Who:Cyndy Harnett Cyndy currently works at Kelley Services, a staffing company that specializes in...

61

Who:Cyndy Harnett Cyndy currently works at Kelley Services, a staffing company that specializes in filling business and education positions. Come find out what employers are looking for in employees in today’s market When:Thursday, March 5, 7 p.m. Where:LRC 235 AMS $2 for non-members ADMINISTRATIVE MANAGEMENT SOCIETY

-

Upload

matilda-perry -

Category

Documents

-

view

212 -

download

0

Transcript of Who:Cyndy Harnett Cyndy currently works at Kelley Services, a staffing company that specializes in...

Who:Cyndy Harnett

Cyndy currently works at Kelley Services, a staffing company that specializes in filling business and education positions. Come find out what employers are looking for in

employees in today’s market When:Thursday, March 5, 7 p.m.

Where:LRC 235

AMS

$2 for non-members

ADMINISTRATIVE MANAGEMENT SOCIETY

AFFILIATE OF

Jeff OwensHR Manager, Hogan Taylor

“The HR Practitioner’s Role in Team Building”

11 a.m. Monday, March 9, 2009 GC 3116

$3 for non-members

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

3

presents

Tim Abrahamswith the New York Office of

PricewaterhouseCoopers LLP

“Forensic Accounting”

Monday, March 9 - GC 5116registration 6:10 – 6:25 p.m.meeting begins at 6:30 p.m.

$3 for non-members

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

4

Federal Income Tax

(Business) Deductions

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

5

Perspective

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

6

Gross Income- FOR= AGI- FROM= Taxable Income

Business

Personal

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

7

General Requirements• Problem 6 – 9

– Ordinary

– Necessary

– Reasonable

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

8

General Requirements• Problem 6 – 9

– Ordinary

– Necessary

– Reasonable

• Related to income production• Customary; usual

• Appropriate; helpful• “Prudent person”• Would others have incurred it?

• In amount• Not excessive when compared to industry

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

10

The Four “Nots”

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

11

The Four “Nots”

• Contrary to public policy

• Capital

• Personal

• Related to tax-exempt income

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

12

The Four “Nots”• Problem 6 – 11

Why are expenses related to tax-exempt income disallowed?

• Income not included; expenses not deducted

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

13

Which is better?

For From

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

14

Why is For better?• Reduces TI for full amount even if

standard deduction is used• From not beneficial unless >

standard deduction• Many items from are limited by AGI

percentage reducing the benefit• Taxability of SS benefits based on

AGI

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

15

Business Expenses

• Generally…

–Self-employed = “for”

–Employee = “from”

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

16S

tep

1:

Th

eory

Ste

p 2

?

Ste

p 3

:P

ractic

e

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

17

GI- FOR= AGI- FROM= TI

“Tier 1”

“Tier 2”

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

18

For vs. From• Problem 6 – 13

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

19

Problem 6 - 13

a. Deductible? Yes For or from?

FROM – employEE

b. Two sources of income? Split:

Self-employed = FOR Employed = FROM

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

20

GI- FOR= AGI- FROM= TI

“Tier 1”

“Tier 2”

