YOUR SUCCESS IS AT THE CENTER - …. 374... · YOUR SUCCESS IS AT THE CENTER OF OUR BUSINESS Your...

70

Transcript of YOUR SUCCESS IS AT THE CENTER - …. 374... · YOUR SUCCESS IS AT THE CENTER OF OUR BUSINESS Your...

YOUR SUCCESS IS AT THE CENTER OF OUR BUSINESS

Your success depends on finding opportunities to grow your business to new levels.

As a like-minded ally, we’re focused on helping you boost sales, grow profits, and

retain your valuable customers. Get ahead of the competition today and connect with

one of the industry’s Top 10 New Business Volume Leaders1.

DEDICATED TO YOUR SATISFACTION

• Superior customer service experience from start to finish

• Dedicated Relationship Managers who understand your market

EVERBANK’S CUSTOMIZED APPROACH

• Quicker financing decisions to win the sale

• Supportive strategies to close more profitable transactions

• Incentive programs that bring additional revenue

• Co-branded and private label marketing support

EXPERT SOLUTIONS THAT FIT YOUR NEEDS

• Robust, easy-to-use web portal with 24/7 online secure systems access

• Flexible invoicing options

• Vendor portfolio reporting and end-user transaction management

• Customized back-end execution – upgrade, in-place sale, and renewal options

EverBank® is a division of TIAA, FSB. Finance services may be provided by EverBank Commercial Finance, Inc., which is a subsidiary of TIAA, FSB, and not itself a bank or a member FDIC.

©2017 and prior years TIAA, FSB. 17VEF6123.01

FOCUSED ON THE OFFICE TECHNOLOGY INDUSTRY

INDUSTRY FOCUS

RELATIONSHIP CENTERED

EASE OF BUSINESS

INNOVATIVE SOLUTIONS

PERSONALIZED SERVICE

Contact us today

Call 1.866.879.8795or visit commercial.everbank

1. Top 25: Monitor Vendor Channel New Business Volume Leaders national ranking for 2016.

YOUR SUCCESS IS AT THE CENTER OF OUR BUSINESS

Your success depends on finding opportunities to grow your business to new levels.

As a like-minded ally, we’re focused on helping you boost sales, grow profits, and

retain your valuable customers. Get ahead of the competition today and connect with

one of the industry’s Top 10 New Business Volume Leaders1.

DEDICATED TO YOUR SATISFACTION

• Superior customer service experience from start to finish

• Dedicated Relationship Managers who understand your market

EVERBANK’S CUSTOMIZED APPROACH

• Quicker financing decisions to win the sale

• Supportive strategies to close more profitable transactions

• Incentive programs that bring additional revenue

• Co-branded and private label marketing support

EXPERT SOLUTIONS THAT FIT YOUR NEEDS

• Robust, easy-to-use web portal with 24/7 online secure systems access

• Flexible invoicing options

• Vendor portfolio reporting and end-user transaction management

• Customized back-end execution – upgrade, in-place sale, and renewal options

EverBank® is a division of TIAA, FSB. Finance services may be provided by EverBank Commercial Finance, Inc., which is a subsidiary of TIAA, FSB, and not itself a bank or a member FDIC.

©2017 and prior years TIAA, FSB. 17VEF6123.01

FOCUSED ON THE OFFICE TECHNOLOGY INDUSTRY

INDUSTRY FOCUS

RELATIONSHIP CENTERED

EASE OF BUSINESS

INNOVATIVE SOLUTIONS

PERSONALIZED SERVICE

Contact us today

Call 1.866.879.8795or visit commercial.everbank

1. Top 25: Monitor Vendor Channel New Business Volume Leaders national ranking for 2016.

• 4 •

EDITORIAL AND PUBLISHING

Frank G. Cannata President and CEO/Editor-at-Large

Charles J. Cannata EVP and Publisher

Scott Cullen Editor-in-Chief

Carol C. Cannata SVP, Client Services and Events

Sharon Tosto Esker Editor/Chief Correspondent, Women Influencer Franchise

Doreen Borghoff Design Director

Cathy O’Brien Senior Public Relations and Marketing Consultant

Tetsuo Kubo Japanese Correspondent

Toni McQuilken Production Print Correspondent

Petra Diener European Correspondent

Mark Vruno Contributing Editor

Walter Geer III Executive Director, Digital Strategy

Saul Rosenbaum Senior Director, Digital Operations

Charlene Piro Executive Producer, Print

Joe “Dapp” Foster Digital Video ProductionDapp Studios | dapp.us

Matt Stauble Events PhotographyMatt Stauble Media | mattstaublemedia.com

THECANNATAREPORTtheCannataReport.com

The Cannata Report (ISSN: 0889-5880) is published twelve times yearly by Marketing Research Consultants LLC, P.O. Box 180 Hamburg, New Jersey 07419. Phone: (973) 823-6314; Fax: (973) 823-6316; email: [email protected]. Editor and Publisher, Frank G. Cannata. All rights reserved. No part of this periodical may be reproduced in any manner in any language without the consent of The Cannata Report. The information set forth herein and on its complementary website,thecannatareport.com, has been obtained from sources believed to be reliable but is not guaranteed by The Cannata Report and may be incomplete. The Cannata Report’s expressed views and opinions are based on the foregoing and should be viewed in this context. Printed in the U.S.A. SUBSCRIPTION RATES for The Cannata Report and thecannatareport.com are $475 (exclusive of hard copy) and $525 (inclusive of hard copy) for one year. Subscribe at thecannatareport.com/register or email [email protected]. Bulk subscription rates also available. Email [email protected]. POSTMASTER: Please email address changes to [email protected].

EDITORIAL ADVISORY BOARD

Keith Allison President and CEO I Systel Business

Systems I PO BOX 35910 Fayetteville, NC 28303

Paul Hanna President I Blue Technologies

5885 Grant Avenue Cleveland, OH 44105

Steve Reding President I C.A. Reding

4352 North Brawley Avenue, Suite 101 Fresno, CA 93722

Andrew Ritschel Owner/President I Electronic Office Systems, Inc. I 330 Fairfield Road

Fairfield, NJ 07004

Barry Simon President I Datamax

7400 Kanis Road Little Rock, AK 72204

Mark Steadman President and CEO I Stan’s Office

Technologies I 1375 South Eastwood Drive Woodstock, IL 60098

Subscriptions I Advertising I Licensing I Back Issues I [email protected] (917) 514-9501

hp.com/go/A3/cannata

© 2017 HP Development Company, L.P. The information contained herein is subject to change without notice.

at your serviceThe new HP multifunction printers transform the copier market with a reinvention of device management. Built-in technology

anticipates problems, schedules maintenance, and ensures that your printer is consistently up and running.

A3_Cannata_print_SERV_SEP_8.5x11_FIN.indd 1 7/31/17 9:23 AM

COVER STORY 36 I Channeling a Spirited Sense of Optimism: 32nd Annual Dealer Survey (Part II) 36 I Dealer Concerns, Partner Impressions, and Future Outlooks 38 I Executive Summary (Part II of II) 39 I Results and Analysis (Part II of II) DEPARTMENTS 10 I Hard Copy • From The Editor’s DeskNo. 35: I’m Optimistic TooThe Majority of dealers who participated in our 32nd Annual Dealer Survey are optimistic about future. 24 I Japanese HeadlinesRicoh’s ResetPresident and CEO Yoshinori Yamashita claims that the company’s“Restart” theme for its mid-term management plan has been movingalong quite smoothly. 26 I European HeadlinesAround the World with MPSManaged print services represents a growing global opportunity in many regions. 30 I CR LIVE: 2017 Dealer TourSolid as SteelEdwards Business Systems grows from a typewriter sales and services shop to one of the largest independent office technology companies in North America.

65 I Young InfluencersTalent ScoutAn intimate understanding of the millennial mindset helps Young Influencer Hunter Woolfolk identify young sales talent for his dealership and dispel some clichés about his generation. 68 I From the Vault: 1982–2017October HighlightsRelive memorable moments and milestones as featured in several past October issues of The Cannata Report. 68 I Up NextThe Cannata Report prepares to launch our November Production Print Issue and gets back out on the road again for ACDI Solutions Summit, Sharp’s National Dealer Meeting, and a CR LIVE: 2017 Dealer Tour stop at New England Copy Specialists.

FEATURES 55 I That One ThingKonica Minolta presses dealers to expand their revenue streams beyond core MFP business at FUTUREADY Dealer Meeting. 60 I Should I Stay or Should I Grow?Acquisitions reshape independent dealer landscape and challenge established norms of the acquisitions game.

