Working With Japanese Buyers & SellersSep 13, 2016 · condos in Waikiki” ... • Access to all...

122

Working With Japanese Buyers & Sellers September 13, 2016

Transcript of Working With Japanese Buyers & SellersSep 13, 2016 · condos in Waikiki” ... • Access to all...

Working With Japanese Buyers & SellersSeptember 13, 2016

Membership has its advantages!

Next Event – November 18th

GMM Luncheon at Oahu Country Club

Working With Japanese Buyers & SellersSeptember 13, 2016

Presentation Materials Available at:

www.LuxuryHm.com/for-agents

Thank you to Honolulu HomeLoans

Leonard Loventhal

• Loan officer & manager Honolulu HomeLoans• 23 years of loan experience• Residential & new development

Loan Structures for Japanese Buyers

• 30 years of real estate experience• Over $1 Billion in closed sales• Residential, commercial, finance, development

Patrick W ONeill R MIRM

▪ Hong Kong and Honolulu Offices

▪ Local, National & International clientele

▪ Residential, Commercial, Management, Development

▪ 80% & 90% commission levels

Introduction to Servicing Foreign Clients

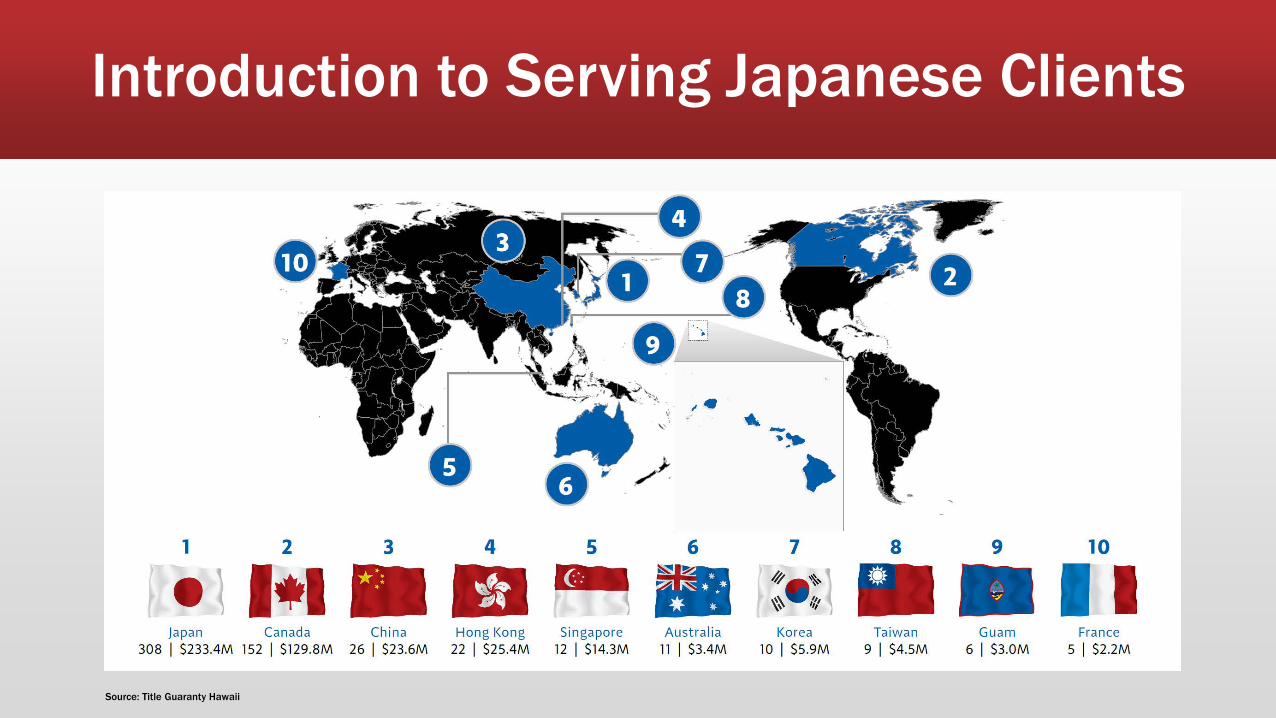

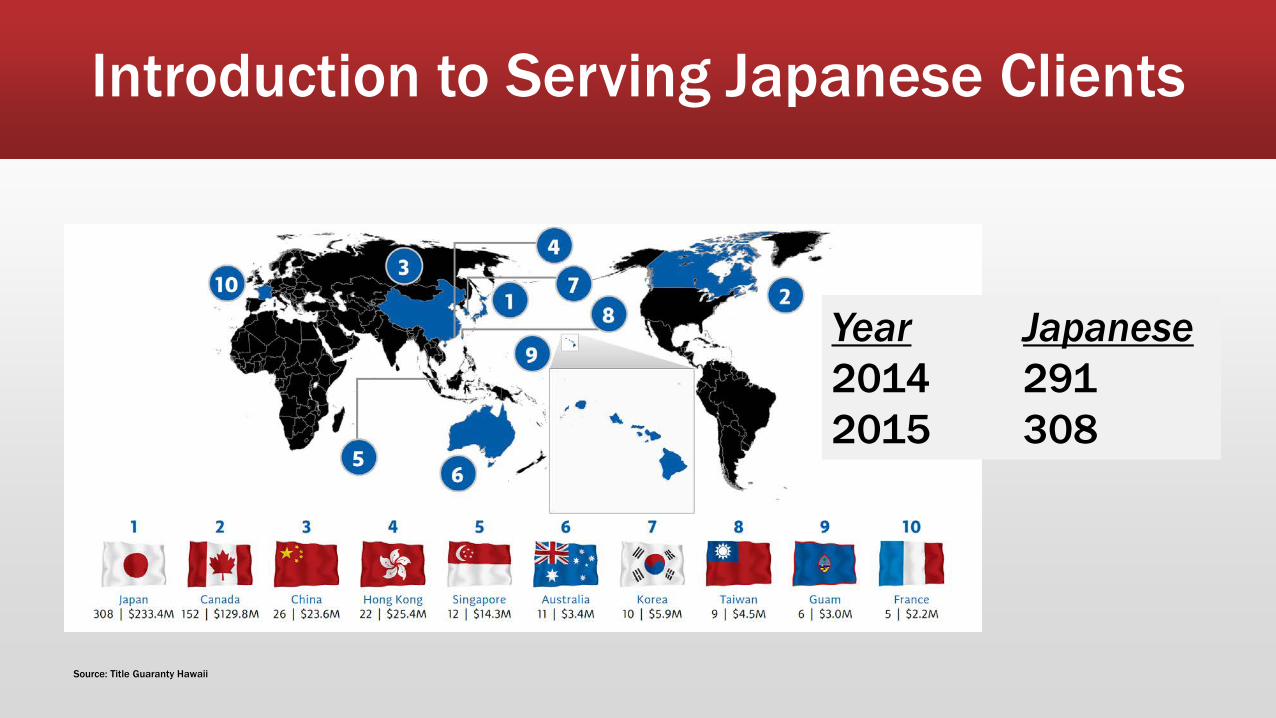

Introduction to Serving Japanese Clients

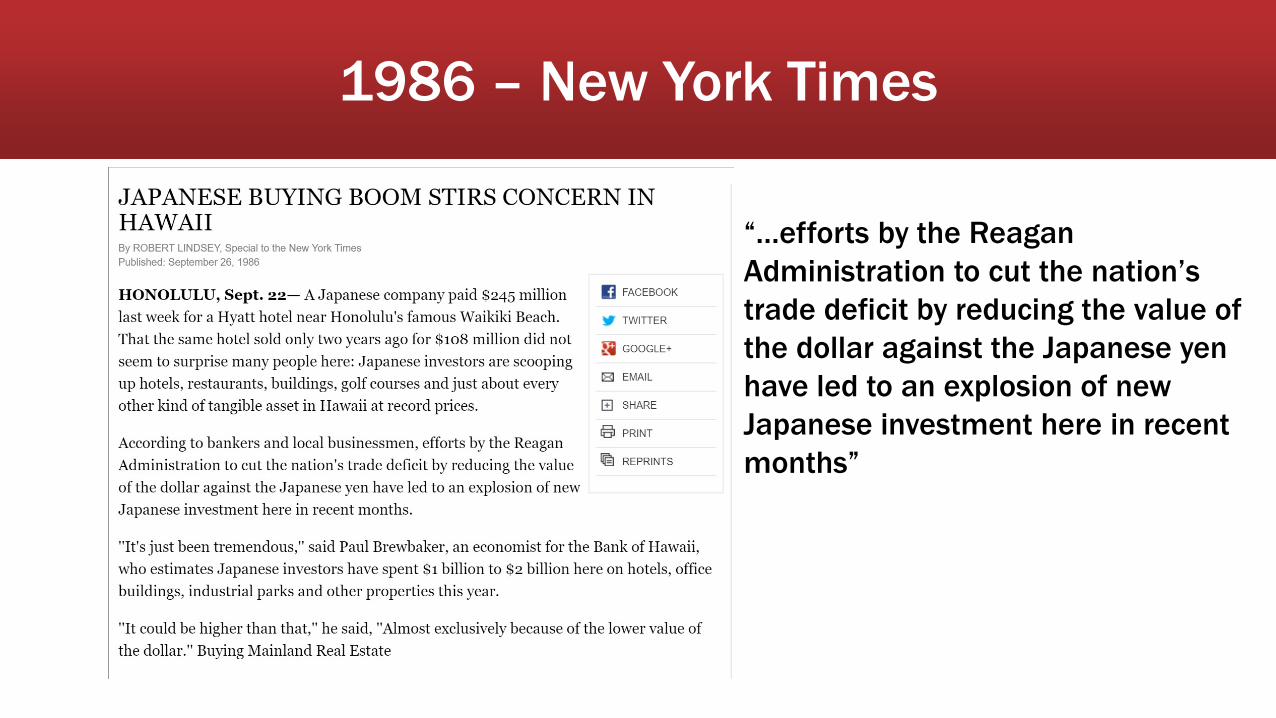

1986 – New York Times

1986 – New York Times

“…efforts by the Reagan Administration to cut the nation’s trade deficit by reducing the value of the dollar against the Japanese yen have led to an explosion of new Japanese investment here in recent months”

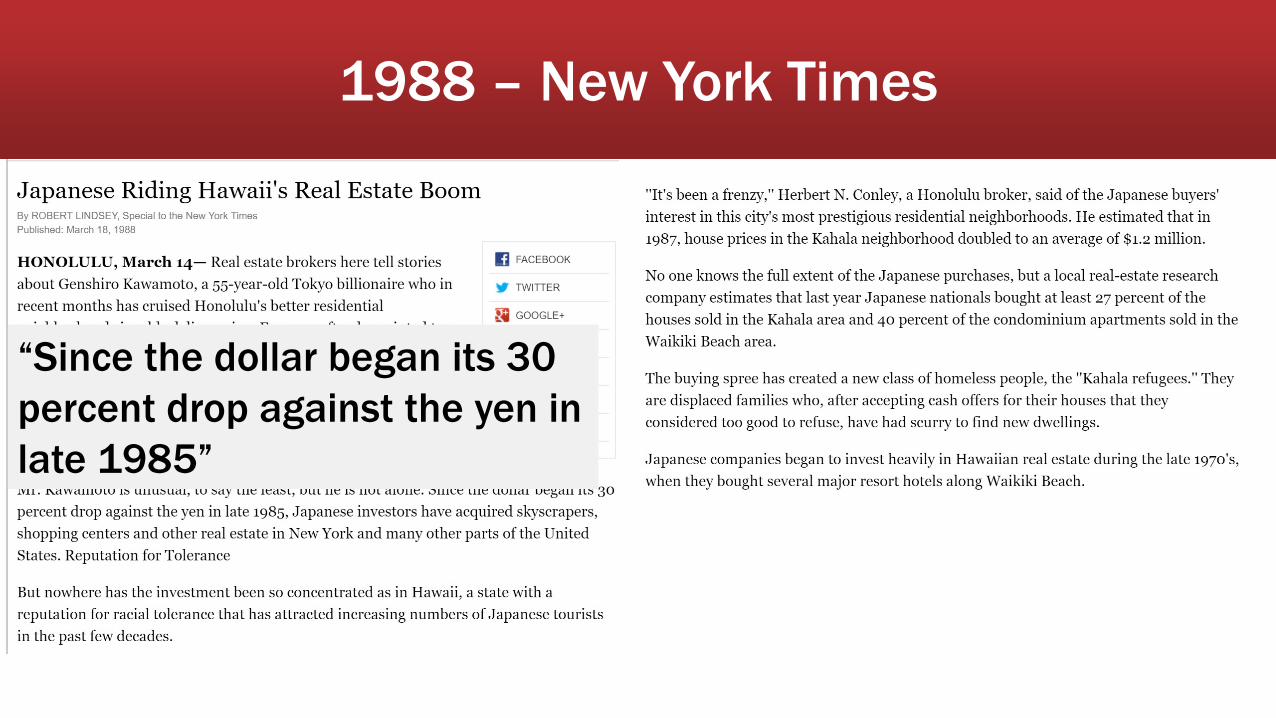

1988 – New York Times

1988 – New York Times

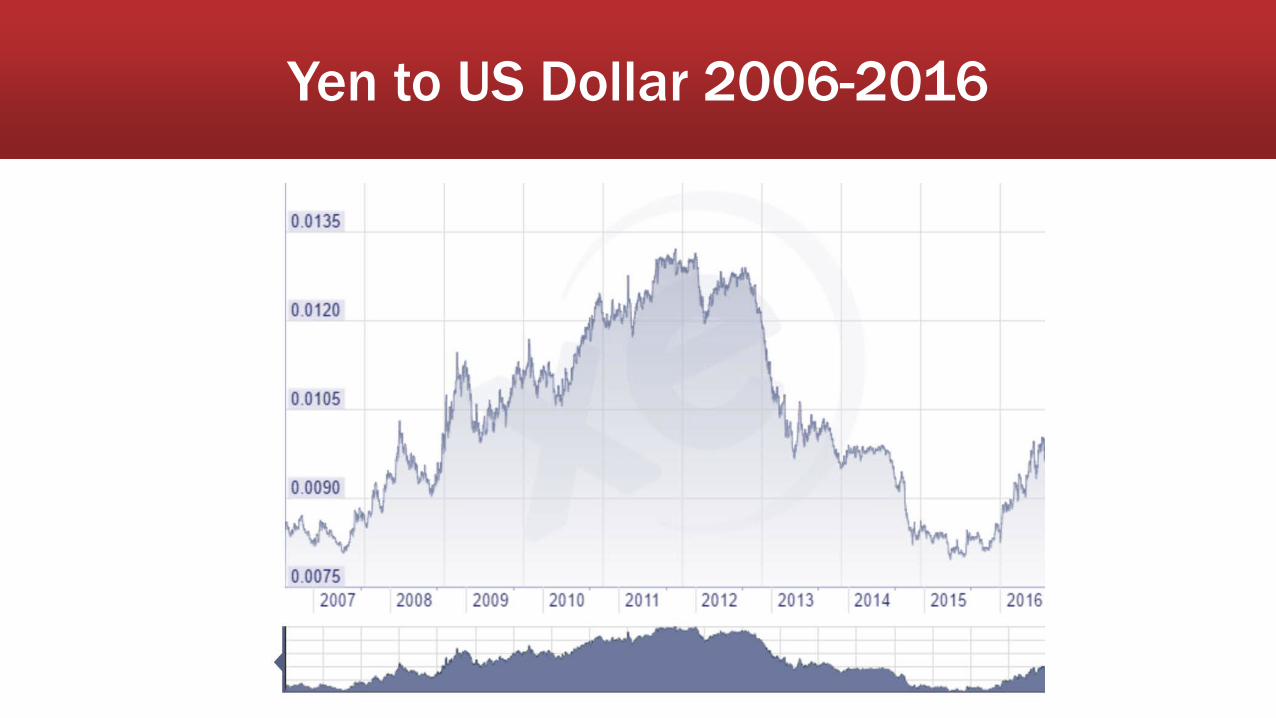

“Since the dollar began its 30 percent drop against the yen in late 1985”

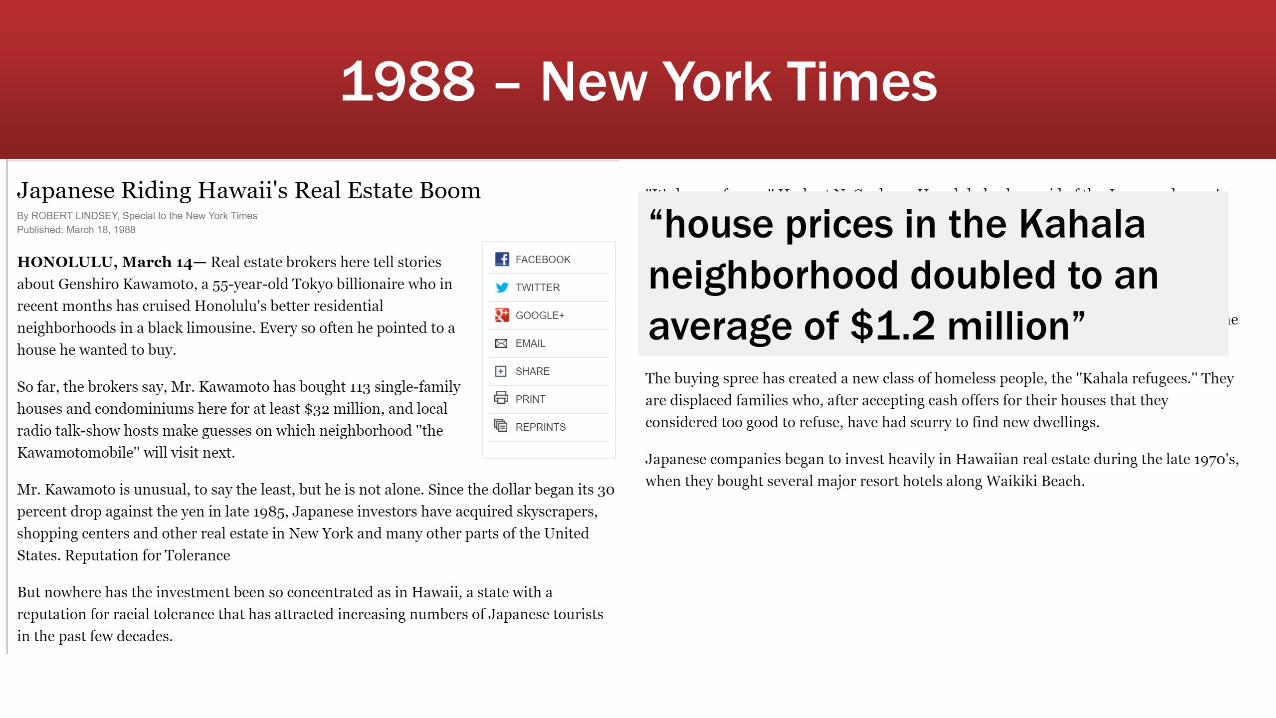

1988 – New York Times

“house prices in the Kahalaneighborhood doubled to an average of $1.2 million”

