Wethersfield Public Schools Course Outline Course … · Wethersfield Public Schools Course Outline...

22

Accounting Page 1 Wethersfield Public Schools Course Outline Course Name: Accounting Department: Business Grade(s): 10-12 Level(s): Unleveled Course Number(s): 62104 Credits: 1 Course Description: This course is a study of how and why financial records are kept in most social and business organizations. It provides an introduction to accounting principles, concepts and techniques used in sole proprietorships, partnerships and corporations. It includes preparation of various documents, simulations and spreadsheet projects demonstrate the language of business by recording, analyzing, and interpreting financial information. Students interested in the field of Computer Science and/or Computer Programming will also benefit from taking the course. Required Instructional Materials: Century 21 Accounting: General Journal, 9th Edition Gilbertson, Lehman South Western 2007 Revised/Approval Date: June 18, 2012 Approved Administrative Team 10/10/12 Approved Student Programs & Services Committee 3/6/13 Authors/Contributors: Joanna Griswold

Transcript of Wethersfield Public Schools Course Outline Course … · Wethersfield Public Schools Course Outline...

Accounting Page 1

Wethersfield Public Schools

Course Outline

Course Name: Accounting

Department: Business

Grade(s): 10-12

Level(s): Unleveled

Course Number(s): 62104

Credits: 1

Course Description:

This course is a study of how and why financial records are kept in most social and business

organizations. It provides an introduction to accounting principles, concepts and techniques

used in sole proprietorships, partnerships and corporations. It includes preparation of various

documents, simulations and spreadsheet projects demonstrate the language of business by

recording, analyzing, and interpreting financial information. Students interested in the field of

Computer Science and/or Computer Programming will also benefit from taking the course.

Required Instructional Materials:

Century 21 Accounting: General Journal, 9th Edition

Gilbertson, Lehman

South Western 2007

Revised/Approval Date: June 18, 2012

Approved Administrative Team 10/10/12

Approved Student Programs & Services Committee 3/6/13

Authors/Contributors: Joanna Griswold

Accounting Page 2

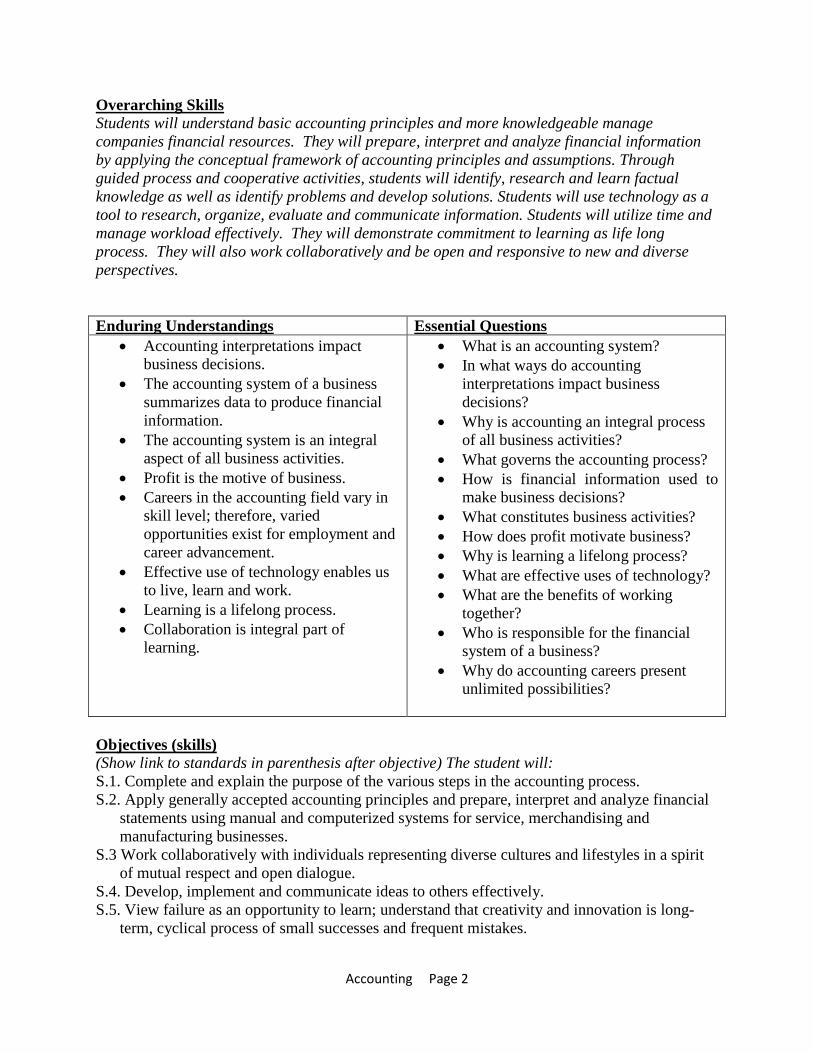

Overarching Skills

Students will understand basic accounting principles and more knowledgeable manage

companies financial resources. They will prepare, interpret and analyze financial information

by applying the conceptual framework of accounting principles and assumptions. Through

guided process and cooperative activities, students will identify, research and learn factual

knowledge as well as identify problems and develop solutions. Students will use technology as a

tool to research, organize, evaluate and communicate information. Students will utilize time and

manage workload effectively. They will demonstrate commitment to learning as life long

process. They will also work collaboratively and be open and responsive to new and diverse

perspectives.

Enduring Understandings Essential Questions

Accounting interpretations impact

business decisions.

The accounting system of a business

summarizes data to produce financial

information.

The accounting system is an integral

aspect of all business activities.

