Yum Cha 飲 茶 · Mobile Company, China Telecom, China Unicom Corporation and China Reform will...

18

Yum Cha 飲 茶 August 8, 2018 INDICES Closing DoD% Hang Seng Index 28248.8 1.5 HSCEI 10866.1 1.5 Shanghai COMP 2779.4 2.7 Shenzhen COMP 1495.0 2.75 Gold 1211.0 0.3 BDIY 1773.0 1.0 Crude Oil, WTI(US$/BBL) 69.0 0.8 Crude Oil, BRENT(US$/BBL) 73.8 0.7 HIBOR, 3-M 1.8 (1.5) SHIBOR, 3-M 3.0 (1.6) RMB/USD 6.9 0.4 RESEARCH NOTES DATA RELEASES DUE THIS WEEK 6-7 August Foreign Direct Investment 7-8 August Trade Balance 8 August PPI YoY 8 August CPI YoY 9-15 August Money Supply M2 YoY 9-15 August New Yuan Loans CNY Source: Bloomberg CHINA TOWER [0788.HK; NOT RATED] - China Tower Corporation (China Tower) raised approximately HK$53,422.8m by issuing 43,114,800,000 H-shares at an offer price of HK$1.26, which is the lowest point of the price range. After the IPO, China Mobile Company, China Telecom, China Unicom Corporation and China Reform will own 28.5%, 20.9%, 21.1% and 4.5% of China Tower respectively. Based on the IPO price of HK$1.26, China Tower is valued at 6.7x 2018 EV/EBITDA after factoring in the IPO proceeds, which doesn’t look particularly expensive. The Chinese govern- ment intends to take the lead in 5G development, and China Tower will be one of the key 5G development names in terms of the global tower industry. After listing, China Tower will be a sizable telecommunications name with a growth angle, trading at a discount to its global peers. We share the view that investors might take a wait-and- see approach to China Tower, given the current market environment. Trading of shares of China Tower will start today. An unexciting post-IPO share price perfor- mance may offer a good opportunity for patient investors. CHINA RAILWAY SECTOR - According to some media news reports, China’s rail- way FAI in 2018 is likely to reach Rmb800bn, exceeding the original target of Rmb732bn set in January. Railway investment is expected to exceed the initial full- year CRC target, driven mainly by 1) CRC’s freight business expansion, which should boost its locomotive and freight wagon procurement, and 2) infrastructure FAI accel- eration, spurred by the central government’s need to stimulate economic growth. Giv- en the 13th FYP target, we expect new line additions in 2018-2020E to likely reach 7,000-8,000 km p.a., more than triple the new line additions in 2016-2017. CRCC (1186.HK) is our top pick in the construction sector. After the share price rally during recent weeks, the stock is still trading below its historical average in terms of valua- tion. In the railway equipment sector, we prefer CRRC (1766 HK). CHINA HEALTHCARE SECTOR - Healthcare stocks started correcting in early June, we believe recent pressure on the healthcare sector is due to a combination of 1) profit-taking after a re-rating since 2017 (especially for the leading players); 2) the vaccine incident, together with the movie Dying to survive, which exposed long- existing problems in China’s medical system once again, i.e. quality regulations, high drug prices, and a high marketing and selling expenses to revenue ratio; and 3) about 6% depreciation in the RMB since early June. The aim of this report is to throw some light on the healthcare sector investment thesis in this market environment and identi- fy possible bottom-fishing opportunities for investors. We comprehensively address the stocks in three areas, screening for candidates that meet the following three crite- ria: 1) they fundamentally comply with government policy direction and have solid visible prospects; 2) they fit into the current investor appetite of having exposure to international certificates, international collaboration, exports or foreign R&D pipelines, etc., which strengthens investors' faith in the Company’s overall quality, credibility and trustworthiness; and 3) they have a relatively attractive valuation after the correction. Following this stock screening logic, our preferred stocks in the current market are CTCM [570.hk], Shanghai Pharm [2607.hk], Genscript [1548.hk] and CSPC [1093.hk]. We believe the argument about a structural de-rating is overly bearish, as some key reasons to invest in the sector remain intact. For example, it is largely im- mune from the impact of the trade dispute, and the leading players have strong cash flow and balance sheets.

Transcript of Yum Cha 飲 茶 · Mobile Company, China Telecom, China Unicom Corporation and China Reform will...

1

Yum Cha 飲 茶 August 8, 2018

INDICES Closing DoD%

Hang Seng Index 28248.8 1.5

HSCEI 10866.1 1.5

Shanghai COMP 2779.4 2.7

Shenzhen COMP 1495.0 2.75

Gold 1211.0 0.3

BDIY 1773.0 1.0

Crude Oil, WTI(US$/BBL) 69.0 0.8

Crude Oil, BRENT(US$/BBL) 73.8 0.7

HIBOR, 3-M 1.8 (1.5)

SHIBOR, 3-M 3.0 (1.6)

RMB/USD 6.9 0.4

RESEARCH NOTES

DATA RELEASES DUE THIS WEEK

6-7 August Foreign Direct Investment

7-8 August Trade Balance

8 August PPI YoY

8 August CPI YoY

9-15 August Money Supply M2 YoY

9-15 August New Yuan Loans CNY

Source: Bloomberg

CHINA TOWER [0788.HK; NOT RATED] - China Tower Corporation (China Tower)

raised approximately HK$53,422.8m by issuing 43,114,800,000 H-shares at an offer

price of HK$1.26, which is the lowest point of the price range. After the IPO, China

Mobile Company, China Telecom, China Unicom Corporation and China Reform will

own 28.5%, 20.9%, 21.1% and 4.5% of China Tower respectively. Based on the IPO

price of HK$1.26, China Tower is valued at 6.7x 2018 EV/EBITDA after factoring in

the IPO proceeds, which doesn’t look particularly expensive. The Chinese govern-

ment intends to take the lead in 5G development, and China Tower will be one of the

key 5G development names in terms of the global tower industry. After listing, China

Tower will be a sizable telecommunications name with a growth angle, trading at a

discount to its global peers. We share the view that investors might take a wait-and-

see approach to China Tower, given the current market environment. Trading of

shares of China Tower will start today. An unexciting post-IPO share price perfor-

mance may offer a good opportunity for patient investors.

CHINA RAILWAY SECTOR - According to some media news reports, China’s rail-

way FAI in 2018 is likely to reach Rmb800bn, exceeding the original target of

Rmb732bn set in January. Railway investment is expected to exceed the initial full-

year CRC target, driven mainly by 1) CRC’s freight business expansion, which should

boost its locomotive and freight wagon procurement, and 2) infrastructure FAI accel-

eration, spurred by the central government’s need to stimulate economic growth. Giv-

en the 13th FYP target, we expect new line additions in 2018-2020E to likely reach

7,000-8,000 km p.a., more than triple the new line additions in 2016-2017. CRCC

(1186.HK) is our top pick in the construction sector. After the share price rally during

recent weeks, the stock is still trading below its historical average in terms of valua-

tion. In the railway equipment sector, we prefer CRRC (1766 HK).

CHINA HEALTHCARE SECTOR - Healthcare stocks started correcting in early June,

we believe recent pressure on the healthcare sector is due to a combination of 1)

profit-taking after a re-rating since 2017 (especially for the leading players); 2) the

vaccine incident, together with the movie Dying to survive, which exposed long-

existing problems in China’s medical system once again, i.e. quality regulations, high

drug prices, and a high marketing and selling expenses to revenue ratio; and 3) about

6% depreciation in the RMB since early June. The aim of this report is to throw some

light on the healthcare sector investment thesis in this market environment and identi-

fy possible bottom-fishing opportunities for investors. We comprehensively address

the stocks in three areas, screening for candidates that meet the following three crite-

ria: 1) they fundamentally comply with government policy direction and have solid

visible prospects; 2) they fit into the current investor appetite of having exposure to

international certificates, international collaboration, exports or foreign R&D pipelines,

etc., which strengthens investors' faith in the Company’s overall quality, credibility and

trustworthiness; and 3) they have a relatively attractive valuation after the correction.

Following this stock screening logic, our preferred stocks in the current market are

CTCM [570.hk], Shanghai Pharm [2607.hk], Genscript [1548.hk] and CSPC

[1093.hk]. We believe the argument about a structural de-rating is overly bearish, as

some key reasons to invest in the sector remain intact. For example, it is largely im-

mune from the impact of the trade dispute, and the leading players have strong cash

flow and balance sheets.

COMPANY NEWS

Analyst: Mark Po, CFA; Tel: (852) 3698 6318; [email protected]

China Tower Corporation Limited [0788.HK; Not Rated] — A symbolic case of SOE reform

Background. China Tower Corp (China Tower) [0788.HK] was established on

15 Jul, 2014 under the name “China Communications Facilities Services Corporation Limited”. The three telecom operators, China Mobile Company, China Telecom and China Unicom Corporation, were the three promoters of the Company. The three telecom operators injected their existing tower assets into China Tower on 31 Oct 2015. In Dec 2015, China Tower issued new shares to the three telecom operators and China Reform Holdings Corp (China Reform).

China Tower raised approximately HK$53,422.8m by issuing 43,114,800,000 H-shares at an offer price of HK$1.26, which is the lowest point of the price range of HK$1.26 to HK$1.58 after deducting professional fees and assuming no exercise of the over-allotment option. Approximately 60% of the IPO proceeds are expected to be used to fund capital expenditure: a) 51% to 54% is expected to be used for new site construction and expansion; and b) 6% to 9% is expected to be used for ancillary facilities replacement and improvement. Approximately 30% of the IPO proceeds are expected to be used to repay bank loans. And approximately 10% is expected to be used for working capital and other general corporate purposes. After the IPO, China Mobile Company, China Telecom, China Unicom Corporation and China Reform will own 28.5%, 20.9%, 21.1% and 4.5% of China Tower, respectively.

China Tower Corp is the world’s largest telecommunications tower infrastructure service provider. As of 31 Mar 2018, the Company operated

and managed 1,886,454 sites and served 2,733,500 tenants. According to the F&S Report, as of 31 Dec 2017, China Tower ranked first among the global telecommunications tower infrastructure service providers in terms of the number of sites, the number of tenants, and revenue. According to the F&S Report, China Tower’s market share in the telecommunications tower infrastructure industry in China was 96.3% in terms of the number of sites and 97.3% in terms of revenue as of 31 Dec 2017.

China Tower is engaged in three types of business:

Tower business: Using its sites, China Tower carries out macro-cell and small-

cell business with telecommunications service providers (TSPs). a) Macro-cell business: China Tower provides site space, including towers and shelters or cabinets, to TSPs and hosts their antennas and other macro-cell equipment. Through its macro-cell business, it supports TSPs in providing extensive coverage of their wireless communications networks in China. b) Small-cell business: China Tower provides site space, including towers, poles, and other infrastructure resources and cabinets, to TSPs and hosts their small-cell equipment. Through its small-cell business, China Tower supports TSPs in densifying their coverage and increasing the capacity of the wireless communications networks built up by their macro cell equipment, particularly in urban areas with a high density of people and buildings, and in certain non-urban areas. In 2015, 2016 and 2017 and Q1 2018, China Tower’s revenue from its macro-cell business accounted for 99.5%, 99.2%, 97.3% and 96.5% of total revenue, respectively. China Tower commenced its small-cell business in 2017. In 2017, revenue derived from its small-cell business was RMB257m and in the three months ended 31 Mar 2018, operating revenue from its small-cell business was RMB84m. As of 31 Mar, 2018, it had 18,058 TSP tenants for its small-cell business.

DAS business: China Tower provides indoor distributed antenna systems to TSPs and to attach their telecommunications equipment. Through its DAS business, China Tower supports TSPs in providing in-depth coverage of wireless communications networks in buildings and tunnels. China Tower has established a track record in its DAS business with increasing revenue and number of tenants. In 2015, 2016 and 2017, revenue from its DAS business amounted to RMB45m, RMB421m and RMB1,284m, respectively. In the three months ended 31 Mar 2018, China Tower’s revenue for its DAS business amounted to RMB391m. As of 31 Dec, 2015, 2016 and 2017 and 31 Mar, 2018, the number of TSP tenants in China Tower’s DAS business was 3,532, 13,646, 23,615 and 25,171, respectively.

Trans-sector site application and information business (TSSAI business): Using its sites dispersed nationwide, China Tower provides site resource

August 08, 2018

[China Tower’s use of proceeds]

services, including infrastructure, maintenance services and power services, to host different types of devices for its customers from different industries and help them to build up different types of national or regional networks. Furthermore, by integrating data collection devices, transmission networks, data platforms and other resources, China Tower provides site-based information services, including data collection, transmission, analysis and application. China Tower has reported rapid growth in revenue from its TSSAI business since January 2016. In 2016 and 2017, China Tower’s revenue from its TSSAI business was RMB19m and RMB169m, respectively. In the three months ended 31 Mar 2018, revenue from its TSSAI business was RMB113m.

Unexciting post-IPO share price performance may offer a good opportunity. Based on the IPO price of HK$1.26, China Tower is valued

at 6.7x 2018 EV/EBITDA after factoring in the IPO proceeds, which doesn’t look particular expensive. We share the view that news flow on industry restructuring at the telecom operator level might create concerns about China Tower. However, at this stage, there is no confirmation of the news flow. If this is the case, it will take time for the deal to be completed, and China Tower should have enough time to mitigate the impact. The market’s lukewarm response to the China Tower IPO is somewhat expected, as investors believe that China Tower Corp doesn’t look attractive in terms of its IPO price, customer mix and profitability. The market might have concerns about the performance of the China Tower Corp’s IPO, given its huge size and the current market environment.

