World Energy Outlook 2010 · World Energy Outlook 2010 ... 1990 1995 2000 2005 2010 2015 2020 2025...

35

© OECD/IEA 2010 World Energy Outlook 2010 Nobuo Tanaka Executive Director International Energy Agency Beijing, 17 November 2010

Transcript of World Energy Outlook 2010 · World Energy Outlook 2010 ... 1990 1995 2000 2005 2010 2015 2020 2025...

© OECD/IEA 2010

World Energy Outlook 2010

Nobuo TanakaExecutive DirectorInternational Energy Agency

Beijing, 17 November 2010

© OECD/IEA 2010

The context: A time of unprecedented uncertainty

The worst of the global economic crisis appears to be over – but is the recovery sustainable?

Oil demand & supply are becoming less sensitive to price – what does this mean for future price movements ?

Natural gas markets are in the midst of a revolution – will it herald a golden era for gas?

Copenhagen Accord & G-20 subsidy reforms are key advances –but do they go far enough & will they be fully implemented ?

Emerging economies will shape the global energy future –where will their policy decisions lead us ?

© OECD/IEA 2010

Overview of WEO-2010 scenarios

New Policies Scenario is the central scenario in WEO-2010

> assumes cautious implementation of recently announced commitments & plans, even if yet to be formally adopted

> provides benchmark to assess achievements & limitations of recent developments in climate & energy policy

Current Policies Scenario takes into consideration only those policies that had been formally adopted by mid-2010

> equivalent to the Reference Scenario of past Outlooks

The 450 Scenario sets out an energy pathway consistent with the goal of limiting increase in average temperature to 2OC

© OECD/IEA 2010

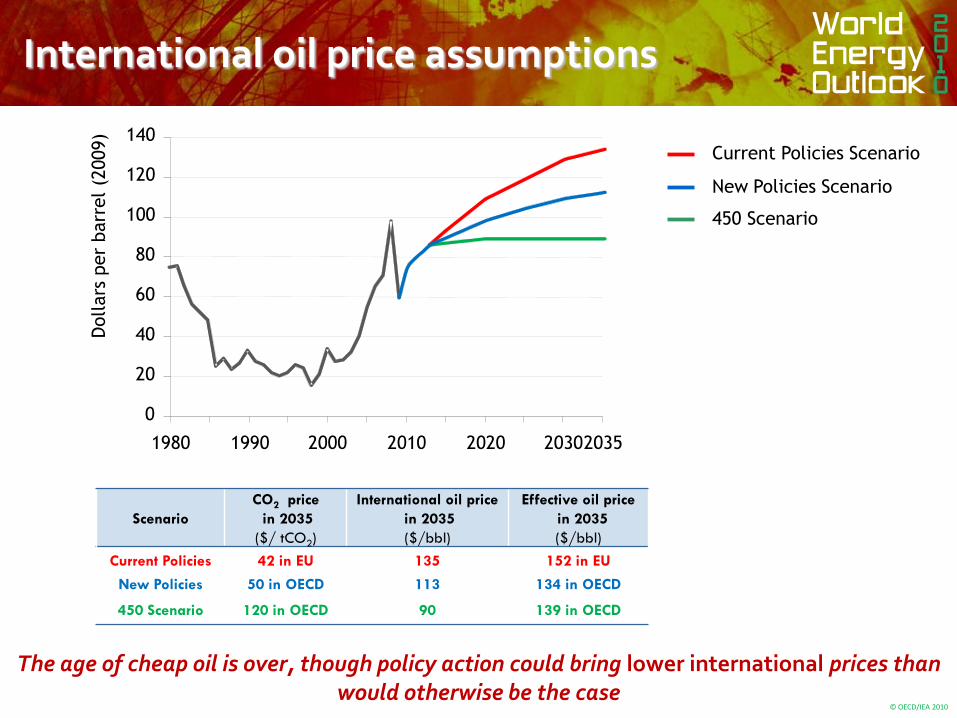

International oil price assumptions

The age of cheap oil is over, though policy action could bring lower international prices than would otherwise be the case

Scenario

CO2 price

in 2035

($/ tCO2)

International oil price

in 2035

($/bbl)

Effective oil price

in 2035

($/bbl)

Current Policies 42 in EU 135 152 in EU

New Policies 50 in OECD 113 134 in OECD

450 Scenario 120 in OECD 90 139 in OECD

0

20

40

60

80

100

120

140

1980 1990 2000 2010 2020 20302035

Dollars

per

barr

el

(2009)