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

21

Tier 2 ExpensesReduced by2% of AGI

to determine deductible amount

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

22

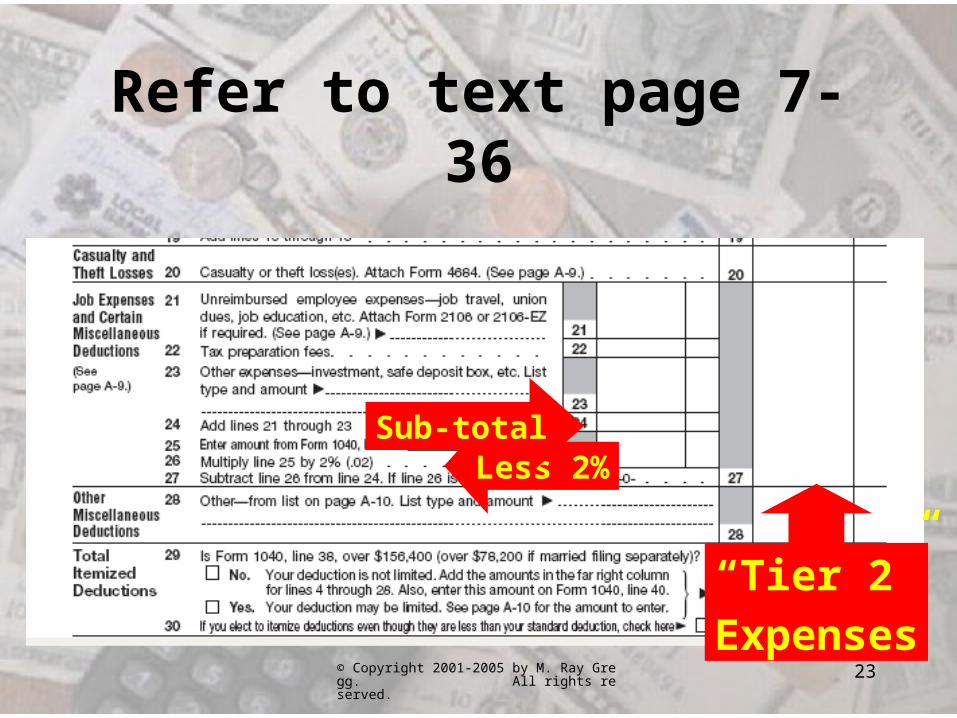

Most itemized deductionsare “Tier 1”

Refer to text page 7-36

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

23

Refer to text page 7-36

Less 2%

“Tier 2”Expenses

Sub-total

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

24

For vs. From• Problem 6 – 13

• Problem 6 – 33

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

25

For or Tier 1Ded? From? or Tier 2?

Travel to clients $750Subs to prof journals 215Lunches w/ clients 400Photocopying 60

Problem 6 - 33

Yes FromYes FromYes FromYes From

a. Deductible?

2222

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

26

GI- FOR= AGI- FROM= TI

“Tier 1”

“Tier 2”

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

27

For orDed? From?

Travel to clients $750Subs to prof journals 215Lunches w/clients 400Photocopying 60

Problem 6 - 33

YesYesYesYes

ForForForFor

b. If reimbursed…

No "Tiers" with FOR

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

28

Business Expenses

• Self-employed–“for”

• Employee–Reimbursed?

•Yes = “for”•No = “from”

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

29

Problem 6 - 33For or

Ded? From?

Travel to clients $750Subs to prof journals 215Lunches w/clients 400Photocopying 60

YesYesYesYes

ForForForFor

c. If self-employed…

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

30

For vs. From• Problem 6 – 13

• Problem 6 – 33

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

32

Chapter 9• Travel and Transportation• Automobile Expenses• Entertainment• Moving Expenses

• Education Expenses• Home Office• Reimbursements• Hobby losses (from Chap 6)

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

33

Travel and Transportation

• Define travel

–“away from home overnight”

–Name some

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

34

Travel and Transportation

• Define travel

–“away from home overnight”

–Name some

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

35

Travel and Transportation

• Define travel

–“away from home overnight”

