W.I.R.C. INITIATION INTO IFRS KISHOR M.PARIKH Lecture - IAS 1_ 22-01-2011... · similar financial...

41

Transcript of W.I.R.C. INITIATION INTO IFRS KISHOR M.PARIKH Lecture - IAS 1_ 22-01-2011... · similar financial...

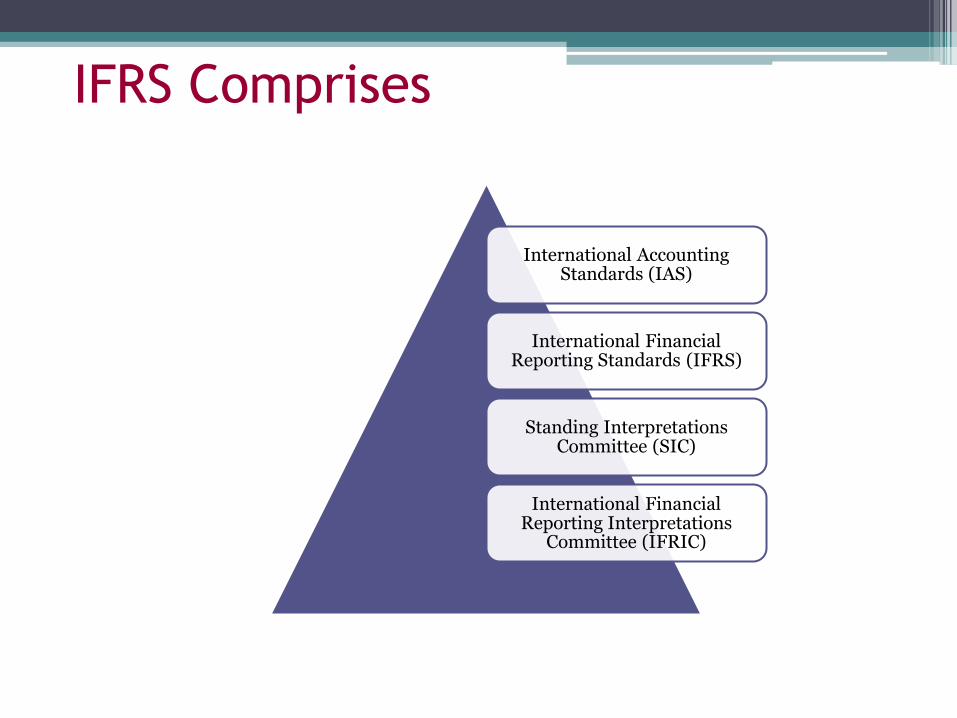

IFRS Comprises

International Accounting Standards (IAS)

International Financial Reporting Standards (IFRS)

Standing Interpretations Committee (SIC)

International Financial Reporting Interpretations

Committee (IFRIC)

List of Standards currently applicable

IFRS-1 – First-time adoption of International FinancialReporting Standards

IFRS-2 – Share-based PaymentIFRS-3 – Business CombinationsIFRS-4 – Insurance ContractsIFRS-5 – Non-current assets held for sale and discontinued

operationsIFRS-6 – Exploration for and evaluation of mineral resourcesIFRS-7 – Financial Instruments and DisclosuresIFRS-8 – Operating SegmentsIFRS 9 – Financial InstrumentsIAS-1 – Presentation of Financial StatementsIAS-2 – InventoriesIAS-7 – Cash Flow StatementsIAS-8 – Net Profits or Loss for the period, fundamentals errors

and changes in accounting policiesIAS-10 – Events after the Balance Sheet DateIAS-11 – Construction ContractsIAS-12 – (Revised) Income TaxesIAS-14 – Segment ReportingIAS-16 – Property, Plant and EquipmentIAS-17 – LeasesIAS-18 – Revenue

IAS-19 – (Revised) Employee BenefitsIAS-20 – Accounting for Government Grants and Disclosure of

Government AssistanceIAS-21 – The Effects of Changes in Foreign Exchange RatesIAS-23 – Borrowing CostsIAS-24 – Related Party DisclosuresIAS-26 – Accounting and reporting by retirement benefit plansIAS-27 – Consolidated Financial statements and accounting for

investment in subsidiariesIAS-28 – Investments in associatesIAS-29 – Financial Reporting in hyperinflationary economiesIAS-30 – Disclosures in the Financial Statements of Banks and

similar financial InstitutionsIAS-31 – Financial Reporting of Interests in Joint VenturesIAS-32 – Financial Instruments: PresentationIAS-33 – Earnings per ShareIAS-34 – Interim financial reportingIAS-36 – Impairment of AssetsIAS-37 – Provisions, Contingent liabilities and ContingentAssetsIAS-38 – Intangible AssetsIAS-39–Financial instruments: Recognition and measurementsIAS-40 – Investment PropertyIAS-41 – Agriculture

3

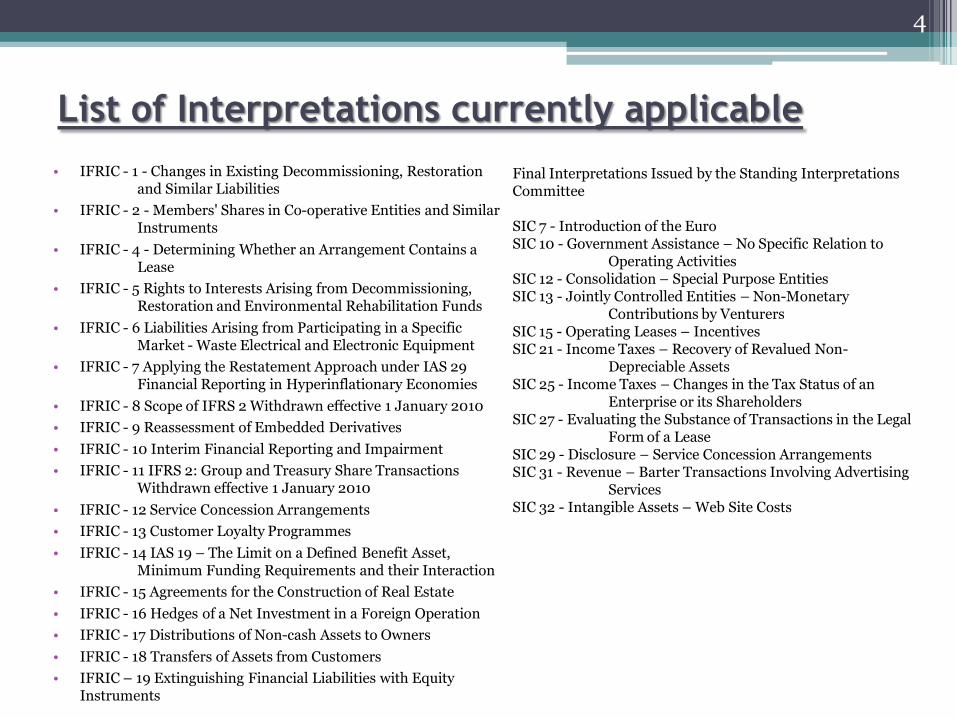

List of Interpretations currently applicable

• IFRIC - 1 - Changes in Existing Decommissioning, Restoration and Similar Liabilities

