Term 2 ................................................................................................................................... 5

Term 3 ................................................................................................................................... 7

Term 4 ................................................................................................................................... 8

Grade 11 ..............................................................................................9

Term 1 ..................................................................................................................................10

Term 2 ..................................................................................................................................12

Term 3 ..................................................................................................................................13

Term 4 ..................................................................................................................................15

Grade 12 ............................................................................................16

Term 1 ..................................................................................................................................17

Term 2 ..................................................................................................................................21

Term 3 ................................................................................................................................. 23

Term 4 ................................................................................................................................. 24

Programme of Assessment ............................................................25

10

Grade 10

10ACCOUNTING

1GRADE 10ACCOUNTING

2 Grade 10 ACCOUNTING Term 1

ACCOUNTING Term 1To

pic

Cont

ent

Tim

e al

loca

tion

Whe

re to

find

it in

Top

Cla

ss A

ccou

ntin

g Gr

ade

10U

nit

LBTG

Base

line

Asse

ssm

ent

Base

line

asse

ssm

ent t

o de

term

ine

the

lear

ning

loss

es fr

om

Grad

e 9.

Wee

k 1

Info

rmal

or

indi

geno

us

book

keep

ing

syst

ems

Com

paris

on o

f the

boo

kkee

ping

syst

ems o

f the

info

rmal

and

fo

rmal

sect

ors:

• Co

ncep

ts•

Man

agem

ent o

f res

ourc

es (c

apita

l, fix

ed a

sset

s, st

ock,

etc

.)•

Proc

ess o

f det

erm

inin

g se

lling

pric

es, c

ost o

f sal

es, l

abou

r co

sts,

inco

me

and

expe

nses

Wee

k 2

Unit

1: In

form

al

or in

dige

nous

bo

okke

epin

g sy

stem

s1–

41–

2

Inte

rnal

con

trol

• D

efini

tion

and

expl

anat

ion

of w

hat i

s mea

nt b

y in

tern

al

cont

rol.

• Id

entifi

catio

n an

d ex

plan

atio

n of

bas

ic in

tern

al c

ontro

l pr

oces

ses.

• In

tern

al c

ontro

l sho

uld

be in

tegr

ated

with

oth

er to

pics

.

Wee

k 3

Unit

4: In

tern

al c

ontro

l14

–15

4–5

Ethi

cs

Expl

anat

ion

of th

e co

de o

f eth

ics a

pplic

able

to a

ll pa

rties

in th

e fin

anci

al e

nviro

nmen

t:•

Code

of e

thic

s•

Basic

prin

cipl

es o

f eth

ics p

rinci

ples

of e

thic

s (le

ader

ship

, di

scip

line,

tran

spar

ency

, acc

ount

abili

ty, f

airn

ess,

sust

aina

bilit

y, re

spon

sible

man

agem

ent)

Unit

2: E

thic

s5–

102–

3

Gene

rally

ac

cept

ed

acco

untin

g pr

inci

ples

(G

AAP)

Defi

nitio

n an

d ex

plan

atio

n of

Gen

eral

ly A

ccep

ted

Acco

untin

g Pr

actic

e (G

AAP)

prin

cipl

es:

• H

istor

ical

cos

t•

Prud

ence

• M

ater

ialit

y•

Busin

ess e

ntity

rule

• Go

ing

conc

ern

• M

atch

ing

• Ap

ply

to a

ll th

e re

leva

nt to

pics

and

link

to to

pic

1 an

d 2.

Unit

3: G

ener

ally

ac

cept

ed a

ccou

ntin

g pr

inci

ples

(GAA

P)11

–13

4

3GRADE 10ACCOUNTING Term 1

© Shuter & Shooter PublishersACCOUNTING Term 1

Book

keep

ing

of th

e so

le

trade

r

• D

efini

tion

and

expl

anat

ion

of a

ccou

ntin

g co

ncep

ts u

p to

fin

anci

al st

atem

ents

: Sol

e tra

der;

Deb

it; C

redi

t; Eq

uity

; Ca

pita

l; As

sets

; Lia

bilit

ies;

Ledg

er; J

ourn

al; P

rofit

; Los

s; Va

lue

Adde

d Ta

x; In

com

e/Re

venu

e; E

xpen

ses;

Fina

l Acc

ount

s; Fi

nanc

ial S

tate

men

ts; D

iscou

nts;

Acco

untin

g Cy

cle;

Fin

anci

al

Acco

untin

g; M

anag

eria

l Acc

ount

ing:

Per

petu

al In

vent

ory

Syst

em

Wee

ks 4

to 7

Unit

5: F

inan

cial

ac

coun

ting:

Sol

e tra

der

16–1

85

Cash

tran

sact

ions

, CRJ

, CPJ

, PCJ

, Gen

eral

Led

ger,

Tria

l Led

ger,

Tria

l Bal

ance

, Acc

ount

ing

Equa

tion:

• Ca

sh R

ecei

pts J

ourn

al C

ash

Paym

ents

Jour

nal (

incl

udin

g lo

ans,

fixed

dep

osits

, int

eres

t inc

ome

and

inte

rest

exp

ense

, di

shon

oure

d ch

eque

s, di

scou

nt a

llow

ed a

nd d

iscou

nt

rece

ived

)•

Petty

Cas

h Jo

urna

l•

Gene

ral J

ourn

al (i

nclu

ding

bad

deb

ts, i

nter

est o

n ov

erdu

e ac

coun

ts, c

orre

ctio

n of

erro

rs)

• Po

stin

g to

the

Gene

ral,

Deb

tors

and

Cre

dito

rs L

edge

rs•

Tria

l Bal

ance

Unit

5: F

inan

cial

ac

coun

ting:

sole

trad

er19

–119

5–44

• An

alys

is an

d an

indi

catio

n of

the

effec

t of t

rans

actio

ns o

n th

e ac

coun

ting

equa

tion

of a

sole

trad

er.

• Al

l tra

nsac

tions

affe

ctin

g a

sole

trad

er u

p to

fina

ncia

l st

atem

ents

.Th

is to

pic

need

s to

be in

tegr

ated

with

all

the

appr

opria

te to

pics

th

roug

hout

the

year

.

Revi

sion

exer

cise

s12

0–13

845

–57

4 Grade 10 ACCOUNTING Term 1

ACCOUNTING Term 1To

pic

Cont

ent

Tim

e al

loca

tion

Whe

re to

find

it in

Top

Cla

ss A

ccou

ntin

g Gr

ade

10U

nit

LBTG

Book

keep

ing

of th

e so

le

trade

r

Cred

it tra

nsac

tions

: DJ,

DAJ,

CJ, C

AJ, G

J, Le

dger

s (GL

, DL,

CL),

Deb

tors

’ List

, Cre

dito

rs’ L

ist, T

rial B

alan

ce, A

ccou

ntin

g Eq

uatio

n:•

Sour

ce d

ocum

ents

• Pr

inci

ples

of D

oubl

e En

try S

yste

m•

Jour

nals

• D

ebto

rs Jo

urna

l, Cr

edito

rs’ J

ourn

al, D

ebto

rs’ A

llow

ance

s Jo

urna

l, Cr

edito

rs’ A

llow

ance

s Jou

rnal

• Ge

nera

l Jou

rnal

(inc

ludi

ng b

ad d

ebts

, can

cella

tions

of

disc

ount

on

dish

onou

red

cheq

ues,

inte

rest

on

over

due

acco

unts

, cor

rect

ion

of e

rrors

)•

Post

ing

to th

e Ge

nera

l, D

ebto

rs a

nd C

redi

tors

Led

gers

• Tr

ial B

alan

ce•

Prep

arat

ion

of d

ebto

rs a

nd c

redi

tors

list

s to

reco

ncile

with

de

btor

s and

cre

dito

rs c

ontro

l acc

ount

s (in

clud

ing

corre

ctio

n of

erro

rs)

Wee

ks 8

to 1

0

Unit

5: F

inan

cial

ac

coun

ting:

sole

trad

er19

–119

5–44

• An

alys

is an

d an

indi

catio

n of

the

effec

t of t

rans

actio

ns o

n th

e ac

coun

ting

equa

tion

of a

sole

trad

er.