Current Policies Scenario

New Policies Scenario

450 Scenario

© OECD/IEA 2010

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

Mto

e

1980 1990 2000 2010 2020 2030 2035

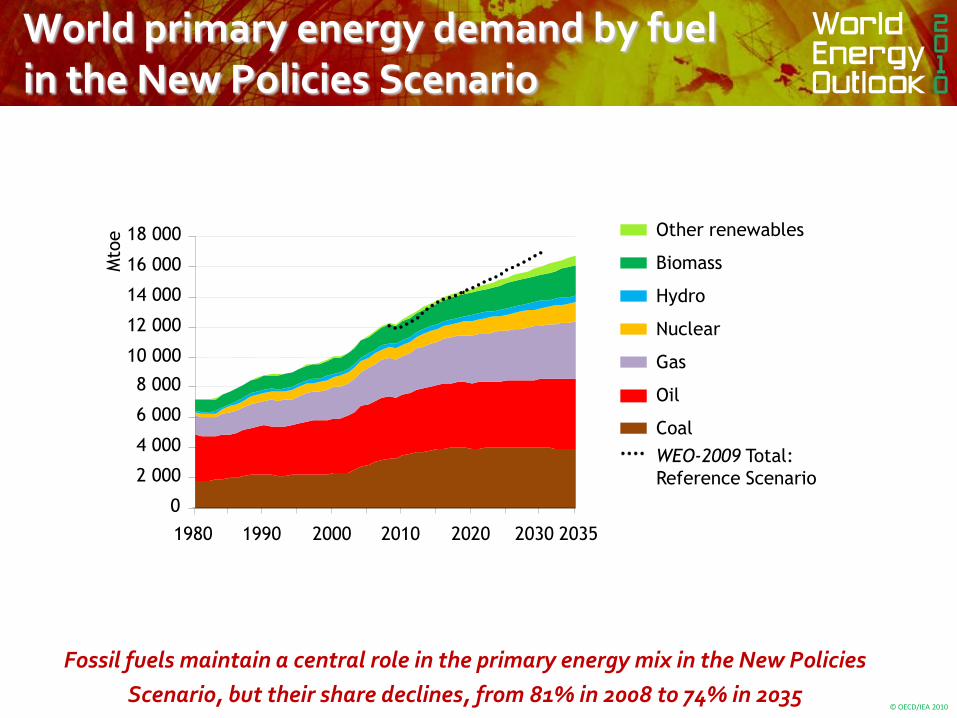

World primary energy demand by fuelin the New Policies Scenario

Fossil fuels maintain a central role in the primary energy mix in the New Policies

Scenario, but their share declines, from 81% in 2008 to 74% in 2035

Other renewables

Biomass

Hydro

Nuclear

Gas

Oil

Coal

WEO-2009 Total:

Reference Scenario

© OECD/IEA 2010

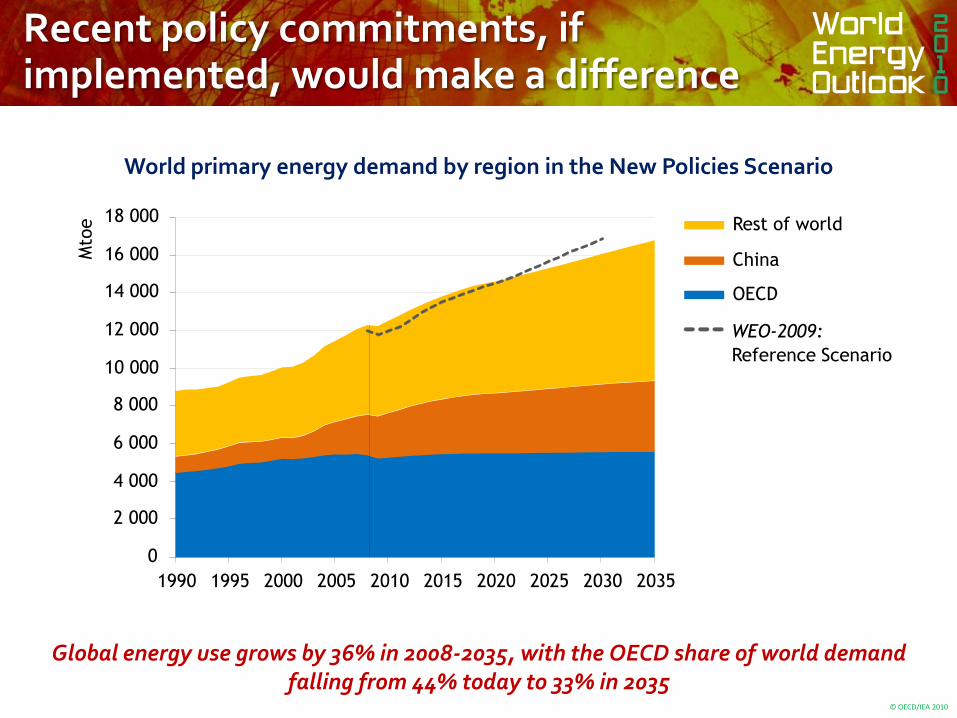

Recent policy commitments, if implemented, would make a difference

Global energy use grows by 36% in 2008-2035, with the OECD share of world demand falling from 44% today to 33% in 2035

World primary energy demand by region in the New Policies Scenario

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

16 000

18 000

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

Mto

e Rest of world

China

OECD

WEO-2009:

Reference Scenario

© OECD/IEA 2010

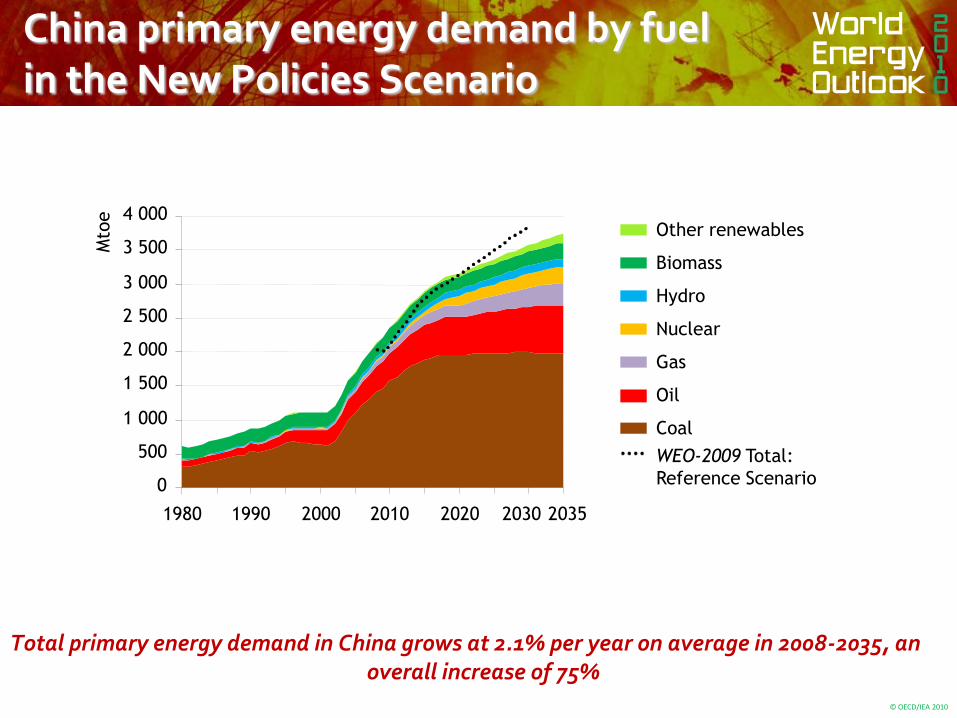

Other renewables

Biomass

Hydro

Nuclear

Gas

Oil

Coal

WEO-2009 Total:

