Wind Energy Update Larry Flowers National Renewable Energy Laboratory December 13, 2007 Ag Outreach...

50

Wind Energy Update Wind Energy Update Larry Flowers Larry Flowers National Renewable Energy Laboratory National Renewable Energy Laboratory December 13, 2007 December 13, 2007 Ag Outreach Webcast Ag Outreach Webcast

-

date post

19-Dec-2015 -

Category

Documents

-

view

219 -

download

2

Transcript of Wind Energy Update Larry Flowers National Renewable Energy Laboratory December 13, 2007 Ag Outreach...

Wind Energy UpdateWind Energy Update

Larry Flowers Larry Flowers National Renewable Energy Laboratory National Renewable Energy Laboratory

December 13, 2007December 13, 2007Ag Outreach WebcastAg Outreach Webcast

2

People Want Renewable Energy!People Want Renewable Energy!

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

55000

60000

65000

70000

75000

80000

85000

Ca

pa

cit

y (

MW

)

United States Europe Rest of World

1. Germany: 21283 MW2. Spain: 13400 MW3. United States: 13223 MW 4. India: 7000 MW5. Denmark: 3134 MW

Source: WindPower Monthly

World total Oct 2007: 82,255 MW

Total Installed Wind CapacityTotal Installed Wind Capacity

3

U.S. Leads World in Annual Wind U.S. Leads World in Annual Wind Capacity Additions; Third in Cumulative CapacityCapacity Additions; Third in Cumulative Capacity

4

U.S Lagging Other Countries for U.S Lagging Other Countries for Wind As a Percentage of Electricity ConsumptionWind As a Percentage of Electricity Consumption

5

Installed Wind Capacities Installed Wind Capacities (‘99 – Oct 07)(‘99 – Oct 07)

6

Drivers for Wind PowerDrivers for Wind Power

• Declining Wind Costs• Fuel Price Uncertainty• Federal and State

Policies• Economic Development• Public Support• Green Power• Energy Security• Carbon Risk

7

Wind Cost of EnergyWind Cost of Energy

0

2

4

6

8

10

12

14

1990 1995 2000 2005 2010 2015 2020

CO

E (

¢/k

Wh

[c

on

sta

nt

20

06

$])

Low wind speed sites

High windspeed sites

Depreciated Coal

Depreciated Wind

New Coal

2006: New Wind

Natural Gas (fuel only)

2007: New Wind

Copper & Steel Price Source: World Bank, Commodity Price Data

Wind Cost Wind Cost DriversDrivers

9

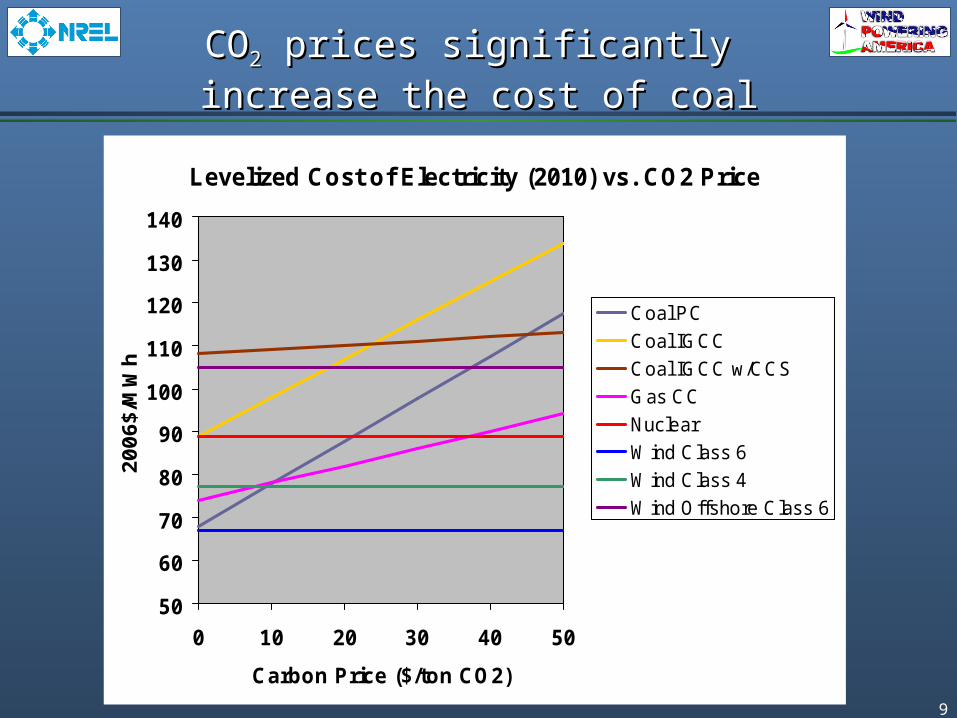

COCO22 prices significantly prices significantly

increase the cost of coalincrease the cost of coal

Levelized Cost of Electricity (2010) vs. CO2 Price

50

60

70

80

90

100

110

120

130

140

0 10 20 30 40 50

Carbon Price ($/ton CO2)

20

06

$/M

Wh

Coal PC

Coal IGCC

Coal IGCC w/CCS

Gas CC

Nuclear

Wind Class 6

Wind Class 4

Wind Offshore Class 6

10

Major Market Distortion: External Costs Major Market Distortion: External Costs of Fossil Fuels not Reflected in Pricingof Fossil Fuels not Reflected in Pricing

(The PTCs are a bargain)(The PTCs are a bargain)

11

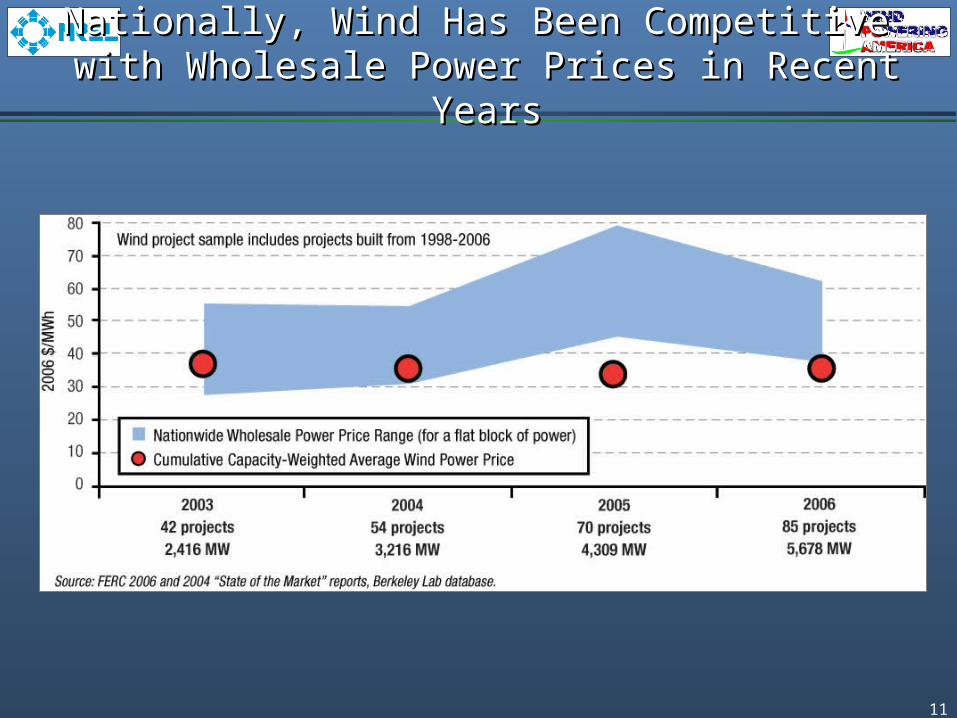

Nationally, Wind Has Been Competitive Nationally, Wind Has Been Competitive with Wholesale Power Prices in Recent Yearswith Wholesale Power Prices in Recent Years

