What Should Commissioners Consider when Reviewing Arizona Resource Plans? Presentation to the...

20

What Should Commissioners Consider when Reviewing Arizona Resource Plans? Presentation to the Arizona Corporation Commission September 11, 2014 Docket No. E-00000V-13-0070 David Berry 1 [email protected]

-

Upload

kathlyn-wilcox -

Category

Documents

-

view

217 -

download

3

Transcript of What Should Commissioners Consider when Reviewing Arizona Resource Plans? Presentation to the...

1

What Should Commissioners Consider when Reviewing Arizona Resource Plans?

Presentation to theArizona Corporation Commission

September 11, 2014Docket No. E-00000V-13-0070

David Berry

2

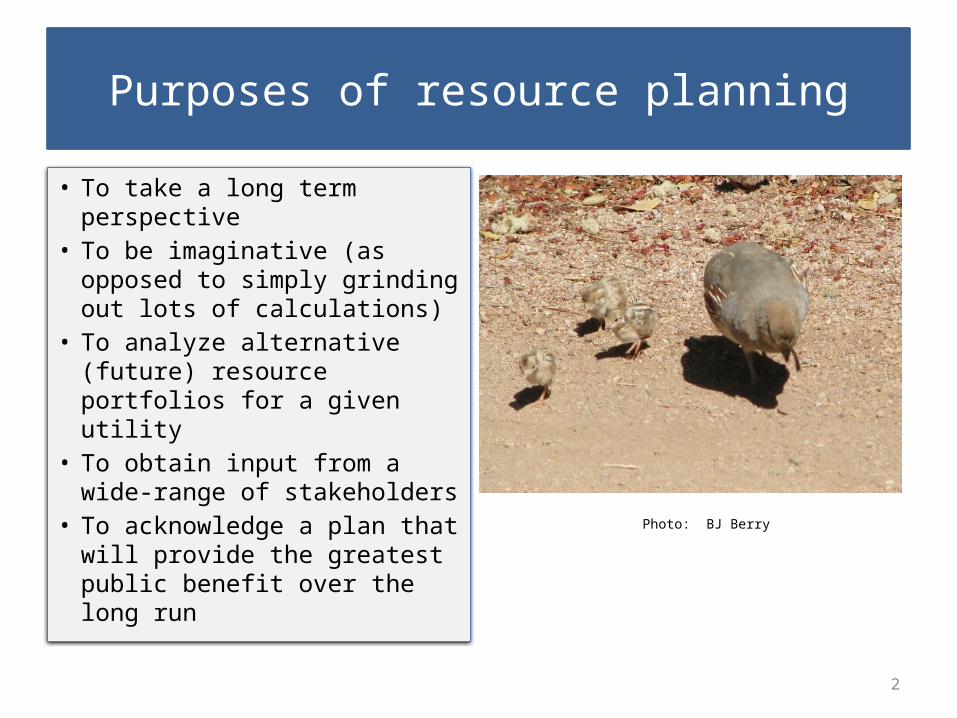

Purposes of resource planning

• To take a long term perspective

• To be imaginative (as opposed to simply grinding out lots of calculations)

• To analyze alternative (future) resource portfolios for a given utility

• To obtain input from a wide-range of stakeholders

• To acknowledge a plan that will provide the greatest public benefit over the long run

