Welcome to ÅF’s Capital Markets Day - AF Consult ... · ÅF Capital Markets Day Stockholm,...

67

Welcome to ÅF’s Capital Markets Day

Transcript of Welcome to ÅF’s Capital Markets Day - AF Consult ... · ÅF Capital Markets Day Stockholm,...

Welcome to ÅF’sCapital Markets Day

Agenda for the day

09.15 History and ÅF in brief

Current position

Strategy

Divisional introduction

BREAK

11.20

12.40

13.00

Deep Dives

• Automotive

• Energy

• Design

• Smart City

Summary and questions

Closing and LUNCH

3

ÅF Capital Markets DayStockholm, November 8, 2017

Jonas Gustavsson, CEO

Development and ÅF in brief

• #3 among Nordic engineering companies

• Markets most comprehensive portfolio of service offer across industries

• International footprint

• ~10,000 employees

• Net sales 11.1 BSEK (2016)

ÅF in brief

Strong positions with diversified portfolio

INFRASTRUCTURE

INDUSTRY

ENERGY

DIGITAL

Private69%

Public31%

Diversified portfolio

Power

15%

Automotive &

Vehicle

16%

Rail & Roads

21%

Real Estate

18%

Life Science, Food &

Pharma

8%

Pulp&Paper

4%

Defence

2%

Telecom

3%

Mining&Steel

Production

2%

Petrocemical

3%

Financial

Services

2%

Other - Mfg

primarily…

Numbers from 2016

Top 10 clients – mix of strong national and international clients

(Volvo Cars

and AB Volvo)

~30 % of total

revenue

Combination of

private and public

clients

Strong base for

international growth

Solid financial performance

3,864,57 4,69 4,34

5,135,80

8,348,80

9,8511,07

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

344

486396

323

436491

843756

817

992

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

ÅF has shown strong growth and competitive performance in the last decade and has outgrown the market ~3 times in the past 10 years with stable margins at 8-9%

+12% p.a. +12% p.a.

Net Sales,

BSEK

EBITA,

MSEK

ÅF has combined solid organic growth with strong inorganic growth

12 10

-1 -4

10 63 3 5 3

129

4

-3

9

7

41

37 10

2007 15121009 14

-8

1308 11 2016

Organic

Inorganic

Inorganic/organic sales growth split, % change from previous year

▪ ÅF has grown by 12% p.a. over the last 10 years

– 8% acquired growth

– 4% organic growth

▪ The largest single contributor to the company’s growth is the acquisition of Epsilon in 2012 (impacting the sales in 2013)

ÅF has combined solid organic growth with strategic acquisitions

Acquired sales, BSEK

2.15

Epsilon 2012

7.01

Advansia 2012

80 additional acquisitions

0.430.32

0.36

Reinertsen 2016

0.55

Edy Toscano 2016

3.21

PRC 2015 Total

▪ Between 2008 and 2017, ÅF acquired 85 companies

▪ More than 50% of the total acquired sales stems from the five largest acquisitions

▪ Epsilon is the single largest acquisition

Good shareholder return

Total return

SEK

Source: Nasdaq OMX Nordic

Continued increase of dividends

0,410,31

0,130,25

0,50

0,880,69

1,00

1,88

0,44

1,631,63

0,25

0,00

0,33

0,630,75

1,631,63

2,002,00

2,50

2,75

3,25

3,50

3,75

4,50

0,00

0,50

1,00

1,50

2,00

2,50

3,00

3,50

4,00

4,50

5,00

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

14

SEK

Ex Date Split

From

Split

To

Adjustment

Factor

13/06/2014 1 2 2

31/05/2010 1 2 2

02/05/2006 1 2 2

Stock Splits

Source: Nasdaq OMX Nordic

Current position and new structure

Today #3 among Nordic engineering companies

11,070

13,486

16,531

5,019

ÅF has the market’s most comprehensive range of competencies and services to meet current global trends