63 I Imaging Reality CheckVirtual and augmented reality impact world of print.

Visit TheCannataReport.comOctober 2017

• 6 •

Celebrating 35 Years

36 Quote:

“Running down a dreamThat never would come to meWorking on a mysteryGoing wherever it leadsRunning down a dream…”

–Tom Petty, (October 20, 1950–October 2, 2017), American singer-songwriter, multi-instrumentalist, record producer, and actor

Industry Announcements, Awards, Acknowledgments & Sightings

12 • Living It Up at Konica Minolta’s Hotel California 16 • Toshiba Elevates Larry White and Ted LeBlanc to New Senior Roles 16 • Marco Acknowledged as CRN Triple Crown Award Winner 18 • POA Renovates and Opens Historic Building in Salem, Oregon 18 • HP Names Supplies Network “Partner of the Year” at HP Reinvent: World Partner Forum 20 • Marco Acquires KOPI in Jefferson City, Missouri 20 • GRAMMY Museum at L.A. Live Selects Toshiba as Venue’s Digital Signage Partner 22 • Anaheim Ducks Name Toshiba Official Document Solutions Partner 22 • Claw and Order: AIS Annual Customer Appreciation Lobster Dinner

I N K

2017 Special Survey Issue

Channeling a Spirited Sense of Optimism

In business,“can-do” does.

“World’s Most Ethical Companies” and“Ethisphere” names and marks are registered trademarks of Ethisphere LLC.

Member FDIC ©2017 U.S. Bank. 17-0111 MMWR-102140 (2/17)

usbank.com/oevs

There is no limit to how far your company can go when you believe you can and have a partner who believes it, too. At U.S. Bank, we have the competitive products and services that may help you on your way. Get started on making your possible happen today.

To find your company’s possible, contactDan Nack David TurnerDirector of Sales (East) Director of Sales (West)715.381.0207 801.756.0653

THIS MONTH ON Imaging Reality Check:

Video Series

When you hear the term “virtual reali-ty,” the odds are good your first thought isn’t about print. It’s probably not even your second or third thought. But virtualreality (VR) and augmented reality (AR) are where many brands are starting to turn when it comes to marketing their services and products.That means print needs to follow.

Watch how five brands, including Mc-Donald’s, Pizza Hut, and Garage mag-azine truly innovate a variety of printed items for increased engagement.

TheCannataReport.com

Check out these features and more in “This Week,”“Live Wire,” and “Video” at thecannatareport.com

NEW

S MACHINE

LDI Celebrates Celebrates Opening of New Facility

Puttin’ on the Ritz at BPCA PSIGEN Looks Beyond the Document and the Cloud

DEALERS SOFTWAREDEALER GROUPS

Under Pressure Designtex Set as Beta Text Site for Ricoh Pro T7210

Konica Minolta Prepares Dealers for the Future

MANUFACTURERS

INTERESTED IN BECOMING AN AUTHORIZED PARTNER?

Contact our Scanner Sales Specialists:[email protected] or

visit PanasonicPartnerPortal.com to apply today.

Soft sell your way to new businessHelp your client unlock the full potential of their automated document workflow with a reliable, stand-alone scanner from Panasonic. Often the missing piece in a total document solution, a Panasonic scanner tackles high-volume jobs that MFPs just can’t do.

Now you can offer your customers not only a complete document management system, but professional services as well. Panasonic scanners are compatible with most document management applications including companies like Square 9, Kofax, and more. Partner with Panasonic and we’ll not only set you up as a complete, end-to-end solutions provider, but also give you the tools to succeed with performance rebate programs and incentives that will increase your profit margins.

©2017 Panasonic Corporation of North America. All rights reserved. 04/17

@PanasonicUSA PanasonicUSAPanasonic Business Solutions

CAPTURE NEW BUSINESS

• 10 •

No. 35: I’m Optimistic Too Whew! The second part of our annual survey is finished and in the books, or should I say in the book, as in this book.

I had a general idea of what I was getting into when CJ asked me to take over the bulk of the survey this year. Little did I know how much blood, sweat, and tears Frank has devoted to this survey, until I found myself immersed over the last four months crunching numbers over and over again, making sure they were correct, working with our graphic designer to create charts that populate these pages, and analyzing the findings. Frank deserves a lot of credit for tackling this monumental task, year after year, for 31 years. And truth be told, he helped crunch a few numbers this year as well and provided me with many valuable insights throughout the process.

It’s only fitting that the second portion of our survey ends with dealers sharing their degrees of optimism about this industry. Spoiler alert: The majority is still optimistic about the future of this industry and their businesses.

Just as they are optimistic about their businesses and the industry, I feel a sense of optimism as well. I just returned from PRINT17 and although traditional office technology dealers were not in abundance at that show, I finally saw the light that Frank has been shining on commercial and industrial print. He has been one of the biggest advocates in our industry for dealers to move into that space. I’ve finally seen that potential and it makes me optimistic.

A number of other exciting developments in our industry also make me bullish. From the manufacturers, I see what Konica Minolta is doing with its “Workplace of the Future,” opening up a new world of possibilities for dealers, and that makes me optimistic. Companies like Kyocera and Konica Minolta are acquiring software companies, while other OEMs such as Canon are partnering with software companies that add value to their hardware offerings, and that makes me optimistic. Ricoh is shaking things up with its distribution, relying less on its branches than it has in a long time. HP is making a monumental effort to gain traction in our industry, possibly doing it right this time. And while those efforts may negatively impact some of the established OEMs, I view that potential shock to the established system as a positive.

On the product development side, inkjet technology is picking up steam within the imaging channel. Software companies and other players in the industry are enhancing what had become a stale and commoditized MPS business model.

And finally for the dealers, we are seeing large and mid-size dealers continuing to grow organically and through acquisition, which is the best news we can report. I talk to dealers all the time, and most are still as enthusiastic as they’ve ever been when talking about their businesses and this industry.

Yes, this industry still has numerous challenges ahead, as clicks continue to decline and the focus within dealerships shift in new and different directions—exciting to some, frightening for others. But what I’m seeing is an industry—from dealers to the OEMs, to the solutions companies, to the leasing companies, and everyone else associated with the imaging industry— is that they are embracing these changes. And that makes me optimistic too.

What about you?

Scott Cullen Editor-in-Chief

HARDCOPY From the Editor’s Desk

© 2017 AMETEK Electronic Systems Protection. All rights reserved.

Increase the Profitabilityof Your Business

Reduce equipment lock-ups, reboots, and service calls with the most advanced power protection

and conditioning technology available.

ESP has validated research that shows our technology significantly improves MCBV, CPC, and labor costs.

2017 Konica Minolta Dealer Awards Categories and WinnersMarco Receives Top Honor; POA and Imagetec Score Hat-Tricks

Konica Minolta 2017 Dealer Award category winners were announced as follows:

Award of Excellence: Marco

Top Revenue Growth (Up to $1.9M): Imagetec, LP($2-4.9M): UBEO, LLC ($5M+): DEX Imaging, Inc.

Top Percentage Revenue Growth(Up to $1.9M): Imagetec, LP($2-4.9M): Central Office Systems Corporation($5M+): Systel Business Equipment Company, Inc.

Top Managed IT RevenueAll Copy Products, LLCImpact Networking, LLC The Swenson Group

Top Solutions RevenuePacific Office Automation, Inc.PERRY proTECH, Inc.DEX Imaging

Top Production Print Units (up to $1.9M): Imagetec, LP($2-4.9M): Advanced Imaging Solu-tions, Inc.($5M+): Pacific Office Automation

Top A3 Color Units(Up to $1.9M): United Office Systems($2-4.9M): ImageNet Consulting, LLC($5M+): Pacific Office Automation

Konica Minolta Business Solu-tions U.S.A., Inc. (Konica Mi-nolta) hosted a closing bash at its 2017 FUTUREADY Dealer Meeting in Carlsbad, Califor-nia (October 3–5), that fea-tured a combination of come-dy, charity, dealer awards, and a live performance.

Lenny Clarke, the American

comedian and actor best known for his role as Uncle Teddy on the FX cable series Rescue Me (2004–2011), starring Dennis Leary, with his thick, trade-mark Boston accent, rallied the audience with Konica Mi-nolta President and CEO Rick Taylor and incited a bidding war over various raffle prizes among dealers that ultimately

pitted DEX Imaging, Documa-tion, Inc., and Pacific Office Automation, among others, against each other. These ef-forts were to raise money for the The Blue Angels Founda-tion, a 501(c)(3) public chari-ty whose mission is to support wounded veterans in a variety of ways. (For more informa-tion about the organization,

visit blueanglesfoundation.org). Konica Minolta increased contributions to the charity from $95,000 to $250,000 in approximately 30 minutes.

Following these fundraising efforts, SVP, Business Intel-ligence Services and Product Planning, Kevin Kern emceed a dealer award ceremony.

INDUSTRY ANNOUNCEMENTS, AWARDS, ACKNOWLEDGMENTS & SIGHTINGSI N K

BY CJ CANNATA

• 12 •

Living It Up at Konica Minolta’s Hotel California

Kevin Kern serves as 2017 Konica Minolta Dealer Awards emcee. Select dealers shown accepting awards flanked (left to right) by Sam Errigo, EVP, Sales and Business Development, and President and CEO Rick Taylor: 1. Steve Gau, VP, Sales, Marco; 2. Brad Knepper, President and CEO, All Copy; 3. Keith Allison, President and CEO, Systel Business Equipment, Inc.