The Chinese government is taking the lead in 5G development, and

China Tower will be one of the main 5G development names in terms of

the global tower industry. After listing, China Tower will be sizable

telecommunications name with a growth angle, trading at a discount to

its global peers. We share the view that investors might take a wait-and-

see approach to China Tower, given the current market environment.

Trading of shares of China Tower will start today. An unexciting post-IPO

share price performance may offer a good opportunity for patient

investors.

Source: Company Data, CGIS Research,

Source: Bloomberg, Company Data, CSIS Research; *: IPO price .

●

●

●

Key Financials

(in RMBm)2015 2016 2017 2018E 2019E

Revenue 8,802.0 55,997.0 68,665.0 71,877.6 76,121.3

Change (YoY %) 536.2 22.6 4.7 5.9

Gross Profit (4,161.0) 5,070.0 7,715.0 8,582.8 9,908.8

Gross Margin % (47.3) 9.1 11.2 11.9 13.0

Net Profit (3,596.0) 76.0 1,943.0 1,990.5 2,816.0

Net Margin % (40.9) 0.1 2.8 2.8 3.7

EPS (Basic) (0.02) 0.00 0.01 0.01 0.02

Change (YoY %) (100.0) (102.1) 2,456.6 2.4 41.5

DPS $0.000 $0.000 $0.000 $0.006 $0.008

ROE (%) (5.0) 0.1 1.5 1.3 1.6

Dividend Yield (%) - - - 0.54 0.76

PER (x) (51.6) 2,443.8 95.6 93.3 66.0

PBR (x) 1.5 1.5 1.5 1.1 1.1

FCF Yield (%) -0.02% -99.26% -5.31% -2.57% 1.75%

Capex (m) - (208,807.0) (46,364.0) (39,244.8) (31,735.8)

Free cash flow per share (0.0) (1.3) (0.1) (0.0) 0.0

Net Gearing (%) 8.2 25.7 102.9 53.0 51.8

August 08, 2018

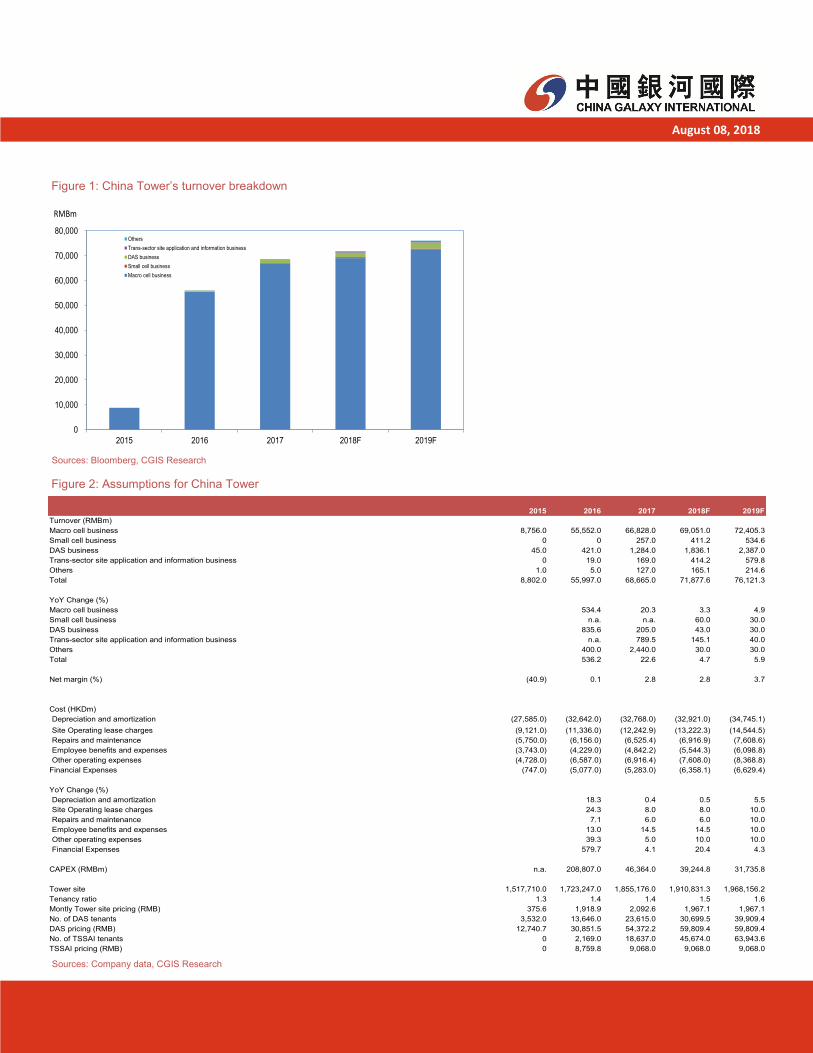

Figure 1: China Tower’s turnover breakdown

Sources: Bloomberg, CGIS Research

Figure 2: Assumptions for China Tower

Sources: Company data, CGIS Research

2015 2016 2017 2018F 2019F

Turnover (RMBm)

Macro cell business 8,756.0 55,552.0 66,828.0 69,051.0 72,405.3

Small cell business 0 0 257.0 411.2 534.6

DAS business 45.0 421.0 1,284.0 1,836.1 2,387.0

Trans-sector site application and information business 0 19.0 169.0 414.2 579.8

Others 1.0 5.0 127.0 165.1 214.6

Total 8,802.0 55,997.0 68,665.0 71,877.6 76,121.3

YoY Change (%)

Macro cell business 534.4 20.3 3.3 4.9

Small cell business n.a. n.a. 60.0 30.0

DAS business 835.6 205.0 43.0 30.0

Trans-sector site application and information business n.a. 789.5 145.1 40.0

Others 400.0 2,440.0 30.0 30.0

Total 536.2 22.6 4.7 5.9

Net margin (%) (40.9) 0.1 2.8 2.8 3.7

Cost (HKDm)

Depreciation and amortization (27,585.0) (32,642.0) (32,768.0) (32,921.0) (34,745.1)

Site Operating lease charges (9,121.0) (11,336.0) (12,242.9) (13,222.3) (14,544.5)

Repairs and maintenance (5,750.0) (6,156.0) (6,525.4) (6,916.9) (7,608.6)

Employee benefits and expenses (3,743.0) (4,229.0) (4,842.2) (5,544.3) (6,098.8)

Other operating expenses (4,728.0) (6,587.0) (6,916.4) (7,608.0) (8,368.8)

Financial Expenses (747.0) (5,077.0) (5,283.0) (6,358.1) (6,629.4)

YoY Change (%)

Depreciation and amortization 18.3 0.4 0.5 5.5

Site Operating lease charges 24.3 8.0 8.0 10.0

Repairs and maintenance 7.1 6.0 6.0 10.0

Employee benefits and expenses 13.0 14.5 14.5 10.0

Other operating expenses 39.3 5.0 10.0 10.0

Financial Expenses 579.7 4.1 20.4 4.3

CAPEX (RMBm) n.a. 208,807.0 46,364.0 39,244.8 31,735.8

Tower site 1,517,710.0 1,723,247.0 1,855,176.0 1,910,831.3 1,968,156.2

Tenancy ratio 1.3 1.4 1.4 1.5 1.6

Montly Tower site pricing (RMB) 375.6 1,918.9 2,092.6 1,967.1 1,967.1

No. of DAS tenants 3,532.0 13,646.0 23,615.0 30,699.5 39,909.4

DAS pricing (RMB) 12,740.7 30,851.5 54,372.2 59,809.4 59,809.4

No. of TSSAI tenants 0 2,169.0 18,637.0 45,674.0 63,943.6

TSSAI pricing (RMB) 0 8,759.8 9,068.0 9,068.0 9,068.0

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

2015 2016 2017 2018F 2019F

Others

Trans-sector site application and information business

DAS business

Small cell business

Macro cell business

RMBm

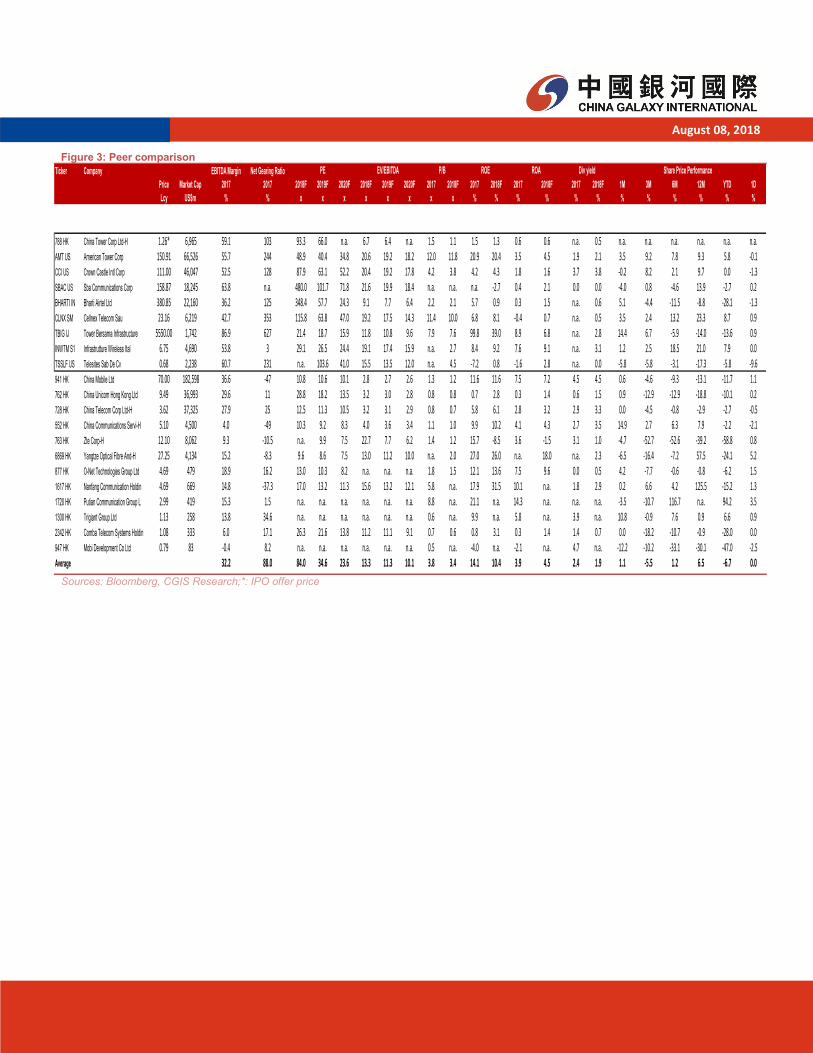

Figure 3: Peer comparison

Sources: Bloomberg, CGIS Research;*: IPO offer price

August 08, 2018

Ticker Company EBITDA Margin Net Gearing Ratio

Price Market Cap 2017 2017 2018F 2019F 2020F 2018F 2019F 2020F 2017 2018F 2017 2018F 2017 2018F 2017 2018F 1M 3M 6M 12M YTD 1D

