WORLD MONEY ANALYST - Mauldin Economics · 2015-05-06 · job” mindset – rules and ethics be...

31

• Commodities The euro is headed into Act II of its epic death throws. Here’s a way to profit from the fall .................. Page 9 IN THIS ISSUE: Dear reader, A recent row between German and Swiss government officials again showed just how imperative it is for anyone with assets to scrutinize exactly where in the world those assets call home. To bolster revenue, part of the multi-pronged German response has been to task state revenue agents with buying information stolen from Swiss banks in pursuit of German citizens “hiding” money. The Swiss fired back with arrest warrants issued against three German tax inspectors, charging “industrial espionage.” German officials defended the action as legal and said they will shield the accused from any legal process. In stark contrast, the Swiss constitution prohibits information that is illegally obtained from being used as evidence. So, where do we want to place our assets: Under the rule of law, or the thumb of man? And just to be fair, the British, French, and Italian governments have the same “just doing our job” mindset – rules and ethics be damned. With that in mind, we have an expanded review of international brokers for your consideration coming up later in the issue, and jurisdictional safety is the top benchmark in our selection process. Our field of view at World Money Analyst is exactly as our name suggests. We are cartographers surveying the globe in search of opportunity, while also avoiding the land mines. Important developments can occur anywhere, be they close to home, or time zones afar. This month, more than one of our analysts have their eye on the next act in the European sovereign debt meltdown. No sooner had Greece slipped off the radar—interpreted by many to mean it was time to exhale—before Spain took the stage. Grant Williams shows us where this might lead. Kevin Brekke WORLD MONEY ANALYST INTERNATIONALIZE YOUR MONEY. YOUR LIFE. A MAULDIN ECONOMICS PUBLICATION ISSUE 3 • April 2012 International Overview Massive construction loan write- downs await Spain’s banks ...... Page 3 • • Recent developments have more emerging market money headed to Russia. Plus a new stock review ............................................... Page 6 Russia • International Investor’s Toolkit We review seven international brokers from Central America to Luxembourg to Hong Kong. Page 12 • The “unknown knowns” resurface in Europe, and a review of our positions .............................. Page 23 Europe • Weldon’s World Breaking down the US employment data debunks the alleged jobs recovery ................................ Page 17 • Currency Watch This is possibly the most “fiscally fit” currency in the world ........... Page 26 • China Non-market driven commodity demand will have market driven price consequences ............. Page 29

Transcript of WORLD MONEY ANALYST - Mauldin Economics · 2015-05-06 · job” mindset – rules and ethics be...

• CommoditiesThe euro is headed into Act II of its epic death throws. Here’s a way to profit from the fall ..................Page 9

IN THIS ISSUE:Dear reader,

A recent row between German and Swiss government officials again showed just how imperative it is for anyone with

assets to scrutinize exactly where in the world those assets call home.

To bolster revenue, part of the multi-pronged German response has been to task state revenue agents with buying information stolen from Swiss banks in pursuit of German citizens “hiding” money. The Swiss fired back with arrest warrants issued against three German tax inspectors, charging “industrial espionage.”

German officials defended the action as legal and said they will shield the accused from any legal process. In stark contrast, the Swiss constitution prohibits information that is illegally obtained from being used as evidence.

So, where do we want to place our assets: Under the rule of law, or the thumb of man? And just to be fair, the British, French, and Italian governments have the same “just doing our job” mindset – rules and ethics be damned.

With that in mind, we have an expanded review of international brokers for your consideration coming up later in the issue, and jurisdictional safety is the top benchmark in our selection process.

Our field of view at World Money Analyst is exactly as our name suggests. We are cartographers surveying the globe in search of opportunity, while also avoiding the land mines. Important developments can occur anywhere, be they close to home, or time zones afar.

This month, more than one of our analysts have their eye on the next act in the European sovereign debt meltdown. No sooner had Greece slipped off the radar—interpreted by many to mean it was time to exhale—before Spain took the stage. Grant Williams shows us where this might lead.

Kevin Brekke

WORLD MONEY ANALYSTINTERNATIONALIZE YOUR MONEY. YOUR LIFE.

A MAULDIN ECONOMICS PUBLICATION ISSUE 3 • April 2012

International Overview

Massive construction loan write-downs await Spain’s banks ...... Page 3

•

•Recent developments have more emerging market money headed to Russia. Plus a new stock review ............................................... Page 6

Russia

• International Investor’s ToolkitWe review seven international brokers from Central America to Luxembourg to Hong Kong. Page 12

•The “unknown knowns” resurface in Europe, and a review of our positions ..............................Page 23

Europe

• Weldon’s World

Breaking down the US employment data debunks the alleged jobs recovery ................................Page 17

• Currency Watch

This is possibly the most “fiscally fit” currency in the world ...........Page 26

• China

Non-market driven commodity demand will have market driven price consequences .............Page 29

WORLD MONEY ANALYST ISSUE 3 • April 20122

The inter-connected web of global economies means one country’s problems will have repercussions for others. With many global economies cooling and looking to the US consumer to keep the party rolling, any hint at trouble ahead for the US will be bad news for many. To gauge the claimed “US economic recovery,” Greg Weldon digs into the latest employment numbers to see just how robust job growth really is. (Hint: he’s short industrial metals, and shows you how to do the same.)

Alexei Medved, our Russian insider, takes a look at the country and its emerging market status. Russia is the world’s major oil and gas exporter, and Alexei singles out one of the country’s big energy companies selling at mouth-wateringly low valuations.

We also need to mention a change in the way WMA will track and report the companies mentioned in our service. Seeing that WMA is not an “alert” or trading service—nor is it priced like one, which typically costs thousands yearly—attempting to give trading advice doesn’t seem prudent. Nor would it be fair to our subscribers.

Our analysts are tasked with uncovering opportunities, and their analysis is the starting point from which subscribers should continue their own diligent research and monitoring. We will provide quarterly updates on the companies mentioned in our letter.

We cover much more this month, including how to profit from the inevitable fall in the euro, and a valuation method that reveals one of the world’s most “fiscally sound” currencies. All of our actionable information is distilled into easy reading in the Recap section at the end of the issue.

We’ll be back next month with insights from our global network of contributors with more value plays for your consideration.

Thank you for subscribing to the World Money Analyst!

Kevin Brekke

Managing Editor

Fribourg, Switzerland

WORLD MONEY ANALYST ISSUE 3 • April 20123

Remarkably, Spain seems to have suddenly become a problem to an investing public (temporarily) robbed of Greece as a focus for its fears. In truth, Spain has been a problem for quite some time and will continue to be one for the foreseeable future – potentially a

defining problem. It therefore makes sense for us to take a look at the main causes for concern on the Iberian Peninsula and familiarize ourselves with some of the metrics that will shape the future of Spain, and quite possibly the European Union.

Perhaps the most commonly offered statistic to gauge the Spanish economy is the numbers of unemployed. Currently, the overall number stands at 22.87%, while the number aged below 25 is a staggering 50.50% (according to Eurostat). These two markers are rolled out with ever-increasing regularity whenever talk turns to Spain’s “dire straits.”

But these unemployment numbers are hardly a “new, huge problem.” In June of 2011, Spain’s total number of unemployed was 20.93% and hasn’t been below 20% since March 2010. The number out of work under the age of 25 last registered below 40% way back in January of 2010, and hasn’t been below 30% since the dog days of 2008.

Another metric getting regular airtime is Spain’s public debt to GDP, currently at 61% but is forecast by the OECD to reach 73% by year’s end. This level is certainly sustainable and a long way from the often cited “tipping point” of 90%, and far below the UK’s 80%, the US’ 115%, or Japan’s mind-boggling 253%. However, recent research by Carmel Asset Management shows that if regional debt, as well as that guaranteed by banks and local government is included, Spain’s national debt soars 50% - smashing through the magic 90% barrier.

Regional governments get creativeSpanish regional governments have taken an inventive approach to avoid running up their

debt – they stopped paying their bills. In fairness, that tactic has proved quite effective thus far. But according to estimates, there are between €80 and €90 billion of unpaid bills, and creditors are increasingly agitated. Throw in the €50+ billion in debts guaranteed by State corporations and another €60 billion held by the social security fund, and the full scope of Spain’s indebtedness comes into view.

But as bad as the public finances are, Spain’s private balance sheet contains the real horrors, as its banking sector deals with the fallout from a construction boom that dwarfs that in the US. Private debt in Spain stands at a terrifying 227% of GDP. Corporations hold twice the debt relative to their output as those in the US and six times that of Germany’s corporate sector, with the banking and construction sectors the main culprits.

During the go-go years the construction industry peaked at 17% of GDP, as Spain’s property developers were building one home for every new member of the population between 2000 and 2008. Think about that for a second. In equivalent terms, that would mean a staggering 27 million

Mi Casa Es Su CasaBy Grant Williams

International Overview

WORLD MONEY ANALYST ISSUE 3 • April 20124

additional homes built in the United States in the same time period, when, according to the US Census Bureau, a “paltry” 15.8 million homes were added between 2000 and 2010. And where did the money come from to finance this Spanish tsunami of construction? Yes, you guessed it: Spain’s banks.

Loan write-down fallout could mirror Ireland’sIn 2010, outstanding construction loans made by the Spanish banking system were estimated

to equal roughly 50% of Spain’s GDP, and a wave of write-downs and provisions is beginning to sweep across the sector, leaving chaos in its wake. Open Europe recently estimated that of the roughly €400 billion in loans still outstanding to the Spanish construction sector, €80 billion is considered at serious risk of default. The banks hold a mere €50 billion in reserves to cover potential losses on those loans.

