Languages

Pages

Legal

1

Women’s Policy, Inc.Washington, DC

November 10, 2010

Lynne Cutler, President

2010 Chestnut StreetPhiladelphia, PA 19103

Telephone: (215) 564-5500 Facsimile: (215) 564-0933Website: www.worc-pa.com

2

Mission, Services, & Philosophy

Mission To promote social and economic self-sufficiency for economically

disadvantaged women and their families.

Services Microenterprise Training

Microenterprise is a business with:

1-5 employees

Capital needs under $35,000 (50k)

Access to Capital

Incentive Savings Program

Philosophy Asset-Building Strategy

3

WORC Accomplishments

Impact Trained 3,000 individuals; 800+ businesses currently

generate $20 Million in annual revenues;

361 loans totaling $1.18 million 1000+IDA graduates; Economic impact of $36.7

million. Awards/ Recognition

Presidential Award for Excellence in Microenterprise Development, U.S. Department of Treasury (2001).

Technology Innovation Award for Building Blocks to Financial Success (2005).

4

Financial Disparity in America

Income Poverty: 12.3% of Americans live

below federal income poverty line

Asset Poverty: 27.3% of families with

children have less than 3 months’ savings

37.2% of minority population have zero or negative assets

Statistics: CFED Assets and Opportunities Scorecard, 2010

Why Microenterprise? History

WORC’s Microenterprise Program Started in 1985 500+ Microenterprise Programs nationwide

Importance Viable Career Path Small Business

Small businesses created 60-80% of the net new jobs since the mid-1990’s.

87% of all businesses in US today are microenterprises Women start businesses at twice the rate of men

Strengthen Communities Buy local Tax revenue

Precious Jewels Daycare – Elsie D

Home-based day care center since 1998 with 3 employees.

Revenues of approximately $75,000/year.

Developed business plan and registered business as S Corp.

$1,800 loan to buy a computer, fax machine and copier and a $2,500 loan for a down payment to expand her business to a larger facility.

Grew business – also trains Haitian immigrants on establishing of day care business

7

Classic Design Jewelers - Diane C.

Virtual jewelry store - 1998 Two employees $150,000 annual gross sales

8

Why Microenterprise?

1990-91 & 2001-02 recessions: More businesses started up than closed down Creation rate goes up in a downturn

"Starting a business in a recession is like vacationing in the off-season. It's a little less

crowded, and everything starts going on sale.“–Eric Ryan, Method Cleaning Products

Statistics: SBA, US News & World Report, NWBC, US Census

9

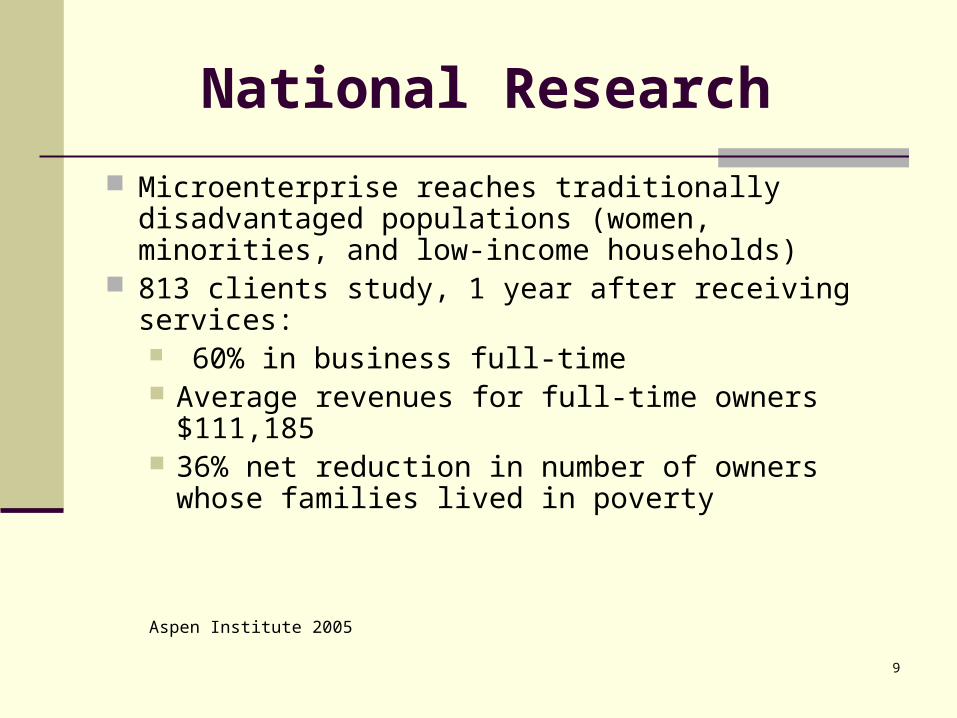

National Research

Microenterprise reaches traditionally disadvantaged populations (women, minorities, and low-income households)

813 clients study, 1 year after receiving services: 60% in business full-time Average revenues for full-time owners $111,185 36% net reduction in number of owners whose

families lived in poverty

Aspen Institute 2005

10

WORC’s Microenterprise Training Program

Training 36 hours, 6 weeks, 2 times per

week. Management, Marketing, and

Financial. Trainers with business experience.

