Yum Cha 飲 茶 - 中國銀河國際金融控股有限公司 Yum Cha 飲 茶 May 11, 2016 Source:...

12

Yum Cha 飲 茶 May 11, 2016 Source: Bloomberg INDICES Closing DoD% Hang Seng Index 20,242.7 0.4 HSCEI 8,486.2 0.4 Shanghai COMP 2,832.6 0.02 Shenzhen COMP 1,802.3 (0.1) Gold 1,265.8 0.2 BDIY 594.0 (3.6) Crude Oil, WTI(US$/BBL) 44.7 2.8 Crude Oil, BRENT(US$/BBL) 45.5 4.3 HIBOR, 3-M 0.5 0.3 SHIBOR, 3-M 2.9 - RMB/USD 6.5 0.1 TALKING POINT: CSRC to Restrict Local Backdoor Listings Last Friday, the China Securities Regulatory Commission (CSRC) said it is studying the impact of the delisting of some overseas-listed Chinese companies and their possible return to the A-share market. According to news flow, the CSRC is considering possible restrictions on reverse mergers and backdoor listings, such as: a) a cap on valuation mul- tiples for deals involving companies that previously traded overseas, and b) a quota on the number of reverse mergers each year. The restrictions are to avoid: a) instability trig- gered by overly high valuations for the companies involved, and b) capital flows which put pressure on the RMB. The CSRC has held talks with investment banks and other market participants to gauge their views on the potential curbs. Shares of US-traded Chinese companies such as YY Inc., Momo Inc. and Qihoo 360, which have already announced privation plans, are under heavy selling pressure. As discussed earlier, some proposed privatizations in Hong Kong, such as Wanda Commercial [3699.HK], may face much high- er policy risks. There has been speculation that Evergrande Real Estate Group Ltd. [3333.HK] may return to A-share market through a back-door listing; this is now less cer- tain. DATA RELEASES DUE THIS WEEK May 07/12 Foreign Direct Investment YoY CNY Analyst: Mark Po, CFA Huaneng Renewables Corporation [0958.HK; HK$3.80;BUY] - HNR’s total power generation in April jumped 32.4% YoY to 2,044GWh, with wind power generation surging 32.6% YoY to 1,954GWh and solar power generation increasing 29.1% YoY to 90GWh. We estimate wind utilization increased ~2.6% YoY in April, which was much better than the 11% decline reported by China Longyuan [0916 HK; BUY]. We continue to like HNR because of its fast-growing power generation on the back of its strong execution, better-than-peers regional mix and lower grid-curtailment rate. HNR is trading at below 9x 2016E PER, which we believe has yet to reflect the fast earnings growth. Reiterate BUY with a DCF-based TP of HK$3.80 (unchanged). Daqo New Energy [DQ.US; US$25.06; Not rated] – Q1 2016 results in line with expectations; Positive management guidance for Q2 2016 RESEARCH NOTES

Transcript of Yum Cha 飲 茶 - 中國銀河國際金融控股有限公司 Yum Cha 飲 茶 May 11, 2016 Source:...

1

Yum Cha 飲 茶 May 11, 2016

Source: Bloomberg

INDICES Closing DoD%

Hang Seng Index 20,242.7 0.4

HSCEI 8,486.2 0.4

Shanghai COMP 2,832.6 0.02

Shenzhen COMP 1,802.3 (0.1)

Gold 1,265.8 0.2

BDIY 594.0 (3.6)

Crude Oil, WTI(US$/BBL) 44.7 2.8

Crude Oil, BRENT(US$/BBL) 45.5 4.3

HIBOR, 3-M 0.5 0.3

SHIBOR, 3-M 2.9 -

RMB/USD 6.5 0.1

TALKING POINT: CSRC to Restrict Local Backdoor Listings

Last Friday, the China Securities Regulatory Commission (CSRC) said it is studying the

impact of the delisting of some overseas-listed Chinese companies and their possible

return to the A-share market. According to news flow, the CSRC is considering possible

restrictions on reverse mergers and backdoor listings, such as: a) a cap on valuation mul-

tiples for deals involving companies that previously traded overseas, and b) a quota on

the number of reverse mergers each year. The restrictions are to avoid: a) instability trig-

gered by overly high valuations for the companies involved, and b) capital flows which put

pressure on the RMB. The CSRC has held talks with investment banks and other market

participants to gauge their views on the potential curbs. Shares of US-traded Chinese

companies such as YY Inc., Momo Inc. and Qihoo 360, which have already announced

privation plans, are under heavy selling pressure. As discussed earlier, some proposed

privatizations in Hong Kong, such as Wanda Commercial [3699.HK], may face much high-

er policy risks. There has been speculation that Evergrande Real Estate Group Ltd.

[3333.HK] may return to A-share market through a back-door listing; this is now less cer-

tain.

DATA RELEASES DUE THIS WEEK

May 07/12 Foreign Direct Investment YoY CNY

Analyst: Mark Po, CFA

Huaneng Renewables Corporation [0958.HK; HK$3.80;BUY] - HNR’s total power

generation in April jumped 32.4% YoY to 2,044GWh, with wind power generation

surging 32.6% YoY to 1,954GWh and solar power generation increasing 29.1% YoY

to 90GWh. We estimate wind utilization increased ~2.6% YoY in April, which was

much better than the 11% decline reported by China Longyuan [0916 HK; BUY]. We

continue to like HNR because of its fast-growing power generation on the back of its

strong execution, better-than-peers regional mix and lower grid-curtailment rate.

HNR is trading at below 9x 2016E PER, which we believe has yet to reflect the fast

earnings growth. Reiterate BUY with a DCF-based TP of HK$3.80 (unchanged).