• Al

l tra

nsac

tions

affe

ctin

g a

sole

trad

er u

p to

fina

ncia

l st

atem

ents

.Th

is to

pic

need

s to

be in

tegr

ated

with

all

the

appr

opria

te to

pics

th

roug

hout

the

year

.

Revi

sion

exer

cise

s12

0–13

845

–57

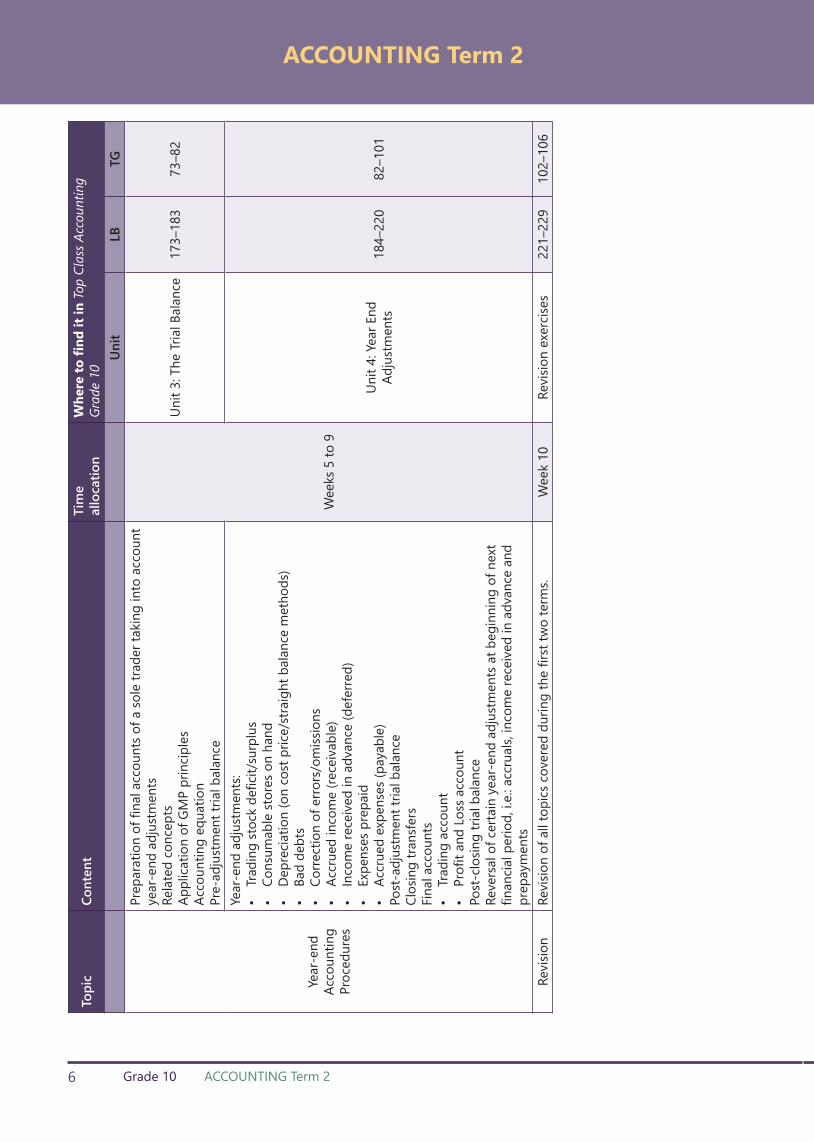

5GRADE 10ACCOUNTING Term 2

© Shuter & Shooter PublishersACCOUNTING Term 2

Book

keep

er o

f th

e so

le tr

ader

• Co

mpe

tenc

y in

dea

ling

with

com

bine

d ac

tiviti

es in

clud

ing

cash

and

cre

dit t

rans

actio

ns•

Com

plet

ing

of th

e re

leva

nt jo

urna

ls fro

m g

iven

info

rmat

ion

• Po

stin

g to

subs

idia

ry le

dger

and

the

gene

ral l

edge

r•

Extra

ctin

g th

e tri

al b

alan

ce in

the

corre

ct fo

rmat

Cons

olid

atio

n:

• Re

conc

iliat

ions

: abi

lity

to a

naly

ze th

e co

ntro

l acc

ount

s (d

ebto

rs a

nd c

redi

tor)

and

com

pare

with

list

of d

ebto

rs/

cred

itors

• Id

entif

ying

erro

rs a

nd o

miss

ions

and

pre

pare

deb

tors

and

cr

edito

rs li

st to

reco

ncile

with

the

cont

rol a

ccou

nts.

• Re

leva

nt in

tern

al c

ontro

l and

eth

ics (

inte

grat

ed):

rela

ted

to

hand

ling

stoc

k, d

ebto

rs, c

redi

tors

and

cas

h.

• Id

entifi

catio

n of

eth

ical

scen

ario

s (ac

coun

tabi

lity

and

trans

pare

ncy)

Wee

ks 1

to 2

Unit

5: F

inan

cial

ac

coun

ting:

sole

trad

er16

–119

5–44

Sala

ries a

nd

Wag

es Jo

urna

l

Expl

anat

ion,

cal

cula

tion

and

reco

rdin

g of

sala

ry a

nd/o

r wag

e sc

ales

and

pay

men

ts in

the

jour

nals

and

post

to th

e le

dger

. Thi

s ca

n be

don

e m

anua

lly o

r on

a co

mpu

teris

ed sp

read

shee

t.•

Nor

mal

tim

e•

Ove

rtim

eD

educ

tions

• PA

YE•

Pens

ion

fund

• Un

empl

oym

ent I

nsur

ance

Fun

d•

Med

ical

aid

• Un

ion

mem

bers

hip

Empl

oyer

con

tribu

tions

• Pe

nsio

n fu

nd•

Unem

ploy

men

t Ins

uran

ce F

und

• M

edic

al a

id•

Skill

s dev

elop

men

t lev

yAc

coun

ting

equa

tion

Ethi

cal c

ondu

ct re

late

d to

Sal

arie

s and

Wag

es. F

or e

xam

ple,

co

ntra

cts,

paym

ent i

n lin

e w

ith re

spon

sibili

ties,

role

of u

nion

s

Wee

ks 3

to 4

Unit

2: S

alar

ies a

nd

wag

es14

2–17

259

–72

6 Grade 10 ACCOUNTING Term 2

ACCOUNTING Term 2To

pic

Cont

ent

Tim

e al

loca

tion

Whe

re to

find

it in

Top

Cla

ss A

ccou

ntin

g Gr

ade

10U

nit

LBTG

Year

-end

Ac

coun

ting

Proc

edur

es

Prep

arat

ion

of fi

nal a

ccou

nts o

f a so

le tr

ader

taki

ng in

to a

ccou

nt

year

-end

adj

ustm

ents

Rela

ted

conc

epts

Appl

icat

ion

of G

MP

prin

cipl

esAc

coun

ting

equa

tion

Pre-

adju

stm

ent t

rial b

alan

ce

Wee

ks 5

to 9

Unit

3: T

he T

rial B

alan

ce17

3–18

373

–82

Year

-end

adj

ustm

ents

:•

Trad

ing

stoc

k de

ficit/

surp

lus

• Co

nsum

able

stor

es o

n ha

nd•

Dep

reci

atio

n (o

n co

st p

rice/

stra

ight

bal

ance

met

hods

)•

Bad

debt

s•

Corre

ctio

n of

erro

rs/o

miss

ions

• Ac

crue

d in

com

e (re

ceiv

able

)•

Inco

me

rece

ived

in a

dvan

ce (d

efer

red)