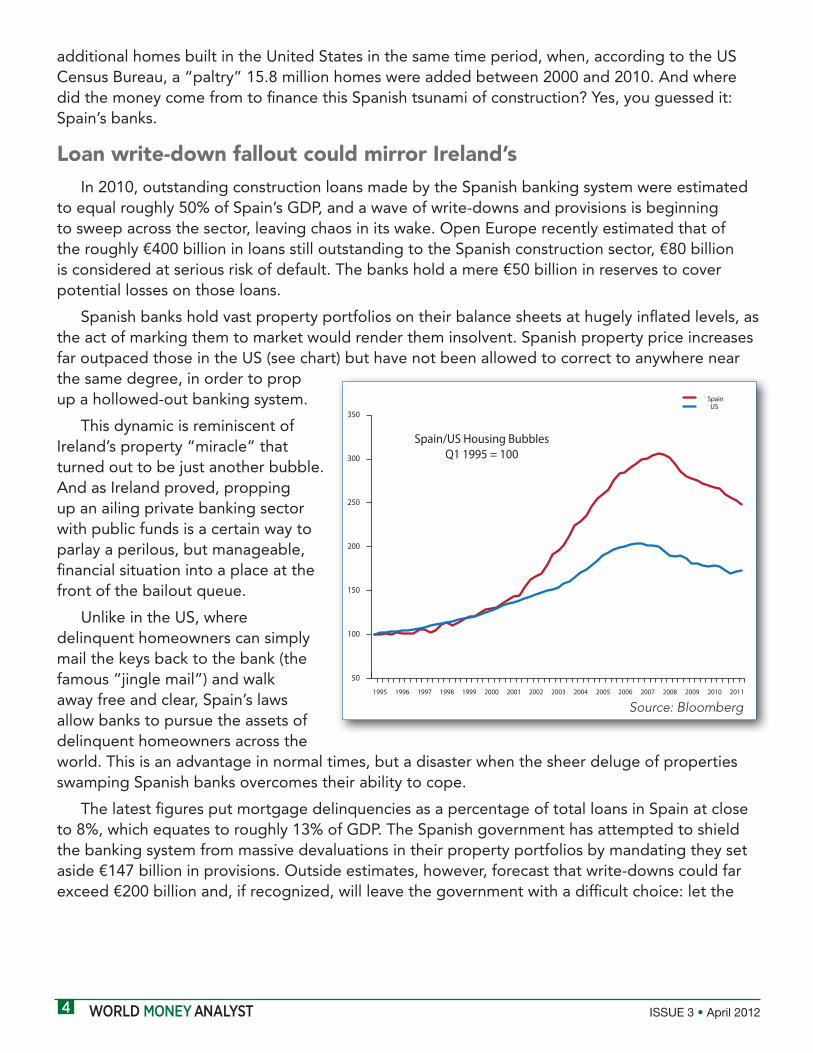

Spanish banks hold vast property portfolios on their balance sheets at hugely inflated levels, as the act of marking them to market would render them insolvent. Spanish property price increases far outpaced those in the US (see chart) but have not been allowed to correct to anywhere near the same degree, in order to prop up a hollowed-out banking system.

This dynamic is reminiscent of Ireland’s property “miracle” that turned out to be just another bubble. And as Ireland proved, propping up an ailing private banking sector with public funds is a certain way to parlay a perilous, but manageable, financial situation into a place at the front of the bailout queue.

Unlike in the US, where delinquent homeowners can simply mail the keys back to the bank (the famous “jingle mail”) and walk away free and clear, Spain’s laws allow banks to pursue the assets of delinquent homeowners across the world. This is an advantage in normal times, but a disaster when the sheer deluge of properties swamping Spanish banks overcomes their ability to cope.

The latest figures put mortgage delinquencies as a percentage of total loans in Spain at close to 8%, which equates to roughly 13% of GDP. The Spanish government has attempted to shield the banking system from massive devaluations in their property portfolios by mandating they set aside €147 billion in provisions. Outside estimates, however, forecast that write-downs could far exceed €200 billion and, if recognized, will leave the government with a difficult choice: let the

50

100

150

200

250

300

350

SpainUS

20112010200920082007200620052004200320022001200019991998199719961995

Spain/US Housing BubblesQ1 1995 = 100

Source: Bloomberg

WORLD MONEY ANALYST ISSUE 3 • April 20125

banks go under, or back them with public funds to “save the system.”

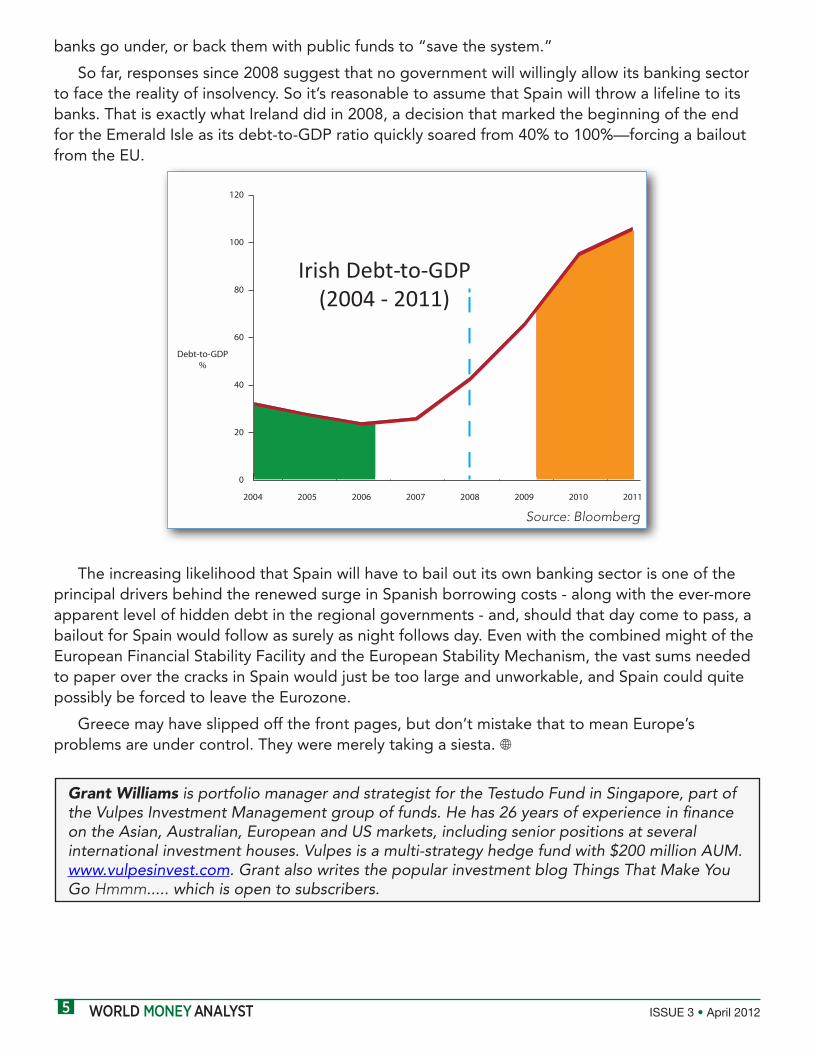

So far, responses since 2008 suggest that no government will willingly allow its banking sector to face the reality of insolvency. So it’s reasonable to assume that Spain will throw a lifeline to its banks. That is exactly what Ireland did in 2008, a decision that marked the beginning of the end for the Emerald Isle as its debt-to-GDP ratio quickly soared from 40% to 100%—forcing a bailout from the EU.

The increasing likelihood that Spain will have to bail out its own banking sector is one of the principal drivers behind the renewed surge in Spanish borrowing costs - along with the ever-more apparent level of hidden debt in the regional governments - and, should that day come to pass, a bailout for Spain would follow as surely as night follows day. Even with the combined might of the European Financial Stability Facility and the European Stability Mechanism, the vast sums needed to paper over the cracks in Spain would just be too large and unworkable, and Spain could quite possibly be forced to leave the Eurozone.

Greece may have slipped off the front pages, but don’t mistake that to mean Europe’s problems are under control. They were merely taking a siesta. •

0

20

40

60

80

100

120

20112010200920082007200620052004

Debt-to-GDP%

Irish Debt-to-GDP(2004 - 2011)

Source: Bloomberg

Grant Williams is portfolio manager and strategist for the Testudo Fund in Singapore, part of the Vulpes Investment Management group of funds. He has 26 years of experience in finance on the Asian, Australian, European and US markets, including senior positions at several international investment houses. Vulpes is a multi-strategy hedge fund with $200 million AUM. www.vulpesinvest.com. Grant also writes the popular investment blog Things That Make You Go Hmmm..... which is open to subscribers.

WORLD MONEY ANALYST ISSUE 3 • April 20126

Boring is Not BadBy Alexei Medved

Russia

I would like to start with an old Russian joke:

A wife is sitting near her dying husband. "Masha, do you remember how I was fired and couldn't find a job for 3 years? You stayed with me then." "Yes, darling, I remember." "Masha, do you remember how I was drunk and got my car smashed up in an accident? You were visiting me in the hospital for 5 years." "Yes, honey, I remember." "And now when I'm dying you are sitting here with me." "(Crying) Yes, my treasure!" "Masha, I'm starting to believe you bring me bad luck..."

This joke yet again reminds us how one should never confuse correlation with causation, as investors often do.

Russian Presidential elections are now behind us and Putin won a decisive victory. Big opposition rallies anticipated by much of the Western media following the elections have not materialised. The market participants’ perception of Russian political risk improved significantly, and added certainty descended onto Russian markets. All this led to significant inflows of cash to the Russian market. While the crisis in Europe and the general "risk-off" attitude of the Western markets had negatively affected investors’ willingness to invest in Russian assets that are seen as being risky, several recent developments were positive for the Russian market.

As the Brazilian Central Bank recently introduced a 6% tax on short-term (under 5 years) investments in Brazilian US$-denominated bonds to slow the inflows of cash and weaken the real, it is expected that some emerging market investors will move more of their money into the Russian market. With oil prices still high, and Russia being the world's major oil and gas exporter, the country’s economic position remains strong. Recently, the Russian government placed US$17 billion of Eurobonds that was well received by Western investors. This confirms that sophisticated investors see Russia as an acceptably attractive risk.

Bored in RussiaOver the last month or so, the Russian bond market was steady, with no major ups and downs.

One could even say that it was a fairly boring market. However, I think that for the bond market, boring is good. One can look for excitement elsewhere. I like boring bonds when every day brings the investor income from an attractive coupon interest rate. Depending upon the investor’s risk tolerance, one can buy Russian sovereign or “First Tier” corporate bonds that are issued by the strongest Russian companies.

WORLD MONEY ANALYST ISSUE 3 • April 20127

Country risk for Russia is currently rated as “investment grade,” and the strongest companies also share that rating. Depending upon the investor’s preference, bonds are available denominated in either US dollars or roubles. I discussed the currency diversification issue and the rouble’s attractiveness in my March column.

Given our concern about the potential increase in US inflation, we recommend that investors buy only short- and medium-term bonds.

Here are some examples of currently available “First Tier” bonds:

The above bonds are among the very safest in the Russian market, and could easily be bought without worrying about their quality. With over 20 years experience on the Russian market, we know what the risks are and how to evaluate them, and have been successful in buying higher-yielding Russian bonds.

We think the high returns offered by these bonds often more than compensate the investor for any added risk.

We believe that, ultimately, an investor’s concern is whether the bond is redeemed at maturity, even if it is perceived to carry a higher risk.

We only recommend our clients buy those bonds where we have strong belief that they will be repaid by the issuer. This requires monitoring the companies while holding their bonds. Any deterioration in a company’s financials means re-evaluating the risk and whether one should continue to hold its bonds or sell them.

US$ BondsIssuer Maturity Yield to Maturity

Gazprom 2013 2.3%

Gazprom 2016 4.3%VTB* 2018 6.1%

Rouble BondsIssuer Maturity Yield to Maturity

Gazprom 2013 6.2%VTB* 2013 8.0%VTB* 2014 8.5%

* Major state-owned bank

WORLD MONEY ANALYST ISSUE 3 • April 20128

Alexei Medved was born and raised in Russia and later moved to the West. He received an MBA from Wharton Business School and worked for a major global investment bank, where from 1989, he developed the East European investment banking business. Since 1992, he has been running an independent business which concentrates on investments in Russia and the CIS. Contact: [email protected]

Russian oil companies remain attractiveI would also like to take a look at Russia shares, in particular, Surgutneftegas (LSE: SGGD;

ADR), the fourth largest Russian oil company. Surgutneftegas’ oil production in 2011 was about 1,444 kboe/day, or, 527 million barrels of oil per year. At its current price of US$9.78 per ADR, the company’s market cap is around US$39 billion.