Daqo New Energy [DQ.US; US$25.06; Not rated] – Q1 2016 results in line with expectations; Positive management guidance for Q2 2016

RESEARCH NOTES

2

Huaneng Renewables Corporation [0958.HK]

HNR’s total power generation in April jumped 32.4% YoY to 2,044GWh, with wind

power generation surging 32.6% YoY to 1,954GWh and solar power generation in-

creasing 29.1% YoY to 90GWh. We estimate wind utilization increased ~2.6% YoY in

April, which was much better than the 11% decline reported by China Longyuan

[0916 HK; BUY]. We continue to like HNR because of its fast-growing power genera-

tion on the back of its strong execution, better-than-peers regional mix and lower grid-

curtailment rate. HNR is trading at below 9x 2016E PER, which we believe has yet to

reflect the fast earnings growth. Reiterate BUY with a DCF-based TP of HK$3.80

(unchanged).

Strong performance in April. HNR’s wind-utilization hours growth (+2.6% YoY)

was consistent with the 2.9% increase in average wind speed in China based on

our check. While we estimate Inner Mongolia reported a 14% YoY decline in utili-

zation hours, this weakness was more than offset by the strong performance in

Liaoning, Yunnan and Shanxi. The wind power generation growth of 32.6% YoY

in April was an acceleration from the 20% reported in March.

Total power generation +30% YoY to 6,646GWh in 4M16. Of this, wind and

solar power generation increased 30% and 23% YoY, respectively. In 4M16, total

power generation accounted for 35.8% of our full-year estimate, compared to

34.9% of full-year output in 4M15.

Risks: (1) capacity ramp-up risk; (2) unexpected decline in wind speed; (3) high

gearing; (4) delay in power transmission line construction; (5) potential fund-

raising exercise.

Wayne Fung, CFA—Analyst

(852) 3698-6319

Wong Chi Man, CFA—Head of Research

(852) 3698-6317

Wind Power Sector Total power generation in April +32%, outpacing peers

BUY

(Unchanged)

Close: HK$2.24 (May 10, 2016)

Target Price: HK$3.80 (+70%)

Share Price Performance

Market Cap US$2,807m

Shares Outstanding 9,728m

Auditor KPMG

Free Float 43%

52W range HK$1.39-3.80

3M average daily T/O US$5.8m

Major Shareholding Huaneng Group

(56.9%)

May 11, 2016

Key Financials (RMB m) 2013 2014 2015 2016E 2017E

Revenue 5,798 6,151 7,357 9,209 10,876

Change (YoY) 44% 6% 20% 25% 18%

Other income 79 168 435 253 305

Adjusted EBIT 2,649 3,178 3,681 4,622 5,437

Change (YoY) 34% 20% 16% 26% 18%

Recurring net profit 971 1,041 1,499 2,082 2,474

Change (YoY) 114% 7% 44% 39% 19%

Recurring EPS 0.113 0.115 0.154 0.214 0.254

Change (YoY) 112% 2% 34% 39% 19%

PER (x) 15.8 15.7 12.3 8.9 7.5

Dividend yield 1.2% 1.2% 1.6% 2.3% 2.7%

PBR (x) 1.2 1.1 1.0 0.9 0.9

EV/EBITDA (x) 13.4 11.1 9.1 7.6 6.4

Net debt/equity 182% 215% 241% 250% 250%

ROE 7.6% 7.0% 8.8% 11.1% 12.0%

Source: Company, CGIS Research estimates

3

Figure 1: HNR monthly power generation

Sources: Company, CGIS Research

Power generation (GWh) Jan-15 Feb-15 Mar-15 Apr-15 Jan-16 Feb-16 Mar-16 Apr-16

Wind power

Inner Mongolia 193 167 288 346 323 297 373 414

Liaoning 126 65 213 265 140 89 234 331

Shandong 153 119 185 220 173 129 180 189

Yunnan 166 199 248 218 278 235 343 319

Shanxi 135 105 150 87 129 94 130 137

Hebei 53 36 80 71 62 34 73 87

Guizhou 69 81 103 104 124 68 121 118

Guangdong 61 48 64 55 86 88 86 74

Xinjiang 33 21 38 37 19 17 47 99

Shanghai 8 8 7 11 22 23 20 16

Jilin 9 7 22 25 14 11 19 50

Shaanxi 6 10 9 9 8 13 12 11

Sichuan 34 37 45 26 106 51 106 102

Zhejiang 0 0 0 0 4 5 5 7

Wind total 1,046 904 1,452 1,474 1,486 1,155 1,749 1,954

Solar power

Solar total 54 55 67 70 65 63 84 90

Total 1,100 959 1,519 1,544 1,551 1,218 1,833 2,044

(Change YoY) Jan-15 Feb-15 Mar-15 Apr-15 Jan-16 Feb-16 Mar-16 Apr-16

Wind power

Inner Mongolia - - - - 67% 77% 30% 20%

Liaoning - - - - 11% 38% 10% 25%

Shandong - - - - 13% 8% -2% -14%

Yunnan - - - - 67% 18% 38% 46%

Shanxi - - - - -4% -11% -13% 57%

Hebei - - - - 16% -7% -9% 22%

Guizhou - - - - 78% -16% 18% 13%

Guangdong - - - - 40% 84% 34% 35%

Xinjiang - - - - -43% -16% 21% 167%

Shanghai - - - - 165% 199% 208% 41%

Jilin - - - - 48% 51% -15% 102%

Shaanxi - - - - 39% 30% 29% 24%

Sichuan - - - - 216% 37% 136% 301%

Zhejiang - - - - n/a n/a n/a n/a

Wind average - - - - 42% 28% 20% 33%

Solar power

Solar average - - - - 20% 16% 26% 29%

Average - - - - 41% 27% 21% 32%

4

Figure 2: HNR quarterly power generation

Note: The solar power generation growth in 1Q15 would be 74.4% YoY if we included the contribution of Huaneng Ge’ermu in 1Q14 (Huaneng Ge’er-

mu was acquired by HNR in April 2014).