1988 – New York Times

“estimates Japanese nationals bought...27% of houses sold in Kahala area and 40% of condos in Waikiki”

Introduction to Serving Japanese Clients

Source: Title Guaranty Hawaii

Introduction to Serving Japanese Clients

Year Hong Kong2015 22

Source: Title Guaranty Hawaii

Introduction to Serving Japanese Clients

Year Japanese2014 2912015 308

Source: Title Guaranty Hawaii

Yen to US Dollar 2006-2016

Yen to US Dollar 2006-2016

30% Drop

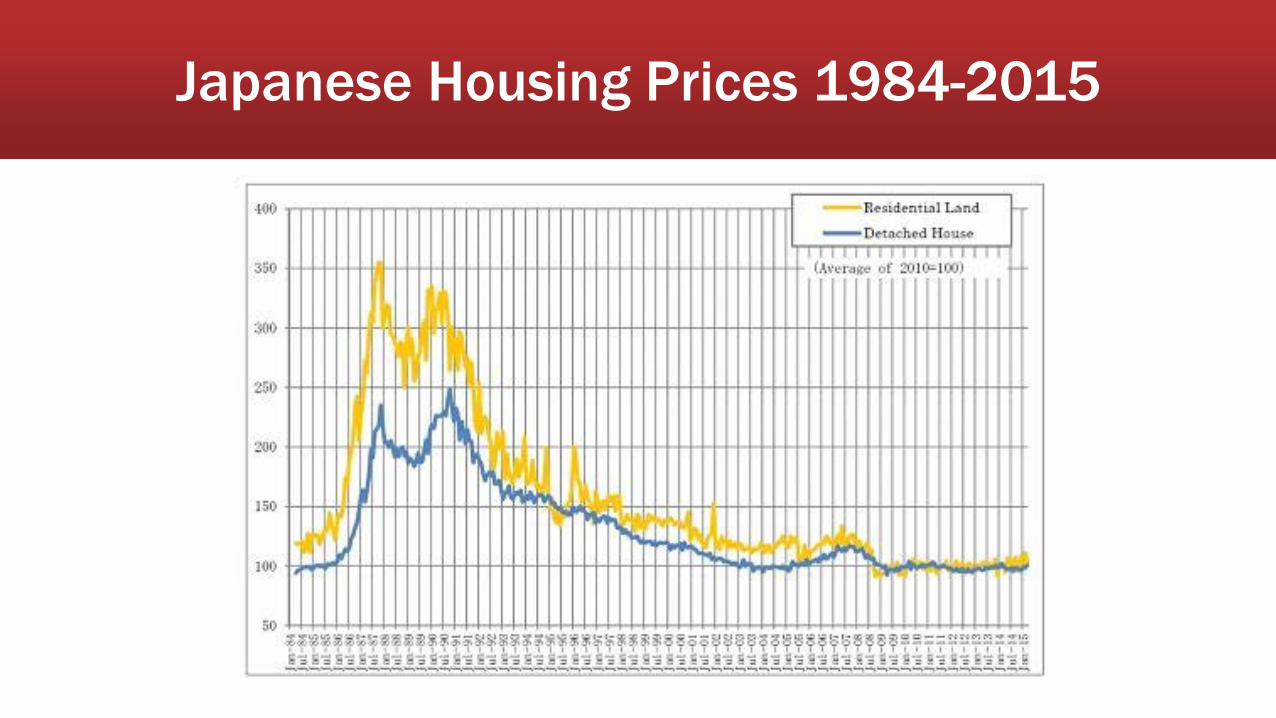

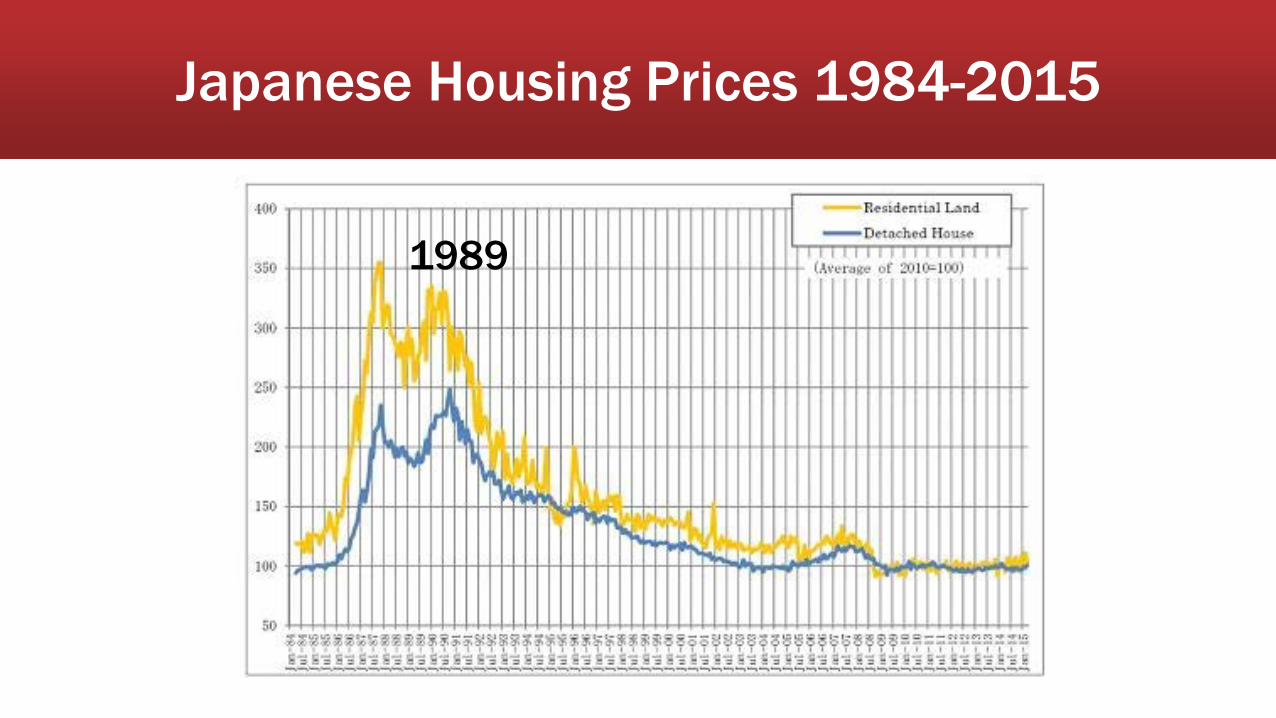

Japanese Housing Prices 1984-2015

Japanese Housing Prices 1984-2015

1989

1. Cultural sensitivity

2. Business differences3. Misconceptions about US property4. Intro to taxation

5. Managing the process

Introduction to Servicing Foreign ClientsBuyer Side Transactions

Business DifferencesWorking with Buyers

Hawaii versus Japan

Business DifferencesHawaii vs Japan

MLS No MLS

Business DifferencesHawaii vs Japan

Work with one broker

Work with multiple brokers

Business DifferencesHawaii vs Japan

Seller pays commission to buyers broker

Buyer pays commission to buyer’s broker

Business DifferencesHawaii vs Japan

Buyers fee agreement optional

Buyers fee agreement used

Business DifferencesHawaii vs Japan

Full disclsoure

Limited disclosure

Business DifferencesHawaii vs Japan

Contracts prepared by brokers

Contracts prepared by attorneys

Business DifferencesHawaii vs Japan

Written negotiations

Verbal negotiations

Business DifferencesHawaii vs Japan

Escrow companies

Attorneys orshoshi

Business DifferencesWorking with Buyers

Presentation points to client

Business DifferencesWorking with Buyers

Presentation points to client

• Access to all properties for sale via MLS

Business DifferencesWorking with Buyers

Presentation points to client

• Access to all properties for sale via MLS• Commission paid by seller

Business DifferencesWorking with Buyers

Presentation points to client

• Access to all properties for sale via MLS• Commission paid by seller• Written negotiations

Business DifferencesWorking with Buyers

Presentation points to client

• Access to all properties for sale via MLS• Commission paid by seller• Written negotiations• Contracts prepared by broker

Business DifferencesWorking with Buyers

Presentation points to client

• Access to all properties for sale via MLS• Commission paid by seller• Written negotiations• Contracts prepared by broker• Escrow and title insurance

Common misconceptions about buying in the US

Introduction to Servicing Foreign ClientsBuyer Side Transactions

Common MisconceptionsAbout Owning US property

• US taxes penalize foreign ownership

Common MisconceptionsAbout Owning US property

• US taxes penalize foreign ownership• US has the highest capital gains taxes

Capital Gains Tax Rates (Does not include State and Municipal tax)

US 15%-20%

Capital Gains Tax Rates

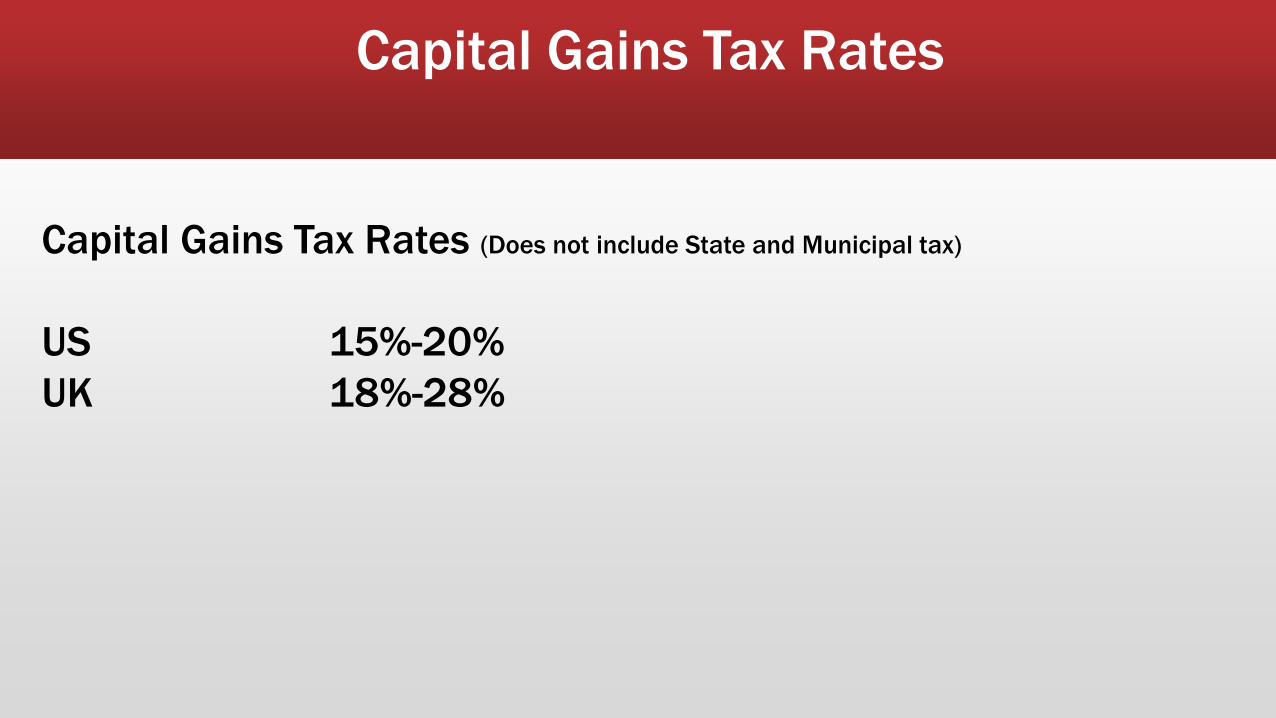

Capital Gains Tax Rates (Does not include State and Municipal tax)

US 15%-20%UK 18%-28%

Capital Gains Tax Rates

Capital Gains Tax Rates (Does not include State and Municipal tax)

US 15%-20%UK 18%-28%Japan 15%-30% (15% 5 years+ / 30% 5 years-)

Capital Gains Tax Rates

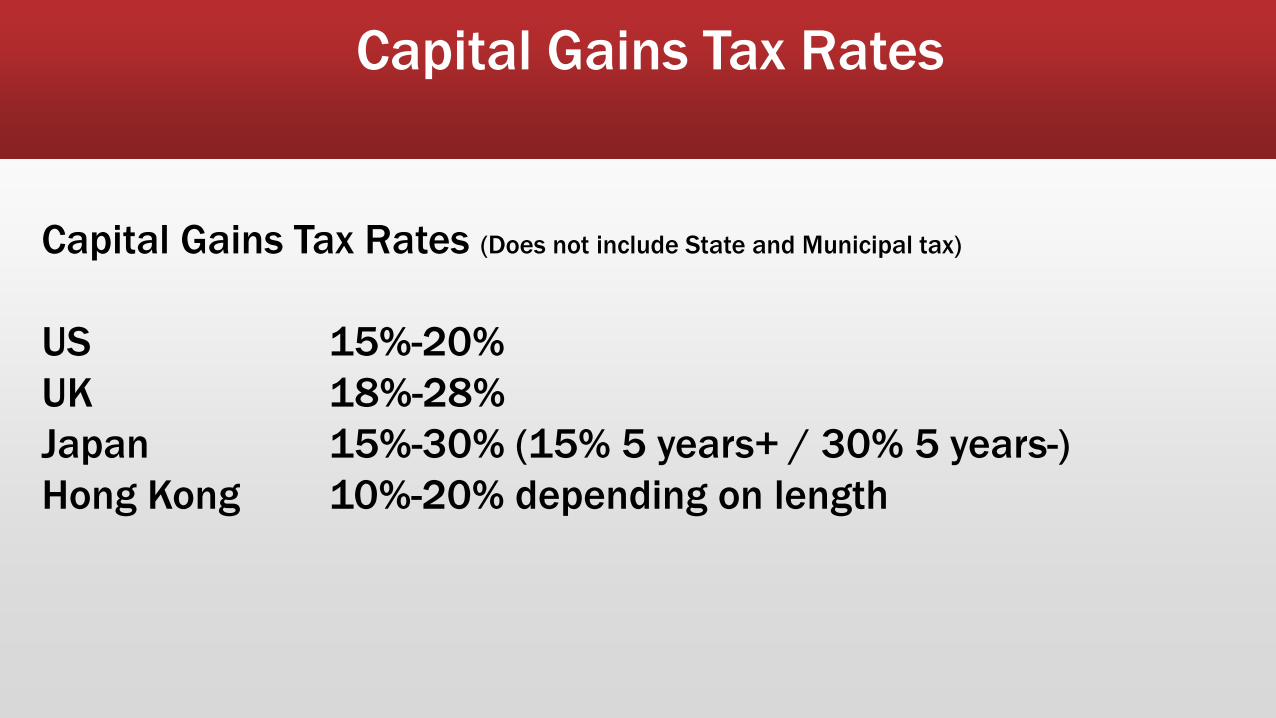

Capital Gains Tax Rates (Does not include State and Municipal tax)

US 15%-20%UK 18%-28%Japan 15%-30% (15% 5 years+ / 30% 5 years-)Hong Kong 10%-20% depending on length

Capital Gains Tax Rates

Capital Gains Tax Rates (Does not include State and Municipal tax)

US 15%-20%UK 18%-28%Japan 15%-30% (15% 5 years+ / 30% 5 years-)Hong Kong 10%-20% depending on lengthKorea 8%-38% progressive (28% in year 3)

Capital Gains Tax Rates

Common MisconceptionsAbout Owning US property

• US taxes penalize foreign ownership• US has the highest capital gains taxes• ITIN / IRS requires tax filing of global assets

Common MisconceptionsAbout Owning US property

• US taxes penalize foreign ownership• US has the highest capital gains taxes• ITIN / IRS requires tax filing of global assets• Should hold property in off-shore company (BVI, GT)

Common MisconceptionsAbout Owning US property

• US taxes penalize foreign ownership• US has the highest capital gains taxes• ITIN / IRS requires tax filing of global assets• Should hold property in off-shore company (BVI, GT)• No estate tax shelters ($13k /35% vs $5M)

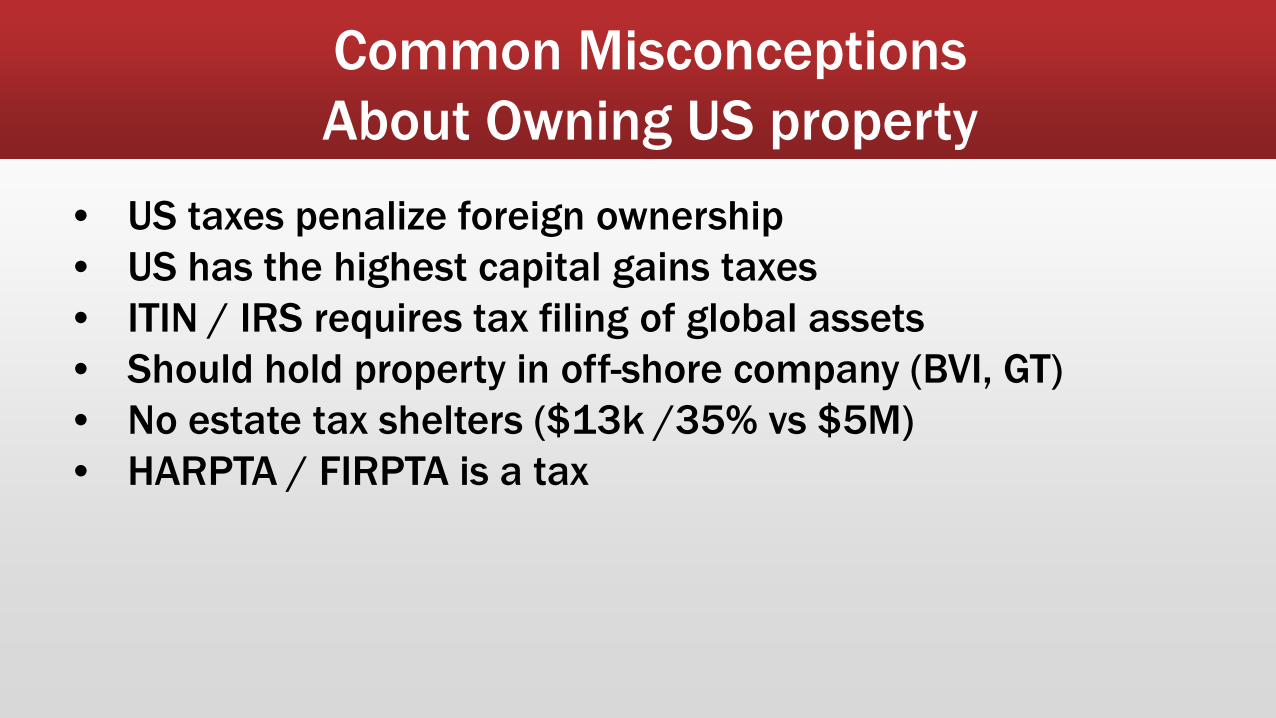

Common MisconceptionsAbout Owning US property

• US taxes penalize foreign ownership• US has the highest capital gains taxes• ITIN / IRS requires tax filing of global assets• Should hold property in off-shore company (BVI, GT)• No estate tax shelters ($13k /35% vs $5M)• HARPTA / FIRPTA is a tax

