Welcome to CommInsure. -...

28

Welcome to CommInsure.

Transcript of Welcome to CommInsure. -...

Welcome to CommInsure.

Important informationThis information is provided by CommInsure, a registered business name of Commonwealth Insurance Limited ABN 96 007 524 216 AFSL 235030 (CIL) and The Colonial Mutual Life Assurance Society Limited ABN 12 004 021 809 AFSL 235035 (CMLA), which are wholly owned but non-guaranteed subsidiaries of Commonwealth Bank of Australia ABN 48 123 123 124. Motor Insurance is issued by Allianz Australia Insurance Ltd ABN 15 000 122 850 AFSL 234708 (Allianz). The Commonwealth Bank of Australia does not guarantee the obligations or performance of Allianz or the products they offer.

This document is for use by advisers and Commonwealth Bank Group employees only.

1

Contents

2 Introduction

3 Why CommInsure?

4 Financial strength

5 Flexible remuneration structures

7 Competitive premiums

10 Life, Disability and Trauma Cover

13 Income protection insurance

15 Guaranteed annuities

16 Investment Growth Bond

17 Underwriting

19 Claims

20 Superior service standards

21 Sales and marketing support

23 How to contact us

24 CommInsure product offerings

CommInsure helps to protect the lifestyles of Australians with a fresh approach to insurance through innovation, simplicity, competitive products and responsive service.We are a leader in the Australian insurance industry dedicated to providing our partners and customers with professional and supportive service. CommInsure is the insurance arm of the Commonwealth Bank Group.

CommInsure has a fresh approach to personal risk insurance, backed by a strong history – as one of Australia’s largest life risk insurers, with over three million clients and a national presence dating back over 130 years.

CommInsure represents the union of many experienced and trusted life risk insurers including Prudential, Legal and General, Scottish Amicable and Colonial. Our statutory fund currently has one of the highest solvency ratios of some life risk insurers in Australia (see page 4), and our financial strength is shown through The Colonial Mutual Life Assurance Society’s (CMLA)1 very strong Standard & Poor’s AA rating (see page 4).

Our awards include:

Life Insurance Company of the Year• , Australia and New Zealand Institute of Insurance and Finance Awards 2005 and 2007.

Best Life Insurance Company• , Australian Banking & Finance Insurance Awards 2005.

Best Life Insurance Product• , Australian Banking & Finance Insurance Awards 2003, 2004 and 2005.

Term Life Product of the Year• , Personal Investor Magazine Awards for Excellence in Financial Services 2005.

Most Innovative Income Protection Product• , Asset Magazine Awards 2006.

Best Income Protection• , Money Magazine, Best of the Best 2007 Awards.

Joint winner of • Trauma Product of the Year, Personal Investor Magazine Awards for Excellence in Financial Services 2005.

Annuity Provider of the Year• , Plan For Life – awarded CommInsure a Gold award in the Long Term Annuity category and a Gold in the Lifetime Annuity category in 2006.

Winner of Money Magazine’s • Best of the Best Annuity Award for 2005, and again in 2006.

Best Call Centre• , Australian Banking & Finance Insurance Awards 2005.

Commitment to customersCommInsure is committed to providing all customers with innovative, straight forward insurance products that provide them with protection and a high level of understanding and service when they need it most. We will continue to do this through:

ongoing product developments•

continual monitoring of customer satisfaction•

prompt and efficient payment of all genuine claims•

employment of dedicated insurance specialists•

clear and simple product information.•

Introduction

2

1 CommInsure is a registered business name of CMLA.

Commitment to financial advisersCommInsure is committed to building awareness of the need for insurance, and providing the best possible service to advisers.

To do this we will continue to:

• engageyou,ourbusinesspartners,tohelpfurtherdevelop our products and services

• advertisethebenefitsofinsurancethroughtargetedmarketing campaigns

• provideyouwitharangeofsalesandmarketing material, and

• ensurethatourspecialistsareavailabletoprovideadditional assistance and technical expertise.

On a local level, we provide you with state-based sales and underwriting teams that are dedicated to helping improve our service delivery and help support and grow your business.

Claims philosophyCommInsure’s claims philosophy is simple: we pay all genuine claims promptly and efficiently. Our claims history substantiates our commitment to this philosophy. For the 2006 calendar year, the following claims were paid in our retail area:

Life Care $63.0 million•

TPD/Trauma $34.8 million•

Income Protection $44.5 million•

Leading product rangeCommInsure offers a range of straightforward products to help your clients build their wealth and protect it.

Income Care Range

Income Protection• Total and Permanent Disability (TPD) paid as a tax-free

lump sum.

• Unemployment Benefit – helps cover Commonwealth Bank loan repayments if the client is involuntarily unemployed.

• Flexibility to reduce waiting period without further underwriting.

Rewards Cover Benefit – complimentary $50,000 •accidental death cover after holding policy for three years.

Total Care Plan RangeTrauma

Trauma Buy Back Benefit – reinstates full trauma cover •at no cost after twelve months from a trauma cover claim payment.

Trauma Plus offers cover for an extensive range of events •including Heart Attack, Stroke and Cancer.

Full Trauma Benefit upon diagnosis of degenerative •conditions including Parkinson’s Disease, Dementia and Alzheimer’s Disease.

Life, TPD and TraumaDay one TPD – payable on specific conditions without •waiting period.Financial Planning Benefit – up to $5,000.•Accommodation Benefit – helps cover carer’s •accommodation costs.Loyalty Bonus Benefit – 5% bonus benefit after five years •of maintaining a policy.Stand-alone Accidental Death Cover.•

Investment Range

Investment Growth Bonds• Combines benefits of a managed fund with the security

and tax benefits of a life insurance policy.An insurance bond that provides a range of investment •options, in a simple tax-effective investment.

AnnuitiesCommInsure offers an extensive range of award-winning guaranteed annuities including Lifestream Guaranteed Income and Guaranteed Index Tracked Annuity.

Well regarded within the industryAt CommInsure, we continually achieve high ratings from research houses’ product reports for the comprehensive features offered in all our personal risk products.

Providing cover to more of your clientsCommInsure aims to provide cover to more Australians by improving the accessibility and availability of personal risk insurance.

To help improve accessibility, CommInsure Life Care offers the Limited Term – a first within the Australian insurance industry. This means that for clients who would otherwise have significant loadings applied – or even be declined insurance – they can now be insured for a period of five through to 15 years (instead of to age 65, 80 or 99) in most cases. The most common situation where this type of policy would be of value, is for clients who are suffering from medical conditions – such as Diabetes and Multiple Sclerosis. These clients are often unable to receive life cover from any of our competitors. This feature means more Australians and their families can afford protection.

CommInsure has also recently introduced a Child Cover Option which makes insurance accessible to young Australians. CommInsure’s Child Cover Option provides the ability for parents to attach Life and Trauma Cover on their child’s life to their policy, helping to ease the financial strain and stress caused in the event of a child’s illness or death.

Simpler applicationsWe have made applying for insurance easier for you and your clients by speeding up the underwriting process with our new Short Personal Statement. The Short Personal Statement can be completed when you are applying for cover up to $1 million each for Life, TPD and Trauma and $6,000 per month for Income Protection. You can download the Short Personal Statement on the Adviser web site https://adviser.comminsure.com.au.

