WORLD ENERGY INVESTMENT OUTLOOKsiteresources.worldbank.org/EXTENERGY2/Resources/4114199...WORLD...

37

Dr. Fatih Birol Chief Economist Head, Economic Analysis Division International Energy Agency / OECD WORLD ENERGY INVESTMENT OUTLOOK

Transcript of WORLD ENERGY INVESTMENT OUTLOOKsiteresources.worldbank.org/EXTENERGY2/Resources/4114199...WORLD...

Dr. Fatih BirolChief Economist Head, Economic Analysis DivisionInternational Energy Agency / OECD

WORLDENERGYINVESTMENTOUTLOOK

Global Strategic Challenges

l Security of energy supplies

l Threat of environmental damage caused by energy use

l Uneven access of the world’s population to modern energy

l Investment in energy-supply infrastructure

Global Energy Global Energy Investment OutlookInvestment Outlook

World Energy Investment2001-2030

Total investment: 16 trillion dollars

Oil 19%

Electricity60%

Coal 2%Gas 19%

OtherRefining

E&D 72%

13%15%

E&D

LNG Chain

T&D and Storage

55%

37%

8%

Power generation

T&D54%

46%

Mining

Shipping and ports

12%

88%

Production accounts for the majority of investment in the supplychain – except for electricity

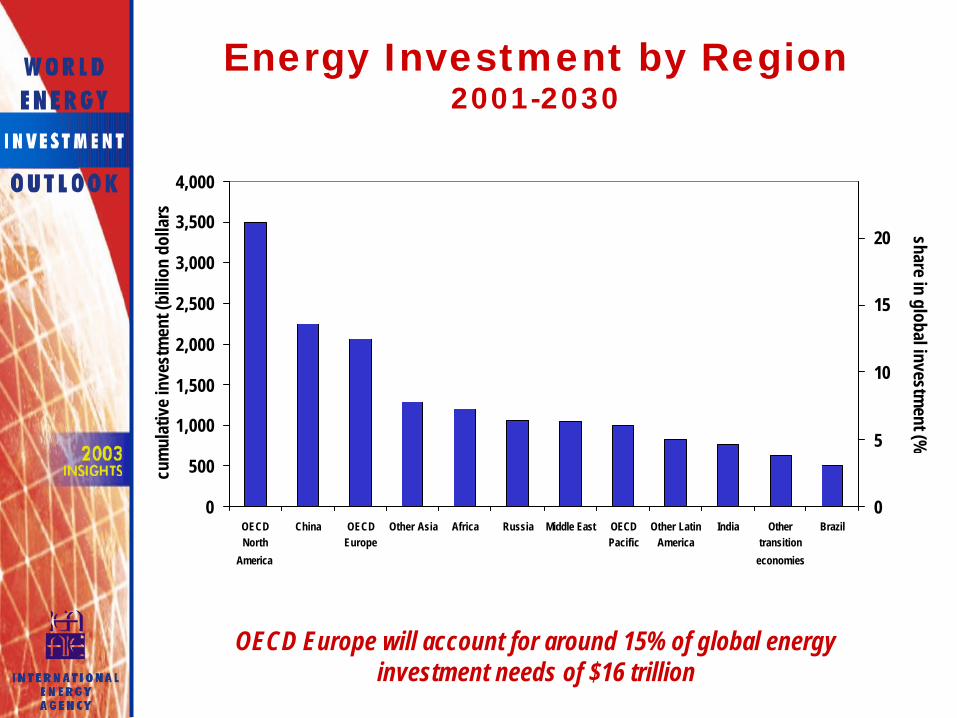

Energy Investment by Region 2001-2030

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

OECDNorth

America

China OECDEurope

Other Asia Africa Russia Middle East OECDPacific

Other LatinAmerica

India Othertransition

economies

Brazil

cum

ulat

ive

inve

stm

ent (

billi

on d

olla

rs)

0

5

10

15

20 share in global investment (%

)

OECD Europe will account for around 15% of global energy investment needs of $16 trillion

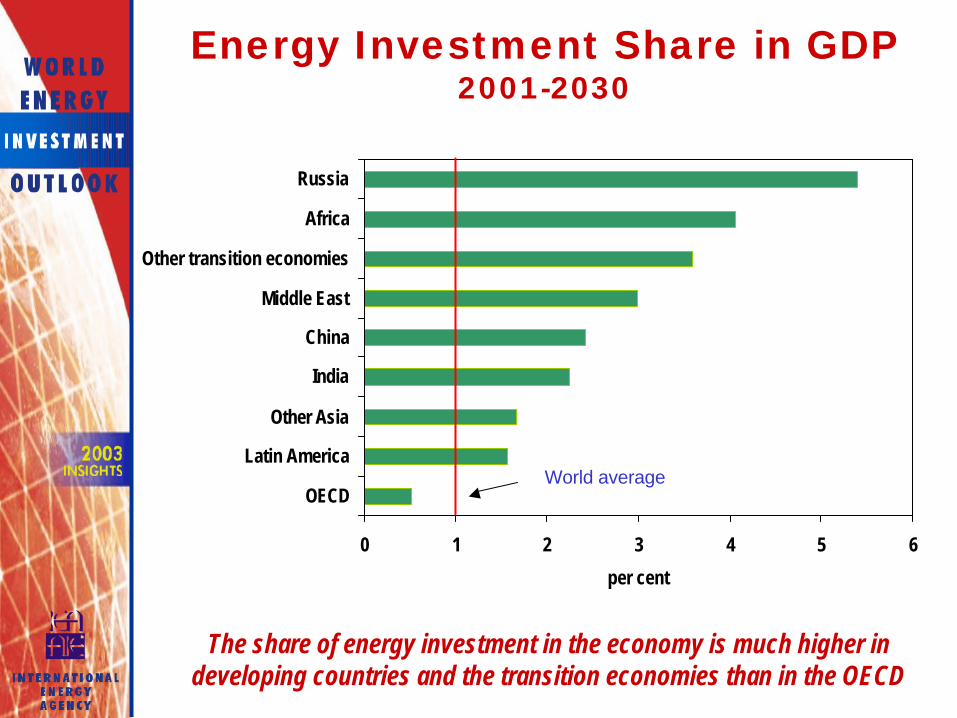

Energy Investment Share in GDP2001-2030

0 1 2 3 4 5 6

OECD

Latin America

Other Asia

India

China

Middle East

Other transition economies

Africa

Russia

per cent

World average

The share of energy investment in the economy is much higher in developing countries and the transition economies than in the OECD