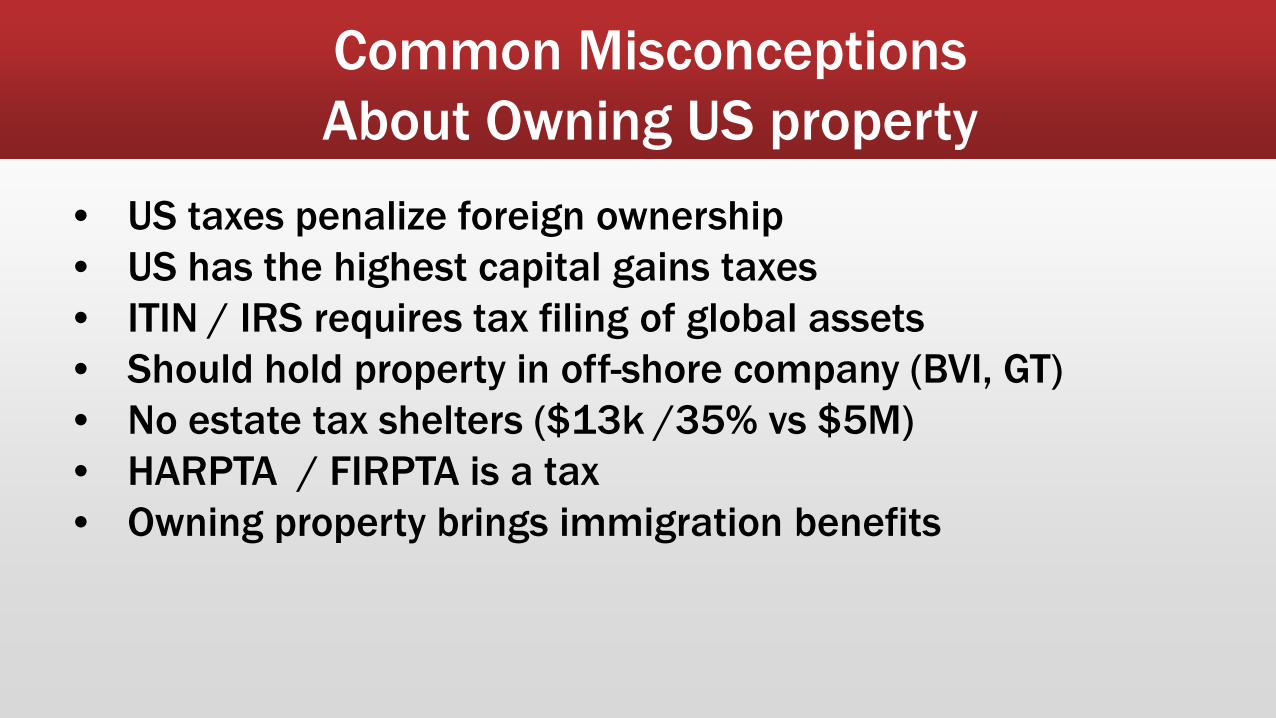

Common MisconceptionsAbout Owning US property

• US taxes penalize foreign ownership• US has the highest capital gains taxes• ITIN / IRS requires tax filing of global assets• Should hold property in off-shore company (BVI, GT)• No estate tax shelters ($13k /35% vs $5M)• HARPTA / FIRPTA is a tax• Owning property brings immigration benefits

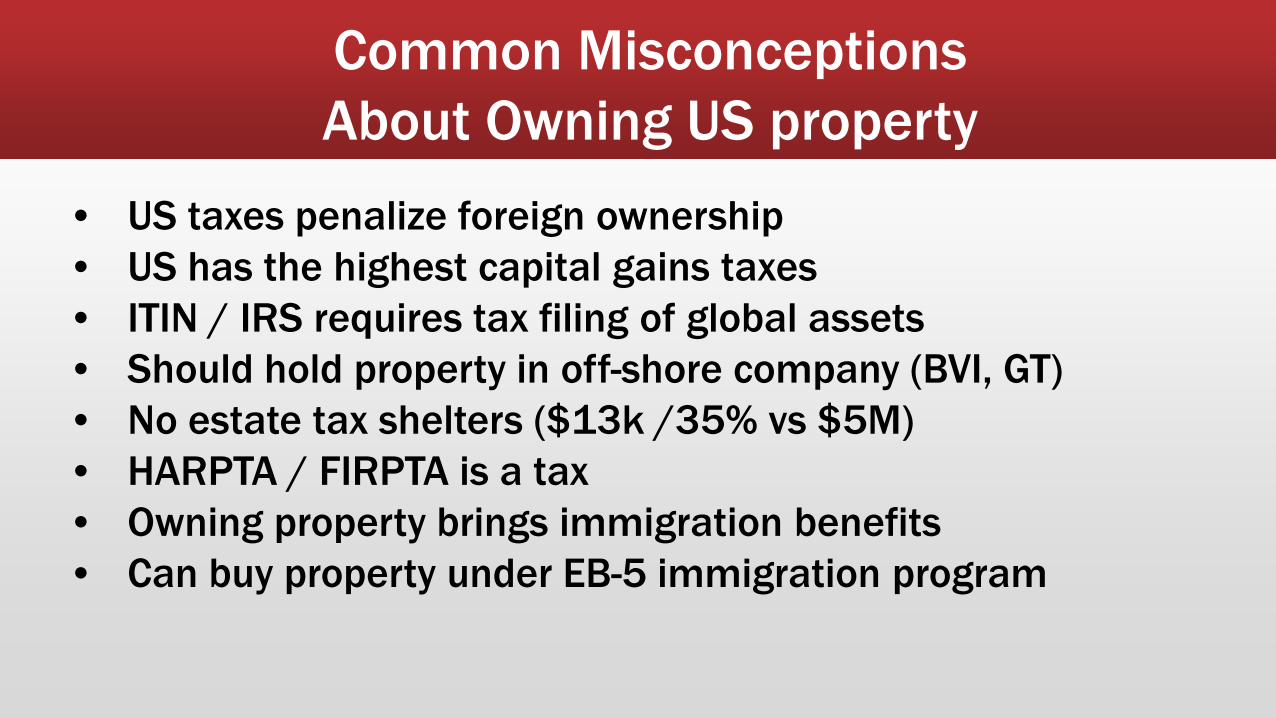

Common MisconceptionsAbout Owning US property

• US taxes penalize foreign ownership• US has the highest capital gains taxes• ITIN / IRS requires tax filing of global assets• Should hold property in off-shore company (BVI, GT)• No estate tax shelters ($13k /35% vs $5M)• HARPTA / FIRPTA is a tax• Owning property brings immigration benefits• Can buy property under EB-5 immigration program

Introduction to Serving Japanese Clients

Shimpei Oki, Attorney

• Real estate, immigration, corporate law• Residential, commercial, golf course, resort• Cum laude, William Richardson Law School• Fluent in Japanese and English

September 13, 2016Shimpei Oki, Esq.

(Areas of practice: real estate, corporate and immigration law)

• Cautioning your clients: The U.S. is not Japan –Don’t think everything works in the United States as they work in Japan.

• Language Barrier – Don’t just sign where people tell you to sign.

• Taxes – Don’t believe the Japanese accountant can take care of everything, collaborative effort with a U.S. accountant is critical.

• Death – Don’t wait until you’re on your deathbed to think of what to do when you pass away.

• Tenancies• Taking Title• Estate Planning • Transacting in Foreign Currency• Duties as a Broker

Things to consider before you decide:

• Source of funding• Estate planning• Asset management

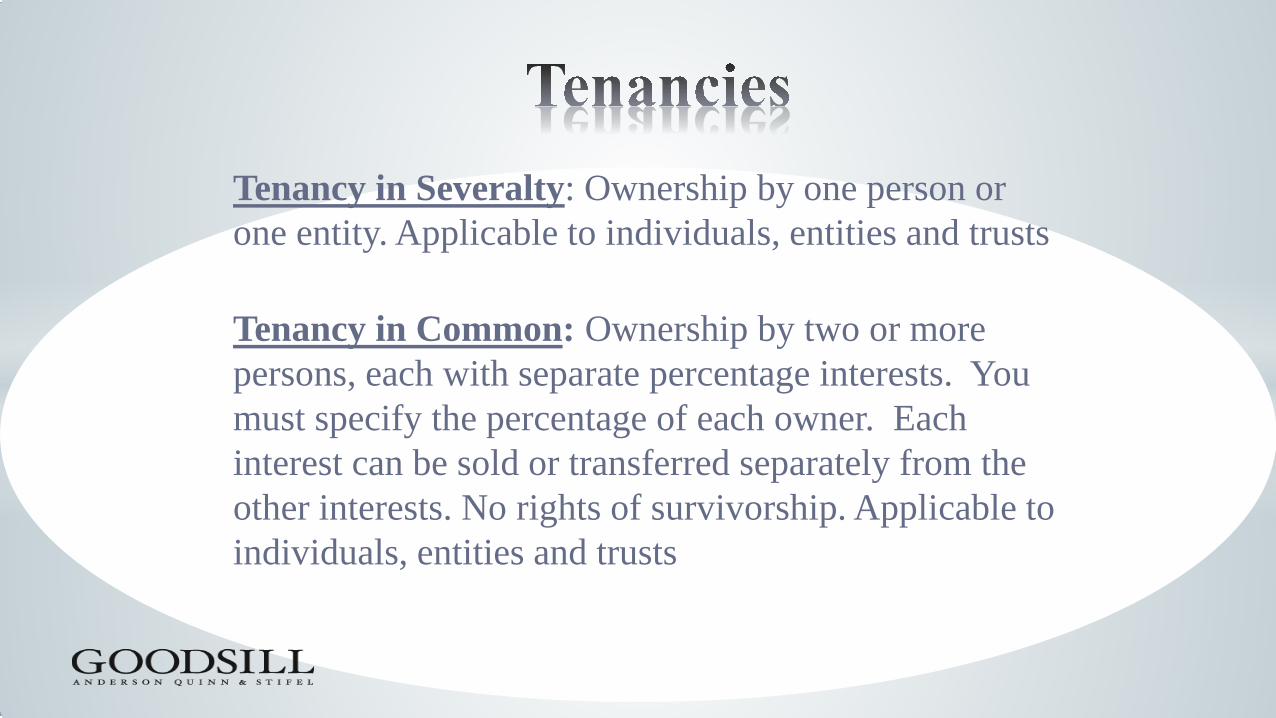

Tenancy in Severalty: Ownership by one person or one entity. Applicable to individuals, entities and trusts

Tenancy in Common: Ownership by two or more persons, each with separate percentage interests. You must specify the percentage of each owner. Each interest can be sold or transferred separately from the other interests. No rights of survivorship. Applicable to individuals, entities and trusts

Tenancy by the Entirety:Ownership available only to husband and wife. One advantage – if one spouse owes money to a creditor, the creditor cannot lien property owned in this tenancy. Applicable to married individuals only (civil union applies). Right of survivorship to spouse. For Land Court property a petition will be required.• For Japan nationals, this does not resolve their estate tax

obligations. • For Japanese nationals, if the spouse has no income and is

named as a co-owner, possible gift tax obligations under Japanese tax law.

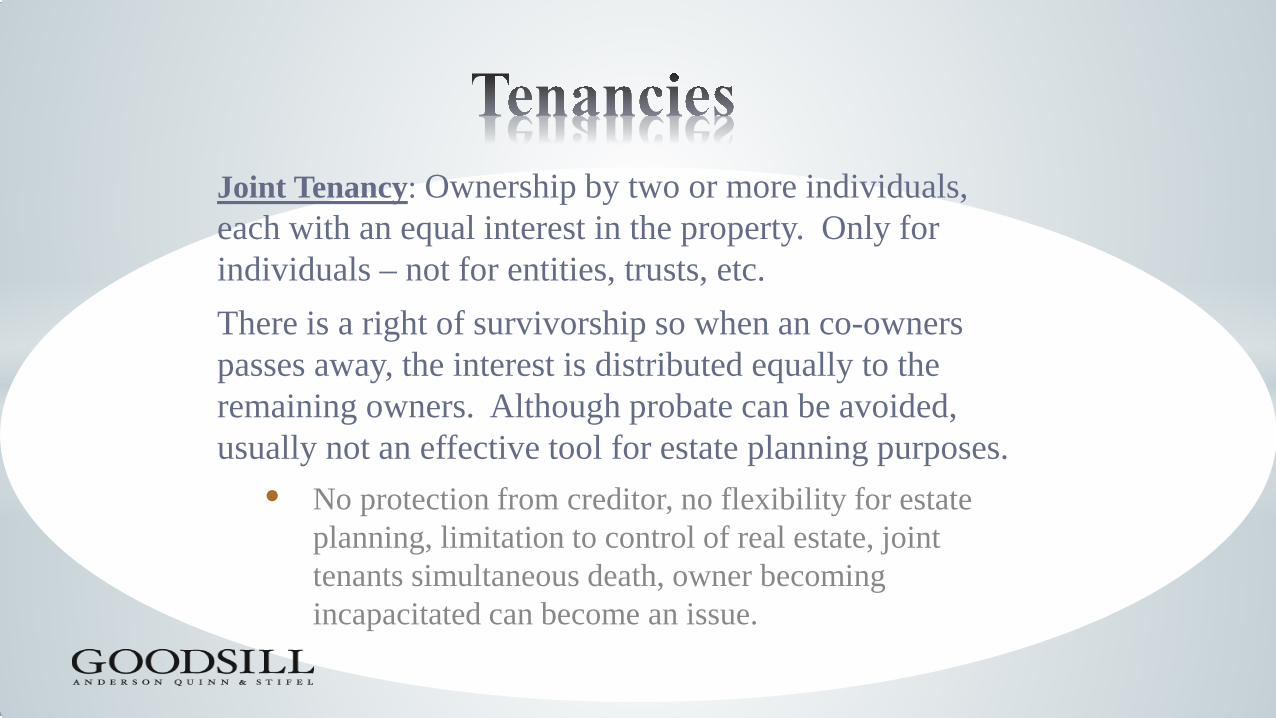

Joint Tenancy: Ownership by two or more individuals, each with an equal interest in the property. Only for individuals – not for entities, trusts, etc. There is a right of survivorship so when an co-owners passes away, the interest is distributed equally to the remaining owners. Although probate can be avoided, usually not an effective tool for estate planning purposes.

• No protection from creditor, no flexibility for estate planning, limitation to control of real estate, joint tenants simultaneous death, owner becoming incapacitated can become an issue.

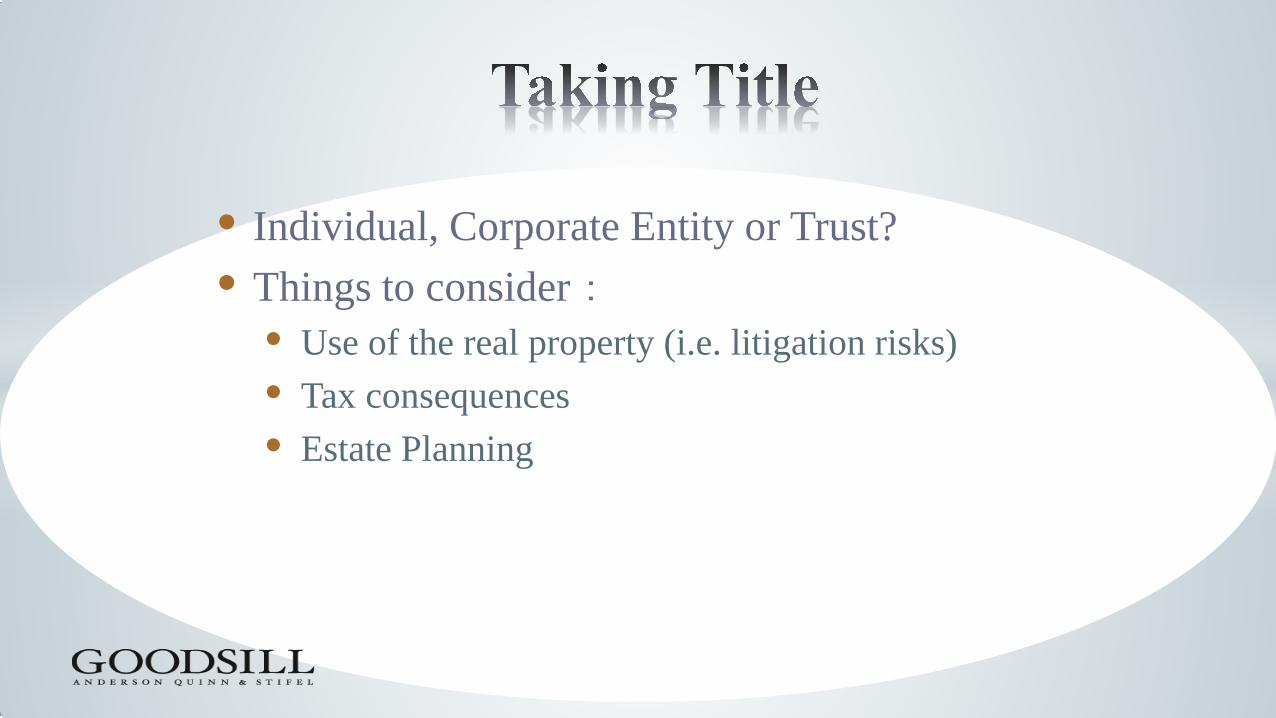

• Individual, Corporate Entity or Trust?• Things to consider:

• Use of the real property (i.e. litigation risks)• Tax consequences• Estate Planning

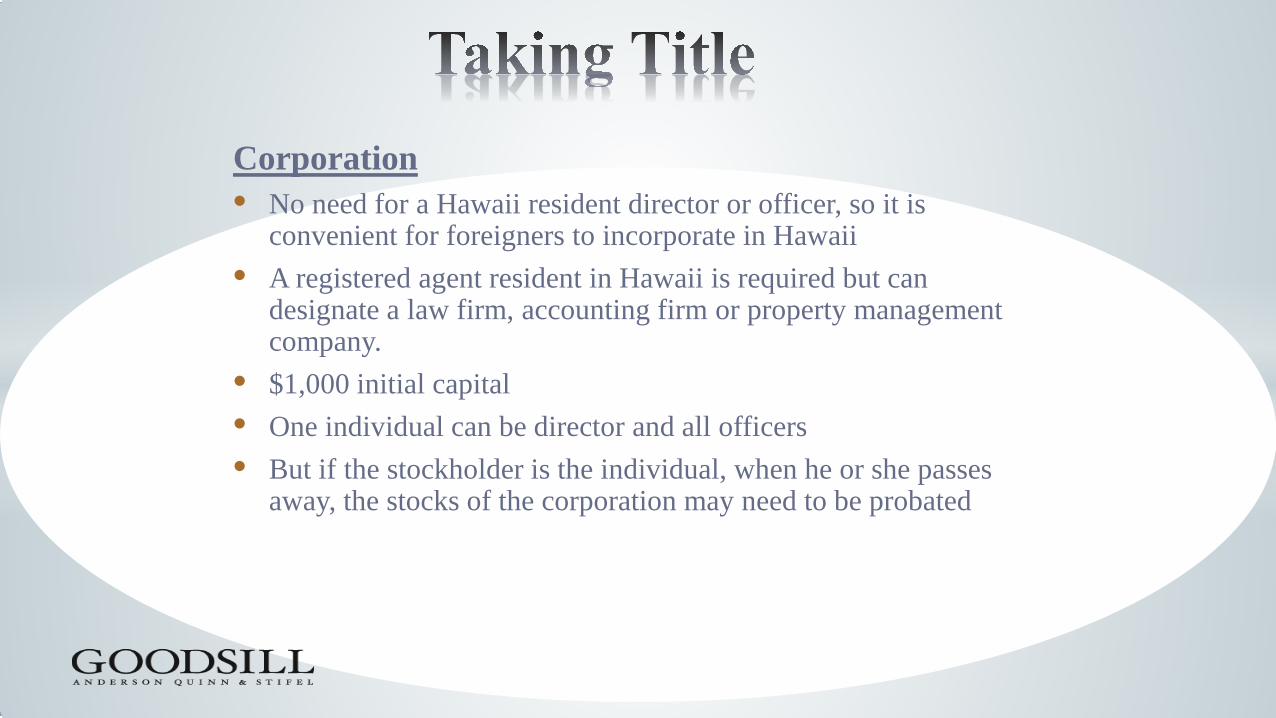

Corporation• No need for a Hawaii resident director or officer, so it is

convenient for foreigners to incorporate in Hawaii• A registered agent resident in Hawaii is required but can

designate a law firm, accounting firm or property management company.

