Why the retail banking - Verdict

27

Transcript of Why the retail banking - Verdict

Why the retail banking model is broken

Alex Letts: Chief Executive, FFrees

Why the retail banking model is broken

…....but not in the way some people think.

The great dance-off: a fair contest?

BANKS FINTECHS

A perception not helped by.... “I see the other banks playing the same old game.... When you think about things we’re doing.. my view is, the challenger bank is RBS.”

Mr McEwan said that his decision to remove bonuses from front-line branch and business banking staff, to simplify terms and conditions on products, remove teaser rates, and to focus on new customers as much as existing customers set the two brands (RBS/NatWest) apart from the pack.

Bankenstein’s Monster: a fintech view of bank’s typical app test lab.....!

We are ready to disrupt this status quo…..

We are ready to disrupt this status quo…..

But what do we all mean by disruption?

“Disruption” is…..

• A cool app?

• A cool name?

• Some funky tools?

• New features?

• Slideware?

“Disruption” is…..

• A cool app?

• A cool name?

• Some funky tools?

• New features?

• Slideware?

• The Banks can, or will, do this too (maybe better)?

Where is the creative destruction?

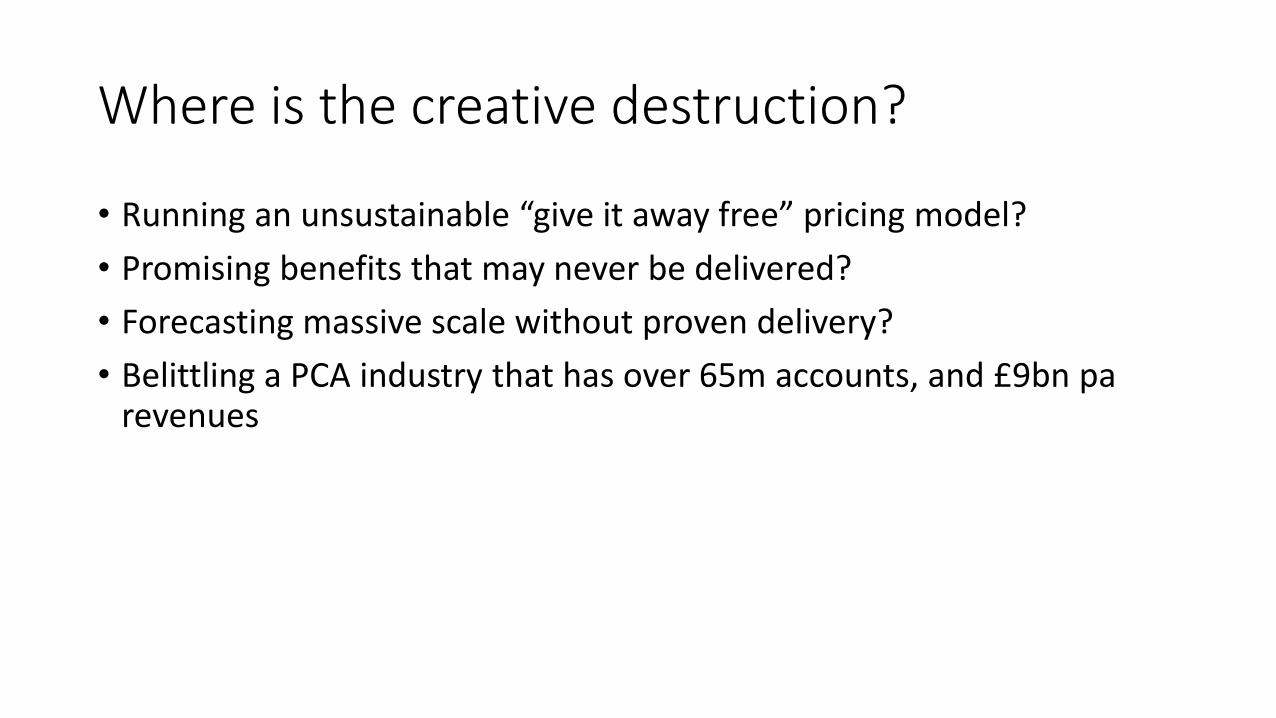

Where is the creative destruction?

• Running an unsustainable “give it away free” pricing model?

• Promising benefits that may never be delivered?

• Forecasting massive scale without proven delivery?

