World Bank Document · Document of The World Bank Report No: 25429 IMPLEMENTATION COMPLETION REPORT...

41

Document of The World Bank Report No: 25429 IMPLEMENTATION COMPLETION REPORT (SCL-41490) ON A LOAN IN THE AMOUNT OF US$13.0 MILLION TO THE GOVERNMENT OF GUATEMALA FOR A PRIVATE PARTICIPATION IN INFRASTRUCTURE TECHNICAL ASSISTANCE LOAN (PPI-TAL) June 19, 2003 Finance, Private Sector and Infrastructure Department Central America Country Management Unit Latin America and the Caribbean Region Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of World Bank Document · Document of The World Bank Report No: 25429 IMPLEMENTATION COMPLETION REPORT...

Document of The World Bank

Report No: 25429

IMPLEMENTATION COMPLETION REPORT(SCL-41490)

ON A

LOAN

IN THE AMOUNT OF US$13.0 MILLION

TO THE

GOVERNMENT OF GUATEMALA

FOR A

PRIVATE PARTICIPATION IN INFRASTRUCTURE TECHNICAL ASSISTANCE LOAN (PPI-TAL)

June 19, 2003

Finance, Private Sector and Infrastructure Department Central America Country Management Unit Latin America and the Caribbean Region

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

(Exchange Rate Effective October 2002)

Currency Unit = Quetzal (Q) Q 1.00 = US$ 0.13

US$ 1.00 = 7.8 Q

FISCAL YEARJanuary 1 December 31

ABBREVIATIONS AND ACRONYMS

AMM Administrator of the Wholesale Market (Administrador del Mercado Mayorista)BCIECAS

Banco Centroamericano de Integración EconómicaCountry Assistance Strategy

CNEE National Electrical Energy Commission (Comisión Nacional de Energía Eléctrica)COPRE

DEOCSA

Presidential Commission for State Restructuring (Comisión Presidencial para la Restructuración del Estado) or OCMOE (Oficina del Comisionado para la Modernización del Organismo Ejecutivo) or COMODES (Comisión Presidencial para la Modernización y Descentralización del Estado)Central-Western Power Distribution Company (Distribuidora de Electricidad del Occidente Central, Sociedad Anónima)

DEORSA Rural-Western Power Distribution Company (Distribuidora de Electricidad del Occidente Rural, Sociedad Anónima) DGCT General Directorate of Post and Telegraph Services (Dirección General de Correos y Telégrafos)ECE Electricity Trading Enterprise (Empresa Comercializadora de Electricidad)EEGSAEGEE

Guatemala Electrical Company (Empresa Eléctrica de Guatemala, Sociedad Anónima)National Power Generation Enterprise (Empresa Guatemalteca de Electricidad)

ETCEE Power Transmission and Coordination Enterprise (Empresa Transportadora y Coordinadora de Energía Eléctrica)FEGUA National Railroads Enterprise (Ferrocarriles de Guatemala)FONDETEL Telecommunications Fund (Fondo Nacional de Telecomunicaciones)GUATEL National Telecommunications Enterprise (Guatemala Telecomunicaciones)ICB International Competitive BiddingICRICTIDB

Implementation Completion ReportInformation and Communication TechnologiesInter-American Development Bank

IMF International Monetary FundINDE National Electrification Institute (Instituto Nacional de Electrificación)INFOM Municipal Development Institute (Instituto de Fomento Municipal)IPPIPSLACMEMMICIVI

Independent Power ProducersInternational Postal Services, Ltd. (Canada)Latin America and the Caribbean RegionMinistry of Energy and Mining (Ministerio de Energía y Minas)Ministry of Communications, Infrastructure and Housing (Ministerio de Comunicaciones, Infraestructura y Vivienda)

MMA Ministry of Environment (Ministerio del Medio Ambiente)

ABBREVIATIONS AND ACRONYMS (cont.)

PADPERPIUPPIPPIAF

Project Appraisal DocumentRural Electrification PlanProject Implementation UnitPrivate Participation in InfrastructurePublic-Private Infrastructure Advisory Facility

PRONACOM National Competitiveness Project (Proyecto Nacional de Competitividad)SIT Telecommunications Superintendency (Superintendencia de Telecomunicaciones)TAL Technical Assistance LoanTELGUATELMEXUNDPUSAID

Guatemala Telephone Company (Telefónica Guatemalteca)Telephone Company of Mexico (Teléfonos de Mexico S.A.)United Nations Development ProgrammeUnited States Agency for International Development

MEASUREMENT UNITS

kW Kilowatt (a measure of electric power) MWh Megawatt-hour (1000 kWh)MW Megawatt (1000 kW) GWh Gigawatt-hour (1000 MWh)kWh Kilowatt-hour (a measure of electric energy)

Vice President: David de FerrantiCountry Manager/Director: Jane Armitage

Sector Manager/Director: Danny Leipziger Task Team Leader/Task Manager: Eduardo Zolezzi

GUATEMALAPRIVATE PARTICIPATION IN INFRASTRUCTURE

TECHNICAL ASSISTANCE LOAN

CONTENTS

Page No.1. Project Data 12. Principal Performance Ratings 13. Assessment of Development Objective and Design, and of Quality at Entry 14. Achievement of Objective and Outputs 55. Major Factors Affecting Implementation and Outcome 176. Sustainability 197. Bank and Borrower Performance 218. Lessons Learned 239. Partner Comments 2410. Additional Information 24Annex 1. Key Performance Indicators/Log Frame Matrix 25Annex 2. Project Costs and Financing 28Annex 3. Economic Costs and Benefits 30Annex 4. Bank Inputs 31Annex 5. Ratings for Achievement of Objectives/Outputs of Components 33Annex 6. Ratings of Bank and Borrower Performance 34Annex 7. List of Supporting Documents 35

Map

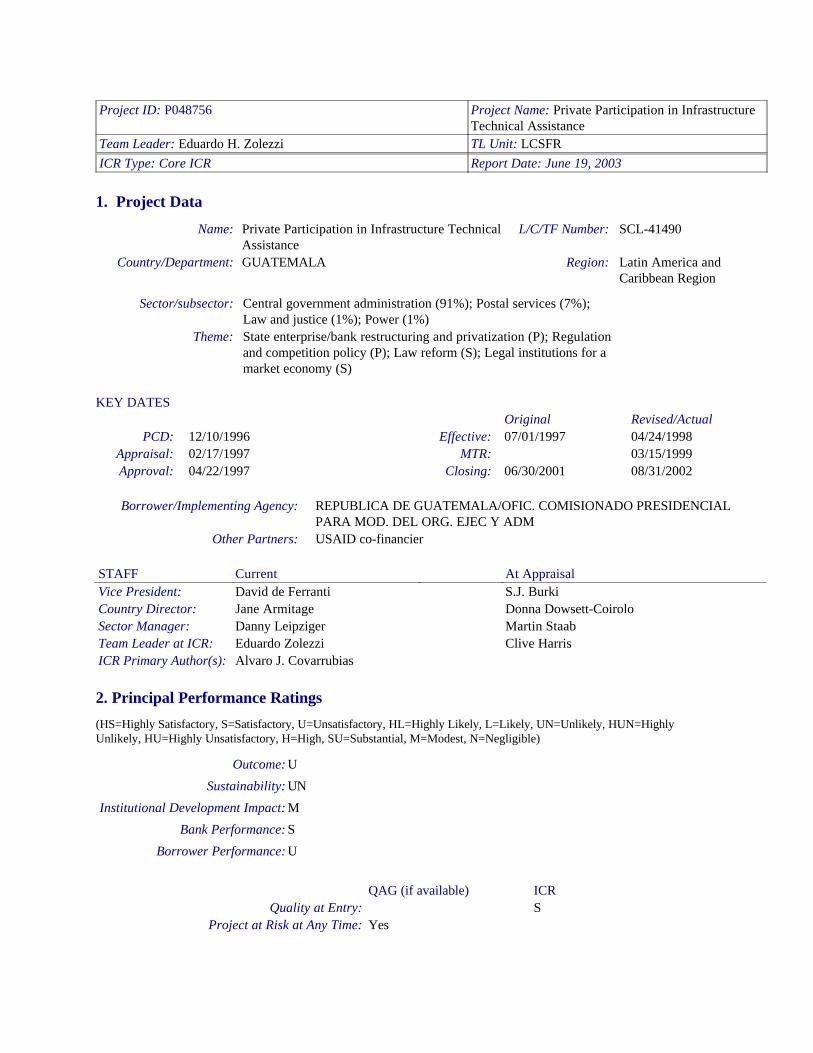

Project ID: P048756 Project Name: Private Participation in Infrastructure Technical Assistance