2

1 3

I NKKonica Minolta arranged for a full set by Don Felder, for-mer Eagles lead guitarist and songwriter (1974–2001), and

his band to close out the eve-ning and event. By mid-show, the dance floor was packed as Felder ran through Eagles tunes

he co-wrote, including “Hotel California,” “Victim of Love,” and “Those Shoes,” in addition to a full array of Eagles clas-

sics, such as “Take It Easy,” “Witchy Woman,” “One of These Nights,” “Life in the Fast Lane,” and Heartache Tonight.”

• 14 •

DON FELDER BAND

DON FELDER KEVIN KERN AND DON FELDER

LENNY CLARKE JIM D’EMIDIO, CAROL CANNATA, AND GUESTS

PSIGEN makes powerful, scalable content capture and workflow solutions with a stratospheric track record.

Call us and we’ll prove it.

software inc.PSIGEN

Toshiba America Business Solutions, Inc. (Toshiba) an-nounced on October 2 that Larry White has been named its Chief Revenue Officer (CRO), effective immediate-ly. White, a 21-year veteran of Toshiba, had previously served as its senior vice presi-dent of sales for the Americas.

In this newly created position, White will be responsible for achieving company revenue objectives, developing revenue and profit growth strategies, and driving customer value through both the company’s di-rect and indirect channels.

Ten days after announcing

White’s new role, Toshiba an-nounced the promotion of Ted LeBlanc to vice president of U.S. dealer sales. In filling this new role, reporting to White, LeBlanc will oversee Toshiba’s

U.S. dealer channel sales. LeB-lanc is an established industry executive and a 10-year Toshi-ba employee who previously served as the company’s East-ern region director of sales.

• 16 •

I NK

For the second year in a row, CRN, a brand of The Chan-nel Company, awarded me-ga-dealer Marco with its es-teemed 2017 Triple Crown Award, as the influential dealer announced on Octo-ber 2. Forty North American solution providers had the

necessary revenue, growth, and technical expertise to be recognized on three of CRN’s pre-eminent solution provider lists, earning them the Triple Crown Award this year.

CRN assembles lists and rank-ings each year to recognize solution providers that are set-ting the bar in the IT industry, including the Solution Provid-er 500, which lists the largest solution providers in North America by revenue; the Fast Growth 150, which ranks the fastest-growing solution pro-viders; and the Tech Elite 250, which recognizes solution providers that have received the highest-level certifications from leading vendors.

According to Robert Faltera, CEO, The Channel Company, it is a considerable achieve-ment for a solution provider To make any one of these lists, let alone to make it onto all three of them—as this year’s Triple Crown Award winners have done—is a substantial achievement by any entity. A company must simultaneous-ly have enough revenue to be ranked on the Solution Provid-er 500 list, record double- or triple-digit growth for rec-ognition on the Fast Growth 150, and invest heavily in top certifications to attain Tech Elite 250 status. Marco earned CRN’s Tech Elite 250, Solu-tions Provider 500, and Fast Growth 150 awards, which led

to winning this year’s Triple Crown Award.

2017’s Triple Crown Award winners will be featured in CRN’s October issue and are posted at crn.com/triplecrown.

Marco Acknowledged as CRN Triple Crown Award Winner

“This year’s CRN Triple Crown Award winners boast multiple advanced technical certifications from leading vendors, rank among the top-earning IT solution providers in North America, and are some of the fastest-growing organi-zations in the channel today

–Robert Faletra, CEO, The Channel Company

“Larry White has consistently demonstrated the ability to lead his team to profitable revenue growth in a very challenging market. In this new role, Larry will have the opportunity to leverage a more cohesive and integrated organization toward continued great success.” –Scott Maccabe, president and CEO, Toshiba

“Throughout his tenure at Toshiba, Ted LeBlanc has established him-self as an impactful sales leader who consistently exceeds expecta-tions. Ted has the perfect blend of sales experience and expertise to successfully grow our reseller channel.” –Larry White, CRO, Toshiba

LARRY WHITE TED LEBLANC

ROBERT FALTERA

Toshiba Elevates Larry White and Ted LeBlanc to New Senior Roles

899617A | Clover Imaging Group and its logo are trademarks owned by Clover Technologies Group, LLC, and may be registered in the United States and other countries.

Grow Your Business With CIG Solutions

Get Started Today 1.866.734.6548 | cloverimaging.com/solutions

DON’T SETTLE FOR JUST ONE SCOOPNO ONE IS INVESTING IN MORE SERVICES AND SOLUTIONS TO GROW YOUR BUSINESS

Axess Express

Cost-Per-Seat Billing

TCO and Proposal Tool

Remote Monitoring

Auto Toner Fulfillment

SalesPro Training Videos

Tablet app

PrintReleaf

AMPLIFYContent marketing platform

EMPOWEREmail marketing platform

IMPACTCustom branded collateral

and videos

Tech Support & In Field Services

Custom Branded Help Desk

Live Chat

Service Shield & Service Shield+

Boxscore

Printer Service Training

CIG’s comprehensive portfolio of

customer-focused solutions enables

you to accelerate your business

growth by driving customer

engagement and retention.

The

Other Guys

Pacific Office Automation’s Salem branch officially opened the doors to its new office space on Friday, Sep-tember 1, in the heart of the downtown area. The move

had been a long time com-ing and was celebrated with a grand opening event at the new location. In late 2016, the Oregon-based office solu-tions company purchased and began renovating this historic building with plans to make it a home for several businesses in the area.

Located at 260 Liberty Street NE, the building had been va-cant for ten years. After being purchased by Pacific Office Automation, it received an interior and exterior facelift in early 2017. This project in-

cluded completely gutting and remodeling the building in preparation for its new tenants. The refurbished building has a new storefront, a sprinkler sys-tem, and electrical upgrades. It also features ADA accommo-dations, an elevator, and struc-tural upgrades to meet earth-quake safety standards.

POA currently occupies part of the building, leaving the rest for other businesses to rent out spaces. The ground floor of the building was transformed into an office equipment showroom to display the latest printers,

copiers, and more from POA’s partner manufacturers, includ-ing Konica Minolta, Ricoh, and Pitney Bowes.

POA’s newly renovated Sa-lem branch is just one of its 18 locations across the West Coast. As the company con-tinues to expand its reach by offering office equipment and services to more organi-zations, the company’s teams are looking to grow. Visit POA’s website. pacificof-fice.com, to see why people choose to make a career with Pacific Office Automation.

• 18 •

I NK

HP, Inc. (HP) announced Supplies Network, a U.S. dis-tributor of print and imaging products, “HP Partner of the Year” at HP Reinvent: World Partner Forum event in Chi-cago late this sumer on Sep-tember 13. The forum brought together more than 1,400 HP partners from across the globe, along with HP’s CEO, Dion Weisler, and his entire executive channel team.

Supplies Network was recog-nized in the sub-category of U.S. Supplies Distributor of the Year.

HP evaluated the winning partners across a variety of criteria including innovation, category leadership across print, PC and supplier, dis-tributor, and re-seller catego-ries. Globally, more than 50 partners were honored.

POA Renovates and Opens Historic Building in Salem, Oregon

CJ CANNATA AND DOUG PITASSI

STEPHANIE DISMORE, VP AND GM, AMERICAS, HP, INC.; GREG WELCHANS, PRESIDENT AND CMO, SUPPLIES NETWORK;

CHRISTOPH SCHELL, PRESIDENT, AMERICAS, HP, INC.

HP Names Supplies Network “Partner of the Year” at HP Reinvent: World Partner Forum

“Supplies Network was chosen out of a select group of valued partners based on a variety of revenue and growth factors that were reviewed and ultimately determined by our channel lead-ership team. This year’s award winners are perfect examples of what happens when we focus on driving strategic growth togeth-er. Congratulations on this well-deserved award!”

– Stephanie Dismore, vice president and general manager, Amer-icas Channels, HP, Inc.

• 20 •

I NK

On September 25, Marco an-nounced it purchased Koest-ner Office Products, Inc. (KOPI), a copier/printer com-pany based in Jefferson City,

Missouri, and run by President Sherri Wilbers.

Accordingly to Marco CEO Jeff Gau, the purchase will al-

low Marco to further expand its technical expertise and ser-vices in the state of Missouri, and the industry leader looks forward to continuing KO-PI’s commitment to satisfying their copier clients and pro-viding opportunities for their valued employees.

This is the 17th acquisition the company has completed over the past three years. In addi-tion to Jefferson City, Marco now has three other locations in Missouri.

Marco has 1,100 employees

and serves more than 32,500 customers from its 46 loca-tions throughout the Midwest and nationally.

Marco Acquires KOPI in Jefferson City, Missouri

Toshiba America Business Solutions, Inc. (Toshiba) an-nounced on September 13 the

implementation of digital sig-nage for the GRAMMY Mu-seum, run by Scott Goldman,

GRAMMY Museum execu-tive director, at L.A. LIVE, an AEG-owned venue in Los Angeles. Toshiba claims that the addition of its digital tech-nology in the GRAMMY Mu-seum strengthens the compa-nies’ alliance, which extends across many high-profile AEG assets and venues throughout North America and Europe.

