Wüstenrot & Württembergische AG, Stuttgart · Wüstenrot & Württembergische AG, Stuttgart Dr....

24

Wüstenrot & Württembergische AG, Stuttgart Dr. Jan Martin Wicke, CFO 26 April 2013 Berenberg Roadshow Frankfurt

Transcript of Wüstenrot & Württembergische AG, Stuttgart · Wüstenrot & Württembergische AG, Stuttgart Dr....

Wüstenrot & Württembergische AG, Stuttgart

Dr. Jan Martin Wicke, CFO

26 April 2013Berenberg Roadshow Frankfurt

page 2

Agenda

1. Who we are

2. External challenges

3. New strategy: "W&W 2015"

4. Financial results

5. Outlook

6. Why invest in W&W shares?

1828 1991 20121921

Established in 1828,Württembergische Privat-Feuer-Versicherungsgesellschaft is the oldest private property insurance in southern Germany.

Founded 1921, Wüstenrotwas Germany‘s first

home loan and savings bank.

In 1833, Allgemeine Rentenanstalt, the first pension insurance in Germany, was established.

In 1991, both companies formed the Württembergische Insurance Group .

In 1999, merger between Wüstenrot & Württembergische. With its two well established, strong brands "Wüstenrot" and "Württembergische", the W&W Group is a specialized one-stop shop for financial planning for retail clients and small/medium commercial customers in Germany and the Czech Republic:

� Mobile sales force of about 6,000 tied agents

� 10,000 employees, 450 trainees

� 6 million customers

� No 2 in German home loan savings

� No 9 in German property/casualty insurance

� No 12 in German life insurance

page 3

Our roots – Foundations of sound expertise

Who we are

Our strengths – W&W is close to the customer

Potential access to 40 m private and commercial

customers in Germany

Products of Württembergische Lebensversicherung

Products of Wüstenrot Bausparkasse

Products of Württem-bergische Versicherung

Products of Wüstenrot Bank and Asset Management

3,000 tied agents Wüstenrot

3,000 tied agents Württembergische

Direct distribution channel

5,000 brokersFinancial services providers

Banks

Insurances

Product range Distribution channelsCustomer potential

�Our customer potential, our business model and our independence form a strong basis for successful future developme nt.