• $1,000 initial capital• One individual can be director and all officers• But if the stockholder is the individual, when he or she passes

away, the stocks of the corporation may need to be probated

Partnership • Often used in the past by Japan nationals for tax advantages• Now LLCs have taken over

Limited Liability Company• Popularity has increased because of the ability to pass

through the income to the member, so no LLC tax filing is necessary

• For a Japanese national, it may not be the best vehicle because if you pass through the income, the Japanese national will have to file taxes in the United States individually

• Also, U.S. LLCs are not considered pass though entities under Japan tax law

Revocable Living Trust• Serves 2 major functions:

1. Avoiding Probate2. Deferring estate taxes for surviving spouse

• Unlike U.S. Citizens, foreign nationals may not make unlimited amounts of gifts to spouses without being taxed

• For foreign nationals, exemption is limited to $60,000 so they will require a special type of trust called the “Qualified Domestic Trust” (QDOT).• Requires a U.S. Citizen trustee so often a U.S. bank is designated.

• U.S.-Japan Tax Treaty based filing may be used to utilize estate tax exemptions. Under this method disclosure of worldwide assets is required.

• Collaborative effort of an U.S. CPA and Japan tax advisor is critical for tax planning.

Revocable Living Trust: Setting it up• Each trust is individualized and personal, so there is no such thing

as a standard trust• It is best that the client meet with the attorney to discuss what

he/she wants to do and how he /she wants the property to pass upon death

• Instead of holding assets in your own individual name, you will hold title as trustee under the terms specified in the trust document you create

• You have the right to all income and the right to use all your trust assets at your pleasure

• You can revoke or amend the trust at any time• Upon your death, the assets in the trust are administered pursuant

to your instructions and distributed to the beneficiaries identified by you – without the need of court approval

Estate Planning– Other important documents

• Durable Power of Attorney – to avoid guardianship in case of disability. But a trust can appoint a successor trustee

• Health Care Directives – Health Care Power of Attorney or Living Will. You can appoint someone to make decisions on termination of life support, or you can direct the physician yourself.

• Pour-over will• Funeral Instructions

Three basic methods:• Probate:

• Process through probate court• Time consuming, expensive, document intensive, sometime

outcome is unexpected.• Tilting and Tenancy of Title:

• Gifting or reserving life estate• Lack of control and flexibility, no creditor protection, gift taxes

(limit of $14,000 per year) • Revocable Living Trust:

• Flexible, private, flexible and can address tax matters• Some may feel initial set up cost is expensive

Transfer on Death Deed (TODD)• Introduced July 1, 2011 • Designate beneficiary in the TODD and recorded during Owner's

lifetime• Can designate a Successor Beneficiary• Effective only upon the owners death• Can be amended or cancelled during lifetime• Beneficiary can refuse upon death of owner (property taken

subject to any mortgages or liens)

Transfer on Death DeedIssues:• Not effective in situations where owner begins to lack

capacity. Cannot sell property for medical costs and can no longer amend the TODD.

• Because the TODD is recorded, the names of the beneficiaries become public record. What if beneficiary is not family or someone expecting to inherit the property??

• Not effective for tax planning• If you hold title in Tenancy by the Entirety, cannot convey

50% by TODD to heirs upon one spouse’s death

• Often when the Seller and Buyer are both Japan nationals, they may want to transact in Yen so save currency exchange costs.

• This is possible but escrow must be notified.• FIRPTA, HARPTA, conveyance tax and of course

broker’s commissions will need to be deposited into escrow in U.S. dollars.

• An escrow system does not exist in Japan so verifying the transfer of funds is difficult.

• Usually used when transaction is between family, friends or related entities.

• Your duties as a broker may only require you to make sure your client is able to acquire the property in an appropriate tenancy

• However, your client may be eternally grateful to you should you advise them of the pitfalls

• It is not too late even after the transaction has closed to consider title issues and post-life transfers

SHIMPEI OKI, ESQ.Goodsill Anderson Quinn & Stifel LLP999 Bishop Street Suite 1600Honolulu, Hawaii 96813(808)[email protected]

Tetsuko Ho, CPA

• 37 years as licensed CPA• Former tax auditor at State Tax Office• Licensed Hawaii real estate agent• Fluent in Japanese and English

Hawaii International Real Estate Council 2016

Tetsuko S. Ho, C.P.A., Inc. 1833 Kalakaua Ave., Suite 910

Honolulu, Hawaii 96815 Tel: (808)942-5464 Fax: (808)942-1087

Email: [email protected]

September 13, 2016

Disclaimer

The materials for this seminar are provided for information purpose only and is not intended as tax advice or advertising.

Please do not rely on this information without consulting a tax advisor. Use of the materials provided does not established any client relationship with TETSUKO S. HO, CPA, INC.

Table of Contents

Individual Taxpayer Identification Number (ITIN) Federal Employer Identification Number (FEIN) Hawaii Tax ID Number (GET/TAT) Real Property Tax FIRPTA/HARPTA 1031 Exchange Property Title Estate and Gift Tax Utilizing Japan Depreciation and useful-life tax rule for investing in

Hawaii real property Foreign Financial Asset Disclosure

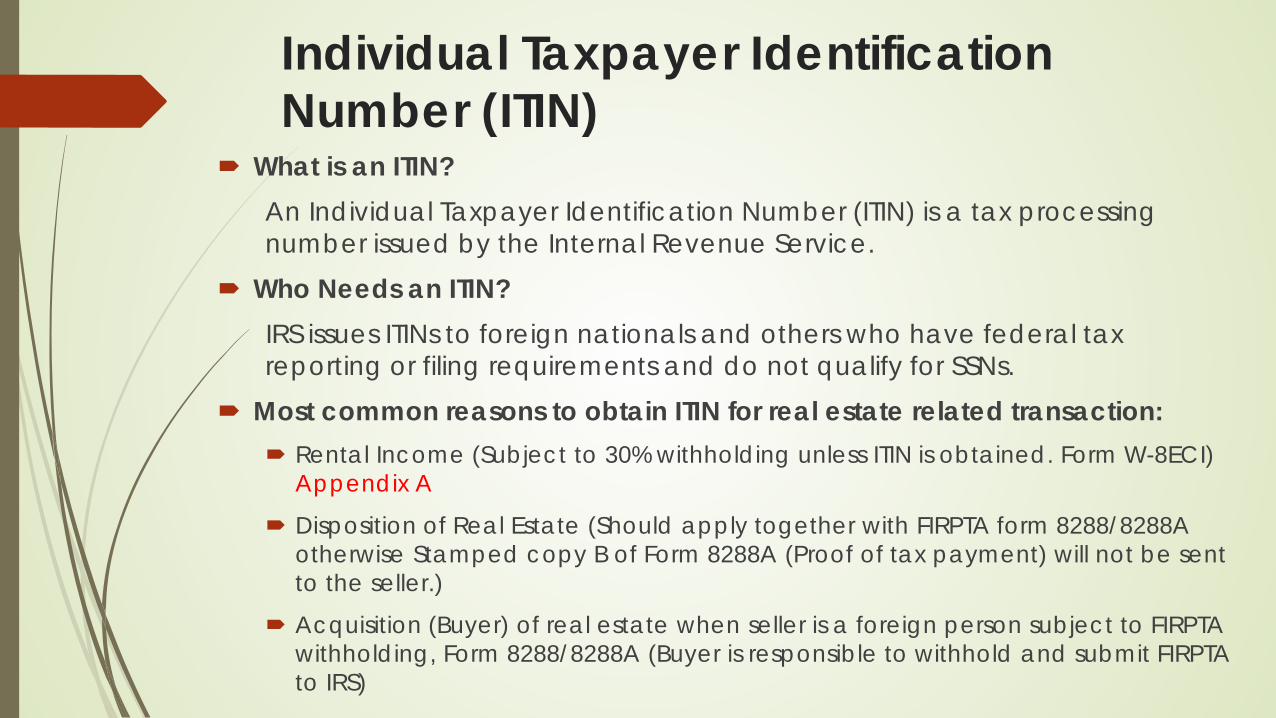

Individual Taxpayer Identification Number (ITIN)

What is an ITIN?An Individual Taxpayer Identification Number (ITIN) is a tax processing number issued by the Internal Revenue Service.

Who Needs an ITIN?IRS issues ITINs to foreign nationals and others who have federal tax reporting or filing requirements and do not qualify for SSNs.

Most common reasons to obtain ITIN for real estate related transaction: Rental Income (Subject to 30% withholding unless ITIN is obtained. Form W-8ECI)

Appendix A

Disposition of Real Estate (Should apply together with FIRPTA form 8288/8288A otherwise Stamped copy B of Form 8288A (Proof of tax payment) will not be sent to the seller.)

Acquisition (Buyer) of real estate when seller is a foreign person subject to FIRPTA withholding, Form 8288/8288A (Buyer is responsible to withhold and submit FIRPTA to IRS)

Continue: How to Apply for an ITIN

Documents needed to apply for ITIN:

ITIN Application (Form W-7: Appendix B) Note: Preparer needs to be careful to check appropriate box – reason for applying ITIN (a,b & h).

Original Passport or Certified copy of passport *

Supporting documents: Tax Return OR

- Rental: Property management agreement AND letter from property manager requesting ITIN. - Disposition: Purchase contract, Settlement Statement AND Copy of Form 8288/8288A

* Passport must be certified by one of the following: Consulate General of Japan in Honolulu – No longer Certifying

U.S. Embassy/Consulate in Japan (Appointment only) – Appendix C

IRS Office in Honolulu (300 Ala Moana Blvd. Honolulu, HI 96850 - Appointment only)

Certified Acceptance Agent:

11 CAA in Honolulu https://www.irs.gov/individuals/acceptance-agents-hawaii

Tetsuko S. Ho, C.P.A., Inc. will be a CAA starting from October 2016.

Continue:

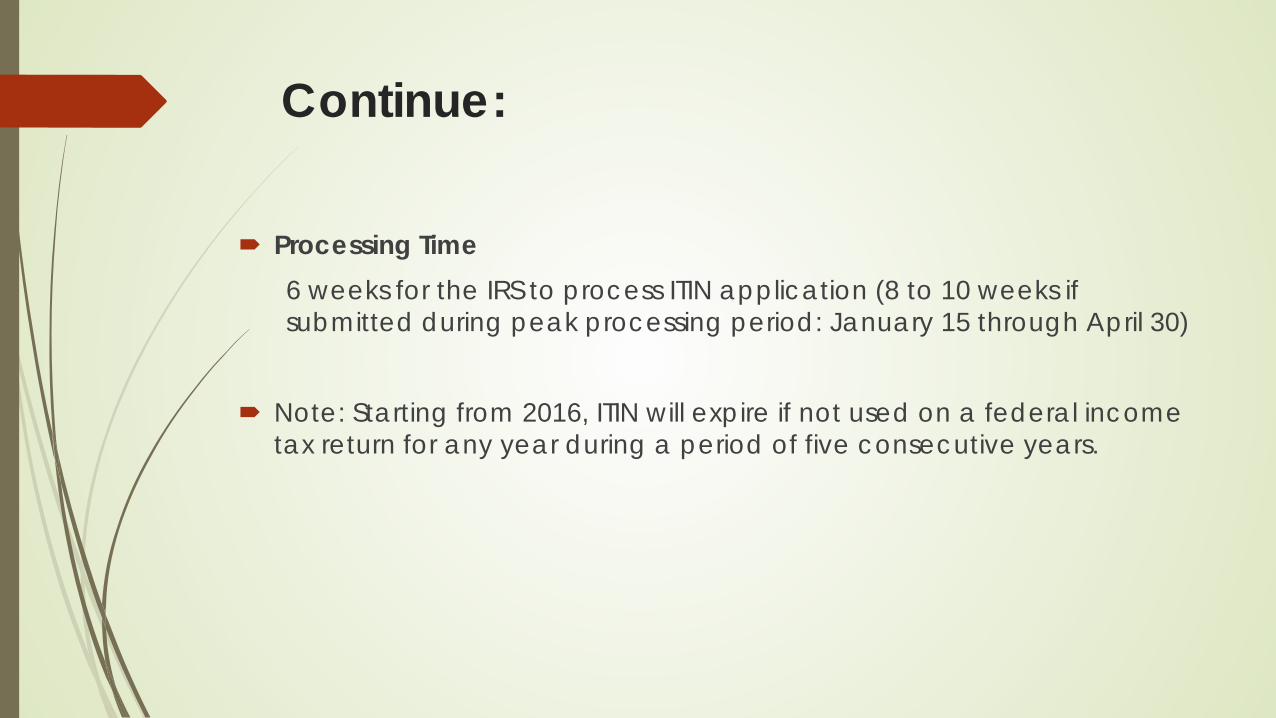

Processing Time6 weeks for the IRS to process ITIN application (8 to 10 weeks if submitted during peak processing period: January 15 through April 30)

Note: Starting from 2016, ITIN will expire if not used on a federal income tax return for any year during a period of five consecutive years.

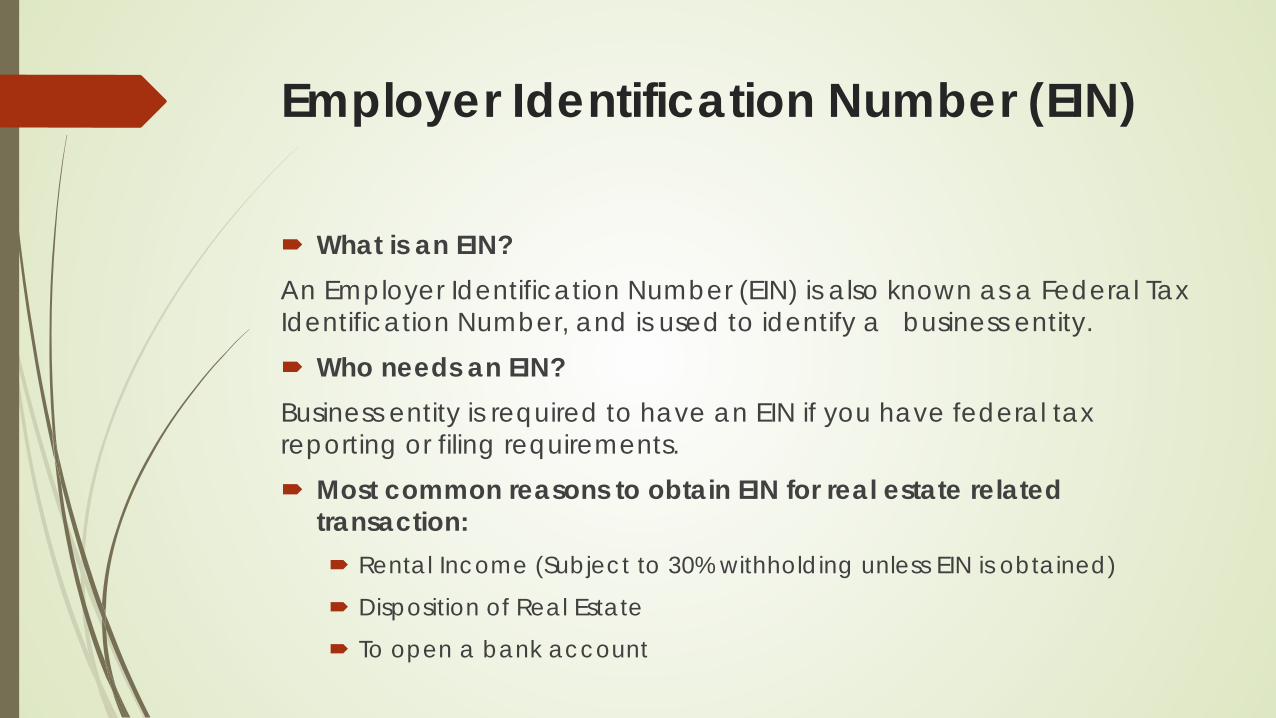

Employer Identification Number (EIN)

What is an EIN?An Employer Identification Number (EIN) is also known as a Federal Tax Identification Number, and is used to identify a business entity. Who needs an EIN?Business entity is required to have an EIN if you have federal tax reporting or filing requirements. Most common reasons to obtain EIN for real estate related

transaction: Rental Income (Subject to 30% withholding unless EIN is obtained)

Disposition of Real Estate

To open a bank account

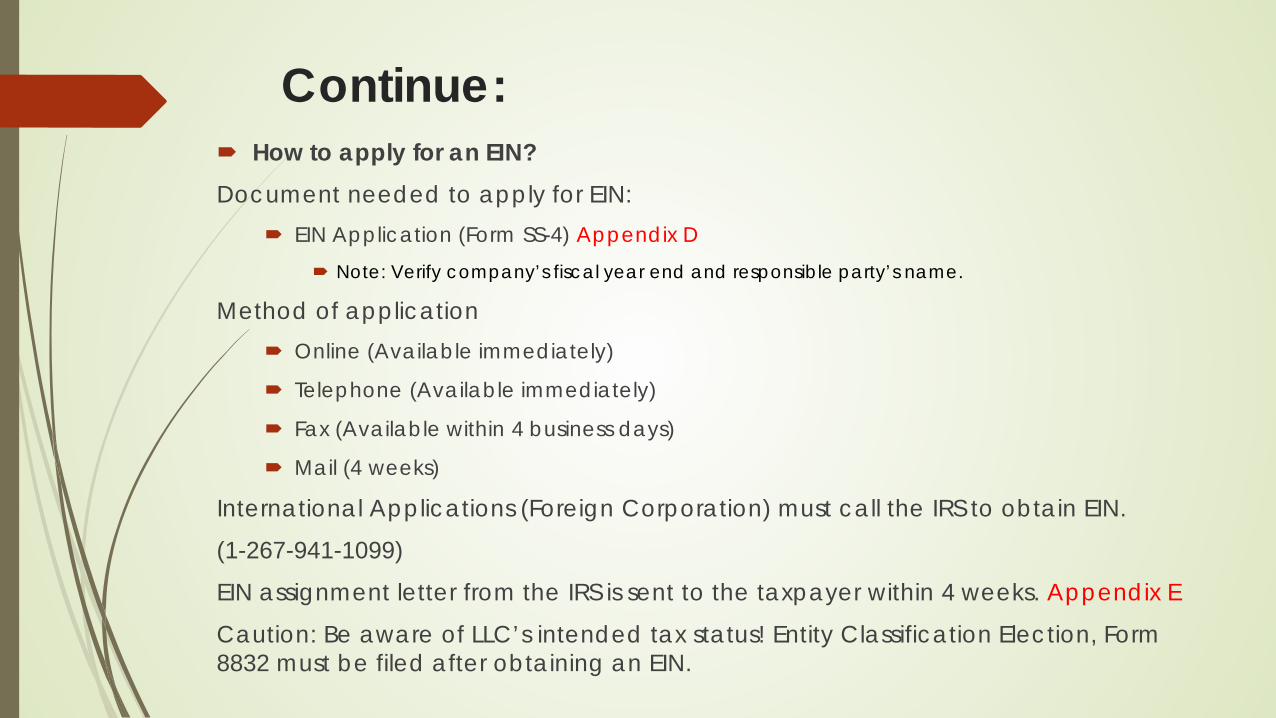

Continue: How to apply for an EIN?Document needed to apply for EIN:

EIN Application (Form SS-4) Appendix D Note: Verify company’s fiscal year end and responsible party’s name.

