Creatività, schizofrenia ed immagini in blu - di Giuseppe Costantino Budetta

Upload

filippo-budettaCategory

view

48download

1

Filippo Budetta 152313 Paris MIB 2015 2017

Wine Industry An in depth analysis of the wine industry and its players

Filippo Budetta 152313 Paris MIB 2015 2017

Agenda The Wine

Wine industry overview

Numbers of rivalry

Scope of competitive rivalry

Numbers of Buyers

Product features

Research &Development role within the wine industry

Supply and demand conditions

Technological changes

Vertical Integration level

Economies of scales

Changyu winery

Cantina Valentini

Filippo Budetta 152313 Paris MIB 2015 2017

The wine

The Wine from Latin “vinum” is retained to be the oldest alcoholic beverage in the world, as there are some evidences which prove that this drink was already largely consumed in the Neolithic era. The earliest form of grape fermented was found in northern China, but several are the sources that confirm the presence of this beverage in many other countries. Later, during the medieval ages, the wine knew a further exploit becoming popular among all the different social classes and in some case assuming sacred aspects as seen in the catholic religion. The growth of wine continued through the following centuries, arriving to represent a beverage consumed worldwide besides than a millenary tradition.

Nowadays, the wine industry finds itself in a decline phase in the European market and the winery makers to sustain their profits are offering its products are opening its business to new markets such as: American, South African, Australian and New Zealand markets.

The following chapters aim to analyse and investigate about the features, dynamics and

characteristics relative to the wine industry, and an in-depth point of view would be given regarding

the Changyu winery and the cantina Valentini and their peculiarities.

Wine industry overview

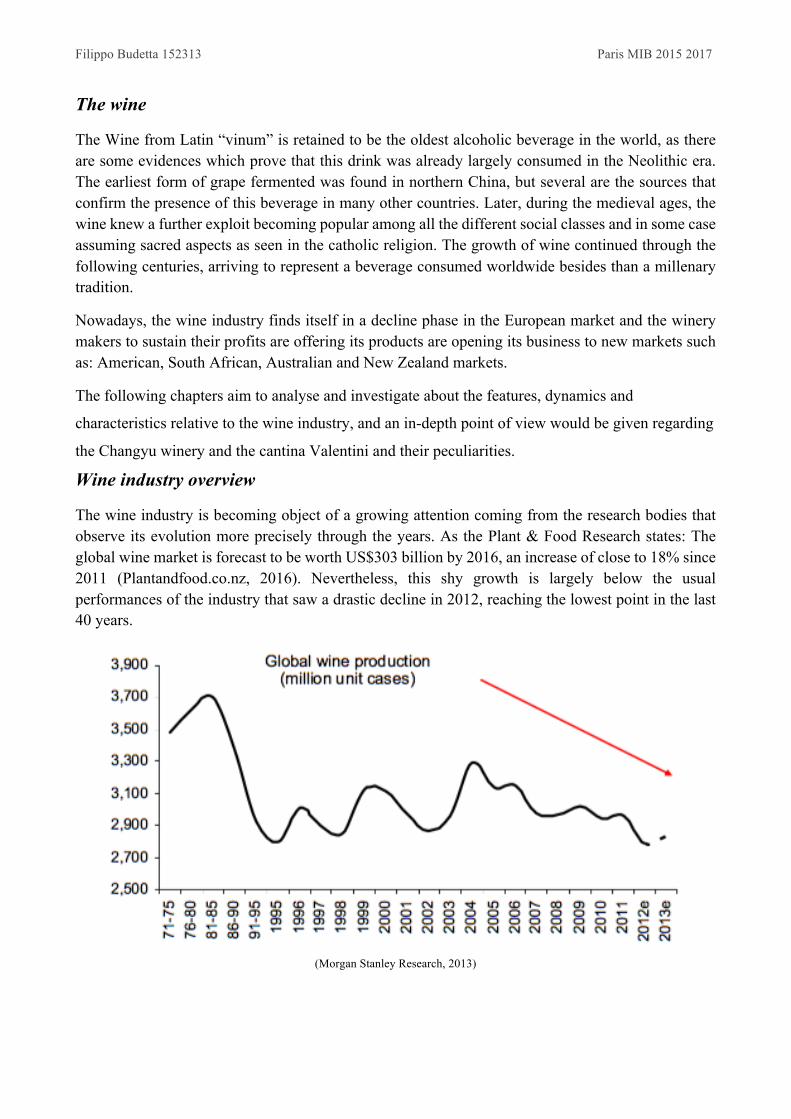

The wine industry is becoming object of a growing attention coming from the research bodies that observe its evolution more precisely through the years. As the Plant & Food Research states: The global wine market is forecast to be worth US$303 billion by 2016, an increase of close to 18% since 2011 (Plantandfood.co.nz, 2016). Nevertheless, this shy growth is largely below the usual performances of the industry that saw a drastic decline in 2012, reaching the lowest point in the last 40 years.

(Morgan Stanley Research, 2013)

Filippo Budetta 152313 Paris MIB 2015 2017

The data seem suggesting that the wine industry is founding itself in a decline phase, as the market

reveals some critical points concerning: a declining production for the top10 producers over the last

ten years, a lowering consumption and a slight decrease in the hectares of the vineyard surface as

shown in the picture below.

