Languages

Pages

Legal

1H15 Earnings Release

Hyundai Capital Services

1

Disclaimer

This presentation material is being presented to you solely for your information only and may not be taken away by you and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, in whole or in part, for any purpose.

These presentation materials have been prepared by Hyundai Capital Services., Inc. (“HCS or the Company”), solely for the use at this presentation and have not been independently verified. No representations or warranties, express or implied, are made as to, and no reliance should be placed on, the accuracy, fairness or completeness of the information presented or contained in this presentation. Neither the Companies nor any of theirs affiliates, advisers or representatives accepts any responsibility whatsoever for any loss or damage arising from any information presented or contained in this presentation. The information presented or contained in this presentation is current as of the date hereof and is subject to change without notice and its accuracy is not guaranteed. Neither the Companies nor any of their affiliates, advisers or representatives make any undertaking to update any such information subsequent to the date hereof. This presentation should not be construed as legal, tax, investment or other advice.

Certain information and statements made in this presentation contain “forward-looking statements.” Such forward-looking statements can be identified by the use of forward-looking terminology such as “anticipate,”“believe,”“considering,”“depends,”“estimate,”“expect,”“intend,”“plan,” “planning, ”planned,” “project,” “trend,” and similar expressions. All forward-looking statements are the Companies’ current expectation of future events and are subject to a number of factors that could cause actual results to differ materially from those described in the forward-looking statements. Caution should be taken with respect to such statements and you should not place undue reliance on any such forward-looking statements.

Certain industry and market data in this presentation was obtained from various trade associations, and the Companies have not verified such data with independent sources. Accordingly, the Companies make no representations as to the accuracy or completeness of that data, and such data involves risks and uncertainties and is subject to change based on various factors.

This presentation does not constitute an offer or invitation to purchase or subscribe for any shares or other securities of the Companies and neither any part of this presentation nor any information or statement contained therein shall form the basis of or be relied upon in connection with any contract or commitment whatsoever. Any decision to purchase shares in any offering of shares of the Companies should be made solely on the basis of the information contained in the offering document which may be published or distributed in due course in connection with any offering of shares of the Companies, if any.

2

Major Issues in 1H15

Asset growth through Enhanced Business as a Captive Finance despite unfavorable market conditions

Laid foundations for better profitability through Asset Quality improvement and Bad Debt Expense decrease, as a result of constant risk management.