The company has about US$29 billion in cash and essentially no debt. It is trading at a P/E of 4.0 (based on 2011 earnings).

Surgutneftegas is a very conservatively run company, and management makes a virtue of meticulously complying with all its legal and tax obligations. It also has a good relationship with the Russian government.

We particularly like its preferred shares that trade in Russia at US$0.65/share. Just to clarify, in Russia, preferred shares are entitled to a dividend which is not fixed like it often is for Western companies, but will vary depending on company profits. This dividend is usually paid annually. Based on a projected dividend for 2011, the preferred shares will yield around 11%.

The important catalyst for future price appreciation is likely to be the recent change in Russian accounting rules that will essentially force the company to pay a higher dividend on preferred shares.

These shares are likely to rise, as the market will see them as increasingly attractive. This looks like an attractive and fairly conservative investment.

Update on Gazprom. On April 13, Gazprom announced that management recommended a dividend for 2011 of RUR8.97/share, representing a payout ratio of 25% of the Russian Accounting Standards unconsolidated net profit of RUR879.6 billion.

This is somewhat higher than expected, so good news. If this is accepted by the Board of Directors and approved at the annual general meeting on June 26, at the current share price of RUR176/share, the yield will be 5.1%. ADR owners will also receive a dividend, proportional to the ratio of how many local shares are in the ADR, and converted into the currency of the ADR – in this case euros. •

WORLD MONEY ANALYST ISSUE 3 • April 20129

Traders who missed the first leg of the big down-move in the euro made the mistake of focusing on Greece and not the larger issue the Greek crisis illuminated: the euro has deep structural faults that require a political solution, not an economic one. These

structural issues are as real today as they were a year ago. Many believe they have gotten worse. As we write this, the common currency is trading at $1.3100. We expect it to fall to $1.2000 – and possibly as low as parity with the US dollar before it is over.

Four Reasons the Euro Will Continue to Drop1) Greece has already defaulted. Portugal is probably next. 10-year Portuguese government

bonds are yielding over 12.5%. A yield this high assumes a high risk of default. Greek bonds traded at similar levels back when markets still believed it could be saved. It could not. The Greek economy shrank 6.9% in 2011, essentially guaranteeing default. Citigroup expects the Portuguese economy to contract 5.7% in 2012, damaging its ability to service debt. This increases its odds of default.

2) Spain is not far behind. With an unemployment rate of 23.3%, a real estate market that is falling off a cliff (down 11.2% in the 4th quarter) and the highest debt load on record, Spain is an economic basket case. The Spanish economy is much larger than Portugal’s, making a potential default or restructuring far more destructive, and a run on Spanish debt far more damaging. Spanish bond yields are approaching 6%, a level which traders watch very carefully.

3) Austerity has plenty of enemies. Spring elections in France and Greece could throw financial rescue operations into disarray. Big gains by opposition parties more interested in growth than sacrifice could undo austerity pledges and cause the euro to weaken dramatically.

4) A stronger US economy decreases the odds of QE3 and increases the odds of a surprise rate increase. Any indication by the Fed that its zero interest rate policy could be ending would be extremely euro negative. In fact, the expectation of a possible QE3 in the US is one of the only things keeping a bid under the euro right now.

Single Currency, Divided CulturesAsk a Texan his nationality and he will inevitably say, “American.” Ask a Californian hers and

she’ll say the same. But ask a German or Frenchman and the odds are good he or she will say “German” or “French,” not “European.” Americans migrate all over the 50 states in search of work. And while Europeans can theoretically do the same, differences in language, culture and skill-sets make this kind of economic flexibility rare in practice.

Death of the Euro: Act IICommodities

By Steve Belmont

WORLD MONEY ANALYST ISSUE 3 • April 201210

The problem with the European Union and the euro is simple: Greeks and Portuguese won’t move to Germany or France in search of work and, more importantly, the Germans and French don’t want them to.

Before the euro, the weaker nations of Southern Europe would do what weaker nations always do: lower interest rates and weaken their currencies. This would (1) make their debt cheaper in real terms, and (2) increase exports, boosting their domestic economies while providing more cash flow for debt service. But Portugal, Ireland, Italy, Greece and Spain (the PIIGS) can’t do this because they are not in control of their currencies. The European Central Bank (ECB) is.

“LTRO” Another Way to Say “QE”This is not to say the ECB isn’t trying to do its best. Instead of lending to individual countries

by purchasing their bonds directly – something prohibited in its charter – the ECB is lending to European banks directly at super-cheap interest rates in the hope the banks will take the cash and invest it in the very same government bonds the ECB is prohibited from buying – keeping a bid under the market and preventing a credit freeze.

This is essentially a “back door” form of Quantitative Easing (QE). The ECB calls this a Long Term Refinancing Operation (LTRO), but QE by any other acronym is still QE. So far, the ECB has committed €1.1 trillion ($1.45 trillion), little more than half of the money the Fed created ($2.3 trillion) in its QE1 and QE2 operations.

This has temporarily “fixed” Europe’s near-term problem of liquidity but done virtually nothing to fix the long-term problem of solvency. Flooding the market with newly-created euros has merely “kicked the can down the road.” Meanwhile, real dangers wait down that road.

Because it created trillions of new dollars and artificially increased supply, the Fed’s version of QE was dollar-negative. More dollars mean each dollar buys less. We expect the European version of QE to be euro-negative as well. More euros mean each euro buys less. While the increased liquidity due to the ECB’s creation of 1.1 trillion new euros has done its job and stabilized the European sovereign debt market, it has done nothing to fix the underlying causes of the crisis. Despite the flood of new ECB money, Portuguese bonds are still pricing in a potential default. Yields on Spanish and Italian sovereign debt continue to climb, approaching danger zones as well.

Déjà Vu All Over AgainSince they can’t cheapen their currencies, the Eurozone’s problem children have few options.

They can raise taxes, cut spending, or both. The trouble is these actions will negatively affect growth. Without economic growth, default may be delayed but it can’t be averted.

This is what has happened to Greece. Enforced austerity led to a shrinking economy, which led to less tax revenue and more indebtedness. This same dynamic is threatening both Portugal and Spain. Citigroup expects the Portuguese economy to contract 5.7% in 2012. The Spanish government expects its economy to shrink 1.7% in 2012. Spain’s debt to foreigners is now 100% of GDP. As GDP shrinks, the percentage of debt owed to foreigners grows. Default looms larger for both nations even with the ECB’s big LTRO.

WORLD MONEY ANALYST ISSUE 3 • April 201211

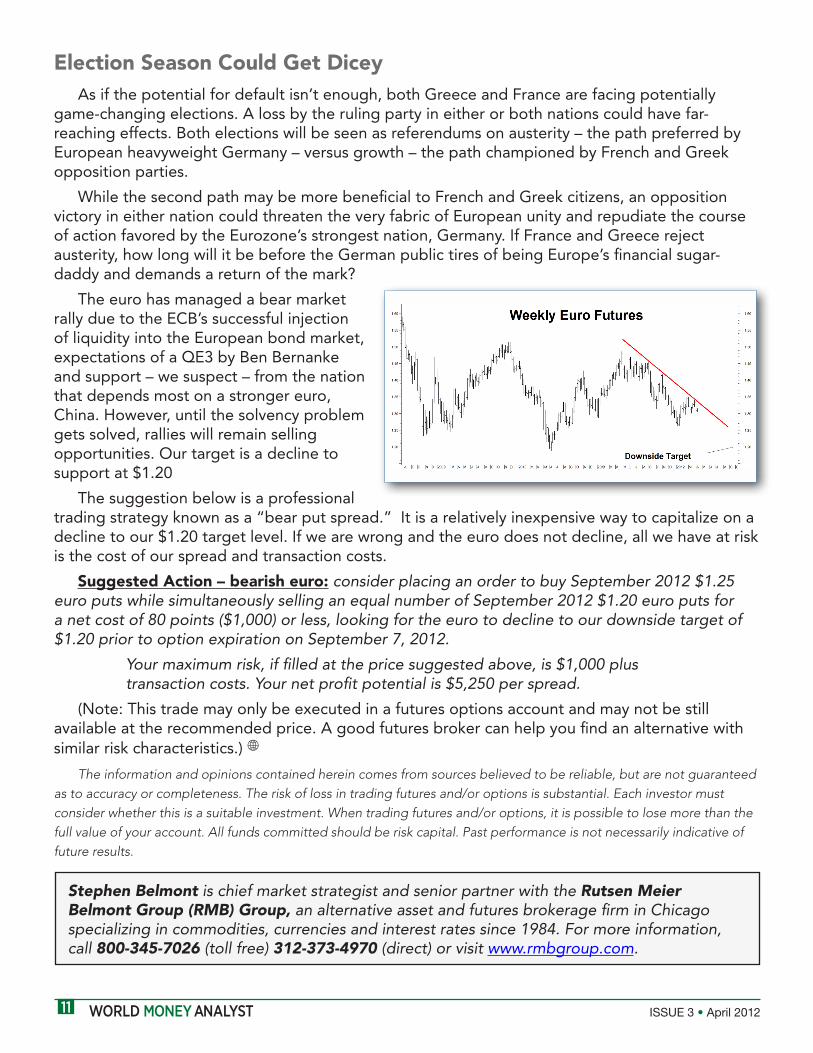

Election Season Could Get DiceyAs if the potential for default isn’t enough, both Greece and France are facing potentially

game-changing elections. A loss by the ruling party in either or both nations could have far-reaching effects. Both elections will be seen as referendums on austerity – the path preferred by European heavyweight Germany – versus growth – the path championed by French and Greek opposition parties.

While the second path may be more beneficial to French and Greek citizens, an opposition victory in either nation could threaten the very fabric of European unity and repudiate the course of action favored by the Eurozone’s strongest nation, Germany. If France and Greece reject austerity, how long will it be before the German public tires of being Europe’s financial sugar-daddy and demands a return of the mark?

The euro has managed a bear market rally due to the ECB’s successful injection of liquidity into the European bond market, expectations of a QE3 by Ben Bernanke and support – we suspect – from the nation that depends most on a stronger euro, China. However, until the solvency problem gets solved, rallies will remain selling opportunities. Our target is a decline to support at $1.20

The suggestion below is a professional trading strategy known as a “bear put spread.” It is a relatively inexpensive way to capitalize on a decline to our $1.20 target level. If we are wrong and the euro does not decline, all we have at risk is the cost of our spread and transaction costs.

Suggested Action – bearish euro: consider placing an order to buy September 2012 $1.25 euro puts while simultaneously selling an equal number of September 2012 $1.20 euro puts for a net cost of 80 points ($1,000) or less, looking for the euro to decline to our downside target of $1.20 prior to option expiration on September 7, 2012.

