Your Flexible Benefits Program 2020...2 Your Flexible Benefits Program Welcome to Schlumberger Flex...

32

Your Flexible Benefits Program 2020

Transcript of Your Flexible Benefits Program 2020...2 Your Flexible Benefits Program Welcome to Schlumberger Flex...

Your Flexible Benefits Program2020

Schlumberger Canada Limited wants to ensure and support both your physical and financial wellness. Schlumberger Flex offers you a comprehensive benefits program that you can tailor to your unique needs and adjust as your needs change. The medical and dental plans support your physical well-being while the disability, life, accident and critical illness coverage provide financial security against the unexpected.

This is about you. And for your benefits to really deliver on the promise of quality and value, you need to understand how they work and then use them to your advantage. That’s why we prepared this booklet and have put a number of resources in place through our different providers.

Please take the time to review this guide. In addition to information about how Schlumberger Flex works, you’ll find guidance on how to make your flex decisions and information on what others have chosen. You may also want to check out our provider websites – Employee Self Service, Sun Life, Industrial Alliance and Cigna. (You’ll find their contact information on the next page.)

Schlumberger Flex is focused on providing you with maximum flexibility and choice, so please invest some time to understand the variety of options available to you and make the right decision for you.

And remember – you’re not alone. If you have questions, you can contact the Schlumberger Canada Benefits Centre toll-free at 1-866-557-5222. It’s open Monday to Friday from 6:30 a.m. to 3:00 p.m. (Mountain time).

ContentsWho to contact 1

Welcome to Schlumberger Flex 2

Make Schlumberger Flex Work for You 2

How Schlumberger Flex Works 4

Dental Options 6

Extended Health Care Options 9

Life Insurance Options 13

Accidental Death and Dismemberment Insurance 17

Disability Plans 18

Optional Critical Illness Coverage 21

Your Health Care Spending Account 23

Your Personal Spending Account 24

Using Schlumberger Flex and Making Changes 26

Enroll Online in Your Flexible Benefits 28

Please note: The information in this document is a general description of your employer-sponsored benefits plans. These plans are subject to change from time to time. In the event of any discrepancy or misunderstanding, benefits will be paid according to the applicable contracts, policies, plan documents and legislation.

Your Flexible Benefits Program 1

Schlumberger Canada Benefits Centre Toll-free: 1-866-557-5222Monday to Friday: 6:30 a.m. to 3:00 p.m. (Mountain time)

When you call you will need: • Your Schlumberger Global Identification Number (GIN)

Employee Self Service website https://schlumberger.seb-admin.com Flex Plus Mobile App

For information about enrolling, changing your coverage or adding/removing dependents, beneficiary designations, payroll deductions and your coverage.

Sun Life Customer Care Centre Toll-free: 1-866-896-6976 Monday to Friday: 6:00 a.m. to 6:00 p.m. (Mountain time) mysunlife.ca Sun Life Mobile App

You’ll need your access ID, password and contract number.• Health and dental – contract 150939• Personal Spending Account – contract 151039• Basic and optional life insurance – contract 103039• Critical illness insurance – contract 105739

Allianz Global Assistance In the USA and Canada, call: 1-800-511-4610 From anywhere else: 1-519-514-0351 Call collect through an international operator.

Contact Allianz Global Assistance if you need any medical assistance while traveling, available 24 hours a day, seven days a week.

HumanaCare Toll-free: 1-877-305-9551 Monday to Friday: 6:30 a.m. to 4:00 p.m. (Mountain time)

For information on short- and long-term disability claims and claims- related inquiries.

Industrial Alliance Toll-free: 1-800-266-5667 Monday to Friday: 7:30 a.m. to 5:30 p.m. (Mountain time)

For information on accidental death and dismemberment claims and claims-related inquiries.

Shepell Toll-free: 1-800-387-4765 www.shepell.com

Your employee assistance program provides confidential counseling and information services for personal and work-related concerns. Counselors are available 24 hours a day, seven days a week.

Human Resources Toll-free: 1-877-927-5479 (9ASKHR9) Online: askhr.slb.com Email: [email protected]

Contact Ask HR, Schlumberger’s HR help team, if you need to:• Update your mailing address• Change any incorrect information on file• Ask a question about your pay slip* If you’re an active employee from Cameron, please log into your account and make changes via My Services https://mysap.c-a-m.com/irj/portal

Who to contact

2 Your Flexible Benefits Program

Welcome to Schlumberger FlexSchlumberger employees are a diverse lot. That’s what makes us interesting! We have different lifestyles, are at various ages, have varying degrees of family responsibilities and have different health care and financial security needs. Schlumberger Flex was created with that diversity in mind. It recognizes that we all have different needs and that these needs change over time. With Schlumberger Flex, you choose the benefits you need now – as your needs change, you can adjust your coverage.

Schlumberger provides you with flex dollars that you can use to purchase the benefits you need. You decide how these flex dollars are spent. If you have flex dollars left over, you can use them for a broad variety of health- and wellness-related expenses. If your health and financial security needs are more extensive, you can pay your additional coverage through payroll deductions. The plan was also created to be tax-effective; for example, there are some situations in which you pay for a benefit through payroll deductions rather than using flex dollars. Why? Because when your deductions are made with post-tax income, any benefit you receive will be tax free. The many features built into this flexible program make it convenient and easy to make your benefit choices and meet your changing needs. Schlumberger Flex is a key part of your overall total compensation package, is highly competitive within the industry, and puts you in control. With Control Comes Responsibility

It’s your responsibility to take the time to learn about the different options and choose the ones that work best, given your personal situation. And, because your benefit choices affect your whole family, talk to your spouse about your family’s benefits needs and any opportunities to coordinate plans.

There are a number of tools and resources to help you choose your benefit options. If you have questions, you can call the Benefits Centre toll-free at 1-866-557-5222. It’s open Monday to Friday, 6:30 a.m. to 3:00 p.m. (Mountain time). You can also get more information on our website (slb-benefits.ca) or through the Sun Life website www.mysunlife.ca/Schlumberger or the Sun Life app for iPhone and Android.

Make Schlumberger Flex Work for You

Step 1: UnderstandThis guide and other materials will help you understand your choices and how to use your benefits. You should also review:

� Employee Self Service website – At https://schlumberger.seb-admin.com you can:

� Enroll in your flexible benefits;

� Review coverage information throughout the year; and

� Your claims history – Look at your claims history for the last year to better understand how you and your family use your benefits. Your spouse’s benefits plan – If your spouse has a benefits plan, review the information about that plan and ensure that you understand the coverage and options available to you and your family. Schlumberger Flex gives you several ways to combine two benefits plans cost-effectively.

Step 2: DecideDecide which dependents you want to cover and the level of coverage for each benefit that’s right for you and your family. You can go to the website to model your choices and review the prices before you make your final decision.

Step 3: EnrollThe online enrollment process provides a fast and easy approach to registering your benefit choices each year. When you enter your choices on the Employee Self Service website, you can model different scenarios to determine which mix of coverage best meets your needs. Please ensure you enroll before the deadline. See page 31 of this Enrollment Guide for detailed instructions about how to enroll online at Employee Self Service.

Your Flexible Benefits Program 3

Employee Self ServiceEmployee Self Service is the online enrollment and information website. You can access ESS from anywhere you have Internet access! Or download the FlexPlus mobile app for greater access to your benefits enrollment information.

If You Do Not EnrollIf you do not enroll by your enrollment deadline, you will be assigned the default benefits coverage shown below. You cannot change your default coverage until the next annual enrollment period, unless you experience a life event (like marriage or the birth of a child).

BenefitDefault Coverage

For Re-enrollment For New Employees*

Extended Health Care Option 1 — Same dependent coverage as you currently have

Option 1 — Single coverage

Provincial Health Care (British Columbia only)

Current coverage No coverage

Dental Option 1 (unless you were within the 2-year lock-in period for Option 3) – Same dependent coverage as you currently have

Option 1 – Single coverage

Basic Employee Life 2 x eligible compensation 2 x eligible compensation

Basic Spouse Life (if spouse on file) $10,000 No coverage

Basic Child Life (if child on file) $5,000 No coverage

Optional Employee Life Coverage currently on file No coverage

Basic Accidental Death and Dismemberment (AD&D)

2 x base pay or admissible compensation, whichever is higher

2 x base pay or admissible compensation, whichever is higher

Schlumberger Long Term Disability (LTD)

Option 1 Option 1

Health Care Spending Account (HCSA) $0 $0

Unused flex dollars Your Personal Spending Account (PSA) Your Personal Spending Account (PSA)

* You will receive default coverage if you do not enroll within 30 days of the date on your New Hire enrollment letter. Default coverage will

remain in effect until the next annual enrollment or life event, whichever comes first.