Who we are

page 4

� Wüstenrot Bausparkasse AG

� Wüstenrot Bank AGPfandbriefbank

� Wüstenrot Bausparkasse AG

� Wüstenrot Bank AGPfandbriefbank

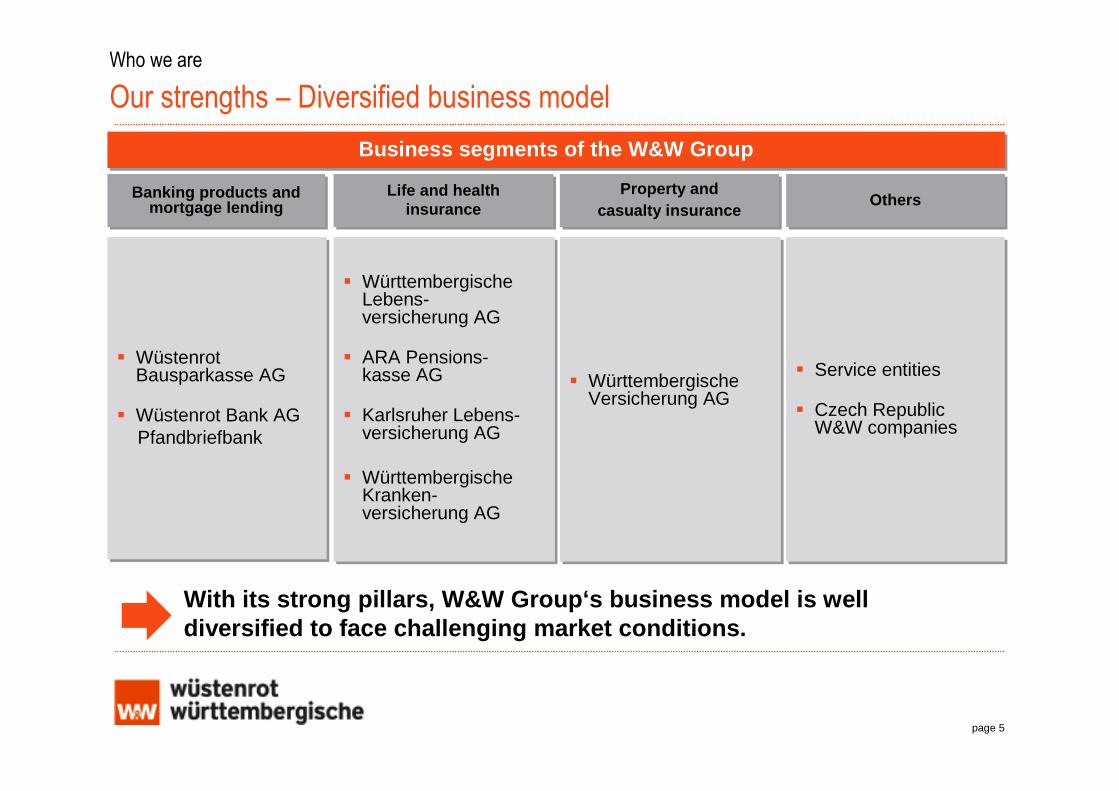

Business segments of the W&W GroupBusiness segments of the W&W Group

� Württembergische Lebens-versicherung AG

� ARA Pensions-kasse AG

� Karlsruher Lebens-versicherung AG

� Württembergische Kranken-versicherung AG

� Württembergische Lebens-versicherung AG

� ARA Pensions-kasse AG

� Karlsruher Lebens-versicherung AG

� Württembergische Kranken-versicherung AG

� Württembergische Versicherung AG

� Württembergische Versicherung AG

� Service entities

� Czech RepublicW&W companies

� Service entities

� Czech RepublicW&W companies

Property andcasualty insurance

Property andcasualty insurance OthersOthersBanking products and

mortgage lending Banking products and

mortgage lending Life and health

insurance Life and health

insurance

�With its strong pillars, W&W Group‘s business model is well diversified to face challenging market conditions.

Who we are

Our strengths – Diversified business model

page 5

How we earn money

� Credit risk: Strong track record in underwriting retail mortgages

� P/C insurance risk: Long term combined ratio target < 96 %

� Market risk: Unavoidable in particular in building society and life insurance

� Behavioural risk of customers: Strong trackrecord in managing these risks

� Operational risk: Strong internal controlsystem in order to minimize operationalrisk

� Liquidity risk:Particularly low due to regular premium income

�Well diversified business model; systematic approac h in managingrisk diversification

Who we are

page 6

40,9 %

10,8 %

44,1 %

3,9 % 0,3 %

Credit risk Insurance risk Market risk

Operational risk Behavioural risk

Risk profileRisk profile

page 7

Agenda

1. Who we are

2. External challenges

3. New strategy: "W&W 2015"

4. Financial results

5. Outlook

6. Why invest in W&W shares?

Challenges by capital markets and increasing regulation

External challenges

Interest rates

�The new strategy programme "W&W 2015" is designed to manage these challenges. W&W will keep its financial stabil ity.