Why CommInsure?

3

Financial strength

When considering personal risk insurance, it is important to consider the insurer’s credit rating. A strong rating means security of payment in the event of a claim. This is especially important when looking at income protection products where there may be ongoing claims for up to 40 years.CommInsure is a registered business name of The Colonial Mutual Life Assurance Society Limited (CMLA) which has a very strong Standard & Poor’s AA credit rating. Below are the Standard & Poor’s credit ratings for CommInsure and some of our competitors.

AIG Life AA+ Asteron Life Limited A

CommInsure AA Aviva A

AMP AA- Macquarie Life A

AXA/AC&L AA- Suncorp A

MetLife AA- Zurich A

MLC Limited AA- Tower BBB+

ING Life Limited A+ ASGARD NR

St George A+ Westpac Life NR

Source: Pro Planner, June 2007.

In March 2006, CommInsure enjoyed sales of $176 million in the life insurance risk market. At the end of 2006, we had excess reserves in the order of $5.3 billion in life insurance risk products. The table below shows CommInsure’s ratio of free reserves to net solvency liabilities, and compares this with some of the other life risk insurers in Australia.

Company Net solvency liabilities $M Excess reserves $MRatio of free reserves to net solvency liabilities

AIG Life 459.8 50.5 11.0%

AMP 25,209.0 2,683.0 10.6%

Asteron 805.1 105.6 13.1%

Aviva 1,448.3 137.7 9.5%

AXA Australia 10,689.1 1,430.3 13.4%

CommInsure 5,941.4 9,612.2 161.8%

ING Australia 5,018.3 424.8 8.5%

MetLife 2,479.0 259.5 10.5%

MLC 3,641.0 446.1 12.3%

Suncorp 2,141.4 509.1 23.8%

TOWER 987.4 172.6 17.5%

Zurich 655.9 73.2 11.2%

Table source: Plan for Life, March 2006.

4

Flexible remuneration structures

Personal Insurance PortfolioWe offer a wide choice of commission options and our levels are very competitive. We also offer the option of dial up or duration based commission structures.

Preferred commission rates (GST inclusive)

Commission option* Initial Hybrid 1 Hybrid 2 Level

Initial commission (year one) % of basic annual premium 114.95% 60% 85% 31%

Renewal commission (year two onwards) % of annual premium 10.04% 25% 20% 31%

* As selected by the adviser.

Where:

‘Basic Annual Premium’ is the first year’s premium excluding stamp duty and frequency loadings.•

‘Annual Premium’ is the premium received each year, after the first year, excluding stamp duty.•

Commission options (GST inclusive)Syndicate plans allow advisers to dial commission rates down or up. Where syndicate plan options are selected, the initial commission rates (% of basic annual premium) and the change in future premium rates will be the amounts shown in the following table. Premium changes are for the life of the policy, unless otherwise specified. Syndicate plan options do not alter the renewal commission rates (% of annual premium) outlined in the preferred commission rate table, with the exception of:

1. Level commission plans, where initial and renewal commission is paid at the same rate, and

2. Plan 8, where 0% renewal commission applies.

CommInsure’s 5-4-3-2-1 premium reduction Our 5-4-3-2-1 premium reduction gives advisers the ability to offer reduced premiums to clients across the CommInsure Personal Insurance Portfolio while maintaining the same percentage commission. The permanent reduction applies to all components excluding the policy fee and is labelled in the table below as ‘1 Special’.

Option Preferred rates syndicate plan number

Initial 1 2 3 4 5 6 7 8 9 1 Special

Initial commission 114.95% 90.06% 99.96% 90.06% 59.95% 29.98% 0% 0% 135.02% 114.95%

Renewal commission 10.03% 10.03% 10.03% 10.03% 10.03% 10.03% 10.03% 0% 10.03% 10.03%

Premium effect 0% -15%1 -2.5% -5% -10% -15% -20% -25% +5% -5%2

Hybrid 1 1 2 3 4 5 6 7 8 9

Initial commission 59.95% N/A 44.96% 29.98% 0% N/A N/A N/A 80.02% N/A

Renewal commission 25.02% N/A 25.02% 25.02% 25.02% N/A N/A N/A 25.02% N/A

Premium effect 0% N/A -2.5% -5% -10% N/A N/A N/A +5% N/A

Hybrid 2 1 2 3 4 5 6 7 8 9

Initial commission 85% N/A N/A N/A N/A N/A N/A N/A N/A N/A

Renewal commission 20% N/A N/A N/A N/A N/A N/A N/A N/A N/A

Premium effect 0% N/A N/A N/A N/A N/A N/A N/A N/A N/A

Level 1 2 3 4 5 6 7 8 9

Initial commission 31% N/A 29.01% 26.5% 21.01% 14.5% 8% N/A 35% N/A

Renewal commission 31% N/A 29.01% 26.5% 21.01% 14.5% 8% N/A 35% N/A

Premium effect 0% N/A -2.5% -5% -10% -15% -20% N/A +5% N/A

5

1 Plan 2 reduces premium in the first four years only: -15% in year one, -5% in year two, -5% in year three and -2.5% in year four. No discount applies thereafter.2 Plan 1 Special reduces premiums in the first five years only: – 5% in year one

– 4% in year two – 3% in year three – 2% in year four – 1% in year five.

(no discount applies thereafter).

Flexible remuneration structures

Guaranteed annuities and Investment Growth BondAdvisers may receive commission in two separate components across our annuity and insurance bond range – an initial commission and ongoing service commission.

Initial commission is paid when the policy commences. It is a percentage of the investment made and, in the case of annuities, depends on the term of the policy. The commission options payable are outlined below:

Lifestream Guaranteed Annuities

Term of policyInitial commission (% of amount invested)

Ongoing service commission

One year 0.66% Nil

Two years 1.32% Nil

Three years 1.98% Nil

Four years 2.64% Nil

Five years 3.30% Nil

Six to 25 years 3.30% 0.33% p.a. of the original amount invested

Guaranteed Index Tracked Annuity (GITA)

Term of policyInitial commission (% of amount invested)

Ongoing service commission

Two years 1.10% Nil

Three years 1.65% Nil

Four years 2.20% Nil

Five years 2.75% Nil

Six to 25 years 2.75% 0.66% p.a. of the withdrawal value of the investment

An additional amount of up to 10% of the remuneration may be paid by way of bonus, for meeting certain sales targets.

Investment Growth Bond (IGB)

Term of policyInitial commission (% of amount invested)

Ongoing service commission

Unlimited Up to 4.40% 0.44% p.a. of account balance

Advisers may receive an additional incentive of up to 1% of the amount invested. This is issued from time to time and is at no additional cost to investors.

6

CommInsure has a profitable and sustainable portfolio and offers both level and stepped premium rates across our Income Care Range, Total Care Plan and Total Care Plan Super product ranges.Competitive pricesUnlike some other insurers, CommInsure operates with a low level of reinsurance. We are able to do this because of our large size and the strength of our statutory fund. This means that CommInsure’s premium rates are less exposed to rate changes imposed by some of our reinsurers, allowing us to operate with more independence.

We offer rates that are competitive across our product range – offering stepped or level premium rates payable annually, half yearly, quarterly or monthly that may be payable by Bpay®, direct debit or credit card. Alternatively, you can make half yearly or annual payments by cheque.

