What happens when property finance goes wrong (before and after lending)? Monday 14 September 2009...

27

What happens when property finance goes wrong (before and after lending)? Monday 14 September 2009 Jonathan Lawrence, Partner, K&L Gates LLP

-

Upload

teresa-robbins -

Category

Documents

-

view

218 -

download

2

Transcript of What happens when property finance goes wrong (before and after lending)? Monday 14 September 2009...

What happens when property finance goes wrong (before and after lending)?

Monday 14 September 2009 Jonathan Lawrence, Partner, K&L Gates LLP

2

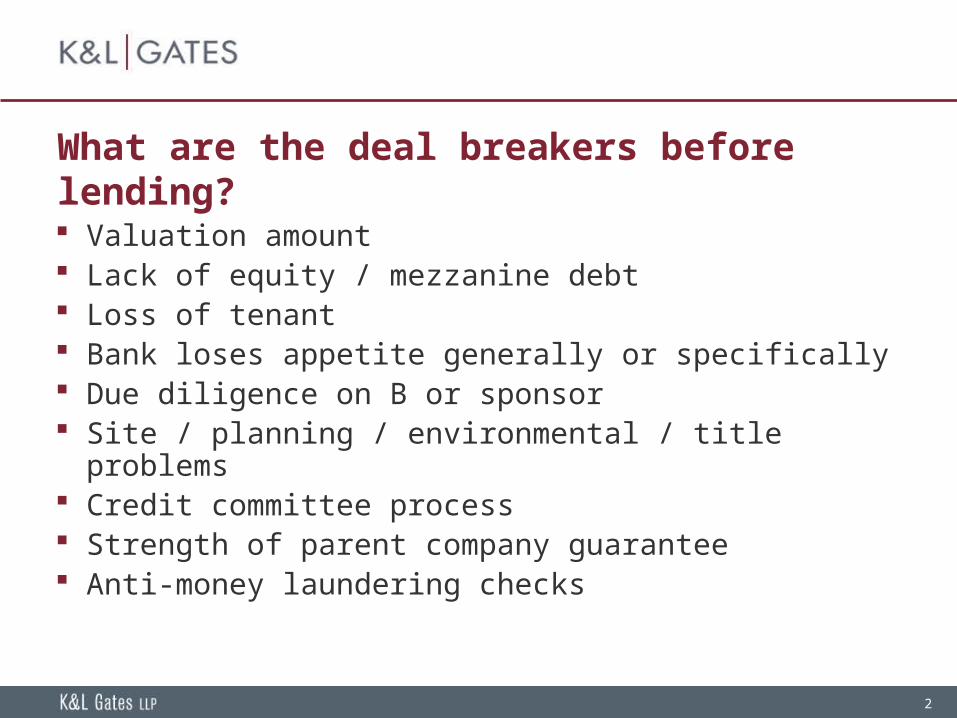

What are the deal breakers before lending? Valuation amount Lack of equity / mezzanine debt Loss of tenant Bank loses appetite generally or specifically

Due diligence on B or sponsor Site / planning / environmental / title problems

Credit committee process Strength of parent company guarantee Anti-money laundering checks

3

What happens when a loan can’t be serviced? Amendment and waiver (especially of interest rate, covenants and payment schedules)

Offering cash deposits, more security and guarantees

Finding new tenants / upgrading the property

Handing back the keys Court proceedings Insolvency / receivership

4

Security

Legal mortgage Fixed charge Assignment of rental income Floating charge Guarantees Negative pledge

5

Legal mortgage

Over specified real estate Transfer of legal ownership from mortgagor (B) to mortgagee (L)

Mortgagor has right to return of property and payment of any balance after satisfaction of mortgage (right of redemption)

6

Fixed charge

All other freehold and leasehold property All buildings, fixture, plant and machinery on the property

All future interests in land Benefit of all agreements relating to land Right and interest in proceeds of sale of charged property

