Workshop: Introduction to Private...

73

Teheran, 28 th of April, 2016 Omer Rehman/Beate Rupp Workshop: Introduction to Private Equity

Transcript of Workshop: Introduction to Private...

1

Teheran, 28th of April, 2016

Omer Rehman/Beate Rupp

Workshop: Introduction to Private Equity

We are no bank.

We finance entrepreneurial opportunities.

Alpine Equity

successfully takes mid-sized

companies international.

Omer Rehman

4

• Master in Business Administration, University of Innsbruck

• PhD in Business Administration, Stockholm School of Economics and Vienna University

• Creditanstalt AG (Bank Austria/UniCredit), Austria– Retail & commercial banking– Special projects

• Roland Berger Strategy Consultants, Austria/CEE/Russia– Growth strategy consulting– M&A activities– Restructuring projects– Post-merger integration projects

• Alpine Equity Management AG, Austria– Co-founder and Managing Director– Various Board memberships– Member of the Board of Austrian Private Equity Association

Omer Rehman

Omer Rehman

5

Beate Rupp

• Master in Business Economics, University of Innsbruck/Vienna

• Executive MBA City University/Cass Business School, London

– Focus Finance and Strategy

• Bayerische Hypovereinsbank, New York

– Internship

• Deloitte, Vienna

– Senior Audit Assistant

– Audit of (investment) banks, private equity funds etc.

• Alpine Equity Management GmbH

– Investment manager, authorized representative

– Assessment and execution of new investments

– Support and development of portfolio investments

– Exit execution

Beate Rupp

6

6

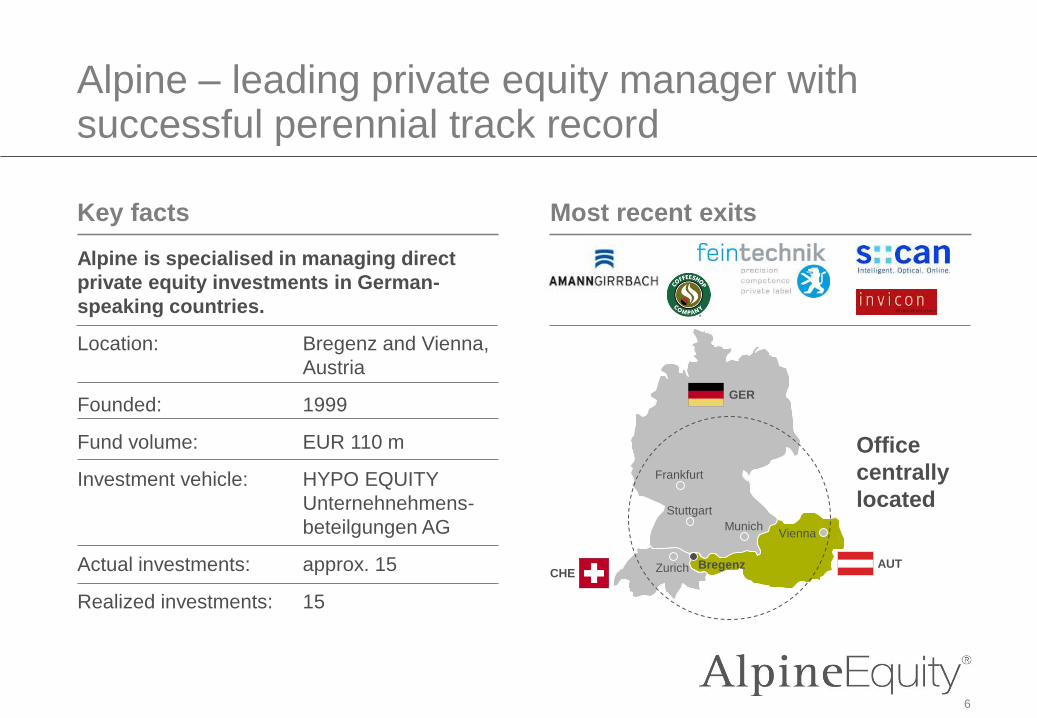

Alpine – leading private equity manager with successful perennial track record

Key facts Most recent exits

Alpine is specialised in managing direct

private equity investments in German-

speaking countries.

Location: Bregenz and Vienna,

Austria

Founded: 1999

Fund volume: EUR 110 m

Investment vehicle: HYPO EQUITY

Unternehnehmens-

beteilgungen AG

Actual investments: approx. 15

Realized investments: 15

Office

centrally

located

Bregenz

Vienna

Zurich

Munich

Stuttgart

Frankfurt

GER

AUTCHE

7

Short introduction to Alpine Equity

• Private equity for medium-sized

companies

– Succession solutions

– MBO/MBI

– Growth capital

– Turnarounds

• Strategy: Internationalisation of mid-

sized businesses

• Volume: ca. EUR 110 m

• Dental technology – 6 years:

– Entry: EUR 7 m

– Exit: EUR 47 m

• Packaging – 2 years:

– Entry: EUR 12 m

– Exit: EUR 30 m

• Razor blades – 6 years:

– Entry: EUR 22 m

– 2013: EUR 52 m

Strategy and Focus Examples − Sales development

8

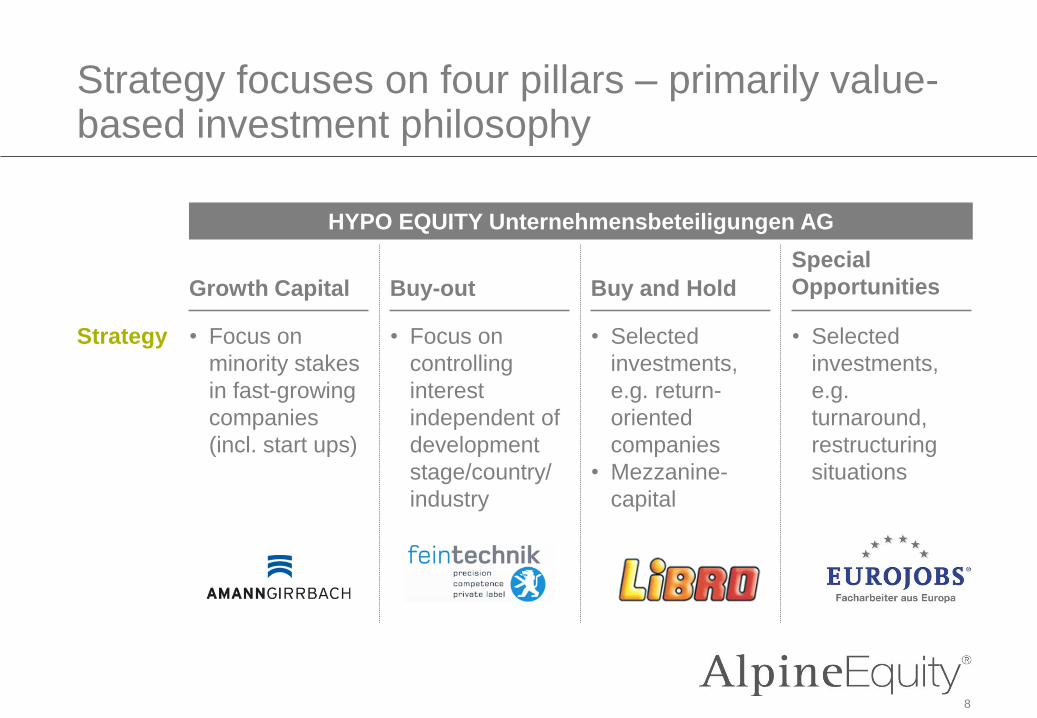

Strategy focuses on four pillars – primarily value-based investment philosophy

Strategy • Focus on

controlling

interest

independent of

development

stage/country/

industry

Buy-out

• Focus on

minority stakes

in fast-growing

companies

(incl. start ups)

Growth Capital

• Selected

investments,

e.g. return-

oriented

companies

• Mezzanine-

capital

Buy and Hold

• Selected

investments,

e.g.

turnaround,

restructuring

situations

Special

Opportunities

HYPO EQUITY Unternehmensbeteiligungen AG

9

Structure – sketch of current fund set up

Management

HUBAG

Insurance compsBanks

Investment CInvestment A Investment B

Family Offices

Alpine Equity

Management GmbH

Management contract

10

Overview

A. Introduction to Private Equity

B. Global/European Private Equity Market

C. Case Studies: Types of Private Equity Investors

D. Case Studies: Mid-Market Segments

E. Case Study: FinTech

F. Legal Environment

G. Investment Philosophy

H. Key Considerations for Setting Up a Fund

I. Conclusion and Next Steps

11

Overview

A. Introduction to Private Equity

B. Global/European Private Equity Market

C. Case Studies: Types of Private Equity Investors

D. Case Studies: Mid-Market Segments

E. Case Study: FinTech

F. Legal Environment

G. Investment Philosophy

H. Key Considerations for Setting Up a Fund

I. Conclusion and Next Steps

12

What is private equity?

