Wind power in Central America - platts.com · Wind power in Central America Platts Conference June...

14

Wind power in Central America Platts Conference June 2012 Jay Gallegos, Managing Director, Globeleq Mesoamerica Energy

Transcript of Wind power in Central America - platts.com · Wind power in Central America Platts Conference June...

Wind power in Central America

Platts Conference June 2012

Jay Gallegos, Managing Director, Globeleq Mesoamerica Energy

This information is confidential and was prepared by Mesoamerica Investments solely for the use of our client; it is not to be relied on by any 3rd party without Mesoamerica's prior written consent.

• GME is the leading company in the development and operation of wind energy projects in Central America

- 23 wind MW operating in Costa Rica since 1996 (Plantas Eolicas, SRL-PESRL)

- 102 wind MW operating in Honduras since 2011 (Cerro de Hula)

- 44 MW under construction in Nicaragua – COD December 2012 (Eolo)

- 50 MW awarded – Costa Rica

- Over 140 professionals with experience in project development and O&M

• Founded by Mesoamerica Investments in 2004 with the acquisition of Plantas Eólicas SRL in Costa Rica

• Globeleq acquires 70% of the company in 2010

Globeleq Mesoamerica Energy

This information is confidential and was prepared by Mesoamerica Investments solely for the use of our client; it is not to be relied on by any 3rd party without Mesoamerica's prior written consent.

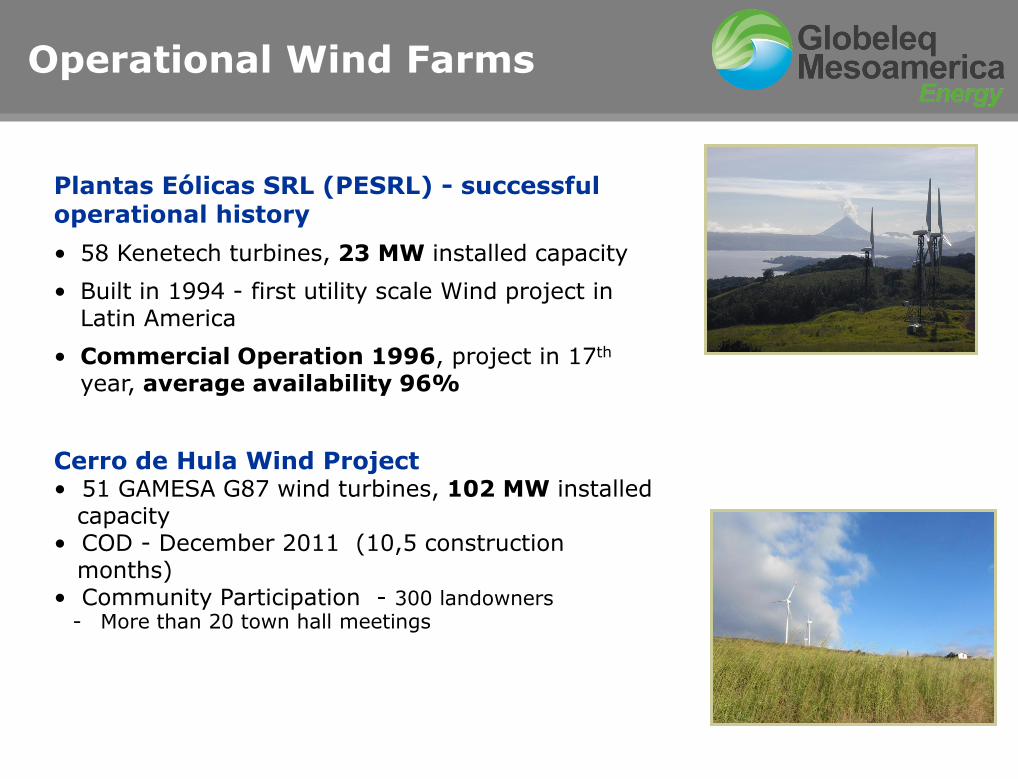

Operational Wind Farms

Plantas Eólicas SRL (PESRL) - successful operational history

• 58 Kenetech turbines, 23 MW installed capacity

• Built in 1994 - first utility scale Wind project in Latin America

• Commercial Operation 1996, project in 17th year, average availability 96%

Cerro de Hula Wind Project • 51 GAMESA G87 wind turbines, 102 MW installed

capacity • COD - December 2011 (10,5 construction

months) • Community Participation - 300 landowners

- More than 20 town hall meetings

This information is confidential and was prepared by Mesoamerica Investments solely for the use of our client; it is not to be relied on by any 3rd party without Mesoamerica's prior written consent.