Your maximum risk, if filled at the price suggested above, is $1,000 plus transaction costs. Your net profit potential is $5,250 per spread.

(Note: This trade may only be executed in a futures options account and may not be still available at the recommended price. A good futures broker can help you find an alternative with similar risk characteristics.) •

The information and opinions contained herein comes from sources believed to be reliable, but are not guaranteed as to accuracy or completeness. The risk of loss in trading futures and/or options is substantial. Each investor must consider whether this is a suitable investment. When trading futures and/or options, it is possible to lose more than the full value of your account. All funds committed should be risk capital. Past performance is not necessarily indicative of future results.

Stephen Belmont is chief market strategist and senior partner with the Rutsen Meier Belmont Group (RMB) Group, an alternative asset and futures brokerage firm in Chicago specializing in commodities, currencies and interest rates since 1984. For more information, call 800-345-7026 (toll free) 312-373-4970 (direct) or visit www.rmbgroup.com.

WORLD MONEY ANALYST ISSUE 3 • April 201212

An Update on Global Brokerages By Kevin Brekke

International Investors Toolkit

I In response to many requests from our readers, this month we have assembled a select list of brokerage service providers to assist our international subscribers in trading the equities we cover. We always suggest trading equities on their native exchanges versus a US OTC listing,

and we have identified several of the best-in-class brokers to help you do just that.

Many of the brokers reviewed below do not accept US persons or restrict their options. Unfortunately, that is the new reality in today’s financial climate where onerous reporting mandates placed on non-US financial companies by the American tax authorities has created a costly and time-consuming burden that many choose not to endure. However, four of our selected brokers will accept US persons as clients, although we point out that two of them come with strings attached.

There are hundreds of brokers in dozens of countries all competing for a slice of the global investment trade, and the pool of “possibles” is daunting. So, how did we sift through the pool?

Here is the “criteria filter” through which each broker must pass:

• Offer online accounts. Using an online trading account gives the investor total control over his or her investments and the freedom to trade 24/7 from any location with Internet access.

• Charge lower commissions. Another benefit of using an online account for self-directed trades is that commissions are almost always less than placing a broker-assisted trade.

• Solid business. Your online account is only as safe as the company it keeps – literally. We look for brokers with a solid history in the stock broking trade, a large user base, and that are profitable businesses.

• In a safe jurisdiction. The intrusion of national governments into the operations of financial institutions and the private affairs of individuals is an ever-present threat. Only a broker domiciled in a country with strong financial regulation and oversight, and that will uphold the rule of law and defend property rights is considered.

As with all decisions concerning whom to trust with your investment money, please conduct your own due diligence when considering any of the following companies; this includes enquiring about the availability of specific investment products you intend to purchase. Each company’s access to markets and products is fluid and can change without warning.

Additionally, various trading fees are imposed by certain country exchanges—e.g., stamp duty, clearing fee, transfer tax—and some brokers charge an inactivity fee for accounts that fail to meet broker-specific minimum activity. The transfer of funds by wire, stock transfer to/from a broker, foreign currency conversion, margin rates, and other standard charges will vary between brokers.

It is important to dedicate the time to understand the total fee structure for each broker prior to opening an account to avoid any surprises.

Lastly, the theme of diversification applies here as well. Just as we advise not to hold all your wealth in any single country, bank, industry sector, or investment, the same caution applies to brokerages.

WORLD MONEY ANALYST ISSUE 3 • April 201213

With the fine print out of the way, here are our hand-picked brokers that we believe are worthy of your consideration. Company headings are clickable links to their respective websites.

Saxo Bank - Denmark Saxo Bank is a Denmark-domiciled licensed and regulated European global investment bank

specializing in online trading with offices in Copenhagen, London, Madrid, Paris, Singapore, Tokyo and Zurich.

Trading accounts can be opened online with a US$2,000 minimum (or its equivalent in another currency). Their SaxoWebTrader and SaxoMobileTrader (trading from a mobile phone) trading platforms give access to 30 world markets in the US, Canada, S. Africa, Western/Eastern Europe, Scandinavia, and Asia/Pacific. Trading is offered in currencies, forex options, shares, futures, commodities, ETFs, bonds, ETCs* and CFDs**.

Their commissions are aggressively competitive. Here are examples for share trading: U.S. exchanges, $0.02/share, $15 min.; Europe exchanges, 0.10%, €12 min.; Canada TSE, CAD0.03/share, CAD25 min; Hong Kong exchange, 0.15%, HKD150 min. (≈US$20); UK LSE exchange, 0.10%, GBP8 min.

Nationality Restrictions: U.S. citizens/residents not accepted as clients.

optionsXpress - US & Int’l Accounts

(In March 2011, Charles Schwab announced the acquisition of optionsXpress, and the merger was completed in the second half of 2011. According to the FAQ section on the optionsXpress website, existing Schwab and optionsXpress customers will experience no change in using their accounts.)

Opening an account online is straightforward and there is no minimum. And don’t let their name fool you; with optionsXpress you can trade shares, futures, ETFs, bonds, and mutual funds as well as options – and do it all from a single trading account.

The website is easy to navigate and their investor-friendly trading platform includes real-time streaming quotes and online tutorials to get you started.

Commissions: a flat US$8.95 per trade for US clients; optionsXpress Europe, Singapore, Australia, and Canada, US$9.95-US$14.95 for trades up to 1,000 shares; option contracts are a flat US$14.95, but varies with higher trading volumes. Margin trading is also available.

With a presence in Australia, Netherlands, Singapore, and Canada, optionsXpress might work for international subscribers that want to buy the equities covered in World Money Analyst that trade on the U.S. and Canadian exchanges. For U.S. accounts, keep in mind that non-U.S. companies can be traded only if they have a cross-listing on a US exchange or a US-listed ADR. For many foreign companies, this will mean trading on the OTC market, something we do not recommend.

Nationality Restrictions: U.S. persons limited to a U.S.-based (Chicago) account.

WORLD MONEY ANALYST ISSUE 3 • April 201214

Internaxx - Luxembourg Based in Luxembourg, Internaxx is owned by TD Waterhouse, one of the UK’s leading brokers.

The parent company of TD Waterhouse is the Toronto-Dominion Bank.

Users have access to real-time online share dealing on 18 exchanges in North America, Europe, and Asia/Pacific. Multi-currency trading accounts are available in AUD, CAD, CHF, EUR, GBP, HKD, SEK, SGD, and USD. Internaxx offers trading in shares, currencies, interest rates, commodities, futures, CFDs** and several hundred equity, bond, and money market funds from leading international providers.

Examples of commission rates: for orders under €5,000: €28 on US/Canada/Europe exchanges; €45 on Asia exchanges. For orders between €5,000 and €10,000: €35 on US/Canada/Europe exchanges; €55 for Asia exchanges. For broker-assisted trades add €20/trade. Frequent traders—30 or more trades per calendar year—earn a 20%-30% commission discount, depending on the exchange traded.

Nationality Restrictions: U.S. citizens/residents and Canadian residents not welcome.

iOCBC - Singapore

Started in1986 as Oversea-Chinese Banking Corporation Limited, in 2001 this Singapore-based company acquired UBS Warburg & Associates Private Limited (Singapore) and Keppel Capital Holdings. The acquisitions propelled OCBC Securities into the ranks of Singapore’s leading stock broking firms.

iOCBC is the company’s online trading division offering commodity futures, forex, ETFs, shares, warrants, and Extended Settlement contracts***. Although the depth of products offered is comparatively shallow, the breadth of exchanges traded is impressive: Australia (ASX), Hong Kong (HKEX), Indonesia (IDX), London (LSE), Malaysia (BURSA), Philippines (PSE), Shanghai (SSE) & Shenzhen (SZSE) B-shares only, Singapore (SGX), Thailand (SET), Tokyo (TSE), and the U.S. (NYSE, AMEX, NASDAQ).

Marginable securities, product availability, commissions, and settlement currencies depend on the exchange being traded and account type.

Commission example on the SGX exchange: for orders under US$30,000, 0.275% with a US$14 min. Complete mobile trading from an iPhone is available. Consult the website for details.

Nationality Restrictions: U.S. citizens/residents accepted as clients but barred from trading on U.S. exchanges. All non-Singapore citizens/permanent residents must make a US$2,000 deposit to open an account.

WORLD MONEY ANALYST ISSUE 3 • April 201215

SWISSQUOTE - Switzerland

SWISSQUOTE is part of Swissquote Group and headquartered in Gland (in canton Vaud) with offices in Zürich. Launched in 2000, it has rapidly grown into Switzerland’s leading online broker and lists on the Swiss Market Exchange (SIX: SQN).

Electronic share dealing is available on the following exchanges: Switzerland (SIX), U.S. (NYSE, Arca, AMEX, NASDAQ), Austria (ATX), UK (LSE), Italy (Borsa Italiana), Frankfurt (XETRA), Euronext, Canada (TSX, TSX-V), and the pan-Nordic OMX trading facility (Stockholm, Helsinki, Oslo, and Copenhagen). Another 60 markets in 40 countries, including Brazil, S. Africa, Middle East, Asia and Australia are traded via phone-executed orders. Trading in options, futures, warrants, bonds, structured products and forex is also available

Commission on ETFs and over 3,000 funds is a flat 9 CHF/9 EUR/9 USD. Commission for an equity order between 2,000 and 10,000 (in either CHF/USD/CAD/EUR/GBP) is 35 CHF/USD/CAD/EUR/GBP. Accounts can be held in Swiss francs, Euros or USD.

Nationality Restrictions: U.S. citizens/residents not accepted as clients.

Thales Securities - Panama

Founded in 1998, Thales Securities is the largest brokerage firm in Panama and is headquartered in Panama City. It is fully licensed and regulated by the National Securities Commission of Panama.

Thales is a discount online brokerage offering trading in stocks, forex, options, futures, ETFs and CFDs**. Exchanges traded include: US (NYSE, Arca, NASDAQ, AMEX), Euronext, Amsterdam (AMS), Australia (ASX), OMX (Copenhagen, Helsinki, Stockholm), Frankfurt (XETRA), Hong Kong (HKEX), London (LSE), Borsa Italiana (MIL), Oslo (OSE), Spain (SIBE), Switzerland (SIX), Canada (TSE, TSX), Vienna (VIE), and Warsaw (WSE).

There are no monthly or activity fees and no account-opening minimum. Commission examples: US markets, US$0.03/share for shares over USD10, US$0.05/share for shares under US$10, min. US$19.95; mutual funds, min. US$50; Hong Kong, 0.15% of order, min. HKD150 (≈US$20); Frankfurt, 0.25% of order, min. EUR30.

A 30-day free trial of the Thales Trader platform is available and customer support is handled in both English and Spanish.

Nationality Restrictions: None.