• Direct participation in equity

• Co-entrepreneurship

• Make the investment more valuable by developing the

company

• Sell the portfolio company after three to six years

13

Private equity is not a new development – early types date back to the 15th century

The history of private equity (selected examples)

Source: Leopold/Frommann: "Eigenkapital für den Mittelstand"; Roland Berger Strategy Consultants

Since early days entrepreneurs and adventurous people cooperate

to make money with innovative but risky ideas

1) Industrial and Commercial Finance Corp. (heute: 3i Group plc.) 2) American Research and Development Corporation

15th century 16th century 19th century 20th century

• In 1492, Columbus

discovered America.

• Roughly 85 % of the

exploration costs were

mainly financed by the

Spanish crown

• In 1572, Sir Francis

Drake became a

famous pirate

• 50 % of the prey went

to the British crown

• Drake‘s sponsors still

generated 4700%

return on their capital

invested

• In 1830, Hamburg

native banker Mr.

Heine founded a bank

for craftsmen and and

industrials (Vor-

schusskasse) – first

German subsidy

scheme for founders

• In 1945, the ICFC1)

was founded in the

UK

• In 1946, the first

independent

institutional equity

investor (AR&D2)) was

founded in the US

• In 1965 first VC/PE

funds emerged in

Germany

…

14

Typical private equity examples in the past years

15

What's the difference

Mezzanine

Capital

• Equity in very early stages (no or very little sales and losses)

• Typically 90% of investments fail; IRR expectation > 30%

• Professional VCs, Angel investors, crowdfunding

Venture

Capital

Private

Equity

• Equity for established, fast growing companies

• Success rate far higher than for VC investments

• IRR expectation roughly 20%

• Equity-like financing of cash-flow strong firms

• Subordinate loans with higher interest and equity kicker

• Typical IRR 13-18%

16

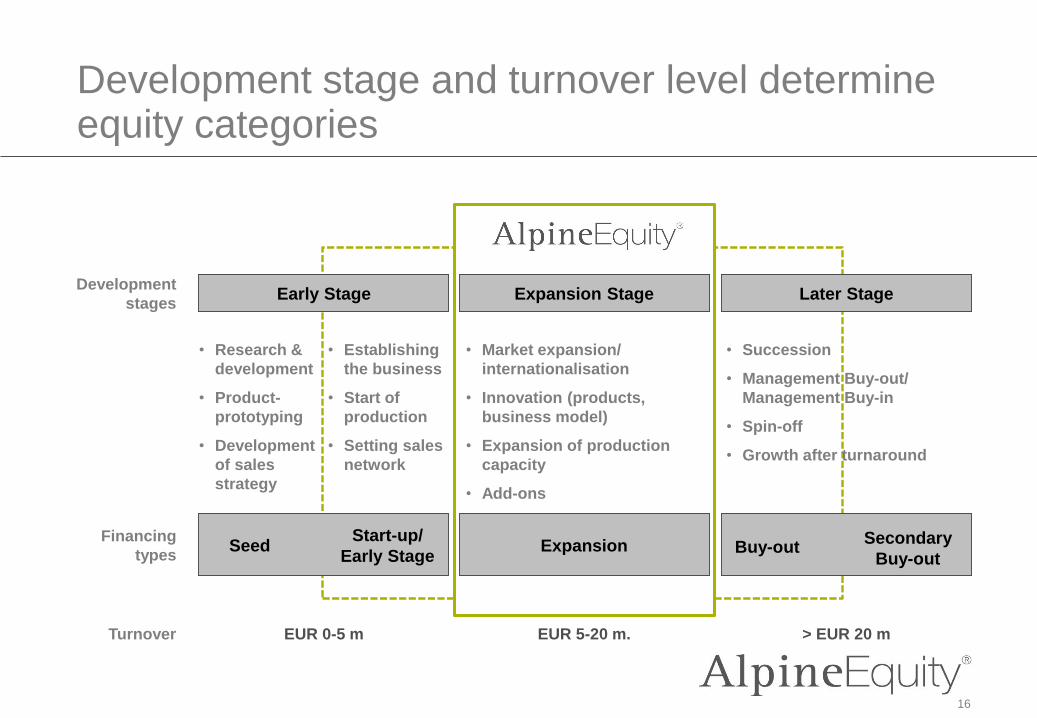

Development stage and turnover level determine equity categories

Early Stage Expansion Stage Later StageDevelopment

stages

ExpansionFinancing

types

Start-up/

Early StageSeed Buy-out

Secondary

Buy-out

Turnover EUR 0-5 m EUR 5-20 m. > EUR 20 m

• Succession

• Management Buy-out/

Management Buy-in

• Spin-off

• Growth after turnaround

• Market expansion/

internationalisation

• Innovation (products,

business model)

• Expansion of production

capacity

• Add-ons

• Research &

development

• Product-

prototyping

• Development

of sales

strategy

• Establishing

the business

• Start of

production

• Setting sales

network

17

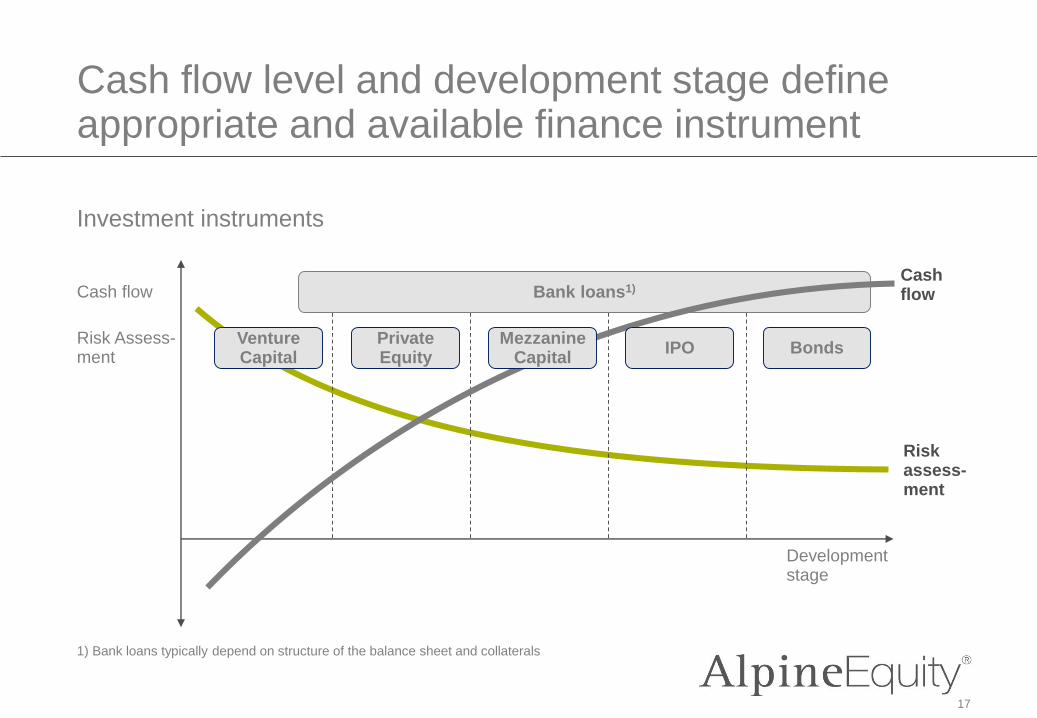

Cash flow level and development stage define appropriate and available finance instrument

Cash flow

Development stage

Investment instruments

Bank loans1)

1) Bank loans typically depend on structure of the balance sheet and collaterals

Cash flow

Risk assess-ment

VentureCapital

PrivateEquity

MezzanineCapital

IPO BondsRisk Assess-ment

18

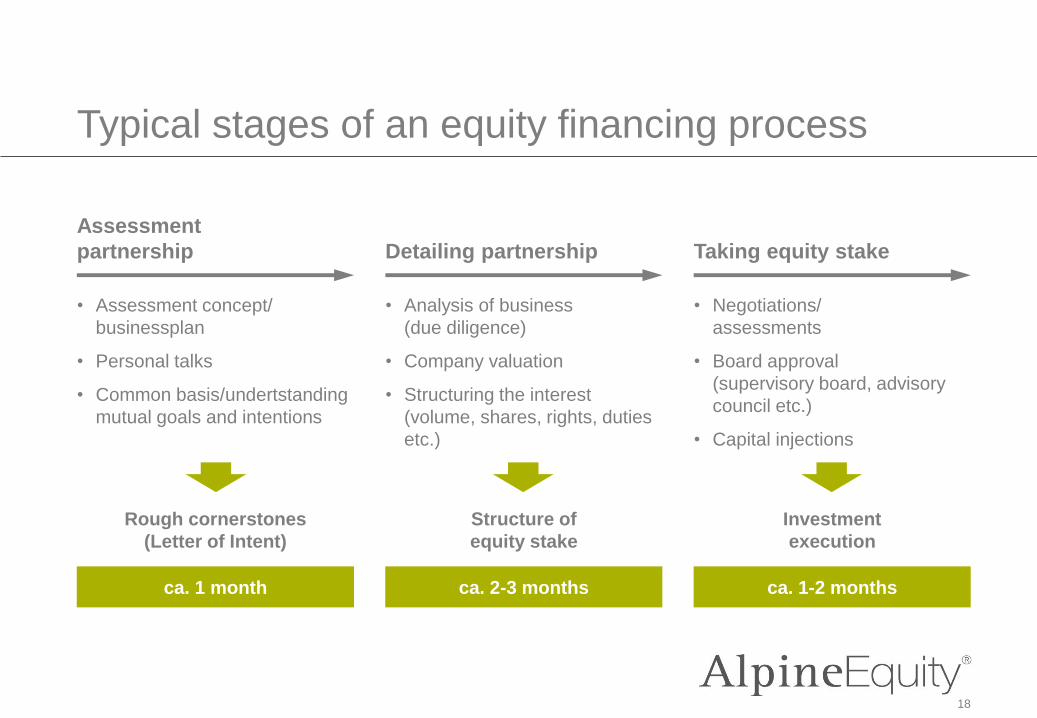

Typical stages of an equity financing process

Assessment

partnership

ca. 1 month ca. 2-3 months ca. 1-2 months

Detailing partnership Taking equity stake

Rough cornerstones

(Letter of Intent)

Structure of

equity stake

Investment

execution

• Assessment concept/

businessplan

• Personal talks

• Common basis/undertstanding

mutual goals and intentions

• Analysis of business

(due diligence)

• Company valuation

• Structuring the interest

(volume, shares, rights, duties

etc.)