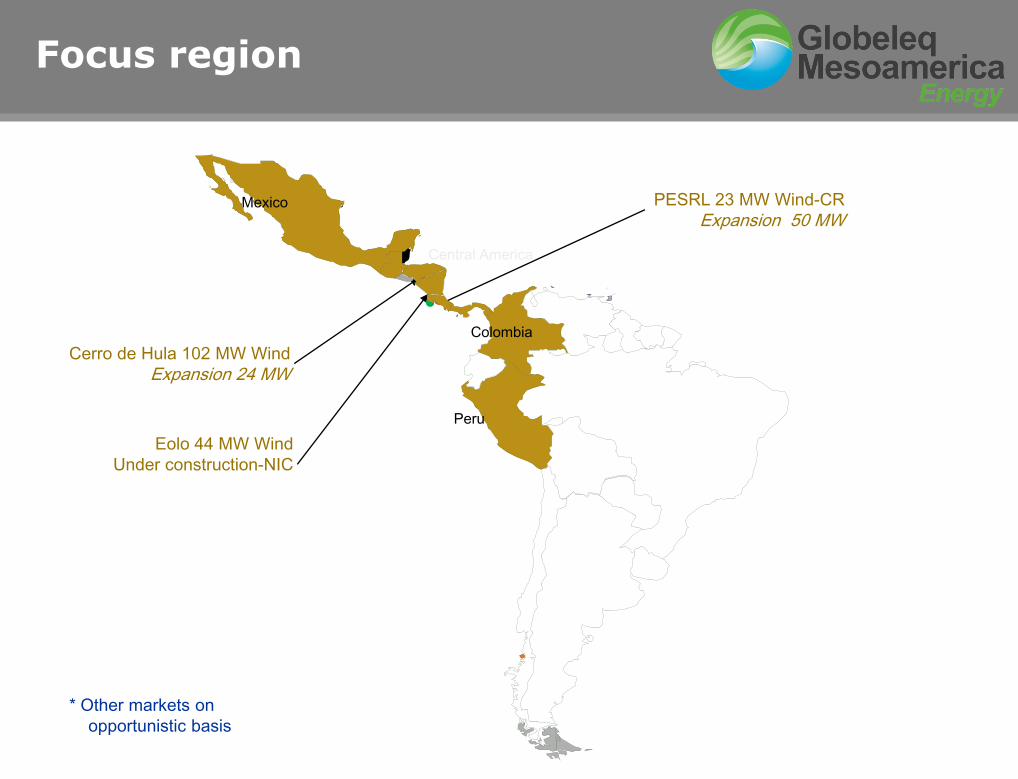

PESRL 23 MW Wind-CR

Expansion 50 MW

Cerro de Hula 102 MW Wind

Expansion 24 MW

Eolo 44 MW Wind

Under construction-NIC

Focus region

Central America

Mexico

Peru

Colombia

* Other markets on

opportunistic basis

This information is confidential and was prepared by Mesoamerica Investments solely for the use of our client; it is not to be relied on by any 3rd party without Mesoamerica's prior written consent.

