Languages

Pages

Legal

© Cumming & Johan (2013) Exits

Exit Outcomes

Cumming and Johan (2013 Chapter 21)

Plus some supplementary material

1

© Cumming & Johan (2013) Exits

Venture Capital Exits

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

IPOsAcquisitionsSecondary SalesBuybacksWrite-offs

2

© Cumming & Johan (2013) Exits

What is a “Venture Capital Exit” ?

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

• The means by which venture capitalists (VCs) dispose of their investments (recall introductory statistics lecture)

• Exit Types» IPO» Merger/Acquisition» Secondary Sale» Buyback» Writeoff

3

© Cumming & Johan (2013) Exits

What Drives Choice of VC Exit?

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

1. Entrepreneurial firm characteristics

2. VC characteristics

3. Cash flow and control rights between VC and entrepreneur

4. Market conditions

5. Legality and institutional factors across countries

4

© Cumming & Johan (2013) Exits

1. Entrepreneurial Firm Characteristics

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

Entrepreneurial firm characteristicsVC characteristicsCash flow and control rights between VC and entrepreneurMarket conditionsLegality and institutional factors across countries

• Size– Minimum listing standards for IPO

• Quality– Not possible to take bad companies public?!– Important to minimize information problems to max sale price (next slide)

• Industry– High Market/Book high growth potential

• Location

• Transaction synergies with new owner(s)– Very important for acquisitions, & possibly IPOs

5

© Cumming & Johan (2013) Exits

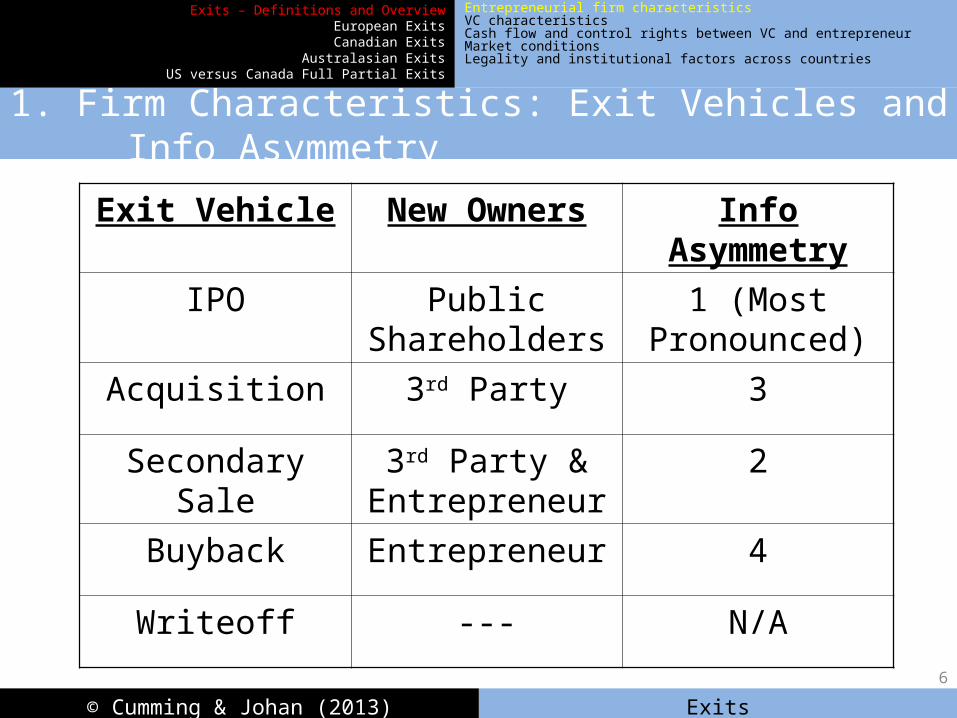

1. Firm Characteristics: Exit Vehicles and Info Asymmetry

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

Entrepreneurial firm characteristicsVC characteristicsCash flow and control rights between VC and entrepreneurMarket conditionsLegality and institutional factors across countries

Exit Vehicle New Owners Info Asymmetry

IPO Public Shareholders

1 (Most Pronounced)

Acquisition 3rd Party 3

Secondary Sale

3rd Party & Entrepreneur

2

Buyback Entrepreneur 4

Writeoff --- N/A

6

© Cumming & Johan (2013) Exits

2. VC Characteristics

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

Entrepreneurial firm characteristicsVC characteristicsCash flow and control rights between VC and entrepreneurMarket conditionsLegality and institutional factors across countries

• LPs versus corporate• & versus Government funds!

• Kliener Perkins versus “Fargo” VC Fund

• Fund Capital

• Connections with Investment Banks and/or Microsoft type companies

7

© Cumming & Johan (2013) Exits

3. Control Rights

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

Entrepreneurial firm characteristicsVC characteristicsCash flow and control rights between VC and entrepreneurMarket conditionsLegality and institutional factors across countries

• Entrepreneurs have a non-pecuniary preference for IPOs

• Weak VC control rights and common equity IPOs more likely?

• Strong VC control rights and convertible securities acquisitions more likely?

8

© Cumming & Johan (2013) Exits

4. Market conditions

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

Entrepreneurial firm characteristicsVC characteristicsCash flow and control rights between VC and entrepreneurMarket conditionsLegality and institutional factors across countries

• Significant factor in IPOs– 1999 – April 14, 2000

• Also a significant factor in write-offs!– Post April 14, 2000

9

© Cumming & Johan (2013) Exits

5. Legality / Institutional Factors

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

Entrepreneurial firm characteristicsVC characteristicsCash flow and control rights between VC and entrepreneurMarket conditionsLegality and institutional factors across countries

• Legal– Quality of shareholder rights– Corruption– Contract repudiation– Rule of Law– Efficiency of Judiciary

• Institutional– Size of country’s stock market

10

© Cumming & Johan (2013) Exits

Control Rights and VC Exits

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

Cumming and Johan (2013 Chapter 21)

11

© Cumming & Johan (2013) Exits

Data

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

• 223 entrepreneurial firms• Hand-collected from 35 private equity funds• 11 continental European countries: Germany (50), The

Czech Republic (5), The Netherlands (73), Switzerland (15), Italy (23), Denmark (11), France (6), Belgium (12), Poland (12), Austria (10) and Portugal (6).

• Investment Years 1995 – 2002. • Exit Years 1996 – 2005.