• Belittling a PCA industry that has over 65m accounts, and £9bn pa revenues

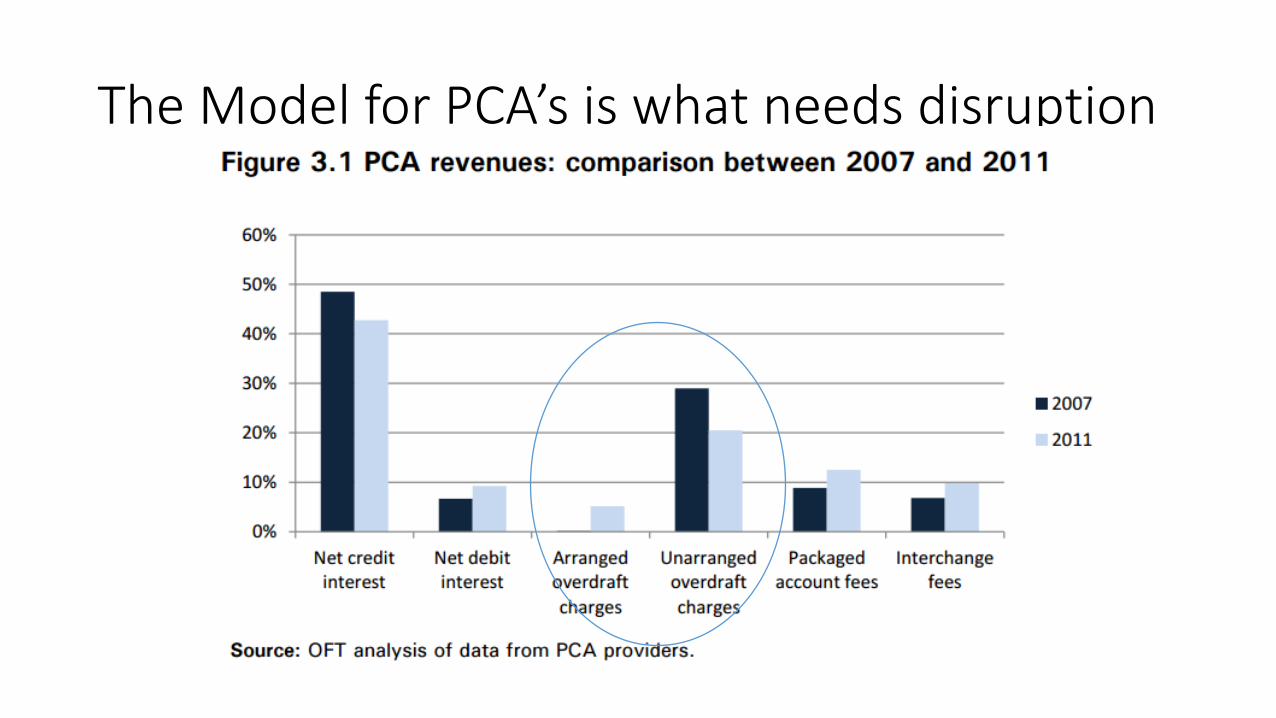

The Model for PCA’s is what needs disruption

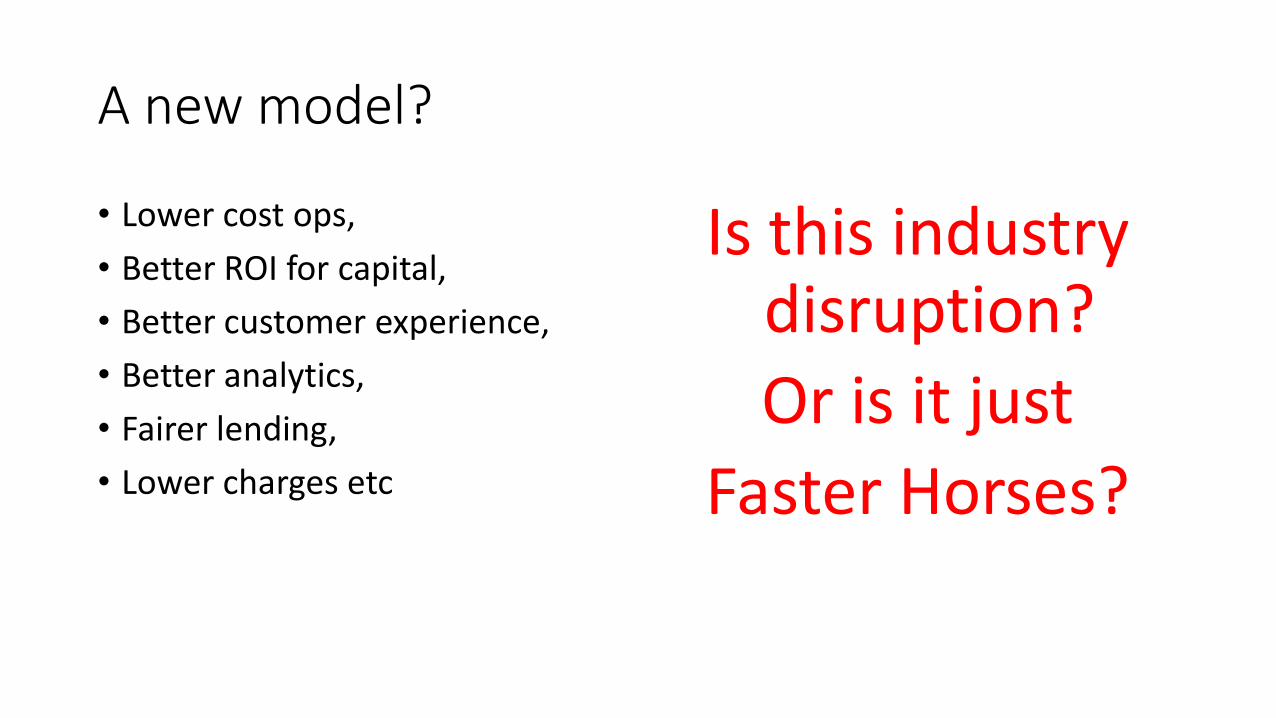

A new model?

• Lower cost ops,

• Better ROI for capital,

• Better customer experience,

• Better analytics,

• Fairer lending,

• Lower charges etc

Is this industry disruption?

Or is it just

Faster Horses?

The challenge for disruptors

• The bank business model is vulnerable and counter-intuitive: don’t copy it!

The challenge for disruptors

• The bank business model is vulnerable and counter-intuitive: don’t copy it!

• Current accounts subsidised by lending: the well trodden road to perdition?

The challenge for disruptors

• The bank business model is vulnerable and counter-intuitive: don’t copy it!

• Current accounts subsidised by lending: the well trodden road to perdition?

• Poorer customers subsidising free accounts for richer customers creates exclusion

The challenge for disruptors

• The bank business model is vulnerable and counter-intuitive: don’t copy it!

• Current accounts subsidised by lending: the well trodden road to perdition?

• Poorer customers subsidising free accounts for richer customers creates exclusion

• Egregious penalties for poor money management creates a bad relationship and distress

The challenge for banks

• Slavish devotion to outdated platforms

• Post rationalisation of physical retail estate

• Management attention is elsewhere

The challenge for banks

• Slavish devotion to outdated platforms

• Post rationalisation of physical retail estate

• Management attention is elsewhere

AND Attitude

The challenge for banks

• Slavish devotion to outdated platforms

• Post rationalisation of physical retail estate

• Management attention is elsewhere

AND Attitude

• “we could do any of this ourselves” (your systems can’t)

• Digital is a way to reduce cost (it does, but that’s a side benefit)

• Profit before purpose (oh dear)