Photo: BJ Berry

3

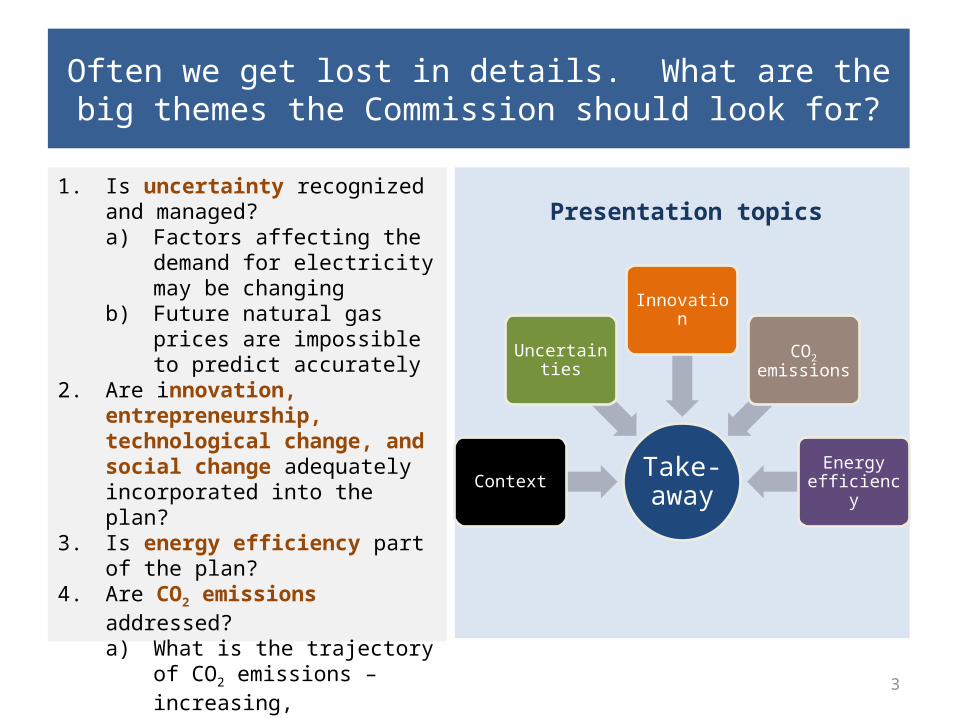

Often we get lost in details. What are the big themes the Commission should look for?

1. Is uncertainty recognized and managed? a) Factors affecting the demand for

electricity may be changingb) Future natural gas prices are

impossible to predict accurately2. Are innovation, entrepreneurship,

technological change, and social change adequately incorporated into the plan?

3. Is energy efficiency part of the plan?4. Are CO2 emissions addressed?

a) What is the trajectory of CO2 emissions – increasing, decreasing?

b) How can CO2 emissions be reduced?

Take-awayContext

Uncertainties

Innovation

CO2 emissions

Energy efficiency

Presentation topics

4

Context: AZ electricity prices are generally lower than 20 years ago:

electricity prices reflect additions of new facilities & fuel prices 19

9019

9119

9219

9319

9419

9519

9619

9719

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

125

6

7

8

9

10

11

12

13

14

15

Average Arizona Electricity Prices(2009 cents/kWh)

residential commercialindustrial total

2009

cen

ts p

er k

Wh

Factors affecting prices• Depreciation of large capital

additions – Coal & nuclear plants

completed in the 1980s and 1990:• Springerville 2, 1990• Palo Verde (1986-1988)• Springerville 1, 1985• 1980: Cholla 3, Craig 1,

Coronado 2

– Springerville 4, 2009• Very high natural gas prices,

2005-2008 (lagged effect via fuel adjustors)

• RES, DSM program costs (much less than $0.01/kWh)

5

Context: APS’s vision of 2029 according to its resource plan (selected portfolio)

Energy mix: over half the MWh come from fossil fuel combustion

Capacity mix ~ 70% relies on fossil fuelsNote: gas capacity factor = 23%

nuclear; 1,146

coal; 1,932

gas; 7,137

renewable; 827

distributed energy;

261

demand response;

275

efficiency; 1,447

APS MW Contribution at Peak in 2029: Selected Portfolio(13,025 MW total)

