Zambia - International University of Japan · Country Report March 2004 Zambia March 2004 The...

31

Country Report March 2004 Zambia March 2004 The Economist Intelligence Unit 15 Regent St, London SW1Y 4LR United Kingdom Zambia at a glance: 2004-05 OVERVIEW Although the political scene will remain volatile, the Economist Intelligence Unit expects the president, Levy Mwanawasa, and the ruling Movement for Multiparty Democracy (MMD) to remain in power throughout the forecast period. Government expenditure restraint should be sufficient for a new poverty reduction and growth facility to be agreed with the IMF by mid-2004. Continued tight monetary policy will allow average inflation to fall to 16% in 2004 and 15% in 2005. This high inflation, coupled with a strong demand for foreign exchange, will cause the kwacha to depreciate to an average of ZK4,904:US$1 in 2004 and ZK5,645:US$1 in 2005. Rising copper exports will reduce the current-account deficit to 4.7% of GDP in 2004 and 4.5% of GDP in 2005. Key changes from last month Political outlook • The dissident 'True Blue' faction of the MMD had little impact on the party's first provincial convention, in Lusaka on February 21st, as the convention adopted Mr Mwanawasa as its candidate for the MMD in the 2006 presidential election. Mr Mwanawasa may face a tougher challenge at the party's national convention, due in April or May, but he is likely to be confirmed as the party's candidate for the next election. Economic policy outlook • The government has announced further expenditure cutbacks in an attempt to appease unions angered by the public-sector pay freeze and the apparent lack of sacrifice at the upper levels of government. Donors are unlikely to welcome the use of these funds for higher public-sector pay, as the unions want, and we expect the government to withstand union demands. Economic forecast • Mopani Copper Mines, the country's second-largest copper producer, has announced that it intends to increase output from 134,000 tonnes in 2003 to 160,000 tonnes in 2004. This is higher than we had previously anticipated, and we have therefore raised our forecast for total copper production, which has caused our projection for real GDP growth to rise from 3.2% to 3.4% in 2004. A further increase in copper production will lift real GDP growth to 4% in 2005.

Transcript of Zambia - International University of Japan · Country Report March 2004 Zambia March 2004 The...

Country Report March 2004

Zambia

March 2004

The Economist Intelligence Unit15 Regent St, London SW1Y 4LRUnited Kingdom

Zambia at a glance: 2004-05

OVERVIEWAlthough the political scene will remain volatile, the Economist IntelligenceUnit expects the president, Levy Mwanawasa, and the ruling Movement forMultiparty Democracy (MMD) to remain in power throughout the forecastperiod. Government expenditure restraint should be sufficient for a newpoverty reduction and growth facility to be agreed with the IMF by mid-2004.Continued tight monetary policy will allow average inflation to fall to 16% in2004 and 15% in 2005. This high inflation, coupled with a strong demand forforeign exchange, will cause the kwacha to depreciate to an average ofZK4,904:US$1 in 2004 and ZK5,645:US$1 in 2005. Rising copper exports willreduce the current-account deficit to 4.7% of GDP in 2004 and 4.5% of GDP in2005.

Key changes from last month

Political outlook• The dissident 'True Blue' faction of the MMD had little impact on the party's

first provincial convention, in Lusaka on February 21st, as the conventionadopted Mr Mwanawasa as its candidate for the MMD in the 2006presidential election. Mr Mwanawasa may face a tougher challenge at theparty's national convention, due in April or May, but he is likely to beconfirmed as the party's candidate for the next election.

Economic policy outlook• The government has announced further expenditure cutbacks in an attempt

to appease unions angered by the public-sector pay freeze and the apparentlack of sacrifice at the upper levels of government. Donors are unlikely towelcome the use of these funds for higher public-sector pay, as the unionswant, and we expect the government to withstand union demands.

Economic forecast• Mopani Copper Mines, the country's second-largest copper producer, has

announced that it intends to increase output from 134,000 tonnes in 2003 to160,000 tonnes in 2004. This is higher than we had previously anticipated,and we have therefore raised our forecast for total copper production, whichhas caused our projection for real GDP growth to rise from 3.2% to 3.4% in2004. A further increase in copper production will lift real GDP growth to 4%in 2005.

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The Economist Intelligence Unit delivers its information in four ways: through its digital portfolio, where thelatest analysis is updated daily; through printed subscription products ranging from newsletters to annualreference works; through research reports; and by organising seminars and presentations. The firm is amember of The Economist Group.

LondonThe Economist Intelligence Unit15 Regent StLondonSW1Y 4LRUnited KingdomTel: (44.20) 7830 1007Fax: (44.20) 7830 1023E-mail: [email protected]

New YorkThe Economist Intelligence UnitThe Economist Building111 West 57th StreetNew YorkNY 10019, USTel: (1.212) 554 0600Fax: (1.212) 586 0248E-mail: [email protected]

Hong KongThe Economist Intelligence Unit60/F, Central Plaza18 Harbour RoadWanchaiHong KongTel: (852) 2585 3888Fax: (852) 2802 7638E-mail: [email protected]

Website: www.eiu.com

Electronic deliveryThis publication can be viewed by subscribing online at www.store.eiu.com

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, online databasesand as direct feeds to corporate intranets. For further information, please contact your nearest EconomistIntelligence Unit office

Copyright© 2004 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication norany part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means,electronic, mechanical, photocopying, recording or otherwise, without the prior permissionof The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However, theEconomist Intelligence Unit does not accept responsibility for any loss arising from reliance on it.

ISSN 1478-0372

Symbols for tables"n/a" means not available; "–" means not applicable

Printed and distributed by Patersons Dartford, Questor Trade Park, 151 Avery Way, Dartford, Kent DA1 1JS, UK.

Zambia 1

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Contents

3 Summary

4 Political structure

5 Economic structure5 Annual indicators6 Quarterly indicators

7 Outlook for 2004-057 Political outlook8 Economic policy outlook10 Economic forecast

13 The political scene

17 Economic policy

23 The domestic economy23 Economic trends24 Mining26 Infrastructure26 Financial services28 Tourism28 Foreign trade and payments

List of tables10 International assumptions summary12 Forecast summary19 Income tax bands21 Budget performance in 200323 Real growth by sector26 Telecoms providers, 200327 Stockmarket indicators29 Net official development assistance

List of figures

12 Gross domestic product12 Consumer price inflation18 Budgeted expenditure20 Budgeted revenue24 Inflation25 Copper price28 Tourism29 Foreign-exchange reserves

Zambia 3

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Summary March 2004

Although the political scene will remain volatile, the Economist IntelligenceUnit expects the president, Levy Mwanawasa, and the ruling Movement forMultiparty Democracy (MMD) to stay in power throughout the forecast period.Government expenditure restraint should be sufficient for a new povertyreduction and growth facility to be agreed with the IMF by mid-2004. Real GDPgrowth will slow to 3.4% in 2004 as growth in the agriculture sector eases.Higher copper production will lift real GDP growth to 4% in 2005. Continuedtight monetary policy will allow average inflation to fall to 16% in 2004 and 15%in 2005. This high inflation, coupled with a strong demand for foreignexchange, will cause the kwacha to depreciate to an average of ZK4,904:US$1 in2004 and ZK5,645:US$1 in 2005. Rising copper exports will reduce the current-account deficit to 4.7% of GDP in 2004 and 4.5% of GDP in 2005.

The director of public prosecutions has been replaced after questions over hisintegrity were raised following the poor start to the corruption trials being facedby the former president, Frederick Chiluba. The first national one-day strike for16 years was held to protest against a public-sector wage freeze announced inthe budget. Mr Mwanawasa has survived a potential challenge by a dissidentfaction of the MMD and has been selected as the party's candidate for the 2006election at the Lusaka provincial party convention. Most opposition partieshave struggled after losing senior officials to the MMD. Mr Mwanawasa hasquashed death sentences for 44 soldiers convicted of treason in 1999.

The government has tightened fiscal policy in the 2004 budget, which aims toreduce the fiscal deficit to 2% of GDP, from 5.1% in 2003. Wage and salarypayments have been frozen as a percentage of GDP, but debt-servicing costs areprojected to rise substantially. Two new top rates of tax have been introduced,but little attempt has been made to broaden the tax base. Yields on governmentdebt have fallen, as demand has remained strong after a recent cut incommercial bank reserve requirements. Some commercial banks have startedto offer basic services to townships.

Real GDP growth has been estimated at 4.3% in 2003, owing to strong growth inthe agriculture, manufacturing and construction sectors. Year-on-year inflationfell to 16.8% in February, owing to an easing of food price inflation. Doubtshave emerged over the sale of Konkola Copper Mines to Sterlite Industries ofIndia. Two mobile-phone providers have announced major expansionprogrammes. The stock exchange has been hit by tax changes in the budget.

Debt repayments to the IMF have caused foreign-exchange reserves to plunge toUS$245m in January, from US$558m in May. New data from the OECD showthat donor lending to Zambia rose to US$641m in 2002.