Team Leader: Eduardo H. Zolezzi TL Unit: LCSFRICR Type: Core ICR Report Date: June 19, 2003

1. Project Data

Name: Private Participation in Infrastructure Technical Assistance

L/C/TF Number: SCL-41490

Country/Department: GUATEMALA Region: Latin America and Caribbean Region

Sector/subsector: Central government administration (91%); Postal services (7%); Law and justice (1%); Power (1%)

Theme: State enterprise/bank restructuring and privatization (P); Regulation and competition policy (P); Law reform (S); Legal institutions for a market economy (S)

KEY DATESOriginal Revised/Actual

PCD: 12/10/1996 Effective: 07/01/1997 04/24/1998Appraisal: 02/17/1997 MTR: 03/15/1999Approval: 04/22/1997 Closing: 06/30/2001 08/31/2002

Borrower/Implementing Agency: REPUBLICA DE GUATEMALA/OFIC. COMISIONADO PRESIDENCIAL PARA MOD. DEL ORG. EJEC Y ADM

Other Partners: USAID co-financier

STAFF Current At AppraisalVice President: David de Ferranti S.J. BurkiCountry Director: Jane Armitage Donna Dowsett-CoiroloSector Manager: Danny Leipziger Martin StaabTeam Leader at ICR: Eduardo Zolezzi Clive HarrisICR Primary Author(s): Alvaro J. Covarrubias

2. Principal Performance Ratings

(HS=Highly Satisfactory, S=Satisfactory, U=Unsatisfactory, HL=Highly Likely, L=Likely, UN=Unlikely, HUN=Highly Unlikely, HU=Highly Unsatisfactory, H=High, SU=Substantial, M=Modest, N=Negligible)

Outcome: U

Sustainability: UN

Institutional Development Impact: M

Bank Performance: S

Borrower Performance: U

QAG (if available) ICRQuality at Entry: S

Project at Risk at Any Time: Yes

3. Assessment of Development Objective and Design, and of Quality at Entry

3.1 Original Objective:Background:

This Technical Assistance Project spanned two Guatemalan Administrations. In 1997, the Administration of President Alvaro Arzú Irigoyen (1996-2000) recognized that in order to accelerate the pace of economic growth and spread the benefits of growth, it was necessary to improve the quality of infrastructure service provision and widen the coverage of these services through private sector participation in infrastructure. This goal was to be accomplished by introducing private sector management, ownership and competition into service provision (where possible); in addition to transforming the Government’s role of service provider to that of regulator and policy-maker. This initiative in infrastructure was part of a wider reform encompassing modernization of the public sector, reform of the hydrocarbon sector and promotion of foreign investment in Guatemala. The Administration of President Arzú Irigoyen prepared and appraised the Project, made the loan effective and initiated project implementation. The current Administration, headed by President Alfonso Portillo, has continued project implementation.

Necessary legal reforms included amendments to both the Ley de Contrataciones and Ley de Telecomunicaciones, and the enactment of a new Ley General de Electricidad. The Ley de Contrataciones, which governs the concessions of activities and the contracting out of services by the public sector, as amended in March 1997, now permits the sale of shares of autonomous state-owned entities to the public, among other reforms. The Ley de Telecomunicaciones, as amended in October 1997, provided for the break-up of the government-owned telephone service and its sale to private entrepreneurs. The new Ley General de Electricidad, as enacted in 1996, unbundled generation, transmission and distribution of electricity. It provided for the break-up of the government-owned electricity enterprises and their sale to the private sector in order to compete in generation and to operate regulated concessions of distribution companies.

The specific sectors addressed in this project were ports, roads, power (electricity), telecommunications and the postal service. These sectors have had a varied history in terms of development, private sector involvement and productivity. As described below, before the reforms were implemented under this project, these infrastructure sectors were under a mix of government ownership, leasing arrangements and, to a lesser extent, management and concession contracts.

In the power sector, the Government’s reforms involved complete restructuring. The sector already had experience with private sector participation through power purchase agreements. The objective of the project, however, was to implement broader reforms that would involve privatization of state-owned assets, and legal and regulatory reform, to increase the sector’s efficiency and improve coverage. This objective also included unbundling of generation, transmission and distribution activities, and the creation of a wholesale market. To that end, the technical assistance goal was to design and implement a new legal and regulatory framework and prepare the state-owned electrical enterprises for privatization. Capacity building was designed to strengthen the capacity of the Government's regulatory agency, the entities in charge of the privatization program and the entity in charge of the administration of the electricity wholesale market. Project preparation activities assisted in preparation of a new electricity law that was enacted in 1996, prior to project effectiveness.

In the telecommunications sector, service was provided by the state-owned, autonomous company GUATEL, which also held the monopoly for the provision of fixed telephony. The objective of the project

- 2 -

was to assist with the privatization of GUATEL, and to develop a new legal and regulatory framework that would open the sector gradually to competition. To accomplish this objective, an amendment to the telecommunications law was necessary, which was obtained in October 1997.

In 1997, the ports sector had a mixed record of productivity. Overall productivity of the three ports of Puerto Barrios, Puerto Quetzal and Puerto Santo Tomás de Castilla was estimated to be at 50% of international standards. However, there were significant differences between the individual ports. Puerto Barrios, operated by a private operator under a 25-year concession, was the second most efficient and reliable port in Central America. In contrast, the performance of publicly-owned Puerto Quetzal and Puerto Santo Tomás were deemed inadequate. Puerto Quetzal had partial private sector participation in some port activities, while Puerto Santo Tomás was entirely publicly owned and operated. It was expected that the performance of these two ports could be improved through greater private participation in the operation.

In the rest of the transport sector, the experience with private sector participation was very limited. There was no experience with road concessioning at that time, and the only limited experience was gained in the railway sector, with the leasing of railroad equipment, facilities and territories to a private operator. The experience with this arrangement, however, was mixed. The objective of the project was to increase private participation in the road sub-sector through setting up an appropriate legal and regulatory framework and concessioning selected roads.

At the start of the project in 1997, the postal service provided by the Directorate of Post and Telegraph Services (Dirección General de Correos y Telégrafos, DGCT) suffered from over-staffing, an extremely weak financial position and poor and unreliable service. Annual losses were around US$2 million. Moreover, small private courier services were using DGCT’s staff and facilities on an informal basis. To improve the situation, the Government established three basic goals for the postal sector: (i) ensure an acceptable level of universal postal services for the entire country in terms of access, affordability and quality; (ii) reduce the Government deficit associated with providing these services; and (iii) increase private participation in the postal sector. To achieve these goals, the DGCT was to enter into a management contract with a private firm with solid experience in the provision of postal services.

Original Objective:

As stated in the PAD, the project objectives sought to prepare selected infrastructure sectors – power, telecommunications, ports, roads and highways, and postal services – for privatization and concessions within a sound legal and regulatory framework. Achieving this objective would contribute to the Government’s goals of improving the efficiency of infrastructure service provision and widening service coverage. To accomplish this objective, the project would provide technical assistance to draw up regulations for existing sectoral legislation and develop new legislation where required; strengthen regulatory agencies and sectoral ministries charged with overseeing the infrastructure sectors listed above; restructure and prepare for privatization entities within these sectors; and strengthen the ability of the Government to manage and implement the program of privatization and concessions in the infrastructure sector.

Assessment: The project objectives were appropriate, as they supported the Government’s efforts to reform the infrastructure sector, which for decades had been controlled and partly financed with public funds. The objectives of the project reflected the Bank’s assistance to the Government, as stated in the Bank’s Country Assistance Strategy (CAS) of that time. The infrastructure sectors were controlled by the state, and most of the sectors were inefficient and delivered low quality services. Moreover, the prices of

- 3 -

public services did not usually reflect economic costs, causing distortions in the economy and deficits that had to be covered with public funds. The project development objective was to redress this situation by (i) introducing private participation in infrastructure under the form of either private ownership or management services as appropriate, (ii) developing an appropriate legal and regulatory framework for each sector, and (iii) building the capacity of the newly created entities to accomplish their functions. However, it should be noted that a completion of comprehensive reforms in five infrastructure sectors was an extremely ambitious objective. In retrospect, more consideration could have been given to the institutional capacity and government commitment needed to support reforms in so many sectors all at once. In particular, transport sector reforms are in general more difficult and lengthy to achieve. Throughout the project, government support was stronger to the power and telecommunications sectors and weaker to the transport sectors. A project focusing on fewer sectors might have been more effective. All things considered, however, the project objectives were adequate.