Sources: Company, CGIS Research

Power generation (GWh) 1Q14 2Q14 3Q14 4Q14 2014 1Q15 2Q15 3Q15 4Q15 2015 1Q16

Wind power

Inner Mongolia 539 744 572 942 2,796 648 1,025 586 875 3,134 992

Liaoning 398 533 340 786 2,057 403 706 370 696 2,175 464

Shandong 441 478 215 553 1,687 457 522 192 508 1,679 482

Yunnan 475 412 123 537 1,547 613 620 262 630 2,125 856

Shanxi 270 291 143 396 1,100 390 290 169 293 1,141 353

Hebei 124 140 73 167 503 170 192 82 143 587 169

Guizhou 178 143 182 173 676 253 295 195 306 1,049 313

Guangdong 143 104 53 177 477 173 167 102 263 705 260

Xinjiang 117 174 120 123 534 92 102 84 43 321 83

Shanghai 37 25 23 31 117 22 29 45 41 137 65

Jilin 20 29 20 35 104 39 58 33 52 181 44

Shaanxi 9 8 8 10 35 26 29 30 35 119 34

Sichuan 0 0 8 35 43 116 73 77 197 464 263

Zhejiang 0 0 0 0 0 0 3 16 15 34 14

Wind total 2,751 3,082 1,878 3,963 11,675 3,402 4,110 2,243 4,096 13,852 4,390

Solar power

Solar total 64 165 144 130 503 176 204 238 200 818 213

Total 2,816 3,247 2,022 4,093 12,178 3,578 4,314 2,481 4,296 14,669 4,602

(Change YoY) 1Q14 2Q14 3Q14 4Q14 2014 1Q15 2Q15 3Q15 4Q15 2015 1Q16

Wind power

Inner Mongolia -26% 4% -35% 22% -10% 20% 38% 2% -7% 12% 53%

Liaoning -26% -15% -14% 41% -3% 1% 32% 9% -11% 6% 15%

Shandong 9% -10% -16% 14% 0% 4% 9% -11% -8% 0% 6%

Yunnan 2% 41% 24% 100% 37% 29% 50% 114% 17% 37% 40%

Shanxi 6% 21% 22% 44% 24% 44% 0% 18% -26% 4% -9%

Hebei -5% -7% -13% 5% -4% 37% 37% 13% -14% 17% -1%

Guizhou -2% 5% 2% 79% 14% 42% 106% 7% 77% 55% 23%

Guangdong 18% -6% -33% 3% -1% 21% 60% 93% 49% 48% 50%

Xinjiang 76% 45% 7% 70% 44% -22% -41% -30% -65% -40% -10%

Shanghai 13% -17% -26% -9% -9% -39% 14% 94% 31% 18% 189%

Jilin -2% -9% -20% 11% -4% 89% 99% 70% 49% 75% 13%

Shaanxi 35% 0% 17% 62% 26% 187% 271% 270% 258% 246% 32%

Sichuan n/a n/a n/a n/a n/a n/a n/a 917% 456% 976% 127%

Zhejiang n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a

Wind average -7% 3% -17% 35% 5% 24% 33% 19% 3% 19% 29%

Solar

Solar average n/a n/a n/a 10755% 41845% 174% 24% 66% 54% 63% 21%

Average -5% 8% -11% 40% 9% 27% 33% 23% 5% 20% 29%

5

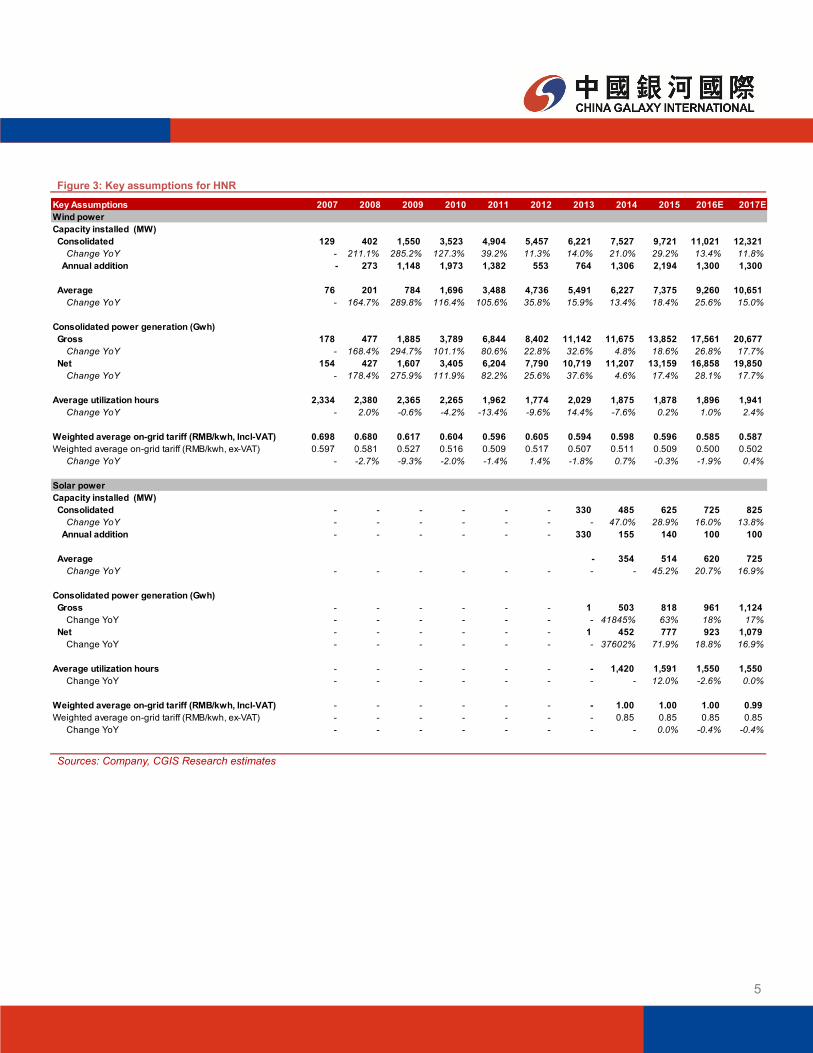

Figure 3: Key assumptions for HNR

Sources: Company, CGIS Research estimates

Key Assumptions 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E

Wind power

Capacity installed (MW)