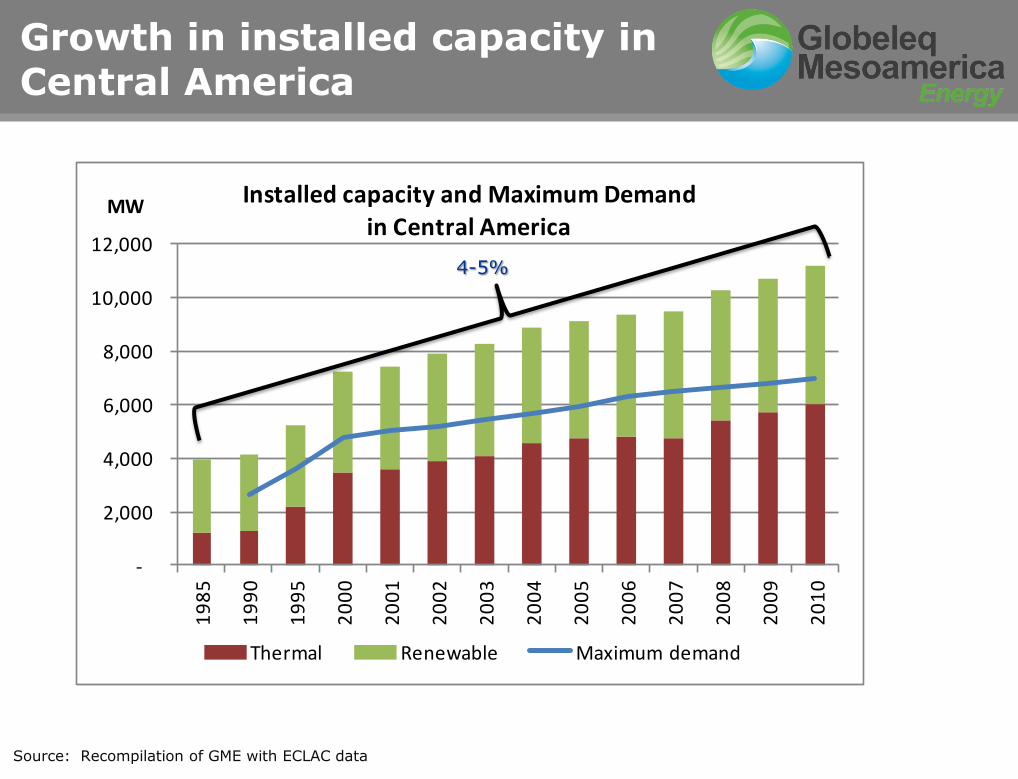

Growth in installed capacity in Central America

Source: Recompilation of GME with ECLAC data

-

2,000

4,000

6,000

8,000

10,000

12,000

19

85

19

90

19

95

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

MWInstalled capacity and Maximum Demand

in Central America

Thermal Renewable Maximum demand

4-5%

This information is confidential and was prepared by Mesoamerica Investments solely for the use of our client; it is not to be relied on by any 3rd party without Mesoamerica's prior written consent.