12

© Cumming & Johan (2013) Exits

Securities Used by Year of Investment in European Data (Chapter 21)

0

5

10

15

20

25

30

35

40

1995 1996 1997 1998 1999 2000 2001 2002

Year

To

tal N

um

ber

per

Yea

r

Straight Debt or Straight Preferred Preferred or Debt and Common Common Equity Convertible Debt or Convertible Preferred Equity

13

© Cumming & Johan (2013) Exits

Table 21.5. Multinomial Logit Regressions (selected variables excluded to fit on this slide)

IPO Acquisition Buyback Write-off IPO Acquisition Buyback Write-off

Constant -0.613 3.173* -0.013 -1.260 -1.056 3.259* 0.226 -0.984

Investor Characteristics

Log (Fund Capital) -0.011 -0.036 -0.047** -0.001 0.030 -0.108 -0.050* 0.037

Non-Captive VC Fund -0.004 -0.221* 0.103** 0.048 0.058 -0.214* 0.084* 0.012

Transaction Characteristics

Log (Private Investment Value) 0.019 -0.043 0.005 0.039 0.014 -0.031 0.004 0.023

Prior Rounds 0.029 0.282** -0.019 -0.301** 0.030 0.395** -0.019 -0.413**

Replace CEO -0.068 0.386*** 0.024 -0.159 -0.068 0.236* 0.036 -0.028

Majority Board -0.106** 0.237*** -0.039 0.035 -0.092* 0.184* -0.043 0.082

Majority Vote 0.040 -0.059 0.006 -0.085

Control Rights Index -0.066** 0.122** 0.014 -0.072

Veto Rights 0.011 0.056 -0.008 -0.052

Market Characteristics

Log (MSCI 0-3 Months) 1.007*** -1.668*** 0.290 0.366 0.916*** -1.682** 0.254 0.603

Investment Year Dummies? Yes Yes Yes Yes Yes Yes Yes Yes

Institutional and Legal Variables

Log (Legality) -0.026 -0.833 0.110 0.203 0.046 -0.787 0.060 0.116

Log (Market Capitalization) 0.052* 0.063 0.014 0.003 0.022 0.093 0.013 0.005

Country Dummies? Yes Yes Yes Yes Yes Yes Yes Yes14

© Cumming & Johan (2013) Exits

Some Key Findings

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

• Strong VC control rights Acquisition

• Weak VC control rights / common equity IPO

• Why?

15

© Cumming & Johan (2013) Exits

Puzzle

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

• Legality less important than size of stock market in driving exit outcomes in Europe

• Legality more important than size of stock market in driving exit outcomes in Asia-Pacific region

• Why?

16

© Cumming & Johan (2013) Exits

Supplementary Material

VC exits from other parts of the world

17

© Cumming & Johan (2013) Exits

Canadian Exits

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

Cumming and Johan (2008 Venture Capital)

18

© Cumming & Johan (2013) Exits

Summary Testable Hypotheses

This table summarizes the central hypotheses and describes the variables used to test the hypotheses.

Hypo-thesis #

Variable Description Hypothesized Effect on Exit Outcomes

Venture Capital Characteristics

Limited Partnership Venture Capitalist

20.1The fraction of the number of limited partnership venture capital funds that were syndicated venture capital funds at the first round investment.

IPOs and acquisitions are more likely than secondary sales, buybacks and write-offs for limited partnership venture capital funds.

Corporate Venture capital fund

20.2The fraction of the number of corporate venture capital funds that were syndicated venture capital funds at the first round investment.

Acquisitions are more likely than IPOs as the corporate venture capital has strategic incentives to invest.

Government Venture capital fund

20.3The fraction of the number of government venture capital funds that were syndicated venture capital funds at the first round investment.

Weaker governance structure associated with government funds, and therefore a greater probability of secondary sales, buybacks and write-offs.

Number of Syndicated Venture capital funds

20.4The number of syndicated venture capital funds in the first round investment.

A greater number of syndicate venture capital funds will reduce adverse selection problems and facilitate value added, thereby increasing the probability of an IPO

Entrepreneurial Firm Characteristics

Life Science Industry 20.5A dummy variable equal to one for firms in one of the life sciences industries (biotechnology or medical)

Increases the probability of an IPO, as IPO investors often have an appetite for technology companies

Other High-Tech Industry

20.5A dummy variable equal to one for firms in one of the high-tech industries other than the life sciences industries.

Increases the probability of an IPO, as IPO investors often have an appetite for technology companies

Seed or Early Stage 20.6A dummy variable equal to one for seed or early stage investments in the first round of investment

Higher probability of a write-off as risks are greater the earlier the stage of investment

Expansion Stage 20.6A dummy variable equal to one for expansion stage investments in the first round of investment

Lower risks relative to seed and early stage investments, and therefore a lower probability of a write-off

Entrepreneur Capital Requirements

[Log (Deal Size)]20.7

The log of the amount invested in the first round investment across all syndicated venture capital funds, in thousands of 2004 Canadian dollars.

Larger investments are more likely to go public as there are minimum capital requirements for listing.

Venture capital fund and Entrepreneur in Same

Province20.8

A dummy variable equal to one if the venture capital fund and the entrepreneur were located with the same province at the time of first round investment

Higher probability of an IPO and acquisition as adverse selection problems are mitigated and value-added facilitated by regional proximity. 19

© Cumming & Johan (2013) Exits

Summary Testable Hypotheses

(Continued)

Hypo-thesis #

Variable Description Hypothesized Effect on Exit Outcomes

Transaction Characteristics

Common Equity and/or Warrants

20.9

The fraction of the number of first-round investment securities in the form of common equity and/or warrants. If only common equity was used then the variable equals 1, and if common equity was not used then the variable equals 0.

Increases the probability of an IPO over an acquisition, as common equity signals favorable information to the public market. As well, higher quality entrepreneurs are more likely to negotiate common equity contracts. Further, entrepreneurs typically have stronger control rights when the venture capital fund uses common equity, and therefore entrepreneurs with a non-pecuniary preference for an IPO are less likely to be acquired than go public.

Convertible Securities 20.10

The fraction of the number of first-round investment securities in the form of convertible preferred equity and/or convertible debt. If only convertible securities were used then the variable equals 1, and if convertible securities were not used then the variable equals 0.

Provides incentives for the venture capital fund to add value and thereby increase the probability of both IPOs and acquisitions over secondary sales, buybacks and write-offs.

Control Variables: Institutional and

Economic Conditions

Entrepreneur A dummy variable equal to one for an entrepreneur based in Higher probability of an IPO and acquisition as economic activity is greater in the of and than other provinces.

Entrepreneur A dummy variable equal to one for an entrepreneur based in Higher probability of an IPO and acquisition as economic activity is greater in the of and than other provinces.

Log (1+MSCI Index in Year of Exit)

The log of 1+ the Morgan Stanley Capital International stock index return for in the year of exit

Higher probability of an IPO or acquisition in boom market conditions; greater probability of secondary sales, buybacks and write-offs in bad market conditions

Log (1+MSCI Index in Year Prior to Exit)

The log of 1+ the Morgan Stanley Capital International stock index return for in the year prior to exit

Higher probability of an IPO or acquisition in boom market conditions; greater probability of secondary sales, buybacks and write-offs in bad market conditions

Dummy for Exit in 1999 A dummy variable equal to one for exits in 1999Higher probability of an IPO or acquisition in boom market conditions; greater probability of secondary sales, buybacks and write-offs in bad market conditions

Dummy for Exit in 2000 A dummy variable equal to one for exits in 2000Higher probability of an IPO or acquisition in boom market conditions; greater probability of secondary sales, buybacks and write-offs in bad market conditions 20

