Global Oil Supply, Demand and Price Outlook With Special ...

Organization of the Petroleum Exporting Countries

The Organization of Petroleum Exporting Countries

World Oil Outlook

8th November, 2009

The International Energy Forum

Riyadh, Saudi Arabia

Hasan M Qabazard

Director, Research Division

OPEC Secretariat

Organization of the Petroleum Exporting Countries

2.7

-1.2

2.9

0.6

-3.6

1.0

5.1

1.2

3.8

-6

-4

-2

0

2

4

6

8

05 06 07 08 09 10

World OECD DCs

2

The world has confronted a major economic turmoil andextreme price volatility

World real GDP growth (in %) Weekly average spot WTI prices, (US$/b)

Spill-over of the financial crisis to the real economy has led to a severe global downturn

Present world recession is the deepest and most synchronized contraction in the past sixty years

Price escalation and high volatility was inconsistent with market fundamentals

Financialization of oil and commodity markets led to significant speculation

79

143

3230

60

90

120

150

Jan Mar May Jul Sep Nov Jan Mar May Jul Sep Nov

2006-2007

2008-2009

Organization of the Petroleum Exporting Countries

Global oil demand erosion has been considerable(year-on-year change, mb/d)

3

-4

0

4

8

1977 1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010

-3

0

3

6

OECD demand Non-OECD demand

OECD GDP DCs GDP

(dem

and g

row

th: m

b/d

)(GD

P g

row

th:

%)

The collapse in oil demand is largely a consequence of the two-pronged economic crisis

World oil demand has declined in two successive years for the first time since early ’80s

Oil demand reduction may be partly irreversible: contraction in OECD is to reach 4.5 mb/d in 2010

Organization of the Petroleum Exporting Countries

Large overhang in oil stocks underlines weak fundamentals(mb)

4

81

25

106

0

70

140

210

Jan Feb Mar Apr May Jun Jul Aug Sep

Crude

Total Products

75

55

130

0

50

100

150

Jan Feb Mar Apr May Jun Jul Aug Sep

Crude

Total products

OECD commercial oil stocks

(deviation from five years average)Estimated floating storage:

(absolute level)

Besides ample supply, inventory overhang reflects still weak state of market fundamentals

Total OECD commercial oil stocks end-September ‘09 are still 106 mb above 5-year average

Forward demand cover in September estimated at around 59 days

Around 130 mb crude oil (~55 mb) & products (~75 mb) are kept in floating storage

Organization of the Petroleum Exporting Countries

Crude price fluctuations in tandem with financial markets

Increasing use of oil as an asset class exposed the oil market to financial market volatility

Crude prices have been closely following the movements in equity markets and US Dollar

WTI price vs. US $

(weekly average)WTI price vs. equity market

(weekly average)

30

60

90

120

150

Jul Aug Sep Nov Dec Jan Mar Apr Jun Jul Aug Oct

1.25

1.35

1.45

1.55

1.65

(2008-2009)

(US$/€)(US$/b)

US$/€

WTI

30

60

90

120

150

Jul Aug Sep Nov Dec Jan Mar Apr Jun Jul Aug Oct

650

900

1150

1400

1650

(2008-2009)

(S&P 500 Index)(US$/b)

S&P 500

WTI

5

Organization of the Petroleum Exporting Countries

0

10

20

30

40

50

60

Sep-

07

Dec-

07

Mar-

08

Jun-

08

Sep-

08

Dec-

08

Mar-

09

Jun-

09

Sep-

09

Euro zone Japan USA

6

OECD quarterly GDP growth

(% annualized)

Manufacturing index in the OECD area

(September ’07 – ’09)

-18

-12

-6

0

6

1Q07 4Q07 3Q08 2Q09f 1Q10f 4Q10f

USA Japan Euro-zone

The world economy is showing signs of stabilization

World economy now appears to be moving from a period of containing the crisis to one of recovery

The 2Q is now seen to mark the bottom of the recession

Economic recovery may be a lengthy one: deficits, debts, unemployment pose considerable risks

Organization of the Petroleum Exporting Countries 7

Medium-term prospects: greater uncertainties

24

28

32

36

40

2008 2009 2010 2011 2012 2013

2

4

6

8

10Spare capacity (rs) Capacity (ls) Crude supply (ls)

OPEC crude capacity and crude supply

(reference case)

Oil demand & non-OPEC supply

growth prospects

-2

-1

0

1

2

2009 2010 2011 2012 2013

Oil demand growth

Non-OPEC supply growth

reference

protracted

recession

reference

protracted

recession

World oil demand growth is expected to rise gradually to 1.2 mb/d by 2013 (exposed to higher risks)