Profit is the motive of business.

Careers in the accounting field vary in

skill level; therefore, varied

opportunities exist for employment and

career advancement.

Effective use of technology enables us

to live, learn and work.

Learning is a lifelong process.

Collaboration is integral part of

learning.

What is an accounting system?

In what ways do accounting

interpretations impact business

decisions?

Why is accounting an integral process

of all business activities?

What governs the accounting process?

How is financial information used to

make business decisions?

What constitutes business activities?

How does profit motivate business?

Why is learning a lifelong process?

What are effective uses of technology?

What are the benefits of working

together?

Who is responsible for the financial

system of a business?

Why do accounting careers present

unlimited possibilities?

Objectives (skills)

(Show link to standards in parenthesis after objective) The student will:

S.1. Complete and explain the purpose of the various steps in the accounting process.

S.2. Apply generally accepted accounting principles and prepare, interpret and analyze financial

statements using manual and computerized systems for service, merchandising and

manufacturing businesses.

S.3 Work collaboratively with individuals representing diverse cultures and lifestyles in a spirit

of mutual respect and open dialogue.

S.4. Develop, implement and communicate ideas to others effectively.

S.5. View failure as an opportunity to learn; understand that creativity and innovation is long-

term, cyclical process of small successes and frequent mistakes.

Accounting Page 3

S.6. Use various types of reasoning such as inductive and deductive as appropriate to the

situation.

S.7. Reflect critically on learning experiences and processes.

S.8 Evaluate information critically and competently.

S.9 Use technology as a tool to research, organize, evaluate and communicate information.

S.10 Demonstrate commitment to learning as a lifelong process.

S.11 Monitor, define, prioritize and complete tasks without direct oversight.

S. 12 Utilize time and manage workload efficiently.

S.13 Identify accounting careers.

CT Career & Technical Education Performance Standards and Competencies 2011

E9. Use word processing, desktop publishing, database, spreadsheet, presentation, and

multimedia software to improve academic achievement across the curriculum.

A1 Describe career opportunities in the accounting profession.

A2. Explain the need for a code of ethics in accounting and ethical responsibilities required of

accountants.

B3. Describe and explain the conceptual framework of accounting principles and assumptions.

C.20 Describe the purpose of a uniform accounting system.

C21. Describe the purpose of journals and ledgers and their relationship.

C22. Describe the impact of technology on the accounting process.

C23. Analyze and describe how basic business transactions impact the accounting equation.

C24. Apply the double-entry system of accounting to record basic transactions and prepare a trial

balance.

C25. Explain the need for adjusting entries and record basic adjusting entries.

C26. Complete the closing process.

C27 Apply the double-entry system of accounting to record complex transactions and prepare a

trial balance.

C28 Explain the need for adjusting entries and record complex adjusting entries.

D29 Identify sources of information to prepare basic financial reports.

D30 Describe the users and uses of financial information.

D31 Describe the information provided in each financial statement and how the statements

relate.

E.1 Apply appropriate accounting principles to payroll.

E.2 Prepare and maintain payroll records.

E.3 Calculate and record transactions related to employee payroll.

E.4 Calculate and record employer’s payroll taxes.

E.5Calculate and record payroll accruals. 36. Journalize payroll transactions.

F37. Calculate component percentages.

Instructional Support Materials

Microsoft Office

Automated Accounting Software

Websites

Book Companion Site; www. Cengage.com

Century 21 Accounting: General Journal, 9th Edition

Accounting Page 4

Suggested Instructional Strategies

Think/Pair/Share

Oral Descriptions

Modeling

Group Problem Solving

Graphic Organizers

Differentiated Tasks

Guided Practice

Vocabulary Reinforcement

Cooperative Activities

Problems Presented in Context

Classification Charts

Semantic Maps

Computer Simulations

Suggested Assessment Methods

(Include use of school-wide analytic and course specific rubrics)

Quizzes

Chapter Tests

Computer Simulations

Web Quests

Presentations

Projects

Performance Based Assessment

School wide rubrics

Accounting Page 5

Unit 1: In this unit, students will learn about the accounting industry, explore accounting career

opportunities and the methods of communicating accounting information. They will also learn

about how ethical decisions are made and the laws that govern compliance.

Time Frame: September

Length of Unit:2 Weeks

Enduring Understandings Essential Questions

Accounting is governed by general

accounting principles.

Jobs in the accounting field vary in skill

level; therefore, varied opportunities

exist for employment and career

advancement.

Accounting is the language of business.

It is important for businesses to keep

track of their money and be honest in

their financial records.

The accounting system of a business

summarizes data to produce financial

information.

A code of ethics in an essential element

of accounting and accountants are

required to follow ethical

responsibilities.

Accountants play a major role in

business and society.

Why is Accounting considered the

language of business?

How is accounting information used to

make business decisions?

Why are financial records important?

Why is it important to understand

different methodologies in the

accounting process?

What do Accountants do?

Who is responsible for the financial

system of a business?

What are the legal consequences of

unethical and dishonest business

behavior?

How does the accounting system of a

business summarize data to produce

financial information?

What are the different careers in

Accounting?

How do current events impact the

accounting profession?

What kind of business fraud can be

committed?

Objectives (knowledge and skills)

(Show link to standards in parenthesis after objective) The student will:

1.1 Explore accounting career opportunities and describe the areas of specialization within the

accounting profession.