© Cumming & Johan (2013) Exits

0

10

20

30

40

50

60

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

Nu

mb

er o

f E

xits

Figure 20.1. Number of Venture Capital - Backed Exits by Year, 1991-1994

IPO Acquisition Secondary Sale Buyback Write-off 21

© Cumming & Johan (2013) Exits

IPO

Acquisition

SecSale

BuybackWriteof f

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

Co

rpo

rate

Go

vern

men

t

Hyb

rid

Lab

our

Sp

ons

ore

d

Priv

ate

Ind

epen

den

t

Unk

now

n

Figure 20.2. Percentage of Exit Outcomes for Each Type of Investor

22

© Cumming & Johan (2013) Exits

Write-of f

IPO

Secondary Sale

Buyback

Acquisition

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

50.00%

SeedEarly

ExpansionBuyout

TurnaroundUnknown

Figure 20.3. Percentage of Exit Outcomes for Each Stage of First Investment

23

© Cumming & Johan (2013) Exits

IPOSecondary Sale BuybackWrite-of fAcquisition

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

50.00%

Co

mm

on

and

/or W

arra

nts

Pre

ferr

ed

Co

nver

tible

Pre

ferr

ed

Co

nver

tible

Deb

t

Mix

ed C

om

mo

n w

ith P

refe

rred

and

/or D

ebt

Deb

t

Unk

now

n

Figure 20.4. Percentage of Exit Outcomes for Each Type of Security

24

© Cumming & Johan (2013) Exits

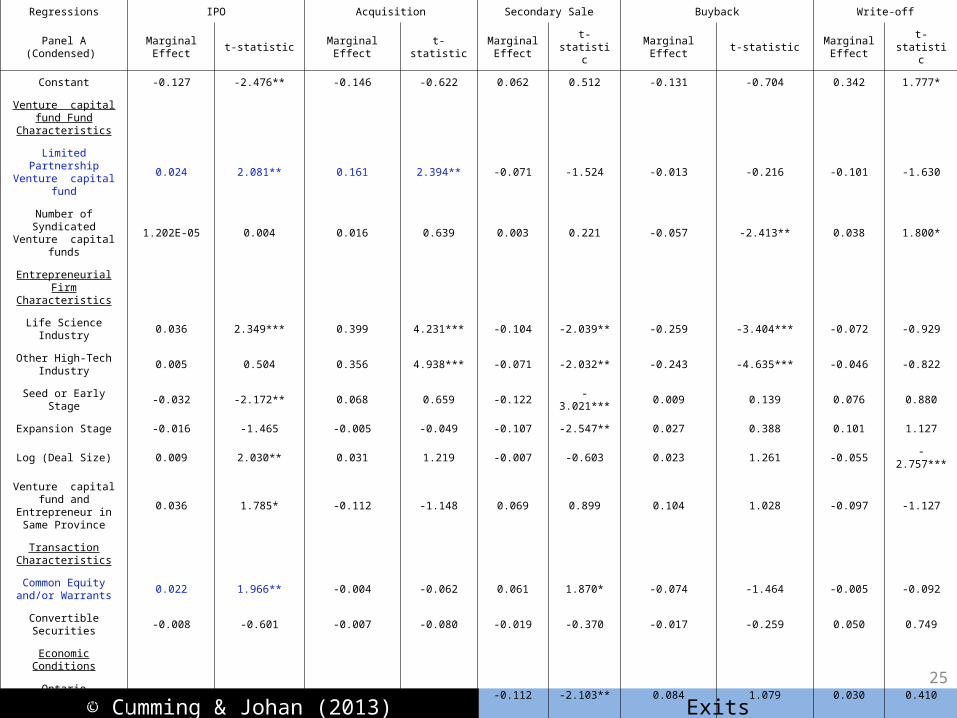

Regressions IPO Acquisition Secondary Sale Buyback Write-off

Panel A (Condensed) Marginal

Effectt-statistic Marginal Effect t-statistic

Marginal Effect

t-statistic Marginal Effect t-statisticMarginal

Effectt-statistic

Constant -0.127 -2.476** -0.146 -0.622 0.062 0.512 -0.131 -0.704 0.342 1.777*

Venture capital fund Fund Characteristics

Limited Partnership Venture capital fund

0.024 2.081** 0.161 2.394** -0.071 -1.524 -0.013 -0.216 -0.101 -1.630

Number of Syndicated Venture capital funds

1.202E-05 0.004 0.016 0.639 0.003 0.221 -0.057 -2.413** 0.038 1.800*

Entrepreneurial Firm Characteristics

Life Science Industry 0.036 2.349*** 0.399 4.231*** -0.104 -2.039** -0.259 -3.404*** -0.072 -0.929

Other High-Tech Industry

0.005 0.504 0.356 4.938*** -0.071 -2.032** -0.243 -4.635*** -0.046 -0.822

Seed or Early Stage -0.032 -2.172** 0.068 0.659 -0.122 -3.021*** 0.009 0.139 0.076 0.880

Expansion Stage -0.016 -1.465 -0.005 -0.049 -0.107 -2.547** 0.027 0.388 0.101 1.127

Log (Deal Size) 0.009 2.030** 0.031 1.219 -0.007 -0.603 0.023 1.261 -0.055 -2.757***

Venture capital fund and Entrepreneur in

Same Province0.036 1.785* -0.112 -1.148 0.069 0.899 0.104 1.028 -0.097 -1.127

Transaction Characteristics

Common Equity and/or Warrants

0.022 1.966** -0.004 -0.062 0.061 1.870* -0.074 -1.464 -0.005 -0.092

Convertible Securities -0.008 -0.601 -0.007 -0.080 -0.019 -0.370 -0.017 -0.259 0.050 0.749

Economic Conditions

Ontario Entrepreneur -0.015 -1.354 0.012 0.155 -0.112 -2.103** 0.084 1.079 0.030 0.410

Quebec Entrepreneur -0.014 -1.472 -0.309 -3.935*** 0.049 1.170 0.219 3.081*** 0.055 0.801

Log (1+MSCI Index in Year of Exit)

-0.049 -1.847* -0.118 -0.924 0.034 0.506 0.098 0.953 0.034 0.325

Log (1+MSCI Index in Year Prior to Exit)

0.007 0.296 0.137 1.135 -0.062 -1.019 0.196 2.197** -0.278 -2.665***

Dummy for Exit in 1999 0.049 2.211** 0.358 2.337** 0.024 0.391 -0.452 -2.551** 0.021 0.175

Dummy for Exit in 2000 0.028 1.954* 0.028 0.326 -0.081 -1.498 -0.265 -3.638*** 0.290 4.291***

25

© Cumming & Johan (2013) Exits

Regressions IPO Acquisition Secondary Sale Buyback Write-off

Panel B (Condensed) Marginal

Effectt-statistic Marginal Effect t-statistic Marginal Effect t-statistic

Marginal Effect

t-statisticMarginal

Effectt-statistic

Constant -0.107 -2.296** 0.055 0.232 -0.028 -0.348 -0.241 -1.229 0.321 1.570

Venture capital fund Fund Characteristics

Corporate Venture capital fund

0.015 1.202 0.282 2.362** -0.351 -3.102*** -0.136 -1.236 0.191 1.902*

Government Venture capital fund or LSVCC

-0.021 -1.841* -0.229 -3.137** 0.071 2.047** 0.146 2.309** 0.034 0.503

Number of Syndicated Venture capital funds

0.000 0.082 0.006 0.212 0.014 1.562 -0.053 -2.142** 0.034 1.503

Entrepreneurial Firm Characteristics

Life Science Industry 0.039 2.312** 0.410 4.185*** -0.071 -1.882* -0.268 -3.405*** -0.110 -1.305

Other High-Tech Industry

0.007 0.702 0.332 4.389*** -0.040 -1.630 -0.229 -4.165*** -0.070 -1.126

Log (Deal Size) 0.008 1.951* 0.026 1.013 -0.004 -0.515 0.026 1.361 -0.056 -2.660***