Overseas operation expansion through strengthened Global Business capabilities

3

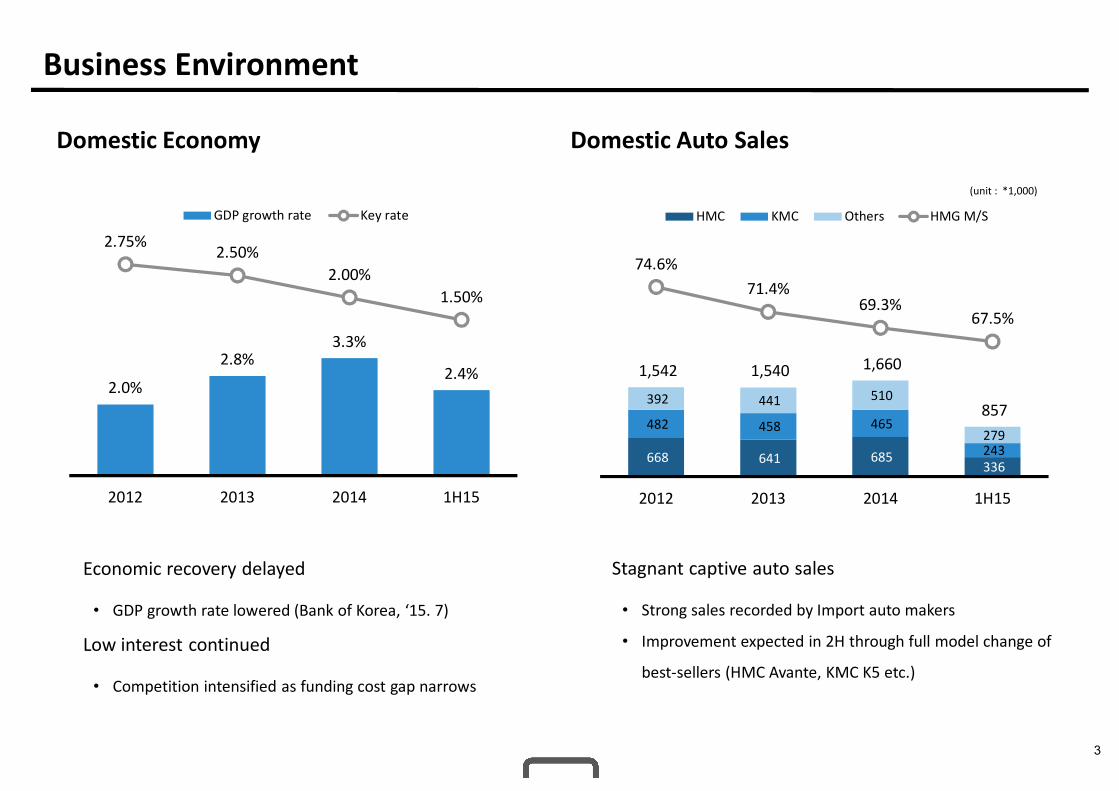

Business Environment

Domestic Economy Domestic Auto Sales

Stagnant captive auto sales

• Strong sales recorded by Import auto makers

• Improvement expected in 2H through full model change of

best-sellers (HMC Avante, KMC K5 etc.)

(unit : *1,000)

Economic recovery delayed

• GDP growth rate lowered (Bank of Korea, ‘15. 7)

Low interest continued

• Competition intensified as funding cost gap narrows

2.0%

2.8%3.3%

2.4%

2.75% 2.50%2.00%

1.50%

2012 2013 2014 1H15

GDP growth rate Key rate

668 641 685 336

482 458 465

243

392 441 510

279

1,542 1,540 1,660

857

74.6%71.4%

69.3%67.5%

2012 2013 2014 1H15

HMC KMC Others HMG M/S

4

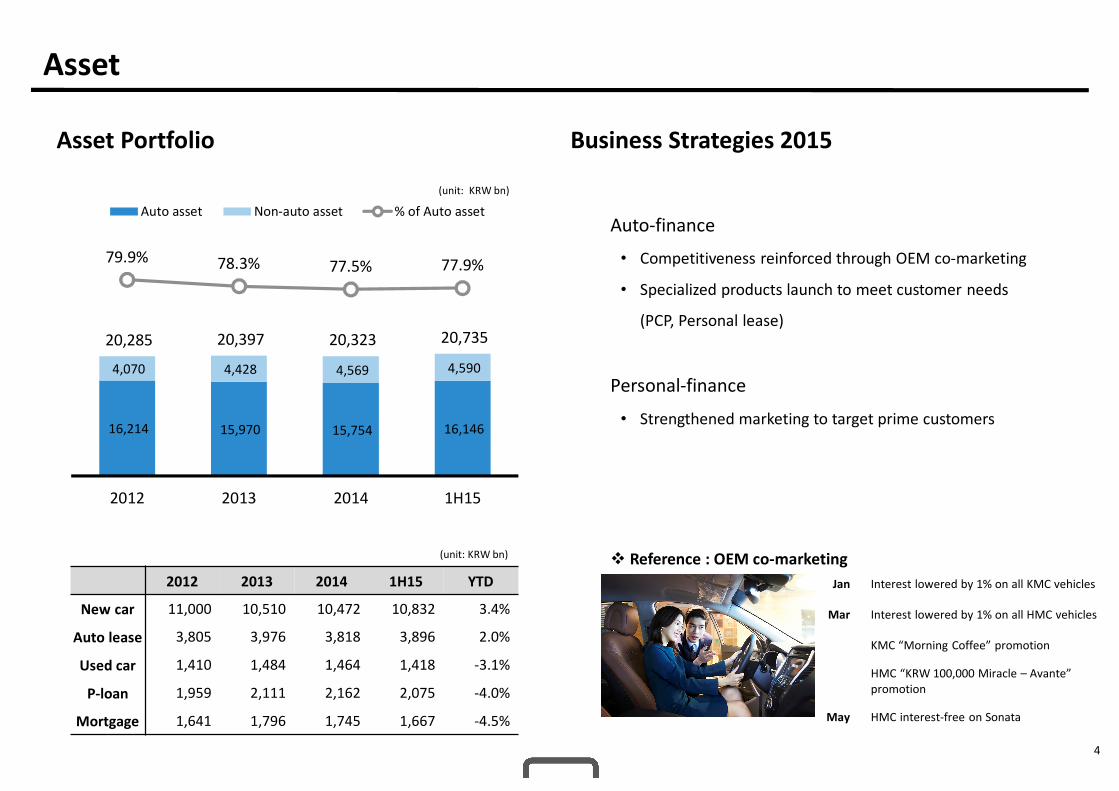

Asset

Asset Portfolio Business Strategies 2015

(unit: KRW bn)

