World Bank Document - Documents &...

165

Document of The World Bank FOR OFFICIAL USE ONLY Report No. 12662-IND STAFF APPRAISAL REPORT INDONESIA SIJMATERA AND KALIMANTAN POWER PROJECT MAY 27, 1994 IT;.'I ~ .41-r P'.er-rl Nt<: 1_C 'tvpe .;d•y Industry and Energy Operations Division Country Department III East Asia and Pacific Regional Office This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorizaion. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of World Bank Document - Documents &...

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. 12662-IND

STAFF APPRAISAL REPORT

INDONESIA

SIJMATERA AND KALIMANTAN POWER PROJECT

MAY 27, 1994

IT;.'I ~ .41-r

P'.er-rl Nt<: 1_C

'tvpe .;d•y

Industry and Energy Operations DivisionCountry Department IIIEast Asia and Pacific Regional Office

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorizaion.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency Unit - Indonesian Rupiah (Rp)(As of January 1994)

US$1 = Rp2,105Rp 1 billion = US$0.475 million

FISCAL YEARApril 1 - March I

WEIGHTS AND MEASURES

1 metric ton = 1,000 kiliograms (kg)1 liter (1) = 0.0063 barrels (bbl)1 kilometer (km) = 0.6215 mile (mi)1 kilovolt (kV) = 1,000 volts (V)1 megavolt ampere (MVA) = 1000 kilovolt ampere (kVA)1 megawatt (MW) = 1,000 kilowatts (kW)1 gigawatt hour (GWh) = 1 million kilowatt hours (kWh)1 terrawatt hol'r (TWh) = 1 billion kilowatt hours (kWh)

ABBREVILATIONS

BAKOREN - National Energy BoardBAPPENAS - National Development Planning AgencyDGEED - Directorate-General of Electricity and Energy DevelopmentEA - Environmental AssessmentGOI - Government of IndonesiaIERR - Internal Economic Rate of RetumLNG - Liquefied Natural GasLRMC - Long Run Marginal CostMIS - Management Information SystemMME - Ministry of Mines and EnergyPAP - Project Affected PersonsPERTAMINA - National Oil and Gas CompanyPLN - State Electricity CorporationPPE - Engineerng Services Center of PLNRE - Rural ElectrificationRENSALITA - Five-Year Corporate PlanREPELITA - Five-Year Development PlanROR - Rate of ReturnTA - Technical Assistance

FOR OFFICIAL USE ONLY

INDONESIASUMATEtA AND KALM[ANTAN POWER PROJECT

LOAN AND PROJECr SUMMARY

Borrower: Republic of Indonesia

Benefidary: State Electricity Corporation (PLN)

Amount: US$260.5 million equivalent

Terms: Repayable in 20 yea s, ii.cluding five years of grace at the standard variableinterest rate

Onlending The proceeds of the loan, except $3.2 million for technical assistance to theTerms: Government of Indonesia (GOI), will be onlent from GOI to PLN for 20 years,

including a grace period of 5 years; the subsidiary loan will be denominated inUS dollars and the onlending interest rate would be equal to the Bank's standardvariable interest rate plus 0.5 percent per annum. PLN will bear the foreigrexchange risk.

Project The proposed project has a policy component and several physical components.Description: The policy component of the project entails: (a) establishing a policy framework

for private sector participation; (b) restructuring PLN and establishingcommercial operations as i limited liability company (Persero); (c) implementingfrmework for regulatory oversight of the power sector; and (d) introducingformula-based power tariffs, as well as bulk power purchase and supply tariffs.The physical components of the project would help finance economical andenviromnentally sustainable expansion of PLN's generation capacity, withassociated transmission lines, in the islands of Sumiatera and Kalimantan andimprove service reliability. The physical project components are:(a) construction of a hydroelectric power plant with an initial generating capacityof 90 MW at Besai in South Sumatera and related transmission facilities;(1) construction of a mine-mouth lignite fired thermal power plant with an initialgenerating capacity of 130 MW at Asam Asam near Banjarmasin in SouthKalimantan and related transmission facilities; (c) procurement of two barge-mounted power plants of 10 MW and 30 MW capacity respectively; and(d) technical assistance comprising: (i) engineering and construction supervisionof Besai hydroelectric and Banjarmasin thermal power plants; (ii) strengtheningthe capability of GOI for environmental management in the coal mining sector;(iii) promoting demand management; (iv) strengthening the enviromnentalmanagement capability of PLN; and (v) implementing pilot projects for PLN'sRegions IV and VI in South Sumatera and South Kalimantan respectively toimprove their operating efficiency.

Benefits: The policy reform underlying the project will change the structure and dynamicsof Indonesia's power sector. Opening the sector to private investors andrestructuring PLN will expand the financial envelope for system expansion and

This document has a restricted distnbution and may be used by recipients only in the performance of theirafficial duties. Its contents may not othewise be disclosed without World Bank authorization.

enhance incentives for lowering the cost and improving the reliability of service.Specifically, the investment components of the proposed project will help PLNmeet increases in eleciricity demand in South Sumatera and South Kalimantanand improve service reliability, as wel' as mitigate periodic power shortages inthese regions. The Besai hydroelectric power plant will help substitute oil-firedgeneration in the region by a renewable energy source. The Banjarmasinthermal power plant will produce electricity at the mine mouth utilizing a cheapsource of fuel Oignite) that is non-tradeable and of no other cormercial value.Further, technical assistance will help strengthen the environmental managementcapabilities of the Bureau of Environment and Technology in the Ministry ofMines and Energy, as well as PLN. Support for demand management will helpreduce the growth rate in electricity demand and curtail peak load in theinterconnected grid systems of PLN. Also, the proposed pilot projects in PLN'sRegions IV and VI will help transformation of the respective systems into profitcenters to improve the efficiency of operations.

Rialks: The GOI has an excellent track record in carrying out reforms to which it hascommitted. While the scope of the proposed sector, institutional and regulatoryreform is ambitious, the main elements are firmly embedded in theGovernment's policy agenda. The risks of delays in implementing the reformare within a relativel-' smal! range, considering the magnitude of the envisagedchanges. Specifically, there is a risk that delays in carrying out the plannedlarge development program would not reduce supply shortages and substitutecostly captive power generation to the extent expected. There is litfle risk thatthe px er generation components of the proposed project would becomeredundant if the projected levels of electricity demand fail to materialize, sincethey are part of the core expansion program of PLN and justified under theprojected demand scenarios. Project implementation risks are small; thegeological and hydrological conditions of the Besai site well known and stable,respectively. The risks of schedule slippage and cost overruns in theimplementation of the coal-fired Banjarmasin thermal power plant are minorconsidering PLN's experience in project management and carefully worked outimplementation schedule.

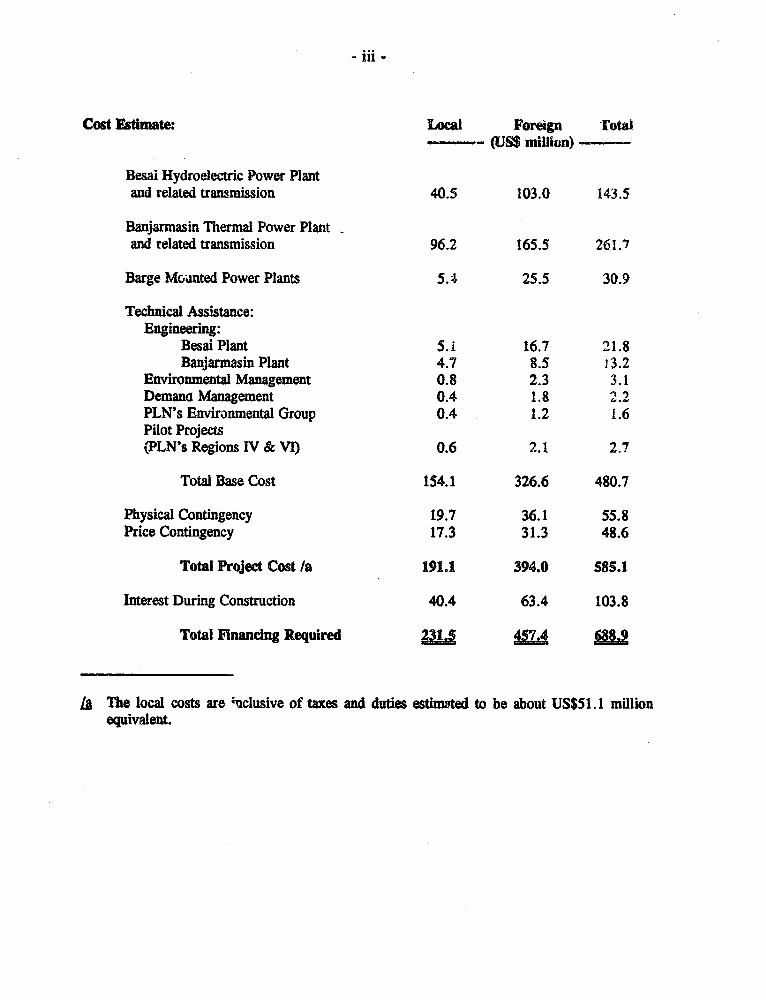

- iii -

Cost Estimate: Local Foreign -Toiw(US$ million)-

Besai Hydroelectric Power Plantand related transmission 40.5 103.0 143.5

Banjarmasin Thermal Power Plantand related transmission 96.2 165.5 261.7

Barge Moimted Power Plants 5.4 25.5 30.9

Technical Assistance:Engineering:

Besai Plant 5.1 16.7 21.8Banjarmasin Plant 4.7 8.5 1 3.2

Environmental Management 0.8 2.3 3.1Demana Management 0.4 1.8 2.2PLN's Environmental Group 0.4 1.2 1.6Pilot ProjectskPLN's Regions IV & VI) 0.6 2.1 2.7

Total Base Cost 154.1 326.6 480.7

Physical Contingency 19.7 36.1 55.8Price Contingency 17.3 31.3 48.6

Total Project Cost /a 191.1 394.0 585.1

Interest During Construction 40.4 63.4 103.8

Total Flnancing Required 31 1.4 !