(Wine production worldwide in 2015, 2016)

On the other hand, it has to be said that some positive events are mitigating the bad externalities

abovementioned giving new hopes to the wine makers.

These positive effects are typical of an industry in the growing phase and they comprehend the source

of new markets, that so far remained behind: America, South Africa, Australia and Chile in the last

“years have increased their export volume by 370%”(BNPParibas, 2015). Another interesting data is

concerning the increasing demand of the American consumers that have “overtaken France as the

world’s foremost wine consumer, with average annual consumption of 12 litres per person”

(BNPParibas, 2015).

Last but at least, significant are the data highlighted by the analysis of the supply demand models of

the two macro classes: “Old World” composed by France, Italy, Portugal and Spain and “New world

“composed by Usa, Chile, Australia and South Africa.

These two markets show a substantial difference in quantity referred to the production and

consumption, infect while the consumption in “Old World” is levelling out causing a spread of 379

Filippo Budetta 152313 Paris MIB 2015 2017

million of unit case, the “New World” reports a positive trend characterized by a remarkable growth

with a really small spread of 186 million unit cases.

(Morgan Stanley Research, 2013)

(Morgan Stanley Research, 2013)

Furthermore, those there are the future previsions for the market confirm a positive trend in demand,

particularly the demand for fine and premium quality wine will increase from 9% to 13% of the whole

demand. Positive, are the data concerned to lower priced wines, infect the sales of bottles above $10

will rise between 4% and 8% (SVB, 2016).

Numbers of rivals

The industry counts more of 1 million of wine makers, spread all around the world, but in spite of

this few are the leading companies as the quality wine is strictly connected to the region of origin.

Filippo Budetta 152313 Paris MIB 2015 2017

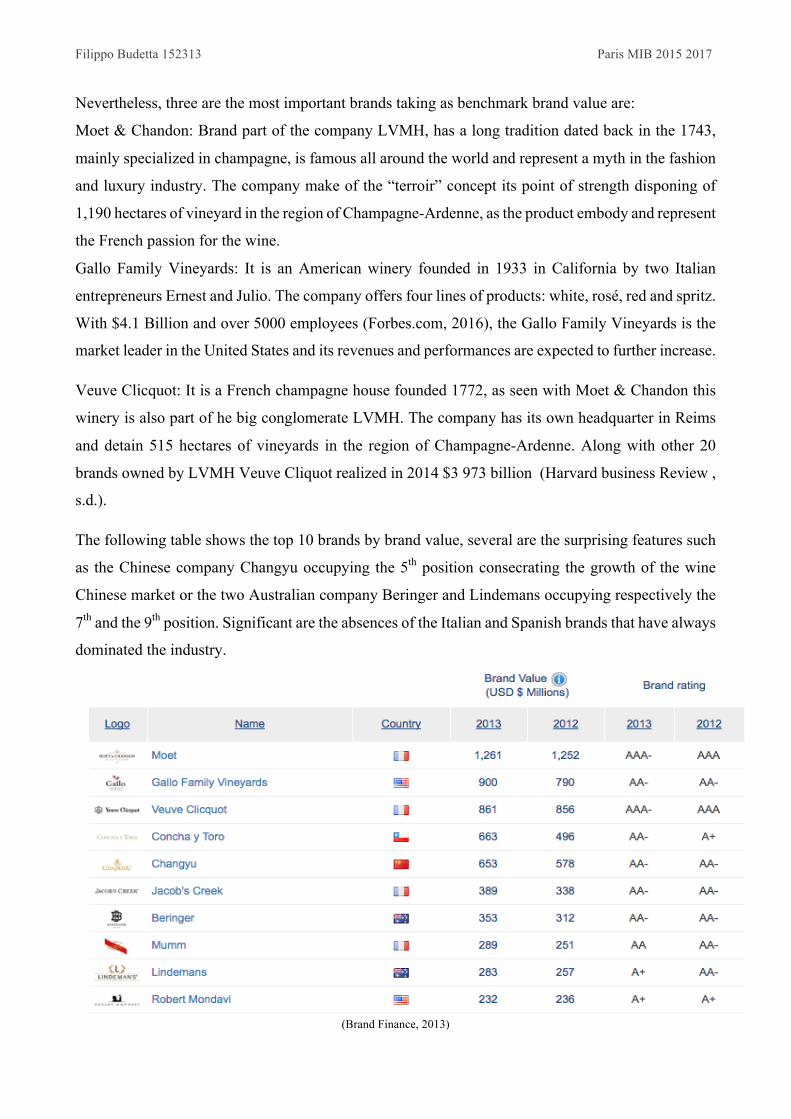

Nevertheless, three are the most important brands taking as benchmark brand value are:

Moet & Chandon: Brand part of the company LVMH, has a long tradition dated back in the 1743,

mainly specialized in champagne, is famous all around the world and represent a myth in the fashion

and luxury industry. The company make of the “terroir” concept its point of strength disponing of

1,190 hectares of vineyard in the region of Champagne-Ardenne, as the product embody and represent

the French passion for the wine.

Gallo Family Vineyards: It is an American winery founded in 1933 in California by two Italian

entrepreneurs Ernest and Julio. The company offers four lines of products: white, rosé, red and spritz.

With $4.1 Billion and over 5000 employees (Forbes.com, 2016), the Gallo Family Vineyards is the

market leader in the United States and its revenues and performances are expected to further increase.