12

In 2006, Wind Projects Built Since 1997 Were In 2006, Wind Projects Built Since 1997 Were Competitive with Wholesale Power Prices in Most RegionsCompetitive with Wholesale Power Prices in Most Regions

13

Renewables Portfolio StandardsRenewables Portfolio Standards

☼ Minimum solar or customer-sited RE requirement* Increased credit for solar or customer-sited RE

¹PA: 8% Tier I / 10% Tier II (includes non-renewables); SWH is a Tier II resourceDSIRE: www.dsireusa.org

September 2007

☼ PA: 18%¹ by 2020

☼ NJ: 22.5% by 2021

CT: 23% by 2020

MA: 4% by 2009 +1% annual increase

WI: requirement varies by utility; 10% by 2015 goal

IA: 105 MW

MN: 25% by 2025(Xcel: 30% by 2020)

TX: 5,880 MW by 2015

☼ AZ: 15% by 2025

CA: 20% by 2010

☼ *NV: 20% by 2015

ME: 30% by 200010% by 2017 - new RE

HI: 20% by 2020

RI: 16% by 2020

☼ CO: 20% by 2020 (IOUs)*10% by 2020 (co-ops & large munis)

☼ DC: 11% by 2022

☼ NY: 24% by 2013

MT: 15% by 2015

IL: 25% by 2025

VT: RE meets load growth by 2012*WA: 15% by 2020

☼ MD: 9.5% in 2022

☼ NH: 23.8% in 2025

OR: 25% by 2025 (large utilities)5% - 10% by 2025 (smaller utilities)

*VA: 12% by 2022

MO: 11% by 2020

☼ *DE: 20% by 2019

☼ NM: 20% by 2020 (IOUs)10% by 2020 (co-ops)

☼ NC: 12.5% by 2021 (IOUs)10% by 2018 (co-ops & munis)

ND: 10% by 2015

State Goal

State RPS

Solar water heating eligible

14

Wind Energy InvestorsWind Energy Investors

15

16

Economic Impacts of Economic Impacts of Alternative GenerationAlternative Generation

Economic impacts of wind vs. coal in Colorado (construction + 20 yrs of operation)

$-

$100

$200

$300

$400

$500

$600

$700

$800

Wind (607 MW) Coal (250 MW fromPRB)

Coal (40% in-state)

Do

llars

in M

illio

ns

Landowner revenue

Property taxes

Coal mining & transport

Operations

Construction

Colorado uses mostly out-of-state coal. But even with in-state coal…

17

Economic Development ImpactsEconomic Development Impacts

• Land Lease Payments: 2-3% of gross revenue $2500-4000/MW/year

• Local property tax revenue: ranges widely - $300K-1700K/yr per 100MW

• 100-200 jobs/100MW during construction

• 6-10 permanent O&M jobs per 100 MW

• Local construction and service industry: concrete, towers usually done locally

18

Case Study: Texas Case Study: Texas

Utilities and wind companies invested $1B in 2001 to build 912 MW of new wind power, resulting in:

• 2,500 quality jobs with a payroll of $75M

• $13.3M in tax revenues for schools and counties

• $2.5M in 2002 royalty income to landowners

• Another 2,900 indirect jobs as a result of the multiplier effect

• $4.6M increase in Pecos County property tax revenue in 2002

19

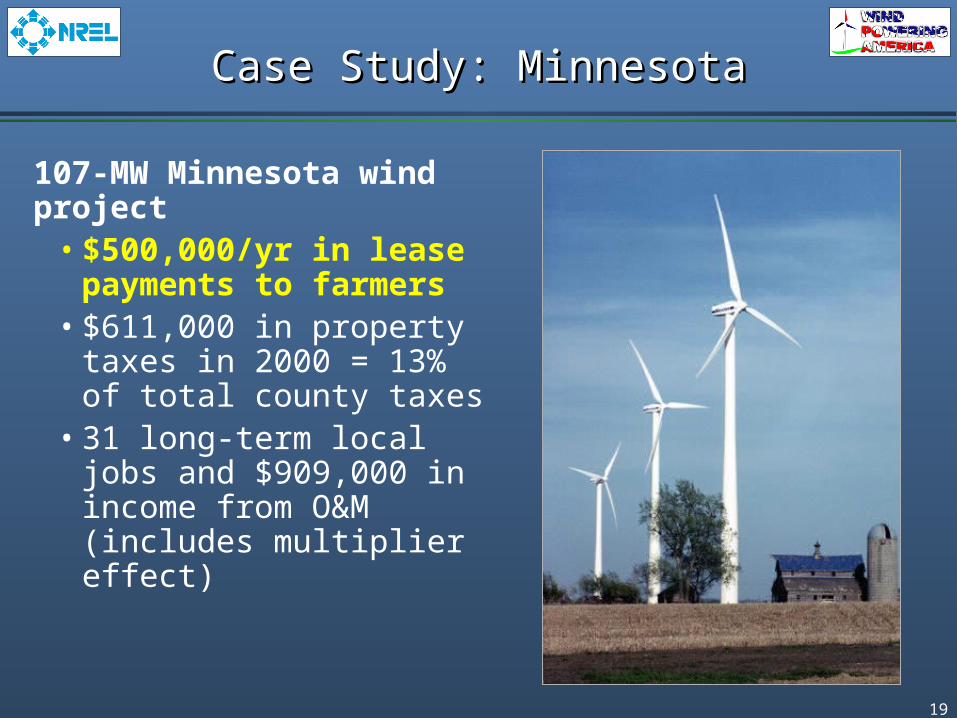

Case Study: MinnesotaCase Study: Minnesota

107-MW Minnesota wind project

• $500,000/yr in lease payments to farmers

• $611,000 in property taxes in 2000 = 13% of total county taxes

• 31 long-term local jobs and $909,000 in income from O&M (includes multiplier effect)

20

Case Study: IowaCase Study: Iowa

240-MW Iowa wind project

• $640,000/yr in lease payments to farmers ($2,000/turbine/yr)