• Ex

pens

es p

repa

id•

Accr

ued

expe

nses

(pay

able

)Po

st-a

djus

tmen

t tria

l bal

ance

Clos

ing

trans

fers

Fina

l acc

ount

s•

Trad

ing

acco

unt

• Pr

ofit a

nd L

oss a

ccou

ntPo

st-c

losin

g tri

al b

alan

ceRe

vers

al o

f cer

tain

yea

r-en

d ad

just

men

ts a

t beg

inni

ng o

f nex

t fin

anci

al p

erio

d, i.

e.: a

ccru

als,

inco

me

rece

ived

in a

dvan

ce a

nd

prep

aym

ents

Unit

4: Y

ear E

nd

Adju

stm

ents

184–

220

82–1

01

Revi

sion

Revi

sion

of a

ll to

pics

cov

ered

dur

ing

the

first

two

term

s.W

eek

10Re

visio

n ex

erci

ses

221–

229

102–

106

7GRADE 10ACCOUNTING Term 3

© Shuter & Shooter PublishersACCOUNTING Term 3

Fina

ncia

l ac

coun

ting

of

a so

le tr

ader

–

prep

arat

ion

of fi

nanc

ial

stat

emen

ts

Prep

arat

ion

of fi

nanc

ial s

tate

men

ts o

f a so

le tr

ader

taki

ng in

to

acco

unt y

ear-

end

adju

stm

ents

Rela

ted

conc

epts

Appl

icat

ion

of G

AAP

prin

cipl

esAc

coun

ting

equa

tion

Year

-end

adj

ustm

ents

:•

Trad

ing

stoc

k de

ficit/

surp

lus

• Co

nsum

able

stor

es o

n ha

nd•

Dep

reci

atio

n•

bala

nce

met

hods

)•

Bad

debt

s•

Corre

ctio

n of

erro

rs/o

miss

ions

• Ac

crue

d in

com

e (re

ceiv

able

)•

Inco

me

rece

ived

in a

dvan

ce (d

efer

red)

• Ex

pens

es p

repa

id•

Accr

ued

expe

nses

(pay

able

)Fi

nanc

ial s

tate

men

ts a

nd n

otes

:•

Inco

me

stat

emen

t•

Bala

nce

shee

t

Wee

ks 1

to 7

Unit

1: F

inan

cial

st

atem

ents

230–

257

107–

120

Fina

ncia

l ac

coun

ting

of

a so

le tr

ader

–

anal

ysis

and

inte

rpre

tatio

n of

fina

ncia

l st

atem

ents

Anal

ysis

and

inte

rpre

tatio

n of

fina

ncia

l sta

tem

ents

and

not

es:

• Gr

oss p

rofit

on

sale

s•

Gros

s pro

fit o

n co

st o

f sal

es•

Net

pro

fit o

n sa

les

• O

pera

ting

expe

nses

on

sale

s•

Ope

ratin

g pr

ofit o

n sa

les

• Cu

rrent

ratio

• Ac

id te

st ra

tio•

Solv

ency

ratio

• Re

turn

on

equi

ty

Wee

ks 8

to 1

1Un

it 2:

Ana

lysis

and

in

terp

reta

tion

of

Fina

ncia

l Sta

tem

ents

258–

272

121–

126

8 Grade 10 ACCOUNTING Term 4

Topi

cCo

nten

tTi

me

allo

catio

nW

here

to fi

nd it

in T

op C

lass

Acc

ount

ing

Grad

e 10

Uni

tLB

TG

Valu

e-Ad

ded

Tax

(VAT

)

Expl

anat

ion

of th

e ba

sic c

once

pts o

f VAT

:•

Nee

d fo

r VAT

• Pu

rpos

e of

VAT

• Pr

inci

ples

of V

AT•

Zero

-rat

ed it

ems

• VA

T ex

empt

ed it

ems

• VA

T-ab

le it

ems

Curre

nt V

AT ra

te

Wee

k 1

Unit

1: V

alue

Add

ed Ta

x (V

AT)

139–

141

58–5

9

Cost

ac

coun

ting

Defi

nitio

n an

d ex

plan

atio

n of

bas

ic c

ost c

once

pts:

• D

irect

labo

ur•

Indi

rect

labo

ur•

Dire

ct m

ater

ials

(raw

mat

eria

ls)•

Indi

rect

mat

eria

ls•

Fact

ory

over

head

cos

ts•

Prim

e co

st•

Varia

ble

cost

s•

Fixe

d co

sts

• W

ork-

in-p

roce

ssAp

plic

atio

n of

prin

cipl

es o

f int

erna

l con

trol

Ethi

cal b

ehav

iour

rela

ted

to a

man

ufac

turin

g bu

sines

s

Wee

k 2

Unit

1: C

ost A

ccou

ntin

g28

2–28

813

4–13

6

Budg

etin

g

Defi

ne a

nd e

xpla

in b

asic

bud

getin

g co

ncep

ts:

• Ca

sh b

udge

t•

Zero

bas

e bu

dget

• Ca

pita

l bud

get

• Lo

ng te

rm b

udge

t•

Med

ium

term

bud

get

Wee

k 3

Unit

2: B

udge

ts28

9–29

413

6–13

8

Revi

sion

Revi

se to

pics

cov

ered

dur

ing

the

term

.W

eek

4 to

6Re

visio

n ex

erci

ses

295–

323

139–

162

ACCOUNTING Term 4

11

Grade 11

11ACCOUNTING

9GRADE 11ACCOUNTING

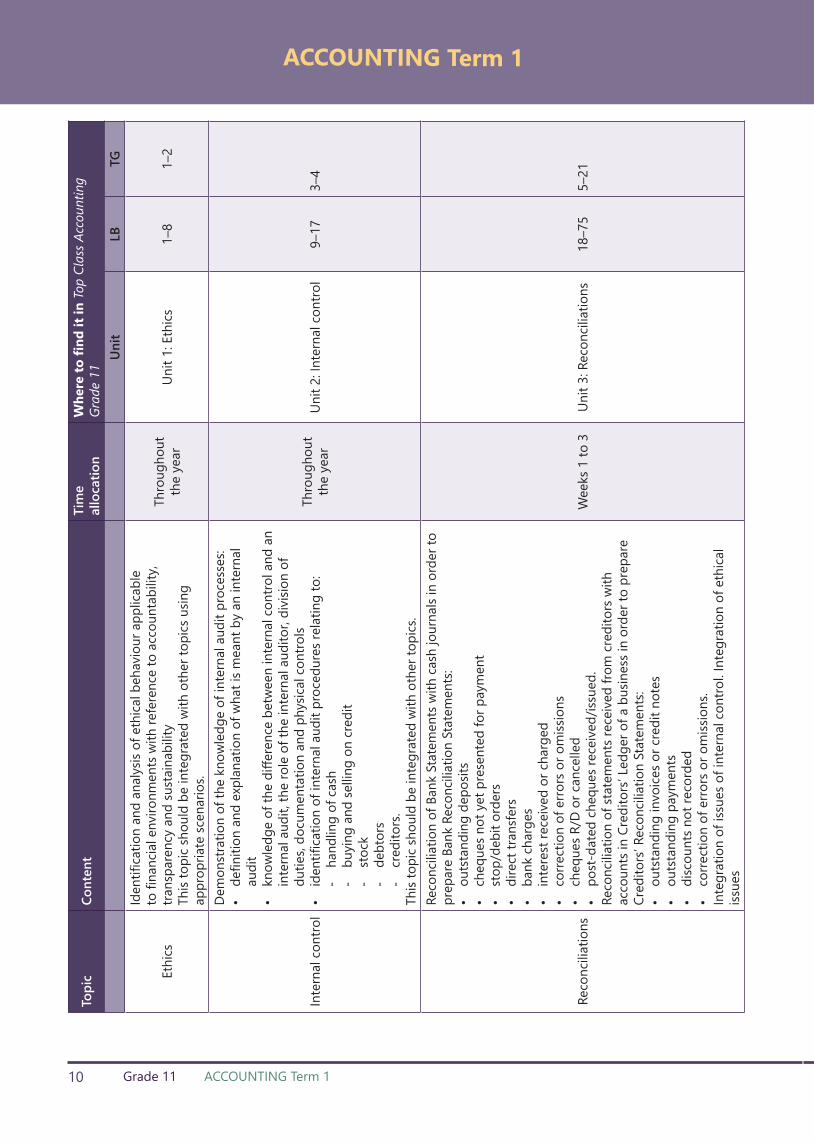

10 Grade 11 ACCOUNTING Term 1

ACCOUNTING Term 1To

pic

Cont

ent

Tim

e al

loca

tion

Whe

re to

find

it in

Top

Cla

ss A

ccou

ntin

g Gr

ade

11U

nit

LBTG

Ethi

cs

Iden

tifica

tion

and

anal

ysis

of e

thic

al b

ehav

iour

app

licab

le

to fi

nanc

ial e

nviro

nmen

ts w

ith re

fere

nce

to a

ccou

ntab

ility

, tra

nspa

renc

y an

d su

stai

nabi

lity

This

topi

c sh

ould

be

inte

grat

ed w

ith o

ther

topi

cs u

sing

appr

opria

te sc

enar

ios.

Thro

ugho

ut

the

year

Unit

1: E

thic

s1–

81–

2

Inte

rnal

con

trol

Dem

onst

ratio

n of

the

know

ledg

e of

inte

rnal

aud

it pr

oces

ses:

• de

finiti

on a

nd e

xpla

natio

n of

wha

t is m

eant

by

an in

tern

al

audi

t•

know

ledg

e of

the

diffe

renc

e be

twee

n in

tern

al c

ontro

l and

an

inte

rnal

aud

it, th

e ro

le o

f the

inte

rnal

aud

itor,

divi

sion

of

dutie

s, do

cum

enta

tion

and

phys

ical

con

trols

• id

entifi

catio

n of

inte

rnal

aud

it pr

oced

ures

rela

ting

to:

- ha

ndlin

g of

cas

h-

buyi

ng a

nd se

lling

on

cred

it-

stoc

k-

debt

ors

- cr

edito

rs.

This

topi

c sh

ould

be

inte

grat

ed w

ith o

ther

topi

cs.

Thro

ugho

ut

the

year

Unit

2: In

tern

al c

ontro

l9–

173–

4

Reco

ncili

atio

ns

Reco

ncili

atio

n of

Ban

k St

atem

ents

with

cas

h jo

urna

ls in

ord

er to

pr

epar

e Ba

nk R

econ

cilia

tion

Stat

emen

ts:

• ou

tsta

ndin

g de

posit

s•

cheq

ues n

ot y

et p

rese

nted

for p

aym

ent

• st

op/d

ebit

orde

rs•

dire

ct tr

ansf

ers

• ba

nk c

harg

es•

inte

rest

rece

ived

or c

harg

ed•

corre

ctio

n of

erro

rs o

r om

issio

ns•

cheq

ues R

/D o

r can

celle

d•

post

-dat

ed c

hequ

es re

ceiv

ed/is

sued

.Re

conc

iliat

ion

of st

atem

ents

rece

ived

from

cre

dito

rs w

ith

acco

unts

in C

redi

tors

’ Led

ger o

f a b

usin

ess i

n or

der t

o pr

epar

e Cr

edito

rs’ R

econ

cilia

tion

Stat

emen

ts:

• ou

tsta

ndin

g in

voic

es o

r cre

dit n

otes

• ou

tsta

ndin

g pa

ymen

ts•

disc

ount

s not

reco

rded

• co

rrect

ion

of e

rrors

or o

miss

ions

.In

tegr

atio

n of

issu

es o

f int

erna

l con

trol.

Inte

grat

ion

of e

thic

al

issue

s

Wee

ks 1

to 3

Unit

3: R

econ

cilia

tions

18–7

55–

21

11GRADE 11ACCOUNTING Term 1

© Shuter & Shooter PublishersACCOUNTING Term 1

Tang

ible

/Fix

ed

asse

ts

Unde

rsta

ndin

g th

e co

ncep

t of a

Tang

ible

/Fix

ed A

sset

Reg

ister

Reco

rdin

g th

e ac

quisi

tion

of ta

ngib

le/fi

xed

asse

tsCa

lcul

atio

n an

d re

cord

ing

of d

epre

ciat

ion

• on

cos

t pric

e (s

traig

ht-li

ne m

etho

d)•

dim

inish

ing

bala

nce

met

hod.

Unde

rsta

ndin

g ho

w ta

ngib

le/fi

xed

asse

ts a

re re

cord

ed w

hen

they

are

fully

dep

reci

ated

Reco

rdin

g th

e di

spos

al o

f tan

gibl

e/fix

ed a

sset

s (ca

sh, c

redi

t, tra

de in

):•

at th

e be

ginn

ing

of a

fina

ncia

l yea

r•

durin

g a

finan

cial

yea

r•

at th

e en

d of

a fi

nanc

ial y

ear.

Inte

grat

ion

of is

sues

of i

nter

nal c

ontro

l – c

ontro

l mea

sure

s ove

r fix

ed a

sset

sIn

tegr

atio

n of

eth

ical

issu

es re

latin

g to

fixe

d as

sets

– re

spon

sible

us

e of

fixe

d as

sets

Wee

ks 4

to 6

Unit

4: F

ixed

/Tan

gibl

e As

sets

– A

cqui

sitio

n,

Dep

reci

atio

n an

d D

ispos

al

76–1

1722

–41

Fina

ncia

l Ac

coun

ting

of

partn

ersh

ips

• D

efine

and

exp

lain

acc

ount

ing

conc

epts

uni

que

to

partn

ersh

ips,

i.e. P

artn

ersh

ip; C

apita

l acc

ount

s; Cu

rrent

ac

coun

ts; I

nter

est o

n ca

pita

l; Sa

larie

s to

partn

ers;

Bonu

s to

partn

ers;

Prim

ary

/ Fin

al d

istrib

utio

n of

pro

fits o

r los

ses ·

• D

efine

and

exp

lain

IFRS

and

GAA

P pr

inci

ples

(hist

oric

al c

ost;

prud

ence

; mat

eria

lity;

bus

ines

s ent

ity ru

le; g

oing

con

cern

; m

atch

ing)

•

Acco

untin

g cy

cle

of p

artn

ersh

ips:

docu

men

ts; j

ourn

als;

ledg

ers;

trial

bal

ance

; fina

l acc

ount

s •

Acco

untin

g eq

uatio

n •

Prep

are

final

acc

ount

s and

fina

ncia

l sta

tem

ents

of a

pa

rtner

ship

taki

ng in

to a

ccou

nt y

ear-

end

adju

stm

ents

:-

Revi

se th

e fo

llow

ing:

Tra

ding

stoc

k de

ficit

/ sur

plus

; Co

nsum

able

stor

es o

n ha

nd; D

epre

ciat

ion

(on

cost

and

di

min

ishin

g ba

lanc

e); B

ad d

ebts

; Bad

deb

ts re

cove

red

(incl

. ins

olve

nt e

stat

e); C

orre

ctio

n of

erro

rs /

omiss

ions

(in

cl. e

rrors

and

om

issio

ns re

latin

g to

sala

ries /

wag

es) ;

