Languages

Pages

Legal

Agenda

CEO’s reviewVeli-Matti Mattila, CEO

Financial reviewJari Kinnunen, CFO

2

CEO’s review

• Q2 2011 financial and operational highlights• Segment review• Execution of the strategy• Progress of new services and smartphone market development• Outlook for 2011

3

Q2 2011 highlights

• Strong revenue growth continued• Profitability was at a good level• Mobile subscription base and usage continued to grow• Smartphone market and 3G data services continued strong

growth trend• New data roaming service – predictable cost and excellent

coverage across Europe• New video conferencing service for corporate customers

4

Q2 2011 financial highlights

New services and smartphones boosted revenue

• Revenue € 378m (364)– Growth in equipment sales, mobile,

online and ICT services– Decrease in fixed telephony business

and MTR• EBITDA € 121m (119)• CAPEX € 54m (47), 14% of revenue

– Excluding IFRS booking of the new lease agreement € 47m, 12% of revenue

• Net debt € 845m (752)– Cash flow € 59m– Net debt / EBITDA 1.7 (1.5)

5

355 360 365353

364 363

383374 378

33 %

36 %

33 % 33 % 33 %35 %

32 %31 %

32 %

Q2/09 Q3/09 Q4/09 Q1/10 Q2/10 Q3/10 Q4/10 Q1/11 Q2/11

Revenue, EURm EBITDA-%

Q2 2011 operative highlights

Strong growth in mobile subscriptions continued

• Mobile net adds 92,500 in Q2/11– Growth in both customer segments– Strongest growth in mobile broadband– Estonia +14,600 subscriptions

• Slight decrease in fixed broadband– Decrease 3,000 subscriptions in Q2/11– Seasonality

6

3 153 3 2183 329

3 4323 550

3 6523 797

3 898 3 991

482 476 467 462 462 464 467 478 475

Q2/09 Q3/09 Q4/09 Q1/10 Q2/10 Q3/10 Q4/10 Q1/11 Q2/11

Mobile subs ('000) Fixed broadband subs ('000)

Q2 2011 operative highlights

Mobile churn decrease continued

• Growth in mobile services– Outgoing minutes growth +3% YoY– SMS growth +9% YoY

• Mobile churn 11.9% (15.9)– Both voice and mobile broadband

churns decreased– Competition has remained keen

7

1 589 1 586

1 645 1 652

1 719 1 707

1 749 1 739

1 76814,7 % 14,5 % 14,7 %

15,4 % 15,9 %

18,1 %

15,0 %14,3 %

11,9 %

Q2/09 Q3/09 Q4/09 Q1/10 Q2/10 Q3/10 Q4/10 Q1/11 Q2/11

Usage (outgoing minutes, million) Churn*

* Annualised

Business Segments

8

Q2 2011 Consumer Customers

Growth in online services and equipment sales

• Revenue € 227m (217)– Growth in mobile usage, smartphone

sales and online services– Decrease in fixed telephony business

and mobile interconnection revenue• EBITDA € 72m (68), 32% of revenue

– Revenue growth– Cost efficiency

• CAPEX € 32m (27)

9

209220 217 214 217

225 229224 227

33 %

37 %

33 %34 %

31 %

34 %

31 %30 %

32 %

Q2/09 Q3/09 Q4/09 Q1/10 Q2/10 Q3/10 Q4/10 Q1/11 Q2/11

Revenue, EURm EBITDA-%

Q2 2011 Corporate Customers

Growth in corporate customers’ ICT services

• Revenue € 150m (147)– Growth in ICT services and equipment

sales– Decrease in fixed network business

and mobile interconnection revenue• EBITDA € 49m (51), 32% of revenue

– Investments in ICT and video conferencing services

• CAPEX € 22m (20)