• $2M/yr in property taxes• $5.5M/yr in O&M income• 40 long-term O&M jobs• 200 short-term

construction jobs• Doesn’t include multiplier

effect

21

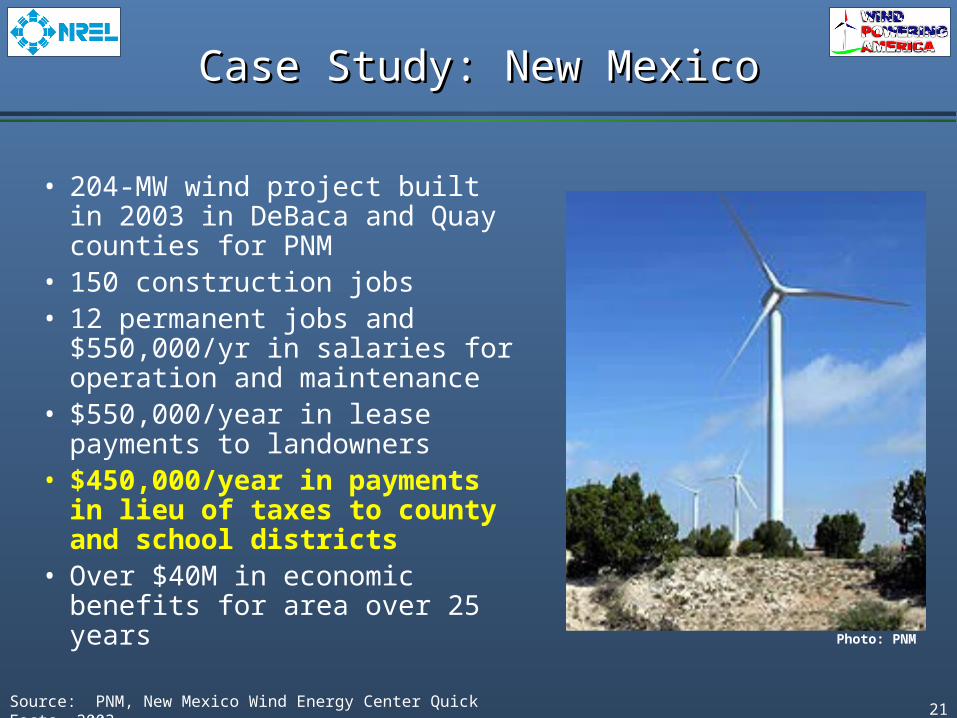

Case Study: New MexicoCase Study: New Mexico

• 204-MW wind project built in 2003 in DeBaca and Quay counties for PNM

• 150 construction jobs• 12 permanent jobs and

$550,000/yr in salaries for operation and maintenance

• $550,000/year in lease payments to landowners

• $450,000/year in payments in lieu of taxes to county and school districts

• Over $40M in economic benefits for area over 25 years

Source: PNM, New Mexico Wind Energy Center Quick Facts, 2003.

Photo: PNM

22

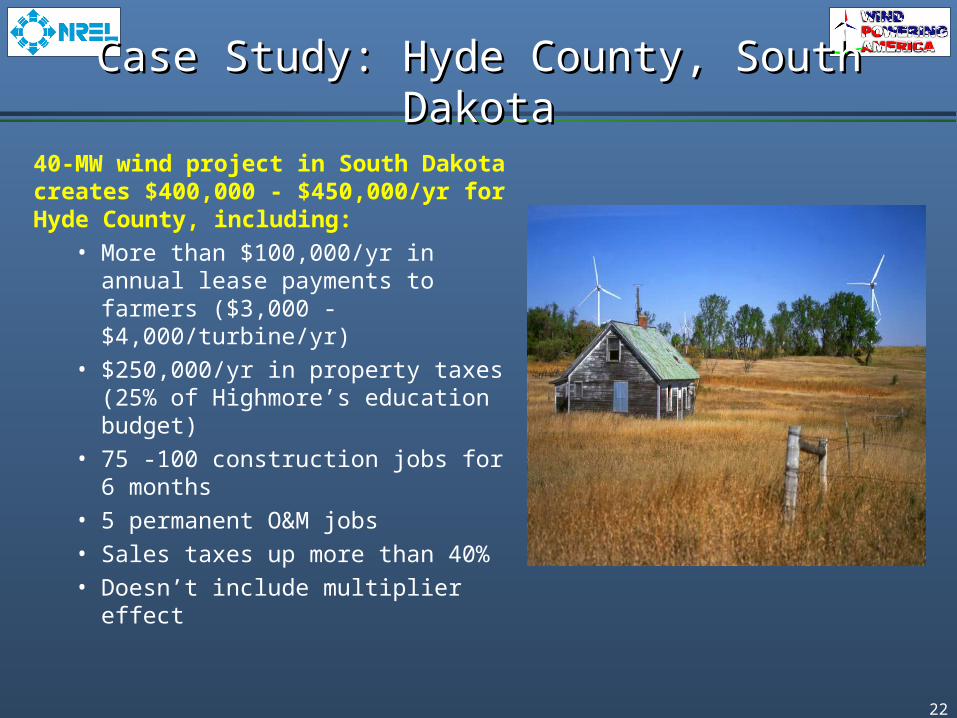

Case Study: Hyde County, South DakotaCase Study: Hyde County, South Dakota

40-MW wind project in South Dakota creates $400,000 - $450,000/yr for Hyde County, including:

• More than $100,000/yr in annual lease payments to farmers ($3,000 - $4,000/turbine/yr)

• $250,000/yr in property taxes (25% of Highmore’s education budget)

• 75 -100 construction jobs for 6 months

• 5 permanent O&M jobs• Sales taxes up more than 40%• Doesn’t include multiplier effect

23

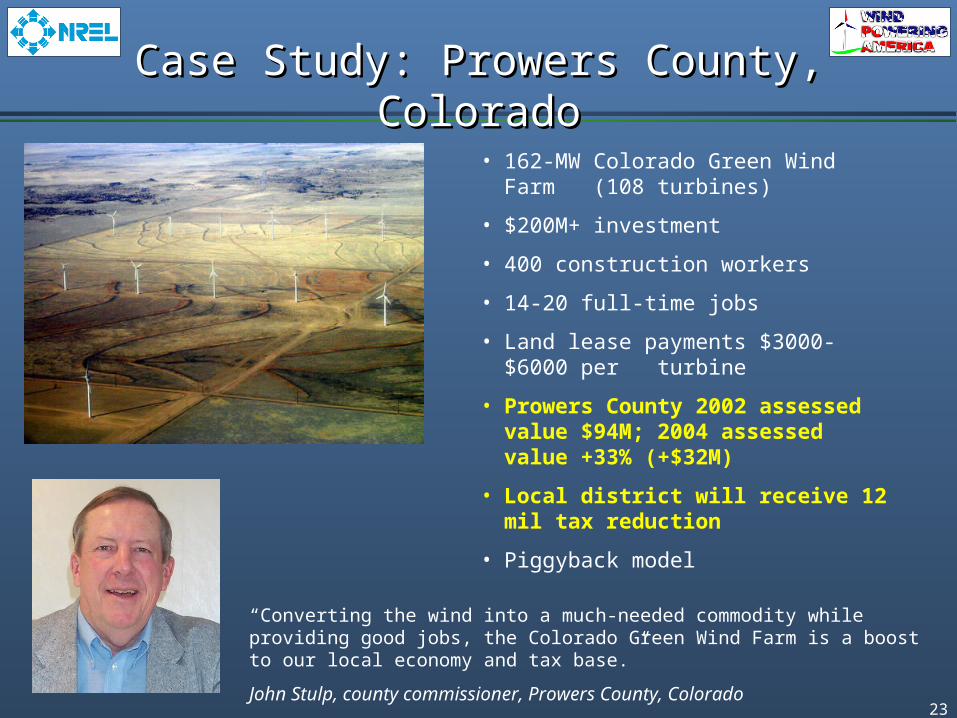

Case Study: Prowers County, ColoradoCase Study: Prowers County, Colorado

“Converting the wind into a much-needed commodity while providing good jobs, the Colorado Green Wind Farm is a boost to our local economy and tax base.”