SEK M

Four divisions with full P&L and international responsibility

International

Divisions

Decentralised

governance

BA:s with different

challenges

INFRASTRUCTURE INDUSTRY ENERGY DIGITAL

SOLUTIONS

39% 34% 12% 16%

Approx share of total net sales

International

Divisions

Decentralised

governance

BA:s with different

challengesBA BA BA BA

BA

• Buildings

• Rail&Road

• Project Management

• Water and Environment

• Architecture & Design

INFRASTRUCTURE INDUSTRY ENERGY DIGITAL

SOLUTIONS

Four divisions with full P&L and international responsibility

International

Divisions

Decentralised

governance

BA:s with different

challengesBA BA BA BA

BA BA BA

• Advanced

Manufacturing

• Automotive R&D

• Food & Pharma

• Process Industry

• Product

Development

• Product

Development

• Plant

Engineering

• Advanced

Technical

Service

• Buildings

• Rail&Road

• Project Management

• Water and

Environment

• Architecture &

Design

INFRASTRUCTURE INDUSTRY ENERGY DIGITAL

SOLUTIONS

Four divisions with full P&L and international responsibility

BA BA BA BA

BA

International

Divisions

Decentralised

governance

BA:s with different

challenges

• Buildings

• Rail&Road

• Project Management

• Water and

Environment

• Architecture &

Design

• Advanced

Manufacturing

• Automotive R&D

• Food & Pharma

• Process Industry

• Product

Development

• Product

Development

• Plant

Engineering

• Advanced

Technical

Service

• Energy Scandinavia

• Energy Switzerland

• Energy Czech

Republic

• Energy Finland

• International

Operations

Four divisions with full P&L and international responsibility

INFRASTRUCTURE INDUSTRY ENERGY

BA BA BA BA

BA BA BA

BA BA BA BA

BA

BA BA BA BA

BA

DIGITAL

SOLUTIONS

International

Divisions

Decentralised

governance

BA:s with different

challenges

• Advanced

Manufacturing

• Automotive R&D

• Food & Pharma

• Process Industry

• Product

Development

• Product

Development

• Plant

Engineering

• Advanced

Technical

Service

• Energy Scandinavia

• Energy Switzerland

• Energy Czech

Republic

• Energy Finland

• International

Operations

• Experience Design

• IT Solutions

• Embedded Systems

• Systems

Management

Four divisions with full P&L and international responsibility

INFRASTRUCTURE INDUSTRY ENERGY DIGITAL

SOLUTIONS

BA BA BA BA

BA BA BA

BA BA BA BA

BA

BA BA BA BA

BA

BA BA BA BA

• Buildings

• Rail&Road

• Project Management

• Water and

Environment

• Architecture &

Design

INFRASTRUCTURE INDUSTRY ENERGY DIGITAL

SOLUTIONS

… and structured country organisations supporting efficiency and local business

Strategy

Providing leading solutions for generations to come

ÅF - Making Future

Our vision

We create sustainable engineering and design solutions

Our mission

Our values

Brave

Devoted

Team players

WE ARE

27

Smart cities and

infrastructure

Industrial

digitalisation

Future

mobility

Changing

energy

landscape

Growth drivers

Changing customer dynamic

Partnership and alliances

related to new disruptive areas

Function and project delivery in

customers development process

Internationalisation with strong

partners

Design thinking

R&D

29

• ”The Sweden negotiation” – Highspeed trains, subways and residences.

• ” Norwegian National TransportationPlan 2018” –100 Bn NOK/each year

Urbanisation drives public investments

Internationalexpansion into

leading positions

GROWTH

Business modelshift to deliverhigher value

VALUE CREATION

Operationalexcellence

OPERATIONS

Best in classpeople practices

PEOPLE

Strategy based on four pillars

The new strategy

Geographical expansion in

core countries

• Solid market growth and

market share gain

• Leading/substantial

position

• Infrastructure, and full

leverage from Industry,

Energy and Digital

International growth in

selected niches

• Distinct ÅF competences

and capabilities - establish

footprint and expand

• Current areas:

o Automotive R&D

o Advanced Manufacturing

o Food & Pharma

o Process Industries

o Lighting

Expansion in global

investment projects

• Expert competence

services and projects

related to significant one-

off CAPEX project globally

• Structured evaluation to

ensure leverage in core-

countries

GROWTH - International expansion into leading positions

M&A – “bolt” on and platforms

VALUE CREATION

Business model shift to deliver higher value

Scale and leverage

– repetitive deliveries

State of the art project model – enabling most

complex projects

Partnering and cooperation

Development of “professional service model”

– XF-Teams

Professional services (T&M)

“Professional Team” (T&M)