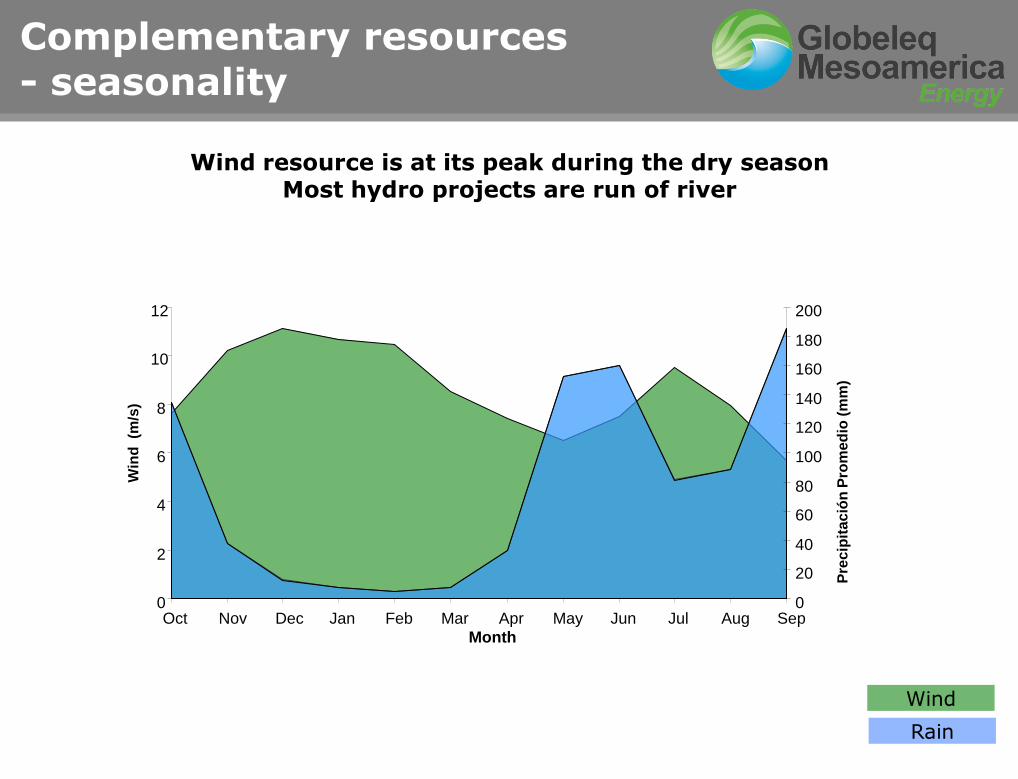

0

2

4

6

8

10

12

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Month

Win

d (m

/s)

0

20

40

60

80

100

120

140

160

180

200

Pre

cip

ita

ció

n P

rom

ed

io (

mm

)

Wind

Rain

Complementary resources

- seasonality

Wind resource is at its peak during the dry season Most hydro projects are run of river

This information is confidential and was prepared by Mesoamerica Investments solely for the use of our client; it is not to be relied on by any 3rd party without Mesoamerica's prior written consent.

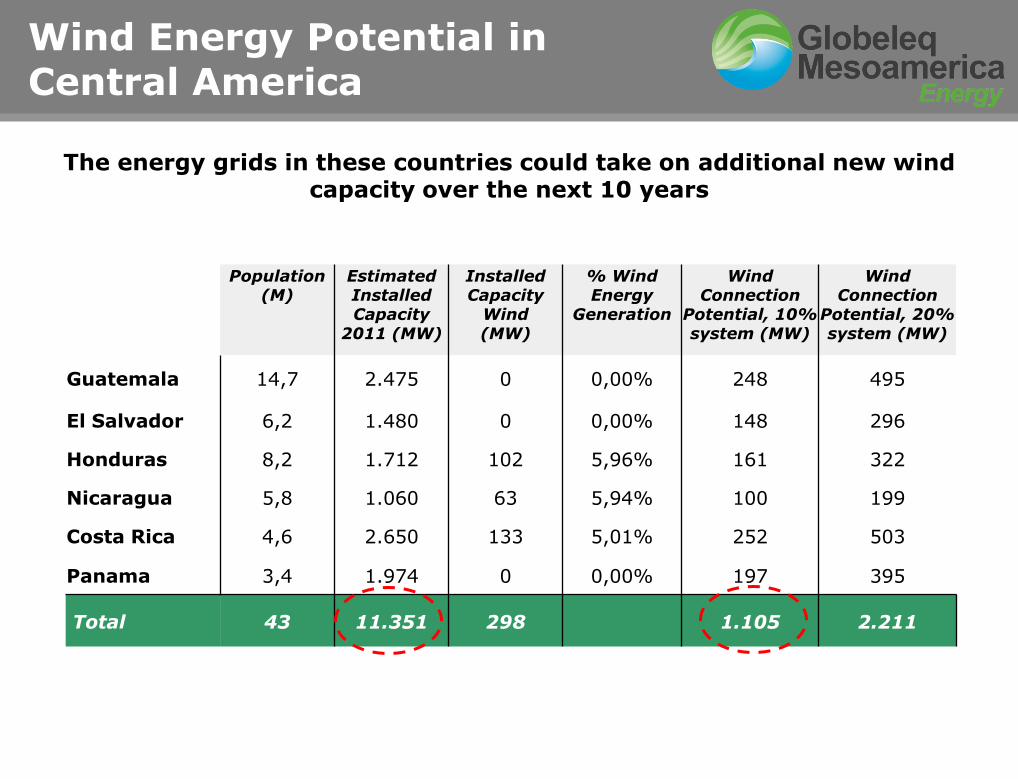

Wind Energy Potential in Central America

Population (M)

