WHAT DO I DO IF I MADE A CARELESS MISTAKE IN MY MATHS PROBLEM SUM? WHAT DOES MY TEACHER DO WHEN HE...

30

WHAT DO I DO IF I MADE A CARELESS MISTAKE IN MY MATHS PROBLEM SUM? WHAT DOES MY TEACHER DO WHEN HE MARKS A QUESTION WRONGLY? WHAT DOES THE CASHIER DO IF SHE GIVES ME THE WRONG CHANGE? WHAT DOES THE UNCLE AT THE GROCERY SHOP DO WHEN HE ADDS UP WRONGLY FOR MY GROCERIES?

-

Upload

avis-young -

Category

Documents

-

view

228 -

download

0

Transcript of WHAT DO I DO IF I MADE A CARELESS MISTAKE IN MY MATHS PROBLEM SUM? WHAT DOES MY TEACHER DO WHEN HE...

WHAT DO I DO IF I MADE A CARELESS MISTAKE IN MY MATHS PROBLEM SUM?

WHAT DOES MY TEACHER DO WHEN HE MARKS A QUESTION WRONGLY?

WHAT DOES THE CASHIER DO IF SHE GIVES ME THE WRONG CHANGE?

WHAT DOES THE UNCLE AT THE GROCERY SHOP DO WHEN HE ADDS UP WRONGLY FOR MY GROCERIES?

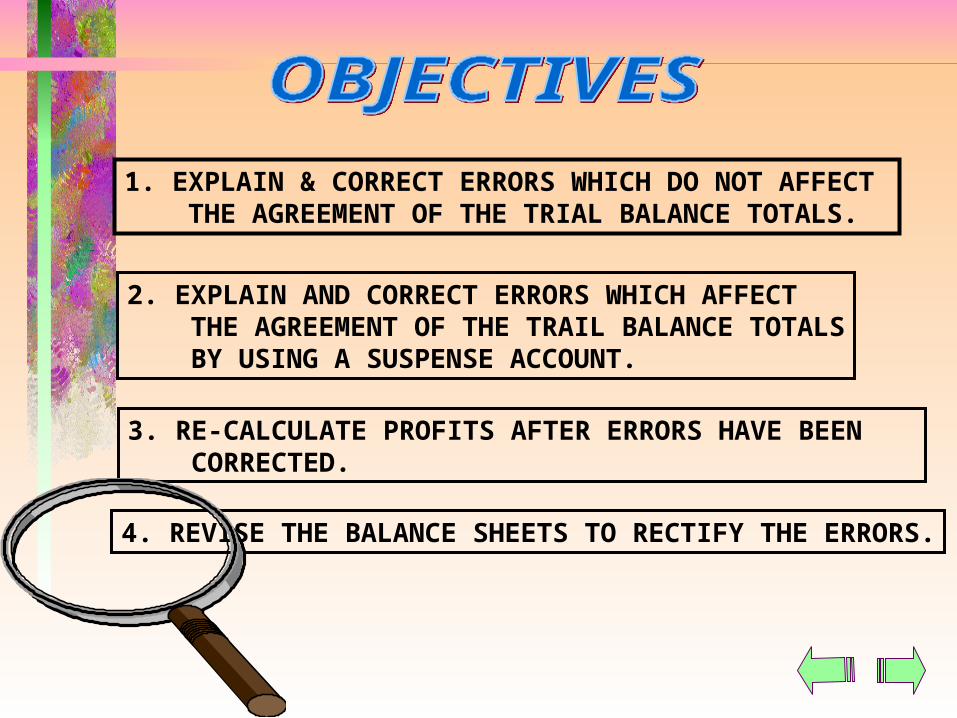

1. EXPLAIN & CORRECT ERRORS WHICH DO NOT AFFECT THE AGREEMENT OF THE TRIAL BALANCE TOTALS.

2. EXPLAIN AND CORRECT ERRORS WHICH AFFECT THE AGREEMENT OF THE TRAIL BALANCE TOTALS BY USING A SUSPENSE ACCOUNT.

3. RE-CALCULATE PROFITS AFTER ERRORS HAVE BEEN CORRECTED.

4. REVISE THE BALANCE SHEETS TO RECTIFY THE ERRORS.

Errors of omission

Errors of commission

Errors of principle

Errors of original entry

Compensating errors

Complete reversal of entries

Errors of omission of one entry

Errors in calculations

Errors in amount

Posting to the wrong side of an account

When a transaction has been completely omitted from the books.

By making a double-entry to record the transaction.

Main

An entry has been posted to the wrong account of the same category.

To reverse the entry in the wrong account and to post the correct entry.