• Negotiations/

assessments

• Board approval

(supervisory board, advisory

council etc.)

• Capital injections

19

Leveraged buyout (LBO) process – what it really means

Purchase of the Chicken Inc.

1

Reducing the staff

3

And with the rest … On the stock exchange !

5

Asset stripping

4

Replacement of the management

2

20

Private equity is a cyclical business …

2000-07

Liquidity increase

Credit bubble

1990-99

GDP growth

Multiple expansion

1980-89

Inefficient conglomerates

Prospering junk bond market

0

200

400

600

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12

US buyout deal value [USD billion]

Source: Bain US LBO deal database

21

Private equity managers mainly apply three drivers to increase company value

• Finance relationship between equity, debt and mezzanine

capitalLeverage Effect1

• Value leverage to increase company valueMultiple Expansion2

• Focus on sustainable increase of annual results (cost

reduction, productivity, employee contribution)Earnings Growth3

Value driver Description

22

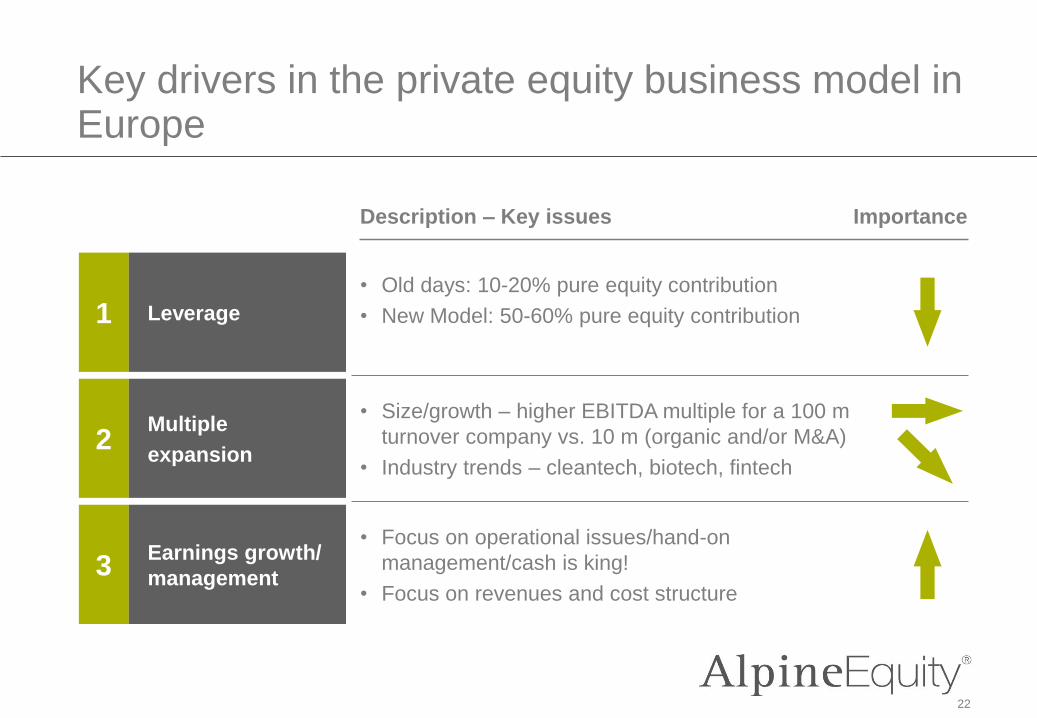

Key drivers in the private equity business model in Europe

1 Leverage

2Multiple

expansion

3Earnings growth/

management

• Old days: 10-20% pure equity contribution

• New Model: 50-60% pure equity contribution

Description – Key issues Importance

• Size/growth – higher EBITDA multiple for a 100 m

turnover company vs. 10 m (organic and/or M&A)

• Industry trends – cleantech, biotech, fintech

• Focus on operational issues/hand-on

management/cash is king!

• Focus on revenues and cost structure

23

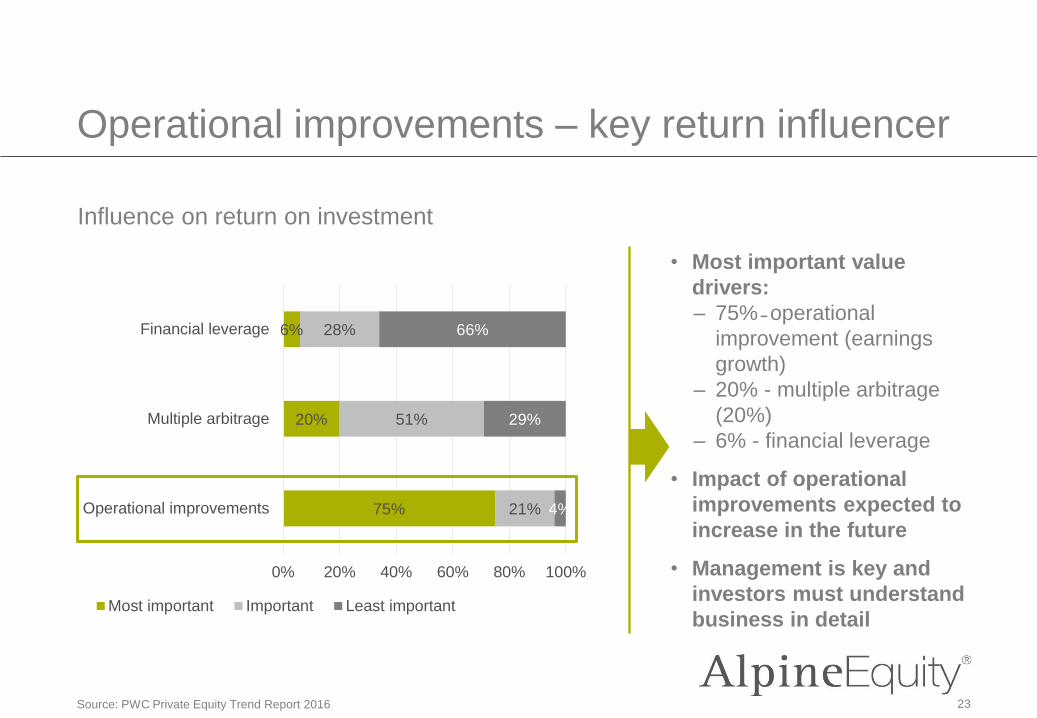

Operational improvements – key return influencer

Source: PWC Private Equity Trend Report 2016

75%

20%

6%

21%

51%

28%

4%

29%

66%

0% 20% 40% 60% 80% 100%

Operational improvements

Multiple arbitrage

Financial leverage

Most important Important Least important

• Most important value

drivers:

– 75% ̵ operational

improvement (earnings

growth)

– 20% - multiple arbitrage

(20%)

– 6% - financial leverage

• Impact of operational

improvements expected to

increase in the future

• Management is key and

investors must understand

business in detail

Influence on return on investment

24

Leverage Effect – Optimizing the finance structure can lead to higher performance

Example – Buy-out1)

1) Assumption: Tax effect not considered

• Purchase of a business for EUR 100 m (100%)

• Exit business after 5 years for EUR 200 m

Initial

situation

Financing

models

[EUR m]

Multiple

[EUR m]

Equity

Debt

Mezzanine

Equity

100

––

100

Equity+Debt

45

55

–

100

Eq.+Deb.+Mezz

30

55

15

100

1

Exit

Debt+interest

Mezz.+interest

200

–

–

200

200

69

–

131

200

69

25

106

2 3

Multiple 2.0 2.9 3.5

1

25

Multiple expansion – raise company value through strategic repositioning

Extension of value chain – e.g.

producer with higher valuation

compared to pure merchant

M&A

Size & consolidation

Consolidation of (e.g.

regionally) fragmented

industries by organic

growth and/or buy-and-

build strategy

Industry trends as main

drivers – e.g. FinTech,

disruptive business models

Industry trends

Multiple Expansion

2

26

Earnings growth – both income and cost focus for sustainable increase of profits

Costs

• Ongoing optimization

• Sale of non-core assets

• Lean structures/ outsourcing

assessment

Sales/

Gross

profit

• Growth strategy

• Focus on margin and turnover

• M&A/consolidation/buy and build –

income synergies

Strategy

Continuous optimization

Sales/GP

Costs

3

Private equity: increase of profits as ultimative goal/

no 'principle of hope'

27

Typical exit routes

• Synergies

• Improve product

pipeline

• High cash piles –

low interest rates

Strategic

buyers

Financial

sponsorsMBO/MBI IPO Write-offs

30% 5% 5% 30%30%

• Business model

• A lot of money at

hand ('dry powder')

• Current employee/

industry insider

• Become

entrepreneur

• Current

shareholders keep

influence in

company

• BUT: volatile

capital markets

• Failed strategy

• Outdated business

model

• Unaffordable

restructuring costs

• etc.