4 Your Flexible Benefits Program

How Schlumberger Flex WorksYour Flex Dollars Each year, Schlumberger Canada gives you flex dollars to spend. Schlumberger provides you with enough flex dollars to cover the cost of Option 2 for both health and dental for you and all of your covered dependents. The flex dollars represent Schlumberger’s contribution towards your extended health care coverage, dental coverage, Health Care Spending Account and Personal Spending Account. The flex dollars, combined with your payroll deductions, where applicable, will be used to buy your benefits coverage for the upcoming calendar year. You will see your annual flex dollars when you enroll online.

Your ChoicesSchlumberger Flex offers you different levels of coverage, or options, for some benefits and mandatory coverage for others.

� Extended health care

� Dental

� Basic and optional employee life insurance

� Basic and optional spouse life insurance

� Basic and optional child life insurance

� Basic and optional employee AD&D insurance

� Optional spouse AD&D insurance

� Optional child AD&D insurance

� Long-term disability coverage

If you have flex dollars remaining after selecting your options, these dollars can be deposited in your Health Care Spending Account, Personal Spending Account and/or Registered Retirement Savings Plan (see page 25 for details).

You will also choose a coverage category for your dental and extended health care options from among these three:

� Employee only;

� Employee plus one dependent (spouse or child); or

� Employee plus two or more dependents.

The CostEach option has an annual price tag, which is the cost of buying that coverage. The more comprehensive the coverage, the higher the price tag. The enrollment website automatically calculates your flex dollars and price tags, as well as any payroll deductions, based on who you cover and what you choose.

EnrollingBe sure to enroll by the deadline – default coverage may not be right for you.

Default Coverage Is Not for Everyone

Default coverage may not meet your needs or the needs of your family. That is why it is important to actively make your Schlumberger Flex choices and enroll before the deadline.

Default coverageDefault coverage could be more or less coverage than you need and may or may not meet the needs of you and your family. It makes sense to enroll. Why pay for benefits you don’t need or pay for expenses that could have been covered by Schlumberger?

Your Flexible Benefits Program 5

Changing Your ChoicesAs your life changes, so do your benefits needs. With flexible benefits, you can change your benefit choices and dependents each autumn during the annual enrollment period. You also can change your choices during the year if you experience a life event, such as marriage, birth or adoption, or if your spouse loses his or her benefits coverage (see page 29). You will have 30 days after a life event to go online to register the life event and re-enroll. Otherwise, you can change your benefits and update your dependents only during the annual enrollment period.

Covering Your DependentsSpouse

Your spouse is defined as a person to whom you are married or within any other formal union recognized by law, or someone who is living with and has been living with you in a conjugal relationship for six consecutive months.

Children

A dependent child is your natural, adopted or step-child who is entirely dependent on you for maintenance and support and who is:

� Under 21 years of age; or

� Under 25 years of age (26 years of age for extended health care benefit for Quebec residents only) and attending a college or university full-time; or

� Physically or mentally disabled and incapable of self-support; and

� Not married or in a formal union recognized by law.

If a dependent child becomes disabled, you must submit proof of the child’s disability to Sun Life within 31 days of the disability. Please contact the Schlumberger Canada Benefits Centre at this time as well.

The definition of disabled for purposes of the extended health care and dental plans is as follows:

� The child is incapable of self-sustaining employment because of mental or physical handicap.

� The child became disabled prior to reaching age 21.

� The child is chiefly dependent on the participant for support and maintenance.

6 Your Flexible Benefits Program

Dental OptionsOur dental needs change over time – from sealants on baby teeth, to orthodontia, to root canals to crowns and bridges. The good news is that you can change your Schlumberger Flex dental options as your needs change. For example, you can choose no dental coverage at all and use your Health Care Spending Account to pay for your dental expenses; you can choose basic/major coverage only; or you can choose comprehensive coverage through a combination of basic, major and orthodontic coverage. The choice is yours!

Each option provides a different percentage of reimbursement and has different maximums. If you cover dependents, the maximums shown are per person. You can compare each of the options in the chart on page 9 to decide what’s right for you now and see what’s available for when your needs change.

Covering Your DependentsYou have a choice of three dental coverage levels. If you wish, you may choose different coverage categories for dental and extended health care.

� Employee only;

� Employee plus one eligible dependent (your spouse or an only child); or

� Employee plus two or more eligible dependents.

Important!Your dependents must be enrolled on the Employee Self Service website if you want to cover them under the dental and extended health care plans. When you log in to enroll, check the list of dependents to ensure all your dependents are listed and that the information shown is correct. You may update the information online.

If you add new dependents during enrollment, make sure that you enter the benefits you want to cover them under as well.

Serge

We couldn’t be happier with our newborn twins, and I was sure to enroll them in the right extended health option. But they’re not going to have teeth for a while. I think I’ll choose Employee plus one for dental now and switch to Employee plus two or more when they actually have teeth!

“

Your Flexible Benefits Program 7

Prices and Flex DollarsThe more comprehensive the option and the more people you cover, the higher the price tag will be for your dental benefits. Price tags and flex dollars are built right into the enrollment tool and do all the calculations for you. Watch to see how your balances change as you model different choices.

Don’t forget, Schlumberger provides you with enough flex dollars to pay the full cost of Option 2, and that’s no matter which coverage category you choose – whether you cover yourself only or yourself plus your dependent(s).

Changing Your Dental Coverage You can choose any dental option and any coverage category during your initial enrollment in Schlumberger Flex; however, there are some rules in place to ensure that the plan continues to be sustainable:

� If you choose dental Option 1, 2 or 4: you can choose any dental option during your next annual enrollment. Option 4 is the “opt-out” option and does not provide any coverage.

� If you choose dental Option 3: there is a two-year “lock-in” period. You cannot change this coverage for two years. This is our most comprehensive dental option and the cost to provide this coverage is spread over two years.

Dental Plan FeaturesWhen making your dental option decision, be sure to know what the different services include:

� Basic Dental Services – Includes services such as routine oral exams, cleaning, x-rays, tooth extractions, fillings, oral surgery and root canals. Sealants are also covered, but only for dependent children age 18 and under.

� Major Dental Services – Includes major restorative procedures such as dentures, crowns and bridgework.

� Orthodontia – Includes services and supplies related to orthodontic treatment, such as braces. Orthodontia is covered, but only for dependent children age 18 and under.

Andrea

“Unfortunately, my three girls inherited my overbite – something I’ve always hated. I’m choosing Option 3 and we’ll start taking our eldest to the orthodontist early in the new year. With three kids requiring treatment, we’ll need the option offering the highest lifetime maximum.

8 Your Flexible Benefits Program

Option 1 Option 2 Option 3 Option 4

Deductible None None None No coverage

Basic dental services

� Recall examinations

� Periodontics — scaling and root planing

60%Every 6 months

16 units

90%Every 6 months

16 units

100%Every 6 months

16 units

Major dental services

� Dentures and implants

50%

Included

70%

Included

80%

Included

Orthodontia

� Dependent children under 18

� Lifetime maximum

No coverage50%

$2,000

50%

$3,000

Annual maximumBasic and major restorative combined

$1,500 $2,000 $3,000

Dental fee guide Current year Current year Current year plus 20% (for basic services only)

Is It Covered? Check to Be Sure!

Before having any major dental procedure, you’ll want to be sure it’s covered and for how much. Ask your dentist to send in a Pre-determination Form that contains a listing of the necessary procedures with procedure codes. Sun Life will determine what’s eligible, what will be covered and what you may be required to pay out of pocket.

You can also call the Sun Life Customer Care Centre at 1-866-896-6976. You’ll need your access ID and contract number. There are different contract numbers for each plan. You’ll find them all on page 1 of this booklet.

