What can EIS & Seed EIS do for your business? accounts What are the rules for EIS? EIS Relief...

58

beyond accounts What can EIS & Seed EIS do for your business?

Transcript of What can EIS & Seed EIS do for your business? accounts What are the rules for EIS? EIS Relief...

beyond accounts

What can EIS & Seed EIS do for your business?

beyond accounts

What are the rules for SEIS?

• History – From April 2012 and originally until April2017, now indefinite.

• Individual investor limit - £100k pa 2017/18

• Company investment limit - £150k pa 2017/18

• Income tax relief for investor - 50%, can be carriedback subject to p/y limit

beyond accounts

SEIS Relief Example

Gross investment in SEIS shares £10,000

Income tax relief at 50% £5,000

Net cost of SEIS investment £5,000

beyond accounts

What are the rules for SEIS?

• Capital gains on disposal of shares after 3 years are exempt

SEIS Relief Example:

Capital Gains Tax Relief

beyond accounts

What are the rules for SEIS?

• Income tax relief available on losses on disposal of shares, net of income tax relief obtained

SEIS Relief Example:Loss Relief

Gross Investment into SEIS shares £10,000

Less income tax relief at 50% £5,000

Less loss relief £5,000 at 45% £2,250

Net cost of investment £2,750

beyond accounts

What are the rules for SEIS?

SEIS Relief Example:Capital Gains Exemption

Assumes top rate CGT of 20%

Applies to gains made in year of investment

Gross Investment into SEIS shares £10,000

Less income tax relief at 50% £5,000

Less capital gain exemption £1,000

Net cost of investment £4,000

beyond accounts

What are the rules for SEIS?

• Tax relief clawed back if company rules not met for 3 years

• Employees and their associates (ancestors/descendants/spouses) excluded, but not directors even if already paid.

• Individual can have no more than 30% of shares/votes/capital – includes associates’ rights

• Company employees – less than 25

• Company gross assets - £200k before investment

• Company must not have been trading for more than 2 years

beyond accounts

What are the rules for SEIS?

• Company qualifying activities – non-qualifying are defined

• Company must use money within 3 years

• Newly-issued non redeemable ordinary shares with no preferential rights issued for cash

• Company need not be UK resident, but must have permanent establishment here

• Company must be unquoted

• Value received by investor will lead to withdrawal of all or

part of the reliefs

beyond accounts

EIS Relief Example

Gross investment in EIS shares £10,000

Income tax relief at 30% £3,000

Net cost of EIS investment £7,000

beyond accounts

What are the rules for EIS?

• Capital gains on disposal of shares after 3 years are exempt

beyond accounts

What are the rules for EIS?

• Income tax relief available on losses on disposal of shares, net of income tax relief obtained

EIS Relief Example:Loss Relief

• You may also have claimed capital gains deferral

relief of £2,000

beyond accounts

What are the rules for EIS?

EIS Relief Example:Capital Gains Deferral Relief

NB The deferred charge of £2,000 is brought back into charge when the EIS shares are disposed of but investors have an opportunity to defer this again by reinvesting in another EIS company.

Assumes top rate CGT of 20%.

Can apply to gains 3 years before or 1 year after investment

Entrepreneurs relief now available on clawback charge (if qualifies)

Gross investment into EIS shares £10,000

Less income tax relief at 30% £3,000

Less capital gains deferral relief* £2,000

Net cost of investment £5,000

beyond accounts

What are the rules for EIS?

• Tax relief clawed back if company rules not met for 3 years

• Paid directors and employees excluded, unless director where entitlement to payment starts after issue of shares (business angels)

• Individual can have no more than 30% of shares/votes/capital – includes associates’ rights (ancestors/descendants/spouses)

• Company employees – less than 250 (500 for ‘knowledge-intensive’ companies)

beyond accounts

What are the rules for EIS?