Oil Investment OutlookOil Investment Outlook

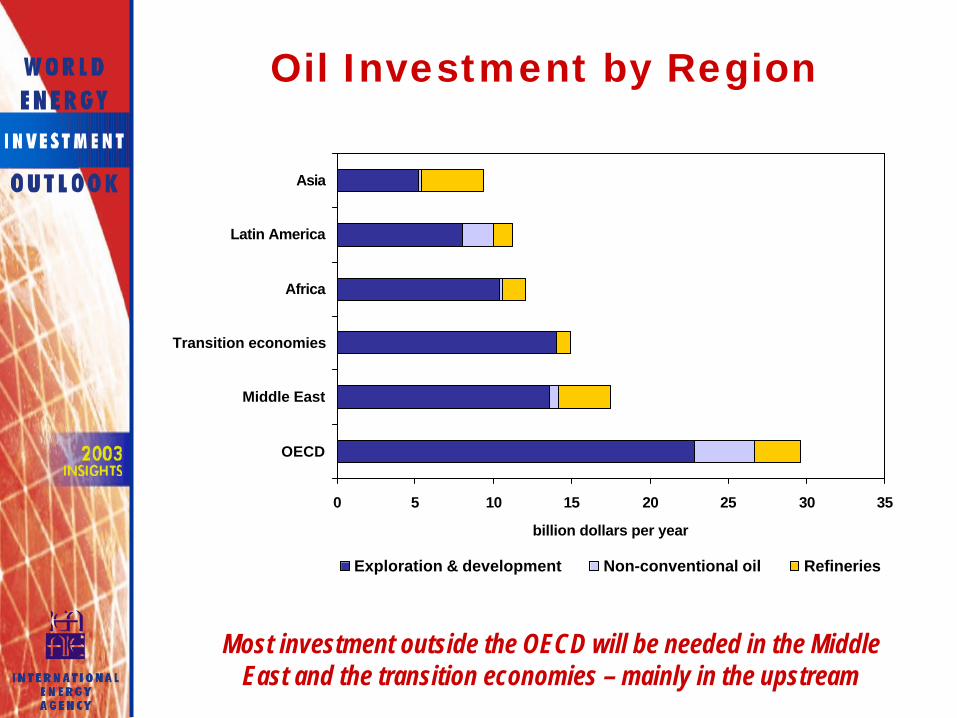

Oil Investment by Region

Most investment outside the OECD will be needed in the Middle East and the transition economies – mainly in the upstream

0 5 10 15 20 25 30 35

OECD

Middle East

Transition economies

Africa

Latin America

Asia

billion dollars per year

Exploration & development Non-conventional oil Refineries

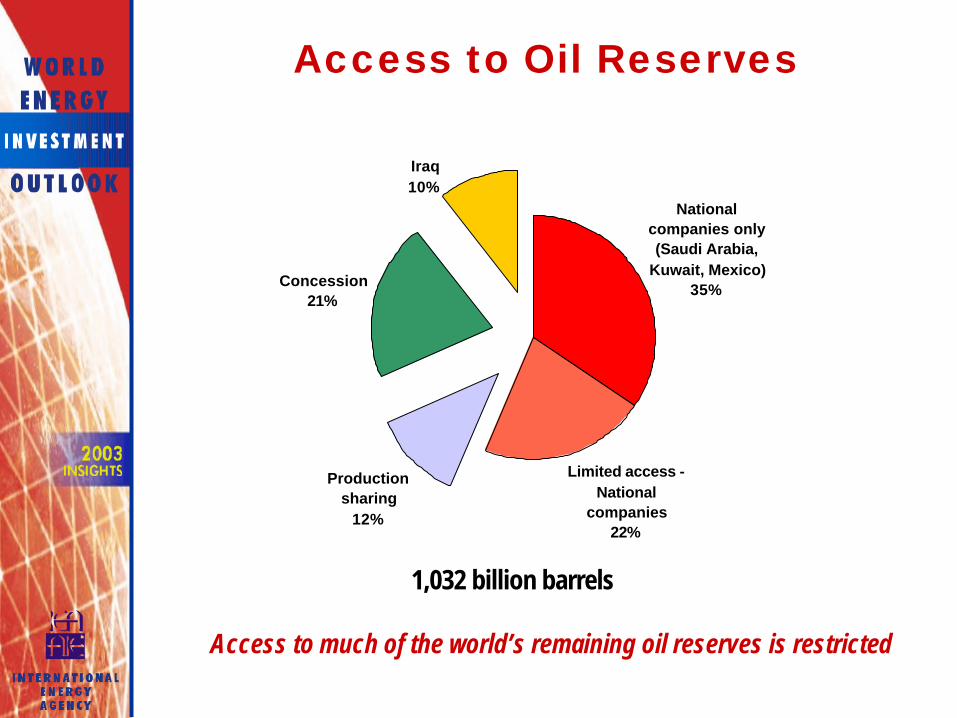

Access to Oil Reserves

National companies only (Saudi Arabia,

Kuwait, Mexico)35%

Limited access - National

companies 22%

Production sharing

12%

Concession21%

Iraq10%

1,032 billion barrels

Access to much of the world’s remaining oil reserves is restricted

Restricted Middle East Oil Investment Scenario

OPEC Middle East Share in Global Oil Supply

OPEC Middle East’s share of global oil production is assumed to remain flat at under 30% in Restricted Investment Scenario

0

10

20

30

40

50

1970 1980 1990 2000 2010 2020 2030

per

cent

Restricted Investment Scenario Reference Scenario

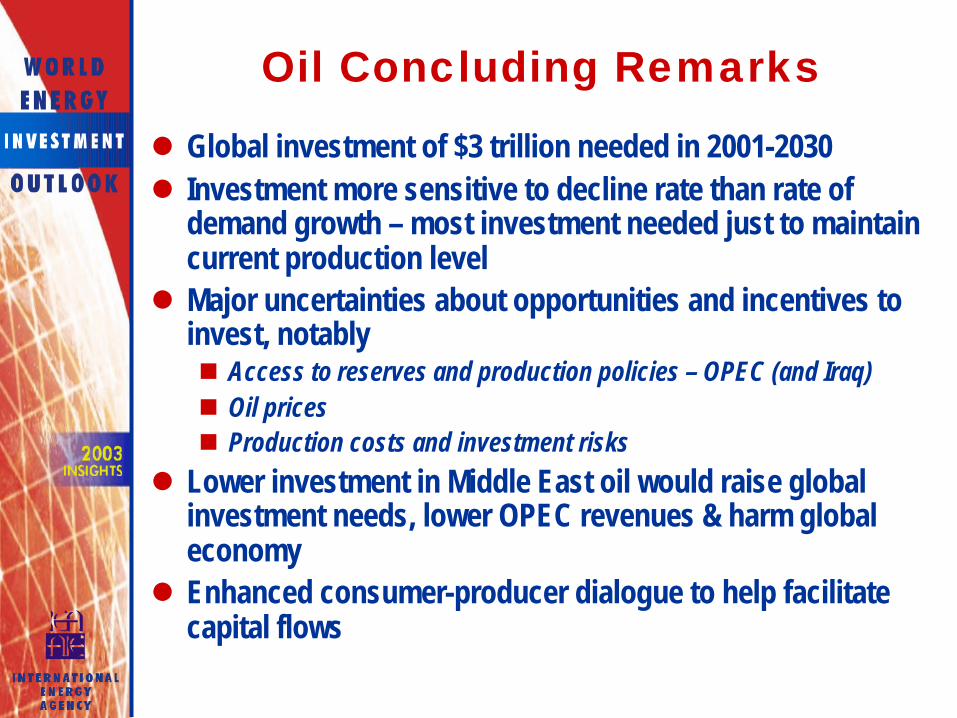

Oil Concluding Remarks

l Global investment of $3 trillion needed in 2001-2030l Investment more sensitive to decline rate than rate of