10

146

139

148

139

147

139

154150 150

33 %

36 %34 %

31 %

34 %36 %

34 % 34 %32 %

Q2/09 Q3/09 Q4/09 Q1/10 Q2/10 Q3/10 Q4/10 Q1/11 Q2/11

Revenue, EURm EBITDA-%

11

Integration of One Elisa

New services and new markets

Strengthening marketposition in core markets

Strategy execution

Mobile broadband and smartphones growth continues

• Broad assortment of smartphones

• Smartphones top the list of most sold phones in June 2011

1. iPhone 4 2. Nokia C2-01 (feature phone)3. Samsung Galaxy Gio4. Nokia C6-015. ZTE Blade6. Samsung Galaxy S II

• 64% of all models sold were smartphones in Q2/2011

– In Q1/2011 50%, year ago 3%

12

11,5 %

17,0 %

19,5 %

22,0 %23,5 %

26,0 %

0,4 % 0,5 %1,5 %

3,5 %

6,5 %8,0 %

Q1/10 Q2/10 Q3/10 Q4/10 Q1/11 Q2/11

Mobile broadband penetration 1) Smartphone penetration 2)

1) Dongles and mobile BB add-on services of the total subscription base2) iOS (iPhone), Android ,Symbian 3^ and Windows phones

of the total phone base

Penetrations in Elisa’s network in Finland

1) Mobile BB penetration restated based on Ficora’sdefinition. Includes also multi-SIM BB subscriptions

Best 3G coverage in Finland

• Elisa’s investments in 3G network guarantee high quality user experience

• Research of European Communications Engineering, spring 2011

– Best 3G coverage– Most 3G base stations– Lowest interference levels

Bringio – new video conferencing service for corporate

• World’s first multiparty and multideviceHD video conferencing

• Video conferencing between– mobile phones– tablets– laptops– video conference rooms

€1/MB up to 5 MB

€4/MBup to 5 MB

€15/50 MB €50/50 MB

In the EU area Globally

Transparency for data roaming: Elisa Daily Traveller

• Predictable pricing for data usage abroad– mobile devices– laptops

• Excellent coverage through cooperation with Vodafone and Telenor

Outlook for 2011

• Positive trends of the Finnish economy have continued

• Competition remains challenging

• Slight increase in revenue

• EBITDA excluding one-offs to improve slightly

• CAPEX maximum 12 per cent of revenue

16

Agenda

CEO’s reviewVeli-Matti Mattila, CEO

Financial reviewJari Kinnunen, CFO

17

Revenue and earnings continued to grow

18

1) 1H/11 EBITDA excluding one off items EUR 240m2) CDO guarantee expense in H1/10 EUR 45m, and in 2010 EUR 40m

EUR million Q2/11 Q2/10 Δ 1H/11 1H/110 Δ 2010Revenue 378 364 13 752 717 35 1463Other operating income 2 1 3 2 5Operating expenses -259 -247 -12 -516 -485 -31 -984EBITDA 1) 121 119 2 239 234 5 485EBITDA-% 32 % 33 % 32 % 33 % 33 %Depreciation and amortisation -53 -54 2 -105 -108 3 -217EBIT 69 65 4 134 126 8 268EBIT-% 18 % 18 % 18 % 18 % 18 %Profit before tax 61 53 8 119 63 56 197Profit before taxes w/o one-off 2) 61 53 8 119 107 12 237Income taxes -16 -13 -3 -31 -15 -16 -47Profit for the period 45 40 5 88 48 40 151Profit for the period w/o one-off 2) 45 40 5 88 81 7 180EPS, EUR/share 0.29 0.26 0.03 0.56 0.31 0.25 0.96 EPS w/o one-off 1) 0.29 0.26 0.03 0.56 0.52 0.04 1.15

Revenue change YoY

19

22

13

Q2 2011

378

Corporatecustomers

Consumer customers

Equipment salesInterconnection and roaming

-4

Q2 2010

364+ Mobile+ Online Services+ Estonia- Fixed broadband- Cable TV- PSTN

+ ICT services+ M&A +/- Estonia- Mobile- PSTN

- MTR reduction+ Smartphones

Equipment sales and acquisitions increased OPEX

• OPEX decreases– Interconnections and roaming– Productivity improvements

– Network operating expenses– e.g. marketing and administration

• OPEX increases– Cost of equipment sales– Acquisitions in 2010

– Videra (June 2010) and Appelsiini(December 2010)