Transaction Characteristics

Common Equity and/or Warrants

0.025 2.039** 0.014 0.206 0.035 1.522 -0.071 -1.331 -0.003 -0.051

Convertible Securities -0.007 -0.478 -0.027 -0.321 -0.008 -0.262 0.010 0.148 0.032 0.448

Economic Conditions

Log (1+MSCI Index in Year of Exit)

-0.050 -1.801* -0.103 -0.781 0.018 0.414 0.099 0.919 0.036 0.320

Log (1+MSCI Index in Year Prior to Exit)

0.000 0.014 0.130 1.045 -0.033 -0.846 0.211 2.251** -0.309 -2.759***

Dummy for Exit in 1999 0.053 2.257** 0.388 2.455** 0.004 0.093 -0.462 -2.562** 0.017 0.138

Dummy for Exit in 2000 0.031 2.004** 0.042 0.462 -0.070 -1.768* -0.318 -4.120*** 0.315 4.361***

26

© Cumming & Johan (2013) Exits

Summary

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

• Fund Type– Limited partners: IPO or acquisition– Corporate: acquisition– LSVCC: buyback or secondary sale

• Transaction type– Common equity: IPO– Consistent with European evidence discussed in Chapter 21

• Entrepreneur characteristics and economic conditions also important

27

© Cumming & Johan (2013) Exits

Some Further Evidence… Asia Pacific

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

Cumming, Fleming & Schwienbacher (2006, Journal of Corporate Finance)

28

© Cumming & Johan (2013) Exits

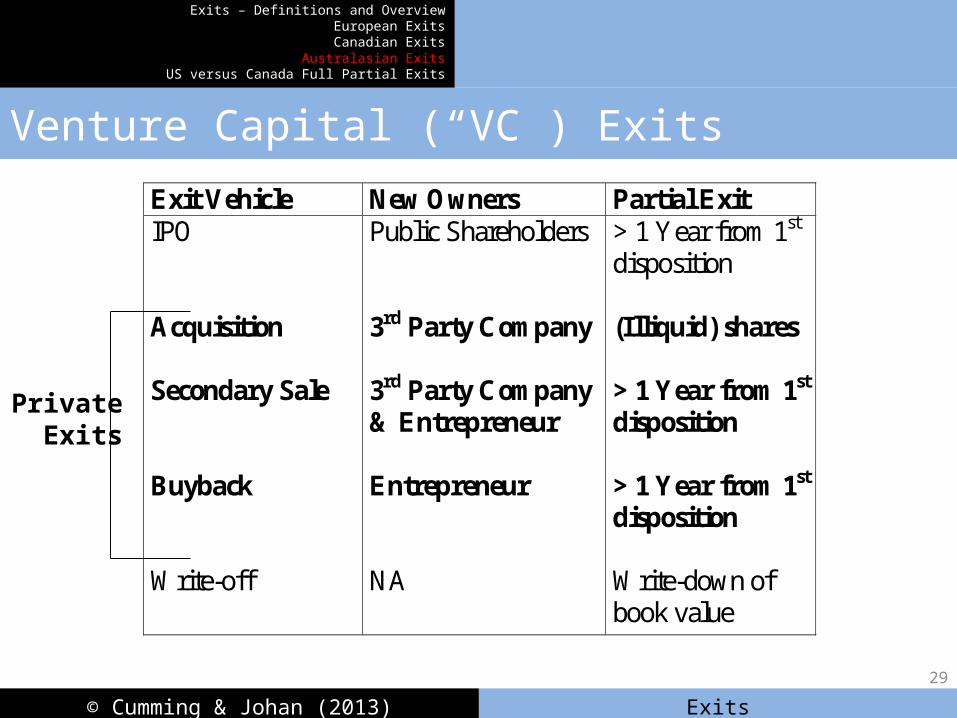

Venture Capital (“VC”) Exits

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

Exit Vehicle New Owners Partial Exit IPO Acquisition Secondary Sale Buyback Write-off

Public Shareholders 3rd Party Company 3rd Party Company & Entrepreneur Entrepreneur NA

> 1 Year from 1st disposition (Illiquid) shares > 1 Year from 1st disposition > 1 Year from 1st disposition Write-down of book value

PrivateExits

29

© Cumming & Johan (2013) Exits

Core Research Question

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

• Does legality affect VC exit outcomes? IPO private sale (acquisition, secondary sale, buyback) write-off

• Related questions in companion work:1. Does legality affect investment decisions2. Does legality affect decision to move company from Asia-

Pacific to the United States

30

© Cumming & Johan (2013) Exits

Competing Theories

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

• Black and Gilson (1998 JFE Discussion Paper) Venture Capital Markets Require Strong Stock Markets to

Facilitate IPOs Proposition not previously subject to empirical scrutiny

• Shleifer and Wolfenzon (2002 JFE) IPOs facilitated by Legality Proposition not previously subject to empirical scrutiny

31

© Cumming & Johan (2013) Exits

Cumming Fleming Schwienbacher 2006 Journal of Corporate Finance

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

1st Multi-country dataset on VC exits 12 Asia-Pacific countries – new look at VC in the region

Relation between legality (La Porta et al variables) and venture capital exits

“Horse Race” on role of Legality versus Size of Stock Market

Cross-country comparisons on other dimensions

32

© Cumming & Johan (2013) Exits

Central Findings in this Paper

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

1. Legality facilitates VC-backed firms achieving IPO (supports Shleifer and Wolfenzon 2002 JFE)

2. Size of a country’s stock market unrelated to probability of an IPO (reject Black & Gilson 1998 JFE)

3. VC-backed firms also more likely to go IPO when:a. Higher market/book frimsb. Larger firmsc. Limited partnership VCs (not captive VCs)d. VCs with more capital (reputation)

33

© Cumming & Johan (2013) Exits

Primary Competing Hypotheses

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

HypothesesDataEmpirical TestsConclusion

• Legality VC IPO exits Legality mitigates agency problems between outside

shareholders and entrepreneurs Shleifer and Wolfenzon (2002 JFE)

No empirical tests considered

• Stock Market Capitalization VC IPO exits Black and Gilson (1998 JFE)

No empirical tests considered

34

© Cumming & Johan (2013) Exits

Control Variables

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

HypothesesDataEmpirical TestsConclusion

• Market & Institutional Conditions MSCI Returns Country dummy variables (esp. for moves to US)

• VC Fund Characteristics Age, size US-affiliation Captive versus Limited Partnership

• Entrepreneurial Firm & Investment Characteristics Industry market / book Size Syndication, Co-investment

35

© Cumming & Johan (2013) Exits

Data

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

HypothesesDataEmpirical TestsConclusion

• 468 VC-backed companies, 1989 – 2001 Australia, China, Hong Kong, India, Indonesia, Malaysia, New

Zealand, Philippines, Singapore, South Korea, Taiwan, Thailand These countries’ VC investments in US-based entrepreneurial

firms Source: Wilshire and Associates, Ltd.