Ac

crue

d in

com

e (re

ceiv

able

); In

com

e re

ceiv

ed in

adv

ance

(d

efer

red)

; Pre

paid

exp

ense

s; Ac

crue

d ex

pens

es (p

ayab

le);

- N

ew in

Gr 1

1: P

rovi

sion

for b

ad d

ebts

; Int

eres

t on

loan

(c

apita

lised

) -

Partn

ersh

ip re

late

d ad

just

men

ts: S

alar

ies t

o pa

rtner

s; Bo

nus t

o pa

rtner

s; In

tere

st o

n ca

pita

l; Ap

prop

riatio

n of

pr

ofit /

loss

· Fi

nal a

ccou

nts:

- Tr

adin

g ac

coun

t; Pr

ofit a

nd L

oss a

ccou

nt; A

ppro

pria

tion

acco

unt ·

Rev

ersa

l of c

erta

in y

ear-

end

adju

stm

ents

at

begi

nnin

g of

nex

t fina

ncia

l per

iod,

i.e.

acc

rual

s, in

com

e re

ceiv

ed in

adv

ance

and

pre

paym

ents

Wee

ks 7

to 1

0

Unit

5: F

inan

cial

Ac

coun

ting

of

Partn

ersh

ips –

Pr

epar

atio

n

118–

213

42–8

6

12 Grade 11 ACCOUNTING Term 2

ACCOUNTING Term 2To

pic

Cont

ent

Tim

e al

loca

tion

Whe

re to

find

it in

Top

Cla

ss A

ccou

ntin

g Gr

ade

11U

nit

LBTG

Partn

ersh

ips

– Fi

nanc

ial

Stat

emen

ts a

nd

Not

es

• Pr

epar

e Fi

nanc

ial s

tate

men

ts a

nd n

otes

:-

Stat

emen

t of C

ompr

ehen

sive

Inco

me

- St

atem

ent o

f Fin

anci

al P

ositi

on-

Not

es to

the

Fina

ncia

l Sta

tem

ents

Foc

us o

n th

e fo

llow

ing

note

s: Fi

xed

/ Tan

gibl

e as

sets

, Tra

de a

nd o

ther

rece

ivab

les;

Trad

e an

d ot

her p

ayab

les;

Capi

tal;

Curre

nt a

ccou

nts

• Ap

ply

the

IFRS

and

GAA

P pr

inci

ples

Wee

ks 1

–4

Unit

5: F

inan

cial

Ac

coun

ting

of

Partn

ersh

ips –

Pr

epar

atio

n

118–

213

42–8

6

Fina

ncia

l ac

coun

ting

of

partn

ersh

ips

– an

alys

is an

d in

terp

reta

tion

• An

alys

e an

d in

terp

ret fi

nanc

ial s

tate

men

ts a

nd n

otes

• Re

vise

the

follo

win

g fin

anci

al in

dica

tors

:

- Pr

ofita

bilit

y: G

ross

pro

fit o

n sa

les;

Gros

s pro

fit o

n co

st o

f sa

les;

Net

pro

fit o

n sa

les;

Ope

ratin

g ex

pens

es o

n sa

les;

Ope

ratin

g pr

ofit o

n sa

les

- Li

quid

ity: C

urre

nt ra

tio; A

cid

test

ratio

- So

lven

cy: S

olve

ncy

ratio

•

Intro

duce

the

follo

win

g fin

anci

al in

dica

tors

: -

Liqu

idity

: Sto

ck tu

rnov

er ra

te; S

tock

hol

ding

per

iod;

Av

erag

e de

btor

s’ co

llect

ion

perio

d; A

vera

ge c

redi

tors

’ pa

ymen

t per

iod

-

Risk

/Gea

ring:

Deb

t-eq

uity

ratio

-

Retu

rn: o

n ea

ch p

artn

er’s

equi

ty o

n av

erag

e pa

rtner

s’ eq

uity

Wee

ks 6

to 9

Unit

1: F

inan

cial

Ac

coun

ting

of

Partn

ersh

ips –

Ana

lysis

an

d In

terp

reta

tion

225–

254

94–1

02

Revi

sion

Revi

se to

pics

cov

ered

dur

ing

first

two

term

s.W

eek

10Re

visio

n Ex

erci

ses

332–

337

136–

139

13GRADE 11ACCOUNTING Term 3

© Shuter & Shooter PublishersACCOUNTING Term 3

Cash

bud

get

and

proj

ecte

d in

com

e st

atem

ent f

or

sole

trad

ers

Prep

arat

ion

and

pres

enta

tion

of a

cas

h bu

dget

for s

ole

trade

rs:

• pr

ojec

ted

rece

ipts

and

pay

men

ts•

proj

ecte

d de

btor

s’ co

llect

ion

• pr

ojec

ted

cred

itors

’ pay

men

ts•

Cash

bud

get.

Prep

arat

ion

and

pres

enta

tion

of P

roje

cted

Inco

me

Stat

emen

t•

proj

ecte

d re

venu

e an

d ex

pend

iture

.In

tegr

atio

n of

eth

ical

issu

esIn

tegr

atio

n of

inte

rnal

aud

it an

d in

tern

al c

ontro

l iss

ues

Wee

ks 1

to 4

Unit

2: B

udge

ting

367–

418

151–

169

Inve

ntor

y sy

stem

s

Defi

nitio

n an

d ex

plan

atio

n of

the

follo

win

g st

ock

syst

ems:

• Pe

rpet

ual s

tock

syst

em•

Perio

dic

stoc

k sy

stem

Know

ledg

e of

the

adva

ntag

es a

nd d

isadv

anta

ges o

f the

per

iodi

c an

d pe

rpet

ual s

tock

syst

ems

Reco

rdin

g of

tran

sact

ions

usin

g th

e pe

riodi

c st

ock

syst

em in

th

e jo

urna

ls an

d le

dger

s, co

mpa

ring

it w

ith th

e pe

rpet

ual s

tock

sy

stem

:•

purc

hase

s acc

ount

as o

ppos

ed to

Tra

ding

Sto

ck a

ccou

nt•

Ope

ning

Sto

ck a

nd C

losin

g St

ock

acco

unts

• Tr

adin

g ac

coun

t•

carri

age

on p

urch

ases

• cu

stom

and

impo

rt du

ties

Wee

ks 5

to 6

Unit

3: In

vent

ory

syst

ems

419–

465

170–

183

14 Grade 11 ACCOUNTING Term 3

ACCOUNTING Term 3To

pic

Cont

ent

Tim

e al

loca

tion

Whe

re to

find

it in

Top

Cla

ss A

ccou

ntin

g Gr

ade

11U

nit

LBTG

Cost

Ac

coun

ting

in a

m

anuf

actu

ring

envi

ronm

ent

Calc

ulat

ion

of th

e fo

llow

ing

cost

s in

a m

anuf

actu

ring

envi

ronm

ent:

• va

riabl

e an

d fix

ed c

osts

• th

e co

st o

f a p

rodu

ct u

sing

varia

ble

and

fixed

cos

ts•

unit

cost

• co

ntrib

utio

n pe

r uni

t•

Brea

k-ev

en p

oint

.Pr

epar

atio

n of

ledg

er a

ccou

nts o

f a m

anuf

actu

ring

busin

ess

Bala

nce

Shee

t Sec

tion:

• ra

w m

ater

ial s

tock

• w

ork-

in-p

rogr

ess s

tock

• fin

ished

goo

ds st

ock

• co

nsum

able

stor

es st

ock

(indi

rect

mat

eria

ls).

Nom

inal

Acc

ount

s Sec

tion:

• sa

les

• co

st o

f sal

es•

raw

mat

eria

ls iss

ued

• fa

ctor

y w

ages

• fa

ctor

y el

ectri

city

• fa

ctor

y re

nt•

depr

ecia

tion

on fa

ctor

y eq

uipm

ent,

etc.