Lcy US$m % % x x x x x x x x % % % % % % % % % % % %

788 HK China Tower Corp Ltd-H 1.26* 6,965 59.1 103 93.3 66.0 n.a. 6.7 6.4 n.a. 1.5 1.1 1.5 1.3 0.6 0.6 n.a. 0.5 n.a. n.a. n.a. n.a. n.a. n.a.AMT US American Tower Corp 150.91 66,526 55.7 244 48.9 40.4 34.8 20.6 19.2 18.2 12.0 11.8 20.9 20.4 3.5 4.5 1.9 2.1 3.5 9.2 7.8 9.3 5.8 -0.1CCI US Crown Castle Intl Corp 111.00 46,047 52.5 128 87.9 63.1 52.2 20.4 19.2 17.8 4.2 3.8 4.2 4.3 1.8 1.6 3.7 3.8 -0.2 8.2 2.1 9.7 0.0 -1.3SBAC US Sba Communications Corp 158.87 18,245 63.8 n.a. 480.0 101.7 71.8 21.6 19.9 18.4 n.a. n.a. n.a. -2.7 0.4 2.1 0.0 0.0 -4.0 0.8 -4.6 13.9 -2.7 0.2BHARTI IN Bharti Airtel Ltd 380.85 22,160 36.2 125 348.4 57.7 24.3 9.1 7.7 6.4 2.2 2.1 5.7 0.9 0.3 1.5 n.a. 0.6 5.1 -4.4 -11.5 -8.8 -28.1 -1.3CLNX SM Cellnex Telecom Sau 23.16 6,219 42.7 353 115.8 63.8 47.0 19.2 17.5 14.3 11.4 10.0 6.8 8.1 -0.4 0.7 n.a. 0.5 3.5 2.4 13.2 23.3 8.7 0.9TBIG IJ Tower Bersama Infrastructure 5550.00 1,742 86.9 627 21.4 18.7 15.9 11.8 10.8 9.6 7.9 7.6 99.8 39.0 8.9 6.8 n.a. 2.8 14.4 6.7 -5.9 -14.0 -13.6 0.9INWTM S1 Infrastrutture Wireless Ital 6.75 4,690 53.8 3 29.1 26.5 24.4 19.1 17.4 15.9 n.a. 2.7 8.4 9.2 7.6 9.1 n.a. 3.1 1.2 2.5 18.5 21.0 7.9 0.0TSSLF US Telesites Sab De Cv 0.68 2,238 60.7 231 n.a. 103.6 41.0 15.5 13.5 12.0 n.a. 4.5 -7.2 0.8 -1.6 2.8 n.a. 0.0 -5.8 -5.8 -3.1 -17.3 -5.8 -9.6941 HK China Mobile Ltd 70.00 182,598 36.6 -47 10.8 10.6 10.1 2.8 2.7 2.6 1.3 1.2 11.6 11.6 7.5 7.2 4.5 4.5 0.6 -4.6 -9.3 -13.1 -11.7 1.1762 HK China Unicom Hong Kong Ltd 9.49 36,993 29.6 11 28.8 18.2 13.5 3.2 3.0 2.8 0.8 0.8 0.7 2.8 0.3 1.4 0.6 1.5 0.9 -12.9 -12.9 -18.8 -10.1 0.2728 HK China Telecom Corp Ltd-H 3.62 37,325 27.9 25 12.5 11.3 10.5 3.2 3.1 2.9 0.8 0.7 5.8 6.1 2.8 3.2 2.9 3.3 0.0 -4.5 -0.8 -2.9 -2.7 -0.5552 HK China Communications Servi-H 5.10 4,500 4.0 -49 10.3 9.2 8.3 4.0 3.6 3.4 1.1 1.0 9.9 10.2 4.1 4.3 2.7 3.5 14.9 2.7 6.3 7.9 -2.2 -2.1763 HK Zte Corp-H 12.10 8,062 9.3 -10.5 n.a. 9.9 7.5 22.7 7.7 6.2 1.4 1.2 15.7 -8.5 3.6 -1.5 3.1 1.0 -4.7 -52.7 -52.6 -39.2 -58.8 0.86869 HK Yangtze Optical Fibre And-H 27.25 4,134 15.2 -8.3 9.6 8.6 7.5 13.0 11.2 10.0 n.a. 2.0 27.0 26.0 n.a. 18.0 n.a. 2.3 -6.5 -16.4 -7.2 57.5 -24.1 5.2877 HK O-Net Technologies Group Ltd 4.69 479 18.9 16.2 13.0 10.3 8.2 n.a. n.a. n.a. 1.8 1.5 12.1 13.6 7.5 9.6 0.0 0.5 4.2 -7.7 -0.6 -0.8 -6.2 1.51617 HK Nanfang Communication Holdin 4.69 669 14.8 -37.3 17.0 13.2 11.3 15.6 13.2 12.1 5.8 n.a. 17.9 31.5 10.1 n.a. 1.8 2.9 0.2 6.6 4.2 125.5 -15.2 1.31720 HK Putian Communication Group L 2.99 419 15.3 1.5 n.a. n.a. n.a. n.a. n.a. n.a. 8.8 n.a. 21.1 n.a. 14.3 n.a. n.a. n.a. -3.5 -10.7 116.7 n.a. 94.2 3.51300 HK Trigiant Group Ltd 1.13 258 13.8 34.6 n.a. n.a. n.a. n.a. n.a. n.a. 0.6 n.a. 9.9 n.a. 5.8 n.a. 3.9 n.a. 10.8 -0.9 7.6 0.9 6.6 0.92342 HK Comba Telecom Systems Holdin 1.08 333 6.0 17.1 26.3 21.6 13.8 11.2 11.1 9.1 0.7 0.6 0.8 3.1 0.3 1.4 1.4 0.7 0.0 -18.2 -10.7 -0.9 -28.0 0.0947 HK Mobi Development Co Ltd 0.79 83 -0.4 8.2 n.a. n.a. n.a. n.a. n.a. n.a. 0.5 n.a. -4.0 n.a. -2.1 n.a. 4.7 n.a. -12.2 -10.2 -33.1 -30.1 -47.0 -2.5Average 32.2 88.0 84.0 34.6 23.6 13.3 11.3 10.1 3.8 3.4 14.1 10.4 3.9 4.5 2.4 1.9 1.1 -5.5 1.2 6.5 -6.7 0.0

ROE ROA Div yield Share Price PerformancePE EV/EBITDA P/B

1

Sector Report

August 8, 2018

Source: Bloomberg, CGIS Research, Note: based on

closing prices on 7 August 2018

Kelly Zou—Analyst

(852) 3698-6319

Wong Chi Man—Head of Research

(852) 3698-6317

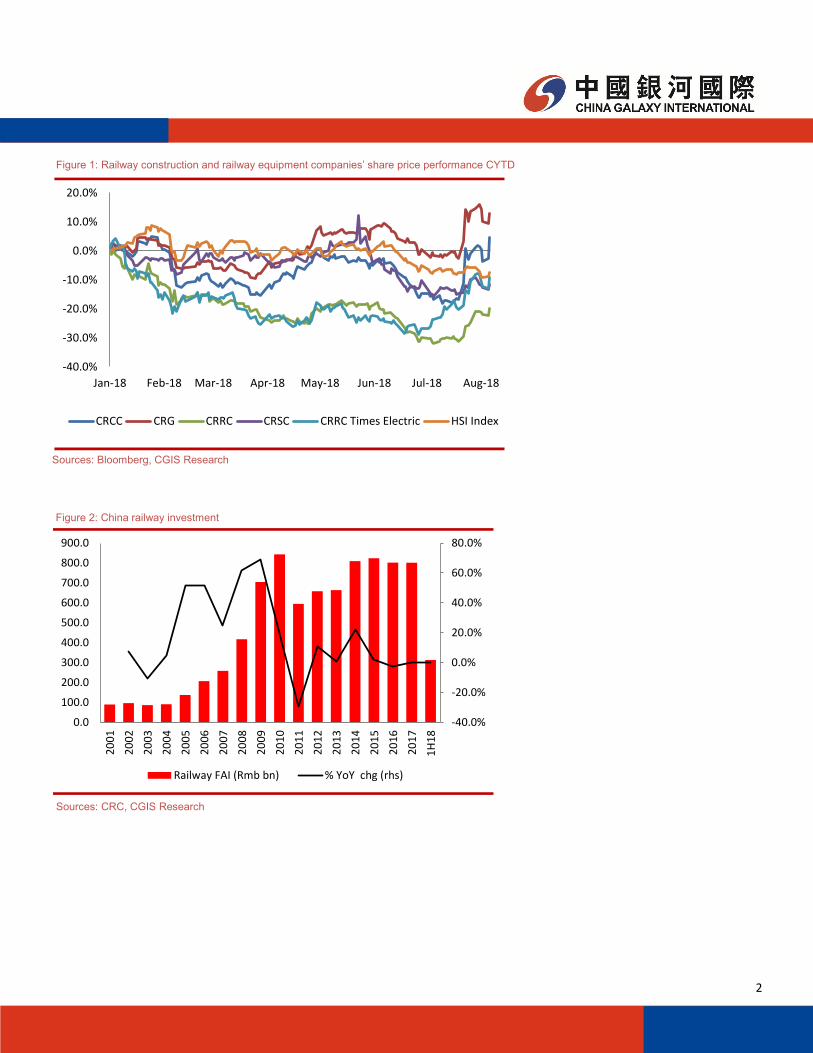

Upward trend in railway FAI expected to improve market sentiment

2018 railway FAI is likely to reach Rmb800bn, exceeding the initial full-year target of

Rmb732bn. According to some media news releases on 7 August, China’s railway FAI in

2018 is likely to reach Rmb800bn, exceeding market expectations. Under the

deleveraging environment, China Railway Corporation (CRC) set the railway investment

target for 2018 at Rmb732bn in January, implying a YoY decrease of 8.6%. Facing a

challenging environment and great uncertainties related to the US trade dispute, the

central government has decided to put more stimulus on infrastructure FAI to stabilize

economic growth and prevent a hard landing. The railway segment is the key area for

central government’s infrastructure investment boost in our view, considering railway’s

importance in resolving traffic congestion and air pollution problems and reducing logistics

costs. According to CRC data, railway investment in 1H18 reached Rmb312.7bn, which

was largely flat YoY. As railway investment accelerates, we expect railway investment to

reach no less than Rmb800bn in 2018.

New railway project starts expected to further accelerate from 2H18. Railway

investment is expected to exceed the initial full-year CRC target, driven mainly by 1)

CRC’s freight business expansion, which should boost its locomotive and freight wagon

procurement, and 2) infrastructure FAI acceleration, spurred by the central government’s

need to stimulate economic growth. CRC’s priority is railway reform to improve profitability

and reduce leverage. So it slowed down new project starts in 2016 and 2017. The two

leaders in China’s railway construction market, CRCC (1186 HK) and CRG (390 HK), saw

new contract wins in the railway sector decline for two consecutive years in 2016 and

2017. Towards the end of the 13th FYP, in 1H18, growth in railway new contract wins

recovered. We expect the central government’s support for infrastructure investment,

especially railway investment, to further accelerate new railway project starts from 2H18

on.

Increases in new line additions and railway reforms expected to boost demand

growth for the railway equipment sector. CRC’s freight business expansion is expected

to boost its locomotive and freight wagon procurement. The railway aims to grow its

freight transportation volume by 30% in 2017-2020. According to recent Caixin news, the

CRC is expected to spend over Rmb100bn to purchase 216,000 freight wagons and 3,756

locomotives in the next three years. In 2017, CRC ordered 722 locomotives and 43,048

freight wagons. The increases in new line additions are also expected to drive demand

growth for MUs in 2019-2020. Given the 13th FYP target, we expect new line additions in

2018-2020E to likely reach 7,000-8,000 km p.a., more than triple the new line additions in

2016-2017.

CRCC and CRRC (1766 HK) are our top picks in the railway sector. CRCC is our top

pick in the construction sector. After the share price rally during recent weeks, the stock is

still trading below its historical average in terms of valuation. We prefer CRCC over CRG

(390 HK) and CCC (1800 HK) because of CRCC’s stronger balance sheet. The Company

also stands to benefit more than its peers from railway investment acceleration from 2H18

onwards. In the railway equipment sector, we prefer CRRC (1766 HK). The stock is still a

laggard in terms of share price performance compared to construction companies and its

railway equipment peers. The share price has fallen about 20% CYTD. With the potential

of earnings bottoming out in 2018, there should be a re-rating opportunity for CRRC.

(Please click here for our latest note on CRCC and click here for our latest note on

CRRC.)

China railway sector

Ticker RatingPrice

(HK$)

TP

(HK$)+/-upside

CRCC 1186 HK BUY 9.73 11.60 19.2%

CRG 390 HK BUY 6.66 7.90 18.6%

CRCC 1766 HK BUY 6.96 9.10 30.7%

CRSC 3969 HK BUY 5.49 8.00 45.7%

CRRC Times 3898 HK HOLD 46.25 36.40 -21.3%

2

Figure 1: Railway construction and railway equipment companies’ share price performance CYTD

Sources: Bloomberg, CGIS Research

Figure 2: China railway investment

Sources: CRC, CGIS Research

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

1H

18

Railway FAI (Rmb bn) % YoY chg (rhs)

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18

CRCC CRG CRRC CRSC CRRC Times Electric HSI Index

3

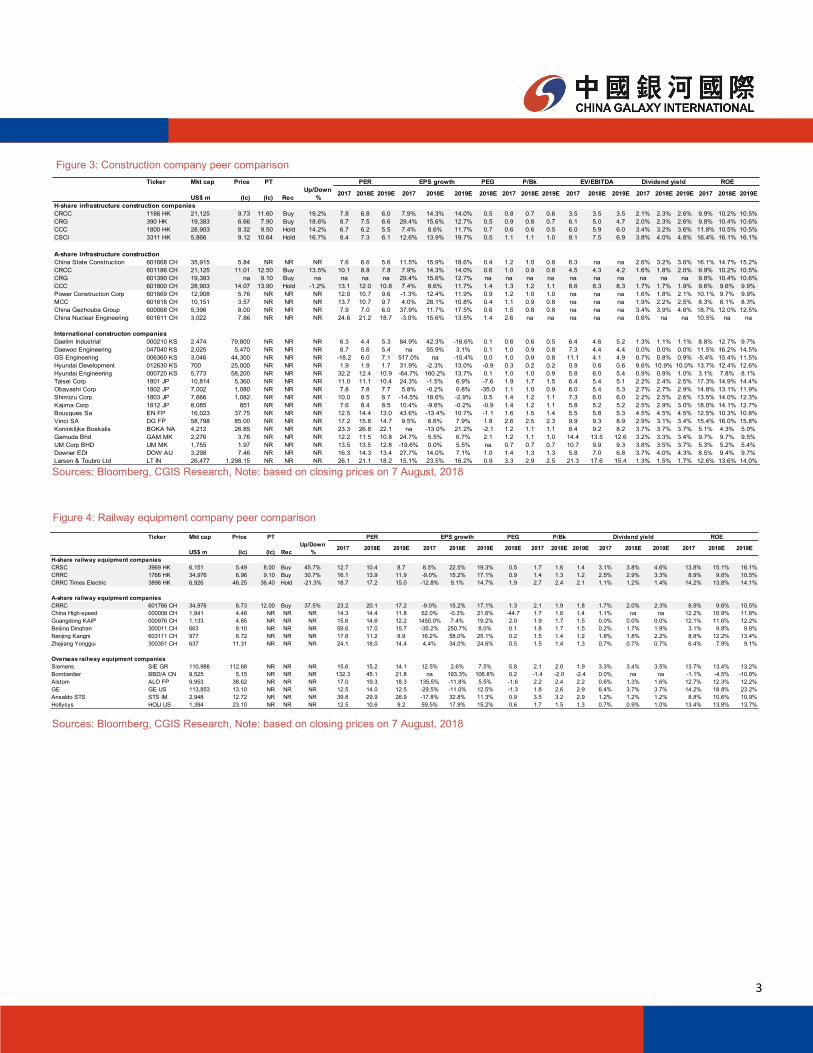

Figure 3: Construction company peer comparison

Sources: Bloomberg, CGIS Research, Note: based on closing prices on 7 August, 2018

Figure 4: Railway equipment company peer comparison

Sources: Bloomberg, CGIS Research, Note: based on closing prices on 7 August, 2018

Ticker Mkt cap Price PT PEG

US$ m (lc) (lc)