Individual Business Assistance Market Access/ Commercial

Linkages WORCweb.com: Online business

directory. Access to contract opportunities. Participation at expos.

Capital

11

WORC’s Training Impact

70% complete training 40% start or expand their business

within six months 30% employed or pursue further

training 50% stay in business over time

12

Keys to Success

Practical / action-oriented Trainers - business people Intake criteria Peer support One-on-one counseling Access to capital Market access & commercial linkages On-going support

13

Markets Served

Low-income/Underemployed workers People with disabilities Dislocated workers (SEA) Retirees (RIS) Immigrants

14

Self-Employment Assistance (SEA) Program

1993 North American Free Trade Agreement (NAFTA) HR Bill 3450, Title V, Sec. 507

Allows unemployed individuals to receive UC benefits while starting a business.

8 states participate: DE, ME, MD, NJ, NY, OR, PA, WA

1997 PA HR Bill No: 1475 established PA SEA Program

PA SEA Results – 1997 to 2008 Over 1,700 businesses statewide

$45 million in annual revenues $8.8 million employee annual earnings

15

SEA Program Results

Overall Results 800 businesses

$20 Million annual gross revenue 250 additional jobs created $4.6 Million annualized payroll

Aspen Institute Follow-Up Study FY 2006 WORC Participants 73% operating a business one year after receiving services 90% still in business at 18 months $4 million gross annual revenues with estimated $240,000 sales

tax revenue in 2007 1 in 5 businesses created new jobs Cost per business created $4,315 Cost per job $2,890

16

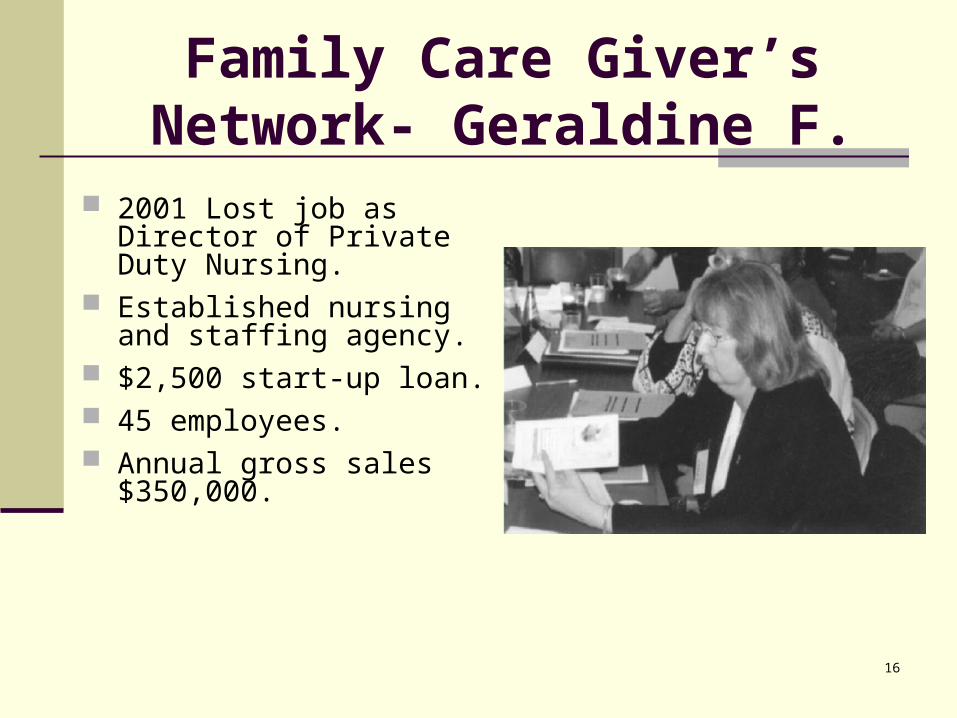

Family Care Giver’s Network- Geraldine F.

2001 Lost job as Director of Private Duty Nursing.

Established nursing and staffing agency.

$2,500 start-up loan. 45 employees. Annual gross sales

$350,000.

Mugshots Coffeehouse & Café – Jill F. & Angela V.

Completed training in 2002 2 coffee shops Voted Best of Philly 2005 Committed to positive

contribution to the community by being mindful of the environment and their neighbors, both locally and globally.

sends day’s end surplus food to a local homeless shelter.

Leaders formed a cooperative of local independent coffee houses

Turned profitable after just one year.

18

Barriers to SEA Implementation

Not eligible for extended benefits

Funding Performance standards PA 15 benchmarks:

Completion of training Business plan Legal entity Checking account Home office Lease signed Equipment & supplies Marketing package Solicited customers Insurance Licenses Staff Schedule C for Income Tax Full-time Other

Sen. Wyden (D-OR) Proposal – “Self-Employment Assistance Act of 2010” Self-employment assistance programs were

established following enactment of NAFTA in 1993.