3.2 Revised Objective:The objective of the project was not revised.

3.3 Original Components:The project included the following components:

Electricity: Assist the establishment of the electricity wholesale market, restructure the National Institute of Electricity (INDE), privatize the Guatemala Electricity Company (EEGSA), procure equipment, train staff of the National Electric Energy Commission (CNEE) and the Ministry of Energy and Mining (MEM), develop all required regulations, conduct environmental audits and establish environmental regulations.

Telecommunications: Provide training and equipment to the regulatory body, draft detailed regulations for interconnections, prepare GUATEL for privatization (funded by the Borrower), assist in auctioning and monitoring of the radio spectrum including the purchase of software and develop regulations dealing with the radio spectrum.

Ports: Offer technical assistance to the concessioning process, draft sector legislation, conduct environmental audits and prepare environmental regulations, develop a strategy for the minor ports, and conduct a training program for the staff in port authorities.

Highways: Offer technical assistance to identify roads for possible concessions and develop model concession agreements and bidding documents.

Postal services: Assist in the development of a regulatory framework; the preparation of concession documents and the strategy for postal services; offer technical assistance to prepare a management contract; and train staff for a new regulatory role.

Cross-sectoral activities: Fund a public information campaign, study tours and the promotion and dissemination of investment opportunities; handle project management (funding for implementing unit, procurement agent and external audit); and offer technical assistance and training for additional privatization requirements and cross-sectoral issues.

3.4 Revised Components:Component Cost RatingHiring of Procurement Agent $600,000 SPorts $700,000 U

- 4 -

Road Concessioning; $700,000 UElectricity $4,900,000 STelecommunications $5,200,000 SPostal Services $600,000 SCross-Sectoral Activities $5,200,000 U

Following a request made by the Borrower in February 2000, the Bank added one component to the project without changing the project objectives. The additional component included activities to improve the delivery of municipal services (electricity, water, water and sanitation, and solid waste disposal) with private participation. There has also been a gradual change in the scope of the power and telecom components, as the sector needs shifted from sector restructuring and privatization to post-privatization issues, including fine-tuning of the regulatory framework, capacity building activities, and formulation of policies and implementation mechanisms for rural investment.

3.5 Quality at Entry:Both the Bank and the Government were actively involved in project preparation. Initially, the Government considered an umbrella technical assistance loan from the Bank, which would have covered aspects of public sector modernization, tax reform and infrastructure privatization. Subsequently, the Bank and the Government reached the conclusion that such a broad operation would be difficult to manage and implement and therefore, decided to unbundle the initiative into separate lending operations of which the Private Participation in Infrastructure (PPI) Project was the first. Even so, the project was still quite complex, and this has been the project's main weakness. In particular, experience shows that reforms in the transport sector are relatively difficult to implement in comparison to telecommunications and power sector reforms. During the project preparation, the Government, as well as the heads of the key state entities involved in the privatization effort (MEM, MICIVI, GUATEL, EEGSA and INDE) showed strong commitment to the project. Early in the project cycle, the Government demonstrated strong ownership of the project by obtaining Congressional approval of the Ley General de Electricidad, and the amendments to the Ley de Contrataciones and the Ley de Telecomunicaciones, triggering the initiative to modernize the Executive Branch and appoint a Commissioner to oversee the implementation of the new laws. These events led the project appraisal team to rate project risks as moderate. There was no way to mitigate the risk that later Administrations would not show the same type of commitment to the reforms, and it was a risk that has proved to be real and significant.

On the other hand, the Bank involvement was seen as critical for successful completion of the announced reforms. The Bank's presence gave international credibility to the project and provided the Government with advice on the project design based on its worldwide experience with similar operations in other countries. Also, the Bank alerted the Government of the need to ensure support from the legislative body to pass timely reform laws; to involve trade unions, affected workers and potential investors in the process; and to use transparent mechanisms to award privatization bids.

All things considered, quality at entry is rated as satisfactory.

4. Achievement of Objective and Outputs

4.1 Outcome/achievement of objective:

Electricity Sector

The development objective applicable to the electricity sector was achieved satisfactorily. In addition to

- 5 -

privatization, the power sector reforms included a comprehensive legal and regulatory reform with the objective of increasing efficiency and ensuring adequate expansion. These reforms included restructuring of the power sector, creation of a wholesale market, creation of a regulatory agency (CNEE), and passage of key regulations, including tariff setting and quality of service. Installed capacity and electricity coverage have been increasing. Power supply has become reliable, and increases in efficiency and implementation of the rural electrification program resulted in a significant increase in electricity coverage from 56% in 1997 to 82% in 2001. Even though privatization was not fully completed ( the transmission company and hydroelectric plants of INDE remain public), the private sector owns the majority of generation and its share keeps growing. Government's ownership of transmission has not led to any market distortions, since transmission is independent from generation. Due to delays in making the loan effective, loan proceeds were not used for this privatization; the Government used its own funds. The project, however, has supported various post-privatization activities, including drafting of key regulations and technical norms, consolidation of the wholesale market, capacity building of newly created entities (particularly CNEE and AMM) and development of new policies, such as for rural electrification. All things considered, the performance of the electricity sector has been very satisfactory.

Restructuring of the power sector has been completed. In November 1996, while the project was in the preparation stage, a new General Electricity Law (Ley General de Electricidad) was enacted, which during more than five years of application, has generally proved to be adequate for the country's power sector. The key features of the Law are: (a) unbundling the activities of the sector in generation, transmission, distribution and commercialization of energy; (b) competition in the generation and commercialization activities; (c) unrestricted and open access to the transmission system, which currently is owned by a Government utility; (d) unregulated generation prices, and transmission and distribution prices regulated according to established and transparent norms; (e) freedom of energy users to choose their supplier; and (f) definition of the rights of energy users.

The new power sector entities function satisfactorily. The National Electrical Energy Commission (Comisión Nacional de Energía Eléctrica, CNEE), the sector regulator, and the Administrator of the Wholesale Market (Administrador del Mercado Mayorista, AMM), the wholesale market operator, were created by the new Electricity Law and are now established, staffed and functioning well. The companies resulting from the restructuring and privatization of state-owned power generation, transmission and distribution service (DEORSA, DEOCSA, EGEE, EEGSA, ECE, ETCEE and the new INDE) are also well established and performing well. The State has retained ownership of all the hydroelectric stations and the enterprise in charge of the transmission. Hydroelectric plants account for 40% of the power generating capacity installed in the country. Private companies operating steam and diesel generating plants own the rest. As all new investment is private, the importance of INDE’s share of the power generation capacity is falling. The three private distribution companies (DEORSA, DEOCSA and EEGSA) have also been functioning satisfactorily, gradually expanding the distribution network. One of the constraints to expansion, however, is the existence of several municipal companies that are in charge of power distribution and have been characterized by inefficient operations and financial difficulties, adversely affecting the quality of service and the possibilities of expansion in their respective distribution areas. These companies, however, serve only a fraction of total users (roughly 7%). Economic tariff setting, but retail tariff deficiencies. Tariffs of generating plants and the transmission and distribution companies are based on cost-recovery principles. Tariffs are regulated by CNEE, according to the methodology established by the Electricity Law and corresponding regulations. The main problem with tariff setting relates to the Government’s subsidization of households. The State (through INDE) subsidizes the retail price of electricity for those users consuming less than 300 kWh per month. This “social tariff”, as it is called, subsidizes 90% of all residential users. It is a very inefficient subsidy,

- 6 -

as it targets primarily the middle class and not the poor.

Fast electricity coverage expansion. The electrification index rose from 56% in 1997 to 82% in 2001 and is expected to reach 90% in 2004 (well above the Latin American average). This achievement was a direct result of the reform of the electricity sector and private participation in the sector. Privatization proceeds were used to help subsidize the expansion of the distribution network in an efficient manner (see Viewpoint Note, "Private Rural Power: Network Expansion Using an Output-Based Scheme in Guatemala," Clive Harris, June 2002.)

