Ying & Yen

21

Ying & Yen Carson Marries Anthony Mader Mickey Sun Edgar Torres Alex Vicente

description

Ying & Yen. Carson Marries Anthony Mader Mickey Sun Edgar Torres Alex Vicente. Ying & Yen. Carson Moko Anthony Kamakazi Mickey Sumimato Edgar Terriaki Alex Yamamuchi. Data. From 1971 to Present (Monthly) 387 Observations Federal Reserve Bank St Louis (Fred). - PowerPoint PPT Presentation

Transcript of Ying & Yen

Ying & Yen

Carson MarriesAnthony MaderMickey SunEdgar TorresAlex Vicente

Ying & Yen

Carson MokoAnthony KamakaziMickey SumimatoEdgar TerriakiAlex Yamamuchi

Data From 1971 to Present (Monthly) 387 Observations Federal Reserve Bank St Louis

(Fred)

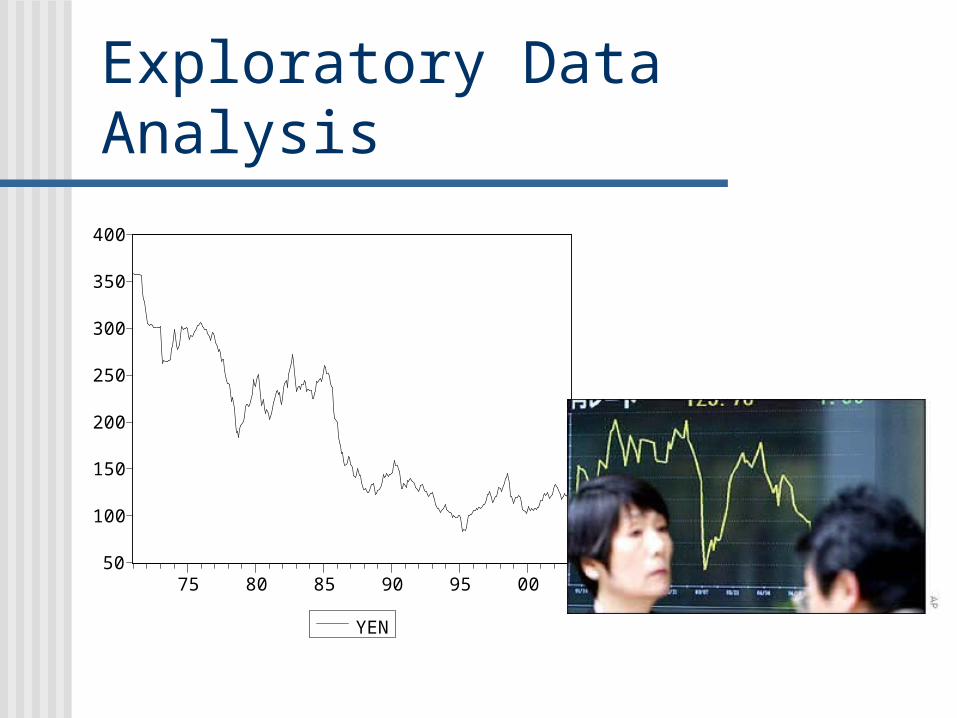

Exploratory Data Analysis

50

100

150

200

250

300

350

400

75 80 85 90 95 00

YEN

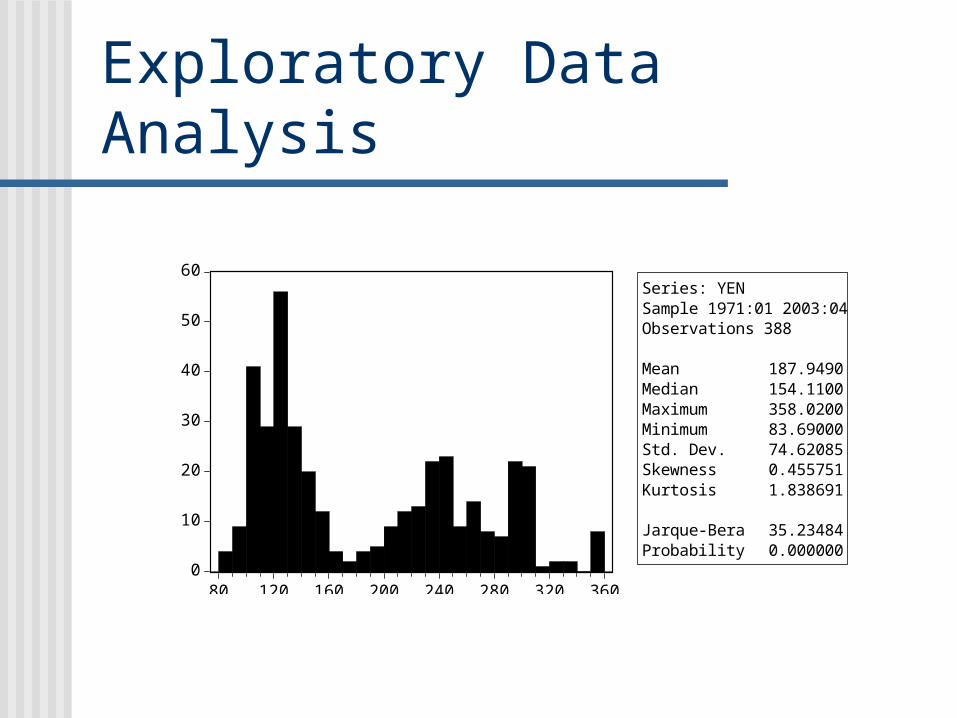

Exploratory Data Analysis

0

10

20

30

40

50

60

80 120 160 200 240 280 320 360

Series: YENSample 1971:01 2003:04Observations 388

Mean 187.9490Median 154.1100Maximum 358.0200Minimum 83.69000Std. Dev. 74.62085Skewness 0.455751Kurtosis 1.838691