• IFRIC - 2 - Members' Shares in Co-operative Entities and Similar Instruments

• IFRIC - 4 - Determining Whether an Arrangement Contains a Lease

• IFRIC - 5 Rights to Interests Arising from Decommissioning, Restoration and Environmental Rehabilitation Funds

• IFRIC - 6 Liabilities Arising from Participating in a Specific Market - Waste Electrical and Electronic Equipment

• IFRIC - 7 Applying the Restatement Approach under IAS 29 Financial Reporting in Hyperinflationary Economies

• IFRIC - 8 Scope of IFRS 2 Withdrawn effective 1 January 2010

• IFRIC - 9 Reassessment of Embedded Derivatives

• IFRIC - 10 Interim Financial Reporting and Impairment

• IFRIC - 11 IFRS 2: Group and Treasury Share Transactions Withdrawn effective 1 January 2010

• IFRIC - 12 Service Concession Arrangements

• IFRIC - 13 Customer Loyalty Programmes

• IFRIC - 14 IAS 19 – The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their Interaction

• IFRIC - 15 Agreements for the Construction of Real Estate

• IFRIC - 16 Hedges of a Net Investment in a Foreign Operation

• IFRIC - 17 Distributions of Non-cash Assets to Owners

• IFRIC - 18 Transfers of Assets from Customers

• IFRIC – 19 Extinguishing Financial Liabilities with Equity Instruments

Final Interpretations Issued by the Standing Interpretations Committee

SIC 7 - Introduction of the Euro SIC 10 - Government Assistance – No Specific Relation to

Operating Activities SIC 12 - Consolidation – Special Purpose Entities SIC 13 - Jointly Controlled Entities – Non-Monetary

Contributions by Venturers SIC 15 - Operating Leases – Incentives SIC 21 - Income Taxes – Recovery of Revalued Non-

Depreciable Assets SIC 25 - Income Taxes – Changes in the Tax Status of an

Enterprise or its Shareholders SIC 27 - Evaluating the Substance of Transactions in the Legal

Form of a Lease SIC 29 - Disclosure – Service Concession Arrangements SIC 31 - Revenue – Barter Transactions Involving Advertising