– Personnel expenses– Acquired companies in 2010– Salary increases based on collective

labor agreements 1 October 2010

20

EURmQ2 10

Q3 10

Q4 10

Q1 11

Q2 11

Materials and services 148 148 163 158 159

Employee benefit expenses

52 46 55 58 57

Other operating expenses 46 42 44 41 43

Total expenses 247 237 262 257 259

Depreciation 54 54 55 52 53

CAPEX/Sales in line with guidance

• Total CAPEX in Q2 EUR 54m (47), excl. new long term lease EUR 47m

– CAPEX/Sales 12% (13%) 1)

– Long-term data center infrastructure lease agreement classified as CAPEX in IFRS

• Q2/11 by segments 1)

– Consumer EUR 28m (27)– Corporate EUR 19m (20)

• Major CAPEX areas– Fixed access and backbone networks– 3G network– Customer equipment– IT systems

21

19 22

33

24 27 2631

2328

1719

28

15

2016

25

18

191

11

4

2010 %

11 %

17 %

11 %13 %

11 %

15 %

11 %12 %

-20 %

-15 %

-10 %

-5 %

0 %

5 %

10 %

15 %

20 %

Q2/09 Q3/09 Q4/09 Q1/10 Q2/10 Q3/10 Q4/10 Q1/11 Q2/11 1)

Consumer Corporate Shares 2) Capex/Sales

1) Excluding EUR 7m data center infrastructure lease Q2/112) Including acquisitions of business assets

Cash flow

22

EUR million Q2/11 Q2/10 Δ H1/11 H1/10 Δ 2010EBITDA 121 119 2 239 234 5 485Change in receivables 9 16 -7 12 21 -9 2Change in inventories 1 -2 3 -4 1 -5 -6Change in payables -21 6 -27 -33 -6 -27 11

Change in NWC -11 20 -31 -25 16 -41 7Finance income and expenses -1 0 -1 -18 -15 -3 -28CDO Guarantee settlement 0 0 0 0 0 0 -40

Financials (net) -1 0 -1 -18 -15 -3 -68Taxes for the year -11 -13 2 -26 -25 0 -47Taxes for the previous year 0 -6 6 0 -6 6 -6

Taxes -11 -19 8 -26 -31 6 -53CAPEX -45 -46 1 -86 -85 -1 -182Investments in shares 0 -5 5 -5 -5 0 -19Sale of assets and adjustments 5 1 4 6 2 4 2Cash flow after investments 59 70 -11 86 115 -29 172