CommInsure premium rates are regularly reviewed so that they remain competitive, yet sustainable, to ensure the profitability and security of the risk portfolio. Our claims experience, market forces and our targeted profitability levels affect the pricing of our products.

Our level premiums for both the Income Care and Total Care Plan ranges are consistently competitive across all groups. CommInsure also bases all CPI premium increases for level premium policies on the age at which the client originally takes out the policy. Many other insurance companies base the premium paid on CPI increases on the age of the policyholder when the CPI increase occurs. This translates to long-term savings for your customers, when they take out a level premium policy with indexation attached, with CommInsure.

We aim to provide affordable solutions to meet your clients’ insurance needs and are constantly analysing our claims experience and competitive position to provide your clients with competitively priced cover.

Our Income Care Range stepped premiums with waiting periods of 30 days or more are competitive and our stepped Trauma premiums are also very competitive.

We also offer a 10% discount on Business Overheads Cover rates if your client also has an Income Care or Income Care Plus policy with us.

Large sums insuredWe offer discounts in rates for higher levels of cover across Life, TPD and Trauma. These discounts increase as the level of cover increases:

In Total Care Plan we offer up to a • 35% discount for larger sums insured.

The discounts for larger sums insured under the Income •Care Range are shown in the table below.

Income Care Range large sum insured discounts

Monthly benefit

Premium discount

Income Care Plus

Income Care

Business Overheads Cover

$3,000 to $4,999 5.0% 2.5% 5.0%

$5,000 to $9,999 7.5% 7.5% 7.5%

$10,000 and over 12.5% 12.5% 12.5%

CALQ – our quoting systemCommInsure annuities and life quoting system, CALQ, is designed to make quoting quick and easy. With same screen quotations, you can quickly cross-reference and update quotes to match all client’s needs. CALQ is available at https://adviser.comminsure.com.au.

To obtain a password, click on the ‘Forgot my Password’ link and follow the prompts.

7

Competitive premiums

® Registered to Bpay Pty Limited ABN 69 079 137 518.

8

Competitive premiums

Comparison of the cost of optionsThere are a number of different additional options that can be taken up in a policy from the Income Care Range, Total Care Plan or Total Care Plan Super. The following examples are intended to give an indication of the cost of these additional options and are priced as at 24 April 2007.

Income Care Range comparisonBelow are two premium examples comparing the basic stepped monthly premium with the addition of other options such as the Accident Option.

Example 1

35-year-old•

male•

non-smoker•

accountant•

benefit period to age 65•

policy expiry at age 65•

monthly benefit $3,125•

waiting period one month•

agreed value•

NSW resident as at 24 April 2007.•

Example 2

35-year-old•

male•

non-smoker•

electrician•

benefit period five years•

policy expiry at age 65•

monthly benefit $3,125•

waiting period one month•

indemnity•

QLD resident as at 24 April 2007.•

BaseSteppedPremium

$82.87$85

$90

$95

$100

$70

$75

$80

Monthlypremium

Increasing Claim Option

$84.42

Cash Back Option

$90.48

SuperContinuance

Option

$92.00

AccidentOption

$92.81

$40

$45

$50

$55

$60

$25

$30

$35

Monthlypremium

BaseSteppedPremium

Increasing Claim Option

Cash Back Option

SuperContinuance

Option

AccidentOption

$47.37

$52.63 $51.46 $51.28 $50.85

9

Total Care Plan comparisonBelow are two premium examples comparing the basic stepped monthly premium with the basic stepped monthly premium with the addition of each of the options available for a Life Care policy, such as Plan Protection.

$30$31.21 $31.65

$35.71 $36.61

$35

$40

$45

$50

$15

$20

$25

Monthlypremium

BaseSteppedPremium

Plan Protection

GuaranteedInsurability

(Personal Events)

GuaranteedInsurability

(BusinessEvents)

35-year-old•

male•

non-smoker•

accountant•

Life Care $500,000•

VIC resident as at 24 April 2007.•

$45

$50

$55

$60

$52.07$53.43

$54.59 $56.93

$65

$40

Monthlypremium

BaseSteppedPremium

Plan Protection

GuaranteedInsurability

(Personal Events)

GuaranteedInsurability

(BusinessEvents)

35-year-old•

female•

non-smoker•

accountant•

Life Care $200,000•

TPD $200,000 (any occupation)•

Trauma $200,000•

WA resident as at 24 April 2007.•

Total Care Plan Super comparisonBelow are two premium examples comparing the basic stepped monthly premium and the stepped monthly premium with each of the options available for a Total Care Plan Super policy.

$35

$40

$45$39.91 $40.91

$45.58$47.45$50

$55

$25

$30

Monthlypremium

BaseSteppedPremium

Plan Protection

Accidental Death Cover

$200,000

TPD ownoccupationdefinition

35-year-old•

female•

non-smoker•

accountant•

Life Care $500,000•

TPD Cover $500,000 (any occupation)•

NSW resident as at 24 April 2007.•

$40$40.02 $41.05

$45.85

$54.60

$45

$50

$55

$60

$30

$35

$25

$20

Monthlypremium

BaseSteppedPremium

Plan Protection

Accidental Death Cover

$200,000

Accidental Death Cover

$500,000

35-year-old•

female•

non-smoker•

architect•

Life Care $1,000,000•

TAS resident as at 24 April 2007.•

10

Life, Disability and Trauma Cover

Total Care Plan (TCP) provides a variety of options to protect the insured and their family in the event of the insured’s death, total and permanent disablement or if they suffer one of our specified trauma conditions.

Benefits designed with understandingThe benefits of the Total Care Plan and Total Care Plan Super have been designed with an understanding of what clients want, as well as what they need.

Life Care featuresCommInsure’s Life Care offers a range of features that help to set it apart from the market.

Our • Life Care Severe Hardship Booster Benefit pays a higher Life Care benefit (up to $250,000 additional to the Life Care sum insured) if death or terminal illness are due to specific conditions such as Meningococcal Disease, Loss of Limbs or Sight.

Our Total Care Plan offers a • Life Care Advance Payment Benefit. This benefit may pay part of the Life Care benefit in advance to help with funeral costs.

Our Total Care Plan Life Care also helps support the family •of an insured, with the Financial Planning Benefit. This benefit helps cover the cost of financial planning up to $5,000 after the Life Care benefit is paid.

If your clients are paid a benefit under Trauma or TPD •Cover, the Buy Back feature reinstates 100% of the amount of any Life Care benefit reduced by the claim one year from the date their Trauma or TPD claim was accepted. This feature is included in all Life Care products at no extra cost.

Accidental death cover can be selected to go with Life •Care, or just by itself. It’s a low cost death cover and pays a lump sum in the event of death by accident. This cover is not available with Total Care Plan Super.

Total and Permanent Disability (TPD) Cover featuresThe • TPD Cover Severe Hardship Booster Benefit pays a higher TPD Cover benefit (up to $250,000 additional to TPD sum insured) for specific conditions such as Meningococcal Disease, Loss of Limbs or Sight.

The TPD • Financial Planning Benefit helps cover the cost of financial planning up to $5,000 after the TPD Benefit has been paid.

In an industry first, CommInsure offers • Day 1 TPD Cover which waives the three month qualification period if the insured is totally and permanently disabled by one of 18 nominated conditions (including paralysis).