page 8

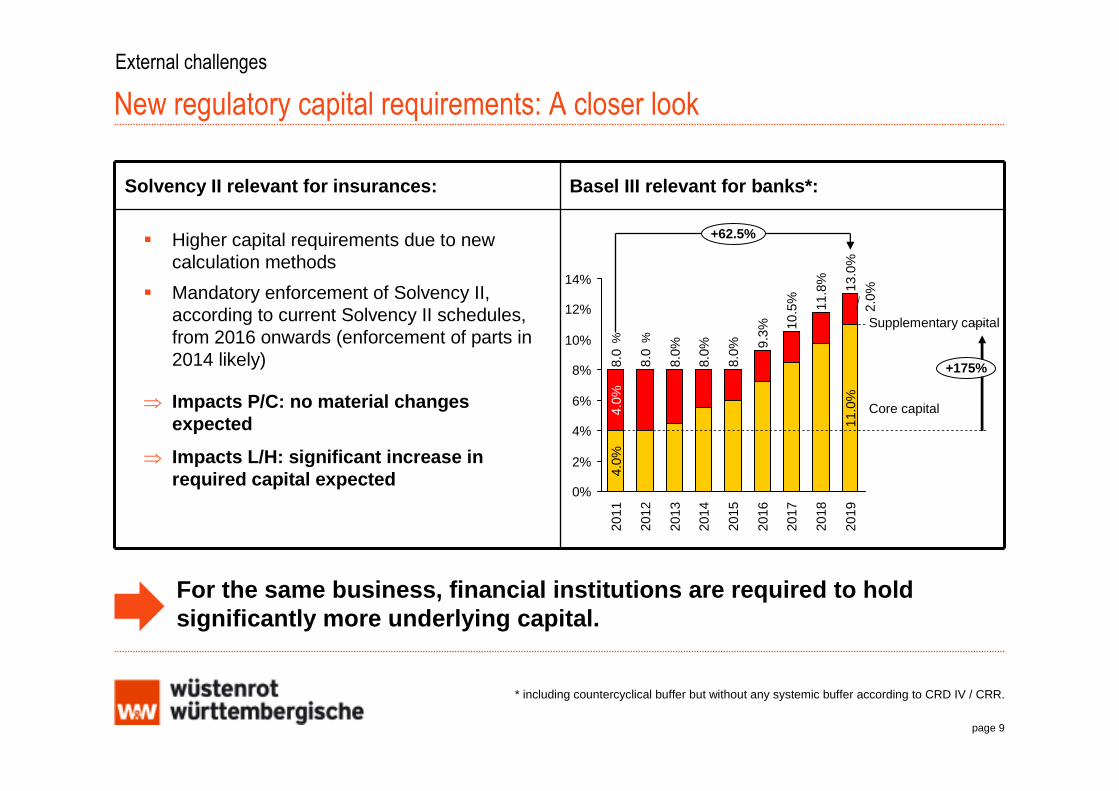

� Capital markets: In order to meet interest guarantees given to our customers, we are invested in bonds to a large extent

� Low interest rates create a challenging environment for asset management � Volatile credit spreads lead to higher risk capital requirements

� Regulation: W&W has to comply with increasing regulatory requirements from banking and insurance supervision alike (Basel III and Solvency II)

� Implementation of the new regulatory measures is both costly and absorbing work capacity� Capital requirements will rise significantly for banks and life insurers

Euro crisisin %

Greece

in %10y Swap

New regulatory capital requirements: A closer look

External challenges

�For the same business, financial institutions are r equired to hold significantly more underlying capital.

Solvency II relevant for insurances: Basel III relev ant for banks*:

� Higher capital requirements due to new calculation methods

� Mandatory enforcement of Solvency II, according to current Solvency II schedules, from 2016 onwards (enforcement of parts in 2014 likely)

⇒ Impacts P/C: no material changes expected

⇒ Impacts L/H: significant increase in required capital expected

Core capital

Supplementary capital

2019

11.0

%

2.0%

+62.5%

+175%

14%

12%

10%

8%

6%

4%

2%

0%

13.0

%

2018

11.8

%

2017

10.5

%

2016

9.3%

2015

8.0%

2014

8.0%

2013

8.0%

2012

8.0”

2011

8.0!