Telecommunications sector

The development objectives applicable to the telecommunications sector were achieved satisfactorily. The telecom sector has transformed profoundly. Provision of telecom services is fully private and competition is increasing. Guatemala now has more than 800,000 fixed lines and more than one million new mobile lines, increasing the penetration rate (fixed and mobile combined) from 4.6% in 1997 to 17.2% in 2001. The number of fixed lines increased by 15% in this period, while the number of mobile phones grew by 204%. This achievement is a direct result of the privatization and the sector reform that introduced competition. Now, most of the urban population in Guatemala has access to telephone service, either fixed or mobile. Moreover, the tariffs, overall, have decreased. The main challenge now is the extension of telecom services to rural areas. All things considered, the performance of the telecommunications sector is very satisfactory.

Sector restructuring and privatization. Under the project, the state-owned communications entity was split into TELGUA and GUATEL. TELGUA retained the majority of GUATEL’s telecommunications assets and was privatized in 1998 to TELMEX, a Mexican telecom operator. GUATEL is a residual entity, which was left in charge of the management of the remaining assets, debt service and some rural telecommunications networks. Sector liberalization brought three new strong competitors in the mobile market: a subsidiary of Millicom (USA); Telefónica of Spain; and Bell South, and several companies started competing with Entel in the long-distance market. A sector regulator (Superintendencia de Telecomunicaciones) was established and strengthened by the Project, and has been functioning satisfactorily. The new Administration which took office in 2000 originally questioned GUATEL’s privatization and attempted to reverse this transaction. As a result, the project’s support in the telecommunications sector was interrupted for about 18 months, between 2000 and 2001. This issue was eventually resolved and a new agreement between the Government and TELMEX was signed in October 2002. This interruption mainly affected the support provided to the regulator (Superintendencia de Telecomunicaciones). By 2000, however, the regulator was well-established and had sufficient internal resources to support its functions. (The regulator is funded from a levy based on sector revenues).

- 7 -

Remaining challenges. The main unresolved issue in the telecommunications sector relates to the inadequate strategy and institutional arrangements for rural telecommunications (see below). Although this issue is extremely important, it was not a part of the original project’s objectives and description. This is because the reforms of 1996-97 did not address the universal service issue, and also created an institutional duplication between GUATEL and the Telecommunications Fund (FONDETEL). On one hand, the Government has left the responsibility for operating the original GUATEL rural phone networks with the new GUATEL, the residual entity. On the other hand, FONDETEL was created, as a fund to channel the subsidies to the private sector to install and operate new rural telephones. The contract is awarded to the eligible operator requiring the lowest subsidy. FONDETEL was funded with proceeds of the spectrum auctions. FONDETEL’s approach is consistent with international best practices as applied in many other LAC countries, such as Peru, Chile or Colombia. However, the unclear objectives and roles for GUATEL have led this institution into expanding its own rural telephone network, resulting in inefficient investments, duplications of networks, and the resulting need for excessive subsidies. FONDETEL would appear to be a more efficient and transparent mechanism for channeling public subsidies, but most of its original funds have already been invested, and no new funding arrangement has been set in place. The Ministry of Communications, Infrastructure and Housing (Ministerio de Comunicaciones, Infraestructura y Vivienda, MICIVI), in charge of the sector, does not have adequate resources to develop or implement new policies. This became very important in the era of the knowledge economy, as the Government has had to take the lead in the use of information and communication technologies (ICT) to help in the development of Guatemala.

Transport

In contrast to the telecom and electricity sectors, the development objectives applicable to the transport sector (ports and roads) were not achieved. Private participation experience in financing and operating transport infrastructure in Guatemala is still very modest. In the road sector, some experience has been gained through concessioning one segment of a road between Guatemala city and Puerto Quetzal. The concessioning process, however, was not supported by the project. The bidding process to select a concessionaire was deficient, as were the environmental and social assessments. Thus, the outcome for the road sector is unsatisfactory. In the port sector, the most successful experience has been with the Puerto Barrios concession (which, however, was carried out before the project), and limited leases of selected port operations to private operators in Puerto Quetzal, and to a lesser extent in Puerto Santo Tomas. A new draft of Port and Maritime Law was prepared (with the assistance of the project) but it has not been presented to the Congress. Therefore the outcome of this component is also unsatisfactory.

Postal services

In 1997, the General Directorate of Post and Telegraph Services (Dirección General de Correos y Telégrafos, DGCT) entered into a five-year management contract with a private operator (Canadian postal operator). The postal service has improved significantly. All indicators, including coverage, efficiency and reliability have improved, while the requirements of subsidies were dramatically reduced. The main issue, however, is the sustainability of these benefits, given that the management contract is expiring this year, and the future of the postal service remains unsure. The outcome for this sub-component is rated as marginally satisfactory.

Municipal services

At the request of the Government, the project also financed activities related to municipal infrastructure

- 8 -

(electricity, water and sanitation, and solid waste). The purpose of this component was to improve the delivery of these services, which in general suffered problems of low coverage, efficiency and financial sustainability. The project financed diagnostic studies and provided recommendations for improving the delivery of these services. These activities, however, were only complementary and were not a part of the original project components. Therefore, this sub-component is not rated here.

Assessment

The overall project outcome is unsatisfactory. Although major achievements were recorded by reforming and privatizing power and telecommunications sector, and partially the postal sector, these accomplishments were not extended to port and road sectors. The lack of commitment from the Government and the unsatisfactory performance of the project coordinating unit and the implementing agencies led to very slow implementation progress, particularly since 2000. Despite several efforts made by the Bank to revive the project since the mid-term review, and the late positive reaction made by the Government in late 2001 and early 2002, the Bank concluded that it was highly unlikely that the principal project objectives in the transport sector would be achieved by extending the project life beyond the already extended and elapsed 14 months. In retrospect, it would have been advisable to amend the loan agreement in 2000 reducing the project objectives to match the political support for few sectors and the limited implementation capacity of the project implementation unit.

4.2 Outputs by components:A more detailed account is presented below on the output of the project for each component, and project’s main contributions to this outcome. Particular attention is given to the power and telecommunications sector, the main beneficiaries of the project.

Power sector

The legal and regulatory framework. The National Electrical Energy Commission (Comisión Nacional de Energía Eléctrica, CNEE) and the Administrator of the Wholesale Market (Administrador del Mercado Mayorista, AMM) are in full operation. They were created by the General Electricity Law enacted on November 21, 1996 (Congress Decree No. 93-96). The project contributed to the drafting of the original regulatory framework, and its consolidation and fine-tuning throughout the project period.

The CNEE. The Regulations of the General Electricity Law (Government Agreement No. 256-97 of March 21, 1997) created the CNEE as the regulator of the electricity sector. The CNEE is performing its policy making functions satisfactorily. It has issued and monitored the application of 12 technical norms on safety of electrical installations, quality of technical and commercial services, and the design and operation of transmission and distribution lines. CNEE has also established the methodology and calculated the electricity tariffs of the regulated transmission and distribution companies, and of the subsidized social tariffs applicable to consumption lower than 300 kWh per month. It has supervised the retail tariffs being charged to consumers by the distribution companies EEGSA, DEOCSA and DEORSA. The Executive Board of the CNEE is composed of a President and three Directors appointed by the President of the Republic. The Executive Board serves a 5-year term. Although technically the CNEE is part of the Ministry of Energy and Mines, it has a semi-autonomous status, and its budget is financed with the proceeds of a 0.3 % tax on the electricity sales of distribution companies. The Government has been respecting CNEE's legal responsibilities and autonomy. (Creation of autonomous entities require an approval in the Congress by a two-third majority, which is difficult to achieve). CNEE has been performing satisfactorily and appears to be a sustainable institution. The project provided considerable resources for CNEE capacity building. This included technical assistance for CNEE’s activities (such as tariff revision,

- 9 -

quality audits etc.), and specific training activities on regulatory issues. Notwithstanding, it is important that these capacity building activities continue after the closure of the project. CNEE appears to now have sufficient resources to comply with its regulatory functions and to continue financing the training of its staff.

The AMM. Since 1998, the AMM has been engaged in real-time commercial transactions among generators, distributors and large consumers of electricity connected to the national interconnected system, in accordance with its regulations (Government Agreement No. 299-98 of May 25, 1998). Each group of generators, transmitters, distributors and large consumers has one representative and one alternate in the Board of Directors of the AMM; the Presidency of the Board rotates every two years. The wholesale market is composed of 20 generators, 16 distributors, 2 transmitters, 5 brokers and 26 large consumers. The project helped to establish AMM, and design its operating rules in 2001. With it, the regulatory framework of the electricity sector has been completed. The project also provided initial support in training the AMM staff. The AMM is now staffed with highly qualified professionals, supported by top- of-the-line communications, telemetering, telecontrol devices and computer hardware and software. The AMM monthly performs the physical and monetary balances of the wholesale market and resulting bank transfers. The AMM is also a sustainable entity. It is a nonprofit organization financed by the agents of the wholesale market, based on their proportional participation. As a private entity, it is autonomous and is likely to be sustainable.