Trauma Cover features (TCP only)We recognise that some conditions can cause more •hardship than others. Where these conditions have been identified, we pay additional benefits to offer extra support to your clients in this time of need. Trauma can be applied for up to age 62.

The • Trauma Cover Severe Hardship Booster Benefit pays a higher Trauma Cover benefit (up to $250,000 additional to Trauma Cover sum insured) for certain medical conditions.

The • Trauma Financial Planning Benefit helps cover the cost of financial planning up to $5,000 after the Trauma Benefit has been paid.

Life Care Total Care Plan Super

Life Care Life Care and TPD Cover

••

Trauma Cover

Total Care Plan Super

Accidental Death Cover

TPD Cover

Total Care Plan

Life Care Total Care Plan Super

Life Care Life Care and TPD Cover

••

Trauma Cover

Total Care Plan Super

Accidental Death Cover

TPD Cover

Total Care Plan

11

Payment of claimsOur Trauma Cover is offered for • 48 specified events (58 if Trauma Plus is selected), and includes conditions such as Waiting List for Major Organ Transplant and Removal of Carcinoma in situ of the Breast and Advanced Diabetes. The Trauma Plus Cover options provides cover for an additional ten partial trauma conditions including diabetes complications, melanoma and female specific conditions such as Carcinoma in situ of the Cervix Uteri, Carcinoma in situ of the Vulva or Vagina.

If your clients are paid a Trauma Benefit, the buy back •feature reinstates 100% of the cover amount reduced by the claim one year from the date the claim was paid. This feature is included for no additional premium for both Trauma as a rider to Life Cover and stand-alone Trauma.

When your client makes a trauma claim and it is accepted by us, our promptness of payment is essential and can make a real difference in the lives of your clients. This is why CommInsure prides itself on paying accepted trauma claims quickly, helping to relieve the financial stress during difficult times.

Upgrade provision (for both TCP and ICR)CommInsure has updated its products four times in the last four years, passing all changes to existing customers and ensuring clients policies have the most up to date benefits and features.

Loyalty rewardedCommInsure values loyalty and, for this reason, we reward policyholders with additional benefits after policies have been in place for five years.

The Trauma Cover Loyalty Bonus Benefit (TCP only) automatically increases your client’s Trauma Cover Benefit and Trauma Cover Advance Payment Benefit by 5% after the policy has been in place for five years.

The Life Care Loyalty Bonus Benefit automatically increases your client’s Life Care or Terminal Illness Benefit by 5% after the policy has been in place for five years.

Under the TPD Cover Loyalty Bonus Benefit, any TPD Cover benefit which becomes payable will be increased by 5% after the policy has been in place for five years.

Tailoring this cover furtherThe Total Care Plan and Total Care Plan Super ranges allow the policyholder to tailor the Life Care cover further by selecting from the following options:

Accidental Death Cover Option• (TCP only)

Plan Protection Option•

Evidence of Severity Option• (TCP only)

Child Cover Option• (TCP only)

Guaranteed insurabilityTotal Care Plan allows the policyholder to tailor the Life Care cover further and remove the underwriting hassles for you and your client by selecting from the following options:

Guaranteed Insurability Option• (Personal Events)

Guaranteed Insurability Option• (Business Events)

Business Safe Cover Option• (TCP only)

Life, Disability and Trauma Cover

12

Total Care Plan Super options for death benefit paymentsDeath benefits for your clients covered by Total Care Plan Super will be paid according to the benefit payment selection that has been made from the following options:

Non-binding nomination • – requires the Trustee to consider the client’s nomination but is not bound to pay the death benefit in accordance with the nomination. Under a non-binding nomination, the Trustee retains an overriding discretion to pay the death benefit in the way it decides, which could be to your client’s dependant(s) (as defined in the Trust Deed) or legal personal representative or a combination of both. If your client has a non-binding nomination in place and subsequently makes a binding nomination, the binding nomination will automatically supersede the non-binding nomination.

Binding nomination• – requires the trustee to pay the policyholder’s death benefit to the person(s) they nominate. Binding nominations must be updated every three years to remain valid. A Binding Nomination will provide your client with greater certainty than a Non-binding Nomination on the payment of a benefit when they die.

13

Income protection insurance

The Income Care Range offers two levels of personal income protection as well as one specifically tailored to cover business expenses.

CommInsure is currently one of a few companies to offer agreed value and indemnity style policy options on both our basic and advanced income protection products.

Across our Income Care Range we offer a strong set of core benefits with real value options that are designed to cater for our clients’ individual needs.

Benefits designed with understandingCommInsure now offers improved income protection cover to meet the needs of more of your clients. Below, we have summarised where CommInsure’s Income Care Range exceeds similar products in the marketplace.

Income Care Range benefits We will not reduce the monthly benefit if the insured receives •any TPD or Trauma benefit paid under an insurance policy.

A reduction in monthly Partial Disability benefits will only •be made if your client’s monthly income and any other payment exceeds 100% of their pre-disability income.

Rehabilitation benefits Rehabilitation benefits paid by CommInsure are considered to be leading in the industry. We also have internal rehabilitation consultants, showing CommInsure’s commitment to providing real support to helping your clients get back to work.

Agreed valueWhere the agreed value cannot be substantiated at claim time, your clients have the flexibility of providing their highest average income for any twelve month period in the three years prior to disability.

CommInsure is one of only a few companies that pay a partial disability benefit to all occupations classified as professional, super professional, medical and legal without the insured having to be first totally disabled, and one of the only companies to offer true agreed value policies to blue collar occupations. In this way, CommInsure can offer a more comprehensive cover to a wider range of your clients.

Understanding people who take leave or are unemployedWe understand that employment circumstances may change and we will continue to provide policyholders income protection cover if they become involuntarily unemployed or go on maternity, paternity or long service leave, as long as they continue to pay premiums. If the policyholder becomes involuntarily unemployed prior to turning age 65, our Unemployment Premium Waiver, will waive their premiums for up to three months over the duration of the policy.

The Maternity Premium Waiver will waive premiums for up to three months over the duration of the policy if the policy holder goes on maternity leave prior to turning age 65.

Reduction in waiting periodCommInsure now allows the waiting period to be reduced with no further underwriting when a customer reaches the age of 65 and no longer has a group salary continuance policy.

A common strategy is to offer an Income Protection policy with a two year waiting period where the insured also has a group salary continuance policy with a two year benefit period. This ensures the life insured is adequately covered up to age 65.

However when the customers leaves their employer and the group policy ends, they are left with a retail policy with a long waiting period.

CommInsure now has the solution, allowing the waiting period to be reduced with no further underwriting.

Income Care

Provides basiccover where your clients can insure up to 75% of their income and is a low cost alternative to Income Care Plus.

Income Care PlusBusinessOverheads Cover

Helps provide cover for the fixed operating expenses of a business.

Income Care Plan

Provides the basic cover of Income Care, as well as a number of additional benefits designed to help get your clients back to work.

14

Features designed for added support

Guaranteed InsurabilityWith our Guaranteed Insurability feature the policyholder is able to increase their cover by up to 10% without further evidence of health (on top of any increase under the Indexation Benefit), once every three years.

Recurrent disability If the policyholder goes back to work after receiving certain benefits, but needs to claim again for the same sickness or injury, within twelve months of returning to work on a full-time basis the waiting period does not reapply.