Veuve Clicquot: It is a French champagne house founded 1772, as seen with Moet & Chandon this

winery is also part of he big conglomerate LVMH. The company has its own headquarter in Reims

and detain 515 hectares of vineyards in the region of Champagne-Ardenne. Along with other 20

brands owned by LVMH Veuve Cliquot realized in 2014 $3 973 billion (Harvard business Review ,

s.d.).

The following table shows the top 10 brands by brand value, several are the surprising features such

as the Chinese company Changyu occupying the 5th position consecrating the growth of the wine

Chinese market or the two Australian company Beringer and Lindemans occupying respectively the

7th and the 9th position. Significant are the absences of the Italian and Spanish brands that have always

dominated the industry.

(Brand Finance, 2013)

Filippo Budetta 152313 Paris MIB 2015 2017

Paradoxical is the position of the Italian companies, infect as already mentioned above none of the

Italian wineries are rated among the Top 10 brands, despite the Italian sector this year has

confirmed its position of best producer with a production of 49,5 million hectolitres (see the chart

below). This would certainly mean that the Italian production is mostly based on the SMEs that are

not comparable in size and financial capabilities with a large conglomerate such a s LVMH.

Therefore, the industry is remaining stable showing an interesting number of different competitors

really heterogeneousness in size production volume and sales.

(Wine production worldwide in 2015, 2016)

Scope of competitive rivalry

Historically, the two countries with a high demand for bottle of wine were also the two countries

with the highest volumes of production; France and Italy. Most of their production was consumed

within their own boundaries, but through the years the different tastes of the consumers and the

2008 financial recession cause a deep fall the wine in demand.

Nowadays, the European wine consumption, in the so called “Old World”, where all the famous

and historically wineries are located, is drastically declining. The two graphs bellow show how this

Filippo Budetta 152313 Paris MIB 2015 2017

data is becoming more and more serious for the wine companies that have to seek for new markets

over seas.

(Morgan Stanley Research, 2013)

(Morgan Stanley Research, 2013)

On the other hand, positive trends are shown that countries such as United States and China are likely

to be the new most important markets. The volumes of importations are rapidly growing, especially

referred to the European one rather then the South African or Australian one.

For example, it is proven that the Chinese consumers are becoming more and more fascinated by the

wine and particularly by the Italian and French products that are well known for being a niche of the

market. Therefore, is clear enough that these foreign consumers are becoming less sensible

concerning to higher premium prices.

Italianwine

Frenchwine

Filippo Budetta 152313 Paris MIB 2015 2017

The graphs in the following pages further highlights this trend showing how the Chinese consumption

of wine is growing over the years accounting in the 2012 for almost 250 million unit cases.

(Morgan Stanley Research, 2013)

The picture that the data describe in China is that the country must necessarily import to satisfy the

huge demand of the customers as the country despite its dimension arrive to produce a modest

quantity of hectolitres accounting just for 11,1 million unit cases. Moreover, the country imports

mostly from France that accounts for almost the 50% of the total imports that in 2012 accounted for

$35 million

(Morgan Stanley Research, 2013)

Filippo Budetta 152313 Paris MIB 2015 2017

(Morgan Stanley Research, 2013)