Privatization and restructuring. Privatization has been largely completed. All distribution and most of the generation facilities are in private hands. The State still owns hydroelectric generation and transmission. Although the Government owns a part of the generation capacity (about 40%), it does not invest in new generation projects. The state-owned generation represents about 40% of the installed capacity and its share is declining as private investment is increasing. In addition, 11 small electricity distribution networks are owned by municipalities but they serve only about 7 % of the users. The sector has been completely restructured. Generation, transmission and distribution were unbundled. There is competition in generation. Independent Power Producers (IPP) that had power purchase agreements (PPAs) negotiated before the reforms were integrated into the new sector structure. This resulted in a more efficient market operation and a lower electricity price.

Generation and transmission. The Instituto Nacional de Electrificación (INDE) was split into three entities: The new INDE, the Empresa Transportadora y Coordinadora de Energía Eléctrica (ETCEE) and the Empresa Comercializadora de Electricidad (ECE). The thermal generating plants were privatized, but INDE became the owner of the hydroelectric plants which contribute about 40 % of the installed capacity of the country. ETCEE is owned by the State and operates all transmission lines and substations of the 220 kV and 69 kV. ECE performs marketing functions in the retail electricity market. The installed capacity in the SIN has been increasing steadily with the 8 % average annual increase of the peak load. Installed capacity grew from 1,314 MW in 1996 to 1,670 MW in 2002, equivalent to a 27 % increase. Sixty percent of installed capacity is in private hands, generating about 50 % of electricity sales. The balance is mainly hydroelectric generation by INDE. Distribution. Electricity distribution was privatized in 1998. Three private enterprises emerged: the Distribuidora de Electricidad de Occidente S.A. (DEOCSA), the Distribuidora de Electricidad del Oriente Rural S. A. (DEORSA) and the Empresa Eléctrica de Guatemala S. A (EEGSA). The latter serves the central zone of the country. Eighty percent of DEOCSA and DEORSA were sold to Union Fenosa of Spain for US$101 million under an International Competitive Bidding (ICB) process. Eighty percent of EEGSA was sold to Iberdrola of Spain in US$520 million under an ICB. The remaining 20 % was sold to local investors.

- 10 -

Rural electrification. The US$101 million paid for DEOCSA and DEORSA were deposited in a trust fund (escrow account) to finance rural electrification expansion and the connection of 280,000 rural users (about US$ 1.57 million) located in 2,633 villages within a strip of 200 meters along the rural distribution lines of DEOCSA and DEORSA. This trust fund, increased by a Government contribution of US$202 million, is financing the Rural Electrification Plan (PER). The PER and the trust fund are administered by INDE. By May 2002, the PER, through DEOCSA and DEORSA had connected 220,000 users in 100 villages, at a cost of US$120.8 million financed by the PER trust fund. At the same time, the construction of 420 km of 230 kV transmission lines and 840 km of sub-transmission lines expanded the reach of the power system. Moreover, DEOCSA and DEORSA financed the connection of 240,000 additional rural users with their own resources. This remarkable effort in private rural electrification lifted the country electrification index to 82 % in early 2002, and accounting for ongoing and planned works, that index may reach 90 % in 2004. This result can be considered as a highly satisfactory social achievement by the private sector. DEORSA and DEOCSA now serve about 1,100,000 clients; EEGSA serves about 634,000 clients; and the municipalities serve about 118,000 clients.

- 11 -

Table - Power System Performance Indicators

Electricity Production

%

By technology (GWh) Gas turbines generators 106.94 1.85 % Steam turbines generators 1,426.60 24.71 % Engine driven generators 1,780.71 30.85 % Total thermal generation 3,314.25 57.42 % Total hydroelectric generation 2,264.32 39.23 % Total geothermal generation 193.68 3.36 % Total generation 5,772.25 100.00 % By origen (GWh) Interconnected system generation 5,772.25 99.09 Imports 53.0 0.91 Total 5,825.25 100.00 International trade (GWh) Year 2001 Year 2000 Imports 53.00 122.94 Exports 362.84 827.34 Net exchange 309.84 704.04 Exchange without losses 415.84 950.28 Export losses 6.17 13.53 Spot price (US$/MWh) Annual average 43.11 Monthly maximum average 53.25 Monthly minimum average 31.22 Other indicators Annual consumption in SIN (GWh)

5,293 5,068

Electricity consumption growth rate

4.43 % 9.68 %

Local losses 2.81 % 2.65 % Export losses 0.11 % 0.22 % Maximum demand in SIN (MW) 1,074.6 1,017.3 Maximum demand without exports (MW)

1,133.6 1,105.3

Power demand growth rate in SIN

5.63 % 8.21 %

Electricity pricing. The final price paid by the consumer is composed of the sum of generation and transmission costs plus the value added of electricity distribution. The electricity distributors buy power

- 12 -

and energy from the generators which they supply to their users. The distributors buy the balance in the spot market at the prevailing prices. In the spot market the average price of one MWh in 2001 was US$43.11 and had a minimum of US$31.22 in May and a maximum of US$53.25 in March. The transmission cost is a toll regulated by the CNEE. The value added of distribution is regulated by the CNEE based on a model distribution company. However, the retail price set for final users consuming up to 300 kWh per month is highly subsidized since 2000, in accordance with the Social Tariff Law. This has distorted the technical and economic principles used to determine the tariffs as demonstrated by the fact that the average monthly bill of clients of the distribution companies is about 55 kWh. It is doubtful that 90 % of the population consuming 300 kWh per month is composed only of the most economically vulnerable people. A social tariff with a ceiling of 300 kWh/month for 90 % of the population is indeed a general subsidy. A more targeted social tariff would benefit clients consuming no more than 60 kWh per month. The subsidy of about Q0.60/kWh is financed by the State through the low price of electricity bought by the distribution companies from the hydroelectric plants of EGEE.

The tables below indicate the retail electricity tariffs with and without subsidy and the price of hydroelectric generation paid for by the distribution companies. Table - Electricity tariff of one kWh sold to final consumer Company Social Tariff Normal Tariff EEGSA Q0.60 (US$0.075) Q 1.07 (US$0.130) DEOCSA Q0.59 (US$0.076) Q 0.93 (US$0.112) DEORSA Q0.59 (US$0.077) Q 0.92 (US$0.113) Table - Hydroelectric price of one MWh sold to distribution companies Company Social Price Normal Price EEGSA US$47.0 US$56.00 DEOCSA US$25.0 US$54.87 DEORSA US$29.0 US$55.13 The average price of hydro electricity sold to distribution companies is US$32.0/MWh. Telecommunications sector

Sector development. Since the 1996 and 1997 telecommunications reform, the sector has privatized significantly during the period between 1997-2001. Fixed lines have almost doubled from 430,000 to 756,000 lines and the number of mobile lines have grown 20 fold, from 64,000 to 1,126,000. Altogether, the number of telephone lines has grown from 494,000 in 1997 to 1,882,000 in 2001 at an average of 40 % per year.

The legal and regulatory framework. The new legal and regulatory framework for the telecom sector has been established. The Superintendency of Telecommunications (SIT) has been established as a regulatory entity and has been functioning satisfactorily. The project contributed to drafting the legal and regulatory framework and its fine-tuning and capacity building activities for SIT.

Privatization and market liberalization. The successful privatization of the telecommunications sector can be credited to the privatization of the main assets of the state-owned GUATEL. First, in 1997, GUATEL was split into TELGUA and GUATEL. TELGUA was privatized in 1998, and GUATEL, a residual entity, was in charge of disinvesting the remaining assets, and the operation of some smaller rural telecom networks. Teléfonos de Mexico S.A. (TELMEX) paid US$520 million for TELGUA. At the same time,

- 13 -

the sector was liberalized from the outset. This opening of the sector to competitive market forces allowed 15 companies to provide fixed local telephone services. Although they account for only 6 % of the local service market, they pose competition to TELGUA. Four companies provide mobile telephone services: SERCOM PCS Digital (subsidiary of TELGUA, 44%), Comunicaciones Celulares (subsidiary of Millicom International, 35%), Telefónica Centroamericana Guatemala (subsidiary of Telefónica de España, 14%), and Bell South Guatemala (7%). Several companies compete in the long-distance market.

