XIII. Monetarism

41

XIII. Monetarism

description

XIII. Monetarism. XIII.1 Introduction. Milton Friedman. 1912-2006 Economist, monetarist 1946-1977: University of Chicago 1977-2006: Hoover Institution - PowerPoint PPT Presentation

Transcript of XIII. Monetarism

XIII. Monetarism

XIII.1 Introduction

Milton Friedman• 1912-2006• Economist, monetarist• 1946-1977: University of Chicago• 1977-2006: Hoover Institution• Essays in Positive Economics, A

Theory of Consumption Function, Capitalism and Freedom, A Monetary History of the United States (1867-1960) - with Anna Schwartz, Free to Choose, etc.

• Nobel Prize in Economics, 1976• Considered as conservative, in

reality liberal economist• Advisor to President Nixon

Roots and ambitions

• Roots: Quantity Theory of Money• Ambitions: challenge Keynesianism

– not so much as a theory for a depression period– mainly the policy conclusions

• Main points of this Lecture:– QTM and demand for money– Expectation-augmented Phillips Curve– Monetary approach to BoP and ExR determination– Other characteristics

• Crucial implications for stabilization policies

XIII.2 Demand for money

Previous models (1)

QTM (Fisher version)

• M.V = P.Y – implicit demand function MD=(1/V).P.Y

• Velocity V assumed constant, supply of money MS determines stock of money M

• M > MD → price level P↑ and vice versa

• Real interest determined by thrift and marginal productivity of capital (see LIV, in particular IV.2.3, loanable funds interpretation)

Previous models (2)

Keynesian• Transaction, precautionary (function of Y)• Speculative, inversely determined by real

interest r• Interest rate – reward for parting with liquidity

or for not hoarding money• Speculative motive: there will be always some

preference for cash vis-à-vis other financial assets (“bonds”)

• Because of uncertainty, demand for money volatile (unstable) → velocity of money unstable

Friedman’s demand for money

• Demand for money is a stable function of limited number of variables

where WH is total wealth (approximate by permanent income, see Appendix to this Lecture), r is real return on other assets, πe is expected inflation, u represents individual tastes, preferences and other factors

• Demand of money is higher– the higher is wealth– the lower is yield on other asset– the lower is expected inflation and vice versa

u,r,WH,fP

M eD

Transmission mechanism• How do the changes in money stock affect the

real sector of the economy (Y, employment, etc.)?

• Keynesian (see LVII and VIII): ∆M → ∆r →I → ∆Y– Important assumption in the background: there is

always substitution between money and other assets (“bonds”)

• Monetarist– all individuals maximize utility and reallocate their

wealth among many other assets till marginal rates of return are the same

– M↑ → marginal return from money↓ → M>MD → demand for other assets ↑ → their prices↑ → continues up to the point when all marginal returns equal

– conclusions: demand for money stable (and stable velocity V), no obvious relation between change in money and change in real output, direct impact of change in money on change in price level

– Quantity theory as a theory of money demand

Empirical evidenceMixed• Originally (1950s): Friedman asserted that

interest rate totally insignificant for demand for money– Later not confirmed by the data

• 1970s and 1980s: data confirmed unstable velocity (but a very turbulent period, see later Lectures), i.e. unstable demand for money

• However, in the long term, demand for money reasonable stable and link between money and prices confirmed

• If money influences instability in the economy, then mainly as a consequence of fluctuations in the money supply, induced by the monetary authorities

Today’s assessment• Changes in money stock are main factor

explaining changes in money income• If state (Central Bank) decides to control

money supply then actual path of money income will be different from the situation when money supply is left endogenous

• Long time lags between money stock changes and impact on the change of money income → monetary policy maybe rather destabilizing

• The money supply should be allowed to grow at a fixed rate in line with the underlying growth of output to maintain long-term price stability

XIII.3 The expectations-augmented Phillips curve

Inflation and unemploymentUSA, 1950-1969

-1

0

1

2

3

4

5

6

7

8

9

3 4 5 6 7

Unemployment (%)

Infl

atio

n (

%)

Inflation and unemploymentUSA, 1970-2000

0

2

4

6

8

10

12

14

4 5 6 7 8 9 10

Unemployment (%)

Infl

atio

n (

%)

Phillips curve - a wrong concept? (1)

Two 1968 contributions:• M.Friedman: The Role of Monetary Policy• E.Phelps: Money-Wage Dynamics and Labor-

Market EquilibriumOriginal Phillips curve:• For a period, when long-term average

inflation is zero and workers expect the next year’s inflation zero as well. This was true until 1960’s.