John Stulp, county commissioner, Prowers County, Colorado

• 162-MW Colorado Green Wind Farm (108 turbines)

• $200M+ investment

• 400 construction workers

• 14-20 full-time jobs

• Land lease payments $3000-$6000 per turbine

• Prowers County 2002 assessed value $94M; 2004 assessed value +33% (+$32M)

• Local district will receive 12 mil tax reduction

• Piggyback model

24

Environmental BenefitsEnvironmental Benefits

• No SOx or NOx

• No particulates

• No mercury

• No CO2

• No water

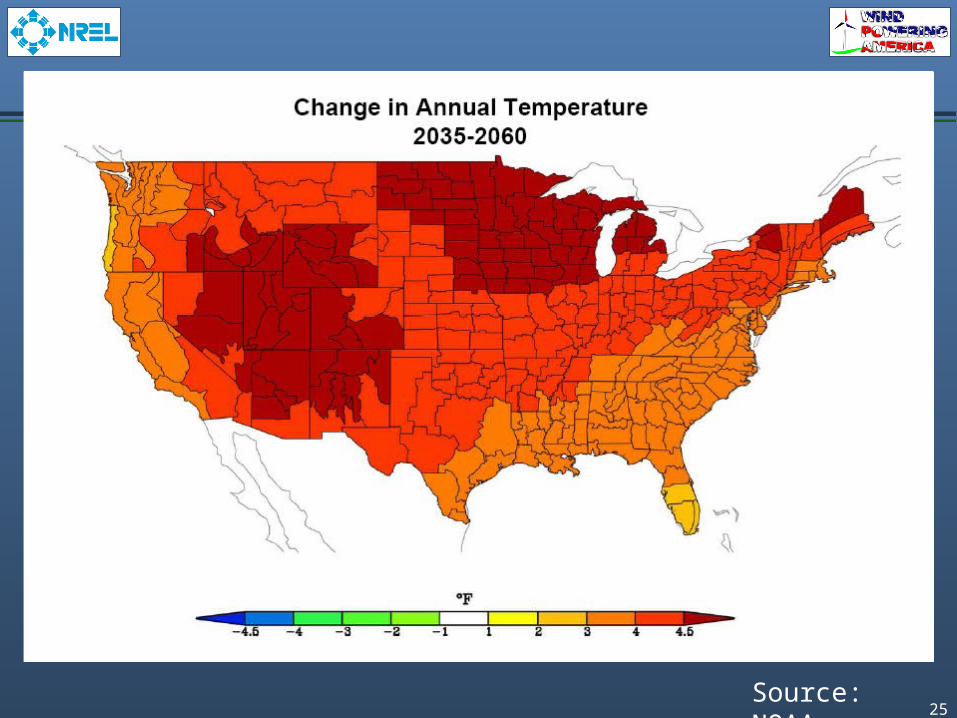

25Source: NOAA

26Source: NOAA

27

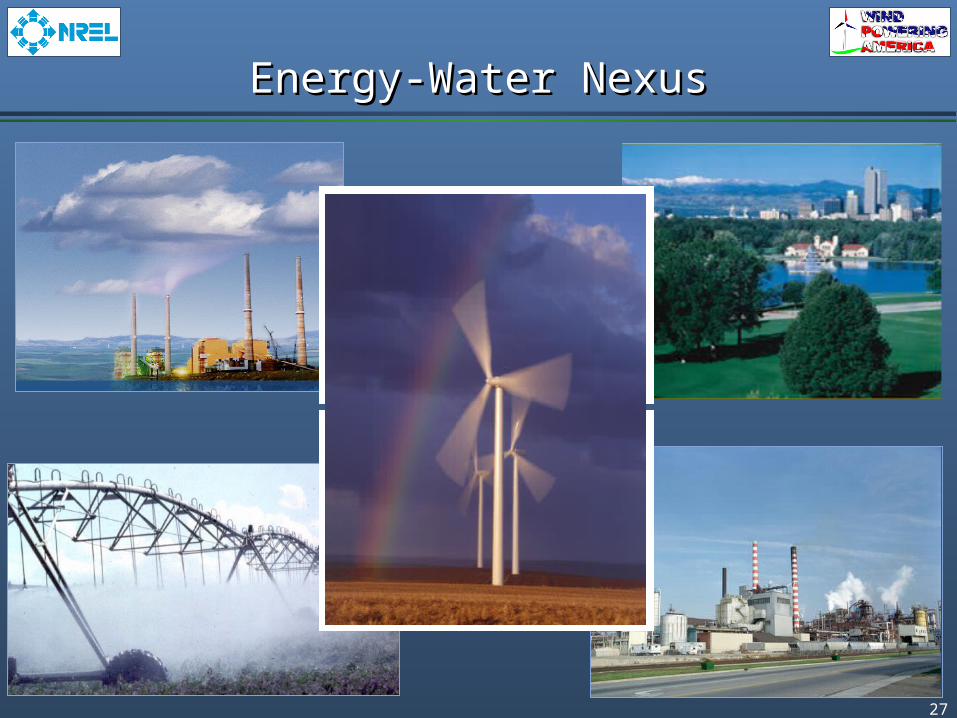

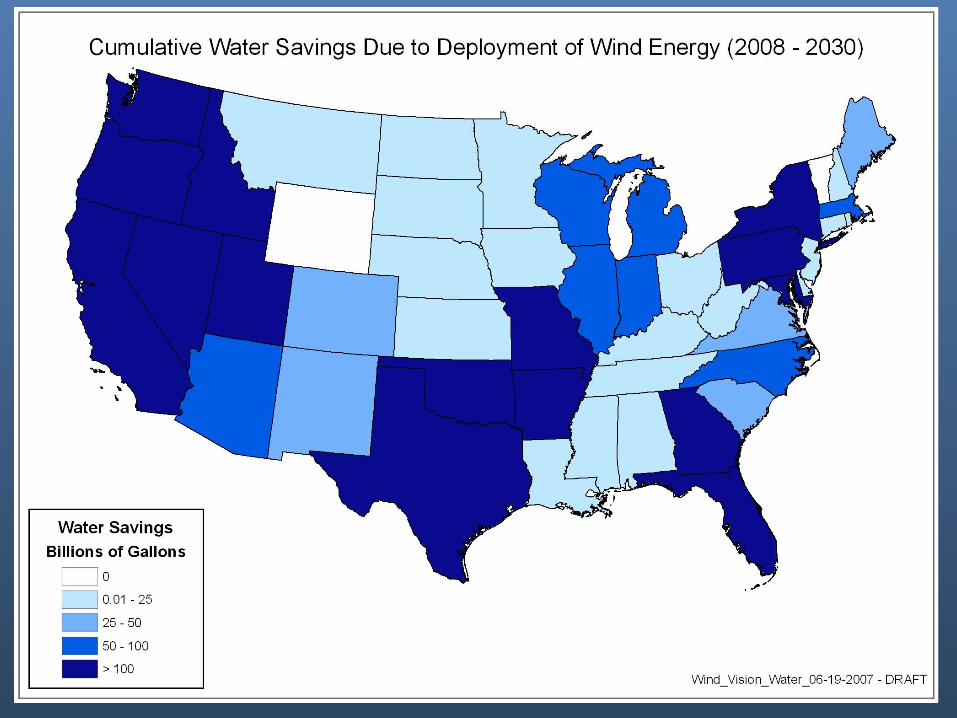

Energy-Water NexusEnergy-Water Nexus

28

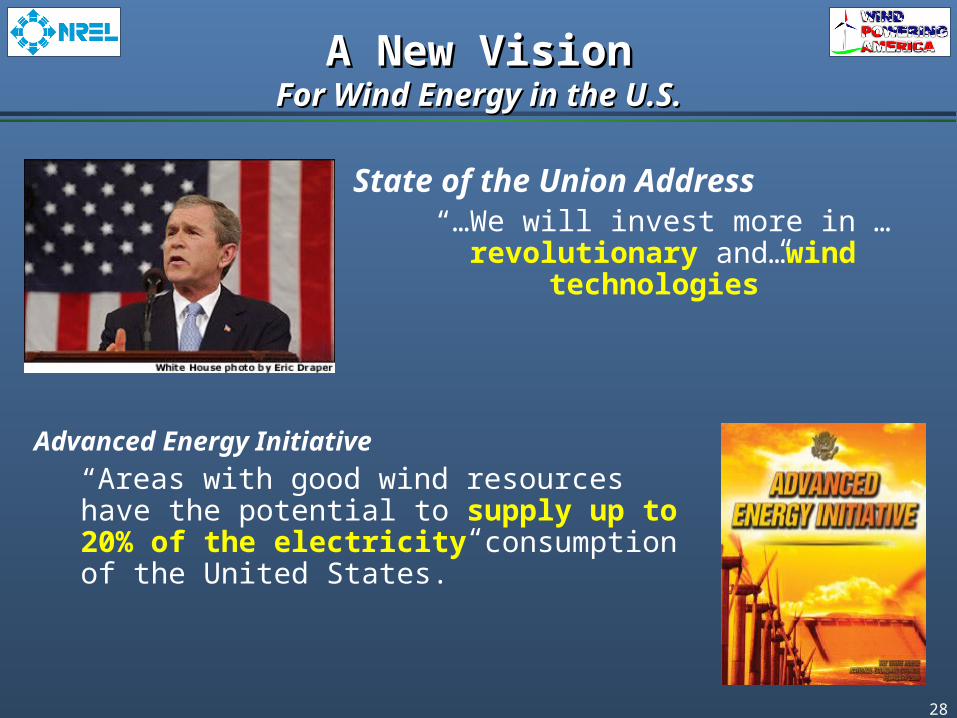