Up/Down

%2017 2018E 2019E 2017 2018E 2019E 2018E 2017 2018E 2019E 2017 2018E 2019E 2017 2018E 2019E

CRSC 3969 HK 6,151 5.49 8.00 Buy 45.7% 12.7 10.4 8.7 8.5% 22.5% 19.3% 0.5 1.7 1.6 1.4 3.1% 3.8% 4.6% 13.8% 15.1% 16.1%

CRRC 1766 HK 34,976 6.96 9.10 Buy 30.7% 16.1 13.9 11.9 -9.0% 15.2% 17.1% 0.9 1.4 1.3 1.2 2.5% 2.9% 3.3% 8.9% 9.6% 10.5%

CRRC Times Electric 3898 HK 6,926 46.25 36.40 Hold -21.3% 18.7 17.2 15.0 -12.8% 9.1% 14.7% 1.9 2.7 2.4 2.1 1.1% 1.2% 1.4% 14.2% 13.8% 14.1%

CRRC 601766 CH 34,976 8.73 12.00 Buy 37.5% 23.2 20.1 17.2 -9.0% 15.2% 17.1% 1.3 2.1 1.9 1.8 1.7% 2.0% 2.3% 8.9% 9.6% 10.5%

China High-speed 000008 CH 1,841 4.46 NR NR NR 14.3 14.4 11.8 62.0% -0.3% 21.6% -44.7 1.7 1.6 1.4 1.1% na na 12.2% 10.9% 11.8%

Guangdong KAIP 000976 CH 1,133 4.85 NR NR NR 15.6 14.6 12.2 1450.0% 7.4% 19.2% 2.0 1.9 1.7 1.5 0.0% 0.0% 0.0% 12.1% 11.6% 12.2%

Beijing Dinghan 300011 CH 663 8.10 NR NR NR 59.6 17.0 15.7 -35.2% 250.7% 8.0% 0.1 1.8 1.7 1.5 0.2% 1.7% 1.9% 3.1% 9.8% 9.8%

Nanjing Kangni 603111 CH 977 6.72 NR NR NR 17.6 11.2 8.9 16.2% 58.0% 25.1% 0.2 1.5 1.4 1.2 1.8% 1.8% 2.2% 8.8% 12.2% 13.4%

Zhejiang Yonggui 300351 CH 637 11.31 NR NR NR 24.1 18.0 14.4 4.4% 34.0% 24.6% 0.5 1.5 1.4 1.3 0.7% 0.7% 0.7% 6.4% 7.9% 9.1%

Siemens SIE GR 110,988 112.68 NR NR NR 15.6 15.2 14.1 12.5% 2.6% 7.5% 5.8 2.1 2.0 1.9 3.3% 3.4% 3.5% 13.7% 13.4% 13.2%

Bombardier BBD/A CN 9,525 5.15 NR NR NR 132.3 45.1 21.8 na 193.3% 106.8% 0.2 -1.4 -2.0 -2.4 0.0% na na -1.1% -4.5% -10.8%

Alstom ALO FP 9,953 38.62 NR NR NR 17.0 19.3 18.3 135.5% -11.8% 5.5% -1.6 2.2 2.4 2.2 0.6% 1.3% 1.6% 12.7% 12.3% 12.2%

GE GE US 113,853 13.10 NR NR NR 12.5 14.0 12.5 -29.5% -11.0% 12.5% -1.3 1.8 2.6 2.9 6.4% 3.7% 3.7% 14.2% 18.8% 23.2%

Ansaldo STS STS IM 2,948 12.72 NR NR NR 39.8 29.9 26.9 -17.8% 32.8% 11.3% 0.9 3.5 3.2 2.9 1.2% 1.2% 1.2% 8.8% 10.6% 10.9%

Hollysys HOLI US 1,394 23.10 NR NR NR 12.5 10.6 9.2 59.5% 17.9% 15.2% 0.6 1.7 1.5 1.3 0.7% 0.9% 1.0% 13.4% 13.8% 13.7%

EPS growth P/Bk Dividend yield ROE

H-share railway equipment companies

A-share railway equipment companies

Overseas railway equipment companies

Rec

PER

Ticker Mkt cap Price PT PEG

US$ m (lc) (lc)

Up/Down

%2017 2018E 2019E 2017 2018E 2019E 2018E 2017 2018E 2019E 2017 2018E 2019E 2017 2018E 2019E 2017 2018E 2019E

CRCC 1186 HK 21,125 9.73 11.60 Buy 19.2% 7.8 6.8 6.0 7.9% 14.3% 14.0% 0.5 0.8 0.7 0.6 3.5 3.5 3.5 2.1% 2.3% 2.6% 9.9% 10.2% 10.5%

CRG 390 HK 19,383 6.66 7.90 Buy 18.6% 8.7 7.5 6.6 29.4% 15.6% 12.7% 0.5 0.9 0.8 0.7 6.1 5.0 4.7 2.0% 2.3% 2.6% 9.8% 10.4% 10.6%

CCC 1800 HK 28,903 8.32 9.50 Hold 14.2% 6.7 6.2 5.5 7.4% 8.6% 11.7% 0.7 0.6 0.6 0.5 6.0 5.9 6.0 3.4% 3.2% 3.6% 11.8% 10.5% 10.5%

CSCI 3311 HK 5,866 9.12 10.64 Hold 16.7% 8.4 7.3 6.1 12.6% 13.9% 19.7% 0.5 1.1 1.1 1.0 8.1 7.5 6.9 3.8% 4.0% 4.8% 16.4% 16.1% 16.1%

China State Construction 601668 CH 35,915 5.84 NR NR NR 7.6 6.6 5.6 11.5% 15.9% 18.6% 0.4 1.2 1.0 0.8 6.3 na na 2.6% 3.2% 3.6% 16.1% 14.7% 15.2%

CRCC 601186 CH 21,125 11.01 12.50 Buy 13.5% 10.1 8.8 7.8 7.9% 14.3% 14.0% 0.6 1.0 0.9 0.8 4.5 4.3 4.2 1.6% 1.8% 2.0% 9.9% 10.2% 10.5%

CRG 601390 CH 19,383 na 9.10 Buy na na na na 29.4% 15.6% 12.7% na na na na na na na na na na 9.8% 10.4% 10.6%

CCC 601800 CH 28,903 14.07 13.90 Hold -1.2% 13.1 12.0 10.8 7.4% 8.6% 11.7% 1.4 1.3 1.2 1.1 8.6 8.3 8.3 1.7% 1.7% 1.9% 9.6% 9.6% 9.9%

Power Construction Corp 601669 CH 12,908 5.76 NR NR NR 12.0 10.7 9.6 -1.3% 12.4% 11.9% 0.9 1.2 1.0 1.0 na na na 1.6% 1.8% 2.1% 10.1% 9.7% 9.9%

MCC 601618 CH 10,151 3.57 NR NR NR 13.7 10.7 9.7 4.0% 28.1% 10.8% 0.4 1.1 0.9 0.8 na na na 1.9% 2.2% 2.5% 8.3% 8.1% 8.3%

China Gezhouba Group 600068 CH 5,396 8.00 NR NR NR 7.9 7.0 6.0 37.9% 11.7% 17.5% 0.6 1.5 0.8 0.8 na na na 3.4% 3.9% 4.6% 18.7% 12.0% 12.5%

China Nuclear Engineering 601611 CH 3,022 7.86 NR NR NR 24.6 21.2 18.7 -3.0% 15.6% 13.5% 1.4 2.6 na na na na na 0.6% na na 10.5% na na

Daelim Industrial 000210 KS 2,474 79,800 NR NR NR 6.3 4.4 5.3 84.9% 42.3% -16.6% 0.1 0.6 0.6 0.5 6.4 4.6 5.2 1.3% 1.1% 1.1% 8.8% 12.7% 9.7%

Daewoo Engineering 047040 KS 2,025 5,470 NR NR NR 8.7 5.6 5.4 na 55.9% 3.1% 0.1 1.0 0.9 0.8 7.3 4.4 4.4 0.0% 0.0% 0.0% 11.5% 16.2% 14.5%

GS Engineering 006360 KS 3,046 44,300 NR NR NR -18.2 6.0 7.1 517.0% na -15.4% 0.0 1.0 0.9 0.8 11.1 4.1 4.9 0.7% 0.8% 0.9% -5.4% 15.4% 11.5%

Hyundai Development 012630 KS 700 25,000 NR NR NR 1.9 1.9 1.7 31.9% -2.3% 13.0% -0.9 0.3 0.2 0.2 0.9 0.6 0.6 9.6% 10.9% 10.0% 13.7% 12.4% 12.6%

Hyundai Engineering 000720 KS 5,773 58,200 NR NR NR 32.2 12.4 10.9 -64.7% 160.2% 13.7% 0.1 1.0 1.0 0.9 5.8 6.0 5.4 0.9% 0.9% 1.0% 3.1% 7.8% 8.1%

Taisei Corp 1801 JP 10,814 5,360 NR NR NR 11.0 11.1 10.4 24.3% -1.5% 6.9% -7.6 1.9 1.7 1.5 6.4 5.4 5.1 2.2% 2.4% 2.5% 17.3% 14.9% 14.4%

Obayashi Corp 1802 JP 7,002 1,080 NR NR NR 7.8 7.8 7.7 5.8% -0.2% 0.8% -35.0 1.1 1.0 0.9 6.0 5.4 5.3 2.7% 2.7% 2.9% 14.8% 13.1% 11.9%

Shimizu Corp 1803 JP 7,666 1,082 NR NR NR 10.0 8.5 8.7 -14.5% 18.6% -2.9% 0.5 1.4 1.2 1.1 7.3 6.0 6.0 2.2% 2.5% 2.6% 13.5% 14.0% 12.3%

Kajima Corp 1812 JP 8,085 851 NR NR NR 7.6 8.4 8.5 10.4% -9.6% -0.2% -0.9 1.4 1.2 1.1 5.8 5.2 5.2 2.5% 2.9% 3.0% 18.0% 14.1% 12.7%

Bouygues Sa EN FP 16,023 37.75 NR NR NR 12.5 14.4 13.0 43.6% -13.4% 10.7% -1.1 1.6 1.5 1.4 5.5 5.8 5.3 4.5% 4.5% 4.5% 12.5% 10.3% 10.8%

Vinci SA DG FP 58,798 85.00 NR NR NR 17.2 15.8 14.7 9.5% 8.6% 7.9% 1.8 2.6 2.5 2.3 9.9 9.3 8.9 2.9% 3.1% 3.4% 15.4% 16.0% 15.8%

Koninklijke Boskalis BOKA NA 4,212 26.85 NR NR NR 23.3 26.8 22.1 na -13.0% 21.2% -2.1 1.2 1.1 1.1 8.4 9.2 8.2 3.7% 3.7% 3.7% 5.1% 4.3% 5.0%

Gamuda Bhd GAM MK 2,276 3.76 NR NR NR 12.2 11.5 10.8 24.7% 5.5% 6.7% 2.1 1.2 1.1 1.0 14.4 13.5 12.6 3.2% 3.3% 3.4% 9.7% 9.7% 9.5%

IJM Corp BHD IJM MK 1,755 1.97 NR NR NR 13.5 13.5 12.8 -19.6% 0.0% 5.5% na 0.7 0.7 0.7 10.7 9.9 9.3 3.8% 3.5% 3.7% 5.3% 5.2% 5.4%

Downer EDI DOW AU 3,298 7.46 NR NR NR 16.3 14.3 13.4 27.7% 14.0% 7.1% 1.0 1.4 1.3 1.3 5.8 7.0 6.8 3.7% 4.0% 4.3% 8.5% 9.4% 9.7%

Larsen & Toubro Ltd LT IN 26,477 1,298.15 NR NR NR 26.1 21.1 18.2 15.1% 23.5% 16.2% 0.9 3.3 2.9 2.5 21.3 17.6 15.4 1.3% 1.5% 1.7% 12.6% 13.6% 14.0%