Your Dental CoverageYou have four different dental options to choose from, as outlined in the chart below. Note that Option 3 has a two-year lock-in provision. This means that if you choose this option, you cannot change your coverage for two years. Maximums shown are for each covered person each year. Please choose from the following options for your dental package:

What Is the Dental Fee Guide?A dental fee guide contains a summary of suggested charges for all dental services, set annually by provincial dental associations and used by Sun Life to determine the reasonable and customary charge for a service.

Alex

“I’m single and, except for massage therapy and one or two prescriptions a year, my medical needs are pretty minimal. When I look at my benefit dollars and the price tag of each option, I’m better off choosing Option 1 and having my remaining flex dollars go into my Health Care Spending Account to cover any unforeseen medical expenses I may have.

Your Flexible Benefits Program 9

Extended Health Care OptionsThe extended health care plan offers a range of options to supplement coverage provided by your provincial health plan. Through Schlumberger Flex, you will be able to choose the option that provides the level of coverage you need for prescription drugs and other medical services and supplies. The extended health care plan will reimburse your eligible expenses at the percentages shown in the following chart. If you cover dependents, the maximums are per covered person.

Option 1 Option 2 Option 3

Reimbursement

� For all eligible expenses* 60% 90% 100%

Prescription drugsGeneric substitution unless physical override

� Deductible (per prescription)

� Annual out-of-pocket

All drugs legally requiring a prescription plus life-sustaining drugs

Dispensing fee

None

All drugs legally requiring a prescription plus life-sustaining drugs

Dispensing fee

None

All drugs legally requiring a prescription plus life-sustaining drugs

Dispensing fee

None

Hospital Semi-private Semi-private Private

Paramedical services**

� Maximum per paramedical service

� Annual combined maximum

$500

$1,500

$500

$1,500

$1,000

$1,500

Psychologist services***(annual maximum)

$500 $1,000 $1,500

Vision care(every 24 months)

No coverage $150 $350

Foot orthotics(every 36 months for adults and every 12 months for children)

$400 $400 $400

* Includes other expenses like ambulance coverage, diabetic supplies and hearing aids.** Acupuncturist; dietitian; chiropodist/podiatrist; chiropractor; massage therapist; naturopath; osteopath; physiotherapist; social worker; and speech therapist.*** Psychologist include all mental health practitioners that Sun Life standardly covers: Clinical Counsellor / Clinical Therapist; Marriage & Family Therapist; Mental Health Counsellor; Psychiatrist; Psychoanalyst; Psychotherapist.

Please choose from the following options for your extended health care package:

10 Your Flexible Benefits Program

Important!Your dependents must be enrolled on the Employee Self Service website if you want to cover them under the extended health care and dental plans. When you log in to enroll, check the list of dependents to ensure all your dependents are listed and that the information shown is correct. You may update the information online.

Note: If you add new dependents during enrollment, check to ensure that they are covered under your chosen extended health care option..

Costco Deal Means Prescription Savings for YouWhen you purchase your prescription drugs from a Costco pharmacy, you don’t pay any dispensing fees, and that’s money in your pocket. Membership not required.

Covering Your DependentsYou have a choice of three coverage categories under the extended health care plan. If you wish, you may choose different coverage categories for extended health care and dental.

� Employee only;

� Employee plus one eligible dependent (your spouse or an only child); or

� Employee plus two or more eligible dependents.

Changing Your Extended Health Care Coverage You can choose any extended health care option and any coverage category when you enroll in Schlumberger Flex. If you experience a life event (see page 29) during the year and report it to Schlumberger Canada Benefits Centre within 30 days of the event, you can change your extended health care coverage to any option.

Choosing Your Health and Dental CoverageTo decide what medical and dental coverage is right for you, you’ll need to have a good understanding of the plan details. If you’ve read through the overview provided in the last section, you’re in a good place to make your decisions.

If you have a spouse with employer benefits, you’ll need to consider what both plans provide and choose options that will maximize your coverage at the lowest cost. This will leave you with more flex dollars to use elsewhere. It takes a little thought and some planning, but it’s worth it to have a plan that is customized to your personal needs.

Joe

After throwing my back out helping my son move back to university, I’ve been seeing my chiropractor every two weeks. Choosing Option 3 will give me $1,000 towards my chiropractor benefits ... although I really hope I won’t need it.

“

Your Flexible Benefits Program 11

Looking BackThe first step in choosing your health and dental options is to look back at how you used your benefits in the past. A quick way to do this is to look at the claims you made last year. Or, if you did not have health and dental coverage last year, check your tax returns for health and dental receipts from last year or the last few years.

Reviewing your health and dental history will give you a clearer picture of your health and dental needs, so you can choose an appropriate level of coverage. Think About It:

� If you had a high number of prescription drug claims to manage an ongoing condition like high blood pressure, you may want to choose an extended health care option that provides you with the highest reimbursement level.

� Suppose you had a lot of paramedical claims, like massage therapy or physiotherapy, then you may want to choose an extended health care option that will give you enough coverage so you can continue to use these services.

� Don’t just choose a benefit because it has the coverage you need. Look at the price tag. If it’s more than the actual cost of the benefit, you might be better choosing a less comprehensive option and seeking reimbursement from your Health Care Spending Account.

� Don’t forget about your spouse’s plan. You might be able to choose a less comprehensive option, coordinate benefits with your spouse and still get 100% reimbursement. You’ll also have more leftover flex dollars if you do this – dollars you can direct to your HCSA, RRSP or PSA. (See Coordination of Benefits: Submitting Claims to Two Benefits Plans on page 30 for more information.)

Mike

“

Mike is single with minimal dental care needs except for regular check-ups. An average recall exam with polishing and two units of scaling costs about $275 in Alberta. Mike has two check-ups a year, totaling $550. Mike wants to buy enough coverage to minimize his expense, but he doesn’t want to pay for coverage he won’t use. Let’s take a closer look:

� With Option 1, Mike receives $605 flex dollars, leaving him $300 in leftover flex dollars; the price tag is only $305 rather than Option 3’s $994. With a 60% reimbursement plus the leftover flex dollars, Mike will have $80 flex dollars leftover and no out of pocket.

� Option 2 provides him with 90% reimbursement. The flex dollars cover the full cost of the benefit, although there are none left over. If Mike chooses Option 2, he’ll be out of pocket $55; however, if he has additional dental expenses, they’ll be reimbursed at a higher rate than Option 1.

� With Option 3, Mike receives the full $550 reimbursement on his dental expenses; however, he has payroll deductions of $343 per year and no leftover flex dollars. When we consider his payroll deductions, he’s actually out of pocket $343.

� Option 4 provides no reimbursement and is typically chosen by those employees who have coverage elsewhere. If Mike chooses Option 4, he’ll be $550 out of pocket.

Mike decides on Option 1. He’s still pretty sure that he won’t have any additional dental expenses, but even if he does, the 60% reimbursement covers a good percentage of the cost.

12 Your Flexible Benefits Program

Looking ForwardOnce you have evaluated your past benefits needs, it’s time to look forward and anticipate what your needs may be over the next year. Yes, life can be unpredictable, but you can think ahead.

Think About It:

� Some things don’t change – for example, regular prescription medication to manage an ongoing condition like diabetes.

� Perhaps you or a family member has recently experienced a change in health? Been diagnosed with a chronic condition? Experienced a sports injury? You can plan ahead and choose the appropriate option for claims associated with these types of issues.

� You can also plan ahead for certain expenses like prescription glasses or contact lenses for you or a family member, and don’t forget about your HCSA. Your HCSA can help to cover any amounts above the maximum.

� You can speak to your dentist to see if he or she anticipates the need for any major dental work in the next 12 months. Thinking ahead allows you to plan ahead.

� Will your children require orthodontics in the coming year? These projected expenses would mean that you should consider selecting more comprehensive dental coverage. And remember: dental Option 3 has a two-year lock-in.

Take the time to think ahead and consider the coverage you’ll need over the next year. It will help ensure that you don’t select too little or too much coverage. And remember, it’s up to you to decide what to do with your excess flex dollars.