demand growth – most investment needed just to maintain current production level

l Major uncertainties about opportunities and incentives to invest, notablyn Access to reserves and production policies – OPEC (and Iraq)n Oil pricesn Production costs and investment risks

l Lower investment in Middle East oil would raise global investment needs, lower OPEC revenues & harm global economy

l Enhanced consumer-producer dialogue to help facilitate capital flows

Gas Investment Gas Investment OutlookOutlook

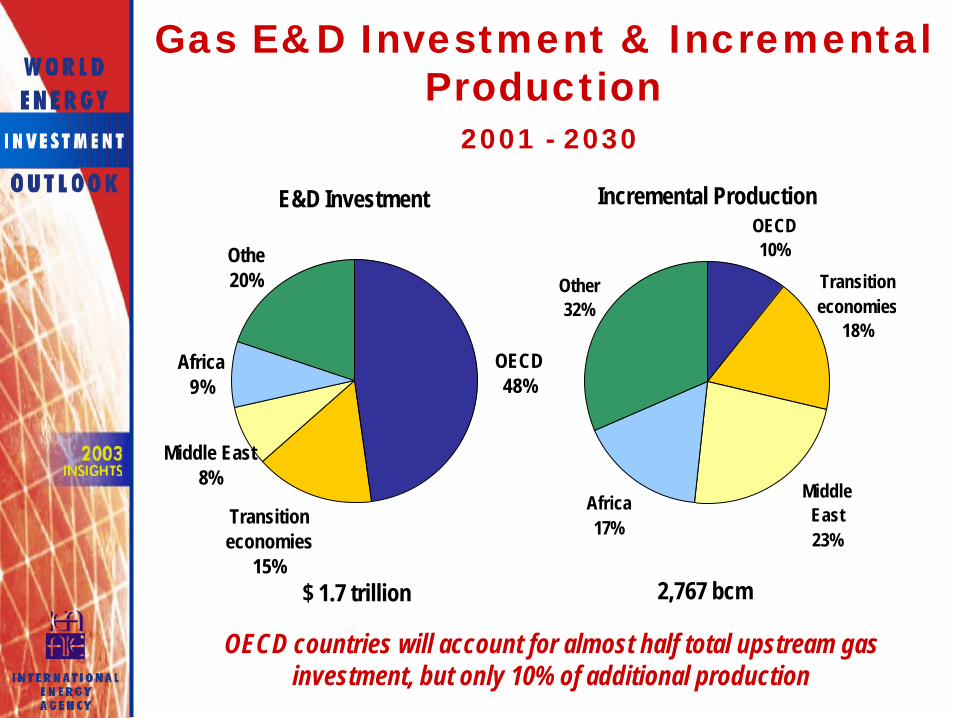

Gas E&D Investment & Incremental Production

2001 - 2030

Middle East 8%

OECD48%

Othe20%

Transition economies

15%

Africa9%

Africa17%

Middle East23%

Other32%

OECD10%

Transition economies

18%

E&D Investment Incremental Production

$ 1.7 trillion 2,767 bcm

OECD countries will account for almost half total upstream gas investment, but only 10% of additional production

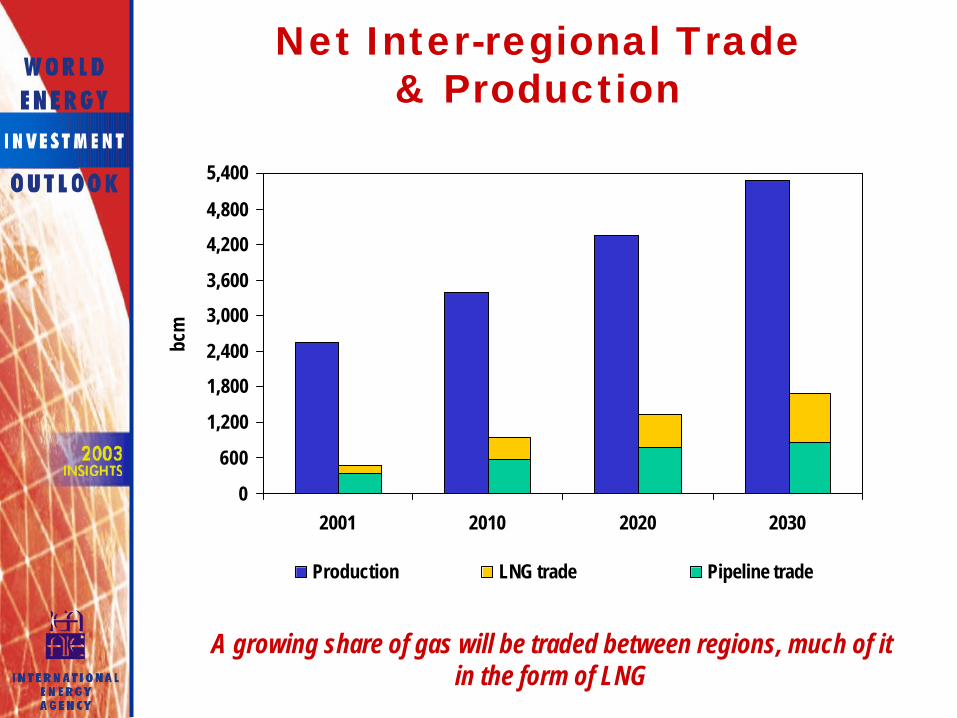

Net Inter-regional Trade & Production

0

600

1,200

1,800

2,400

3,000

3,600

4,200

4,800

5,400

2001 2010 2020 2030

bcm

Production LNG trade Pipeline trade

A growing share of gas will be traded between regions, much of it in the form of LNG