• Company gross assets - £15m before and £16m after

• Company ‘lifetime limit’ of £12m introduced (£20m for ‘KIT’s)

• Trading time limit of 7 years unless previous EIS/SEIS issue andfundamental change in business

• Company qualifying activities – non-qualifying are defined

• Money must be used within 2 years

• Must be trade or R&D for 4 months

beyond accounts

What are the rules for EIS?• Newly-issued non redeemable ordinary shares with no preferential rights

issued for cash

• Company need not be UK resident, but must have permanent establishment here

• Value received by investor will lead to withdrawal of all or part of the reliefs

• Company must be unquoted

beyond accounts

Thinking inside the Box -Maximise your Assets through

the Patent Box

beyond accounts

What is the Patent Box

• A gift from the treasury

• UK tax incentive designed to encourage innovation & protect technical inventions

• Patent required – protect inventive concept

• Automatically published

• Lasts up to 20 years

beyond accounts

Tax Relief

• Calculate income related to Patents (net of losses)

• Corporation tax rate applicable to these profits is 10% as opposed tocurrent main rate of 19%

• Arrived at by appropriate deductions from taxable profit to give tax rate of10% on relevant profit.

beyond accounts

Tax Relief – cont’d

• Phasing in – profits arising after 31/03/2017 will attract full reliefbut restricted for periods between 01/04/2013 and 31/03/2017 asfollows

Year Ended 31/03 % Relief Available

2014 60%

2015 70%

2016 80%

2017 90%

2018 100%

beyond accounts

Research & Development and Creative Industry Tax Credits

beyond accounts

Research and Development Tax Credits

Introduction:

• In order to claim R&D relief your company must be liable to corporation tax.

• Research & Development or R&D relief is a corporation tax relief that aims toreduce a business’ corporation tax liability.

• If your company is an SME it may be possible to receive a tax credit from HMRCinstead.

• A SME company is a company with fewer than 500 employees, annual turnover notexceeding €100 million and a balance sheet not exceeding €86 million

beyond accounts

Research and Development Tax Credits

Does your R&D work qualify for Relief?

In order to qualify for relief the work undertaken must aim to achieve an advance inoverall knowledge or capability in a field of science or technology through theresolution of scientific or technological uncertainty. It is not just an advance in its ownstate of knowledge or capability.

The questions you need to be able to answer are:

1. What is the scientific or technological advance?2. What were the scientific or technological uncertainties involved in the project?3. How and when were the uncertainties actually overcome?4. Why was the knowledge being sought not readily deducible

by a competent professional?

beyond accounts

Research and Development Tax Credits

What costs qualify for relief?

• Employee costs including employers NI• Staff providers• Materials• Payments to clinical trials and volunteers• Utilities• Software• Subcontracted expenses – 65% of costs• Capital expenditure (in certain cases)

beyond accounts

Research and Development Tax Credits

Rates of relief

• For SME’s, from 1 April 2012 up until 31 March 2015 the taxrelief allowable on R&D costs is 225%. Therefore for every £100of qualifying expenditure, a company could reduce its taxableprofits chargeable to corporation tax by an additional £125.From 1 April 2015, this increases to 230% or an additional £130.

• From 1 April 2012, where applicable, a company could surrenderlosses in return for a payable tax credit from HMRC at 11% of theloss surrendered and from 1 April 2014 this has been increasedto 14.5%.

beyond accounts

Research and Development Tax Credits

Example 1 – R&D relief where a company has made a taxable profit of £50,000 for the year ended 31 March 2017

• Normally this would result in corporation tax payable of £10,000 (@ 20%)

• Assume qualifying R&D expenditure of £20,000

• R&D relief would be £20,000 x 130% = £26,000

• Taxable profit £50,000 less R&D relief £26,000 = Revised taxable profit of£24,000

• Revised corporation payable would be £4,800.