Jarque-Bera 35.23484Probability 0.000000

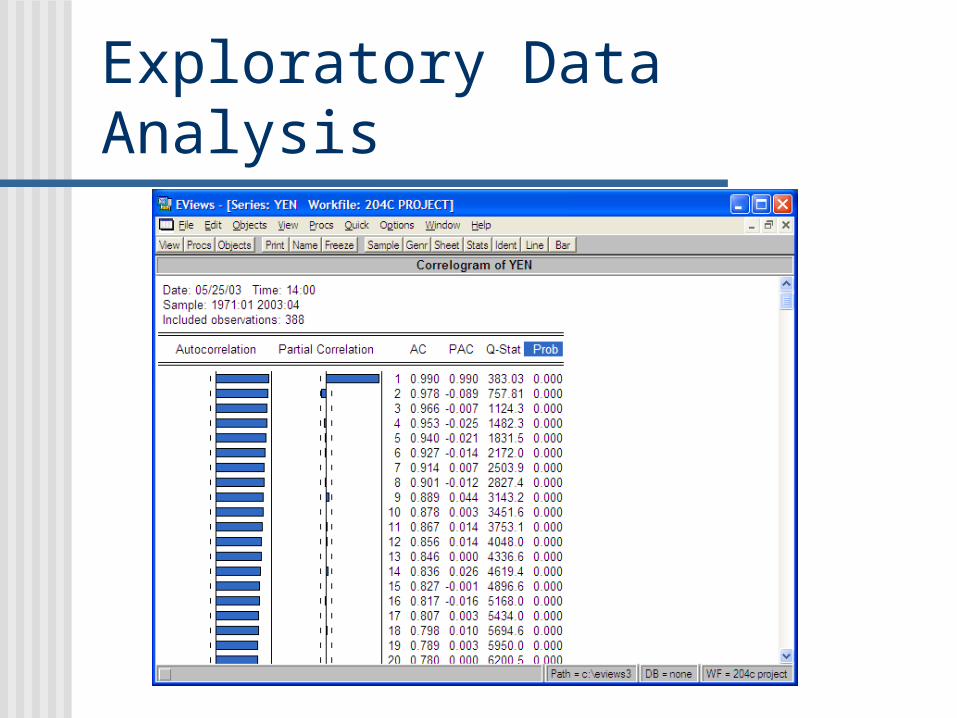

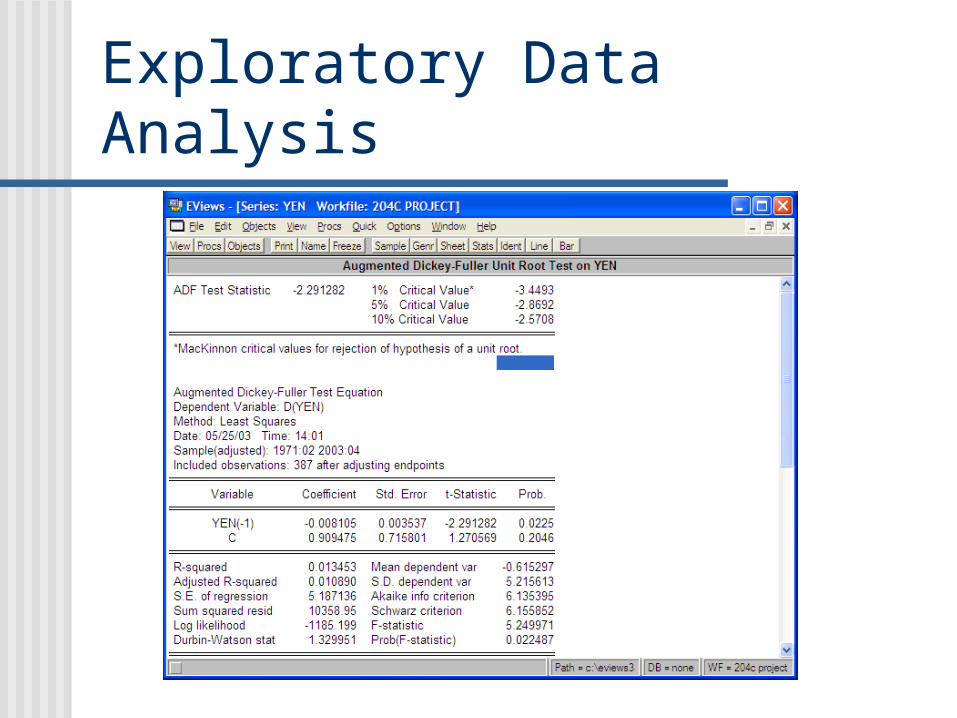

Exploratory Data Analysis

Exploratory Data Analysis

Breaking Yen into Change $ Ln, Difference Fractional Change Pre-Whitening

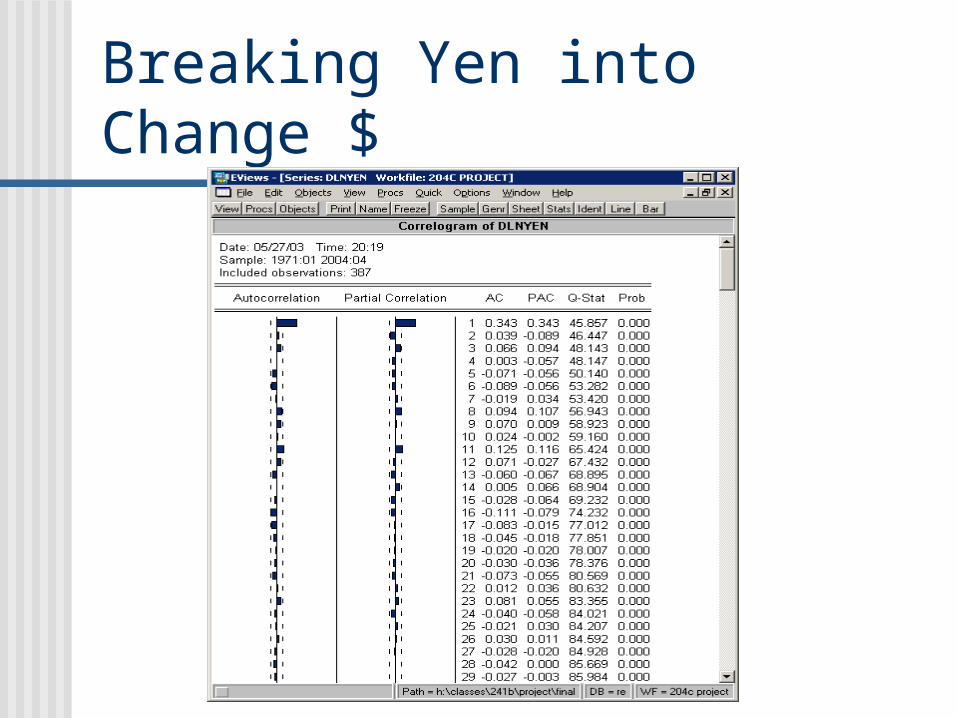

Breaking Yen into Change $

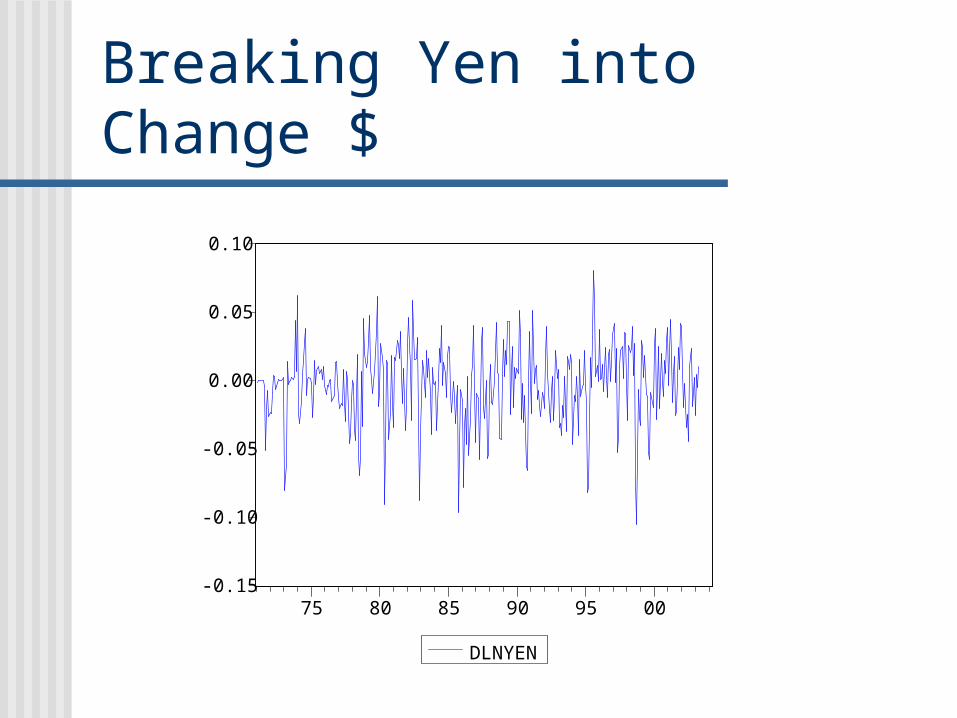