Self-employment assistance programs serve as a cost-effective method for promoting rapid reemployment & reducing time individuals require unemployment compensation.

In 2009 more than 588,000 business were started every month in the United States.

Self-Employment Assistance Act of 2010$150,000,000

(Under Development by Senator Wyden)

WHO CAN APPLY: States that has already enacted self-employment assistance programs, or States that establish programs and wish to extend the program to eligible

individuals. COVERED COSTS:

100% of allowances paid to individuals, plus administrative expenses incurred by State.

CONDITIONS: Number of individuals receiving Self-Employment Assistance may NOT exceed

1% of the number of individuals receiving unemployment compensation. ONE grant per State.

Eligibility

Any individual who was not eligible to participate in SEAP while collecting unemployment because:

1. They were not identified as likely to exhaust their regular benefits, or2. SEAP was not available in their state.

Any individual who is eligible for emergency unemployment benefits.

21

Why Provide Access to Capital?

Lack of access, especially among low-income & women

48% increase in demand for microloans since May ’08

Repair credit through financial education & counseling

Pathway to traditional financing

22

Small Business Job Act of 2010 – HR 5297

Modernizes and increases SBA funding: Max. size of microloans increased

from $35,000 to $50,000. Increased microloan intermediary

borrowing cap from $3.5 million to $5 million.

23

Economic Opportunities Fund Loan Products

Impact 361 microloans totaling $1.18 million

Products Credit Builder Loan- $500 to $1000 Line of Credit - up to $2,500 Small Business Loan - up to $20,000 Near Equity Product - up to $35,000

Use of Funds: Start Up Costs Working capital Equipment Inventory

“Step” loans

24

Beautiful Beginnings Childcare, Inc. - Lalita P.

Certified childcare instructor 3 loans:

$2,500 Start-up loan in 2004

$2,500 to continue marketing & outreach

$7,000 for 2nd location start-up costs

14 employees 50 children Grossed over $200,000 in

2nd year of operations Recently opened a 2nd

childcare center

25

Pennsylvania Family Savings Account Program Developed in partnership with PA

Governor’s Office in 1997 One of largest statewide IDA

Programs in nation. One-to-one match up to $2,000. Savings can be used for:

Business start-up or expansion Home purchase/home

improvement Education for themselves or child Other (car, debt/credit repair)

Basic Financial Education Classes.

Why Savings & Assets? Pew Economic Mobility

Higher personal savings promote greater upward income mobility

66% of individuals who had low savings remained in the bottom quartile of personal wealth compared to 45% who had high savings

71% of children of low-income, high-saving parents are more likely to experience upward income mobility compared to 50% of children of low-saving parents

“A Penny Saved Is Mobility Earned,” Cramer, R., O’Brien, R. et al CFFI 2009

27

WORC’s Family Savings Account Program – 9/30/10

1010 graduates Home purchases: 245 Home Improvement: 156 Education: 124 Business: 58 Retirement: 51 Car: 228

Economic Impact $36.7 million $2 million saved $1.8 million matched

Leveraged with $ 3.1 million in personal savings and other resources $ 29.6 million in mortgages and loans

28

National Research

Current research on the outcomes and impact of asset-building IDA programs show IDA savers are: 84% more likely to own a

business. Twice as likely to attend college. 35% more likely to own home. More than half who previously

received public assistance no longer receive assistance

Low incidence of foreclosure 1 of 171 in WORC’s study

29

Community Economic Development Benefits

Homeownership Real estate taxes More stable community Equity for future business

start-up Education

Workforce Small business

Job creation Tax base

30

INVEST NOW!Federal Funding Sources

Program Enacted FY2009

President Request FY2010

House Request FY2010

Senate Request FY2010

SBA Microloan $21 million $25 million $25 million $25 million

Technical Assistance $20 million $10 million $10 million $22 million

PRIME $5 million $3.1 million $8 million $5.5 million

Women’s Business Centers $13.8 million $13.1 million $14 million $14.3 million

Treas. CDFI Fund $107 million $243 million $244 million $167 million

HHS Assets for Independence (AFI) $24 million $24 million $24 million $24 million

Beginning Farmer and Rancher IDA N/A $5 million none none

HUD Community Development Block Grants $3.9 billion $4.5 billion $4.6 billion $4 billion

USDA Rurdev

Rural Business Enterprise Grants $38.7 million $38.7 million $38.7 million $38.7 million

Intermediary Relending $33.5 million $33.5 million $33.5 million $33.5 million

Rural Microentrepreneur Investment $4 million $22 million $4 million $22 million

31

Economic Development – Useful Websites

Program Website

CFED cfed.org

AEO microenterpriseworks.org

Opportunities Finance Network opportunityfinance.net

CDFI Fund cdfifund.gov

Rural Entrepreneurship Center ruraleship.org

Renewing the Countryside renewingthecountryside.org

Individual Development Accounts

www.ida.gov

SBA Micro-loan Program www.sba.gov/financial

32

Invest Now!Small investment,

Big returns