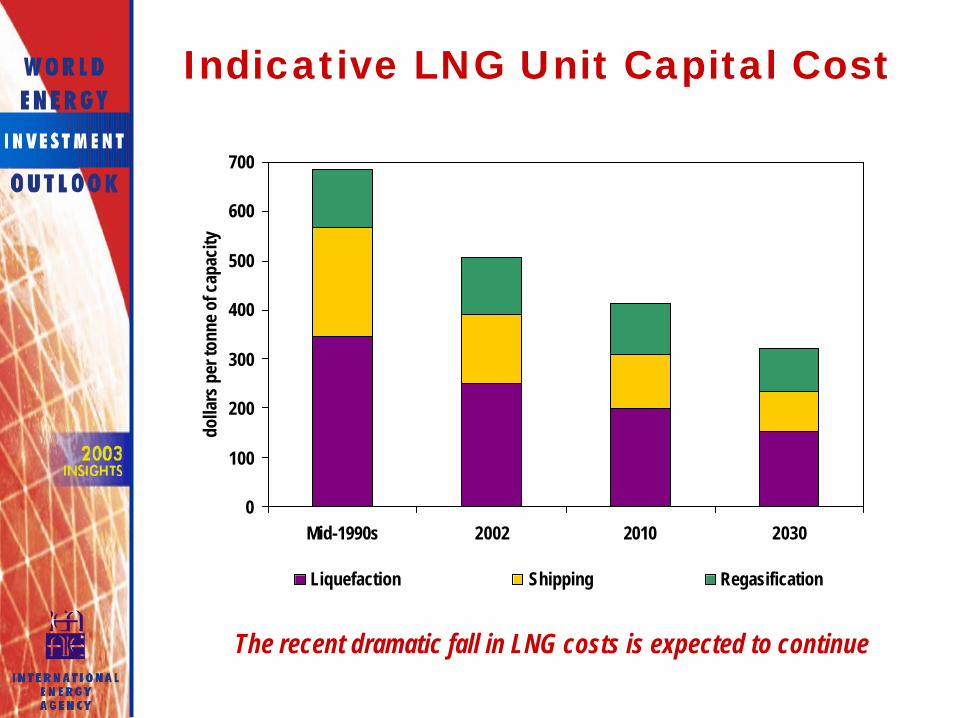

Indicative LNG Unit Capital Cost

0

100

200

300

400

500

600

700

Mid-1990s 2002 2010 2030

dolla

rs p

er to

nne

of c

apac

ity

Liquefaction Shipping Regasification

The recent dramatic fall in LNG costs is expected to continue

Gas Investment Uncertainties

l Balance of risk and return – price is key

l Complexity of financing very large-scale projects –especially in developing countries

l Access to reserves and fiscal regime – most new investment will be private

l Impact of market reforms on investment risk – long-term contracts will remain necessary

These factors could lead to shortfall in investment, supply bottlenecks and higher prices in some cases