• Similar in scope to related VC papers with hand-collected datasets (typically 100 – 200 observations) E.g., Lerner and Schoar (2003)

36

© Cumming & Johan (2013) Exits

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Investment Years

Exit Years

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

Percentageof All

Investments(of All Exits

for Subsampleof Exited

Investments)

Figure 1 . Investment and Exit Years in the Dataset

37

© Cumming & Johan (2013) Exits

-100 -75

-50

-25 0

25 50 7510

012

515

017

520

022

525

027

530

0

325

350

375

400

425

450

475

500

1000

No Exit

Partial Realization

Write-off

Private Exit

IPO

0

20

40

60

80

100

120

Numberof Exits

IRR (%)

Figure 2. Frequency of and Returns to Alternative Exit Outcomes

38

Table 2. Countries Represented in the Exits Database, and the Legality Components

Country LegalityTotal Market

Capitalization (Billions US$)

Average IRR

Median IRR

# IPOs#

Private Exits

# Write-offs

# Unexited Investments

New Zealand 21.55 19.69 0.905 0.365 4 10 0 1

Asia-Pacific VC Inv. in US

20.85 12380.03 0.480 0.064 9 49 21 38

Australia 20.44 242.26 0.164 0.189 27 43 23 22

Singapore 19.53 130.42 0.341 0.145 1 7 3 2

Hong Kong 19.11 278.95 -0.056 0.070 2 11 3 8

Malaysia 16.67 108.65 -0.168 -0.168 0 1 0 0

India 12.80 213.19 1.020 1.020 2 1 0 0

Thailand 12.94 70.02 -0.101 -0.101 0 9 3 0

China 19.23 461.42 -0.063 0.084 2 12 2 2

Taiwan 17.62 388.13 0.723 0.445 31 39 0 62

South Korea 14.23 260.00 0.145 0.250 0 3 0 0

Indonesia 9.16 25.68 -0.029 -0.015 0 14 0 0

Philippines 8.51 13.04 -0.003 -0.003 0 1 0 039

© Cumming & Johan (2013) Exits

Table 3. Difference Tests and Summary Statistics

Characteristic Tested # FirmsProportion

of IPO Exits

Difference Test Statistic

Full Sample 468 0.167

Average Legality Index > 20 (Excluding US and Taiwan) 132 0.235

2.303**

Average Legality Index < 20 (Excluding US and Taiwan) 87 0.080

Average Market Cap. > 300 (Excluding US and Taiwan) 22 0.182

0.082

Average Market Cap. < 300 (Excluding US and Taiwan) 197 0.173

US Only 117 0.077-2.574**

Taiwan 132 0.235

US Only 117 0.077-2.488**

Australia 115 0.235

Taiwan 132 0.2350.001

Australia 115 0.235

Taiwan 132 0.2351.990**

All Other Countries Excluding US, Australia 104 0.106 40

© Cumming & Johan (2013) Exits

Regressions (Tables 5 – 7)Regressions (Tables 5 – 7)

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

HypothesesDataEmpirical TestsConclusion

Focus of Empirical Tests Probability of exit outcomes Multinomial regressions of the likelihood of an IPO versus private sale

transaction and versus write-off Other tests considered (not discussed today)

Robustness Tests Endogeneity, collinearity, heteroscedasticity Definitions of variables Single / multi-step estimation Binomial / multinomial logit estimates Heckman (1976, 1979) selection effects Other

41

© Cumming & Johan (2013) Exits

Multinomial Logit Regressions

Probability

IPO

Probability

Private Exit

Probability

Write-off

Log (Legality)

Log (Market Cap)

Market Conditions:

MSCI Variables

VC Fund Characteristics:

Captive VC

Log (VC Fund Capital)

Ent. Firm / Trans Char.:

Industry Market / Book

Log (Book Value)

Syndication

Co-Investment

0.854**

-0.0001

0.216

-0.030

0.181***

0.080**

-0.008

0.073

0.001

-1.389***

-0.058

-0.895***

-0.018

-0.217***

-0.070

0.015*

0.015

0.0001

-0.150

-0.011

0.352**

0.089**

-0.051**

0.008

-0.002

-0.084*

0.002***42

© Cumming & Johan (2013) Exits

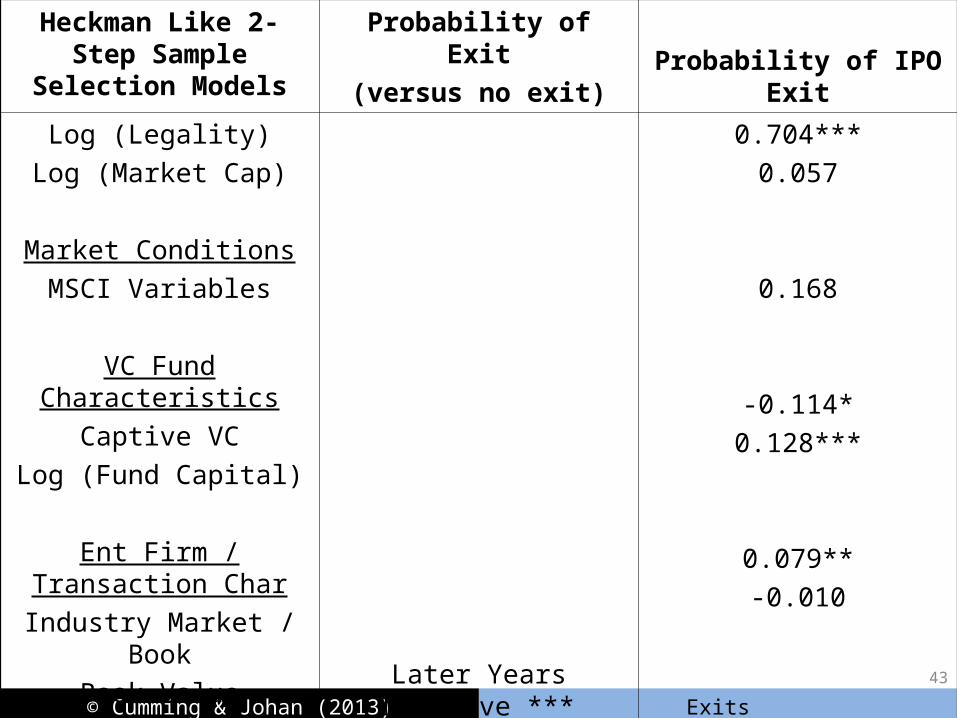

Heckman Like 2-Step Sample Selection Models

Probability of Exit

(versus no exit) Probability of IPO Exit

Log (Legality)

Log (Market Cap)

Market Conditions

MSCI Variables

VC Fund Characteristics

Captive VC

Log (Fund Capital)

Ent Firm / Transaction Char

Industry Market / Book

Book Value

Investment Year DummiesLater Years Negative ***

0.704***

0.057

0.168

-0.114*

0.128***

0.079**

-0.010

43

© Cumming & Johan (2013) Exits

Primary Results Re Legality

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

HypothesesDataEmpirical TestsConclusion

• An increase in the Legality index from 20-21 (e.g., Hong Kong Australia)increases the probability of an IPO by 1.7%

• An increase in Legality from 10-11(e.g., Philippines Indonesia)increases the probability of an IPO by 3.3%

44

© Cumming & Johan (2013) Exits

Central Findings in this Paper

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

HypothesesDataEmpirical TestsConclusion

1. Legality facilitates VC-backed firms achieving IPO (supports Shleifer and Wolfenzon 2002 JFE)

2. Size of a country’s stock market unrelated to probability of an IPO (reject Black & Gilson 1998 JFE)

3. VC-backed firms also more likely to go IPO when:a. Higher market/book frimsb. Larger firmsc. Limited partnership VCs (not captive VCs)d. VCs with more capital (reputation)