Editors: Paul Gamble (editor); Angus Downie (consulting editor)Editorial closing date: March 12th 2004

All queries: Tel: (44.20) 7830 1007 E-mail: [email protected] report: Full schedule on www.eiu.com/schedule

Outlook for 2004-05

The political scene

Economic policy

The domestic economy

Foreign trade and payments

4 Zambia

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Political structure

Republic of Zambia

Unitary republic

Based on the 1996 constitution

National Assembly; 150 members elected by universal suffrage, serving a five-year term.The president can appoint eight further members

Presidential and legislative elections due in late 2006 (last presidential and legislativeelections December 2001)

President, elected by universal suffrage for a term of five years

The president and his appointed cabinet. The last major reshuffle was in May 2003

The Movement for Multiparty Democracy (MMD) is the ruling party and holds a slimparliamentary majority. The United Party for National Development (UPND), formed inlate 1998, is the largest opposition party in parliament, followed by the former sole party,the United National Independence Party (UNIP) and the recently formed Forum forDemocracy and Development (FDD). Other parties represented in parliament are theHeritage Party, the Zambia Republican Party (ZRP) and the Patriotic Front

President & minister of defence Levy MwanawasaVice-president Nevers Mumba

Agriculture & co-operatives Mundia SikatanaCommerce, trade & industry Dipak PatelCommunications & transport Bates NamuyambaEducation Andrew MulengaEnergy & water development George MpomboFinance & national planning Ng'andu MagandeForeign affairs Kalombo MwansaHealth Brian ChituwoHome affairs Ronnie ShikapwashaInformation & broadcasting Mutale NalumangoLands Judith KapijimpangaLabour & social security Patrick KafumukacheLegal affairs George KundaLocal government & housing Sylvia MaseboMines & minerals development Kaunda LembalembaScience, technology & vocational training Abel ChambeshiTourism, environment & natural resources Patrick KalifungwaWorks & energy development Ludwig Sondashi

Caleb Fundanga

Official name

Form of state

Legal system

National legislature

Main political parties

Key ministers

National elections

Central bank governor

Head of state

National government

Zambia 5

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Economic structure

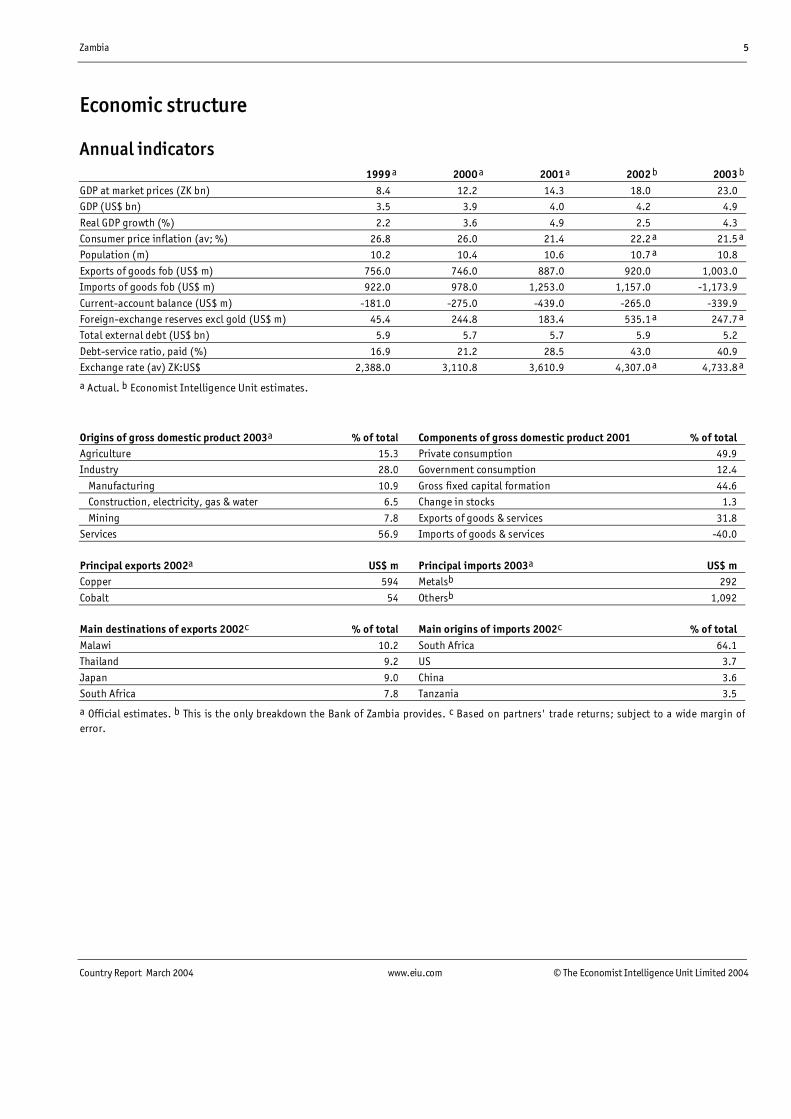

Annual indicators1999 a 2000 a 2001a 2002 b 2003 b

GDP at market prices (ZK bn) 8.4 12.2 14.3 18.0 23.0GDP (US$ bn) 3.5 3.9 4.0 4.2 4.9

Real GDP growth (%) 2.2 3.6 4.9 2.5 4.3Consumer price inflation (av; %) 26.8 26.0 21.4 22.2 a 21.5 a

Population (m) 10.2 10.4 10.6 10.7 a 10.8

Exports of goods fob (US$ m) 756.0 746.0 887.0 920.0 1,003.0Imports of goods fob (US$ m) 922.0 978.0 1,253.0 1,157.0 -1,173.9

Current-account balance (US$ m) -181.0 -275.0 -439.0 -265.0 -339.9Foreign-exchange reserves excl gold (US$ m) 45.4 244.8 183.4 535.1 a 247.7 a

Total external debt (US$ bn) 5.9 5.7 5.7 5.9 5.2

Debt-service ratio, paid (%) 16.9 21.2 28.5 43.0 40.9Exchange rate (av) ZK:US$ 2,388.0 3,110.8 3,610.9 4,307.0 a 4,733.8 a

a Actual. b Economist Intelligence Unit estimates.

Origins of gross domestic product 2003a % of total Components of gross domestic product 2001 % of totalAgriculture 15.3 Private consumption 49.9Industry 28.0 Government consumption 12.4

Manufacturing 10.9 Gross fixed capital formation 44.6 Construction, electricity, gas & water 6.5 Change in stocks 1.3

Mining 7.8 Exports of goods & services 31.8Services 56.9 Imports of goods & services -40.0

Principal exports 2002a US$ m Principal imports 2003a US$ mCopper 594 Metalsb 292

Cobalt 54 Othersb 1,092

Main destinations of exports 2002c % of total Main origins of imports 2002c % of totalMalawi 10.2 South Africa 64.1Thailand 9.2 US 3.7

Japan 9.0 China 3.6South Africa 7.8 Tanzania 3.5

a Official estimates. b This is the only breakdown the Bank of Zambia provides. c Based on partners' trade returns; subject to a wide margin oferror.

6 Zambia

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Quarterly indicators2002 20031 Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr 2 Qtr 3 Qtr 4 Qtr

PricesConsumer prices (1994=100) 672.3 684.9 712.2 765.7 828.3 843.5 858.3 911.7Consumer prices (% change, year on year) 19.0 20.7 23.7 25.3 23.2 23.2 20.5 19.1Copper, LME (US$/tonne) 1,559.0 1,612.1 1,516.7 1,553.4 1,662.7 1,641.4 1,753.1 2,060.3

Financial indicatorsExchange rate ZK:US$ (av) 3,895 4,130 4,504 4,699 4,652 4,846 4,740 4,696Exchange rate ZK:US$ (end-period) 3,936 4,481 4,557 4,334 4,874 4,828 4,802 4,771Deposit rate (av; %) 24.30 23.80 22.43 22.77 22.50 22.43 21.50 21.37Weighted lending base rate (av; %) 48.57 45.97 43.67 42.59 43.47 41.42 39.10 38.30Treasury bill, 91-day rate (av; %) 45.00 33.72 29.15 30.28 31.97 31.32 30.97 25.64M1 (end-period; ZK bn) 928.7 1,056.7 1,132.5 1,339.3 1,254.1 1,427.9 1,459.5 n/aM1 (% change, year on year) 17.5 20.9 11.8 28.6 35.0 35.1 28.9 n/aM2 (end-period; ZK bn) 2,704.4 3,129.6 3,227.9 3,619.2 3,673.5 3,896.6 4,073.3 n/aM2 (% change, year on year) 30.6 34.5 21.7 31.1 35.8 24.5 26.2 n/aSectoral trendsCopper in concentrates, production ('000 tonnes 77.8 81.1 86.1 91.7 74.3 87.4 91.9 96.2Copper in concentrates, exports ('000 tonnes) 79.0 83.7 81.1 85.1 79.3 90.1 97.0 87.0Cobalt production (tonnes) 1,097 1,016 1,015 854 742 859 953 649Cobalt exports (tonnes) 1,131 1,079 1,018 788 756 858 822 938Foreign trade (US$ m)a

Exports fob 195.3 199.8 213.1 193.4 248.3 222.2 241.7 n/aImports fob -238.2 -266.8 -310.0 -371.6 -271.9 -298.0 -342.0 n/aTrade balance -42.9 -67.0 -96.9 -178.2 -23.6 -75.9 -100.3 n/aForeign reserves (US$ m)Reserves excl gold (end-period) 170.6 364.7 379.5 535.1 509.6 415.6 403.7 247.7

a DOTS estimates.

Sources: Bank of Zambia, Statistics Fortnightly; IMF, International Financial Statistics; Direction of Trade Statistics.

Zambia 7

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Outlook for 2004-05

Political outlook

The president, Levy Mwanawasa, and the ruling Movement for MultipartyDemocracy (MMD) are expected to remain in power throughout the forecastperiod. Several opposition figures, including some of the president's sternestcritics, have been appointed to government, in most cases without the consentof their respective parties. While weakening the opposition, this has split theruling party and highlighted the fact that many politicians are only concernedwith the patronage and status that political office confers. Aggrieved MMDmembers—mainly supporters of the former president, Frederick Chiluba,including influential businessmen—have been trying to form parallel partystructures in order to challenge Mr Mwanawasa's leadership at the long-overdue party convention. These dissident MMD members—known as the"True Blue" faction—did not have much of an impact on the first provincialMMD convention, in Lusaka on February 21st, and will need to be betterorganised to challenge the president when a national convention is held.