Consolidated 129 402 1,550 3,523 4,904 5,457 6,221 7,527 9,721 11,021 12,321

Change YoY - 211.1% 285.2% 127.3% 39.2% 11.3% 14.0% 21.0% 29.2% 13.4% 11.8%

Annual addition - 273 1,148 1,973 1,382 553 764 1,306 2,194 1,300 1,300

Average 76 201 784 1,696 3,488 4,736 5,491 6,227 7,375 9,260 10,651

Change YoY - 164.7% 289.8% 116.4% 105.6% 35.8% 15.9% 13.4% 18.4% 25.6% 15.0%

Consolidated power generation (Gwh)

Gross 178 477 1,885 3,789 6,844 8,402 11,142 11,675 13,852 17,561 20,677

Change YoY - 168.4% 294.7% 101.1% 80.6% 22.8% 32.6% 4.8% 18.6% 26.8% 17.7%

Net 154 427 1,607 3,405 6,204 7,790 10,719 11,207 13,159 16,858 19,850

Change YoY - 178.4% 275.9% 111.9% 82.2% 25.6% 37.6% 4.6% 17.4% 28.1% 17.7%

Average utilization hours 2,334 2,380 2,365 2,265 1,962 1,774 2,029 1,875 1,878 1,896 1,941

Change YoY - 2.0% -0.6% -4.2% -13.4% -9.6% 14.4% -7.6% 0.2% 1.0% 2.4%

Weighted average on-grid tariff (RMB/kwh, Incl-VAT) 0.698 0.680 0.617 0.604 0.596 0.605 0.594 0.598 0.596 0.585 0.587

Weighted average on-grid tariff (RMB/kwh, ex-VAT) 0.597 0.581 0.527 0.516 0.509 0.517 0.507 0.511 0.509 0.500 0.502

Change YoY - -2.7% -9.3% -2.0% -1.4% 1.4% -1.8% 0.7% -0.3% -1.9% 0.4%

Solar power

Capacity installed (MW)

Consolidated - - - - - - 330 485 625 725 825

Change YoY - - - - - - - 47.0% 28.9% 16.0% 13.8%

Annual addition - - - - - - 330 155 140 100 100

Average - 354 514 620 725

Change YoY - - - - - - - - 45.2% 20.7% 16.9%

Consolidated power generation (Gwh)

Gross - - - - - - 1 503 818 961 1,124

Change YoY - - - - - - - 41845% 63% 18% 17%

Net - - - - - - 1 452 777 923 1,079

Change YoY - - - - - - - 37602% 71.9% 18.8% 16.9%

Average utilization hours - - - - - - - 1,420 1,591 1,550 1,550

Change YoY - - - - - - - - 12.0% -2.6% 0.0%

Weighted average on-grid tariff (RMB/kwh, Incl-VAT) - - - - - - - 1.00 1.00 1.00 0.99

Weighted average on-grid tariff (RMB/kwh, ex-VAT) - - - - - - - 0.85 0.85 0.85 0.85

Change YoY - - - - - - - - 0.0% -0.4% -0.4%

6

HNR Income Statement Projection

Note: Adjusted EBITDA and adjusted EBIT exclude "other net income"

Net interest coverage = EBITDA/net finance expenses

Sources: Company, CGIS Research estimates

Income Statement (RMB m) 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E

Revenue 570 918 1,769 3,196 4,027 5,798 6,151 7,357 9,209 10,876

Sales of electricity 248 847 1,759 3,160 4,025 5,440 6,114 7,354 9,209 10,876

Service concession construction revenue 318 67 0 0 0 355 33 0 0 0

Others 4 5 10 36 1 2 4 3 0 0

Other net income 36 85 250 683 190 79 168 435 253 305

Income from CDM projects 16 29 165 484 105 0 0 0 0 0

Government grants 19 37 83 109 84 78 115 182 198 250

Others 0 19 2 90 1 0 53 252 55 55

Operating expenses (367) (167) (250) (358) (432) (1,217) (703) (940) (1,216) (1,457)

Service concession construction costs (318) (67) 0 0 0 (355) (33) 0 0 0

Labour costs (26) (45) (79) (118) (151) (205) (260) (370) (460) (544)

Admin expenses (11) (20) (96) (118) (127) (146) (187) (189) (258) (315)

Repairs & maintenance (4) (15) (28) (30) (50) (91) (86) (109) (157) (196)

Others (8) (20) (47) (92) (104) (420) (136) (272) (341) (402)

EBITDA 239 836 1,768 3,521 3,784 4,659 5,616 6,851 8,247 9,724

Adjusted EBITDA 204 751 1,518 2,838 3,595 4,580 5,448 6,417 7,994 9,419

D&A (81) (297) (634) (1,169) (1,612) (1,931) (2,270) (2,735) (3,372) (3,982)

EBIT 158 540 1,134 2,351 2,172 2,728 3,346 4,116 4,875 5,742

Adjusted EBIT 123 454 885 1,669 1,983 2,649 3,178 3,681 4,622 5,437

Net finance expenses (63) (239) (493) (1,212) (1,542) (1,740) (2,112) (2,073) (2,530) (2,880)

Finance income 9 12 22 48 99 211 78 170 70 85

Finance expenses (72) (251) (515) (1,260) (1,641) (1,951) (2,189) (2,242) (2,599) (2,965)