• Inflation/unemployment trade-off: not a long-term concept, as there is always some level of unemployment – a natural rate

Phillips curve - a wrong concept? (2)

Original Phillips curve: wage negotiations, when with high unemployment and expectation of zero inflation, firms easily find workers, ready to take a low wage.

Positive inflation expectation: workers negotiate much harder for higher nominal wages to keep real wages unchanged.

Phillips curve - a wrong concept? (3)

Define expected price as Pe and expected inflation as

and original Phillips curve can be expressed

However, whenever , than inflation might rise, even with high unemployment

→ no unemployment x inflation trade-off

e Pe P 1

P 1

e .u, with e 0

e 0

Phillips curve - a wrong concept? (4)

No permanent inflation/unemployment trade-off; consequences:

• Permanent positive inflation, which generates an expectation about a positive inflation further on;

• Unemployment can not – for a longer period of time – be kept bellow a certain level, called natural rate (consistent with full employment output).

Over time, Phillips curve trade-off disappears.

Expectations-augmented Phillips curve

Suppose thatthan

This fits the data for the period even beyond 1970 rather well.

Back to more usual notation: than

↔ expectations-augmented Phillips curve

0 and, say, e 1

1 .u

0u*

u u* -1

Change of inflation and unemploymentUSA, 1970-2000

-5

-4

-3

-2

-1

0

1

2

3

4

5

4 5 6 7 8 9 10

Unemployment (%)

Ch

ange

of

infl

atio

n (

%)

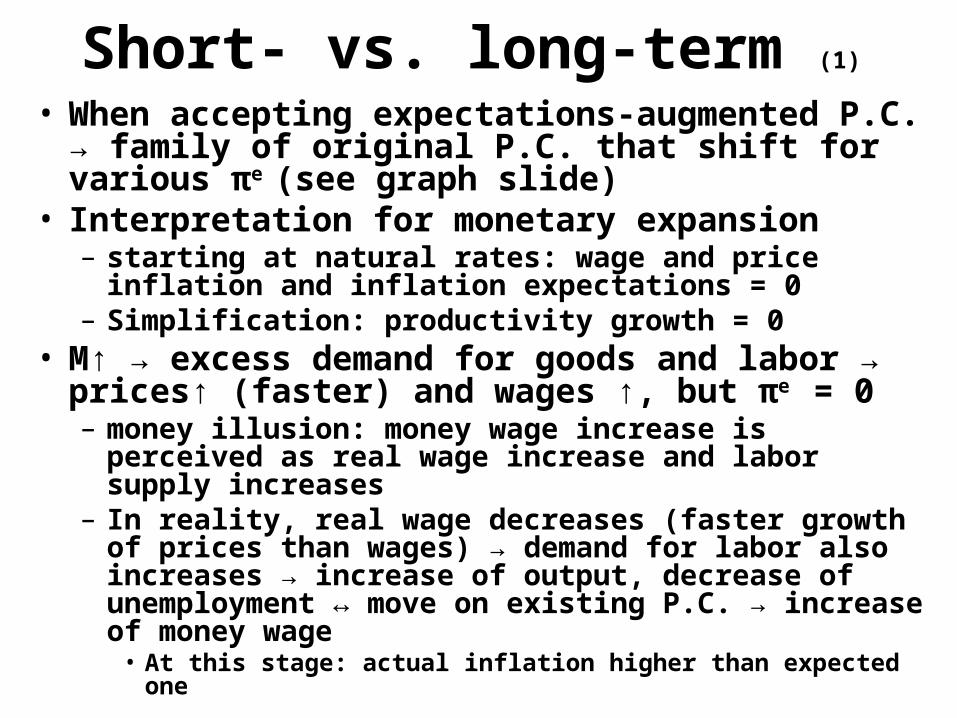

Short- vs. long-term (1)

• When accepting expectations-augmented P.C. → family of original P.C. that shift for various πe

(see graph slide)• Interpretation for monetary expansion

– starting at natural rates: wage and price inflation and inflation expectations = 0

– Simplification: productivity growth = 0• M↑ → excess demand for goods and labor →

prices↑ (faster) and wages ↑, but πe = 0– money illusion: money wage increase is perceived as

real wage increase and labor supply increases– In reality, real wage decreases (faster growth of

prices than wages) → demand for labor also increases → increase of output, decrease of unemployment ↔ move on existing P.C. → increase of money wage

• At this stage: actual inflation higher than expected one

Short- vs. long-term (2)

