You & Your Money Class 3, Part 1 – Your Credit International Center at Catholic Charities...

36

You & Your Money Class 3, Part 1 – Your Credit International Center at Catholic Charities Community Services December 2013 Instructor: Virginia Guilford

-

date post

20-Dec-2015 -

Category

Documents

-

view

215 -

download

3

Transcript of You & Your Money Class 3, Part 1 – Your Credit International Center at Catholic Charities...

You & Your MoneyClass 3, Part 1 – Your Credit

International Centerat Catholic Charities Community Services

December 2013Instructor: Virginia Guilford

Class Schedule

2

• Class 1 - Thursday December 5, 3:30 -5 PM– Your Income– Your Taxes

• Class 2 – Thursday December 12, 3:30 -5 PM– Your Budget– Your Bank Accounts

• Class 3 – Thursday December 19, 3:30 -5 PM– Your Credit– Learning More

Please Be Aware

• This course does not give you professional advice– I am not a lawyer.– I am not an accountant.– I am not a banker.

• This course explains the basic concepts and vocabulary that you need for understanding work, taxes, budgeting, banking and credit.

3

Your Credit

• A lender will generally loan you money if:– You have a regular, verifiable source of income– You have a good credit score.

• Sometimes, the lender also wants to have an extra guarantee that you will pay the money back– Security– Collateral

4

Managing Credit

• Good Credit vs Bad Credit • How Much Debt is Too Much?

– No more than 28% of your gross income should go to paying all debt for home ownership (mortgage payment, property taxes and home owner’s insurance).

– No more than 36% of your gross income should go to all debt: your home ownership debt plus credit card debt and auto loans.

5

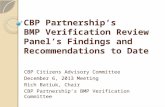

Your Credit Score• Your credit score is based on five

factors, each weighted differently.– Payment History – 35% - how

good you are at always paying your bills on time.

– Amount Owed – 30% - how much you owe.

– Length of Credit History – 15% - how long you have been using credit.

– New Credit – 10% - how much credit have you recently asked for.

– Types of Credit Used – 10% - how many different types of credit do you have.

6

Your Credit Score

• Credit Scores range between 300 – 850– 780 to 850 – Excellent– 720 to 780 – Very good, above average– 650 to 720 – Average, OK– Under 650 – Not so good, ‘sub-prime’

Improving Your Credit ScoreTo improve your credit score:• Pay your bills on time. • Keep your credit card balances low, ideally,

below 25% of your available credit limit. • Increase the length of your credit history by

keeping the same credit card for a long time. • Minimize the frequency of new card requests.

Don’t sign up for a lot of new credit cards. • Keep a combination of different types of debt

– car loans and mortgages and credit cards.

8

Credit Reporting Agencies Credit reporting agencies are required to

provide you with a free copy of your credit report once a year.

The three main credit reporting agencies:

• Experian

• Equifax

• TransUnion

9

The web site Annual Credit Report can show you how to make this request. www.annualcreditreport.com/cra/index.jsp

Consumer Credit

• Bank Credit Cards• Bank Debit Cards• Store Credit Cards• Pre-paid Debit Cards

10

Bank Credit Cards

• How do Credit Cards Work?– Accepted widely; many locations in the US

and Worldwide– You receive your purchase, payment is not

due until the next billing date– If you don’t pay the whole amount, you will

owe interest on the remaining amount due

• Rewards Cards– Frequent flier miles– ‘Points’ good for purchases– Cash back

11

Choosing a Credit Card• Things to Consider When Choosing a Card

– APR (Annual Percentage Rate) or Finance Charge (Average for all credit cards is about 14%

– Balance Calculation Method– Grace Period– Fees

• Web Sites to Help You Choose a Card– www.credit.com– www.CreditCardConnection.org – www.LowCards.com

12

Bank Debit Cards

• Bank Debit Cards are not credit cards.– Debit cards can be used in many places that take

credit cards.– The payment is taken immediately from your bank

account.

13

Store Credit Cards

• Can only be used in the store that issued the card.

• Don’t open a store credit account unless you really need it and will use it.

• Too many store credit card accounts may reduce your Credit Score.

14

Prepaid Debit Cards

• Examples– Green Dot Visa or MasterCard– Rush Visa– Net Spend Visa or MasterCard

• Technically, not credit cards at all• You purchase the card with cash, and

then use the card until it is empty.• Most Prepaid debit cards charge a

monthly fee.