Johanne

“I’ve always taken care of my teeth, so it was quite a shock when my dentist told me that I’d need two new crowns. I can put them off until January, which is right when my dental Option 2 will be in place, providing me with 70% reimbursement on major services and a $2,000 maximum. I compared the cost of the coverage to what the dentist has quoted, and I checked in with Sun Life to see what will and won’t be reimbursed. Option 2 is the right choice for me.

Your Flexible Benefits Program 13

Life Insurance OptionsSchlumberger Flex provides you and your family with the security that comes with a basic level of life insurance.

You can add to that by choosing optional life insurance for both you and your dependents. You’ve got well-priced coverage and the convenience of payroll deductions.

Schlumberger Flex offers term life insurance. It pays a benefit if you die of accidental or natural causes.

Basic Employee Life Insurance You automatically receive basic employee life insurance equal to two times last year’s admissible compensation, or base pay, whichever is higher. You do not have to make any choices under the basic employee life insurance benefit – it’s yours automatically. What’s more, Schlumberger pays the entire cost of basic employee life insurance.

Because Schlumberger pays for your employee and dependent basic life insurance coverage, it is reported as a taxable benefit to you for income tax purposes. You’ll see it on your T-4.

Designating a Beneficiary – Basic and Optional Employee Life Insurance

Be sure to designate one or more beneficiaries for your basic and optional employee life insurance. If there is no beneficiary information registered for you at the Employee Self Service website, you will be prompted to complete the form online.

You must then print the form, sign it and return it to the address on the form before your beneficiary designation will be valid. There must be a signed version of the form on file in order for your beneficiary designation to be legal.

What is Eligible Compensation?Eligible compensation is the higher of:

� Your current base pay; or

� Your admissible compensation at December 31 of the preceding calendar year.

Admissible compensation includes base pay, overtime, bonuses, commissions and geographical coefficients.

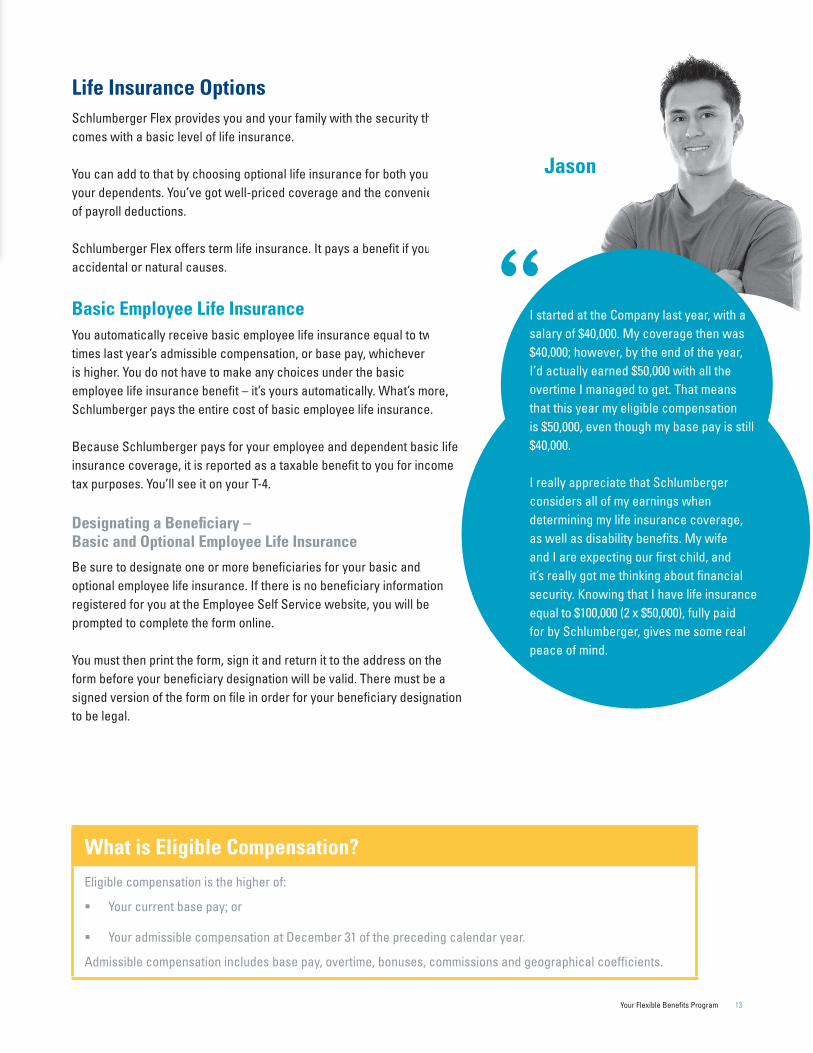

Jason

“I started at the Company last year, with a salary of $40,000. My coverage then was $40,000; however, by the end of the year, I’d actually earned $50,000 with all the overtime I managed to get. That means that this year my eligible compensation is $50,000, even though my base pay is still $40,000.

I really appreciate that Schlumberger considers all of my earnings when determining my life insurance coverage, as well as disability benefits. My wife and I are expecting our first child, and it’s really got me thinking about financial security. Knowing that I have life insurance equal to $100,000 (2 x $50,000), fully paid for by Schlumberger, gives me some real peace of mind.

14 Your Flexible Benefits Program

Smokers Pay DoubleIs this the year you quit?

Smoking is an expensive habit. All the more when you consider that life insurance premiums for smokers are double those of non-smokers.If you’re thinking of quitting, Schlumberger wants to help. Unlike many other employers, Schlumberger places no maximum on smoking cessation drugs. If the time is right for you, talk to your doctor.

Optional Employee Life Insurance You can purchase up to $500,000 of optional employee life insurance in multiples of $25,000. This coverage will be in addition to your basic employee life insurance coverage. If you choose to purchase or increase your optional life insurance, you must provide evidence of your good health to Sun Life. When you enroll, you will be prompted to complete an Evidence of Insurability Form, which you’ll need to send to Sun Life within 90 days of the day you enroll. Once you are approved, your payroll deductions will begin and you will be covered for the new insurance amount.

Prices

The price of optional employee life insurance is based on your age, sex and smoker status as of January 1 each year per $1,000 of coverage. You do not receive flex dollars for this benefit. You pay the entire cost through payroll deductions.

Smoker Status

If you select the non-smoker coverage category, you must complete an online non-smoker declaration. If at any time it is determined that you are a smoker, your coverage may be invalid. If it’s determined that you were a smoker at the time of your death, the benefit may not be paid.

Evidence of Insurability

An Evidence of Insurability (EOI) Form contains a medical questionnaire and is used to provide Sun Life with proof of your good health. While you don’t need this form for your basic employee life insurance coverage, you will need to complete the form if you decide to purchase optional life insurance for the first time or increase your coverage. The good news is that the enrollment tool will prompt you to print the form, complete it and return it to Sun Life at the address provided on the form.

Sun Life will use the EOI form to determine whether to approve the higher coverage or to request additional information. Your coverage is based on the information you provide to Sun Life. Coverage will not go into effect until an approval is received by the insurer, and you must be actively at work. You will automatically be enrolled in the highest amount of coverage that does not require EOI until your application is approved. If your completed EOI Form is not received within 90 days of your enrollment deadline, your application will be closed.

Keith

After comparing the costs and benefits, I decided to purchase optional employee life insurance through Schlumberger Flex instead of renewing my mortgage insurance. I still get the same coverage and peace of mind, but at a lower rate and without having to worry about multiple policies. The convenience of payroll deductions means I don’t even need to think about it.

“

“

Your Flexible Benefits Program 15

Basic Life Insurance for Your Spouse Schlumberger Flex provides you with basic spouse life insurance equal to $10,000. There is no EOI required for your spouse’s basic life insurance coverage.

Optional Life Insurance for Your SpouseYou can purchase up to $500,000 of optional spouse life insurance in multiples of $25,000. This coverage will be in addition to your basic spouse life insurance coverage.

Details About Optional Spouse Life Insurance Pricing for this benefit is similar to the pricing for optional employee life insurance. The prices per $1,000 of coverage are based on the amount of coverage you choose as well as your spouse’s age (as of January 1 each year), sex and smoker status. Your benefit is paid with payroll deductions and you are automatically the beneficiary of this coverage.If you choose the non-smoker coverage category, you will need to complete a non-smoker declaration about your spouse.