Non-OPEC liquids negatively affected by lower prices (cancellations/delays)

OPEC is investing $110-120 billion

Medium-term requirements for OPEC crude oil by 2013 would not be higher than 2008 levels

In the reference case spare OPEC crude oil capacity settles around 6 mb/d

Organization of the Petroleum Exporting Countries

Energy and oil demand are set to grow(demand by fuel type, mtoe)

Demand for energy will grow, albeit at a lower paceFossil fuels satisfy more than 80% of global energy needs over the projection period Oil remains the leading source of energy – fast growth in natural gasLow base for renewable energy – continue to grow fast, but limited impact on energy mix

Growth (% pa) Fuel shares (%)

2007-2030 2007 2010 2020 2030

Oil 0.8 36.4 35.1 33.1 30.9

Coal 1.5 28.2 28.5 28.8 28.1

Gas 1.9 22.3 22.6 23.2 24.1

Nuclear 1.6 6.6 6.7 6.5 6.7

Hydro 2.3 2.4 2.6 2.7 2.8

Biomass 3.4 3.5 3.9 4.6 5.4

Other renewables 7.4 0.5 0.6 1.1 1.9

Total 1.5

8

Organization of the Petroleum Exporting Countries 9

World oil demand outlookreference case (mb/d)

Oil demand grows by 1%, or less then 1 mb/d per annum over the forecast period

World oil demand increases by 20 mb/d from 2008 to 2030, but nearly 8 mb/d lower than WOO 2008

Structural shift: OECD demand declines

Developing countries consumption accounts for over 95% of the net increase, mainly in Asian region

Disparity in per capita oil use among regions will remain a critical issue

Change Growth ('08-'30) p.a.

2008 2015 2020 2025 2030 '30 -'08 % mb/d

OECD 47.5 45.5 45.0 44.3 43.4 -4.1 -0.4 -0.19

DCs 33.0 39.3 44.8 50.2 56.1 23.1 2.4 1.05

China 8.0 10.4 12.3 14.1 15.9 8.0 3.2 0.36

Other Asia 9.3 11.0 12.9 14.9 17.2 8.0 2.9 0.36

Transition economies 5.1 5.4 5.7 5.9 6.1 1.0 0.8 0.05

World 85.6 90.2 95.4 100.4 105.6 20.1 1.0 0.91

Organization of the Petroleum Exporting Countries

Transportation sector: main source of oil demand growth

Nearly half of world oil consumption will stem from transportation by 2030

Passenger cars and commercial vehicles: saturation versus economic activity

Greater potential for growth in the stock of vehicles in developing countries

Passenger car ownership

per 1,000 of population, 2006Average annual global growth

in oil demand by sector

10

Organization of the Petroleum Exporting Countries

Conventional liquids’ resource base is sufficient

Date of assessment release

Increasing resource base levels (improved technology, enhanced recovery)

Technology blurs distinction between conventional and non-conventional oil

Resource base likely to continue to grow … especially with non-conventional oil

World’s conventional oil resources Incremental world oil supply 1980-2030

11

Organization of the Petroleum Exporting Countries 12

World oil supply long-term outlookreference case (mb/d)

Non-OPEC crude oil plus NGL supply: a steady plateau of 45 mb/d before beginning a gradual

decline after 2020

Total non-OPEC supply continues to rise (large growth from Canadian oil sands and biofuels)

Rapid increase in OPEC NGL

Demand for OPEC crude rises to 41 mb/d by 2030, however it is 2.5 mb/d lower than WOO 2008

Change Growth ('08-'30) p.a.