1.2 Describe how current events impact the accounting profession.

1.3 Describe methods of communicating accounting information.

1.4 Evaluate how ethical decisions are made.

1.5 Identify the general principles and guidelines which govern the process of accounting.

1.6 Recognize why accounting is the language of business.

1.7 Explain why it’s important for businesses to keep track of their money.

1.8 List the various skills required in Accounting.

Accounting Page 6

1.9 Describe what is required to be a CPA.

1.10 Research information about the Accounting Industry.

1.11 Apply technology to accounting process.

1.12 Debate the consequences of unethical and fraudulent behavior.

1.13 Demonstrate understanding of accounting profession through role play.

CT Career & Technical Education Performance Standards and Competencies 2011

E9. Use word processing, desktop publishing, database, spreadsheet, presentation, and

multimedia software to improve academic achievement across the curriculum.

C20. Describe the purpose of a uniform accounting system.

A1. Describe career opportunities in the accounting profession.

A2. Explain the need for a code of ethics in accounting and ethical responsibilities required of

accountants.

B3. Describe and explain the conceptual framework of accounting principles and assumptions.

C22. Describe the impact of technology on the accounting process.

D30. Describe the users and uses of financial information.

Instructional Support Materials

Microsoft Office

Automated Accounting

Websites

Book Companion Site; www. Cengage.com

Accounting Conference

Suggested Instructional Strategies

Think/Pair/Share

Oral Descriptions

Modeling

Group Problem Solving

Graphic Organizers

Differentiated Tasks

Guided Practice

Vocabulary Reinforcement

Cooperative Activities

Problems Presented in Context

Classification Charts

Semantic Maps

Suggested Assessment Methods

(Include use of school-wide analytic and course specific rubrics)

Quizzes

Chapter Tests

Computer Simulations

Web Quests

Presentations

Accounting Page 7

Projects

Performance Based Assessment

School Wide Rubrics

Accounting Page 8

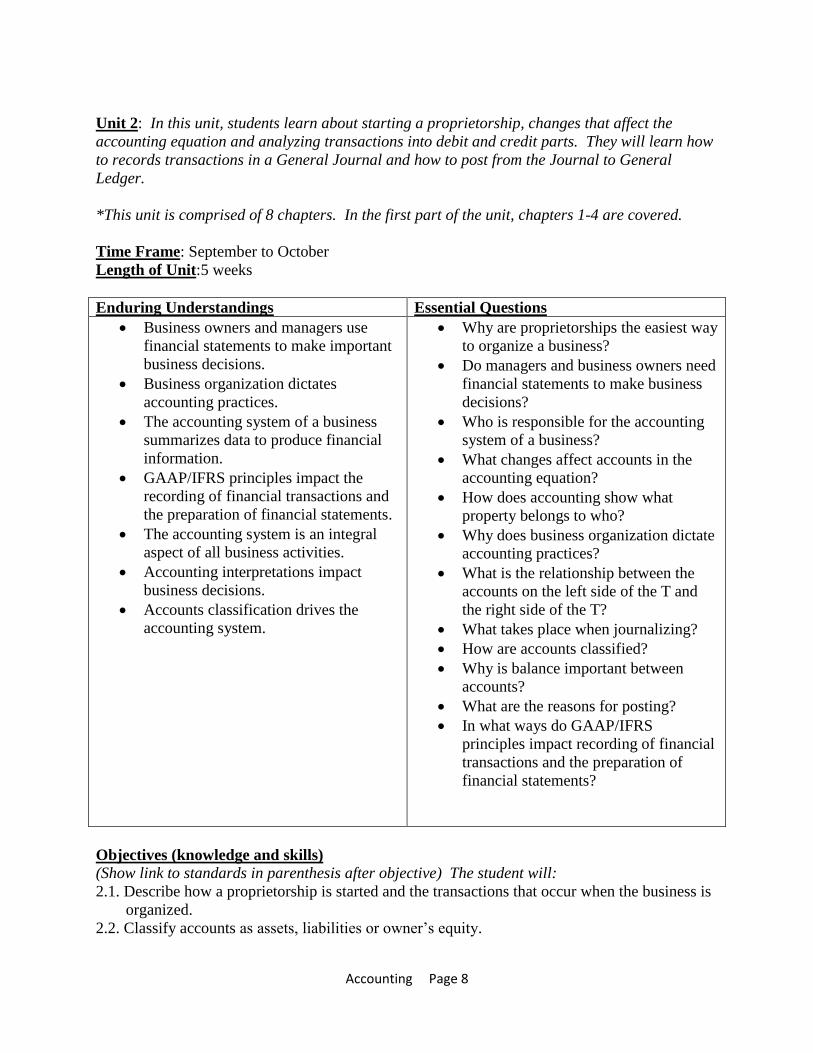

Unit 2: In this unit, students learn about starting a proprietorship, changes that affect the

accounting equation and analyzing transactions into debit and credit parts. They will learn how

to records transactions in a General Journal and how to post from the Journal to General

Ledger.

*This unit is comprised of 8 chapters. In the first part of the unit, chapters 1-4 are covered.

Time Frame: September to October

Length of Unit:5 weeks

Enduring Understandings Essential Questions

Business owners and managers use

financial statements to make important

business decisions.

Business organization dictates

accounting practices.

The accounting system of a business

summarizes data to produce financial

information.

GAAP/IFRS principles impact the

recording of financial transactions and

the preparation of financial statements.

The accounting system is an integral

aspect of all business activities.

Accounting interpretations impact

business decisions.

Accounts classification drives the

accounting system.

Why are proprietorships the easiest way

to organize a business?

Do managers and business owners need

financial statements to make business

decisions?

Who is responsible for the accounting

system of a business?

What changes affect accounts in the

accounting equation?

How does accounting show what

property belongs to who?

Why does business organization dictate

accounting practices?