Basic Life Insurance for Your Child(ren)Schlumberger Flex provides you with basic child life insurance of $5,000. You do not have to make any choices, and this benefit is fully paid by Schlumberger. The price for basic child life insurance is based on a flat rate per $5,000 of coverage, regardless of how many children you have. Because Schlumberger pays for this coverage, it’s considered a taxable benefit and will appear on your T-4.

Optional Life Insurance for Your Child(ren) You can purchase up to $25,000 of optional child life insurance in multiples of $5,000. This coverage will be in addition to your basic child life insurance coverage. You may change your coverage amount in the future.

Details About Optional Child Life Insurance The option you choose will cover all of your eligible dependent children, whether or not they are registered on the Employee Self Service website as dependents. The cost is the same for one or more children. You are automatically the beneficiary of this coverage.Evidence of insurability is not required for basic or optional child life insurance.

Evidence of InsurabilityYour spouse will need to complete an Evidence of Insurability (EOI) Form when you first choose optional spouse life insurance or if you decide to increase his or her coverage. Only once Sun Life has approved your spouse’s application will your payroll deductions begin and your spouse be covered. (See “Evidence of Insurability” on page 16 for more information.)

Warren

“My wife and I have been talking about kicking the habit for years, but now we’re finally going to do it. We’ll use our Personal Spending Account to reimburse us for the cost of a smoking cessation program, and then, after one year of being smoke-free, we’ll see a substantial savings in our optional life insurance costs. Better health and lower costs. What’s not to like?

16 Your Flexible Benefits Program

Choosing Your Life InsuranceHow Much Do You Need?As you evaluate how much life insurance coverage to purchase, for both you and your dependents, it is important to first determine how much you need. Consider the following questions:

� Are you the primary earner in your family? How would your family replace your earnings if you were to pass away? If you die, does your family have an alternative source of income? What effect would the death of your spouse have on your family’s financial situation?

� Do you have dependents? Are they still young? Will your family face additional expenses, such as child care, if your spouse dies?

� Are there significant long-term expenses in your family’s future (e.g., mortgage, college or university tuition)? How much debt do you currently have (including your mortgage)?

Think about your current expenses, such as your mortgage and other monthly bills. Also consider longer-term expenses, such as paying for your children’s education. Alternatively, if you do not have children, or if your children are older, you may not need as much coverage.

How Much Do You Already Have?Be sure to look at the life insurance you may already have from other sources. For example:

� Do you have any private coverage as part of a professional organization? Do you or your spouse have life insurance from another source? Is the coverage adequate for your needs? Is it competitively priced?

� Are you covered under your spouse’s plan?

� Do you have insurance on your mortgage, or would the Schlumberger Flex coverage be a less expensive way to insure your mortgage?

With your Schlumberger Flex basic employee life insurance, you may already have enough insurance from other sources. Or you may want to consider replacing other sources with your Schlumberger coverage. Be sure to do some cost comparisons.

Reviewing your other sources of coverage will also help you evaluate whether you need to purchase optional coverage for your spouse or children.

Zaheed

My wife and I were just looking into increasing our life insurance coverage with the birth of our daughter. When we looked at the rates available through Schlumberger Flex, there was no question. It was a lot less expensive for the same coverage. Our family’s protected, we’re getting a great deal, and it’s all looked after through payroll deductions.

“

Your Flexible Benefits Program 17

Accidental death and dismemberment (AD&D) insurance Accidental death and dismemberment (AD&D) insurance pays a benefit if you die or are seriously injured in an accident. In addition to the basic employee AD&D insurance, Schlumberger Flex gives you the opportunity to buy optional AD&D insurance for yourself and your dependents.

Basic Employee AD&D InsuranceYou automatically receive basic AD&D insurance equal to two times eligible compensation. You do not have to make any choices under the basic employee AD&D insurance benefit, and Schlumberger pays the entire cost of this benefit.

Schlumberger pays the cost of your basic employee AD&D insurance, and it is considered a taxable benefit by the Canada Revenue Agency. You will pay tax on the premiums paid by Schlumberger.

Designating Beneficiaries

If you have a covered injury, you will receive the benefits payable from the AD&D plan.

If you die as a result of an accident, your AD&D benefit will be paid to the beneficiary we have on file. When you enroll on Employee Self Service (ESS), you will be prompted to complete the Beneficiary Designation Form; however, note that you must print the form, sign it and return it to the address on the form before your beneficiary designation is effective.

Optional Employee AD&D Insurance You can purchase up to $500,000 of optional employee AD&D insurance in multiples of $25,000. This coverage will be in addition to your basic employee AD&D insurance coverage.

Prices

The price of optional employee AD&D insurance is based on a flat rate per $1,000 of coverage. You may use available flex dollars for this benefit.

Optional AD&D Coverage for Your Spouse and ChildrenYou can purchase optional AD&D insurance for your spouse and children. The plans are similar to the employee AD&D plan:

� You can choose any option at any enrollment. Evidence of insurability is not required.

� The price for spouse coverage is based on a flat rate per $1,000 of coverage. The price for children covers all your eligible dependent children; they do not need to be registered on the Employee Self Service website.

� You are the beneficiary for these plans.

� The actual benefit will be based on the option you choose, the nature of the loss and the chart of eligible losses.

Spouse’s AD&D Insurance

You can purchase up to $500,000 of optional spouse AD&D insurance in multiples of $25,000.

Child AD&D Insurance

You can purchase up to $25,000 of optional child AD&D insurance in multiples of $5,000.

Eligible Losses and Benefits

If a covered person is seriously injured or killed in an accident, the benefit will be based on a chart of eligible or qualifying losses and on the coverage amount you’ve chosen.

Business Travel Accident Insurance

In addition to your basic employee AD&D insurance, Schlumberger also provides business travel accident insurance equal to 4.5 times your eligible compensation to a maximum of $1 million (in the event of your accidental death). This coverage pays a benefit in the event you die or suffer dismemberment as a result of an accident while travelling on Schlumberger business. This is a taxable benefit.

Evidence of Insurability

You may choose any level of AD&D insurance at any enrollment. You do not need to provide evidence of insurability for this benefit.

18 Your Flexible Benefits Program

Choosing Your Accident CoverageAccidental death and dismemberment insurance is not a replacement for life insurance – it only provides a benefit if injury or death comes as the result of an accident. Nevertheless, the decision-making process is similar. Even though it is difficult to predict an accident, your lifestyle should be taken into consideration when choosing your accident insurance. Do you engage in extreme sports? Do you spend a lot of time driving? Are you single with only yourself to depend on financially? Are you the family’s primary wage earner? What would the loss of a particular ability mean to your capacity to support yourself

(and your family)? To determine your accident insurance needs, you also need to consider what would happen if you or your dependents were injured and unable to work. What impact would this have on your family situation and finances? Consider, as well, potential changes to your lifetime income and unexpected or increased expenses as a result of the accident – home or vehicle modification and ongoing medical and rehabilitation costs should you suffer a severe lifetime injury.

Disability PlansThe long-term disability (LTD) plan works with your short-term disability (STD) plan to provide income protection if you are ill or injured and unable to perform all of your regular job duties for a prolonged period of time.

Short-Term Disability (STD) PlanSchlumberger Canada pays for this benefit and provides it automatically to help you avoid financial hardship in the event you become disabled and cannot work due to a non-work-related injury, illness or disease that exceeds five consecutive work days. If you are unable to perform the essential job duties, the STD plan provides you with 100% of your base salary for the first 6 months (26 weeks) of your disability and 80% of your base salary for the remaining period to a maximum of 12 months (27 to 52 weeks). This includes Cameron Group field direct employees who receive base pay and overtime.

Legacy Schlumberger field direct employees who receive a larger portion of their compensation as variable pay receive 130% of their base pay for the first 6 months (26 weeks) of disability and 110% of base salary for the remaining period to a maximum of 12 months (27 to 52 weeks). These include employees who work directly at wellsite and may be classified as:

� Operators;

� Equipment operators; and

� Field specialists (e.g., directional drillers).

This income is taxed, just like your pay.