Share of profit/(loss) of JV and associates 0 3 0 0 0 (3) (2) (3) 3 3

Pretax profit 95 303 641 1,139 631 984 1,232 2,041 2,348 2,866

Income tax 1 (22) (32) (32) (30) (67) (86) (141) (202) (315)

After tax profit 96 281 609 1,107 601 917 1,147 1,899 2,146 2,550

Profit from discontinued operation 11 39 0 0 0 0 0 0 0 0

After tax profit 107 321 609 1,107 601 917 1,147 1,899 2,146 2,550

Minority interest (54) (56) (81) (84) (43) (29) (26) (40) (64) (77)

Net profit 53 264 528 1,023 558 888 1,121 1,860 2,082 2,474

Recurring net profit 37 236 363 684 453 971 1,041 1,499 2,082 2,474

Exceptional item 16 29 165 339 105 (83) 80 360 0 0

Recurring EPS (RMB) n/a n/a 0.06 0.09 0.05 0.11 0.12 0.15 0.21 0.25

EPS (RMB) n/a n/a 0.09 0.14 0.07 0.10 0.12 0.19 0.21 0.25

DPS (RMB) n/a n/a n/a 0.00 0.02 0.02 0.02 0.03 0.04 0.05

Growth rates (YoY) 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E

Revenue 325.4% 61.0% 92.6% 80.7% 26.0% 44.0% 6.1% 19.6% 25.2% 18.1%

Sales of electricity 170.9% 241.4% 107.6% 79.7% 27.4% 35.1% 12.4% 20.3% 25.2% 18.1%

EBITDA 271.5% 249.7% 111.4% 99.1% 7.5% 23.1% 20.5% 22.0% 20.4% 17.9%

Adjusted EBITDA 261.7% 269.0% 102.2% 86.9% 26.7% 27.4% 19.0% 17.8% 24.6% 17.8%

EBIT 442.7% 240.8% 110.2% 107.3% -7.6% 25.6% 22.7% 23.0% 18.4% 17.8%

Adjusted EBIT 482.5% 270.1% 94.7% 88.7% 18.8% 33.6% 20.0% 15.8% 25.5% 17.6%

Pretax profit 302.1% 218.1% 111.4% 77.6% -44.6% 56.1% 25.2% 65.6% 15.1% 22.0%

After tax profit 240.2% 199.6% 90.1% 81.6% -45.7% 52.6% 25.0% 65.6% 13.0% 18.8%

Net profit 412.0% 397.1% 99.8% 93.7% -45.5% 59.1% 26.3% 65.9% 12.0% 18.8%

EPS n/a n/a n/a 54.4% -53.0% 57.0% 19.5% 54.2% 12.0% 18.8%

Recurring net profit 297.8% 538.0% 54.2% 88.3% -33.8% 114.4% 7.3% 44.0% 38.8% 18.8%

Recurring EPS n/a n/a n/a 50.1% -43.0% 111.5% 1.5% 33.9% 38.8% 18.8%

Margins 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E

EBITDA margin 96.4% 98.7% 100.5% 111.4% 94.0% 85.6% 91.9% 93.2% 89.5% 89.4%

Adjusted EBITDA margin 82.0% 88.7% 86.3% 89.8% 89.3% 84.2% 89.1% 87.3% 86.8% 86.6%

EBIT margin 63.8% 63.7% 64.5% 74.4% 54.0% 50.1% 54.7% 56.0% 52.9% 52.8%

Adjusted EBIT margin 49.5% 53.6% 50.3% 52.8% 49.3% 48.7% 52.0% 50.1% 50.2% 50.0%

Pretax profit margin 38.4% 35.8% 36.5% 36.0% 15.7% 18.1% 20.2% 27.7% 25.5% 26.3%

After tax profit margin 43.1% 37.9% 34.7% 35.0% 14.9% 16.9% 18.8% 25.8% 23.3% 23.4%

Net margin 21.4% 31.2% 30.0% 32.4% 13.9% 16.3% 18.3% 25.3% 22.6% 22.7%

Recurring net margin 14.9% 27.8% 20.7% 21.7% 11.3% 17.8% 17.0% 20.4% 22.6% 22.7%

Net Interest coverage 3.8 3.5 3.6 2.9 2.5 2.7 2.7 3.3 3.3 3.4

7

HNR Balance Sheet Projection

Sources: Company, CGIS Research estimates

Balance sheet (RMB m) 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E

Non current assets

PP&E 8,544 14,336 27,803 36,956 39,859 45,599 57,873 68,658 76,690 84,008

Lease prepayments 15 23 65 102 122 138 157 317 317 317

Intangible assets 358 412 395 381 364 703 696 682 657 632

Investment in associates and JV 52 0 0 85 85 82 112 109 113 116

Other assets 21 1,165 2,690 3,824 3,717 3,516 4,153 5,131 5,240 5,186

Deferred tax assets 21 16 13 7 6 6 5 4 4 4

9,012 15,951 30,966 41,356 44,153 50,044 62,997 74,901 83,020 90,263

Current assets

Inventories 2 0 1 2 4 4 13 43 (16) 48

Trade and bill receivables 117 391 960 2,010 3,303 2,908 3,160 2,900 4,165 5,073

Prepayments and other current assets 121 597 208 584 562 403 176 122 122 122

Restricted deposits 29 16 1 59 209 170 2 27 27 27

Cash 1,644 819 1,309 7,518 5,469 6,265 7,786 4,504 6,221 7,926

Others 0 7 1 0 0 3 4 56 56 56

1,912 1,830 2,479 10,174 9,546 9,754 11,141 7,652 10,575 13,252

Total assets 10,924 17,781 33,445 51,531 53,699 59,798 74,138 82,553 93,595 103,515