Coal Investment Coal Investment OutlookOutlook

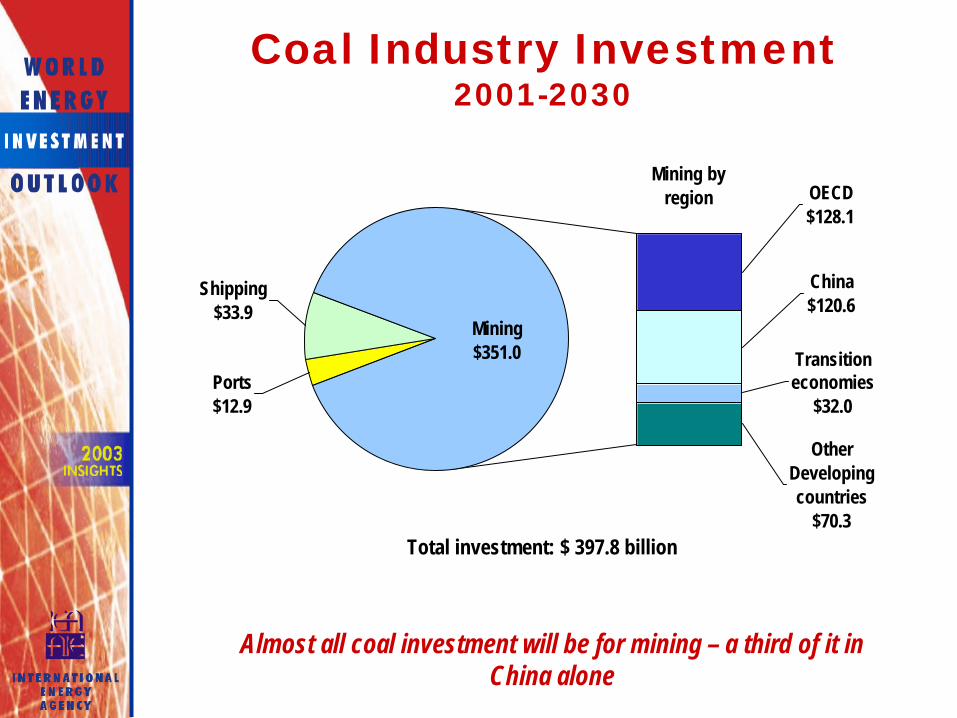

Coal Industry Investment 2001-2030

OtherDeveloping countries

$70.3

Transition economies

$32.0

China $120.6

OECD $128.1

Ports $12.9

Shipping $33.9

Mining $351.0

Mining by region

Total investment: $ 397.8 billion

Almost all coal investment will be for mining – a third of it in China alone

Electricity Investment Electricity Investment OutlookOutlook

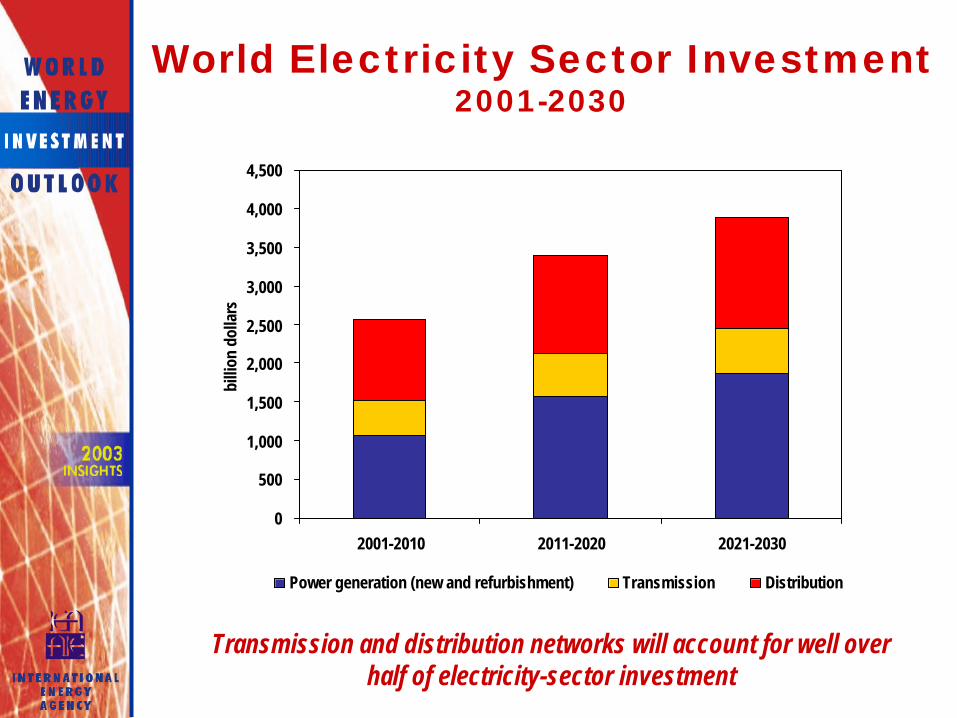

World Electricity Sector Investment2001-2030

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2001-2010 2011-2020 2021-2030

billi

on d

olla

rs

Power generation (new and refurbishment) Transmission Distribution

Transmission and distribution networks will account for well over half of electricity-sector investment

Electricity Sector Investment by Region

2001-2030

China will need more electricity investment than any other country or region

0

500

1,000

1,500

2,000

2,500

China OtherAsia

LatinAmerica

Africa MiddleEast

US andCanada

EuropeanUnion

OECDPacific

OtherOECD

Russia Rest ofTE

billi

on d

olla

rs

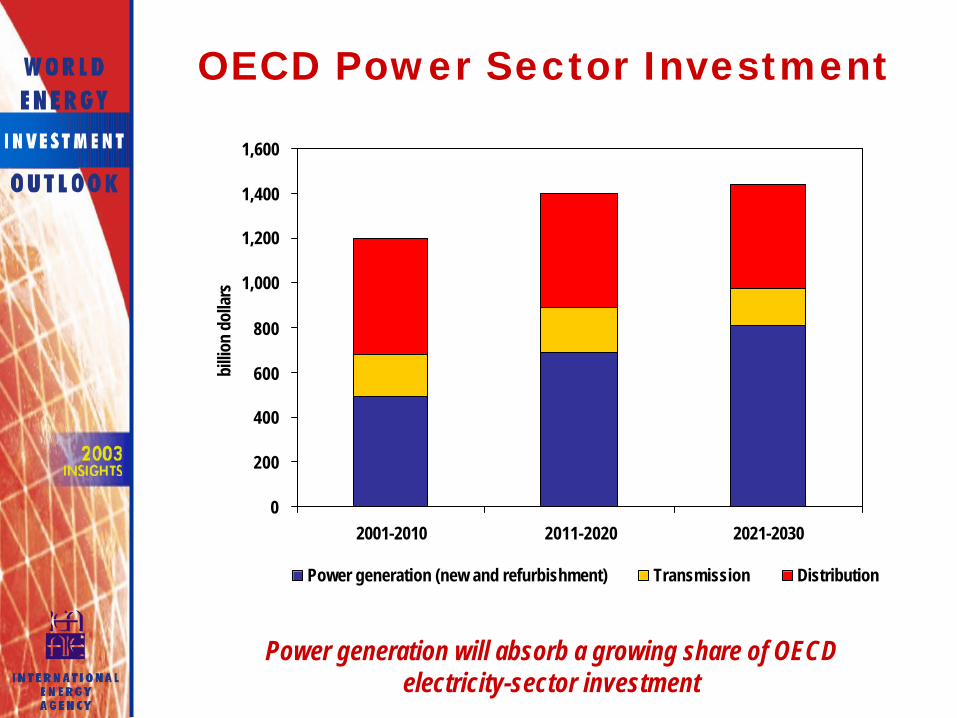

OECD Power Sector Investment

0

200

400

600

800

1,000

1,200

1,400

1,600

2001-2010 2011-2020 2021-2030

billi

on d

olla

rs

Power generation (new and refurbishment) Transmission Distribution

Power generation will absorb a growing share of OECD electricity-sector investment

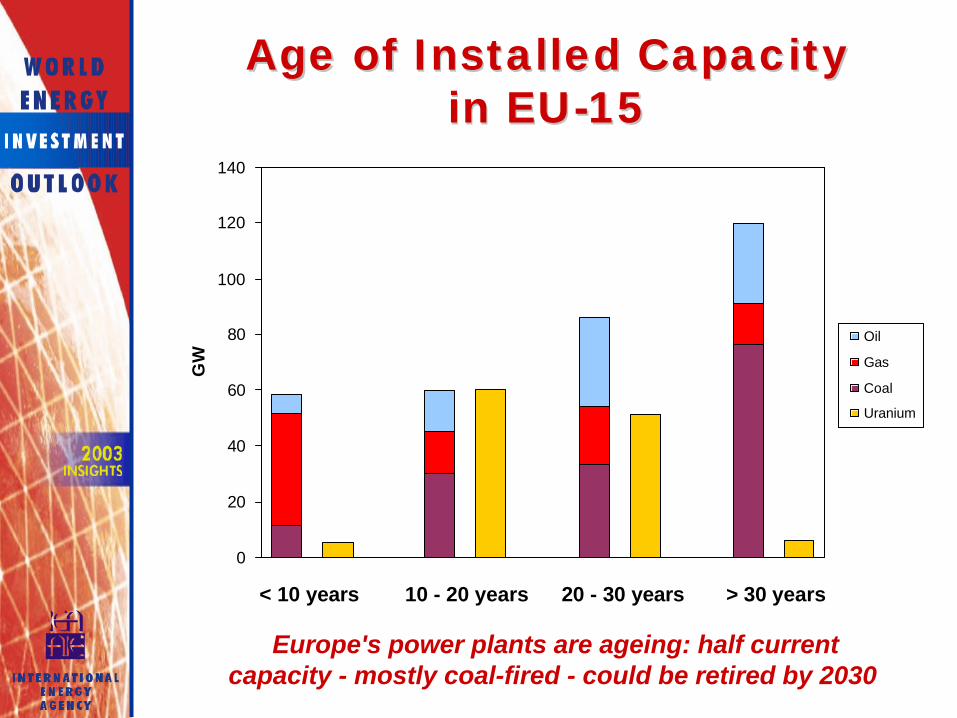

Age of Installed CapacityAge of Installed Capacityin EU-15in EU-15

0

20

40

60

80

100

120

140

GW

Oil

Gas

Coal

Uranium

< 10 years 10 - 20 years 20 - 30 years > 30 years

Europe's power plants are ageing: half currentcapacity - mostly coal-fired - could be retired by 2030