Long-Term Disability (LTD)If your disability continues beyond your 12 months of STD benefits and you are approved for LTD benefits, the LTD plan will continue a portion of your income. You have four LTD options from which to choose:

� Option 1 provides you with basic coverage and is a low-cost option.

� Option 2 and 3 provides you with enhanced coverage, and it may be the right choice for you if you have a number of financial responsibilities but do not need the inflation protection that Option 4 provides.

� Option 4 provides you with enhanced coverage plus inflation protection – likely the ideal option for young families with significant current and future financial obligations.

What is the difference?Option 4 provides an indexing of your disability payments. Indexing means your disability payment will increase with inflation to a maximum of 3% per year. If you select Option 1, 2 or 3 and become disabled, your disability payment remains unchanged for the entire length of your disability.

Short-term DisabilityPlease refer to Enrollment Central to review the short-term disability policy.

Your Flexible Benefits Program 19

Paying for your LTD coverageThe prices are based on a flat rate per $100 of coverage and your eligible compensation. You do not receive flex dollars for this benefit, and you pay for it with after-tax payroll deductions. Therefore, if you are approved for LTD benefits, your income benefit is tax free.

Alternatively, you can pay for your LTD option with excess flex dollars that you direct to your Personal Spending Account. Personal Spending Account flex dollars are taxable, which means that any LTD benefits you may receive will remain tax free.

Your eligible compensationFor employees with more than one year of service, eligible compensation is defined as the greater of last year’s admissible compensation or this year’s base salary. For employees with less than one year of service, your eligible compensation is your base salary only.

LTD options

What Is Eligible Compensation?Eligible compensation is the greater of your current year’s base pay or your prior year’s admissible compensation. Your eligible compensation is used to determine your life and accident insurance benefits.

What Does Admissible Compensation Include?Admissible compensation includes base pay, overtime, bonuses, commissions and geographical coefficients.

What Does Base Pay Include?Base pay includes your salary or regular hourly pay.

Option 1 Option 2 Option 3 Option 4

Formula for monthly disability benefit

55% of first $3,000 of eligible compensation+40% of remainder

60% of first $3,000 of eligible compensation+50% of next $4,000+45% of remainder

65% of first $7,500 of eligible compensation+50% of remainder

65% of first $7,500 of eligible compensation+50% of remainder

Indexing None None None Yes, based on Consumer Price Index, to a maximum of 3% per year

Monthly maximum benefit

$15,000 per month $15,000 per month $15,000 per month $15,000 per month

20 Your Flexible Benefits Program

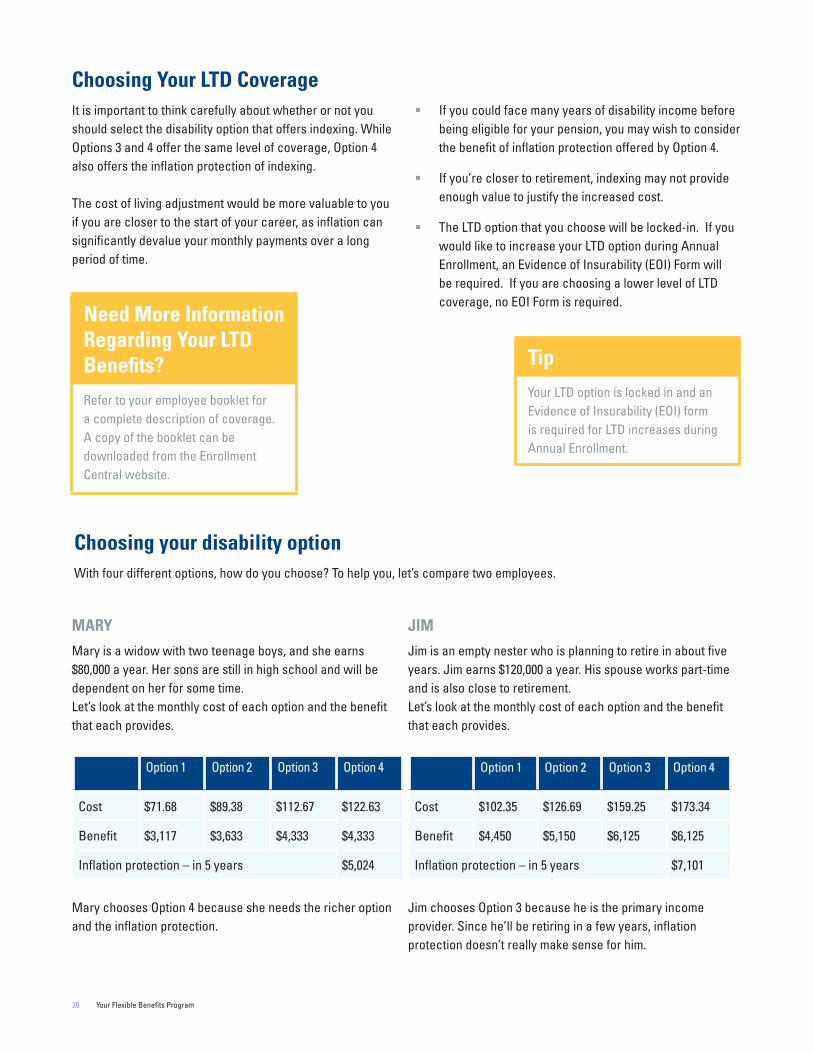

Choosing Your LTD CoverageIt is important to think carefully about whether or not you should select the disability option that offers indexing. While Options 3 and 4 offer the same level of coverage, Option 4 also offers the inflation protection of indexing.

The cost of living adjustment would be more valuable to you if you are closer to the start of your career, as inflation can significantly devalue your monthly payments over a long period of time.

� If you could face many years of disability income before being eligible for your pension, you may wish to consider the benefit of inflation protection offered by Option 4.

� If you’re closer to retirement, indexing may not provide enough value to justify the increased cost.

� The LTD option that you choose will be locked-in. If you would like to increase your LTD option during Annual Enrollment, an Evidence of Insurability (EOI) Form will be required. If you are choosing a lower level of LTD coverage, no EOI Form is required.

Choosing your disability optionWith four different options, how do you choose? To help you, let’s compare two employees.

MARY

Mary is a widow with two teenage boys, and she earns $80,000 a year. Her sons are still in high school and will be dependent on her for some time. Let’s look at the monthly cost of each option and the benefit that each provides.

Option 1 Option 2 Option 3 Option 4

Cost $71.68 $89.38 $112.67 $122.63

Benefit $3,117 $3,633 $4,333 $4,333

Inflation protection – in 5 years $5,024

Mary chooses Option 4 because she needs the richer option and the inflation protection.

JIM

Jim is an empty nester who is planning to retire in about five years. Jim earns $120,000 a year. His spouse works part-time and is also close to retirement. Let’s look at the monthly cost of each option and the benefit that each provides.

Option 1 Option 2 Option 3 Option 4

Cost $102.35 $126.69 $159.25 $173.34

Benefit $4,450 $5,150 $6,125 $6,125

Inflation protection – in 5 years $7,101

Jim chooses Option 3 because he is the primary income provider. Since he’ll be retiring in a few years, inflation protection doesn’t really make sense for him.

Need More Information Regarding Your LTD Benefits?Refer to your employee booklet for a complete description of coverage. A copy of the booklet can be downloaded from the Enrollment Central website.

TipYour LTD option is locked in and an Evidence of Insurability (EOI) form is required for LTD increases during Annual Enrollment.

Your Flexible Benefits Program 21

Optional Critical Illness CoverageThe diagnosis of a critical illness can be overwhelming – a time of uncertainty, navigating the health care system as well as managing your own fears and emotions. It’s a time when you want to focus on getting well; however, treatment and recovery can come with a number of financial costs.

Critical illness insurance provides you with a tax-free lump sum that you can spend how you choose. This may include treatment outside of Canada, or treatments not covered by your provincial health care plan, child care, travel to a regional treatment centre, meals and parking costs when attending treatment, new or experimental drugs, as well as lost income for a family member to support the patient.

The fact is, some serious illnesses can last for months or years and financial support is important to protect you and your family.