Cost

Acc

ount

s Sec

tion:

• di

rect

(raw

) mat

eria

ls co

st•

dire

ct la

bour

cos

t•

fact

ory

over

head

cos

t•

adm

inist

ratio

n co

st•

selli

ng a

nd d

istrib

utio

n co

st.

Inte

grat

ion

of e

thic

al is

sues

rela

ted

to a

man

ufac

turin

g en

viro

nmen

tIn

tegr

atio

n of

inte

rnal

aud

it an

d in

tern

al c

ontro

l iss

ues r

elat

ed

to a

man

ufac

turin

g en

viro

nmen

t

Wee

ks 7

to 8

Unit

1: C

ost a

ccou

ntin

g33

8–36

614

0–15

0

Revi

sion

Revi

sion

of te

rm’s

wor

kW

eeks

9 to

11

Revi

sion

Exer

cise

s46

6–47

018

4–18

7

15GRADE 11ACCOUNTING Term 4

© Shuter & Shooter PublishersACCOUNTING Term 4

Valu

e Ad

ded

Tax

(VAT

)

Perfo

rm V

AT c

alcu

latio

ns:

• us

e cu

rrent

rate

• ad

d VA

T to

cos

t pric

e pl

us m

ark-

up a

mou

nt•

calc

ulat

e VA

T fro

m V

AT-in

clus

ive

amou

nt•

invo

ice

or re

ceip

t bas

e.Un

ders

tand

the

effec

t of b

ad d

ebts

, disc

ount

s and

goo

ds

retu

rned

on

VAT

Inte

grat

e et

hics

rela

ting

to V

AT –

VAT

frau

d, e

tc.

Inte

grat

e in

tern

al a

udit

and

inte

rnal

con

trol p

roce

sses

ove

r co

llect

ion

of V

AT fr

om c

usto

mer

s and

pay

men

t of V

AT to

SAR

S.

Wee

ks 1

to 3

Unit

1: V

alue

Add

ed Ta

x47

1–48

418

8–19

3

Revi

sion

Revi

sion

of a

ll to

pics

in p

repa

ratio

n fo

r the

fina

l exa

min

atio

n.W

eeks

4 to

6Re

visio

n Ex

erci

ses

485–

515

194–

215

Grade 12 ACCOUNTING

12

16 GRADE 12 ACCOUNTING

17GRADE 12ACCOUNTING Term 1

© Shuter & Shooter Publishers

12ACCOUNTING Term 1

Topi

cCo

nten

tTi

me

allo

catio

nW

here

to fi

nd it

in T

op C

lass

Acc

ount

ing

Grad

e 12

Uni

tLB

TG

Com

pani

es:

Uniq

ue

Tran

sact

ions

Defi

nitio

n an

d ex

plan

atio

n of

acc

ount

ing

conc

epts

uni

que

to

com

pani

es:

• Co

mpa

nies

– p

rivat

e an

d pu

blic

• Co

mpa

nies

Act

• Re

gist

rar o

f Com

pani

es –

Reg

istra

tion

Certi

ficat

e.•

Mem

oran

dum

of I

ncor

pora

tion

• In

com

e Ta

x an

d pr

ovisi

onal

pay

men

ts•

Div

iden

d•

Shar

es•

Earn

ings

• Sh

areh

olde

r•

Dire

ctor

s•

Audi

tors

• Li

mite

d lia

bilit

y•

Sepa

ratio

n of

ow

ners

hip

from

con

trol

• Re

tain

ed in

com

e•

Auth

orise

d sh

are

capi

tal

• Iss

ued

shar

e ca

pita

l•

Joha

nnes

burg

Sto

ck E

xcha

nge

(JSE)

Wee

ks 1

and

2

Unit

1: F

inan

cial

ac

coun

ting

of

com

pani

es –

con

cept

s an

d un

ique

ledg

er

acco

unts

1–7

1–14

• D

efini

tion

and

expl

anat

ion

of In

tern

atio

nal F

inan

cial

Re

porti

ng S

tand

ards

(IFR

S) a

nd G

ener

ally

Acc

epte

d Ac

coun

ting

Prac

tices

(GAA

P)•

Defi

nitio

n an

d ex

plan

atio

n of

the

follo

win

g GA

AP p

rinci

ples

:-

Hist

oric

al c

ost

- Pr

uden

ce-

Mat

eria

lity

- Bu

sines

s Ent

ity-

Goin

g co

ncer

n-

Mat

chin

g

7–10

18 Grade 12 ACCOUNTING Term 1

Topi

cCo

nten

tTi

me

allo

catio

nW

here

to fi

nd it

in T

op C

lass

Acc

ount

ing

Grad

e 12

Uni

tLB

TG

Com

pani

es:

Uniq

ue

Tran

sact

ions

Acco

untin

g cy

cle

for a

Com

pany

:•

Jour

nals

• Le

dger

acc

ount

s•

Tria

l Bal

ance

Tran

sact

ions

incl

ude:

• Iss

uing

of s

hare

s at i

ssue

pric

e (N

OTE

: Par

val

ue a

nd sh

are

prem

ium

no

long

er e

xist

s in

term

s of C

ompa

nies

Act

.)•

Buyi

ng b

ack

of sh

ares

.•

Loan

s and

inte

rest

(NO

TE: I

nter

est o

n lo

an is

cap

italiz

ed.

• In

com

e Ta

x•

Div

iden

ds•

Dire

ctor

s’ Fe

es•

Audi

t Fee

s

Wee

ks 1

and

2

Unit

1: F

inan

cial

ac

coun

ting

of

com

pani

es –

con

cept

s an

d un

ique

ledg

er

acco

unts

11–4

91–

14

ACCOUNTING Term 1

19GRADE 12ACCOUNTING Term 1

© Shuter & Shooter PublishersACCOUNTING Term 1

Com

pani

es –

Fi

nal a

ccou

nts

and

finan

cial

st

atem

ents

Prep

arat

ion

of fi

nal a

ccou

nts a

nd d

etai

led

finan

cial

stat

emen

ts o

f a c

ompa

ny ta

king

into

acc

ount

yea

r-en

dad

just

men

ts.

YEAR

EN

D A

DJU

STM

ENTS

:•

Trad

ing

Stoc

k de

ficits

/ sur

plus

es.

• Co

nsum

able

stor

es o

n ha

nd.

• D

epre

ciat

ion

(on

cost

pric

e/st

raig

ht li

ne a

nd o

n di

min

ishin

g ba

lanc

e m

etho

ds).

• Ba

d de

bts

• Co

rrect

ion

of e

rrors

/ om

issio

ns•

Accr

ued

inco

me

(rece

ivab

le)

• In

com

e re

ceiv

ed in

adv

ance

(def

erre

d)•

Expe

nses

pre

paid

• Ac

crue

d ex

pens

es (p

ayab

le)

• Pr

ovisi

on fo

r bad

deb

ts•

Adju

stm

ents

rela

ted

to in

com

e ta

x.•

Adju

stm

ents

rela

ted

to th

e pa

ymen

t and

dec

lara

tion

of

divi

dend

s.FI

NAL

ACC

OUN

TS:

• Tr

adin

g ac

coun

t•

Profi

t and

Los

s acc

ount

• Ap

prop

riatio

n ac

coun

t•

Reve

rsal

of c

erta

in a

djus

tmen

ts (i

e. a

ccru

als,

inco

me

rece

ived

in

adv

ance

and

pre

paym

ents

)FI

NAN

CIAL

STA

TEM

ENTS

AN

D N

OTE

S:•

Inco

me

Stat

emen

t•

Bala

nce

Shee

t•

Cash

Flo

w S

tate

men

tAn

alys

is an

d in

dica

tion

of th

e eff

ect o

f tra

nsac

tions

on

the

acco

untin

g eq

uatio

n of

a c

ompa

ny; a

ll tra

nsac

tions

affe

ctin

g a

com

pany

up

to fi

nanc

ial s

tate

men

ts.

