Will LNG Exports from North America / East Africa Drive ... · ON LIQUEFIED NATURAL GAS (LNG 17)...

12

MONTH 2008 © POTEN & PARTNERS 2008 CONFIDENTIAL <Title of Presentation> By: <Author Name>, <Organization> <Date> <Title of Presentation> By: <Author Name>, <Organization> <Date> 17 th INTERNATIONAL CONFERENCE & EXHIBITION ON LIQUEFIED NATURAL GAS (LNG 17) Will LNG Exports from North America / East Africa Drive Global Price Integration? By: Kyoichi Miyazaki Majed Limam Poten & Partners, Inc. 17 April 2013 17 th INTERNATIONAL CONFERENCE & EXHIBITION ON LIQUEFIED NATURAL GAS (LNG 17)

Transcript of Will LNG Exports from North America / East Africa Drive ... · ON LIQUEFIED NATURAL GAS (LNG 17)...

MONTH 2008

© POTEN & PARTNERS 2008

CONFIDENTIAL

<Title of Presentation>

By: <Author Name>, <Organization>

<Date>

<Title of Presentation> By: <Author Name>, <Organization>

<Date>

17th INTERNATIONAL CONFERENCE & EXHIBITION

ON LIQUEFIED NATURAL GAS (LNG 17)

Will LNG Exports from North America / East

Africa Drive Global Price Integration?

By: Kyoichi Miyazaki

Majed Limam

Poten & Partners, Inc.

17 April 2013

17th INTERNATIONAL CONFERENCE & EXHIBITION ON

LIQUEFIED NATURAL GAS (LNG 17)

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

APRIL 2013 Page 1

Gas prices worldwide continue to diverge

Oil linked

LNG

prices

Gas on

gas

market

prices

Shale gas revolution has driven down Henry Hub prices

0

5

10

15

20

25

2007 2008 2009 2010 2011 2012

$/M

MB

tu

JCC

Japan

LNG Price

NBP

Henry Hub

Source: Poten & Partners

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

APRIL 2013 Page 2

Will LNG exports from North America / East Africa

drive global price integration?

Oil Product

Henry

Hub/

NBP / Brent

JCC/Brent

NBP

Oil-linked markets Gas-on-gas markets

? ?

?

?