45

© Cumming & Johan (2013) Exits

Outliers and Further Research

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

HypothesesDataEmpirical TestsConclusion

• High legality not necessary in special cases: Taiwan: successful VCs despite low legality index Entrepreneurial culture in Taiwan

• Legality not sufficient in special cases:Asia-Pacific VC investments in US entrepreneurial firms: less likely to go IPO Weak VC certification in IPOs across the Pacific

46

© Cumming & Johan (2013) Exits

Now…Full versus Partial Exits

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

Source: Cumming and MacIntosh (2003 Journal of Banking and Finance)

2004 Ido Sarnat Best Paper Award in the Journal of Banking and Finance

47

© Cumming & Johan (2013) Exits

Full and Partial VC Exits

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

DefinitionsHypothesesDataEmpirical TestsConclusion

• IPO, Secondary Sale and Buyback Exits:Full: dispose of investment within 1 year of 1st distribution;Partial: more than 1 year

• Acquisition Exits: Full: cash paymentPartial: (illiquid) shares

• Write-off Exits:Full: liquidationPartial: write-down

48

© Cumming & Johan (2013) Exits

Research Questions

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

DefinitionsHypothesesDataEmpirical TestsConclusion

Does the extent of VC exit depend on:

1. Characteristics of Entrepreneurial Firm?

2. Duration of Venture Capital Investment?

3. Exit vehicle selected?

4. Regulatory Environment?

49

© Cumming & Johan (2013) Exits

Contributions

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

DefinitionsHypothesesDataEmpirical TestsConclusion

1. Relate VC investment duration, exit vehicles, and entrepreneurial firm characteristics to exit strategies

2. Introduce the first empirical evidence on the extent of exit for the complete set of VC exits

3. Document the first cross-country evidence [Canada and the US] to illustrate the effect of legal and institutional constraints on efficient exit strategies

4. Consider implications for the risk & return to venture capital

50

© Cumming & Johan (2013) Exits

VC Exit Strategies

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

DefinitionsHypothesesDataEmpirical TestsConclusion

• Minimizing agency costs (moral hazard and adverse selection) between entrepreneurial firm and its new owners maximizes the value of the firm upon VC exit

• Partial exits reduce informational asymmetry between entrepreneurial firm and new owner(s)

• Informational asymmetry and agency costs vary by:1. Length of VC investment,2. Entrepreneurial firm characteristics (e.g., the nature of its

assets, market & book values)3. Exit vehicle

51

© Cumming & Johan (2013) Exits

Exit Vehicle New Owners Info Asymmetry

IPO Public Shareholders

1 (Most Pronounced)

Acquisition 3rd Party 3

Secondary Sale 3rd Party & Entrepreneur

2

Buyback Entrepreneur 4

Write-off --- N/A

Exit Vehicles and Info AsymmetryInfo asymmetry Partial Exits

52

© Cumming & Johan (2013) Exits

Entrepreneurial Firm Characteristics-Market & Book Value-Technology Firm-Stage of Development-Other

Institutional andRegulatory Environment-Securities Regulation-Government Sponsorship of Venture Capital-Other

Venture Capital Investment Duration

Venture Capital Exit Vehicle

Extent of Venture Capital Exit

53

© Cumming & Johan (2013) Exits

Investment Duration and Exit Strategy

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

DefinitionsHypothesesDataEmpirical TestsConclusion

• Longer VC investment duration mitigates informational asymmetries between the entrepreneurial firm and its new owners

• E.g., evidence that longer VC investment duration mitigates IPO underpricing [Megginson & Weiss (1991) JF]

• Longer investment duration less need for partial exit

54

© Cumming & Johan (2013) Exits

Firm Characteristics & Exit Strategy

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

DefinitionsHypothesesDataEmpirical TestsConclusion

• Asset intangibility greater informational asymmetry partial exit

• Buyout transactions: VC facilitates transfer of ownership interest through a partial exit

• Other firm characteristics …

5555

© Cumming & Johan (2013) Exits

Legal & Institutional Barriers to Efficient Exit Strategies

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

DefinitionsHypothesesDataEmpirical TestsConclusion

US: Private Venture Capital Funds

Canada: Government Sponsorship of VC (25% in1992 to 50% in 1995)

LSVCFs less able to credibly certify the quality of their investments to the new owner(s)

E.g., Must invest new funds within a few months!

Greater need to commit to a partial exit strategy to certify firm quality in Canada

56

© Cumming & Johan (2013) Exits

Securities Regulation & Institutional Differences

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

DefinitionsHypothesesDataEmpirical TestsConclusion

More onerous in Canada (MacIntosh, 1994) less liquidity of SME securities in Canada

Legal uncertainty with hold-periods and escrow requirements in Canada “cumbersome and confusing for issuers and investors” (Tucker, 1999, CVCA Newsletter “Enterprise”)

Fewer institutional IPO purchasers in Canada, and Canadian underwriters are less specialized relative to their US counterparts

* Greater need for VCs to commit to partial IPO exits to certify firm quality in Canada

57

© Cumming & Johan (2013) Exits

Data

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

DefinitionsHypothesesDataEmpirical TestsConclusion

• 112 U.S. Exits (Table 1a) • Source: Venture Economics• 1992-1995 (Approx 10% of Industry Exits)

• 134 European Exits (Table 1b)• Source: Macdonald & Associates• 1992-1995 (Approx 32% of Industry Exits)

58

© Cumming & Johan (2013) Exits

Data Limitations

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

DefinitionsHypothesesDataEmpirical TestsConclusion

• Non-IPO exits (acquisitions, secondary sales, buybacks and writeoffs) are private exits

• Some private data not obtainable, such as exact timing of partial distributions

• But for all exit vehicles, we do know if VC exit was complete within 1 year of the first distribution

59

© Cumming & Johan (2013) Exits

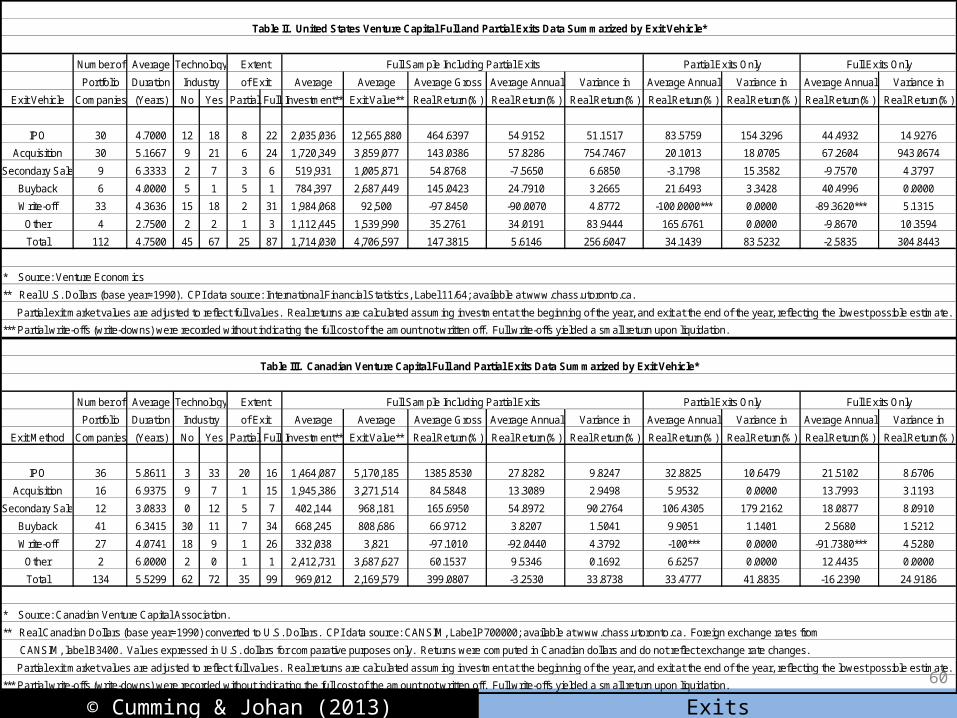

Table II. United States Venture Capital Full and Partial Exits Data Summarized by Exit Vehicle*