2012 2013 2014 1H15 YTD

New car 11,000 10,510 10,472 10,832 3.4%

Auto lease 3,805 3,976 3,818 3,896 2.0%

Used car 1,410 1,484 1,464 1,418 -3.1%

P-loan 1,959 2,111 2,162 2,075 -4.0%

Mortgage 1,641 1,796 1,745 1,667 -4.5%

Auto-finance

• Competitiveness reinforced through OEM co-marketing

• Specialized products launch to meet customer needs

(PCP, Personal lease)

Personal-finance

• Strengthened marketing to target prime customers

Reference : OEM co-marketing(unit: KRW bn)

Jan Interest lowered by 1% on all KMC vehicles

Mar Interest lowered by 1% on all HMC vehicles

KMC “Morning Coffee” promotion

HMC “KRW 100,000 Miracle – Avante” promotion

May HMC interest-free on Sonata

16,214 15,970 15,754 16,146

4,070 4,428 4,569 4,590

20,285 20,397 20,323 20,735

79.9% 78.3% 77.5% 77.9%

2012 2013 2014 1H15

Auto asset Non-auto asset % of Auto asset

5

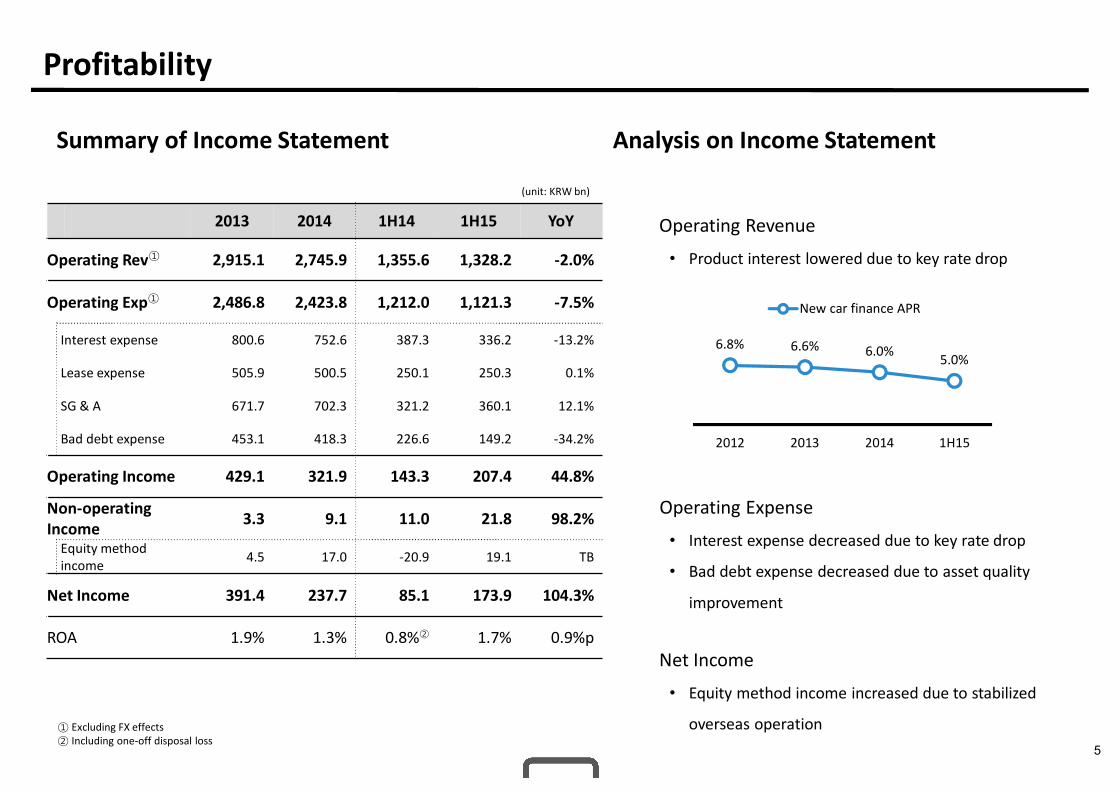

Profitability

① Excluding FX effects② Including one-off disposal loss

Summary of Income Statement