nuclear18%

coal24%gas

28%

re+de14%

ee15%

APS Energy (MWh) Mix, 2029, Selected Portfolio, Current Path Scenario

6

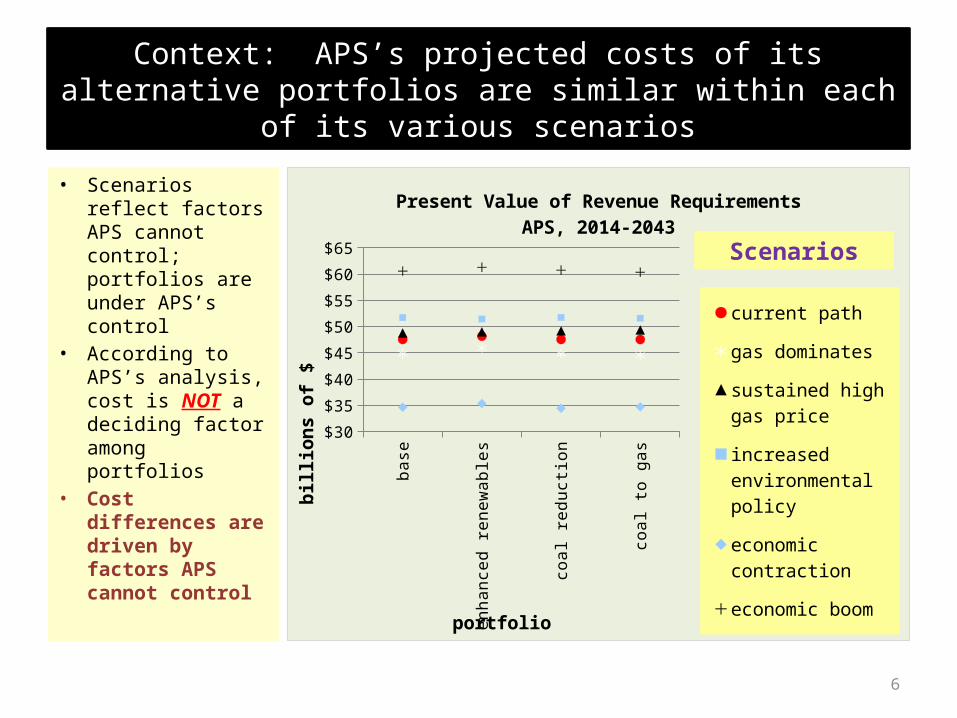

Context: APS’s projected costs of its alternative portfolios are similar within each of its various scenarios

• Scenarios reflect factors APS cannot control; portfolios are under APS’s control

• According to APS’s analysis, cost is NOT a deciding factor among portfolios

• Cost differences are driven by factors APS cannot control

base

enha

nced

ren

ewab

les

coal

red

uctio

n

coal

to g

as

$30

$35

$40

$45

$50

$55

$60

$65

Present Value of Revenue RequirementsAPS, 2014-2043

current path

gas dominates

sustained high gas price

increased environmen-tal policy

economic contraction

economic boomportfolio

billi

ons

of $

Scenarios

7

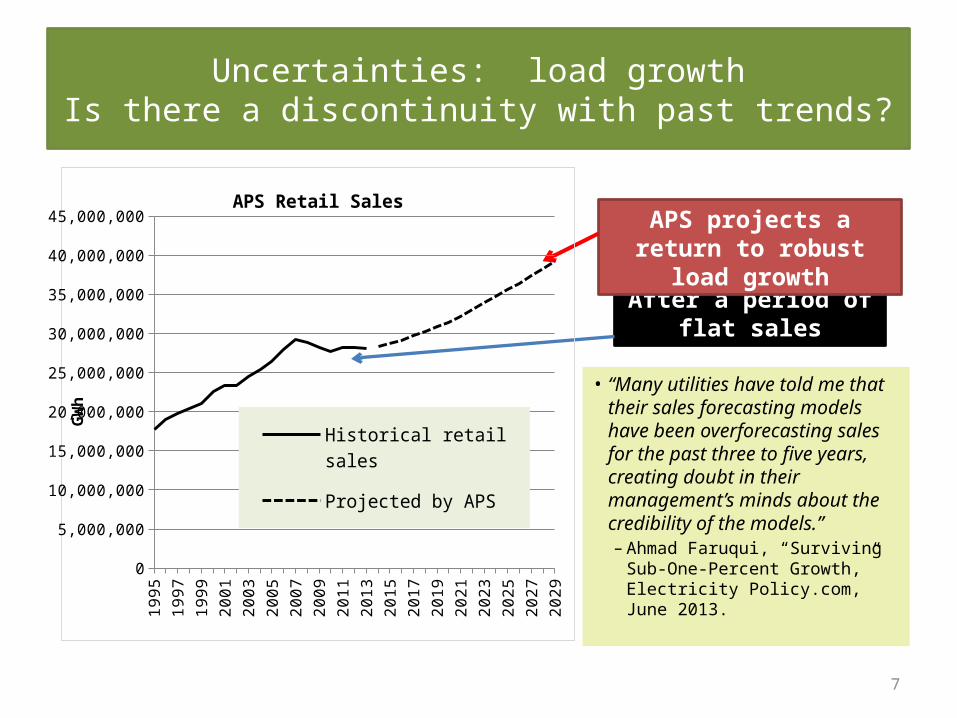

Uncertainties: load growthIs there a discontinuity with past trends?