WORLD MONEY ANALYST ISSUE 3 • April 201216

Monex Boom Securities - Hong Kong

Monex Boom Securities started life as BOOM Securities, founded in 1997 as a fully licensed broker/dealer regulated by the Securities and Futures Commission of Hong Kong and headquartered in Hong Kong. BOOM was bought by Monex Securities in 2010 and is now part of the Monex Group, one of Japan’s largest online brokers and headquartered in Tokyo.

Monex Boom is an online broker only with trading on the following markets: Hong Kong (HKEX), US (NYSE, NASDAQ), Japan (Tokyo, Fukuoka, Nagoya, Osaka and Sapporo exchanges), Singapore (SGX), Thailand (SET), Taiwan (TWSE), China (SSE, SZSE; B and H shares), Indonesia (IDX), Korea (KRX), Malaysia (BURSA), Australia (ASX), and the Philippines (PSE).

Commissions are competitive with other online brokers: Hong Kong, 0.18% of order, US$12 min.; US, flat US$20 up to 5,000 shares; Singapore, 0.30% of order, US$17.50 min.; Australia, 0.40% of order, AUD35 min.

There is an account-opening fee of HKD200 (≈US$25) and a yearly administrative fee of HKD200 as well. Cash in accounts can be held in six currencies: HKD, RMB, USD, JPY, SGD and AUD. Monex Boom charges something we haven’t come cross so far, a dividend fee. It is assessed for all exchanges and ranges from a fixed US$3-US$6.50, to a set percentage of 0.50% to 1.0%. This is something to keep in mind if buying a stock for its dividend.

Nationality Restrictions: None. •

* Exchange Traded Commodities. Similar to ETFs, ETCs track the performance of an underlying commodity index. You can take short and long positions and employ varying degrees of leverage either way.

** Contracts for Difference. A CFD is a derivative product mirroring the movement of an underlying share, index or commodity. It works like a futures contract in that there is no limit to the gain or loss that can be realized by the holder, and the contract has no expiry date. It works like an option in that it has a time decay aspect, but with a twist: whereas for an option you pay a set price and the option is either sold or it expires and you lose your premium, a CFD is bought on margin, long or short, and the holder is assessed a daily interest fee against the holding’s value. So the longer you hold the CFD, the higher your cost basis.

*** Extended Settlement contract. An ES contract is a contract between two parties to buy or sell a specific quantity of shares, of a specific underlying stock, at a specific price, for settlement at a specific future date when the contract matures or expires. Translation: this is an option contract.

We continue to scout the globe for additional brokers that meet our selection criteria, and will update our list when successful. Comments or a suggestion about a broker you think is worth considering can be sent to [email protected].

WORLD MONEY ANALYST ISSUE 3 • April 201217

From the Grateful Dead, a band whose name exemplifies the US labor market following the release of the BLS Employment Situation Report on Friday, April 6:

“Red and white, blue suede shoes,

I’m Uncle Sam, how do you do?

Gimme five, I’m still alive.

Ain’t no luck, I learned to duck.

I’ll drink your health, share your wealth,

Run your life, steal your wife.

Wave that flag, wave it wide and high.”

It “ain’t no luck” that the US labor market was prevented from weaving downward, into a deflationary spiral. Uncle Sam has “learned to duck” under the leadership of the US Federal Reserve and Ben “Boom-Boom” Bernanke, who are now saying “gimme five” amid the suggestion that their monetary work is “done.”

The labor market data says otherwise.

At a time when the Administrative branch of the US government is proposing to “share your wealth” and “run your life” …

… Gasoline prices are threatening to breakout to unprecedented levels …

… and downward pressure remains the dominant force in housing.

US consumers are in DESPERATE need of “real” job growth and some good old-fashioned wage income reflation. There is NOTHING of the kind to be found, anywhere, in the March labor market report. Rather, there are some VERY disturbing facts and figures to be extracted from the employment-unemployment data.

For example, the Birth-Death Model “added” 90,000 jobs to the headline Payroll Employment figure (+120,000), meaning that “real” job growth was a mere 30,000.

Moreover, the gain in headline Payroll Employment (+120,000) lagged the +169,000 rise in the civilian population during March, meaning that real job growth was NEGATIVE.

Digging deeper, some very disturbing trends are revealed.

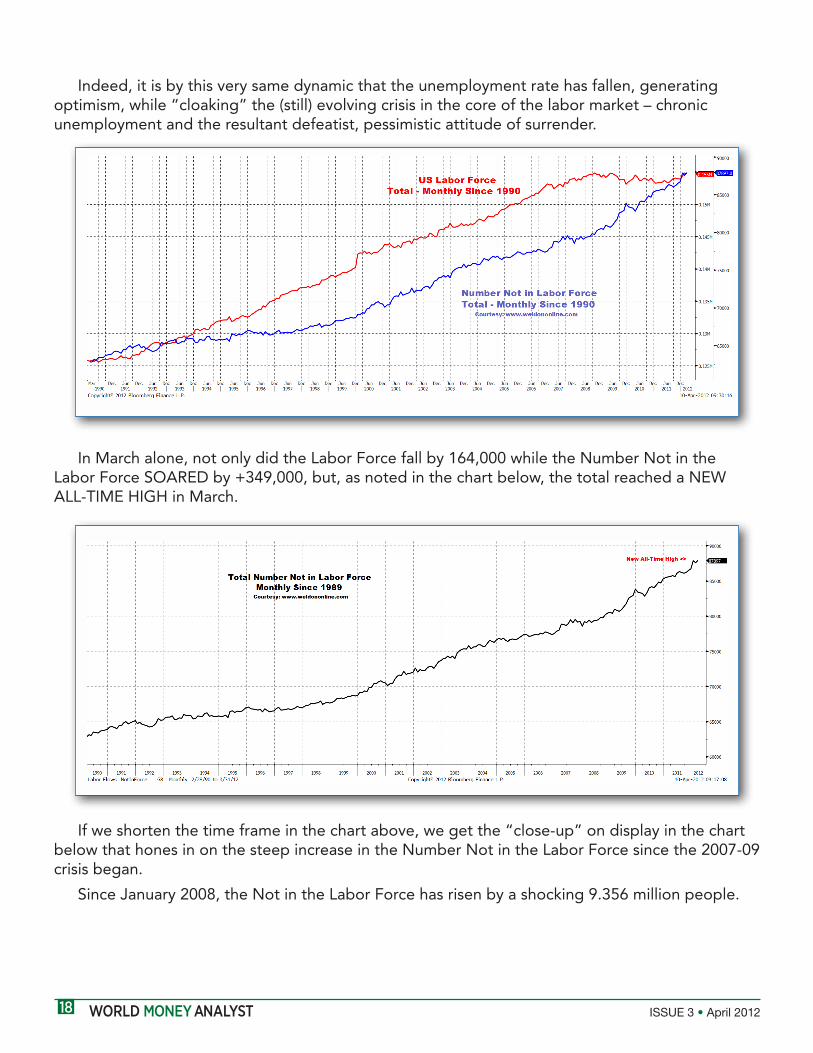

The “core” problem preventing the US labor market from achieving real growth is represented in the overlay chart below. In short, the degree of deflation in the US labor market during the 2007-09 crisis was SO SEVERE, that the growth in unemployed workers who were (are) falling out of the labor force has (is) outpaced the growth in the labor force.

Macro-USA: Wave That FlagWeldon’s World

By Greg Weldon

WORLD MONEY ANALYST ISSUE 3 • April 201218

Indeed, it is by this very same dynamic that the unemployment rate has fallen, generating optimism, while “cloaking” the (still) evolving crisis in the core of the labor market – chronic unemployment and the resultant defeatist, pessimistic attitude of surrender.

In March alone, not only did the Labor Force fall by 164,000 while the Number Not in the Labor Force SOARED by +349,000, but, as noted in the chart below, the total reached a NEW ALL-TIME HIGH in March.

If we shorten the time frame in the chart above, we get the “close-up” on display in the chart below that hones in on the steep increase in the Number Not in the Labor Force since the 2007-09 crisis began.

Since January 2008, the Not in the Labor Force has risen by a shocking 9.356 million people.

WORLD MONEY ANALYST ISSUE 3 • April 201219

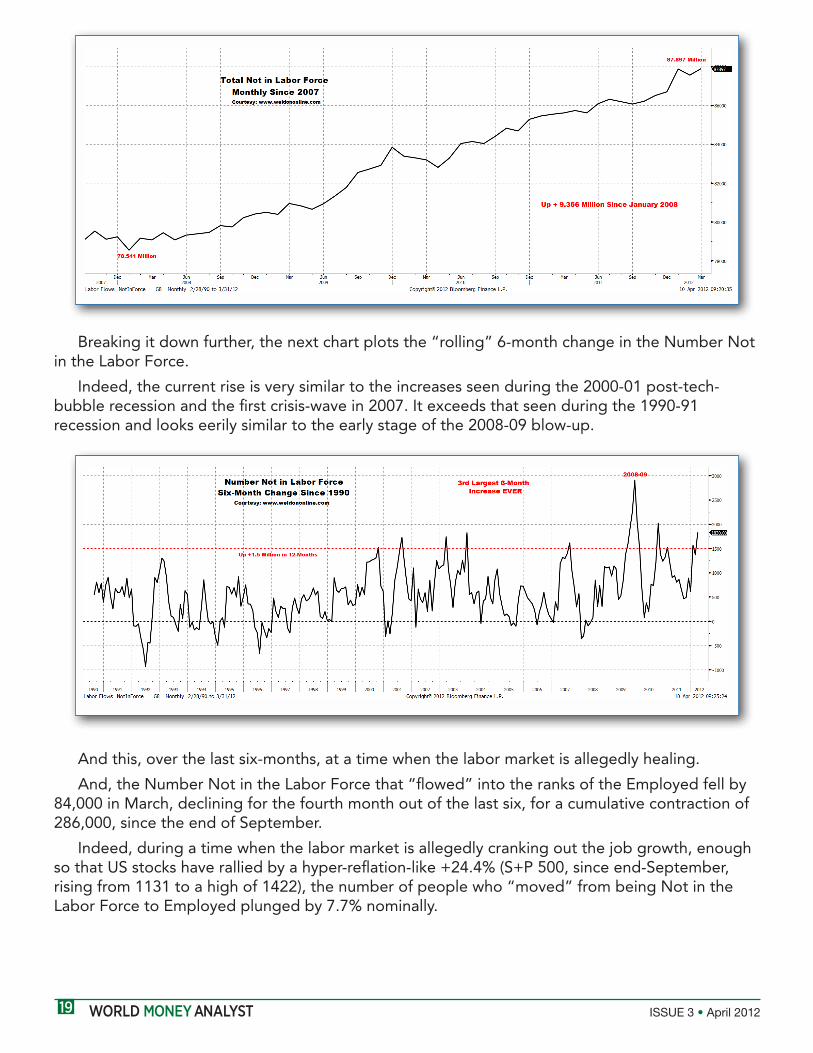

Breaking it down further, the next chart plots the “rolling” 6-month change in the Number Not in the Labor Force.

Indeed, the current rise is very similar to the increases seen during the 2000-01 post-tech-bubble recession and the first crisis-wave in 2007. It exceeds that seen during the 1990-91 recession and looks eerily similar to the early stage of the 2008-09 blow-up.