This coverage is optional. If you choose critical illness coverage, you’ll pay for it through payroll deductions. It’s available for you and your spouse in units of $10,000, starting at $20,000 to a maximum of $250,000. New employees may select up to $50,000 in coverage without providing evidence of insurability (EOI). You may also select up to $50,000 for the 2017 benefit year as this is the first year that optional critical illness insurance is being offered, without providing evidence of insurability. Any future increases to your coverage, regardless of the amount, will also require EOI. Premiums are based on your gender, age and smoking status.

You can also purchase $5,000 in critical illness coverage for your child(ren).

This coverage goes into effect 90 days after the beginning of the year in which coverage begins.

There are additional restrictions and you can find more information on Schlumberger Enrollment Central (slb-benefits.ca) on the Insurance and Disability screen.

� Aortic surgery

� Bacterial meningitis

� Benign brain tumour

� Blindness

� Cancer (life-threatening)

� Coronary artery bypass surgery

� Deafness

� Dementia, including Alzheimer’s disease

� Heart attack

� Kidney failure

� Loss of independent existence

� Loss of limbs

� Loss of speech

� Major organ transplant

� Motor neuron disease

� Multiple sclerosis

� Paralysis

� Parkinson’s disease and specified atypical parkinsonian disorders

� Stroke

� Cerebral palsy

� Congenital heart disease

� Cystic fibrosis

� Down syndrome

� Muscular dystrophy

� Type 1 diabetes mellitus

What Does This Look Like?If you are earning $5,000 a month, pre-tax, and you are eligible for long-term disability benefits, you will receive $3,000 a month, tax free. Play with the enrollment tool to get details on how much you need to pay.

Covered Illnesses Include

For Children

22 Your Flexible Benefits Program

Total Health IndexYour THI tells you what you need to do to improve your wellness; your Personal Spending Account will help you make it happen.

Be Sure to Take Your Total Health Index AssessmentThe Total Health Index (THI) is a great way to understand how your lifestyle affects your wellness and how even small changes can improve your well-being.

This isn’t a one-time thing. You can retake the assessment as your behaviours change. Think of it as your personal wellness record. Let it capture your success.

It’s confidential, too. In fact, the THI is managed by the same people who operate our employee assistance program. Schlumberger will never see anyone’s individual results.

Ready to Understand Your Health Risks?1. Go to www.thidiscoveryinsight.com/Schlumberger

2. If it’s your first time, you need to create a profile.a. Enter your email b. Complete the profile that will include your name,

gender, age, location, language, and password.

3. Complete the questionnaire and check out some of the suggested resources for help in addressing your health risks.

Your Leftover Flex DollarsWhen you enroll, your flex dollars and payroll deductions will be assigned automatically to pay for your coverage.Depending on the options you’ve selected, you may have remaining flex dollars to spend that you could choose to have deposited in your Registered Retirement Savings Plan (RRSP), your Health Care Spending Account (HCSA) or your Personal Spending Account (PSA).

Your Retirement Savings PlanThe Registered Retirement Savings Plan (RRSP) is a great option if you’re focused on saving for retirement. If you choose to divert left over flex dollars to an RRSP, the amount will be deposited on the first pay period of the year. You must divert a minimum of $25 flex dollars to the RRSP and will be required to enroll in an RRSP account with Sun Life. If you do not enroll in an RRSP account with Sun Life within the specified time given at Annual Enrollment, your RRSP contribution will be diverted to the Personal Spending Account. Note, the option to divert left over flex dollars to your RRSP is only available once per year, during Annual Enrollment”.

Your Flexible Benefits Program 23

Your Health Care Spending AccountThe Health Care Spending Account (HCSA) can be used to reimburse yourself – tax free (except in Quebec) – for dental and extended health care expenses that are not covered or fully covered by Schlumberger Flex or your provincial health program. It’s a tax-effective way to spend unused flex dollars. (If you live in Quebec, the value of claims reimbursed from the HCSA will be taxed at your provincial income tax rate.)

You also can submit claims for any dependents who are eligible for coverage under Schlumberger Flex, plus claims for additional relatives who live with you and are financially dependent on you. An example might be an elderly parent or sibling.

Why Is This Account So Valuable?For example, if you are in a 39% tax bracket, you will only have $61 to spend from every $100 you earn. However, if you put 100 flex dollars into your HCSA, you’ll have the full $100, tax free, available to spend on eligible expenses.

Here’s an overview of how your HCSA works

The flex dollars you allocate to your HCSA will be deposited in a lump sum each January 1. You may submit claims for eligible dental and health care expenses for yourself and any eligible dependents. All reimbursements will be tax free (except in Quebec). In exchange for the tax-free status of your reimbursement, the Canada Revenue Agency imposes several rules on this account:

� You have two years to use each year’s flex dollar contribution or you forfeit the unused balance at the end of the second year. You must claim expenses in the year they occur. Your deadline to file claims is 90 days after December 31 each year.

� Once flex dollars are deposited into the account, they may not be withdrawn except to reimburse eligible health and dental expenses.

� If your employment ends, you have 90 days to submit eligible claims that are incurred up to your last day at work. You will forfeit any remaining balance.

Examples of Eligible ExpensesYou can use your HCSA to pay for:

� 40% of basic dental services if you have dental coverage under Option 1;

� 10% of prescription drugs if you have extended health care coverage under Option 2;

� The dispensing fee deductible you pay under all three options for extended health care;

� Any portion of the cost of prescription eyeglasses, contact lenses or prescription sunglasses not covered under the plan;

� Dental expenses for dentures and orthodontia that are not fully covered by the plan;

� Any item listed as tax deductible under the Income Tax Act and related regulations; and

� Adaptive devices for hearing- or sight-impaired individuals (e.g., for a computer or telephone).

TipYou can use your Health Care Spending Account to pay for certain expenses that are not covered, or are only partially covered, by your dental and extended health care options.

24 Your Flexible Benefits Program

Your Personal Spending Account Feeling and being well often involves more than taking care of your basic health and medical needs. Sometimes it means making a lifestyle change, and sometimes you need a little help. That’s what Schlumberger’s Personal Spending Account (PSA) offers – access to programs that will help you improve your wellness – your physical and financial wellness.

When you allocate your excess flex dollars to this account, they can be put towards a range of expenses such as allergy and cholesterol screenings, smoking cessation, financial planning, nutritional counselling, pregnancy or orthopedic expenses, as well as alternative medicine and exercise specialists.

Note that these services must be provided by an accredited professional.

How Your Personal Spending Account WorksSetting up and using your Personal Spending Account is easy. Each year, during annual enrollment, you can allocate some or all of your leftover flex dollars after you have selected your other health and dental coverage, including your Health Care Spending Account. The amount you put in your Personal Spending Account will be deposited at the beginning of January, and at that time you can start to use your flex dollars right away. You can use your Personal Spending Account for your dependents’ expenses too.

Like your HCSA, you have two years to use any allocation you make to your PSA.

This Is a Taxable AccountUnlike your HCSA, your PSA is taxable. The amount of taxable benefit associated with your expense reimbursements will be reported on your T4 slip.

You pay tax only on your reimbursed expenses – not on your allocation to the account.

Submitting ClaimsYou must submit your PSA claims using the printed form available on Enrollment Central and on the Sun Life website at mysunlife.ca.

Like your HCSA, your PSA claims must be received by Sun Life within 90 days of the end of the calendar year.

TipYour Personal Spending Account isn’t just about services. You can also be reimbursed for fitness classes, exercise equipment, fitness league fees and comprehensive medical exams using your flex dollars. And, if you prefer to relieve some of your other costs, you can also use your Personal Spending Account to pay for Schlumberger Flex LTD premiums.

