Workers Of The World Untied - ETF To Use Own Indexes ... Workers Of The World Untied By Tyler Mordy...

68

Workers Of The World Untied Tyler Mordy Navigating The New Normal Jeremy Siegel, Vineer Bhansali, Dennis Gartman, Robert Whitelaw and more The Case For A Global Portfolio Approach Michael Branch Using VIX-Based Instruments Nick Cherney, William Lloyd and Geremy Kawaller Plus Blitzer on the survival of indexing, Clark on a different kind of volatility index and Arnuk and Saluzzi on phantom indexes

Transcript of Workers Of The World Untied - ETF To Use Own Indexes ... Workers Of The World Untied By Tyler Mordy...

Workers Of The World Untied

Tyler Mordy

Navigating The New Normal

Jeremy Siegel, Vineer Bhansali, Dennis Gartman, Robert Whitelaw and more

The Case For A Global Portfolio Approach

Michael Branch

Using VIX-Based Instruments

Nick Cherney, William Lloyd and Geremy Kawaller

Plus Blitzer on the survival of indexing, Clark on a different kind

of volatility index and Arnuk and Saluzzi on phantom indexes

www.journalofindexes.com

POSTMASTER: Send all address changes to Charter Financial Publishing Network, Inc., P.O. Box 7550, Shrewsbury, N.J. 07702. Reproduction, photocopying or incorporation into any information-retrieval system for external or internal use is prohibited unless permission is obtained in writing beforehand from the Journal of Indexes in each case for a specific article. The subscription fee entitles the subscriber to one copy only. Unauthorized copying is considered theft.

www.journalofindexes.com

f e a t u r e s

V o l . 1 4 N o . 6

1November / December 2011

44

32

14

d a t a

n e w s

Selected Major Indexes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

Returns Of Largest U.S. Index Mutual Funds . . . . . . . . . . 60

U.S. Market Overview In Style . . . . . . . . . . . . . . . . . . . . . . . 61

U.S. Industry Review . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

Exchange-Traded Funds Corner . . . . . . . . . . . . . . . . . . . . . 63

BlackRock To Use Own Indexes . . . . . . . . . . . . . . . . . . . . . 50MSCI Focuses On Enhanced Beta. . . . . . . . . . . . . . . . . . . . 50Six HOLDRS To Become Van Eck Sector ETFs . . . . . . . . 50Case-Shiller Indexes Up In Q2 . . . . . . . . . . . . . . . . . . . . . . . 50Indexing Developments. . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52Around The World Of ETFs. . . . . . . . . . . . . . . . . . . . . . . . . . 56Back To The Futures. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57 Know Your Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57From The Exchanges . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57On The Move . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

Workers Of The World UntiedBy Tyler Mordy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Examining some unsettling economic developments.

Navigating The New NormalFeaturing Jeremy Siegel, Vineer Bhansali, Dennis Gartman,

Robert Whitelaw, Bill Witherell and Jeremy Held . . . . . . . 14

Experts tell investors how to keep up with the times.

Indexing In A Time Of Market Turmoil By David Blitzer . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

How did indexing weather the financial meltdown?

The Case For Global Stock PortfoliosBy Michael Branch. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Investors should take a “big picture” approach.

Portfolio Applications For VIX-Based InstrumentsBy Nick Cherney, William Lloyd and Geremy Kawaller . . 32

Harnessing volatility to improve diversification.

Realized Volatility IndexesBy Andrew Clark. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

Looking beyond the VIX—a different kind of volatility index.

Phantom IndexesBy Joseph Saluzzi and Sal Arnuk . . . . . . . . . . . . . . . . . . . . . 44

Your index may not be measuring what you think.

Modern Portfolio TheoryBy Bruce Greig. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

Test your knowledge with an MPT-focused crossword puzzle.

Contributors

2 November / December 2011

Jose

ph

Sa

luz

zi

Ty

ler

Mo

rdy

Bru

ce

Gre

ig

An

dre

w C

lark

Nic

k C

he

rne

y

Mic

ha

el

Bra

nc

h

Da

vid

Bli

tze

rDavid Blitzer is managing director and chairman of the Standard & Poor’s Index Committee. He has overall responsibility for security selection for S&P’s indexes and index analysis and management. Blitzer previously served as chief economist for S&P and corporate economist at The McGraw-Hill Companies, S&P’s parent corporation. A graduate of Cornell University, he received his M.A. in economics from George Washington University and his Ph.D. in economics from Columbia University.

Michael Branch is a research analyst for asset management firm Aperio Group LLC. His research is focused on the areas of after-tax indexing, customized beta and global equities, and he has authored several research papers on topics of concern to institutional and high-net-worth audiences. Branch received his B.S. in finance from the University of Arizona. He holds the Chartered Financial Analyst designation and is a member of the CFA Society of San Francisco.

Nick Cherney is the chief investment officer, co-founder and member of the board of directors of VelocityShares. Previously, he had product development and management responsibilities for iPath ETNs at Barclays Capital. Prior to that, Cherney was a portfolio manager for iShares at Barclays Global Investors, where he managed over $25 billion of ETF assets. Cherney holds a B.A. with highest honors in economics from UC Berkeley and is a Chartered Financial Analyst.

Andrew Clark is chief index strategist for Thomson Reuters Indices. In this role, he is responsible for vetting index methodologies proposed by the firm’s partners. Clark is the chief “evangelist” for the Thomson Reuters index busi-ness, and has won several awards for his research. His work has appeared in several peer-reviewed journals, and more of his research will appear in the Journal of Index Investing and the Journal of Investing by the end of 2011.

Bruce Greig, CFA, CAIA, CMT, is the portfolio manager for Altin Holdings LLC. Altin Holdings is a commodity pool operator and registered invest-ment advisor specializing in managed futures and alternative invest-ments. Previously, he was co-founder and managing director of Symphony Investment Group LLC. Greig obtained his B.S. in mathematics and statis-tics from the University of Michigan and his MBA in finance from the Ross School of Business at the University of Michigan.

Tyler Mordy is the director of research for Hahn Investment Stewards, which delivers separate-account, ETF-only solutions. He is also a member of Hahn’s investment committee and writes the market commentary publi-cation ETFocus. Prior to joining Hahn Investment, Mordy was employed by Deutsche Asset Management in London. He earned his bachelor’s degree in both mathematics and English literature at the University of British Columbia; he is also a Chartered Financial Analyst.

Joseph Saluzzi is a partner, co-founder and co-head of equity trading of Themis Trading LLC, an independent agency brokerage firm that trades equities for institutional money managers and hedge funds. Prior to join-ing Themis, he headed an institutional equity sales and trading team at Instinet Corp. Saluzzi graduated from the University of North Carolina at Chapel Hill with an MBA in finance and received his bachelor’s degree in finance from New York University.

To download a copy of a prospectus, visit PowerShares.com/DBOpro

T H E P O W E R S H A R E S D B

OIL FUND

DBO

Copyright © 2011 by IndexUniverse LLC

and Charter Financial Publishing Network

Inc. All rights reserved.