– Increase of nominal wage and zero productivity growth → π = increase of wage → new expected inflation πe

• Workers do not suffer from money illusion any more and press for further nominal wage increase– Actual wage increase: original increase due to

lower unemployment + additional increase due to expected inflation πe

– Horizontal shift of P.C. to the right– Higher real wage → fall of labor demand → lower

output → return to normal levels of output and unemployment and to the situation when expected inflation equals an actual one, but this inflation is not zero any more

Short- vs. long-run Phillips curve

W

U

SRPC1

UNU1

1W

SRPC2

πe

A

BC

U < UN

π > πe

U = UN

π = πe U > UN

π < πe

LRPC

Short- vs. long-term (3)

• In the long-run, when economy operating at normal output and unemployment– Rate of increase of money wage = expected

inflation, e.g. point C– One other (but just another one) point A,

where expected inflation = 0

• In the long-run:– Economy always at normal levels– Wage inflation = expected price inflation, but

is not linked to unemployment– LRPC vertical at UN → no inflation x

unemployment trade-off

XIII.4 Monetary approach to exchange rate determination

Purchasing Power Parityreminder from LIII

• Suppose that markets (both domestic and foreign) are fully competitive and prices quickly adjust (monetarists’ position)

• Than prices, when converted into same currency, must be equal, i.e. PPPxP*=P or

PPP = P/P*

• This definition: absolute PPP• Relative PPP: percentage change in the ExR between

two currencies is equal the difference in percentage changes in national price levels

• Formally– where inflation

• Remark: the expression is good approximation for small inflation values

*1-1- -EE-E

1-1- PP-P

Basic relation of monetary approach• Changes in (absolute) PPP solely determined by changes in

relative price levels: faster domestic inflation → depreciation, faster foreign inflation → appreciation

• Formally:

• In another words: in the long run, the ExR (defined as PPP) is determined by relative supplies of monies and relative demands for them (relative with respect to domestic and foreign country in quesiton)

• In the long run, ExR (PPP) reacts similarly to change in money supplies and to output level as ExR, defined by the short term, asset approach

• But difference: in asset approach, when interest increases, r, then ExR appreciates; here the opposite: when r, ExR (PPP) depreciates - see the ratios above. Why?

P=MS L Y,r , P*=MS,* L Y*,r* and PPP=

MS

L Y,r MS,*

L Y*,r* =

MS

MS,*.L Y*,r* L Y,r

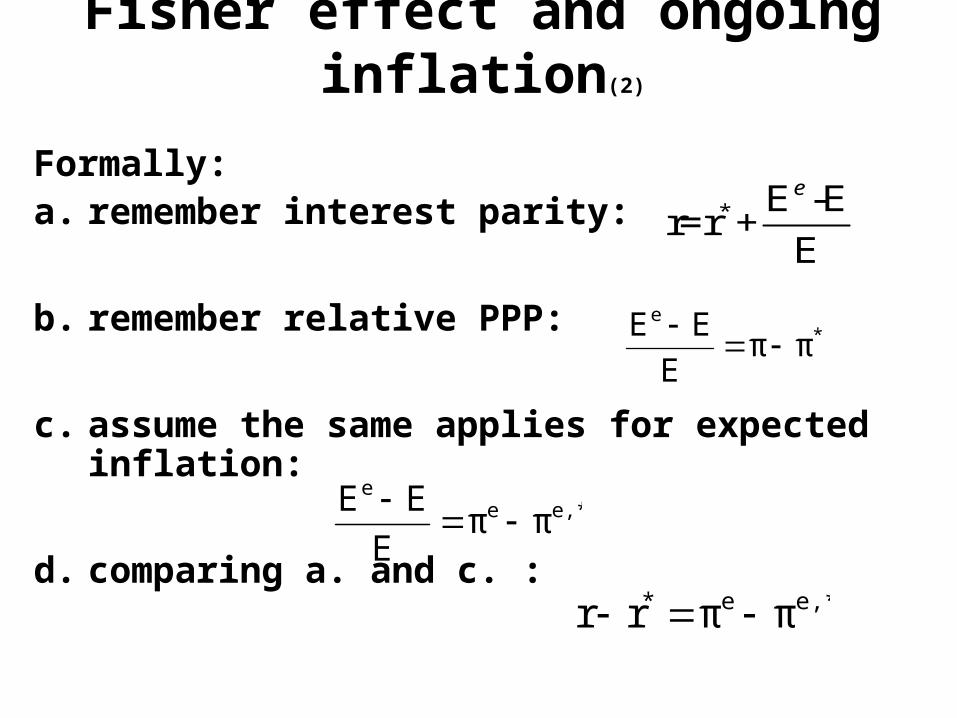

Fisher effect and ongoing inflation(1)