Current liabilities

Borrowings 2,396 2,799 4,818 6,759 8,276 10,389 17,306 18,727 23,527 28,527

Obligations under finance leases 0 119 232 283 361 386 434 496 496 496

Tax payable 4 13 6 18 31 32 40 60 60 60

Other payables 1,574 2,082 6,255 8,839 6,214 8,435 7,961 9,250 10,438 11,224

3,974 5,012 11,311 15,899 14,882 19,242 25,741 28,533 34,521 40,307

Non current liabilities

Borrowings 4,437 8,087 13,201 19,257 22,005 22,606 26,842 30,677 33,877 35,877

Obligations under finance leases 0 806 1,768 2,384 2,257 1,883 2,769 2,018 2,018 2,018

Others 49 324 762 1,547 1,572 1,086 1,634 2,450 2,450 2,450

Deferred income 176 234 249 258 273 265 248 231 231 231

Deferred tax liabilities 9 21 34 27 18 19 19 20 20 20

4,670 9,472 16,015 23,472 26,126 25,859 31,512 35,395 38,595 40,595

Equity

Share capital 452 452 5,800 8,447 8,447 9,029 9,728 9,728 9,728 9,728

Reserves 1,223 2,132 (516) 2,885 3,373 4,832 6,373 8,070 9,860 11,917

Attributable to equity owner 1,674 2,583 5,284 11,332 11,820 13,861 16,101 17,798 19,588 21,645

Minority interests 605 713 835 828 871 836 784 827 891 968

2,280 3,297 6,119 12,159 12,691 14,697 16,885 18,624 20,479 22,613

Total equity and liabilities 10,924 17,781 33,445 51,531 53,699 59,798 74,138 82,553 93,595 103,515

BVPS (RMB) - - - 1.34 1.40 1.54 1.66 1.83 2.01 2.23

8

HNR Cash Flow Projection; Valuation and Ratios

Sources: Company, CGIS Research estimates

Cash flow statement (RMB m) 2008 2009 2010 2011 2012 2013 2014 2015E 2016E 2017E

Pretax profit 108 360 641 1,139 631 984 1,232 2,041 2,348 2,866

Income tax (1) (20) (15) (22) (25) (68) (77) (141) (202) (315)

Depreciation 101 283 614 1,150 1,591 1,910 2,237 2,696 3,347 3,957

Amortization 1 14 19 20 21 21 29 34 25 25

Interest expense 95 251 514 1,059 1,620 1,870 2,143 2,241 2,599 2,965

Interest income (5) (8) (13) (43) (92) (51) (55) (170) (70) (85)

Dividend income (2) (4) (4) (3) (4) (9) (8) 0 0 0

Share of profit / (loss) of JV and associates (0) (3) 0 0 0 3 2 3 (3) (3)

Change in working capital (96) (114) (485) (921) (619) 1,116 689 1,520 (18) (132)

Others (4) (84) (12) 183 (10) 140 (68) (516) 0 0

Operating cash flow 197 674 1,260 2,562 3,113 5,918 6,125 7,709 8,027 9,276

Purchase/(disposal) of PP&E and intangible assets (4,988) (7,164) (10,417) (7,699) (6,580) (7,157) (13,394) (13,062) (11,150) (10,890)

Acquisition of subsidiaries/disposal of subsidiaries 0 138 0 0 0 (2) (361) 0 0 0

Investment in/(disposal of) financial assets, JV & associates (3) (357) (33) (328) (192) 0 0 0 0 0

Interest received 5 8 13 43 87 58 58 170 70 85

Dividend received 4 4 4 3 4 9 8 0 0 0

Others 99 215 713 194 (1,674) 439 728 (500) 0 0

Investing cash flow (4,883) (7,156) (9,720) (7,787) (8,355) (6,653) (12,961) (13,393) (11,080) (10,805)

Net proceeds from issuance of shares 0 0 0 5,403 0 1,230 1,358 0 0 0

Capital contribution - equity owner 780 700 2,172 0 0 0 0 0 0 0

Capital contribution - minority interest 223 207 86 5 62 0 0 0 0 0

Proceeds from /(repayment of) borrowings 4,953 4,615 7,134 7,998 4,263 2,709 10,489 5,256 8,000 7,000

Interest paid (213) (484) (705) (1,316) (1,858) (1,850) (2,228) (2,660) (2,937) (3,350)

Dividend paid to equity owner 0 0 0 0 0 (127) (181) (195) (292) (416)

Others (9) 590 280 (510) (964) (598) (550) 0 0 0

Financing cash flow 5,735 5,627 8,968 11,580 1,503 1,364 8,889 2,401 4,771 3,234

Net change in cash 1,048 (855) 509 6,355 (3,739) 630 2,053 (3,283) 1,718 1,705

Valuation

P/E (recurring earnings) n/a n/a 30.9 19.7 33.9 15.8 15.7 12.3 8.9 7.5

Dividend yield n/a n/a n/a 0.0% 0.8% 1.2% 1.2% 1.6% 2.3% 2.7%

P/B n/a n/a n/a 1.4 1.3 1.2 1.1 1.0 0.9 0.9

EV/EBITDA n/a n/a 35.3 17.7 16.5 13.4 11.1 9.1 7.6 6.4

Ratios

Recurring net margin 14.9% 27.8% 20.7% 21.7% 11.3% 17.8% 17.0% 20.4% 22.6% 22.7%

Recurring ROE - 11.1% 9.2% 8.2% 3.9% 7.6% 7.0% 8.8% 11.1% 12.0%

Recurring ROA - 1.6% 1.4% 1.6% 0.9% 1.7% 1.6% 1.9% 2.4% 2.5%

Net debt / Equity 227.6% 305.4% 273.1% 152.1% 195.5% 181.9% 215.3% 241.1% 249.9% 249.8%

Current ratio 0.48 0.37 0.22 0.64 0.64 0.51 0.43 0.27 0.31 0.33

9

COMPANY UPDATE

Analyst: Wayne Fung, CFA

Daqo New Energy [DQ.US; US$25.06; Not rated] – Q1 2016 results in line with expectations; Positive management guid-

ance for Q2 2016

Daqo’s Q1 2016 net profit came in at US$8.3m, compared to

US$1.2m in Q1 2015 and US$9.6m in Q4 2015. Adjusting for costs

related to the non-operational Chongqing polysilicon base and

share-based compensation expenses, the non-GAAP net profit

would be US$11.7m, versus US$6.4m and US$11.9m in Q1 2015

and Q4 2015, respectively. Revenue increased 38% YoY to

US$57.7m, but dropped 2.7% QoQ. The gross margin expanded

slightly 0.5ppt QoQ to 29%, while the non-GAAP gross margin was

32.6% in Q1 2016, up from 31.9% in Q4 2015.