Services SIC 32 - Intangible Assets – Web Site Costs

4

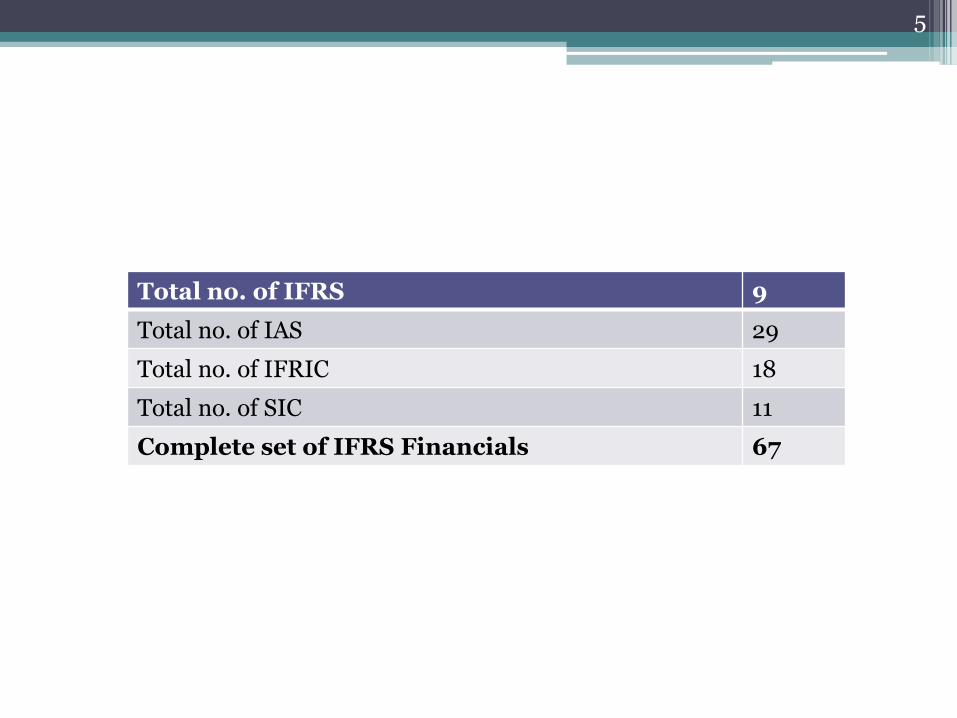

Total no. of IFRS 9

Total no. of IAS 29

Total no. of IFRIC 18

Total no. of SIC 11

Complete set of IFRS Financials 67

5

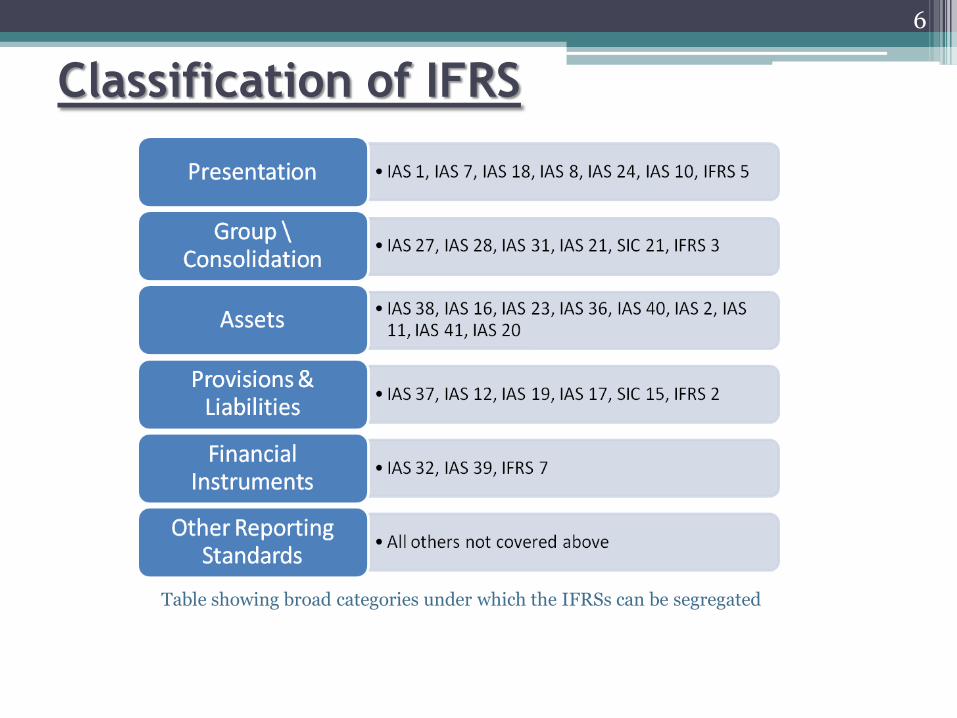

Classification of IFRS

Table showing broad categories under which the IFRSs can be segregated

6

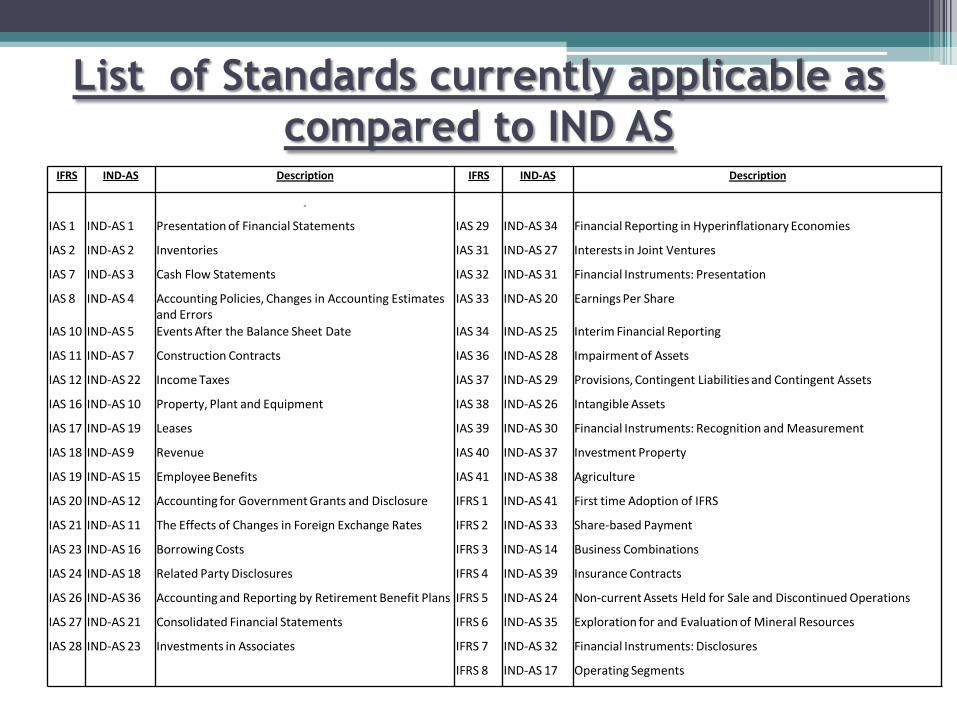

List of Standards currently applicable as

compared to IND ASIFRS IND-AS Description IFRS IND-AS Description

IAS 1 IND-AS 1 Presentation of Financial Statements IAS 29 IND-AS 34 Financial Reporting in Hyperinflationary Economies

IAS 2 IND-AS 2 Inventories IAS 31 IND-AS 27 Interests in Joint Ventures

IAS 7 IND-AS 3 Cash Flow Statements IAS 32 IND-AS 31 Financial Instruments: Presentation

IAS 8 IND-AS 4 Accounting Policies, Changes in Accounting Estimates and Errors

IAS 33 IND-AS 20 Earnings Per Share

IAS 10 IND-AS 5 Events After the Balance Sheet Date IAS 34 IND-AS 25 Interim Financial Reporting

IAS 11 IND-AS 7 Construction Contracts IAS 36 IND-AS 28 Impairment of Assets

IAS 12 IND-AS 22 Income Taxes IAS 37 IND-AS 29 Provisions, Contingent Liabilities and Contingent Assets

IAS 16 IND-AS 10 Property, Plant and Equipment IAS 38 IND-AS 26 Intangible Assets

IAS 17 IND-AS 19 Leases IAS 39 IND-AS 30 Financial Instruments: Recognition and Measurement

IAS 18 IND-AS 9 Revenue IAS 40 IND-AS 37 Investment Property

IAS 19 IND-AS 15 Employee Benefits IAS 41 IND-AS 38 Agriculture

IAS 20 IND-AS 12 Accounting for Government Grants and Disclosure IFRS 1 IND-AS 41 First time Adoption of IFRS

IAS 21 IND-AS 11 The Effects of Changes in Foreign Exchange Rates IFRS 2 IND-AS 33 Share-based Payment

IAS 23 IND-AS 16 Borrowing Costs IFRS 3 IND-AS 14 Business Combinations

IAS 24 IND-AS 18 Related Party Disclosures IFRS 4 IND-AS 39 Insurance Contracts

IAS 26 IND-AS 36 Accounting and Reporting by Retirement Benefit Plans IFRS 5 IND-AS 24 Non-current Assets Held for Sale and Discontinued Operations

IAS 27 IND-AS 21 Consolidated Financial Statements IFRS 6 IND-AS 35 Exploration for and Evaluation of Mineral Resources

IAS 28 IND-AS 23 Investments in Associates IFRS 7 IND-AS 32 Financial Instruments: Disclosures

IFRS 8 IND-AS 17 Operating Segments

Introduction• Issued in September 2007

• Replaces the previous version of 2003

• Mandatory for period starting on or after January 1, 2009

• Earlier adoption permitted

• Equivalent Indian GAAP

▫ Schedule VI

▫ AS 1 : Disclosure of Accounting Policies

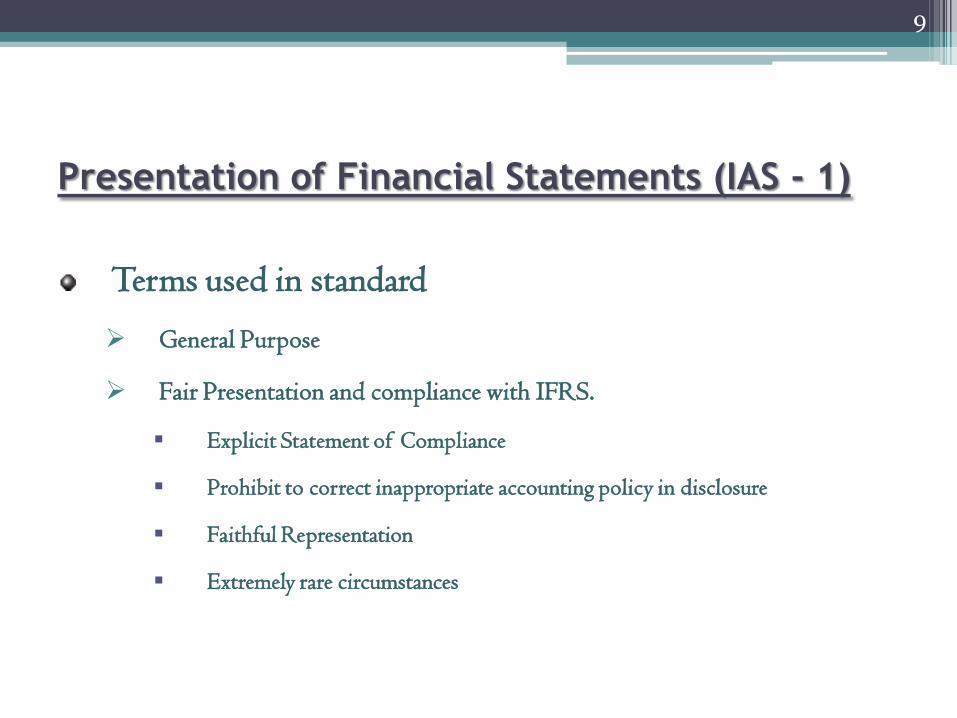

Presentation of Financial Statements (IAS - 1)

Terms used in standard

General Purpose

Fair Presentation and compliance with IFRS.