Toshiba’s digital signage highlights the exterior of the GRAMMY Museum while promoting the venue’s up-coming performances, exhib-its, and education initiatives. The recently installed Toshi-ba LED signage was designed to enhance the exterior of the GRAMMY Museum and in-crease museum attendance, especially foot traffic from L.A. LIVE.

GRAMMY MUSEUM

GRAMMY Museum at L.A. Live Selects Toshiba as Venue’s Digital Signage Partner

SCOTT GOLDMAN

“We have already seen a positive impact from Toshi-ba’s digital signage. Our staff has reported a steady increase in attendance for all events.”

–Scott Goldman, GRAMMY Museum executive director

“We are excited to sell our company to Marco. They are a high performing com-pany that is committed to excellence and outstanding customer service. They are also consistently recog-nized as a great place to work.”

– Sherri Wilbers, president, KOPI

JOIN US for a

WEBINAR

WWW.SUPPLIESNETWORK.COM | 800-729-9300

PRODUCTS, SERVICES AND SOLUTIONS TO GROW YOUR BUSINESS.

SINGLE SOURCEF O R Y O U R I M A G I N G B U S I N E S S

THE

Simplify with our Device Tracker Service.

Wednesday, November 29 @ 1:30 pm CST www.gotowebinar.com | Webinar ID: 864-727-891

EQUIPMENT mpsSELECTSUPPLIES PARTS EXPERIENCETHERMAL

Communicate stale, moved and new devices to your customers

• Provide monthly reporting

• Restore stale devices

• Initiate reporting for new devices

• Offer portal training for your customers

We all know non-reporting devices have an immediate impact on your

profitability, customer satisfaction and service levels, but the time it takes

to keep track of status changes in an environment is exhausting – not to

mention, frustrating. It’s no wonder smart decision-makers want a solution

that tackles this administrative burden for them.

Avoid service interruptions and lost profits with Device Tracker.

• 22 •

I NK

If it’s the beginning of fall, it must be time for Fraser Ad-vanced Information Systems’ annual customer appreciation lobster dinner. It’s a seafood bacchanal in the woods of Blandon, Pennsylvania, with a bounty of oysters and clams on the half shell, all served during the cocktail hour, followed by

trays brimming with lobsters at dinner, resulting in the ultimate customer bonding experience.

Bill Fraser and his team do an amazing job of entertain-ing and feeding up to 80-plus guests and this year’s dinner on September 28 at the Maid-encreek Hunt & Fish Club

was another winning event. The dinner was once again co-sponsored by Sharp, one of Fraser’s key business partners, with Sharp’s Senior Vice Pres-ident of Sales Laura Black-mer and Senior Vice Presi-dent Steve Oda in attendance, mixing and mingling with the guests. As we’ve seen time and

time again, the dealer commu-nity has a knack for fostering long-term relationships. It’s clear that cooking more than 450 pounds of lobster is one of the best ways we’ve seen for keeping customers satisfied.

By Scott Cullen

Claw and Order: AIS Annual Customer Appreciation Lobster Dinner

Toshiba America Business Solutions, Inc. (Toshiba) an-nounced it is now the official document solutions partner of the Anaheim Ducks team late this summer on September 12. The multiyear partnership equips the National Hockey

League team with Toshiba’s industry-recognized e-STU-DIO multifunction printers (MFPs) featuring Elevate, a new technology that enables Toshiba MFPs to provide a custom-designed user inter-face for clients.

Toshiba endeavors to improve productivity and workflow via its e-STUDIO MFPs for Anaheim Ducks’ personnel throughout the team’s Hon-da Center home, corporate offices, and nearby Anaheim Ice training facility. Toshi-ba’s e-STUDIO print fleet will be deployed across the team’s functional areas from

operations and the executive suite, to the marketing depart-ment and press box. Whether producing high quality pro-motional materials, team and player statistics, or game day food and beverage menus, Toshiba solutions will help manage the team’s entire array of document needs throughout the year.

Anaheim Ducks Name Toshiba Official Document Solutions Partner

CR

“The Anaheim Ducks are excited to partner with Toshiba America Business Solutions as the official document solutions partner of the Ducks. Toshiba continues to provide top of the line business solutions and shares the same commitment to quality as our organization. We look forward to this partnership and utilizing Toshiba’s premium products and services.”

–Bill Pedigo, chief commercial officer, Anaheim Ducks

BILL FRASER AND SCOTT CULLENLAURA BLACKMER AND SCOTT CULLEN

*Konica Minolta Business Solutions USA, Inc. surveyed its sales representatives and lease administrators, and asked them to rate their four primary leasing providers on a number of factors. CIT Bank earned top honors for: Top Overall Partner, Best in Class, Overall Performance, Best Customer Satisfaction, Best Sales Representatives, and Best Processes/Systems.

©2017 CIT Group Inc. All rights reserved. CIT Bank and the CIT Bank logo are registered trademarks of CIT Group Inc. CIT Bank, N.A. is a subsidiary of CIT Group Inc.

Konica Minolta employees selected CIT Bank as “Best in Class” with the highest Net Promoter Score among their primary financing

providers.* We humbly thank Konica Minolta for the recognition

and are proud to serve the office imaging industry through our

customer-focused approach.

Learn about our winning solutions for manufacturers and dealers atcit.com/equipment-finance

Konica Minolta Selects CIT Bank as Top Overall Partner

On July 28, 2017, Yoshinori Ya-mashita, president and CEO of Ricoh Company, Ltd., stated that

the company’s “RICOH Restart” theme for the mid-term management plan from FY2017 through FY2019 has been mov-ing along quite smoothly.

Ricoh’s Q1 FY2017 financial statement, announced that same day, showed rev-enue of 495.5 billion yen (1% increase from Q1 FY2016), operating profit of 18.9 billion yen (74.1% increase), net profit before tax of 16.8 billion yen (61.7% increase), and quarterly net prof-it of $12.2 billion yen (91.3% increase). While the revenue experienced a modest increase, profit improved significantly. This uptick indicates Ricoh’s perfor-mance is recovering well in the wake of the profit-oriented policy implemented by Mr. Yamashita. As detailed by Yamashita’s presentation, the following outlines the key highlights resulting from the restructuring related to North America. Sales and Service Structure Reform in North America

In North America, Ricoh’s direct sales operation had some MIF with low profit-ability, particularly among SMB custom-ers. As a result, Ricoh has been focusing on establishing a remote sales structure by enhancing its inside sales and increas-ing indirect sales locations (reps). Due to the switch from door-to-door sales to in-sides sales, sales expense efficiency has increased by 20% to 30% for 50% to 60%

of the MIF for SMB customers. This has had the greatest impact for customers in remote or rural areas. Further, the company is trying to improve profitability by transferring the MIF for its direct operation to some of its leading dealers that can provide enhanced service and support. The profit from selling the direct MIF to those dealers was 6.3 bil-lion yen in Q1 FY2017. For major accounts, Ricoh has hired ex-perts for each category of service and industry, and is strengthening the com-pany’s ability to make sales proposals by becoming more knowledgeable about customer workflows in those accounts. Restructuring Production Locations

Production facilities for REI (Ricoh Elec-tronics, Inc.), a production subsidiary in North America, have been divided be-tween locations in California and Georgia with the intent of optimizing the produc-tion function. The company will consoli-date the entire MFP production function by moving it to Japan from California by next spring. The completion of the tran-sition of the headquarters’ function to the Georgia factory is expected by the com-pany’s second fiscal quarter. The California factory will continue to maintain its warehouses and be respon-sible for the customization and recycling of some products, remaining as a location to receive the products manufactured in Asia. However, the overall size of the fac-tory will become much smaller.

Additional Measures for Further Re-structuring

Mr. Yamashita is not only focusing on cost restructuring, but also is keen on creating a solid profit structure through operational process transformation. To accomplish this, he revealed the company would implement the following addition-al measures to the original plan.

1. Optimization of function and opera-tions between Ricoh headquarters and regional sales headquarters;

2. Enhancement of the supply chain man-agement (SCM) function at the global level;

3. Business process transformation for headquarters and indirect divisions utilizing RPA (robotics process auto-mation) and AI (artificial intelligence); and

4. Optimum location arrangement based on the streamlined operations.

By following this restructuring strate-gy, Ricoh indeed expects to achieve a substantial reduction in costs of 100 bil-lion yen in FY2019 compared to that of FY2016, all while continuing to exam-ine how to aggressively achieve this goal ahead of schedule.

• 24 •

JAPANESE HEADLINES BY TETSUO KUBO

CR

Questions About This Story? Contact Scott Cullen

Phone: (609) 406-1424

Email: [email protected]

Ricoh’s Reset President and CEO Yoshinori Yamashita claims the company’s “Restart” theme for its mid-term management plan has been moving along quite smoothly.

Innovolt offers companies that specialize in office technology a competitive advantage by improving efficiency and managing incremental costs.

For clear and direct answers to these questions, talk to the only company with proven state-of-the-art technology that helps you profitably retain and win customers. www.innovolt.com/cannata

QUESTIONING THE VALUE OF POWER PROTECTION?

YOU'RE RIGHT TO DO SO.

Does it offer any incremental

protection beyond the power supply?