–Name some

• Define transportation

• Problem 9 -56

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

36

Problem 9 - 56

Airfare $ 450

Meals ($50 per day) 250

Hotel ($100 per day) 500

Entertainment 500

Total $1,700

assume he was NOT reimbursed

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

37

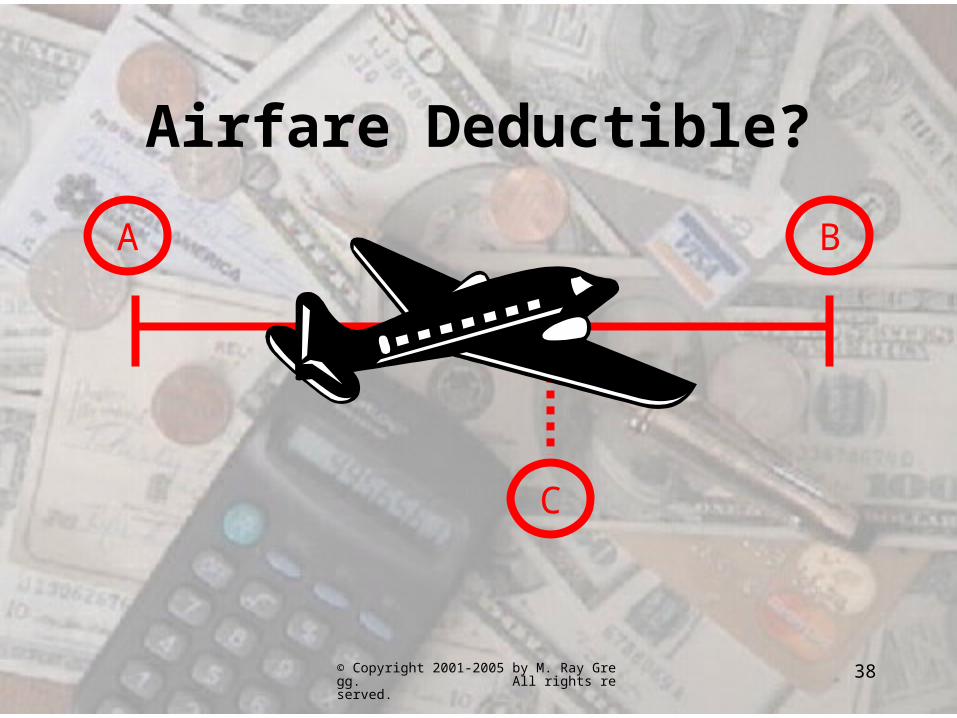

Airfare Deductible?

A B

C

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

38

Airfare Deductible?

A B

C

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

39

Airfare Deductible?

A B

C

1/32/3

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

40

Exemption

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

41

Prorate Exemption?

1/3? 2/3?

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

42

Airfare Deductible?

A B

CNever prorate airfare.

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

43

Airfare Deductible?

A B

CPrimary reason?

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

44

Airfare Deductible?