Breaking Yen into Change $

-0.15

-0.10

-0.05

0.00

0.05

0.10

75 80 85 90 95 00

DLNYEN

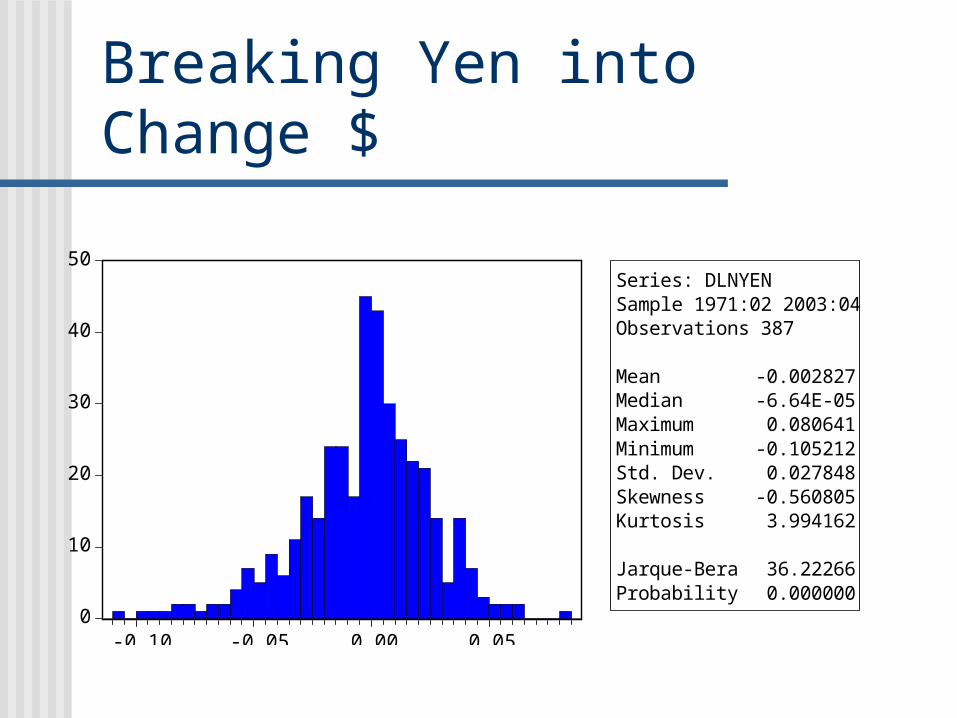

Breaking Yen into Change $

0

10

20

30

40

50

-0.10 -0.05 0.00 0.05

Series: DLNYENSample 1971:02 2003:04Observations 387

Mean -0.002827Median -6.64E-05Maximum 0.080641Minimum -0.105212Std. Dev. 0.027848Skewness -0.560805Kurtosis 3.994162