H-share infrastructure construction companies

A-share infrastructure construction

International constructon companies

Rec

PER EPS growth P/Bk Dividend yield ROEEV/EBITDA

4

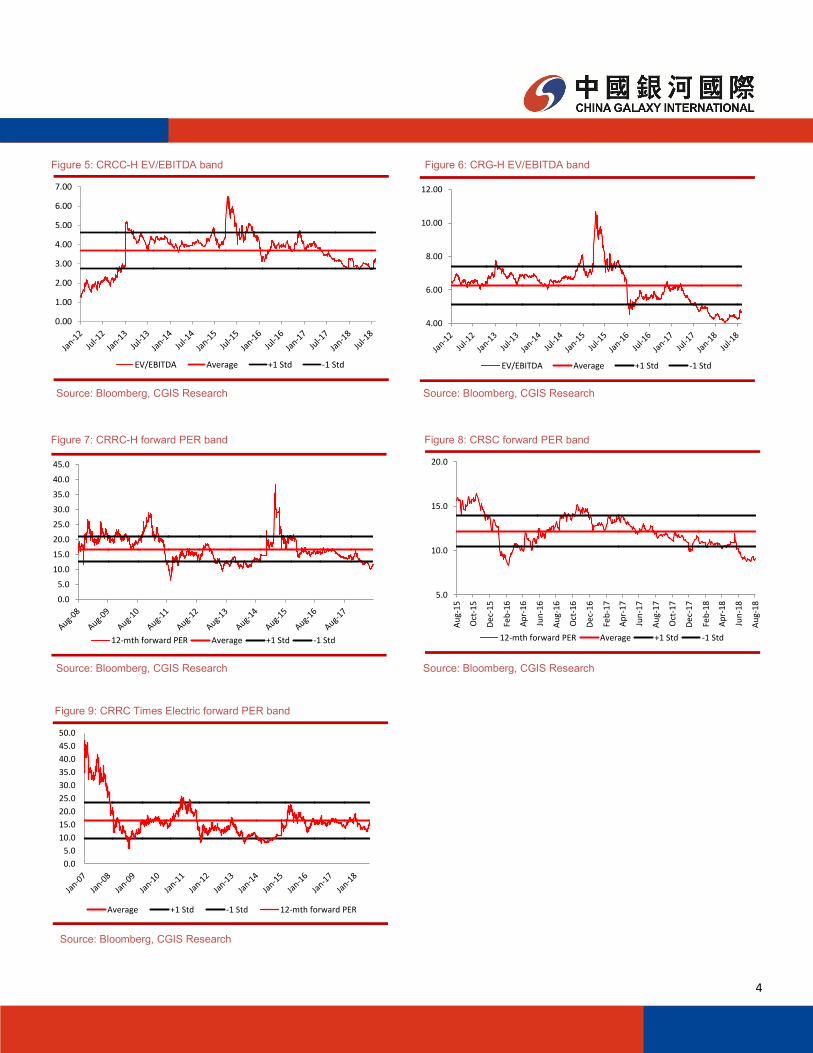

Figure 5: CRCC-H EV/EBITDA band

Source: Bloomberg, CGIS Research Source: Bloomberg, CGIS Research

Figure 6: CRG-H EV/EBITDA band

Figure 7: CRRC-H forward PER band

Source: Bloomberg, CGIS Research Source: Bloomberg, CGIS Research

Figure 8: CRSC forward PER band

Figure 9: CRRC Times Electric forward PER band

Source: Bloomberg, CGIS Research

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

EV/EBITDA Average +1 Std -1 Std

4.00

6.00

8.00

10.00

12.00

EV/EBITDA Average +1 Std -1 Std

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

12-mth forward PER Average +1 Std -1 Std

5.0

10.0

15.0

20.0A

ug-

15

Oct

-15

De

c-1

5

Feb

-16

Ap

r-1

6

Jun

-16

Au

g-1

6

Oct

-16

De

c-1

6

Feb

-17

Ap

r-1

7

Jun

-17

Au

g-1

7

Oct

-17

De

c-1

7

Feb

-18

Ap

r-1

8

Jun

-18

Au

g-1

8

12-mth forward PER Average +1 Std -1 Std

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

Average +1 Std -1 Std 12-mth forward PER

Healthcare sector– Don't throw the baby out with the bathwater

Aug 8, 2018

Analyst: Harry He ([email protected]; Tel: 852 - 3698 6320);

Wong Chi Man, CFA, Head of research ([email protected]; Tel: (852) 3689 6317)

Healthcare stocks started correcting in early June, prior to the vaccine incident and the movie Dying to survive, which caused wide public reaction. We believe recent pressure on the healthcare sector is due to a combination of 1) profit-taking after a re-rating since 2017 (especially for the leading players); 2) the vaccine incident, together with the movie, which ex-posed long-existing problems in China’s medical system once again, i.e. quality regulations, high drug prices, and a high marketing and selling expenses to revenue ratio; and 3) about 6% depreciation in the RMB since early June. The aim of this report is to throw some light on the healthcare sector investment thesis in this market environment and identify possible bottom-fishing opportunities for investors. We comprehensively address the stocks in three areas, screening for candidates that meet the following three criteria: 1) they fundamentally comply with government policy direction and have solid visible prospects; 2) they fit into the current investor appetite of having exposure to international certificates, international collabo-ration, exports or foreign R&D pipelines, etc., which strengthens investors' faith in the Company’s overall quality, credibility and trustworthiness; and 3) they have a relatively attractive valuation after the correction. Following this stock screening logic, our preferred stocks in the current market are CTCM [570.hk], Shanghai Pharm [2607.hk], Genscript [1548.hk] and CSPC [1093.hk]. We believe the argument about a structural de-rating is overly bearish, as some key reasons to invest in the sector remain intact. For example, it is largely immune from the impact of the trade dispute, and the leading players have strong cash flow and balance sheets. Vaccine incident more of a company-specific issue The sector correction started in early June, prior to the movie Dying to survive and the vaccine incident. The correction of the Hang Seng Index since early June triggered some profit-taking, as the sector had been re-rated since 2017, and the movie and the vaccine incident subsequently led to more sell-offs. But we believe the vaccine incident is company specific and fundamentally, we should not turn negative towards the whole sector, as 1) CFDA’s drug review standards are benchmarking the FDA; 2) we have seen many do-mestic players filing international NDAs and performing international multi-centre clinical trials; 3) GMP regulation will become more and more stringent, and government policy is calling for industry consolidation by encouraging the introduction of imported innovative drugs to stimulate the consolidation of innovative domestic players through chemical generics consistency and efficacy evaluation to push generics consolidation, etc. In the long term, Industry consolidation will squeeze out relatively inferior players; 4) investors have long been aware of high drug prices and the fact that the government is always calling for ASP price cuts (e.g. national NRDL negoti-ations); and 5) the whole medical system in China is still under reform (stricter regulation, GMP certificates and regular checks, zero price mark-up, and increasing physicians’ salaries to reduce the possibility of bribery and corruption. Reforms have touched on the sensitive and stubborn problems in China’s healthcare system, and they are on the right track, so we should give them more time.

We agree that investors may become more prudent in picking stock. Investors may prefer names with qualified proven standards. Following this logic, we screened out the following names:

CTCM [570.hk], whose CCMG is exported to Germany, so German officials come to investigate its production facilities regular-

ly.

Distributors Shanghai Pharm [2607.hk], as there is strong demand for pharmaceutical logistics, which are not impacted by the

vaccine incident. If capital flows out from the leading manufacturers and funds have to maintain a certain position in the healthcare sector as part of their strategic allocation, then distributors may be their best choice.

Drug manufacturers that have drug filings with the U.S. ANDA or have sales in foreign countries, including CSPC [1093.hk],

which has a strong U.S. ANDA pipeline, Luye [2186.hk], which has U.S. 505(b)2 filings with drugs such as Risperidone, Genscript [1548.hk], whose CAR-T targeting BCMA published its clinical trial results at the U.S. oncology summit, leading China CRO Wuxi [2269.hk], which has foreign clients and whose WX cGMP meets FDA standards, and CMS [867.hk], which sells im-ported drugs.

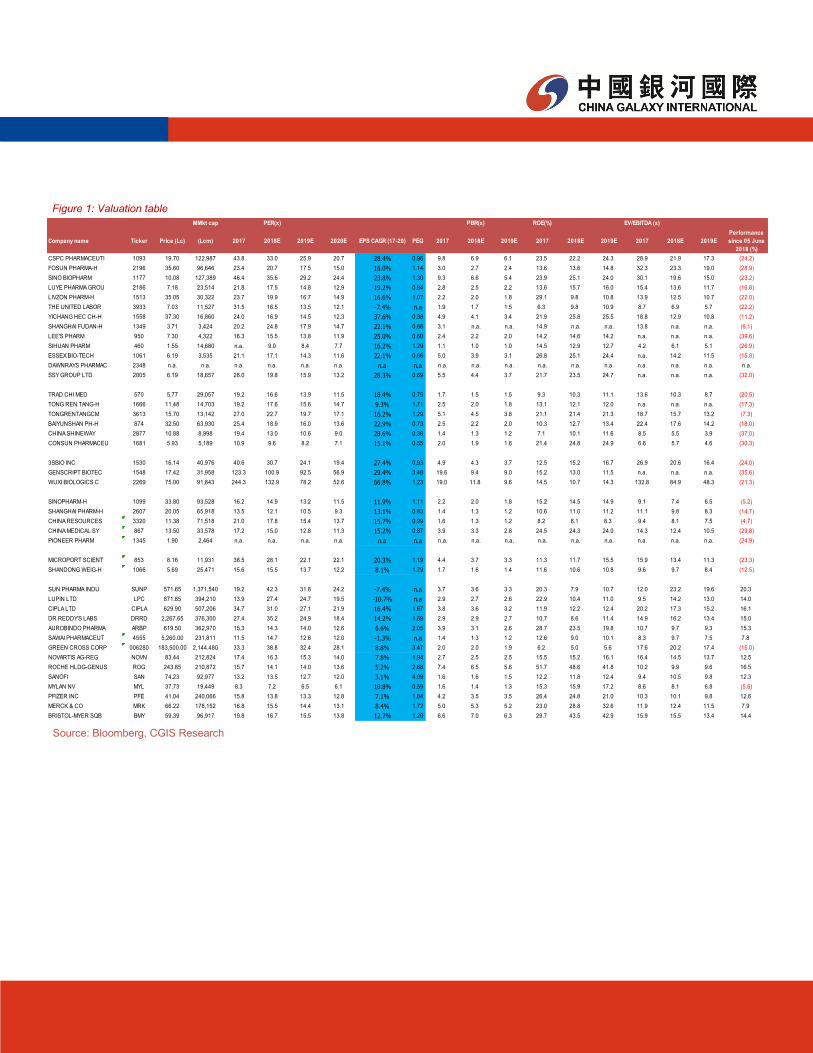

Figure 1: Valuation table MMkt cap ROE(%) EV/EBITDA (x)

Company name Ticker Price (Lc) (Lcm) 2017 2018E 2019E 2020E EPS CAGR (17-20) PEG 2017 2018E 2019E 2017 2018E 2019E 2017 2018E 2019E

Performance

since 05 June

2018 (%)

CSPC PHARMACEUTI 1093 19.70 122,987 43.8 33.0 25.9 20.7 28.4% 0.96 9.8 6.9 6.1 23.5 22.2 24.3 28.9 21.9 17.3 (24.2)

FOSUN PHARMA-H 2196 35.60 96,646 23.4 20.7 17.5 15.0 16.0% 1.14 3.0 2.7 2.4 13.6 13.6 14.8 32.3 23.3 19.0 (28.9)

SINO BIOPHARM 1177 10.08 127,389 46.4 35.6 29.2 24.4 23.8% 1.30 9.3 6.6 5.4 23.9 25.1 24.0 30.1 19.6 15.0 (23.2)

LUYE PHARMA GROU 2186 7.18 23,514 21.8 17.5 14.8 12.9 19.2% 0.84 2.8 2.5 2.2 13.6 15.7 16.0 15.4 13.6 11.7 (16.8)

LIVZON PHARM-H 1513 35.05 30,322 23.7 19.9 16.7 14.9 16.6% 1.07 2.2 2.0 1.8 29.1 9.8 10.8 13.9 12.5 10.7 (22.0)

THE UNITED LABOR 3933 7.03 11,527 31.5 16.5 13.5 12.1 -7.4% n.a 1.9 1.7 1.5 6.3 9.8 10.9 8.7 6.9 5.7 (22.2)

YICHANG HEC CH-H 1558 37.30 16,860 24.0 16.9 14.5 12.3 37.6% 0.38 4.9 4.1 3.4 21.9 25.8 25.5 18.8 12.9 10.8 (11.2)

SHANGHAI FUDAN-H 1349 3.71 3,424 20.2 24.8 17.9 14.7 22.1% 0.66 3.1 n.a. n.a. 14.9 n.a. n.a. 13.8 n.a. n.a. (6.1)

LEE'S PHARM 950 7.30 4,322 16.3 15.5 13.8 11.9 25.0% 0.60 2.4 2.2 2.0 14.2 14.6 14.2 n.a. n.a. n.a. (39.6)

SIHUAN PHARM 460 1.55 14,680 n.a. 9.0 8.4 7.7 16.2% 1.29 1.1 1.0 1.0 14.5 12.9 12.7 4.2 6.1 5.1 (26.9)

ESSEX BIO-TECH 1061 6.19 3,535 21.1 17.1 14.3 11.6 22.1% 0.66 5.0 3.9 3.1 26.8 25.1 24.4 n.a. 14.2 11.5 (15.8)

DAWNRAYS PHARMAC 2348 n.a. n.a. n.a. n.a. n.a. n.a. n.a n.a n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.