Main

An entry has been posted to the wrong account of a different category.

To reverse the entry in the wrong account and to post the correct entry.

Main

A wrong amount is recorded in a book of original entry or a documentsuch as an invoice and subsequently posted to the ledger accounts.

To correct the difference in the correct and wrong amount accordingly.

Main

An error on the debit side is compensated by an error of equal amounton the credit side.

To reverse the error on both debit and credit sides of the accounts concerned.

Main

When recording a transaction, the debit and credit entries are reversed.

By making the necessary posting of an amount double the amount of the original error.

Main

Forgetting to either debit or credit one side of a transaction.

By making the necessary posting which has been omitted against an entry in the Suspense Account.

Main

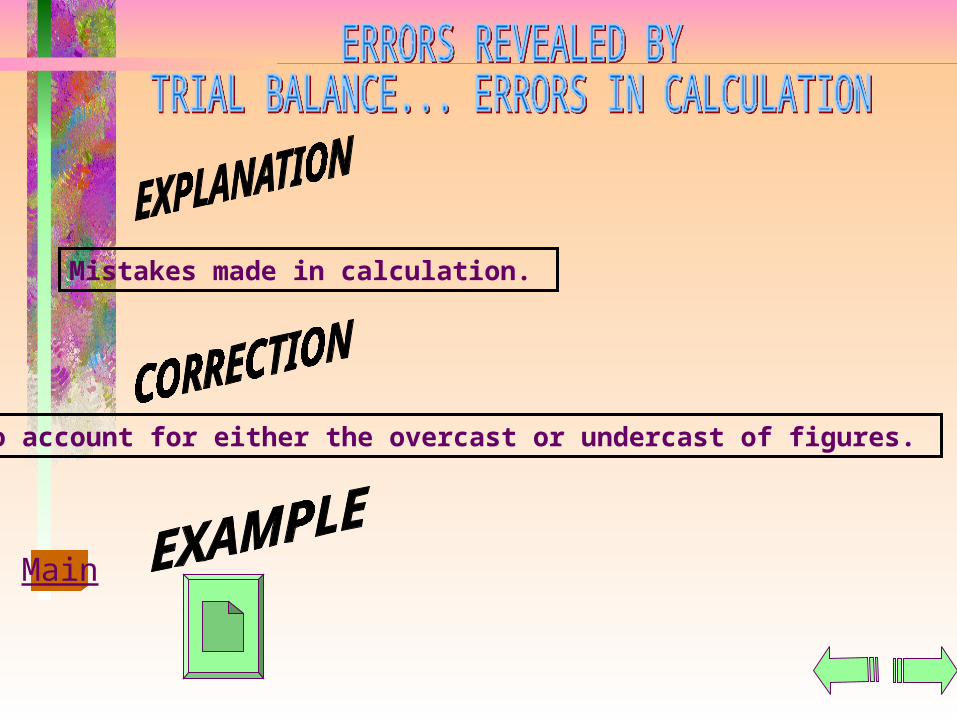

Mistakes made in calculation.

To account for either the overcast or undercast of figures.

Main

The amount debited and the amount credited are different.

To account for either the overcast or undercast of figures accordingly.

Main

Causing one side of the ledger to be more than the other by twice the value of the error.

To make the necessary adjustments against Suspense Account.

Main

A cash payment of $2,000 for purchases has been omittedfrom the books.

Purchases Account $

Cash Account $

Cash 2,000

Purchases 2,000Main

Journal entry

A sale of $1,000 to Carrefour has been posted to Cold Storage -Causeway Point.