Reference Scenario0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

1980 1990 2000 2010 2020 2030

Mto

e

2035

China primary energy demand by fuel in the New Policies Scenario

Total primary energy demand in China grows at 2.1% per year on average in 2008-2035, an overall increase of 75%

© OECD/IEA 2010

Emerging economies dominate the growth in demand for all fuels

Demand for all types of energy increases in non-OECD countries, while demand for coal & oil declines in the OECD

Incremental primary energy demand in the New Policies Scenario, 2008-2035

- 600 - 300 0 300 600 900 1 200 1 500

Other renewables

Hydro

Nuclear

Gas

Oil

Coal

Mtoe

OECD

China

Rest of world

© OECD/IEA 2010

Fossil-fuel subsidies are distorting price signals

Fossil-fuel consumption subsidies amounted to $312 billion in 2009, down from $558 billion in 2008, with the bulk of the fall due to lower international prices

Economic value of fossil-fuel consumption subsidies by country, 2009

Turk

menis

tan

Electricity(generated from

fossil fuels)

Gas

Oil

Coal

Additional

subsidy in 2008

Iran

Saudi Ara

bia

Russ

ia

India

Chin

a

Egypt

Venezuela

Indonesi

a

UAE

Uzbekis

tan

Iraq

Kuw

ait

Pakis

tan

Arg

enti

na

Ukra

ine

Alg

eri

a

Mala

ysi

a

Thailand

Bangla

desh

Mexic

o

South

Afr

ica

Qata

r

Kazakhst

an

Lib

ya

0

Billion d

ollars

20

40

60

80

100

© OECD/IEA 2010

Booming demand for mobility in the emerging economies drives up oil use

The global car fleet will continue to surge as more & more people in China & other emerging economies buy a car, overshadowing modest growth in the OECD

0

200

400

600

800

1 000

1 200

1 400

1 600

1980 1990 2000 2008 2020 2035

Million China

Other non-OECD

United States

Other OECD

Passenger vehicles in the New Policies Scenario

© OECD/IEA 2010

0

20

40

60

80

100

1990 1995 2000 2005 2010 2015 2020 2025 2030 2035

mb/d

Crude oil:

fields yet to be developed

Crude oil:

currently producing fields

Total crude oil

Oil production becomes less crude

Global oil production reaches 96 mb/d in 2035 on the back of rising output of natural gas liquids & unconventional oil, as crude oil production plateaus

World oil production by type in the New Policies Scenario

Unconventional oil

Natural gas liquids

Crude oil:

fields yet to be found

© OECD/IEA 2010

More oil from fewer producers

Production rises most in Saudi Arabia & Iraq, helping to push OPEC’s market share from 41% today to 52% by 2035, a level last seen prior to the first oil shock of 1973-1974

Incremental oil production by key country in the New Policies Scenario, 2009-2035

0 1 2 3 4 5 6

Algeria

Libya

Nigeria

Qatar

Iran

Kuwait

UAE

Venezuela

Canada

Kazakhstan

Brazil

Iraq

Saudi Arabia

mb/d

OPEC

Non-OPEC

© OECD/IEA 2010

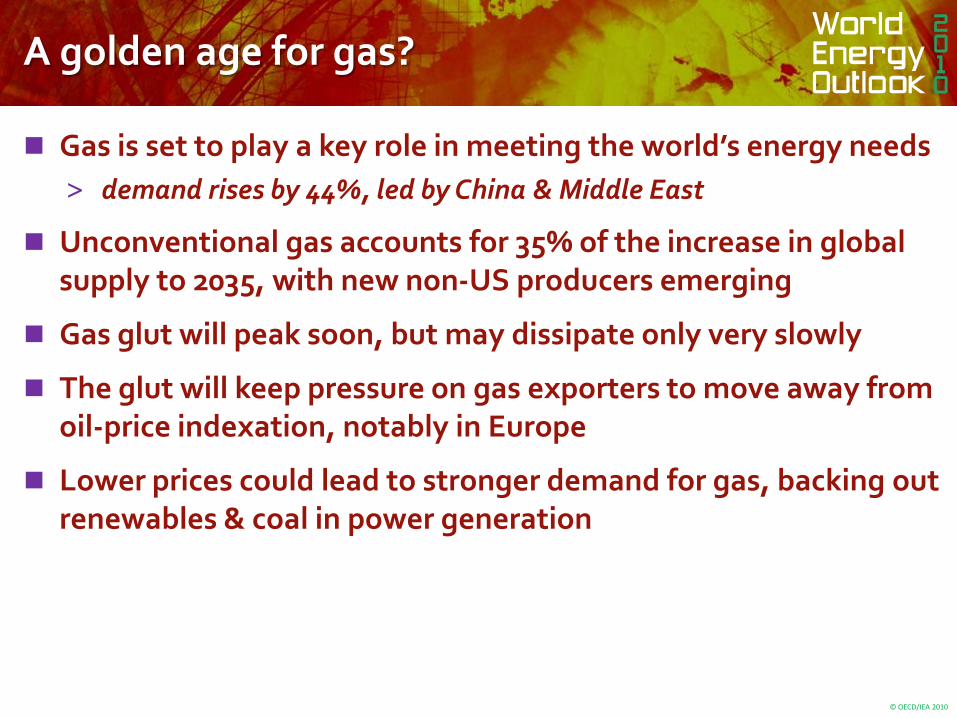

A golden age for gas?