La The local costs are :uclusive of taxes and duties estimated to be about US$51.1 millionequivalent.

- v -

Fnacing Plan: Local Foreign Total- (LJS$ mililon)

IBRD -Earlier Loans, a 1.5 4.8 6.3- Proposed Loan 6.9 253.6 260.5

Export Credits 15.5 76.5 92.0

Other Sources - 23.7 23.7

PLN 207.6 98.8 306.4

Total 231.5 M

lA Expenditures for preliminary engineering and design fmnareed under earlier loans for:a. Besai Hydroelectric Power Plant (US$ 3.3 million) under Loan 3602-INI)b. Banjarmasin Thermal Power Plant (US$ 3.0 million) under Loans 3501-IND

Estimated Disbursenent:

Bank FY 1995 1996 1997 1998 1999 2000

Annual 10.0 36.0 62.0 75.5 60.0 17.0Cumulative 10.0 46.0 108.0 183.5 243.5 260.5

Rate of Return: Besai Hydroelectric Power Plant - 14 percentBanjarmasin Thermal Power Plant - 15 percent

Poverty Category: Not Applicable

- v -

INDONESIA

SUMATERA .AND KALIMANTAN POWER PR-JECT

CONrENTSPage No.

1 THE ENERGY SECTOR ............................... I

Sector Overview ...................................... 1Energy and the Environment .............................. 1The Government's Objectives and Strategy ...................... 2Institutions in the Energy Sector ............................ 3

2 ELECTRIC OV ......POW............................ 5

The Electrcity Sector ................................... S

The Outer Islands ..................................... 7Electricity Consumption Forecasts ........................... 7Development and Investment Program ........ ................ sStrategic Sector Issues .................................. 9

3 THE BANK'S EXPERIENCE WITH PAST LENDING,AND STRATEGY IN THE POWER SECTOR ................. 1!

Experience with Past Lending .............................. 11Strategy in Support of Sector Policy Agenda ..................... 12- Private Sector Participation .. ................... 12- Restucturing PLN ................................... 13- Regulatory Reform ................................... 14- Adjusting Power Tariffs ................................ 16- Energy Efficiency and Environmental Protection ................. 16

4 THE BENEFICLARY .................................. 17

PLN's Orgamzation ................................... 17Institutional Change ...... : .............................. 17Staff Development and Training ............................ 18Accounting and Budgeting ................................ 19Billing and Collections ................ 19Audit and Internal Control ................ 19Insurance .......................................... 20

The report is based on the findings of an appraisal mission comprising Messws/Mme. Mihir Mitra,Sushffil hatnagar, Hernan Garcia, Arun Sanghvi, Judith Magyari and Subodh Matur (Consultant)who visited Indonesia in October/November 1993. Peer reviewers wore Messrs. Peter Cordukes,Anthony Sparkes and John Irving. Mrs. Marianne Hag, Director (EA3DR) and Mr. Peter R.Scherer, Division Chief (EA3IE) have endorsed the project.

- vi -

Page No.

5 THE PROJEOCT .................... 21

Background ........................................ 21Rationale for Bank Involvement ...... ...................... 22Project Objectives ..................................... 22Project Description .................................... 22The Sumatera and Kalimantan Power Project: Physical Components ..... 23- Besai Hydroelectric Power Plant .... I ...................... 23- Banjarmasin Thermal Power Plant .......................... 24- Mobile Power Plants .................................. 24- Tedhnical Assistance .............. 25Cost Estimate ........................................ 26Financing Plan . ...................................... 27- Procurement . ...................................... 28- Allocation of Loan Proceeds .............................. 30- Disbursements ..................................... 31Monitoring and Evaluation .............. ................. 31Supervision Arrangements ................................ 32

6 FINANCIAL ANALYSIS ................................ 33

Past Operating Results and Financial Position .................... 33Financial Objectives and Performance Monitoring ................. 34Present and Future Performance ............................ 35Tariffs . ............................................ 38Overall Development Fund ............................... 38Financing Policy .... ................................. 39Asset Revaluation ..................................... 40

7 PROJECT JUSIFICATION ...... ....................... 41

Demand Growth and Need for the Plants ....................... 41Least Cost Option ........... 42Plant Size and Timing Alternatives ........................... 42Internal Economic Rate of Return ...... ...... ............... 43Project Benefits. 44Project Risks .44

8 AGREEENTS REACHEI AND RECOMmENDATION .45

Agreements Reached with the Borrower .45Agreements Reached with PLN .46Condition of Effectiveness .47Recommendation .47

- vii .

ANNEXES

1.1 Indonesia - Sector Overview ............................. 491.2 Organization Chart of MME ............................. 522.1 Growth of Captive Power in Indonesia ....................... 532.2 Growth of PLN's Consumers and Sales ....................... 542.3 Electricity Consumption Forecasts and Assumptions ............... 552.4 Peak Load, Production and bnstalled Capacity: Java-Bali .... ....... 572.5 Peak Load, Producton and Installed Capacity: Outer Islands .... ..... 592.6 PLN's Investment Progran for Java-Bali System ................. 612.7 PLN's Investment Program for Outer Is!nds ................... 623.1 Power Subsector - List of IDA Credits and Bank Loans .... ........ 63a.2 Policy Statement (Goals and Policies for the Development of the

Electric Power Sub-Sector) ................. 644.1 Organization Chart of PLN .............................. 704.2 PLN: Performance Indicators ............................ 715.1 Besai Hydroelectric Power Plant - Design Features ............... 725.2 Hanjarwasin Thcrmal Power Plant - Design Features .............. 795.3 Environmental Assessment Summary - Besai Hydro Plant .... ....... 845.4 Summary Implementation Schedule - Besai Hydro Plant .... ........ 915.5 Procurement Schedule - Besai Hydro Plant .................... 945.6 Environmental Assessment Summary - Banjarmasin Thermal Plant ... ... 955.7 Summary Implementation Scheidiule - Banjarmasin Thermal Plant ... .... 1025.8 Procurement Schedule - Banjarmasin Thermal Plant ............... 1065.9 TOR - PLN's .-vironmental Management Capability .. . 1075.10 TOR - Demnn danagement .e..... .. ............... 1175.11 TOR - Pilot Projects for PLN's Regions IV and VI ....... ........ 1195.12 Cost Estimate - Besai Hydroelectric Power Plant ...... .. ......... 1215.13 Cost Estimate - Banjarmasin Thermal Power Plant ...... .. ........ 1235.14 Procurement Efficiency ................................ 1255.15 Disbursement Schedule .............. ................... 1275.16 Implementation Schedule for TA .......................... 1285.17 Supervision PI-is .......................... 1296.1 PLN's Financial Statements - Past Results and Forecasts ...... ...... 1316.2 Notes and Assumptions for the Financial Forecasts ..... .. ........ 1396.3 PLN's Tariff ................... .................... 1427.1 Forecast PLN Electricity Sales and Peak Load - Region IV .... ...... 1467.2 IERR Calculation ..... ............. .................. 1487.3 Internal Economic Rate of Return - Besai and Banjarmasin Plants ...... 1508.0 Selected Documents and Data in Project File ....... .. .......... 154

MAPS: 1 IBRD 25506 R2 IBRD 25507 R3 IBRD 25508 R

-1-

THE ENERGY SECTOR

1.1 l-donesia is endowed with large and diverse energy resources including crude oil,natural gas, coal, hydropower and geothermal. Oil has played a crucial role in the country'sdevelopment. In the early 1980s, oil's importance in the Indonesian economy peak.d as oilaccounted for 80 percent of the country's export earnings, and most of the government's rev;uuescame from oil. Following the collapse of oil prices in the first half of the 1980s, Indonesia initiateda series of fundamental reforms to restructure and diversify the economy by providing incentivesfor non-oil/LNG manufacturing and exports. While the oil and gas sectors continue to retai-, afundamental role in Indonesia's economy, with oilALNG exports of about US$10.5 billion in 1992,(about 30 percent of total exports), non-oil/LNG exports have now become the engine oIndonesia's external trade with about US$24.8 bHilion in 1992. A detailed overview of the energyresources is given in Annex 1.1.