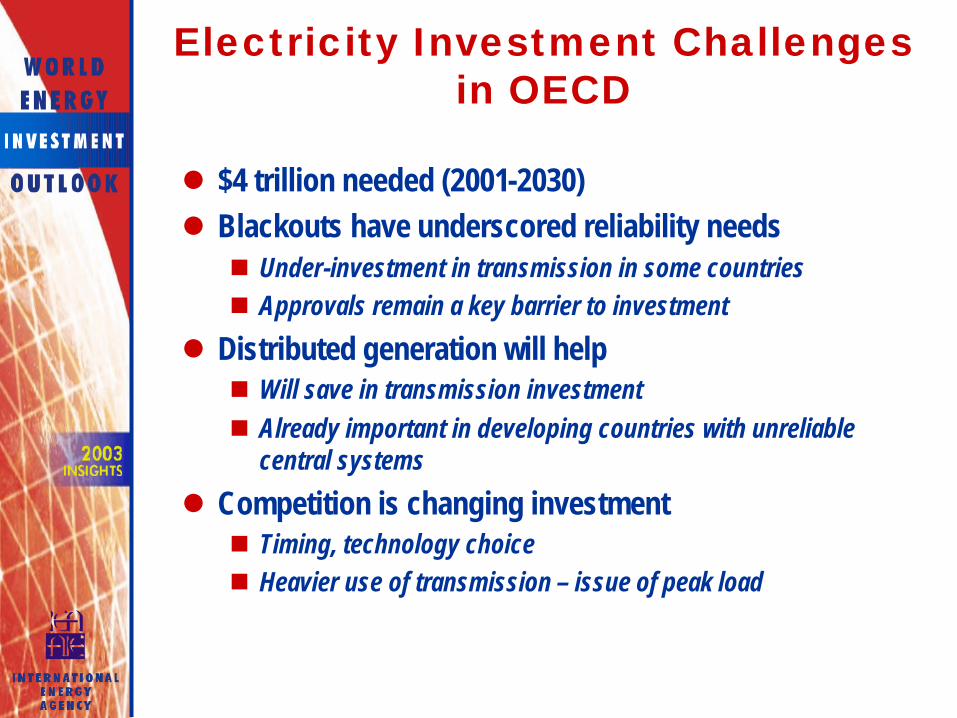

Electricity Investment Challenges in OECD

l $4 trillion needed (2001-2030)l Blackouts have underscored reliability needsn Under-investment in transmission in some countriesn Approvals remain a key barrier to investment

l Distributed generation will helpn Will save in transmission investmentn Already important in developing countries with unreliable

central systems

l Competition is changing investmentn Timing, technology choicen Heavier use of transmission – issue of peak load

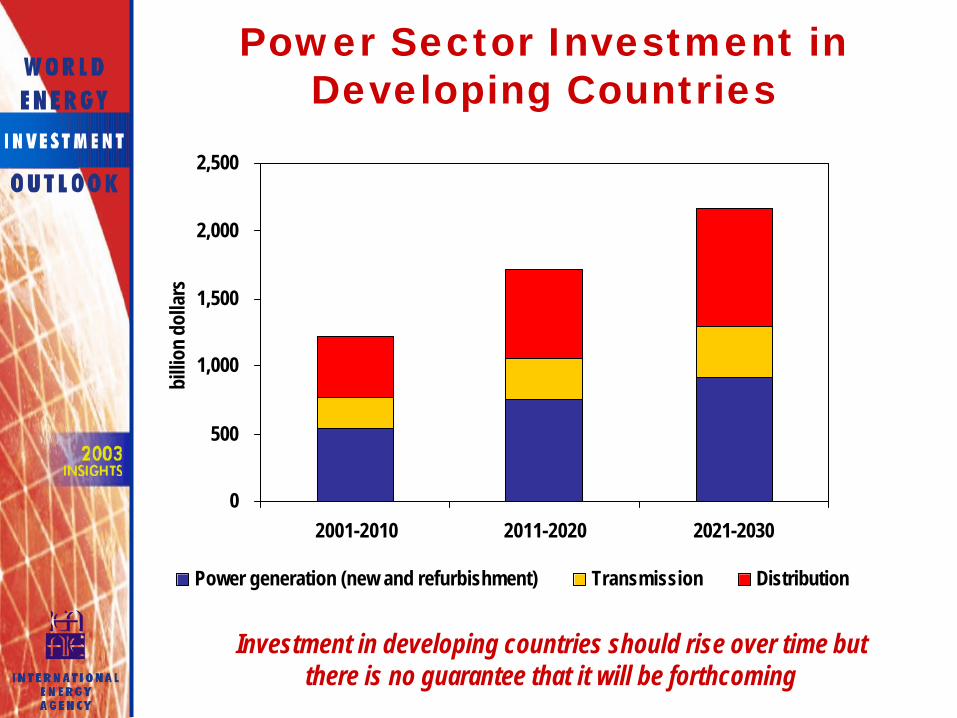

Power Sector Investment in Developing Countries

0

500

1,000

1,500

2,000

2,500

2001-2010 2011-2020 2021-2030

billi

on d

olla

rs

Power generation (new and refurbishment) Transmission Distribution

Investment in developing countries should rise over time but there is no guarantee that it will be forthcoming