beyond accounts

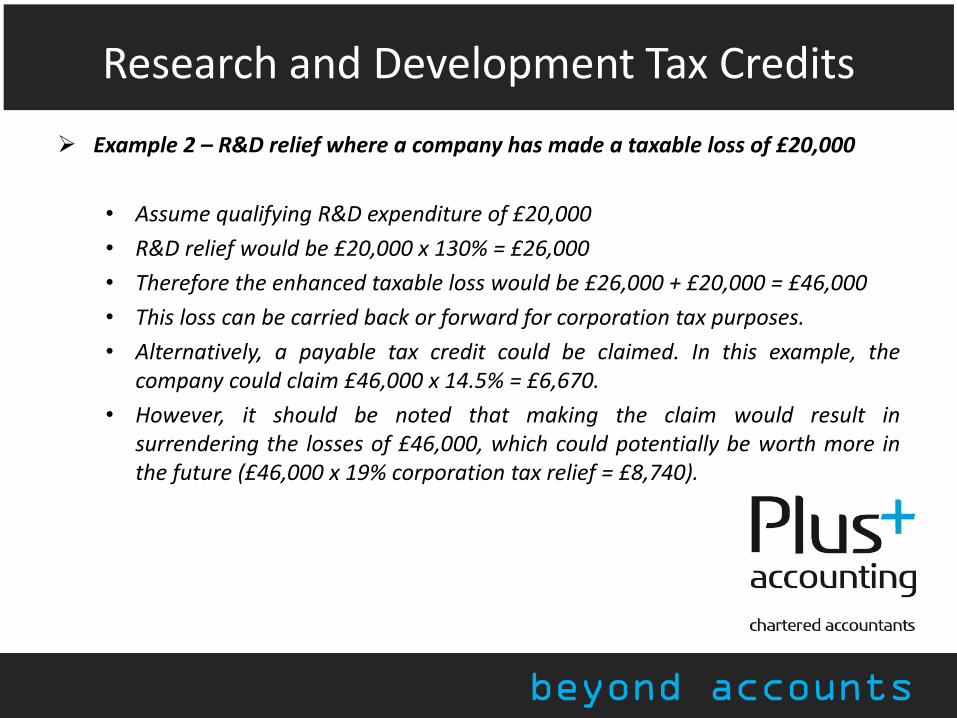

Research and Development Tax Credits

Example 2 – R&D relief where a company has made a taxable loss of £20,000

• Assume qualifying R&D expenditure of £20,000

• R&D relief would be £20,000 x 130% = £26,000

• Therefore the enhanced taxable loss would be £26,000 + £20,000 = £46,000

• This loss can be carried back or forward for corporation tax purposes.

• Alternatively, a payable tax credit could be claimed. In this example, thecompany could claim £46,000 x 14.5% = £6,670.

• However, it should be noted that making the claim would result insurrendering the losses of £46,000, which could potentially be worth more inthe future (£46,000 x 19% corporation tax relief = £8,740).

beyond accounts

Creative Industry Tax Reliefs

• Film Tax Relief (FTR)

• Animation Tax Relief (ATR)

• High-end Television Tax Relief (HTR)

• Children’s Television Tax Relief (CTR)

• Video Games Tax Relief (VGTR)

• Theatre Tax Relief (TTR)

• Orchestra Tax Relief (OTR)

beyond accounts

Creative Industry Tax Reliefs

What companies can qualify for CITR?

Your company qualifies for and can claim CITR if it is:

• liable to Corporation Tax

• directly involved in the production and development of certain films,'high-end' and children’s television programmes, animation programmesor video games and most recently, theatrical production and orchestralconcerts.

beyond accounts

Creative Industry Tax Reliefs

The 'cultural test'

• To qualify for the CITR all films, television programmes, animations orvideo games must pass a 'cultural test' or qualify through aninternationally agreed co-production treaty - certifying that theproduction is a 'British film', 'British programme' or 'British video game'. Inall cases, formal certification is required to qualify. But, theatrical andorchestral productions don’t need to pass a cultural test.