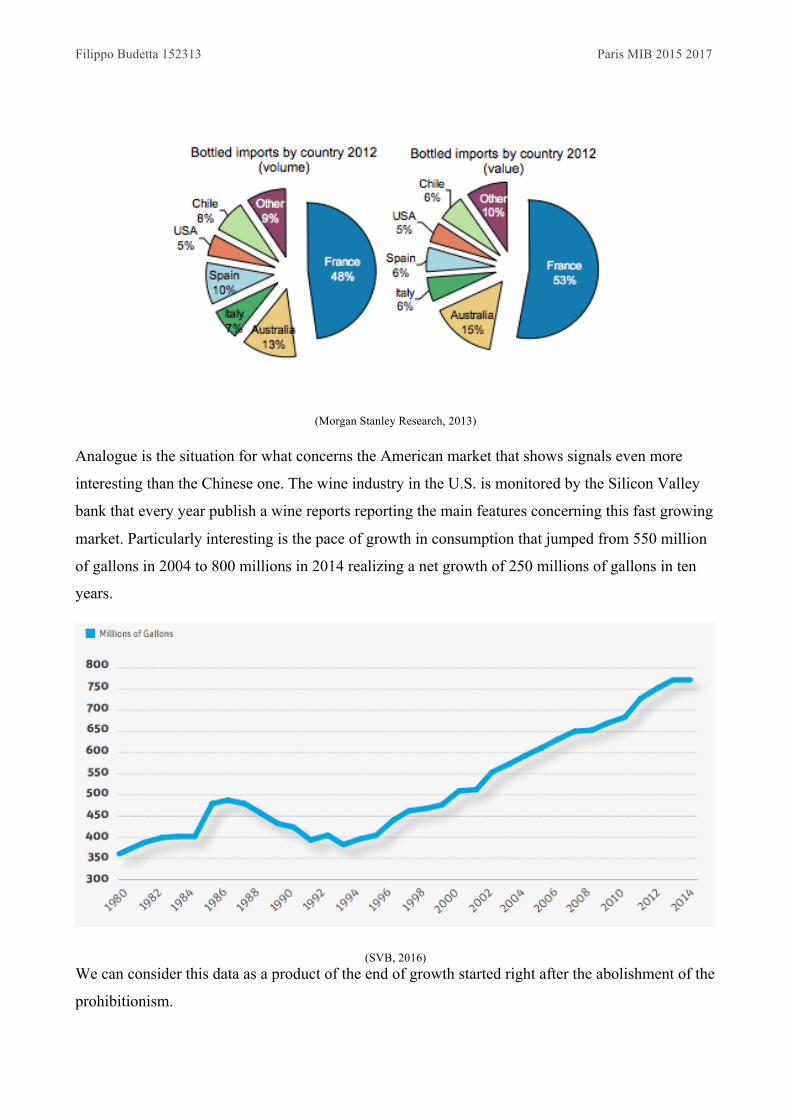

Analogue is the situation for what concerns the American market that shows signals even more

interesting than the Chinese one. The wine industry in the U.S. is monitored by the Silicon Valley

bank that every year publish a wine reports reporting the main features concerning this fast growing

market. Particularly interesting is the pace of growth in consumption that jumped from 550 million

of gallons in 2004 to 800 millions in 2014 realizing a net growth of 250 millions of gallons in ten

years.

(SVB, 2016) We can consider this data as a product of the end of growth started right after the abolishment of the

prohibitionism.

Filippo Budetta 152313 Paris MIB 2015 2017

Therefore, it is significantly important that the European wineries keep on supply the demands

coming from China and USA feeling the gap of demand and supply. Peculiarly, is to let understand

the customers the great difference between a product coming from the “Old World” and one coming

from the “New One”.

Numbers of Buyers

The wine is one of the most spread consumer good in the world, therefore giving an exact number

of the buyers might be a hard challenge. Studies conducted by the winery house constellation on the

biggest market, the American one, revel that six are the different segments of buyers and each of

them has a particular attitude concerning the purchase behaviour. By going more into the detail we

can find: Price driven customers, in the US the account for the 21% of the entire demand, they are

firmly convinced that a good bottle of wine has not to be necessarily expensive, at the base of their

choice there is the price rather than any other feature. Everyday loyal customers, representing the

20% of the demand, they consume wine regularly and they are more concerned about one brand.

The Overwhelmed customers segment is the third by size of these six segments, it accounts for a

large 19% of the total customers and contain those consumers who are not everyday drinkers. Their

purchase is mostly random as it does not imply a fix choice of a particular brand, generally

speaking they find the purchasing choice complex and overwhelming. Image seekers, accounting

for the 18% of consumers. They are not really fascinated by the product by itself but they are more

interested by the image and the status linked to the wine, this segment is rather rich and has an

appreciable propensity to consume up to 12$ per bottle.

Engaged Newcomers customers counts for the 12% of the entire demand, are consumers interested

to the world of the wine, mostly young and passionate arrive to spend up to 13$ per bottle. The last

segment is occupied the Enthusiast customers which are not sensible to price and represent the 10%

of the consumers, they arrive to spend in wine the 15% of their profits and up to pay a premium

price for a bottle of wine. Nevertheless, the different segments have heterogeneous levels of

Filippo Budetta 152313 Paris MIB 2015 2017

switching costs due to their loyalty level.