Method of application Online (Available immediately)

Telephone (Available immediately)

Fax (Available within 4 business days)

Mail (4 weeks)

International Applications (Foreign Corporation) must call the IRS to obtain EIN.

(1-267-941-1099)

EIN assignment letter from the IRS is sent to the taxpayer within 4 weeks. Appendix E

Caution: Be aware of LLC’s intended tax status! Entity Classification Election, Form 8832 must be filed after obtaining an EIN.

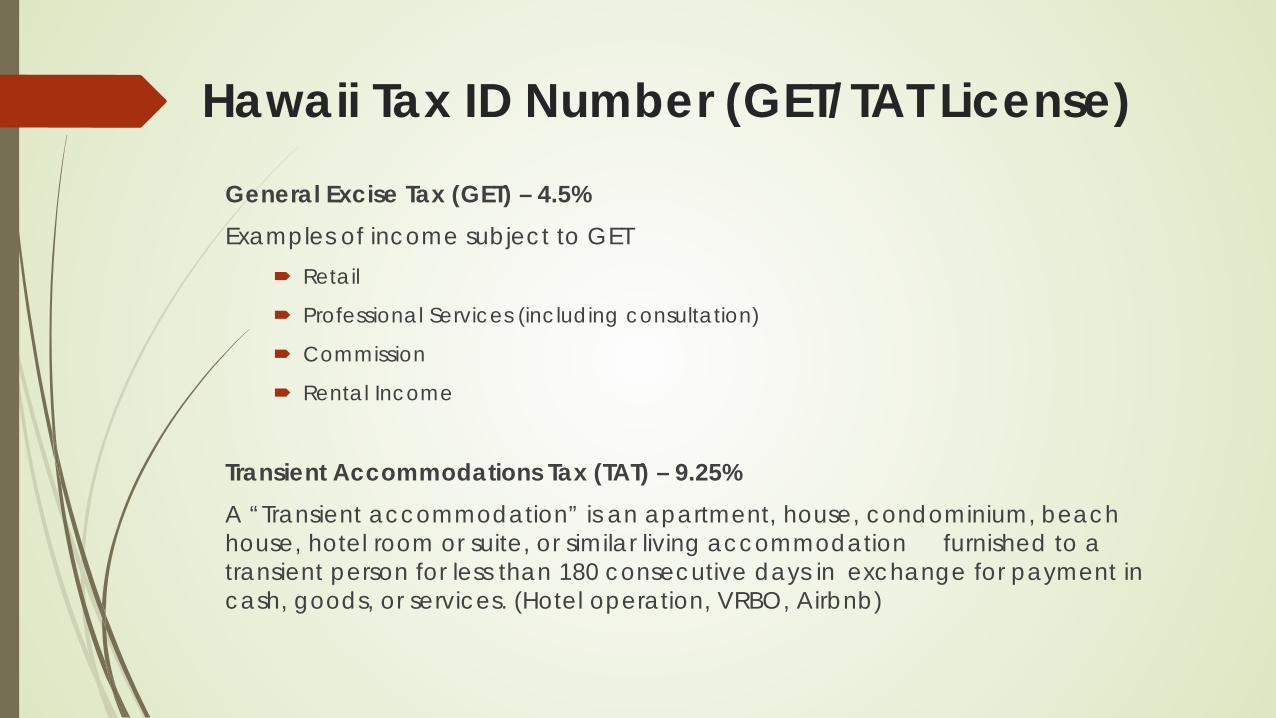

Hawaii Tax ID Number (GET/TAT License)General Excise Tax (GET) – 4.5%Examples of income subject to GET

Retail

Professional Services (including consultation)

Commission

Rental Income

Transient Accommodations Tax (TAT) – 9.25%A “Transient accommodation” is an apartment, house, condominium, beach house, hotel room or suite, or similar living accommodation furnished to a transient person for less than 180 consecutive days in exchange for payment in cash, goods, or services. (Hotel operation, VRBO, Airbnb)

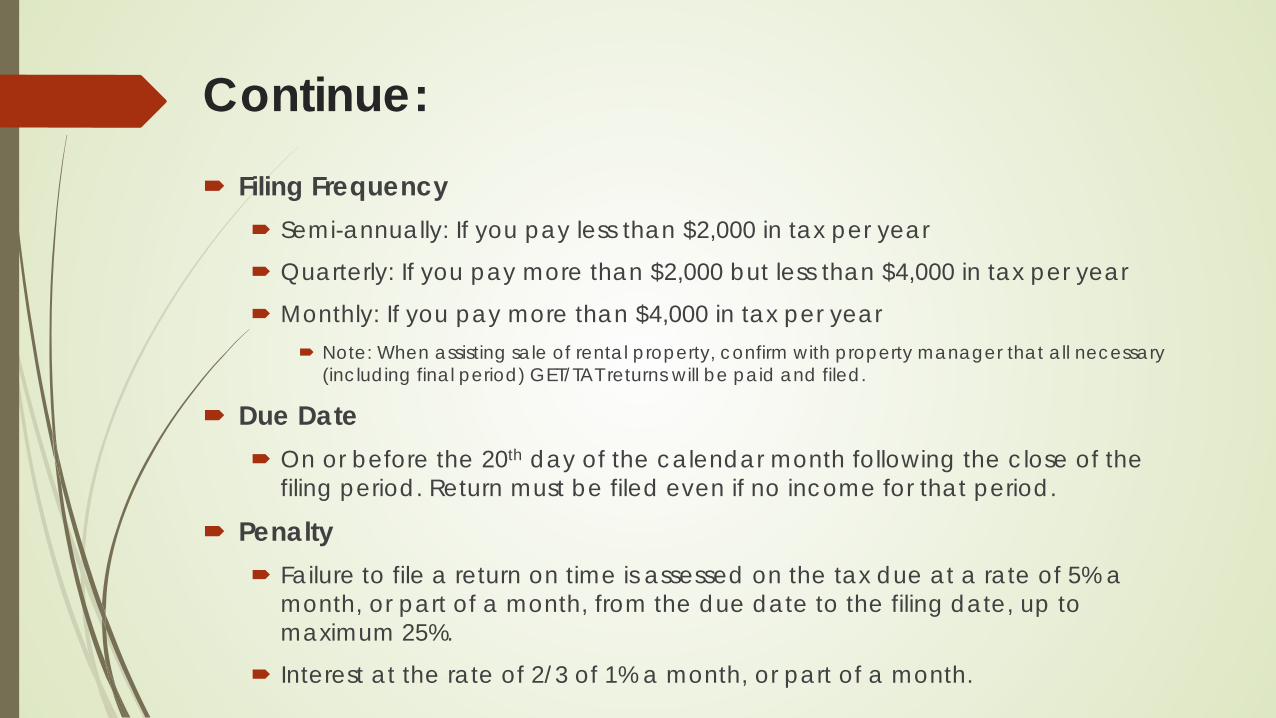

Continue: Filing Frequency

Semi-annually: If you pay less than $2,000 in tax per year

Quarterly: If you pay more than $2,000 but less than $4,000 in tax per year

Monthly: If you pay more than $4,000 in tax per year Note: When assisting sale of rental property, confirm with property manager that all necessary

(including final period) GET/TAT returns will be paid and filed.

Due Date On or before the 20th day of the calendar month following the close of the

filing period. Return must be filed even if no income for that period.

Penalty Failure to file a return on time is assessed on the tax due at a rate of 5% a

month, or part of a month, from the due date to the filing date, up to maximum 25%.

Interest at the rate of 2/3 of 1% a month, or part of a month.

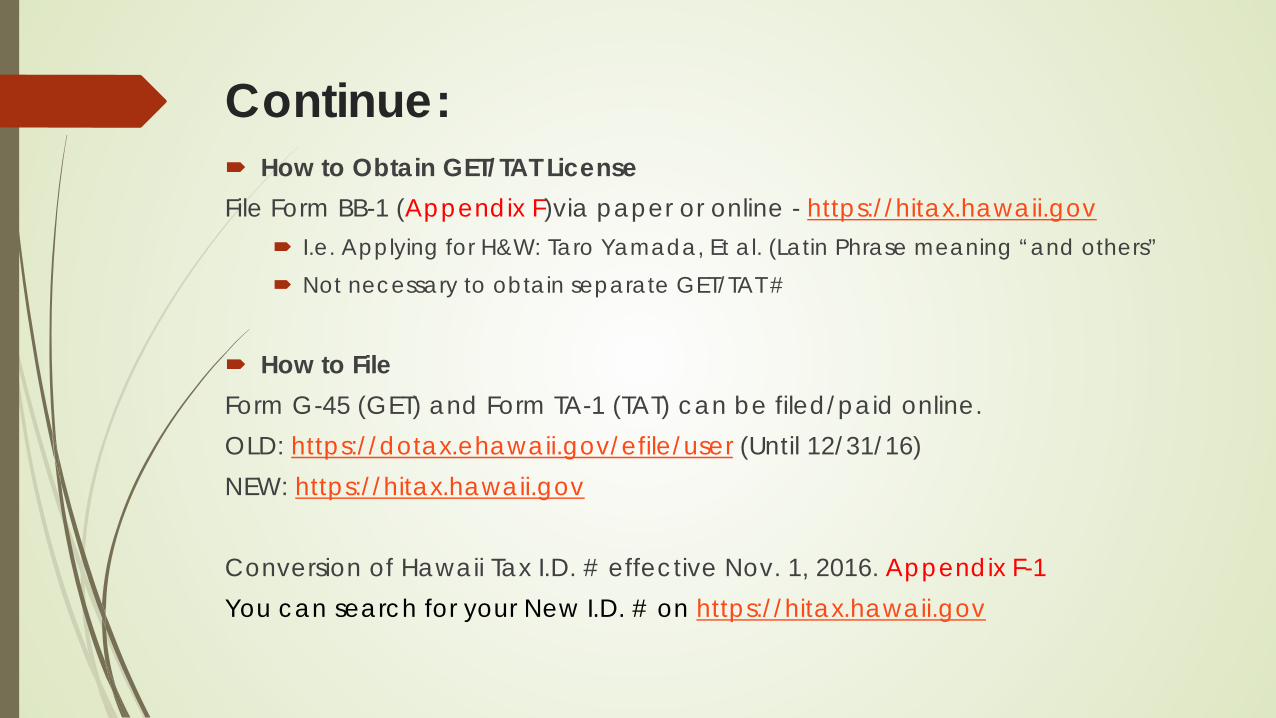

Continue: How to Obtain GET/TAT LicenseFile Form BB-1 (Appendix F)via paper or online - https://hitax.hawaii.gov

I.e. Applying for H&W: Taro Yamada, Et al. (Latin Phrase meaning “and others” Not necessary to obtain separate GET/TAT #

How to FileForm G-45 (GET) and Form TA-1 (TAT) can be filed/paid online.OLD: https://dotax.ehawaii.gov/efile/user (Until 12/31/16)NEW: https://hitax.hawaii.gov

Conversion of Hawaii Tax I.D. # effective Nov. 1, 2016. Appendix F-1You can search for your New I.D. # on https://hitax.hawaii.gov

Real Property Tax

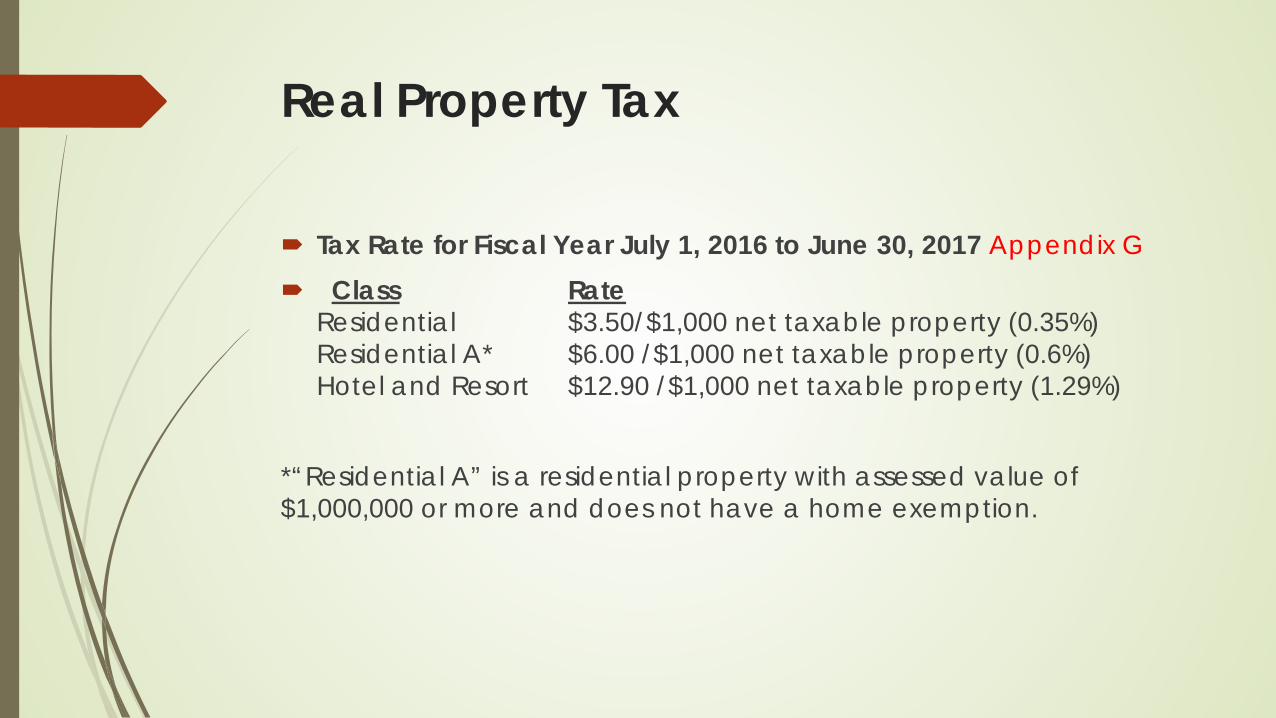

Tax Rate for Fiscal Year July 1, 2016 to June 30, 2017 Appendix G Class Rate

Residential $3.50/$1,000 net taxable property (0.35%)Residential A* $6.00 /$1,000 net taxable property (0.6%)Hotel and Resort $12.90 /$1,000 net taxable property (1.29%)

*“Residential A” is a residential property with assessed value of $1,000,000 or more and does not have a home exemption.

Continue:

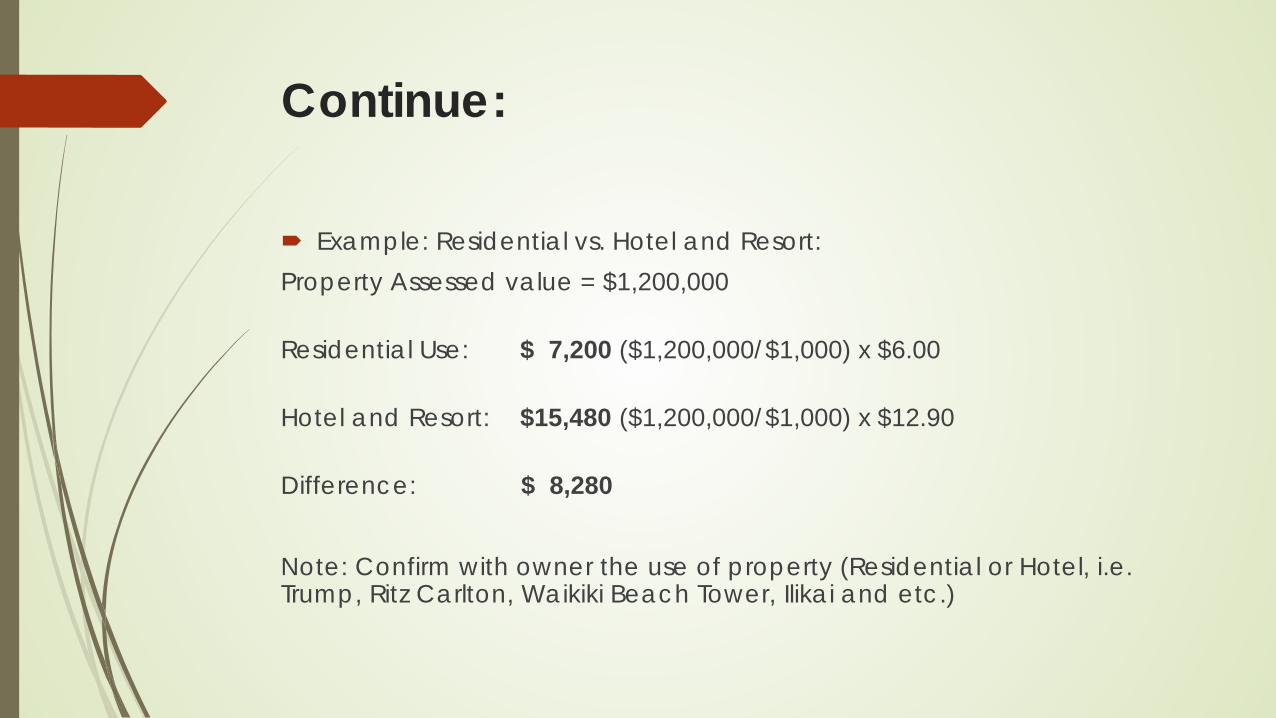

Example: Residential vs. Hotel and Resort: Property Assessed value = $1,200,000

Residential Use: $ 7,200 ($1,200,000/$1,000) x $6.00

Hotel and Resort: $15,480 ($1,200,000/$1,000) x $12.90

Difference: $ 8,280

Note: Confirm with owner the use of property (Residential or Hotel, i.e. Trump, Ritz Carlton, Waikiki Beach Tower, Ilikai and etc.)