Extended cover If at age 65 the policyholder is not receiving any benefits, their Total Disability Cover will continue until age 70.

Medical Professionals Benefit If the policyholder is a medical professional, this benefit provides a lump sum payment if, while performing or assisting in exposure-prone medical procedures, monthly on average or more frequently, they contact HIV (Human Immunodeficiency Virus), Hepatitis B or Hepatitis C, and are prevented from practicing exposure-prone medical procedures.

Loyalty rewardedThe Reward Cover Benefit rewards your client for maintaining their policy with us for three years or more. After their cover has been in place for three years, we will reward the policyholder with $50,000 of Accidental Death Cover at no extra cost. The Accidental Death Cover will then increase by $10,000 on each of the following five policy anniversaries, giving a total of $100,000 Accidental Death Cover after eight years.

We will even double the Reward Cover Benefit for those clients who also have a Total Care Plan or equivalent policy with CommInsure. That is $100,000 of accidental death cover after a policy has been in place for three years, increasing by $20,000 each year for the next five years to a maximum of $200,000.

Shorter waiting periodsIf your client belongs to one of the professional occupation groups and has taken out Income Care Plus, then the conditions of the waiting period for a disability benefit are significantly relaxed.

CommInsure provides one of the widest ranges of benefit and waiting periods, providing your clients with more scope to find the cover that best suits their needs.

Tailoring this cover furtherThe Income Care Range allows the policyholder to tailor the cover and cost further by selecting from the following options:

Total and Permanent Disability (TPD) Cover OptionProvides the life insured with greater choice in the event of total and permanent disablement and helps to maximise tax benefits at the time of claim. With this option the life insured can choose to receive the benefit payment as a tax free lump sum cash payment instead of a monthly benefit that is taxed as income.

Super Continuance OptionThis option allows your client to insure their regular superannuation contributions of up to 15% of their annual income so that their super will continue to accumulate during periods of total and partial disability. This effectively means that your client can insure up to 90% of their income. CommInsure is one of only a few insurers to offer this level of replacement cover.

Cash Back OptionIf your client selects the Cash Back Option, they will stand to receive a refund of up to 20% of premiums paid when the policy ends, provided they have not made a claim on their policy.

Accident Option If your client is totally disabled due to an injury for three days in a row during the waiting period, they will be paid a benefit under the Accident Option, providing support for your clients much earlier in the process.

Premium Saver OptionThe Premium Saver Option provides a 10% premium discount in return for the client accepting certain restrictions on the cover provided.

Increasing Claim OptionIf your client is receiving a claim benefit, this option increases the amount of benefit they receive each year to keep in line with inflation.

Business Overheads CoverBusiness Overheads Cover provides cover for the regular fixed operating expenses incurred in the month. Features include:

the capacity to return to work up to ten hours a week•

a pro rata payment for annual expenses incurred but not •paid in the month of the claim

maximum payments of twelve times the monthly benefit.•

covering the principal amount and interest payments •of a loan.

We offer a discount of 10% on Business Overheads Cover when your client takes out an Income Care or an Income Care Plus policy.

15

Guaranteed annuities

Now more than ever Australia’s ageing population is looking for better, safer and more reliable investment options – especially in the long term.Guaranteed annuities may be a suitable long-term investment for pre-retirees/retirees and investors looking for a guaranteed return which may not be offered by other pension products.

What is an annuity?An annuity is a contract sold by an insurance company to provide a series of payments of a set amount and frequency. It’s a long-term investment for investors looking for a guaranteed return. An annuity provides a low risk way of locking in a set level of income and potential social security benefits in retirement.

Retirees commonly invest their retirement money in annuities and draw down a regular income from annuities for their living expenses during retirement. You can invest both superannuation and non-superannuation money into an annuity.

Guaranteed income payments Unlike an annuity investment, selecting the fixed interest investment option in a market linked allocated pension will not provide a ‘guaranteed’ return.

Accepts both super and non super savings The ability to invest with superannuation savings or personal savings makes guaranteed annuities very flexible. Market linked pension products are not as flexible as they do not accept investments from personal savings.

No ongoing management feesThere are no ongoing management fees with CommInsure’s guaranteed annuities. The regular payments in the quote take into account any amount paid as commission and the fees and costs associated with administering the investment.

Which guaranteed annuities does CommInsure offer?CommInsure offers an extensive range of award-winning guaranteed immediate annuities which include:

Lifestream Guaranteed Income range – secure investments •with guaranteed return.

Guaranteed Index Tracked Annuity range – secure •investments which provide some exposure to the upside of the stock market, without the downside risk.

Personal savings Superannuation money(ordinary funds) (tax free for retirees over 60)

Personal savings Superannuation money(ordinary funds) (tax free for retirees over 60)

16

Investment Growth Bonds – a flexible tax-effective investmentThe Investment Growth Bond (the Bond) combines the benefits of a managed fund with the security and tax benefits of a life insurance policy.

The Investment Growth Bond is an insurance bond that provides you with a range of investment options, in a simple tax-effective package. You can also take advantage of estate planning features such as the ability to nominate beneficiaries or use the Bond as a savings vehicle for a child’s education by setting up a child advancement policy.

The Bond is simple because investment earnings do not have to be declared in a tax return unless a withdrawal is made within the first ten years. Investors are free to switch (without personal tax consequences) between a range of investment options, tailored to suit various risk profiles.

What are the tax advantages of the Bond?The Bond is considered tax effective because investors on a marginal tax rate greater than 30% may pay less tax on investment earnings that they would if they were invested in a managed fund. Tax advantages include:

the value of the Bond is not subject to capital gains tax•

you do not need to include any earnings from the Bond in •your tax return unless you make a withdrawal within ten years. Withdrawals are also free of personal income tax in the event of special circumstances such as death, disability, illness and financial hardship

earnings from the Bond’s investments are taxed at a •maximum of 30%

if you withdraw, you may be able to take advantage of the •30% tax offset which may also be used to reduce your tax on income received from other sources

switching between investment options while holding the •Bond has no personal capital gains tax consequences.

Investment optionsWe offer seven investment options tailored to suit individual risk profiles. You are free to switch between the investment options as often as you like. You can also diversify your investment by investing in multiple options. More information on investment options can be found in the Product Disclosure Statement (PDS).

Who should invest?Investment Growth Bond has been designed for investors:

seeking a simple, tax effective, longer term investment•

in higher marginal tax brackets•

looking to minimise taxable income•

seeking a longer term investment for children (who usually •pay penalty tax rates on investment income)

with incomes near thresholds where Government benefits •cut out or higher taxes cut in

interested in utilising the estate planning and wealth transfer •(you can nominate a beneficiary to receive the proceeds on death with no tax payable).

GuaranteesAs the Investment Growth Bond is a life policy issued by CMLA, we can offer guarantees such as:

a death benefit that will pay at least what the investor has •contributed into the Bond (less any withdrawals made)

a Capital Guaranteed Cash option where we guarantee the •unit price will never fall

unit price guarantees in the Stable and Fixed Interest •options, subject to conditions.