What is the relationship between the

accounts on the left side of the T and

the right side of the T?

What takes place when journalizing?

How are accounts classified?

Why is balance important between

accounts?

What are the reasons for posting?

In what ways do GAAP/IFRS

principles impact recording of financial

transactions and the preparation of

financial statements?

Objectives (knowledge and skills)

(Show link to standards in parenthesis after objective) The student will:

2.1. Describe how a proprietorship is started and the transactions that occur when the business is

organized.

2.2. Classify accounts as assets, liabilities or owner’s equity.

Accounting Page 9

2.3. Analyze how transactions affect the accounting equation.

2.4. Differentiate between transactions and how they affect owner’s equity.

2.5. Use T accounts to analyze transactions and show which accounts are debited or credited.

2.6. Match expenses with revenue.

2.7. Relate the double-entry system of accounting to record transactions using technology.

2.8. Describe the purpose of journals and ledgers and their relationship.

2.9. Prepare a chart of accounts for a service business.

2.10. Apply accounting practices while posting from General Journal to General Ledger.

2.11. Prove cash.

2.12. Analyze and journalize correcting entries.

2.13 Demonstrate how account classification drives the accounting system.

CT Career & Technical Education Performance Standards and Competencies 2011

E9. Use word processing, desktop publishing, database, spreadsheet, presentation, and

multimedia software to improve academic achievement across the curriculum.

B3. Describe and explain the conceptual framework of accounting principles and assumptions.

B4. Define assets, liabilities, equity, revenue, expenses, gains and losses.

B12. Record transactions for accounts payable and other short-term debt.

B14. Describe the criteria used to determine revenue recognition.

B17. Describe and record expense-related transactions.

C20. Describe the purpose of a uniform accounting system.

C21. Describe the purpose of journals and ledgers and their relationship.

C22. Describe the impact of technology on the accounting process.

D30. Describe the users and uses of financial information.

Instructional Support Materials

Microsoft Office

Automated Accounting

Websites

Book Companion Site; www. Cengage.com

Suggested Instructional Strategies

Think/Pair/Share

Oral Descriptions

Modeling

Group Problem Solving

Graphic Organizers

Differentiated Tasks

Guided Practice

Vocabulary Reinforcement

Cooperative Activities

Problems Presented in Context

Semantic Maps

Accounting Page 10

Suggested Assessment Methods

(Include use of school-wide analytic and course specific rubrics)

Quizzes

Chapter Tests

Computer Simulations

Web Quests

Presentations

Projects

Performance Based Assessment

School Wide Rubrics

Accounting Page 11

Unit 3: Accounting for Service Business Organized as a Proprietorship

In this unit, students learn about cash control systems for a service business organized as a

proprietorship. They learn how to prepare a worksheet and financial statements. At the end of

the fiscal period, students will perform the closing process and analyze business performance.

Students will also reflect on the accounting process for a service business organized as a

proprietorship and its integral part of all business activities.

*This unit is comprised of 8 chapters and is split into two parts. This is the second part of the

unit and chapters 5-8 are covered.

Time Frame: November to December

Length of Unit: 7 weeks

Enduring Understandings Essential Questions

Financial statements provide essential

information to help business owners and

managers make important business

decisions.

The accounting system is an integral

aspect of all business activities.

It is important for businesses to have

good control systems for cash.

Without consistent reporting, it would be

difficult for businesses to compare

results from year to year.

Accounting interpretations impact

business decisions.

Every business must complete the

closing process at the end of fiscal

period.

What kind of cash control systems do

businesses use?

Why do banks dishonor a check?

What financial statements do

accountants prepare?

How are income statements justified?

What are the consequences of

inadequate disclosure?

Why is a worksheet considered a

planning tool?

Is it important to be consistent when

reporting financial information?

How do businesses generate revenue?

How do you determine financial

condition of a business?

Why is it necessary to adjust the

balances of certain accounts?

What are the steps for recording

closing entries?

Objectives (knowledge and skills)

(Show link to standards in parenthesis after objective) The student will:

3.1 Specify the practices related to using a checking account.

3.2 Reconcile a bank statement.

3.3 Establish and replenish a petty cash fund.

3.4 Analyze the pros and cons of using Electronic Funds Transfer.

3.5 Prepare a worksheet and plan adjustments.

3.6 Explain why matching expenses with revenue is important.

3.7 Describe how disclosure requirements impact financial reporting.

3.8 Complete the closing process.

3.9 Use Automated Accounting Software and Excel to record transactions and prepare financial

statements.

3.10 Discuss the relationship between the accounting equation and balance sheet.

Accounting Page 12

CT Career & Technical Education Performance Standards and Competencies 2011

E9. Use word processing, desktop publishing, database, spreadsheet, presentation, and

multimedia software to improve academic achievement across the curriculum.

C23. Analyze and describe how basic business transactions impact the accounting equation.

C24. Apply the double-entry system of accounting to record basic transactions and prepare a trial

balance.

C25. Explain the need for adjusting entries and record basic adjusting entries.

C26. Complete the closing process.

C27. Apply the double-entry system of accounting to record complex transactions and prepare a

trial balance.

C28. Explain the need for adjusting entries and record complex adjusting entries.

D29. Identify sources of information to prepare basic financial reports.

D31. Describe the information provided in each financial statement and how the statements

relate.

F37. Calculate component percentages.