Inte

grat

ion

and

repo

rting

and

con

trol o

f fixe

d as

sets

Inte

grat

ion

of e

thic

al c

onsid

erat

ions

rela

ting

toco

mpa

nies

– ro

le o

f sha

reho

lder

s and

dire

ctor

s,m

anip

ulat

ion

of sh

are

pric

es, c

orpo

rate

gov

erna

nce,

etc.

Inte

grat

ion

of in

tern

al a

udit

and

cont

rol p

roce

sses

rela

ting

to c

ompa

nies

.Ap

plic

atio

n of

GAA

P pr

inci

ples

and

IFRS

.

Wee

ks 3

to 7

Unit

2: F

inan

cial

Ac

coun

ting

of

Com

pani

es –

Pr

epar

atio

n of

Fin

al

Acco

unts

and

Fin

anci

al

Stat

emen

ts

50–1

4715

–63

20 Grade 12 ACCOUNTING Term 1

ACCOUNTING Term 1To

pic

Cont

ent

Tim

e al

loca

tion

Whe

re to

find

it in

Top

Cla

ss A

ccou

ntin

g Gr

ade

12U

nit

LBTG

Com

pani

es –

An

alys

is an

d in

terp

reta

tion

of fi

nanc

ial

stat

emen

ts

Anal

ysis

and

inte

rpre

tatio

n of

Inco

me

Stat

emen

t,Ba

lanc

e Sh

eet a

nd N

otes

Revi

sion

of th

e fo

llow

ing

indi

cato

rs:

• Gr

oss p

rofit

on

sale

s•

Gros

s pro

fit o

n co

st o

f sal

es•

Net

pro

fit o

n sa

les

• O

pera

ting

expe

nses

on

sale

s•

Ope

ratin

g pr

ofit o

n sa

les

• Cu

rrent

ratio

• Ac

id te

st ra

tio•

Stoc

k tu

rnov

er ra

te•

Stoc

k ho

ldin

g pe

riod

• Av

erag

e de

btor

s’ co

llect

ion

perio

d•

Aver

age

cred

itors

’ pay

men

t per

iod

• So

lven

cy ra

tioIn

trodu

ctio

n an

d co

vera

ge o

f the

follo

win

g fin

anci

alin

dica

tors

:•

Deb

t equ

ity ra

tio•

Retu

rn o

n sh

areh

olde

rs’ e

quity

• Re

turn

on

tota

l cap

ital e

mpl

oyed

• N

et a

sset

val

ue p

er sh

are

• D

ivid

ends

per

shar

e•

Earn

ings

per

shar

e

Wee

ks 8

and

9

Unit

3: F

inan

cial

Ac

coun

ting

of

Com

pani

es –

Ana

lysis

an

d In

terp

reta

tion

of

Fina

ncia

l Sta

tem

ents

148–

188

64–8

2

Anal

ysis

of a

com

pany

’s pu

blish

ed fi

nanc

ial s

tate

men

ts a

nd

annu

al re

ports

com

prisi

ng D

irect

ors’

Repo

rt,In

depe

nden

t Aud

itors

’ Rep

ort,

Abrid

ged

Inco

me

Stat

emen

t, Ba

lanc

e Sh

eet a

nd C

ash

Flow

Sta

tem

ent,

toge

ther

with

ad

ditio

nal i

nfor

mat

ion

rela

ting

to g

over

nanc

e an

d th

e co

mpa

ny’s

activ

ities

.

Wee

k 10

Unit

4: F

inan

cial

Ac

coun

ting

of

Com

pani

es –

Ana

lysis

of

Pub

lishe

d Fi

nanc

ial

Stat

emen

ts

189–

209

83–9

0

21GRADE 12ACCOUNTING Term 2

© Shuter & Shooter PublishersACCOUNTING Term 2

Inve

ntor

y va

luat

ion

Valid

atio

n, v

alua

tion

and

calc

ulat

ion

of in

vent

orie

s of b

usin

esse

s us

ing

the

perp

etua

l and

per

iodi

c in

vent

ory

syst

ems:

• Sp

ecifi

c id

entifi

catio

n (o

f cos

t pric

e pe

r uni

t)•

Firs

t in,

firs

t out

(FIF

O)

• W

eigh

ted

Aver

age

Inte

grat

ion

of G

AAP

prin

cipl

es re

latin

g to

inve

ntor

ies

Inte

grat

ion

of e

thic

al is

sues

rela

ting

to in

vent

orie

sIn

tegr

atio

n of

inte

rnal

aud

it an

d co

ntro

l pro

cedu

res r

elat

ing

to

inve

ntor

ies

Wee

ks 1

to 2

Unit

5: In

vent

ory

syst

ems

294–

314

116–

126

Fixe

d As

sets

Inte

rpre

tatio

n an

d re

porti

ng o

n th

e m

ovem

ents

of fi

xed

asse

ts:

• Ag

e of

ass

ets

• Re

plac

emen

t rat

e•

Life

span

of a

sset

sIn

tegr

atio

n of

GAA

P pr

inci

ples

rela

ting

to fi

xed

asse

ts.

Inte

grat

ion

of e

thic

al is

sues

rela

ting

to fi

xed

asse

ts.

Inte

grat

ion

of in

tern

al a

udit

and

cont

rol p

roce

dure

sre

latin

g to

fixe

d as

sets

Wee

ks 3

to 4

Unit

2: Ta

ngib

le (F

ixed

) As

sets

253–

269

104–

108

Inte

rnal

con

trol

Appl

icat

ion

of in

tern

al c

ontro

l and

inte

rnal

aud

itpr

oces

ses i

n a

busin

ess e

nviro

nmen

t:•

Mea

ns o

f gat

herin

g au

dit e

vide

nce

• Ba

sis fo

r gat

herin

g au

dit e

vide

nce

• Ba

sic sa

mpl

ing

tech

niqu

es•

Inte

rnal

aud

it re

ports

• Ac

coun

tabl

e m

anag

emen

t of r

esou

rces

Unde

rsta

ndin

g th

e di

ffere

nce

betw

een

the

role

s of

inte

rnal

and

ext

erna

l aud

itors

This

topi

c sh

ould

be

cons

olid

ated

, hav

ing

been

inte

grat

ed w

ith o

ther

topi

cs.

Unit

4: In

tern

al C

ontro

l27

8–29

311

1–11

5

22 Grade 12 ACCOUNTING Term 2

ACCOUNTING Term 2To

pic

Cont

ent

Tim

e al

loca

tion

Whe

re to

find

it in

Top

Cla

ss A

ccou

ntin

g Gr

ade

12U

nit

LBTG

Cost

ac

coun

ting

Defi

nitio

n an

d ex

plan

atio

n of

acc

ount

ing

conc

epts

uniq

ue to

a m

anuf

actu

ring

busin

ess.

Prep

arat

ion,

pre

sent

atio

n, a

naly

sis, i

nter

pret

atio

nan

d re

porti

ng o

n co

st in

form

atio

n fo

r man

ufac

turin

gen

terp

rises

:•

Prep

arat

ion

of a

pro

duct

ion

cost

stat

emen

t with

not

es fo

r m

anuf

actu

ring

cost

s.•

Prep

arat

ion

of a

shor

t for

m In

com

e St

atem

ent w

ith n

otes

for

adm

inist

ratio

n co

st a

nd se

lling

and

dist

ribut

ion

cost

s.•

Calc

ulat

ion

of g

ross

pro

fit o

n fin

ished

goo

ds so

ld.