Explicit Statement of Compliance

Prohibit to correct inappropriate accounting policy in disclosure

Faithful Representation

Extremely rare circumstances

9

Faithful Representation

A fair representation is achieved by compliance with applicable IFRSs. A fairrepresentation also requires the following from an entity:

• To select and apply accounting policies in accordance with IAS 8 –Accounting policies, changes in accounting estimates and errors. IAS 8 setsout hierarchy of authoritative guidance that management considers in theabsence of a standard or an interpretation that specifically applies to anitem.

• To present information, including accounting policies, in a manner thatprovides relevant, reliable, comparable and understandable information.

• To provide additional disclosures when compliance with the specificrequirements in IFRSs is insufficient to enable users to understand theimpact of particular transactions, other events and conditions on theentity’s financial position and financial performance.

10

Extremely Rare Circumstances

• If management believes that compliance with a particular requirement of IFRS is so misleading that it would conflict with the objectives of the financial statements as laid down in the IASB’s framework, then the entity is allowed to depart from that requirement (of the IFRS).

11

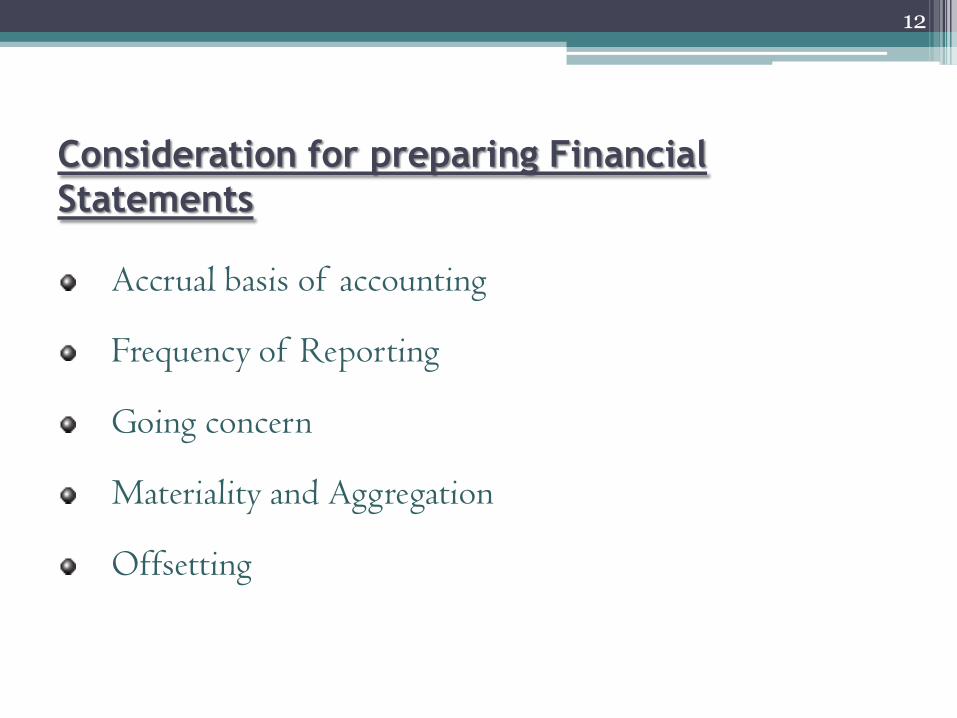

Consideration for preparing Financial

Statements

Accrual basis of accounting

Frequency of Reporting

Going concern

Materiality and Aggregation

Offsetting

12

Going Concern• How to assess:

▫ Consider all available information about the future (minimum 12 months from the reporting date) particularly

Current and expected profitability

Debt repayment schedules

Potential sources of replacement financing

▫ Depends on the facts of each case

Materiality and Aggregation• Definition:

▫ Omissions or misstatements of items are material if they could, individually or collectively, influence the economic decisions that users make on the basis of financial statements.

▫ Materiality depends on the size and nature of the omission or misstatement judged in the surrounding circumstances

▫ The determining factor could be The size or nature of the item, or a combination of both

Offsetting• Not to offset

▫ Assets and liabilities

▫ Income and expenses

unless permitted by an IFRS

Characteristics of Financial Statements

Understandability – The objective of understandability is achieved with the help

of the following essentials components:

1. Those preparing the statements present/disclose full information that is material

for the understanding of the statement and present it in an understandable

manner.

2. Users have a reasonable knowledge of business and economic activities and

accounting principles and show willingness to study the information.

Relevance – Information has the quality of relevance when it influences the

economic decisions of users by helping them evaluate past, present or future

events or confirming, or correcting, their past evaluations.

Reliability – if users are to take decisions based on the financial statements, the

information in the statements has to be reliable; otherwise it cannot be recognised

even if it is relevant.

16

• Comparability –

1. Within the entity over time: the user should be able to compare the amounts of

different periods and identity trends, if any, in the financial position and

performance.

2. Between different entities: the user should find it possible to evaluate the relative

financial position, changes in the financial position and performance of the

entity.