Does it provide your service team

with information to help more quickly

resolve issues?

Does it drive meaningful service call reductions that allow you to compete and grow without

increased fixed cost?

www.innovolt.com/cannata

There are three ways to look at the global managed print services (MPS) landscape—around the

world in 80 leading countries, or making a simple split between established mar-kets—USA, Europe, some MEA (Mid-dle East and Arabic), some APAC (Asia Pacific), and all the DMOs (Developing Market opportunities).

Alternatively, we can explore the offer-ings of the usual suspects such as HP, Lexmark, Ricoh, and Xerox, closely fol-

lowed by Canon, Konica Minolta, and Kyocera, around the globe, as well as the findings of the market research com-panies that track these markets such as Gartner’s Magic Quadrant, Quocirca’s Landscape, IDC’s MarketScape, and Forrester’s Wave.

What do we know about MPS in the world’s 197 countries? How relevant is MPS globally? What elements of an MPS portfolio are of importance? And finally, what stages of MPS are available

where? Let’s try to answer some of those questions as we take a global tour of the MPS world.

An Essential Offering

Most anyone selling office imaging equipment, hardware, and software in the U.S. believes MPS should be an es-sential offering from almost any dealer to nearly any client. The same is true in Canada and Europe, particularly the U.K., Germany, France, and almost all

EUROPEAN HEADLINES BY PETRA DIENER

• 26 •

Managed print services represents a growing global opportunity in many regions.

Around the World with MPS

For more information on becoming a Lexmark Business Solutions Dealer, contact Ernie Browning, 972-896-9899.

Business Solutions Dealer

17C

H73

53

Lexmark dealers are color superstarsLexmark wins 2017 Color Printer/MFP Line of the Year from Buyers Lab.

Lexmark International Inc. was chosen by BLI analysts as the winner

of the 2017 Color Printer/MFP Line of the Year award for its:

} Exceptional reliability, simple maintenance and high-yield supplies for minimal downtime

} Full spectrum security

} Consistently outstanding color output

} Strong value proposition across its line, offering standout performances and functionality for a low-to-competitive total cost of ownership

Lexmark devices gave a superb performance across its entire color line. From small workgroups to large enterprise environments, Lexmark’s impressive portfolio of color printers and MFPs has you covered.”

Marlene Orr

BLI DirectorOffice Equipment Product Analysis

© 2017 Lexmark. All rights reserved. Lexmark and the Lexmark logo are trademarks or registered trademarks of Lexmark International, Inc. in the United States and/or other countries. All other trademarks are the property of their respective owners.

17CH7353_TheCannataReportAd1_092917.indd 1 9/29/2017 10:08:25 AM

members of the E.U. and even beyond where MPS is expected and accepted.

There’s also a growing community in South America and Central America with Brazil and Mexico leading the pack.

Some of the northern African states are under the European MPS influence, fol-lowing its hardware and software trends. South Africa has an active community as well with offerings similar to those in the northwest African markets.

But what about the large number of countries between South Africa and let’s say, Morocco? What do we know about them? Frankly, not much. We should, however, be aware that in some societ-ies, print hasn’t had and will never have a strong position, as they simply skipped this step, from a “classic” workflow to a super modern, digital one.

But let’s continue the journey east to the MEA region. Depending on the area (Dubai and Kuwait, for example) with their digital initiatives, we see enough high-level activities, skipping even basic MPS and diving right on into an aggres-sive digital transformation of the office document process.

From Russia with Love and Beyond

What about countries like Russia, China, and India? These countries are among the most populated in the world and have some of the highest monthly print volumes.

I spoke with an IT manager at a Russian university not too long ago. He was very excited about Ricoh’s offerings and the upcoming implementation within his university. We also know printer, car-tridge, and toner production in Russia is doing well, and a recently published success story by HP, detailing how it

is providing MPS for Gazprom, a Rus-sia-based global energy company, is only the tip of the iceberg.

An Indian startup company recently re-leased a device-tracking software similar to PrintFleet and Print Audit. With an es-timated 10 billion pages per month, the Indian market is, according to Gartner, still offering plenty of growth opportu-nities for MPS.

Moving on to the country of China, some might feel like we’re hitting a big blank spot on the MPS map, as we rarely hear or read about MPS activities in this country. However, China has one of the strongest MPS markets globally and is without a doubt the most active in Asia with an annual growth rate around 15%, making it a battleground for all the key MPS players.

Almost forgotten on the MPS map is South Korea, which has a booming MPS market with a similar growth rate and speed as China, Brazil, and Mexico.

Down Under and on the Top

Let’s leave the vast Eurasian continent behind and move on down under to Aus-tralia. Here, MPS is everywhere. Aus-tralia has a great active MPS communi-ty with one of the leading independent

global thought leaders on the subject, Mitchell Filby, at the forefront. Australia is the place to be for anyone who wants to see MPS going strong and ready for the future.

Money Makes the Word Go ‘Round

Analysts predict revenue growth for MPS from $26 billion ($U.S.) in 2015 to a minimum of $70 billion ($U.S.) by 2024 worldwide. Some even expect that figure to reach $97 billion ($U.S). Global players such as HP and Xerox are investing heavily in training and cer-tification programs for their teams and partners around the world. Solutions of-ferings, both hardware and software, are becoming more sophisticated, including industry programs, far beyond financial savings, and in support of the digital transformation of traditional office im-aging processes, from document creation to capturing, to output and archiving.

But in particular, DMOs are looking for much more than savings; they want security. Printers and related processes must meet the highest demands for data, content, and network access protection.

Summing It Up

As we’ve just seen at PRINT17, print is well alive and kicking. The predicted death of the printing industry and the radical drop in paper output doesn’t even have an ETA yet, but you might want to be part of the MPS movement now to ce-ment your position as a valuable partner for your clients, enterprise, and SMB go-ing forward—no matter what continent you call home.

CR

Questions About This Story? Contact Scott Cullen

Phone: (609) 406-1424

Email: [email protected]

• 28

The predicted death of the printing industry and the radical drop in pa-

per output doesn’t even have an ETA yet, but you might want to be part of the MPS movement now.

© 2016 Wells Fargo Bank, N.A. All rights reserved. All transactions are subject to credit approval. Some restrictions may apply. Wells Fargo Equipment Finance is the trade name for certain equipment leasing and fi nance businesses of Wells Fargo Bank, N.A. and its subsidiaries. Based on current net assets of Wells Fargo Equipment Finance (including Wells Fargo Rail) compared to net assets of the largest equipment fi nance/leasing companies (excluding GE Capital) ranked in the Monitor’s 2016 special edition. WCS-3001801 (09/16)

We’re dedicated to making it easier for your business to fi nd customized fi nancial solutions to help you and your customers grow and stay ahead of evolving equipment needs. With our recent acquisition, we’re now a leading equipment fi nance provider in the U.S. and Canada.

Whether you or your customers are trying to improve working capital, manage risks, or capitalize on market opportunities, you can count on the strength of our local market insight and tailor-made fi nancing.

Learn more at wholesale.wf.com/vendor.

Wells Fargo Vendor Financial Services

Delivering equipmentfi nancing solutions toNorth Americanbusinesses

• 30 •

OOne of the genuine pleasures of conducting this year’s dealer tour has been meeting with people who were in the business when I attended my first NOMDA convention in 1973 in New Orleans. At that time, dealers

were focused on selling typewriters and dictation equipment, while some were also selling office furniture and office supplies. A few had broadened their op-portunities by carrying copiers manufactured by companies such as APECO, AB Dick, SCM, Saxon, Royal, 3M, and others. This was the genesis of the indepen-dent dealer within the copier industry.

As we’ve been visiting legacy dealerships such as Les Olson, Gordon Flesch, and most recently, Edwards Business Systems, we’ve been transported back to those dealerships’ beginnings all those years ago. It has been more than a learning expe-rience for us, particularly for CJ, who has had the honor of meeting some of our industry’s earliest trailblazers.

It is hard to describe, but every one of the dealers we have visited has rolled out the red carpet and warmly welcomed us into their businesses and even their homes. When we contacted Ray Fuentes of Edwards Business Machines about visiting

SOLID AS STEEL

Edwards Business Systems

grows from a typewriter sales

and servicing shop to one of

the largest independent office

technology companies in

North America.

By Frank G. Cannata

Collaborate Like Never BeforeWith AQUOS BOARD® interactive display systems

• Open platform for seamless integration within your existing IT infrastructure

• Smooth and fast, intuitive touch technology

• Brilliant definition and large format display

Learn More: sharpusa.com/AQUOSBOARD

© 2017 Sharp Electronics Corporation. All rights reserved.

2017 DEALER TOURpresented by Sharp Electronics

Collaborate Like Never BeforeWith AQUOS BOARD® interactive display systems

• Open platform for seamless integration within your existing IT infrastructure

• Smooth and fast, intuitive touch technology

• Brilliant definition and large format display

Learn More: sharpusa.com/AQUOSBOARD

© 2017 Sharp Electronics Corporation. All rights reserved.