After a period of flat sales

• “Many utilities have told me that their sales forecasting models have been overforecasting sales for the past three to five years, creating doubt in their management’s minds about the credibility of the models.”– Ahmad Faruqui, “Surviving Sub-

One-Percent Growth,” Electricity Policy.com, June 2013.

APS projects a return to robust load growth

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

2021

2023

2025

2027

20290

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

45,000,000APS Retail Sales

Historical retail sales

Projected by APS

GW

h

8

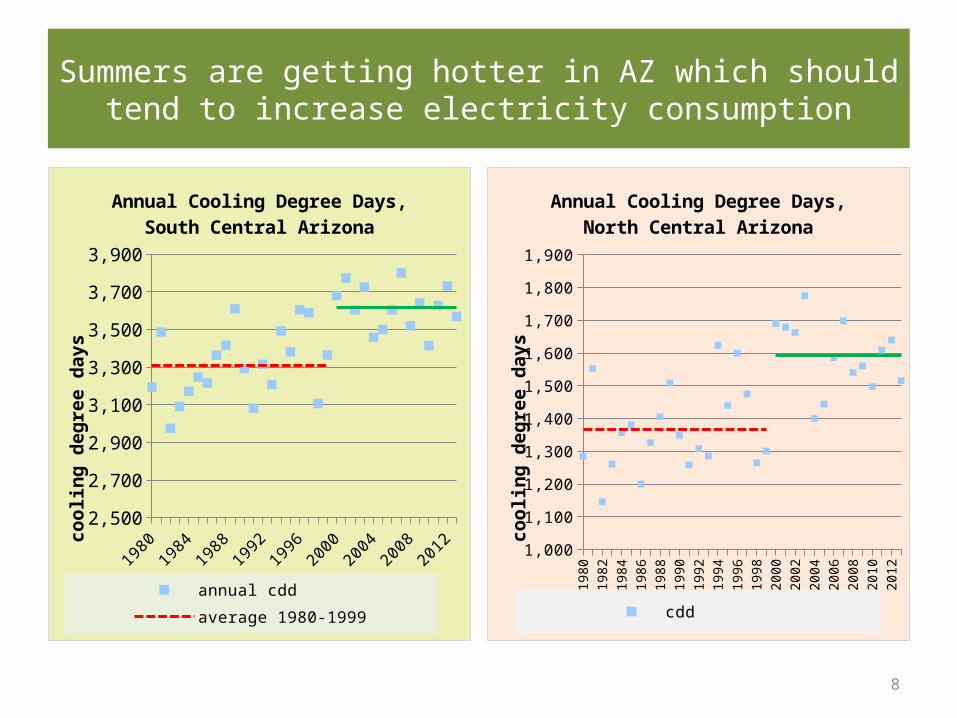

Summers are getting hotter in AZ which should tend to increase electricity consumption