And this, over the last six-months, at a time when the labor market is allegedly healing.

And, the Number Not in the Labor Force that “flowed” into the ranks of the Employed fell by 84,000 in March, declining for the fourth month out of the last six, for a cumulative contraction of 286,000, since the end of September.

Indeed, during a time when the labor market is allegedly cranking out the job growth, enough so that US stocks have rallied by a hyper-reflation-like +24.4% (S+P 500, since end-September, rising from 1131 to a high of 1422), the number of people who “moved” from being Not in the Labor Force to Employed plunged by 7.7% nominally.

WORLD MONEY ANALYST ISSUE 3 • April 201220

In other words, job growth since the end of September has completely FAILED to make a DENT in “reversing” the nine-million-plus rise in those Not in the Labor Force, or in the underlying problem – the chronic unemployment crisis.

And, by this “measure,” rather than being just “less weak” the labor market’s situation actually got overtly WORSE in March.

In fact, we note the following statistics from the Labor Force Flow figures:

• From Employed to Not in Labor Force rose by +260,000, or +7.3%, nominally, in a single-month.

• From Unemployed to Not in Labor Force rose by +142,000, or +5.4% nominally in just one-month.

Also:

• From Employed to Unemployed ROSE

• From Unemployed to Employed FELL

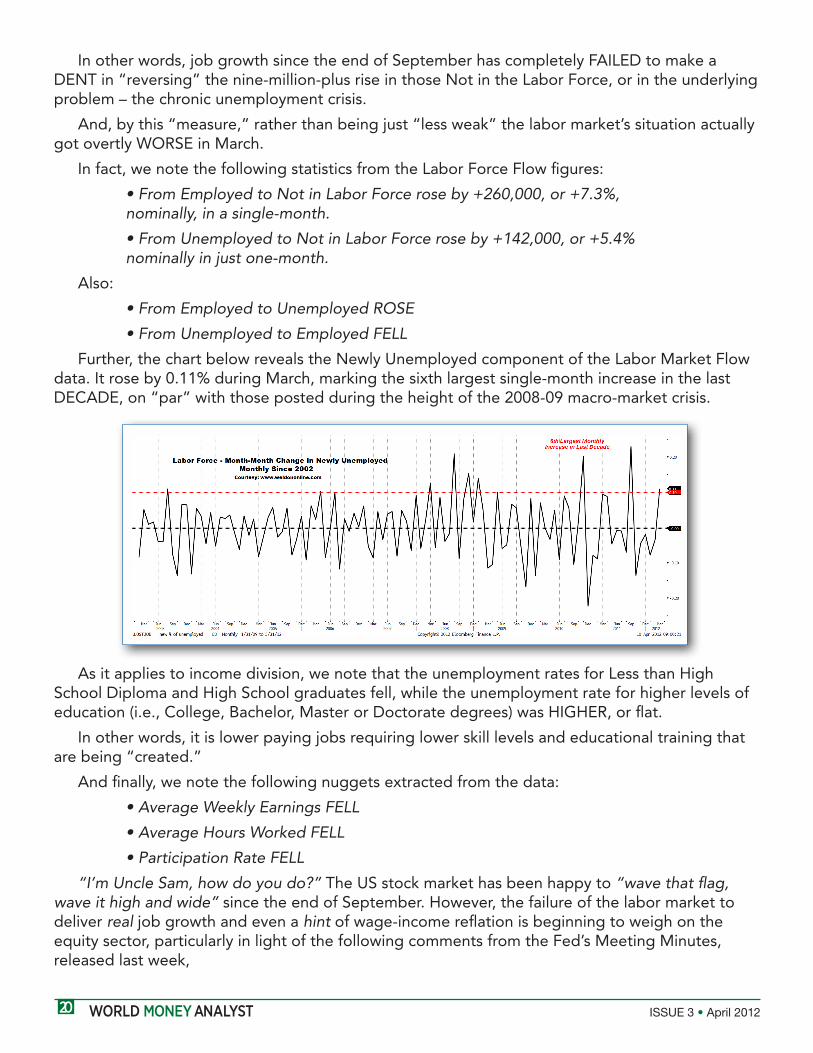

Further, the chart below reveals the Newly Unemployed component of the Labor Market Flow data. It rose by 0.11% during March, marking the sixth largest single-month increase in the last DECADE, on “par” with those posted during the height of the 2008-09 macro-market crisis.

As it applies to income division, we note that the unemployment rates for Less than High School Diploma and High School graduates fell, while the unemployment rate for higher levels of education (i.e., College, Bachelor, Master or Doctorate degrees) was HIGHER, or flat.

In other words, it is lower paying jobs requiring lower skill levels and educational training that are being “created.”

And finally, we note the following nuggets extracted from the data:

• Average Weekly Earnings FELL

• Average Hours Worked FELL

• Participation Rate FELL

“I’m Uncle Sam, how do you do?” The US stock market has been happy to “wave that flag, wave it high and wide” since the end of September. However, the failure of the labor market to deliver real job growth and even a hint of wage-income reflation is beginning to weigh on the equity sector, particularly in light of the following comments from the Fed’s Meeting Minutes, released last week,

WORLD MONEY ANALYST ISSUE 3 • April 201221

One member anticipated that a tightening of monetary policy would be necessary well before the end of 2014, in order to keep inflation close to the Committee’s target … (and that) … maintaining the current degree of policy accommodation much beyond the end of this year would be inappropriate.

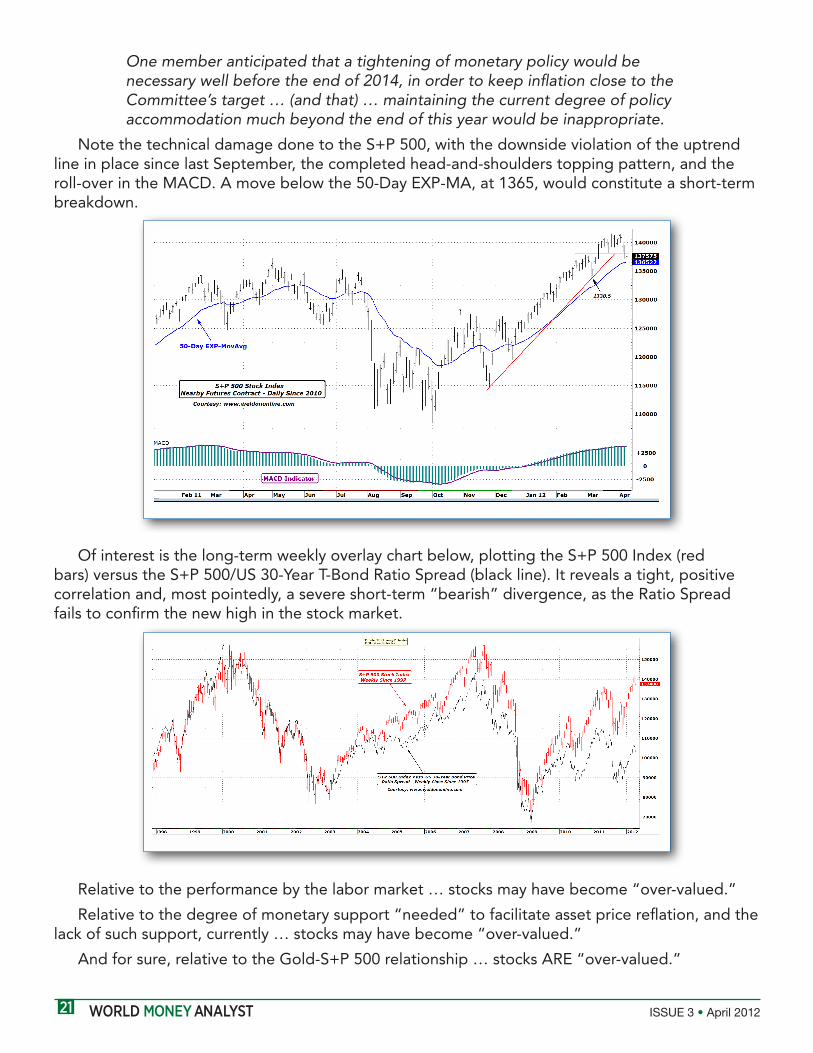

Note the technical damage done to the S+P 500, with the downside violation of the uptrend line in place since last September, the completed head-and-shoulders topping pattern, and the roll-over in the MACD. A move below the 50-Day EXP-MA, at 1365, would constitute a short-term breakdown.

Of interest is the long-term weekly overlay chart below, plotting the S+P 500 Index (red bars) versus the S+P 500/US 30-Year T-Bond Ratio Spread (black line). It reveals a tight, positive correlation and, most pointedly, a severe short-term “bearish” divergence, as the Ratio Spread fails to confirm the new high in the stock market.

Relative to the performance by the labor market … stocks may have become “over-valued.”

Relative to the degree of monetary support “needed” to facilitate asset price reflation, and the lack of such support, currently … stocks may have become “over-valued.”

And for sure, relative to the Gold-S+P 500 relationship … stocks ARE “over-valued.”

WORLD MONEY ANALYST ISSUE 3 • April 201222

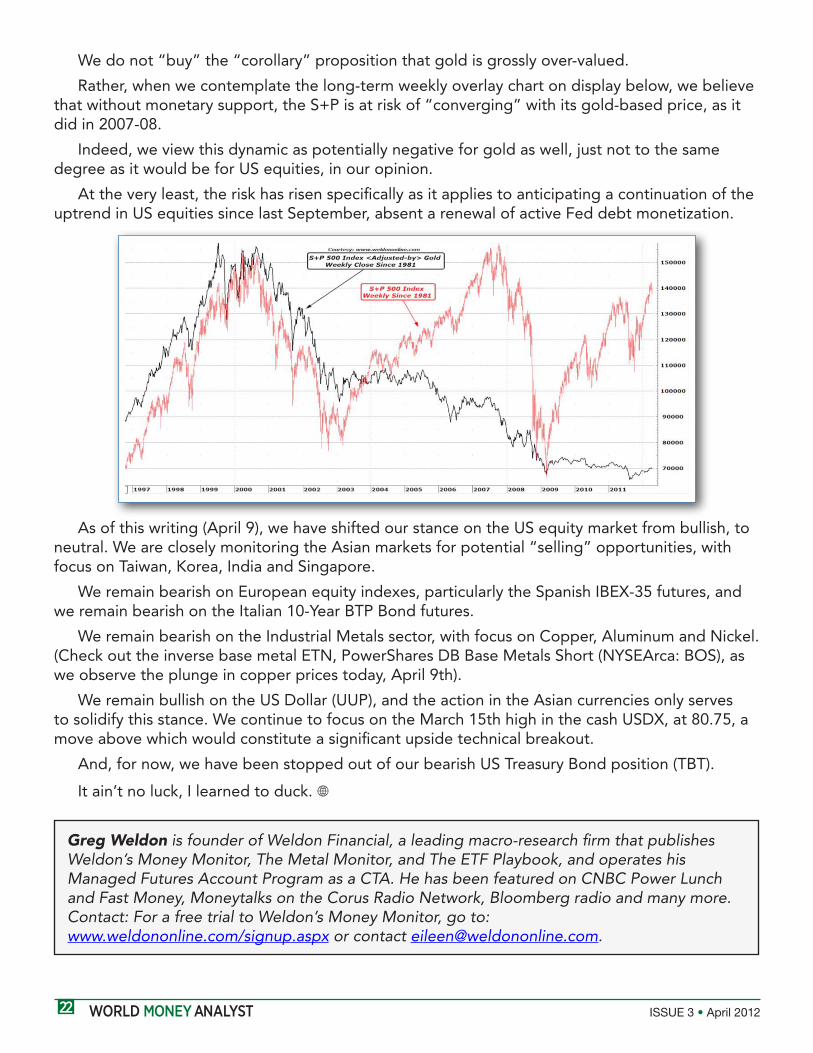

We do not “buy” the “corollary” proposition that gold is grossly over-valued.

