What to do about financial markets? Clas Wihlborg Chapman University and Copenhagen Business School.

24

What to do about financial markets? Clas Wihlborg Chapman University and Copenhagen Business School

-

Upload

cristal-hare -

Category

Documents

-

view

213 -

download

0

Transcript of What to do about financial markets? Clas Wihlborg Chapman University and Copenhagen Business School.

What to do about financial markets?

Clas Wihlborg

Chapman University and Copenhagen Business School

Starting point

We are still not out of the woods; the woods being the financial crisis that begun with the subprime loan failures in the US in 2007.

The financial markets can themselves handle even larger wealth losses without causing crises. Evidence: IT bubble bursting in 2001

Some actors, in particular financial institutions do not seem able to handle large losses. Why not? Why then do they get themselves into such situations? What legal and regulatory remedies are available for the future?

Outline Reviewing the debate:

Why the inability to handle losses this time? Why then did financial institutions get themselves

into the problems? What legal and regulatory remedies are there for

the future? General approaches• The Band-aid approach. Costs • Rein in greed through regulation. Costs • Market discipline; can it be made to work?

Market failures as basis for regulation 1. Externalities; systemic risk/contagion 2. Agency problems 3. Financial markets as markets for information

Implications for role of markets and governments; Policy proposals

Why the inability to handle losses? Leverage of financial institutions Externalities: Contagion/Systemic risk

meaning that individual firms do not take into account effects of own decisions on other firms Runs on opaque banks Payment and settlement system Price effects of fire sales Liquidity effects

Lack of procedures for allocation of losses Waiting for government action to resolve

problems

Why then do FIs get into such vulnerable position? Look at: Weak incentives to hold buffers against credit

losses (capital) and liquidity drain. (Lack of) Market discipline on risk-taking Regulation (Basel) substituting for analysis

Incentives of management on different levels Externalities (as above) Markets for information in system of layers of

institutions (for example, use of ratings) Behavioral explanations (time horizon, band

wagons, risk-evaluation models) Macroeconomic policy and environment

encouraging credit growth and leverage

What legal and regulatory remedies are available for the future? Approaches 1. The Band-Aid approach 2. Rein in market greed through regulation 3. Remove sources of failing incentives 4. Politics and institutions for loss allocation Current politics in the US: Populism, tax payer

and middle class revolt against bail-outs and greed

In Europe: “Schadenfreude” that the failure originated in Anglo-saxon financial system Not much awareness that Europe’s contribution to

the crisis was substantial; 40% of subprime mortgages held in Europe.

Band-aid approach

Apply remedy where-ever behavior seems to have contributed to crisis (G-20 list)

Costs: No coherent philosophy Each remedy has unintended and unforeseeable

consequences “Boundary problem”: If regulation is contrary to

incentives, market participants find a way Complexity Regulatory resources and capabilities

Rein in “greed”; “moral capitalism”

E.g. regulation of compensation, constraints on activities, regulate hedge funds, etc. based on presumption that markets cannot be

made to work with social efficiency that government/regulator knows what risks are,

where credit should go, what compensation is appropriate, etc.

Costs Requires strict regulation Lack of competition and pluralism Lack of innovation in financing and governance Boundary problem and unintended consequences

Remove sources of failing incentives

Limit explicit and implicit protection of banks’ shareholders, managers and creditors

Identify sources of market failure Lack of competition (not discussed) Externalities (systemic effects) Agency problems Financial markets as markets for information Legal framework for contractual enforcement Time (in) consistency in government policy

Costs Can market failures be addressed sufficiently?

Limiting protection

Explicit deposit insurance Primarily for purpose of consumer protection But system must have credibility

• Fast payout• Large enough to discourage government from issuing

“blanket guarantee”

Implicit protection of shareholders and creditors No “Too Big to Fail”

Key issue is that groups of creditors must face risk in addition to shareholders in order to avoid moral hazard problem (shifting risk to deposit insurance fund and tax-payers)

Externalities (systemic effects) Traditional banking view:

Runs on opaque banks Contagion through payment and settlement systems

Extending contagion beyond banking Price effects from fire sales Liquidity effects in markets for securities (Increased

reliance on markets implies price sensitivity to liquidity; “disappearing markets)

If financial institutions (FIs) do not “internalize” effects of their own possible distress on distress of others they will accept too high a likelihood of insolvency and too high a likelihood of illiquidity. Depends on risk-incentives (to incorporate systemic

effects)

Agency problems (i) Limited liability + protection of FI’s creditors (ii) Layers of FIs with potential agency

problem between layers Originate, distribute, service of securities; possible

separation of functions with securitization Unbundling of interest rate and default risk

(iii) Compensation schemes Sufficient incentives for risk-evaluation in

markets? Market for risk-assessment services (ratings) Does regulation of risk evaluation (e.g. Basel)

substitute for own analysis?