2013 2014 1H14 1H15 YoY

Operating Rev① 2,915.1 2,745.9 1,355.6 1,328.2 -2.0%

Operating Exp① 2,486.8 2,423.8 1,212.0 1,121.3 -7.5%

Interest expense 800.6 752.6 387.3 336.2 -13.2%

Lease expense 505.9 500.5 250.1 250.3 0.1%

SG & A 671.7 702.3 321.2 360.1 12.1%

Bad debt expense 453.1 418.3 226.6 149.2 -34.2%

Operating Income 429.1 321.9 143.3 207.4 44.8%

Non-operating Income 3.3 9.1 11.0 21.8 98.2%

Equity method income 4.5 17.0 -20.9 19.1 TB

Net Income 391.4 237.7 85.1 173.9 104.3%

ROA 1.9% 1.3% 0.8%② 1.7% 0.9%p

Analysis on Income Statement

Operating Revenue

• Product interest lowered due to key rate drop

Operating Expense

• Interest expense decreased due to key rate drop

• Bad debt expense decreased due to asset quality

improvement

Net Income

• Equity method income increased due to stabilized

overseas operation

(unit: KRW bn)

6.8% 6.6% 6.0% 5.0%

2012 2013 2014 1H15

New car finance APR

6

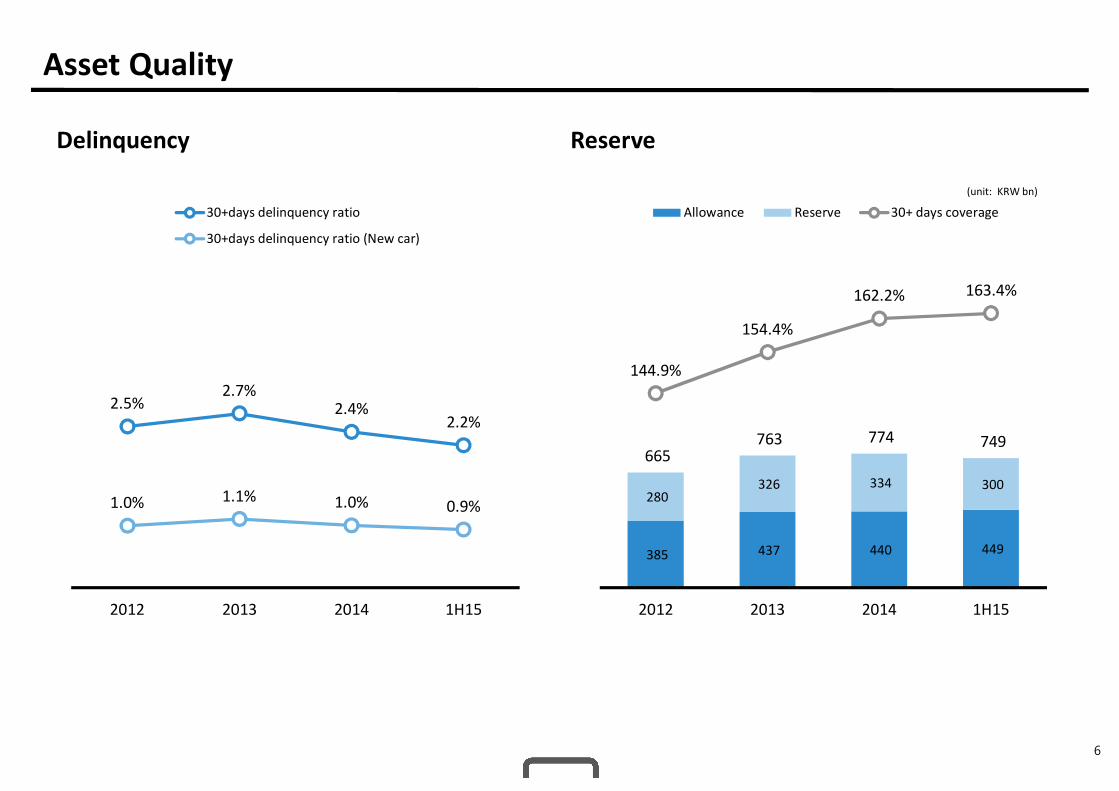

Asset Quality

Delinquency Reserve

(unit: KRW bn)