4.0%

4.0%

page 9

%%

* including countercyclical buffer but without any systemic buffer according to CRD IV / CRR.

page 10

Agenda

1. Who we are

2. External challenges

3. New strategy: "W&W 2015"

4. Financial results

5. Outlook

6. Why invest in W&W shares?

W&W meets the challenge by setting up a new strategy programme

"W&W 2015" secures economic success

� Earnings increase

� Risk reduction

� Efficiency improvement and cost reduction

Being a reliable partner in financial services is the top priority of W&W

� Being a one-stop shop for financial planning and a reliable financial services provider is characteristic of all business activities of the W&W Group.

� W&W will remain a reliable partner in the future –proactive steps are taken now.

"New reality" for financial services providers

�The strategy programme and ongoing businesses are d esigned to protect the good reputation of the group.

New strategy: "W&W 2015"

page 11

Measures are developed to improve efficiency in financial services, to actively manage risk-reward profiles of existing business and the product portfolio

"W&W 2015" comprises seven areas for action

Quick-win measures � Implementation of first ad-hoc measures: Sophisticated hiring freeze, restrictions on contracting external service providers, and optimization of purchasing

� Adaptation of business model to the changed economic environment� This will be achieved through simplification of products, modification of the operating

model, and focusing on bank functions

Business modelfor BausparBank

� Significant reduction of overall cost structure� All types of functions and costs are affected: Control functions, production and service

functions, sales, and non-personnel costs� Guiding principles: Avoid, reduce costs, simplify

Cost programme

1

2

3

� Earnings stabilization through an optimized investment portfolio and definition of possible courses of action in the low-interest environment

� Advanced management of the portfolio based on value � Further reduction of high-interest tariffs in building savings and life insurance

Resources/IT

Asset allocation

Portfoliomanagement

� Improvement of efficiency and effectiveness in the project execution through holistic optimization approach and reduction of costs of day-to-day business

4

5

6

Capital optimization7� Optimization of the risk capital requirements and the risk capital structure, e.g.,

through RWA reduction, hedging strategies, and equity increase

DescriptionDescriptionArea for actionArea for action

New strategy: "W&W 2015"

page 12

Conclusion

� Like all financial services providers, W&W has to face up to the new reality.

� The groupwide "W&W 2015" programme is the response to the new reality.

� "W&W 2015" strengthens earning capacity as well as capital base and manages risk capital requirements accordingly.

New strategy: "W&W 2015"

page 13

�The strategy programme "W&W 2015" is our answer to the new reality, guaranteeing a prosperous future of the wh ole group.