Instructional Support Materials

Microsoft Office

Automated Accounting

Websites

Book Companion Site; www. Cengage.com

Guest Speaker

Suggested Instructional Strategies

Active Learning

Oral Descriptions

Modeling

Group Problem Solving

Graphic Organizers

Differentiated Tasks

Guided Practice

Vocabulary Reinforcement

Problems Presented in Context

Case Studies

Suggested Assessment Methods

(Include use of school-wide analytic and course specific rubrics)

Quizzes

Chapter Tests

Computer Simulations

Webquests

Presentations

Projects

Performance Based Assessment

School wide rubrics

Accounting Page 13

Unit 4: Accumulative Review Project of the Accounting Cycle for a service business organized

as a sole proprietorship. In this unit, students will complete a reinforcement project using

Automated Accounting Software. The project encompasses the entire accounting cycle of a

service business organized as a sole proprietorship.

Time Frame: January

Length of Unit:2 Weeks

Enduring Understandings Essential Questions

The accounting system is an integral

aspect of all business activities.

The accounting system of a business

summarizes data to produce financial

information.

Without consistent reporting, it would

be difficult for businesses to compare

results from year to year.

GAAP/IFRS principles impact the

recording of financial transactions and

the preparation of financial statements. Accounting interpretations impact

business decisions.

How are GAAP principles applied to

the accounting process?

Why is it necessary to adjust the

balances of certain accounts?

Why do businesses compare results

from year to year?

How is financial data summarized?

What is the accounting process?

How is technology used in the

accounting process?

What is the closing process?

Objectives (knowledge and skills)

(Show link to standards in parenthesis after objective) The student will:

4.1. Apply the double-entry system of accounting to record basic transactions and prepare a trial

balance.

4.2 Prepare a worksheet and plan adjustments.

4.3 Prepare financial statements including the balance sheet and income statement.

4.4 Explain and analyze the information provided in each financial statement and how the

statements relate.

4.5. Calculate component percentages.

4.6. Assess the financial condition and operating results of a company.

4.7 Complete the closing process.

4.8 Apply technology to accounting process.

4.9 Self reflect on the accounting process.

CT Career & Technical Education Performance Standards and Competencies 2011

E9. Use word processing, desktop publishing, database, spreadsheet, presentation, and

multimedia software to improve academic achievement across the curriculum.

B3. Describe and explain the conceptual framework of accounting principles and assumptions.

C20. Describe the purpose of a uniform accounting system.

C22. Describe the impact of technology on the accounting process.

C23. Analyze and describe how basic business transactions impact the accounting equation.

Accounting Page 14

C24. Apply the double-entry system of accounting to record basic transactions and prepare a trial

balance.

C25. Explain the need for adjusting entries and record basic adjusting entries.

C26. Complete the closing process.

C27. Apply the double-entry system of accounting to record complex transactions and prepare a

trial balance.

C28. Explain the need for adjusting entries and record complex adjusting entries.

D29. Identify sources of information to prepare basic financial reports.

D31. Describe the information provided in each financial statement and how the statements

relate.

F37. Calculate component percentages.

Instructional Support Materials

Automated Accounting Software

Excel

Book Companion Website

Suggested Instructional Strategies

Computer Simulation

Active Learning

Data Analysis

Focused Practice

Suggested Assessment Methods

(Include use of school-wide analytic and course specific rubrics)

Formative and Summative Assessment

Performance Based Assessment

School wide rubrics

Accounting Page 15

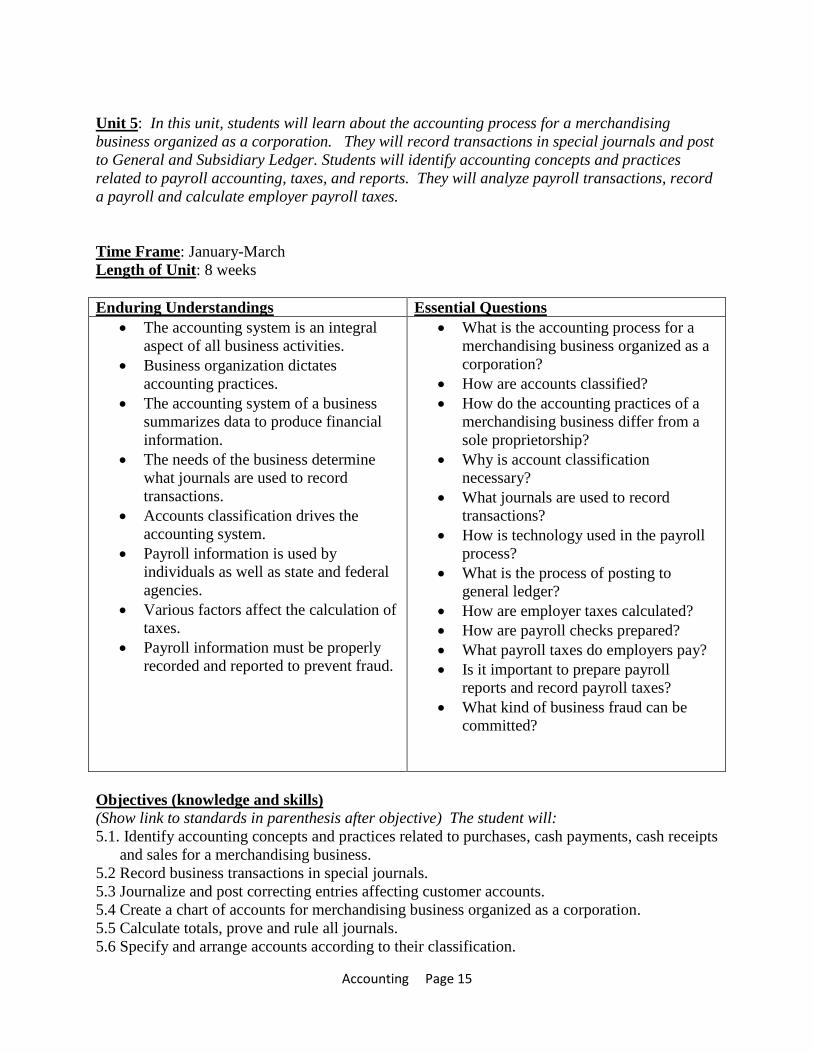

Unit 5: In this unit, students will learn about the accounting process for a merchandising

business organized as a corporation. They will record transactions in special journals and post

to General and Subsidiary Ledger. Students will identify accounting concepts and practices

related to payroll accounting, taxes, and reports. They will analyze payroll transactions, record

a payroll and calculate employer payroll taxes.