Gas is set to play a key role in meeting the world’s energy needs

> demand rises by 44%, led by China & Middle East

Unconventional gas accounts for 35% of the increase in global supply to 2035, with new non-US producers emerging

Gas glut will peak soon, but may dissipate only very slowly

The glut will keep pressure on gas exporters to move away from oil-price indexation, notably in Europe

Lower prices could lead to stronger demand for gas, backing out renewables & coal in power generation

© OECD/IEA 2010

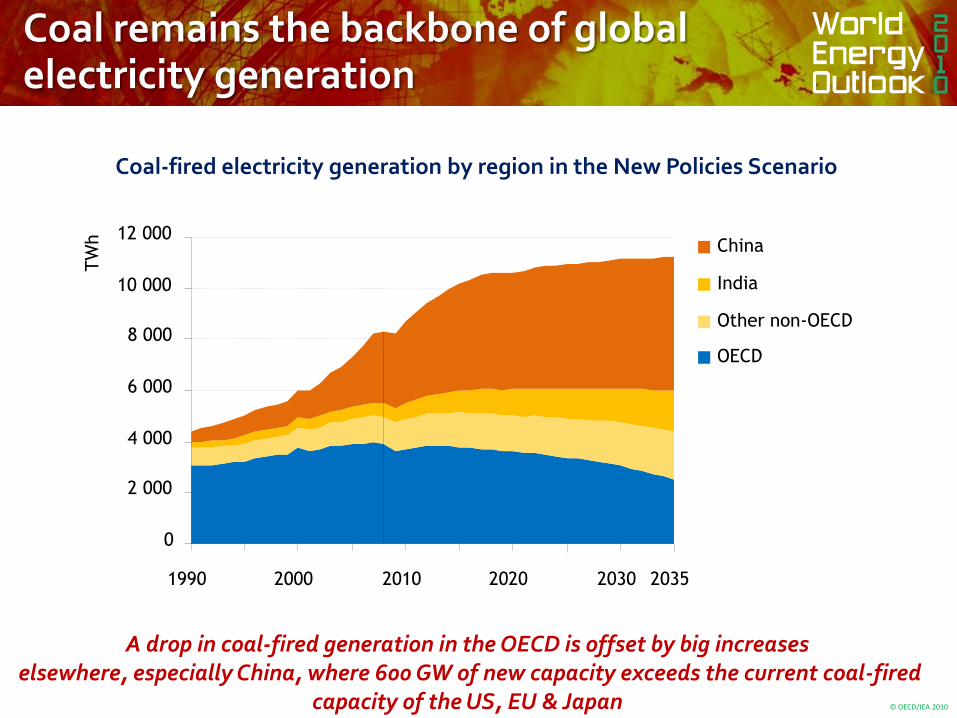

Coal remains the backbone of global electricity generation

A drop in coal-fired generation in the OECD is offset by big increaseselsewhere, especially China, where 600 GW of new capacity exceeds the current coal-fired

capacity of the US, EU & Japan

0

2 000

4 000

6 000

8 000

10 000

12 000

1990 2000 2010 2020 2030 2035

TW

h China

India

Other non-OECD

OECD

Coal-fired electricity generation by region in the New Policies Scenario

© OECD/IEA 2010

Renewables enter the mainstream….

The use of renewable energy triples between 2008 & 2035, driven by the power sector where their share in electricity supply rises from 19% in 2008 to 32% in 2035

Renewable primary energy demand in the New Policies Scenario

0 100 200 300 400 500

European Union

United States

China

Brazil

India

Africa

OECD Pacific

Mtoe

2008

2035

© OECD/IEA 2010

….but only if there is enough government support

Government support remains the key driver – rising from $57 billion in 2009 to $205 billion in 2035 – but higher fossil-fuel prices & declining investment costs also spur growth

Annual global support for renewables in the New Policies Scenario

Billion d

ollars

(2009)

Biofuels

Renewables-based

electricity

0

30

60

90

120

150

180

210

2007 2008 2009 2015 2020 2025 2030 2035

© OECD/IEA 2010

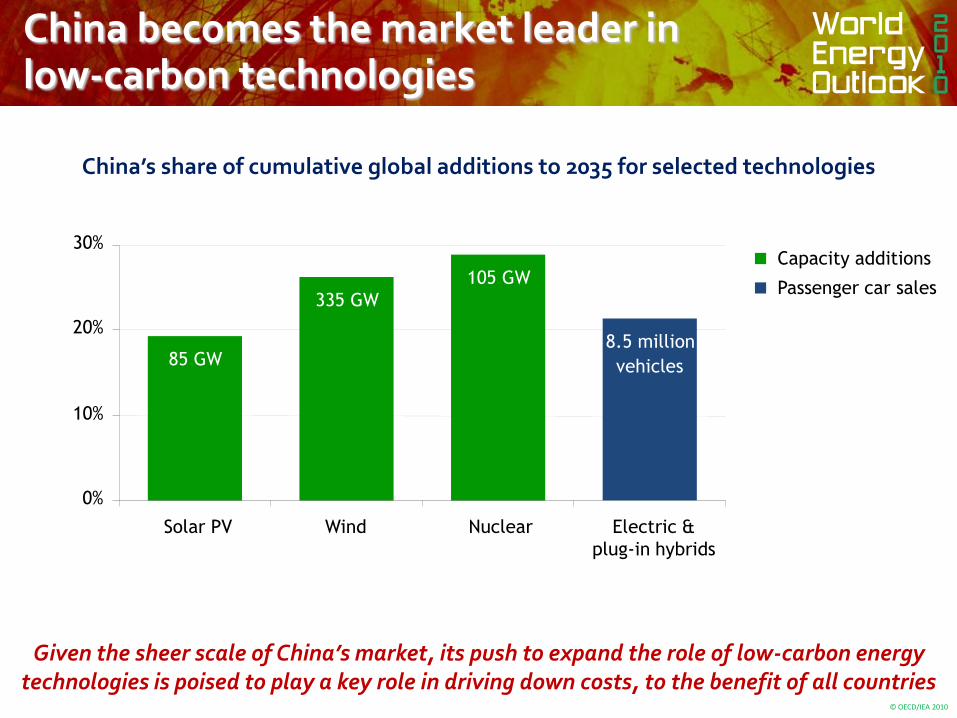

China becomes the market leader inlow-carbon technologies

Passenger car sales

Capacity additions

China’s share of cumulative global additions to 2035 for selected technologies

Given the sheer scale of China’s market, its push to expand the role of low-carbon energy technologies is poised to play a key role in driving down costs, to the benefit of all countries