Jim Wiandt

Editor

Heather Bell

Managing Editor

Matt Hougan

Senior Editor

Lisa Barr

Copy Editor

Laura Zavetz

Creative Director

Jodie Battaglia

Art Director

Jennifer Van Sickle

Graphics Manager

Andres Fonseca

Online Art Director

Aimee Melli

Production Manager

Editorial Board

Rolf Agather: Russell Investments

David Blitzer: Standard & Poor’s

Lisa Dallmer: NYSE Euronext

Henry Fernandez: MSCI

Deborah Fuhr

Gary Gastineau: ETF Consultants

Joanne Hill: ProShare and ProFund Advisors LLC

John Jacobs: The Nasdaq Stock Market

Mark Makepeace: FTSE

Kathleen Moriarty: Katten Muchin Rosenman

Don Phillips: Morningstar

John Prestbo: Dow Jones Indexes

James Ross: State Street Global Advisors

Gus Sauter: The Vanguard Group

Steven Schoenfeld: Global Index Strategies

Cliff Weber: NYSE Euronext

Review Board

Jan Altmann, Sanjay Arya, Jay Baker, William

Bernstein, Herb Blank, Srikant Dash, Fred

Delva, Gary Eisenreich, Richard Evans,

Gus Fleites, Bill Fouse, Christian Gast,

Thomas Jardine, Paul Kaplan, Joe Keenan,

Steve Kim, David Krein, Ananth Madhavan,

Brian Mattes, Daniel McCabe, Kris

Monaco, Matthew Moran, Ranga Nathan,

Jim Novakoff, Rick Redding, Anthony

Scamardella, Larry Swedroe, Jason Toussaint,

Mike Traynor, Jeff Troutner, Peter Vann,

Wayne Wagner, Peter Wall, Brad Zigler

4 November / December 2011

This information does not constitute an offer of services in jurisdictions where Standard & Poor’s does not have necessary licenses. Standard & Poor’s receives compensationThiss innforrmaatioon dooes noot cconnstitutte aan offfer of seerviicees in juurisdiictiions wwheree Stanndaardd & Pooorr’s ddoees not have nneccessary licensess. SStaandardd && PPoor’s receivees ccommpensationin connection with licensing its indices to third parties. It is not possible to invest directly in an index. Exposure to an asset class is available through investable instrumentsin coonnnecctioon with licensinng iits inddices to third paartiies. It is noot pposssibblee too innvest dirrectly in ann inndeex. Exxposure to ann assseet cclass is avvailable tthrrough investaablee innsttrummentsbased on an index. There is no assurance that investment products based on an index will accurately track index performance or provide positive investment returns. Standard &baaseed oon an inddexx. TTheere is no asssuuranncee thhatt investmmennt pprooduuctss baseed onn ann inndeex wwill acccuuraatelly tracck iinddex peerfoormmanncee or provvide ppospossitivve invvestmentt reeturnss. SStandardd &&Poor’s does not sponsor, endorse, sell, promote or manage any investment fund or other vehicle that is offered by third parties and that seeks to provide an investment returnPooor’s ddoees nott sponnsoor, endorsee, sselll, pprommoote or managee aanyy investmmennt ffunnd or othherr veehiclee thhat is offfered byy thy thhirdd parttiess and that seeekss too provvide aan invvesstment retuurnbased on the returns of any of our indices. For more information on any S&P Index and any further disclosures please go to www.standardandpoors.com. Copyright © 2010basedd oon tthee reeturns oof aanyy off ouur inddicees. Foor mmoore infformaatioon on anny S&&P Inddexx and anny ffurrtheer ddiscloosuures ppleasee ggo tto wwwww.sttandardaanddpooorrs.ccomm. Copyright © 2010Standard & Poor’s Financial Services LLC, a subsidiary of The McGraw-Hill Companies, Inc. All rights reserved. STANDARD & POOR’S and S&P are registered trademarksStaanddard && PPooor’ss Fiinaanccial Seervvicees LLC, a subbsidiaary of Thhe McGraww-HHill Commpaaniees, Innc. All rights resserrveed. STTANNDAARRD & POOORR’S and S&&P arre reggisttered traadeemarkksof Standard & Poor’s Financial Services LLC.o Sof SStandard && Poor’s Finnanncialal Services LLC

There’s nothing passive

about tactical precision.

Opportunities abound. With almost countless combinations

of sectors, industries and regions, your role is about seizing

those opportunities quickly. But where do you start?

Look to S&P Indices. With the vast number of ETFs that

track to and actively trade on our wide-ranging menu of

indices, you can make timely tactical moves.

• Act with speed to implement rotation strategies that move

between sectors such as materials or utilities.

• Consider fi ner-tuned, narrow industry positions in more

than a dozen specialized industries including biotech,

semiconductors, pharmaceuticals, or oil & gas services.

• Plan precise exposures that leverage macro and micro

trends in regions such as Latin America, Emerging Asia,

Europe, the BRIC countries and more.

Achieve more focus and agility with tactical solutions from

S&P Indices.

www.spindices.com/fi nancialadvisors

Project1 1/26/11 9:18 AM Page 1

Charter Financial Publishing Network Inc. also publishes: Financial Advisor magazine, Private Wealth magazine, Nick Murray Interactive and Exchange-Traded Funds Report.

Foster Wright

Publisher

�������������r�'BY��������������

Don Friedman

Director of Business Development

�������������r�'BY��������������

Fernando Rivera

Reprint Sales Director

�������������r�'BY��������������

Ivana Zivkovic

Subscriptions

�������������r�'BY��������������

Dan Benveniste

Executive Vice President, Analytics & Data

������������

Charter Financial

Publishing Network Inc.

����#SPBE�4USFFU �4VJUF����

4ISFXTCVSZ �/+������

�������������r�'BY�������������

Charlie Stroller, President/CEO/CFO

IndexUniverse LLC

����4BDSBNFOUP�4USFFU �4VJUF�����

4BO�'SBODJTDP �$"�������

�������*/%&9��r�'BY�������������

Jim Wiandt, President

6

For a free subscription to the Journal of Indexes, IndexUniverse.com or Financial Advisor magazine,

or a paid subscription to ETFR, please visit www.indexuniverse.com/subscriptions.

November / December 2011

The Journal of Indexes is the premier source for financial index research, news and data. Written by and for industry experts and

financial practioners, it is the book of record for the index industry.To order your FREE subscription, complete and fax this form

to 732.450.8877 or subscribe online at www.indexuniverse.com/subscriptions.

All questions must be answered to qualify for free subscription. Publisher reserves the right to reject unqualified applications.

� Q�Yes! Send me a free

subscription to Journal

of Indexes magazine

Name

Company

Address

City State ZIP

Phone Fax

Signature Date

Title

The following best describes my primary business activity (check one):

(1) Q�Plan Sponsor (2) Q�Financial Advisor

(3) Q�Investment Management (4) Q�Mutual Fund Management

(5) Q�Pension Fund Consulting (6) Q�Pension Fund Management

(7) Q�Brokerage (8) Q�Academic

(9) Q�Ordinary Investor (10) Q�Other:__________________

Do you personally sell, recommend or manage investments, work in the index

industry or advise clients on investment and/or asset management?

�������������������������������Q�Yes Q�No

If you advise clients as to their investments, how do you charge them?

���Q�Commission only Q�Fee only Q�Fee and commission

If you manage investments, what are your total assets under management?

(1) Q�Over $500 million (2) Q�$100 million - $500 million

(3) Q�$50 million - $99.9 million (4) Q�$25 million - $49.9 million

(5) Q�$10 million - $24.9 million (6) Q�Under $10 million

FREE SUBSCRIPTION OFFER!

����������������"���"

� � ,-' (-��&&$�(� ���-���, ���.".,-�������,,. ���2� �+�&�2,� �(%�������.-#)+$3 ���(��+ ".&�- ���2�-# ��$(�(�$�&�� +/$� ,��.-#)+$-2��(����' '� +�)!�-# ��)(�)(��-)�%��1�#�(" �� �+�&�2,���*$-�&�$,�-# �$(/ ,-' (-���(%$("��$/$,$)(�)!� �+�&�2,� �(%������0#$�#�.(� +-�% ,����, �.+$-$ ,��.,$( ,,�$(�-# �(�' �)!�$-,�0#)&&2�)0( ��,.�,$�$�+2� �+�&�2,���*$-�&��(�����(�������(��������' '� +��4���� �+�&�2,� �(%�������&&�+$"#-,�+ , +/ ��� �+�&�2,���*$-�&�$,���-+�� '�+%�)!� �+�&�2,� �(%�������&&�)-# +�-+�� '�+%,��, +/$� '�+%,�)+�+ "$,- + ��-+�� '�+%,��+ �-# �*+)* +-2���(��., ��0$-#�-# �* +'$,,$)(��)!�-# $+�+ ,* �-$/ �)0( +,�

INDICES CLEARLY FOCUSED

ON YOUR WORLD.

��������"��#����������������� ������������������������������������������ �������!�����!�������

���������"�� �����������"����"������������� ����������"�������������������+�0$("�)(�( �+&2���2 �+,��

)!� 1* +$ (� �$(�-# �$(� 1��.,$( ,,��0 �)!! +�2).���!.&&�,* �-+.'�)!�$(�$� ,��!+)'�� -��-)��&*#����&)("�0$-#��

�.,-)'$3�-$)(��(��$(()/�-$/ �,-+�- "$ ,�-)�' -��(2�$(/ ,-' (-�( ����)( 2�'�(�" +,��+).(��-# �0)+&��., ��

).+�51 ��$(�)' �$(�$� ,��(��+$,%��(�&2-$�,�-)�� (�#'�+%�-# �* +!)+'�(� �)!�-+$&&$)(,�)!��)&&�+,�)!�!.(�,���0#$�#��

$,�0#2�).+��)(��$(�$� ,��+ �-# �'),-�0$� &2�., ���2�����*+)/$� +,��0$-#�)/ +������$&&$)(�$(������ (�#'�+% ���

-)�-# '�"&)��&&2���)(( �-�2).+�0)+&��-)��� �+�&�2,���*$-�&��(� 1��(���& �+&2�!)�.,�)(�2).+�,.�� ,,���

�)+�$(� 1��(��+$,%�'�(�" ' (-�,)&.-$)(,��*& �, � '�$&�$(� 1���+��*��)'�

����������������� ���������������

8

Editor’s Note

Jim Wiandt

Editor

November / December 2011

A few years ago, investors around the globe found out that the choo-choo train ride they thought they were on was actually one of those amped-up roller coasters. You know, the kind that go through a lot of loops and dives and seem like they last

forever. Some people cry, some folks bargain with God and others throw up. The dismal state of the global economy, the sequential crises in various markets and

the dubious health of entitlements, pensions and retirement funds have all contrib-uted to the wild ride we’ve been experiencing. It appears that there’s no end in sight, and it looks like stomach-churning twists and turns are all that lie in our foreseeable future. So what’s an index investor to do? (Hint: The answer isn’t sewing your retire-ment money into the sofa cushions.)