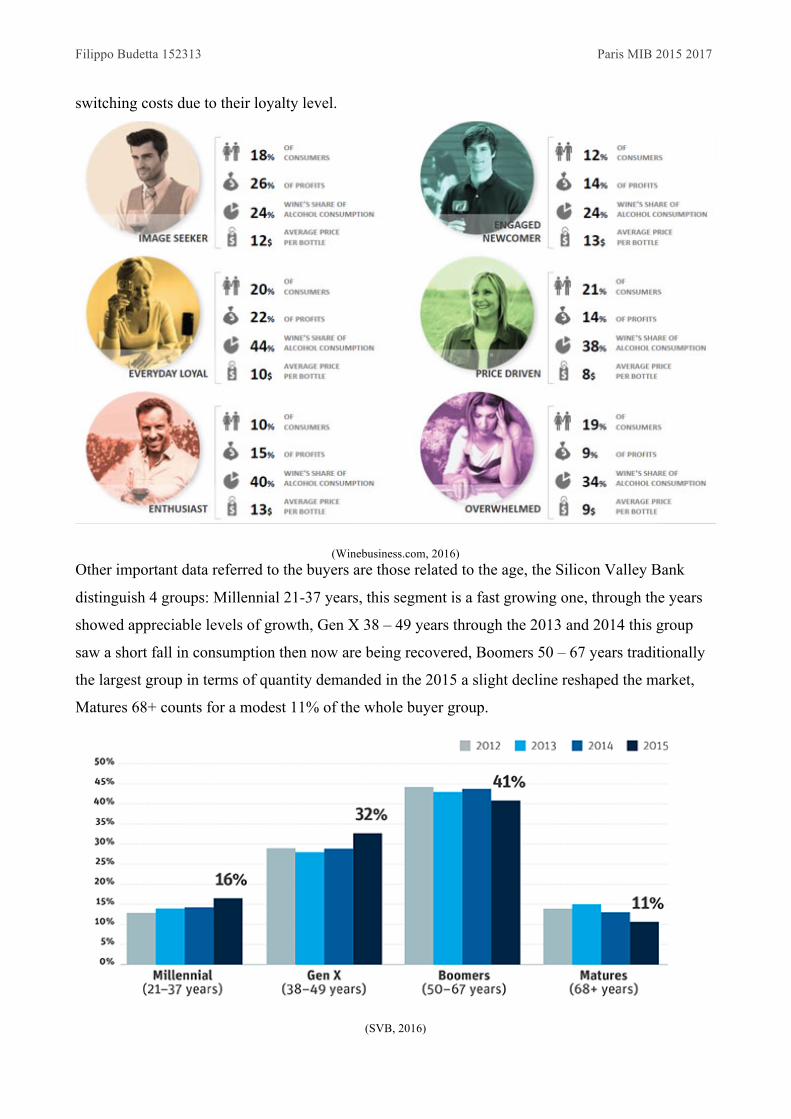

(Winebusiness.com, 2016) Other important data referred to the buyers are those related to the age, the Silicon Valley Bank

distinguish 4 groups: Millennial 21-37 years, this segment is a fast growing one, through the years

showed appreciable levels of growth, Gen X 38 – 49 years through the 2013 and 2014 this group

saw a short fall in consumption then now are being recovered, Boomers 50 – 67 years traditionally

the largest group in terms of quantity demanded in the 2015 a slight decline reshaped the market,

Matures 68+ counts for a modest 11% of the whole buyer group.

(SVB, 2016)

Filippo Budetta 152313 Paris MIB 2015 2017

Product features

The “old world” wineries should be afraid of the competitiveness brought to the markets by

company belonging to the “new world”, wines coming from the states and from Australia are

becoming more and more sophisticated and really alike to those European. Indeed, that this may

erode the selling proposition of the Italian and French company that might lost important market

shares. On the other hand, it has to be said that thanks to a long heritage the European wines are

inimitable and the European products keep on showing very different features maintaining the

different products considerably different from each other.

Research &Development role within the wine industry

Generally speaking, the wine has a really long life cycle, actually being aged represents a

distinction for a bottle of wine rather than a demerit. A winery quality is mainly based on traditions

and heritage rather than innovation and research.

In spite of this, in Australia one of the fastest growing wine market in the world have been founded

two institutes: The Australian Wine Research Institute and the Cooperative Research Centre for

Viticulture. The first aims to “carry out applied research and to service the needs of winemakers, be

involved in both undergraduate and postgraduate teaching and to coordinate information on

oenology and viticulture research to the benefit of the Australian wine industry” (Ro.uow.edu.au,

2016). The latter is more concerned about biotechnology research into grape quality improvement,

viticulture, education and technology transfer.

Therefore, is clear enough that “the coordination of this R&D has ensured that the industry remains

at the leading edge”(Aylward, 2016) and may be focal for achieve new goal.

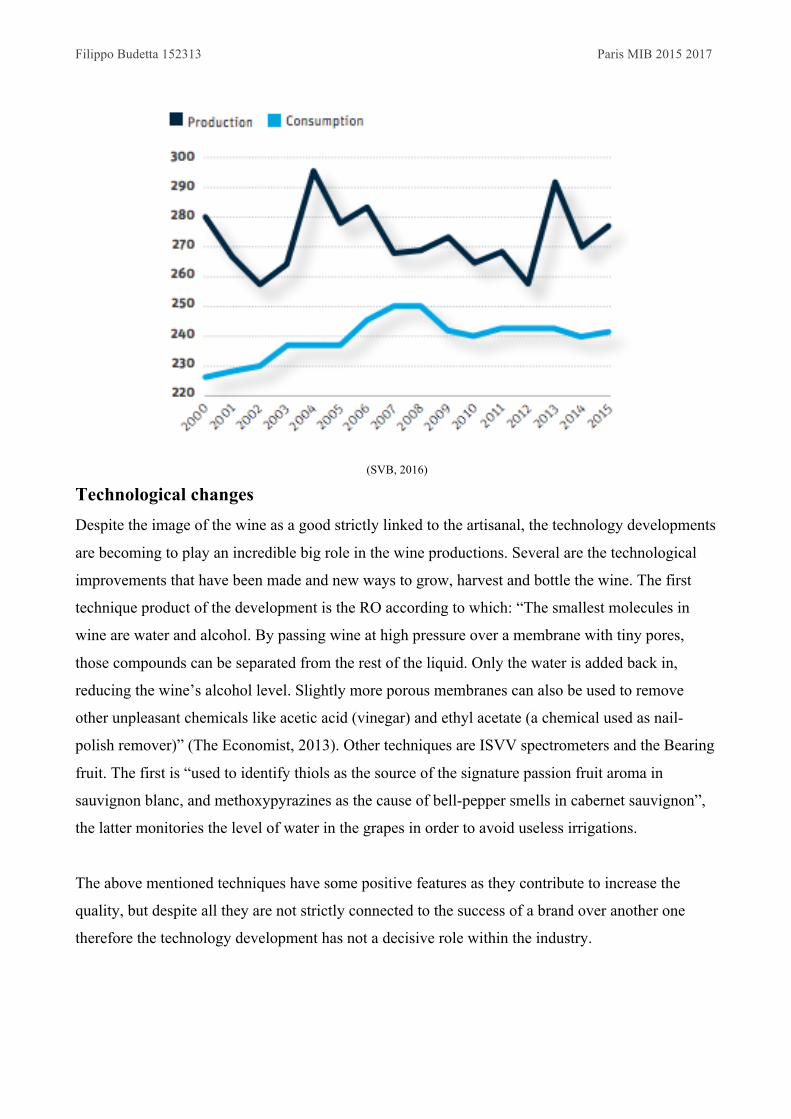

Supply and demand conditions Really districted is the supply and demand condition as in the early years of 90s, the governments

used to buy the fermented grapes unsold to make industrial ethanol. This largely justifying the

extreme abundance in production, that has been later interrupt when the EU realized the disastrous

effects of this oversupply that was levelling out the prices to shortest prices ever.