19801983

19861989

19921995

19982001

20042007

20102013

2,500

2,700

2,900

3,100

3,300

3,500

3,700

3,900

Annual Cooling Degree Days, South Central Arizona

annual cddaverage 1980-1999average 2000-2013

cool

ing

degr

ee d

ays

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

Annual Cooling Degree Days, North Central Arizona

cdd avg 1980-1999avg 2000-2013

cool

ing

degr

ee d

ays

9

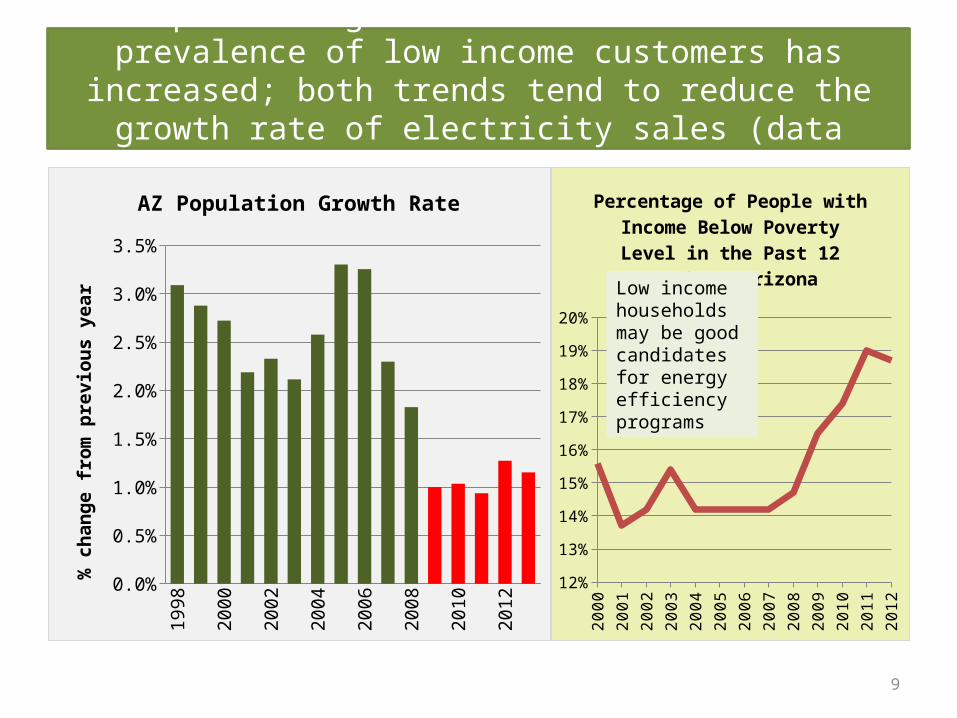

Population growth has slowed and the prevalence of low income customers has increased; both trends tend to reduce the growth

rate of electricity sales (data source: Census Bureau)19

9819

9920

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

13

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

AZ Population Growth Rate

% c

hang

e fr

om p

revi

ous

year

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

12%

13%

14%

15%

16%

17%

18%

19%

20%

Percentage of People with Income Below Poverty Level in the Past 12

Months: Arizona

Low income households may be good candidates for energy efficiency programs

10

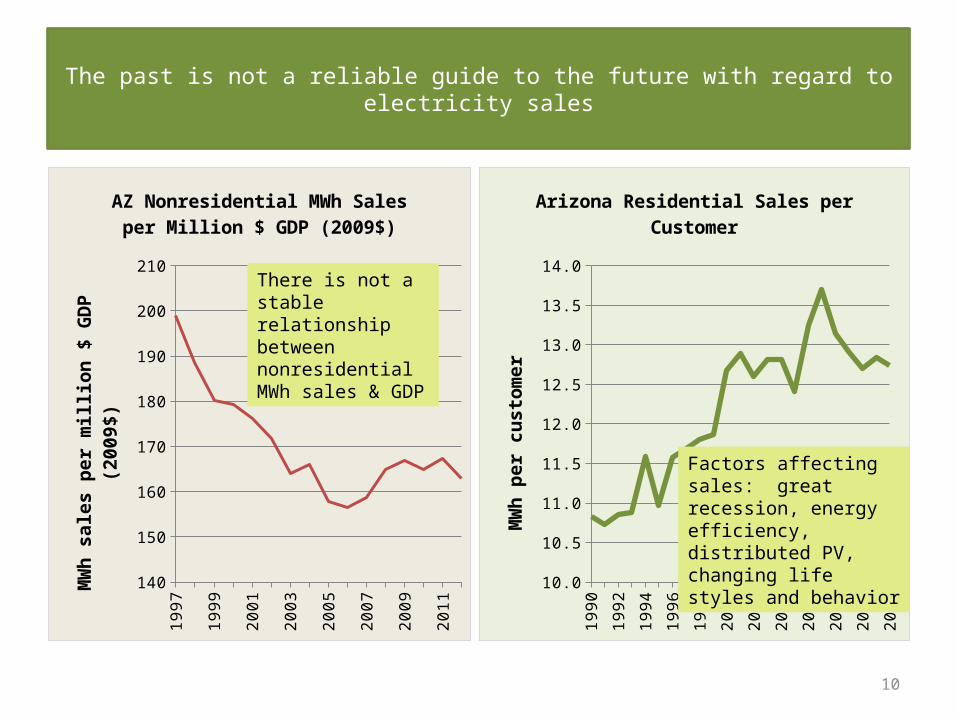

The past is not a reliable guide to the future with regard to electricity sales

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

10.0

10.5

11.0

11.5

12.0

12.5

13.0

13.5

14.0

Arizona Residential Sales per Customer

MW

h pe

r cus

tom

er

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

140

150

160

170

180

190

200

210

AZ Nonresidential MWh Sales per Million $ GDP (2009$)