First, Tyler Mordy pragmatically sums up the new (economic) world order in a thought-provoking piece that concludes with some practical suggestions for investors using passive vehicles. Fast on his heels is a group of experts—including Wharton’s Jeremy Siegel, Pimco’s Vineer Bhansali, Dennis Gartman of “The Gartman Letter,” and more—brimming with opinions on what you should be doing to navigate these murky waters. What’s probably the most surprising in this par-ticular roundtable is the unusual degree of consensus.

Then David Blitzer argues that what doesn’t kill indexing makes it stronger, offering examples of how the philosophy has demonstrated comparatively strong returns and some of the innovations that have flourished in the market turmoil.

Michael Branch of Aperio Group follows with an argument for taking a big-picture approach to international markets, in light of the globalization trend; he offers stats and examples to support his thesis that it results in greater efficiency and lower turnover.

Globalization isn’t the only trend that’s been growing over time—volatility had its big moment in the spotlight with the 2008 market meltdown, and it hasn’t conceded center stage since. An article from Nick Cherney, William Lloyd and Geremy Kawaller of VelocityShares discusses strategies investors can use to harness the VIX as a diversi-fication tool; Andrew Clark follows their lead with a discussion of the Thomson Reuters Realized Volatility Index and how it measures a different type of volatility than the VIX.

Joseph Saluzzi and Sal Arnuk of Themis Trading are up next, raising a very interest-ing point about the indexes we’re using today: Most of them rely on prices from com-ponent stocks’ primary exchanges, but that leaves out an awful lot of data. Can they really be considered accurate measures?

Bruce Greig of Altin Holdings LLC closes out the issue with a crossword puzzle built around a theory that has weathered the market gyrations fairly well. You’ll have fun with this one.

Wishing you solid footing in a rapidly evolving marketplace!

Our New Normal

Jim Wiandt

Editor

November / December 201110

By Tyler Mordy

Has capitalism come undone?

Workers Of The World Untied

www.journalofindexes.com 11November / December 2011

“In the long run, the workman may be as necessary to his master as his master is to him; but the necessity is not so immediate.” —Adam Smith, “The Wealth of Nations” (Book 1, Chapter 8)

In recent years, the most conspicuous feature of the financial landscape has been the growing divergence between U.S. labor and corporate profit trends.

While household incomes have languished, corporate earnings have soared—despite the most difficult eco-nomic cycle in the postwar period. These trends are having a significant impact on current and future equity market index returns.

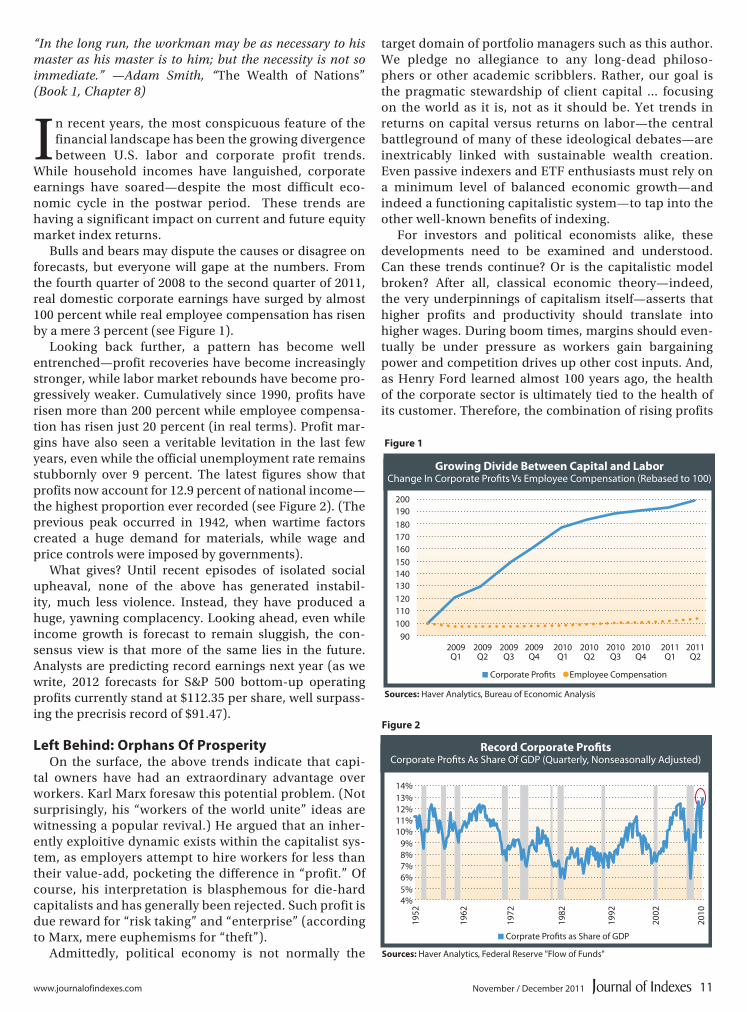

Bulls and bears may dispute the causes or disagree on forecasts, but everyone will gape at the numbers. From the fourth quarter of 2008 to the second quarter of 2011, real domestic corporate earnings have surged by almost 100 percent while real employee compensation has risen by a mere 3 percent (see Figure 1).

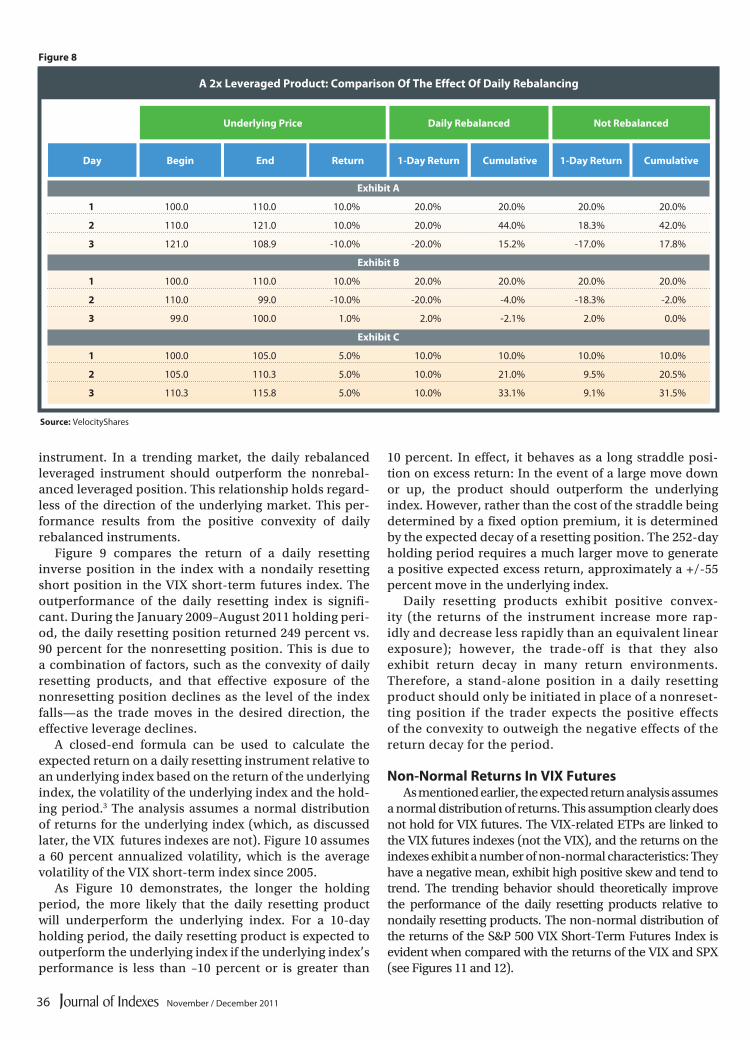

Looking back further, a pattern has become well entrenched—profit recoveries have become increasingly stronger, while labor market rebounds have become pro-gressively weaker. Cumulatively since 1990, profits have risen more than 200 percent while employee compensa-tion has risen just 20 percent (in real terms). Profit mar-gins have also seen a veritable levitation in the last few years, even while the official unemployment rate remains stubbornly over 9 percent. The latest figures show that profits now account for 12.9 percent of national income—the highest proportion ever recorded (see Figure 2). (The previous peak occurred in 1942, when wartime factors created a huge demand for materials, while wage and price controls were imposed by governments).