• 32 •

EDWARDS BUSINESS SYSTEMS

1. Office entry way 2. Conference room and showroom

3. Office entry way ceiling art, as de-

signed by Jamie Musselman, wife of Edwards Business Systems’ CEO Jim Edwards

1

3

2

his Pennsylvania-based dealership, he put together an itinerary that was part busi-ness and a lot of fun. In addition, the invi-tation was for the entire Cannata family, which Carol appreciated immensely.

Edwards Business Systems is primar-ily located in the Lehigh Valley area of Eastern Pennsylvania. The company has spread out and today has 11 locations in Pennsylvania and Virginia. Edwards Busi-ness Systems has no intention of stopping there. The company was founded in 1954 in West Reading, Pennsylvania, and has grown from selling and servicing type-writers and adding machines to serving as one of the largest independent office equipment companies in North America.

Edwards Business Systems has kept a keen eye set on growth through acqui-sition. In 1993, the company acquired Virginia Copiers, now known as Virgin-ia Business Systems. Edwards Business System’s most recent acquisitions include The Tamblyn Co. in the Scranton/Wilkes Barre area and Image Tec of Roanoke, Virginia. These two purchases have ex-panded the company’s footprint to 11 dif-ferent locations. Collectively, the 11 Ed-wards Business System locations provide services and support from the SMB space to the enterprise in Eastern Pennsylvania and Central Virginia. The dealership rep-resents Konica Minolta, Xerox, and Lex-mark, encompassing A3 and A4 MFPs to production print.

PRE-MUSIKFEST COCKTAIL PARTY

4. From left to right: Jamie Musselman, Cathy Dotter and Jim Edwards

5. Jennie Fisher, GM and SVP, Office Equipment Group, GreatAmerica Commer-

cial Finance and Frank Cannata

6. From left to right: Ray Fuentes; Jim Morrissey VP, Sales, Document Technology

Partners; and Jim Edwards

7. From left to right: Jim Dotter and Frank Cannata

8. From left to right: Jamie Musselman and Barb Fuentes

• 33 •

5

4

A Memorable Visit

During the first day of our visit, we spent the better part of three hours in the Ed-wards conference room, located in the company’s City Line Road location in Bethlehem, Pennsylvania. Our host was Ray Fuentes, president of Edwards, who was joined by Jim Dotter, president of Virginia Business Systems, and Edwards’ CEO Jim Edwards, son of the company’s founder. While most of the conversation was off the record, I can say that both CJ and I learned quite a bit about what this company thinks and feels about various aspects of our industry.

Even though Jim Edwards told us, “I

don’t give advice,” he still had plenty of wisdom to share, as did Ray and Jim Dot-ter. We learned that there doesn’t seem to be any single secret to the company’s success. All the changes that have taken place in the industry and continue to take place have made it challenging for many dealerships, including Edwards Business Systems, to make definitive plans for the future. Reflecting on what we learned and saw during our visit, the company’s success is the result of having a nimble organization that is prepared to respond to market changes and adapt quickly. It’s a formula not all that unfamiliar to many other independent dealerships.

We also walked away with the impression 8

7

6

that this is a dealership that understands its strengths, its customers, which mar-kets to target effectively, and the value of hiring the right people and letting them do their jobs.

Our discussion was followed up by a tour of the facility, led by Jim Edwards, who took great delight in sharing with us that he was aware of everything that goes on in the business that bears his family name. The West Reading location is the corpo-rate center where the financial side of the business is based. The City Line Road lo-cation is the hub in Pennsylvania, while Richmond is central to the five Virginia locations. It is visible the company’s op-erations are truly a team effort, and the collaborative spirit was readily apparent throughout our visit.

After the meeting and tour, we enjoyed dinner at an elegant restaurant and con-tinued our pleasant conversation, which turned more toward family. Ray specifi-cally had invited us to visit at this time of year, as this is when MusikFest in Beth-lehem is held. The next day, we were in-vited to Jim Edwards’ home for cocktails before going to MusikFest as guests of Edwards Business Systems.

After the cocktail reception, we attended a dinner hosted by Edwards for its cus-tomers and employees, and then, we had the great pleasure of seeing Santana per-form. He put on quite a show and it was a fitting end to our visit with Edwards Busi-ness Systems.

Frankly Speaking It is challenging for me to express exact-ly how I feel about the authentic kindness and generosity extended toward my fam-ily and myself by each of the dealers we have visited as part of our CR LIVE: 2017 Dealer Tour (which will expand to include a 2018 leg). When we began MRC in Jan-uary 1979 and started publishing in 1982, I hitched my star to the independent dealer. I was determined this was one of the best distribution networks in the United States and if I was smart, I would truly come to not only know the dealers, but also fully understand their business model. It was the best decision I ever made in my life.

As we progress through our dealer tour, my main goal has been to introduce CJ to some of the people who are central to our business and who are the core foundation of our own successful business. From Lit-tle Rock, Arkansas, to Bethlehem, Penn-sylvania, our dealer tour of the U.S. con-tinues. Next up is E. Johnson in Wausau, Wisconsin, followed by a visit to an old friend, Bryan Ammons, of Standard Of-fice in Duluth, Georgia. We will continue the tour through April 2018 and conclude it with a trip to Japan and a visit with Can-on, Konica Minolta, Kyocera, Sharp, and Toshiba in May of 2018.

MUSIKFEST

9. From left to right: Carol Cannata and Jim Edwards a private dinner hosted by

Edwards Business Systems at MusikFest

10 & 11. Carlos Santana performing live MusikFest 2017

• 34 •

CR

Questions About This Story? Contact Frank G. Cannata

Email: [email protected]

Phone: (860) 614-5711

9

11

10

1/19/17 SALT LAKE CITY • UT • LES OLSON COMPANY

2/21/17 MADISON • WI • GORDON FLESCH COMPANY

5/24/17 FAYETTEVILLE • NC • SYSTEL BUSINESS EQUIPMENT

6/29/17 SACRAMENTO • CA • SMILE BUSINESS PRODUCTS

7/18/17 TAMPA • FL • DEX IMAGING

8/4/17 BETHLEHEM • PA • EDWARDS BUSINESS SYSTEMS

9/7/17 WAUSAU • WI • E.O. JOHNSON BUSINESS TECHNOLOGIES

10/25/17 DULUTH • GA • STANDARD OFFICE SYSTEMS

CR Live: 2018 Dealer Tour and dates to be announced

Read about our visits in The Cannata Report and thecannatareport.com. For inquires about The Cannata Report’s CR Live: 2017 Dealer Tour, contact [email protected].

2017 DEALER TOURpresented by Sharp Electronics

Presented by

The Cannata Report Visits Top Performers Nationwide

Breakdown of Survey Respondents

Manufacturer Number of % of Mfg’s. Number of % of Mfg’s. Respondents Dealer in Respondents Dealer in 2016 Survey 2016 2017 Survey 2017

Canon 57 19% 57 20%Konica Minolta 61 21% 54 19%Kyocera 39 14% 22 8% Ricoh 55 19% 47 17%Sharp 33 11% 28 10%Toshiba 43 15% 56 20%

Over the years, we’ve discovered dealers aren’t shy about expressing their true feelings

about anything and everything related to the imaging industry. Dealers can be their OEM’s and business partner’s sharpest critics and some of those critiques make its way into our editorial coverage throughout the year.

Despite this criticism—sometimes constructive, sometimes harsh—the dealers’ general levels of satisfaction with their major equipment and technology suppliers and leasing partners never fails to surprise us. And with all the challenges dealers face— whether it’s keeping up with technology or everyday competitive pressures—there is still an overall sense of optimism among the participants in this year’s survey.

As reported in this year’s Part I, we went from a survey in 2016 that yielded a more balanced group of respondents by

manufacturer than any of our surveys to date to one this year that was somewhat less balanced. This year’s survey had 12 fewer responses than last year—277 compared to 289. That slight decline in respondents resulted in fewer dealers representing Konica Minolta, Ricoh, Sharp, and Kyocera compared to 2016. The same number of Canon dealers (57) contributed to the survey as last year, while the number of Toshiba dealers participating increased from 43 in 2016 to 56 this year. We commend Toshiba for doing such a fine job of encouraging its dealers to participate.

Although fewer dealers responded this year, the end result is the same as last year—a wealth of valuable and valid data. Once again, we are compelled to caution our readers that when the number of Kyocera dealers participating drops from 39 to 22 as it did this year, it becomes more difficult to interpret the results from such a small group of dealers about that

company’s performance. Anecdotally, based on past conversations with Kyocera dealers, we believe there’s some validity in the data we’re presenting in Part II.