• Certification and qualification is administered by the British Film Institute(BFI) on behalf of the Department for Culture Media and Sport. The BFIwill issue an interim certificate for uncompleted work (so that

you can make interim claims) or a final certificate where

production has finished.

beyond accounts

Film Tax Relief (FTR)

Your company will be entitled to claim FTR on a film as long as:

• the film passes the culture test - it is considered a 'British film‘

• the film is intended for theatrical release

• at least 10% of the total production costs relate to activities in the UK

• the first day of principal photography took place on or after 1 January2007

beyond accounts

Animation Tax Relief (ATR)

Your company will be entitled to claim ATR on an animation programme if:

• the programme passes the cultural test

• the programme is intended for broadcast

• at least 51% of the total core expenditure is on animation

• at least 10% of the total production costs relate to activities in the UK

beyond accounts

Children’s Television Tax Relief (CTR)

Your company will be entitled to claim CTR on a programme if:

• the programme passes the cultural test

• the programme is intended for broadcast

• It is for children (primary audience expected under age 15)

• at least 10% of the total production costs relate to activities in the UK

beyond accounts

High-end Television Tax Relief (HTR)

Your company will be entitled to claim HTR on a programme if:

• the programme passes the cultural test

• the programme is intended for broadcast

• the programme is a drama, comedy or documentary

• at least 10% of the total production costs relate to activities in the UK

• the average qualifying production costs per hour of production

length is not less than £1million per hour

• the slot length in relation to the programme must be greater than

30 minutes

beyond accounts

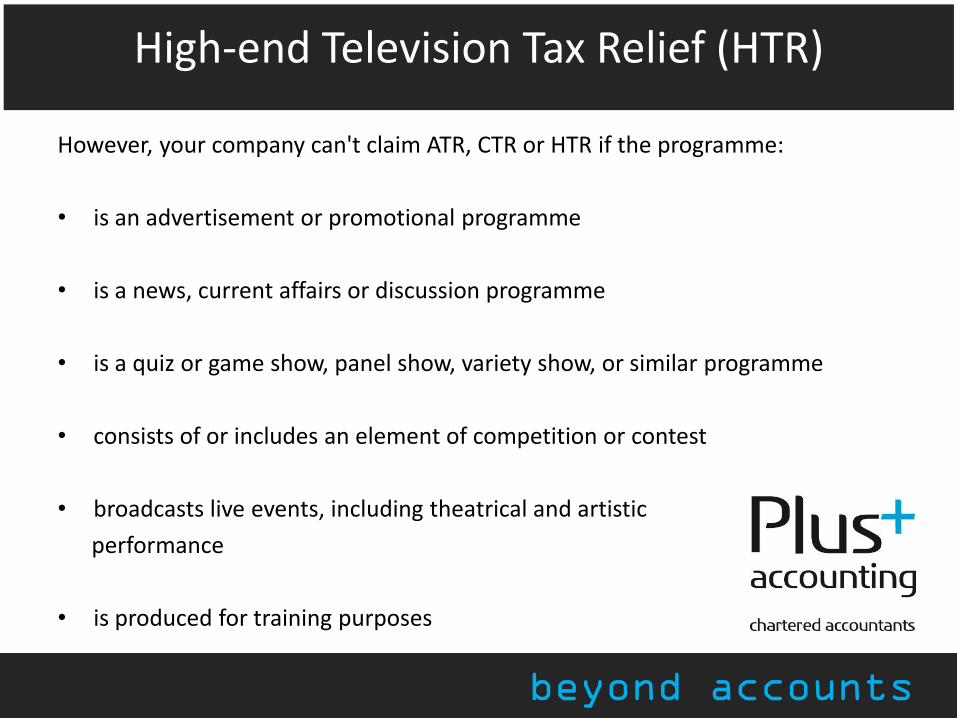

High-end Television Tax Relief (HTR)

However, your company can't claim ATR, CTR or HTR if the programme:

• is an advertisement or promotional programme

• is a news, current affairs or discussion programme

• is a quiz or game show, panel show, variety show, or similar programme

• consists of or includes an element of competition or contest

• broadcasts live events, including theatrical and artistic

performance

• is produced for training purposes

beyond accounts

Video Games Tax Relief (VGTR)

Video Games Tax Relief (VGTR) became available from 1 April 2014.