An additional reason for parliamentarians to support Mr Mwanawasa is thatthey do not want to be caught up in the trials that Mr Chiluba and six othersare facing over corruption, which could implicate several politicians within thecurrent administration. So far the trials, currently suspended, have gone well forthe former president, as none of the witnesses called by the prosecution haveimplicated Mr Chiluba in the theft of public funds. This disappointing start tothe case from Mr Mwanawasa's perspective has raised questions over the roleof the director of public prosecutions (DPP), Mukelabai Mukelabai. He wasappointed by Mr Chiluba, and is alleged to have met with one of the co-accused over the Christmas holidays. In reaction to this Mr Mwanawasa hasappointed an interim replacement for Mr Mukelabai, who was subjected to alegal tribunal. The results of the tribunal have yet to be made public, but itseems unlikely that he will be reinstated. Although the acting DPP, CarolineSokoni, is considered more credible than Mr Mukelabai, the difficulty inproducing a paper trail that would conclusively prove Mr Chiluba's directinvolvement in corruption suggests that he will not be convicted.

Mr Mwanawasa is facing a court challenge himself, as the opposition iscontesting his victory in the presidential election. This case too is likely to proveunsuccessful, as, although the court will be able to point to numerousirregularities in the conduct of the poll, these will not be sufficient to warrantthe constitutional confusion that would arise if the election were to beannulled. Furthermore, the president has said that the defence will take fouryears to present its case—the prosecution closed its case on November 10th—taking it beyond the 2006 election, after which a rerun of the 2001 poll wouldbe nonsensical.

During 2004 much domestic political attention will focus on the constitutionalreview process, which began in August. Debate has been raging over the modeof adopting the new constitution, which is currently being prepared by a

Domestic politics

8 Zambia

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

constitutional review commission handpicked by Mr Mwanawasa. The govern-ment is keen for the responsibility for approval to lie with parliament, as theMMD's majority means that recommendations to weaken the presidencywould not be countenanced. Civil society groups are stepping up pressure forapproval by a constituent assembly (which would include all interested parties)in order that a partisan document is not produced—the main criticism of the1996 constitution. The government acknowledges this, but is likely to maintainthat it cannot afford to fund a constituent assembly.

Zambia is not expected to face any external threats over the forecast period—theEconomist Intelligence Unit expects the peace in neighbouring Angola to hold,which will allow repatriation of most of the Angolan refugees who had settledover the border in Zambia. Instead, the focus will be on relations with keydonors. The IMF and bilateral donors suspended much of the budgetarysupport scheduled for 2003 in protest at the government's fiscal laxity.Although we expect funding to be resumed in mid-2004, donors will bevigilant over governance issues. Should Mr Mwanawasa be implicated in thecorruption trials or in manipulation of the presidential election, bilateral donorsmay well stop funding the government.

Economic policy outlook

The immediate policy priority is to restore IMF budgetary support, which wassuspended in June 2003 owing to government overspending (largely caused bya higher-than-budgeted pay rise for public-sector workers). In his state of thenation address in parliament in January, Mr Mwanawasa emphasised thatexpenditure restraint was vital and that the government would not exceed thepublic-sector wage ceiling agreed with the IMF. This paved the way for thegovernment to announce a freeze in public-sector pay in the 2004 budget,along with other expenditure-reduction and revenue-raising measures. Weexpect this commitment to be broadly adhered to, and this should lead to theannouncement of a new lending programme under the poverty reduction andgrowth facility (PRGF) in mid-2004—the previous one lapsed in March 2003.This should allow Zambia to reach completion point under the IMF-World Bankheavily indebted poor countries (HIPC) debt-relief initiative by the end of 2004,leading to a reduction in external debt stock. The main stumbling block to thiswill be the public-sector unions, who were already aggrieved after pressurefrom the IMF caused the government to withdraw a 40% pay increase in 2003.The unions are pressing for a pay rise in 2004, but donor pressure means thatthe government is likely to withstand their demands until a new PRGF isagreed. The other area of strain between the government and the Fund isprivatisation, a policy that Mr Mwanawasa and the minister of finance andnational planning, Ng'andu Magande, both oppose. Tension over donordemands for the sales of Zamtel, the telecommunications parastatal, theZambia State Insurance Corporation and the Zambia National CommercialBank could prevent the resumption of donor funding or may cause it to besuspended until later in the forecast period.

Policy trends

International relations

Zambia 9

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

The main goals of a new PRGF are likely to reflect the poverty reductionstrategy paper (PRSP), which is supposed to form the basis of economic policy.Therefore, the government will attempt to pursue policies aimed at diversifyingthe economy away from mining, developing agriculture and reducing poverty.Capacity constraints, weak political commitment, confusion and potentialcompetition with other economic plans that the government has produced willprevent much progress from being made.

The 2004 budget unveiled by Mr Magande, the finance minister, onFebruary 6th, projects a decline in the fiscal deficit, from 5.1% of GDP in 2003 to2% of GDP. The budget is clearly focused on austere measures to facilitatequalification for a new PRGF by June. Public-sector wages have been frozen,while two new rates of income tax have been introduced (at 35% and 40%).This latter move reflects a clear trend towards increasing the tax burden of high-income earners; little was done to broaden the personal tax base. Most of thespecific tax measures introduced will be successful at raising revenue, althoughsome of this could be offset by reducing the spending power of the formalsector, hitting overall tax revenue. The perennial problem of lax fiscalmanagement will make it difficult for the government to contain spending.Nonetheless, the carrot of IMF funding and HIPC debt relief means that thegovernment should be able to do enough to ensure the resumption of donorfunding around mid-year. This will boost revenue in the second half of 2004.The shortfall in donor funding in 2003 and the first half of 2004 is forcing thegovernment to finance its deficit domestically, contributing to an increase in thedomestic debt-service bill in 2004. Expenditure restraint in the first half of theyear and an increase in donor budgetary support in the second half shouldlead to a reduction in the fiscal deficit to 3.1% of GDP in 2004.

A full year of donor support in 2005 will increase revenue but, with thegovernment beginning to focus on the elections in 2006, expenditure will alsorise. In addition, political expediency means that the government is highlylikely to raise public-sector pay again. Public finance management and account-ability reforms are being implemented in 2004 and should create savings byimproving the quality and coherence of spending plans. Although capacityconstraints in the civil service will prevent those areas being reformed fromfunctioning optimally, the expected improvement in expenditure control willcause the fiscal deficit to narrow to 2.9% of GDP in 2005. Greater externalfinancing in 2004 and 2005 should reduce the need for the government to issuenew domestic debt to finance the deficit.

Monetary policy is focused on achieving year-end inflation targets of 15% in2004 and 10% in 2005. Although we expect these to be missed, the Bank ofZambia (BoZ, the central bank) will continue to aim to reduce inflationthroughout the forecast period by slowing growth in reserve money throughthe use of open-market operations. The BoZ may also make further reductionsto the commercial bank reserve requirement in order to encourage greatercommercial bank lending. The statutory reserve requirement was reduced from17.5% to 14% in October and the BoZ would like to reduce it to single figures. Asthis frees up funds for banks to lend, it should allow an increase in bank

Fiscal policy

Monetary policy

10 Zambia

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

profitability and therefore a reduction in the spread between lending anddeposit rates (currently around 17 percentage points). It is, however, alsoinflationary, so the BoZ is likely to be cautious in reducing the reserverequirement further. Even if the spread is substantially lowered, there are manyother bank charges that borrowers face and it is not clear whether banks wouldbecome any more willing to lend—strong commercial bank demand hasallowed Treasury bill rates to fall to near zero in real terms. We therefore expectreal lending rates to remain high and real deposit rates to remain negligible,owing to the low level of financial intermediation. The government's loosefiscal policy means that we expect only a slight decline in nominal rates, in linewith the forecast fall in inflation.

Economic forecast

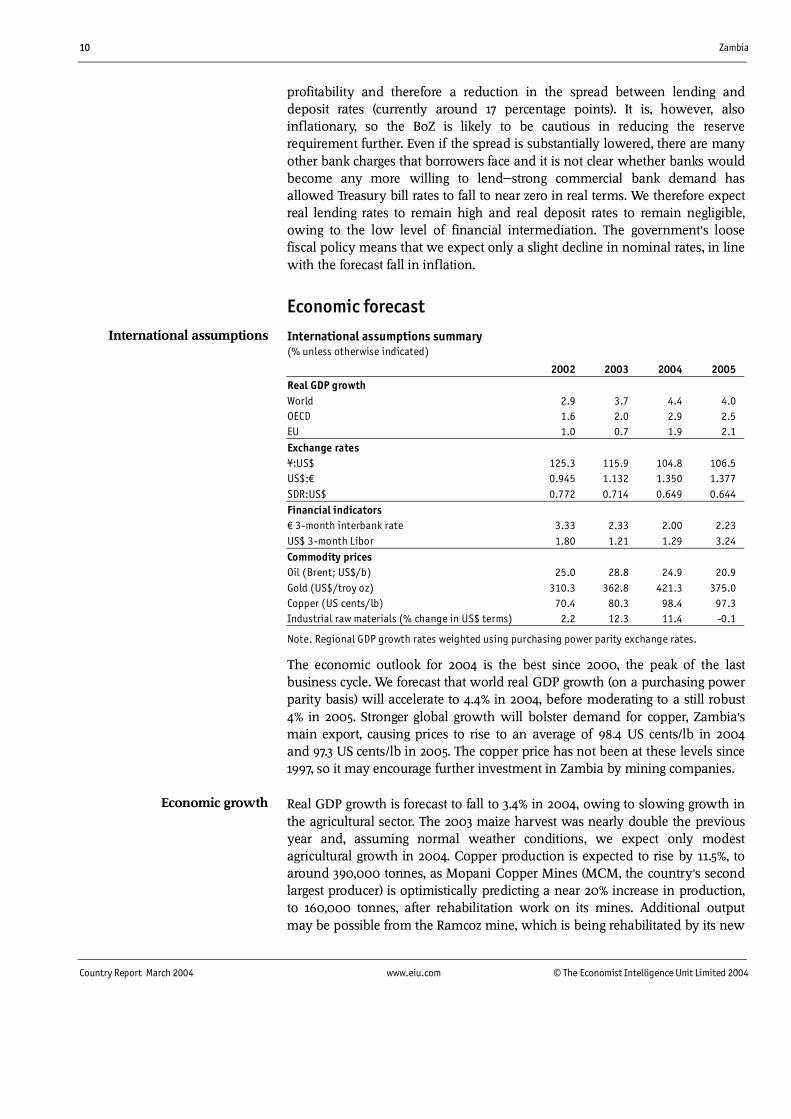

International assumptions summary(% unless otherwise indicated)

2002 2003 2004 2005Real GDP growthWorld 2.9 3.7 4.4 4.0OECD 1.6 2.0 2.9 2.5EU 1.0 0.7 1.9 2.1

Exchange rates¥:US$ 125.3 115.9 104.8 106.5US$:€ 0.945 1.132 1.350 1.377SDR:US$ 0.772 0.714 0.649 0.644Financial indicators€ 3-month interbank rate 3.33 2.33 2.00 2.23US$ 3-month Libor 1.80 1.21 1.29 3.24Commodity pricesOil (Brent; US$/b) 25.0 28.8 24.9 20.9Gold (US$/troy oz) 310.3 362.8 421.3 375.0Copper (US cents/lb) 70.4 80.3 98.4 97.3Industrial raw materials (% change in US$ terms) 2.2 12.3 11.4 -0.1

Note. Regional GDP growth rates weighted using purchasing power parity exchange rates.