2.5%2.7%

2.4%2.2%

1.0% 1.1% 1.0% 0.9%

2012 2013 2014 1H15

30+days delinquency ratio

30+days delinquency ratio (New car)

385 437 440 449

280 326 334 300

665 763 774 749

144.9%

154.4%

162.2% 163.4%

2012 2013 2014 1H15

Allowance Reserve 30+ days coverage

7

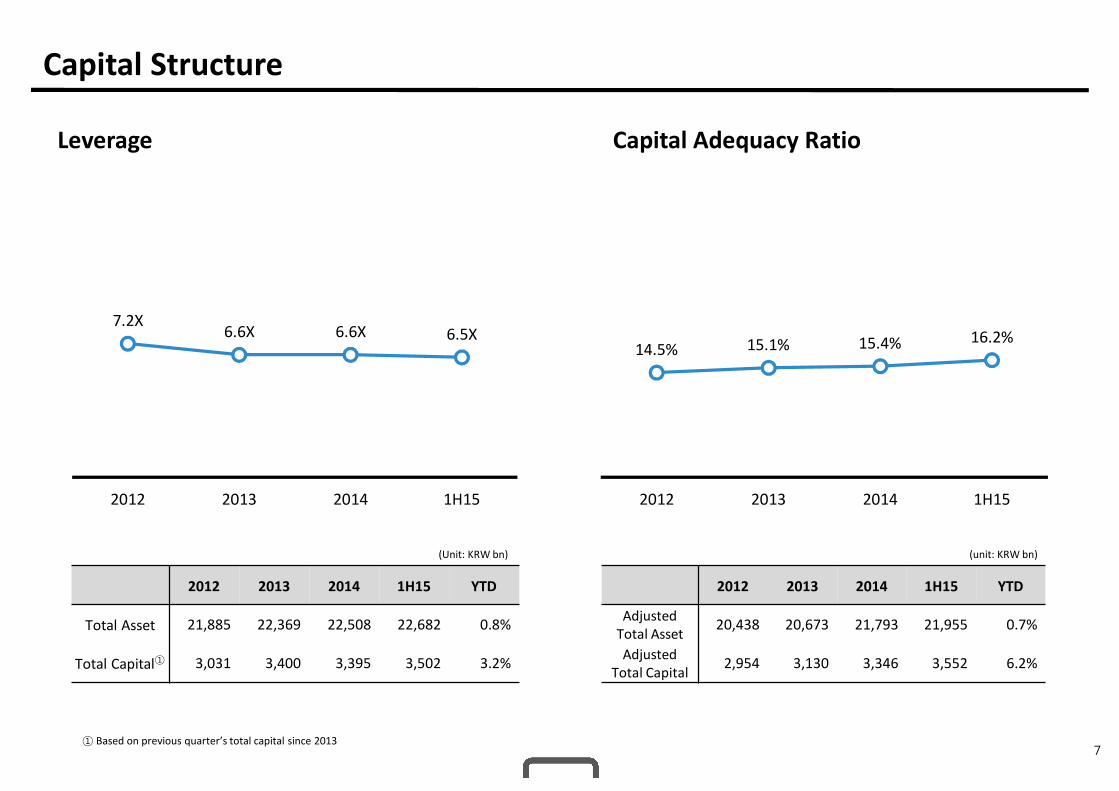

Capital Structure

Capital Adequacy RatioLeverage

① Based on previous quarter’s total capital since 2013

2012 2013 2014 1H15 YTD

Total Asset 21,885 22,369 22,508 22,682 0.8%

Total Capital① 3,031 3,400 3,395 3,502 3.2%

(unit: KRW bn)

2012 2013 2014 1H15 YTD

AdjustedTotal Asset 20,438 20,673 21,793 21,955 0.7%

AdjustedTotal Capital 2,954 3,130 3,346 3,552 6.2%

(Unit: KRW bn)