What gives? Until recent episodes of isolated social upheaval, none of the above has generated instabil-ity, much less violence. Instead, they have produced a huge, yawning complacency. Looking ahead, even while income growth is forecast to remain sluggish, the con-sensus view is that more of the same lies in the future. Analysts are predicting record earnings next year (as we write, 2012 forecasts for S&P 500 bottom-up operating profits currently stand at $112.35 per share, well surpass-ing the precrisis record of $91.47).

Left Behind: Orphans Of ProsperityOn the surface, the above trends indicate that capi-

tal owners have had an extraordinary advantage over workers. Karl Marx foresaw this potential problem. (Not surprisingly, his “workers of the world unite” ideas are witnessing a popular revival.) He argued that an inher-ently exploitive dynamic exists within the capitalist sys-tem, as employers attempt to hire workers for less than their value-add, pocketing the difference in “profit.” Of course, his interpretation is blasphemous for die-hard capitalists and has generally been rejected. Such profit is due reward for “risk taking” and “enterprise” (according to Marx, mere euphemisms for “theft”).

Admittedly, political economy is not normally the

target domain of portfolio managers such as this author. We pledge no allegiance to any long-dead philoso-phers or other academic scribblers. Rather, our goal is the pragmatic stewardship of client capital ... focusing on the world as it is, not as it should be. Yet trends in returns on capital versus returns on labor—the central battleground of many of these ideological debates—are inextricably linked with sustainable wealth creation. Even passive indexers and ETF enthusiasts must rely on a minimum level of balanced economic growth—and indeed a functioning capitalistic system—to tap into the other well-known benefits of indexing.

For investors and political economists alike, these developments need to be examined and understood. Can these trends continue? Or is the capitalistic model broken? After all, classical economic theory—indeed, the very underpinnings of capitalism itself—asserts that higher profits and productivity should translate into higher wages. During boom times, margins should even-tually be under pressure as workers gain bargaining power and competition drives up other cost inputs. And, as Henry Ford learned almost 100 years ago, the health of the corporate sector is ultimately tied to the health of its customer. Therefore, the combination of rising profits

2009Q1

2009Q2

2009Q3

2009Q4

2010Q1

2010Q2

2010Q3

2010Q4

2011Q1

2011Q2

200

190

180

170

160

150

140

130

120

110

100

90

� Corporate Profits Employee Compensation

Growing Divide Between Capital and LaborChange In Corporate Profits Vs Employee Compensation (Rebased to 100)

Sources: Haver Analytics, Bureau of Economic Analysis

Figure 1

Record Corporate Profits�������������������� ���������������������������������������������

Sources: +�/���������.-���*�������,����/���*��0����*�����

!$�

!#�

!"�

!!�

! �

)�

(�

'�

&�

%�

$�

!)%"

!)&"

!)'"

!)("

!))"

" "

" !

� ������������������� �����������

Figure 2

November / December 201112

and stagnant income growth (and thus weak aggregate demand) cannot possibly last forever.

Or can it? In a globalized era, a new investment class has emerged—the multinational corporation. Rising out of a more interconnected world, these companies transcend the restrictions of individual nation states, roving the globe for arbitrage and profit opportunities. They can seamlessly shift production from country to country, accessing better tax regimes and, importantly, cheaper labor. The same advantages are now also available to global portfolio man-agers, as client capital can be invested in profitable econo-mies or enterprises anywhere around the world.

A Crisis Of Capitalism?To be sure, predicting the demise of capitalism is noth-

ing new. Time magazine’s April 1980 cover story, titled “Is Capitalism Working?”, bemoaned the decline of free enter-prise and the “vitality and élan” of capitalists.1 That article printed immediately before profit margins made a secular trough and a generational stock market upswing began.

Also, on one point, let’s be clear. Capitalism, in its pure form, hardly exists today. If it did, governments would also allow market discipline to work on the downside. Clearly, that has not been the observable case recently. Witness banking bailouts, sovereign bond guarantees and numerous other government interventions. Clearly, the “socialization of losses” and “privatization of gains” is today’s status quo.

Still, looking beyond this asymmetric form of capitalism, perhaps the largest threat to the long-term health of the domestic economy remains the disparity between labor and capital trends. To understand forward risks, a look back at historical trends in profit margins is instructive.

Beyond cyclical influences, secular forces also have been at work. Two major margin troughs have occurred since the 1930s. The first occurred immediately after the Great Depression, where the combination of World War II military spending and the 1950s reconstruction boom restored profit margins from the difficult 1930s. For the next two decades, however, the environment was less hos-pitable, as rapid unionization and high inflation initiated a structural decline in margins to the end of the 1960s.

The second significant trough happened in the early 1980s. So-called Reaganomics—supply-side reforms aimed at reducing both government regulation and mar-ginal income taxes—swept across Western economies. This also led to the systematic dismantlement of unions, increasing labor mobility and competition. Meanwhile, free-market capitalism was taking hold in developing parts of the world, creating a boom in international trade, cross-border capital flows and, of course, global labor arbitrage. The net result was a marked improvement in labor productivity and, consequently, profit margins.

Why is the above important? Because these trends have contributed to an income distribution progres-sively skewed toward capital at the expense of labor in many Western countries. Statistical measures of income inequality (such as the Gini coefficient) have steadily drifted higher over the last few years. Until recently, households did not take notice. Aided and abetted by easy monetary policy, they relied on lower savings, asset bubbles and housing-financed debt growth to plug the gap between subdued increases in wage growth and con-tinuing increases in consumption.

Capitalism (as it has been sold in the West) is hardly supposed to work this way. Having a more egalitarian income distribution (i.e., a middle class) results in not only a more stable, equitable society but also generates greater prosperity over the long run. A prosperous middle class buys houses and cars, and sees its children, properly edu-cated, become leaders and entrepreneurs of tomorrow.

In a globalized world, the same trends that favor the multinational corporation also place workers in a weak negotiating position. It has become increasingly difficult for workers to overcome the pressures of mobile capital and regain a greater share of any prosperity. However, if a country cannot sell its products internally, which country ultimately wins? It should not come as a surprise that the most income-skewed nations including the United States are now facing weak domestic demand.

Shareholder-Driven Capitalism

Restrained wage growth has not been the only corporate cost-cutting measure supporting record margins. In fact, other structural trends, in place for some time now, have acted to bolster short-term profits while simultaneously undermining both labor growth and longer-term profits. Importantly, maximizing shareholder value has often been placed ahead of productive wealth accumulation. This is primarily an outgrowth of changing incentive structures since the early 1980s. Facing short-term quarterly earnings pressures, option-laden managers (whether consciously or not) favor measures that immediately boost share prices rather than securing long-term profit growth. For example, since the late 1990s, spending on capital equipment and software has significantly lagged earnings growth (see Figure 3). Over time, these actions deplete productive capital formation, reduce macroeconomic growth and ulti-mately contribute to a reduction in employment.

Does all this matter to investors? After all, many of

Capital Formation DecliningEquipment and Software Spending, % of GDP

(Quarterly, Seasonally Adjusted)

Source: Haver Analytics

14%

13%12%11%10%

9%8%

7%6%5%4%

19

47

19

57

19

67

19

77

19

87

19

97

20

07

20

10

� Corporate Profits as Share of GDP� Capital Equipment and Software as Share of GDP

Figure 3

www.journalofindexes.com 13November / December 2011

these trends in labor arbitrage and other short-term performance enhancers can persist for some time. And, much of the above may only be important over the very long run (as Keynes once said, “... the long run is a mis-leading guide to current affairs. In the long run we are all dead.”). Yet looking at the current economic cycle, many of these factors do indeed have a finite life, even for the indomitable multinational corporation.

In fact, profit margins will likely confront trouble in the period immediately ahead. Many factors that contributed to record margins, both on a cyclical and a structural basis, have either run their course or have simply been “one-off” profit boosters. Of course, subdued labor costs have been a key prop here. But other factors have been similarly important. For example, the Bernanke Fed has lowered interest rates to nearly zero. Correspondingly, corporate net interest payments have fallen dramatically since the onset of the financial crisis (see Figure 4). How likely is this to be repeated? Rates cannot fall much lower, certainly not to the extent that they already have.

There are many more notable examples, not least of which is fading government stimulus and a shift toward austerity measures. But the important point is that

further productivity gains will be more difficult in the period directly ahead without either employee hiring or renewed capital spending. In fact, a productivity down-turn may have already begun. Labor costs and tensions have been rising this year. Figures from the Bureau of Labor Statistics show nonfarm business productivity contracting in the first and second quarters of 2011 by 0.6 percent and 0.3 percent, respectively.