An industry challenge

• Everyone knows that neither side will win on its own

• We are all tearing through capital, and you are wasting time

• New models are within our grasp, but scale is a long process

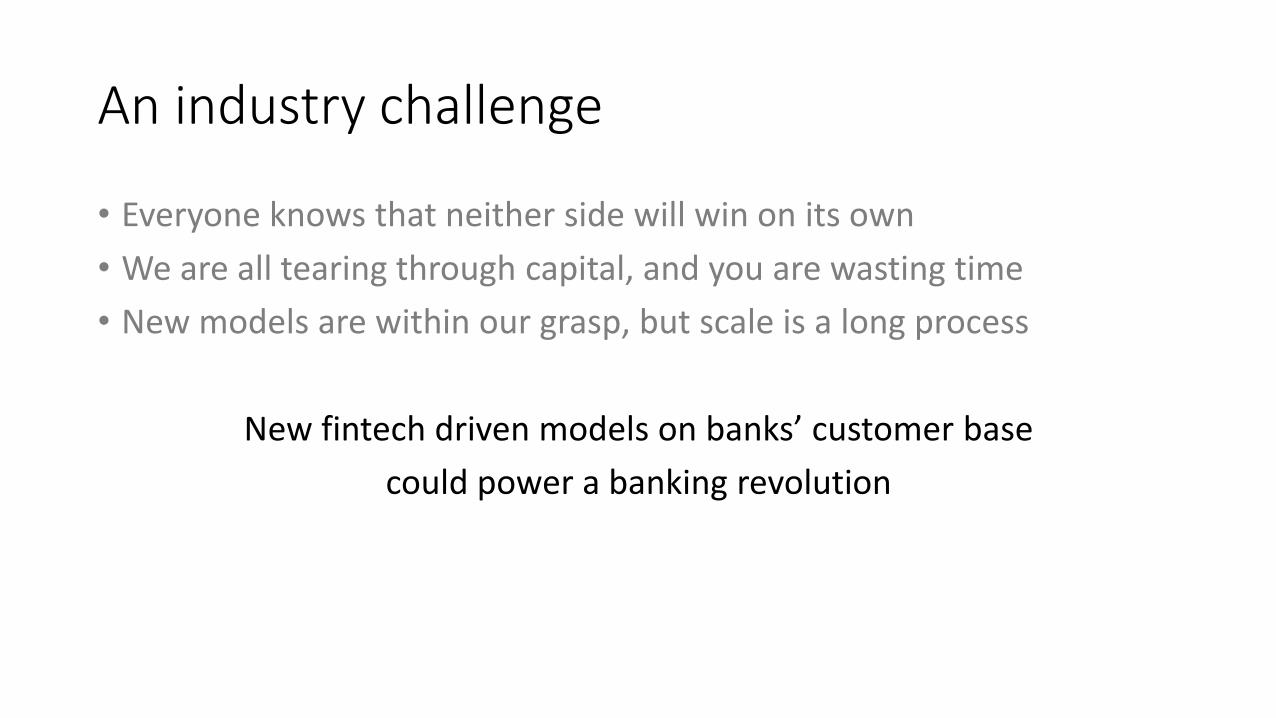

An industry challenge

• Everyone knows that neither side will win on its own

• We are all tearing through capital, and you are wasting time

• New models are within our grasp, but scale is a long process

New fintech driven models on banks’ customer base

could power a banking revolution

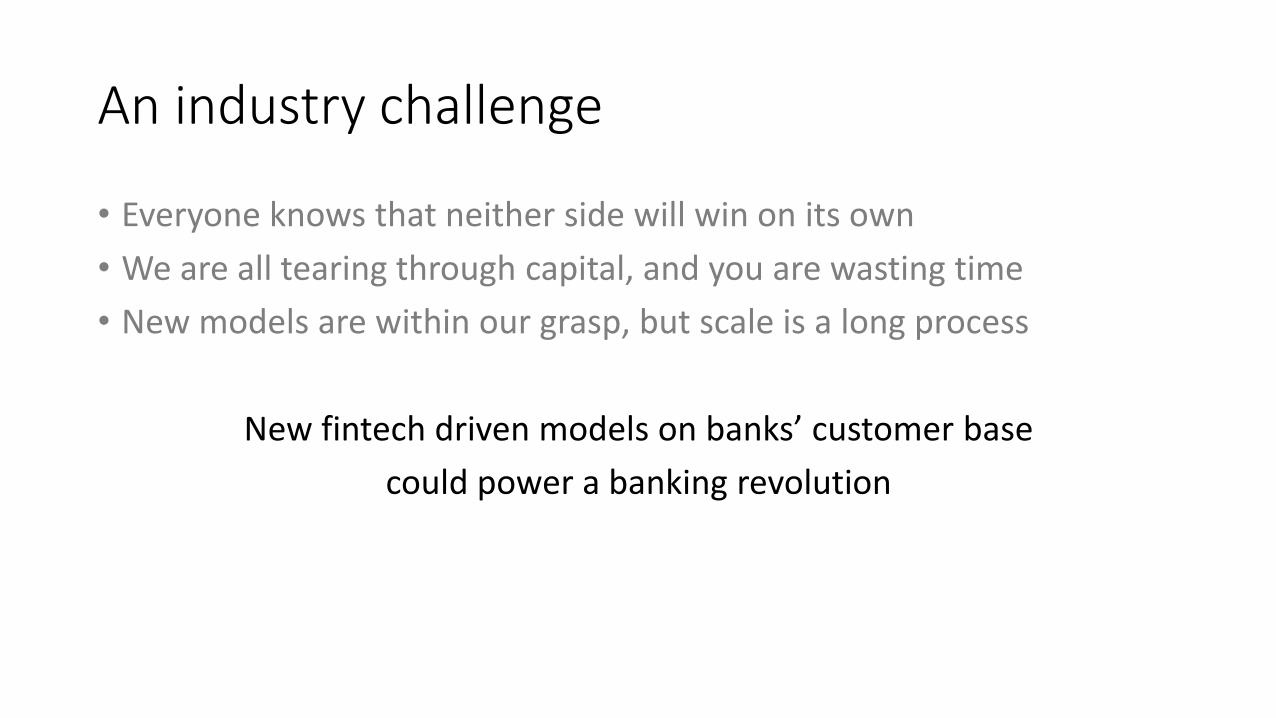

An industry challenge

• Everyone knows that neither side will win on its own

• We are all tearing through capital, and you are wasting time

• New models are within our grasp, but scale is a long process

New fintech driven models on banks’ customer base

could power a banking revolution