• In most of examples so far: theoretical exercise with one-time increase in money supply

• Reality: usually permanent change in monetary policy (at least lasting one)– Changes in expectations, and both firms and

workers adjust prices, i.e. permanent change in money growth rate is followed by proportional change in inflationary rate

• In monetarist, long run view (as in classical model) this does not change real variables, including real returns, but changes nominal interest rate

Fisher effect and ongoing inflation(2)

Formally:a. remember interest parity:

b. remember relative PPP:

c. assume the same applies for expected inflation:

d. comparing a. and c. :

r=r*+Ee-E

E

*e

ππE

EE

e,*ee

ππE

EE

e,*e* ππrr

Fisher effect and ongoing inflation(3)

• Fisher effect: rise in country’s expected inflation leads to an equal rise in the interest rate that deposits of its currency offer; vice versa for a decrease

• Why PPP depreciates when interest raises relative to the interest of foreign currency?

– Because, due to Fisher effect and the fact that - as monetarists never assumed - we are not in the (Keynesian) world of sticky prices, difference in domestic and foreign interest equals differences in expected inflation

Summarizing …

• Monetarist assume that nominal exchange rates are predominantly determined by relative money supplies in domestic and foreign countries

• Much stronger believe in a speed of adjustment (long-run “not so long”)

XIII.5 Other basic characteristics of monetarism

Stable private sectorKeynesians - AD less stable• Private sector inherently unstable• Subject to erratic shocks• mainly: changes in MEI

Monetarists: AD more stable• Inherent stability• If unstable, than as a result of un-stability

of money supply

It’s not MEI, but un-proper changes in money supply what leads to instability of AD

High level of aggregation

• Expenditures determined by excess supply/demand of real balances

• Belief in fluidity of capital markets

• Short-term income changes do not depend on the situation in the different sectors of the economy

Price level vs. individual prices

Price level – aggregate phenomena, determined by ADxAS

Pricing decisions in particular industries – effect on relative prices only

Keynesian attention to cost (microeconomic) basis of the pricing

Large vs. small models

• Friedman: do we know enough?

• No need of detailed knowledge of different sectors

Literature to Ch. XIII• Thomas Meyer, The structure of monetarism, Kredit

und Kapital 8(1975), pp. 191-215, 292-313. Probably the best, albeit a bit old overview

• Snowdon, Vane, Modern Macroeconomics, Edvard Elgar, 2005, Ch.4. Basic text

• Laidler, D., The Demand for Money (4th ed.), HarperCollins, 1993. Very accessible treatment of different theories.

• Samuelson, P.A., Sollow, R.M., Analytical Aspects of Anti-Inflationary Policy, American Economic Review, May 1960. Classical text defining original Phillips curve – worth of comparing with Friedman’s approach

• Friedman, M. The Role of Monetary Policy, American Economic Review, March 1968. Basic text on expectations-augmented Phillips curve and on “natural” values

• Krugman, Obstfeld, International Economics, Ch. 15, pp. 373-381 PPP and monetary approach to ExR

Appendix: Permanent income hypothesis

• Milton Friedman (1957)• Similar as life cycle hypothesis (see your

course on Macroeconomics): current consumption does not depend on current income only

• PIH: differentiates between stable, expected income and one-time fluctuations

Basic propositions

• In current period, income is decomposed into permanent and transitory part

• Permanent – people expect that this is going to be their stable income also in the future (kind of an “average” income)

• Transitory – people know that these are temporary (random) fluctuations of the income

Y=YP +YT

Consumption function

• Consumption depends on permanent income only

and is proportional to permanent income

• Average propensity to consume (APC) is given by a ratio of permanent and actual income

C=YP

APC=C Y=YP Y

Strength of PIH• Short-term consumption function uses

wrong data (observed data on income reflect both permanent and temporary components)

• It can explain a fall of APC at higher income for short-term consumption function (APC depends on ratio of permanent and total income, if income raises in the short-term, it is a consequence of change in a temporary component, observed APC falls, but real APC does not change)

• This applies both for cross-sectional data (for households), and for time-series (for shorter period of time)

• When using long-term data – income reflects more permanent component and APC is constant

![Paper Class Xiii[Leader(Xii Xiii)]](https://static.fdocuments.net/doc/165x107/577cc5851a28aba7119ca7e3/paper-class-xiiileaderxii-xiii.jpg)