1.2 Indonesia's domestic energy consumption has been growing rapidly. Overalldomestic net energy use has grown from about 166 milliec barrels of oil equivalent (boe) in 1985to about 263 million boe in 1992, a compound rate of 6.8 per cent per annum; with liquidpetroleum products accounting for about 78 percent of net energy consumed, and the share ofnatural gas at approximately 10 percent. Liquid petroleum product consumption is currentlyincreasing at about 13 percent annually, after having grown at an average annual rate of about 6percent from 1986 to 1989. During the 1980s, electricity consumption grew about 15 percentannually and gas sales grew about 9 percent annually.

1.3 A primary objective of the energy policy in Indonesia is to satisfy the rapidlygrowing demand for energy, while channeling liquid petroleum products for exports. TheGovernment is conscious of the need to conserve Indonesia's exportable surplus of crude oil andthereby slow Indonesia's transition to net oil importer status. This requires the efficient use ofenergy resources to be accomplished through appropriate pricing and other means, and thedevelopment of alternative energy resources that can economically substitute for domestic petroleumuse, such as coal, non-exportable gas, geothermal, and hydropower. The power sector is a majoruser of petroleuit fuels, especially in the Outer Islands (islands other than Java). Plans call forfurther reducing oil's share in power generation, from about 44 percent in 1991 ( about 33 millionbarrels of diesel and fuel oil), to about g percent by the end of this decade (10 million barrels peryear).

Energy and the Environment

1.4 The Environment Law in Indonesia (Law No. 4, 1982) provides that every projectlikely to have a significant impact on the environment must be accompanied by an environmentalImpact analysis (AMDAL). Pursuant to this law, the Ministry of Mines and Energy, in its Decree

- 2 -

1158 (1989), established uniform procedures and guidelines for preparation, submission andapproval of an environmental impact analysis, as well as subsequent and periodic reporting onenvirormental management and monitoring during the project implementation phase. In the powersubscr, Techni9al assistane.e was provided under Loan 3098-4ND (Paiton Thermal PowerProject) to train a number of staff of the Ministry of Mines and Energy on environmentalmanagement, and provide documentation for environmental guideiines and monitoring [para.1.7(f)]. A separate directorate (Bureau of Environment & Technology) has recently been set upto carry out the environmental management functions under a Director who also chairs the CentralCommission (AMDAL) for environmental clearances. Indonesia's emission standards are evenstricter in some respects th-n those of developed countries; for e-zample, the GOI standard forsulfur dioxide emission is 260 lglm3 only as opposed to the USEPA and Bank standard of 500,4gIm3 , while the nitrous oxide emission standard is 92.5 /Ag/m3 against the USEPA and Bankstandard of 100 ug/m3 . In order to monitor emission compliance, the Suraaya Thermial PowerProject (Loan 3501-IND) provides for the installation of receptors at strategic locations to monitorthe ground level concentrations of sulfurous and nitrous oxides, as well as of particulates, whenall seven units of the plant are placed into operation. The proposed project includes technicalassistance to both MME and PLN to further enhance their environmental management capabilides.

The Government's Objectives and Strategy

1.5 The energy sector is expected to continue to play a key role in the futuredevelopment of the economy. The GOI's main objectives for ttie sector are:

(a) the economic (ecficency) objective: to ensure efficient and reliable supply ofelectricity at least cost, while closing the gap between supply and demand, byconstructing new generating capacity and extending the transmission and distributionnetwork; to promote private sector participation to produce electricity and harnessthe capacity from captive power plants.

(b) the resource mobilizaion (fiscal and financial) objective: to maximize thecountry's foreign exchange earnings and budgetary revenues from the sector, mainlythrough the export of tradeable energy resources, including oil, gas and coal; to setpower tariffs at economic costs to enable producers of energy to recover their costsand obtain sufficient resources to finance their growth and development;

(c) the instutonal objective: to restructure the energy institutions and regulations inresponse to new challenges emanating from the reform of the sector, and to improvethe efficiency of the energy institutions, while enhan.,ing the quality of manpowerresources;

(d) the social (equality and fairness) objective: to promote a regionally balanceddevelopment of the country and to enable the majority of the people to afford thebasic services provided by electricity (lighting, cooking) at affordable rates toimprove their standard of living;

(e) the enionmental objective: to define and promote energy conservation measuresand environmental protection to promote the production ana utilization of energyresources in a manner that will ensure sustainable development and help conservethe environment for future generations.

- 3 -

1.6 In pursuing the above objectives, GO has relied on the following key policyimprovements:

(a) petroleum product prices: While several adjustments were made earlier, but sinceJanuary 1993, the GOI has maintained the average price of petroleum products atinternational parity, (efficiency pricing) while cross-subsidizing the price of kerosenewith an implicit tax on gasoline through the operation of the BBM (petroleumproducts) Fund (Annex 1.1). However, with the recent softening of crude oilprices, the domestic prices of petroleum products, including kerosene, are nowpegged above their economic cost.

(b) electicity tariff: The GOI maintains electricity rates at low levels for smallresidential, commercial and industrial consumers, who account for about 40 percentof PLN's sales. Periodic adjustments in the average sale price (the latest averageincrease of 13 percent, effective February 1, 1993) have generally maintained theaverage price close to the long-run marginal cost of supply in Java (para 6.15).

(c) private sector participation: The private sector operates significant captive powercapacity, and is expected to play an increasingly important role in the supply of gasand electricity. Independent power generation projects, which would supply powerto PLN's grids, totaling about 2,600 MW of capacity are expected to becommi&sioned over the next five years on a build, own and operate (BOO) basis(para. 2.11), of which about 500 MW -would be outside Java.

(d) protecting the poor: Historically, the GOI has subsidized the consumption ofelectricity by small residential, as well as small non-residential customers. The GOIhad maintained the price of kerosene below its econovaic cost, though this is nolonger the case [para 1.6 (a)I.

(e) regionally balanced development: The GOI has (i) maintained a uniform pricestructure for petroleum products and electricity in all parts of the country, and(ii) extended the supply of petroleum products and electricity in a balanced mannerto all parts of the country. These policies entail the subsidization of the higher costof energy supplies to the Outer Islands and to remote areas.

(t) environmental protection: In 1992, the Government created a Bureau ofEnvironment in the Ministry of Mines and Energy with permanent staff to supervisevarious environmental aspects in the energy and mining sectors. In addition, aseparate body in the Ministry of Mines and Energy, the Commission forEnvironment has the authority to review and approve Environmental Assessments,including their mitigation, management and monitoring plans, for all investmentprojects.

Institutions in the Energy Sector

1.7 The principal agency responsible for implementing Government policies in the energysector is the Ministry of Mines and Energy (MME). MME coordinates all activities in the energysector and supervises the state enterprises in the sector: Pertamina (oil, gas and geothermal),P.T. Bukit Asam (coal), PGN (gas distribution) and PLN (electricity). Other ministries and

-4-

agencies are also Involved in the sector; for example, the Ministry of Public Works, which isresponsible for hydropower resource surveys and the operation of multipurpose hydro plants, dheNational Atomic Energy Commission, which is responsible for nuclear development, andBAPPENAS, which provides sector planning and policy guidelines. An inter-ministerial NationalEnergy Board (BAKOREN) coordinates energy policies and development with those of othersectors. BAKOREN is supponed by a Technical Committee (PTE) consisting of senior officialsof different departments, chaired by the Director General of Electricity and Energy Development(DGEED). The organization chart of the MME is shown in Annex 1.2.

-5 -

2ELECTRIC POWER

The Electricity Sector

2.1 The Electricity Act (Law No. 15 of 1985) defines the legal framework for electricitysector. Under this Act, PLN, the State Electricity Corporation that was established by GovernmentRegulation No. 18/1972, has both the right and obligation to supply power in Indonesia. Theprovisions of the Electricity Act are amplified in Government Regulation No. 17/1990 for PLN,the State Electricity Corporation; and No. 10/1989 for others. The Electricity Act permitsestablishment of private power producers, distributors and licensees. Presidential Decree No.37/1992 specifically authorizes private sector participation under Build-Operate-Own (BOO)schemes, and allows cooperatives and other legal entities to generate, transmit, and distribute powerfor public use.

2.2 At present, the sector comprises: (i) PLN; (ii) captive plants installed by privateparties for their own use; (iii) three Government-sponsored rural electric cooperatives; and (iv) alarge number of informal microenterprises providing electricity to clusters of customers in ruralvillages not served by PLN. PLN accounts for about half of the electricity used by industries, andthe rest is provided by captive generation facilities. In 1992, the total installed captive generationcapacity was about 8,500 MD of which about 3,300 MD was reserve capacity that served as abackup to PLN supply (Table 2.1). Annex 2.1 shows the growth in captive plants in Indonesia.

2.3 Indonesia's power sector has grown rapidly during the 1980s and 1990s. PLN'sinstalled capacity increased five-fold from 2,288 MW in 1978 to 10,874 MW in 1992, as its salesgrew at an annual average rate of 16 percent from 4,287 GWh in 1978 to 34,964 GWh in 1992.A statistical profile of the power sector is presented in Table 2.1, while Annex 2.2 shows thegrowth in PLN's consumers, connected load, and energy sales. In spite of this rapid growth, thereis considerable unmet demand at economic prices. In 1992, PLN could serve only about 44percent of the urban households and 29 percent of the rural households, for an overall householdelectrification ratio of about 34 percent (Table 2.1), whereas at least 90 percent of the urbanhouseholds and two thirds of the rural households are estimated to be able to afford purchase ofelectricity.