So far, our profit discussion has centered on “bot-tom line” factors. However, “top line” factors are equal-ly crucial. Most of recent earnings growth has come from government-sponsored growth rather than organic expansion in aggregate demand or consumer incomes. Ultimately, however, growth in top-line revenue depends on the financial health of its customers (whether they are domiciled domestically or internationally). In a postcred-it-driven world, consumer spending—certainly in most slow-growth Western regions—will rely more on income growth than rising debt burdens. Yet it’s highly unlikely there will be wage growth acceleration given the high level of unemployment and corresponding weakness of labor’s bargaining position. That makes the revenue out-look, which has already been anemic, less than rosy (see Figure 5). Margins and, importantly, earnings will have little protection during the next economic downturn.

Undoubtedly, however, corporations will remain focused on cost control and productivity gains. As part of that equation, financial engineering will remain key. Consider that companies have a number of options when utilizing their capital. They can reinvest in the underlying business, retire debt, buy back shares or pay out divi-dends. Why would corporate executives pursue the first two options when aggregate demand is weak and interest rates are at historic lows (and pledged to remain there until at least mid-2013)?

A more rational approach, even if not beneficial to labor, attempts to boost stock prices by reducing share count or increasing dividends. That has been the observ-able case, as corporations have been actively increasing dividends or share buybacks. For the first half of 2011, the net domestic common stock dividend increase of $30.2 billion already surpasses all of 2010, representing an 11.1 percent increase (4.1 percent for Q2 and 6.7 percent Q1). From a capital allocation standpoint, these trends are completely logical and likely to continue for some time.

Investment OutlookMany are predicting that high corporate cash positions and

healthy balance sheets will lead to stronger domestic employ-ment growth and higher incomes. However, a more likely scenario is that corporations will emphasize overseas expan-sion instead of domestic hiring and investment. This would be consistent with recent trends. In the past five years, U.S. direct investment overseas has been 20 percent higher than domestic nonresidential investment. During the 1960s and 1970s, that ratio averaged 6 percent before climbing to a 13.5 percent average between the mid-1990s and mid-2000s.2

2009Q1

2009Q2

2009Q3

2009Q4

2010Q1

2010Q2

2010Q3

2010Q4

2011Q1

2011Q2

0$100

-$100-$200-$300-$400

$200$300$400$500$600$700$800$900$1,00

� Corporate Profits GDP Net Interest Payments

Enormous Interest Rate Relief

Change In Corporate Net Interest Payments (With IVA and CCA)

Sources: Haver Analytics, Bureau of Economic Analysis

Bill

ion

s

Business Cycle Will Not Be Repealed����������������������������������� ���

Sources: &�������*��)������

� �

��

�

!�

#�

$�

���

� "�

� ����"�����

�"���

���

��

�%%!

�%%#

�%%$

���

��

��!

��#

��$

���

���

"�

�"�

▲▲▲▲▲▲▲▲▲▲

� ���������������"���������(&���

� ����"����������� �����'&����

Figure 4

Figure 5

continued on page 48

November / Dece,mber 201114

A roundtable

Navigating The New Normal

www.journalofindexes.com November / December 2011 15

We’ve been through an unprecedented few years, such

that it seems almost as if the markets and the accepted

rules that governed them have evolved at a fundamental

level. Journal of Indexes sat down with a group of experts

to discuss the changed market environment and what it

means for investors.

Jeremy Siegel, Senior Investment

Strategy Advisor, WisdomTree;

Russell E. Palmer Professor of Finance,

Wharton, University of Pennsylvania

JOI: Has the nature of investing changed

in the last few years?

Siegel: What’s difficult is that what people are doing

and what people should be doing, in my opinion, is not

the same thing. The last 10 years have not been good for

stocks—we all know that. And we know there are quite

a few economic problems facing this country and the

world. But it’s my feeling that investors are overreacting

to all this negative sentiment in the market and are taking

too cautious a position with regard to investments, and

are ignoring the long-term data.

This is something that has occurred throughout history,

where stocks don’t do well and people are down on stocks.

Then when stocks do perform well, they get up—in fact, too

far up—on stocks. Right now, we see a very risk-averse invest-

ment strategy—a fearful investment strategy—where people

are willing to lock in yields on bonds that, to me, are extremely

poor compared to any historical calculation of stock returns.

JOI: Given a decade of negative returns and massive vol-

atility, does traditional index investing still make sense?

Siegel: There are several types of index investment. There

is the original capitalization-weighted indexing. There

are newer forms of indexing, called fundamental index-

ing, which tilt portfolios towards value stocks, towards

high-dividend stocks and high-earning stocks. My feeling

is the next 10 years will be good for straight capitalization-

weighted indexing, but will be even better for those who

invest with an index tilted towards high-dividend and high-

earning stocks. In fact, what is interesting is that had inves-

tors in 2000 invested in value stocks, the returns through

this last decade would have been much, much better. One

of the major reasons for the very poor performance of the

market over the last 10 years was the bust in technology

stocks from the very overvalued position that they achieved

when we reached the turn of the century.

JOI: What have been the biggest paradigm shifts in the

global economy in the last five years?

Siegel: I think the greatest paradigm shift has definitely

been the rise of the emerging markets—India, China,

Brazil. Their economic growth has been excellent. They

have come through the financial crisis in a Great Recession

much better than the developed world. And I think that any

investment policy has to be a global policy with a signifi-

cant weight given to emerging markets.

JOI: Is program trading driving short-term stock move-

ments? Are ETFs to blame?

Siegel: One has to realize that in bear markets in reces-

sions, stock volatility has always been higher. We are in

unusual economic times, clearly, with debt building up

rapidly in the developed world, the downgrading of U.S.

Treasury bonds and a very weak recovery in the United

States, Europe and Japan. Whenever it is unusual times,

that brings about volatility. But we had extreme volatility in

the 1970s, high inflation and severe recessions. The great-

est volatility was in the 1930s, and we’re nowhere near that,

even today. That was the Great Depression.

I do not believe that program trading is responsible

for that. I don’t believe ETFs are responsible for that. The

main difference as time goes on in the markets is that

the speed of information travels faster and faster, and

rumors travel faster and faster, and your ability to get a

trade in and out is faster than ever—and at the lowest

cost. So you will see a lot of short-term volatility.

I don’t think investors should be scared off by that,

because if they’re going in for long-term value, they can

sometimes pick up some good values when the short-

term volatility drives prices downward. I would advocate

that investors use those opportunities to accumulate

equities and actually thank program traders for giving

them bargains in the market.

JOI: When rates finally start to rise, will fixed-income

index investors suffer? Are they prepared for that?

Siegel: It will happen by necessity, because I believe that

the expectations of interest rate increases that are built

into bonds are too low. I myself do not believe that the

Fed absolutely will be able to keep interest rates as low as

they claim they intend to over the next two years, because

I believe that we will resume economic growth in the next

six to 12 months, and that would force the Fed to raise

rates. If they do raise it before the summer of 2013, you

can be sure that the bondholders will suffer some severe

capital losses, and I do not believe that most investors in

bond funds are recognizing those real risks.

JOI: Are investors in danger of overweighting emerging markets?

Siegel: I think most investors are still underweight in

international stocks. International stocks in developed

and emerging markets are approximately 60 percent

of the value of total equities outstanding, and very few

investors have that much in foreign stocks. An aggressive

position in emerging markets would be an allocation of

one-third of your total equities, and that would be diversi-

fied across all emerging markets. Anything above a third

is certainly taking on extra risk. It may be rewarded, but it

is extra risk. Also, it’s dangerous to put all your eggs in one

basket. Clearly, any one country can go south and disap-

point. That’s why diversification is the key.

But I would overweight emerging markets in the portfolio

compared to their market value weight, which is probably

around 10 or 15 percent. Up to a third, although aggressive, I

would say, is not uncalled for in the long run.

JOI: At what price is gold too expensive?Siegel: I believe that five years from now, investors in gold will be disappointed in their returns compared to stocks. It doesn’t mean it might not go up in the short run—it might go up to $2,500 or $3,000. In the short run, there is no way to predict. But in terms of long-run value, I think that as our world economy improves, fewer and fewer investors will be fleeing to gold as a safe haven, and that will cut its return.

JOI: What key wisdom would you offer investors faced with extreme volatility and fear in the market? Siegel: Again, buy good dividend-paying stocks with good yields, companies that have been around for a while and have earnings that cover their dividends quite adequately. Diversify on a worldwide basis. If you pick those with high earnings and high dividends and diversify them, I think you’re going to get extraordinary values that are going to please you very much with their returns over the next five to 10 years.