State of the Union Address“…We will invest more in … revolutionary and…wind

technologies”

Advanced Energy Initiative

“Areas with good wind resources have the potential to supply up to 20% of the electricity consumption of the United States.”

A New VisionA New VisionFor Wind Energy in the U.S.For Wind Energy in the U.S.

29

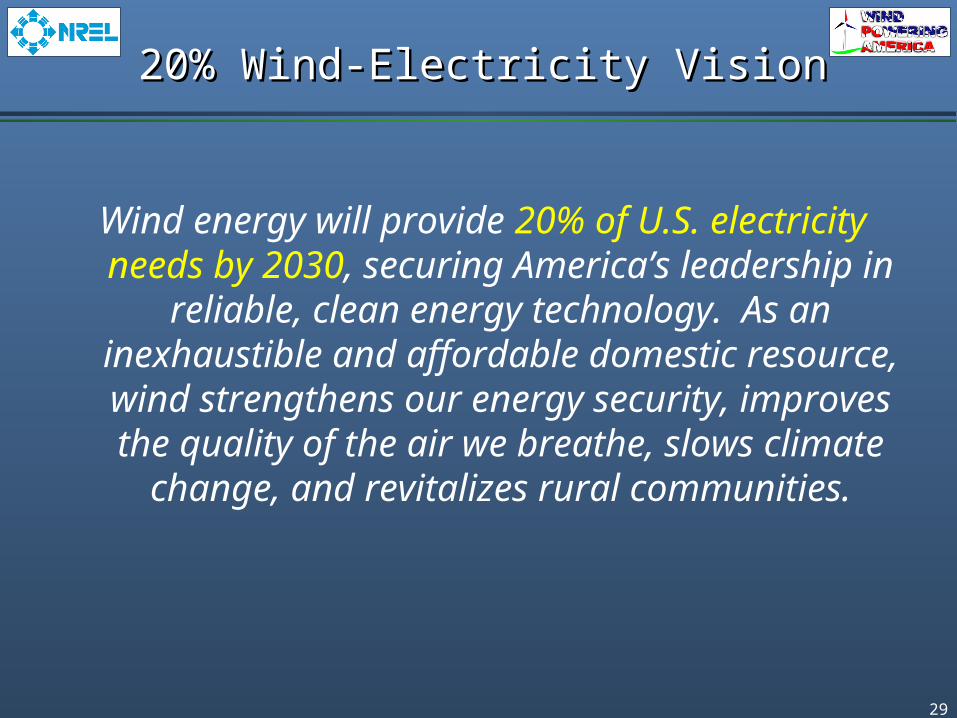

20% Wind-Electricity Vision20% Wind-Electricity Vision

Wind energy will provide 20% of U.S. electricity needs by 2030, securing America’s leadership in

reliable, clean energy technology. As an inexhaustible and affordable domestic resource, wind strengthens our energy security, improves the quality of the air we breathe, slows climate

change, and revitalizes rural communities.