SSY GROUP LTD 2005 6.19 18,657 28.0 19.8 15.9 13.2 28.3% 0.69 5.5 4.4 3.7 21.7 23.5 24.7 n.a. n.a. n.a. (32.0)

TRAD CHI MED 570 5.77 29,057 19.2 16.6 13.9 11.5 18.4% 0.75 1.7 1.5 1.5 9.3 10.3 11.1 13.6 10.3 8.7 (20.5)

TONG REN TANG-H 1666 11.48 14,703 19.2 17.6 15.6 14.7 9.3% 1.71 2.5 2.0 1.8 13.1 12.1 12.0 n.a. n.a. n.a. (17.3)

TONGRENTANGCM 3613 15.70 13,142 27.0 22.7 19.7 17.1 16.2% 1.29 5.1 4.5 3.8 21.1 21.4 21.3 18.7 15.7 13.2 (7.3)

BAIYUNSHAN PH-H 874 32.50 63,930 25.4 18.9 16.0 13.6 22.9% 0.73 2.5 2.2 2.0 10.3 12.7 13.4 22.4 17.6 14.2 (18.0)

CHINA SHINEWAY 2877 10.88 8,998 19.4 13.0 10.6 9.0 28.6% 0.36 1.4 1.3 1.2 7.1 10.1 11.6 8.5 5.5 3.9 (37.0)

CONSUN PHARMACEU 1681 5.93 5,189 10.9 9.6 8.2 7.1 15.1% 0.55 2.0 1.9 1.6 21.4 24.8 24.9 6.6 5.7 4.6 (30.3)

3SBIO INC 1530 16.14 40,976 40.6 30.7 24.1 19.4 27.4% 0.93 4.9 4.3 3.7 12.5 15.2 16.7 26.9 20.6 16.4 (24.0)

GENSCRIPT BIOTEC 1548 17.42 31,958 123.3 100.9 92.5 56.9 29.4% 3.48 19.6 9.4 9.0 15.2 13.0 11.5 n.a. n.a. n.a. (35.6)

WUXI BIOLOGICS C 2269 75.00 91,843 244.3 132.9 78.2 52.6 66.8% 1.23 19.0 11.8 9.6 14.5 10.7 14.3 132.8 84.9 48.3 (21.3)

SINOPHARM-H 1099 33.80 93,528 16.2 14.9 13.2 11.5 11.9% 1.11 2.2 2.0 1.8 15.2 14.5 14.9 9.1 7.4 6.5 (5.2)

SHANGHAI PHARM-H 2607 20.05 65,918 13.5 12.1 10.5 9.3 13.1% 0.83 1.4 1.3 1.2 10.6 11.0 11.2 11.1 9.8 8.3 (14.7)

CHINA RESOURCES 3320 11.38 71,518 21.0 17.8 15.4 13.7 15.7% 0.99 1.6 1.3 1.2 8.2 8.1 8.3 9.4 8.1 7.5 (4.7)

CHINA MEDICAL SY 867 13.50 33,578 17.2 15.0 12.8 11.3 15.2% 0.87 3.9 3.3 2.8 24.5 24.3 24.0 14.3 12.4 10.5 (29.8)

PIONEER PHARM 1345 1.90 2,464 n.a. n.a. n.a. n.a. n.a n.a n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a. (24.9)

MICROPORT SCIENT 853 8.16 11,931 38.5 28.1 22.1 22.1 20.3% 1.19 4.4 3.7 3.3 11.3 11.7 15.5 15.9 13.4 11.3 (23.3)

SHANDONG WEIG-H 1066 5.69 25,471 15.6 15.5 13.7 12.2 8.1% 1.79 1.7 1.6 1.4 11.6 10.6 10.8 9.6 9.7 8.4 (12.5)

SUN PHARMA INDU SUNP 571.65 1,371,540 19.2 42.3 31.8 24.2 -7.4% n.a 3.7 3.6 3.3 20.3 7.9 10.7 12.0 23.2 19.6 20.3

LUPIN LTD LPC 871.85 394,210 13.9 27.4 24.7 19.5 -10.7% n.a 2.9 2.7 2.6 22.9 10.4 11.0 9.5 14.2 13.0 14.0

CIPLA LTD CIPLA 629.90 507,206 34.7 31.0 27.1 21.9 16.4% 1.67 3.8 3.6 3.2 11.9 12.2 12.4 20.2 17.3 15.2 16.1

DR REDDY'S LABS DRRD 2,267.65 376,300 27.4 35.2 24.9 18.4 14.2% 1.69 2.9 2.9 2.7 10.7 8.6 11.4 14.9 16.2 13.4 15.0

AUROBINDO PHARMA ARBP 619.50 362,970 15.3 14.3 14.0 12.6 6.6% 2.05 3.9 3.1 2.6 28.7 23.5 19.8 10.7 9.7 9.3 15.3

SAWAI PHARMACEUT 4555 5,260.00 231,811 11.5 14.7 12.6 12.0 -1.3% n.a 1.4 1.3 1.2 12.6 9.0 10.1 8.3 9.7 7.5 7.8

GREEN CROSS CORP 006280 183,500.00 2,144,480 33.3 38.8 32.4 28.1 8.8% 3.47 2.0 2.0 1.9 6.2 5.0 5.6 17.6 20.2 17.4 (15.0)

NOVARTIS AG-REG NOVN 83.44 212,824 17.4 16.3 15.3 14.0 7.8% 1.94 2.7 2.5 2.5 15.5 15.2 16.1 16.4 14.5 13.7 12.5

ROCHE HLDG-GENUS ROG 243.85 210,872 15.7 14.1 14.0 13.6 5.2% 2.68 7.4 6.5 5.6 51.7 48.6 41.8 10.2 9.9 9.6 16.5

SANOFI SAN 74.23 92,977 13.2 13.5 12.7 12.0 3.1% 4.09 1.6 1.6 1.5 12.2 11.8 12.4 9.4 10.5 9.8 12.3

MYLAN NV MYL 37.73 19,449 8.3 7.2 6.5 6.1 10.8% 0.59 1.6 1.4 1.3 15.3 15.9 17.2 8.6 8.1 6.8 (5.6)

PFIZER INC PFE 41.04 240,066 15.8 13.8 13.3 12.8 7.1% 1.84 4.2 3.5 3.5 26.4 24.8 21.0 10.3 10.1 9.8 12.6

MERCK & CO MRK 66.22 178,152 16.8 15.5 14.4 13.1 8.4% 1.72 5.0 5.3 5.2 23.0 28.8 32.6 11.9 12.4 11.5 7.9

BRISTOL-MYER SQB BMY 59.39 96,917 19.8 16.7 15.5 13.8 12.7% 1.20 6.6 7.0 6.3 29.7 43.5 42.9 15.9 15.5 13.4 14.4

PER(x) PBR(x)

Source: Bloomberg, CGIS Research

Valuation To review the healthcare sector valuation in depth, we divided healthcare names into several sub-sectors, and in each sub-sector, we

chose representative proxies. We conducted a valuation review from both a relative premium to the healthcare sector and the absolute

PEG angle.

Chemicals representatives: CSPC [1093.hk], Luye [2186.hk], Lee’s [950.hk], SinoBio [1177.hk], Livzon [1513.hk], Fosun

[2196.hk], TUL [3933.hk], HEC [1558.hk] and SSY [2005.hk]

Leading bio names: 3SBio [1530.hk], Genscript [1548.hk.hk] and Wuxi [2269.hk]

Proxies for Chinese Traditional Medicine: CTCM [570.hk], Consun [1681.hk], TongRenTangCM [3613.hk], TongRenTang

[1666.hk], BaiYunShan [874.hk] and ShineWay [2877.hk]

Distributors: SinoPharm [1099.hk], Shanghai Pharm [2607.hk], CR Pharm [3320.hk] and CMS [867.hk]

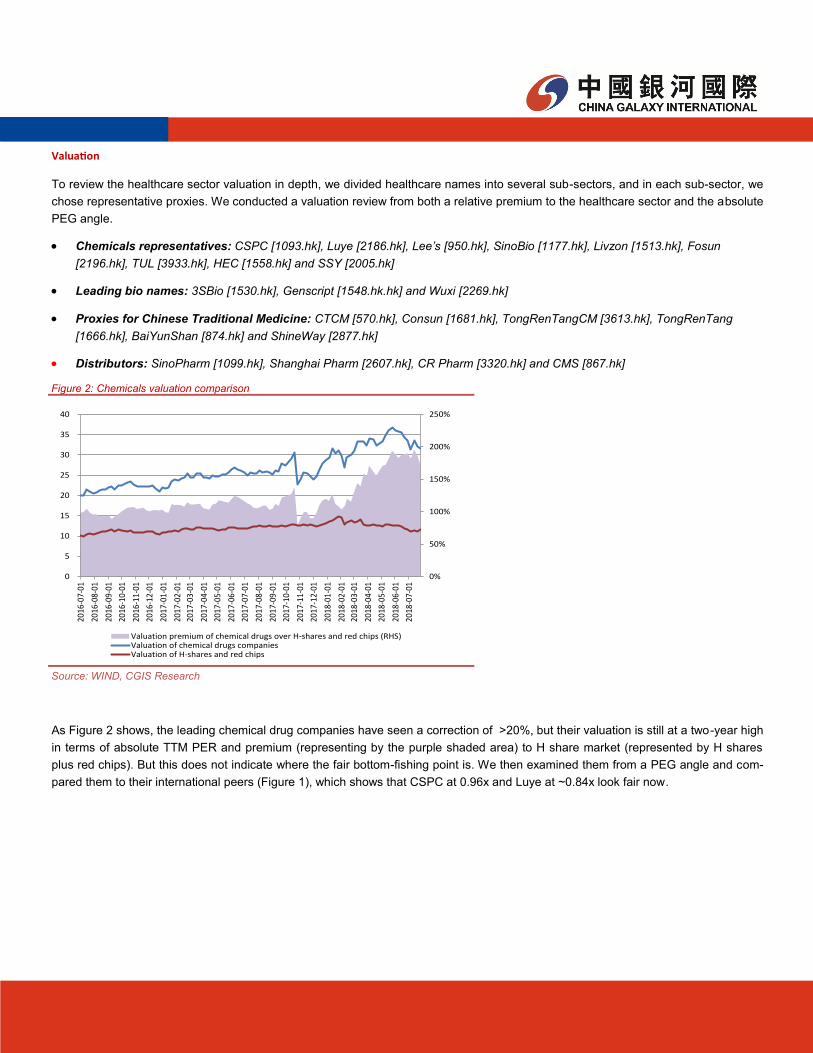

As Figure 2 shows, the leading chemical drug companies have seen a correction of >20%, but their valuation is still at a two-year high

in terms of absolute TTM PER and premium (representing by the purple shaded area) to H share market (represented by H shares

plus red chips). But this does not indicate where the fair bottom-fishing point is. We then examined them from a PEG angle and com-

pared them to their international peers (Figure 1), which shows that CSPC at 0.96x and Luye at ~0.84x look fair now.

Figure 2: Chemicals valuation comparison

0%

50%

100%

150%

200%

250%

0

5

10

15

20

25

30

35

40

2016

-07-

01

2016

-08-

01

2016

-09-

01

2016

-10-

01

2016

-11-

01

2016

-12-

01

2017

-01-

01

2017

-02-

01

2017

-03-

01

2017

-04-

01

2017

-05-

01

2017

-06-

01

2017

-07-

01

2017

-08-

01

2017

-09-

01

2017

-10-

01

2017

-11-

01

2017

-12-

01

2018

-01-

01

2018

-02-

01

2018

-03-

01

2018

-04-

01

2018

-05-

01

2018

-06-

01

2018

-07-

01

Valuation premium of chemical drugs over H-shares and red chips (RHS)Valuation of chemical drugs companiesValuation of H-shares and red chips

Source: WIND, CGIS Research

Figure 3: Bio proxy

Sources: WIND, CGIS research

TTM PER is not a good indicator for the valuation of bio firms, especially Genscript and Wuxi Bio, whose main value lies several years

in the future.

Genscript [1548.hk] valuation from CGIS research: Multiple Myeloma’s (MM) incidence rate is ~2-3/100,000 in China and ~4-

5/100,000 in the U.S., i.e. ~30,000 patients a year in China and 15,000 in the U.S. With the expected life span of ~5 years for MM

patients, the total market size of MM in China and the U.S could be ~150,000 and 75,000 patients, respectively. If we assume it pene-

trates 10% of patients in China (considering GS’s first mover advantage in BCMA target in China, other domestic players such as AN-

KE Bio (300009.CH) and Galaxy Bio (000806.CH) focus mainly on CD19 protein target) and 5% of patients in the U.S. because of its

price advantage (GS is likely to price its BCMA target CAR-T at ~RMB500,000 or ~1/6 of Novartis’ KYMRIAH), GS’s CART could treat

~19,000 patients/year overall, generating total revenue of about RMB9.5bn (~half of the market expectation for JUNO’s CD19 CAR-T

peak sales of ~US$3bn). Assuming a 30% profit margin, this would generate profit of about RMB2.9bn in ~2023 (assuming a launch

in 2019 and peak sales for four years) or ~RMB1.7bn in 2018 in terms of present value if we use a discount rate of 10%. If we give

CAR-T a 25x PER (comparable to H-market leading innovative drug manufacturers and consider the current market healthcare valua-

tion pressure and RMB depreciation) for 2018, GS’s CAR-T is worth HK$49bn or ~HK$28/share.

In summary, GS’s CAR-T potential valuation should be ~HK$30.5/share, including existing CRO business worth ~HK$2.5/share (the

15x 2018E Bloomberg consensus PER, 15x multiple is justified by its expected existing CRO business’s mid- to high-teen growth), we

estimate that the fair value for GS lies at HK$30.5/share, implying ~60% upside. The Company has already announced a share buy-

back plan of up to HK$700m, or about 4% of its free float.

Wuxi [2269.hk] valuation by CGIS research: There is no direct comparison to WX in the H-share/red chip market. The market’s

near-term horizon EPS forecasts for 2017-2019E CAGR vary widely, ranging from 68% to 100% (excluding one exceptionally low

outlier), while in the relative medium term of 2017-2020E, the EPS CAGR fluctuation tends to narrow, ranging from 68% to 74%. Our

view is that in the near term due to high uncertainty related to biologics R&D, WX’s earnings can be affected by many factors, such as

new contracted customers’ upfront fees and milestone fees associated with the progression of early stage projects to later stages. The

main growth driver for strong 2018 growth is expected to be milestone fees from project progression and new contract services fees.

In the medium to longer term, we expect to see a reduction in its earnings fluctuation, with gradual convergence with the China biolog-

ics industry growth rate of ~35% (China’s biologics market is expected to grow at a CAGR of 34.8% in 2016-2021, reaching

RMB9.2bn in 2021). Also, in the medium to long term, more and more stable commercialized CMO revenue will help mitigate WX

earnings’ fluctuation. Currently, its valuation is ~1.2x PEG, but this may not be excessive, given 1) WX’s efficient operations (~4

weeks from contract signing to CRO commencement vs. the industry average of 16-24 weeks) and proven biologics R&D technology;

2) WX’s cGMP meeting FDA standards, which deserves a valuation premium; 3) the scarcity of CDMOs targets in the H-share market;

and 4) the potential upside to earnings, given WX’s proved contract-lock historical track record and plentiful order backlog. In the cur-

rent market environment, there may be relatively limited further upside room from a valuation perspective.