2.4 The potential for future growth in electricity sales remains high in Indonesia.Residential energy sales are expected to increase as the household electrification ratio and incomesincrease, and industrial sales are expected to increase as the industrial sector GDP grows at anexpected rate of about 10 percent per annum for this decade (Annex 2.3).

-6 -

Table 2.1: POWER SECFOR PROFILE: JAVA-BALI AND TME OUTER ISLANDS (1992)

Indonesi Java-Bali O sShare (%) Share (%)

Population (million) 186 114 61 72 39

Power Subsector: PLNGeneration

- Number of Generating Units 3,369 293 9 3,076 91- Installed Capacity (MW) 10,874 7,630 70 3,242 30- Diesel Generator Capacity (MW) 2,062 115 5 1,947 95- Coal Consumption ('000 tons) 4,959 4617 93 342 7- Load Factor (%) 72.8 79.4 na 54.1 na

Length of Transmission Lines (kmc)< = 30 kV 1,856 1,621 87 235 13

70 kV 4,366 3,631 83 734 17150 kV 10,255 7>273 70 2,982 30500 kV 1,189 1,189 100 0 0

Total Consumers (millions) 13.4 8.9 66 4.5 34

Household electrification ratio (%) 34 38 na 27 na

Energy Sales (CWh) 35.0 27.8 80 7.1 20- Residential 11.7 8.6 73 3.1 27- Industrial 17.8 15.1 84 2.7 16

Employee Productivity- Consumers per employee 242 na na- MWh sold per employee 627 na na

Power Subsector: Captive Power

Installed Capacity (MW) 8,548 3,914 46 4,634 54- Connected to PLN La 3,405 2,532 74 873 26

La Reserve capacity that serves as a backup to PLN supply.na: not applicable.

Source: PLN; Statisdcal Yearbook.

-7 -

The Outer Islands

2.5 The Outer Islands comprise all of Indonesia's islands except iava,.j includingSumatera (population: 34 million), Sulawesi (population: 12.5 million), Kalimantan (population:9 million), and some 3,000 smaller inhabited islands of Indonesia. The Outer Islands constituteapproximately 95 percent of Indonesia's land mass, with approximately 40 percent of the country'spopulation, while accounting for only about 20 percent of PLN's sales and about 30 percent ofPLN's installed capacity. The household electrification level in the Outer Islands is about 27percent (1992), compared to about 38 percent in Java-Bali. At the same time, residential salesconstitute about 47 percent of PLN's sales in the Outer Islands, but only 31 percent in Java-Bali.Further, PLN's average energy sales per customer in the Outer Islands is about half the Java-Baliaverage.

2.6 The operational characteristics of the power supply systems in Outer Islands aredifferent from those in Java-Bali. The Java-Bali grid is an extensive interconnected system witha number of large, central generating plants, a relatively high load factor, and high capacity (500kV) transmission lines. In contrast, except for a few small grid systems based on low capacity(150 kV or lower) transmission lines, PLN's operations in the Outer Islands depend upon a largenumber of small, isolated diesel generators, with a lower load factor than in Java-Bali. Most ofPLN's electricity sales within the Outer Islands are concentrated within the urban areas of theterritories. Further, the share of captive power in total installed capacity is significantly higher inthe Outer Islands than in Java-Bali (Table 2.1).

2.7 PLN's operations in the Outer Islands are organized into 11 geographical Regions.The proposed Besai hydroelectric plant (para 5.3) would be located in Region IV (southernSumatera), which is the second largest of PLN's Outer Islands Regions in terms of energysales,Z/ and the proposed Banjarmasin thermal plant (para 5.4) would be located in Region VI(southern Kalimantan), which is the third largest of PLN's Regions.

Electricity Consumption Forecasts

2.8 The electricity consumption forecasts, along with the key underlying assumptions,for Java-Bali and the Outer Islands are presented in Annex 2.3. The average annual growth rateof sales over 1991-2003 is projected to be around 12 percent, including PLN sales as well ascaptive power self-consumption, for both Java-Bali and the Outer Islands. The industrial andresidential sectors account for the bulk of the growth in sales for both the Java-Bali system and theOuter Islands.

2.9 PLN's sates forecasts. The forecasts show that PLN's energy sales, including powerpurchased from private producers (para 2.11), are expected to grow at annual average rates in therange of 12-14 percent per year over 1991-2003, with the growth rate in the Outer Islands higherthan in Java-Bali. PLN's share in total electricity consumption is projected to increase slightlyfrom 76 percent (1992) to 81 percent (2003) for Java-Bali, and from 32 percent to 36 percent forthe Outer Islands over the same period. A substantial part of the increase in PLN's sales isexpected to come from additional sales to industrial consumers, with the share of industrial

1/ Bali is served by the interconnected Java-Bali grid.

2/ The largest is Region 1I (North Sumatera).

- 8 -

consumers in PLN's sales rising from 54 percent (1992) to 56 percent (2003) for Java-Bali, andfrom 37 percent to 49 percent for the Outer Islands over the same period.

Development and Investment Program

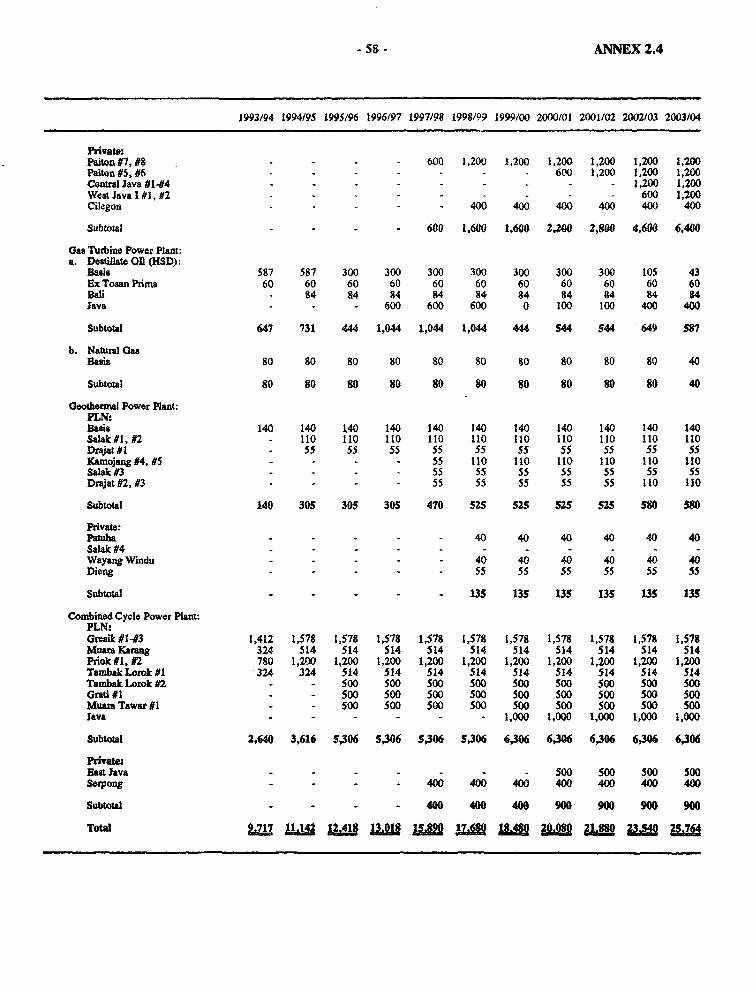

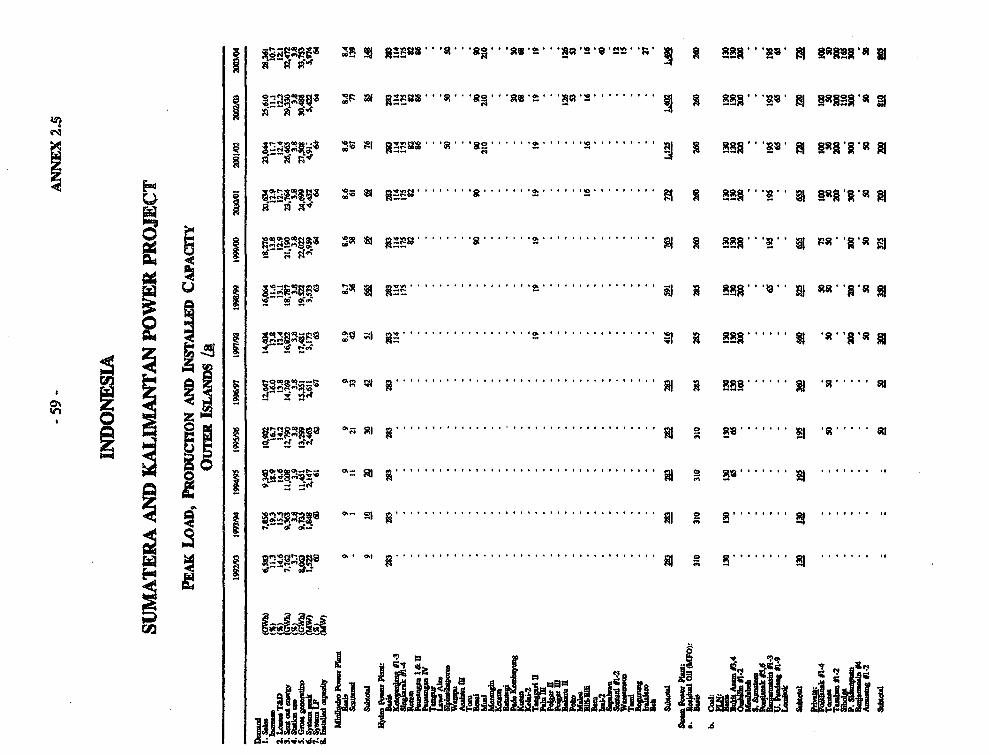

2.10 The development program to meet the projected increase in PLN's sales takesaccount of the expected participation by private generators. Annexes 2.4 and 2.5 siummarize theprogram's generation expansion component for the Java-Bali system and for the Outer Islands asa whole up to the year 2003.