Strong production volume in Q1. Daqo’s polysilicon capacity

was running at full utilization and surpassed its name plate an-

nual capacity of 12,150t. Polysilicon production volume jumped

89.1% YoY to 3,405t in Q1 2016, driven mainly by increased

capacity. Compared to Q4 2015, production volume dropped

4%, but this was largely due to fewer calendar days and the

Chinese New Year effect. External sales volume of polysilicon

surged 93% YoY to 2,905t (within management guidance of

2,800-3,000t), but dropped 6% QoQ because of higher in-

house consumption versus Q4 2015. On the wafer side, sales

volume increased 22% YoY and 5% QoQ to 22.1m pieces.

Cost reduction well on track. Daqo’s polysilicon production

cost in Q1 2016 fell slightly to US$9.65/kg from US$9.74/kg. Of

this, the cash cost fell US$0.07/kg QoQ to US$7.62/kg.

Guidance for Q2 2016. Daqo expects polysilicon sales volume

to be 2,850-2,950t and wafer sales to be 23.5-24.0m pieces.

Daqo maintains the production cost target of <US$10/kg and

cash cost target of <US$8/kg for 2016. Daqo plans to raise

annual wafer capacity to 100m pieces in Q2 2016 from the cur-

rent level of 90m pieces.

Management remained bullish on the polysilicon pricing

outlook during the conference call. On the supply side, man-

agement sees limited new production capacity in China this

year, while at the same time import volume will decline in the

near term as a result of the government’s administrative

measures to crack down on illegal polysilicon imports. On the

demand side, management expects 7GW of new mono-

crystalline wafer capacity, which will offer more opportunities for

polysilicon sales going forward. Management expects the pol-

ysilicon ASP in Q2 2016 to be higher than that in Q1. Daqo is

currently selling its polysilicon at US$19/kg. Management esti-

mates that even if the polysilicon price stays at US$18-19/kg,

wafer makers can still achieve a gross margin of 15-20%.

Daqo New Energy [DQ.US]

Market cap: US$258m

Listing on New Third Board progressing well. On

April 27, Daqo’s subsidiary, Xinjiang Daqo, received

approval to list its shares on the New Third Board.

Management believes Xinjiang Daqo will be regarded

as a tier one company when listed there. Management

expects it to be completed in 2H16E.

Valuation. The stock is currently trading only 7.2x and

5.6x of 2016E and 2017E consensus earnings esti-

mates respectively.

May 11, 2016

(US$ m) Q1 15 Q2 15 Q3 15 Q4 15 Q1 16

Income statement

Revenue 41.9 34.3 46.6 59.3 57.7

Cost of sales (33.4) (30.7) (38.0) (42.4) (40.9)

Gross profit 8.5 3.6 8.6 16.9 16.7

SG&A expenses (4.6) (2.8) (2.9) (2.3) (4.1)

R&D expenses (0.1) (0.2) (0.1) (0.5) (0.1)

Other operating income/(loss) 0.3 0.7 1.1 1.7 0.7

Impairment of long-lived assets 0.0 0.0 0.0 (1.6) 0.0

EBIT 4.1 1.2 6.7 14.3 13.3

Interest expense (3.2) (2.6) (3.1) (4.3) (3.9)

Interest income 0.1 0.1 0.1 0.3 0.1

FX gain/(loss) 0.5 0.2 0.0 (0.0) 0.0

Pretax profit 1.4 (1.1) 3.6 10.3 9.5

Income tax expenses (0.2) 0.2 (0.6) (0.5) (1.1)

After tax profit 1.2 (0.9) 3.1 9.7 8.4

MI 0.0 0.0 0.0 (0.1) (0.1)

Net profit 1.2 (0.9) 3.1 9.6 8.3

Margin

Gross margin 20.2% 10.5% 18.4% 28.5% 29.0%

EBIT margin 9.7% 3.6% 14.3% 24.1% 23.1%

Pretax profit margin 3.3% -3.2% 7.8% 17.3% 16.5%

Net margin 2.8% -2.7% 6.6% 16.2% 14.4%

Sources: Company, CGIS Research

10

Figure 1: Daqo polysilicon sales volume Figure 2: Daqo wafer sales volume

Sources: Company, CGIS Research Sources: Company, CGIS Research

Figure 3: Daqo Polysilicon ASP Figure 4: Daqo polysilicon unit cost (for Xinjiang production base)

Sources: Company, CGIS Research Sources: Company, CGIS Research

15.8

12.2 11.8 12.0 11.8 11.5 10.7 10.9 10.5 10.6 8.7 7.7 7.6

4.8

5.4 4.2 3.8

2.7 2.7 2.3 2.4 2.3 2.4

2.4 2.1 2.0

0.0

5.0

10.0

15.0

20.0

25.0

Q1 13 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16

Cash cost Depreciation

1,406 1,391 1,528 1,646 1,502 1,363

2,277

3,092 2,905

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16

Polysilicon sales volume (t)

18.0 17.1 18.3 18.1 18.3 19.1

21.0 22.1

0

5

10

15

20

25

Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16

Wafer sales volume (m pieces)

16.7 16.7

18.0 18.7

21.6

22.0 21.5

20.5

18.1

16.0 15.0

13.9 13.7

0.0

5.0

10.0

15.0

20.0

25.0

Q1 13 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15 Q3 15 Q4 15 Q1 16

Polysilicon ASP (US$/kg)

11

Figure 5: Daqo polysilicon historical and projected capacity (metric tonne)

Note: Wanzhou polysilicon facility discontinued polysilicon production in Q4 2012.