Estimated Installed Capacity

2011 (MW)

Installed Capacity

Wind (MW)

% Wind Energy

Generation

Wind Connection

Potential, 10% system (MW)

Wind Connection

Potential, 20% system (MW)

Guatemala 14,7 2.475 0 0,00% 248 495

El Salvador 6,2 1.480 0 0,00% 148 296

Honduras 8,2 1.712 102 5,96% 161 322

Nicaragua 5,8 1.060 63 5,94% 100 199

Costa Rica 4,6 2.650 133 5,01% 252 503

Panama 3,4 1.974 0 0,00% 197 395

Total 43 11.351 298 1.105 2.211

The energy grids in these countries could take on additional new wind capacity over the next 10 years

This information is confidential and was prepared by Mesoamerica Investments solely for the use of our client; it is not to be relied on by any 3rd party without Mesoamerica's prior written consent.

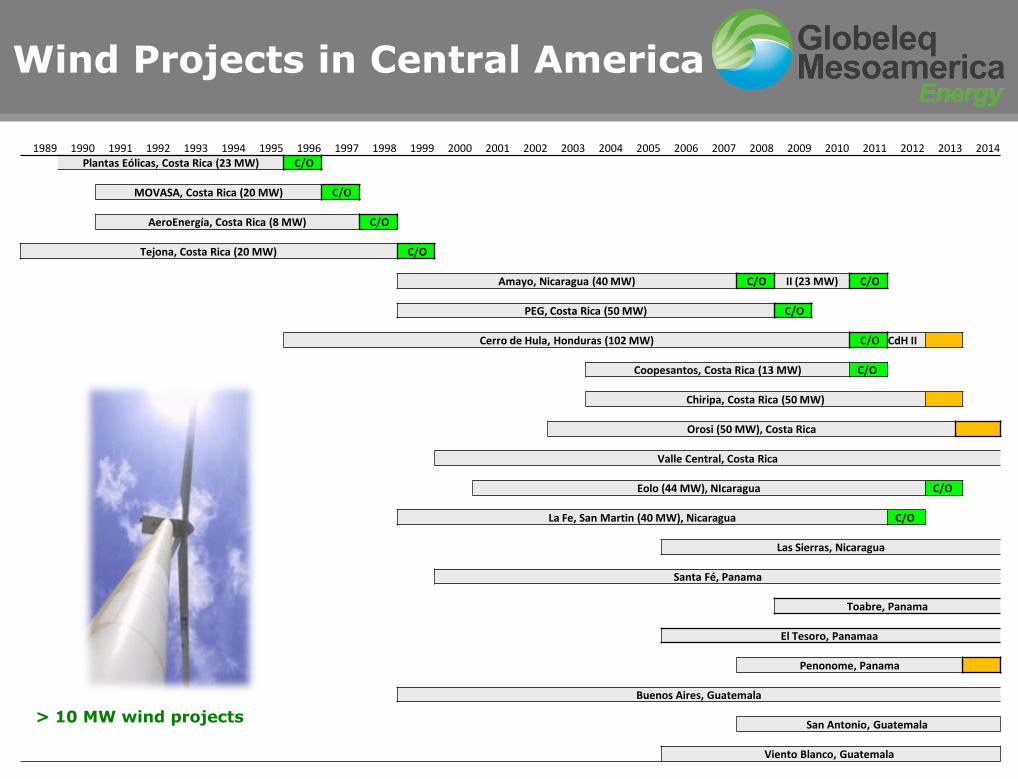

Wind Projects in Central America

> 10 MW wind projects

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 Plantas Eólicas, Costa Rica (23 MW) C/O

MOVASA, Costa Rica (20 MW) C/O

AeroEnergía, Costa Rica (8 MW) C/O

Tejona, Costa Rica (20 MW) C/O

Amayo, Nicaragua (40 MW) C/O II (23 MW) C/O

PEG, Costa Rica (50 MW) C/O

Cerro de Hula, Honduras (102 MW) C/O CdH II

Coopesantos, Costa Rica (13 MW) C/O

Chiripa, Costa Rica (50 MW)