The opening of the telecommunications market achieved a notable success by investing in mobile telephone services, but less in fixed telephone lines. The main beneficiary of the investment in fixed lines was Guatemala City, where 69% of all fixed telephones are now installed. 21% of the remaining fixed lines are spread almost evenly in nine cities and 10% are scattered in the rural areas of the country. Guatemala now has a telephone density of 6.3 fixed lines/100 inhabitants which is less than the density in El Salvador, Mexico, Panama, and Costa Rica but more than the density in Honduras and Nicaragua. As the concession contract did not give any exclusivity to TELGUA, it also did not require any investments in the local networks. At the same time, although 15 companies compete with TELGUA in the local fixed-line services, they represent only 6% of the market, and concentrate primarily on the more lucrative market segments. In 2001, the Government and TELGUA renegotiated the concession contract, agreeing on a specific investment program of Q 1,950 million (US$253.5 million) consisting of the installation of fixed lines, mobile lines and public telephones. Although the new Government in 2000 initially attempted to revise the privatization, the dispute was settled by the 2001 agreement described above. The Government is committed now to sector reforms, privatization and promoting greater competition.

SIT. Superintendencia de Telecomunicaciones (SIT) was established as a regulator for the telecommunications sector. Like CNEE, this is an autonomous entity, financed through a sector-based levy. The Government has been respecting this autonomy. SIT is fully staffed with competent professionals and has been functioning satisfactorily. The project provided considerable resources for technical assistance and capacity building activities for SIT, particularly in the earlier years of the project. SIT now appears to have sufficient resources to comply with its regulatory functions and to continue financing the training of its staff.

Local telephone tariffs. A 3-minute local call costs the equivalent of US$0.08, which is high compared to the tariff in El Salvador, Costa Rica and Panama (US$0.02 to US$0.06) but very low compared to the tariff in Mexico (US$0.14). Residential service does not have a fixed monthly charge (it is US$3 to US$13 in other Central American countries). The commercial tariff has a monthly fixed charge of US$5.57 which is very low compared to the commercial fixed charge in the range of US$6 to US$21 prevailing in other Central American countries.

International telephone tariffs. The competitive market has reduced the price of international calls significantly. A call from Guatemala to USA now costs US$0.10/minute. This has produced a strong increase in the level of international telephone traffic, which has reached 536 million minutes of incoming calls and 156 million minutes of outgoing calls annually.

Mobile telephone services tariffs. A very competitive market has also resulted in reduction of tariffs for mobile telephone services. A prepaid call costs 1.0 Q/minute (US$0.12), which is low compared to other Latin American countries, because of the very low fixed-to-mobile interconnection charge (US$0.015/minute). In Guatemala, the mobile telephone service works under “the calling party pays” system. The caller pays 0.356 Q/minute.

- 14 -

Internet Access. There are 80,000 users of the Internet. This is 0.7 % of the population, a figure comparable to El Salvador but very low compared to Mexico, Costa Rica and Panama (2.6 to 6.25 %). One of the reasons for the low access to the Internet is the high cost of a local call. One hour of Internet use costs Q 21.0. A flat tariff for Internet access may contribute to solve the cost problem, but the Law does not permit SIT to regulate Internet tariffs.

Rural and suburban telephone services. The institutional framework for rural and suburban telephone services is not clear in Guatemala. There are two institutions in charge of rural telephony. The lack of coordination leads to inefficient investments and duplication of efforts. On one hand, GUATEL is in charge of some 2,000 rural community telephones remaining after the separation and privatization of TELGUA in 1997. GUATEL also implemented new investment projects, such as a high capacity microwave network (63 E1) linking the Guatemala-Mexico border at a cost of US$5 million plus Q5.0 million financed with a private loan and a grant. This network links 1,000 communities. GUATEL also began to operate 3,000 suburban telephone lines it bought in suburban areas of Guatemala City before privatization. GUATEL has a staff of 300 and an annual operating deficit of about Q3.0 million (US$0.40 million). A rural telecommunications strategy, financed by the Project, pointed out various deficiencies in GUATEL’s operation and its investment programs, particularly the relatively high costs of its investment programs due to over-dimensioning of investment, use of inappropriate technologies and a need to finance the operations deficit.

On the other hand, the telecommunications law established FONDETEL to award subsidies under competitive bidding to private operators. FONDETEL is financed from the proceeds from the spectrum auctions in the telecom sector. In 1991-2001, FONDETEL awarded contracts to four enterprises for the installation of 7,063 telephone lines in 2,443 rural communities, using satellite and radio technology. The total subsidy was Q66.5 million (US$8.64 million) averaging a subsidy of Q9,415 (US$1,223.95) per line. FONDETEL has been structured on a basis similar to institutions in LAC and worldwide, which are considered best practices. Its main problem, however, is financing, as there would not be new revenues from the spectrum auctions. In other countries, the financing is often provided by a small levy (about 1%) of all sector revenues. In Guatemala, however, this would require a change of the law. The project provided support to FONDETEL in the design of its first operations and capacity building. Most importantly, however, the project financed a rural telecommunications strategy study, which identified the strengths and weaknesses in both GUATEL and FONDETEL and provided specific recommendations for improving the provision of the rural telecommunications services in Guatemala. Efficient use of resources is essential, given the continued deficit in rural telecommunications services. It is estimated that only 5,000 rural communities have access to telephones and another 45,000 have no access. In addition, the efforts have concentrated so far only on voice service. A strategy is needed to promote more advanced Information and Communication Technologies (ICT), including Internet and their applications for rural development.

Transport

Private participation in ports. Almost no progress has been achieved in terms of private participation in the ports sector. The present situation in the three main ports of Guatemala is not much different from what existed before the project started. Puerto Barrios is operated under a 25-year concession contract of which twelve years have elapsed. Puerto Barrios is the second most efficient port in Central America, which clearly shows the benefits of private sector participation and contrasts sharply with the performance of the other two major ports which are in public hands. In particular, the largest port, Puerto Santo Tomas is in bad condition, overstaffed with very low productivity and efficiency indicators. Some activities were leased to the private sector to increase efficiency, but greater private sector involvement is blocked by

- 15 -

powerful labor unions. Puerto Quetzal is in an intermediary position. Although it is state owned, a considerable number of operations are under private management. However, there is still significant room for improvement. For comparison, Puerto Barrios operates around 1.7 million tons a year with 70 employees, while Puerto Quetzal operates 5 million tons a year with 900 employees, and Santo Tomas operates 4.5 million tons with 1,500 employees. Although the project assisted the Government in drafting the new legal framework (Ley Portuaria y Maritima), the law has never been enacted. The Law would also establish a new maritime regulatory authority. By the closing date of the project, the draft law was still under discussion in the cabinet and among the stakeholders. This activity is currently followed by a separate technical assistance financed through a Public-Private Infrastructure Advisory Facility (PPIAF).

Private participation in roads. Only one concession has been operating since 1998: the highway from Palín to Escuintla, which is a segment of an important road between Guatemala and Puerto Quetzal. The Palín – Escuintla highway was constructed by the Government and concessioned to a private company, with an obligation to operate and maintain the road, and to build an additional US$22 million highway segment from Escuintla to Puerto Quetzal. Although this is a rather unusual arrangement (the concession usually involves the construction, operation and maintenance of the same road segment), the Ministry of Transport regards the four year operating experience with the concession as satisfactory. The concessioning process, however, was not supported by the project. The bidding process to select the concessionaire was deficient, as well as the environmental and social assessments.

Postal services

In 1997, the General Directorate of Post and Telegraph Services (Dirección General de Correos y Telégrafos, DGCT) entered into a five-year management contract with a private operator -- International Postal Services Ltd. (IPS) from Canada. Under the terms of the contract, IPS was required to provide basic postal services, known as “Official Mail” (letters up to 20 grams, delivery of all incoming international mail covered by the Universal Postal Union Convention, telegrams up to 20 words and money orders up to a value of US$1,000, and the Government's official mail). In return, IPS was to receive a set amount for each letter processed. Government’s objectives for these contracts were:§ Ensure an acceptable level of universal postal services for the entire country in terms of access, affordability and quality;§ Reduce the Government deficit associated with providing these services; and§ Increase private participation in the postal sector of Guatemala.