Who can invest and what is the minimum amount?If you’re over 16 and under 90 you can invest as little as $1,000 in the Investment Growth Bond. Children between the ages of ten and 16 may invest with parental consent. Alternatively, you may invest on behalf of a child under 16 and transfer the ownership of the Bond to the child when they reach an age nominated by you (any time between the ages of 10 and 25). This is known as a child advancement policy.

Investment Growth Bond

Underwriting

Underwriting strengthCommInsure’s underwriting team are dedicated to making informed decisions quickly. Our team consists of:

one Chief Underwriter•

two Technical Underwriting Managers•

nine mobile underwriters with over 120 years •of experience

30 senior underwriters and managers with an average •of 16 years of experience each

13 intermediate underwriters with a total of over •100+ years of experience

three junior underwriters with a total of •six years’ experience

one Forensic Accountant•

one Chief Medical Officer (for underwriting)•

one Chief Medical Officer (for claims).•

Among our experienced team we have eight ex-chief underwriters from different companies. We have the best financial underwriting limits in the market.

Authority levels:

$6 million for Life•

$2.5 million for TPD•

$1.5 million for Trauma•

$15,000 per month for Income Protection.•

CommInsure currently underwrites approximately 50,000 cases each year.

Approachable underwritersOur experienced underwriters pride themselves on being approachable and helpful. They recognise the importance of developing a good relationship with advisers and the mutual benefits created. Our underwriting team is firmly committed to providing financial advisers with a consistently high level of service.

Turnaround timesBecause CommInsure uses a low level of reinsurance, our underwriters are able to achieve faster turnaround times.

The average turnaround time for a cleanskin policy is four working days (96 hours).

Reviewing applicationsWe do everything that we can to offer insurance including:

premium loadings•

limited duration contracts•

exclusion clauses.•

State-based underwriting supportUnderwriting support is also provided on a state level, ensuring advisers receive a greater level of support and assistance.

Mobile underwritersCommInsure offers a Mobile Underwriting Service. For details on this service, contact your state based Business Development Manager.

17

1 As at 1 January 2007.

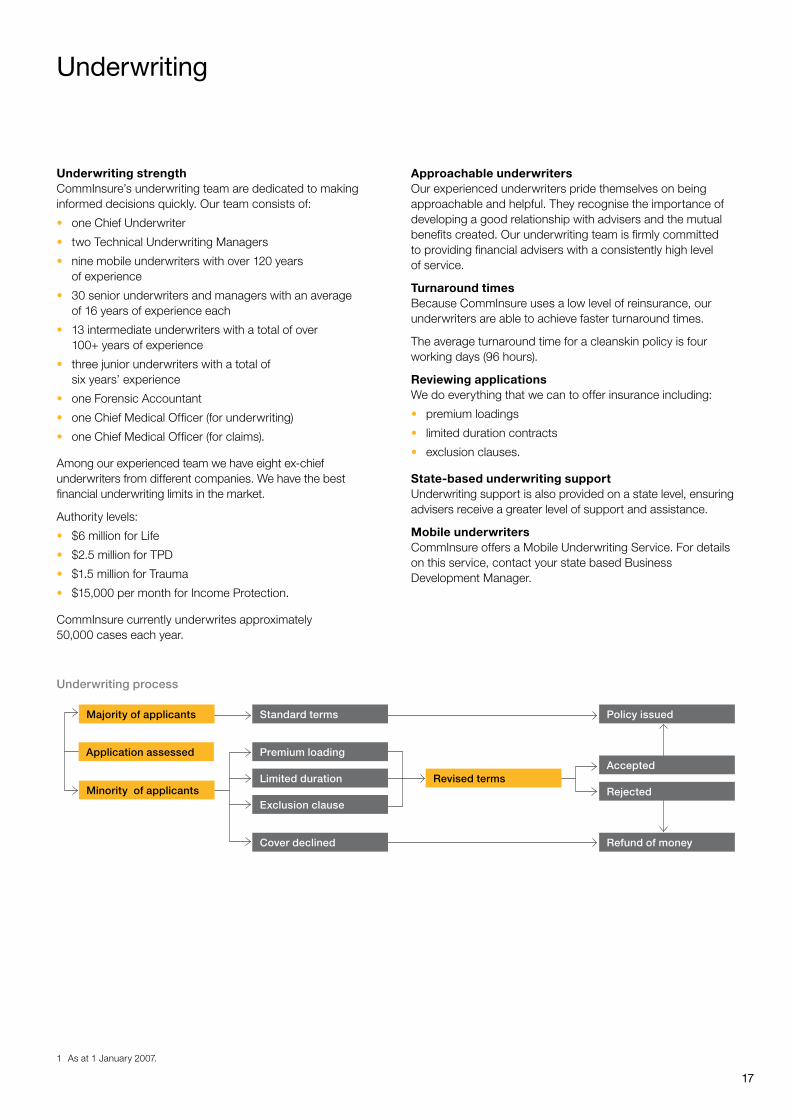

Underwriting process

Majority of applicants

Minority of applicants

Policy issued

Accepted

Rejected

Refund of money

Standard terms

Premium loading

Limited duration

Cover declined

Exclusion clause

Revised terms

Application assessed

Underwriting

Underwriting the applicationAfter you have identified the need for risk insurance with your client and sent us a completed application, we immediately commence underwriting.

Of all applications received, around 90% are accepted by both the clients and us. The majority of these applications are accepted at standard premium rates.

Underwriting HotlineOur Underwriting Hotline facility offers you access to pre-assessment underwriting seven days a week. Whether you have a general pre-assessment question or want to discuss a complicated insurance plan, call us on 1800 257 328. Underwriters are available Monday to Friday from 8.30 am to 10 pm (Sydney time), Saturday from 9 am to 2 pm, and Sunday from 10 am to 2pm.

18

Short form underwritingWe have made applying for insurance easier for you and your clients by speeding up the underwriting process with our new Short Personal Statement. The Short Personal Statement can be completed when you are applying for cover up to $1 million each for Life, TPD and Trauma and $6,000 per month for Income Protection.

You can download the Short Personal Statement on the Adviser web site https://adviser.comminsure.com.au.

Claims

Claims strengthOur claims assessment team is one of the largest in the country and includes:

40 case managers with an average of eight years experience•

six managers with an average claims experience •of six years

two rehabilitation specialists• 1.

We employ people with backgrounds in rehabilitation, nursing, commerce, law, economics, medicine, medical science, health science and psychology.

Our claims team also includes a full-time Doctor (Chief Medical Officer, psychiatrist) and Forensic Accountant. These professionals liaise with our case managers, assisting them to make informed decisions.

Claims philosophyOur claims philosophy is simple. We pay all genuine claims as soon as possible after all the necessary documentation has been received and assessed. And because of CommInsure’s low level of reinsurance, our claims are processed faster.

We pay special attention to our customers when managing their claims.

Where appropriate, each claim is allocated to a case manager, who looks after the client throughout the claim process.

Our target case loads for assessment ensure that each case manager is responsible for only a medium size portfolio of claims, so they are able to maintain a very high standard of service.

We maintain regular contact with each claimant, either by telephone or personally through our representatives. This allows us to better understand their circumstances and needs and enhances the partnership approach in managing claims.

For income protection claims, we actively work with your clients and yourself as well as their doctors and specialists to assist their recovery and return to work.

Our claims professionals are experienced, skilled personnel. They receive ongoing training to continually grow their expertise within the life insurance industry.