Jarque-Bera 36.22266Probability 0.000000

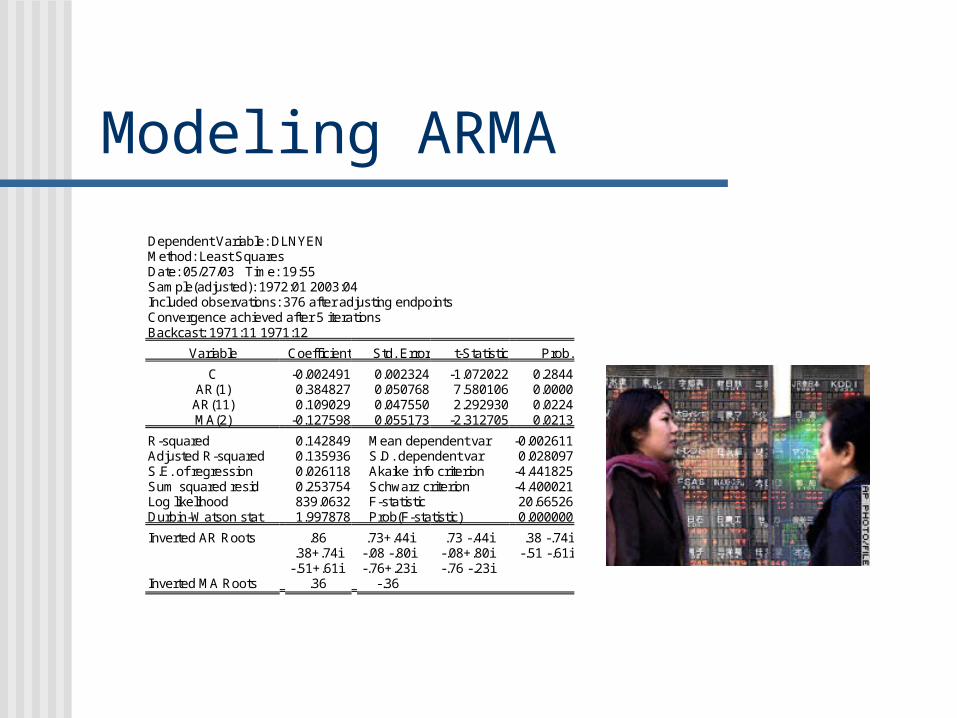

Modeling ARMA

Dependent Variable: DLNYEN Method: Least Squares Date: 05/27/03 Time: 19:55 Sample(adjusted): 1972:01 2003:04 Included observations: 376 after adjusting endpoints Convergence achieved after 5 iterations Backcast: 1971:11 1971:12

Variable Coefficient Std. Error t-Statistic Prob.