15

Other Kinds of Credit

• Mortgages

• Auto Loans

• Student Loans

16

Mortgages

• Down Payment• Term Length• Mortgage Rate – Fixed or ARM• Interest or Principal• Risk of Foreclosure

17

Mortgage Down Payment

• Down Payment – a percentage of the value of the home paid in cash– The down payment proves to the bank that you

are disciplined enough to be able to save money– A bigger down payment means less that you need

to borrow with the mortgage

18

Mortgage Term Length

• Term Length – the amount of time that you have to pay back the mortgage– A mortgage usually gives you a longer time than

other kinds of debt• 15 years• 20 years• 30 years

19

Mortgage Rate

• Mortgage Rate – Fixed– Rate is fixed for the entire term of the mortgage– Is good if you want to know for sure how much you will have to pay

each month

• Mortgage Rate – ARM– Rate is adjustable and can change.– Often starts at a low rate, but can increase– Some ARMs have a limit on the amount of increase, or when the first

increase can occur– Might be good if you are only planning to live there for one or two

years

20

Mortgages – Interest & Principal

• Interest – the amount you are paying extra as a charge for the loan

• Principal – the basic amount that you borrowed• Each mortgage payment will include some payment

for interest, and some payment against the principal. – The balance between principal and interest in each

payment will change over the life of the mortgage.– If you ever get extra money, you might make an extra

mortgage payment. But make sure that the payment goes toward paying off the principal that you owe.

21

Mortgages - Foreclosure

• Risk of Foreclosure• Your home is used for collateral for your

mortgage• If you stop making your mortgage payments,

or if you don’t make your payments on time, the bank can foreclose (take back) your home.– You can no longer live in your home– You lose all the payments you have made so far

22

Auto Loans• Your Car is your Collateral

– If you miss some car loan payments, or if your payments are late, the lender can ‘repossess’ the car

– You will lose the car– You will lose any of the payments you have made up to that date

• Auto Loan from a Bank– Check out the cost of an auto loan at your bank

• A bank auto loan may have a lower rate• Knowing what you qualify for helps in negotiations

• Auto Loan from the Car Dealership– Dealers sometimes offer a special rate, but you won’t know if it is a good

deal or not unless you can compare it to your bank’s offer

23

Student Loans

• Types of Student Loans– Federal– Private– Available from a bank, credit union, or directly

from the government

• Repayment of Student Loans– Repayment does not start until you have left school– Missing one semester may trigger the start of repayment

• Student Loans and Bankruptcy

24

Credit Card Security

• Basic Security– Keep passwords for credit & debit cards private &

secure, even in your own home.– Shred bills with account numbers or other

identifying information before discarding– Review all bills & statements regularly.– Request credit score reports – you are entitled to

a free report once a year from each of the three major credit reporting agencies

25

Signs of Identity Theft

• Signs You May be a Victim of Identity Theft – Your bank account has withdrawals that you do not recognize.– Mysterious charges appear on your bills and statements (especially

credit card bills or cell phone bills).– You get disruptive phone calls from debt collectors trying to collect on

bills that you don’t recognize.– You receive “final notice” bills in the mail for products or services

you’ve never bought.– Your credit report lists an address that you’ve never lived at.– Your credit report lists credit accounts (such as a credit card or loan)

that you’ve never applied for

26

Identity Theft• If You Think You Are a Victim of Identity Theft

– Contact the Federal Trade Commission (FTC) to report the situation at (877) 438-4338, or online at http://www.consumer.ftc.gov/features/feature-0014-identity-theft

– Contact your local Post Office, if you think that your address has been changed by someone else.

– Contact the Social Security Administration if you think that your social security number is being used by someone else.

– Contact the IRS if you suspect tax fraud.– Report your information to the fraud unit of each of the three credit

reporting companies:• Equifax - (800) 525-6285• Experion - (888) 397-3742• TransUnion - (800) 680-7289

27

You & Your MoneyClass 3, Part 2 – Learning More

International Centerat Catholic Charities Community Services

December 2013Instructor: Virginia Guilford

Learning More

• This course cannot be the final word about your finances.

• Banks and Credit Card companies are always changing.

29

Evaluating Information & Advice

• Credible Information– Believable information.– Trustable information.

• Disinterested Advice– Advice from someone who will not be affected by

what you choose to do.

30

General Sources

• finance.yahoo.com/personal-finance • money.cnn.com/pf/ • www.nytimes.com/pages/your-money/index.

html

• www.forbes.com/ • www.kiplinger.com/

31

Financial Institutions & Organizations

• www.bankofamerica.com/studentbanking/ • www.schwabmoneywise.com/home/index.php • https://

online.citibank.com/US/JRS/pands/detail.do?ID=PlanningOverview

• www.findabetterbank.com/

32

Loans & Credit Cards

• www.finaid.org/calculators/loanpayments.phtml • www.annualcreditreport.com/cra/index.jsp• www.credit.com• www.CreditCardConnection.org • www.LowCards.com

33

Government Sites

• http://www.fdic.gov/quicklinks/consumers.html• http://www.occ.treas.gov/ • www.tax.state.ny.us/• www.irs.gov • www.consumer.ftc.gov

34

Instructional Videos

• Bank of America in partnership with Khan Academy.

• Simple, conversational, self-paced videos– Understanding Credit– Home Buying– Saving and Budgeting

• http://www.bettermoneyhabits.com

You & Your Money Glossary

• Contains simple definitions of the most commonly used financial terms.

• Log on to www.virginiaguilford.com and download the Word document from the “Docs and Links” page. (The PowerPoint presentations used in this class are also available there)

• Or send your request [email protected]

36