85 GW

335 GW

105 GW

0%

10%

20%

30%

Solar PV Wind Nuclear Electric &

plug-in hybrids

8.5 million

vehicles

© OECD/IEA 2010

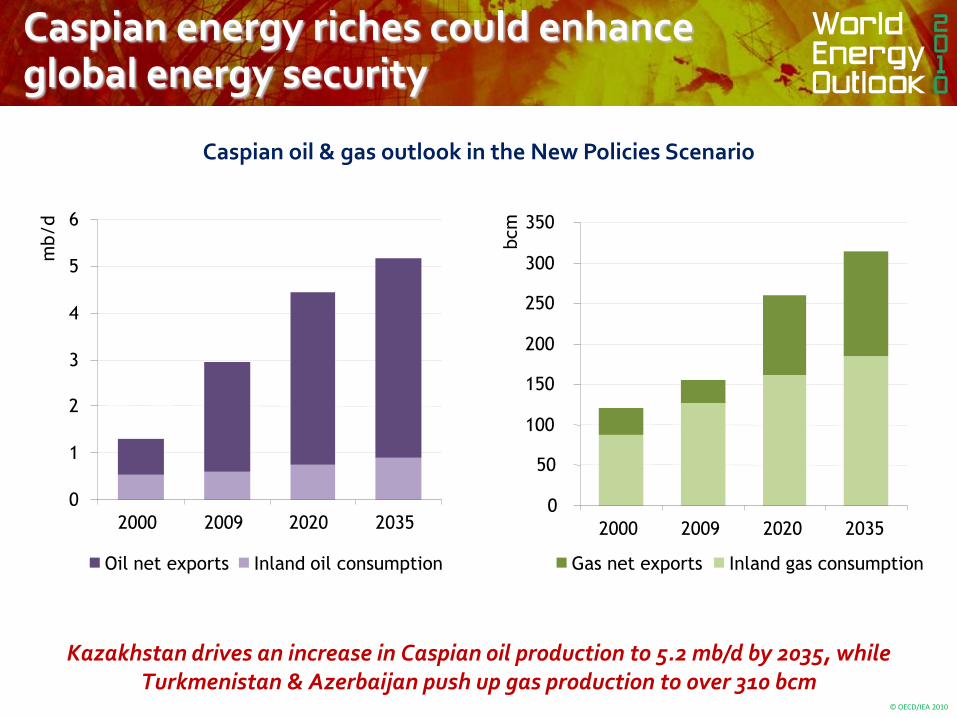

Caspian energy riches could enhance global energy security

Kazakhstan drives an increase in Caspian oil production to 5.2 mb/d by 2035, while Turkmenistan & Azerbaijan push up gas production to over 310 bcm

Caspian oil & gas outlook in the New Policies Scenario

0

1

2

3

4

5

6

2000 2009 2020 2035

mb/d

Oil net exports Inland oil consumption

0

50

100

150

200

250

300

350

2000 2009 2020 2035bcm

Gas net exports Inland gas consumption

© OECD/IEA 2010

Number of people without access to electricity(million)

Today, there are 1.4 billion people lacking access to electricity. Based on current trends, 1.2 billion people – or 15% of the world’s population –

will still lack access in 2030

© OECD/IEA 2010

The 450 Scenario:A roadmap from 3.5C to 2C

The 450 Scenario sets out an energy pathway consistent with limiting the increase in temperature to 2C

Assumes vigorous implementation of Copenhagen Accord pledges to 2020 & much stronger action thereafter

The failure of the Copenhagen Accord pledges:

> As many lack transparency, there is 3.9 Gt of uncertainty over the level of abatement pledged to 2020

> As many lack ambition, the cost of achieving the 2 C goal has increased by $1 trillion in 2010-2030 compared with WEO-2009

© OECD/IEA 2010

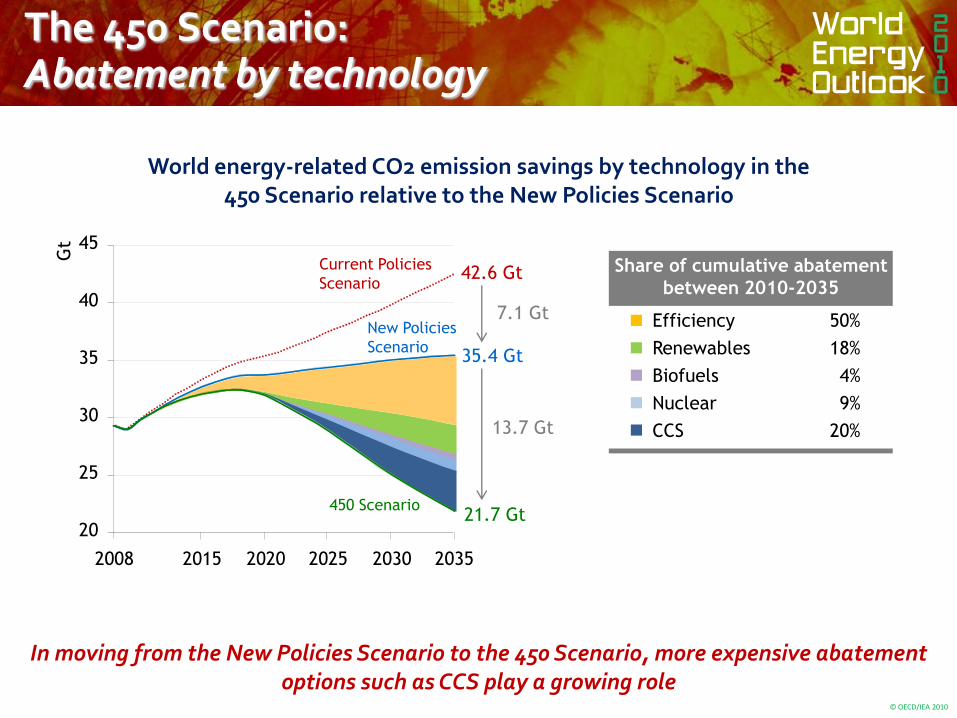

In the 450 Scenario, compared with the Current Policies Scenario, efficiency measures provide 53% of the necessary abatement, but renewables, CCS & nuclear are also crucial