Occurence

Investment

Motives

Source: Alpine Equity Analysis

28

Overview

A. Introduction to Private Equity

B. Global/European Private Equity Market

C. Case Studies: Types of Private Equity Investors

D. Case Studies: Mid-Market Segments

E. Case Study: FinTech

F. Legal Environment

G. Investment Philosophy

H. Key Considerations for Setting Up a Fund

I. Conclusion and Next Steps

29

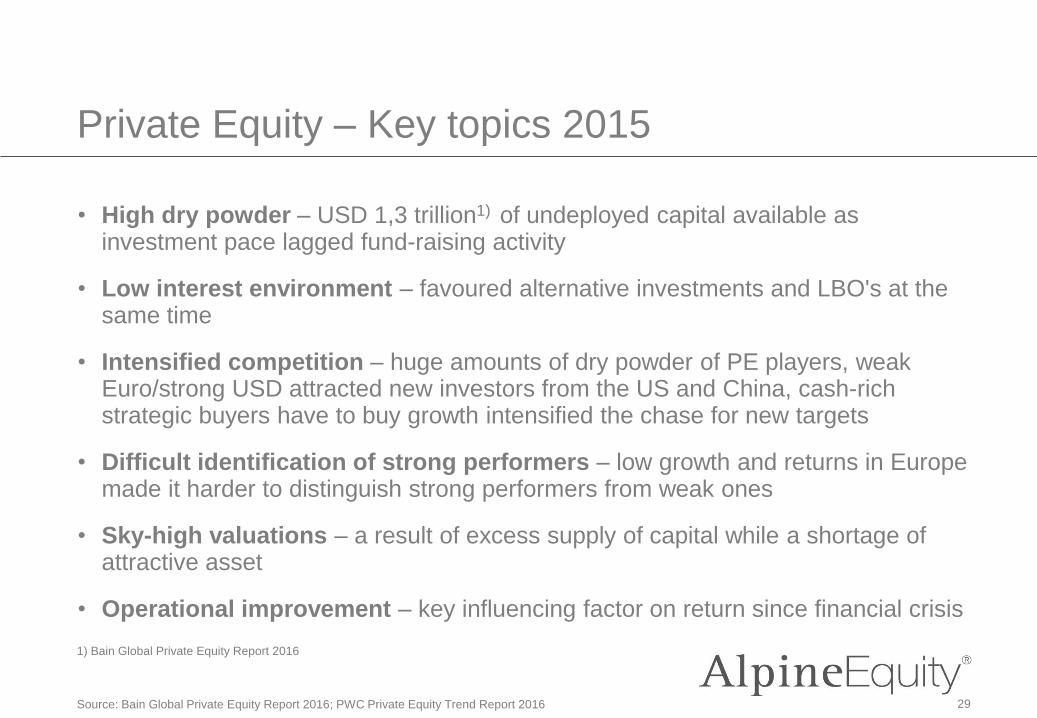

Private Equity – Key topics 2015

1) Bain Global Private Equity Report 2016

• High dry powder – USD 1,3 trillion1) of undeployed capital available as investment pace lagged fund-raising activity

• Low interest environment – favoured alternative investments and LBO's at the same time

• Intensified competition – huge amounts of dry powder of PE players, weak Euro/strong USD attracted new investors from the US and China, cash-rich strategic buyers have to buy growth intensified the chase for new targets

• Difficult identification of strong performers – low growth and returns in Europe made it harder to distinguish strong performers from weak ones

• Sky-high valuations – a result of excess supply of capital while a shortage of attractive asset

• Operational improvement – key influencing factor on return since financial crisis

Source: Bain Global Private Equity Report 2016; PWC Private Equity Trend Report 2016

30

In 2015, the industry spent USD 282 billion to acquire companies

422

0

100

200

300

400

500

600

2011 12 13 14 15

527

0

100

200

300

400

500

600

2011 12 13 14 15

282

0

100

200

300

400

500

600

2011 12 13 14 15

USD 500 bn USD 500 bnUSD 600 bn

Source: Bain Global Private Equity Report 2016

• Cash-rich strategic buyers bought growth

• Rich M&A activity

• Cash distributions run well ahead of calls of LPs

• Abundant fresh capital facilitated fund raising

• Sky-high valuations• Growing uncertainty in debt

markets

Global buyout exits Global buyout funds raised Global buyout investments

31

Private equity compared with Iranian figures

1) USD 422 bn / USD 415 bn GDP Iran2) USD 282 bn global buyout investments / USD 415 bn GDP Iran 3) USD 527 bn funds raised / 78 million Iranians

1 xGlobal buyout exits equal Iran's GDP1)

USD 6,750per Iranian citizen equals total global buyout funds raised3)

~70%of the Iranian GDP

invested in buyouts2)

Source: Bain Global Private Equity Report 2016; Roland Berger How to do business in Iran

32

Buyouts are dominating

25%

Buy-out

75%

Other

1) As of 2014 – total European investments

2) Seed: Financing provided to research, assess and develop initial concepts before a business has

reached the start-up phase

3) Start-up: financing provided for product development and initial marketing. Companies have not yet

sold their product commercially.

4) Later-stage venture: financing expansion of company which might or might not be break-even yet.

Probably company has already been backed by venture capital firms.

Source: EVCA 2014 European Private Equity Activity

Overview1) Segment Type

• Buy-out

• Venture

Capital

• Growth

capital

• Special

opportunity

MBO/LBO

Seed2), start-up3), later-stage

venture4)

Minority stakes/

expansion capital

Replacement capital/

restructuring

33

LBO-valuations are up again – in the US record highs were hit!

Source: Bain Global Private Equity Report 2016

5 5,1

6

4,8

3,7

4,64,9

5,15,3

5,85,5

20

05

06

07

08

09

10

11

12

13

14

H1 1

5

EBITDA multiple for LBO transactions

5,25,4

6,1

5,2

4,04,4 4,5 4,6 4,7

5,14,9

20

05

06

07

08

09

10

11

12

13

14

H1 1

5

Ø 9.2 x

EBITDA multiple for LBO transactions

Ø 8.9 x

US Europe

34

--- Beate Only ----

5,0 5,1

6,0

4,8

3,7

4,64,9

5,15,3

5,85,5

20

05

06

07

08

09

10

11

12

13

14

H1 1

5

5,25,4

6,1

5,2

44,4 4,5 4,6 4,7

5,14,9

20

05

06

07

08

09

10

11

12

13

14

H1 1

5

Ø 4.9 xØ 5.1 x

Source: Bain Global Private Equity Report 2016

Average debt-to-EBITDA multiples for LBOtransactions

Average debt-to-EBITDA multiples for LBOtransactions

US Europe

35

How private equity contributes to Europe's economy

€ 307 bninvested by private equity in Europeancompanies from 2007 to 2013 in the12 largest private equity markets in Europe

5,600new business created every year in Europe, either through direct investment or via a "spillover" effect, caused by knowledge sharing, networking and inspiring role models

4.5-8.5 %the percentage by which private equity backing improves the operating performance of portfolio companies during the first three years of investment

25.000companies backed by private equity in Europe …

83%… of which are SMEs

€ 350 bnis the economic value of patents granted to private equity-backed companies in Europe between 2006 and 2011

Up to

50 %the percentage by which private equity-backed companies are less likely to fail than non-private-equity-backed companies with similar characteristics

12 %of all industrial innovation in Europe is attributable to private equity-backed companies

> 50 %of the total invested into European private equity in 2013 came from outside Europe

Source: EVCA Private Equity‘s cntribution to building European businesses

Euro investment Competitiveness Productivity

Innovation

36

Fundraising was rather cyclical in the last years –funds have to find a sweet spot

Fundraising of European PE-Firms [EUR bn]

80

1922

42

25

54

45

2008 09 10 11 12 13 14

• Private equity established as

asset class

• Fund of funds, insurances and

high-net worth individuals as

crucial investors

• Fundraising is becoming a

challenge; investors need to

differentiate themselves from

peers and find a sweet spot in

order to impress new investors

with superior success rates

Source: 2014 EVCA European Private Equity Activity; Bain Global Private Equity Report 2016; PWC Private Equity Trend Report 2016; Alpine Equity Analysis