2.11 Private Sector Participation. The power sector has already been opened to privatesector participation, beyond captive power generation. In a major change from the past, the privatesector is expected to supply power to PLN's grid systems, and the Government has earmarkedseveral generating projects for independent power producers on a Build, Own, and Operate (BOO)basis. In this context, PLN has very recently signed a power purchase agreement with a privateproducer to supply 2 x 600 MW of power at PLN's Paiton thermal power station site in East Java,and the GOI is actively seeking private sector participation in the construction of two additionalunits of 600 MW each at Paiton. Further, a private promoter, Cikarang Listrindo, has installed76 MW of open cycle capacity (2 x 38 MW) to sell electricity to consumers located in fiveindustrial estates in the vicinity of Bekasi, West Java. This plant is also connected to PLN's 150kV network, and supplies a limited amount of power to PLN.

2.12 Overall, the private sector is expected to play a significant role in the developmentprogram to meet PLN's projected sales. This program envisages that, over 1994-1998, privatesector participants will account for about 27 percent of the net capacity addition of about 8,000MW for the Java-Bali grid, and about 18 percent of the net capacity addition of about 2,700 MWin the Outer Islands. Private sector investments in generation facilities that will sell power to PLNare estimated to be about US$3.8 billion over REPELrrA VI (1994-1998), of which about US$2.9billion wi}l be in Java-Bali, and about US$0.9 billion outside Java, while PLN's investments areexpected to be about US$17.4 billion (para 2.14). These investments include initial expendituresfor plants that will be commissioned after REPELITA VI.

2.13 In addition to grid based generating capacity, the private sector will also installadditional captive power plants, based on its own needs. Captive plant owners are expected tocontinue to produce significant amounts of power for their own use. In 1992, captive powerowners produced about 23 of the electricity consumption in Java-Bali, and about 65 percent of theelectricity consumption in the Outer Islands; by 2003, these shares are projected to decreaseslightly to about 18 percent in Java-Bali and to 63 percent in the Outer Islands (Annex 2.3).

2.14 PLN. PLN's expansion of its operations to meet the additional future load, aftertaking account of expected private sector participation, is constrained by the financial resourcesavailable to it. The outer envelope of financing available to PLN for REPELITA VI from allsources-Government contributions, self-financing, and borrowings-has been estimated at aboutRp. 50 trillion (US$17.4 billion in constant 1993 prices). PLN has prepared a core plan consistentwith this resource mobilization constraint (Table 2.2). After accounting for the estimated privatesector participation, PLN will continue to be responsible for the bulk of the investment in thepower sector. Annexes 2.6 and 2.7 provide estimates of PLN's annual requirements of investmentsup to year 2003, expressed in constant 1993 US dollar equivalent, for the Java-Bali system and theOuter Islands, respectively.

9-

Table 2.2: PLN's INVEsrMENr REQUIREMTS: REPExrA VI (1994-1998)

Local Foreign TotalCosts Costs Costs

- billions of US$ equivalent constant 1993 prices ---Java-Bali Grid 2.29 9.11 11.40

Outer Islands 1.60 4.16 5.96

Total 3.89 37.36

Source: PLN Core Plan, December 1993.

2.15 PLN's generation expansion plans are derived from least-cost planning models. Forthe Java-Bali grid, about 70 percent of the planned gross generation expansion over 1994-2003 isbased on coal, while the expansion plan for the Outer Islands calls for a substantial reduction inthe share of diesel-based generation of (from 68 percent in 1992 to 26 percent by 2003), withincreases in the shares of coal, hydro, geothermal, and natural gas.

Strategic Sector Issues

2.16 The challenge. After two decades of rapid growth in electricity production,Indonesia's power sector is now at a crossroads. Maintaining past rates of growth and improvingfurther the efficiency of operations and quality of service will require structural changes in orderto mobilize financing and manage operations effectively. The time has come for fundamentalchanges, amounting to a major reform of Indonesia's power sector. Several key issues have to beaddressed in a coordinated manner in order to bring about these changes.

2.17 Private sector participation. The 001 has concluded that private sectorparticipation is a pre-requisite for reducing the financial burden on the GOI as well as increasingthe efficiency of electricity production. While the GOI has already earmarked several generationprojects for private investors, and the power sector's development program is predicated upon theirparticipation, (para. 2.12), major policy and institutional changes are needed to encourage privateinvestments.

2.18 PLN's performance. While PLN has been steadily improving its operations, andhas successfully constructed and operated the Java-Bali grid, PLN's performance does not yet meetbest utility practices. Since piece-meal, incremental changes would not any longer allow PLN togo beyond marginal improvements, structurl changes are needed to further improve PLN'sperformance. Efficiency improvements are particularly needed in the Outer Islands, wheremanagement constraints have impeded progress. Several policy and institutional changes have tobe made to facilitate the development in the Outer Islands of interconnected grids, based on largegenerating plants, to replace the small, isolated uneconomical diesel-based generating units.

- 10-

2.19 Sectoral development and regulation. With the emergence of a significant role forthe private sector, a new sectoral agency would be required to regulate both PLN and the privateoperators. There would also be a need for a central agency to jointly optimize PLN's and privateinvestors' development strategies, based on least-cost considerations.

2.20 Power tariffs. The present ad hoc tariff setting modalities will not be appropriatein the future. The mechanism for setting power tariffs should allow PLN to deal effectively withthe private sector, and to be able to maintain its financial health in an increasingly competitiveenvironment.

3THE BANK'S EXPERIENCE WITH PAST LENDING,

AND STRATEGY IN THE POWER SECTOR

Experience with Past Lending

3.1 Overview. The Bank group has played a very active role in the development of thepower sector in Indonesia. Since 1969, it has provided about $4.1 billion for the power sector,through three IDA Credits, 18 loans and one supplemental loan. The primary focus of the Bank'sactivities was the Java-Bali grid, although some of the projects had nation-wide benefits. A list ofpast lending operationrL is provided in Annex 3.1. Project Performance Audit Reports (PPARs) andProject Completion Reports (PCRs) on the first 14 projects have concluded that the Bank has madepositive contributions towards the development of the Indonesian power sector over the past 20years by improving PLN's project implementation, operational and managerial capabilities andhelping Indonesia meet critical demands for electricity. These reports attribute the success ofpower operations in Indonesia to the facts that: (i) there was a long-term vision for thedevelopment of the sector and this vision was shared by the Bank, Govermment and PLN; (ii) thevision was translated into a long-term strategy which was resolutely pursued, and (iii) a reasonablebalance was struck between the physical and the institutional development components of theprojects.

3.2 Power Facilities. The infrastructure components of the Bank-supported projectshelped PLN expand its generation capacity of thermal, hydroelectric and geothermal power plants,and associated transmission and distribution facilities. These projects also supported theGovernment's objective of diversifying domestic energy consumption away from oil by the use ofcoal, hydropower and geothermal. At the beginning of this decade, PLN's installed capacity hadgrown to more than 10 times what it was at the beginning of the 1970s, and to more than 2.5 timeswhat it was at the beginning of the 1980s; Bank-financed projects have accounted for 3,800 MWof the approximately 7,600 MW of generating capacity operating in Java in 1992/93.

3.3 Institutional Development. Bank operations have consistently focused on institutionbuilding. During its association with the Bank, PLN has substantially improved its projectimplementation, operational and managerial performance. PLN has made significant progress inimproving the efficiency of its operations. In particular, over the period 1983/841992/93, PLN'stransmission and distribution losses have decreased from 21 percent to 12 percent; annual energysales per employee have increased from 223 MWh to 627 MWh; and overall consumers' accountsreceivable have decreased from 68 to 36 days' sales (Annex 4.2). Technical Assistance has alsobeen provided, inter alia, to strengthen PLN's corporate and financial planning and accountingfunctions.

- 12 -

3.4 Fnancal Performance. Bank operations have also focused on PLN's financialperformance. In view of PLN's negative rate of return (ROR) at that time, a ROR covenant wasadopted under the Fourteenth Power Project Loan (Loan 2443-IND) in 1984. This covenant wasmodified in 1987 under the Power Transmission and Distribution Project (Loan 2778-IND) toprovide for separate financial performance targets for PLN's operations in Java (ROR of no lessthan 8 percent) and outside Java (to breakeven), in view of their different operationalcharacteristics. Initially, the government did not permit the necessary tariff increases, with theresult that the Bank did not approve further loans in 1987 and 1988, although project preparationcontinued. The Government increased tariffs in 1989, 1991, and most recently, effective February1, 1993. PLN's operations in Java-Bali are largely profitable, but PLN makes a loss on itsoperations in the Outer Islands (paras. 6.2-6.3).