page 14

Agenda

1. Who we are

2. External challenges

3. New strategy: "W&W 2015"

4. Financial results

5. Outlook

6. Why invest in W&W shares?

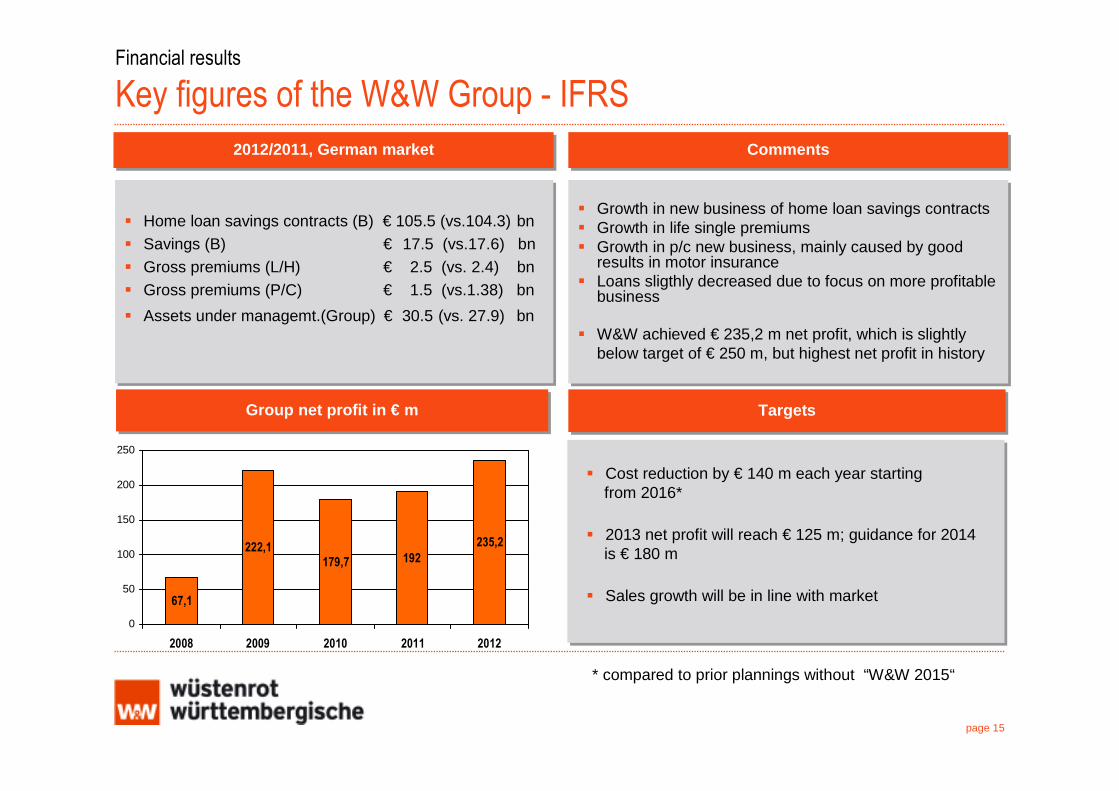

235,2

192179,7222,1

67,1

0

50

100

150

200

250

2008 2009 2010 2011 2012

Financial results

Key figures of the W&W Group - IFRS

2012/2011, German market2012/2011, German market

� Growth in new business of home loan savings contracts� Growth in life single premiums� Growth in p/c new business, mainly caused by good

results in motor insurance � Loans sligthly decreased due to focus on more profitable

business

� W&W achieved € 235,2 m net profit, which is slightlybelow target of € 250 m, but highest net profit in history

� Growth in new business of home loan savings contracts� Growth in life single premiums� Growth in p/c new business, mainly caused by good

results in motor insurance � Loans sligthly decreased due to focus on more profitable

business

� W&W achieved € 235,2 m net profit, which is slightlybelow target of € 250 m, but highest net profit in history

Group net profit in € mGroup net profit in € m

CommentsComments

� Home loan savings contracts (B) € 105.5 (vs.104.3) bn� Savings (B) € 17.5 (vs.17.6) bn � Gross premiums (L/H) € 2.5 (vs. 2.4) bn� Gross premiums (P/C) € 1.5 (vs.1.38) bn

� Assets under managemt.(Group) € 30.5 (vs. 27.9) bn

� Home loan savings contracts (B) € 105.5 (vs.104.3) bn� Savings (B) € 17.5 (vs.17.6) bn � Gross premiums (L/H) € 2.5 (vs. 2.4) bn� Gross premiums (P/C) € 1.5 (vs.1.38) bn

� Assets under managemt.(Group) € 30.5 (vs. 27.9) bn

page 15

TargetsTargets

� Cost reduction by € 140 m each year starting from 2016*

� 2013 net profit will reach € 125 m; guidance for 2014is € 180 m

� Sales growth will be in line with market

* compared to prior plannings without “W&W 2015“

� New efficiency programme "W&W 2015" launched in order to cope with low interest rates, tougher competition and increasing regulatory requirements

� New efficiency programme "W&W 2015" launched in order to cope with low interest rates, tougher competition and increasing regulatory requirements