7.2X6.6X 6.6X 6.5X

2012 2013 2014 1H15

14.5% 15.1% 15.4% 16.2%

2012 2013 2014 1H15

8

Domestic bond56.1%

Overseas bond22.0%

Domestic ABS9.3%

Overseas ABS3.9%

Loans7.2%

CP1.5%

Funding

Funding Portfolio by product Asset-Liability Maturity

2014 1H15

Total Funding 5,893 3,317Bond 3,353 1,957

Domestic 2,510 1,511

Overseas 843 446

ABS 600 400CP, Bank loan 1,940 960

2014 1H15

(unit: KRW bn)Funding Guidelines

• Long-term debt : 60% or more

• By Product: ABS <20%, CP <10%

• ALM ratio : 100% or more

2.0yr 2.0yr 1.9yr2.0yr

148.0%142.0%

132.0%139.2%

2012 2013 2014 1H15

Debt maturity ALM ratio

Domestic bond52.0%Overseas

bond26.2%

Domestic ABS7.6%

Overseas ABS5.3%

Loans7.8%

CP1.1%

KRW17.8tn

KRW17.8tn

9

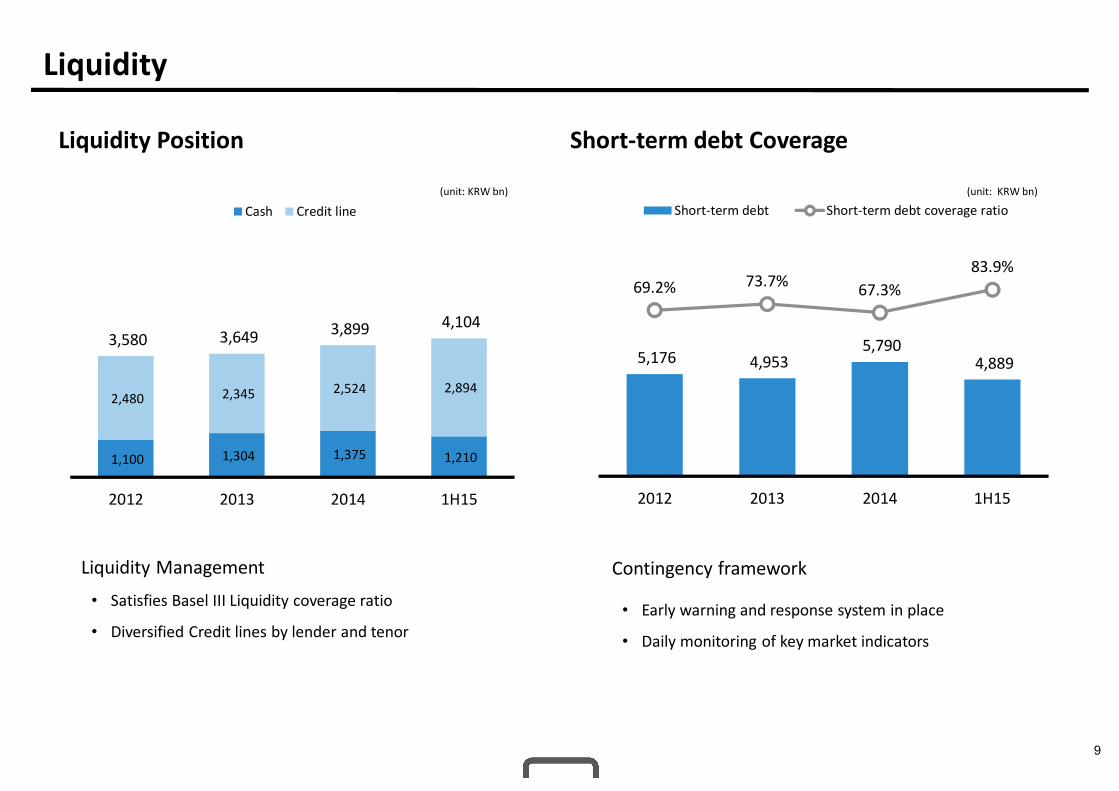

Liquidity

Liquidity Position Short-term debt Coverage

Contingency framework

• Early warning and response system in place

• Daily monitoring of key market indicators

(unit: KRW bn) (unit: KRW bn)