3.5 Implementation Problems. The main problems experienced with theimplementation of power projects in Indonesia have been: (i) delays in the selection andappointment of consultants, procurement of goods and works, acquisition of land and the right-of-way for the construction of transmission and distribution facilities, and (ii) difficulties encounteredin effective absorption of Technical Assistance. Generally, rigid budgetary procedures, outdatedconsultant fee schedules, delays in finalizing contracts with winning bidders, unsatisfactoryperformance of lo. d contractors, and shortage of trained personnel within PLN, have delayed theimplementation of pievious projects. These problems are germane to the implemenion of most,and not just power, projects in Indonesia, and the Government is devising plans to address theseproblems, based on the recent performance review of the projects in the Bank's portfolio.

Strategy in Support of Sector Policy Agenda

3.6 Dialogue with Government. Based on the dialogue between the Bank and 001, aconsensus has emerged that fundamental policy changes are needed for efficient long-rundevelopment of the power sector in Indonesia. The Government has expressed its strategy in aPolicy Statement, "Goals and Policies for the Development of the Electric Power Subsector,*(Annex 3.2) and has stated its intentions to implement it. The Bank intends to support this strategythrough the proposed project as well as the future Rural Electrification H (scheduled for Boardpresentation in the next fiscal year), Sumatera Power Project, and Renewable Energy projects. Thekey elements of the Bank's support are described below.

3.7 Policy Framework. The power sector development agenda has four major aspects:(i) expanding entry to the sector to increase the participation of private investors and operators; (ii)corporatizing and restructuring PLN to improve the efficiency of its operations; (iii) reformingregulatory and sectoral development functions; and (iv) strengthening sector finance throughperiodic power tariff adjustments. Taken together, these policy changes should lead to an increasedrole for the private sector, while restructuring and reorganizing PLN with an ultimate intention ofdivestiture in the future, with the social and public interests safeguarded by an appropriateregulatory agency.

3.8 Private Sector Participation. The Government expects the private sector to playa significant role in satisfying Indonesia's electricity needs in the future (paras. 2.11-2.13). Toachieve this goal, there is a need to expand the options for private sector participation beyond BOOschemes, e.g., purchase of electricity on the basis of competitive bidding, unsolicited proposals,licensing private generation in industil estates and franchising geographical areas to licensees forthe generation andlor distribution of electricity, and transmission access. However, private sector

- 13 -

participation, at present, is constrained by the lack of a transparent, comprehensive and consistentregulatory framework that defines the rules for, and facilitates the operation of private powerenterprises. Some steps towards addressing this constraint have already been completed. First,the Government has established a Directorate of Private Power under DGEED in the Ministry ofMines and Energy. Second, the Governmenit is following-up on the findings of a study by twointernational consulting firms, sponsored by the Bank with financing from the NorwegianConsultant Trust Fund, which addressed, inter alia, structural changes to promote an increasedprivate sector role. (para. 3.16).

3.9 As a follow-up, the GOI is initiating an action-oriented study ("Private PowerDevelopment Study"), with the assistance of experienced consultants to be financed by the Bank,under the Infrastructure Technical Assistance Project (Loan No. 3385-IND), to develop acomprehensive Private Power Program. The TOR for this study have been finalized, and theconsultants are expected to complete their work by March 1995. The TOR call for the consultantsto: (i) assess the current incentives for private sector participation; (ii) evaluate alternative optionsfor private sector participation; (iii) identify changes in sector organization that would encourageprivate investors; (iv) review all existing laws and regulations related to the power sector, andrecommend modifications as well as additional regulations; (v) recommend a financing frameworkfor private power projects to expedite the project negotiation process; and (vi) recommend a PrivatePower Program, including all activities required to implement it, such as development of guidingpolicies and detailed rules, institutional adjustments, staffing, project identification anddevelopment.

3.10 During negotiadons for the proposed loan, an agreewent was reached with theGovernment that it will: (a) undertake and, by March 31, 1995, complete a study on private powerdevelcpment in accordance with terns of reference and in a manner satisfactory to the Bank,(b) upon completion of the said study, furnsh the same for review and comments to, and discussthe results and recommendations thereof with, the Bank, and (c) based on the said stu4's resulsand recommendations and subsequent review, comments and discussions: (1) prepare draft rudesand procedures to govern private sector participation including the solicitation and evaluation ofallforms ofproposalsfor private power supply, f i) furnish the said draft rules and procedures forreview and comments to the Bank, and Riii) by December 31, 1995, finalize, adopt and enforce thesame takiig into account the comments, if any, thereon by the Bank.

3.11 As a precursor to the Private Power Program, the GOI is planning to develop bulkpower purchase and supply tariffs, and is engaged in a dialogue with the Bank on this issue.Concrete actions on these tariffs will be part of the Bank's next power sector lending operation(Rural Electrification IT), and the GOI has also expressed its intention to develop a transmissionaccess procedures and tariff. Bulk purchase power tariffs, pegged to PLN's avoided costs, willencourage efficient private sector levels and modes of participation in electricity generation bysmall producers; the rates for large independent producers would continue to be set by negotiationsin a competitive environment. Similarly, a bulk power supply tariff, based on PLN's economiccost of supply, will encourage efficient private sector participation in distribution. Further, a"transmission service tariff would permit independent producers to sell power direcdy toconsumers by "wheeling" power from their generating facilities to the consumers, and paying PLNa fee for utilizing its transmission network.

3.12 Restructuring PLN. The GOI's strategy for restructuring PLN has two inter-relatedaspects: (i) decentralization and commercialization, and (ii) corporatization. To improve its

- 14 -

financial performance as well as the quality and efficiency of service, PLN has already initiated areorganization of its structure and management system, based on a plan developed with theassistance of consultants under Bank financing. To assist in the ongoing reorganization of PLN,and to further develop a detailed action plan for restructuring PLN ("PLN Restructuring Plan"),an international consulting firm, financed as part of Technical Assistance under the SuralayaThermal Power Project (Loan 3501-IND) has begun work, which is expected to be completed byDecember 1994.

3.13 The TOR for the PLN Restructuring Plan call for the consultants to: (i) helpimplement a decentralized and commercialized organization structure and management system,including the establishment of profit centers along functional (generation, transmission, anddistribution) and geographical lines, with the managers of these profit centers given enhanceddecision-making responsibilities and made accountable for their performance; (ii) identify andevaluate options for contracting out functions currently performed in-house by PLN; and (iii)establish performance benchwarks for evaluating the performance of various PLN units, such asPLN's Regions in the Outer Islands, and develop performance contracts and the incentivesframework for the managers of these units. To complement this activity, the proposed projectprovides for Technical Assistance for PLN to set up pilot projects in PLN's Regions IV and VI todemonstrate the feasibility of commercially oriented operations in the Outer Islands (para. 5.19).

3.14 Another key element of the GOI's strategy in restructuring PLN is a change in itscorporate status from a State-owned agency with a social purpose (Perum) to a group of profit-oriented limited liability companies (Perseros), with private participation in their ownership as soonas their financial performance permits. During negotiations for the proposed loan, an agreementwas reached that the Government shalljointly with PLN: (a) take the necessary measures requiredto reorganize PLNV into a limited liability company (Persr; (b) by December 31, 1994, furnishto the Bank a progress report concerning the reorganization of PLNV together with a draft iebound corporate reorganization and restructuring action planfor PLNto operate according to bestutility practices; (c) discuss the said progress report and draft action plan with the Bank; and(d) immediately thereafter, finalize the said action plan taking into account the comments, if any,thereon by the Bank.

3.15 As an initial step, the Government intends to convert PLN to a Persero with aprovisional balance sheet and the current organization structure. The conversion of PLN's statusto a Persero would require a re-definition of PLN's capital structure and financial operating regime,including the valuation of its assets. Over time, the GOI intends that the group of companieswould compete in a market-oriented environment, with Government exercising strategic controlover them on an "arm's length" basis through performance contracts that specify clear objectivesand efficiency indicators. During negotiations for the proposed loan, an understanding wasreached with the Government that it will appoint, by December31, 1994, an internationally reputedaccounting and management flm to provde advice and assistance on financial issues, includingthe valuation of PLVs assets, related to the conversion of PLN's status to a Persero.

3.16 Regulatory Reform. A Bank sponsored study, with financing from the NorwegianConsultant Trust Fund, has identified the broad elementts of regulatory reform needed in view ofthe evolution of the power sector. An initial step towards the establishment of a sectoral regulatoryoversight agency will be the separation of those functions that relate to the power industry'sregulation and oversight from the functions that relate to power sector policy and planning. To this

- 15 -

end, the Government intends to initially establish a Directorate of Regulation within DGEED, witha view to this later being converted to a higher level agency with greater autonomy and authority.