To face this phenomenon in the 2007 the EU paid growers to “uproot 175,000 hectares (about

430,000 acres) of economically unsustainable and lesser-quality vineyards and decrease the

production” (SVB, 2016). In 2013 the productions rose again as consequence of the emerging of the

new producing countries and there is no doubt that this brought to a new decrease in prices that are

becoming lower and lower.

Filippo Budetta 152313 Paris MIB 2015 2017

(SVB, 2016)

Technological changes Despite the image of the wine as a good strictly linked to the artisanal, the technology developments

are becoming to play an incredible big role in the wine productions. Several are the technological

improvements that have been made and new ways to grow, harvest and bottle the wine. The first

technique product of the development is the RO according to which: “The smallest molecules in

wine are water and alcohol. By passing wine at high pressure over a membrane with tiny pores,

those compounds can be separated from the rest of the liquid. Only the water is added back in,

reducing the wine’s alcohol level. Slightly more porous membranes can also be used to remove

other unpleasant chemicals like acetic acid (vinegar) and ethyl acetate (a chemical used as nail-

polish remover)” (The Economist, 2013). Other techniques are ISVV spectrometers and the Bearing

fruit. The first is “used to identify thiols as the source of the signature passion fruit aroma in

sauvignon blanc, and methoxypyrazines as the cause of bell-pepper smells in cabernet sauvignon”,

the latter monitories the level of water in the grapes in order to avoid useless irrigations.

The above mentioned techniques have some positive features as they contribute to increase the

quality, but despite all they are not strictly connected to the success of a brand over another one

therefore the technology development has not a decisive role within the industry.

Filippo Budetta 152313 Paris MIB 2015 2017

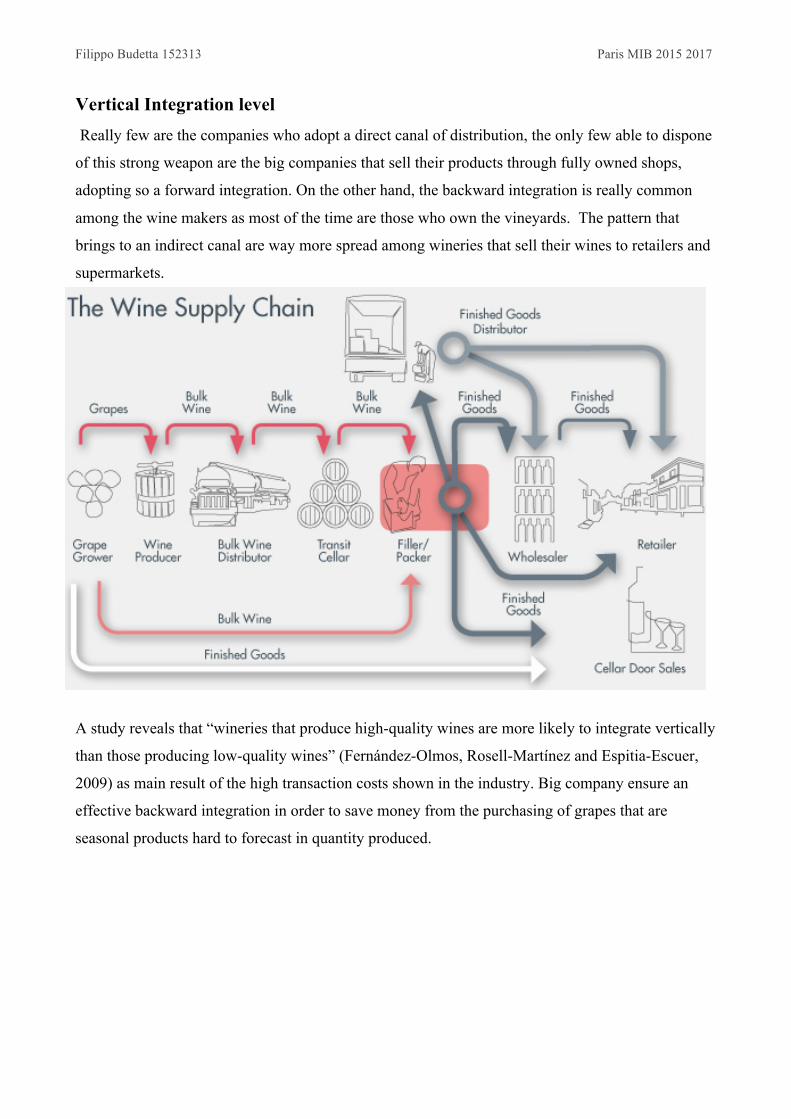

Vertical Integration level Really few are the companies who adopt a direct canal of distribution, the only few able to dispone

of this strong weapon are the big companies that sell their products through fully owned shops,

adopting so a forward integration. On the other hand, the backward integration is really common

among the wine makers as most of the time are those who own the vineyards. The pattern that

brings to an indirect canal are way more spread among wineries that sell their wines to retailers and

supermarkets.