C -0.002491 0.002324 -1.072022 0.2844 AR(1) 0.384827 0.050768 7.580106 0.0000 AR(11) 0.109029 0.047550 2.292930 0.0224 MA(2) -0.127598 0.055173 -2.312705 0.0213

R-squared 0.142849 Mean dependent var -0.002611 Adjusted R-squared 0.135936 S.D. dependent var 0.028097 S.E. of regression 0.026118 Akaike info criterion -4.441825 Sum squared resid 0.253754 Schwarz criterion -4.400021 Log likelihood 839.0632 F-statistic 20.66526 Durbin-Watson stat 1.997878 Prob(F-statistic) 0.000000

Inverted AR Roots .86 .73+.44i .73 -.44i .38 -.74i .38+.74i -.08 -.80i -.08+.80i -.51 -.61i -.51+.61i -.76+.23i -.76 -.23i

Inverted MA Roots .36 -.36

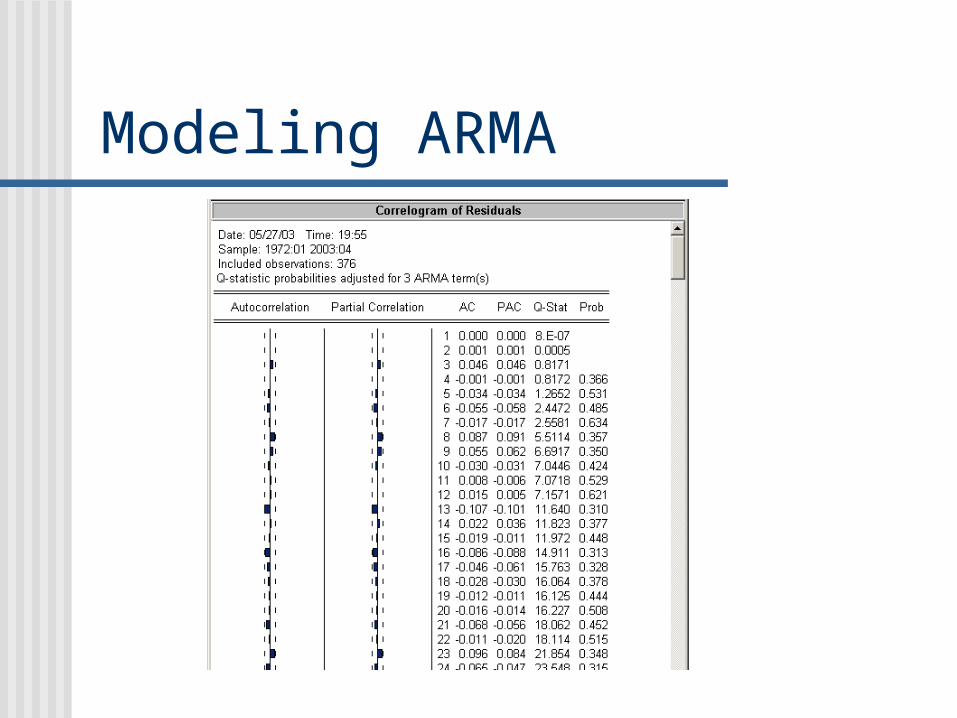

Modeling ARMA

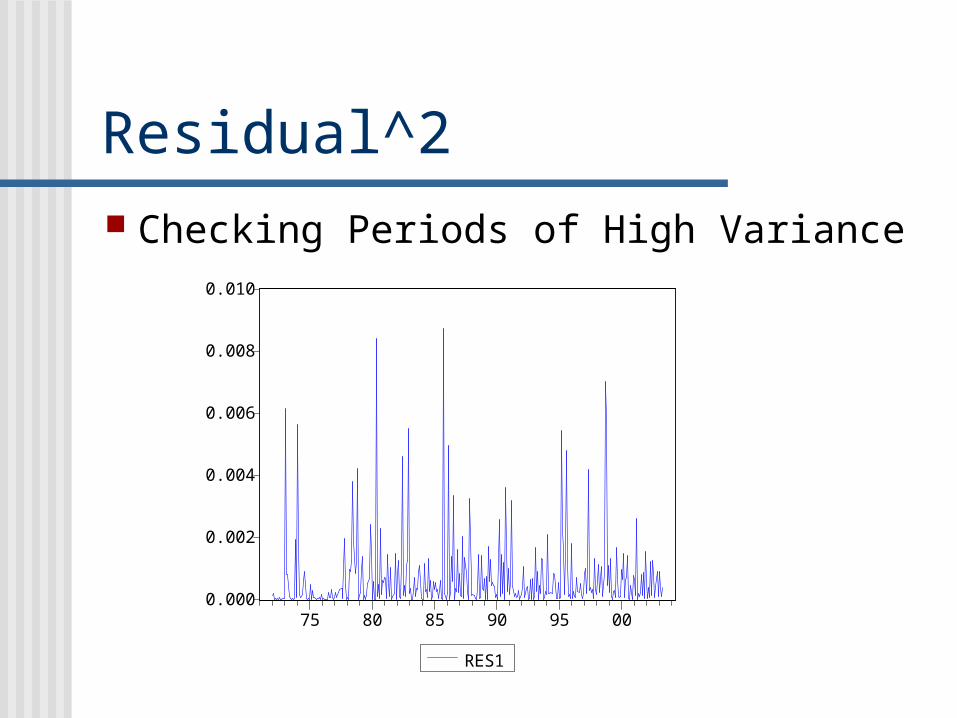

Residual^2 Checking Periods of High Variance

0.000

0.002

0.004

0.006

0.008

0.010

75 80 85 90 95 00

RES1

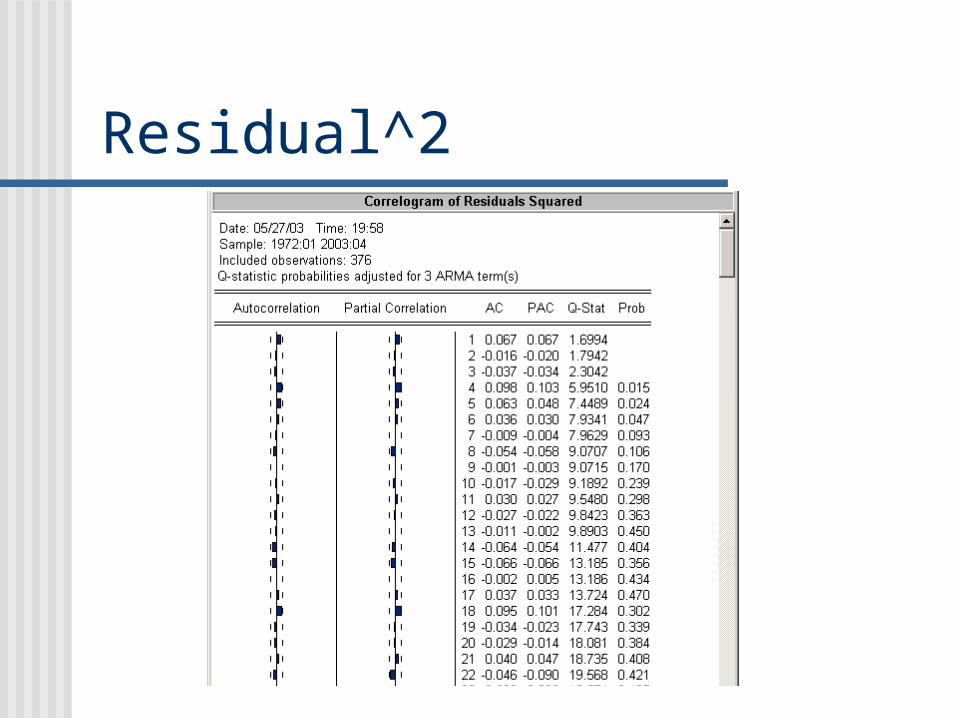

Residual^2

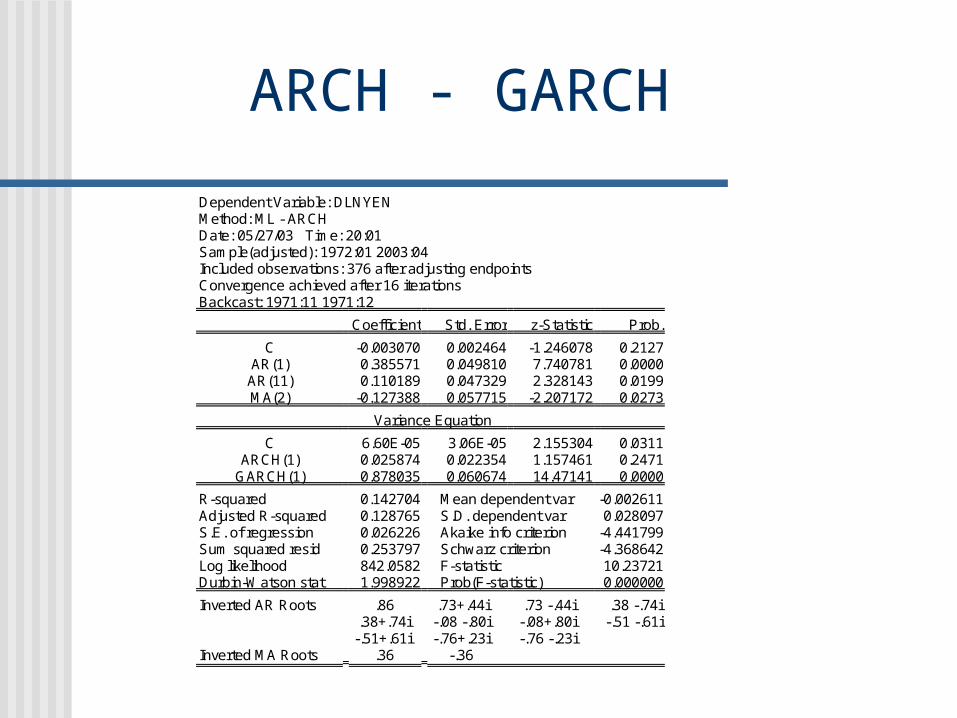

ARCH - GARCH