Cold Storage - Causeway Point $ $

Sales 1,000

Carrefour $

ERROR MADE

CORRECTION MADE

Carrefour 1,000

Cold Storage - 1,000Causeway Point

Main

Journal entry

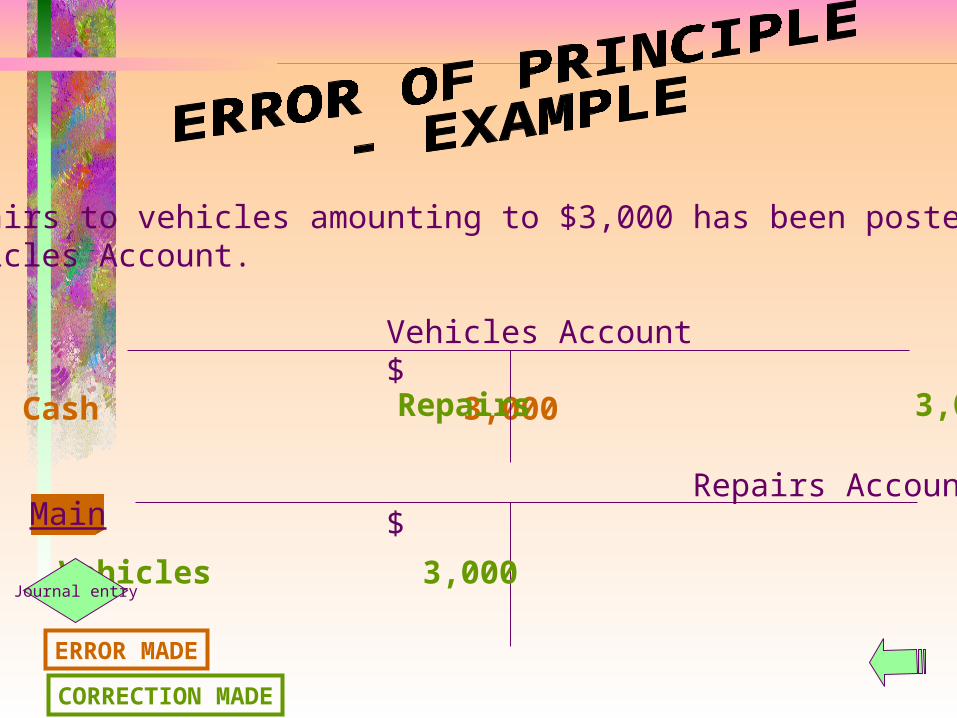

Repairs to vehicles amounting to $3,000 has been posted to Vehicles Account.

Vehicles Account $ $

Cash 3,000

Repairs Account $

ERROR MADE

CORRECTION MADE

Repairs 3,000

Vehicles 3,000

Main

Journal entry

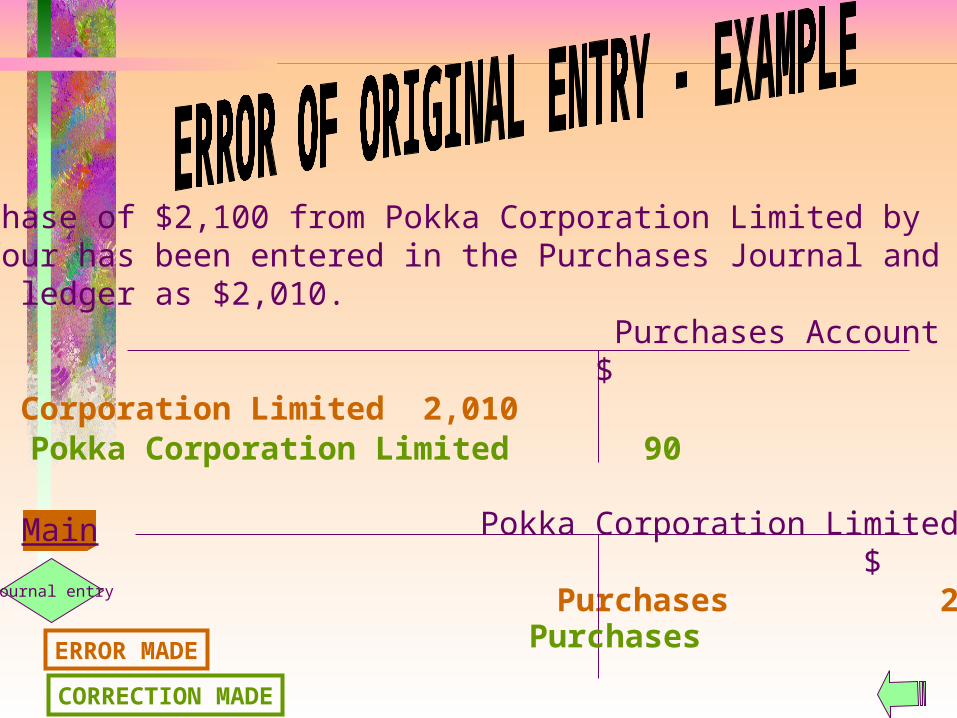

A purchase of $2,100 from Pokka Corporation Limited by Carrefour has been entered in the Purchases Journal and postedto the ledger as $2,010. Purchases Account

$ Pokka Corporation Limited 2,010

Pokka Corporation Limited $ Purchases 2,010

ERROR MADE

CORRECTION MADE

Pokka Corporation Limited 90

Purchases 90

Main

Journal entry

$ $

$ $

ERROR MADE

CORRECTION MADE

Wages 10

Rent received 10

Main

Rent received $340 is correctly debited to the Cash Account butposted as $350 to Rent Revenue Account. Similarly, wages paid,a sum of $590, is correctly credited to the Cash Account but posted as $600 to Wages Account.