37

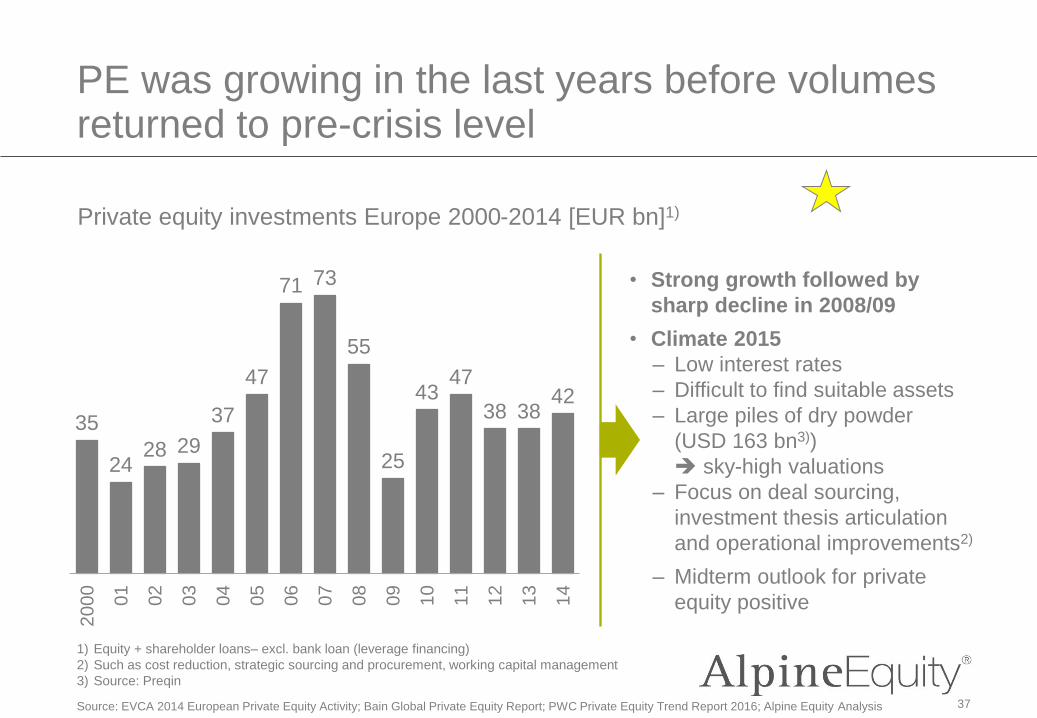

PE was growing in the last years before volumes returned to pre-crisis level

Private equity investments Europe 2000-2014 [EUR bn]1)

Source: EVCA 2014 European Private Equity Activity; Bain Global Private Equity Report; PWC Private Equity Trend Report 2016; Alpine Equity Analysis

• Strong growth followed by

sharp decline in 2008/09

• Climate 2015

– Low interest rates

– Difficult to find suitable assets

– Large piles of dry powder

(USD 163 bn3))

sky-high valuations

– Focus on deal sourcing,

investment thesis articulation

and operational improvements2)

– Midterm outlook for private

equity positive

35

2428 29

37

47

71 73

55

25

4347

38 3842

2000

01

02

03

04

05

06

07

08

09

10

11

12

13

14

1) Equity + shareholder loans– excl. bank loan (leverage financing)

2) Such as cost reduction, strategic sourcing and procurement, working capital management

3) Source: Preqin

38

Private equity investors favour just five industries

0% 2% 4% 6% 8% 10% 12% 14% 16%

Unclassified

Real estate

Agriculture

Transportation

Chemicals and materials

Construction

Energy and environment

Financial services

Business & industrial services

Consumer services

Communications

Business & industrial products

Life sciences

Consumer goods & retail

Computer & consumer electronics

Source: EVCA 2014 European Private Equity Activity

All private equity Europe – investments by sector 2015 [%]

2/3 of all

investments

39

90% of investments go into established companies

3,6

3,7

3,3

3,4

1,6

2010

2011

2012

2013

2014

Venture Capital[EUR bn]

6,3

5,2

4,0

3,6

1,6

2010

2011

2012

2013

2014

Growth Capital[EUR bn]

29,7

28,1

28,0

31,3

2010

2011

2012

2013

2014

Buyout Capital[EUR bn]

2,3

1,5

1,4

1,3

1

2010

2011

2012

2013

2014

Turnaround/replacement capital[EUR bn]

8,7%

13,5% 75,4%

2,4%

Source: EVCA 2014 European Private Equity Activity

40

EVCA – legend

Venture CapitalSeed

Financing provided to research, assess and develop an initial concept before a business has reached the start-up phase

Start-up

Financing provided to companies for product development and initial marketing. Companies may be in the process of being

set up or may have been in business for a short time, but have not sold their product commercially.

Later-stage venture

Financing provided for the expansion of an operating company, which may or may not be breaking even or trading profitably.

Later-stage venture tends to finance companies already backed by venture capital firms.

GrowthA type of private equity investment – most often a minority investment but not necessarily – in relatively mature companies

that are looking for capital to expand operations, restructure operations or enter new markets.

BuyoutFinancing provided to acquire a company. It may use a significant amount of borrowed money to meet the cost of acquisition.

Rescue/TurnaroundFinancing made available to an existing business, which has experienced trading difficulties, with a view to re-establishing

prosperity.

Replacement capitalThe purchase of a minority stake of existing shares in a company from another private equity firm or from another

shareholder or shareholders.

Source: EVCA 2014 European Private Equity Activity

41

Private equity outperforms compared indices in the long-run

Evolution of comparators – 5-year rolling IRRs [%]

-10%

-5%

0%

5%

10%

15%

20%

25%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

FTSE: 3.3%

JP M.: 8.4%

HSBC: 4.4%

Average IRR

PE: 8.5%

Source: EVCA 2013 Pan-European Private Equity Performance Benchmarks Study

JP Morgan Euro Bonds (EMBI+)

European Private Equity

HSBC Small Company Equity

FTSE Europe

42

Buyouts outperform both venture and generalist investments

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Source: EVCA 2013 Pan-European Private Equity Performance Benchmarks Study

5-year rolling IRRs (funds formed 1980-2013) [%]

Generalist

Venture

Buyout

Average IRR range

between 10-15%

43

US investments outperform European investments in the long-run but are more volatile at the same time

Source: EVCA

-10%

0%

10%

20%

30%

40%

50%

60%

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

-10%

0%

10%

20%

30%

40%

50%

60%

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

5-year rolling IRRs for Europe [%] 5-year rolling IRRs for US [%]

EuropeanVenture

European Buyout US

Venture

USBuyout

44

On average private equity generates returns between 10 and 12% annually

Source: EVCA

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

5-year rolling IRRs global benchmark for all private equity

US: 12.2%

Global: 11.7%

Average IRR(1991-2013)

Europe: 10.6%

Global

Europe

US

45

Private Equity Outlook Europe – overall stable but challenging

Source: PWC Private Equity Trend Report; Alpine Equity Analysis

• Financing conditions – availability of LBO capital increased in the second half of 2015 and is expected to improve in 2016

• Investment opportunities – few quality assets together with a many players lead to very competitive processes and demand yield premium valuations

• Start-ups and growth capital – offer more deal opportunities as they are less impacted by economic crisis and less interesting for corporates and large buy-out funds

• Regulation – will set financial boundaries and therefore restrict additional value

• Returns – most likely decrease as a consequence of increased competition and sky-high valuations

• Focused investors – sweet spot investors (2.2 x money multiple) statistically outperform opportunistic investors (1.3 x)

• Operational improvement – has become a key element of a financial investor's business model

OutlookInfluencers

46

Overview

A. Introduction to Private Equity

B. Global/European Private Equity Market

C. Case Studies: Types of Private Equity Investors

D. Case Studies: Mid-Market Segments

E. Case Study: FinTech

F. Legal Environment

G. Investment Philosophy

H. Key Considerations for Setting Up a Fund

I. Conclusion and Next Steps

47

Broad universe of private equity investors

Fund of fundsGenuine global

funds

European mid-

sized funds

Turnaround

fundsCaptive funds

Infrastructure

funds

Real estate

funds

Venture Capital

funds

Private

foundations

University

endowmentsFintech funds

State-owned

funds

48

Types of private equity funds (1)

Captive fund • A VC or PE fund with one main shareholder. This can be e.g. a corporate with both financial and strategic interest.

• A captive fund in a more narrow sense points to a situation where the only shareholder is a financial institution.

• Typical structure for banks (equity + loan)

Leading global fund • Gobal alternative asset manager with several billion USD1) of assets under management across several funds and fund of funds vehicles and worldwide offices

• Typical fund size: Large Buyout USD 1.5m-4.5bn, Mega Buyout > USD 4.5bn

• Typical asset classes: private equity, energy, infrastructure, real estate credit strategies and hedge fund etc.