30

20% Wind-Electricity Vision20% Wind-Electricity Vision

• 6 task forces:– Technology/Manufacturing

– Transmission/Utility Operations

– Siting/Environment

– Markets/Stakeholders

– Policy

– Analysis/Benefits

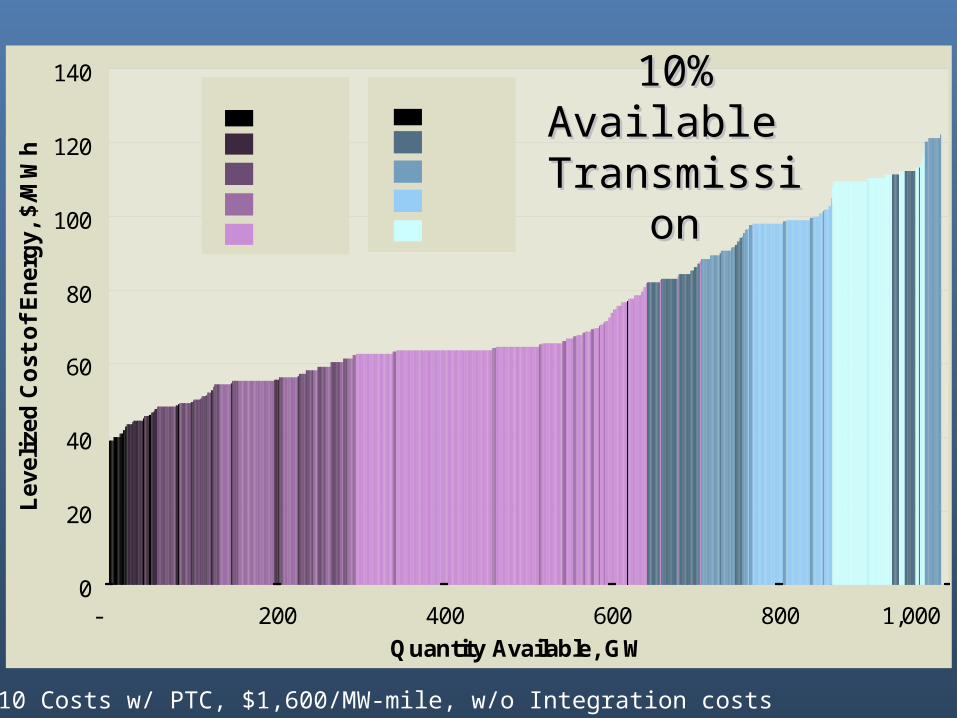

- 200 400 600 800 1,0000

20

40

60

80

100

120

140

Quantity Available, GW

Lev

eliz

ed C

ost

of

En

erg

y, $

/MW

h

Onshore

Class 6

Class 4

Class 7

Class 5

Class 3

Offshore

Class 6

Class 4

Class 7

Class 5

Class 3

10% Available 10% Available

TransmissionTransmission

2010 Costs w/ PTC, $1,600/MW-mile, w/o Integration costs

33

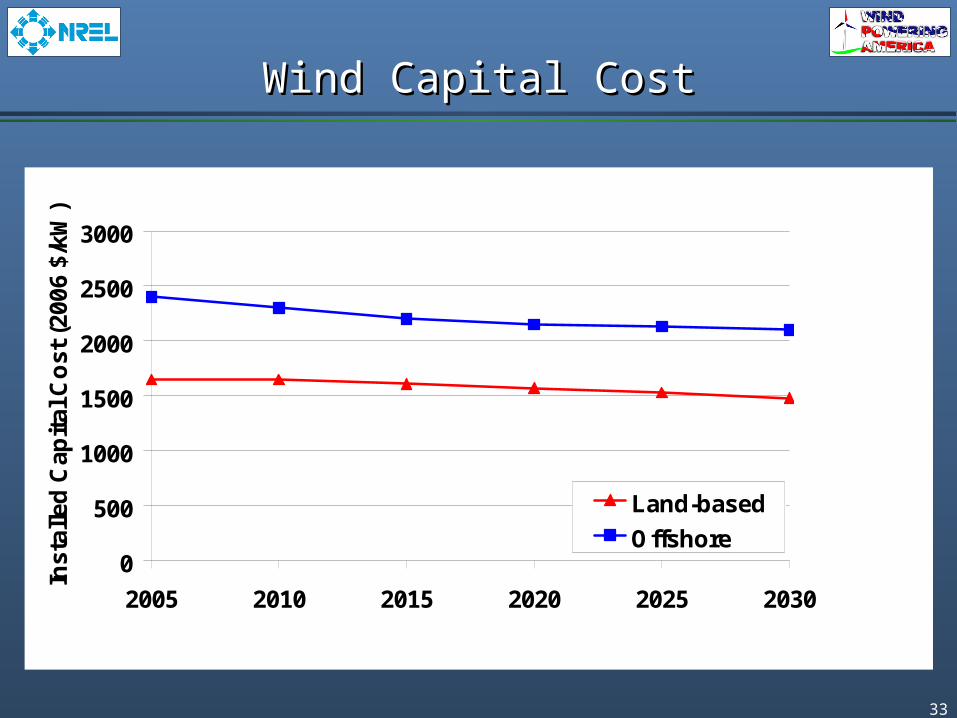

Wind Capital CostWind Capital Cost

0

500

1000

1500

2000

2500

3000

2005 2010 2015 2020 2025 2030

Inst

alle

d C

apit

al C

ost

(20

06 $

/kW

)

Land-based

Offshore

34

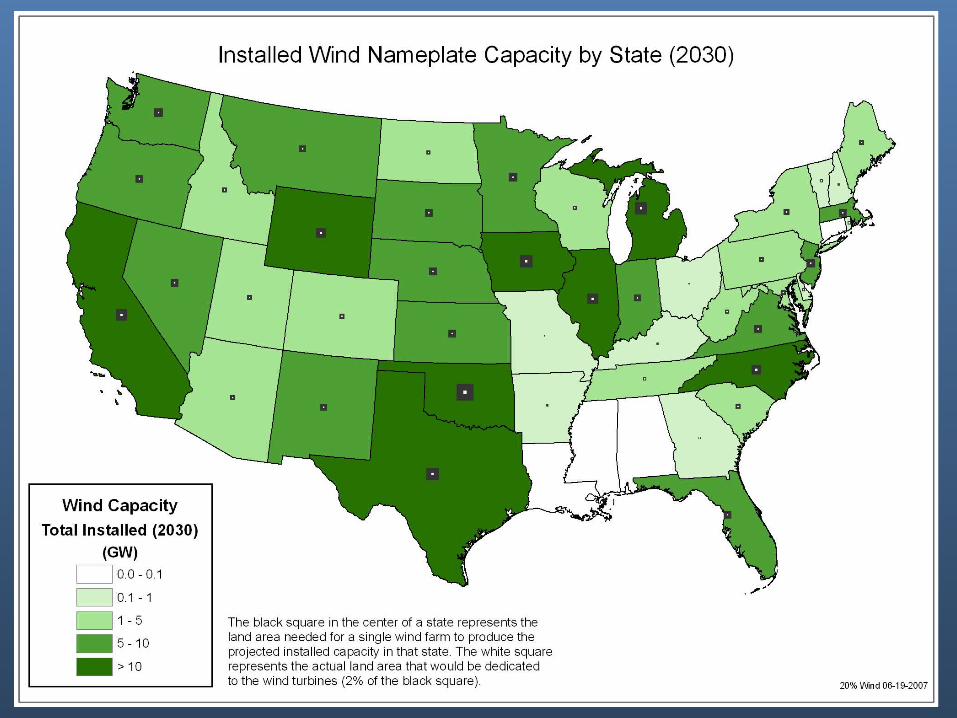

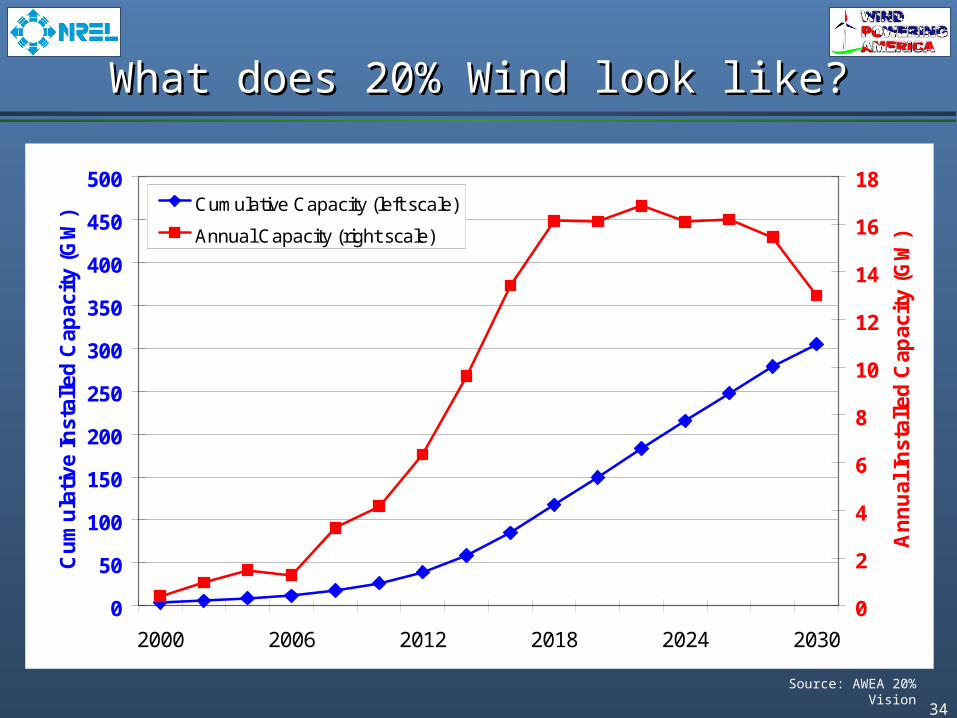

What does 20% Wind look like?What does 20% Wind look like?