W&W strategyW&W strategy

W&W at a glance

Highlights 2012

Business environmentBusiness environment

New businessNew business

Risk assessmentRisk assessment

GuidanceGuidance

� Low domestic interest rates are a challenge for the whole financial industry

� Low domestic interest rates are a challenge for the whole financial industry

� Best new home loan savings business ever (net + 3.4 %)� L/H shows a slight increase in new business (+ 6.4 %)� New business in P/C clearly above market (+ 14.5 %), driven by motor

insurance (+ 19.6 %)

� Best new home loan savings business ever (net + 3.4 %)� L/H shows a slight increase in new business (+ 6.4 %)� New business in P/C clearly above market (+ 14.5 %), driven by motor

insurance (+ 19.6 %)

� W&W has a sound capitalization with a solvency ratio of 133,2 % (financial conglomerate)

� Risk diversification is a strategic key success factor

� W&W has a sound capitalization with a solvency ratio of 133,2 % (financial conglomerate)

� Risk diversification is a strategic key success factor

EarningsEarnings � W&W achieves € 235,2 m (vs € 192 m) net profit, which is slightly below target, but the highest net profit in history

� W&W achieves € 235,2 m (vs € 192 m) net profit, which is slightly below target, but the highest net profit in history

� Cost reduction by € 140 m each year starting from 2016*� 2013 net profit will reach € 125 m; guidance for 2014 is € 180 m� Sales growth will be in line with market

� Cost reduction by € 140 m each year starting from 2016*� 2013 net profit will reach € 125 m; guidance for 2014 is € 180 m� Sales growth will be in line with market