3. Present

▫ When an entity

Applies an accounting policy retrospectively

Makes a retrospective restatement of items in its financial statements

Reclassifies items in its financial statements

▫ disclosing comparative information, as a minimum

Three statements of financial position

Two of each of the other statements

Related notes

17

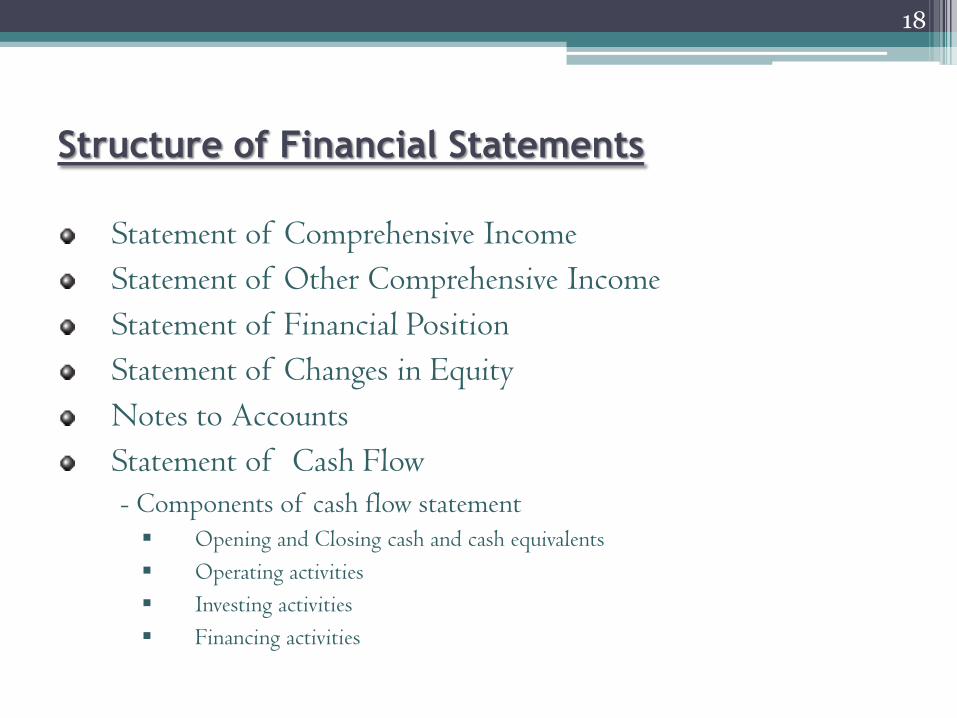

Structure of Financial Statements

Statement of Comprehensive Income

Statement of Other Comprehensive Income

Statement of Financial Position

Statement of Changes in Equity

Notes to Accounts

Statement of Cash Flow

- Components of cash flow statement Opening and Closing cash and cash equivalents

Operating activities

Investing activities

Financing activities

18

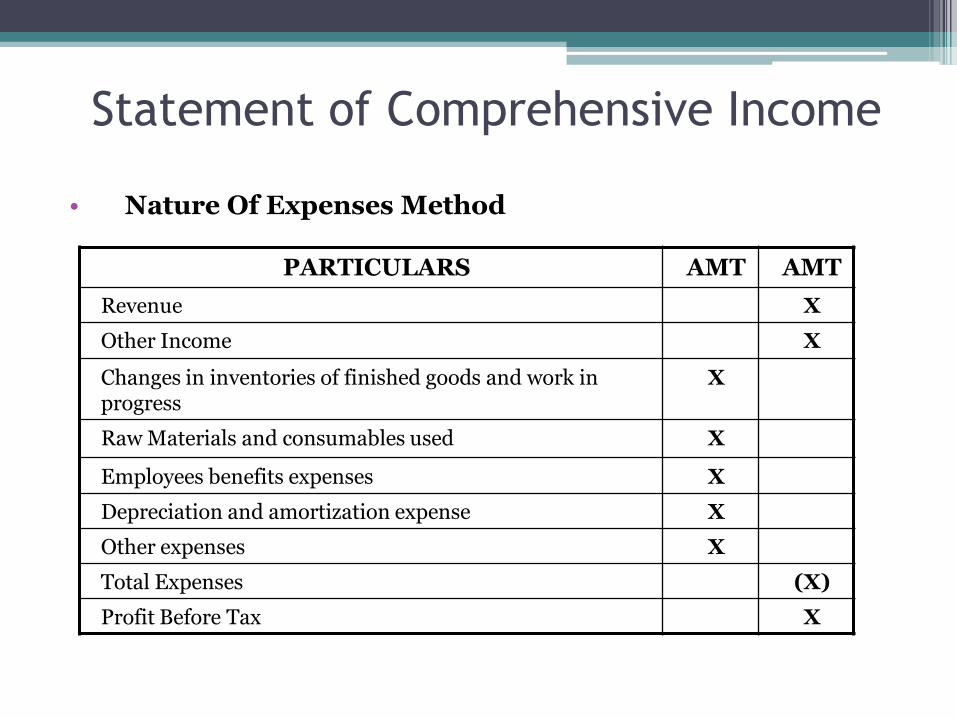

Statement of Comprehensive Income

• Nature Of Expenses Method

PARTICULARS AMT AMT

Revenue X

Other Income X

Changes in inventories of finished goods and work in progress

X

Raw Materials and consumables used X

Employees benefits expenses X

Depreciation and amortization expense X

Other expenses X

Total Expenses (X)

Profit Before Tax X

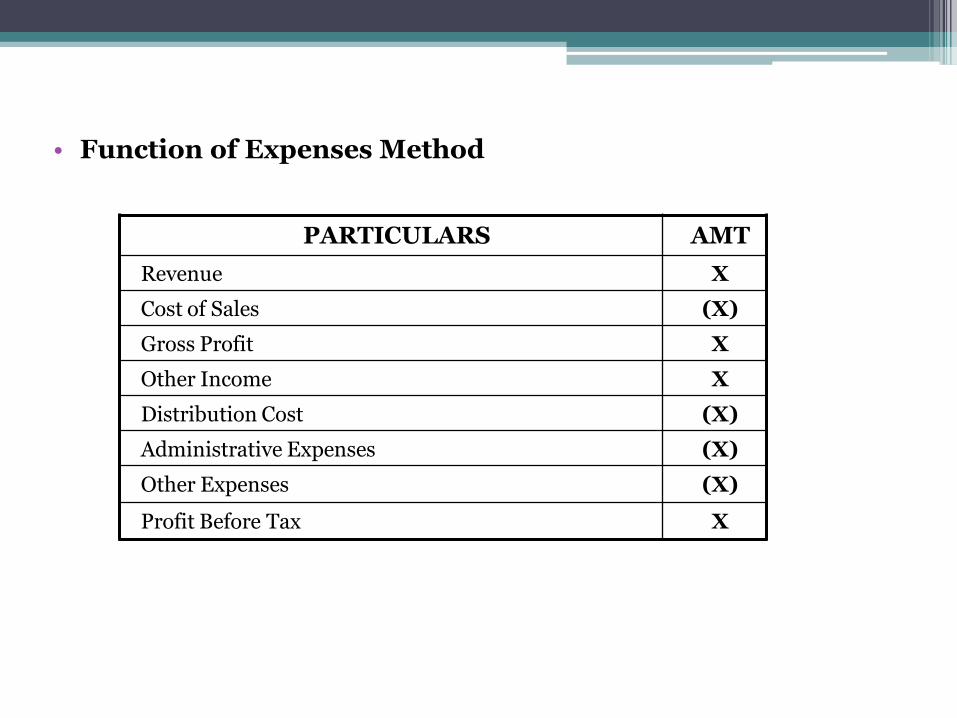

• Function of Expenses Method

PARTICULARS AMT

Revenue X

Cost of Sales (X)

Gross Profit X

Other Income X

Distribution Cost (X)

Administrative Expenses (X)

Other Expenses (X)

Profit Before Tax X

Separate disclosure in the income statement

• Write down of inventory to net realizable valueof P.P.E. to recoverable amount as well asreversal

• Provision for restructuring cost and reversal.

• Disposal of P.P.E.

• Disposal of investment.

• Discontinued operations.

• Litigation settlement.

• Other reversals of provisions.