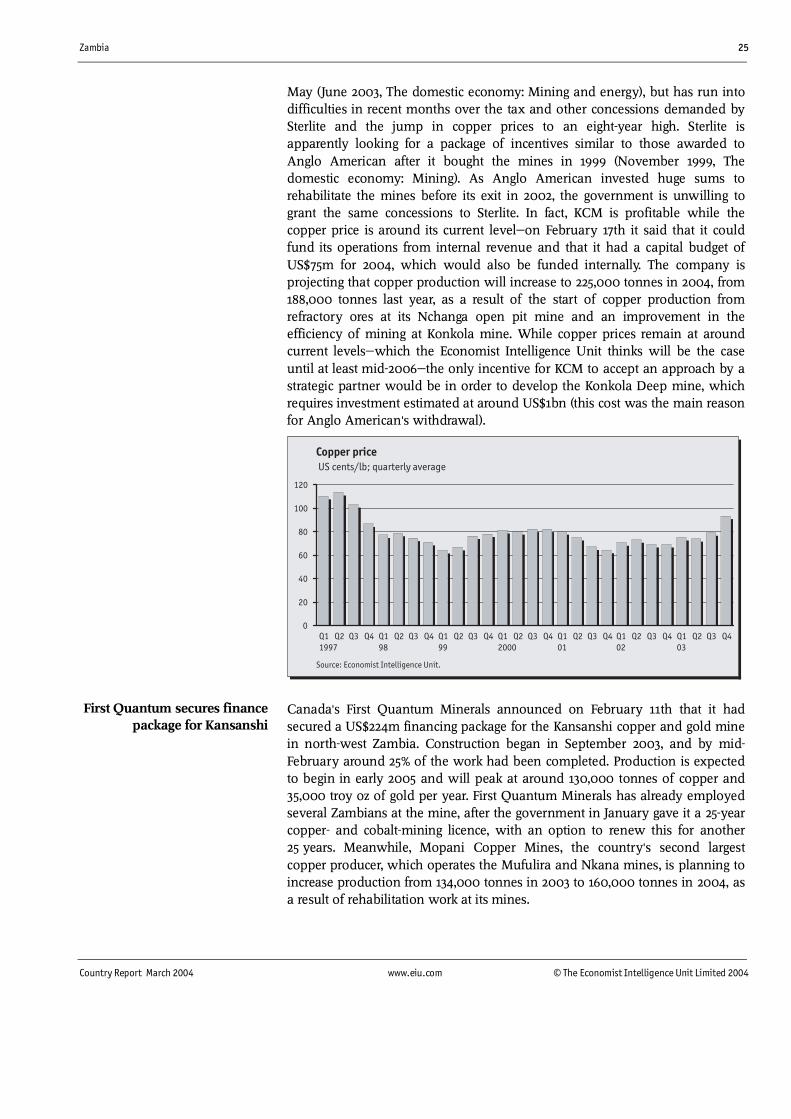

The economic outlook for 2004 is the best since 2000, the peak of the lastbusiness cycle. We forecast that world real GDP growth (on a purchasing powerparity basis) will accelerate to 4.4% in 2004, before moderating to a still robust4% in 2005. Stronger global growth will bolster demand for copper, Zambia'smain export, causing prices to rise to an average of 98.4 US cents/lb in 2004and 97.3 US cents/lb in 2005. The copper price has not been at these levels since1997, so it may encourage further investment in Zambia by mining companies.

Real GDP growth is forecast to fall to 3.4% in 2004, owing to slowing growth inthe agricultural sector. The 2003 maize harvest was nearly double the previousyear and, assuming normal weather conditions, we expect only modestagricultural growth in 2004. Copper production is expected to rise by 11.5%, toaround 390,000 tonnes, as Mopani Copper Mines (MCM, the country's secondlargest producer) is optimistically predicting a near 20% increase in production,to 160,000 tonnes, after rehabilitation work on its mines. Additional outputmay be possible from the Ramcoz mine, which is being rehabilitated by its new

Economic growth

International assumptions

Zambia 11

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

owners, J&W Investments of Switzerland. Only a small increase in productionis expected from Konkola Copper Mines (KCM, the country's largest producer)owing to the uncertainty created by its proposed sale to Sterlite Industries ofIndia, which now looks in doubt. Manufacturing growth is heavily influencedby food processing and will therefore moderate in 2004. Donor-funded workon the rehabilitation of major roads and the construction of private housingwill ensure continued strong construction growth. Services will recover in linewith increasing economic activity and greater demand in the mining sector,stimulated by higher copper prices.

The opening in early 2005 of the Kansanshi mine, operated by Canada's FirstQuantum Minerals, will further boost copper production (Kansanshi is aimingfor peak production of 130,000 tonnes per year). With greater production atRamcoz and incremental production increases by KCM and MCM, we expecttotal production to reach 440,000 tonnes in 2005, which will lift real GDPgrowth to 4%. This boost to the mining sector will stimulate growth in mine-related services, increasing services growth. Agricultural growth is expected toremain at 2.5%, assuming normal weather conditions.

Year-on-year inflation fell to 16.8% in February, from 17.4% in January, owing tothe continued slowdown in food price inflation as a result of improved maizeavailability. There is little scope for year-on-year food price inflation to slowmuch further, as the food supply situation improved significantly in March2003 with the availability of the first of last year's bumper crop. Althoughslightly below average, the current rains are sufficient for good crop develop-ment, so food supply problems are not expected in 2004. Provided that this isthe case and that donor support resumes during the year, thus reducing theneed for inflationary financing of the deficit, we expect inflation to fall to anaverage of 16% in 2004. Continued tight monetary policy should allow inflationto maintain its downward trend in 2005, although poor fiscal managementmeans that it will only fall to an average of 15%.

Higher export revenue, owing to increased copper production and prices,should slow the rate of depreciation of the kwacha compared with previousyears. However, high inflation, a lack of confidence in the currency and astructurally higher demand than supply for foreign exchange will ensure that itcontinues to lose value. We therefore expect the kwacha to weaken to anaverage of ZK4,904:US$1 in 2004 and ZK5,645:US$1 in 2005. Historically, thekwacha has been vulnerable to sharp bouts of depreciation. Similar eventscould occur over the forecast period. Predicting the timing of this is difficult, butproblems are likely to be encountered if a new PRGF is not agreed in June, as iscurrently anticipated. The BoZ will intervene to smooth out short-termfluctuations, but these will postpone, rather than avert, currency depreciation.

Export earnings are forecast to increase in 2004 and 2005 because of highercopper prices and export volumes. The jump will be particularly pronouncedin 2005, owing to investment in the Ramcoz mine bearing fruit, together with anumber of other planned projects coming on stream. As most of theinvestment goods required for the mines will be imported, import growth is

Exchange rates

Inflation

External sector

12 Zambia

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

forecast to rise sharply in 2004. Import growth will remain strong in 2005,owing to the import-dependent nature of the economy. An increase in trade-related costs associated with the rise in imports will more than offset increasedtourism revenues, causing the services deficit to widen. Increased profitremittances will cause the income deficit to rise (this rise will be greater ifSterlite takes over KCM). The expected resumption of donor inflows in 2004will cause the surplus on the current transfers account to rise. A full year ofdonor funding in 2005 will further lift inflows of current transfers. Overall, thecurrent-account deficit is forecast to narrow to 4.7% of GDP in 2004 and 4.5% ofGDP in 2005, owing to increased donor transfers and rising copper exports.

Forecast summary(% unless otherwise indicated)

2002a 2003 a 2004b 2005b

Real GDP growth 2.5 4.3 3.4 4.0Gross industrial growth 9.7 6.4 6.0 6.6

Gross agricultural production growth -1.7 5.0 2.5 2.5Consumer price inflation (av) 22.2c 21.4 c 16.0 15.0Consumer price inflation (year-end) 26.7c 17.2 c 17.0 15.1

Short-term interbank rate 45.2c 40.6 c 39.2 37.0Government balance (% of GDP) -3.3 -5.0 -3.1 -2.9

Exports of goods fob (US$ m) 917.0 1,003.0 1,310.1 1,403.2Imports of goods fob (US$ m) 1,204.0 1,173.9 1,361.7 1,457.0Current-account balance (US$ m) -312.0 -339.9 -260.8 -253.5

Current-account balance (% of GDP) -7.4 -7.0 -4.7 -4.5External debt (year-end; US$ bn) 5.9 5.2 5.3 4.8

Exchange rate ZK:US$ (av) 4,307.0c 4,733.8 c 4,903.9 5,645.3Exchange rate ZK:¥100 (av) 3,436.0c 4,084.4 c 4,681.5 5,300.8

Exchange rate ZK:€ (av) 4,069.7c 5,359.8 c 6,620.2 7,776.4Exchange rate ZK:SDR (av) 5,579.0c 6,631.6 c 7,556.1 8,769.9

a Economist Intelligence Unit estimates. b Economist Intelligence Unit forecasts. c Actual.