Vineer Bhansali, Managing Director and Portfolio Manager, Pimco

JOI: Has the nature of investing changed in the last few years?Bhansali: Market realities have altered.

Investors are now faced with greater volatility, intercon-nectivity and unthinkables becoming possible. Who could have envisioned S&P downgrading the AAA rating of the U.S., or that the institutional integrity of the eurozone would be threatened as policymakers dithered?

The changing global paradigm influences investment positioning, asset allocations, return expectations and risk management.

JOI: Given a decade of negative returns and massive vol-atility, does traditional index investing still make sense?Bhansali: In fixed income in particular, many indexes are structured to represent markets rather than investable strategies. In addition, the performance characteristics of fixed income make negative events, such as defaults, much harder to overcome. As a result, and given increased vola-tility, indexation in fixed income should be approached very carefully, particularly in credit-sensitive sectors.

For investors that value index strategies, we suggest that they seek strategies based on indexes that are thoughtfully constructed for investment purposes, that are optimized based on factor exposures and recognition of default risk, and that use trading strategies based on preserving value. In particular, indexes that are based on forward-looking dynamics, rather than backward-looking market data, may be of particular value in this environment.

JOI: What have been the biggest paradigm shifts in the global economy in the last five years?Bhansali: The importance of structural issues vs. cyclical ones is the ultimate paradigm shift, and, unfortunately, policymakers have been slow to recognize this.

The cyclical rebound many expected and hoped for has

not occurred, and we have long argued it would not occur, as the U.S., U.K. and other finance-dependent major econ-omies come off a “great age” of leverage, debt and entitle-ment. The challenges facing the global economy, including head winds to growth in developed nations and potential overheating in certain emerging markets, are compounded by policymakers’ disagreements over not just how to address them, but the analysis and underlying causes.

Despite the structural impediments to growth, policy-makers in the U.S. and Europe have yet to deploy structural solutions, preferring cyclical instruments (such as the Fed’s quantitative easing) that haven’t proven effective. The politi-cal system must enable that shift to a structural approach.

President Obama’s jobs proposal and related speech on Sept. 8, for example, at long last recognized the severity of America’s unemployment crisis and the need for a com-prehensive policy response.

JOI: Is program trading driving short-term stock move-ments? Are ETFs to blame?Bhansali: High-frequency [HFT] and algorithm-driven trading was estimated to account for about one-third of all U.S. equity trading volume in 2006. It has grown now closer to 75 percent. It is hard to reasonably argue that HFT does not have some effect on intraday price movements. The real question, however, is whether the overall change in equity market structure has increasingly driven short-term stock movements. The elimination of the floor specialists, the increased number of market makers and the growth of electronic trading have all expanded the number of par-ticipants showing two-sided markets at any given time. But the depth of those markets has been shown to be relatively shallow, particularly in times of market stress.

While ETFs are certainly used with increasing frequency to access broad market sectors on the long and short sides, and to manage risks—particularly at times of greater mar-ket volatility—ETFs have not been the drivers of this vola-tility but have certainly been impacted by it. For example, several detailed studies of the “flash crash” point to various potential causes of this event, but most concluded that the structure of the equity market as a whole was the dominant driver, not ETFs. ETFs represent about 25 percent of all equity trading volume, on average, rising to as much as 35 to 40 percent during strong market sell-offs. So while many equity ETFs were impacted by the flash crash, as they rep-resented a significant portion of the trading volume on that day, they were not the unique cause of it.

JOI: When rates finally start to rise, will fixed-income index investors suffer? If so, are they prepared?Bhansali: Investors are navigating a multispeed world, with the potential for their portfolios to be affected by com-plex risks and cross currents, including interest rate risk. The Fed’s pledge to maintain the federal funds rate near zero through mid-2013, coupled with signs of economic slowing in the U.S. and abroad, suggest interest rate risk is likely to be modest in the near term. Over a longer time frame, perhaps three to five years, we expect gradually ris-

November / December 201116

ing inflation. However, we also see heightened volatility as characteristic of the New Normal, with the potential for surprises in inflation and interest rates. Investors may want to actively manage duration exposure, lowering duration if they anticipate substantial inflation and raising—or simply maintaining—duration if inflation is less of a concern.

JOI: What impact will the recent spike in volatility have on investor allocations? Bhansali: Investors may reconsider their approach to risk management across all assets. They arguably need to eval-uate the full spectrum of global developments—economic, financial, institutional, legal, demographic, regulatory and geopolitical—all in a risk-factor framework.

We also believe investors should consider tail risk hedg-ing, since policy mistakes and market accidents are vir-tually inevitable in this New Normal, where traditional market linkages are in flux, and both market and policy infrastructure are increasingly stressed.

JOI: Are investors in danger of overweighting emerging markets?Bhansali: Generally speaking, no. Emerging markets have become centers of global growth, with tail winds pushing these nations up the development curve, and slowly narrow-ing the wealth and production gap with developed nations. We believe global investors remain significantly underweight emerging market assets in relation to both their current and future share of the world economy, as well as in relation to the trends in their relative credit fundamentals. As markets reorient to a New Normal view of the world, we anticipate this under-allocation to emerging markets will decrease, providing multiyear support for the asset class.

To be sure, emerging nations now are confronting chal-lenges from de-leveraging and economic sluggishness in the developed world. Emerging markets are also faced with potential consequences of their own success, includ-ing rapidly appreciating currencies and inflation. Whether emerging markets can continue to manage success is becoming a country-by-country question. For example, we have been anticipating a “soft landing” for China, but the risks of a “hard landing” are becoming greater, in part due to China’s exposure to and reliance on trade with the developed markets, but also due to tighter monetary measures from Chinese authorities intended to curb credit expansion and real estate inflation.

Dennis Gartman, Publisher, The Gartman Letter

JOI: Has the nature of investing changed in the last few years?Gartman: The nature of investing changes

all the time. It’s never the same. But if there’s one major change that I’ve noticed amongst the public, it’s that buy-and-hold has probably died a much-needed and impera-tive death. The idea of buying something and holding it forever is probably not going to survive much longer.

JOI: Given a decade of negative returns and massive vol-atility, does traditional index investing still make sense?Gartman: Oh sure, absolutely. Why would you not? It’s by far the easiest way for the public to get diversification, and it’s clearly the most cost efficient, because the cost of bro-kerage is so much less for the indices than it is for mutual funds. Is the idea of holding an index forever going to stay with us? No; that’s died a much-needed death, as I said.

JOI: What have been the biggest paradigm shifts in the global economy in the last five years?Gartman: The understanding that China is now a major force in the world market, that soon it will surpass the United States as far as gross domestic product is concerned. It will be decades before China comes even close to our GDP in per capita terms, but because of its sheer size and population, it’s going to surpass the United States as far as gross domestic product is concerned. China’s citizenry are moving up the income scale rather rapidly, and in the not-too-distant future, the world will understand that China’s going to be a net importer, not a net exporter. That, I think, is the next tectonic and tidal shift in the understanding of how the global economy is changing.

JOI: Is program trading driving short-term stock move-ments? Are ETFs to blame?Gartman: No, ETFs are not to blame. No, I am not a believer that program trading is discouraging or distorting invest-ment. And in fact, I’m of the opinion that program trading and high-frequency trading do, in fact, create liquidity. They don’t inhibit liquidity—they create liquidity. I’m not one of the people who fear either program trading or high-frequen-cy trading at all. In fact, I would encourage them.

JOI: When rates finally start to rise, will fixed-income investors suffer? Are they prepared for that?Gartman: When rates rise, fixed-income investors will suffer. By definition, that’s the math of the situation. The question is, when will rates rise? And I suspect that they will rise far more distant into the future than almost any-body wants to anticipate now. Some of the saddest people I can ever remember are my friends who bet on rising interest rates in Japan 15 years ago, and or any time since then. And they’re still waiting for rates to rise. The sums of money they have lost trying to be short the Japanese bond market is mind-numbing.

JOI: What impact do you think the recent spike in volatil-ity will have on investor allocations? Gartman: I think it will absolutely have an effect upon investor allocations. The public does not like volatility. The public would much prefer stability. And in fact, most pro-fessionals would much prefer stability rather than volatil-ity. I’m a pro—I’ve been at this 35 years—and I much prefer stable circumstances over volatile circumstances. I think that volatility begets the propensity not to be involved in investment: It makes people hunker down and go to the sidelines, and that’s not a good thing.

www.journalofindexes.com November / December 2011 17

JOI: Are investors in danger of overweighting emerging markets?Gartman: Investors are in danger of doing everything wrong at the wrong time all the time. So are they in danger of over-investing in emerging markets? Probably. Should they be investing in emerging markets? Absolutely. When will I know that they’re over-invested? When prices start to tumble. And so, I would tell them a reasonable portion would be 5 or 10 percent. If you’re a reasonably adept investor, 5 to 10 percent of what you invest should prob-ably be within an emerging market exposure. Beyond 30 percent, you’re probably too exposed.