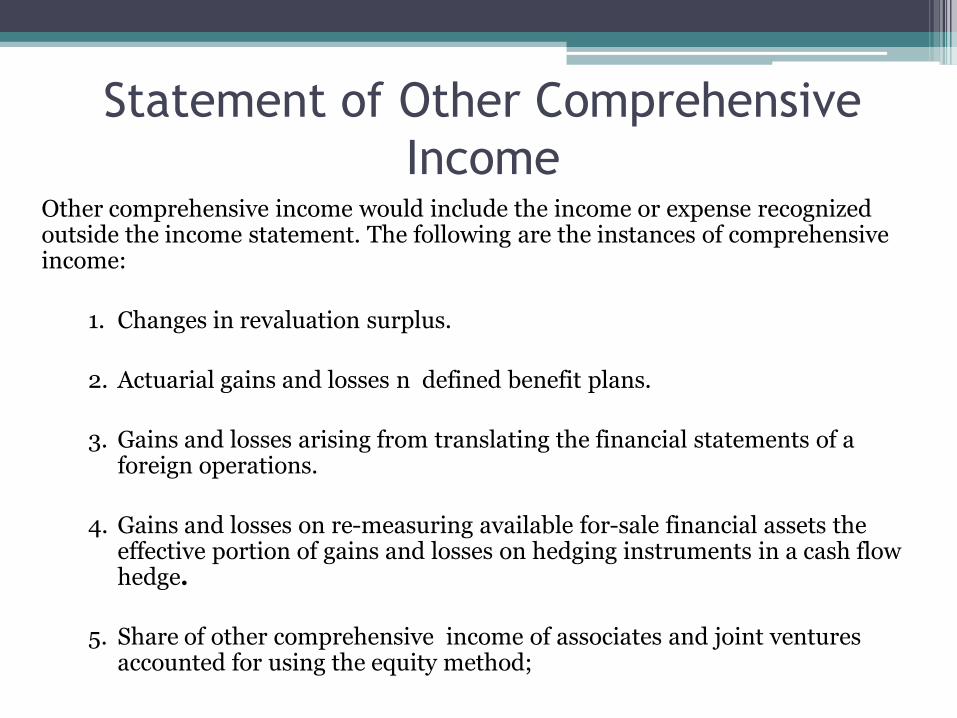

Statement of Other Comprehensive

IncomeOther comprehensive income would include the income or expense recognized outside the income statement. The following are the instances of comprehensive income:

1. Changes in revaluation surplus.

2. Actuarial gains and losses n defined benefit plans.

3. Gains and losses arising from translating the financial statements of a foreign operations.

4. Gains and losses on re-measuring available for-sale financial assets the effective portion of gains and losses on hedging instruments in a cash flow hedge.

5. Share of other comprehensive income of associates and joint ventures accounted for using the equity method;

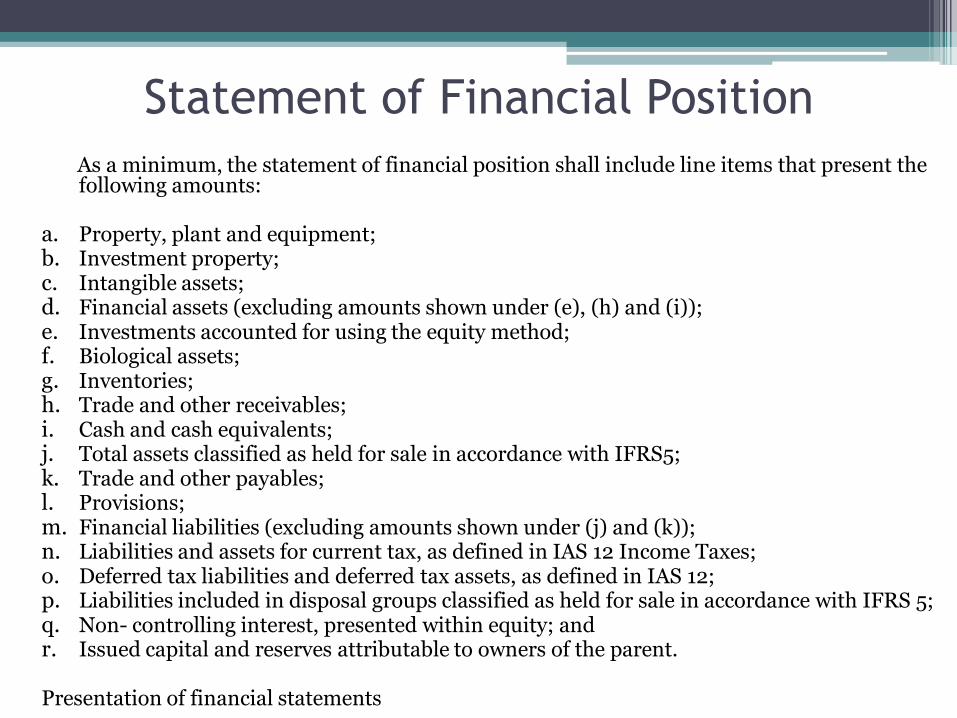

Statement of Financial Position

As a minimum, the statement of financial position shall include line items that present the following amounts:

a. Property, plant and equipment;b. Investment property;c. Intangible assets;d. Financial assets (excluding amounts shown under (e), (h) and (i));e. Investments accounted for using the equity method;f. Biological assets;g. Inventories;h. Trade and other receivables;i. Cash and cash equivalents;j. Total assets classified as held for sale in accordance with IFRS5;k. Trade and other payables;l. Provisions;m. Financial liabilities (excluding amounts shown under (j) and (k));n. Liabilities and assets for current tax, as defined in IAS 12 Income Taxes;o. Deferred tax liabilities and deferred tax assets, as defined in IAS 12;p. Liabilities included in disposal groups classified as held for sale in accordance with IFRS 5;q. Non- controlling interest, presented within equity; andr. Issued capital and reserves attributable to owners of the parent.