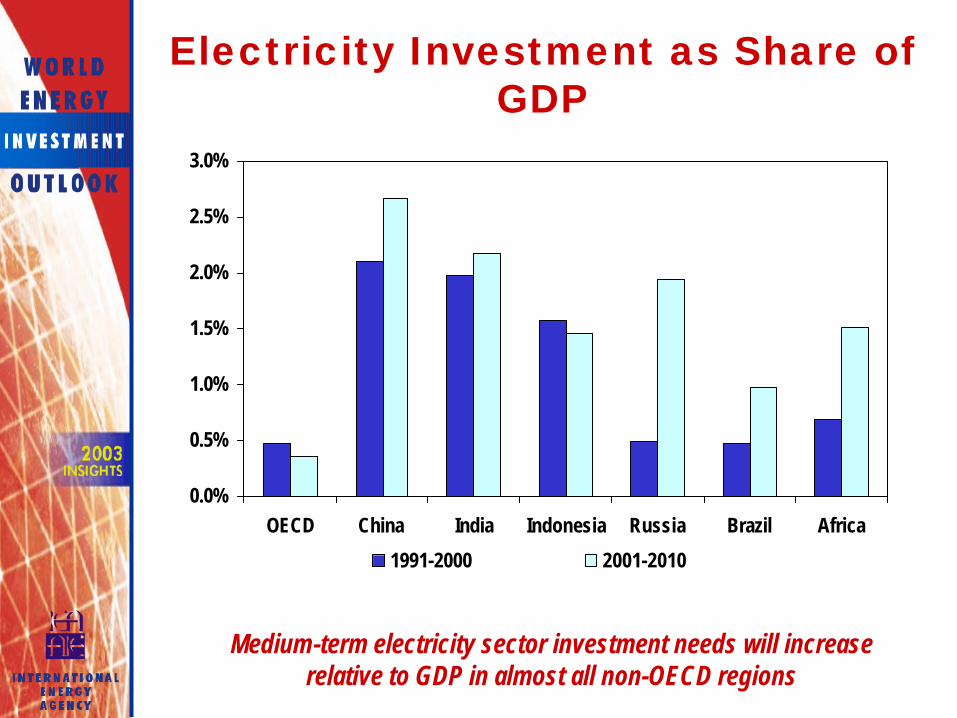

Electricity Investment as Share of GDP

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

OECD China India Indonesia Russia Brazil Africa

1991-2000 2001-2010

Medium-term electricity sector investment needs will increase relative to GDP in almost all non-OECD regions

0

200

400

600

800

1,000

1,200

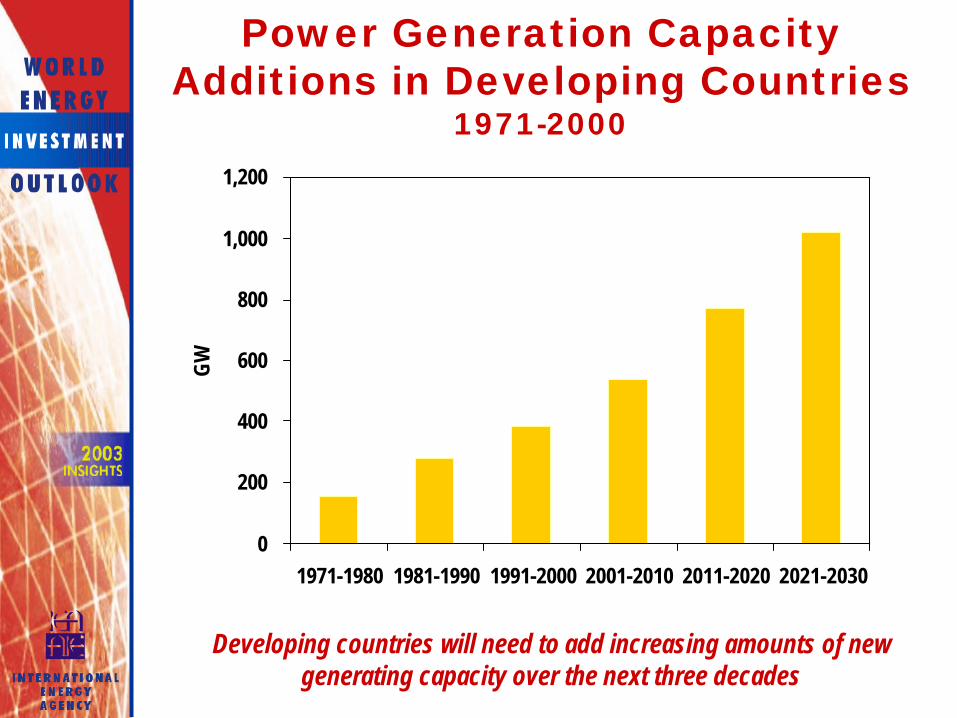

1971-1980 1981-1990 1991-2000 2001-2010 2011-2020 2021-2030

GW

Power Generation Capacity Additions in Developing Countries

1971-2000

Developing countries will need to add increasing amounts of new generating capacity over the next three decades

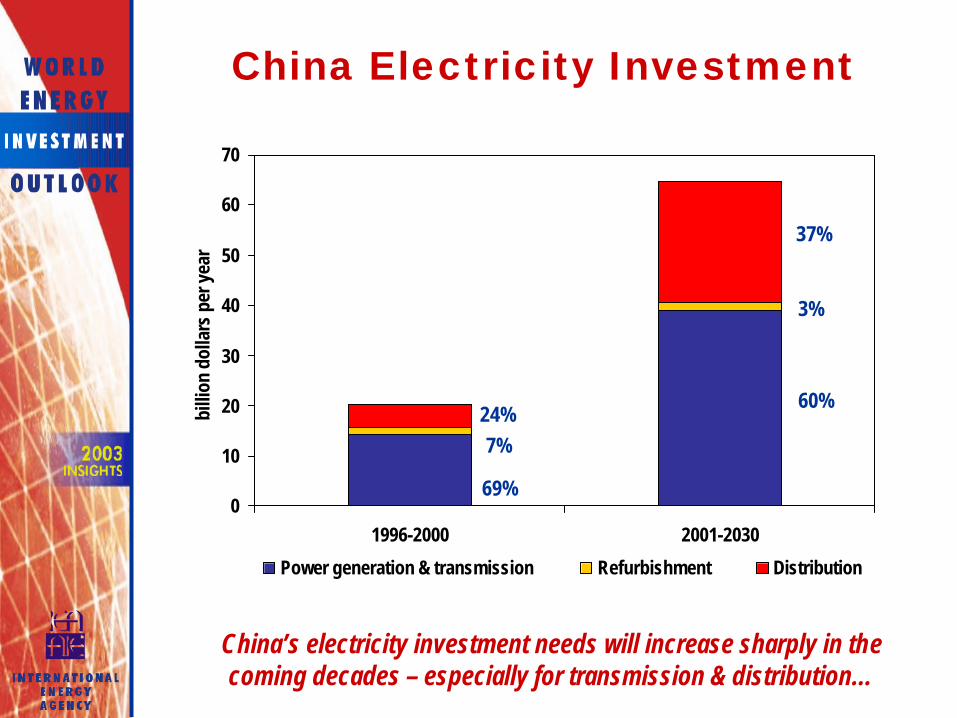

China Electricity Investment

0

10

20

30

40

50

60

70

1996-2000 2001-2030

billi

on d

olla

rs p

er y

ear

Power generation & transmission Refurbishment Distribution

24%7%

69%

37%

3%

60%

China’s electricity investment needs will increase sharply in the coming decades – especially for transmission & distribution…

Ratio of China Electricity Sector Investment to GDP

0

1

2

3

1985 1990 2000 2001-2010 2011-2020 2021-2030

shar

e of

ele

ctric

ity in

vest

men

ts in

GDP

(%)