Source: www.valuewalk.com: Private Equity Buyout Fund: Does Size Really Matter?1) USD 100 – 300 bn

Fund type Description Examples

49

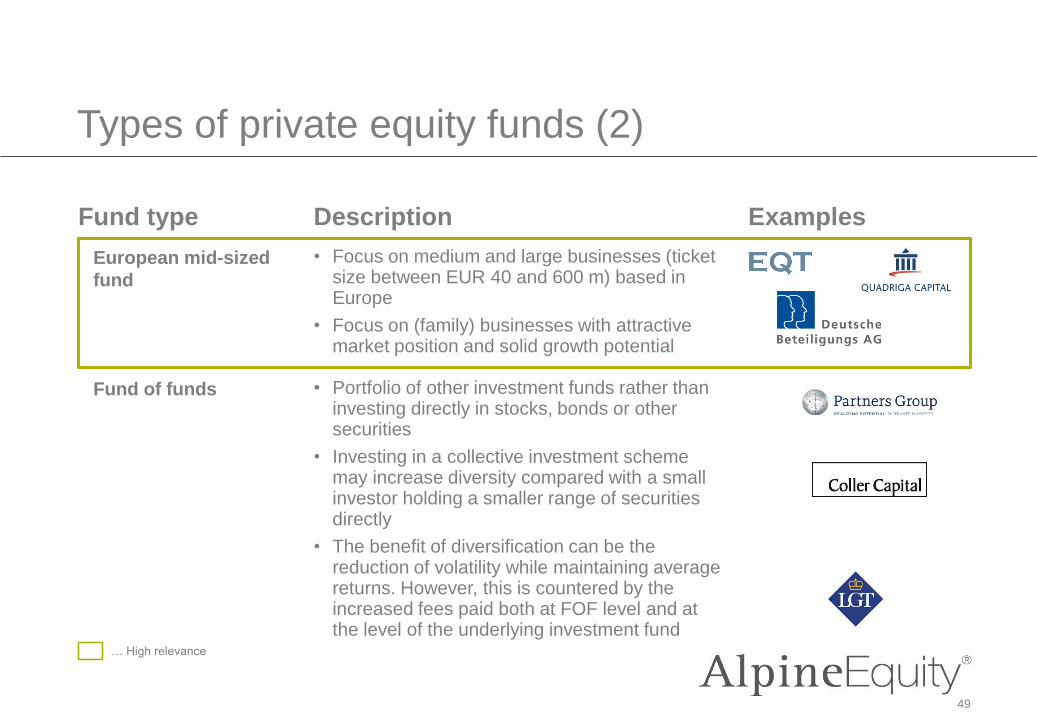

Types of private equity funds (2)

• Focus on medium and large businesses (ticket size between EUR 40 and 600 m) based in Europe

• Focus on (family) businesses with attractive market position and solid growth potential

• Portfolio of other investment funds rather than investing directly in stocks, bonds or other securities

• Investing in a collective investment scheme may increase diversity compared with a small investor holding a smaller range of securities directly

• The benefit of diversification can be the reduction of volatility while maintaining average returns. However, this is countered by the increased fees paid both at FOF level and at the level of the underlying investment fund

… High relevance

Fund type Description Examples

European mid-sized

fund

Fund of funds

50

Types of private equity funds (3)

• Fund either invests in other infrastructure funds or directly in infrastructure businesses

• Typical fund size several billion EUR/USD

• Excess cash (profits of state-owned companies) is invested in listed companies, private equity etc. in order to care for times when natural reserves like oil are fully exploited

• Billions of USD under management

Norwegian State

fund

Abu Dabi State

fund

Infrastructure and

real estate fund

Fund type Description Examples

State-owned

investment fund

51

Types of private equity funds (4)

• A university endowment is a fund created out of donations received by a university or college.

• A small portion of traditional stocks and bonds and a large portion of non-traditional alternative assets in the form of hedge funds, private equity, venture capital and real assets like oil and natural resources

• Often high-net worth industrials follow philanthropic approach to support poorest of the world

• Diversified investment approach and/or industry focus on industry they have profound expertise in

Fund type Description Examples

Endowments of

universities

Private foundations/

Family offices

52

Types of private equity funds (5)

• Private equity stakes in startup and small- and medium-size enterprises with strong growth potential.

• Investments are generally characterized as high-risk/high-return opportunities.

• Turnaround is the financial recovery of a company that has been performing poorly for an extended time.

• Possible characteristics of a troubled company in need of a turnaround include revenues that do not cover costs, an inability to pay creditors, layoffs, salary cuts and a significant decline in stock price. Poor management and/or social, technological and competitive changes may have caused the products or services to be perceived as subpar by consumers.

Sequoia Capital

Avenue Capital

Group

Fund type Description Examples

… High relevance

Venture Capital fund

Turnaround fund

53

Types of private equity funds (6)

• Banks, VC investors try to get get closer to the wave of disruptive innovation in the FinTechspace.

• Combination of entrepreneurial execution, technological capabilities and industry expertise to build companies that reshape finance.

• Help FinTech companies grow from a very early

stage (i.e. seed) to a more mature stage.

Fund type Description Examples

Fintech fund

… High relevance

54

Overview

A. Introduction to Private Equity

B. Global/European Private Equity Market

C. Case Studies: Types of Private Equity Investors

D. Case Studies: Mid-Market Segments

E. Case Study: FinTech

F. Legal Environment

G. Investment Philosophy

H. Key Considerations for Setting Up a Fund

I. Conclusion and Next Steps

55

Overview

A. Introduction to Private Equity

B. Global/European Private Equity Market

C. Case Studies: Types of Private Equity Investors

D. Case Studies: Mid-Market Segments

E. Case Study: FinTech

F. Legal Environment

G. Investment Philosophy

H. Key Considerations for Setting Up a Fund

I. Conclusion and Next Steps

56

"A4

rb_

sta

nd

ard

" –

20

10

07

01

–d

o n

ot

de

lete

th

is te

xt o

bje

ct!56

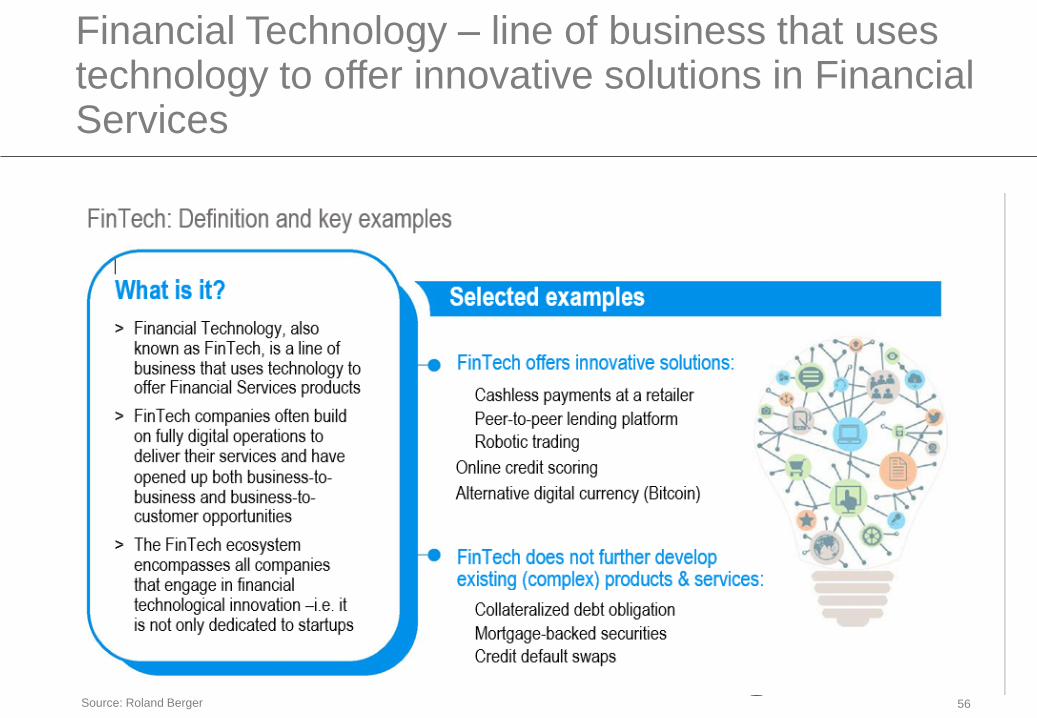

Financial Technology – line of business that usestechnology to offer innovative solutions in Financial Services

Source: Roland Berger

57

"A4

rb_

sta

nd

ard

" –

20

10

07

01

–d

o n

ot

de

lete

th

is te

xt o

bje

ct!