Dependent Variable: DLNYEN Method: ML - ARCH Date: 05/27/03 Time: 20:01 Sample(adjusted): 1972:01 2003:04 Included observations: 376 after adjusting endpoints Convergence achieved after 16 iterations Backcast: 1971:11 1971:12

Coefficient Std. Error z-Statistic Prob.

C -0.003070 0.002464 -1.246078 0.2127 AR(1) 0.385571 0.049810 7.740781 0.0000 AR(11) 0.110189 0.047329 2.328143 0.0199 MA(2) -0.127388 0.057715 -2.207172 0.0273

Variance Equation

C 6.60E-05 3.06E-05 2.155304 0.0311 ARCH(1) 0.025874 0.022354 1.157461 0.2471

GARCH(1) 0.878035 0.060674 14.47141 0.0000

R-squared 0.142704 Mean dependent var -0.002611 Adjusted R-squared 0.128765 S.D. dependent var 0.028097 S.E. of regression 0.026226 Akaike info criterion -4.441799 Sum squared resid 0.253797 Schwarz criterion -4.368642 Log likelihood 842.0582 F-statistic 10.23721 Durbin-Watson stat 1.998922 Prob(F-statistic) 0.000000

Inverted AR Roots .86 .73+.44i .73 -.44i .38 -.74i .38+.74i -.08 -.80i -.08+.80i -.51 -.61i -.51+.61i -.76+.23i -.76 -.23i