… though investment needs will decline relative to GDP as its economy matures

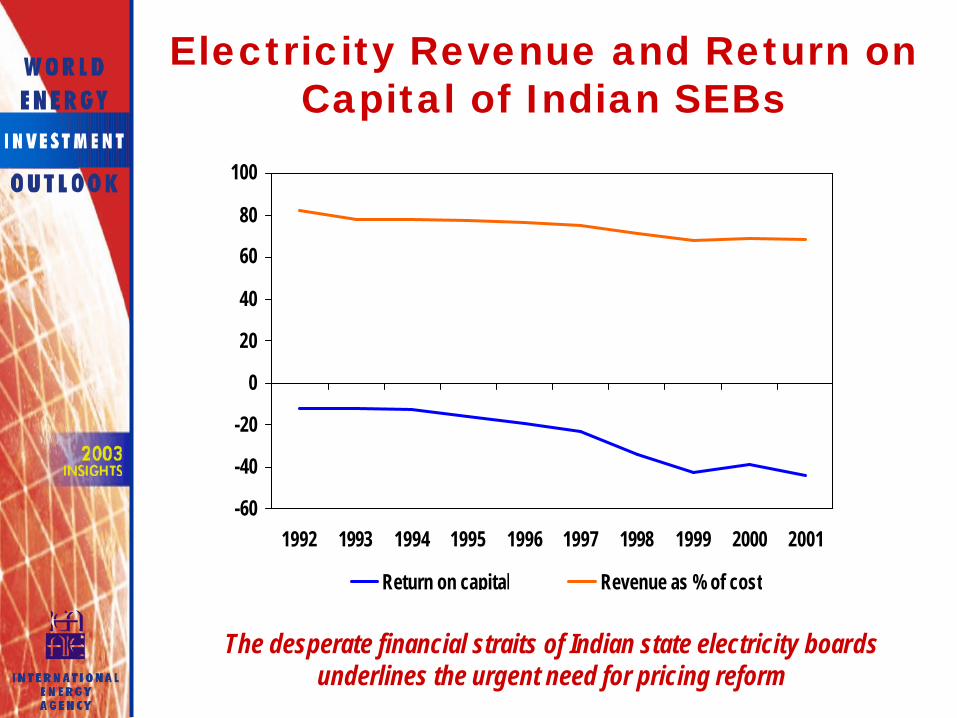

Electricity Revenue and Return on Capital of Indian SEBs

-60

-40

-20

0

20

40

60

80

100

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Return on capital Revenue as % of cost

The desperate financial straits of Indian state electricity boards underlines the urgent need for pricing reform

Power Sector Private Investment in Developing Countries

0

5

10

15

20

25

30

35

40

45

50

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

billi

on d

olla

rs

Developing countries will need to reverse the slump in private capital flows if projected investment is to be forthcoming

Universal Electricity Universal Electricity Access ScenarioAccess Scenario

Investment to Ensure Universal Electricity Access

2001-2030

0

500

1,000

1,500

2,000

China South Asia Africa East Asia LatinAmerica

MiddleEast

billi

on d

olla

rs

Reference Scenario Electrification Scenario

More than $660 billion is needed to supply basic electricity services to the world’s very poor – mainly in Africa and South Asia

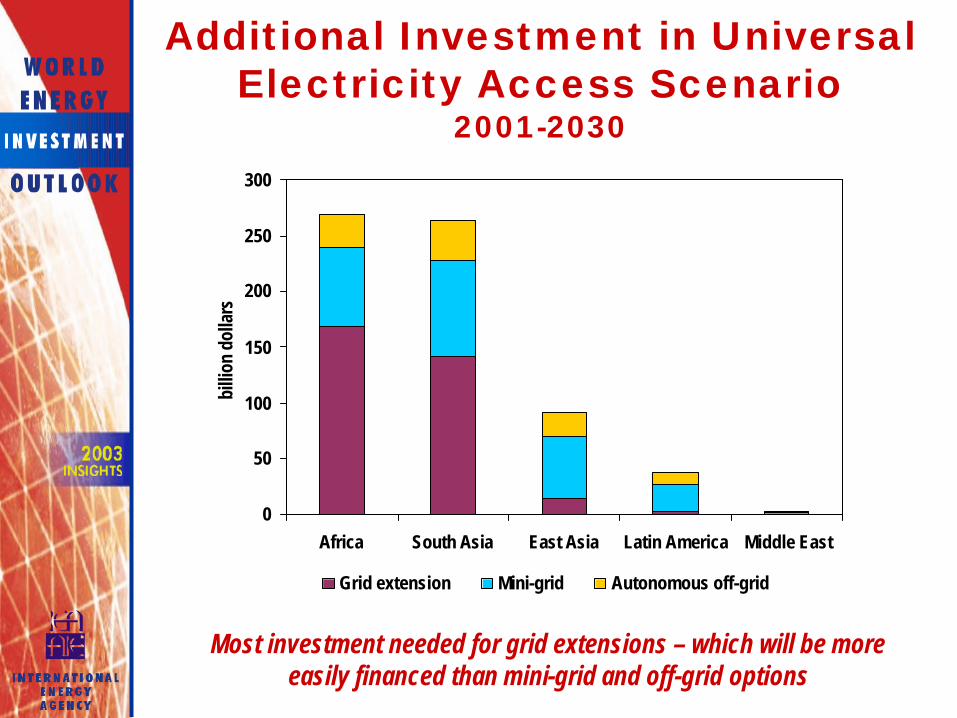

Additional Investment in Universal Electricity Access Scenario

2001-2030

0

50

100

150

200

250

300

Africa South Asia East Asia Latin America Middle East

billi

on d

olla

rs

Grid extension Mini-grid Autonomous off-grid

Most investment needed for grid extensions – which will be more easily financed than mini-grid and off-grid options

Electricity Investment Challenges in Developing Countries

l Almost $6 trillion needed (2001-2030) – far more than in past 3 decades

l Financing this will be challenging – especially in Africa and India

l Realising this investment will call forn More rigorous sector reforms – notably more cost-reflective

pricing and improved collectionn More stable and predictable investment regimesn Better corporate governancen Development of domestic financial markets n Stronger incentives for private and foreign investors

Electricity Concluding Remarks

l Electricity sector will dominate energy investment

l Almost $10 billion needed in 3 decades to 2030

l More than half electricity investment will go to transmission & distribution networks

l Biggest uncertainty in OECD countries concerns impact of market reforms on investment risks and returns –especially for reserve and peak capacity

l Financing electricity investment in non-OECD countries is greatest challenge – pricing reform is fundamental to attracting private capital

Energy Investment Challenge

l Total investment requirements are modest relative to world GDP, but challenge differs by region / fuel

l Energy and financial resources are sufficient, but increasing competition for capital and higher risk

l Capital needs are largest for electricityl Half total energy investment is needed in developing

countries – where financing will be hardestl Policymakers need to ensure basic principles of good

governance are applied and respected – including cost-reflective pricing

l Production accounts for the bulk of investment – more than half just to replace old capacity