A study reveals that “wineries that produce high-quality wines are more likely to integrate vertically

than those producing low-quality wines” (Fernández-Olmos, Rosell-Martínez and Espitia-Escuer,

2009) as main result of the high transaction costs shown in the industry. Big company ensure an

effective backward integration in order to save money from the purchasing of grapes that are

seasonal products hard to forecast in quantity produced.

Filippo Budetta 152313 Paris MIB 2015 2017

Economies of scales

The economies of scale in the wine industry are a spread issue as the quality is significantly more

important than quantity, therefore the price may vary regardless the effective kilos sold. In spite of

this assumption, researchers came out with a model that explains the attractiveness of the economy

of scales referred to one company producing just one type of wine.

(DELORD, COELHO and MONTAIGNE, 2014)

They come up with several conclusions that allow the wine maker to save resources, as unit labour

cost decrease and the productivity of labour increase. The study remains anyway at a theatrical

stage as unpredictable are most of the data taken into account as well as other important variables

ignored.

Changyu winery The Changyu winery is the China’s oldest and most famous winery has a strong heritage with a

foundation dated back in 1892 by Zhangn Bishi. The company is one of the most famous in the

world as confirmed by the chart of the top 10 brands, at March 2016 the revenues accounts for the

remarkable number of 2.12 billion (Quotes.wsj.com, 2016).

Filippo Budetta 152313 Paris MIB 2015 2017

The Chinese winery is benefitting from the success that is having the Chinese wine in the

international markets as well as in the domestic one. Moreover, it dispones of a good return of

image as it embodies the Chinese passions for the spirits as well as an incredible R&D dept. and

well developed brewing equipment. All the efforts of the companies are then combined thanks to

the precious contribution of famous internationally famous wine makers such as: Augusto Reina,

Lenz Moser and John Umberto Salvi.

The revenues are sustained by the strong domestic demand that is living a profitable period in

which Chinese consumers are getting significantly interested by the wine world. “Domestic

production has increased 4x over the past decade, and is now the fifth largest producer of wine

globally. The majority of production occurs in the North East provinces, which are largely in line

with Mediterranean Europe and Californian growing regions” (Morgan Stanley Research, 2013).

The consumption is expected to further grow and the Chinese wineries aware of this eventuality are

ready to satisfy the large demand of over 400 million unit of cases. The market is perfectly balanced

as the production meet perfectly the demand, other signal that tells about the good knowledge of the

Chinese wineries of the domestic markets.

(Morgan Stanley Research, 2013)

On the other hand, significant are the efforts that the company has to put in defeating the foreign

supply, infect as seen in the previous chapter China imports a consistent part of the wine from

Europe. This means that the company has to convince its customers that the Chinese merlots are at

the same level of the European ones. The performances related to this companies are positive and

they are confirmed by the financial data, nevertheless in a market where the tradition is strongly

Filippo Budetta 152313 Paris MIB 2015 2017

influencing the board management through the marketing has to take the heritage to another step the

one of the myth.

Cantina Valentini Trebbiano

With a long tradition dated back in 1856 the cantina Valentini is most probably one of the most

famous Italian name related to the wine, the winery has the typical feature of a family business and

the employees hardly reach the number of 15. The cantina produces some of the finest wine in the

world known for their inimitable quality as well as high prices, infect a bottle of 2010 Trebbiano

d'Abruzzo worth £74,95 while the case £404,70 as reports by BERRY BROS & RUDD Wine

merchant.