page 16

* compared to prior plannings without “W&W 2015“

Financial results

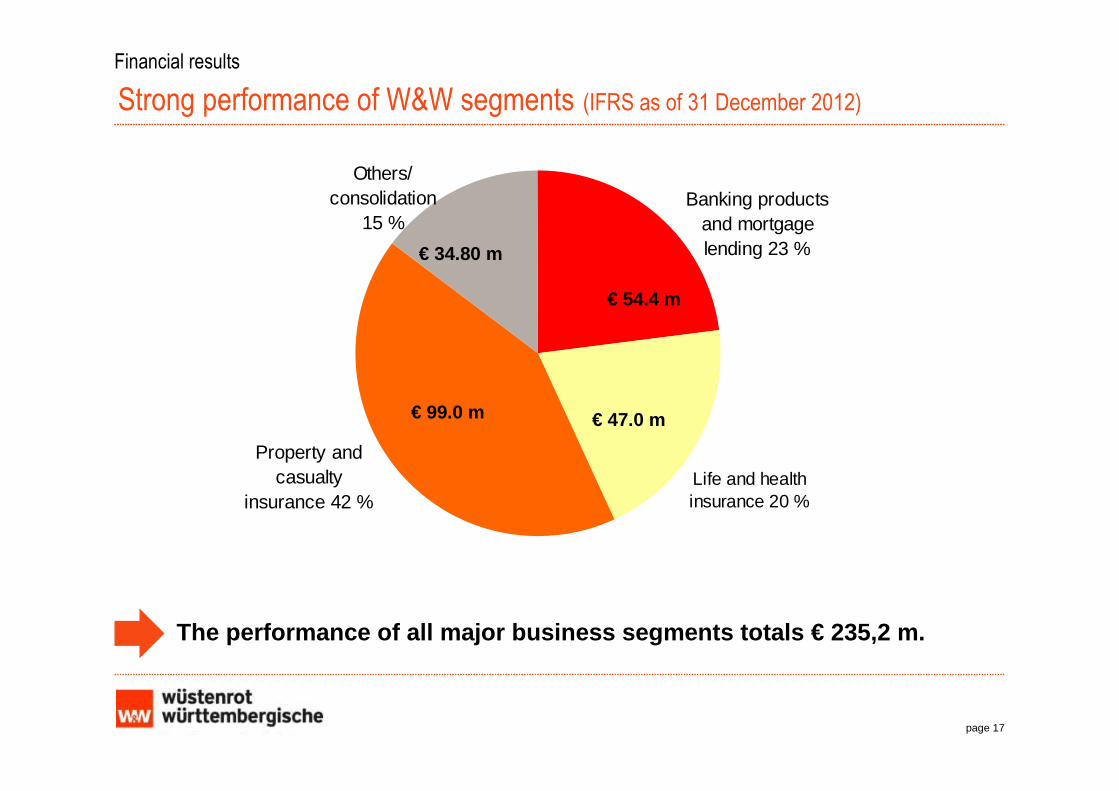

Strong performance of W&W segments (IFRS as of 31 December 2012)

Banking products and mortgage lending 23 %

Property and casualty

insurance 42 %Life and health insurance 20 %

Others/consolidation

15 %

� The performance of all major business segments tota ls € 235,2 m.

€ 34.80 m

€ 54.4 m

€ 99.0 m € 47.0 m

page 17

Building society

Financials

Key figures of W&W segments (IFRS as of 31 December 2012)

∆20112012

+ 3.4 %€ 11.80 bn€ 12.20 bnNew home loan savings, net

- 0.3 %€ 15.32 bn€ 15.26 bnNew home loan savings, gross

∆20112012

- 11.9 %€ 5.92 bn€ 5.22 bnTotal new mortgages (W&W group)

- 7.7 %€ 3.9 bn€ 3.6 bnNew mortgages(Bank only)

∆20112012

New premiums

Gross premiums

∆20112012

+ 2.7 %Gross premiums € 2 479.3 m

Total new premiums

Single premiums life

Regular premiums life

New premiums health

€ 782.1 m

€ 610.3 m€ 154.2 m

€ 17.6 m

€ 734.9 m

€ 549.9 m

€ 167.5 m

€ 17.5 m

+ 6.4 %

+ 11.0 %- 7.9 %

+ 0.6 %

€ 2 413.6 m

€ 236.7 m

€ 1 476.4 bn

€ 206.7 m + 14.5 %

€ 1 379.5 bn + 7.0 %

page 18

Life/Health

P/CBanking

page 19

Agenda

1. Who we are

2. External challenges

3. New strategy: "W&W 2015"

4. Financial results

5. Outlook

6. Why invest in W&W shares?

� Cost reduction by € 140 m each year starting from 2016*

� 2013 net profit will reach € 125 m; guidance for 2014 is € 180 m

� Sales growth will be in line with market

� Cost reduction by € 140 m each year starting from 2016*

� 2013 net profit will reach € 125 m; guidance for 2014 is € 180 m

� Sales growth will be in line with market

W&W GroupW&W Group

� Net profit 2013 will remain below the level of 2012, which was € 54.4 m. In 2014, net profit will rise above the level of 2012.

� Sales growth will be in line with market

� Net profit 2013 will remain below the level of 2012, which was € 54.4 m. In 2014, net profit will rise above the level of 2012.

� Sales growth will be in line with market

Banking products and mortgage lending segment

Banking products and mortgage lending segment

� Net profit 2013 will remain at the level of 2012 level, which was € 47.0 m. In 2014, net profit will remain slightly below the high 2012-level.

Sales growth will be in line with market

� Net profit 2013 will remain at the level of 2012 level, which was € 47.0 m. In 2014, net profit will remain slightly below the high 2012-level.

Sales growth will be in line with market

Life and health segmentLife and health segment

Outlook

Outlook 2013/2014

� Net profit 2013 will be below the 2012 level, which was € 99.0 m. In 2014, net profit will rise again.

� Sales growth will be in line with market

� Net profit 2013 will be below the 2012 level, which was € 99.0 m. In 2014, net profit will rise again.