Time Frame: January-March

Length of Unit: 8 weeks

Enduring Understandings Essential Questions

The accounting system is an integral

aspect of all business activities.

Business organization dictates

accounting practices.

The accounting system of a business

summarizes data to produce financial

information.

The needs of the business determine

what journals are used to record

transactions.

Accounts classification drives the

accounting system.

Payroll information is used by

individuals as well as state and federal

agencies.

Various factors affect the calculation of

taxes.

Payroll information must be properly

recorded and reported to prevent fraud.

What is the accounting process for a

merchandising business organized as a

corporation?

How are accounts classified?

How do the accounting practices of a

merchandising business differ from a

sole proprietorship?

Why is account classification

necessary?

What journals are used to record

transactions?

How is technology used in the payroll

process?

What is the process of posting to

general ledger?

How are employer taxes calculated?

How are payroll checks prepared?

What payroll taxes do employers pay?

Is it important to prepare payroll

reports and record payroll taxes?

What kind of business fraud can be

committed?

Objectives (knowledge and skills)

(Show link to standards in parenthesis after objective) The student will:

5.1. Identify accounting concepts and practices related to purchases, cash payments, cash receipts

and sales for a merchandising business.

5.2 Record business transactions in special journals.

5.3 Journalize and post correcting entries affecting customer accounts.

5.4 Create a chart of accounts for merchandising business organized as a corporation.

5.5 Calculate totals, prove and rule all journals.

5.6 Specify and arrange accounts according to their classification.

Accounting Page 16

5.7 Apply accounting practices while posting from journals to General Ledger.

5.8 Demonstrate how account classification drives the accounting system.

5.9 Organize, analyze and record payroll transactions.

5.10 Summarize the accounting practices related to payroll records.

5.11 Calculate employer payroll taxes.

5.12 Prepare payroll reports.

5.13 Justify the need of individuals and agencies for payroll information.

5.14 Self-reflect on the accounting process.

5.15 Apply technology tools to the accounting process.

CT Career & Technical Education Performance Standards and Competencies 2011

E9. Use word processing, desktop publishing, database, spreadsheet, presentation, and

multimedia software to improve academic achievement across the curriculum.

B3. Describe and explain the conceptual framework of accounting principles and assumptions.

C20. Describe the purpose of a uniform accounting system.

C23. Analyze and describe how basic business transactions impact the accounting equation.

C27. Apply the double-entry system of accounting to record complex transactions and prepare a

trial balance.

E32. Prepare and maintain payroll records.

E33. Calculate and record transactions related to employee payroll.

E34. Calculate and record employer’s payroll taxes.

E35. Calculate and record payroll accruals.

E36. Journalize payroll transactions.

Instructional Support Materials

Automated Accounting Software

Excel

Book Companion Website

Suggested Instructional Strategies

Active Learning

Oral Descriptions

Modeling

Group Problem Solving

Graphic Organizers

Differentiated Tasks

Guided Practice

Vocabulary Reinforcement

Problems Presented in Context

Case Studies

Calculations

Problem Solving

Accounting Page 17

Suggested Assessment Methods

(Include use of school-wide analytic and course specific rubrics)