Your Flexible Benefits Program 25

Eligible ExpensesThe Schlumberger Flex PSA provides reimbursement for expenses that are not eligible under your provincial plan, your Schlumberger Flex options or your HCSA. Things like:

� Acupressurists

� Allergy tests

� Annual golf memberships

� Athletic therapists

� Chinese medical practitioners

� Cholesterol and hypertension screening

� Comprehensive medical exams

� Estate planning

� Exercise equipment (excluding clothing and footwear)

� Exercise physiologists

� Fees associated with maintaining a professional designation

� Financial planning

� Fitness classes

� Fitness league fees

� Golf clubs

� Green fees

� Health assessments/screening

� Health education products (e.g., smoking cessation products)

� Health education programs (e.g., smoking cessation, weight loss, stress management)

� Healthy cooking classes

� Herbalists

� Hobby and general interest classes

� Homeopaths

� Language training

� Life and Critical Illness insurance premiums

� Long-term disability premiums

� Maternity services (e.g., prenatal classes, midwife services)

� Nutritional programs or counselling

� Occupational therapists

� Orthopaedic beds and orthopaedic pillows

� Osteopathic practitioners

� Personal computer and accessories

� Professional membership fees or dues

� Reflexologists

� Shiatsu therapists

� Tax preparation

� Tuition fees for university, college or continuing education (including books and supplies)

� Tutoring

� Vitamins and supplements (including herbal) and naturopathic medicines

� Will preparation

Not Sure If It’s Covered?Call the Schlumberger Canada Benefits Centre at 1-866-557-5222, from Monday to Friday, 6:30 a.m. to 3:00 p.m. (Mountain time), for more information.

26 Your Flexible Benefits Program

Claiming Your LTD Premiums?You’ll need to submit a copy of your pay stub with a completed Personal Spending Account claim form. You’ll find claim forms on the Sun Life website at mysunlife.ca

Using Schlumberger Flex and Making Changes Schlumberger Flex is designed to let you make changes as the needs of you and your family change.

Changing Your Choices During Annual EnrollmentYour benefit choices will apply for one plan year: from January 1 to December 31. Each fall you will have an opportunity to re-enroll and change the options and coverage for yourself and your dependents for the next calendar year. Employees who don’t re-enroll each year will default to the options listed on page 4.

Changing Your Choices as a Result of an Eligible Life EventDuring the year, you may enroll and/or change your options if one of the following events occurs:

� Marriage, civil union (Quebec) or a common-law relationship of six months or more;

� Divorce, separation or end of a common-law relationship;

� Addition of an eligible dependent child;

� Loss of a child’s status as a dependent (marriage, age limit, leaves school, etc.);

� Your spouse gains or loses benefits coverage; or

� Death of a spouse or child.

You are responsible for visiting the Employee Self Service website to update your dependents and coverage within 30 days of the event; otherwise, you must wait until the next annual enrollment or another life event. Your new coverage and any payroll deductions will be retroactive to the date of the event.

Life Events and Unused Flex DollarsIf you change your coverage during the year and you originally had unused flex dollars, there may be a temporary adjustment to your payroll deductions for the balance of the year. At the next annual enrollment, you can adjust how you spend your unused flex dollars.

Submitting ClaimsThese are the deadlines to submit claims:

� Health Care Spending and Personal Spending Accounts: Submit claims within 90 days of the end of the year in which the expense occurred.

� Dental and extended health care plans: Submit claims within 90 days of the end of the year in which the expense occurred (or earlier if you plan to claim the balance from your HCSA).

Which Plan?Let’s say Mike’s birthday is February 9 and his spouse Martha’s birthday is January 9. In this case, any expenses incurred by their children should be submitted to Martha’s plan first.

Your Flexible Benefits Program 27

Coordination of Benefits: Submitting Claims to Two Benefits PlansYour Opportunity for 100% Reimbursement

If your spouse has benefits from an employer, you can usually coordinate the two benefits plans (check the wording of your spouse’s plan). This means you may submit your receipts to both plans and get up to 100% of your eligible expenses reimbursed.

If you plan to submit claims to your benefits plan and your spouse’s benefits plan, insurance industry guidelines determine where to send claims first. The order is important! After submitting your receipts to the first plan (or using your pay-direct drug card), you will receive your reimbursement and an Explanation of Benefits statement. Next, submit the Explanation of Benefits along with a new claim form to the second plan to claim the balance of your expense.

These are the insurance industry guidelines when submitting claims:

Your claims: Submit them to your Schlumberger Flex plan first.

Your spouse’s claims: Submit them to your spouse’s own plan first.

Children’s claims:

� If your birthday is earlier than your spouse’s in the year, submit them to the Schlumberger Flex plan first.

� If your spouse’s birthday is first in the year, submit them to your spouse’s plan first.

A Coordination of Benefits Example

Let’s consider Tom, who works at Schlumberger, and his spouse Sarah, who has extended health care and dental coverage through another large Canadian employer.

Tom has selected extended health care Option 1. Yesterday, Tom filled a prescription for a drug that cost $100 (after the dispensing fee). Since Tom chose Option 1, the extended health care plan will pay 60% (or $60) of the claim. After Schlumberger’s plan administrator (Sun Life) pays Tom’s part of the claim, he can then submit the expense to Sarah’s plan to have the other $40 reimbursed.

The coordination of benefits feature allows Tom to maximize his extended health care and dental claim reimbursements by combining his coverage with the coverage his spouse has at her company. Of course, Tom could also have the $40 reimbursed from his HCSA if he has excess flex dollars in his account, but he is better off claiming against his spouse’s plan first and saving his HCSA balance for other expenses.

TipIf you and your spouse both have pay-direct drug cards, ask the pharmacist if he or she can submit your claim to both plans at the same time. This is possible at most pharmacies.

28 Your Flexible Benefits Program

TipYou can go online and model different enrollment choices to see your flex dollars and prices. You can “cancel” your changes as you leave the website. If you’re not decided, you can “Save as Draft” and “Confirm” them when you are sure.

Enroll Online in Your Flexible Benefits

You can enroll at work, at home or anywhere you have Internet access. To ensure that you have the coverage that is right for you, follow these steps.

1. Review Your Coverage ChoicesBefore you go online to enroll, be sure you understand your choices and have reviewed your spouse’s benefits plan. Look at last year’s claims and any out-of-pocket medical and dental expenses you may have had.

2. Decide What Coverage You Need If you have enrolled in Schlumberger Flex before, when you go online, the Employee Self Service website will show you your current coverage and your dependents (if any) who will be covered, unless you change and “confirm” your choices.

If it’s your first time enrolling, you will see the Schlumberger Flex default coverage with the corresponding flex dollars, prices and payroll deductions.

� If you change your coverage, the amounts will change accordingly.

� If you do not enroll by your deadline, you will be enrolled in the default coverage automatically.

3. Enroll at Employee Self ServiceTo log on, visit https://schlumberger.seb-admin.com or Enrollment Central.

4. Once You Are in the SiteThe main page of the Employee Self Service website will greet you by your name. You will see a link called “Enroll Now!” that allows you to begin your enrollment. Please click on this link and then simply follow the instructions on the website to complete your enrollment in Schlumberger Flex.

When you go online to enroll, please review your beneficiary designations and update this information as needed. If you change your beneficiaries online, you must print, sign and mail the form to the address shown. Your new beneficiary information will not be valid until the form has been received. Print, Complete and Return Forms (If Prompted)

Some forms require an original signature:

� Beneficiary Designation Form

� Evidence of Insurability Form

If prompted, print and complete one or both of these forms, sign them and mail them to the address on each form.

Are You a New Employee?The choices you make during enrollment will be in effect from your start date until the end of the year. You can make changes for the new benefits year (starting January 1) at our next annual enrollment period. If you are hired after the annual enrollment period, you will first enroll for the current year’s benefits and will then immediately be prompted to enroll for the following year.

Review Your Coverage at Any TimeYou may visit Employee Self Service at any time to check your coverage, dependents and beneficiaries.If you have a life event, visit the website within 30 days to register the life event and update your benefits coverage.

Your Flexible Benefits Program 29

Questions?

The Schlumberger Canada Benefits Centre (1-866-557-5222) is available to answer questions about your benefits or enrolling. They’re available Monday to Friday, from 6:30 a.m. to 3:00 p.m. (Mountain time).

AccessYou can access your account via the Employee Self Service website without login if you’re on the Schlumberger intranet. If you are using external computer and no intranet, you will need to enter your LDAP email and LDAP password to login.

Miss The Deadline?Once your window for enrollment closes, the next opportunity to make changes will be at your next annual enrollment the following fall. You’ll be able to choose new coverage for the next plan year at that time.

You also can change your coverage any time you experience a life event (e.g., get married or have a baby). See page 29 for details.

The Schlumberger Canada Benefits Centre https://schlumberger.seb-admin.com

1-866-557-5222

SLB Flex Guide EN 09/19