Your company will be entitled to claim VGTR as long as:

• the video game is British

• the video game is intended for supply

• at least 25% of core expenditure is incurred on goods or services that are provided from within in the European Economic Area (EEA)

beyond accounts

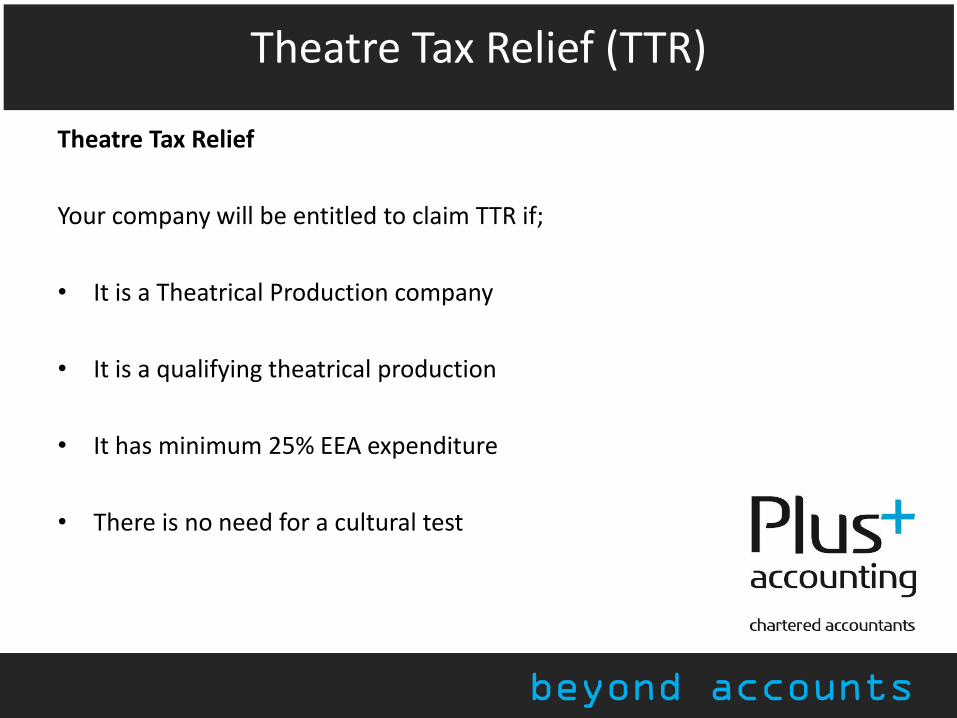

Theatre Tax Relief (TTR)

Theatre Tax Relief

Your company will be entitled to claim TTR if;

• It is a Theatrical Production company

• It is a qualifying theatrical production

• It has minimum 25% EEA expenditure

• There is no need for a cultural test

beyond accounts

Orchestra Tax Relief (OTR)

OTR is the most recent relief, being introduced from 1 April 2016. Your company will be entitled to claim OTR if it is a qualifying orchestra production company putting on a qualifying orchestral concert;

A qualifying concert is one which;

• Is performed by instrumentalists in an orchestra, enable, group or band

• Consists of a minimum of 12 instrumentalists

• All or majority of the instruments must not be electrically amplified

• Instrumentalists must be primary focus of the concert

• Primary focus is to play before the playing public or for educational purposes

• Has a minimum 25% EEA expenditure

• Has no need for a cultural certificate

beyond accounts

Tax Relief

If your company qualifies for one of the tax reliefs, your company is entitled to;

• An additional deduction in computing their taxable profits

• Where that addition reduction results in a loss, to surrender losses for a payabletax credit

• Both the additional deduction and the payable credit are calculated on the basis ofEuropean Economic Area (EEA) core expenditure up to a maximum of 80% of thetotal core expenditure by the company.

beyond accounts

How and when to claim CITR

You can claim for relief in your Company Tax Return once your company hasreceived its certificate from the BFI. If you have received an interim certificateyou must apply for a final certificate after the film, television programme orvideo game has been completed. If you don't, you will have to repay anyinterim relief already paid. Certificates should be sent with the return.