Rent Revenue Account

Wages Account

Cash 350

Cash 600Journal entry

$ $

$ $

ERROR MADE

CORRECTION MADE

Carrefour 700

Cash 700

Main

A payment of $700 to a creditor, Carrefour, should be debitedto Carrefour’s account and credited to the Cash Account, but the entries are reversed.

Cash Account

Carrefour

Carrefour 1,400

Cash 1,400Journal entry

A cash payment of $2,000 for purchases has been omittedfrom the Purchases Account.

Purchases $ $

Cash 2,000

Suspense Account

$ $Purchases 2,000

CORRECTION MADE

Main

Journal entry

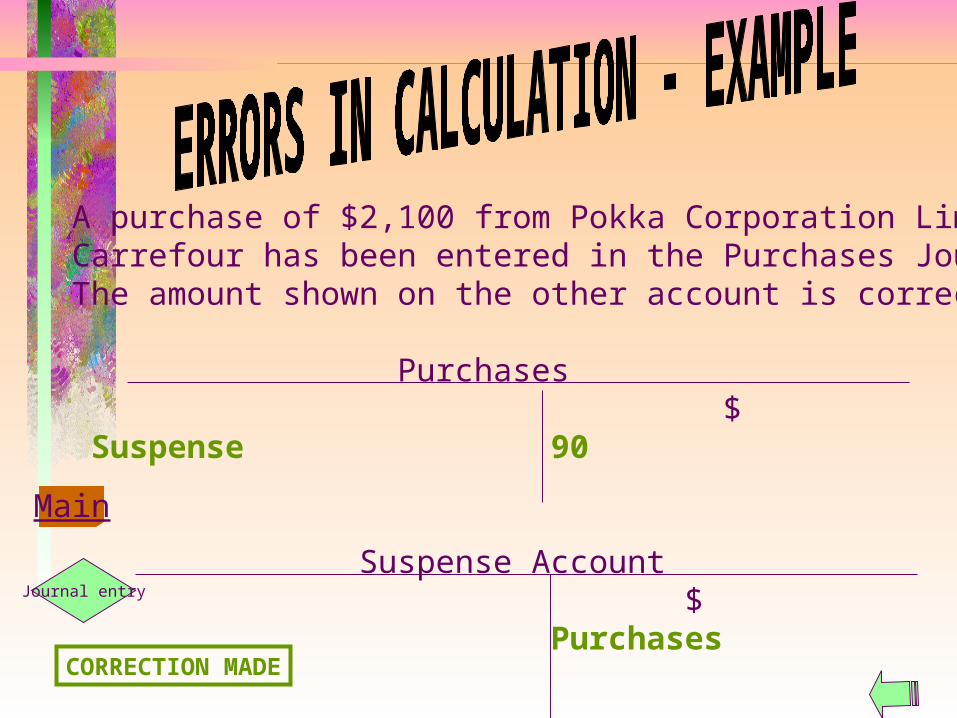

A purchase of $2,100 from Pokka Corporation Limited by Carrefour has been entered in the Purchases Journal as $2,010. The amount shown on the other account is correct.

Purchases $ $

Suspense 90

Suspense Account

$ $Purchases 90

CORRECTION MADE

Main

Journal entry

Rates paid $210 was entered correctly in the Cash Book but wrongly entered as $120 in the Rates Account.

Rates Account $ $

Suspense 90

Suspense Account

$ $Rates Account 90

CORRECTION MADE

Main

Journal entry

Discount received $100 posted to the debit side of the Discount Received Account.

Suspense Account $ $

Discount Received 200

Discount Received Account

$ $Suspense Account 200

CORRECTION MADE

Main

Journal entry

P.S. The suspense account would be self-balancing when all the errorsmade are detected and corrected, otherwise, it would either have a credit or debit balance when closed!

Correcting Net Profit Figure Errors made in the accounts would affect the figures in our final accounts.

Errors that affect the Gross Profit and Net Profit figures are items that are transferred to the Trading and Profit and Loss Accounts ultimately. E.g. Sales, Rent, Commission Received etc.

Errors of items found in the Balance Sheet will not affect the profit figure, instead, they will overstate or understate the assets and liabilities figures.E.g. Furniture, motor vehicles, loan, bank overdraft etc.

Statement of Corrected Net ProfitStatement of Corrected Net Profit

$ $Net Profit before COE 1,700Add Expenses overcast XX Revenue undercast XX

XX XX

Less Expense undercast XX Revenue overcast XX

XXAdjusted Net Profit XX

Note: Overcast means showing more than there actually is Undercast means showing less than there actually is