Channeling a Spirited Sense of OptimismBy Scott Cullen

• 36 •

32ND ANNUAL DEALER SURVEYDealer Concerns, Partner Impressions, and Future Outlooks

Methodology Revisited

As we noted in Part I of our September issue, we conducted this year’s survey online for the fourth consecutive year for easier accessibility and to elicit more responses. This year the survey yielded 277 responses—19 fewer than last year—after we deleted duplicates, those with corrupted data, and incom-plete submissions. Historically, the numbers from the “Big Six”—Canon, Konica Minolta Business Solutions, Inc. (Konica), Kyocera Document Solutions America, Inc. (Kyocera), Ricoh America’s Corp. (Ricoh), Sharp Imaging and Infor-mation Company of America (Sharp), and Toshiba America Business Solu-tions, Inc. (Toshiba)— vary from year to year although last year’s survey was more balanced than any of our past sur-veys as far as OEM population. Howev-er, that was not the case this year with the most noticeable decline being in the number of Kyocera dealers participat-ing—only 22 as compared to 39 last year. You’ll find the universe of our 32nd Annual Dealer Survey in the chart at the bottom of this page. For the majority of this survey, we only used the respons-es from those dealers representing the “Big Six,” totaling 264. When we includ-ed the responses of the “Other” group, we have noted their inclusion, for ex-ample, when presenting their views of acquisitions, production print, areas of concern, annual dealer meetings, and awards selections.

Atlanta | Charlotte | Raleigh | Greensboro | Fayetteville | Hickory | Asheville | Greenville | Wilmington

Change brings new opportunities. As office technology evolves, so does our industry. Systel continues to focus on highlighting our strong servicing capabilities, customer satisfaction, financial stability and company culture.

Systel offers its people the ability to thrive in a fast-paced, successful organization while experiencing a diverse, family oriented and local

community based company dynamic with endless opportunity.

Experience More. systeloa.com/careers

• 38 •

u Dealers’ top three concerns remain consistent with our past years’ surveys as 48% of the 277 dealers responding this year selected declining clicks as one of their top three concerns, followed by hiring and retention of talent (45%) and competition from manufacturer’s direct branches (42%).

u Every dealer that identified competition from direct branches as one of their top three concerns rated this one as their number one concern. Not a single dealer listed this concern in a lower position.

u Succeeding in production print does not seem to be a big concern for most respondents. Only 8.6% of total respondents identified this as a concern and all were aligned with one of the three big production print OEMs—Canon, Konica Minolta, and Ricoh.

u Dealers overall have a positive view of their A3 manufacturers, with the Big Six averaging 4.40 compared to 4.21 last year out of a possible high score of 5.0.

u Last year, 72% of respondents relied on their A3 supplier for A4 product, while this year that number has dropped to 67%. Among the other companies cited by dealers as their A4 supplier were HP, Lexmark, Muratec, OKI, and Samsung, with Lexmark and HP being the strongest of the group.

u When rating their A4 manufacturer, we saw a slight dip in the average rating from last year’s 4.20 to 4.08 this year out of a possible high score of 5.0.

u The average number of leasing partners among dealers representing the Big Six manufacturers is 2.6. That’s a sizable number given that 16% (45) of dealers with less than $5 million in revenue among our 277-dealer universe only have one leasing partner.

u Nearly 20% of dealers responding to our survey cited one of their OEMs as one of their leasing partners. (Dealers could list up to four leasing partners.) This trend was most prevalent among Canon dealers where 79% identified Canon Financial Services (CFS) as one of

their leasing partners. An additional 2% of the remaining dealer population that did not identify Canon as a primary vendor is also using CFS for financing.

u The average percentage of dealers using internal leasing has declined 2% from 10% in 2015 to 8% last year, and has declined even further, by 4.66%, to 5.33% in this year’s survey.

u Looking at how the Big Six dealer universe ranked their leasing partners, 54% were ranked as “Excellent” compared to 64% last year.

u With a 5.0-rating system, the top three leasing companies in our survey all received scores well above 4.0, averaging 4.41%.

u Dealers identified well over 40 different software and service providers as providing the best products and support to allow them to compete most effectively, resulting in our most competitive results ever. Not a single provider scored higher than 8%. This year’s top four includes ACDI, Square 9, Papercut, and FM Audit, all with percentages in the single digits.

u Of the dealers whose core business is A3, 79% are optimistic about their businesses and the industry despite their concerns about declining clicks. Only 12% said that they were pessimistic, while 9% offered no response. The most optimistic dealers in this group belong to Kyocera with 95% feeling optimistic, followed by Ricoh with 85% of its dealers feeling optimistic.

u In the A4 realm, the results were roughly similar to A3 with 80% of dealers feeling optimistic, 8% pessimistic, and 12% offering no response. Once again, Kyocera and Ricoh had the most optimistic dealers with 95% and 89%, respectively feeling optimistic.

u In the Production Print space, only 57% of dealers reported feeling optimistic, while 24% noted pessimistic and 18% did not respond to this question. The dealers that feel the most optimistic are those that market products from Canon, Konica Minolta, and Ricoh.

32ND ANNUAL DEALER SURVEYExecutive Summary (Part II of II)

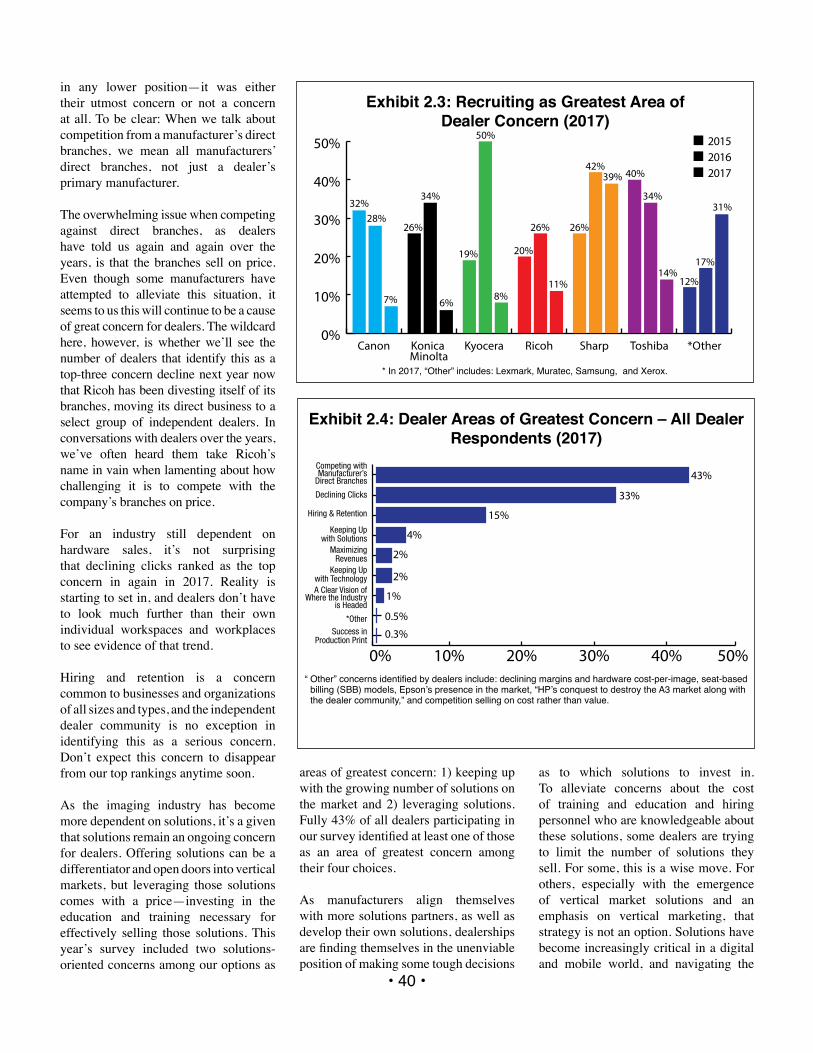

Areas of Greatest Concern Exhibits 2.1–2.4 As we attempt to analyze and interpret the dealer community’s comments pertaining to what they see as areas of greatest concern, we asked dealers to share with us the top four areas of greatest concern from a selection of 10 options, including “Other.” The areas of concern we asked dealers to choose from included:

• A clear vision of where the industry is heading

• Competing against manufacturer’s branches

• Declining clicks • Hiring and retention • Keeping up with new technology in

MPS/print management • Keeping up with the growing number of

solutions on the market • Leveraging solutions • Maximizing revenue and profits • Success in production print

What we discovered, perhaps not so surprisingly, was that dealers have plenty of concerns.

Despite offering a wider selection of areas of concern to choose from compared to previous years, survey respondents remained consistent in identifying competition from direct branches, declining clicks, or hiring and retention as one of their top choices. Looking at our top three concerns, 48% of the 277 dealers responding selected declining clicks as one of their top three concerns, followed by hiring and retention (45%)

and competition from manufacturer’s direct branches (42%).

What’s interesting about competition

from direct branches is that every dealer that identified this factor as one of their top three concerns rated this as the No. 1 concern. No dealer listed this concern

0%

10%

20%

30%

40%

50%

60%

70%80%

2017*20162015

Toshiba

Canon

Sharp

Kyocera

Ricoh

Konica Minolta

Other

Exhibit 2.1: Manufacturers’ Branches as Greatest Area of Dealer Concern (2017)

• 39 •

32ND ANNUAL DEALER SURVEYResults and Analysis (Part II of II)

* In 2017, “Other” includes: Lexmark, Muratec, Samsung, and Xerox.