T&M Projects

Fixed price projects

Solutions

Pro-ducts

~50%

~45%

<5%

1 Cross ÅF projects

and solutions

2 Digitalization

3 After market and

operational maintenance

VALUE CREATION

Business model shift to deliver higher value

OPERATIONSOperational excellence

INFRASTRUCTURE INDUSTRY ENERGY DIGITAL

SOLUTIONS

BA BA BA BA

BA BA BA

BA BA BA BA

BA

BA BA BA BA

BA

BA BA BA BA

Clear structure with full

P&L and accountability

Distinct plans for each BA

– turnaround – profitability

- growth

Strengthened

performance management

36

-10,0%

-5,0%

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

-15,0% -5,0% 5,0% 15,0% 25,0% 35,0% 45,0%

EB

IT

A %

GROWTH %

OPERATIONSOperational excellence

Business Area portfolio

with different challenges

Evaluated on attractivity

and profitable growth

potential

Strong performance

management with

increased accountability

Portfolio Management

OPERATIONSOperational excellence

Adjusted financial steering

• Support cross collaboration

• Continuously improve project steering

• Strengthen performance- and portfolio management

Optimised pricing and sourcing

• Implementation of structured Low Cost Sourcing for key projects and deliveries

• Partner network 27,000

• Strengthening strategic pricing process across ÅF

Ethical commitment

• Adopted rules and principles creating the foundation of ÅF:s Ethical commitment

PEOPLEBest in class people practices

Strategy activation – new clear strategic direction will increase engagement

The most interesting careers

Competence development via own academy – ÅF Academy

Competitive compensation and benefits

PEOPLEPeople engagement and development

PEOPLELeadership

Common leadership platform – manager ‘guiding stars’

Leadership development in ÅF Academy

Proactive and structured management & succession planning

41

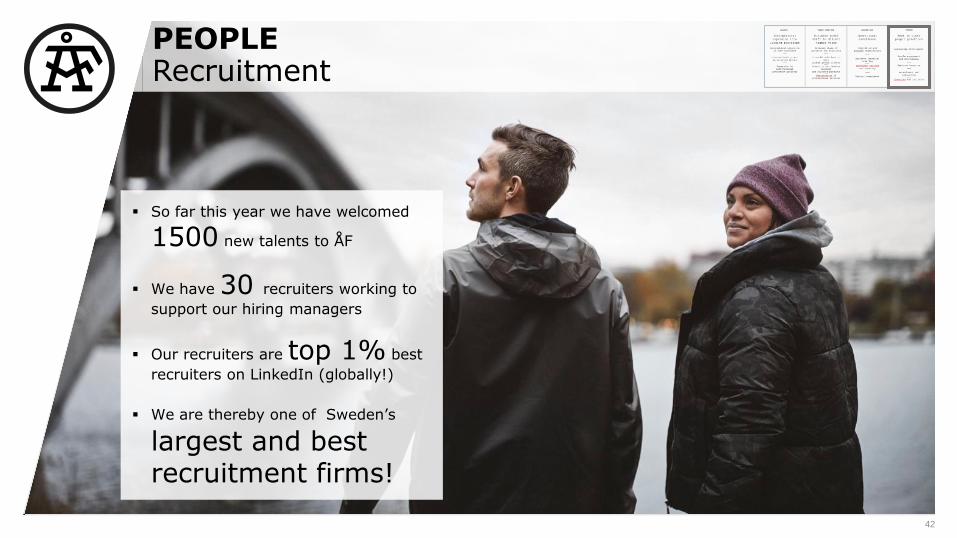

PEOPLEEmployer Branding

42

▪ So far this year we have welcomed

1500 new talents to ÅF

▪ We have 30 recruiters working to

support our hiring managers

▪ Our recruiters are top 1% best

recruiters on LinkedIn (globally!)

▪ We are thereby one of Sweden’s

largest and best recruitment firms!

PEOPLERecruitment

43

PEOPLEDiversity and inclusion

Thank you!

Financial targets

GROWTH

• 10 % organic growth and add on

acquisitions

• Platform acquisitions on top

Growth - Net Sales

46

3,864,57 4,69 4,34

5,135,80

8,348,80

9,8511,07

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

+12% p.a.