Cash Flow after investments excl. one-off items 59 70 -11 86 115 -29 212

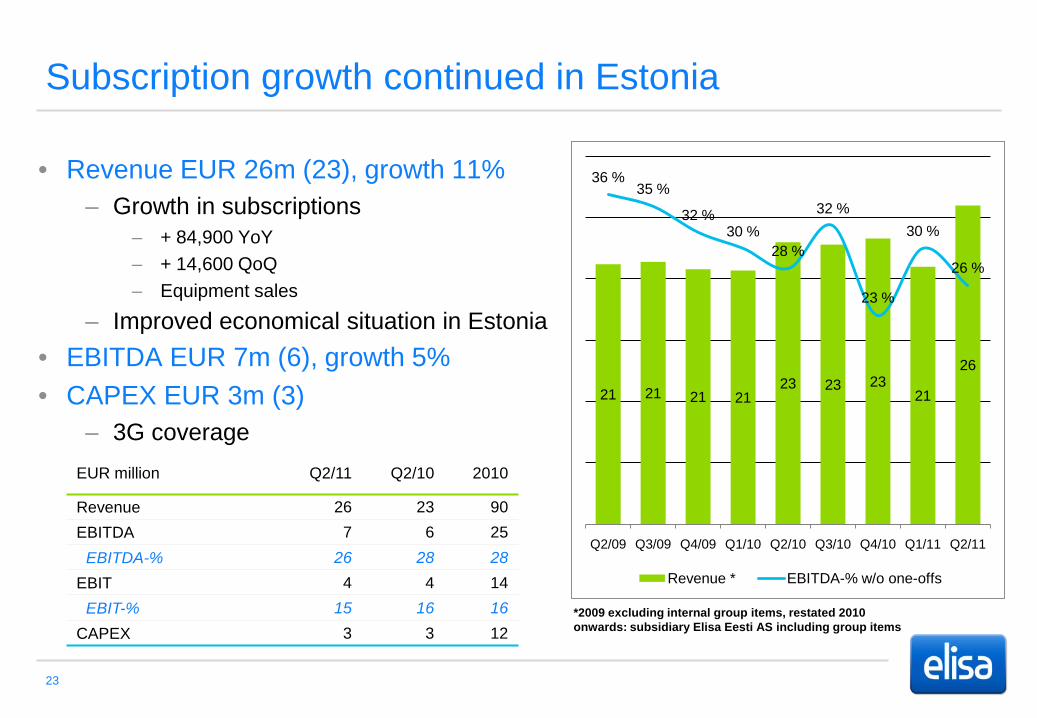

Subscription growth continued in Estonia

• Revenue EUR 26m (23), growth 11%– Growth in subscriptions

– + 84,900 YoY– + 14,600 QoQ– Equipment sales

– Improved economical situation in Estonia• EBITDA EUR 7m (6), growth 5% • CAPEX EUR 3m (3)

– 3G coverage

23

21 21 21 2123 23 23

21

26

36 %35 %

32 %30 %

28 %

32 %

23 %

30 %

26 %

Q2/09 Q3/09 Q4/09 Q1/10 Q2/10 Q3/10 Q4/10 Q1/11 Q2/11

Revenue * EBITDA-% w/o one-offs

EUR million Q2/11 Q2/10 2010

Revenue 26 23 90EBITDA 7 6 25

EBITDA-% 26 28 28EBIT 4 4 14

EBIT-% 15 16 16CAPEX 3 3 12

*2009 excluding internal group items, restated 2010 onwards: subsidiary Elisa Eesti AS including group items

Liquidity position is good, RCF EUR 170m extended

• Cash and undrawn committed facilities EUR 302m (300)

• Revolving Credit Facilities– EUR 130m maturing Nov 2014– EUR 170m maturing Jun 2016, re-

arranged in June 2011• Commercial Paper Program

– EUR 160m in use• Credit ratings constant since 2003

– S&P BBB/Stable outlook– Moody’s Baa2/Stable outlook

24

Bond and Bank loan maturities

226

75

300

10

10 10 10 10

2011 2012 2013 2014 2015 2016 2017 2018

Bonds Loans

Capital structure in line with targets

• Capital structure – Net debt / EBITDA 1.7– Gearing 108%, Equity ratio 40%

• Target setting– Net debt / EBITDA 1.5 – 2x– Equity ratio >35%

25

773 729 719817 752 725 776 752

845

1,61,5 1,5

1,7

1,5 1,51,6

1,5

1,7

45 % 48 % 46 % 40 % 42 % 45 % 43 % 38 % 40 %

Q2/09 Q3/09 Q4/09 Q1/10 Q2/10 Q3/10 Q4/10 Q1/11 Q2/11

Net Debt, EURm Net Debt/EBITDAEquity ratio %

New MTRs agreed until November 2014

26

• Decreases mobile revenue and costs• Neutral for EBITDA• No direct impact on end user prices

Mobile Termination Price per minute, euro cents

Operator 1 Dec 2010 1 Dec 2011 1 Dec 2012-30 Nov 2014

Elisa 4.4 3.82 2.8

TeliaSonera 4.4 3.82 2.8

DNA 4.4 3.82 2.8

Competitive profit distribution

• Distribution capabilities maintained• Capital structure targets unchanged• Cash Flow generation in focus