10%

20%

30%

40%

50%

2017*20162015

Toshiba

Canon

Sharp

Kyocera

Ricoh

Konica Minolta

Other

Exhibit 2.2: Clicks as Greatest Area of Dealer Concern (2017)

* In 2017, “Other” includes: Lexmark, Muratec, Samsung, and Xerox.

in any lower position—it was either their utmost concern or not a concern at all. To be clear: When we talk about competition from a manufacturer’s direct branches, we mean all manufacturers’ direct branches, not just a dealer’s primary manufacturer.

The overwhelming issue when competing against direct branches, as dealers have told us again and again over the years, is that the branches sell on price. Even though some manufacturers have attempted to alleviate this situation, it seems to us this will continue to be a cause of great concern for dealers. The wildcard here, however, is whether we’ll see the number of dealers that identify this as a top-three concern decline next year now that Ricoh has been divesting itself of its branches, moving its direct business to a select group of independent dealers. In conversations with dealers over the years, we’ve often heard them take Ricoh’s name in vain when lamenting about how challenging it is to compete with the company’s branches on price.

For an industry still dependent on hardware sales, it’s not surprising that declining clicks ranked as the top concern in again in 2017. Reality is starting to set in, and dealers don’t have to look much further than their own individual workspaces and workplaces to see evidence of that trend.

Hiring and retention is a concern common to businesses and organizations of all sizes and types, and the independent dealer community is no exception in identifying this as a serious concern. Don’t expect this concern to disappear from our top rankings anytime soon.

As the imaging industry has become more dependent on solutions, it’s a given that solutions remain an ongoing concern for dealers. Offering solutions can be a differentiator and open doors into vertical markets, but leveraging those solutions comes with a price—investing in the education and training necessary for effectively selling those solutions. This year’s survey included two solutions-oriented concerns among our options as

areas of greatest concern: 1) keeping up with the growing number of solutions on the market and 2) leveraging solutions. Fully 43% of all dealers participating in our survey identified at least one of those as an area of greatest concern among their four choices.

As manufacturers align themselves with more solutions partners, as well as develop their own solutions, dealerships are finding themselves in the unenviable position of making some tough decisions

as to which solutions to invest in. To alleviate concerns about the cost of training and education and hiring personnel who are knowledgeable about these solutions, some dealers are trying to limit the number of solutions they sell. For some, this is a wise move. For others, especially with the emergence of vertical market solutions and an emphasis on vertical marketing, that strategy is not an option. Solutions have become increasingly critical in a digital and mobile world, and navigating the

• 40 •

0%

10%

20%

30%

40%

50%

*OtherToshibaSharpRicohKyoceraKonica Minolta

Canon

26% 26%

19% 20%

26%

32%

40%

28%

34%

50%

42%

34%

17%

12%

201520162017

7% 6%

14%

31%

39%

11%8%

Exhibit 2.3: Recruiting as Greatest Area of Dealer Concern (2017)

* In 2017, “Other” includes: Lexmark, Muratec, Samsung, and Xerox.

0% 10% 20% 30% 40% 50%

Success inProduction Print

*Other

A Clear Vision ofWhere the Industry

is Headed

Keeping Upwith Technology

MaximizingRevenues

Keeping Upwith Solutions

Hiring & Retention

Declining Clicks

Competing with Manufacturer’sDirect Branches 43%

33%

15%

4%

2%

2%

1%

0.5%

0.3%

Exhibit 2.4: Dealer Areas of Greatest Concern – All Dealer Respondents (2017)

“ Other” concerns identified by dealers include: declining margins and hardware cost-per-image, seat-based billing (SBB) models, Epson’s presence in the market, “HP’s conquest to destroy the A3 market along with the dealer community,” and competition selling on cost rather than value.

many options and figuring out how to bundle those with one’s product offerings will be an ongoing challenge for all dealers.

Moving forward, we expect to see the OEMs continue to align themselves with solutions providers, as Epson has done recently with Nuance, in an effort to gain increased traction in the high-end A3 space, or to acquire solutions companies as Kyocera did in early August with its acquisition of DataBank. We think the latter is less likely, as solutions providers tend to cast a wide net with their OEM relationships. What we’re more likely to see is consolidation among the solutions providers with companies like Nuance and ECi expanding their menu of solutions offerings via acquisition.

Much to our chagrin, succeeding in production print does not seem to be a big concern for most respondents. The modest percentage of respondents (8.6%) that identified this as a concern was typically aligned with one of the three big production print OEMs—Canon, Konica Minolta, and Ricoh. Either they’re doing just fine in production print or they’re more concerned about other areas of their business.

It is interesting to note that the percentage of dealers concerned there isn’t a clear vision of the future stands at 30% of all survey respondents. To that, we say welcome to the world of technology, a world that is in constant transition

and one in which the vision of the future is often more murky than clear. This is an issue we hope to address next year in a special issue of The Cannata Report, especially as more OEMs extend their own visions of the future beyond traditional print technology.

Dealers also had the option of citing “Other” as a concern beyond the choices we offered them. Some of the “Other” concerns identified by dealers were declining margins and hardware cost-per-image, seat-based billing (SBB) models, Epson’s presence in the market, “HP’s conquest to destroy the A3 market along with the dealer community,” and competition selling on cost rather than value.

A3 MFP Manufacturer RatingsExhibits 2.5–2.12

We asked dealers to rate their primary A3 MFP suppliers as “Excellent,” “Very Good,” “Fair,” or “Poor.” Each year, there are always dealers that decline to give their manufacturer a rating. Historically, we have tossed out those responses when tabulating the percentages shown in the accompanying Exhibits

• 41 •

46%

4% 7%

9%

2%

PoorFairGoodVery GoodExcellent

No Response

31%

Exhibit 2.6: Dealers Rate Primary A3 Manufacturer – Konica Minolta (2017)

Rating: 4.7

44%

5%

28%

14%

PoorFairGoodVery GoodExcellent

7%

No Response

2%

Exhibit 2.5: Dealers Rate Primary A3 Manufacturer – Canon (2017)

Rating: 4.1

• 42 •

49%

13%

2%

30%

PoorFairGoodVery GoodExcellent

No Response

6%

Exhibit 2.8: Dealers Rate Primary A3 Manufacturer – Ricoh

Rating: 4.3

77%

23%

PoorFairGoodVery GoodExcellent

No Response

Exhibit 2.7: Dealers Rate Primary A3 Manufacturer – Kyocera

Rating: 4.7

45%

41%

5%9%

PoorFairGoodVery GoodExcellent

No Response

Exhibit 2.10: Dealers Rate Primary A3 Manufacturer – Toshiba

Rating: 4.4

54%

11%

14%

4%

PoorFairGoodVery GoodExcellent

No Response

14%

4%

Exhibit 2.9: Dealers Rate Primary A3 Manufacturer – Sharp

Rating: 4.2

2.5–2.11. On further reflection, we consider the lack of response relevant to each manufacturer’s ratings. We then awarded five points for “Excellent,” four points for “Very Good,” three points for “Good,” two points for “Fair,” and one point for “Poor.” We then divided the total by the number of dealers participating from that manufacturer.

Overall, dealers still have a positive view of their manufacturers with the Big Six averaging 4.40 compared to 4.21 last year out of a possible score of 5.0. For the sake of transparency, only

three dealers representing one of the Big Six manufacturers gave their A3 manufacturer a “Poor” rating.

While dealers like to vent about their OEMs from time to time, or maybe more often than that, when taking stock of the big picture, our survey still shows a high degree of dealer satisfaction with their manufacturers.

Exhibit 2.12 showcases the differences in ratings for each manufacturer since 2011. This trend chart illustrates how

• 43 •

3

4

5

Percentage Up

201720162015201420132012

1.2

Exhibit 2.11: Dealers Rate Their Primary A3 Manufacturer – Total (2012–2017)

3

4

5

2017201620152014201320122011

Dea

ler A

ppro

val R

atin

g

Toshiba

Canon

Sharp

Kyocera

Ricoh

Konica Minolta

Exhibit 2.12: Dealers Rate Primary A3 Manufacturer by Manufacturer (2011–2017)

dealers’ ratings have evolved over the past seven years to where they are today.

A3 MFP Manufacturer Dealer Meeting Ratings Exhibits 2.13–2.19

Prior to 2016, we evaluated each manufacturer’s dealer meeting by level of attendance, which enabled us in part to gauge the effectiveness of the meeting.

Starting last year, we asked dealers to rate their manufacturer’s meetings as “Excellent,” “Very Good,” “Good,” “Fair,” or “Poor.” At the same time, we also track the number of dealers that did not attend.

Due to the type of responses, we evaluate this data by using the number of dealers that responded rather than the total number of dealers associated with each manufacturer. When a dealer elected not to respond, it was because they did not attend or the dealer decided they could not provide a valid opinion on the event.

It’s also worth noting that not every dealer is invited to those dealer meetings, even if the dealer considers that manufacturer its primary source for A3 products. Those dealerships typically are on the smaller revenue side—with less than $5 million in revenues. As they look to reduce the costs associated with putting on these events, it’s not surprising they are focusing primarily on the dealers that are responsible for the majority of their business.