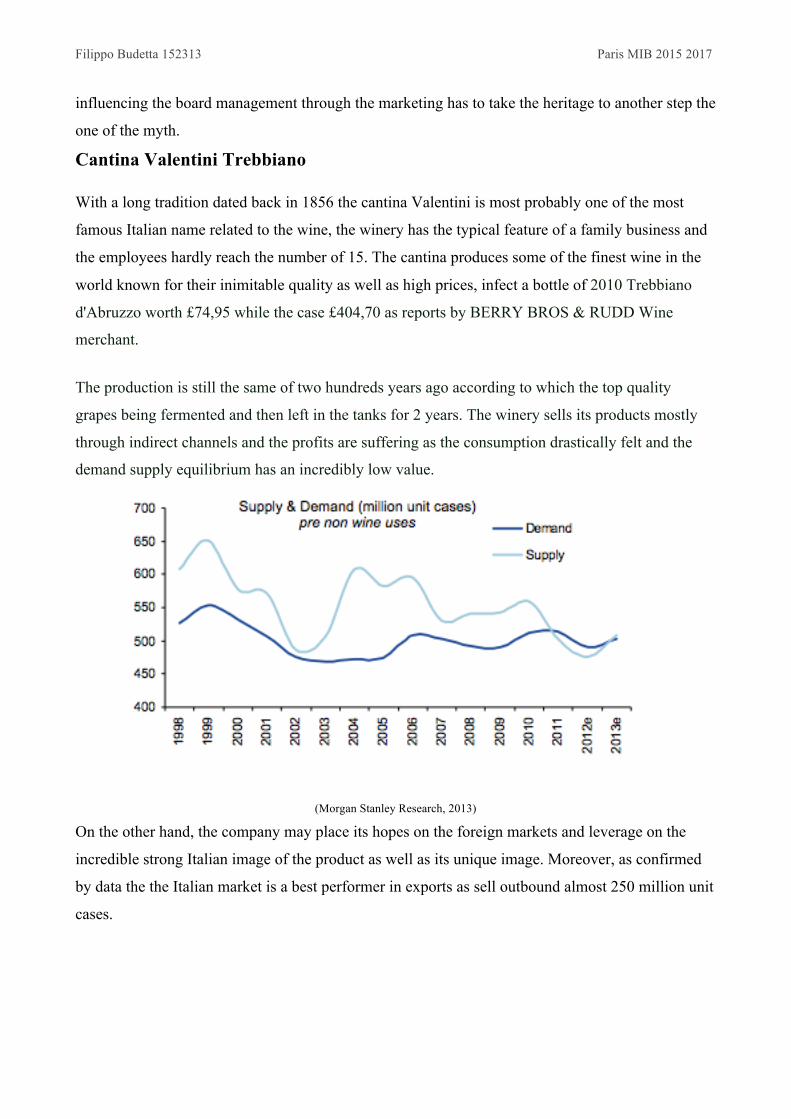

The production is still the same of two hundreds years ago according to which the top quality

grapes being fermented and then left in the tanks for 2 years. The winery sells its products mostly

through indirect channels and the profits are suffering as the consumption drastically felt and the

demand supply equilibrium has an incredibly low value.

(Morgan Stanley Research, 2013)

On the other hand, the company may place its hopes on the foreign markets and leverage on the

incredible strong Italian image of the product as well as its unique image. Moreover, as confirmed

by data the the Italian market is a best performer in exports as sell outbound almost 250 million unit

cases.

Filippo Budetta 152313 Paris MIB 2015 2017

(Morgan Stanley Research, 2013)

Indeed, the company has to review its business as well as its marketing strategy, starting from

developing a web site and a store in one of the fastest growing market.

Filippo Budetta 152313 Paris MIB 2015 2017

References

Plantandfood.co.nz. (2016). Growing Futures: Wine Industry. [online] Available at: http://www.plantandfood.co.nz/growingfutures/wine [Accessed 25 May 2016].

Morgan Stanley Research, (2013). The Global Wine Industry. [online] Available at: http://blogs.reuters.com/counterparties/files/2013/10/Global-Wine-Shortage.pdf [Accessed 25 May 2016].

BNP paribas, (2015). New producers, new consumers: The revolution of the global wine market | Bank BNP Paribas. [online] Bnpparibas.com. Available at: http://www.bnpparibas.com/en/news/press-release/new-producers-new-consumers-revolution-global-wine-market [Accessed 25 May 2016].

Wine production worldwide in 2015, c. (2016). Leading countries in global wine production, 2015 | Statistic. [online] Statista. Available at: http://www.statista.com/statistics/240638/wine-production-in-selected-countries-and-regions/ [Accessed 25 May 2016].

SVB, (2016). 2016 SVB Wine Report. [online] Svb.com. Available at: http://www.svb.com/wine-report/ [Accessed 26 May 2016]. Forbes.com. (2016). Forbes Welcome. [online] Available at: http://www.forbes.com/companies/ej-gallo-winery/ [Accessed 26 May 2016]. http://www.include-digital.com, I. (2016). Best Global Brands | Brand Profiles & Valuations of the World’s Top Brands. [online] Brandirectory.com. Available at: http://brandirectory.com/league_tables/table/top-10-wine-brands-2013 [Accessed 26 May 2016].

Winebusiness.com. (2016). Constellation Segmentation Study Outlines Motivations, Behaviors of .... [online] Available at: http://www.winebusiness.com/news/?go=getArticle&dataid=134683 [Accessed 27 May 2016].

Ro.uow.edu.au. (2016). [online] Available at: http://ro.uow.edu.au/cgi/viewcontent.cgi?article=1085&context=commpapers [Accessed 27 May 2016].

Aylward, D. (2016). Diffusion of R&D within the Australian Wine Industry. Prometheus. [online] Available at: http://www.tandfonline.com/doi/abs/10.1080/0810902021000023345?journalCode=cpro20 [Accessed 27 May 2016].

Filippo Budetta 152313 Paris MIB 2015 2017

The Economist. (2013). Bacchus to the future. [online] Available at: http://www.economist.com/news/technology-quarterly/21590767-high-tech-winemaking-technology-has-already-made-poor-plonk-thing-past [Accessed 27 May 2016].

Fernández-Olmos, M., Rosell-Martínez, J. and Espitia-Escuer, M. (2009). Vertical integration in the wine industry: a transaction costs analysis on the Rioja DOCa. Agribusiness, 25(2), pp.231-250.

DELORD, B., COELHO, A. and MONTAIGNE, É. (2014). [online] Available at: http://academyofwinebusiness.com/wp-content/uploads/2014/07/BM09_Coelho_Alfredo.pdf [Accessed 27 May 2016].

Quotes.wsj.com. (2016). 000869.CN Financial Statements - Yantai Changyu Pioneer Wine Co. Ltd. A - Wall Street Journal. [online] Available at: http://quotes.wsj.com/CN/XSHE/000869/financials [Accessed 27 May 2016].