3.17 In order to identify and define further specific changes needed, the Ministrv of Minesand Energy will undertake a major review, with the assistnce of consultants to be financed by theBank as Technical Assistance under the Cirata Hydroelectric Phase II Project (Loan 3602-IND),of the power sector's current organization and legal and regulatory framework, with the aim offormulating and implementing fresh regulations and strengthening the Directorate of Regulation("Regulatory Reform Study"). The TOR for this study have already been finalized, and theconsultants are expected to complete their work by Ma%ch 1995, in conjunction with the PrivatePower Development Study (para. 3.9). The TOR for the Regulatory Reform study call for theconsultants to: (i) formulate draft by-laws, regulations, and/or decrees necessary to reform theregulatory framework, including (a) the definition and separation of the responsibilities of theassociated government administrative units, and of the publicly-owned and private enterprises, and(b) the structure and staffing needs of an electricity regulatory body; and (ii) a phased action planto progressively implement the proposed reforms.

3.18 During negotiations for the proposed loan, an agreement was reacned with theGovernment that it will: (a) undertake and, by March 31, 1995, complete a study on regulatoryreform in the power sector in accordance with terms of reference and in a manner satisfactory tothe Bank, (b) upon completion of the said study, furnish the samefor review and comments to, anddiscuss the results and recommendations thereof with, the Bank; and fc) based on the said study'sresults and recommendanons and subsequent review, comments and discussons: (O) prepare draftregulations for the power sector, Qii) furn sh the said draft regulations for review and comments tothe Bank, and fiii) by June 30, 1996, finalize, adopt and enforce the same taking into account thecomments, if any, thereon by the Bank.

3.19 Sectoral Development. Effective management of increased private sectorparticipation will require a transfer of responsibility for power sector development to a centralagency in the MME, which would ensure that the demand for electricity is met in jointly optimizedleast-ost manner, taking account of the roles of both PLN and private investors. The centralagency would project the future demand for electricity, and determine the most effective mode ofmeeting the demand, based on an assessment of private sector participation under the prevailingsystem of rules and incentives, and of PLN's resource availability and hnplementation capabilities.This would help to ensure that the iming, size and location of aU large generation plants, includingthose of PLN and private promoters, are part of an overall least-cost generation expansion plan.The Government intends to upgrade DGEED's capacities in the areas of demand forecasting andleast-cost system expansion planning. In this context, PLN is planning to formulate rollingcontingency plans to respond to any supply/demand imbalance due to changes in the anticipatedschedule of private sector participation.

3.20 During negotiations for the proposed loan an agreement was reached with theGovernment that to ensure comitinued soundness of the power sector development program, GOIwill: (a) by December 31 each year, commencing in 1994: O7) review with the Bank. (1) its powersector development program, (2) the least cost planning analysis used to formulate the saidprogram, (3) the roles of PL Wand the private sector in the said program, anu' (4) the transparencyand appropriateness of the busness environment for private power partipatw(n, (i) reviw withthe Bank and PLN, PUW's development and investnent programs with respect to: (1) theirconsistency with GOI's power sector development progran, (2) the balance among generation,

-16-

transmission and distribution investnents, and (3) the balanced development of regions; and(b) ensure that PLN has access to sufficient funds to finance its development and investmentprograms.

3.21 Adjusting Power Tariffs. The Bank supports the importance that the GOI attachesto the pricing of electricity so that there is efficiency in consumption and PLN's financial healthis ensured. The GOI intends to raise power tariffs as needed to ensure that PLN will attain thestipulated rate of return in its operations (para. 6.10). As PLN's purchases of power fromindependent power producers increase, it will become increasingly important that PLN's tariffsadjust in response to changes in purchased power prices. The GOI intends to develop proceduresfor periodic, formula-based adjustments to PLN's tariffs to take account of variations in fuel andpurchase power prices, exchange rate, and inflation. A detailed study on the issue of electricitytariff has already been concluded by PLN with the help of a TA provided under an ADB loan. TheGOI is now considering the modalities of institutionalizing such adjustments (para. 6.11).

3.22 Energy Efrciency. The GOI uses efficiency pricing, complemented by otherappropriate measures, to encourage and induce sound electricity use decisions. In the powersector, the GOI is focusing on more efficient utilization of electricity, introduction of renewableenergy in the rural areas, and demand management (DSM). The proposed project provides fortechnical assistance for PLN to promote DSM (para. 5.19). This TA will assist PLN in: (i)developing a rationalized strategy for DSM and the corresponding action plan, based upon data andconditions specific to Indonesia, (ii) establishing realistic targets of penetration and savings to beachieved, (iii) deternining efficient delivery and incentive mechanisms, and (iv) formulating thefinancing plan for DSM.

3.23 Environmental Protection. The GOI recognizes that safeguarding the environmentis a prerequisite for sustainable development and encouraging conservation and diversification inthe use of energy resources will reduce any possible adverse environmental impacts of energyconsumption. The Bank will continue its support to efforts developed by the Government to putin place the regulatory framework and institutions needed to achieve this. The proposed projectprovides for technical assistance for PLN to improve their environmental management capabilities,and introduce demand management (para. 5.19). This TA will assist PLN in developing itscapabilities to formulate corporate environmental policies, evaluate environmental assessments ofits development projects, and monitor enviromnental impact, and compliance with environmentalguidelines for existing projects. During project supervision, the Bank wiUl pay special attention andresources to ensuring that the environmental protection regulations are implemented as intended.Within the power sector, Bank project preparaion and supervision will be focused on carefulplanning and design of new facilities so as to minimize and mitigate their impacts on theenvironment and affected population, and on effective monitoring designed to ensure propercompliance with applicable standards and practices.

- 17 -

4THE BENEFICIY

4.1 The proposed loan would be made to the Government of Indonesia (GOI). Theproceeds of the proposed loan, except for a part for technical assistance to GOI frc improving theenviromnental management capability of the Bureau of Environment and Technology under theMinistry of Mines and Energy, would be orlent to PLN (para. 5.24), which is responsible for theimplementation of the proposed project. PLN, the sole government-owned national power utility,has been the beneficiary of Bank Group lending to the power sector in Indonesia since 1969(para. 3.1).

PLNs Organization

4.2 PLN was established as a public corporation (Perum) under a Presidential Decreeof 1972, that confers upon it the responsibility and obligation to manage Indonesia's power system,Including the generation, transmission and distribution of electricity, and the planning, constructionand operation of electricity supply facilities (para. 2.1). At present, PLN operates in a centralized,hierarchical manner, with PLN's Board of Directors having both managerial and supervisoryresponsibilities. PLN's organization chart is shown in Annex 4.1.

4.3 For the Java-Bali system, the operational responsibility rests with the managers oftwo generation ani transmission, four distribution centers and the Java-Bali load dispatch center.Major construction is the responsibility of a number of project managers. For the Outer Islands,the operational responsibility rests with the managers of PLN's eleven operating regions and thespecial region of Batam island. Under the Regional Manager, there are four primary departmentswith Deputy Managers in charge of Operations, Construction, Finance, and Administration. EachRegion has a number of branches and sub-branches. The branch manager is responsible for serviceat the customer level, and reports directly to the Regional Manager. A Region may have one ormore generatilg Sectors, depending upon the scale of operations. At present, only Region IV hasa Load Dispatch Uotter. The Construction Divisions in the Regions have responsibility for onlyfor distribution lines anm small generation facilities (under 1 MW), with major construction beingthe responsibility of PLN headquarters.

Jusfitutional Change

4.4 PLN's managing and operating capabilities have increased along with energy sales;it has effectively managed a large investment program, and constructed and operated large coal-fired plants in Java-Bali. However, PLN has reached the limits of its effectiveness under thepresent organizational structure, and a detailed plan for restructring PLN is now being developed(para. 3.12).

- 18 -

4.5 Under centralized control, the Managers of PLN's Regions in the Outer Islands havelimited planning and operational flexibility and discretion; correspondingly, their accountability foroperational efficiency is also limited. As a result, the Managers have little incentives oropportunities to initiate steps to i;hlprove the quality and level of service and/or reduce costs byintroducing efficiency measures. Most of the financial planning is also done at PLN headquarters,though the preparation and submission of the annual budget to headquarters is time-consuming.Further, the staff in the Regions spend a significant part of their time preparing reports to betransmitted to PLN's headquarters, without a clear sense of purpose or use of this information.

4.6 A major operational problem in the Outer Islands is the lack of proper maintenanceof generation facilities. This problem is particularly acute for the isolated diesel-based generationunits, which are comprised of a myriad of makes and vintage. Second, the Regions in the OuterIslands face a shortage of qualified staff in most aspec of their operations, and the training levelsare inadequate. There is also a shortage of computers and computer skills. Further, there is oftena mismatch between skills and responsibilities, such as mechanical engineers working in thedistribution department while electrical engineers work in the planning department. Third, someof the Regions in the Outer Islands have significant captive power capacity that is notinterconnected to PLN's grids, though such interconnections have the potential of lowering PLN'sreserve requirements and improving the reliability of supply.

4.7 These, and other related issues, in the development of the power sector in the OuterIslands point towards the need for institutional changes in PLN. The proposed project includesTechnical Assistance to undertake pilot projects in PLN's Regions IV and VI for this purpose(para. 5.19).