World energy-related CO2 emission savings by technology in the 450 Scenario relative to the Current Policies Scenario

20

25

30

35

40

45

2008 2015 2020 2025 2030 2035

Gt

Efficiency 53%

Renewables 21%

Biofuels 3%

Nuclear 9%

CCS 15%

Share of cumulative abatement

between 2010-203542.6 Gt

21.7 Gt450 Scenario

20.9 Gt

Current Policies

Scenario

The 450 Scenario: Abatement by technology

© OECD/IEA 2010

The 450 Scenario: Abatement by technology

In moving from the New Policies Scenario to the 450 Scenario, more expensive abatement options such as CCS play a growing role

World energy-related CO2 emission savings by technology in the 450 Scenario relative to the New Policies Scenario

20

25

30

35

40

45

2008 2015 2020 2025 2030 2035

Gt

Efficiency 50%

Renewables 18%

Biofuels 4%

Nuclear 9%

CCS 20%

Share of cumulative abatement

between 2010-203542.6 Gt

35.4 Gt

21.7 Gt

Current Policies

Scenario

450 Scenario

New Policies

Scenario

13.7 Gt

7.1 Gt

© OECD/IEA 2010

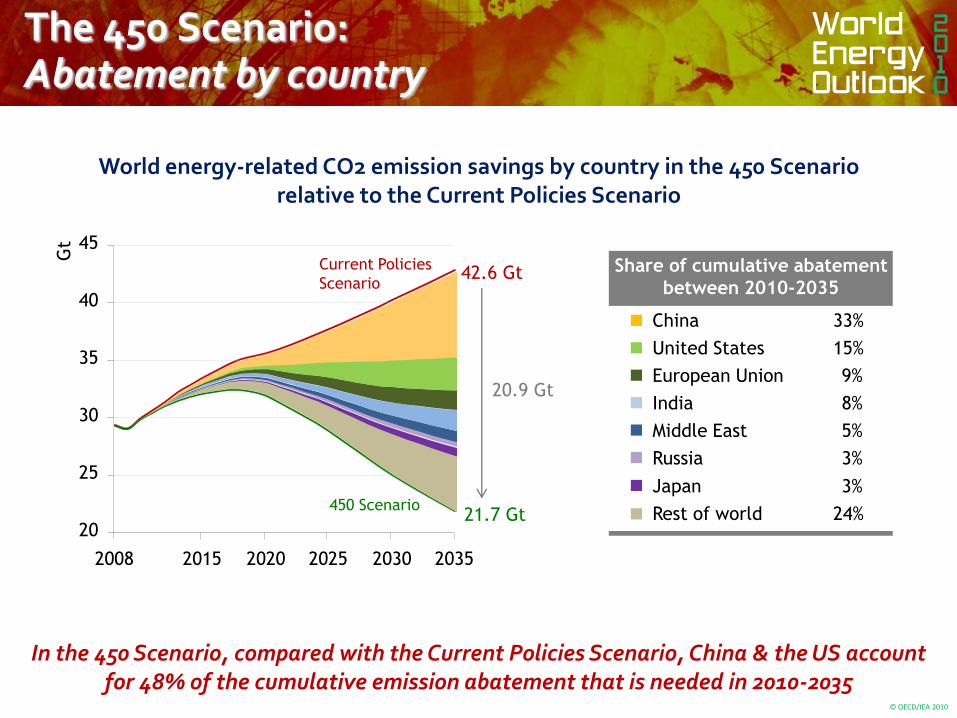

In the 450 Scenario, compared with the Current Policies Scenario, China & the US account for 48% of the cumulative emission abatement that is needed in 2010-2035

World energy-related CO2 emission savings by country in the 450 Scenariorelative to the Current Policies Scenario

20

25

30

35

40

45

2008 2015 2020 2025 2030 2035

Gt

China 33%

United States 15%

European Union 9%

India 8%

Middle East 5%

Russia 3%

Rest of world 24%

Share of cumulative abatement

between 2010-2035

Japan 3%

42.6 Gt

21.7 Gt

Current Policies

Scenario

450 Scenario

20.9 Gt

The 450 Scenario: Abatement by country

© OECD/IEA 2010

Achieving the 2°C goal will require rapid decarbonisation of global energy

Carbon intensity would have to fall at twice the rate of 1990-2008 in the period 2008-2020 & almost four times faster in 2020-2035