Rather, when we contemplate the long-term weekly overlay chart on display below, we believe that without monetary support, the S+P is at risk of “converging” with its gold-based price, as it did in 2007-08.

Indeed, we view this dynamic as potentially negative for gold as well, just not to the same degree as it would be for US equities, in our opinion.

At the very least, the risk has risen specifically as it applies to anticipating a continuation of the uptrend in US equities since last September, absent a renewal of active Fed debt monetization.

As of this writing (April 9), we have shifted our stance on the US equity market from bullish, to neutral. We are closely monitoring the Asian markets for potential “selling” opportunities, with focus on Taiwan, Korea, India and Singapore.

We remain bearish on European equity indexes, particularly the Spanish IBEX-35 futures, and we remain bearish on the Italian 10-Year BTP Bond futures.

We remain bearish on the Industrial Metals sector, with focus on Copper, Aluminum and Nickel. (Check out the inverse base metal ETN, PowerShares DB Base Metals Short (NYSEArca: BOS), as we observe the plunge in copper prices today, April 9th).

We remain bullish on the US Dollar (UUP), and the action in the Asian currencies only serves to solidify this stance. We continue to focus on the March 15th high in the cash USDX, at 80.75, a move above which would constitute a significant upside technical breakout.

And, for now, we have been stopped out of our bearish US Treasury Bond position (TBT).

It ain’t no luck, I learned to duck. •

Greg Weldon is founder of Weldon Financial, a leading macro-research firm that publishes Weldon’s Money Monitor, The Metal Monitor, and The ETF Playbook, and operates his Managed Futures Account Program as a CTA. He has been featured on CNBC Power Lunch and Fast Money, Moneytalks on the Corus Radio Network, Bloomberg radio and many more. Contact: For a free trial to Weldon’s Money Monitor, go to: www.weldononline.com/signup.aspx or contact [email protected].

WORLD MONEY ANALYST ISSUE 3 • April 201223

The Eurozone debt crisis is back in the headlines, and this should be no surprise. But it has unnerved investors. Euroland stocks rose for the first three months of the year and then reversed; half the country indices are now in negative territory for the year.

And investors are unlikely to be calmed over the next few months. Many upcoming events—the “unknown knowns,” to paraphrase Donald Rumsfeld—have the ability to keep Europe on the front pages, shatter investor confidence, and push stocks down even further. These known events whose outcomes are unknown include both the political and financial realms.

More icebergs ahead

France has an election next week that, in all likelihood, will lead to a runoff on May 6th. (No candidate in modern France has won the first round.) In a run off, it is likely that the socialist opposition candidate François Hollande would win. He advocates an even easier monetary policy, but more importantly, wants to renegotiate the Euro fiscal pact.

Next month also sees Greeks go to the polls—the actual date has not yet been set—with the leading opposition parties already pledging to renegotiate the terms of the last bailout. If both oppositions win, there could be quite some negotiations, not to mention more grey hairs, for German Chancellor Angela Merkel.

Meanwhile, there are further long-term bond sales scheduled for Spain and Italy, which, if the latest Spanish offering is any guide, may not go so well. Foreign investors have abandoned these markets, meaning less demand.

Much of the demand for peripheral debt offerings comes from the countries’ banks, but this points up the circular nature of the relationship among banks, countries and the European Central Bank. Undercapitalized banks are buying bonds of over-indebted countries, but only because the governments themselves are all but guaranteeing the banks’ debt holdings and the ECB is essentially giving them the money with which to buy the bonds.

Economies weak

So while over the next few months are several potentially negative events, the opposite results would scarcely mean the debt crises were over. Further out, the incessant drumbeat of potential problems remains: next year Portugal has to roll-over long-term debt which, in relation to its GDP, is far larger than the Italian or Spanish offering this year.

And the austerity measures imposed on Greece ensure a slowing economy, making the odds of the second bailout lasting even until the scheduled 2014 less likely.

Europe: Here We Go AgainEurope

By Adrian Day

WORLD MONEY ANALYST ISSUE 3 • April 201224

The ongoing debt crisis has had an effect on Europe’s economy. Not surprisingly, the austerity measures in Greece and Spain have reduced forecasts for GDP growth. Spain, the Eurozone’s fourth-largest economy, has targeted a budget deficit of 5.8% for this year—down from 9%—with inevitable consequences on the already high unemployment rate of 23%.

Even for Holland, one of the stronger members of “core” Europe, indicators are turning negative, while Germany’s growth is weak, with industrial production down. It should be noted, however, that sentiment among Germany’s business leaders remains positive, and many of the leading indicators are positive as well.

But Germany alone cannot be the train that pulls the rest of Europe, and the burden will either see its economy slow or see political pressure to let go of the worst of the peripheral countries.

That means that Europe is increasingly relying on help from a rather weak U.S. recovery and a less powerful China.

Why buy Europe?

In truth, the outlook for Europe is not particularly positive. Yet the negatives are well known, and hardly different from what they were at the beginning of the year. Surely, to a large extent, they are discounted in the market. But the less appreciated conditions for stronger stocks that we posited earlier remain:

• Stocks are inexpensive. Indeed, with half the markets in Europe now down on the year, prices are even lower, though not for all of our stocks. This is also true of the continent’s largest companies—those in the EuroStoxx 50—down slightly year to date.

• Monetary policy remains easy. The ECB has become even easier in response to Spain’s heightened crisis (many spokesmen have hinted at new programs) while a Hollande victory in France would also add pressure for new stimulus measures. The market has reacted positively to easy money; for example, in mid-April comments from an ECB director suggesting renewed use of the Securities Market Program.

• Investors are underweight, as true for institutions as for retail investors. Large pension funds in Europe, as in the U.S., responded to the 2008 crisis by dramatically cutting equity allocations in their portfolios. This is a positive contrary indicator.

Warren Buffet agrees. At the end of February—with prices appreciably higher than they are today—he invested $1.9 billion into eight (unnamed) European stocks.

We would (for the most part) hold on to inexpensive European stocks, though being more cautious in Spain and Italy. We had thought that the rally that began early in the year would have run a little further without the serious correction that started in March.

However, we see any market setbacks in the coming months as a chance to add to positions for the long term.

WORLD MONEY ANALYST ISSUE 3 • April 201225

Positions review

Brisa (Lisbon: BRI) had recent news. We still like the company, but unfortunately major holders, in making an offer for the company, have taken it out of our hands, offering €2.66 for shares they do not own. Given the improbability of a competing offer, we want to exit our position, even though the offer price still undervalues the company.

The stock hit—and then moved above—the offer price before a modest pull back this week to €2.60. We suggest using a sell limit of €2.64, which would give us a gain of just over 14%.

We would be buying the major markets, including Germany and France. Germany remains inexpensive at a forward P/E of 10 and a yield over 4%. France is even cheaper, with a P/E of 9 and a yield above 5%. You can buy both markets using the ETFs shown in my article in the February issue. We would look for market pullbacks to buy.

Telefonica (NYSE: TEF), the Spanish phone company whose largest unit is in Latin America, is very inexpensive, with a P/E under 10 and a yield approaching 10%.

Italmobiliare (Borsa Italiana: ITM), the Italian conglomerate, is selling at less than one quarter of its book value, which is half of its peer group and half its own recent historical valuations, giving us a wide margin. Given the renewed concerns regarding Spain and Italy, we would hold off buying for now.

Our “peripheral” positions in two undervalued holdings companies remain strong buys for the patient long-term investor. Switzerland’s Pargesa Holding (SIX: PARG), trades at a discount to the public value of its holdings while yielding over 4%. Investor A/B (Stockholm: INVEA), also trades at a discount to its Scandinavian assets, and likewise yields over 4%.

Buying while “blood is in the streets” does not guarantee instant gratification, but does offer the opportunity to buy quality assets at extraordinary valuations. Price earnings under 10 … double-digit yields … and discounts to NAV of up to 35% seem to qualify. •

Adrian Day is a British-born money manager and pioneer in promoting the benefits of global investing with two books on the subject: the ground-breaking Investing Without Borders and his latest Investing in Resources: How to gain the Outsized Potential and Avoid the Risks. A graduate of the London School of Economics, he is a frequent speaker at investment seminars, and has been interviewed by numerous world media, including CNBC, BBC, Bloomberg, Wall Street Journal radio, The Cape Town Argus, La Vie Francais, and The Straits Times. www.AdrianDayAssetmanagement.com

WORLD MONEY ANALYST ISSUE 3 • April 201226

I ’m a fundamentalist. I look for strong fundamentals (or lack thereof) to drive a trend and remain the underlying trend until the fundamental reason has vanished or been corrected. A trend is not a one-way street. There can be periods of volatility that will test one’s resolve in maintaining

positions that go along with the trend.

But, my friends, the underlying trend will always be there until, like I said, the fundamental reason has changed, good or bad.

Have you ever used a set of criteria for valuing a stock? Well, apply that method to valuing a currency, and just consider the currency to be the “stock of that country.” I use the following criteria when valuing a currency:

1) Balance sheet (surplus or deficit country)

2) Have things to sell that other countries want (commodities, raw materials, hoola hoops, etc.)

3) Strong leadership (I use a country’s Central Bank here. Are they prudent in providing price stability (no inflation), or are they more interested in providing growth?)

4) Attractive to buyers, and

5) Not currently overbought.

When you apply this set of criteria to all the world’s currencies, only a handful would meet or pass this test. This month, I’m going to focus on the country with the absolute best set of fundamentals in the world.

Many would argue that Norway is too small of a country to qualify as having the best fundamentals, but I simply don’t care. We’re talking about currencies and each country’s respective fundamentals, not what countries are the largest in the world!

So, I already spilled the beans … and mentioned Norway. I’ve long been a fan of Norway and their fundamentals. In 2009, Time Magazine dubbed the Norwegian krone the “World’s Safest Currency.”

Now, to be clear, the krone can lose value against the dollar, just like any other currency, when the dollar is in demand. But since the fundamental weak dollar trend began in February of 2002, the krone has gained much more against the dollar than it has lost during periods of weakness.