2008 2015 2020 2025 2030 '30 -'08 % mb/d

OECD 19.6 18.7 19.1 19.3 19.6 0.0 0.0 0.00

DCS, excl. OPEC 16.1 17.3 18.0 18.3 18.3 2.2 0.6 0.10

Russia 9.8 10.2 10.5 10.6 10.6 0.9 0.4 0.04

Caspian 2.9 4.0 4.4 4.7 5.1 2.2 2.6 0.10

Non-OPEC 50.3 52.4 54.3 55.4 56.3 6.0 0.5 0.27

non-conventional 3.1 5.0 6.8 8.6 10.7 7.6 5.8 0.34

OPEC 35.5 38.1 41.4 45.3 49.6 14.1 1.5 0.64

OPEC NGLs 4.3 5.8 6.7 7.4 8.0 3.7 2.8 0.17

OPEC crude 31.2 32.0 34.3 37.4 41.1 9.9 1.3 0.45

Organization of the Petroleum Exporting Countries

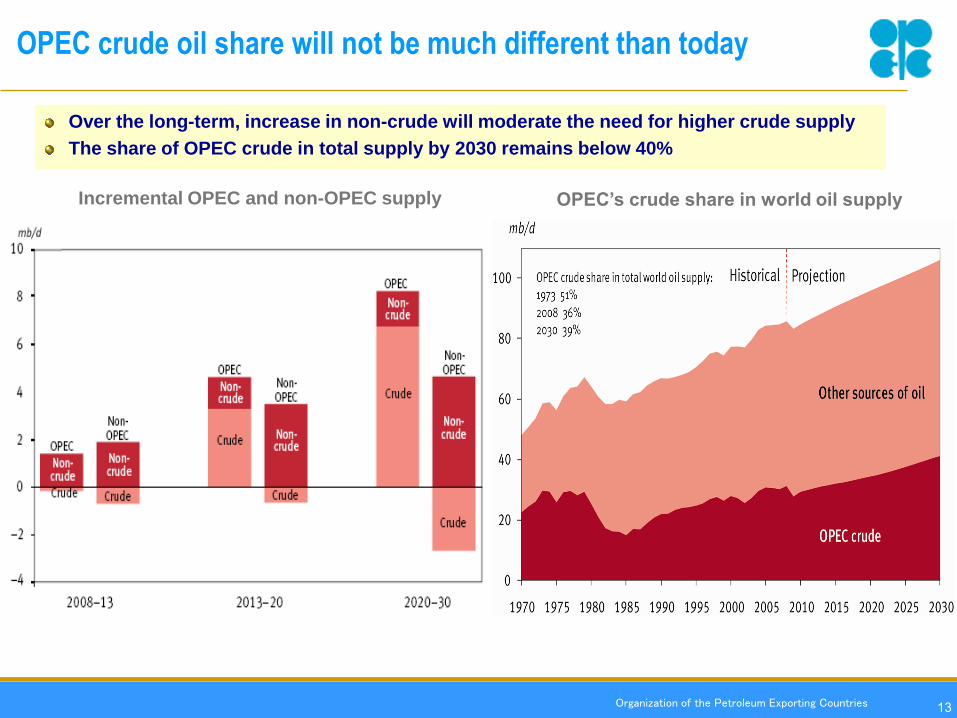

OPEC crude oil share will not be much different than today

Incremental OPEC and non-OPEC supply OPEC’s crude share in world oil supply

13

Over the long-term, increase in non-crude will moderate the need for higher crude supply

The share of OPEC crude in total supply by 2030 remains below 40%

Organization of the Petroleum Exporting Countries

Uncertainties pose investment risks for OPEC MCs

Cumulative OPEC upstream investment requirements

Possible waste of precious resources

Negative effects upon future investments

Upstream development investment requirements by 2020 lie within $180 to $430 billion range

14

31 mb/d → $180 billion

48 mb/d → $430 billion

Organization of the Petroleum Exporting Countries

Security of demand is an integral part of energy security

15

Changing world oil demand projections for 2025

Oil demand projection figures have been repeatedly revised down

The security and predictability of demand are as important as the security of supply

Organization of the Petroleum Exporting Countries 16

Policy measures in major consuming countries impact oil demand

US Energy Independence and Security Act

CAFE standards

Renewable fuels standards (EISA targets)

EU Climate and Energy Legislative Package

20-20-20 package

10% renewables target for the transportation sector

Binding targets for CO2 emissions from new cars

Japan’s promotion of measures to cope with global warming

Energy saving measures in all sectors

China’s energy conservation law

Policy measures promoting new transportation technologies

Electric and hydrogen-fuelled cars

Organization of the Petroleum Exporting Countries

Distillation capacity expansion exceeds requirements

Additional cumulative refinery crude runs required and potential*

*/ Potential: based on expected distillation capacity expansion

Required: based on projected demand increases

The refining tightness for distillation capacity has turned into over-capacity – to the extent that