MW

h sa

les

per m

illio

n $

GD

P (2

009$

)

Factors affecting sales: great recession, energy efficiency, distributed PV, changing life styles and behavior

There is not a stable relationship between nonresidential MWh sales & GDP

11

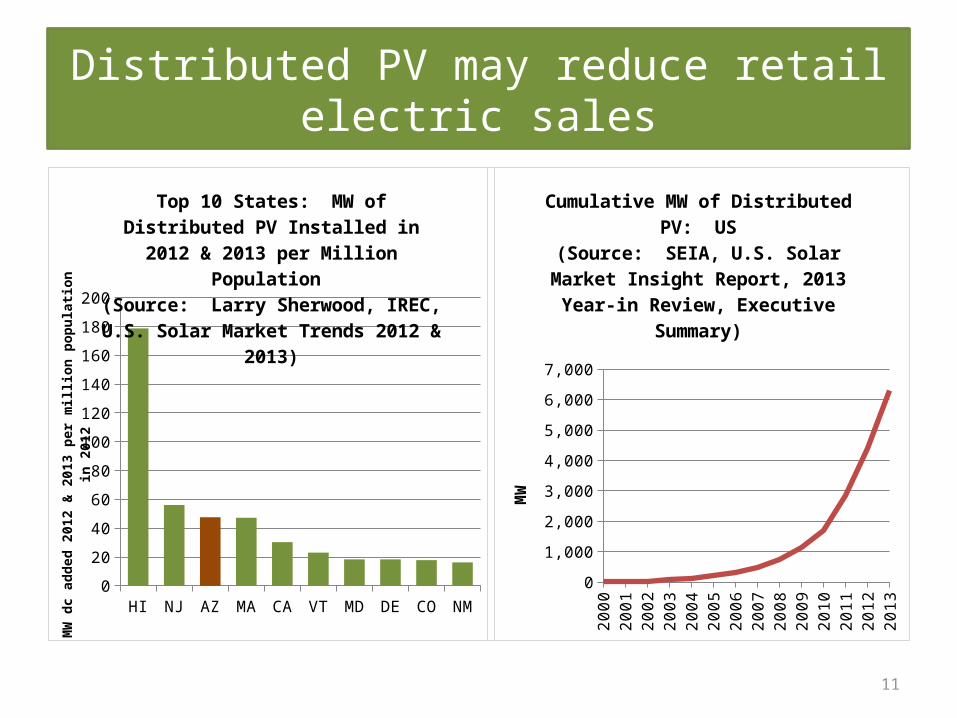

Distributed PV may reduce retail electric sales

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Cumulative MW of Distributed PV: US(Source: SEIA, U.S. Solar Market Insight Report, 2013 Year-in Review, Executive

Summary)

MW

HI NJ AZ MA CA VT MD DE CO NM0

20

40

60

80

100

120

140

160

180

200

Top 10 States: MW of Distributed PV In-stalled in 2012 & 2013 per Million Popula-

tion (Source: Larry Sherwood, IREC, U.S. Solar

Market Trends 2012 & 2013)