Zambia 13

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

The political scene

An acting director of public prosecutions (DPP), Caroline Sokoni, wasappointed on February 5th to replace Mukelabai Mukelabai following concernsover his impartiality in the corruption trials being faced by Frederick Chiluba,the former president, and six former senior government officials (December2003, The political scene). Specifically, Mr Mukelabai is accused of meeting oneof the accused, the former intelligence chief, Xavier Chungu, over the Christmasholidays. Mr Mukelabai pleaded his innocence but the president, LevyMwanawasa, insisted that he should leave office. Legally, a DPP can only beremoved from office for insanity, serious misconduct or if he breaks the law—alegal tribunal must be constituted to remove a DPP for any offences committed.Such a tribunal was appointed in early February and, in accordance withgovernment wishes, was conducted in camera. Although the tribunalcompleted its investigations on February 23rd, there is no indication as to whenits findings will be made public.

Mr Mwanawasa was clearly unhappy with the pace at which evidence wasbeing given against those who are standing trial and the fact that none of thewitnesses called since the case opened on December 9th had implicatedMr Chiluba in the theft of public funds. Mr Mukelabai questioned witnesseswhose testimony was expected to last for a number of days for only a fewhours, even though he was aware of the amount of evidence that they had tooffer while he prepared the prosecution. Mr Mukelabai had also differed withthe two private prosecutors, the brothers Mutembo and Nchima Nchito, whoresigned in December but reversed their decision after intervention from thepresident. The DPP is a political appointment, but there had been few questionsover the integrity of Mr Mukelabai (a Chiluba appointment) ahead of the trial,although his conduct during it was suspicious.

Until the conclusions of the tribunal are released it will be not be possible tojudge how close Mr Mukelabai was to the defendants and whether he wasdeliberately undermining the government's case. The importance of the case toMr Mwanawasa and his much-vaunted fight against corruption cannot be over-stated. If Mr Mukelabai is cleared by the legal tribunal and it is the evidenceagainst Mr Chiluba that is at fault then perceptions might grow that the courtcase is motivated by personal and political reasons rather than the pursuit ofjustice. Furthermore, even though Mr Mwanawasa feels that he can no longerwork with Mr Mukelabai, the president cannot sack the DPP if the tribunalfinds insufficient grounds to dismiss him. Nonetheless, the appointment of theacting DPP indicates that Mr Mukelabai has no future in the role. Mrs Sokoni,who has a reasonably unblemished record, has twice postponed restarting thetrials—they are now due in March—in order to go through the evidence.

The Zambia Congress of Trade Unions (ZCTU) and the Federation for Free TradeUnions of Zambia (FFTUZ) held the first national one-day strike for 16 years onFebruary 18th. This was to protest against a public-sector wage freezeannounced in the national budget on February 6th (see Economic policy). Theunions were not ready to accept a wage freeze and argued that public-sector

The DPP is replaced after a badstart to the ex-president's trial

Public-sector workers strike inresponse to a pay freeze

14 Zambia

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

workers had sacrificed enough after the 40% increase in their housingallowances awarded last year was revoked (September 2003, Economic policy).This was after the IMF and other donors froze lending because of concerns overthe impact that the award would have on the budget deficit and subsequentlycompelled the government to keep the wage bill at under 8.1% of GDP in 2004.The unions also claimed to be protesting about a rise in the top rate of incometax, to 40% from 30%. This was despite the fact that only 51,000 employees—inboth the private and public sectors—out of the 493,000 workers in formalemployment would pay the new top tax rate and vigorous governmentcampaigning to explain that a rise in tax allowances meant that many public-sector workers would be better off after the budget.

The strike was reasonably well attended—union leaders say that about200,000 workers took part, although the government claims that this figurewas a lot lower—but a number of banks and shops remained open. Unionleaders had promised more strikes, but there does appear to be some groundfor compromise. The government has made a number of expenditure cutbackssince the budget was announced—on travel and official parties, for example(see Economic policy)—and the finance minister, Ng'andu Magande, said onMarch 11th that it was considering union proposals for a 15% pay rise.

Further national strikes would pose a problem for Mr Mwanawasa, particularlyif they spiral to encompass more volatile sections of society such as studentsand market traders. However, with the government emphasising the linkbetween the pay freeze and its goal of attaining debt relief under the IMF-WorldBank heavily indebted poor countries (HIPC) initiative, it is not expected toback down in the face of further strikes. Unless any industrial action is widelyobserved and maintained for at least one month it is unlikely to have asignificant impact on the economy, as civil service productivity is generally lowand the work ethic poor. Despite claims to the contrary by the president, theunions are not politicised. While voicing some support for the strike,opposition parties are unlikely to try to strengthen their weak links with tradeunions unless they feel that the strike has mass popular support.

Mr Mwanawasa survived the threat from the recently formed "True Blue"faction of the Movement for Multiparty Democracy (MMD) at the party's firstprovincial convention in Lusaka on February 21st. The "True Blue" group(named after the main colour on the party's flag) combines high-profilesupporters of Mr Chiluba with many of the party rank-and-file who have beendeprived of access to patronage following a clampdown by Mr Mwanawasa forthe purposes of saving the party and the state money. It is rumoured that theywill attempt to challenge Mr Mwanawasa's leadership at the next MMDnational convention (likely to be held in April or May). However, the Lusakaconvention adopted Mr Mwanawasa as the sole candidate for the presidency atthe forthcoming national convention and also for the 2006 presidentialelections. The same decision was taken by the Central province convention onFebruary 28th.

One of main concerns for the president was that the provincial party chairmanand vice-chairman elected at the convention would favour the "True Blue"

The "True Blue" challenge tothe president has little impact

Zambia 15

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

faction. In order to prevent this, the elections were cancelled andMr Mwanawasa appointed both figures himself. As these two officials play akey role in organising the convention and shaping the mood of supportersahead of it, the positive outcome for the president was not surprising. Even ifthe other seven provincial party conventions endorse Mr Mwanawasa'scandidacy for the 2006 elections, it is still likely that there will be a challengerat the party's national convention, particularly if there are concerns over theconduct of the conventions. The size of the "True Blue" faction is not clear.Although the president seems to have consolidated his position since helaunched the anti-corruption crackdown against the Chiluba administration,many MMD members opposed to Mr Mwanawasa have not openly aired theirviews for fear of suspension or expulsion. Aside from those Chiluba supporters,some party members are aggrieved about the number of opposition politiciansthat the president has appointed to parliament in order to undermine theopposition and shore up his support base.

A party convention is long overdue and many of the party officers only holdtheir positions on an acting basis. A lack of finance has proved the maindeterrent to holding a convention in the past. Should Mr Mwanawasa feel thathis position is under serious threat, he will further postpone the convention,although one has to be held before the 2006 elections.

Mr Mwanawasa's recent co-option of a number of leading opposition membersinto government is causing problems for all the main opposition parties, apartfrom the United Party for National Development (UPND), the largest oppositionparty in parliament. In addition to boosting his weak support base, this was themain aim of the president, opposition party members being more interested inthe privileges conferred by office than in ideological principles. This means thatthe opposition parties have failed to offer a credible challenge to the MMD,both over the controversial budget and in recent by-elections (December 2003,The political scene). Even when they agree to oppose certain excesses of theruling party, they struggle to choose a leader for their various alliances,rendering their attempts to work together irrelevant. For example, in Januarythe UPND vowed that it would no longer enter into any agreements with theForum for Democracy and Development (FDD; although certain members ofthe FDD have been co-operating with the UPND in parliament) after a deal tosplit the positions of mayor and deputy mayor of Lusaka collapsed at the lastminute owing to an FDD candidate challenging the UPND candidate at thedeputy mayoral elections (the arrangement was for the FDD to retain theposition of mayor and leave the position of deputy mayor to the UPND). If theopposition cannot agree on small issues such as this, the prospects for greaterco-ordination are slim.

The UPND remains the strongest threat to Mr Mwanawasa's rule, despite thelong absence of its leader, Anderson Mazoka, who has spent most of the lastsix months in a South African hospital with suspected malaria. In spite oflosing three members of parliament (MPs) to the MMD in 2003, the UPND hasregrouped and is co-operating with some MPs from the United NationalIndependence Party (UNIP) and the FDD in the National Assembly. On

The UPND still poses a threatto the MMD

Opposition parties struggle asleading figures are co-opted

16 Zambia

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

February 20th the UPND legislators forced a vote to remove an allocation forby-elections from the budget, arguing that this encouraged the MMD to poachmore legislators from the opposition—a by-election is triggered whenever anMP changes parties. Although the MMD's parliamentary majority meant that itwon the vote, this rare example of opposition co-operation should enhance theprospects for greater parliamentary scrutiny of government policy.

Leadership problems within UNIP have caused the proposed merger with theMMD to collapse (June 2003, The political scene). Two key party officials, bothsons of the former president, Kenneth Kaunda, publicly differed on the merger.The elder of Mr Kaunda's sons, Panji, said in January that the merger was notfeasible, contrary to earlier statements by his younger brother, Tilyenji, the partypresident. The differences hinge mainly over the property that UNIP owns. Keyfigures in the party's central committee want to preserve the companies andbuildings that UNIP owns countrywide, as the revenue from these enable theparty to pay a salary to its central committee members (the only political partyin Zambia that does this). Although a formal merger now appears to be off theagenda, UNIP will continue to co-operate closely with the MMD in parliament.