Continue:

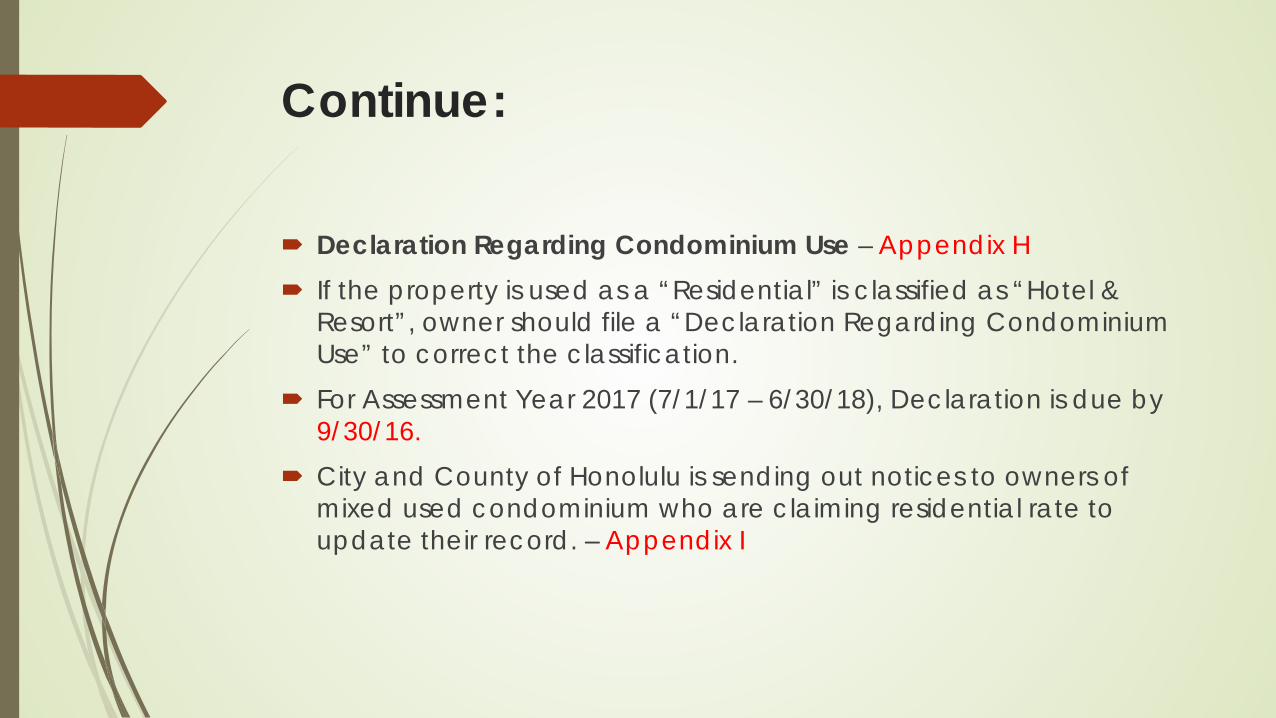

Declaration Regarding Condominium Use – Appendix H If the property is used as a “Residential” is classified as “Hotel &

Resort”, owner should file a “Declaration Regarding Condominium Use” to correct the classification.

For Assessment Year 2017 (7/1/17 – 6/30/18), Declaration is due by 9/30/16.

City and County of Honolulu is sending out notices to owners of mixed used condominium who are claiming residential rate to update their record. – Appendix I

Continue:

Home Exemption (Residents Only) Basic Exclusion: $80,000

65 years and older: $120,000 Qualification: You own and occupy the property as your principal

home. (Principal home requirement may be evidenced by: occupancy of a home in the city for more than 270 calendar days, registered to vote, filing tax return as a resident of the State of Hawaii.

File Form P-3 or apply online https://www.realpropertyhonolulu.comby September 30.

Check your own house to see if you currently have home exemption.-> http://qpublic9.qpublic.net/hi_honolulu_search.php

Continue:

Caution: Real property tax bill may not be delivered to new owner’s address if sales transaction takes place after 10/1/16. Send assessment back to R/P assessment division with “SOLD” and the date it was sold written on the notice.

Remind new owner of property that due date of real property tax payment is February and August 20th every year to avoid penalty and interest.

FIRPTA/HARPTA What is FIRPTA/HARPTA withholding?Foreign person who dispose U.S. real property interest is subject to Income tax withholding. Appendix J

FIRPTA (Federal) – 15% of Gross sales priceHARPTA (State) – 5% of Gross sales price

FIRPTA Exempt from FIRPTA if sales price is less than $300,000 and buyer acquires the

property for use as residence. *You or a member of your family must have definite plans to reside at the property for at least 50% of the number of days the property is used by any person during each of the first two 12-month periods following the date of transfer.

The 10% rate will still apply for those transactions in which the property is to be used by the buyer as a residence, provided the sales price does not exceed $1,000,000.

Foreign person includes: nonresident alien individual and foreign corporation.

Continue:

Withholding Certificate Seller can eliminate or reduce withholding amount by obtaining a withholding certificate from the IRS/State. Withholding certificate/Reduced withholding certificate can be applied if there is no gain or maximum tax liability is less than the tax otherwise required to be withheld.

Federal – Appendix K

File Form 8288B to request for withholding certificate. It takes about 90 days for the IRS to reply. Most escrow company does not hold the FIRPTA fund after the closing date except a few.

State – Appendix L

It has to be a loss to apply for withholding certificate from State Tax Office. Form N-288B must be filed 10 business days before the closing date.

Foreign Corporation is exempt from HARPTA if company is registered with DCCA – Appendix L-1

Continue:

Early RefundIf applying for withholding certificate is not an option, seller can request for an early refund of FIRPTA/HARPTA. Processing time is 4-6 months.

Note: Tax return must be filed in the following year even if you obtained a withholding certificate or requested for an early refund.If transaction takes place after September, it may be better to request refund through normal tax filing.

1031 Exchange

What is a 1031 Exchange?Whenever you sell business or investment property and you have a gain, you generally have to pay tax on the gain at the time of sale. IRC Section 1031 provides an exception and allows you to postpone paying tax on the gain if you reinvest the proceeds in similar property as part of a qualifying like-kind exchange. Gain deferred in a like-kind exchange under IRC Section 1031 is tax-deferred, but it is not tax-free.

Continue:

What Properties Qualify?Must be held for use in a trade or business or for investment. Property used primarily for personal use, like a primary residence or a second home or vacation home, does not qualify for like-kind exchange treatment.Most real estate will be like-kind to other real estate. For example, real property that is improved with a residential rental house is like-kind to vacant land. One exception for real estate is that property within the United States is not like-kind to property outside of the United States. For Hawaii, it still qualifies as 1031 exchange even if replacement property is outside of Hawaii.

Continue:

Other Requirement for 1031 ExchangeReplacement property must be identify within 45 days after you sell the old property and exchange must be completed no later than 180 days after the sale of the exchange property or the due date (with extension) of the income tax return, whichever is earlier.

Continue:

Reverse 1031 Exchange Buy new property first and sell old property later.

“Safeharbor format” Taxpayer have 180 days to sell the old property.

“Traditional format” Taxpayer have 6 years to sell the old property.

Election to choose safeharbor or traditional format must be made when 1031 was initially set up (purchased).

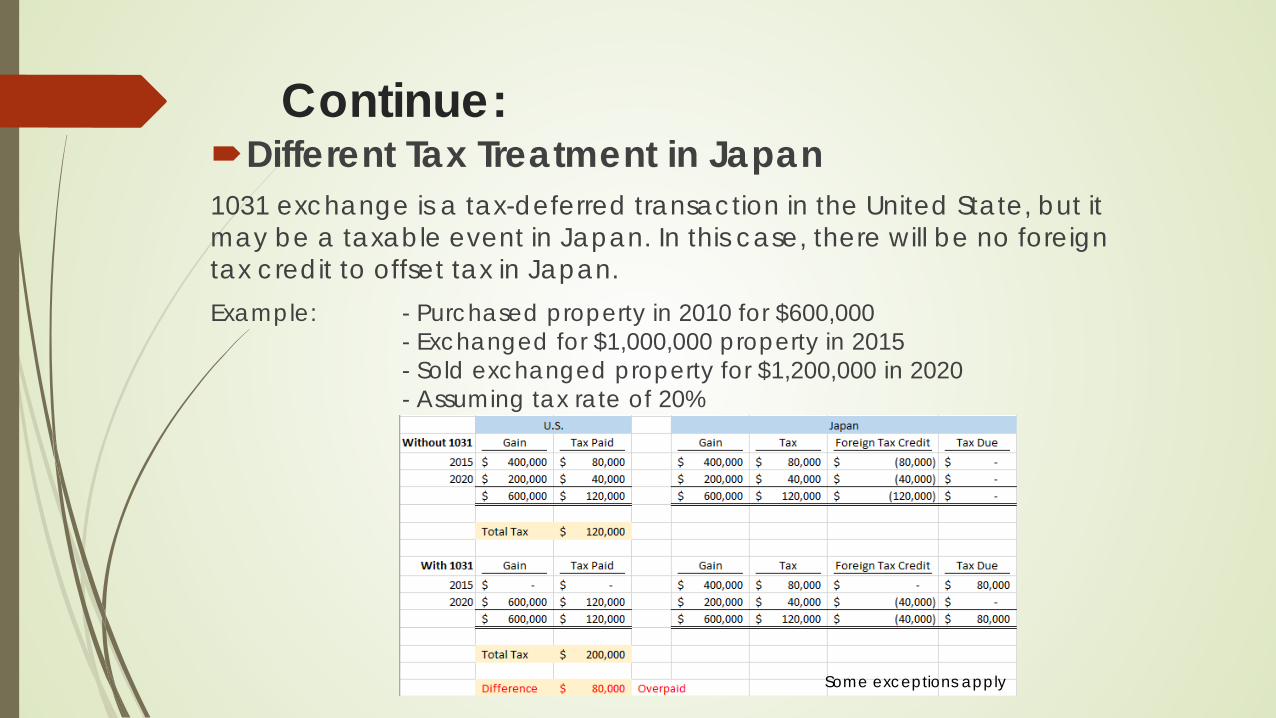

Continue:Different Tax Treatment in Japan1031 exchange is a tax-deferred transaction in the United State, but it may be a taxable event in Japan. In this case, there will be no foreign tax credit to offset tax in Japan.Example: - Purchased property in 2010 for $600,000

- Exchanged for $1,000,000 property in 2015- Sold exchanged property for $1,200,000 in 2020 - Assuming tax rate of 20%

Some exceptions apply

Property Title

Property Title Tenancy by the Severalty: Tenancy by the severalty is held by one

person.

Tenancy by the Entirety: Tenancy by the Entirety is held by husband and wife. Title automatically transfer to surviving spouse upon death. Does not mean not subject to U.S. Estate Tax.

Joint Tenancy: Joint Tenancy is equally owned by two or more people. Title automatically transfers to co-owner upon death. Does not mean not subject to U.S. Estate tax.

Tenancy in Common: Tenancy in Common owned by two or more individual/RLT/TODD/LLC/Inc. Does not need to be equal share.

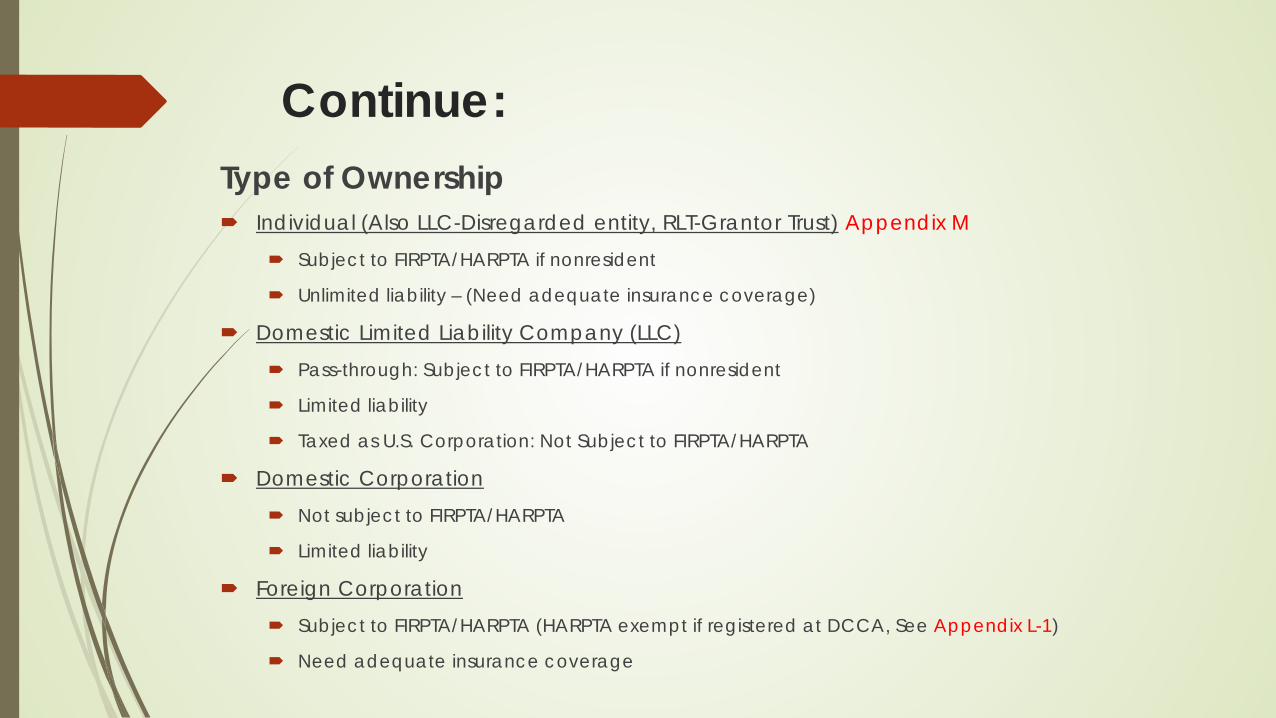

Continue:Type of Ownership Individual (Also LLC-Disregarded entity, RLT-Grantor Trust) Appendix M

Subject to FIRPTA/HARPTA if nonresident

Unlimited liability – (Need adequate insurance coverage)

Domestic Limited Liability Company (LLC) Pass-through: Subject to FIRPTA/HARPTA if nonresident

Limited liability

Taxed as U.S. Corporation: Not Subject to FIRPTA/HARPTA

Domestic Corporation Not subject to FIRPTA/HARPTA

Limited liability

Foreign Corporation Subject to FIRPTA/HARPTA (HARPTA exempt if registered at DCCA, See Appendix L-1)

Need adequate insurance coverage

Continue:To avoid probate, you may consider the following:Transfer on Death Deed (TODD)

Hawaii allows Transfer on Death Deed where it allows you to select beneficiary who will receive your property upon death, thus eliminating cost of creating a will or a trust and avoid probate at the same time. TODD is available for tenancy by the severalty and tenancy in common. Additional planning may be necessary in case of owner’s incapacitation (i.e. durable power of attorney).

Payable on Death Account (POD) Bank, Investment Accounts

POD account is a type of bank account where it allows you to select the beneficiary and money will transfer upon death without going to probate.

Cotton Trust in case of incapacitation (Need approval from two doctors and court).

If bank will not release fund in spite of all necessary actions are taken, report incident to Consumer Financial Protection Bureau (CFPB).

Revocable Living Trust

The out-of-court affidavit procedure (simplified probate) is available in Hawaii if the value of property the deceased person owned is $100,000 or less.

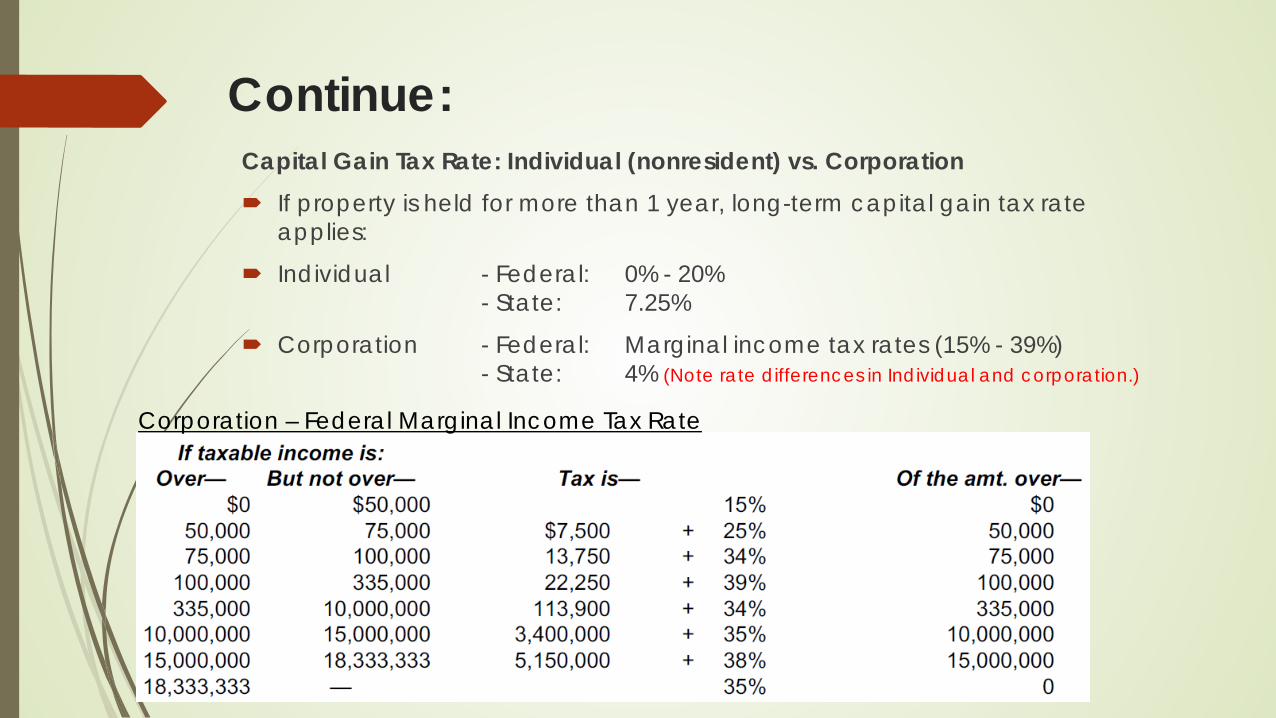

Continue:Capital Gain Tax Rate: Individual (nonresident) vs. Corporation If property is held for more than 1 year, long-term capital gain tax rate

applies:

Individual - Federal: 0% - 20% - State: 7.25%

Corporation - Federal: Marginal income tax rates (15% - 39%)- State: 4% (Note rate differences in Individual and corporation.)