Remember, it’s a two-way street.

When holding currencies to diversify your dollar-denominated investment portfolio, you’ll need patience. Look for long sweeping moves of the currencies you own. Sometimes it will seem as though there is no direction, very much like today’s trading environment, but eventually the focus returns to the U.S. debt situation, and the currencies begin to move higher once again.

How to Value a CurrencyCurrency Watch

By Chuck Butler

WORLD MONEY ANALYST ISSUE 3 • April 201227

Can this go on forever? Well, I guess technically speaking it could … but probably won’t! Until the U.S. gets on the road to correcting its debt problem, the dollar will tread water in hopes of not getting pulled under for good.

Scrutinize currencies like you would stocks

So, let’s apply our criteria to Norway, starting with the balance sheet. Well, we’re talking about a country with the best financial fundamentals in the world. Yes, they use their oil revenues, but many countries have oil revenues but lack the financial surplus that Norway has. This leads us to their Central Bank and government, both of which have long acted very prudently concerning price stability.

Norway experienced a banking crisis in the 90s that they worked through (very differently than the US response to its crisis, I might add) and now have one of the world’s strongest banking sectors.

Returning to Norway’s balance sheet, it’s important to note that its fiscal position is so strong that every Norwegian has a fully funded pension. And, a few years ago, the Norwegian government began to fully fund the pension plans of Norwegians yet to be born!

Rather than spend money willy-nilly on fly-by-night ideas, Norway instead chose to improve its infrastructure and quality of life.

Factor in a greater than US$350 billion sovereign wealth fund to the government’s surplus position, and the country is the cheapest of the world’s ten most-traded currencies to insure against default.

Carrying on, we know that Norway has “something that other countries want” with their oil reserves. In fact, Norway just recently made a second big discovery in the Barents Sea in less than a year, and predicted more to come!

Norway is the world’s 8th largest oil exporter, and the new discovery should keep them at that position (or even higher), should the Barents Sea discovery yield what the Norwegian oil firm Statoil believes it will yield.

The krone is not the euro

And lastly, attractiveness of the currency. Currently, here’s where the krone gets tarred with the same brush as the euro, even though Norway is not part of the euro, maintains its own currency sovereignty, and has a completely different set of fundamentals.

But that’s the markets, and at this point, Norway is not in a position to replace the Swiss franc or Japanese yen as safe havens for all. They have neither a bond market nor an economy that compares to either.

However, I contend that this is beginning to change, and once the markets get it through their thick skulls that Norway is not the euro – that its surplus balance sheet stands above the Eurozone, which is drowning in a pool of debts – that Norway will be the replacement destination

WORLD MONEY ANALYST ISSUE 3 • April 201228

for currency investors.

I also believe that Switzerland will continue to intervene and prevent the franc from strengthening. The Japanese will do likewise with the yen. Recall that investors were badly burned back in September when the Swiss devalued the franc about 10% in one sweeping move, intending to put a floor under the exchange rate with the euro.

In fact, there’s talk among Swiss leaders about taking the euro/franc cross to 1.35 or 1.40. (The current floor is 1.20.) Losing that much ground against the euro would be very bad for franc holders, because the move will play through on the currency crosses against the dollar, and the dollar/franc holders will get burned again.

Norway’s Central Bank (The Riksbank) has expressed a concern that the krone is too strong against the euro. But unless it’s willing to throw all the good capital its earned in the markets out the window and duplicate what the Swiss National Bank did back in September, the Riksbank’s must learn to live with a currency that everyone wants!

So, while the krone might be considered a “not-ready-for-prime-time-player,” it’s still, in my mind, the safe haven of Europe, with the best fundamentals.

China Takes Another Step…(An Update)

Last month I talked to you about the steps that China was taking to replace the dollar standard. Well, this month, the Chinese announced another step toward that goal.

It seems the Chinese Central bank is putting together a global payment system for cross-border transactions in renminbi, aiming to expand the currency’s use in international trade, and to reduce the reliance on the U.S. dollar.

This means that banks worldwide would be free to use the China International payment system.

Just another step, folks… just another step. •

Chuck Butler is President of EverBank World Markets. Everbank is an FDIC insured US-based bank specializing in WorldCurrency® Certificates of Deposit and deposit accounts denominated in select global currencies. Contact: www.EverBank.com.

WORLD MONEY ANALYST ISSUE 3 • April 201229

The planet’s largest importer of nearly every commodity has made miners and drillers around the world rich in recent years. But can today’s prices survive the Chinese slowdown?

On Friday, Beijing’s National Bureau of Statistics announced that the Chinese economy grew 8.1% last quarter, down from 8.9% in the previous period. But as disappointing as the Q1 number was, it looks like it overstates growth, not correlating with the weight of information for the last three months. China is growing, but only about 5% to 6%.

In any event, a slowing economy means that China’s commodity purchases will eventually decline to match lowered industrial demand, and, in fact, March commodity imports slowed. Oil imports fell to 5.55 million barrels per day last month, tumbling 5.8% from February. Copper was off 4.6%, and iron ore shipments down 3.2%. The declines are significant in view of the historical pattern of the Chinese economy picking up in March as it emerges from the Lunar New Year holiday period.

And were it not for stockpiling, the results would have been much worse. As Andrew Driscoll at CLSA Asia-Pacific notes, “The import numbers for most commodities are stronger than expected, which is a little surprising because anecdotal evidence tells us that actual demand continues to be pretty weak.”

So if you sell oil, you must be cheering Beijing’s efforts to build its strategic petroleum reserve. The reserve looks like it is only a sixth of its eventual size of about 700 million barrels, and this means Beijing will be a buyer for a long time to come.

And Beijing is accumulating commodities other than oil. Think copper. China, from all indications, is hoarding the metal. In the last quarter of 2012, about 300,000 tons were added to its already impressive stockpile, and its purchases in the beginning of this year appear to be in excess of anticipated need.

“It is clear that the Chinese were simply stocking up on copper, expecting a seasonal pickup—perhaps towards the end of the second quarter or the second half of this year,” said Andrey Kryuchenkov of VTB Capital to Reuters. Estimates for growth in refined copper consumption this year are generally in the 6.0-6.6% range.

There are many explanations why Chinese enterprises are buying copper like there’s no tomorrow. Some, for instance, maintain Beijing believes there will be shortages of the metal, while others think the Chinese are just taking advantage of price declines.

Then, there are those who argue that central bank officials are replacing holdings of U.S. government paper with hard assets.

China’s Stockpiling Delays Fall in Commodity Prices By Gordon G. Chang

China Watch

WORLD MONEY ANALYST ISSUE 3 • April 201230

And China’s leaders may be trying to decrease politically sensitive trade surpluses by increasing imports, and the way to do that without buying manufactured goods is to acquire commodities.

Stockpiling triggers ramp up in productionChina’s purchase of commodities, in large measure, is driven by considerations divorced from

market factors, and this in turn drives the plans of the world’s commodity producers. Take iron ore miners, for example.

Despite gloomy forecasts for China’s steel sector—mills are diversifying into pig farming as demand for their primary product cools—global iron ore giants are planning to increase capacity for Chinese customers.

BHP Billiton, for instance, said it was going forward with big projects to expand production. Rio Tinto, another Anglo-Australian giant, plans to increase output more than 50% next year by opening mines. Brazil’s Vale, the world’s largest iron ore miner, and Fortescue Metals, the Australian company, are also upping production.

China accounts for about 60% of global trade in iron ore, and, not surprisingly, the country’s prospects underpin every expansion plan of the world’s top mining companies. The story is much the same across commodity sectors. The consensus is that the short-term outlook will remain strong.

At least for the next several months, the majority view appears sound. Chinese enterprises usually replenish their stores of commodities in the early months of a year, and the central government looks like it is continuing to build up its stocks.

Despite China’s unusual—non-market driven—buying of commodities, some analysts are worried. The concern is that, should the downturn ultimately prove worse than expected, Chinese enterprises will cut back on purchases or even unload excess inventory on global markets.

As the Basic Materials team of Credit Suisse noted in a March 19 report, China “made the commodity cycle a lot more powerful on the way up and now can work the other way.”

That’s a warning to heed. Once the recent round of restocking ends, look for China’s commodity imports to dive. And world prices with them. •

Gordon G. Chang is the author of Nuclear Showdown: North Korea Takes On the World, and The Coming Collapse of China. He is a columnist at Forbes.com and The Daily whose writings have also appeared in The New York Times, Wall Street Journal, Far Eastern Economic Review, International Herald Tribune, Commentary, The Weekly Standard, National Review, and Barron’s. More information: www.gordonchang.com. Follow him on Twitter @GordonGChang.

WORLD MONEY ANALYST ISSUE 3 • April 201231

WMA Recap - April 2012

• The fourth largest oil company in Russia, Surgutneftegas (LSE: SGGD; ADR) is a conservatively managed company with US$29 billion in cash, no debt, and selling at a P/E of 4. Page 6.

• Deep structural faults in the EU political union continue to plague the common currency. The Eurozone’s unresolved solvency issues means selling pressure on the euro will continue. Consider this “bear put spread” strategy for an inexpensive way to profit from the euro’s decline. Page 9.

• These 7 international brokers give international readers a choice of trading options and a great way to diversify your investments across multiple jurisdictions, including: Panama, Denmark, Luxembourg, Switzerland, Singapore, and Hong Kong. Page 12.

• With many global economies slowing, the outlook for industrial metals is bearish. Consider the PowerShares DB Base Metals Short ETN (NYSEArca: BOS) to profit from the fall in prices. Page 17.

• The re-emergence of fiscal troubles in the Eurozone’s periphery sends European markets lower. Caution is advised in the Spanish and Italian markets. Our Swiss and Scandinavian picks remain good buys. Page 23.

The Mauldin Economics web site, Yield Shark, Thoughts From the Front Line, Outside the Box, Over My Shoulder, Conversations and World Money Analyst are published by Mauldin Economics, LLC. Information contained in such publications is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The information contained in such publications is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. The information in such publications may become outdated and there is no obligation to update any such information.

John Mauldin, Mauldin Economics, LLC and other entities in which he has an interest, employees, officers, family, contributors and associates may from time to time have positions in the securities or commodities covered in these publications or web site. Corporate policies are in effect that attempt to avoid potential conflicts of interest and resolve conflicts of interest that do arise in a timely fashion.

Any Mauldin Economics, LLC publication or web site and its content and images, as well as all copyright, trademark and other rights therein, are owned by Mauldin Economics, LLC. No portion of any Mauldin Economics, LLC publication or web site may be extracted or reproduced without permission of Mauldin Economics, LLC. Nothing contained herein shall be construed as conferring any license or right under any copyright, trademark or other right of Mauldin Economics, LLC. Unauthorized use, reproduction or rebroadcast of any content of any Mauldin Economics, LLC publication or web site, including communicating investment recommendations in such publication or web site to non-subscribers in any manner, is prohibited and shall be considered an infringement and/or misappropriation of the proprietary rights of Mauldin Economics, LLC.