Liquidity Management

• Satisfies Basel III Liquidity coverage ratio

• Diversified Credit lines by lender and tenor

1,100 1,304 1,375 1,210

2,480 2,345 2,524 2,894

3,580 3,649 3,899 4,104

2012 2013 2014 1H15

Cash Credit line

5,176 4,953 5,790

4,889

69.2% 73.7% 67.3%83.9%

2012 2013 2014 1H15

Short-term debt Short-term debt coverage ratio

10

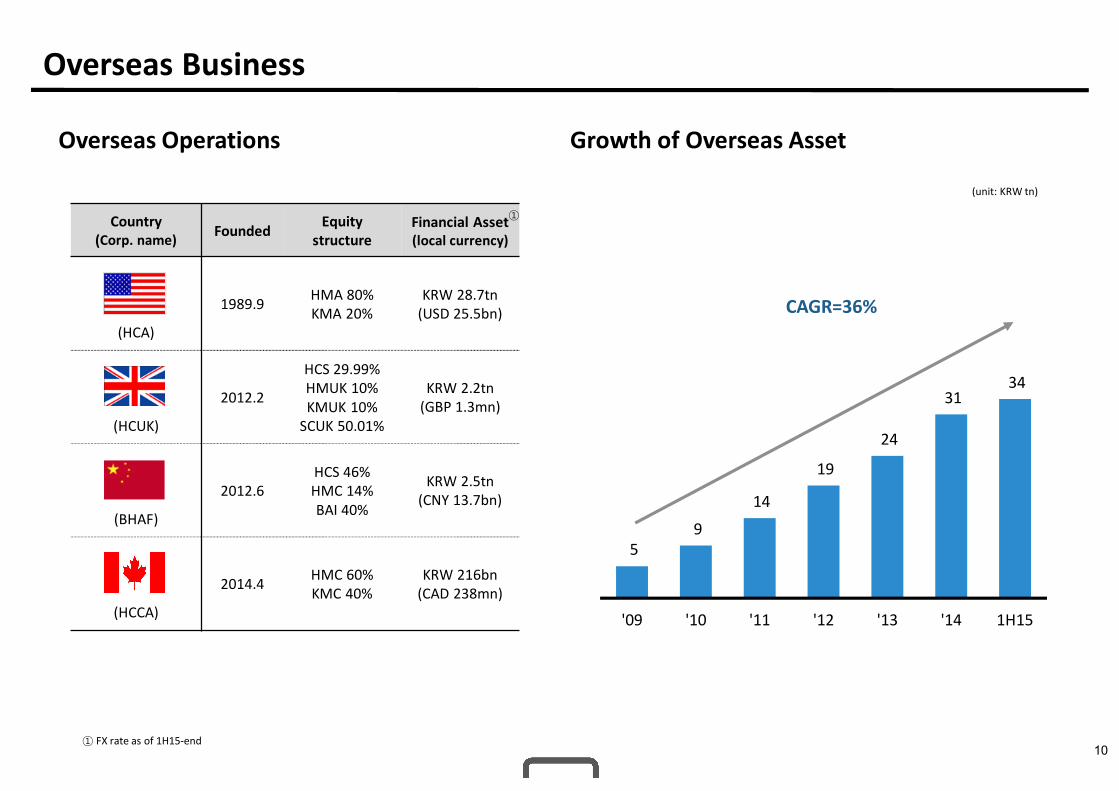

Overseas Business

Overseas Operations

Country(Corp. name) Founded Equity

structureFinancial Asset(local currency)

(HCA)

1989.9 HMA 80%KMA 20%

KRW 28.7tn(USD 25.5bn)

(HCUK)

2012.2

HCS 29.99%HMUK 10% KMUK 10%

SCUK 50.01%

KRW 2.2tn(GBP 1.3mn)

(BHAF)

2012.6HCS 46%HMC 14%BAI 40%

KRW 2.5tn(CNY 13.7bn)

(HCCA)

2014.4 HMC 60% KMC 40%

KRW 216bn(CAD 238mn)

Growth of Overseas Asset

(unit: KRW tn)

CAGR=36%

① FX rate as of 1H15-end

①

5 9

14

19

24

31 34

'09 '10 '11 '12 '13 '14 1H15

11

Appendix

Personal Lease Launch Certified Used Car Center Open

Reinforce Auto-finance Value chain

• Utilize systematically managed Lease-returned vehicles

• Manage Vehicles’ residual value efficiently

Initiate changes on vehicle “possession”

• Boost new car sales and shorten replacement period

• “Use” easy-to-manage cars on lower monthly payment