Presentation of financial statements

PARTICULARS AMOUNT

Assets

Non Current Assets X

Total Non Current Assets X

Current Assets X

Total Current Assets X

Equity and Liabilities

Equity attributable to equity holders of the parent X

Share Capital X

Retained Earnings X

Other components of equity X

Non Controlling interest X

Total Equity X

Non Current Liabilities X

Total Non Current Liabilities X

Current Liabilities X

Total Current Liabilities X

Total Liabilities X

Total equity and liabilities X

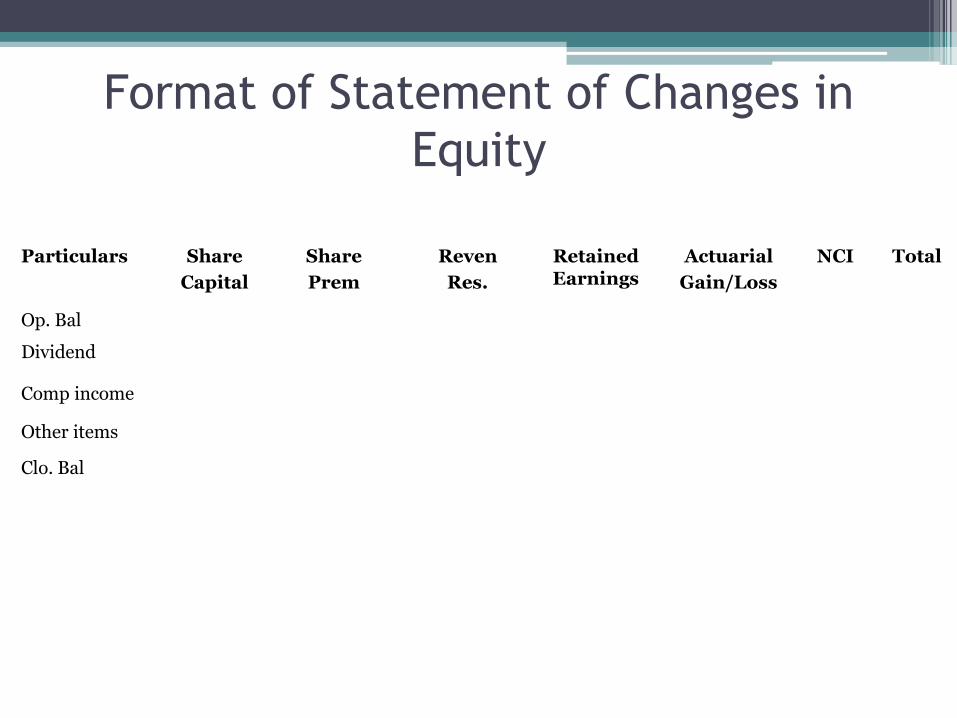

Format of Statement of Changes in

Equity

Particulars Share

Capital

Share

Prem

Reven

Res.

Retained Earnings

Actuarial

Gain/Loss

NCI Total

Op. Bal

Dividend

Comp income

Other items

Clo. Bal

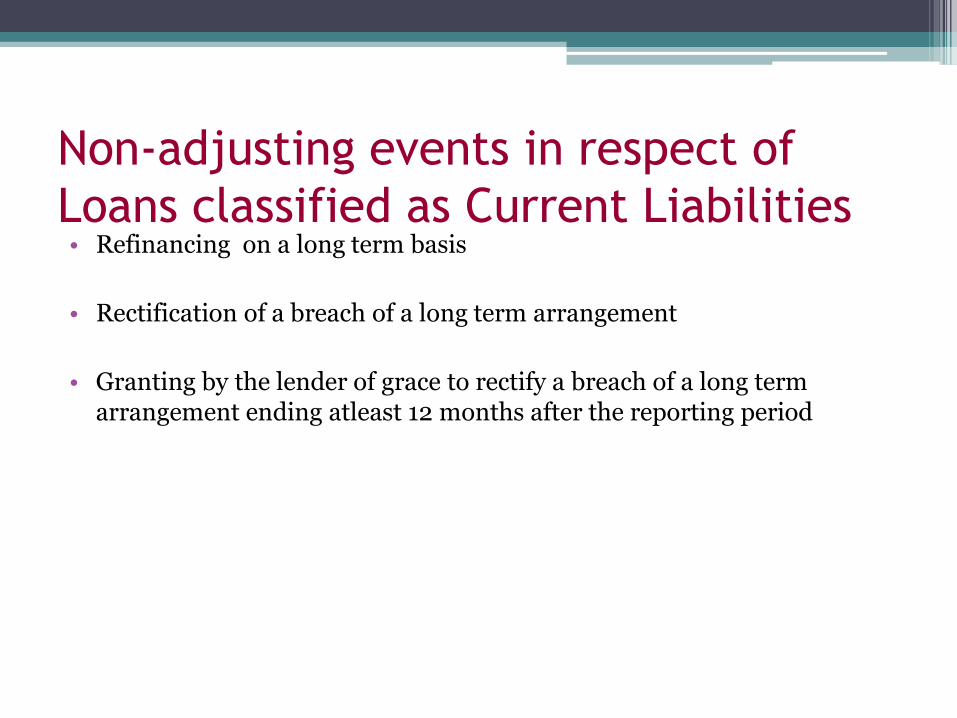

Non-adjusting events in respect of

Loans classified as Current Liabilities• Refinancing on a long term basis

• Rectification of a breach of a long term arrangement

• Granting by the lender of grace to rectify a breach of a long term arrangement ending atleast 12 months after the reporting period

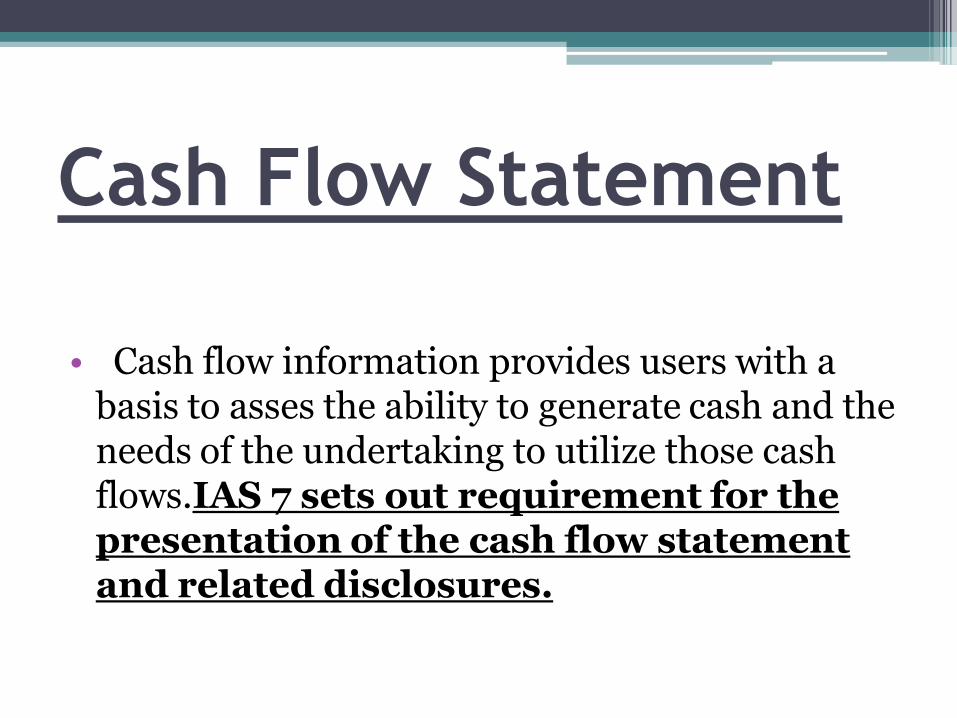

Cash Flow Statement

• Cash flow information provides users with a basis to asses the ability to generate cash and the needs of the undertaking to utilize those cash flows.IAS 7 sets out requirement for the presentation of the cash flow statement and related disclosures.