substantial closures are expected, especially in the OECD

17

Organization of the Petroleum Exporting Countries

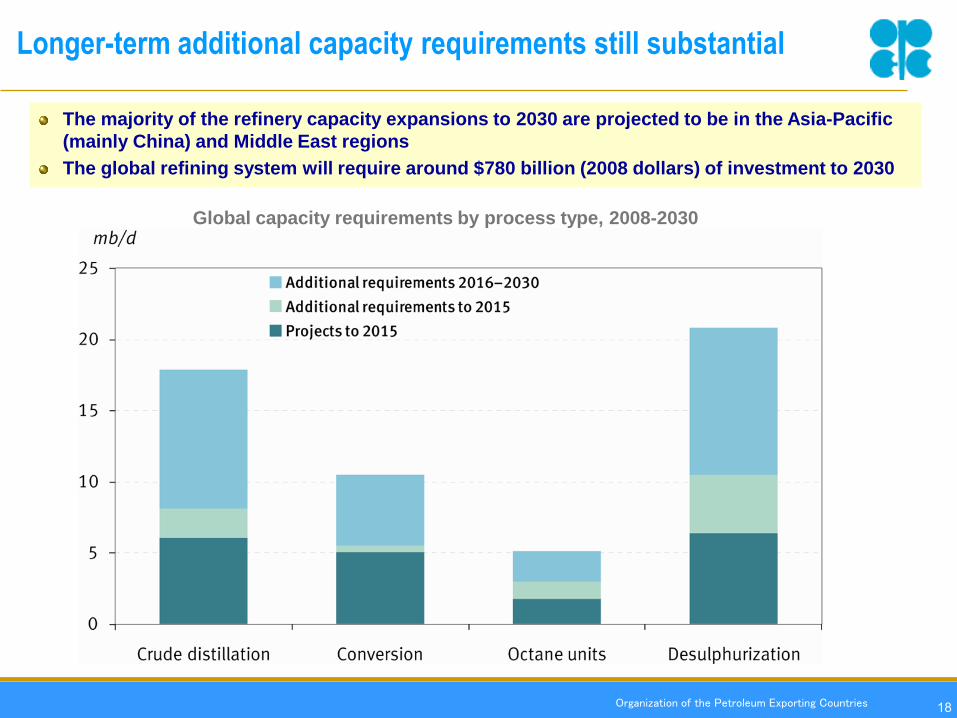

Longer-term additional capacity requirements still substantial

Global capacity requirements by process type, 2008-2030

18

The majority of the refinery capacity expansions to 2030 are projected to be in the Asia-Pacific

(mainly China) and Middle East regions

The global refining system will require around $780 billion (2008 dollars) of investment to 2030

Organization of the Petroleum Exporting Countries

0

10

20

30

40

50

2007 2015 2020 2025 2030

mb/d

Asia - Pacific

Middle East

FSU

Europe

Africa

Latin America

US & Canada

Global crude oil imports by region, 2007 -2030

19

Growing share of the Asia-Pacific in global crude oil imports

The Middle East will remain the major source of imports, but an increasing percentage of

volumes will also come from other regions and countries such as Africa, Russia and the Caspian

Organization of the Petroleum Exporting Countries 20

Sustainable development: a challenge for humanity

Energy is central to poverty eradication, sustainable development and

the achievement of the Millennium Development Goals

1.6 billion people have no access to electricity

2.5 billion people still rely on traditional biomass

Collective responsibility to help poorer nations

Future energy growth must support all three pillars of sustainable

development

Organization of the Petroleum Exporting Countries

CO2 emissions: the historical responsibility of developed countries

Cumulative CO2 emissions since 1900

GHG emissions will grow: mitigation options include Carbon Capture & Storage (CCS),

conservation and sinks

Historical responsibility of developed countries regarding the state of the Earth’s atmosphere

Ensure mitigation response measures and emission reduction commitments are fair and just

Developed countries should take the lead in mitigation, adaptation, funding & technology transfer

Looking for a win-win outcome for climate change negotiations

Per capita CO2 emissions (reference case)

21

Organization of the Petroleum Exporting Countries 22

Core industry challenges

Timely & sufficient investments along the entire supply chain

Adequacy of the human resources skills base

Technology role in

expanding production

improved recovery rates

deployment of cleaner technologies

Technology supporting sustainable development & environment

promotion of technologies that address climate change concerns

industrialized countries should take the lead in CCS

The critical importance of Research & Development & Deployment

Transfer of technology is vital

Organization of the Petroleum Exporting Countries

The role of NOCs and IOCs: enhanced cooperation

Many common objectives and challenges:

Important to enhance relationships among NOCs, as well as between

NOCs and IOCs

On such issues as the environment, the development of new

technologies, such as Carbon Capture and Storage (CCS), and helping

in the development of manpower and training (local content)

Such cooperation can also help bring down the high costs of services,

which are putting further pressure on well-devised output expansion

strategies

Aid further information exchange, as well as help evolve larger and

more developed research networks

Support broader socio-economic development and diversification

23

Organization of the Petroleum Exporting Countries 24

Common interest and shared responsibilities

Increasingly complex global energy system

Challenges und major uncertainties

Growing interdependence

Energy security should be treated as a shared responsibility by all parties

This is essential for the stable and sustainable oil market

Organization of the Petroleum Exporting Countries 25

In conclusion

Critical to bring all strands of the market together

Overall goal is to provide a stable setting for

expanding necessary investments

steady growth in economies

meeting environmental concerns

eradicating energy poverty

In-depth dialogue and cooperation among all stakeholders is the

way forward