0%

200%

400%

600%

800%

1000%

1200%

1400%

0

20

40

60

80

100

120

140

160

180

200

2016

-07-

01

2016

-08-

01

2016

-09-

01

2016

-10-

01

2016

-11-

01

2016

-12-

01

2017

-01-

01

2017

-02-

01

2017

-03-

01

2017

-04-

01

2017

-05-

01

2017

-06-

01

2017

-07-

01

2017

-08-

01

2017

-09-

01

2017

-10-

01

2017

-11-

01

2017

-12-

01

2018

-01-

01

2018

-02-

01

2018

-03-

01

2018

-04-

01

2018

-05-

01

2018

-06-

01

2018

-07-

01

Valuation premium of bio firms over H-shares and red chips (RHS)Valuation of bio firmsValuation of H-shares and red chips

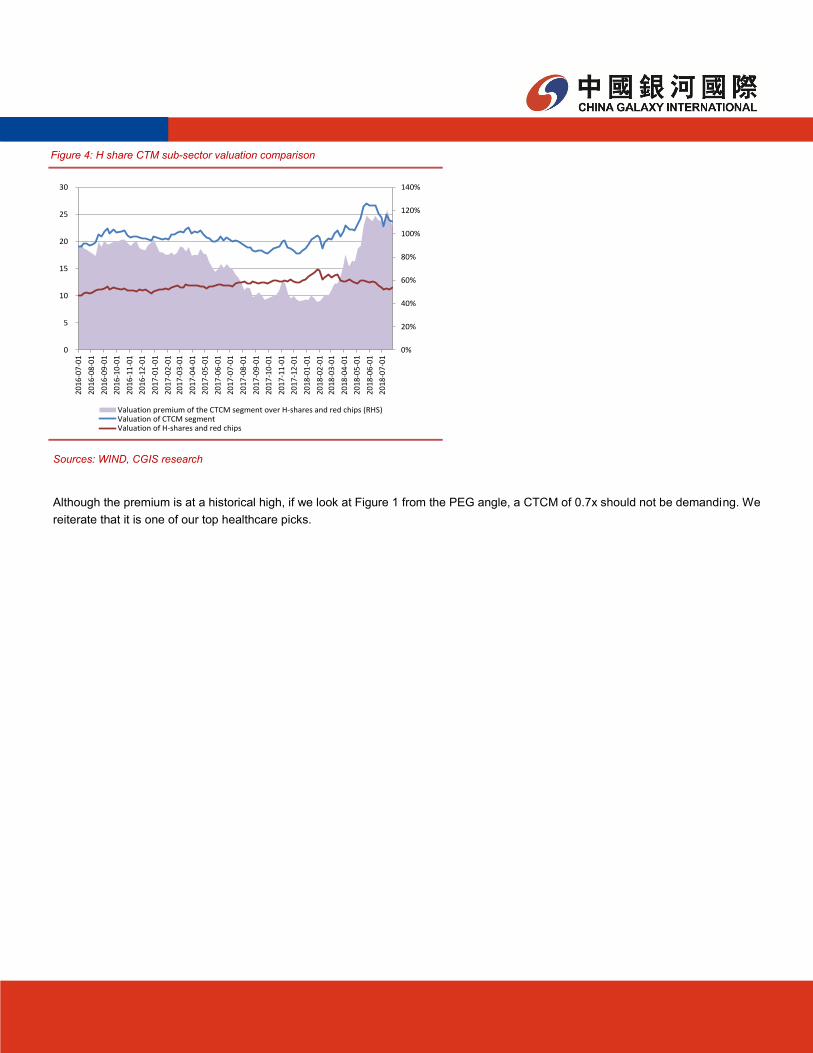

Although the premium is at a historical high, if we look at Figure 1 from the PEG angle, a CTCM of 0.7x should not be demanding. We

reiterate that it is one of our top healthcare picks.

Figure 4: H share CTM sub-sector valuation comparison

Sources: WIND, CGIS research

0%

20%

40%

60%

80%

100%

120%

140%

0

5

10

15

20

25

30

2016

-07-

01

2016

-08-

01

2016

-09-

01

2016

-10-

01

2016

-11-

01

2016

-12-

01

2017

-01-

01

2017

-02-

01

2017

-03-

01

2017

-04-

01

2017

-05-

01

2017

-06-

01

2017

-07-

01

2017

-08-

01

2017

-09-

01

2017

-10-

01

2017

-11-

01

2017

-12-

01

2018

-01-

01

2018

-02-

01

2018

-03-

01

2018

-04-

01

2018

-05-

01

2018

-06-

01

2018

-07-

01

Valuation premium of the CTCM segment over H-shares and red chips (RHS)Valuation of CTCM segmentValuation of H-shares and red chips

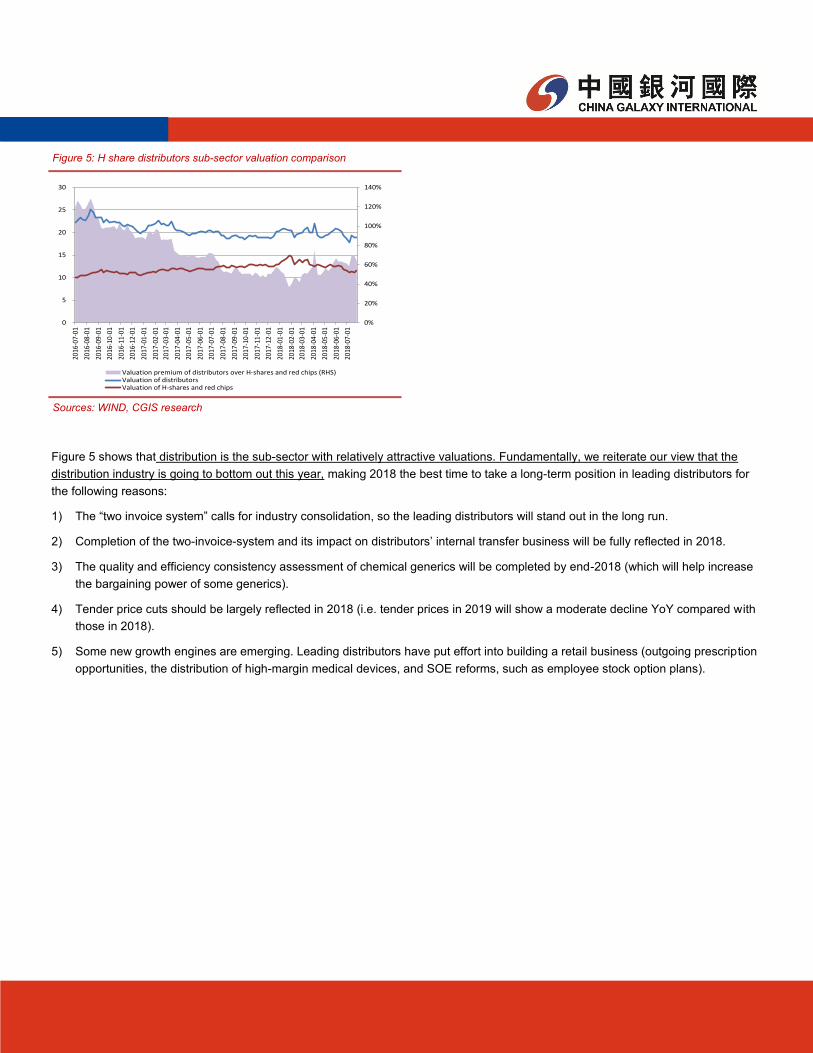

Figure 5 shows that distribution is the sub-sector with relatively attractive valuations. Fundamentally, we reiterate our view that the

distribution industry is going to bottom out this year, making 2018 the best time to take a long-term position in leading distributors for

the following reasons:

1) The “two invoice system” calls for industry consolidation, so the leading distributors will stand out in the long run.

2) Completion of the two-invoice-system and its impact on distributors’ internal transfer business will be fully reflected in 2018.

3) The quality and efficiency consistency assessment of chemical generics will be completed by end-2018 (which will help increase

the bargaining power of some generics).

4) Tender price cuts should be largely reflected in 2018 (i.e. tender prices in 2019 will show a moderate decline YoY compared with

those in 2018).

5) Some new growth engines are emerging. Leading distributors have put effort into building a retail business (outgoing prescription

opportunities, the distribution of high-margin medical devices, and SOE reforms, such as employee stock option plans).

Figure 5: H share distributors sub-sector valuation comparison

Sources: WIND, CGIS research

0%

20%

40%

60%

80%

100%

120%

140%

0

5

10

15

20

25

30

2016

-07-

01

2016

-08-

01

2016

-09-

01

2016

-10-

01

2016

-11-

01

2016

-12-

01

2017

-01-

01

2017

-02-

01

2017

-03-

01

2017

-04-

01

2017

-05-

01

2017

-06-

01

2017

-07-

01

2017

-08-

01

2017

-09-

01

2017

-10-

01

2017

-11-

01

2017

-12-

01

2018

-01-

01

2018

-02-

01

2018

-03-

01

2018

-04-

01

2018

-05-

01

2018

-06-

01

2018

-07-

01

Valuation premium of distributors over H-shares and red chips (RHS)Valuation of distributorsValuation of H-shares and red chips

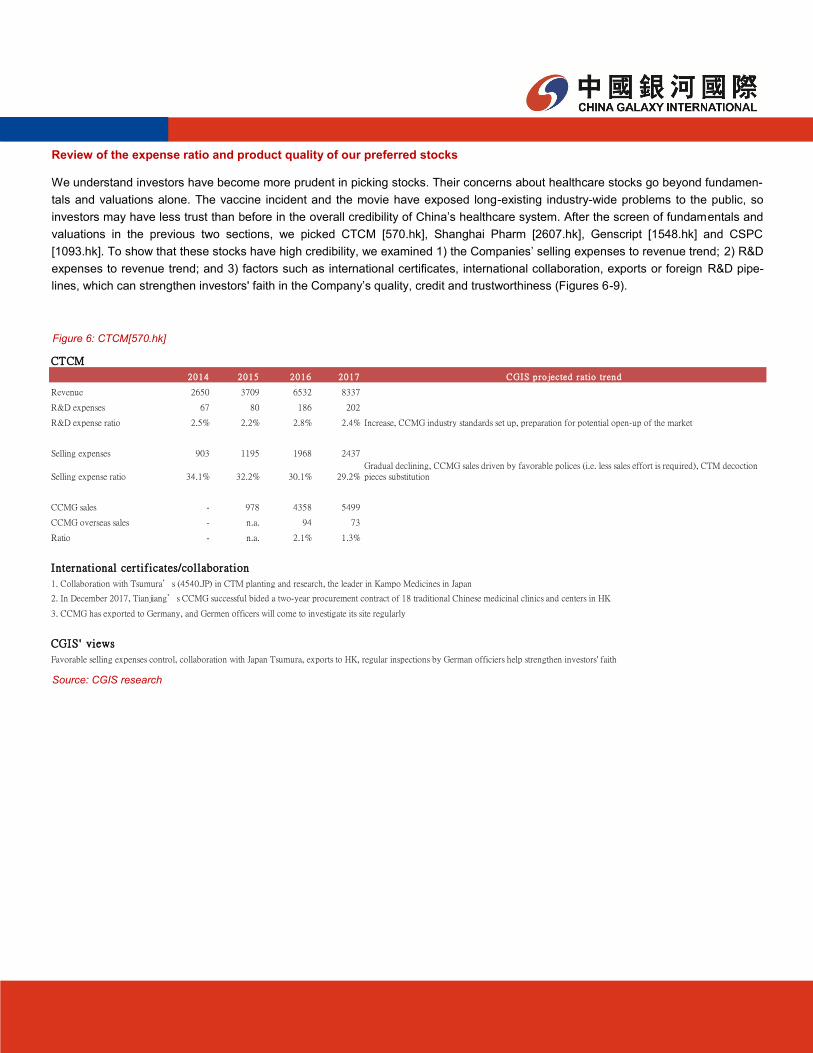

Review of the expense ratio and product quality of our preferred stocks We understand investors have become more prudent in picking stocks. Their concerns about healthcare stocks go beyond fundamen-

tals and valuations alone. The vaccine incident and the movie have exposed long-existing industry-wide problems to the public, so

investors may have less trust than before in the overall credibility of China’s healthcare system. After the screen of fundamentals and

valuations in the previous two sections, we picked CTCM [570.hk], Shanghai Pharm [2607.hk], Genscript [1548.hk] and CSPC

[1093.hk]. To show that these stocks have high credibility, we examined 1) the Companies’ selling expenses to revenue trend; 2) R&D

expenses to revenue trend; and 3) factors such as international certificates, international collaboration, exports or foreign R&D pipe-

lines, which can strengthen investors' faith in the Company’s quality, credit and trustworthiness (Figures 6-9).