Number of Average Technology

Portfolio Duration Industry Average Average Average Gross Average Annual Variance in Average Annual Variance in Average Annual Variance in

Exit Vehicle Companies (Years) No Yes Partial Full Investment** Exit Value** Real Return(%) Real Return(%) Real Return(%) Real Return(%) Real Return(%) Real Return(%) Real Return(%)

IPO 30 4.7000 12 18 8 22 2,035,036 12,565,880 464.6397 54.9152 51.1517 83.5759 154.3296 44.4932 14.9276

Acquisition 30 5.1667 9 21 6 24 1,720,349 3,859,077 143.0386 57.8286 754.7467 20.1013 18.0705 67.2604 943.0674

Secondary Sale 9 6.3333 2 7 3 6 519,931 1,005,871 54.8768 -7.5650 6.6850 -3.1798 15.3582 -9.7570 4.3797

Buyback 6 4.0000 5 1 5 1 784,397 2,687,449 145.0423 24.7910 3.2665 21.6493 3.3428 40.4996 0.0000

Write-off 33 4.3636 15 18 2 31 1,984,068 92,500 -97.8450 -90.0070 4.8772 -100.0000*** 0.0000 -89.3620*** 5.1315

Other 4 2.7500 2 2 1 3 1,112,445 1,539,990 35.2761 34.0191 83.9444 165.6761 0.0000 -9.8670 10.3594

Total 112 4.7500 45 67 25 87 1,714,030 4,706,597 147.3815 5.6146 256.6047 34.1439 83.5232 -2.5835 304.8443

Table III. Canadian Venture Capital Full and Partial Exits Data Summarized by Exit Vehicle*

Number of Average Technology

Portfolio Duration Industry Average Average Average Gross Average Annual Variance in Average Annual Variance in Average Annual Variance in

Exit Method Companies (Years) No Yes Partial Full Investment** Exit Value** Real Return(%) Real Return(%) Real Return(%) Real Return(%) Real Return(%) Real Return(%) Real Return(%)

IPO 36 5.8611 3 33 20 16 1,464,087 5,170,185 1385.8530 27.8282 9.8247 32.8825 10.6479 21.5102 8.6706

Acquisition 16 6.9375 9 7 1 15 1,945,386 3,271,514 84.5848 13.3089 2.9498 5.9532 0.0000 13.7993 3.1193

Secondary Sale 12 3.0833 0 12 5 7 402,144 968,181 165.6950 54.8972 90.2764 106.4305 179.2162 18.0877 8.0910

Buyback 41 6.3415 30 11 7 34 668,245 808,686 66.9712 3.8207 1.5041 9.9051 1.1401 2.5680 1.5212

Write-off 27 4.0741 18 9 1 26 332,038 3,821 -97.1010 -92.0440 4.3792 -100*** 0.0000 -91.7380*** 4.5280

Other 2 6.0000 2 0 1 1 2,412,731 3,687,627 60.1537 9.5346 0.1692 6.6257 0.0000 12.4435 0.0000

Total 134 5.5299 62 72 35 99 969,012 2,169,579 399.0807 -3.2530 33.8738 33.4777 41.8835 -16.2390 24.9186

Partial Exits Only

Partial Exits Only

Partial exit market values are adjusted to reflect full values. Real returns are calculated assuming investment at the beginning of the year, and exit at the end of the year, reflecting the lowest possible estimate.

Partial exit market values are adjusted to reflect full values. Real returns are calculated assuming investment at the beginning of the year, and exit at the end of the year, reflecting the lowest possible estimate.

CANSIM, label B3400. Values expressed in U.S. dollars for comparative purposes only. Returns were computed in Canadian dollars and do not reflect exchange rate changes.

Extent Full Sample Including Partial Exits Full Exits Only

*** Partial write-offs (write-downs) were recorded without indicating the full cost of the amount not written off. Full write-offs yielded a small return upon liquidation.

of Exit

* Source: Canadian Venture Capital Association.

** Real Canadian Dollars (base year=1990) converted to U.S. Dollars. CPI data source: CANSIM, Label P700000; available at www.chass.utoronto.ca. Foreign exchange rates from

Full Sample Including Partial Exits

*** Partial write-offs (write-downs) were recorded without indicating the full cost of the amount not written off. Full write-offs yielded a small return upon liquidation.

** Real U.S. Dollars (base year=1990). CPI data source: International Financial Statistics, Label 11/64; available at www.chass.utoronto.ca.

* Source: Venture Economics

Extent

of Exit

Full Exits Only

60

© Cumming & Johan (2013) Exits

Differences in exit performance between Canada and U.S.

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

DefinitionsHypothesesDataEmpirical TestsConclusion

• Lower risk and return in Canada relative to the US– Securities regulation– Government sponsorship of venture capital

• Partial exits typically associated with a higher risk and return– Selection effects: riskier ventures exited by a partial exit to

mitigate informational problems between the entrepreneurial firm and new owners

61

© Cumming & Johan (2013) Exits

Tables in next slides

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

DefinitionsHypothesesDataEmpirical TestsConclusion

• Negative and significant: partial exit more likely than full exit (and vice versa)

• Table 4 considers the extent of exit for all exits together

• Table 5 considers the extent of exit for each exit vehicle separately

• Important results summarized thereafter below

62

© Cumming & Johan (2013) Exits

Coefficient t-statistic p-value* Coefficient t-statistic p-value* Coefficient t-statistic p-value*

Constant 2.5415 1.7109 0.0871 2.3416 1.5120 0.1305 1.7849 2.0421 0.0411

IPO -0.5653 -0.8049 0.4209 -2.2167 -2.2954 0.0217 -1.1766 -2.4555 0.0141

Secondary Sale -0.0745 -0.0767 0.9389 -2.5584 -2.1063 0.0352 -1.0788 -1.7274 0.0841

Buyback -3.2569 -2.4566 0.0140 -0.4808 -0.5334 0.5938 -0.8364 -1.5009 0.1334

Write-off 1.5403 1.6986 0.0894 0.5694 0.4243 0.6714 1.1194 1.5491 0.1214

Technology -1.4559 -2.1294 0.0332 0.3345 0.4744 0.6352 -0.6341 -1.5760 0.1150

Duration -0.0542 -0.4343 0.6641 -0.0973 -1.2427 0.2140 -0.0851 -1.6360 0.1018

Market/Book 0.0514 0.7094 0.4781 -0.1694 -1.7701 0.0767 -0.0283 -0.5932 0.5530

Seed 0.5762 0.4564 0.6481 1.4040 0.8697 0.3844 0.9533 1.1733 0.2407

Start-up 1.7609 1.2686 0.2046 0.3771 0.3286 0.7425 1.4116 1.8354 0.0664

Early Stage 2.1683 1.5422 0.1230 -0.5629 -0.4531 0.6505 1.0899 1.3588 0.1742

Expansion 0.1150 0.0941 0.9250 0.4802 0.4262 0.6700 0.7645 1.0686 0.2852

Fundraising -0.0003 -1.2266 0.2200 0.0003 0.3842 0.7008 -0.0001 -0.9457 0.3443

* Two-sided test.