Staff Development and Training

4.8 As of March 31, 1993, PLN had 55,737 employees, of whom 45,294 are permanentstaff. PLN had no difficulty in recruiting staff educated at levels up to technical high school, butfaces constraints in recruiting those with higher academic qualifications; the problem is particularlyacute in the Outer Islands. Overall, as well as in Regions IV and VI, less than 5 percent of its staffhave university degrees. To address its training needs, PLN has a separate training department thatplays an important role in PLN's efforts to upgrade the skills of its technical and administrativestaff. These efforts have been largely successfid. In 1992, about 8,000 staff receivedtraining-about 7,800 in the country and about 200 abroad.

4.9 The Bank has supported PLN's training activities and human resources developmentefforts, including the establishment of several training centers. The computer-based training centerat Suralaya has trained many of PLN's power plant staff in the operation and maintenance ofthermal power stations with significant success; the performance record of Suralaya Thermal PowerPlant compares favorably with any power station of comparative size in the industrialized world.Current efforts being supported by the Bank include training in the areas of diesel/thermal plantoperations, distribution management, corporate and financial planning, general accounting and cashmanagement, as well as specific training activities in the rural electrification area and in publicutility practices.

- 19 -

Accounting and Budgeting

4.10 PLN's accounting system, installed in the early 1970s, follows generally acceptedaccounting principles, and normal utility practices, but it needs upgrading to keep pace with thegrowing complexity and volume of accounting transactions. The accounting system needs toproduce more accurate information in a timely manner for decision-making purposes. Also, PLN'sinternal procedures for preparing budgets and monitoring actual expenditures need to bestrengthened through better coordination among and participation by the various functionaldirectorates and regional offices in the process, to enhance the budget's value as a managementtool.

4.11 A major constraint to PLN's accounting has been a lack of trained senior accountantsand uniform application of accounting procedures, and the problem is acute in the Outer Islands.Since 1987, PLN has been implementing an action plan to improve its accounting practices andfunctions. PLN is also attempting to improve coordination between its departments and its regionaloffices in the areas of budget preparation, and monitoring and evaluation of performance.Technical assistance is provided under the Power Sector Efficiency Project (Loan 3097-IND) toimprove the accounting system, The Rural Electrification Project (Loan 3180-IND) providestechnical assistance to continue to enhance the system for the segregation of PLN's accounting ofits RE operations.

Billing and Collections

4.12 PLN's bills are computerized and prepared monthly at the Jakarta headquarters; forthe Outer Islands, the bills are prepared at the branch level, and printed by the Region's FinanceDivision. Overall collection performance is generally satisfactory. The receivables position ofgeneral consumer accounts has been good, as it has been kept below one and one-half months ofthe yearly billing. The overdues from government users (including the Armed Forces and localgovernments), which account for about 10 percent of PLN's total sales, have also been maintainedto under two months' billing.

Audit and Internal Control

4.13 PLN's accounts are required by its charter to be audited by Government auditors.The audits are carried out following generally accepted accounting practices and standards. In theaudit reports for 1989 through 1992 there were no qualifications. As a result of joint efforts byPLN and its auditors, the time required for completing PLN's audits has been reduced significantlyover the last three years. For 1992, the accounts were finalized within three months after theclosing of the fiscal year and the audited accounts were available within four months of the closeof the fiscal year. The audit covenant under Loan 3602-IND, that requires PLN to submit to theBank its audited financial statements and the report of s!fch audits no later than six months afterthe end of eachfiscal year, was also agreed under the proposed project. In addition, PLN wouldfurnish to the Bank (1) a copy of its unaudited annual accounts whenever they are sent to theauditors; and (ii) its segregated financial and operating information on rural activities within sixmonths after the end of each fiscal year.

4.14 The Bank is discussing with Government and PLN the desirability of having PLN'saccounts audited by internationally reputed commercial accounting firms, independently ofGovernment auditors. Such commercial audits would not only ensure timely availability of PLN's

- -0 -

audited accounts, but would also provide greater comfort to the capital markets, both domestic andintemational, that PLN plans to access in future for borrowing as well as equity, the latter afterit is converted to a Persero, for funds to finance its capital expenditures.

4.15 PLN has an effective internal audit group which reports to the President Director forvarious special investigations, in addition to keeping general and project accounting matters underreview.

Insurance

4.16 PLN currently carries transit and marine insurance on equipment and materials intransit. Projects under construction are covered by the contractor's all risk and erection insurance.Fire and other hazards on most of the assets in operation are self-insured. In view of thegeographical spread of PLN's assets, any single loss would be relatively small by comparison withtotal assets and operations, and this policy has been considered satisfactory by the Bank. However,with some very large projects having been completed in recent years and others now underimpleir-ntation, there would be a greater concentration of assets in certain locations than in thepast. An understanding was reached under Loans 3097-IND and 3098-IND that major works, plantand equipment at large power projects would be insured with outside agencies. Accordingly, PLNis currently carrying commercial insurance for major operating plants and equipment at severallarge power projects totalling about 4,900 MW, in and outside Java.

- 21 -

TIE PROJECT

Backfgound

5.I The Bank's involvement in hydroelectric power development in Indonesia dates backto financing of the Saguling hydropower development under the Tenth Power Project (Loans 1950-IND and 19501-IND) and Phase I of the Cirata development under the Thirteenth Power Project(Loan 2300-IND), and Phase II of the Cirata development (Loan 3602-IND). In coal-fired powerdevelopment, the Bank has been involved in the construction of the first coal-fired power staticncomprising 4 x 400 MW generating units at Suralaya in West lava, through the Eighth, Ninth,Twelfth and the Fourteenth Power Projects (Loans 1708-IND, 1872-IND, 2214-IND and 2243-IND), all of which are already in successful operation. Three additional units of 600 MW eachare under construction at Suralaya (Loan 3501-IND). In addition, two coal-fired units of 400 MWeach are being constructed at Paiton in East Java (Loan 3098-IND), the first unit of which hasalready been placed in operation.

5.2 The Sumatera and Kalimantan Power Project focuses on policy agenda of the powersector, as well as institutional restructuring of PLN, which was included in a Policy Letter receivedat negotiations of the proposed loan (para. 3.6). The policy agenda has been dibcussed in Chapter3. The physical components of the project comprise: (a) construction of a hydroelectric powerplant with an initial generating capacity of 90 MW at Besai in South Sumatera and relatedtransmission facilities; (b) construction of a mine-mouth lignite fired power plant with an initialgenerating capacity of 130 MW at Banjarmasin in South Kalimantan and related transmissionfaciities; (c) procurement of two barge-mounted power plants of 10 MW and 30 MW capacityrespectively; and (d) technical assistance to GOI and PLN.

5.3 The Besai hydroelectric scheme is located in the upper reaches of the Besai river,in the Lampung province of South Sumatera, draining into the Java Sea (Map No. IBRD 25507).The Besai plant is planned as a run-of-river type development with a daily regulating storagecapacity. A generating capacity of 90 MW will be supported by the available hydro energy toprovide economical peaking capacity to the grid in close proximity to the load center. It aims tosupply electric power to PLN's Region IV in South Sumatera.

5.4 The mine-mouth Banjarmasin Thermal Power Plant is located at Asam Asam inSouth Kalimantan, about 12 km inland from the coast, and 160 km from Banjarmasin (Map No.IBRD 25508). Two units of 65 MW each will be built initially, using lignite as fuel, which is anon-tradeable resource and available in sufficient quantities in the area. The lignite mine will bedeveloped by the coal company, PT Arutmin, that holds the concession to the coal mines. Thisproject component will service PLN's Region VI in South Kalimantan.

- 22 -

5.5 The demand forecast for PLN's Region VI indicates that shortage of power is likelyto be experienced in the region starting from 1995, until the proposed Banjarmasin thermal powerplant comes on stream. The mobile power plants (barge-mounted), to be procured specifically tomeet regional power shortages in the Outer Islands, are planned to be deployed temporarily inRegion VI for this purpose. The barge-mounted plants are expected to be moved from one areato another as necessary, to cater to load demands when such periodic shortages are encountered.Several areas in the outer islands, such as Banjarmasin, Batam, Pakanbaru, Bali, Pontianak,Tanjung Pinang and Lombok are projected to experience power shortages at different times.

Rationale for Bank Involvement

5.6 The proposed Sumatera and Kalimantan Power Project, in conjunction with thesubsequent Rural Electrification HI Project, forms an integral part of the Bank's lending strategyfor Indonesia. The two projects are supporting the initial phase of a comprehensive reformprogram of the Government for the country's power sector. The Government has drawn on closecooperation from Bank staff and technical assistance from ongoing Bank loans in developing theagenda for reform: (a) opening the sector for substantial private investor/operator participation;(b) restructuring the dominant public power utility PLN; (c) reforming power tariffs; and (d)establishing effective regulatory oversight. These reforms will, through cost effective expansionof reliable electricity services, contribute to strengthening the competitiveness of Indonesia'sproductive and service sectors, as well as to enhancing the welfare of the population at large.Through its focus on the islands of Sunatera and Kalimantan, the proposed project will alsosupport directly the Government's objective of achieving a more balanced inter-regional equity.These objectives are fully consistent with the Country Assistnce Strategy discussed by the Boardon April 12, 1994.