Quizzes

Chapter Tests

Computer Simulations

Web Quests

Presentations

Projects

Performance Based Assessment

School Wide Rubrics

Accounting Page 18

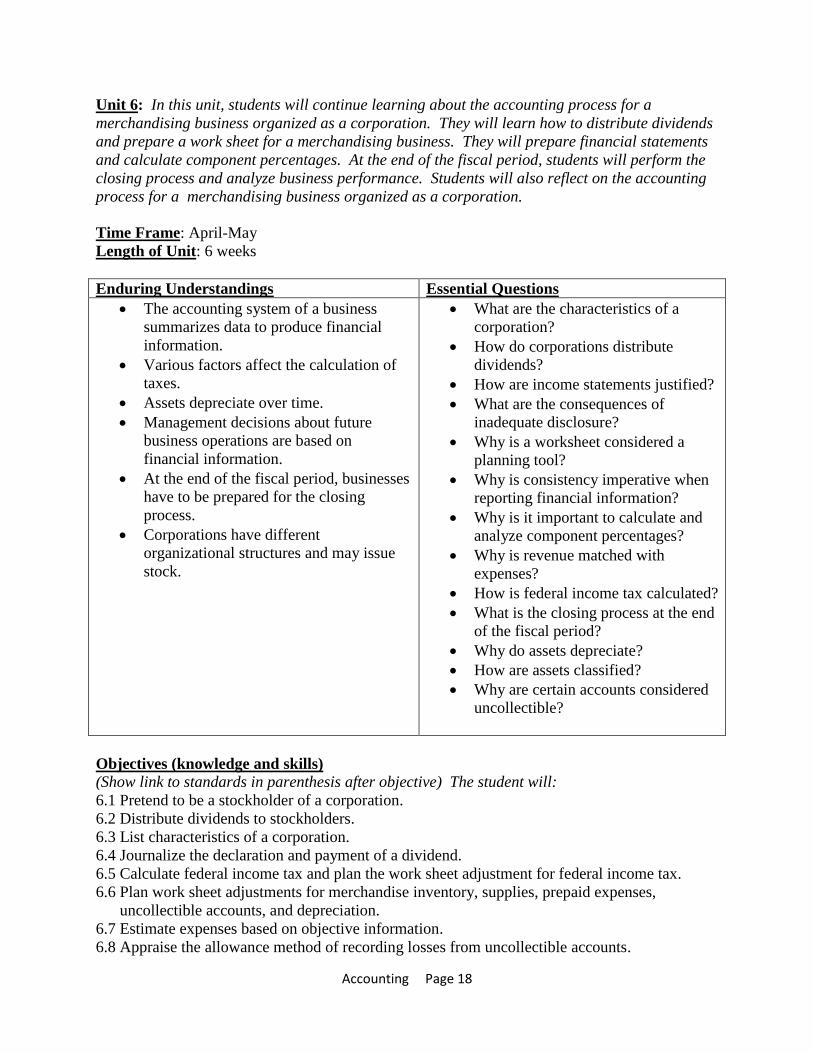

Unit 6: In this unit, students will continue learning about the accounting process for a

merchandising business organized as a corporation. They will learn how to distribute dividends

and prepare a work sheet for a merchandising business. They will prepare financial statements

and calculate component percentages. At the end of the fiscal period, students will perform the

closing process and analyze business performance. Students will also reflect on the accounting

process for a merchandising business organized as a corporation.

Time Frame: April-May

Length of Unit: 6 weeks

Enduring Understandings Essential Questions

The accounting system of a business

summarizes data to produce financial

information.

Various factors affect the calculation of

taxes.

Assets depreciate over time.

Management decisions about future

business operations are based on

financial information.

At the end of the fiscal period, businesses

have to be prepared for the closing

process.

Corporations have different

organizational structures and may issue

stock.

What are the characteristics of a

corporation?

How do corporations distribute

dividends?

How are income statements justified?

What are the consequences of

inadequate disclosure?

Why is a worksheet considered a

planning tool?

Why is consistency imperative when

reporting financial information?

Why is it important to calculate and

analyze component percentages?

Why is revenue matched with

expenses?

How is federal income tax calculated?

What is the closing process at the end

of the fiscal period?

Why do assets depreciate?

How are assets classified?

Why are certain accounts considered

uncollectible?

Objectives (knowledge and skills)

(Show link to standards in parenthesis after objective) The student will:

6.1 Pretend to be a stockholder of a corporation.

6.2 Distribute dividends to stockholders.

6.3 List characteristics of a corporation.

6.4 Journalize the declaration and payment of a dividend.

6.5 Calculate federal income tax and plan the work sheet adjustment for federal income tax.

6.6 Plan work sheet adjustments for merchandise inventory, supplies, prepaid expenses,

uncollectible accounts, and depreciation.

6.7 Estimate expenses based on objective information.

6.8 Appraise the allowance method of recording losses from uncollectible accounts.

Accounting Page 19

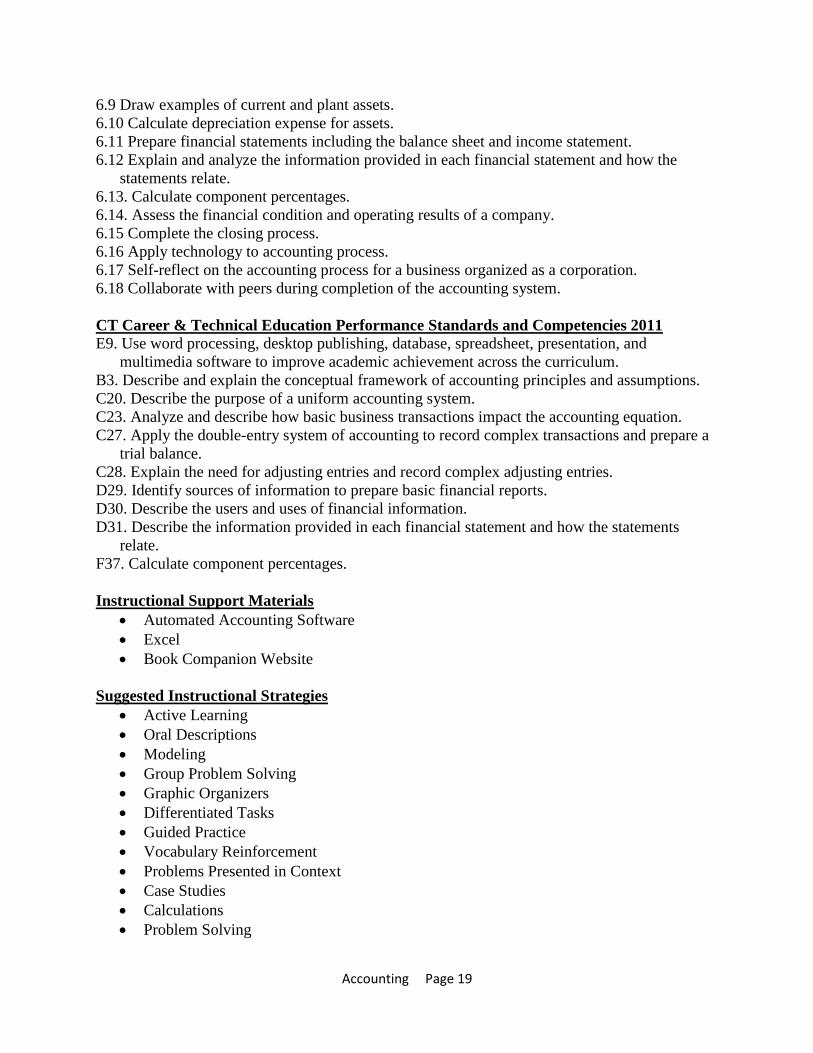

6.9 Draw examples of current and plant assets.

6.10 Calculate depreciation expense for assets.

6.11 Prepare financial statements including the balance sheet and income statement.

6.12 Explain and analyze the information provided in each financial statement and how the

statements relate.