You may make, amend or withdraw a claim to CITR up to 1 year after thecompany's filing date.

HMRC may agree to accept late claims in some circumstances.

beyond accounts

The Plus Approach

If you would like to discuss any of the matters raised in this presentation, please contact Luke Thomas or Alex Koupland on;

01273 701200

Thank you for watching.

Brexit and the Creative Sector:Legal Implications

Mark O’Halloran

26th September 2017

• Immigration & Employment

• IP and Data Exports

• Advertising, Funding &

Investment

Do you think that lawyers are:

A. Rubbing their hands?

B. Scratching their heads?

C. Praying for a deal?

Immigration & Employment

© Sports Interactive

Soft Brexit

free movement of workers

Special status

footballers get same exemptions as

actors

Hard Brexit

same visa rules for non-EU players apply to all non-UK players

Harmonised EU already embedded in UK

UK already negotiated many exemptions

(eg opt out working time regulations)

UK often grants more than the required

minimum (eg holidays)

No political appetite to trash employee

rights

TUPE

Consultation with employees

Harmonisation of contracts

Change of Service Provision rules

Holiday

Accrual during sick leave

Workers

Agency workers

Self-employed in gig economy

Intellectual Property

IPR = M / (JxT)

An IPR is:

a Monopoly

in a certain Jurisdiction

for a certain period of Time

IP in Creative Sector

Brand NoveltyDesign &

ContentCollateral Data

Company

NameInvention Design

Brochures/

websiteMarket reports

Game Name Inventive Use Decoration PhotosMarket

analysis

PackagingBusiness

ProcessSoftware Diagrams Database

Website Know-how

Digital

(games/film/

music)

Adverts/ press

articles

Contact

details

Trademarks/

BNA85/ CA06Patents Design Rights Copyright

Copyright/

dB right

Nominet Rules Confidentiality CopyrightDPA98 /

confidentiality

Patents more relevant to console and toy manufacturers

The so-called European Patent is actually a bundle of national patents Not affected by Brexit

The proposed Unitary Patent is EU-based and already delayed by Brexit UK is a big player, one of the Unitary Patent Courts was

to be in London

UK Government has indicated willingness to continue

EU TMs cover all of European Economic Area If UK outside EEA, they cease to apply in UK

If only used in UK , non-use in EEA may lead to invalidity

EU Registered Designs require only that product placed on market in EEA Not affected

Solutions: Treaty to extend EUTMs to EEA and UK

Turn EUTMs into UKTMs

Copyright is irregular across EU / only partially harmonised

Copyright, Designs and Patents Act 1998 already incorporates relevant EU Directives

“Database Right” incorporated via Copyright and Rights in Databases Regulations 1997

Some small technical tweaks required

If UK leaves EEA, you need to check any IP licences you hold Definition of “Territory”

Boilerplate clauses allowing licence to be re-interpreted in light of Brexit or legislative changes

Exhaustion principle won’t apply between EU and UK Could allow grey imports on physical products (such as

games, music and movies on CD/DVD ) to be blocked

Differential pricing easier even via download and streaming sales

Advertising, Funding &

Investment

Advertising rules already incorporate EU rules

Generally reflect good practice, no real changes

anticipated

Loss of access to Creative Europe and Horizon 2020

PM proposed last week to maintain UK budget

contributions until 2021

UK may not participate in the EU’s Digital Single Market

Strategy

Rely on GATS 1995 rules on full market access

commitment in the area of recreational, cultural, and

sports services

Antigua v USA 2003

The content of this presentation is for general information purposes only. It does not constitute professional advice (legal or otherwise) nor should it be used as such for any specific situation. The information should be read in the context of the entire presentation. We therefore cannot accept responsibility

for any act and/or omission based on the material contained in it.

© Coffin Mew LLP 2017