Amount standing to credit of all bank accounts Book debts and other receivables Goodwill and uncalled capital Right to recover VAT on any supplies relating to charged property

7

Assignment by way of security

Rental income Right to payment under all present and future insurance policies over any charged property

Rights against any tenants of property Benefit of any hedging documentation Rights under any development and acquisition documentation

Benefit of all contracts relating to property

8

Other security

Floating charge Over all other assets of B not covered by the other security

Crystallisation Share charge over shares in B

L has opportunity to take control of B Choice to sell B rather than the property

Negative pledge

9

Practicalities

Security documentation must be correctly registered (“perfected”) English company: Companies House Non-English company: all companies - Slavenburg register (pre 1 October 2009) / only if registered place of business in UK (1 October 2009 and thereafter)

Land Registry Otherwise void against liquidator, administrator, creditor of the company

Governing law – location of assets?

10

Guarantees

Especially relevant when dealing with SPV B with no trading history where real estate is sole asset

L should ensure the guarantor enters guarantee as a primary obligor and therefore has to immediately comply with any demand made on the guarantee without L having to first make demand of B

Guarantor likely to seek grace period

11

Why is the security package so important? Security Trustee has certain control over all assets of B

Ideally only security over property itself is needed to recover the principal amount of the loan

Remaining security satisfies L’s underwriting in case the LTV covenant is breached

12

Pre-insolvency: Protection for the Lender Most importantly through security

Fixed charge Floating charge

Security Trustee Effect? Enforcement and realisation 100% flawless?

No…

13

Deficiencies with taking security

Floating charges and the “prescribed part”

Statutory order of priority of proceeds

Moratorium (with certain insolvency proceedings)

Deficiencies in realisation

14

Who can challenge a bank’s security?

The borrower The guarantor or other security provider

The liquidator or administrator The shareholders (where directors exceed their powers)

15

What challenges to security are available? Lack of commercial benefit Preference Transaction at an undervalue Avoidance of floating charges Unfair contract terms Undue influence Variations to secured sums

16

Enforcement

B unable to repay loan B has breached its covenants Enforcing security and insolvency procedures

17

What is insolvency?

When a corporate entity “is unable to pay its debts” (Section 123 Insolvency Act 1986)

Tests Failure to pay a statutory demand Execution on a judgement is unsatisfied Unable to pay its debts as they fall due (“cash flow” test)

Value of assets less than liabilities (“balance sheet” test)

Threshold amount: £750

18

Relevance to Lenders?

Likelihood of repayment of loans if B insolvent?

Loan agreement contains safeguards: chiefly through events of default and acceleration

How does acceleration help L?

19

Insolvency Procedures

Administrative receivership and fixed asset receivers (e.g. LPA receiver)

Liquidation Administration Compromise arrangements

20

Background to the Enterprise Act 2002

Came into force on 15 September 2003 Promotion of “rescue culture” Abolition of Crown preference Creation of the prescribed part

21

Receiverships, Administrations and Company Voluntary Arrangements in England and Wales registered at Companies House (figures from the Insolvency Service website)

Year Receivership Administrator In Administration Company

Appointments Appointments (Enterprise ActVoluntary

2002) Arrangements

1997 1,837 196 : 6291998 1,713 338 : 4701999 1,618 440 : 4752000 1,595 438 : 5572001 1,914 698 : 5972002 1,541 643 : 6512003 1,261 497 247 7262004 864 1 1,601 5972005 590 4 2,257 6042006 588 0 3,560 5342007 477 2 2,327 399

22

Insolvency Procedures: Receivership The appointment of a person to administer (i.e.

sell) specific property charged to a creditor Administrative Receivership, now relatively rare –

Enterprise Act 2002 limits this to security created before 15 September 2003 and certain other exceptions

Realise certain assets of B charged to appointor to repay indebtedness to appointor

No moratorium Appointment by a qualifying floating charge holder

with a floating charge over all, or substantially all, of the assets of the debtor company