Source: AWEA 20% Vision

0

50

100

150

200

250

300

350

400

450

500

2000 2006 2012 2018 2024 2030

Cu

mu

lati

ve In

stal

led

Cap

acit

y (G

W)

0

2

4

6

8

10

12

14

16

18

An

nu

al In

stal

led

Cap

acit

y (G

W)

Cumulative Capacity (left scale)

Annual Capacity (right scale)

36

Generation Mix with and without 20% WindGeneration Mix with and without 20% Wind

0

500

1000

1500

2000

2500

3000

Hydro

Gas-C

T

Gas-C

C

Coal -

w/ Scr

ubbers

Coal -

No Scr

ubbers

Coal-n

ew

Coal-IG

CC

Nuclea

r

Oil-Gas

-Ste

amW

ind

Gen

erat

ion

(T

Wh

)

20% Wind

No Wind

0

50

100

150

200

250

300

350

Hydro

Gas-C

T

Gas-C

C

Coal w

/Scr

ubbers

Coal-N

o Scr

ub

Coal-N

ew

Coal-IG

CC

Nuclea

r

Oil-Gas

-Ste

amW

ind

Cap

acit

y (G

W)

20% WindNo Wind

38

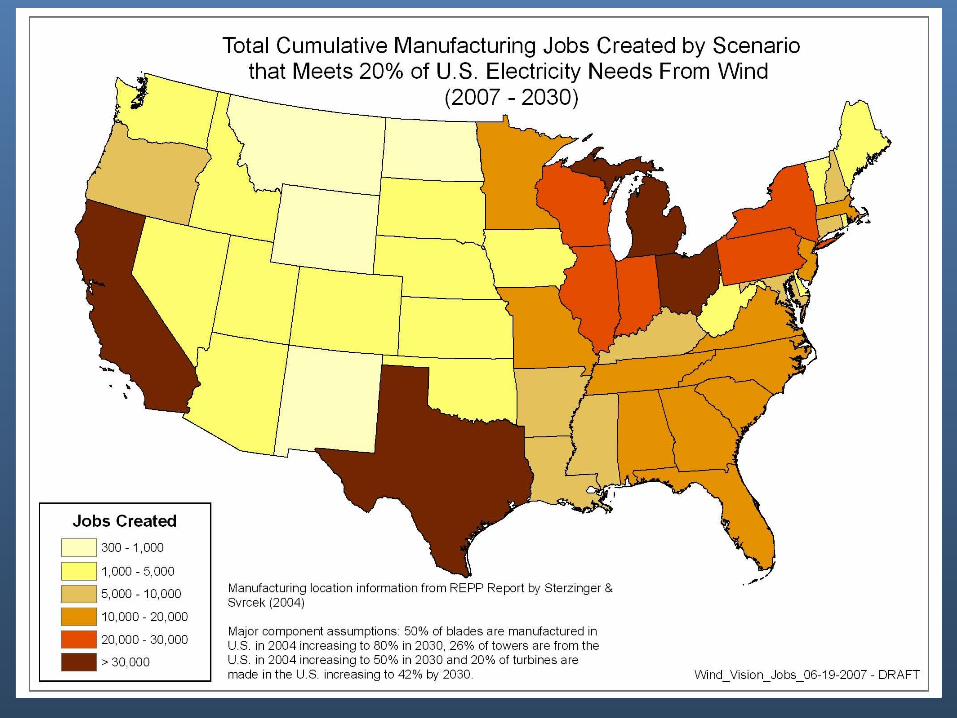

Construction Phase:• 4.46 M FTE jobs• $651 B to the US

economyOperations:• 2.15 M FTE jobs• $293 B to the US

economy

Wind energy’s economic “ripple effect”

All monetary values are in 2006 dollars. Construction Phase = 1-2 years

• Total economic benefit = $1,359 billion

• New jobs during construction = 6.2 M FTE jobs

• New operations jobs =3.3 M FTE jobs

Indirect & Induced Impacts

Totals (construction + 20yrs)

National (U.S.) – Economic Impacts National (U.S.) – Economic Impacts Cumulative impacts from 2007-2030 Cumulative impacts from 2007-2030

From the 20% Scenario- 300 GW new Onshore and Offshore developmentFrom the 20% Scenario- 300 GW new Onshore and Offshore development

Direct Impacts

Payments to Landowners: • $782 MLocal Property Tax Revenue:• $1,877 MConstruction Phase:• 1.75 M FTE jobs• $ 293 B to the US economyOperations:• 1.16 M FTE jobs• $122 B to the US economy

40

20% Wind Vision Employment20% Wind Vision Employment

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

2007

2009

2011

2013

2015

2017

2019

2021

2023

2025

2027

2029

Job

s

Operations

Construction

Manufacturing

42

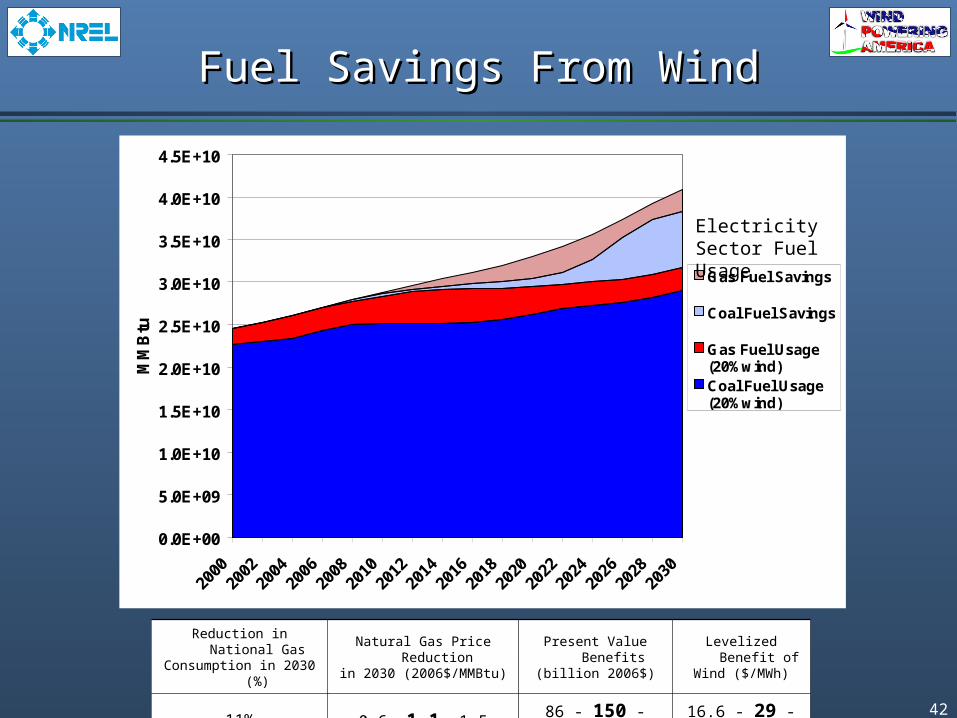

Fuel Savings From WindFuel Savings From Wind

0.0E+00

5.0E+09

1.0E+10

1.5E+10

2.0E+10

2.5E+10

3.0E+10

3.5E+10

4.0E+10

4.5E+10

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

MM

Btu

Gas Fuel Savings

Coal Fuel Savings

Gas Fuel Usage(20%wind)Coal Fuel Usage(20%wind)

Reduction in National GasConsumption in 2030 (%)

Natural Gas Price Reduction in 2030 (2006$/MMBtu)