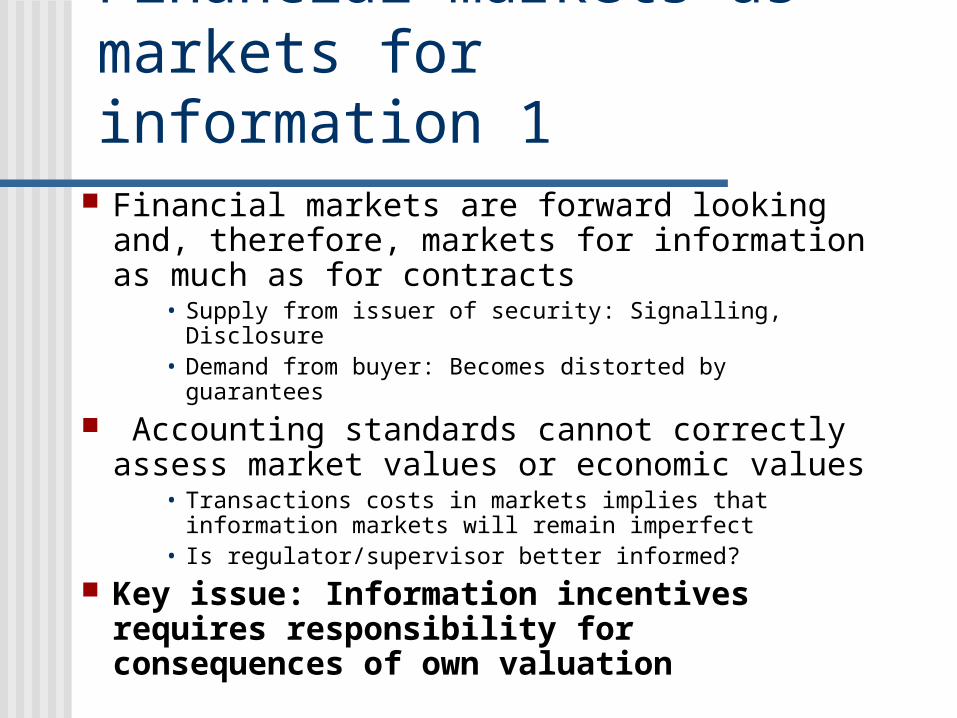

Financial markets as markets for information 1

Financial markets are forward looking and, therefore, markets for information as much as for contracts

• Supply from issuer of security: Signalling, Disclosure• Demand from buyer: Becomes distorted by guarantees

Accounting standards cannot correctly assess market values or economic values

• Transactions costs in markets implies that information markets will remain imperfect

• Is regulator/supervisor better informed?

Key issue: Information incentives requires responsibility for consequences of own valuation

Financial markets as markets for information 2 Incentives to supply information

requires lack of protection and that accounting or other valuation standards do not substitute for own valuation Basel problem

Information intermediaries like ratings agencies must not get official stamp through regulation (Basel problem)

Diversity>>stability

Financial markets as markets for information 3 A Macro prudential digression:

Bubbles are formed when expectations of others’ expectation drive prices without anchor in fundamentals

Expectations about fundamentals are generally diverse when prices are based on fundamentals

Interviewing market participants about where they expect prices to go should provide information about diversity relative to observed price

Can macro prudential agency obtain information about lack of diversity as an indication of bubble?

Otherwise there are serious doubts that an agency is well equipped to judge what price movements are bubbles as opposed to fundamentals.

Contractual enforcement

Legal framework with predictability With respect to consequences of mistakes With respect to losses from lending to financial

institution in distress Allocation of losses of failed FI

• Rules for valuation of failed FIs assets• Prompt valuation• Prompt pay-out with “hair cuts”

Key issue: Need for special insolvency law for banks and similar FIs providing predictability and promptness to reduce likelihood of runs

Time consistency in government policy

Credibility of non-bail out policy requires distress resolution procedures that enable even big FIs to fail without creating great systemic problems through Payment and settlement Price effects of fire sales Liquidity effects