The leadership of the Zambia Republican Party (ZRP) is also split on whether towork with the MMD, and has recently become embroiled in financial scandals.The party president, Benjamin Mwila, was expelled in December 2003 overallegations that he had misappropriated some cash donations to the party.Mr Mwila has complained that his expulsion was illegal, but the partychairman, Ben Kapita, disputes this. The ZRP has been disintegrating ever sinceMr Mwanawasa appointed its only MP, Silvia Masebo, as minister of localgovernment and housing in February 2003 (June 2003, The political scene).

The Heritage Party and the FDD have both lost key members to the MMD andare struggling to survive. The Heritage Party president, Godfrey Miyanda, isseeking a court declaration that the appointment of Nedson Nzowa and RonaldBanda as deputy ministers in Mr Mwanawasa's government is illegal. This isunlikely to be granted and will leave the party in disarray, as most of itsnational executive committee have either resigned from the party to join theMMD or have taken a back seat in politics in order to concentrate on theirpersonal businesses. Nonetheless, Mr Miyanda remains a credible figure, as oneof the few former MMD officials (he was once vice-president) whose image hasnot been tainted by allegations of corruption.

The FDD has also lost key members of its national executive committee to theMMD, and is struggling as a result of a ZK2bn (US$340,000) debt that itincurred in the run-up to the 2001 elections for campaigning and mobilisingsupporters and for other logistics. The debt has caused several key officials toleave the party so that they can no longer be answerable to creditors (except fordebts that they personally obtained) and weakened the party to the extent thatit can no longer participate in by-elections effectively. This makes it likely thatmost of the remaining senior party members will defect to the ruling party.

The anti-corruption task force arrested and charged the former intelligencechief, Xavier Chungu, and other senior Chiluba-era officials with vehicle theft—

UNIP and ZRP are dividedover working with the MMD

Smaller opposition parties arestruggling

Collective opposition parties'failures

Mwanawasa chosen soleMMD candidate

Chiluba's men face morecorruption chargesCivil society demandconstituent assembly

Senior Chiluba-era officials arearrested

Zambia 17

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

a non-bailable offence—in February. Mr Chungu, his former deputy, Yotam Zulu,the former secretary to the Treasury, Benjamin Mweene, and the formerpermanent secretary to the Ministry of Finance, Stella Chibanda, were chargedwith the theft of four tractors. The quartet are likely to be acquitted, as theyused state funds to buy the tractors; under Zambian law, theft of vehicles meanseither altering documents in order to change ownership or physically stealingthem, neither of which was the case in this instance. Lawyers for the accusedsee the charge as an attempt to keep their clients in jail, particularly afterMr Chungu's recent reported meeting with the former DPP. Both Mr Chunguand Mrs Chibanda are facing charges in Mr Chiluba's corruption trials.

Mr Mwanawasa backed calls by many Zambians to abolish capital punishmenton February 27th, when he quashed death sentences for 44 soldiers who wereconvicted of treason in 1999 (November 1999, The political scene). This wasafter the renegade soldiers occupied the state broadcaster and attempted tooverthrow the government of Mr Chiluba, which they accused of corruptionand incompetence, in 1997 (November 1997, The political scene). The soldiers,who lost a Supreme Court appeal last year, pleaded for clemency from thepresident, who is authorised to pardon offenders under Zambian law. (Origin-ally, 59 soldiers were convicted, but ten were discharged after the SupremeCourt appeal and five died in prison.) Several human rights groups have usedthe soldiers' case to lobby for the abolition of the death penalty, a position forwhich the president voiced his support (although he admits that the cabinet isdivided on the subject). There are currently over 200 prisoners on death rowbut there has been no execution in the past 13 years. A final decision to abolishthe death penalty awaits the recommendations of the Constitutional ReviewCommission (CRC). Submissions to the CRC so far suggest that, like the cabinet,Zambians are divided over whether the death penalty should be abolished.

Economic policy

The finance and national planning minister, Ng'andu Magande, presented the2004 budget on February 6th. Entitled Austerity for Posterity, the budget high-lighted yet again how vital it was to restore fiscal discipline. As the president,Levy Mwanawasa, and numerous other ministers have stated, fiscal policy hasto be back on track in order for the IMF to agree to a new poverty reductionand growth facility (PRGF). Without a PRGF, the government will be unable toachieve its goal of reaching completion point under the IMF and World Bank'sheavily indebted poor countries (HIPC) debt-relief initiative (entitling it to adebt write-off on external debt of around US$3.8bn) by end-2004.

The budget deficit is projected to fall from 5.1% of GDP in 2003 to 2% of GDP. Inthe budget presentation the deficit is defined as the level of domestic financing.This therefore assumes that foreign financing will be at budgeted level, which ishighly unlikely given the uncertainty and delay associated with donor inflows.Such a position is normal for African countries and is no great cause forconcern, as most of this money is for project financing; if it does not arrive thenthe projects are not implemented and there is only a limited effect on thedeficit. The way that the budget is presented means that it is difficult to make

Workers strike over wages,taxes

New DPP appointed in anti-graft fallout

The president wants the deathpenalty abolished

Government aims to reduce2004 deficit to 2% of GDP

18 Zambia

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

comparisons with the 2003 outturn (presentation of the detailed projections inthe "yellow book" that accompanies the budget has been changed to the extentthat comparisons with the previous year are not published). Nonetheless, aswith the 2003 outturn, the Economist Intelligence Unit believes that domesticrevenue will be broadly in line with the government's targets (although somerevenue from consumption taxes may fall short of the target owing to thegreater tax squeeze on the formal sector). The government's success in reducingthe fiscal deficit will again depend on its ability to contain expenditure.

Total expenditure is projected at ZK8.33trn (US$1.65bn), ZK5.29trn of which isdomestically funded, which implies a cut in government expenditure in realterms. Usually, a greater proportion of expenditure is externally funded, but thegovernment is being cautious this year, as some donors are withholdingbudgetary support pending the announcement of a new PRGF. Public-sectorpay has been frozen (apart from for the police, immigration and prison service,who did not receive a rise last year) in order for the government to keep wageand salary payments at the level of 8.1% of GDP agreed with the IMF. The civilservice wage bill remains by far the largest area of government expenditure,accounting for 43% of domestically generated revenue, at ZK2.05trn. As thegovernment has placed so much emphasis on not exceeding this target, sincethis would jeopardise a new PRGF, we think it is likely to stick broadly to itsspending plans in this area. The second largest item of government expenditureis debt servicing—domestic debt servicing is up by 65% on the 2003 total, toZK927bn (US$194m), owing to an increase in debt issued that year to cover thedeficit in the absence of donor support. There is scope for savings here, giventhat real interest rates on government Treasury bills have fallen to near zero,which is likely to be well below the level that the government budgeted for, butthe government has increased the issuance of longer maturities—of one to twoyears—for which yields are higher. It will be difficult for the government to holddown recurrent departmental charges, which are projected to fall by ZK24bn in2004. The government hopes that this will be possible through the adoption ofactivity-based budgeting, which links budgetary allocations to service deliveryand outputs, but teething problems are likely with this owing to capacityproblems in the civil service.

Wages costs are held, but debt-servicing spending is up

Zambia 19

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

The main revenue-raising measures in the budget focus on increasing the taxtake from those already in the formal sector, particularly high-income earners,rather than attempting to broaden the tax base to the growing informal sector.Two new income tax bands have been introduced—at 35% and 40%; previouslythe top rate was 30%—which the government is estimating will raise an extraZK23.8bn. Combined with the public-sector pay freeze, this move was heavilycriticised by unions and the opposition parties, and the government was forcedto send ministers around the country to explain that it only affected a verysmall proportion of the workforce. In fact, workers earning below ZK1.58m permonth will pay less under the new fiscal measures, as an increase in theincome tax threshold from ZK160,000 per month to ZK260,000 per month wasincluded in the budget (although this rise makes up for a lack of previousinflationary increments).

Income tax bandsIncome per annum Tax rate (%)First ZK3.12m 0

Next ZK8.64m 30Next ZK48.24m 35Above ZK60m 40

Source: Ministry of Finance and National Planning.

The only real attempt to broaden the tax base was the introduction of a 3%presumptive tax on businesses with a turnover of ZK200m or less. Previously,preparing the necessary accounts for tax purposes was a burden for smallbusinesses (through the cost of hiring accountants, for example) and manyavoided this by not sending in tax returns. The government is hoping that thesimpler tax procedures will encourage greater compliance and estimates thatthis will raise ZK7.3bn. These businesses will not pay corporation tax. In orderto smooth the introduction of the presumptive tax, the threshold on value-added tax (VAT) registration has also been raised, to ZK200m, although theremoval of voluntary registration for VAT is expected to result in a revenue gainof ZK26.3bn. A reduction in the number of goods that are zero-rated for VATpurposes is projected to raise an estimated ZK95.3bn (it is not clear from thebudget speech exactly which goods this applies to).

Other tax measures include:

• an increase in the portion of bank deposits exempt from withholding taxfrom ZK300,000 to ZK750,000 per annum (revenue loss of ZK1.5bn);

• a reduction in customs duty on computers from 15% to 5% (revenue loss ofZK800m);

• the introduction of excise duty on mobile-phone airtime at a rate of 10%(revenue gain of ZK15.6bn); and

• an increase of excise duty on cars from 10% to 20% (revenue gain ofZK8.4bn).