All these objectives were met. The postal service has improved significantly. All indicators, including coverage, efficiency and reliability have improved, while the requirements of subsidies were dramatically reduced: § Quality of service improvements: there were significant improvements in the quality of service, including quantifiable reductions in mail processing, transit and delivery times, as well as in customer claims and inquiries. § Productivity: The contractor was able to minimize labor disputes and significantly increase overall productivity while improving public perception of the postal service, its employees, and products. Total staffing was reduced from 2,300 to 940. The contractor has invested in upgrading postal facilities and management processes.§ Financial: For the years 1995-97, the postal services showed an operational deficit of US$23,110,056. During the first three years of the contract, this deficit was reduced to US$6,364,400. § Volume: While the volume of Official Mail handled by IPS has remained relatively stable, the mail handled by IPS outside the contract has increased significantly. In 2001, Official Mail accounted for only 1/7 of the total of 35 million pieces handled by IPS. These remaining 30 million pieces are mainly

- 16 -

commercial mail.

Despite this progress, however, with the benefit of hindsight, it appears that the subsidies paid to the private operator for the universal service delivery were set unnecessarily high, given that the business platform established for the universal service delivery can be used for commercial activities (courier services etc.). It should be noted, however, that the level of subsidies is still much lower than before the management contract, while the population at large has benefited from expanded coverage and improved quality and reliability of the service. Private participation in the postal service is quite rare in developing countries, and Guatemala can be considered one of the more successful examples.

The main issue, however, is the sustainability of these benefits. The management contract expires in 2003 and its future is uncertain. The project assisted the Government in preparatory works for the new arrangement – the Government was planning to bid out a 10-year concession, but the bidding process has been delayed due to political opposition in the Congress. Finally, the sector still lacks a new, comprehensive law (the current law dates back to 1907).

Municipal services

At the request of the Government, the project also financed activities related to municipal infrastructure (electricity, water and sanitation, and solid waste). These activities, however, were only complementary and were not a part of original project components. They were added to the original activities on specific request of the new Administration in 2000. The objective of this sub-component was to analyze possibilities for improving delivery of municipal infrastructure services through an introduction of private sector participation. The main problem is the poor financial condition of these municipal companies due to unsustainably low tariffs and various management and operational deficiencies. The project financed diagnostic studies and provided initial recommendations for improving the delivery of these services, involving private sector participation. The problem is particularly serious in the electricity sector, where 14 municipal distribution companies coexist with private concessionaires. These companies are highly indebted (they owe US$11 million for energy purchases from INDE) and are not able to comply with the minimum service standards set by CNEE. The most obvious solution would involve an integration of these small municipal companies with the private concessionaires. However, this would require an approval of municipal authorities that own these companies. The project has financed diagnostics studies and organized several workshops to discuss these issues with the municipal authorities and involve them in this process. Due to various implementation delays, however, no specific results were achieved by the closing date of the project.

4.3 Net Present Value/Economic rate of return:Fiscal Impact (see Annex 3)

The ICR reports only a global ex-post estimate of the benefits of the project because the project Implementation Unit (PIU) did not deliver the data requested by the Bank for the preparation of a more detailed analysis of the yield of all the actual benefits and costs incurred by the project. The ICR estimates project benefits at US$1,321 million (the proceeds of the privatization of EEGSA, GUATEL, DEOCSA and DEORSA). The PAD estimated project benefits at about US$750 million. It did not account for the proceeds of the sale of EEGSA. The PAD estimated project costs at about US$40 million corresponding to the severance packages for the agencies to be affected by a reduction in their work force (mainly GUATEL, DGCT and ports). The reduction of transfers to the Government caused by privatization of GUATEL was assumed to be recouped by the corporate tax levied on the new GUATEL, increases in VAT receipts and the potential expansion of a privatized infrastructure. The ICR did not have access to data on severance

- 17 -

packages. The ICR considers that the cost of the PPI project should also be added to the cost of privatization.

Proceeds from the sale of shares of privatized infrastructure (US$million)

Benefits ICR PADGUATEL 700 600DEOCSA and DEORSA 101 100EEGSA 520 --Other infrastructure 0 50TOTAL 1,321 750

The US$101 million from privatization of DEOCSA and DEORSA are being used for expanding rural electrification.

Cost estimate of privatization (US$ million)Costs ICR PADSeverance packages * 40.0Debt reduction * 250.0Project cost 18.5 18.5TOTAL 18.5+ 308.5

Note: (*) Information not provided to the Bank by the Borrower.

4.4 Financial rate of return:Not available.

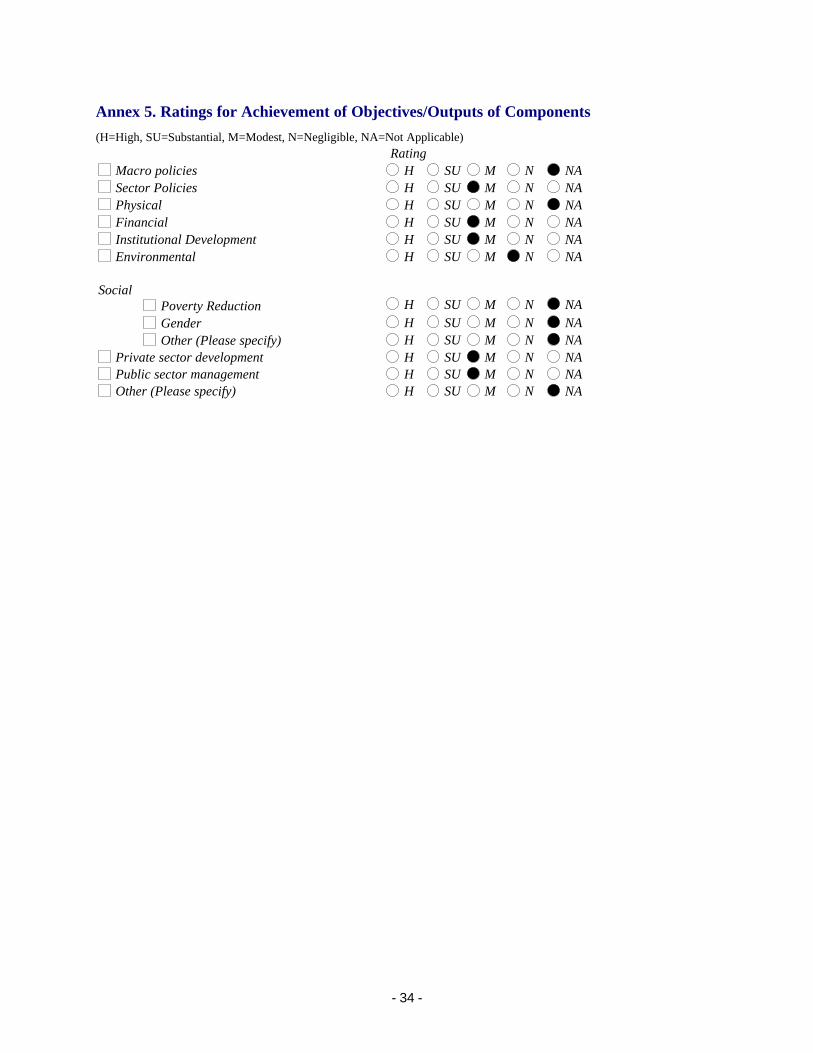

4.5 Institutional development impact:The project had important institutional development impacts, particularly in the power and telecommunications sectors. The project contributed to the creation and strengthening of the key institutions in these sectors, particularly the new regulatory agencies (CNEE and SIT), as well as the wholesale market operator, AMM. These institutions are now firmly established, staffed adequately and working satisfactorily. Their autonomy has been respected by the Government (by both administrations). Less progress was achieved in transport and postal sectors. Despite some capacity-building activities for the policy-making bodies, the institutional situation of these sectors remain weak. Both policy-making and regulatory functions for these sectors remain in the Ministry of Communications, Infrastructure and Housing, with weak capacity and inadequate human and financial resources. All matters related to private sector participation in these two sectors are handled by the Concessions Unit, staffed with only one professional. In other words, the institutional development impact was significant in the power and telecommunications sectors, but insignificant in the other sectors. Therefore, the overall institutional development impact of the project is rated as modest.

5. Major Factors Affecting Implementation and Outcome

5.1 Factors outside the control of government or implementing agency:The project was affected negatively by difficulties in obtaining Congressional approvals. This included a delay in project effectiveness for over a year, difficulties in passing sector legislation prepared by the project, and difficulties in approving a budget for the project in its last two years of implementation. This reflects a lack of broader political support for the project. Failure to secure Congressional approval for the project’s budget (its inclusion in the national budget) in 2002 was the main reason why the Bank could not

- 18 -

respond positively to Government’s late request to consider an additional (second) extension of the loan’s closing date (discussed below).