47

▪ Solid▪ Reinertsen (inkl Tegn 3)▪ Erstad & Lekven▪ Optiman

500

▪ Edy Toscano 430

▪ Aries 50

▪ Midtconsult▪ Traffic team

225

Estimated annual net sales 2,100 MSEK

▪ Koncept Stockholm▪ Vatten & Miljöbyrån▪ Teknoplan▪ Quality Engineering▪ Reinertsen▪ Reinertsen Oil & Gas

850▪ Sjöland&Thyselius▪ Ingenjörsprojekt▪ Alteco▪ sandellsandberg▪ inUse▪ Eitechs Automation business

▪ Light Bureau 6

Growth by acquisitions 2016-2017

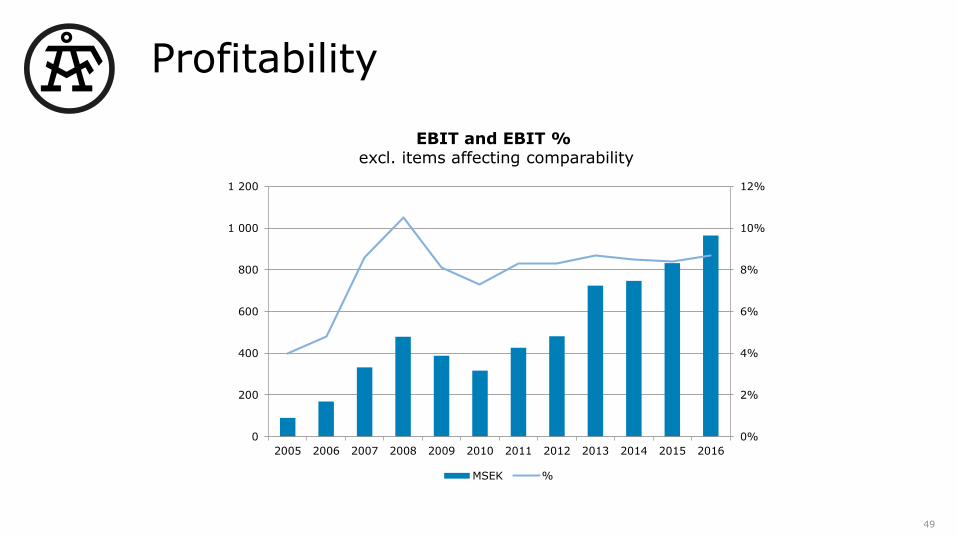

Financial targets

EBITA MARGIN

• 10 % over a business cycle

Profitability

49

0%

2%

4%

6%

8%

10%

12%

0

200

400

600

800

1 000

1 200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

MSEK %

EBIT and EBIT % excl. items affecting comparability

Financial targets

NET DEBT

• Net debt/EBITA 2.5

0

50

100

150

200

250

300

350

-100

0

100

200

300

400

500

600

700

Cash Flow from operating acivities Dividend paid

Stable cash flow

51

Div

idend p

aid

Cash F

low

fro

m o

pera

ting a

ctivitie

s

MSEK

Low volatility in earnings

52

ÅF EBIT marginQ1 2008 – Q2

2017At 3.0x ND/EBITDA

Financial targets

GROWTH

• 10 % organic growth and add on

acquisitions

• Platform acquisitions on top

EBITA MARGIN

• 10 % over a business cycle

NET DEBT

• Net debt/EBITA 2.5

Summarisingour strategy

GROWTH

• 10 % organic growth and

add on acquisitions

• Platform acquisitions on

top

EBITA MARGIN

• 10 % over a business

cycle

NET DEBT

• Net debt/EBITA 2.5

FINANCIAL TARGETS

57

INFRASTRUCTURE DIVISION

Mats PåhlssonDivisional Manager

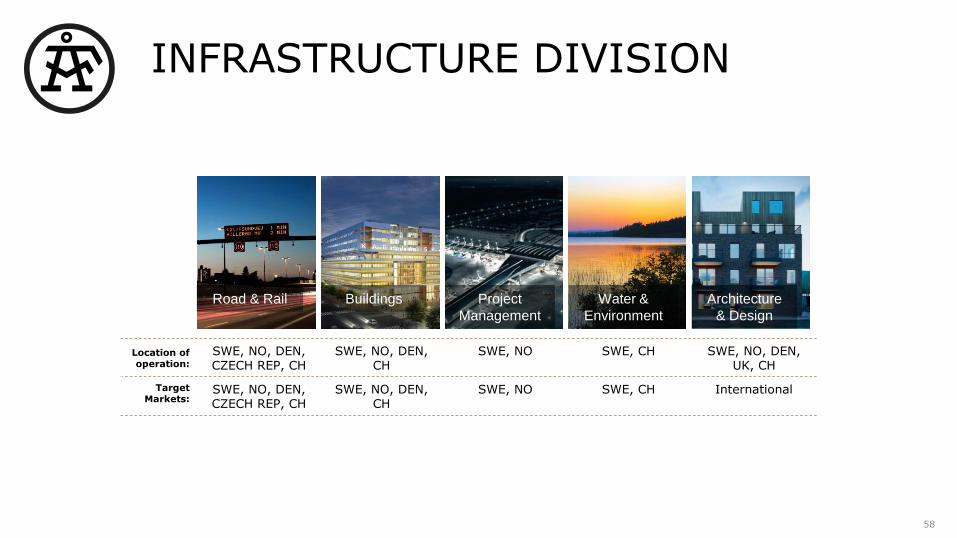

INFRASTRUCTURE DIVISION

58

Location of operation:

SWE, NO, DEN, CZECH REP, CH

SWE, NO, DEN, CH

SWE, NO SWE, CH SWE, NO, DEN, UK, CH

Target Markets:

SWE, NO, DEN, CZECH REP, CH

SWE, NO, DEN, CH

SWE, NO SWE, CH International

Road & Rail Buildings Project

Management

Water &

Environment

Architecture

& Design

INFRASTRUCTURE DIVISION

59

• Urbanisation

• Sustainability

• Digitalisation

Global Trends

as

StrategicDirection

• Smart city

• Growing our local business in core countries

• Developing identified growth areas

60

INDUSTRY DIVISION

Jonas LarssonDivisional Manager

INDUSTRY DIVISION

61

AUTOMOTIVER&D

FOOD &PHARMA

PROCESSINDUSTRY

INDUSTRIALENGINEERING

SPECIALIZED TECHNICAL SERVICES

ADVANCEDMANUFACTURING

PRODUCT DEVELOPMENT

Location of

operation:

SWE SWE, China, BrazilUK

SWE, Denmark, Estonia, NOR

SWE, Czech Republic

SWE, NOR SWE, Denmark SWE

Target Markets:

International International International International SWE, NOR, DEN, FIN

SWE, NOR, DEN, FIN

SWE, NOR, DEN, FIN

INDUSTRY DIVISION

62

High pace in technology development. Calls for partnering and outsourcing of “packages”.

Need for new technology areas, e.g. software/R&D, additive manufacturing

Need for productivity improvements in manufacturing processes.

Changing landscape within Automotive, i.e. electro mobility, autonomy, connectivity.

Global Trends

as

StrategicDirection

Accelerated international growth in four distinct segments.

Strengthen position in Sweden, with growth into core countries for the other three.

Leverage profitability from specialized services in all segments.

Spearhead Industrial digitalization by process and business knowledge

63

ENERGY DIVISION

Roberto GerosaDivisional Manager

ENERGY DIVISION

64

World electricity generation increase of 69% by 2040 due to:• population and economic growth in the

emerging countries• smart cities and future mobility going ”from

fossil fuels to electricity”.

Transition of the energy markets in the European Core markets:

Main growth in Renewable Energy, demand for reliable transmission and distribution networks, storage and digital solutions.”

Bulk energy needed in International markets:

• Investments in traditional generation projectsand T&D grids providing base load capacity

Global Trends

as

StrategicDirection

Core markets:

Stretch along the value chain in each market and expand offering.

“Become the country’s #1 leading energy company.”

International operations:

Selected markets where international competence is valued and which are rich in energy investment opportunities.

“Be a leading player in selected markets.”

ENERGY DIVISION

SegmentsHeat & Power

Nuclear EnergyHydropowerRenewable &

Energy StrategyTransmission &

Distribution

BA International Energy

OperationsBA Switzerland

BA Czech Republic

BA FinlandBA Scandinavia

Sales

66

DIGITAL SOLUTIONS DIVISION

Lennart WaldenströmDivisional Manager

DIGITAL SOLUTIONS DIVISION

67

IT SOLUTIONS

Location of

operation:

SWE, USA SWE, NOR SWE SWE

Target Markets:

International Scandinavian International Scandinavian

EMBEDDED SYSTEMS

SYSTEMS

MANAGEMENT

EXPERIENCE

DESIGN

DIGITAL SOLUTIONS DIVISION

68

Intelligence inside products increasing

Increasing demand for connectivity and low latency communication

Connected products increase the need of analytics, usability and service design

Defense industry is in great demand

Global Trends

as

StrategicDirection

Full service digitalization partner within ÅF Growth pillars

Increase solution delivery in Sweden, and select countries

National expertise in connectivity and information infrastructure

Scandinavian expertise within Systems Engineering for Defense