High earners are squeezedfurther

20 Zambia

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Complaints by public-sector unions, opposition parties and civil society groupsover the public-sector pay freeze and the increase in the top rate of tax wereheightened by the apparent lack of any sacrifices made by senior governmentofficials in the budget. This situation was compounded by the opaqueness ofthe yellow book and the knowledge that the promised ministerial pay cut in2003 was not implemented, as the necessary legislation was not passed byparliament. In response to this, Mr Mwanawasa cut his travel budget fromZK30bn to ZK18bn, while disputing that by travelling abroad regularly,accompanied by huge delegations, he was wasting public money. The presidentalso directed ministers to reduce their foreign travel and banned governmentbureaucrats from receiving attendance allowances for meetings. On February24th Mr Magande announced in parliament that the government had bannedofficial government parties in 2004, apart from independence day celebrationson October 24th, in a bid to save ZK6bn. The government usually throws bigparties for diplomats and a few Zambians on public holidays such as LabourDay and African Freedom Day. The cutbacks in expenditure are an indicationthat the government is beginning to listen to persistent criticism that leaderswere living lavishly while ordinary Zambians were being asked to makesacrifices. They are also a way of trying to pacify vocal civil society groups andpublic-service workers to some extent so that they can support thegovernment's bid to reach HIPC completion point in December 2004.

Data on fiscal performance in 2003 presented with the 2004 budget show thatthe deficit was 5.1% of GDP, compared with a target of 1.55% of GDP. Detaileddata are only available on domestically generated revenue and domesticallyfinanced expenditure, but clearly show that the cause of the fiscal overrun wasdomestically financed expenditure, at ZK4.73trn, exceeding its target by 18.9%.There were four main factors behind this. First, the increase in wages for civilservants announced in April 2003 (June 2003, Economic policy), which causedtotal wage and salary payments to exceed their target by ZK208bn and resultedin the suspension of IMF and other donor assistance. As some donor funds thatwould have been used to repay external debt were included in this suspension,which also required the government to step up domestic financing of thedeficit, the second source of expenditure overshoot was debt servicing, which

Public-sector pay deal causesdeficit to exceed target in 2003

Government cuts expenditureafter union hostility

Zambia 21

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

exceeded its target by ZK342bn. Of more concern is the ZK188bn overrun in thebudget for recurrent departmental charges. According to the Ministry of Financeand National Planning, this was mainly because of increased expenditure inthe cabinet office and on the military and security wings of government. Therationale for an extra-budgetary increase in military and security spending isunclear, given that the solidification of peace in Angola has removed the mainexternal threat. Instead, it is likely that the tight standard of disclosure in theseareas is being abused and much of the additional funds are being used forpatronage or rent-seeking purposes. Abuse of funds can also be captured underthe final main category of overexpenditure, other current expenditure. TheZK176bn overspend here was attributed to the repayment of redundancypayments to workers from the Ramcoz mine (these needed to be cleared as partof the deal under which J&W Investments of Switzerland bought the mine) anda higher allocation to the Zambia Revenue Authority.

Budget performance in 2003(ZK m unless otherwise indicated)

Budgeted Actual Variance Variance (%)Total domestic revenue 3,676,955 3,679,450 2,495 0.1 Tax revenue 3,445,709 3,546,568 100,859 2.9 Income tax 1,472,143 1,610,774 138,631 9.4 Corporation tax 327,577 245,580 -81,997 -25.0 Personal income tax 1,137,529 1,365,194 227,665 20.0 Extraction royalty 7,037 9,992 2,955 42.0 Domestic goods & services 936,073 872,083 -63,990 -6.8 Trade taxes 1,037,493 1,053,719 16,226 1.6 Non-tax revenuea 231,246 132,882 -98,364 -42.5Total domestically financed

expenditure 3,974,608 4,726,733 752,125 18.9 Current expenditure 3,570,958 4,314,354 743,396 20.8 Wages and salaries 1,520,000 1,728,258 208,258 13.7 Public service retrenchment

programme 63,500 10,000 -53,500 -84.3 Recurrent departmental charges 465,158 652,685 187,527 40.3 Transfers & pensions 471,450 361,987 -109,463 -23.2 Debt servicingb 763,850 1,105,407 341,557 44.7 Other current expenditurec 299,000 474,632 175,632 58.7 Capital expenditure 516,100 412,380 -103,720 -20.1Balance -297,653 -1,047,283 -749,630 251.8

a Includes miscellaneous revenue and exceptional revenue. b Domestic and foreign debt. c Includescontingency and constitutional expenditure.

Source: Ministry of Finance and National Planning

Domestically generated revenue exceeded its ZK3.68trn target by ZK2.6bn,owing to tax revenue being 2.9% above target, at ZK3.55trn. Rather thansignalling a pick-up in economic activity or improved performance by the taxauthorities, this was the result of higher-than-budgeted personal income taxrevenue resulting from the civil service pay award in April. Trade taxes wereslightly above target, as increased trade and compliance with the tax authoritieslifted VAT payments on imports. Import tariffs were 9.4% below target becauseof importers switching from goods sourced from South Africa to those from theCommon Market for Eastern and Southern Africa (Comesa), as these are not

Higher wages lift income taxrevenue

22 Zambia

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

subject to import duty under the regional free-trade deal (January 2001, Foreigntrade and payments). Non-tax revenue, excluding miscellaneous revenue andexceptional revenue, was 12.5% below target, owing mainly to poor recovery offunds lent to smallholder farmers to buy the necessary inputs for their crops.Domestic financing of the fiscal deficit caused the domestic debt stock toincrease to ZK6.3trn, from ZK4.9trn.

Commercial banks have responded to the cut in statutory reserve ratios from17.5% to 14% on both kwacha and foreign-currency deposits implemented by theBank of Zambia (BoZ, the central bank) in October (December 2003, Economicpolicy) by reducing lending rates. This was the rationale for the move as, bygenerating additional liquidity—estimated at ZK62bn in local currency andUS$11.5m in foreign-currency deposits—banks would be forced to look foralternative uses for these funds. With commercial bank lending rates previouslytoo high for borrowing to be viable, at 38.2% (17.1% in real terms) in October,banks responded by cutting lending rates by up to 10 percentage points.However, data released by the Treasury in February showed that 81% of thefunds freed by the reduction in reserve ratios were invested in governmentT-bills and bonds, despite T-bill yields halving from late November andcurrently being very close to zero in real terms. The fall in T-bill yields is goodnews for the government, as it will significantly reduce debt-servicing costs, butthe continued purchase of government debt is a reflection that commercialbanks remain strongly averse to lending to the private sector.

In an effort to encourage commercial bank lending to local businesses andentrepreneurs, the BoZ announced in February that it would spearhead theformation of a credit reference bureau (CRB) in 2004. The CRB will act as anadvisory body to commercial banks in a bid to build up a credit history ofpotential borrowers in order to exclude those with a track record of nothonouring their debts. Commercial banks will be provided with informationon all borrowers so that only creditworthy businesses are able to access loans.This is aimed at creating confidence in the money market, as a legacy of baddebts means that commercial banks are hesitant to lend money to any but es-tablished clients, and prefer to invest in less risky T-bills and government bonds.

Although it is unlikely that real T-bill yields will remain so low over a longperiod, the fall in yields and the stagnant deposit base mean that commercialbanks are venturing into other fields. Recently, banks have been developingcommunity banking operations. These aim to increase the proportion of thepopulation with access to a bank by offering basic financial services, such assavings accounts with a very low minimum deposit (but no lending). Com-munity banks have been created in most Lusaka townships and branches arenow being established in rural areas. New Capital Bank, which merged withCavmont Merchant Bank in December, and the National Savings and CreditBank have taken a lead in this area—the state-owned Zambia NationalCommercial Bank has the largest branch network but its finances are too weakto exploit this development.

Commercial banks start tooffer services to townships

A reduction in reserve ratios isonly partly effective

Zambia 23

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

The domestic economy

Economic trends

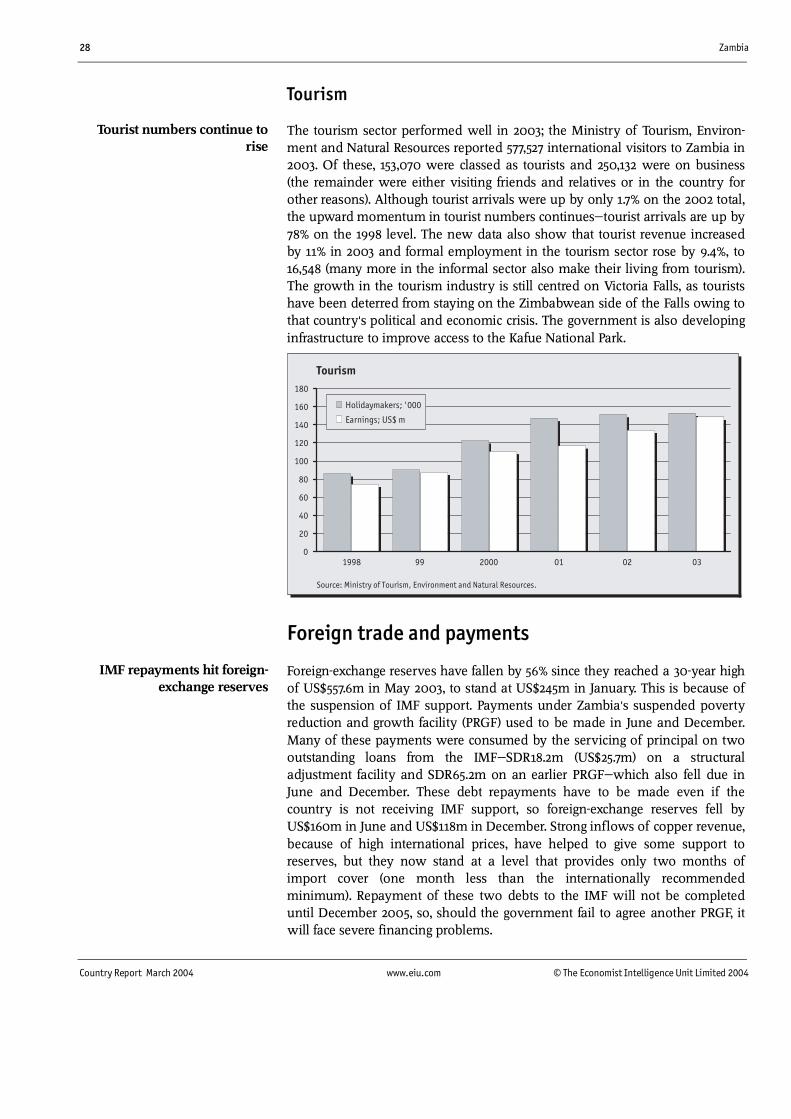

According to provisional government estimates, real GDP grew by 4.3% in 2003,owing to strong growth in the agricultural, manufacturing and constructionsectors. The agricultural sector rebounded after two consecutive years of con-traction, because of favourable weather conditions that caused a doubling ofthe maize harvest. This had a direct impact on manufacturing growth, as foodprocessing is the largest component of the manufacturing sector. Double-digitgrowth was recorded in the construction sector for the third consecutive year.Donor-funded road construction programmes and government housing projectscontinue to be the main sources of growth in this sector. Growth in the miningsector slowed sharply, following strong growth in 2001 and 2002 related todevelopment and rehabilitation work on the Konkola and Nchanga minescarried out by Anglo American, a mining conglomerate. A 3.7% increase incopper production, owing to higher output by Konkola Copper Mines, was themain reason for the 3.3% growth in the mining sector. Tertiary sector growthrose to 4.2%, mainly because of a jump in growth in the transport, storage andcommunications sector, particularly the latter, caused by the entrance of a newmobile-phone provider, which sharply increased usage and caused the otheroperators to drop their charges by around 25%. The restaurants, bars and hotelssector, a proxy for the tourism industry, continued to perform strongly—touristrevenue increased by 11% in 2003.