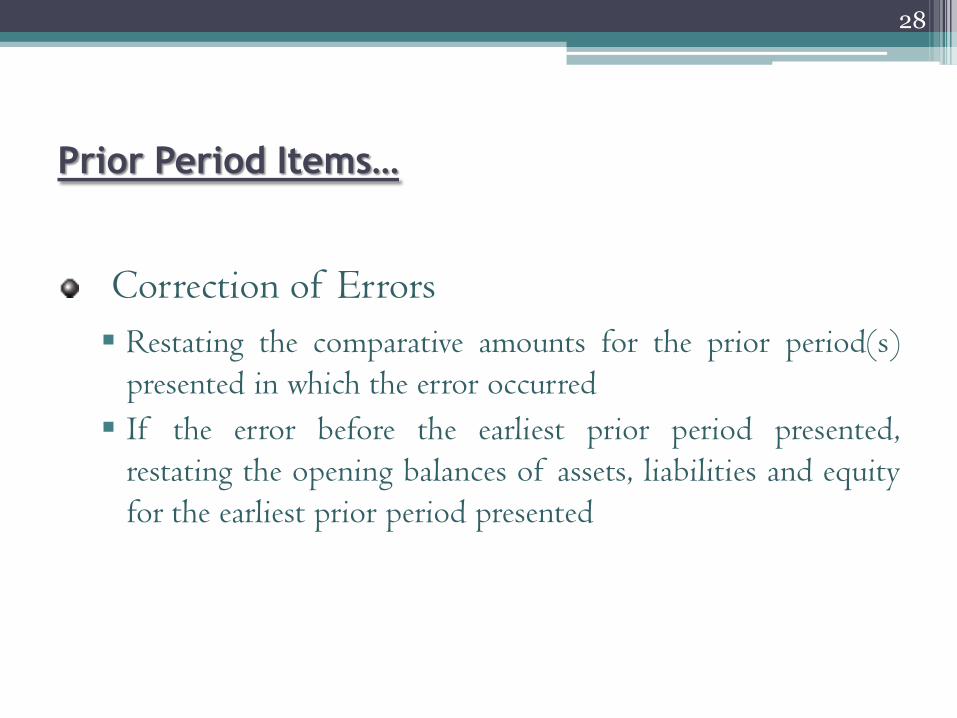

Prior Period Items…

Correction of Errors

Restating the comparative amounts for the prior period(s)

presented in which the error occurred

If the error before the earliest prior period presented,

restating the opening balances of assets, liabilities and equity

for the earliest prior period presented

28

Disclosure of accounting policies.

• An undertaking shall disclose in the summary of significant policies.

• Measurement basis

• Other policies relevant to an understanding of the financial statement.

• key sources of estimation of uncertainty.

• Other disclosures

Disclosure of managing capital

• Qualitative information about its objectives, policiesand processes for managing capital, including:-

1. A description of what it manages as capital;

2. When an entity is subject to externally imposedcapital requirements, the nature of thoserequirements and how those requirements areincorporated into the management of capital; and

3. How it is meeting its objectives for managing capital.

QUESTIONS ON PRESENTATION OF FINANCIAL

STATEMENTS

Q1)

• A company produces airplanes. The length of timebetween first purchasing raw materials to make theplanes to the date the company completes theproduction and delivery is 10 months. The companyreceives payment for the planes 6 months after delivery.

• How should the company show its inventory and tradereceivables in its classified balance sheet?

• Would you answer be different if the production timewas 14 months and the time between delivery andpayment was 15 months?

Q2 The company also has an available for

sale investment that it expects to realize in

15 months. How should this investment be

classified?

Q3 A parent provides a loan to a subsidiary.

Interest of 8% is paid annually. The loan is

repayable on demand. How should the loan be

classified in the parent's balance sheet?

• Q4 Certain employees of a company receive a cash bonus

based on the profits of the year. 50% of this bonus is paid

six months after the year in question and remaining 50% is

paid a year later (that is 18 months after the year end). The

company provides a five year warranty on the goods it sells.

The government has imposed a new law to protect the

environment under which the company has an obligation to

dispose of goods it manufactured at the end of their useful

life, estimated at ten years. How should the company

classify the following liabilities in its balance sheet?

a) Employee bonus accruals?

b) Warranty provisions?

c) Provision for disposal costs?

Q5 M/s XYZ Ltd. needs to refinance its long

term loan. The Balance Sheet is March and it

signs its refinance agreement in April and

authorizes the financial statement in May.

Whether the long term loan can be shown as

a non-current liability?

Q6 Entity X has taken 7% term loan of

Rs.15lakhs from a bank which will fall due for

payment on 30th June; 2007.It has an option to

renew its facility till 30th June, 2009. Entity

finalizes the accounts every December. It signs

refinance agreement in January and authorize

the financial statement in February. Should the

loan be classified as current liability?

Q7 Entity X has taken 10% long term loans of Rs.10,00,000 from a bank

which will fall due for payment on 30 June,2012 provided it is able to

maintain an EBITDA which is 10 times the interest obligation. In case this

financial parameter is not maintained the loan should be paid on demand.

The entity finalizes the accounts every December. It is observed that its

EBITDA is Rs.9,00,000 as on 31-12-2007. The bank has issued a letter

5th January, 2008 allowing a grace to the entity to rectify the breach by

the next year end. The financial statements are authorized for issue on

10th January, 2008.

•Should the loan be classified as non current?

•Would the classification be different had the bank issued the letter

offering grace period on or before the Balance sheet date?

Q8 A company has entered into a facility arrangement

with a bank. It has a committed facility that the bank

cannot cancel unilaterally and the schedule maturity

of this facility is three years from the balance sheet

date. The company has drawn down funds on this

facility and these funds are due to be repaid six

months after the balance sheet date. The company

intends to roll over this debt through the three year

facility arrangement. How should this borrowing be

shown in the company’s balance sheet?

\Would the answer be different if the facility and

existing loan were with different banks?

Q9 An entity has incurred losses for the past four

years and its current liabilities exceed its total assets.

The entity was in breach of its loan covenants and

has been negotiating with the related financial

institutions in order to keep them supporting its

business. These factors raise significant doubt that

the entity will be able to continue as a going concern.

How should the management disclose uncertainties

that affect the entity’s ability to continue as a going

concern?

40

Q10 XYZ Inc. is a manufacturer of televisions. The domestic

market for electronic goods is currently not doing well, and

therefore many entities in this business are switching to exports.

As per the audited financial statements for the year ended Dec

31, 20XX, the entity had net losses of $2 millions. At Dec 31,

20XX, its current assets aggregate to $ 20 millions and the

current liabilities aggregate to $ 25 millions. Due to the expected

favorable changes in the government policies for the electronics

industry, the entity is projecting profits in the coming years.

Furthermore, the shareholders of the entity have arranged

alternative additional sources of finance for its expansion plans

and to support its working needs in the next twelve months.

Should XYZ Inc. prepare its financial statements under the going

concern assumption?

Thank You

Mumbai, India

41