Table 4. Logit Estimates of the Extent of Exits in Canada and the United States

United States Canada Full Sample Estimates

63

© Cumming & Johan (2013) Exits

Coefficient t-statistic p-value* Coefficient t-statistic p-value* Coefficient t-statistic p-value*

Constant -1.7464 -0.6011 0.5478 3.8845 1.4746 0.1403 -0.9414 -0.6502 0.5155

Technology -1.3741 -0.7716 0.4404 -1.0835 -0.6401 0.5221 -0.2668 -0.3236 0.7463

Duration 0.0232 0.1079 0.9141 0.0507 0.2950 0.7680 -0.0646 -0.6511 0.5150

Market/Book 0.1686 1.1524 0.2492 -0.5356 -2.3978 0.0165 -0.0269 -0.4409 0.6593

Seed -1.0031 -0.6911 0.4895 8.4458 1.8914 0.0586 0.2351 0.2283 0.8194

Start-up 0.9551 0.5821 0.5605 0.1227 0.1052 0.9162 0.7264 0.9571 0.3385

Early Stage 2.8746 1.4570 0.1451 -1.9273 -1.4485 0.1475 0.2104 0.2799 0.7795

Fundraising 0.00002 0.0255 0.9796 -0.0003 -0.1914 0.8482 0.0004 1.4318 0.1522

Market Conditions 4.3553 1.9961 0.0459 -1.3877 -0.8020 0.4225 1.1070 1.0651 0.2868

Preplanned Exit 1.9696 1.2263 0.2201 -0.6243 -0.3426 0.7319 1.1470 1.2025 0.2292

Coefficient t-statistic p-value* Coefficient t-statistic p-value* Coefficient t-statistic p-value*

Constant 16.3158 2.0161 0.0438 3.9083 1.3993 0.1617 3.9789 2.9397 0.0033

Technology -5.7817 -1.7299 0.0836 N/A** N/A** N/A** -0.4488 -0.4577 0.6471

Duration -1.7639 -1.9076 0.0564 -0.1461 -0.6908 0.4897 -0.2197 -1.6636 0.0962

Market/Book -0.6524 -1.8228 0.0683 -0.0783 -0.1057 0.9158 -0.2134 -1.5004 0.1335

Market Conditions -1.8654 -0.9307 0.3520 N/A** N/A** N/A** -1.1553 -1.0449 0.2961

* Two-sided test.

** Not Applicable. Variable excluded to avoid collinearity problems. Similarly, variables not shown were excluded to avoid collinearity problems.

Table 5b. Logit Estimates of the Likelihood of Cash Consideration in Venture Capital Acquisition Exits in Canada and the United States

United States Canada Full Sample Estimates

Table 5a. Logit Estimates of the Extent of Venture Capital IPO Exits in Canada and the United States

United States Canada Full Sample Estimates

64

© Cumming & Johan (2013) Exits

Coefficient t-statistic p-value* Coefficient t-statistic p-value* Coefficient t-statistic p-value*

Constant 8.7239 0.8487 0.3960 -0.2319 -0.2139 0.8306 3.4863 1.4486 0.1474

Duration 0.1528 0.4005 0.6888 0.5147 1.0835 0.2786 0.2716 0.9795 0.3273

Market/Book -4.5011 -0.7136 0.4755 -0.1801 -0.6207 0.5348 -0.4544 -1.7349 0.0828

Fundraising -0.0014 -0.8524 0.3940 N/A** N/A** N/A** -0.0010 -1.2967 0.1947

Market Conditions -3.2965 -0.6533 0.5136 N/A** N/A** N/A** -1.7177 -1.0815 0.2795

Coefficient t-statistic p-value* Coefficient t-statistic p-value* Coefficient t-statistic p-value*

Constant -4.1615 -0.8387 0.4017 3.3246 1.8021 0.0715 4.9667 2.9692 0.0030

Technology N/A** N/A** N/A** -0.4461 -0.4109 0.6812 -0.0239 -0.0241 0.9808

Duration -1.0598 -0.4219 0.6731 -0.2537 -1.9289 0.0537 -0.2151 -1.8143 0.0696

Market/Book 1.7273 0.5900 0.5552 -0.0703 -0.3117 0.7552 -0.0309 -0.1558 0.8762

Fundraising N/A** N/A** N/A** 0.0017 1.2522 0.2105 -0.0014 -2.1257 0.0335

Preplanned N/A** N/A** N/A** -2.3292 -1.4464 0.1481 -1.9042 -1.3994 0.1617

Unsolicited Offer N/A** N/A** N/A** -1.0873 -0.7297 0.4656 -0.4738 -0.3403 0.7336

Coefficient t-statistic p-value* Coefficient t-statistic p-value* Coefficient t-statistic p-value*

Constant 3.7177 2.0021 0.0453 5.9173 2.1892 0.0286 4.5620 3.3746 0.0007

Duration -0.2676 -0.7603 0.4471 -0.5285 -1.5436 0.1227 -0.4225 -1.7465 0.0807

Market Conditions 0.1290 0.0875 0.9303 N/A** N/A** N/A** 0.5814 0.4075 0.6836

* Two-sided test.

** Not Applicable. Variable excluded to avoid collinearity problems. Similarly, variables not shown were excluded to avoid collinearity problems.

Table 5c. Logit Estimates of the Extent of Venture Capital Secondary Sale Exits in Canada and the United States

United States Canada Full Sample Estimates

Table 5d. Logit Estimates of the Extent of Venture Capital Buyback Exits in Canada and the United States

United States Canada Full Sample Estimates

Table 5e. Logit Estimates of the Likelihood of Venture Capital Write-offs versus Write-downs in Canada and the United States

United States Canada Full Sample Estimates

65

© Cumming & Johan (2013) Exits

Conclusions (1 of 2)

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

DefinitionsHypothesesDataEmpirical TestsConclusion

• Partial Exits Mitigate informational asymmetries between the entrepreneurial

firm & its new owners But very little overlap in cross-country results – WHY?

• US: Partial exits for buybacks, buyouts, technology firms

• Canada – Greater Legal & Institutional Barriers: Greater need for partial exits for IPOs and secondary sales Inefficient exit strategies for longer VC duration, and technology firms

66

© Cumming & Johan (2013) Exits

Conclusions (2 of 2)

Exits – Definitions and OverviewEuropean ExitsCanadian Exits

Australasian ExitsUS versus Canada Full Partial Exits

DefinitionsHypothesesDataEmpirical TestsConclusion

• Full/Partial Selection Effects: Affect the risk and return to venture capital

• US: Higher risk and higher return Less onerous securities regulation Private funds

• Canada: Lower risk and lower return More onerous securities legislation Government sponsorship of venture capital

67

Top Related