Shale gas

driven Henry

Hub

East

Africa

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

APRIL 2013 Page 3

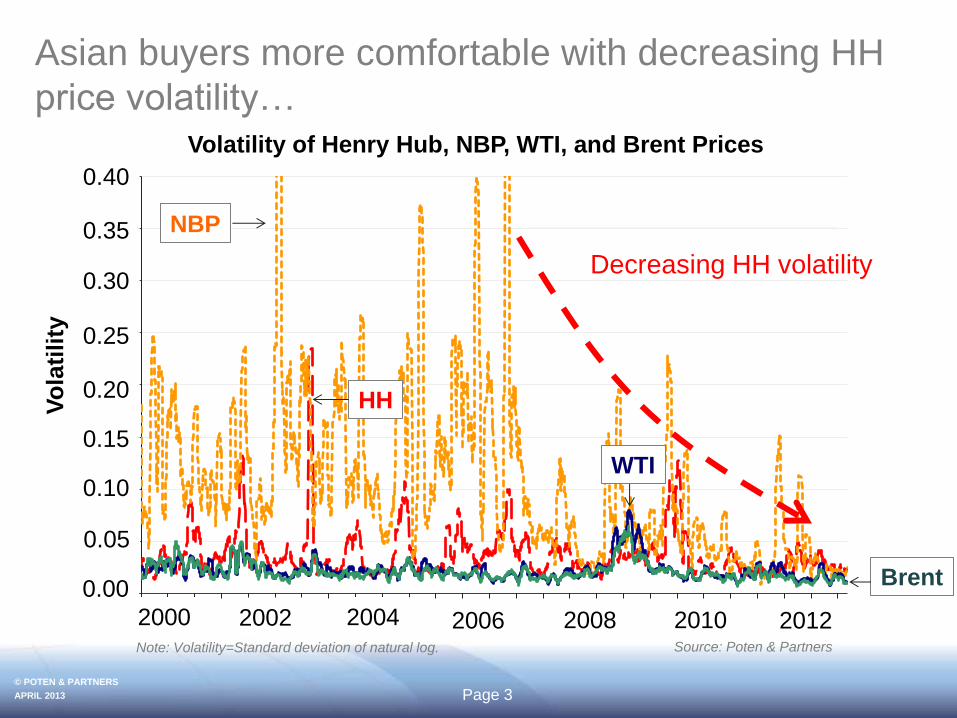

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

HH NBP WTI Brent

Vo

lati

lity

Asian buyers more comfortable with decreasing HH

price volatility… Volatility of Henry Hub, NBP, WTI, and Brent Prices

Source: Poten & Partners Note: Volatility=Standard deviation of natural log.

Decreasing HH volatility

0.40

0.35

0.30

0.25

0.20

0.15

0.10

0.05

0.00

Vo

lati

lity

2000 2002 2004 2006 2008 2010 2012

NBP

HH

WTI

Brent

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

APRIL 2013 Page 4

…but remember large historical variations

2004 2005 2006 2007 2008 2009 2010 2011 2012

10

5

(15)

(10)

(5)

-

$/M

MB

tu

Shale gas revolution impact

Hurricanes Katrina & Rita

HH/oil price surged but S - curve damping effect on Asian LNG contracts

Calculation : Historical Asian LNG price minus hypothetical Henry Hub linked price JLC > HH H

JLC < HH H

Source: Poten & Partners

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

APRIL 2013 Page 5

Increasing new supply sources but still limited share in

the growing Asian LNG market

LNG Supplies into Asia – New Australian supplies remain

the major contributor to Asian market

Source: Poten & Partners

0

50

100

150

200

250

300

2010 2015 2020 2025

North America (US+Canada)

East Africa

New Australia

Others

MM

t/y

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

APRIL 2013 Page 6

Challenging cost structures for green field projects in

Asia Pacific

Australia

US Gulf/East

Source: Poten & Partners

Mounting construction

resource requirement

Ever increasing EPC costs

especially in Australia

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

APRIL 2013 Page 7

Increased competition for the Asian market lowers long

term contract price

Year of finalization of

LNG sale

Poten projected Asian long-

term contract slope

Year of first production

-

1

2

3

4

5

2019 2020 2021 2022 2023 2024 2025

Poten Asia

Pacific Market

Competition

Index

Oil Parity

5 year lag

Source: Poten & Partners

2014 2015 2016 2017 2018 2019 2020

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

APRIL 2013 Page 8

Can local Asian gas-on-gas market develop?

Critical factors:

An interconnected gas

transmission system

Deregulated markets

Transparent market with

limited gov. intervention

A short term and futures

market

Other important factors:

Growing domestic production

Growing pipeline imports and

exports

Substantial storage capacity

LNG trade

High liquidity

+

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

APRIL 2013 Page 9

It took 20 to 30 years for US/UK to develop gas-on-gas

markets

US

UK

1970s 1980s 1990s

1970s 1980s 1990s

Natural Gas

Policy Act -

FERC

US

eliminates

take-or-pay

clauses

Open Access.

NYMEX started

Henry Hub trade

Natural Gas

Act in 1986

British Gas split into

Centrica and BG plc

in 1997, Lattice

transmission in

2000. NBP started in

1996

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

APRIL 2013 Page 10

New pricing mechanisms emerging but no material de-

linkage from oil indexation in Asia

• Even if all North America LNG were to be gas-hub linked, it

represents no more than 10% of the total Asian demand in

2020

• Increased competition will drive down oil indexed prices

• New pricing mechanisms – anywhere between a traditional

oil-linkage and a Henry Hub linkage – are emerging

MONTH 2009

© POTEN & PARTNERS 2009

CONFIDENTIAL

© POTEN & PARTNERS

APRIL 2013 Page 11

LNG & NATURAL GAS CONSULTING CONTACTS:

AMERICAS

Contact: Jim Briggs

Email: [email protected]

Tel: +1 212 230 2000

EUROPE, MIDDLE EAST, AFRICA

Contact: Graham Hartnell

Email: [email protected]

Tel: +44 207 493 7272

ASIA PACIFIC

Contact: Steve Thompson

Email: [email protected]

Tel: +61 8 6468 7942