Claims management principlesOur commitment to our clients means we strive to adhere to the following principles for all claims:

1. Understand that this is a time of great distress and have genuine empathy with our clients.

2. Maintain high quality and accurate communications (written and verbal).

3. Keep our clients and their advisers updated on the status of the claim.

4. Follow up all outstanding requirements promptly.

5. Maintain confidentiality of all claim information and documentation by identifying callers and obtaining authorisation before releasing information to any person or organisation.

6. Make decisions subject to policy terms and conditions, procedures and guidelines in order to maintain consistency across all claims.

Claims experienceIn the 2006 calendar year, CommInsure (Retail):

accepted 92.5% of income protection claims •

helped 1,200 families cope with the loss of a loved one, •paying a total amount of $63 million

paid 937 people a total of $37.7 million, during a sickness •and injury

assisted 1,500 income protection customers with •$45 million via regular payments.

Product Claims paid percentage

Life Care (term) 99%

TPD and Trauma Cover 85%

Income protection 92.5%

19

1 As at 1 January 2006.

Superior service standards

New business turnaround timesThe average number of days to process a ‘cleanskin’ policy is four days.

The average number of working days that CommInsure takes to process a less straightforward policy is:

Life Care 30 days•

Trauma Cover 30 days, and•

Income Care Range 30 days.•

Contact centre service initiativesCommInsure has 65 staff in our personal risk insurance contact centre – their goal is to deliver outstanding service and support when dealing with both adviser and client enquiries.

CommInsure has introduced a number of service initiatives to help improve our service levels for both our advisers and customers. These include:

1. the reduction of telephone numbers used to contact CommInsure

2. the replacement of our interactive voice response (IVR) unit with real people to give CommInsure a human touch, and

3. restructuring the contact centre into teams of specialists to ensure that your query is resolved by ‘the right person the first time’.

We constantly exceed our contact centre’s standard of 80% of clients’ calls being answered in 20 seconds and we will continue to improve on this outstanding level of service.

Our contact centre operates between 8 am and 8 pm (Sydney time), Monday to Friday, for existing policy enquiries and from 8 am to 6 pm, Monday to Friday, for new business enquiries.

Customer enquiries • 13 10 56

Adviser enquiries • 1800 671 040

ComplianceAt CommInsure, we consider strict compliance standards to be a competitive advantage. By having a strong compliance culture throughout CommInsure and by setting our compliance standards at such a high level, we are able to fulfil our obligations to best practice.

ComplaintsCommInsure is a market leader in customer care, which is demonstrated by our complaints handling procedures. All complaints are acknowledged within 24 hours of receipt and CommInsure aims to handle 90% of complaints within four days.

20

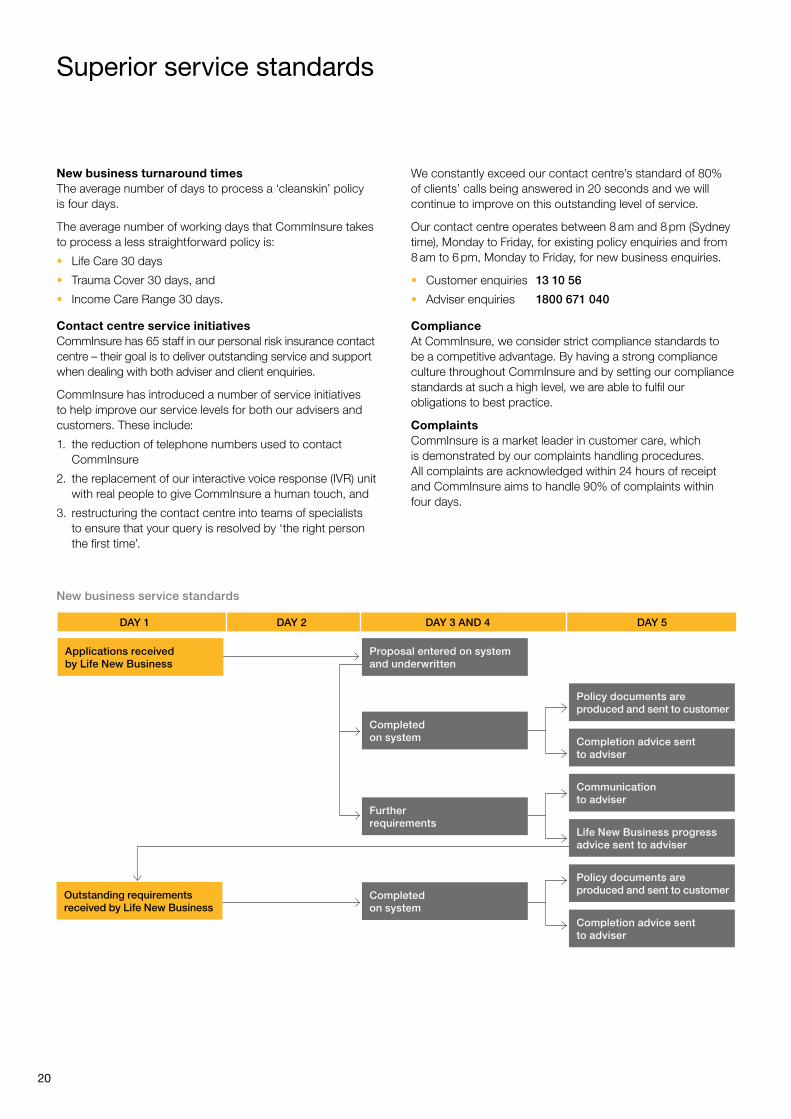

New business service standards

Policy documents are produced and sent to customer

Completion advice sent to adviser

Communication to adviser

Policy documents are produced and sent to customer

Life New Business progress advice sent to adviser

Completion advice sent to adviser

Completed on system

Completed on system

Further requirements

DAY 1 DAY 2 DAY 3 AND 4 DAY 5

Outstanding requirements received by Life New Business

Proposal entered on system and underwritten

Applications received by Life New Business

Sales and marketing support

Sales As Australia’s largest life insurer, CommInsure understands the importance of partnering with advisers to provide straight forward Insurance solutions for Australian families. Our state offices provide dedicated insurance business development support and state-based mobile underwriting services to assist with even the most complex cases.

We also understand the need to support the Dealer Groups through our National Sales Team comprising National Account Managers and the Dealer Group support team. They are in turn supported by Australia’s premier Insurance technical team, Business Growth Services.

Risk Sales Academy The CommInsure Risk Sales Academy was formed to develop and deliver training programs which specifically focus on improving the communication and selling skills of advisers.

The Academy program, now available, has been designed for advisers who have experience in advising clients and who require a learning program which will accelerate their selling ability and translate into increased sales.

Concentrating on the use of empathy and simple yet effective means of communicating insurance solutions to prospects, the program is solidly backed up by the expert input and opinion of some of Australia’s leading risk insurance advisers.

By sharing two very productive days you will learn techniques to improve your communication and selling skills and get practical tools you can use in your business to help you to:

more intimately understand what is important to •your clients.

increase your success rate at sales and advice interviews.•

measure and analyse sales ratios to improve •your productivity.

Contact your CommInsure Business Development Manager for upcoming courses.