• Ca

lcul

atio

n of

var

iabl

e an

d fix

ed c

osts

.•

Calc

ulat

ion

of th

e co

st o

f a p

rodu

ct u

sing

varia

ble

and

fixed

co

sts.

• Ca

lcul

atio

n of

cos

t per

uni

t.•

Calc

ulat

ion

of c

ontri

butio

n pe

r uni

t.•

Calc

ulat

ion

of b

reak

even

poi

nt.

• Ca

lcul

atio

n of

tota

l cos

t of p

rodu

ctio

n.In

tegr

atio

n of

eth

ical

issu

es re

latin

g to

man

ufac

turin

g: p

rodu

ct

age,

raw

mat

eria

ls, su

ppor

t for

loca

l pro

duct

s, pr

ice

fixin

g, th

eft,

fraud

, etc

.In

tegr

atio

n of

inte

rnal

aud

it an

d co

ntro

l pro

cedu

res

rela

ting

to m

anuf

actu

ring.

Wee

ks 5

to 7

Unit

1: C

ost a

ccou

ntin

g39

9–43

815

5–16

9

Reco

ncili

atio

ns

Anal

ysis

and

inte

rpre

tatio

n of

ban

k, d

ebto

rs a

ndcr

edito

rs re

conc

iliat

ions

:•

Reco

ncile

cre

dito

rs’ s

tate

men

ts w

ith th

eir p

erso

nal a

ccou

nts

• Re

conc

ile d

ebto

rs’ l

ists a

nd c

redi

tors

’ list

s with

• co

ntro

l acc

ount

s.•

Anal

yse

and

inte

rpre

t deb

tors

’ age

ana

lysis

• An

alys

e an

d in

terp

ret b

ank

stat

emen

ts a

nd b

ank

reco

ncili

atio

n st

atem

ents

.In

tegr

atio

n of

eth

ical

issu

es re

latin

g to

cas

h, d

ebto

rs a

nd

cred

itors

: pay

men

t per

iods

, int

eres

t, cr

edit

ratin

gs, f

raud

, etc

.In

tegr

atio

n of

inte

rnal

aud

it an

d co

ntro

l iss

ues r

elat

ing

to c

ash,

de

btor

s and

cre

dito

rs.

Wee

ks 8

to 9

Unit

6: R

econ

cilia

tions

315–

356

127–

136

Revi

sion

Revi

sion

of to

pics

cov

ered

dur

ing

the

first

two

term

sW

eeks

10

to 1

1Re

visio

n ex

erci

ses

391–

398

150–

154

23GRADE 12ACCOUNTING Term 3

© Shuter & Shooter PublishersACCOUNTING Term 3

Valu

e Ad

ded

Tax

• VA

T ca

lcul

atio

ns•

Calc

ulat

e th

e am

ount

pay

able

to o

r rec

eiva

ble

from

the

Sout

h Af

rican

Rev

enue

Ser

vice

s (SA

RS)

• Co

mpl

etio

n of

the

VAT

cont

rol l

edge

r acc

ount

from

giv

en

info

rmat

ion

Inte

grat

ion

of e

thic

al is

sues

rela

ting

to V

AT. I

nteg

ratio

n of

in

tern

al a

udit

and

cont

rol p

roce

dure

s rel

atin

g to

VAT

Wee

ks 1

to 2

Unit

7: V

alue

Add

ed Ta

x (V

AT)

357–

390

137–

149

Budg

etin

g

Anal

ysis,

inte

rpre

tatio

n an

d co

mpa

rison

of p

roje

cted

inco

me

stat

emen

ts fo

r the

sole

trad

er o

r com

pani

esPr

ojec

ted

Inco

me

Stat

emen

t:•

Sale

s•

Cost

of s

ales

• Ex

pens

es•

Inco

me

• Pr

ofits

.An

alys

is, in

terp

reta

tion

and

com

paris

on o

f cas

h bu

dget

s for

the

sole

trad

er o

r com

pani

esCa

sh B

udge

ts:

• Re

ceip

ts•

Paym

ents

• D

ebto

rs’ c

olle

ctio

n•

Cred

itors

’ pay

men

t•

Cash

bal

ance

s.In

tegr

atio

n of

eth

ical

issu

es re

latin

g to

bud

getin

g an

d pr

ojec

tions

.In

tegr

atio

n of

inte

rnal

aud

it an

d co

ntro

l pro

cedu

res r

elat

ing

to

rela

ting

to b

udge

ting

and

proj

ectio

ns b

y co

mpa

ring

budg

et to

ac

tual

figu

res.

Wee

ks 3

to 6

Unit

2: B

udge

ting

439–

481

170–

185

Revi

sion

Revi

sion

for e

xam

sW

eeks

7 a

nd 8

Revi

sion

exer

cise

s48

2–49

018

6–19

1

24 Grade 12 ACCOUNTING Term 4

ACCOUNTING Term 4To

pic

Cont

ent

Tim

e al

loca

tion

Whe

re to

find

it in

Top

Cla

ss A

ccou

ntin

g Gr

ade

12U

nit

LBTG

Revi

sion

Revi

sion

of a

ll to

pics

in p

repa

ratio

n fo

r fina

l exa

min

atio

nsW

eeks

1 to

3Re

visio

n ex

erci

ses

494–

534

192–

211

25PROGRAMME OF ASSESSMENT

PROGRAMME OF ASSESSMENT

Grade 10Term Assessment task Page references

1Presentation LB page 126

TG pages 45–51Control Test

2Project LB page 225

TG pages 102–104Control Test

3Case study LB page 278

TG pages 127–130Control Test

4 Final examination LB page 324TG pages 163–171

Grade 11Term Assessment task Page references

1Written report LB page 214

TG pages 87–88Control Test

2Project LB page 325

TG pages 132–135Control Test

3Case Study LB page 463

TG pages 182–183Control Test

4 Final examination LB page 516TG pages 216–228

Grade 12Term Assessment task Page references

1Written report LB page 210

TG page 87–90Control Test

2 Project LB page 386TG page 147–149

3

Case study LB page 477TG page 182–185

Trial examination LB page 535TG page 212–223

4 Final examination

26 PROGRAMME OF ASSESSMENT

27MY NOTES

MY NOTES

28 MY NOTES

MY NOTES

29MY NOTES

SALES CONTACTS

TVET Colleges Vaasna Sing 063 251 8566 [email protected]

Booksellers Vaasna Sing 063 251 8566 [email protected]

Eastern Cape Sydney Nquma 083 253 6761 [email protected]

Free State Dimagatso Makhurane 083 215 6835 [email protected]

Gauteng Themba Msimanga 082 445 6435 [email protected]

KwaZulu-Natal Khanyo Cele 083 281 0849 [email protected]

Limpopo Dimagatso Makhurane 083 215 6835 [email protected]

Mpumalanga Sharmlla Naik 083 287 6883 [email protected]

Northern Cape Colette van der Merwe 071 851 1814 [email protected]

North West Phemelo Maiphehlo 083 378 8725 [email protected]

Western Cape Colette van der Merwe 071 851 1814 [email protected]

Teacher Training Vickesh Thandray 060 545 2264 [email protected]

CUSTOMER SERVICES:Sylvie Doarsamy +27 (0) 33 846 8723 [email protected]

Thandeka Ngcobo +27 (0) 33 846 8724 [email protected]

Zandile Mthethwa +27 (0) 33 846 8721 [email protected]

Mbali Kunene +27 (0) 33 846 8722 [email protected]

HEAD OFFICETel: +27 (0) 33 846 8721 / 22 / 23 / 24

Fax: +27 (0) 33 846 8701

Pietermaritzburg · Johannesburg · Cape Town · East London

OS1

0013

62

www.facebook.com/shuterandshooter • www.shuters.co.za

www.facebook.aceitstudyguides • www.aceitstudyguides.co.za

Top Related