Present Value Benefits(billion 2006$)

Levelized Benefit of Wind ($/MWh)

11% 0.6 -1.1- 1.5 86 - 150 - 214 16.6 - 29 - 41.6

Electricity Sector Fuel Usage

43

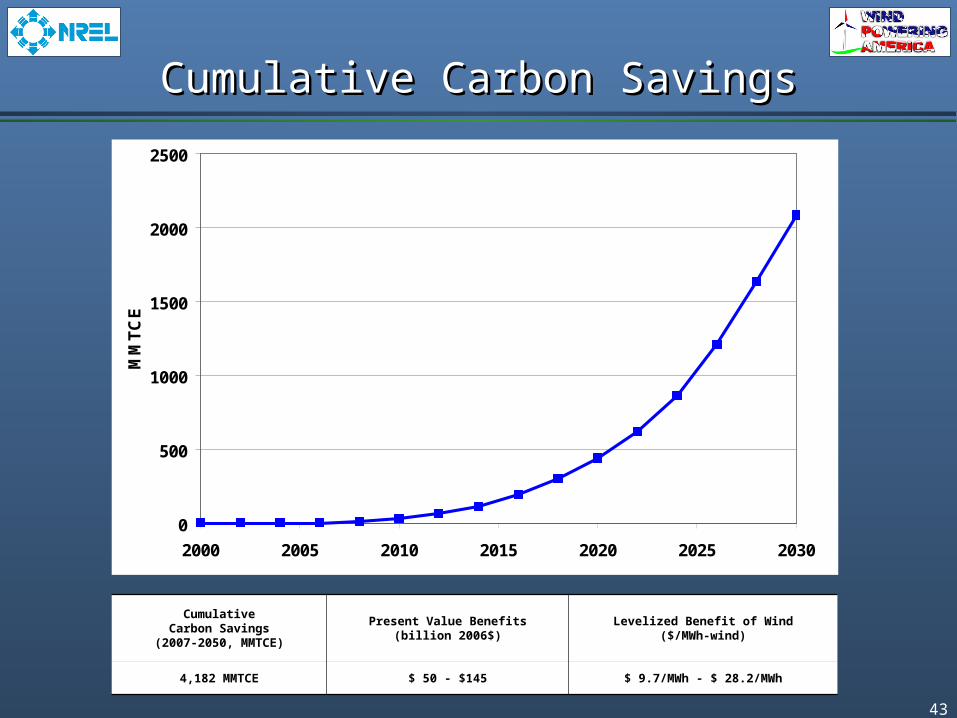

Cumulative Carbon SavingsCumulative Carbon Savings

0

500

1000

1500

2000

2500

2000 2005 2010 2015 2020 2025 2030

MM

TC

E

CumulativeCarbon Savings

(2007-2050, MMTCE)

Present Value Benefits(billion 2006$)

Levelized Benefit of Wind($/MWh-wind)

4,182 MMTCE $ 50 - $145 $ 9.7/MWh - $ 28.2/MWh

44

Electric Sector COElectric Sector CO22 Emissions Emissions

45

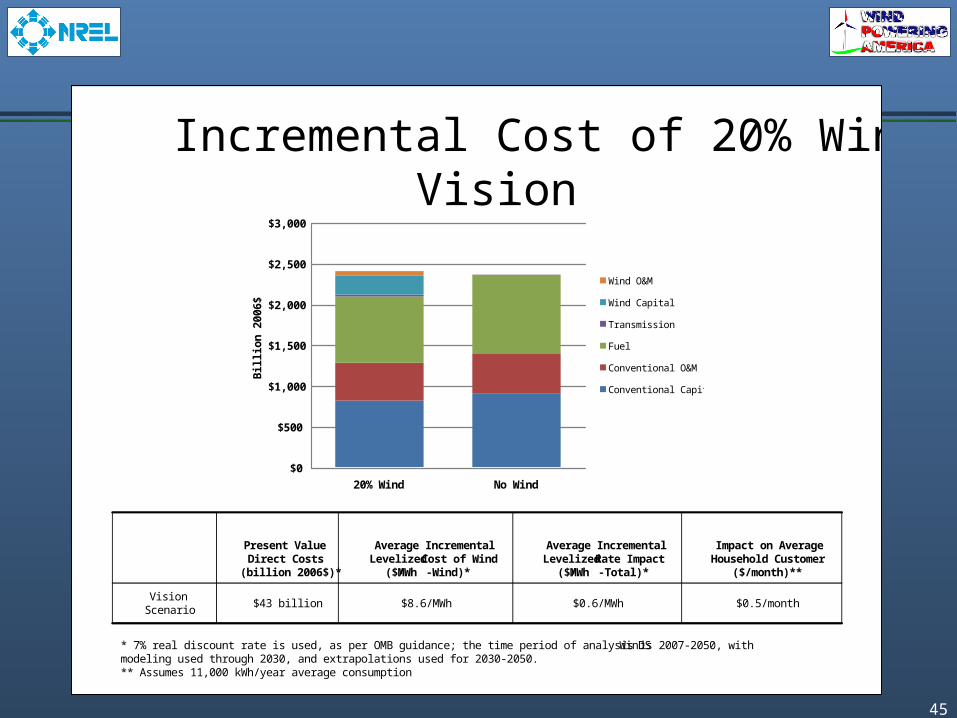

Incremental Cost of 20% WindVision

$0.5/month$0.6/MWh$8.6/MWh$43 billionVision

Scenario

Impact on AverageHousehold Customer

($/month)**

Average IncrementalLevelized Rate Impact

($/MWh-Total)*

Average IncrementalLevelized Cost of Wind

($/MWh-Wind)*

Present ValueDirect Costs

(billion 2006$)*

* 7% real discount rate is used, as per OMB guidance; the time period of analysis is 2007-2050, with WinDSmodeling used through 2030, and extrapolations used for 2030-2050.** Assumes 11,000 kWh/year average consumption

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

20% Wind No Wind

Bil

lio

n 2

00

6$

Wind O&M

Wind Capital

Transmission

Fuel

Conventional O&M

Conventional Capital

46

Incremental direct cost to society $43 billion

Reductions in emissions of greenhouse gasses and other atmospheric pollutants

825 M tons (2030)

$98 billion

Reductions in water consumption 8% total electric

17% in 2030

Jobs created and other economic benefits

140,000 direct

$450 billion total

Reductions in natural gas use and price pressure

11%

$150 billion

Net Benefits: $205B + Water savings

Results: Results: CostsCosts & Benefits& Benefits

47

• National and state policy uncertainty• Mixed stakeholder perspectives and knowledge• Electricity supply planning based on capacity• Variable wind output viewed as unreliable• Incomplete comparative generation assessments• Mismatch of wind and transmission development

timeframes• Federal lending all source requirements for G&T’s• Lack of interstate approach to transmission development• Need for utility financial incentives to own wind facilities• High cost and low turbine availability for community

projects• Uncertainty in emerging emissions REC markets

Market ChallengesMarket Challenges

48

ConclusionsConclusions

• 20% wind energy penetration is possible• 20% penetration is not going to happen under business

as usual scenario• Policy choices will have a large impact on assessing the

timing and rate of achieving a 20% goal• Key Issues: market transformation, transmission, project

diversity, technology development, policy, public acceptance

• 20% Vision report: February 2008

49

“With public sentiment nothing can fail; without it, nothing can succeed.”

- A. Lincoln

Carpe Ventem

www.windpoweringamerica.gov