JOI: At what price is gold too expensive?Gartman: Today’s [Aug. 23, 2011] high. I think today’s high may well be the high for gold for a while. It traded at $1,910 there one time this morning. And the bullish consensus from Market Vane was 95 percent bullish, and I saw some-thing really interesting: GLD, the gold ETF, had a higher capitalization as of Aug. 19 than did SPY, which is the most actively traded ETF. It’s the ETF for the S&P itself. How can gold have a higher capitalization than stocks generally? That’s what happens at the end of manias.

JOI: What key wisdom would you offer investors faced with extreme volatility and fear in the market?Gartman: Get smaller. That’s what every pro tells himself when markets get volatile and confusion reigns—and the great pros follow their own advice. Get smaller, trade smaller, invest smaller and wait until the smoke clears. It will eventually clear. The volatility that we had two weeks ago when we were up 400, down 400, up 400, down 400, as Herb Stein said, “That which cannot continue, won’t.” That couldn’t continue. It won’t.

Trade smaller amounts, invest smaller amounts of money. And trade bigger and better names than you did previously.

Robert Whitelaw, Chief Investment Strategist, IndexIQ; Edward C. Johnson 3D Professor of Entrepreneurial Finance, Stern School of Business, NYU

JOI: Has the nature of investing changed in the last few years?Whitelaw: I don’t think the fundamental principles of investing have changed, but what I think is that inves-tors may have learned some things from the crisis and, of course, the aftermath, which we’re going through right now. As a result, they’ve changed the way that they invest. There are three things that people have learned. One is the reason that risky assets tend to pay higher returns on average—it’s because they’re really risky. And what risk means is that these assets won’t always out-perform even over relatively long periods. I think we’ve gained an appreciation for risk.

I think we’ve also learned that diversification is not just picking a few bonds and adding them to your U.S.-centric stock portfolio. There’s now—certainly I hope—more inter-

est and a greater awareness of non-U.S. assets and alterna-tive asset classes, like emerging markets, commodities, etc.

Finally, I think one thing that people have talked about for a long time but maybe didn’t take as seriously as they should is the notion of liquidity and transparency. We learned from the crisis that liquidity and transparency are really important, and investors are now asking, “Do I understand what I’m holding?” You want to know what’s in your portfolio, and you want to know that you can sell it if the need arises.

JOI: Given a decade of negative returns and massive vol-atility, does traditional index investing still make sense?Whitelaw: I strongly believe that indexing makes sense in terms of passive vs. active management. I really don’t think the past decade has challenged the fundamental idea that indexing provides inexpensive and broad exposure to a market, either the U.S. market or another asset class. And even though the indices have performed badly—horribly you might say in many cases—it’s also the case that in many situations, active managers have still underper-formed because of the fees that they charged and the trans-action costs that they incurred.

However, if you believe “index investing” means invest-ing solely in an S&P 500 index fund, then that, I think, may not make sense going forward. But if you think of indexing in a broader context, considering alternative assets and alternative markets that provide better diversification, then I definitely think that index investing makes sense.

JOI: What have been the biggest paradigm shifts in the global economy in the last five years?Whitelaw: What has the global economy learned? That risk and risk management matter, both from an individual investor perspective and from an institutional perspective.

What else? For better or worse, I think capital markets are truly global. It hasn’t been something that happened just over the past five years; it’s been a gradual process that has come in fits and starts for quite a while now. But what we’ve seen is that shocks can be transmitted around the world. It can be through capital flows: peo-ple, investors, hedge funds pulling money out or putting money into various economies—and also multinational financial institutions. Shocks in the banking sector in one country affect other countries.

There’s a good side and a bad side to that, I think. The bright side is that global capital markets really open up new investment opportunities for investors. The bad side is, as a result, that these markets don’t offer quite the same diver-sification benefits that they used to, because of these strong linkages between various international markets.

One other thing is the rise of ETFs, at least in the U.S. I’ve seen some estimates that say 40 percent of daily trading on the New York Stock Exchange is actually ETF volume. There’s no doubt this kind of shift is going to challenge the traditional asset management business—obviously money invested in ETFs is money that isn’t invested elsewhere. But I think it also offers new opportunities for investors

November / December 201118

because of the huge expansion of the ETF market and the accompanying ability to get, perhaps, better diversification and better risk management in your portfolio.

JOI: When rates finally start to rise, will fixed-income index investors suffer? Are they prepared for that?Whitelaw: Ten-year Treasury yields are at or near record lows, with short-term yields close to zero. Is there anywhere to go but up? No, I don’t think so. But the thing to keep in mind is that it’s not clear what the time frame associated with this rise in rates will be. It’s very difficult to guess. And in fact, without naming any names, there are some people who’ve been predicting it for a while now—and it clearly hasn’t happened. I don’t know what the time frame is for this sort of eventual rise, but when it happens, when rates go up, prices go down. There’s no way around that.

My guess is that many retail investors may well be unprepared for a rising rate environment. I hope they do, but I don’t think they fully understand the interest rate risk of long maturity bonds, how much the prices can move on these securities when interest rates move. That said, there are actually some interesting new assets out there that do a nice job of providing some fixed-income exposure without that kind of duration risk, like the new bank-loan ETF. That may be a way for investors to get fixed-income exposure without this sort of long-term interest rate risk that I suspect they’re taking and that will come back to bite them when rates eventually rise, which I think they will.

JOI: What impact will the recent spike in volatility have on investor allocations?Whitelaw: Have people been whipsawed just once too often to stomach any more of this exposure to U.S. equity mar-kets? I may be the exception here, but I don’t think so. I’m an optimist. I think investors are smarter than that. I think you’re going to see investors looking maybe more broadly—commodities, emerging markets, alternative asset classes. But I really don’t see these major allocation shifts.

Traditionally, which is perhaps a little surprising, retail investors have actually stuck to it better than institutions. Maybe not individual by individual, but as a group their persistence has been good. I don’t see this recent spell of volatility as having a dramatic impact. I don’t think we’re going to see a dramatic bailout from the markets. I certainly hope not.

JOI: Are investors in danger of overweighting emerging markets?Whitelaw: Unfortunately, I think that’s a real possibility. I’m not sure we’re there yet. Emerging markets have been getting a lot of press, and investors are notorious for liking the latest hot thing. There are a lot of trend chasers out there. It wouldn’t surprise me to see an overreaction in terms of portfolio weights, if you will. But in the long run, emerging markets are where the growth is. I think it’s just a fact both in terms of economic growth and in terms of the growth in financial markets.

JOI: At what price is gold too expensive?Whitelaw: It depends on whether you’re buying it or sell-ing it, I guess. Market timing is notoriously difficult, and that applies to commodities as well as to stock markets. At least in stock markets we have some notion of fundamen-tal value. I can look at these valuation ratios, price to cash flow, price to earnings, whatever. But in the case of gold markets, this is not really about fundamental valuation. Are investors going to continue to flock to gold if and perhaps when things get worse in the global economy? It’s certainly possible, and if they do, then gold prices will still go up.

That said, I’m not sure I’d be buying gold at $1,800 an ounce.

Bill Witherell, Portfolio Manager and Chief Global Economist, Cumberland Advisors

JOI: Has the nature of investing changed in the last few years?

Witherell: I think it has. I think more individuals are invest-ing by themselves. It’s a lot easier for an individual to invest these days, particularly using ETFs, and being able to do it over the Internet. That is a major change. It is a dramatic change for some markets, like commodities markets and also currency markets, where individual investors really were not able to—unless they were quite sophisticated—get in these markets in the past.

And then generally, the high-speed trading that profes-sionals do, I think, has changed the nature of the markets, caused them to be more volatile.

JOI: Given a decade of negative returns and massive vol-atility, does traditional index investing still make sense?Witherell: For some people, it’s probably the best they can do—if they’re investing on their own—rather than to try to time the market when they don’t have the time or background to really study the market. For most individual investors, it would be helpful if they had a financial advi-sor. I think indexes will always be an important investment vehicle. In my firm, because we invest on the equity side solely in ETFs, we are, in effect, saying we’re really com-mitted to investing in indexes. But we actively manage the portfolios of those indexes. We don’t just buy and hold.