Average annual change in CO2 intensity in the 450 scenario

0%

1%

2%

3%

4%

5%

6%

1990-2008 2008-2020 2020-2035

A four-fold

increase needed

© OECD/IEA 2010

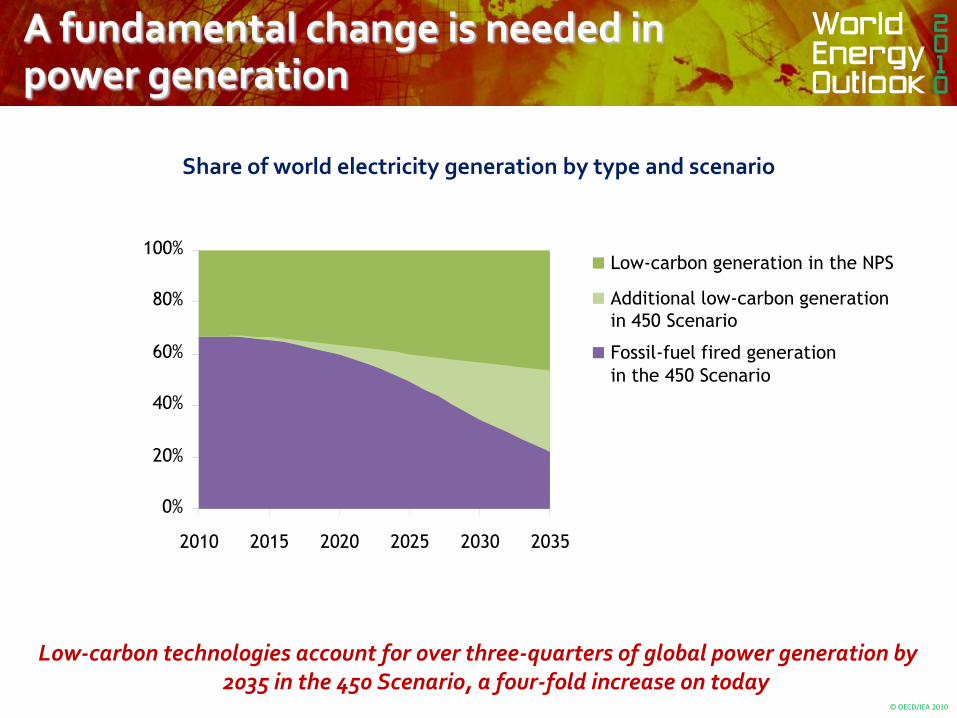

A fundamental change is needed in power generation

Low-carbon technologies account for over three-quarters of global power generation by 2035 in the 450 Scenario, a four-fold increase on today

Share of world electricity generation by type and scenario

Additional low-carbon generation

in 450 Scenario

Low-carbon generation in the NPS

Fossil-fuel fired generation

0%

20%

40%

60%

80%

100%

2010 2015 2020 2025 2030 2035

in the 450 Scenario

© OECD/IEA 2010

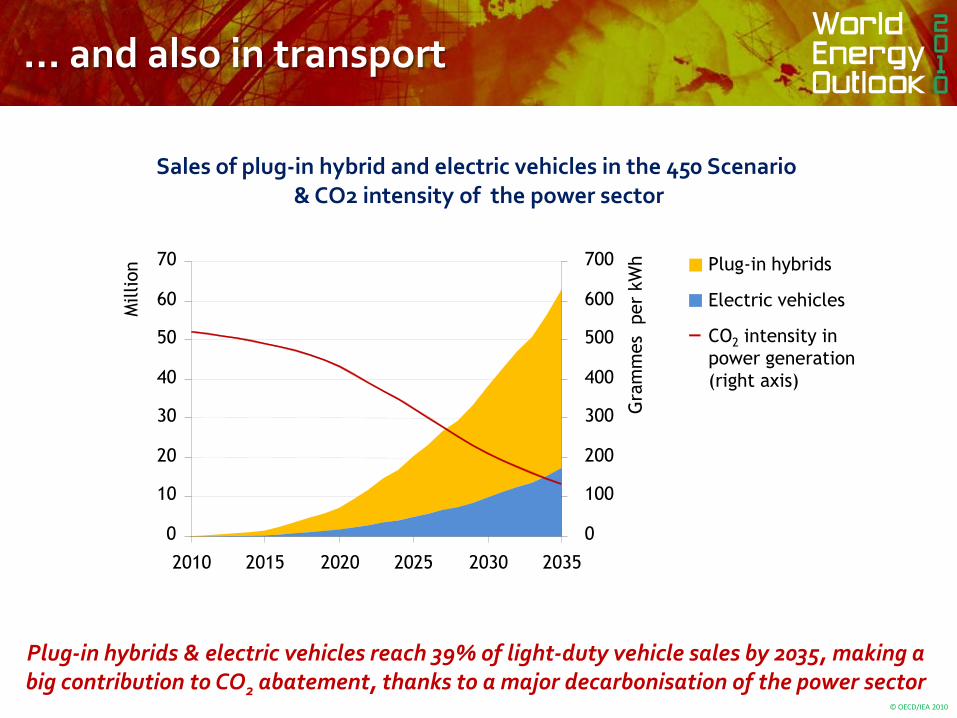

… and also in transport

Plug-in hybrids & electric vehicles reach 39% of light-duty vehicle sales by 2035, making a big contribution to CO2 abatement, thanks to a major decarbonisation of the power sector

Sales of plug-in hybrid and electric vehicles in the 450 Scenario

CO2 intensity in

power generation

(right axis)

Electric vehicles

Plug-in hybrids

& CO2 intensity of the power sector

0

100

200

300

400

500

600

700

Gra

mm

es

per

kW

h

0

10

20

30

40

50

60

70

2010 2015 2020 2025 2030 2035

Million

© OECD/IEA 2010

Will peak oil be a guest or the spectreat the feast?

Oil demand peaks at 88 mb/d before 2020 & falls to 81 mb/d in 2035, with a plunge in OECD demand more than offsetting continuing growth in non-OECD demand

Oil demand

World demand in

450 Scenario

Inter-regional

(bunkers)

Other non-OECD

India

China

OECD

Right axis:

2009 2015 2020 2025 2030 2035

mb/d

68

72

76

80

84

88

92

96

100

mb/d

-16

-12

-8

-4

0

4

8

12

16 World demand in

New Policies Scenario

Peak demand

in the 450 Scenario

© OECD/IEA 2010

Combating climate change will bring economic benefits as well as costs

In the 450 Scenario, annual spending on oil imports in 2035 by the five largest importers is around $560 billion, or one-third, lower than in the New Policies Scenario