MW

dc a

dded

201

2 &

201

3 pe

r mill

ion

popu

latio

n in

201

2

12

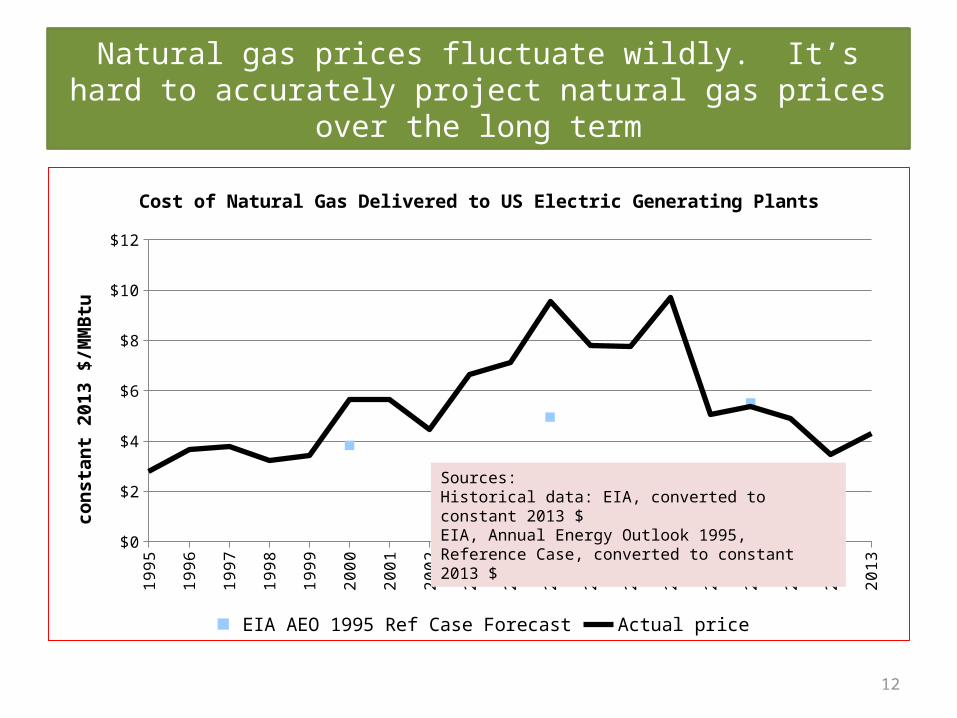

Natural gas prices fluctuate wildly. It’s hard to accurately project natural gas prices over the long term

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

$0

$2

$4

$6

$8

$10

$12

Cost of Natural Gas Delivered to US Electric Generating Plants

EIA AEO 1995 Ref Case Forecast Actual price

cons

tant

201

3 $/

MM

Btu

Sources:Historical data: EIA, converted to constant 2013 $EIA, Annual Energy Outlook 1995, Reference Case, converted to constant 2013 $

13

Innovation can occur rapidly and can profoundly change an industry

• A few examples of recent innovations– PV on noise barriers, at airports, in

the water supply system– PowerParasols®

– Leasing model for rooftop solar– Market transformation for energy

efficiency– Energy storage– Micro-grids– Solar roadways (?)

• Taken together these & other innovations may result in significant disruptions to business as usual

Photo: BJ Berry

14

Energy efficiency market transformation: new pathways to energy efficiency

Through creation of social capital• Social capital consists of shared norms,

expectations, and understanding • Mobilizing resources: community

organizations educate consumers, train contractors, distribute efficiency measures, offer personalized assistance to consumers, etc.

• Creating social capital: these organizations advance energy efficiency by fostering trust, empowering communities to take ownership of efficiency programs, using social networks to increase participation, & using partnerships to expand their own capabilities

Through market opportunities and entrepreneurship

• Opportunities to apply best practices– Many large companies such as Kroger

have clean energy goals & programs• Opportunities for information and

communications – Identifying wasted energy in building

operations by using smart meter data combined with weather & other data

– Using smart phone apps to control thermostats or appliances remotely

– Smart homes• More efficient design

– Meritage Homes

15

What is the trajectory of carbon dioxide emissions?

Factors affecting emissions decline:

• Coal plant retirements

• Improved energy efficiency

• Renewable energy

• The great recession

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

150

160

170

180

190

200

210

220

230

240

250

CO2 Emissions from Electric Generation(AZ, NM, NV, UT, CO, WY)

actual trend

mill

ion

met

ric

tons

of C

O2

16

How can Arizona reduce its CO2 emissions rate (lbs per MWh) from fossil fuel plants to meet the proposed EPA carbon rule?

1. EPA’s proposed rule would require significant decreases in the emission rates of fossil fuel power plants in AZ* EPA’s 2030 goal for AZ is 702 pounds per net MWh. This goal

pertains to the state, not to individual utilities. 2. Practical steps AZ utilities could take to reduce CO2 emissions

Continue energy efficiency programs consistent with the energy efficiency standard

Increase the use of renewable resources (geothermal, solar, & wind)

Substitute gas-fired generation for coal-fired generation* AZ coal units are Apache Station, Cholla, Coronado, and Springerville (other coal plants

serving AZ customers are in Indian country or in other states)

17

Under APS’s IRP, total CO2 emissions will increase but APS‘s emissions intensity declines