JOI: What have been the biggest paradigm shifts in the global economy in the last five years?Witherell: The biggest in the global economy, I think, has been the increased importance of emerging markets—in particular, China, but the others as well. In terms of eco-nomic growth, they’re going to account for, this year and next year, something like 80 percent of the total growth in the global economy. And they are now bigger players in terms of international economic policy as well. They have a seat at the table. China is the largest holder of reserves. That’s a very important change. And then we had a huge financial crisis, which we’re still recovering from, and that has affected investment around the world.

www.journalofindexes.com November / December 2011 19

JOI: When rates finally start to rise, will fixed-income investors suffer? Are they prepared for that?Witherell: By definition, when interest rates rise, fixed-income investors will suffer capital losses because when rates go up, the prices of bonds go down. So there will be capital losses unless the investments are hedged. That’s a concern that must be affecting bond investment because I don’t really expect our rates to go much lower; there’s not much room for it. However, I also do not expect rates to go up until 2013. I think we’re in for a period of prolonged, very low interest rates, both short term and long term. But when rates eventually go up, that will have a negative effect on fixed-income investors (except for bonds held to maturity).

JOI: What impact will the recent spike in volatility have on investor allocations?Witherell: We don’t really know how it will affect allocations. It adds to the risk avoidance that is affecting many investors right now. There’s a lot of cash on the sidelines and when the market’s this volatile, they’re not eager to get back in.

JOI: Are investors in danger of overweighting emerging markets?Witherell: They were in danger last year of doing it. In the first three quarters of this year, the emerging markets have underperformed the global market. And people who were overinvested in emerging markets got hurt by that. But then because emerging markets equity markets haven’t done that well, there’s been a lot of withdrawal—reduced emerging positions on the part of investors. Right now, I wouldn’t say that they face a danger.

Jeremy Held, Director of Research, ALPS Advisors

JOI: Has the nature of investing changed in the last few years?Held: It definitely has. For a long time,

people have realized that how they invest, in terms of which asset class, is a lot more important than whether or not they choose active or passive management inside a certain asset class. I think what’s really changed is that ETFs have actu-ally allowed people to implement in practice what they’ve known about in theory. I think that’s probably one of the big-gest ways that investing has changed within the last decade.

JOI: Given a decade of negative returns and asset volatil-ity, does traditional index investing still make sense?Held: Traditional index investing still does make sense. There are some negative returns in the asset classes that people are most familiar with, particularly U.S. large-cap equities, but if you broaden your perspective a little bit and you go into emerging markets or you look at places like master limited partnerships or high-yield bonds or commodities or even global real estate, certain areas of the globe have had positive returns with even lower volatility in some cases. I think that investing has changed, and ETFs are allowing people to broaden their asset class exposure.

The poor returns that the U.S. equities have had in the last decade are also forcing people to really look beyond the U.S. and also beyond equities. And I think that in those asset classes, as long as you have broad enough exposure and you have diversified exposure, traditional indexing still makes a lot of sense.

JOI: What have been the biggest paradigm shifts in the global economy in the last five years?Held: There are so many. But if I had to put my finger on it, it would be really the change in leadership between the developed world and the emerging world. The emerging markets have really proven themselves to be the developed markets of tomorrow. If you look at just about every metric, whether it’s growth or employment or capital reserves, they continue to show much better fundamentals than the developed markets.

In my opinion, the hardest challenge for the developed markets—which is where most of the investing capital is located—is going to be how they can continue to grow or compete with emerging markets. From an investing perspective, how are people going to create portfolios and create an asset allocation model that adapts and shifts to a world where emerging economies are growing faster with lower debt and much better fundamentals than the developed markets, considering the developed markets are where most of their money is held?

JOI: Is program trading driving short-term stock move-ments? Are ETFs to blame?Held: I think it’s difficult to say with any kind of certainty. There’s been a lot of volatility in recent years and there’s been a really rapid increase in high-frequency trading and algorithmic trading. So it’s easier to connect the two dots and say that they’re related. I think that a lot of the fast trading may exacerbate volatility. But ultimately, the market does set a fair mechanism for buyers and sellers to find an agreed-upon price and a price that’s fair. Also, access to these markets has increased. As information gets processed more rapidly, you’re going to see that informa-tion get executed into pricing better than you did in the past. So I think you just have better price discovery, better visibility and sometimes that leads to more volatility.

But I don’t think ETFs are necessarily to blame for that. ETFs are a vehicle that people use to get access and expo-sure, but the more rapidly information gets processed, sometimes that leads to an increase in volatility in the short term, but better price discovery and better execution and fair value in the long run.

JOI: When rates finally start to rise, will fixed-income index investors suffer? Are they prepared for that?Held: It really depends on how the indexes are construct-ed, and that just sort of speaks to the evolution of indexing and the evolution of ETFs. Asset classes used to be stocks, bonds and cash, and now they’ve obviously expanded quite a bit. Even within the fixed-income spectrum, you have so many different asset classes to choose from. If rates

November / December 201120

rise, it’s not only going to depend on which asset classes are affected, but also why rates are rising.

You could have a scenario where emerging market debt could do very well if rates rise because they’re not necessarily tied to what’s happening in the U.S., and those economies are growing very fast. If you have anoth-er index tied to bank loans, and rates rise, then they could obviously do very well. So it really depends.

JOI: What impact will the recent spike in volatility have on investor allocations?Held: When you get these spikes in volatility, it just increas-es the fear that people have. And when they have a lot more fear, they’re much more reluctant to invest into risky assets. It may force investors to be a little more reluctant to add allocations to risky assets, probably at the time that they should be allocating the most. I think on one hand, it’s going to cause investors to be a little bit more conservative, and people just seem to have a lot more fear, especially U.S. equity investors, who lost half their money twice in the same decade. When you have months like you did in August 2011, people say, “You know, we got fooled twice. We can’t afford to be fooled a third time.”

So really the first ramification of increased volatility is going to be just an overall level of conservatism, particu-larly towards risky assets. I think the second thing is that it’s going to force investors to look at more innovative and creative ways to try and access volatility or harness volatility, and gold has obviously been a very popular way for people to play the fear trade.

JOI: Are investors in danger of overweighting emerging markets?Held: They may be. When you look at the long-term picture, it’s hard to imagine a scenario over the next 10 years where emerging markets from an investment perspective don’t play out well, particularly relative to developed markets. But along the way, there is going to be a lot of volatility. I guess the perfect storm that we’ve had in the developed markets, where everything has gone wrong, has really been the oppo-site in the emerging markets, where everything has gone right. And you still have some emerging economies that are a little bit more fragile than people expect.

I believe that we’re going to end up in a good spot in emerging markets five years, 10 years, 20 years down the road, but there’s going to be a lot of volatility. Where the

risk lies for investors should be viewed more from a timing perspective than from an allocation perspective.

It really depends on which emerging markets, too. Emerging markets get painted with a pretty broad brush, but what’s happening in China and India and Brazil and Russia is quite different, and these are quite distinct markets. So I think you’re going to start to see people pay a little bit more attention to the regional differences among those emerging economies.

JOI: At what price is gold too expensive?Held: It’s hard to say. I had always said $1,000, but I would have been wrong by a long shot. It’s hard to say because it’s something that trades on sentiment and doesn’t nec-essarily trade on fundamentals. It gets lumped in with commodities, but doesn’t really move with commodities. It moves much more with people’s perceptions about what’s happening from a currency perspective and from a global growth perspective and a fear perspective.

The price of gold is going to be so dependent on where everything else is. If we have a strong equity market, if we have a strong dollar, if the developed world gets the bank-ing and debt problems figured out, then $1,800 an ounce

may seem expensive. If all of those things don’t happen and the developed markets and the currency markets and the equity markets continue to struggle, then $1,800 is going to seem cheap. Gold seems to be priced so much more in its value in terms of other asset classes than any-thing else. So a fair price for gold is going to be dependent upon what’s happening in those other areas.

JOI: What key wisdom would you offer investors faced with extreme volatility and fear in the market?Held: Know what you own and really understand what you’re investing in. It sounds like a cliché and it sounds oversimplified, but a lot of people don’t understand what their exposures are. I would think back to the late ’90s when people thought they were diversified because they owned some stocks and some index funds and some mutual funds. Then they found out that the stocks they owned were IBM, Cisco, Microsoft and Intel, and the indexes and the actively managed funds they owned were 40 percent technology. The best thing people can do is to understand what they own, understand where their risks lie, make sure that they’re diversified by sec-tor and by region and by asset class.

www.journalofindexes.com November / December 2011 21

“When you look at the long-term picture, it’s hard to imagine a scenario over the next 10 years where emerging markets from an investment

perspective don’t play out well, particularly relative to developed markets. But along the way, there is going to be a lot of volatility.”

—Jeremy Held

Talking Indexes

November / December 2011

By David Blitzer

22

How have the last few years of market turmoil

changed indexing? For the better!

Indexing In A Time

Of Market Turmoil

The last few years saw more volatile markets than almost any time since the 1930s, as the financial crisis sent the stock market into its second major