Orosi (50 MW), Costa Rica

Valle Central, Costa Rica

Eolo (44 MW), NIcaragua C/O

La Fe, San Martin (40 MW), Nicaragua C/O

Las Sierras, Nicaragua

Santa Fé, Panama

Toabre, Panama

El Tesoro, Panamaa

Penonome, Panama

Buenos Aires, Guatemala

San Antonio, Guatemala

Viento Blanco, Guatemala

This information is confidential and was prepared by Mesoamerica Investments solely for the use of our client; it is not to be relied on by any 3rd party without Mesoamerica's prior written consent.

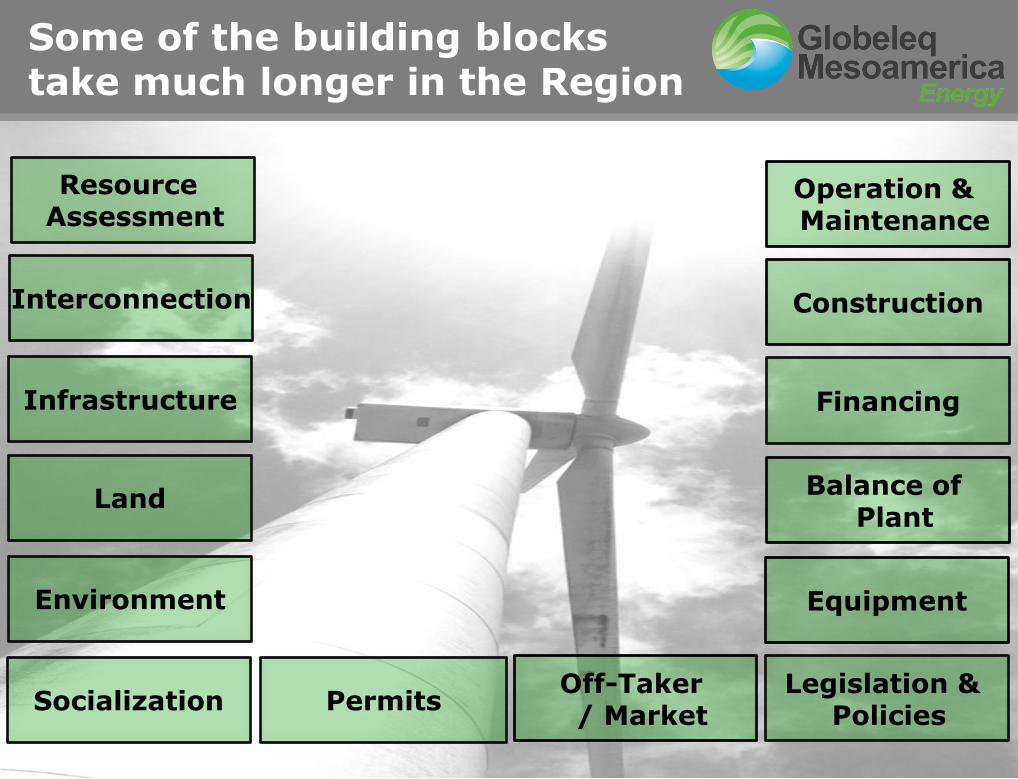

Resource Assessment

Some of the building blocks take much longer in the Region

Permits

Infrastructure

Land

Socialization

Environment

Off-Taker / Market

Interconnection Construction

Operation & Maintenance

Financing

Balance of Plant

Equipment

Legislation & Policies

This information is confidential and was prepared by Mesoamerica Investments solely for the use of our client; it is not to be relied on by any 3rd party without Mesoamerica's prior written consent.