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

10,000,000

11,000,000

12,000,000

13,000,000

14,000,000

15,000,000

16,000,000

17,000,000

18,000,000

19,000,000

APS CO2 Emissions Trajectories:Current Path Scenario

base enhanced renewables

coal reduction coal to gas

mill

ions

of m

etric

tons

of C

O2

Note: this is not EPA’s method of calculating emissions rates

base

enhanced renewables

coal reduction

coal to gas

-300 -250 -200 -150 -100 -50 0

Change in APS CO2 Emission Rate 2014 to 2029(current path scenario; relative to all MWh)

Change in emissions rate (pounds per MWh)

18

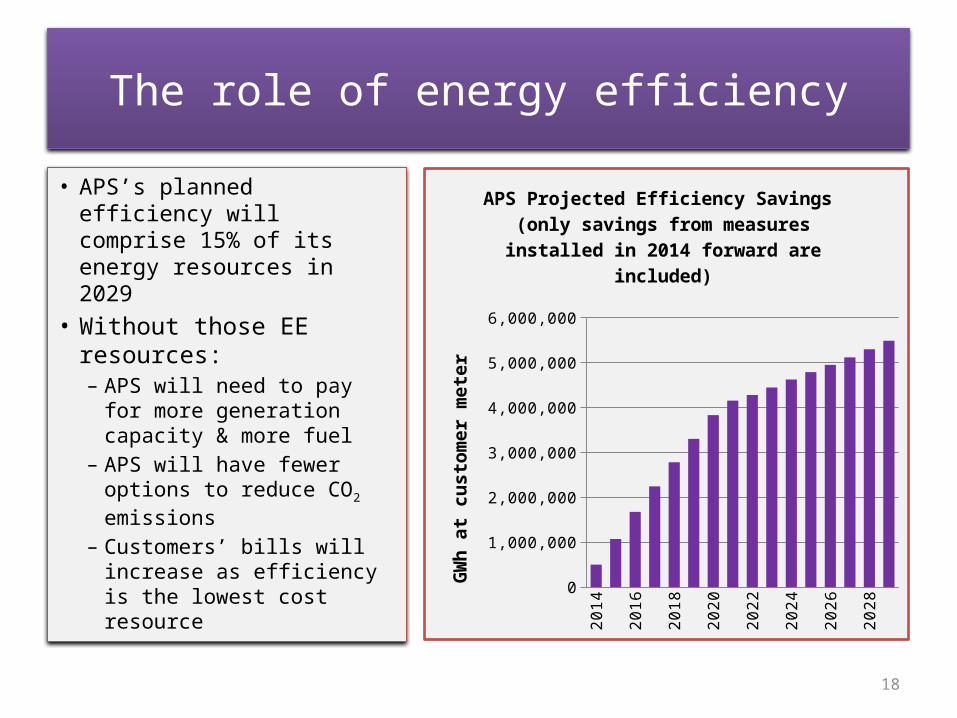

The role of energy efficiency

• APS’s planned efficiency will comprise 15% of its energy resources in 2029

• Without those EE resources:– APS will need to pay for

more generation capacity & more fuel

– APS will have fewer options to reduce CO2 emissions

– Customers’ bills will increase as efficiency is the lowest cost resource 20

1420

1520

1620

1720

1820

1920

2020

2120

2220

2320

2420

2520

2620

2720

2820

29

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

APS Projected Efficiency Savings (only savings from measures installed in 2014

forward are included)

GW

h at

cus

tom

er m

eter

19

2 minute take-away for the Commission

In reviewing the 2014 resource plans, the Commission should consider: The uncertainty of load growth Fossil fuel price risk, especially natural gas prices CO2 emissions & impactsThe role of renewable energy and energy efficiency

• Renewable energy is a stably priced, commercially available resource that manages fuel cost uncertainty and reduces CO2 emissions

• Energy efficiency programs are effective, reduce CO2 emissions, and reduce utility and customer exposure to higher costs of electricity

20

2 minute take-away for the Commission

The Commission should ask whether policies encourage innovation and its benefits or whether policies lock out new technologies or create barriers to new market entrants

• Beneficial change is being driven by:– Innovation and entrepreneurship, especially from

outside the electric utility industry– Increasing societal & market receptivity to energy

efficiency and distributed renewable energy– Learning by consumers, entrepreneurs, utilities