Oil-import bills as share of GDP in selected countries

0%

1%

2%

3%

4%

5%

6%

7%

8%

European

Union

United

States

Japan China India

1980

2008

2009

2035: New Policies Scenario

2035: 450 Scenario

© OECD/IEA 2010

China in the 450 Scenario

© OECD/IEA 2010

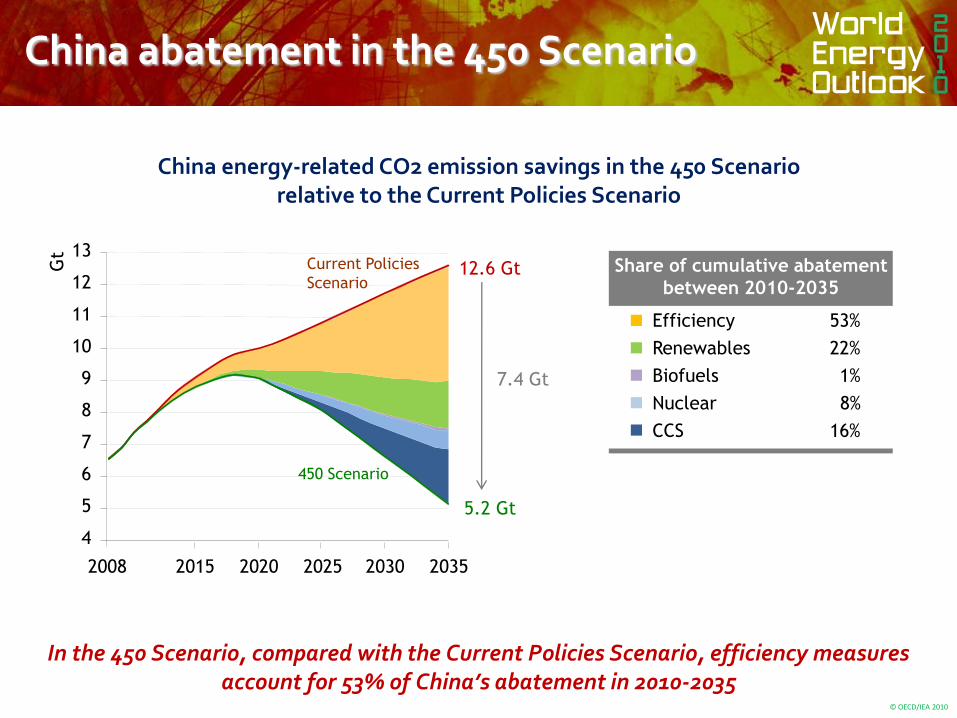

China abatement in the 450 Scenario

In the 450 Scenario, compared with the Current Policies Scenario, efficiency measures account for 53% of China’s abatement in 2010-2035

China energy-related CO2 emission savings in the 450 Scenariorelative to the Current Policies Scenario

Efficiency 53%

Renewables 22%

Biofuels 1%

Nuclear 8%

CCS 16%

Share of cumulative abatement

between 2010-203512.6 Gt

5.2 Gt

7.4 Gt

4

5

6

7

8

9

10

11

12

13

2008 2015 2020 2025 2030 2035

Gt

Current Policies

Scenario

450 Scenario

© OECD/IEA 2010

China abatement in the 450 Scenario

In moving from the New Policies Scenario to the 450 Scenario, China starts to rely more on CCS as room for further abatement from lower-cost options becomes limited

China energy-related CO2 emission savings in the 450 Scenariorelative to the New Policies Scenario

Efficiency 50%

Renewables 18%

Biofuels 1%

Nuclear 8%

CCS 23%

Share of cumulative abatement

between 2010-203512.6 Gt

5.2 Gt

5.0 Gt

4

5

6

7

8

9

10

11

12

13

2008 2015 2020 2025 2030 2035

Gt

Current Policies

Scenario

450 Scenario

10.1 Gt

2.4 GtNew Policies

Scenario

© OECD/IEA 2010

Low-carbon technologies account for 78% of China’s power generation by 2035 in the 450 Scenario, up from 19% today

Share of China electricity generation by type and scenario

Additional low-carbon generation

in 450 Scenario

Low-carbon generation in the NPS

Fossil-fuel fired generation

0%

20%

40%

60%

80%

100%

2010 2015 2020 2025 2030 2035

in the 450 Scenario

Power generation in China in the 450 Scenario

© OECD/IEA 2010

Sales of plug-in hybrid and electric vehicles in the 450 Scenario

CO2 intensity in

power generation

(right axis)

Electric vehicles

Plug-in hybrids

& CO2 intensity of the power sector in China

0

3

6

9

12

15

18

21

24

2010 2015 2020 2025 2030 2035

Million

0

100

200

300

400

500

600

700

800

Gra

mm

es

per

kW

h

Transport in China in the 450 Scenario

In China, plug-in hybrids & electric vehicles reach 45% of new light-duty vehicle sales by 2035

© OECD/IEA 2010

Summary & conclusions

Recently announced policies can make a difference, but fall well short of what is needed for a secure & sustainable energy future

Lack of ambition in Copenhagen has increased the cost of achieving the 2C goal & made it less likely to happen

> Unless commitments are fully implemented by 2020, it will be all but impossible to achieve the goal

The age of cheap oil is over, though policy action could bring lower international prices than would otherwise be the case

Renewables are entering the mainstream, but long-term support is needed to boost their competitiveness

Getting the prices right, by phasing-out fossil-fuel subsidies, is the single most effective measure to cut energy demand

© OECD/IEA 2010

Implications for China

China's role in global energy is set to expand & its policies will significantly impact global energy trends & prospects for limiting climate change

A golden age of gas led by China in the interest of diversifying the fuel mix can contribute greatly to reducing CO2 and other emissions

Continued energy pricing reforms in China is a triple-win for enhancing energy security, reducing emissions & immediate economic gains

China's role as leader in developing, manufacturing & deploying low-carbon technologies can drive down costs, to the benefits of all countries

Growing interconnectedness & China's increasing weight in the energy market links its energy security to global energy security