� Sales growth will be in line with market

Property and casualty segmentProperty and casualty segment

page 20

* compared to prior plannings without “W&W 2015“

page 21

Agenda

1. Who we are

2. External challenges

3. New strategy: "W&W 2015"

4. Financial results

5. Outlook

6. Why invest in W&W shares?

Growth potential of W&W share price

66.10 % Wüstenrot Holding

Competitive and unique business model

Strong reputation

New strategy “W&W 2015“meets market challenges

Sound expertise andinnovative solutions for customers

Low share price

High net asset value

Growth potential based on strong sales channels and products

Financial strength

Sound provider of debt capital

W&W's main shareholders

�A strong market position, a diversified earnings mi x and a clearfinance strategy are just a few of the many reasons to invest in W&W .

Why invest in W&W shares?

page 22

17.58 % Freefloat

8.78 % Horus

7.54 % Unicredit

Strong market position

Thank you for your kind attention!

� Dr. Jan Martin Wicke

� Chief Financial Officer� Gutenbergstraße 30

� 70176 Stuttgart

� phone: +49 711 662 722502

� Investor Relations

� internet: ww-ag.com � phone: +49 711 662 724034

For further information please contact:

page 23

Disclaimer

This presentation and the information contained herein, as well as any additional documents and explanations (together the “material“), are issued by Wüstenrot & Württembergische AG (“W&W”).

This presentation contains certain forward-looking statements and forecasts reflecting W&W management’s current views with respect to certain future events. These forward-looking statements include, but are not limited to, all statements other than statements of historical facts, including, without limitation, those regarding W&W’s future financial position and results of operations, strategy, plans, objectives, goals and targets and future developments in the markets where W&W participates or is seeking to participate. The W&W Group’s ability to achieve its projected results is dependent on many factors which are outside management’s control. Actual results may differ materially from (and be more negative than) those projected or implied in the forward-looking statements. Such forward-looking information involves risks and uncertainties that could significantly affect expected results and is based on certain key assumptions. The following important factors could cause the Group’s actual results to differ materially from those projected or implied in any forward-looking statements:

– the impact of regulatory decisions and changes in the regulatory environment;– the impact of political and economic developments in Germany and other countries in which the Group operates;– the impact of fluctuations in currency exchange and interest rates; and– the Group’s ability to achieve the expected return on the investments and capital expenditures it has made in Germany and in foreign countries.

The foregoing factors should not be construed as exhaustive. Due to such uncertainties and risks, readers are cautioned not to place undue reliance on such forward-looking statements as a prediction of actual results. All forward-looking statements included herein are based on information available to W&W as of the date hereof. W&W undertakes no obligation to update publicly or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as may be required by applicable law. All subsequent written and oral forward-looking statements attributable to W&W or persons acting on our behalf are expressly qualified in their entirety by these cautionary statements. The material is provided to you for informational purposes only, and W&W is not soliciting any action based upon it. The material is not intended as, shall not be construed as and does not constitute, an offer or solicitation for the purchase or sale of any security or other financial instrument or financial service of W&W or of any other entity. Any offer of securities, other financial instruments or financial services would be made pursuant to offering materials to which prospective investors would be referred. Any information contained in the material does not purport to be complete and is subject to the same qualifications and assumptions, and should be considered by investors only in light of the same warnings, lack of assurances and representations and other precautionary matters, as disclosed in the definitive offering materials. The information herein supersedes any prior versions hereof and will be deemed to be superseded by any subsequent versions, including any offering materials. W&W is not obliged to update or periodically review the material. All information in the material is expressed as at the date indicated in the material and is subject to changes at any time without the necessity of prior notice or other publication of such changes to be given. The material is intended for the information of W&W´s institutional clients only. The information contained in the material should not be relied on by any person.

In the United Kingdom this communication is being issued only to, and is directed only at, intermediate customers and market counterparties for the purposes of the Financial Services Authority’s Rules ("relevant persons"). This communication must not be acted on or relied on by persons who are not relevant persons. To the extent that this communication can be interpreted as relating to any investment or investment activity then such investment or activity is available only to relevant persons and will be engaged in only with relevant persons.

page 24