Administrative receiver owes duties solely to appointor

Blocks appointment of administrator LPA Receivership and Fixed Charge Receivership

23

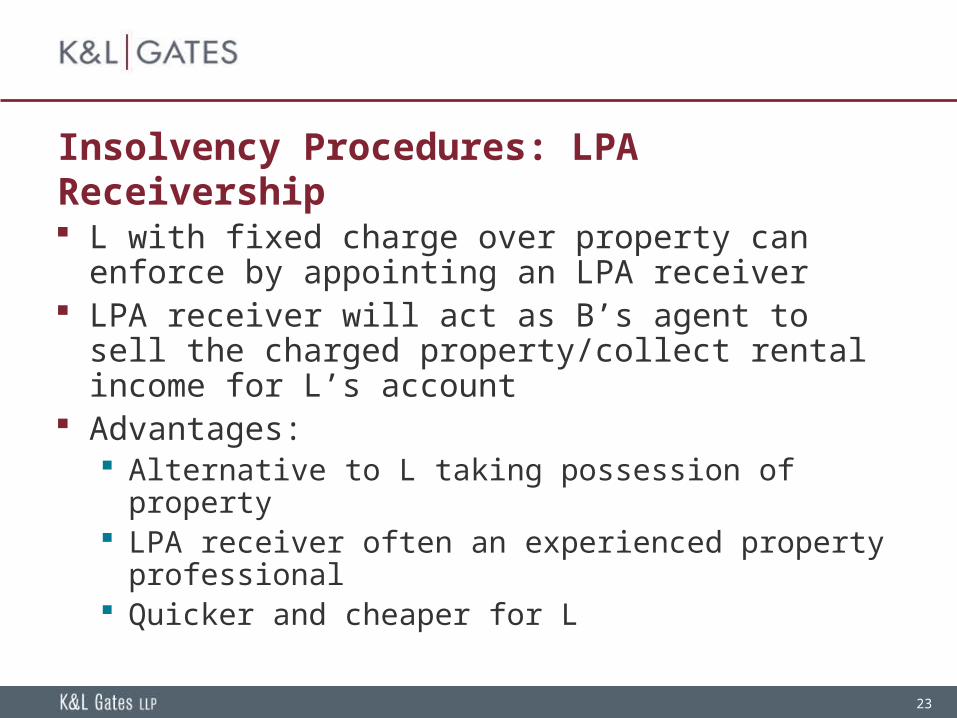

Insolvency Procedures: LPA Receivership L with fixed charge over property can enforce by appointing an LPA receiver

LPA receiver will act as B’s agent to sell the charged property/collect rental income for L’s account

Advantages: Alternative to L taking possession of property

LPA receiver often an experienced property professional

Quicker and cheaper for L

24

Insolvency Procedures: Administration

Active businesses, significant assets, potential Statutory “purposes” brought in by Enterprise Act

2002 Rescue company as a going concern Achieve a better result than in liquidation Realise property for secured (or preferential) creditor

Moratorium Appointment is by notice (company, directors or QFC,

who has overriding powers) or by application to court (company, directors, all creditors)

First ranking QFC can appoint its own choice of administrator

Administrator owes duties to all creditors

25

Insolvency Procedures: Liquidation

Terminal procedure Appointment? Shareholder resolution (voluntary liquidation) or court order (compulsory liquidation)

Realisation, distribution, dissolution Order of priorities Delay in enforcement

26

Administrative Receivership

May be appointed by: Holder of floating charge (created before 15 September 2003) over whole/substantially the whole of assets

Holder of floating charge (created after 15 September 2003) over whole/substantially the whole of assets where a statutory exception applies

Floating charge crystallises Control and management passes to administrative receiver (“AR”)

27

Administrative Receivership

No moratorium triggered AR’s principal duty – realise property in order to repay debt owing to appointer

Often results in quick sale at price sufficient to discharge secured creditor only

Company then usually placed in liquidation