Initial situation

57

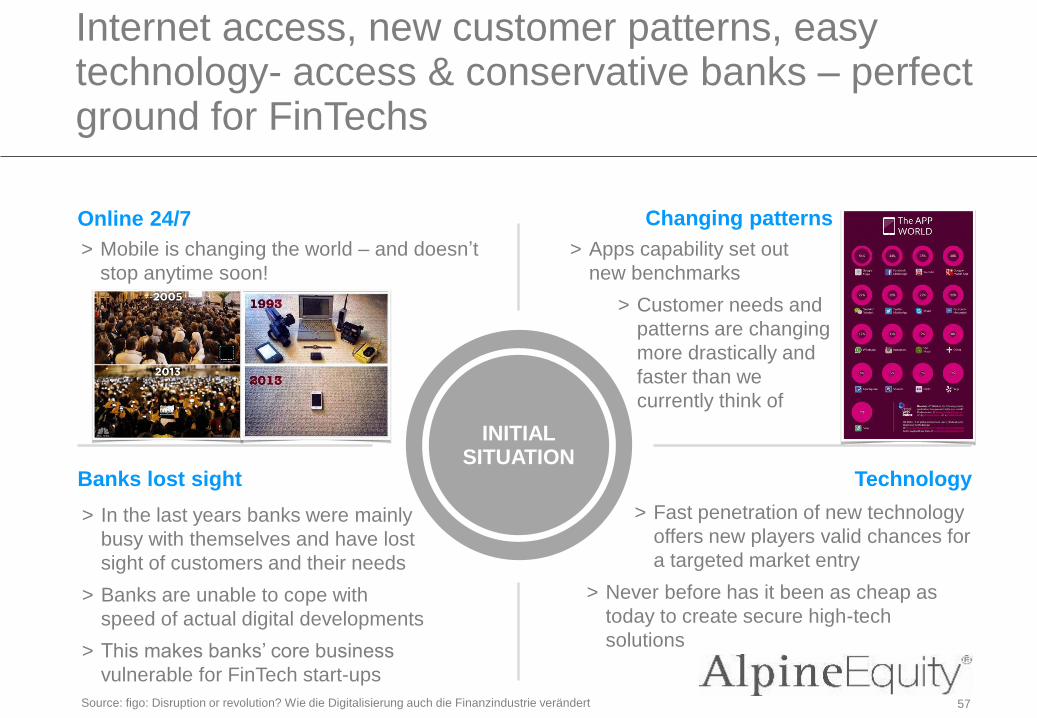

Internet access, new customer patterns, easy technology- access & conservative banks – perfectground for FinTechs

Source: figo: Disruption or revolution? Wie die Digitalisierung auch die Finanzindustrie verändert

> Mobile is changing the world – and doesn’t

stop anytime soon!

INITIAL SITUATION

Online 24/7

> Apps capability set out

new benchmarks

> Customer needs and

patterns are changing

more drastically and

faster than we

currently think of

Changing patterns

> Fast penetration of new technology

offers new players valid chances for

a targeted market entry

> Never before has it been as cheap as

today to create secure high-tech

solutions

Banks lost sight

> In the last years banks were mainly

busy with themselves and have lost

sight of customers and their needs

> Banks are unable to cope with

speed of actual digital developments

> This makes banks’ core business

vulnerable for FinTech start-ups

Technology

58

"A4

rb_

sta

nd

ard

" –

20

10

07

01

–d

o n

ot

de

lete

th

is te

xt o

bje

ct!58

FinTech start-ups have a lot in common …

Source: figo: Disruption or revolution? Wie die Digitalisierung auch die Finanzindustrie verändert

Master technology

FinTech

start-up

attributes!

The newcomer …

Think, live and act digital

Are fast and innovative

Try something, make mistakes and learn quickly

And have a clear eye on customers

59

"A4

rb_

sta

nd

ard

" –

20

10

07

01

–d

o n

ot

de

lete

th

is te

xt o

bje

ct!59

FinTech funding has increased substantially in recent years

Source: CB insights; Crunchbase; Roland Berger; figo

FinTechs are shaping the new banking industry !

• FinTech funding has increased to

USD12bn in 2014 and shows increased

attractivity

• VCs and business angels have spotted

FinTech after watching the evolving

ventures for a long while

• Legal framework to be clarified to fit

FinTech companies – otherwise time-

consuming decisions and unclear

outcomes hinder start-ups!

60

"A4

rb_

sta

nd

ard

" –

20

10

07

01

–d

o n

ot

de

lete

th

is te

xt o

bje

ct!60

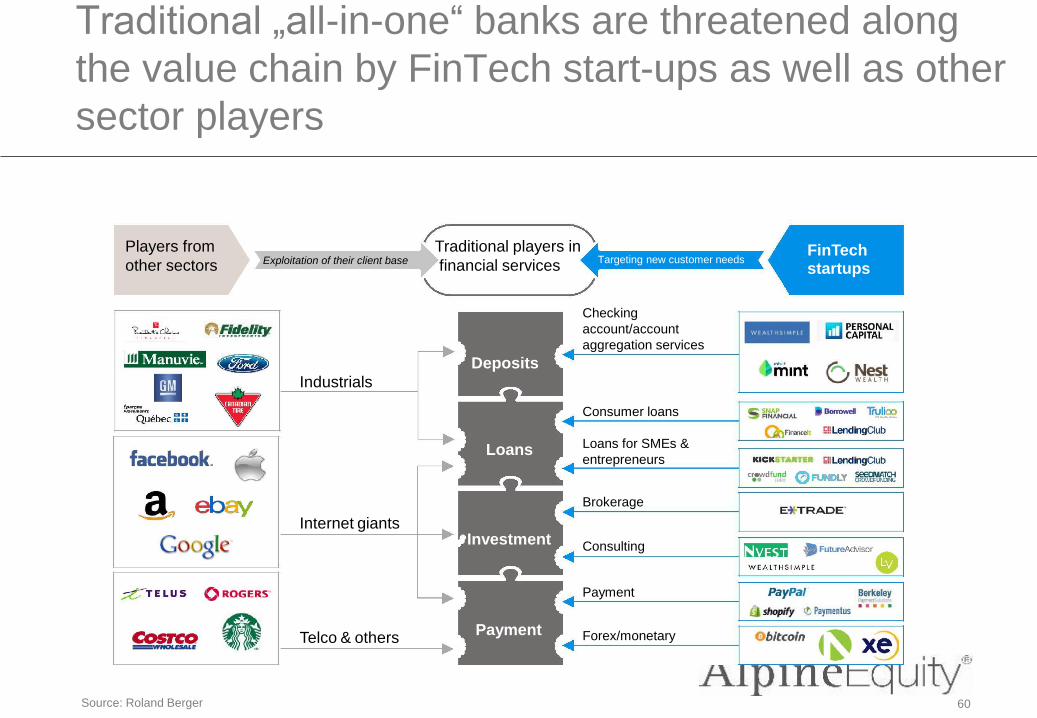

Traditional „all-in-one“ banks are threatened along

the value chain by FinTech start-ups as well as other

sector players

Source: Roland Berger

Deposits

Loans

Investment

Payment

Industrials

Internet giants

Telco & others

Checking

account/account

aggregation services

Consumer loans

Loans for SMEs &

entrepreneurs

Brokerage

Consulting

Payment

Forex/monetary

Players from

other sectors Exploitation of their client baseTraditional players in

financial servicesTargeting new customer needs

FinTechstartups

61

"A4

rb_

sta

nd

ard

" –

20

10

07

01

–d

o n

ot

de

lete

th

is te

xt o

bje

ct!61

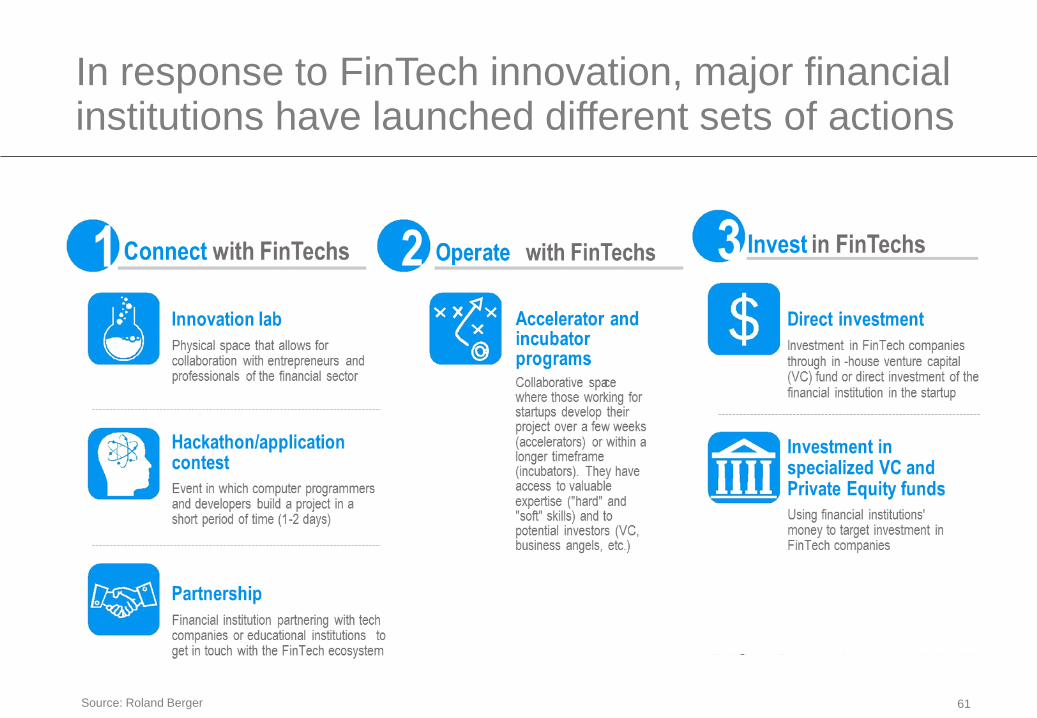

In response to FinTech innovation, major financialinstitutions have launched different sets of actions