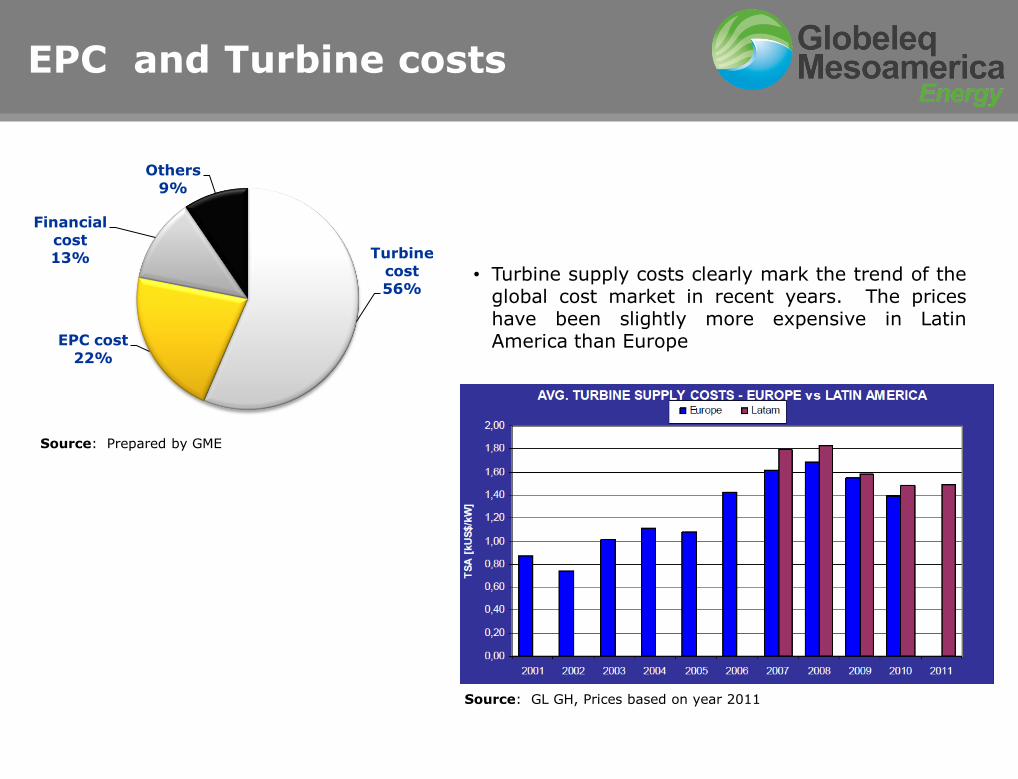

EPC and Turbine costs

Turbine

cost 56%

EPC cost

22%

Financial

cost 13%

Others

9%

Source: Prepared by GME

Source: GL GH, Prices based on year 2011

• Turbine supply costs clearly mark the trend of the global cost market in recent years. The prices have been slightly more expensive in Latin America than Europe

This information is confidential and was prepared by Mesoamerica Investments solely for the use of our client; it is not to be relied on by any 3rd party without Mesoamerica's prior written consent.

Regional risks and effects

• Wind risk & Grid stability

Limited long term references Increase uncertainly on energy production Grid penetration issues

• Social:

Land title Opposition Groups Opportunism

• Delay of Financial close:

Project finance due diligence challenges Offtaker creditworthiness Land and social issues Insurance Permitting process transparency

This information is confidential and was prepared by Mesoamerica Investments solely for the use of our client; it is not to be relied on by any 3rd party without Mesoamerica's prior written consent.

Regional risks and effects

• EPC

Delays in notice to proceed to EPC contractor

LNTP

Weather

Larger project execution teams required

Local contractor mobilization

Shipping & Customs

• Others:

Security

Implementation of renewable incentives

Change in Law clause weaknesses

This information is confidential and was prepared by Mesoamerica Investments solely for the use of our client; it is not to be relied on by any 3rd party without Mesoamerica's prior written consent.

Conclusions

• More wind and social risk

• EPC more expensive

• Require greater owner involvement

• Security

• More difficult to achieve financial close

• Implementation of incentives not easy

• Difficult to enforce change in law provision

Impacts to IRR

This information is confidential and was prepared by Mesoamerica Investments solely for the use of our client; it is not to be relied on by any 3rd party without Mesoamerica's prior written consent.

Thank you!

www.GlobeleqMesoamericaEnergy.com

Tel: +506 2228-9300