A B

C

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

45

• Purely business expenses on a personal trip ARE deductible

• Purely personal expenses on a business trip are NOT deductible

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

46

Problem 9 - 56

Airfare $ 450

Meals ($50 per day) 250

Hotel ($100 per day) 500

Entertainment 500

Total $1,700

assume he was NOT reimbursed

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

47

Problem 9 - 56

Airfare $ 450 $450

Meals ($50 per day) 250

Hotel ($100 per day) 500

Entertainment 500

Total $1,700

assume he was NOT reimbursed

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

48

Problem 9 - 56

Airfare $ 450 $450

Meals ($50 per day) x 3 250 $150

Hotel ($100 per day) 500

Entertainment 500

Total $1,700

assume he was NOT reimbursed

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

49

Problem 9 - 56

Airfare $ 450 $450

Meals ($50 per day) x 3 250 $150

Hotel ($100 per day) 500

Entertainment 500

Total $1,700

assume he was NOT reimbursed

50% limit

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

50

Problem 9 - 56

Airfare $ 450 $450

Meals ($50 per day) x 3 250 $ 75

Hotel ($100 per day) 500

Entertainment 500

Total $1,700

assume he was NOT reimbursed

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

51

Problem 9 - 56

Airfare $ 450 $450

Meals ($50 per day) x 3 250 $ 75

Hotel ($100 per day) x 3 500 $300

Entertainment 500

Total $1,700

assume he was NOT reimbursed

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

52

Problem 9 - 56

Airfare $ 450 $450

Meals ($50 per day) x 3 250 $ 75

Hotel ($100 per day) x 3 500 $300

Entertainment 500 $250

Total $1,700

assume he was NOT reimbursed

50% limit

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

53

Problem 9 - 56

Airfare $ 450 $450

Meals ($50 per day) x 3 250 $150

Hotel ($100 per day) x 3 500 $300

Entertainment 500 $250

Total $1,700

assume he was NOT reimbursed

Deductible FROM – Tier 2

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

54

Problem 9 - 56

Airfare $ 450

Meals ($50 per day) 250

Hotel ($100 per day) 500

Entertainment 500

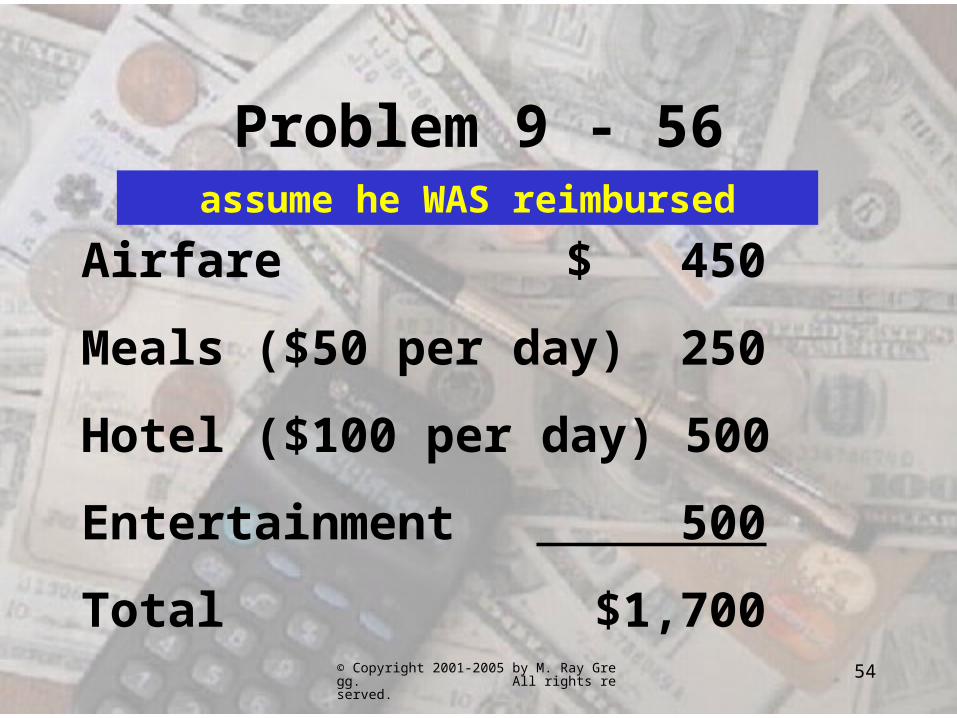

Total $1,700

assume he WAS reimbursed

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

55

Problem 9 - 56

Airfare $ 450 0

Meals ($50 per day) 250 0

Hotel ($100 per day) 500 0

Entertainment 500 0

Total $1,700

assume he WAS reimbursed

a. none deductible by Mike

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

56

Problem 9 - 56

Airfare $ 450 0

Meals ($50 per day) 250 0

Hotel ($100 per day) 500 0

Entertainment 500 0

Total $1,700

assume he WAS reimbursed

b. reimb not reported by Mike

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

57

Problem 9 - 56

Airfare $ 450 450

Meals ($50 per day) 250 75

Hotel ($100 per day) 500 300

Entertainment 500 250

Total $1,700

assume he WAS reimbursed

c. all deductible by employer

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

58

Problem 9 - 52Automobile $2,500Moving Expenses 4,000Entertainment 1,500Travel 2,000Meals 500Prof Dues and Subs 500

Have “issues” with any of these?Same facts as textbook?

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

59

Problem 9 - 52Automobile $2,500Moving Expenses 4,000Entertainment 750Travel 2,000Meals 500Prof Dues and Subs 500

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

60

Problem 9 - 52Automobile $2,500Moving Expenses 4,000Entertainment 750Travel 2,000Meals 250Prof Dues and Subs 500

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

61

Problem 9 - 52Automobile $2,500Moving Expenses FOR 4,000Entertainment 750Travel 2,000Meals 250Prof Dues and Subs 500Total $10,750

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

62

Problem 9 - 52Automobile $2,500Moving Expenses FOREntertainment 750Travel 2,000Meals 250Prof Dues and Subs 500Total $6,000Less: 2% of $120,000 2,400Deduction $ 3,600

b. from; tier 2

© Copyright 2001-2005 by M. Ray Gregg. All rights reserved.

64