– Net debt/EBITDA and gearing expected to decrease

• Authorisation max EUR 70m dividend or max 5 million shares buy back

– Board of Directors plans to pay EUR 0.40 per share

– If paid pro forma dividend yield 8% *

* Total profit distribution / share price as 30 December 2010 (€ 16.27)

27

123 116

402

285

156221

140

79

86

43

77 %

110 %

302 %

149 %

88 %

126 %

94 %

2005 2006 2007 2008 2009 2010 2011e

Dividend / capital repayment Buy-back

EUR 0.40 add. dividend* Pay-out ratio %

136%

* if decided by BoD

APPENDIX SLIDE

Consolidated Cash flow statement

29

EUR million Q2 2011 Q1 2011 Q4 2010 Q3 2010 Q2 2010 Q1 2010 Q4 2009 Q3 2009 Q2 2009Cash flow from operating activitiesProfit before tax 61 58 66 68 53 10 56 70 56Adjustments to profit before tax 61 59 56 60 67 106 64 60 60Change in working capital -11 -13 18 -27 20 -4 26 -23 30Cash flow from operating activities 111 103 140 101 140 112 146 107 146

Received dividends and interests and interest paid 1) -1 -17 -41 -11 0 -15 -1 -12 -2Taxes paid -11 -15 -6 -16 -19 -13 -11 -11 -18Net cash flow from operating activities 99 71 92 74 121 84 134 84 127

Cash flow in investmentsCapital expenditure -45 -41 -55 -42 -46 -38 -61 -40 -36Investments in shares and other investments 0 -5 -10 -4 -5 -1 0 -2Proceeds from asset disposal 5 2 1 0 1 0 0 1Net cash used in investment -40 -44 -64 -45 -51 -39 -61 -41 -37

Cash flow after investments 59 27 28 29 70 45 74 43 89

Cash flow in financingShare Buy Backs and sales (net)Change in interest-bearing receivablesChange in long-term debt 0 0 0 -30 25 -36Change in short-term debt 80 -14 65 -42 -33 69 13 -62 -47Repayment of financing leases -2 -1 -1 -1 -1 -1 -1 -1 -1Dividends paid -140 0 -78 -1 -143 -63 0 -8Cash flow in financing -62 -15 -13 -43 -65 -50 -51 -64 -92

Change in cash and cash equivalents -2 12 15 -15 5 -5 22 -20 -2

1) Includes non recurring item: CDO guarantee settlement Q4/10

APPENDIX SLIDE

Financial situation

30

EUR Million 30 Jun 11 31 Mar 11 31 Dec 210 30 Sep 10 30 Jun 10 31 Mar 10 31 Dec 09 30 Sep 09 30 Jun 09

Interest-bearing debt Bonds and notes 600 600 599 598 598 597 572 572 570 Commercial Papers 160 120 102 68 110 118 74 62 119 Loans from financial institutions 51 52 52 52 52 80 80 80 80 Financial leases 35 24 23 23 24 23 23 24 27 Committed credit lines 1) 40 0 32 0 0 25 0 0 5 Others 2) 0 0 0 0 0 0 0 0 1Interest-bearing debt, total 887 795 808 742 784 843 750 738 802

Security depositsSecuritiesCash and cash equivalents 42 44 32 17 32 26 31 9 29Interest-bearing receivables 42 44 32 17 32 26 31 9 29

Net debt 3) 845 752 776 725 752 817 719 729 773

1) The committed credit lines are EUR 130 million and EUR 170 million revolving credit facilities with five banks, which Elisa Corporation may use flexibly on agreed pricing. The loan arrangements are valid until 23 November 2014 and 3 June 2016.2) Redemption liability for minorities3) Net debt is interest-bearing debt less cash and interest-bearing receivables.

Top Related