Sources: Company, CGIS Research

Figure 6: Solar component spot pricing

Sources: PVinsights, CGIS Research

Wafer price (US$/watt) Cell and module price (US$/watt)

Polysilicon price (US$/kg) Price spread (US$/Watt)

$0.00

$0.20

$0.40

$0.60

$0.80

1/1

/201

2

1/4

/201

2

1/7

/201

2

1/1

0/2

01

2

1/1

/201

3

1/4

/201

3

1/7

/201

3

1/1

0/2

01

3

1/1

/201

4

1/4

/201

4

1/7

/201

4

1/1

0/2

01

4

1/1

/201

5

1/4

/201

5

1/7

/201

5

1/1

0/2

01

5

1/1

/201

6

1/4

/201

6

Cell/wafer spread (US$/W) Module/cell spread (US$/W)

Module/wafer spread (US$/W)

$0

$5

$10

$15

$20

$25

$30

$35

$40

Polysilicon (US$/kg) - 1st grade

$0.0

$0.2

$0.4

$0.6

$0.8

$1.0

$1.2

Module price (US$/W) Cell price (US$/W)

$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

$0.35

$0.40

$0.45

$0.50

Wafer price (US$/Wp) (156mm multi) Wafer price (US$/Wp) (156mm mono)

12

Disclaimer

This research report is not directed at, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any jurisdiction where such distribution, publication, availability or use would be contrary to applicable law or regulation or which would subject China Galaxy International Securities (Hong Kong) Co., Limited (“Galaxy International Securities”) and/or its group companies to any registration or licensing requirement within such jurisdiction.

This report (including any information attached) is issued by China Galaxy International Securities (Hong Kong) Co., Limited, one of the subsidiaries of the China Galaxy International Financial Holdings Limited, to the institutional clients from the information sources believed to be reliable, but no repre-sentation or warranty (expressly or implied) is made as to their accuracy, correctness and/or completeness.

This report shall not be construed as an offer, invitation or solicitation to buy or sell any securities of the company(ies) referred to herein. Past perfor-mance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regard-ing future performance. The recipient of this report should understand and comprehend the investment objectives and its related risks, and where necessary consult their own independent financial advisers prior to any investment decision.

Where any part of the information, opinions or estimates contained herein reflects the personal views and opinions of the analyst who prepared this report, such views and opinions may not correspond to the published views or investment decisions of China Galaxy International Financial Holdings Limited and any of its subsidiaries (“China Galaxy International”), directors, officers, agents and employees (“the Relevant Parties”).

All opinions and estimates reflect the judgment of the analyst on the date of this report and are subject to change without notice. China Galaxy Interna-tional and/or the Relevant Parties hereby disclaim any of their liabilities arising from the inaccuracy, incorrectness and incompleteness of this report and its attachment/s and/or any action or omission made in reliance thereof. Accordingly, this report must be read in conjunction with this disclaimer.

Disclosure of Interests

China Galaxy International may have financial interests in relation to the subjected company(ies) the securities in respect of which are reviewed in this report, and such interests aggregate to an amount may equal to or more than 1 % of the subjected company(ies)’ market capitalization.

One or more directors, officers and/or employees of China Galaxy International may be a director or officer of the securities of the company(ies) men-tioned in this report.

China Galaxy International and the Relevant Parties may, to the extent permitted by law, from time to time participate or invest in financing transac-tions with the securities of the company(ies) mentioned in this report, perform services for or solicit business from such company(ies), and/or have a position or holding, or other material interest, or effect transactions, in such securities or options thereon, or other investments related thereto.

China Galaxy International may have served as manager or co-manager of a public offering of securities for, or currently may make a primary market in issues of, any or all of the entities mentioned in this report or may be providing, or have provided within the last 12 months, significant advice or invest-ment services in relation to the investment concerned or a related investment or investment banking services to the company(ies) mentioned in this report.

Furthermore, China Galaxy International may have received compensation for investment banking services from the company(ies) mentioned in this report within the preceding 12 months and may currently seeking investment banking mandate from the subject company(ies).

Analyst Certification

The analyst who is primarily responsible for the content of this report, in whole or in part, certifies that with respect to the securities or issuer covered in this report: (1) all of the views expressed accurately reflect his or her personal views about the subject, securities or issuer; and (2) no part of his or her compensation was, is, or will be, directly or indirectly, related to the specific views expressed by the analyst in this report.

Besides, the analyst confirms that neither the analyst nor his/her associates (as defined in the code of conduct issued by The Hong Kong Securities and Futures Commission) (1) have dealt in or traded in the securities covered in this research report within 30 calendar days prior to the date of issue of this report; (2) will deal in or trade in the securities covered in this research report three business days after the date of issue of this report; (3) serve as an officer of any of the Hong Kong-listed companies covered in this report; and (4) have any financial interests in the Hong Kong listed companies cov-ered in this report.

Explanation on Equity Ratings

Copyright Reserved

No part of this material may be reproduced or redistributed without the prior written consent of China Galaxy International Securities (Hong Kong) Co., Limited.

China Galaxy International Securities (Hong Kong) Co. Limited, CE No.AXM459

Room 3501-3507, 35/F, Cosco Tower, Grand Millennium Plaza, 183 Queen’s Road Central, Sheung Wan, Hong Kong. General line: 3698-6888.

BUY share price will increase by >20% within 12 months in absolute terms :

SELL share price will decrease by >20% within 12 months in absolute terms :

HOLD no clear catalyst, and downgraded from BUY pending clearer signal to reinstate BUY or further downgrade to outright SELL :