6.13. Calculate component percentages.

6.14. Assess the financial condition and operating results of a company.

6.15 Complete the closing process.

6.16 Apply technology to accounting process.

6.17 Self-reflect on the accounting process for a business organized as a corporation.

6.18 Collaborate with peers during completion of the accounting system.

CT Career & Technical Education Performance Standards and Competencies 2011

E9. Use word processing, desktop publishing, database, spreadsheet, presentation, and

multimedia software to improve academic achievement across the curriculum.

B3. Describe and explain the conceptual framework of accounting principles and assumptions.

C20. Describe the purpose of a uniform accounting system.

C23. Analyze and describe how basic business transactions impact the accounting equation.

C27. Apply the double-entry system of accounting to record complex transactions and prepare a

trial balance.

C28. Explain the need for adjusting entries and record complex adjusting entries.

D29. Identify sources of information to prepare basic financial reports.

D30. Describe the users and uses of financial information.

D31. Describe the information provided in each financial statement and how the statements

relate.

F37. Calculate component percentages.

Instructional Support Materials

Automated Accounting Software

Excel

Book Companion Website

Suggested Instructional Strategies

Active Learning

Oral Descriptions

Modeling

Group Problem Solving

Graphic Organizers

Differentiated Tasks

Guided Practice

Vocabulary Reinforcement

Problems Presented in Context

Case Studies

Calculations

Problem Solving

Accounting Page 20

Suggested Assessment Methods

(Include use of school-wide analytic and course specific rubrics)

Quizzes

Chapter Tests

Computer Simulations

Web Quests

Presentations

Projects

Performance Based Assessment

School Wide Rubrics

Accounting Page 21

Unit 7: Accumulative review project of the accounting cycle for a merchandising business

organized as a corporation. In this unit, students will complete a reinforcement project using

Automated Accounting Software. The project encompasses the entire accounting cycle of a

merchandising business organized as a corporation.

Time Frame: June

Length of Unit:2 Weeks

Enduring Understandings Essential Questions

The accounting system is an integral

aspect of all business activities.

The accounting system of a business

summarizes data to produce financial

information.

Without consistent reporting, it would

be difficult for businesses to compare

results from year to year.

GAAP/IFRS principles impact the

recording of financial transactions and

the preparation of financial statements. Accounting interpretations impact

business decisions.

Various factors affect the calculation of

taxes.

Why is a worksheet considered a

planning tool?

Why do businesses compare results

from year to year?

How is financial data summarized?

What is the accounting process for a

merchandising business organized as a

corporation?

How is technology used in the

accounting process?

What is the closing process?

How are accounts classified?

In what ways are business decisions

affected by accounting interpretations?

Objectives (knowledge and skills)

(Show link to standards in parenthesis after objective) The student will:

7.1 Apply the double-entry system of accounting to record transactions in special journals.

7.2 Prepare a worksheet and plan adjustments.

7.3 Prepare financial statements including the balance sheet and income statement.

7.4 Explain and analyze the information provided in each financial statement and how the

statements relate.

7.5 Demonstrate how account classification drives the accounting system.

7.6 Organize, analyze and record payroll transactions.

7.8 Summarize the accounting practices related to payroll records.

7.9 Calculate employer payroll taxes.

7.10 Prepare payroll reports.

7.11 Calculate component percentages.

7.12 Collaborate with peers and make recommendations.

7.13. Assess the financial condition and operating results of a company.

7.14 Complete the closing process.

7.15 Apply technology to accounting process.

7.16 Self reflect on the accounting process for merchandising business organized as a

corporation.

7.17 Prepare and analyze payroll information.

Accounting Page 22

CT Career & Technical Education Performance Standards and Competencies 2011

E9. Use word processing, desktop publishing, database, spreadsheet, presentation, and

multimedia software to improve academic achievement across the curriculum.

B3. Describe and explain the conceptual framework of accounting principles and assumptions.

C20. Describe the purpose of a uniform accounting system.

C23. Analyze and describe how basic business transactions impact the accounting equation.

C27. Apply the double-entry system of accounting to record complex transactions and prepare a

trial balance.

C28. Explain the need for adjusting entries and record complex adjusting entries.

D29. Identify sources of information to prepare basic financial reports.

D30. Describe the users and uses of financial information.

D31. Describe the information provided in each financial statement and how the statements

relate.

E32. Prepare and maintain payroll records.

E33. Calculate and record transactions related to employee payroll.

E34. Calculate and record employer’s payroll taxes.

E35. Calculate and record payroll accruals.

E36. Journalize payroll transactions.

F37. Calculate component percentages.

Instructional Support Materials

Automated Accounting Software

Excel

Book Companion Website

Suggested Instructional Strategies

Computer simulation

Active Learning

Data Analysis

Focused practice

Suggested Assessment Methods

(Include use of school-wide analytic and course specific rubrics)

Formative and Summative Assessment

Performance Based Assessment

School wide rubrics