Figure 6: CTCM[570.hk]

Source: CGIS research

CTCM

2014 2015 2016 2017 CGIS p ro jected ratio trend

Revenue 2650 3709 6532 8337

R&D expenses 67 80 186 202

R&D expense ratio 2.5% 2.2% 2.8% 2.4% Increase, CCMG industry standards set up, preparation for potential open-up of the market

Selling expenses 903 1195 1968 2437

Selling expense ratio 34.1% 32.2% 30.1% 29.2%Gradual declining, CCMG sales driven by favorable polices (i.e. less sales effort is required), CTM decoctionpieces substitution

CCMG sales - 978 4358 5499

CCMG overseas sales - n.a. 94 73

Ratio - n.a. 2.1% 1.3%

International certif icates/collaboration

1. Collaboration with Tsumura’s (4540.JP) in CTM planting and research, the leader in Kampo Medicines in Japan

2. In December 2017, Tianjiang’s CCMG successful bided a two-year procurement contract of 18 traditional Chinese medicinal clinics and centers in HK

3. CCMG has exported to Germany, and Germen officers will come to investigate its site regularly

CGIS' views

Favorable selling expenses control, collaboration with Japan Tsumura, exports to HK, regular inspections by German officiers help strengthen investors' faith

Figure 8: Genscript[1548.hk]

Source: CGIS research

Source: CGIS research

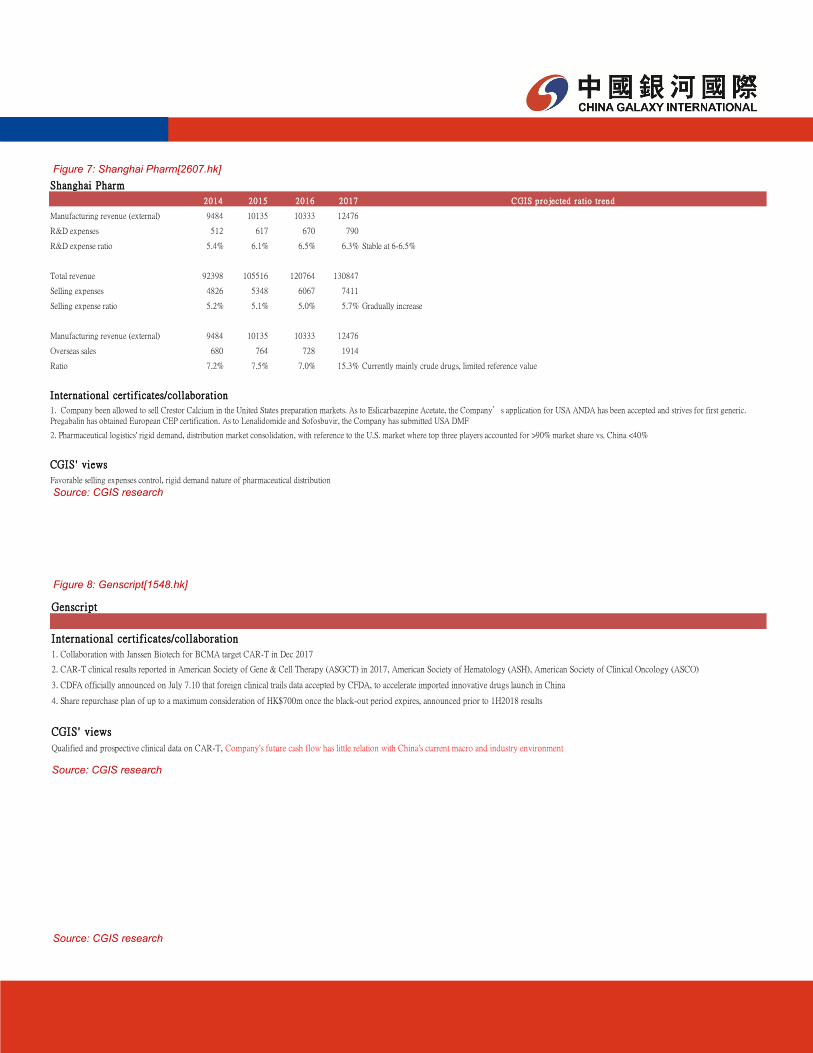

Figure 7: Shanghai Pharm[2607.hk]

Source: CGIS research

Shanghai Pharm

2014 2015 2016 2017 CGIS p ro jected ratio trend

Manufacturing revenue (external) 9484 10135 10333 12476

R&D expenses 512 617 670 790

R&D expense ratio 5.4% 6.1% 6.5% 6.3% Stable at 6-6.5%

Total revenue 92398 105516 120764 130847

Selling expenses 4826 5348 6067 7411

Selling expense ratio 5.2% 5.1% 5.0% 5.7% Gradually increase

Manufacturing revenue (external) 9484 10135 10333 12476

Overseas sales 680 764 728 1914

Ratio 7.2% 7.5% 7.0% 15.3% Currently mainly crude drugs, limited reference value

International certif icates/collaboration

2. Pharmaceutical logistics' rigid demand, distribution market consolidation, with reference to the U.S. market where top three players accounted for >90% market share vs. China <40%

CGIS' views

Favorable selling expenses control, rigid demand nature of pharmaceutical distribution

1. Company been allowed to sell Crestor Calcium in the United States preparation markets. As to Eslicarbazepine Acetate, the Company’s application for USA ANDA has been accepted and strives for first generic.Pregabalin has obtained European CEP certification. As to Lenalidomide and Sofosbuvir, the Company has submitted USA DMF

Genscript

International certif icates/collaboration

1. Collaboration with Janssen Biotech for BCMA target CAR-T in Dec 2017

2. CAR-T clinical results reported in American Society of Gene & Cell Therapy (ASGCT) in 2017, American Society of Hematology (ASH), American Society of Clinical Oncology (ASCO)

3. CDFA officially announced on July 7.10 that foreign clinical trails data accepted by CFDA, to accelerate imported innovative drugs launch in China

4. Share repurchase plan of up to a maximum consideration of HK$700m once the black-out period expires, announced prior to 1H2018 results

CGIS' views

Qualified and prospective clinical data on CAR-T, Company's future cash flow has little relation with China's current macro and industry environment

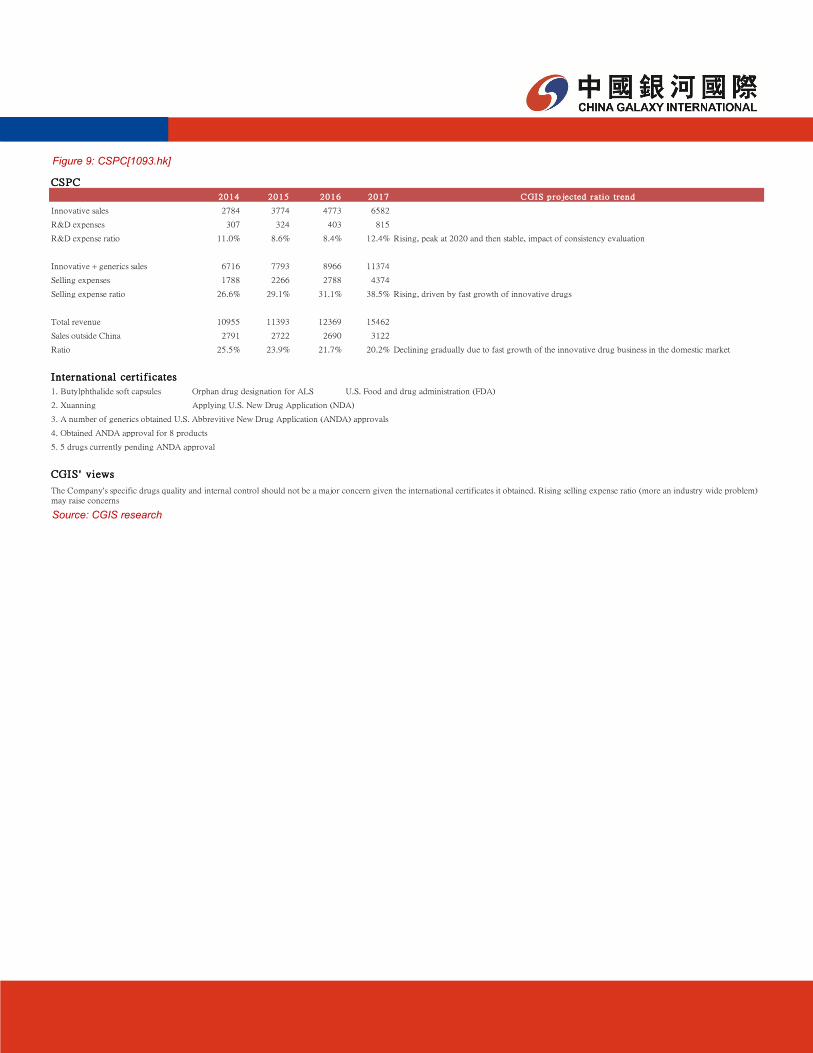

Figure 9: CSPC[1093.hk]

Source: CGIS research

CSPC

2014 2015 2016 2017 CGIS p ro jected ratio trend

Innovative sales 2784 3774 4773 6582

R&D expenses 307 324 403 815

R&D expense ratio 11.0% 8.6% 8.4% 12.4% Rising, peak at 2020 and then stable, impact of consistency evaluation

Innovative + generics sales 6716 7793 8966 11374

Selling expenses 1788 2266 2788 4374

Selling expense ratio 26.6% 29.1% 31.1% 38.5% Rising, driven by fast growth of innovative drugs

Total revenue 10955 11393 12369 15462

Sales outside China 2791 2722 2690 3122

Ratio 25.5% 23.9% 21.7% 20.2% Declining gradually due to fast growth of the innovative drug business in the domestic market

International certif icates

1. Butylphthalide soft capsules Orphan drug designation for ALS U.S. Food and drug administration (FDA)

2. Xuanning Applying U.S. New Drug Application (NDA)

3. A number of generics obtained U.S. Abbrevitive New Drug Application (ANDA) approvals

4. Obtained ANDA approval for 8 products

5. 5 drugs currently pending ANDA approval

CGIS' views

The Company's specific drugs quality and internal control should not be a major concern given the international certificates it obtained. Rising selling expense ratio (more an industry wide problem)may raise concerns

Disclaimer

This research report is not directed at, or intended for distribution to or used by, any person or entity who is a citizen or resident of or located in any jurisdiction where such distribution, publication, availability or use would be contrary to applicable law or regulation or which would subject China Galaxy International Securities (Hong Kong) Co., Limited (“Galaxy International Securities”) and/or its group companies to any registration or licensing requirement within such jurisdiction.

This report (including any information attached) is issued by Galaxy International Securities, one of the subsidiaries of the China Galaxy International Financial Holdings Limited, to the institutional clients from the information sources believed to be reliable, but no representation or warranty (expressly or implied) is made as to their accuracy, correctness and/or completeness.

This report shall not be construed as an offer, invitation or solicitation to buy or sell any securities of the company(ies) referred to herein. Past perfor-mance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regard-ing future performance. The recipient of this report should understand and comprehend the investment objectives and its related risks, and where necessary consult their own independent financial advisers prior to any investment decision.

Where any part of the information, opinions or estimates contained herein reflects the personal views and opinions of the analyst who prepared this report, such views and opinions may not correspond to the published views or investment decisions of China Galaxy International Financial Holdings Limited and any of its subsidiaries (“China Galaxy International”), directors, officers, agents and employees (“the Relevant Parties”).

All opinions and estimates reflect the judgment of the analyst on the date of this report and are subject to change without notice. China Galaxy Interna-tional and/or the Relevant Parties hereby disclaim any of their liabilities arising from the inaccuracy, incorrectness and incompleteness of this report and its attachment/s and/or any action or omission made in reliance thereof. Accordingly, this report must be read in conjunction with this disclaimer.

Disclosure of Interests

China Galaxy Securities Co., Ltd. (6881.HK; 601881.CH) is the direct and/or indirect holding company of the group of companies under China Galaxy International.

China Galaxy International may have financial interests in relation to the subjected company(ies) the securities in respect of which are reviewed in this report, and such interests aggregate to an amount may equal to or more than 1 % of the subjected company(ies)’ market capitalization.

One or more directors, officers and/or employees of China Galaxy International may be a director or officer of the securities of the company(ies) men-tioned in this report.

China Galaxy International and the Relevant Parties may, to the extent permitted by law, from time to time participate or invest in financing transac-tions with the securities of the company(ies) mentioned in this report, perform services for or solicit business from such company(ies), and/or have a position or holding, or other material interest, or effect transactions, in such securities or options thereon, or other investments related thereto.

China Galaxy International may have served as manager or co-manager of a public offering of securities for, or currently may make a primary market in issues of, any or all of the entities mentioned in this report or may be providing, or have provided within the last 12 months, significant advice or invest-ment services in relation to the investment concerned or a related investment or investment banking services to the company(ies) mentioned in this report.

Furthermore, China Galaxy International may have received compensation for investment banking services from the company(ies) mentioned in this report within the preceding 12 months and may currently seeking investment banking mandate from the subject company(ies).

Analyst Certification

The analyst who is primarily responsible for the content of this report, in whole or in part, certifies that with respect to the securities or issuer covered in this report: (1) all of the views expressed accurately reflect his or her personal views about the subject, securities or issuer; and (2) no part of his or her compensation was, is, or will be, directly or indirectly, related to the specific views expressed by the analyst in this report.

Besides, the analyst confirms that neither the analyst nor his/her associates (as defined in the code of conduct issued by The Hong Kong Securities and Futures Commission) (1) have dealt in or traded in the securities covered in this research report within 30 calendar days prior to the date of issue of this report; (2) will deal in or trade in the securities covered in this research report three business days after the date of issue of this report; (3) serve as an officer of any of the Hong Kong-listed companies covered in this report; and (4) have any financial interests in the Hong Kong-listed companies cov-ered in this report.

Explanation on Equity Ratings

Copyright Reserved

No part of this material may be reproduced or redistributed without the prior written consent of China Galaxy International Securities (Hong Kong) Co., Limited.

China Galaxy International Securities (Hong Kong) Co. Limited, CE No.AXM459

20/F, Wing On Centre, 111 Connaught Road Central, Sheung Wan, Hong Kong. General line: 3698-6888.

BUY share price will increase by >20% within 12 months in absolute terms :

SELL share price will decrease by >20% within 12 months in absolute terms :

HOLD no clear catalyst, and downgraded from BUY pending clearer signal to reinstate BUY or further downgrade to outright SELL :