Source: Roland Berger

62

"A4

rb_

sta

nd

ard

" –

20

10

07

01

–d

o n

ot

de

lete

th

is te

xt o

bje

ct!62

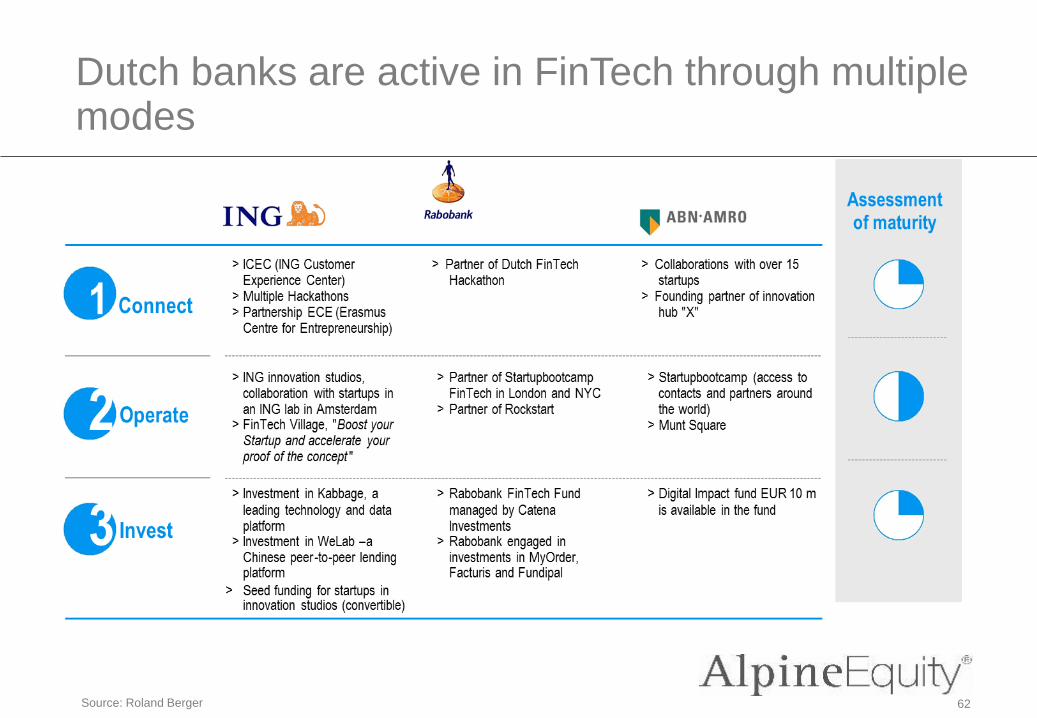

Dutch banks are active in FinTech through multiple modes

Source: Roland Berger

63

Overview

A. Introduction to Private Equity

B. Global/European Private Equity Market

C. Case Studies: Types of Private Equity Investors

D. Case Studies: Mid-Market Segments

E. Case Study: FinTech

F. Legal Environment

G. Investment Philosophy

H. Key Considerations for Setting Up a Fund

I. Conclusion and Next Steps

64

Typical structure of a private equity investment vehicle

Limited partners (investors)

Private equity fund

Investment CInvestment A Investment B

Private

equity firm (general partner)

Fund/investment management

• Tax efficient for investors• Typical locations (Europe):

UK, Luxembourg, Liechtenstein

65

Key issues to consider when setting up a fund

• Executes investment decisions

• Oversees fund’s investments

• Receives fees for this services

• Fund raising

• Substantial commitment for equity interest to PE fund

• Incentive scheme – carried interest (compensation as share of profits earned on investment)

• Direct control of investors – advisory boards, covenants (e.g. 15% investment limit in one firm; use of debt at fund level; distribution vs. reinvestment ratio)

General Partners (management company) Limited Partners (investors)

• Institutional investors (pension funds, financial institutions, foundations, family offices, corporates, fund of funds etc.)

• Member of advisory board1) and/or participation in annual meeting of fund

• Quarterly reporting about progress of investments

• Fees2):

– Management fee approx. 2-2,5% of committed capital

– Carried interest 20% of profits of the fund

– Hurdle rate 8%; carry only payable after invested capital plus 8% p.a. is distributed to investors

1)The advisory board typically meets twice a year to provide guidance and support in matters

relating to running the partnership and deal with potential upcoming conflicts of interest.

2)Fee structures vary from fund to fund; here: only rules of thumb

66

Overview

A. Introduction to Private Equity

B. Global/European Private Equity Market

C. Case Studies: Types of Private Equity Investors

D. Case Studies: Mid-Market Segments

E. Case Study: FinTech

F. Legal Environment

G. Investment Philosophy

H. Key Considerations for Setting Up a Fund

I. Conclusion and Next Steps

67

67

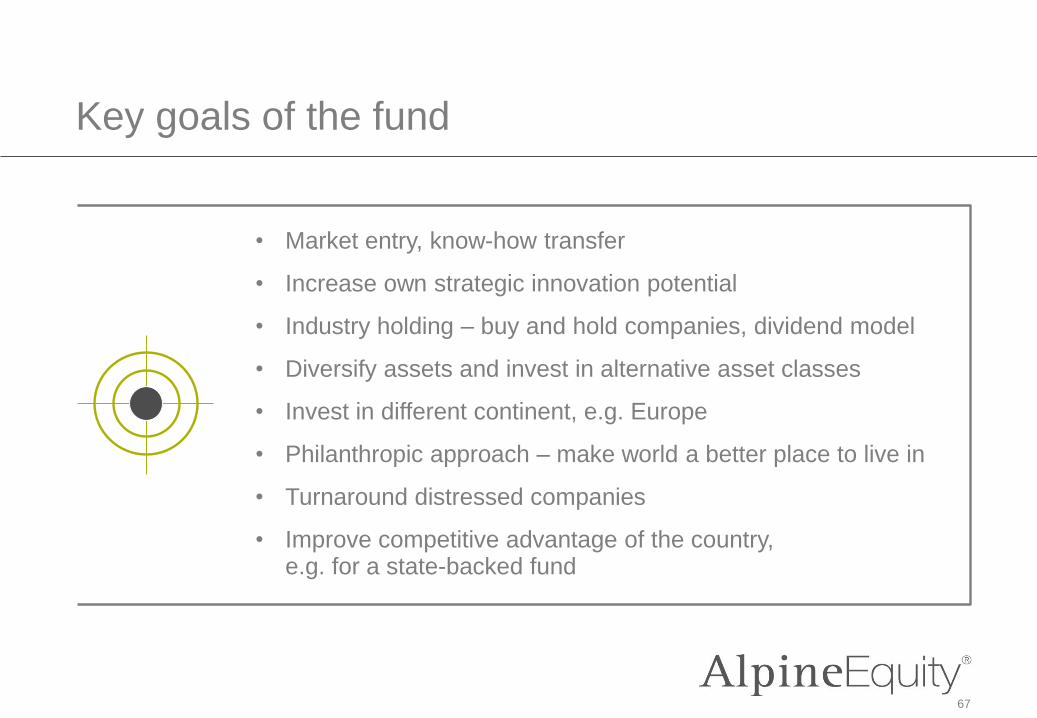

Key goals of the fund

• Market entry, know-how transfer

• Increase own strategic innovation potential

• Industry holding – buy and hold companies, dividend model

• Diversify assets and invest in alternative asset classes

• Invest in different continent, e.g. Europe

• Philanthropic approach – make world a better place to live in

• Turnaround distressed companies

• Improve competitive advantage of the country, e.g. for a state-backed fund

68

Overview

A. Introduction to Private Equity

B. Global/European Private Equity Market

C. Case Studies: Types of Private Equity Investors

D. Case Studies: Mid-Market Segments

E. Case Study: FinTech

F. Legal Environment

G. Investment Philosophy

H. Key Considerations for Setting Up a Fund

I. Conclusion and Next Steps

69

Key Issues to be considered

• Investment strategy – i.e. focus on specific industries, equity/mezzanine, development stage, holding period

• Minimum fund volume – min EUR 50 m for VC; and min. EUR 100 m for PE

• Management team – deal sourcing, value creation, negotiation

• Align interest between management and investors

• Fee structure – incentive scheme for management

• Corporate governance – who is responsible for investment decisions, reporting rhythm, distribution policy

• Subsidy schemes for certain legal entities applicable

70

Overview

A. Introduction to Private Equity

B. Global/European Private Equity Market

C. Case Studies: Types of Private Equity Investors

D. Case Studies: Mid-Market Segments

E. Case Study: FinTech

F. Legal Environment

G. Investment Philosophy

H. Key Considerations for Setting Up a Fund

I. Conclusion and Next Steps

71

Potential next steps

• Fund set up:

A. A fintech fund; volume EUR 50-100 m

B. Industrial fund for certain industries; volume EUR 100-500 m

• Ayandeh Bank as lead investor plus other banks, insurance companies, industrial companies etc.

• Next steps: evaluate proposal, timeframe

72

Conclusion and next steps

• Private equity is all about people

• Private equity as established asset class

• Private equity has positive macro economical impact

• Private equity requires industry knowledge and a network

• Alpine equity as partner for strong growing companies

1.

2.

3.

4.

5.

73

THANK YOU for your INTEREST !