Business Growth ServicesOur Business Growth Services team supports our distribution channel by deepening relationships with key business partners. They are focused on providing support, tools, and product and market information to advisers regarding insurance (personal risk, general insurance and group risk), annuities and Investment Growth Bonds.

Business Growth Services consists of industry experts, focused on business growth and improving productivity within CommInsure to benefit you – our business partners.

Technical Service Hotline CommInsure’s new Technical Service Hotline will allow you to discuss general or client specific queries on insurance and annuities products, legislation, and taxation.

You can contact CommInsure’s Business Growth Services through the Technical Service Hotline from Monday to Friday between 8.30 am and 5.30 pm (Sydney time) on 1800 761 067 or by email on [email protected].

MarketingCommInsure is taking a bolder approach to marketing with the aim to increase awareness of the need for life insurance and income protection. We know our customers circumstances are all different and that one size doesn’t fit all. Our solutions are, therefore, targeted to the goals and objectives common to people in different stages of their lives. The product messaging is broken into these segments to ensure we tailor our offerings to these distinct needs.

Below is just a taste of the campaigns that we have been running throughout the year.

21

Important information. *Customer Experience Survey, November 2006. CommInsure is a registered business name of The Colonial Mutual Life Assurance Society Limited ABN 12 004 021 809, AFSL 235035 (CMLA). CBATLI0063_H_MM

When you recommend CommInsure Life Insurance and Income Protection products, you know it won’t be a slip-up. Because you can count on our market-leading claims team to handle your clients with care. 92% of our customers surveyed were satisfied with how we managed their enquiries*. We also have a proven record of paying claims and solving any problems quickly. So if you’d like to offer your clients better protection, talk to your Business Development Manager, call 1800 671 040 or visit https://adviser.comminsure.com.au

It’s no accident we have 92% customer satisfaction.

CBATLI0063_H_MM_325x228.indd 1 10/10/07 5:15:04 PM

Sales and marketing support

Sales toolsWe are constantly looking for new opportunities to build on our wide range of marketing and support materials, that help to aid you in explaining the benefits of our products to your clients.

Ongoing communication and supportCommInsure produces a number of printed and electronic newsletters to help provide you with additional value and support.

22

Our Personal Insurance Portfolio Product Disclosure Statement provides information on Income Care, Income Care Plus, Business Overheads Cover and Total Care Plan.

Our Update magazine is produced quarterly and provides you with information on industry issues, latest market developments, in-depth articles on products, CommInsure developments, statistics and marketing and sales initiatives.

To order these comprehensive guides, please visit the sales material section at adviser.comminsure.com.au.

Our Guide to business insurance provides you with an overview of the core business insurance concepts. It goes into great depth on business insurance strategies for small-and medium-sized businesses.

Our Newsflash e-newsletter helps us to communicate important product information when required.

Our Guaranteed Annuities Product Disclosure Statement provides you with an overview of guaranteed annuity investments and how they can help provide a secure income for your clients.

Our Did you know? technical updates are produced on a weekly basis and provide you with information on regulatory changes, statistical information and product and strategy updates.

How to contact us

Adviser Assist 1800 671 040For all general enquiries (including new business, quotes and suspense management) please call our Adviser Assist line. Your call will be answered by a real person who will be able to direct you to the right person to help you with your enquiry the first time.

Underwriting Hotline 1800 257 328Our Underwriting Hotline facility is our pre-assessment underwriting hotline. It offers you access to underwriting information, 7 days a week. Whether you have a general pre assessment question or want to discuss a complicated insurance plan, call us on 1800 257 328. Underwriters are available Monday to Friday from 8.30 am to 10 pm (Sydney time), Saturday from 9 am to 2 pm, and Sunday from 10 am to 2pm.

Adviser Technical Help Desk 1800 240 405This team can assist you by providing technical support to help you with any of our risk insurance product systems, including Life400 and CALQ.

Adviser web siteThe adviser site is located at https://adviser.comminsure.com.au.

It allows you to:

access Life400 to view your clients’ policy details online •and track workflow

access technical information and further product details•

view, download and order CommInsure’s brochures •and forms

download software updates, and•

access the latest CommInsure news.•

Customer Assist 13 10 56Your clients may contact the Customer Service Centre directly on 13 10 56, from 8am to 8pm (Sydney time), Monday to Friday.

CommInsure web site The CommInsure web site is located at comminsure.com.au and provides customers with further information on CommInsure products and services.

Technical Service Hotline CommInsure’s new Technical Service Hotline will allow you to discuss general or client specific queries on insurance and annuities products, legislation, and taxation.

You can contact CommInsure’s Technical Service Hotline from Monday to Friday between 8.30 am and 5.30 pm (Sydney time) on 1800 761 067 or by email on [email protected].

Adviser Sales CentreYou can contact our Business Development Consultants who are trained to service advisers on 02 9303 3545, 02 9303 2491 or 02 9303 2490.

23

Sales teamsNSW sales teamLevel 23, 52 Martin Place Sydney NSW 2000

Phone 02 9303 7254 Fax 02 9303 7250

VIC/TAS sales teamLevel 1, 385 Bourke Street Melbourne VIC 3000

Phone 1800 248 819 Fax 03 8628 5655

SA sales teamLevel 4, 100 King William Street Adelaide SA 5000

Phone 08 8418 5747 Fax 08 8418 5741

QLD sales teamLevel 5, 240 Queen Street Brisbane QLD 4000

Phone 07 3328 5877 Fax 07 3328 5858

WA sales teamLevel 4, 55 St Georges Terrace Perth WA 6000

Phone 08 9218 5347 Fax 08 9218 5370

CommInsure product offerings

Life Risk insurancePersonal Insurance Portfolio

Life Care•

Total and Permanent Disability Cover•

Trauma Cover•

Income Care Plus•

Income Care•

Business Overheads Cover•

Total Care Plan SuperLife Care•

Total and Permanent Disability Cover•

Wholesale RiskGroup Life Insurance •– superannuation or non-superannuation

Group Total and Permanent Disablement Cover •– superannuation or non-superannuation

Group Income Protection •– superannuation or non-superannuation

Group Income Protection Plus •– non-superannuation

Investment rangeGuaranteed AnnuitiesLifestream Guaranteed Income – secure investment with a guaranteed return.

Short Term Income (up to five years)•

Long Term Income (six to 30 years or lifetime)•

Lifetime Income (income for as long as you live)•

Guaranteed Index Tracked Annuity – secure investment with some exposure to the upside of the stock market.

Short Term Income (two to five years)•

Long Term Income (six to 25 years)•

Lifetime Income (income for as long as you live)•

Investment Growth BondsCombines benefits of a managed fund with the security •and tax benefits of a life insurance policy.

An insurance bond that provides a range of investment •options, in a simple tax-effective investment.

General insuranceHome Insurance

Residential Home Package•

Investment Home Package•

Motor InsuranceComprehensive•

Third Party Property Damage•

Third Party Property Damage, Fire and Theft•

Travel InsuranceWorldwide Travel•

Economy Travel•

Domestic Travel•

24

Write to: CommInsure Life Insurance, PO Box 320, Silverwater NSW 2128.

13 10 56Customer8 am–8 pm (Sydney time)Monday to Fridaycomminsure.com.au

1800 671 040Adviser8 am–8 pm (Sydney time)Monday to Fridayhttp://adviser.comminsure.com.au

CIL

188

231

107