Real growth by sector(%)

2000 2001 2002 2003a

Agriculture, fishing & forestry 1.6 -2.6 -1.7 5.0Mining & quarrying 0.1 14.0 16.4 3.3Primary sector 1.1 1.9 3.8 4.5Manufacturing 3.6 4.2 5.7 6.3Electricity, gas & water 1.2 12.6 -5.2 0.6

Construction 6.5 11.5 17.4 13.9Secondary sector 4.0 7.5 7.2 7.8Wholesale & retail trade 2.3 5.4 5.0 4.9

Restaurants, bars & hotels 12.3 24.4 4.9 5.9Transport, storage & communications 2.4 2.8 1.8 5.1

Financial institutions & insurance -0.6 0.1 3.5 3.5Real estate & business services 17.0 3.5 4.4 4.0

Community, social & personal services -0.5 5.8 1.6 2.4Tertiary sector 4.1 4.7 3.8 4.2Less FISIMb 2.5 2.5 2.5 2.5

Taxes on products 5.2 7.0 -6.8 -3.0GDP growth 3.6 4.9 3.3 4.3

a Provisional. b Financial intermediation services indirectly measured.

Source: Central Statistical Office.

Year-on-year inflation fell from 17.4% in January to 16.8% in February, the lowestrate since February 1998. This was mainly on account of a continued easing in

Real GDP growth is estimatedat 4.3% in 2003

Year-on year inflationcontinues to fall

24 Zambia

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

food price inflation, owing to much improved food availability compared withthe same period of last year, when maize supplies had run out in some areas asa result of the region-wide famine. There is little scope for year-on-year foodprice inflation to slow much further, as the food supply situation improvedsignificantly in March 2003 with the availability of the first of the year'sbumper crop. Although slightly below average, the current rains are sufficientfor good crop development, so food supply problems are not expected in 2004.

The relative stability of the kwacha against the US dollar has continued, apartfrom a brief period in late December when the currency gained around 10%against the dollar before falling back to the ZK4,700-4,850:US$1 range, where ithas been trading since the opening of the broad-based dealing window onJuly 23rd (September 2003, Economic policy). The dealing window, whichobliges commercial banks to offer two-way price quotes, is the main reason forthe recent stability and has increased the business community's confidence inthe new foreign-exchange regime. The blip in December occurred becausedemand for foreign exchange is strong around the turn of the year, ascorporates need to meet their end-year obligations, and many had beenbuilding up foreign exchange holdings in anticipation of this. As exportproceeds continued to provide foreign exchange, but corporates had alreadycovered their year-end requirements, the glut of foreign exchange on the marketcaused the kwacha to appreciate to a high of ZK4,300:US$1. This rateencouraged banks to come into the market to buy foreign exchange, returningthe kwacha to its trading range of the previous few months by the end ofDecember. Although the kwacha has come under pressure so far in 2004 owingto the return to the market of importers and corporate firms for dividendpayments, it has been supported by the good performance of agriculture,which reduced the need for maize imports, and high copper prices.

Mining

Rising international copper prices have made it doubtful whether KonkolaCopper Mines (KCM, the country's largest producer) will be sold to SterliteIndustries of India in mid-2004. The deal with Sterlite was first announced in

The kwacha remains relativelystable

Doubts are raised over the saleof KCM to Sterlite

Zambia 25

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

May (June 2003, The domestic economy: Mining and energy), but has run intodifficulties in recent months over the tax and other concessions demanded bySterlite and the jump in copper prices to an eight-year high. Sterlite isapparently looking for a package of incentives similar to those awarded toAnglo American after it bought the mines in 1999 (November 1999, Thedomestic economy: Mining). As Anglo American invested huge sums torehabilitate the mines before its exit in 2002, the government is unwilling togrant the same concessions to Sterlite. In fact, KCM is profitable while thecopper price is around its current level—on February 17th it said that it couldfund its operations from internal revenue and that it had a capital budget ofUS$75m for 2004, which would also be funded internally. The company isprojecting that copper production will increase to 225,000 tonnes in 2004, from188,000 tonnes last year, as a result of the start of copper production fromrefractory ores at its Nchanga open pit mine and an improvement in theefficiency of mining at Konkola mine. While copper prices remain at aroundcurrent levels—which the Economist Intelligence Unit thinks will be the caseuntil at least mid-2006—the only incentive for KCM to accept an approach by astrategic partner would be in order to develop the Konkola Deep mine, whichrequires investment estimated at around US$1bn (this cost was the main reasonfor Anglo American's withdrawal).

Canada's First Quantum Minerals announced on February 11th that it hadsecured a US$224m financing package for the Kansanshi copper and gold minein north-west Zambia. Construction began in September 2003, and by mid-February around 25% of the work had been completed. Production is expectedto begin in early 2005 and will peak at around 130,000 tonnes of copper and35,000 troy oz of gold per year. First Quantum Minerals has already employedseveral Zambians at the mine, after the government in January gave it a 25-yearcopper- and cobalt-mining licence, with an option to renew this for another25 years. Meanwhile, Mopani Copper Mines, the country's second largestcopper producer, which operates the Mufulira and Nkana mines, is planning toincrease production from 134,000 tonnes in 2003 to 160,000 tonnes in 2004, asa result of rehabilitation work at its mines.

First Quantum secures financepackage for Kansanshi

26 Zambia

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

Infrastructure

Two of Zambia's three mobile-phone service providers announced majorexpansion programmes for improving communications services. The privatelyowned Celtel-Zambia said that it would spend US$50m with the aim ofexpanding its cellular network across Zambia. Celtel also intends to partnerCeltel-Malawi, Celtel-Congo and Celtel-Tanzania to form a pan-Africantelephone network that will improve communications in these countries. It hasalso applied for an international gateway licence, an area currently under themonopoly of the state telecommunications firm, Zamtel. Zamtel, which startedproviding a Global System for Mobile Communications (GSM) cellular servicein 2003, says that it has so far spent US$40m on new infrastructure to developmobile-phone services. Several remote parts of Zambia, which were completelycut off from the rest of the country, now have telephone services.

Telecoms providers, 2003Company Service SubscribersZamtel PSTN a 84,956

Zamtel/Cell Z Mobile 55,000Telecel Mobile 45,151

Celtel Mobile 91,138Zamnet Internet 3,529

Zamtel Internet 3,983Coppernet Internet 3,913Microlink Internet 329

Uunet Internet 221

a Public switched telephone network, in effect a fixed-line system.

Source: Ministry of Communications and Transport.

Financial services

A South African retail bank, Amalgamated Bank of South Africa (ABSA), hasbeen picked as the preferred bidder for the state-owned Zambia NationalCommercial Bank (Zanaco). ABSA was selected ahead of the AfricaInternational Financial Holdings (Zambia) consortium, which consists of theInternational Finance Corporation, the European Investment Bank, theNetherlands Development Finance Organisation and the National Bank ofMalawi (June 2003, Economic policy). The privatisation of Zanaco is one of thekey conditions for the agreement of a new PRGF with the IMF. The permanentsecretary in the Ministry of Commerce, Trade and Industry, DavidsonChilipamushi, said in February that the government aimed to concludenegotiations with ABSA in June. ABSA is negotiating for a 49% stake (togetherwith management rights), but would be eligible to purchase more shares whenthe government offloads its shares on the Lusaka Stock Exchange (LuSE). (Afterthe sale, the government will retain a 25% stake, 25.8% will be held in trust bythe Zambia Privatisation Agency for sale to Zambians and existing minorityshareholders are to retain a 0.2% stake.)

Zimbabwe farmers settle inZambia

Mobile-phone operatorsexpand their services

A South African bank is pickedto buy Zanaco

Zambia 27

Country Report March 2004 www.eiu.com © The Economist Intelligence Unit Limited 2004

The managing director of the Zambia State Insurance Corporation (ZSIC), IreneMuyenga, said on February 5th that the company was looking for a strategicequity partner to build its capital base. Local and international firms would beeligible to bid for a 30% stake in the firm, which is valued at US$55m. ZSIC hadbeen removed from the list of state firms to be privatised and the president,Levy Mwanawasa, who does not favour the privatisation policy, restated thisposition last year. The change of heart is a clear indication that the firm needs afresh capital injection in order to survive increased competition from smaller,but viable, insurance firms. Although management of the life and pensionsoperations has been contracted out, debts to ZSIC's general insurance businesscover more than one year's income. Given this precarious financial position,there is likely to be little foreign interest in the firm.