Corporation – Federal Marginal Income Tax Rate

Continue:

Transfer of OwnershipOwnership transfer or title name change is considered

taxable event and most of the time it should be transferred at fair market value and reported on tax return. Loss is not recognized if transaction is between related parties.

Estate and Gift Tax Tax RateMaximum Estate and Gift Tax rate is 40%.

Exclusion AmountResident

Applicable exclusion amount for U.S. resident is $5,450,000 in 2016. Total $10.9 million exclusions for husband & wife.

Transfer between U.S. citizen spouses are unlimited marital deduction

Non-resident

Applicable exclusion amount for Non-resident alien is $60,000.

Non-resident alien must file Form 706NA if he/she had a real property located in the U.S. and the fair market value of the property is more than $60,000.

Japan – U.S. Estate, Inheritance and Gift Tax Treaty can be used to reduce tax liability.

Continue:

Example of Tax Treaty Benefit Hawaii property $1,000,000

Japan Asset $4,000,000Worldwide asset $5,000,000

U.S. Estate and Gift Tax without tax treaty $ 322,400[((1,000,000 – 60,000 – 750,000) x 39%) + 248,300]

U.S. Estate and Gift Tax with tax treaty $ 0Exclusion available: [$5,450,000 x (1,000,000/5,000,000)] = $1,090,000

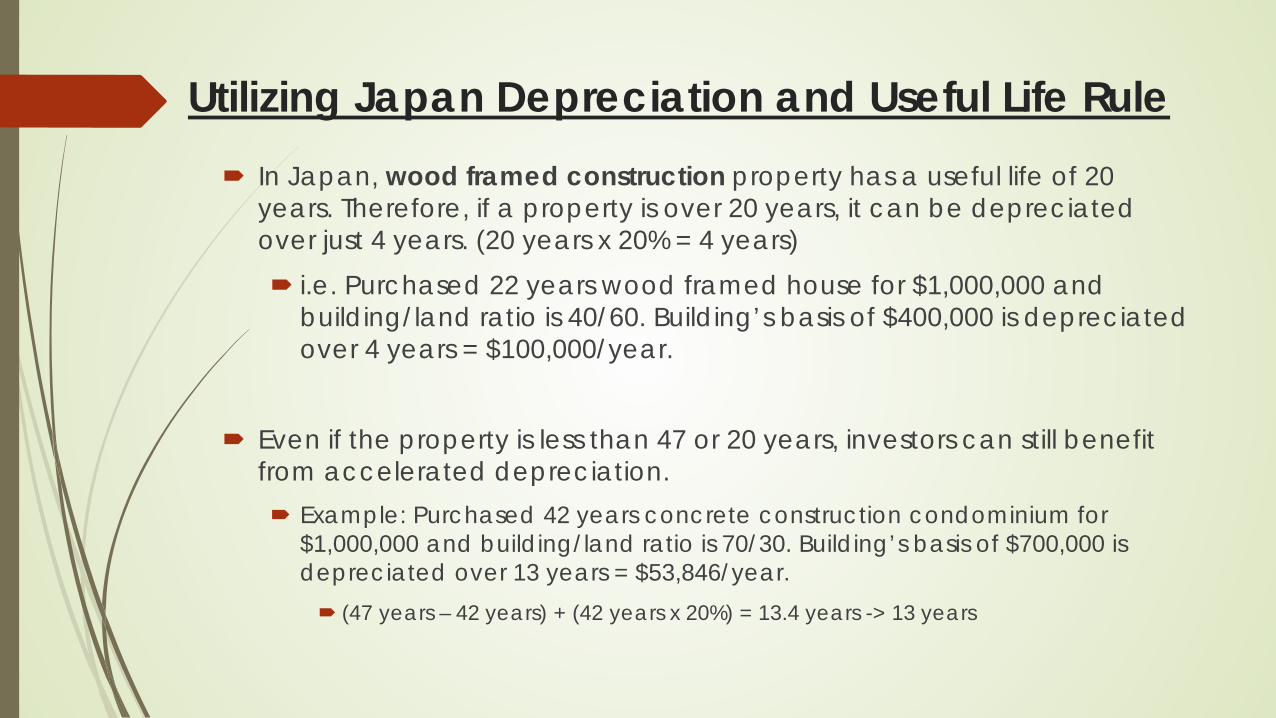

Utilizing Japan Depreciation and Useful Life Rule Japanese investors can achieve a significant tax savings in Japan by

utilizing their depreciation and useful life rule for certain U.S. properties.

Old/used properties that are past their useful life designated by Japan tax law can be depreciated over 20% of its normal recovery period.

Concrete construction condominium has a useful life of 47 years. If a condominium is over 47 years, it can be depreciated over 9 years (47 years x 20% = 9.4 years -> 9 years (rounded off)) i.e. Purchased 47 years concrete construction condominium for $1,000,000

and building/land ratio is 70/30. Building’s basis of $700,000 is depreciated over 9 years = $77,777/year.

Utilizing Japan Depreciation and Useful Life Rule In Japan, wood framed construction property has a useful life of 20

years. Therefore, if a property is over 20 years, it can be depreciated over just 4 years. (20 years x 20% = 4 years) i.e. Purchased 22 years wood framed house for $1,000,000 and

building/land ratio is 40/60. Building’s basis of $400,000 is depreciated over 4 years = $100,000/year.

Even if the property is less than 47 or 20 years, investors can still benefit from accelerated depreciation. Example: Purchased 42 years concrete construction condominium for

$1,000,000 and building/land ratio is 70/30. Building’s basis of $700,000 is depreciated over 13 years = $53,846/year. (47 years – 42 years) + (42 years x 20%) = 13.4 years -> 13 years

Utilizing Japan Depreciation and Useful Life Rule

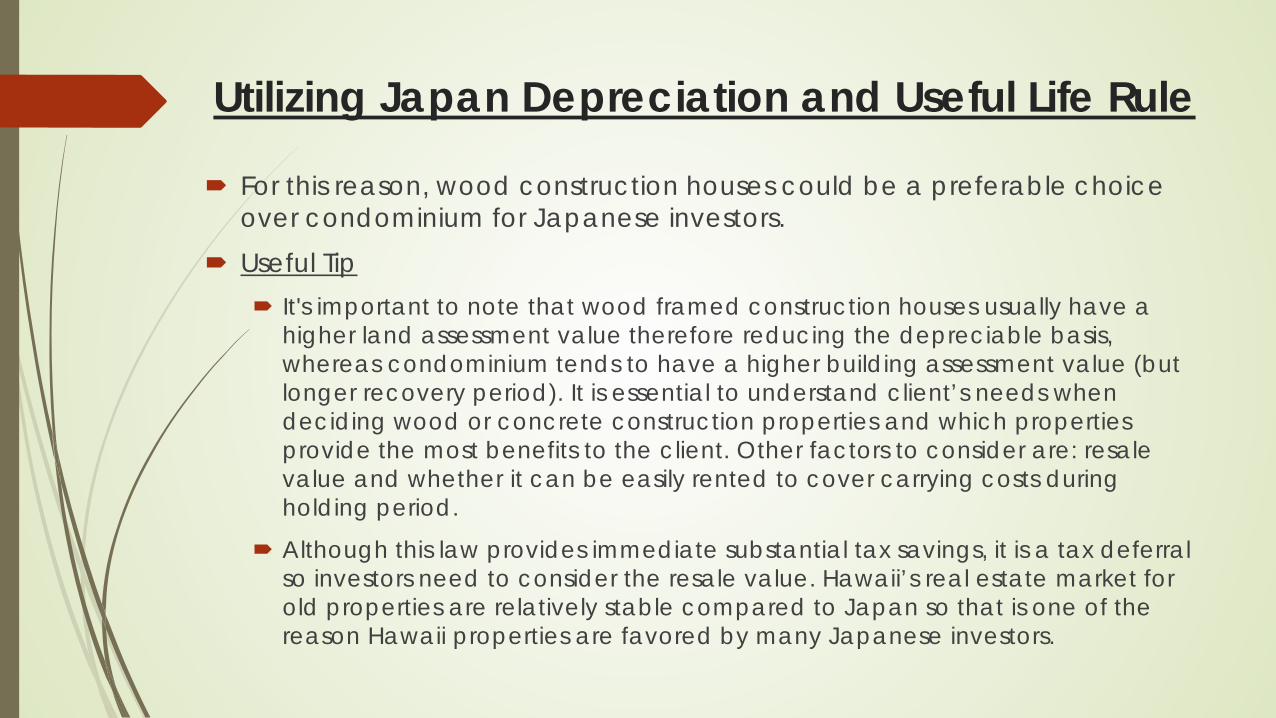

For this reason, wood construction houses could be a preferable choice over condominium for Japanese investors.

Useful Tip It's important to note that wood framed construction houses usually have a

higher land assessment value therefore reducing the depreciable basis, whereas condominium tends to have a higher building assessment value (but longer recovery period). It is essential to understand client’s needs when deciding wood or concrete construction properties and which properties provide the most benefits to the client. Other factors to consider are: resale value and whether it can be easily rented to cover carrying costs during holding period.

Although this law provides immediate substantial tax savings, it is a tax deferral so investors need to consider the resale value. Hawaii’s real estate market for old properties are relatively stable compared to Japan so that is one of the reason Hawaii properties are favored by many Japanese investors.

Utilizing Japan Depreciation and Useful Life Rule

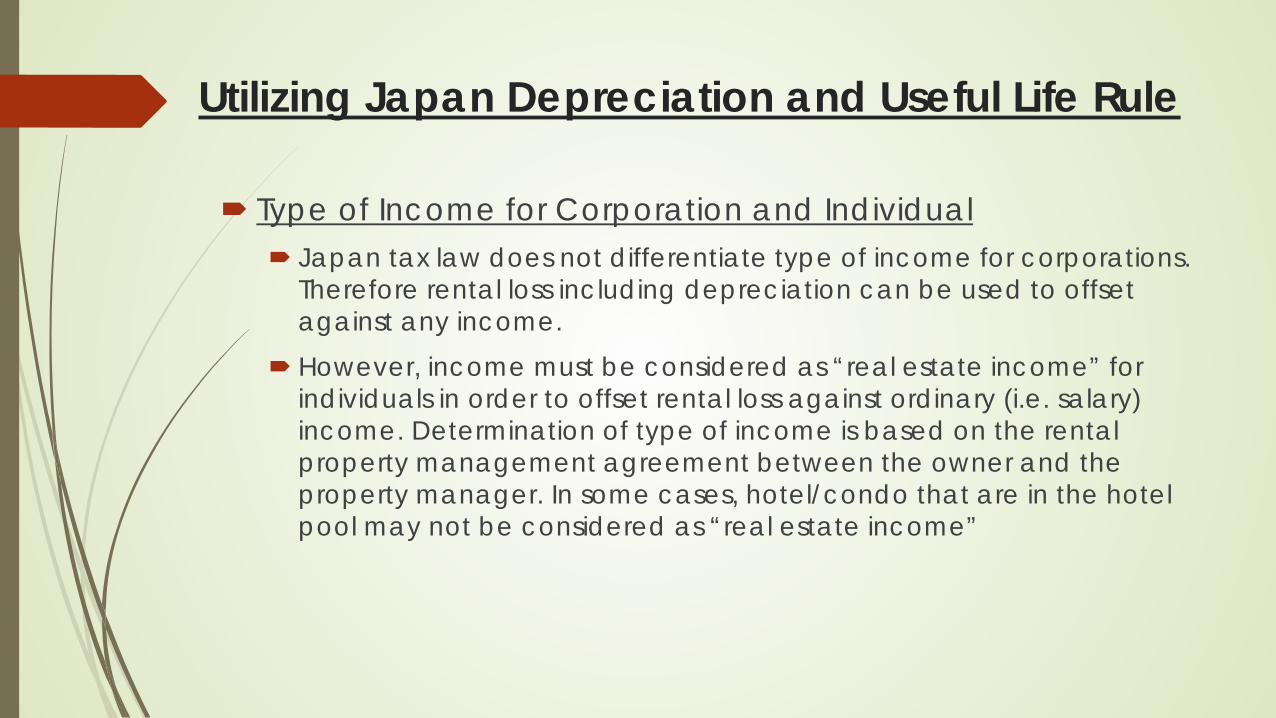

Type of Income for Corporation and Individual Japan tax law does not differentiate type of income for corporations.

Therefore rental loss including depreciation can be used to offset against any income.

However, income must be considered as “real estate income” for individuals in order to offset rental loss against ordinary (i.e. salary) income. Determination of type of income is based on the rental property management agreement between the owner and the property manager. In some cases, hotel/condo that are in the hotel pool may not be considered as “real estate income”

Utilizing Japan Depreciation and Useful Life Rule

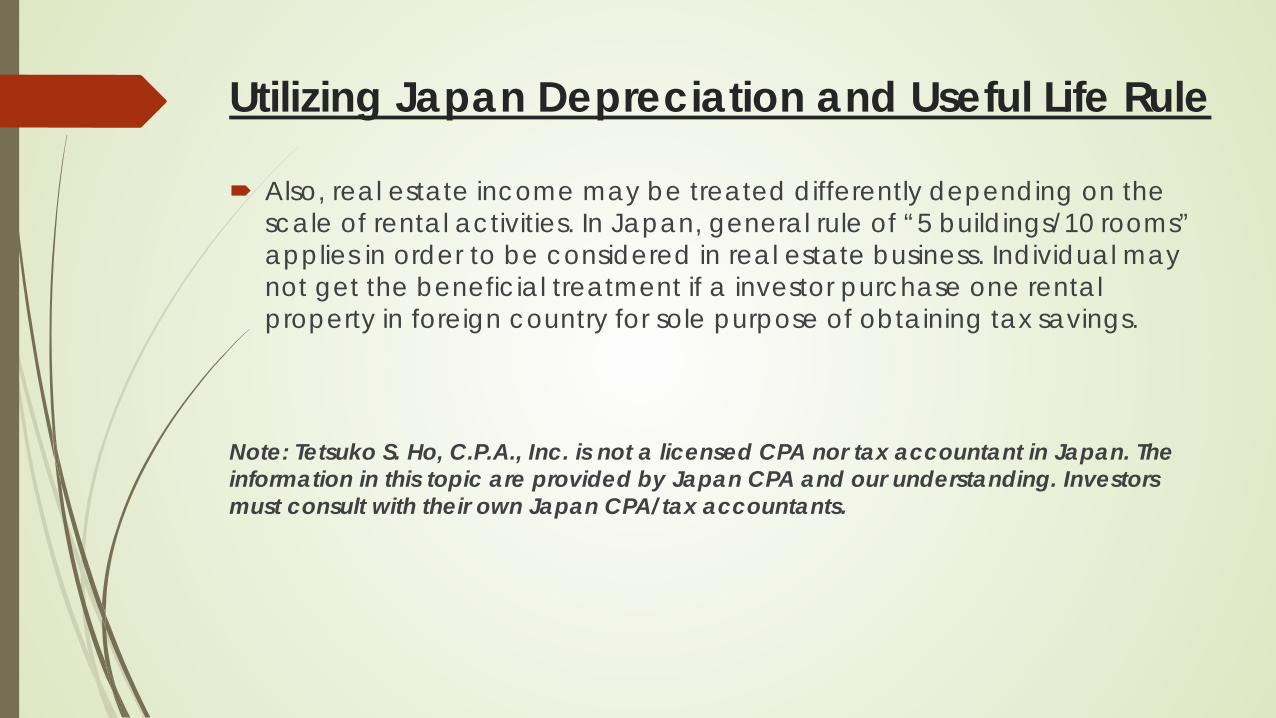

Also, real estate income may be treated differently depending on the scale of rental activities. In Japan, general rule of “5 buildings/10 rooms” applies in order to be considered in real estate business. Individual may not get the beneficial treatment if a investor purchase one rental property in foreign country for sole purpose of obtaining tax savings.

Note: Tetsuko S. Ho, C.P.A., Inc. is not a licensed CPA nor tax accountant in Japan. The information in this topic are provided by Japan CPA and our understanding. Investors must consult with their own Japan CPA/tax accountants.

Foreign Financial Asset Disclosure

U.S. person are required to report their foreign financial assets every year if they meet the filing threshold. There are two different filing requirements.

Report of Foreign Bank and Financial Accounts (FBAR) Statement of Specified Foreign Financial Assets (FATCA)

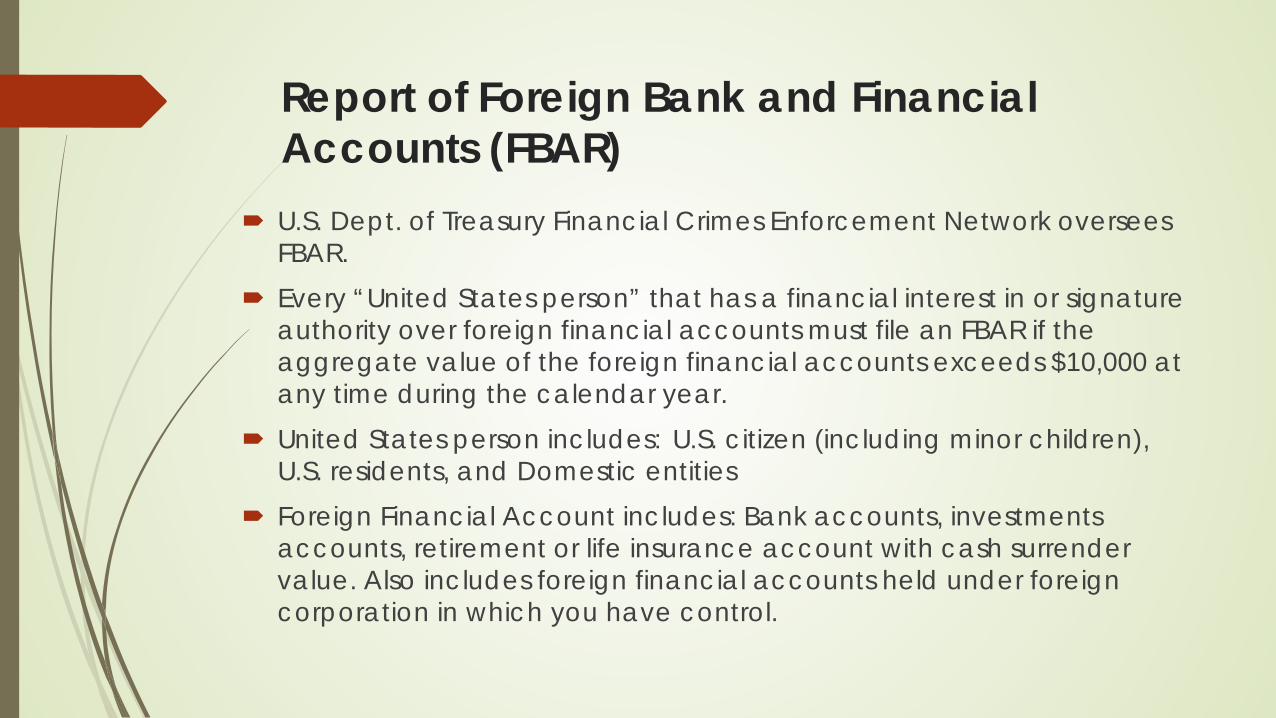

Report of Foreign Bank and Financial Accounts (FBAR)

U.S. Dept. of Treasury Financial Crimes Enforcement Network oversees FBAR.