5.2 Factors generally subject to government control:The weak ownership of the project demonstrated by the Guatemalan Government is the main factor that contributed to the unsatisfactory implementation of the project and the failure to achieve all its objectives fully. The previous Administration demonstrated a strong ownership of the project, particularly during the preparation and in early years of the project. The key sector legislation for electricity and telecom projects were passed in 1996-1997, and the power and telecommunications companies were privatized by 1998, before the project could enter into effectiveness. Project implementation slowed in 1999, due to approaching elections, and the initial pace was never restored. The two Administrations were vocal in stating they had project ownership but tepid in taking the actions to achieve the project objectives during the implementation stage. Only by mid-2002, a few weeks before the planned closing date of the project, the Government’s attitude seemed to have changed. The Government approved a new policy document – Economic Action Plan 2002-2004, calling for comprehensive reforms and introduction of private participation in ports, airports, roads and postal sectors. Regrettably, that request was too late to rescue the project, and the extension did not materialize.

5.3 Factors generally subject to implementing agency control:Project coordination and administration were centralized in a Presidential commission that adopted several names (OCMOE, COMODES and lately COPRE) reflecting various Government reorganizations. COPRE (Comisión Presidencial para la Restructuración del Estado) is the latest name of the project unit. More important than the change in names, however, were changes in COPRE’s roles and responsibilities that negatively affected project implementation. Initially, OCMOE was an agency in charge of privatization and policy/regulatory reforms for all infrastructure sectors. The new Administration, however, changed the agency to COPRE, with the main objective to support the Government’s decentralization efforts. That shifted COPRE’s attention away from project implementation, which was no longer considered its core activity. COPRE also had a major change of director and staff when the new Administration took office in January 2000. The new staff of COPRE had no experience in managing technical assistance operations with Bank financing involving a large number of activities to be coordinated with many Government units. Moreover, COPRE staff was not sufficiently familiar with the Bank's procurement guidelines, a factor that negatively affected coordination with the UNDP and the Bank. Poor coordination and lack of interest in the project activities, compounded with procurement problems, contributed to a very slow pace and near stagnation of the project implementation. Appropriate and timely training of COPRE staff might have helped to moderate some of these problems.

5.4 Costs and financing:At appraisal, the total project cost estimate was US$18.5 million. At loan closing (August 31, 2002), the project cost estimate was also US$18.5 million based on the assumption that the Government may later complete the project without Bank financing. About US$8.0 million have been disbursed from the US$13.0 million Bank loan to finance studies, training, office technology equipment, the UNDP procurement agent and project administration. The remainder of the Bank loan will be cancelled once UNDP submits a final statement of expenditures of the advances received from the Bank. The main reasons for the lower utilization of the Bank loan were the delays in project implementation. The Government financed US$5.0 million of the cost of preparing the new Electricity and Telecommunications Laws, the initial implementation of the power sector reform and the privatization of GUATEL. The Bank recognized those costs as a retroactive contribution of the Government to project financing. The USAID co-financed the preparation of the General Electricity Law and the amendment to the Telecommunications Law with a contribution of US$0.5 million. By the closure of the project, about US$5 million still

- 19 -

remained undisbursed. At the last minute, in June 2002, the Government requested an extension to finance its new ambitious reform program for infrastructure sectors, with a particular focus on transport. The Borrower intended to allocate the remaining of the Bank loan to the activities shown in the table below. In some sense, this table also indicates the scope of activities that could have been and were not implemented by the project.

Table - Activities not implemented by the project Ministry of Communications, Infrastructure and Housing (MCIVI) - General Legal & Regulatory Framework for Concessions 150,000 - Consultants/Advisors and Strengthening of 225,000 Unidad de Concesiones y Desincorporaciones MCIV - Postal Service Concession 150,000 - Legal & Regulatory Framework Ports/Maritime 100,000 - Ports Concessions 625,000 - Strategy for Airports Concession 350,000 - Roads Concessions 1,200,000 - Strategy Restructuring of FONDETEL/GUATEL 300,000 - Implementation of Rural Telephony/Universal Service 300,000 Sub-total 3,400,000 Electricity - Ministry of Energy and Mining (MEM) - Technical Support and Strengthening of Regulator (CNEE) 300,000 - Technical Support to Implement Rural Electrification Strategy 150,000 - Strategy for Promotion of PP in Energy Projects 50,000 - Concession of INDE Small Hydro and Thermal Plant 250,000 - Concession of INDE Zunil Geothermal Generation 250,000 Sub-total 1,000,000 Training and Knowledge Transfer (Global) 300,000 Coordination & Implementation Units (Global) 500,000 Total (US$) 5,200,000

6. Sustainability

6.1 Rationale for sustainability rating:The sustainability of the project's achievements in the power and telecommunications sectors is likely unless the Government, the Congress or extreme political shifts attempt to return these sectors back to state control – a situation considered highly unlikely for the medium term. However, the reform of the power sector may become partially jeopardized, if the Government yields to political pressure to subsidize retail tariffs, bypassing CNEE’s responsibilities and autonomy in tariff-setting areas. Sustainability of postal sector achievements remains an issue. Although the management contract produced important improvements in terms of the coverage, transit time and costs of the universal service, these achievements may be lost quickly if the postal service goes back to Government control. At the time of this ICR, it is still uncertain if the Government will succeed in implementing a new PPI arrangement (concession or another management contract) for this sector. Since little was achieved by the project in the other infrastructure sectors, there is little to rate on sustainability. All things considered, the sustainability of this incomplete

- 20 -

project is rated as uncertain.

6.2 Transition arrangement to regular operations:The sector reforms in telecommunications and electricity sectors, supported by the project, have been largely concluded and no transitional arrangements to regular operations are necessary. For the postal sector, the Government has announced its plan to bid-out longer-term concession (up to 10 years). This policy action, however, still needs to be implemented. In addition, the Government adopted an Economic Action Plan for 2002-2004, based primarily on reforms and increasing private sector participation in the transport sector. The tables below depict a summary picture of the Economic Action Plan for the infrastructure sector and show that most of the works of the Plan and three of the proposed Laws are for the transport sector.

Table - Works included in the Economic Action Plan 2002-2004

Roads SectorConstruction of the Metropolitan RinglConstruction of North Highway (it could be on the border with Belice or México)lConstruction of the Tecún Umán Highway to Pedro de Alvarado citylConstruction of the New Pacific Coast HighwaylRehabilitation and enlargement of the Guatemala – El Rancho Highwayl

Ports SectorSanto Tomás de Castilla PortlQuetzal Portl

Airport SectorOperation of La Aurora International AirportlConstruction of a New International AirportlOperation of the Santa Elena Airport in Petenl

Electricity SectorEscuiltla Thermal Power PlantlComplete the Central America Interconnection ProjectlGeothermal Fields Zunil I y IIlGuatemala-Mexico Electrical InterconnectionlSale of small hydroelectric stationsl

- 21 -

Table - Laws proposed in the Economic Action Plan 2002-2004

1. Public works comcession framework law 2. Production and use of alcohol-based fuel 3. Fiscal incentives for energy generation with renewable resources 4. Stock and Securities Market 5. Non-bank financing intermediaries 6. Maritime and Air Authorities 7. Non conventional guarantees 8. Quality System 9. Weight and size of motor vehicles 10. Consumer protection 11. Promotion of competitiveness 12. National Law for public investment

7. Bank and Borrower Performance

Bank7.1 Lending:As noted before, from the onset the Bank promoted and supported the Government’s program of reform and modernization of the public sector. The identification of the project considered the reform and rehabilitation of the power sector within the overall program of reform and the Bank’s strategy as established in the CAS. At appraisal the Bank ensured that the objectives and components of the project were consistent with the overall program and provided the tools to the executing agencies to tackle the complexity of the project, through training, provision of technological equipment and funds for hiring consultants. Therefore, the lending performance of the Bank is rated satisfactory.

7.2 Supervision:In spite of the high rotation of project management (from appraisal to closing of the project there were four task managers), in general the Borrower received an adequate orientation and support through 11 supervision missions and intensive desk supervision. The supervision missions were less frequent in 1997 due to delays in effectiveness and in 1999 due to elections. Supervision was particularly intensive in 2000 (four supervision missions) when the new Administration assumed office.