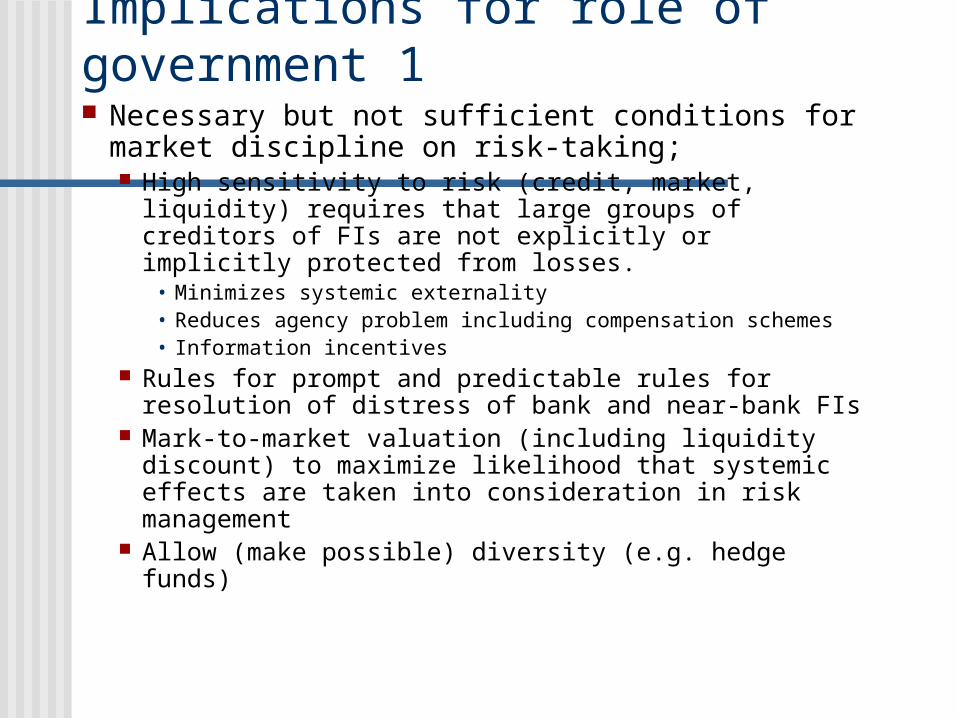

Implications for role of government 1 Necessary but not sufficient conditions for market

discipline on risk-taking; High sensitivity to risk (credit, market, liquidity) requires

that large groups of creditors of FIs are not explicitly or implicitly protected from losses.

• Minimizes systemic externality• Reduces agency problem including compensation schemes• Information incentives

Rules for prompt and predictable rules for resolution of distress of bank and near-bank FIs

Mark-to-market valuation (including liquidity discount) to maximize likelihood that systemic effects are taken into consideration in risk management

Allow (make possible) diversity (e.g. hedge funds)

Implications for role of government 2 Remaining market failures/externalities

requires: LOLR Consideration of Liquidity externality Systemic risk contribution in Capital regulation Preparedness for distress resolution Valuation rules for non-traded assets Consideration of the international dimension

Proposals 1

Capital regulation Higher average capital requirement Allow capital to serve as buffer to reduce

procyclicality Leverage ratio based on market valuation of

assets Link to contribution to systemic risk (TBTF)

• Size• “Interconnectedness”; Note that being large

counterparty to one or few FIs is worse than being small counterparty to many

Consideration of mismatch of maturities

Proposals 2

Rule based, mandatory procedures for distress resolution;promptness, predictability and a minimum of contagion Mandatory rules for Structured early intervention

• Enhance buffer role of capital• Reduce likelihood of insolvency• Mandatory closure rule• Rules for allocation of losses in bridge bank

Mandatory rules should maximize credibility of non-bail out policy

Valuation based on mark-to-market principle• Valuation for external accounting need not be the same

as valuation for regulation and loss allocation. • Mark-to-market does not require efficiency of market

valuation. It increases risk Liquidity risk awareness

Proposals; The international dimension

Cross-border banking increases complexity of distress resolution with conflicts of interest arising among countries Legal subsidiary under host country supervision and

law must be a subsidiary functionally as well as legally (note (New Zealand rule on out-sourcing of functions)

Claims of foreign branches must be treated in a non-discriminatory manner in distress resolution by home authorities

EU single banking license based on mutual recognition was a good idea but it requires a working framework for distress resolution in home or host country.

Macro prudential considerations

Enhance buffer role of capital Role of diversity in markets; Can

government regulator be relied on to identify bubbles vs shifts in fundamentals? Good times vs bad times to reduce

procyclicality of capital requirements?

Final thoughts• In an efficient as well as stable financial

system we would expect to see failures of financial institutions as a normal occurrence

• Failures should not be seen as an aberration threatening the system

• Government involvement in failures should be avoided since expectations about such involvement delay adjustment, distort incentives and conserve inefficient structures