Every “United States person” that has a financial interest in or signature authority over foreign financial accounts must file an FBAR if the aggregate value of the foreign financial accounts exceeds $10,000 at any time during the calendar year.

United States person includes: U.S. citizen (including minor children), U.S. residents, and Domestic entities

Foreign Financial Account includes: Bank accounts, investments accounts, retirement or life insurance account with cash surrender value. Also includes foreign financial accounts held under foreign corporation in which you have control.

Continue(FBAR):

Due Date: 2015: June 30th (No Extension)

2016: April 15th (6 month extension available)

Penalty:Non-willful: up to $10,000 per violationWillful: Greater of $100,000 or 50% of the balance in

the account at the time of the violation. Criminal penalties may also apply.

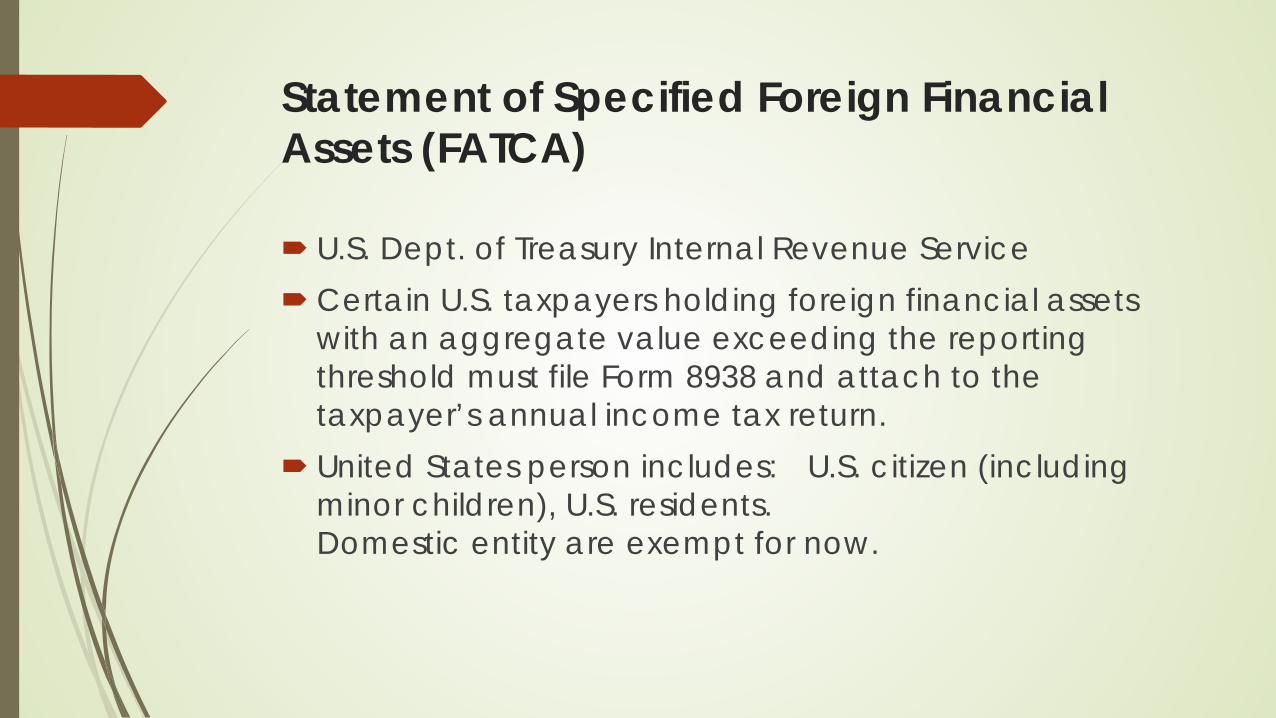

Statement of Specified Foreign Financial Assets (FATCA)

U.S. Dept. of Treasury Internal Revenue ServiceCertain U.S. taxpayers holding foreign financial assets

with an aggregate value exceeding the reporting threshold must file Form 8938 and attach to the taxpayer’s annual income tax return.

United States person includes: U.S. citizen (including minor children), U.S. residents. Domestic entity are exempt for now.

Continue (FATCA):

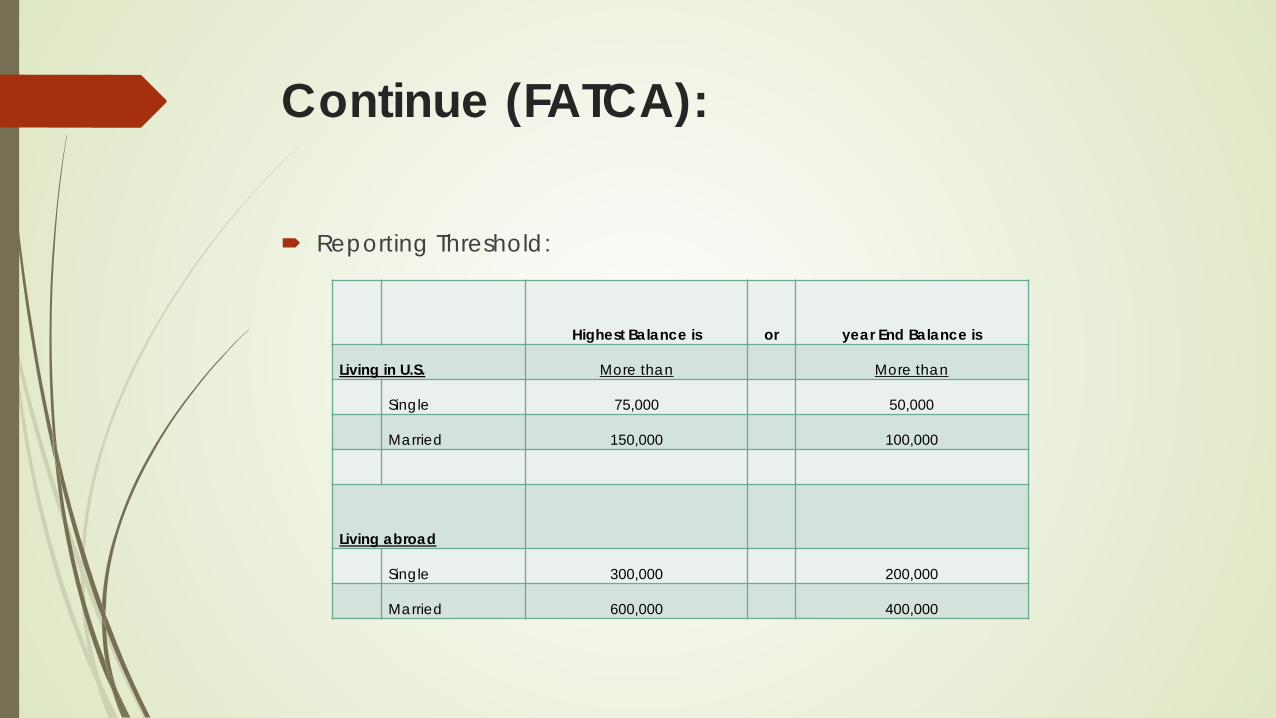

Reporting Threshold:

Highest Balance is or year End Balance is

Living in U.S. More than More than

Single 75,000 50,000

Married 150,000 100,000

Living abroad

Single 300,000 200,000

Married 600,000 400,000

Continue (FATCA):

Foreign Financial Account includes: Bank accounts, investments accounts, retirement or life insurance account with cash surrender value. Also includes loan to foreign person, interest in foreign corporation/partnership and other assets not held in an account.

Due Date: Income tax return due date including extension. Penalty: $10,000 (and a penalty up to $50,000 for continue failure

after IRS notification). Underpayment of tax resulting from non-disclosed foreign financial assets will be subject to additional understatement penalty of 40 percent.

Continue (FATCA):

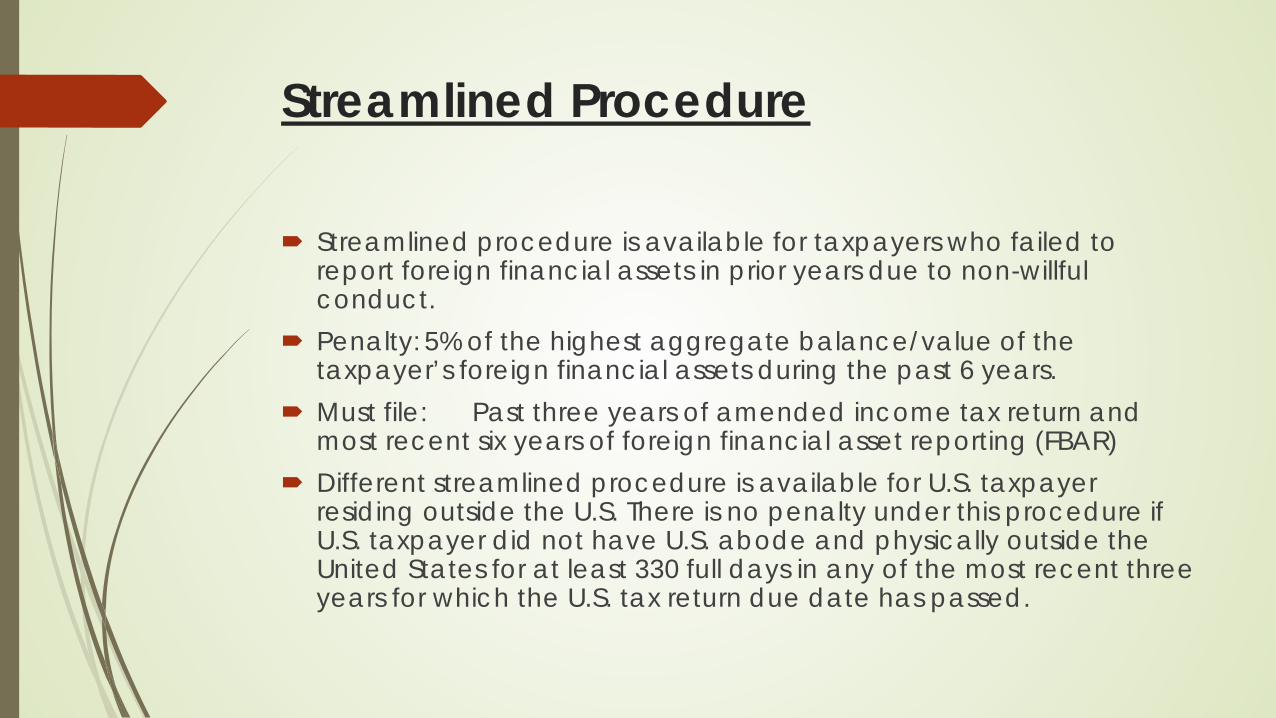

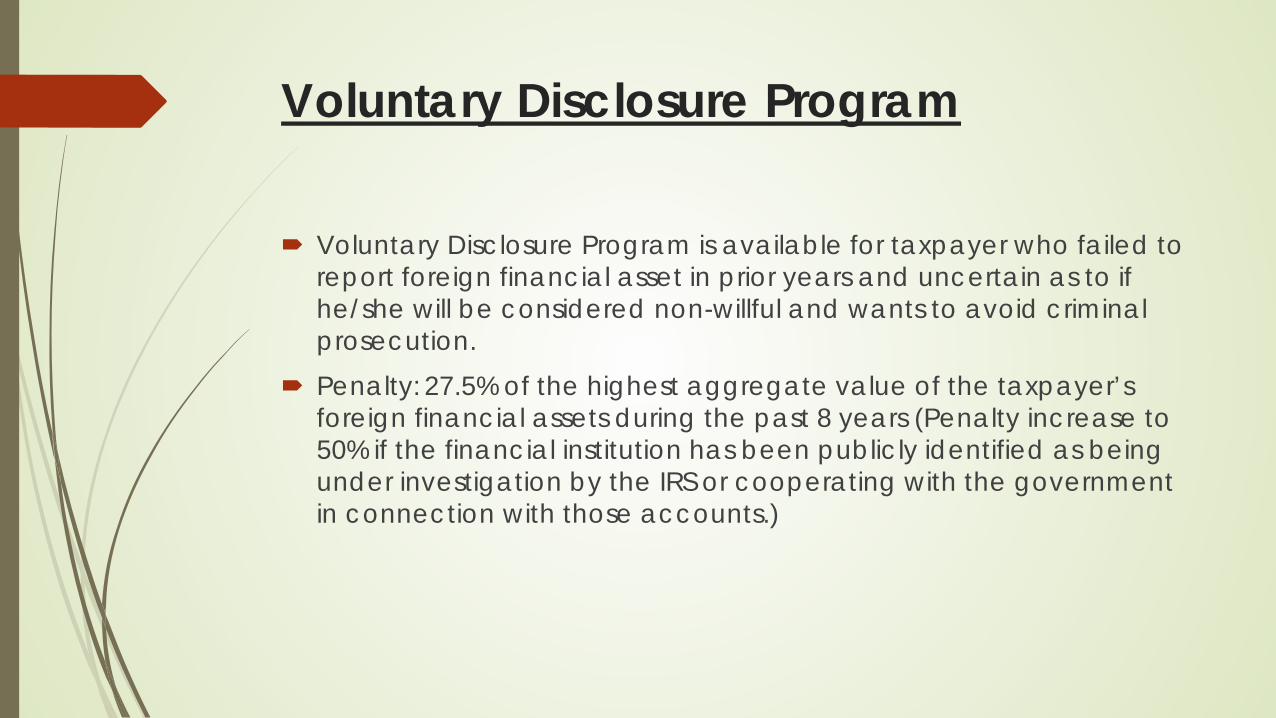

Compliance procedure There are two procedure currently available for those

who failed to report foreign financial assets in prior years. Streamlined Procedure Voluntary Disclosure Program

Streamlined Procedure

Streamlined procedure is available for taxpayers who failed to report foreign financial assets in prior years due to non-willful conduct.

Penalty: 5% of the highest aggregate balance/value of the taxpayer’s foreign financial assets during the past 6 years.

Must file: Past three years of amended income tax return and most recent six years of foreign financial asset reporting (FBAR)

Different streamlined procedure is available for U.S. taxpayer residing outside the U.S. There is no penalty under this procedure if U.S. taxpayer did not have U.S. abode and physically outside the United States for at least 330 full days in any of the most recent three years for which the U.S. tax return due date has passed.

Voluntary Disclosure Program

Voluntary Disclosure Program is available for taxpayer who failed to report foreign financial asset in prior years and uncertain as to if he/she will be considered non-willful and wants to avoid criminal prosecution.

Penalty: 27.5% of the highest aggregate value of the taxpayer’s foreign financial assets during the past 8 years (Penalty increase to 50% if the financial institution has been publicly identified as being under investigation by the IRS or cooperating with the government in connection with those accounts.)

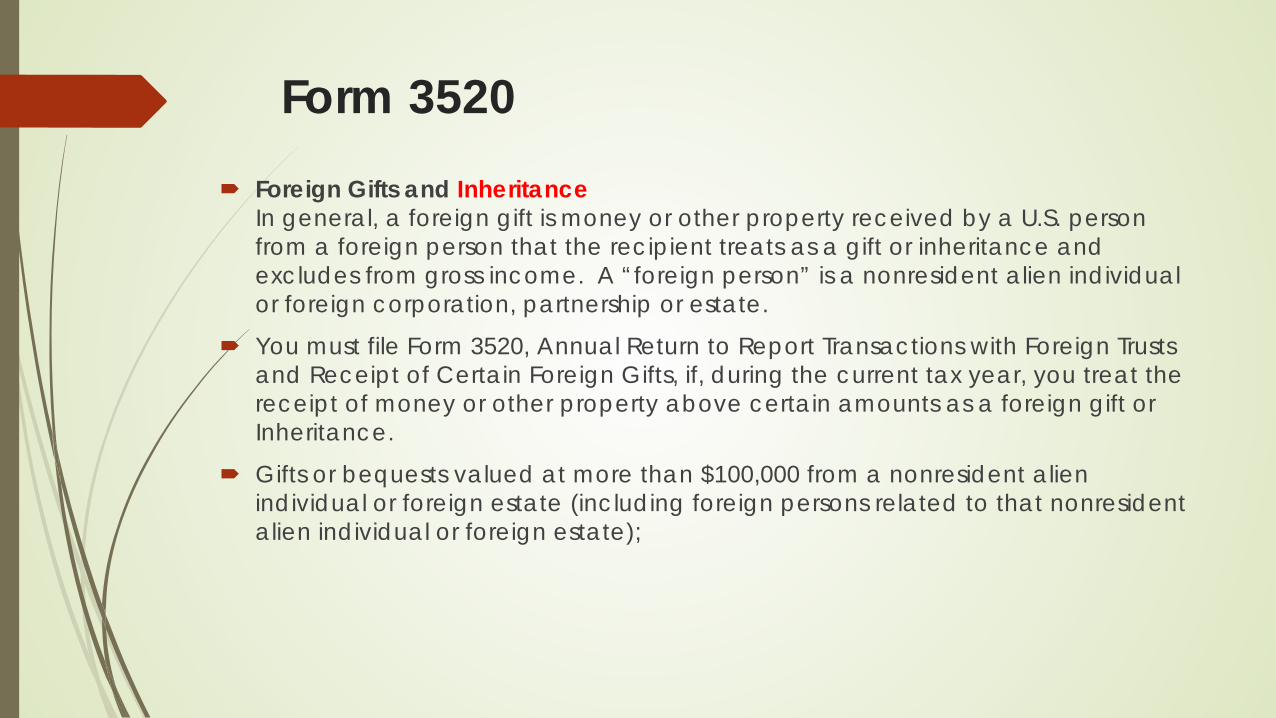

Form 3520 Foreign Gifts and Inheritance

In general, a foreign gift is money or other property received by a U.S. person from a foreign person that the recipient treats as a gift or inheritance and excludes from gross income. A “foreign person” is a nonresident alien individual or foreign corporation, partnership or estate.

You must file Form 3520, Annual Return to Report Transactions with Foreign Trusts and Receipt of Certain Foreign Gifts, if, during the current tax year, you treat the receipt of money or other property above certain amounts as a foreign gift or Inheritance.

Gifts or bequests valued at more than $100,000 from a nonresident alien individual or foreign estate (including foreign persons related to that nonresident alien individual or foreign estate);

Working With Japanese Buyers & SellersSeptember 13, 2016

Presentation Materials Available at:

www.LuxuryHm.com/for-agents

Q & A