Inverted MA Roots .36 -.36

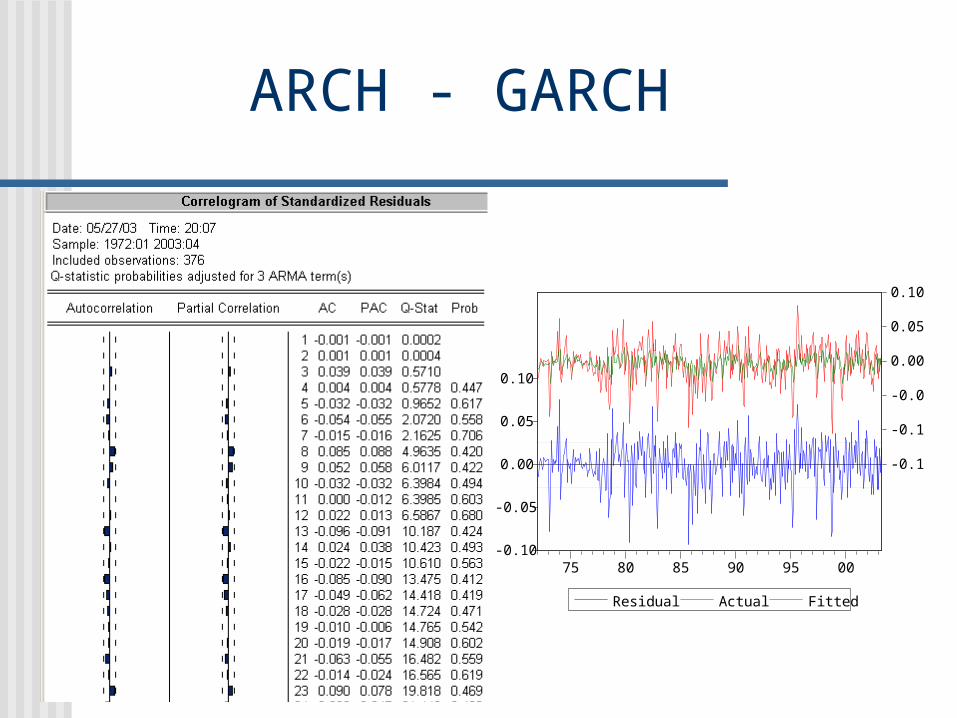

ARCH - GARCH

-0.10

-0.05

0.00

0.05

0.10

-0.15

-0.10

-0.05

0.00

0.05

0.10

75 80 85 90 95 00

Residual Actual Fitted

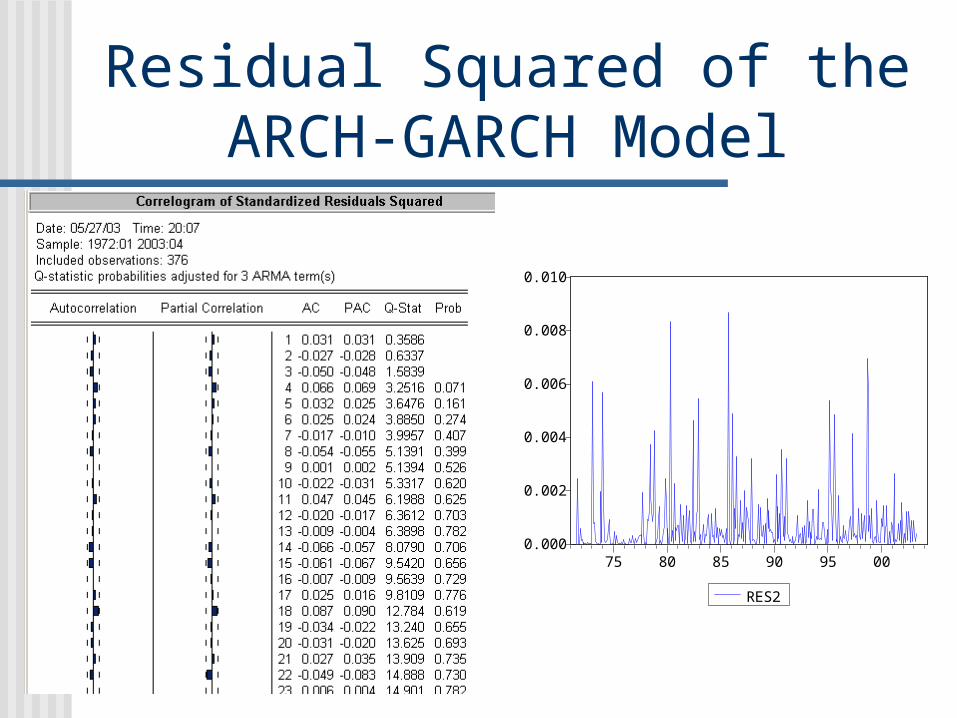

Residual Squared of the ARCH-GARCH Model

0.000

0.002

0.004

0.006

0.008

0.010

75 80 85 90 95 00

RES2

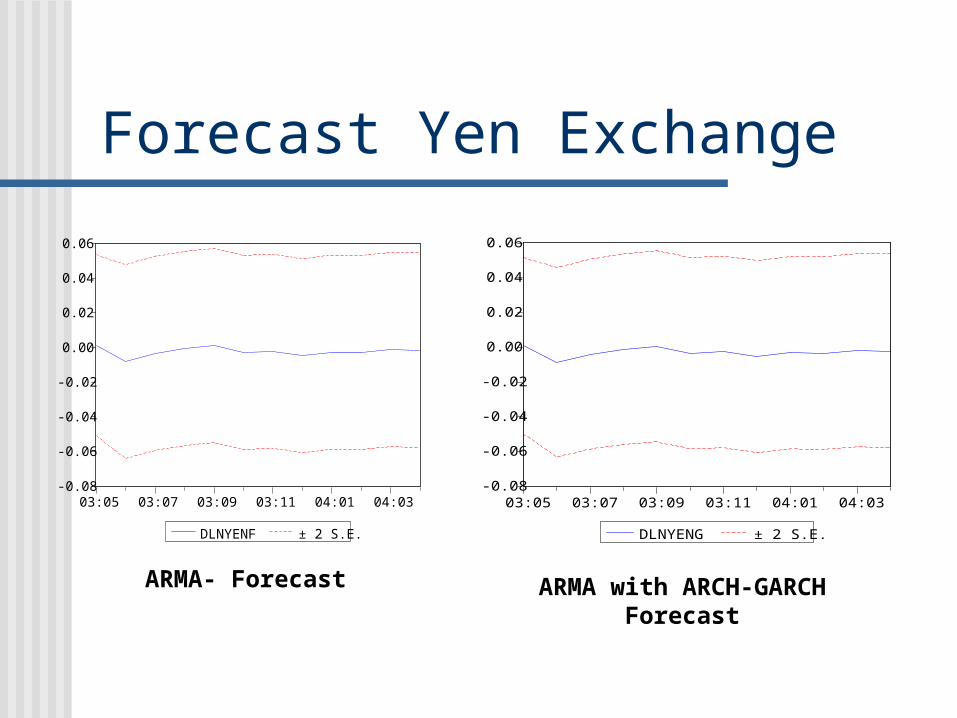

Forecast Yen Exchange

-0.08

-0.06

-0.04

-0.02

0.00

0.02

0.04

0.06

03:05 03:07 03:09 03:11 04:01 04:03

DLNYENF ± 2 S.E.

-0.08

-0.06

-0.04

-0.02

0.00

0.02

0.04

0.06

03:05 03:07 03:09 03:11 04:01 04:03

DLNYENG ± 2 S.E.

0.00064

0.00065

0.00066

0.00067

0.00068

03:05 03:07 03:09 03:11 04:01 04:03

Forecast of Variance

ARMA- Forecast ARMA with ARCH-GARCH Forecast

Conclusion Our model forecasts a relatively flat

fractional change in the ¥/$ over the next twelve months.

We have more confidence in our second model because the ARCH-GARCH terms account for periods of high variance.

Questions?