Practitioner + Assessor. (+ Trainee NABERS NZ assessor) PMAG member

Upload

preston-skinnerCategory

view

213download

0

Welcome

Tax Agent/Attorney MeetingFebruary 26, 2015

ASSESSORPaul D.

Petersen

Paul Petersen – Assessor

oElected November 04, 2014

oStarted in Office January 2006

oPracticing Adoption Attorney

oASU JD and Undergraduate

oDOR Certified Appraiser

ASSESSORPaul D.

Petersen

Introductions

IntroductionsArmando Chavez – Supervisor

o Permits o Appeals o Splits

Ray Bell – Managero Land o Agriculturalo Business Personal Property

Michael Jabri – Managero Residentialo Mobile Homes

Heather Drake – Managero Commercial

ASSESSORPaul D.

Petersen

Tim Boncoskey – Chief Deputy Assessor

David Boisvert – Chief Appraiser

Eric Bails – Chief Technology Officer

Lisa Bowey – Litigation Director

Tom Rief – Ownership\Mapping Manager

Lesley Kratz – Executive Advisor\Special Dis’t\LCV

Marci Williams – Internal\Personal Property Audit Manager

Allen Zingg – Human Resource Manager

Justin Frank– Finance Manager

Robert Pizorno – Communications\Legislative Director

ASSESSORPaul D.

Petersen

Assessor’s Leadership Team

o April 21, 2015 – Appeal Filing Deadline o June 15, 2015 – Incomplete Petitions

must be filed directly to SBOEo July 31, 2015– Internal deadline to have

completed all meetingso August 14, 2015– Deadline for the

Assessor to mail decisions on the appeals

ASSESSORPaul D.

Petersen

Deadline Dates

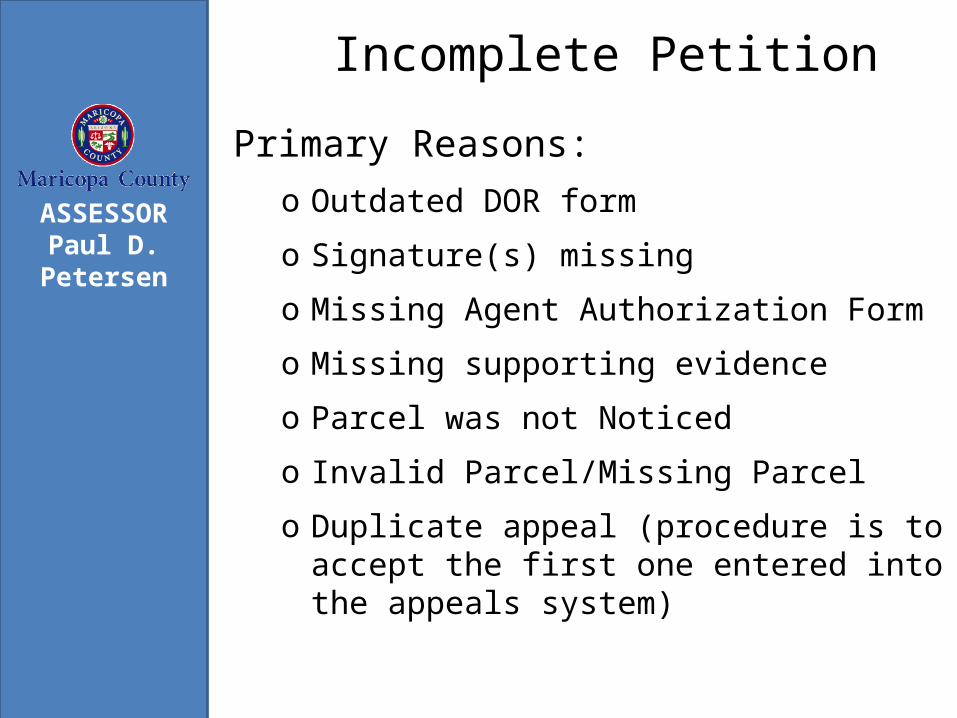

Primary Reasons:o Outdated DOR form

o Signature(s) missing

o Missing Agent Authorization Form

o Missing supporting evidence

o Parcel was not Noticed

o Invalid Parcel/Missing Parcel

o Duplicate appeal (procedure is to accept the first one entered into the appeals system)

ASSESSORPaul D.

Petersen

Incomplete Petition

Petition for Assessor Review ARS 42-16051

“An owner of property that in the owner’s opinion has been valued too high may file a petition with the Assessor”

o Petition shall state:o Owner’s opinion of valueo Basis of valuation approach:

o Market – must include one (1) comparable property in the same geographic area as the subject

o Cost – must include cost to build plus land value

o Income – must include income and expense data relating to the property

ASSESSORPaul D.

Petersen

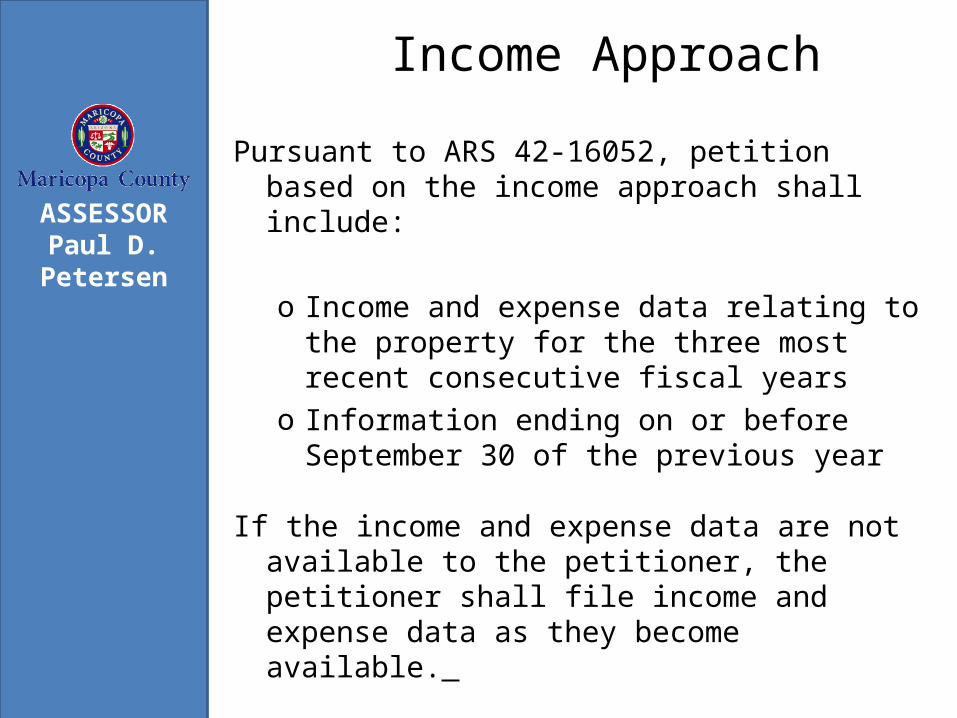

Pursuant to ARS 42-16052, petition based on the income approach shall include:

o Income and expense data relating to the property for the three most recent consecutive fiscal years

o Information ending on or before September 30 of the previous year

If the income and expense data are not available to the petitioner, the petitioner shall file income and expense data as they become available.

ASSESSORPaul D.

Petersen

Income Approach

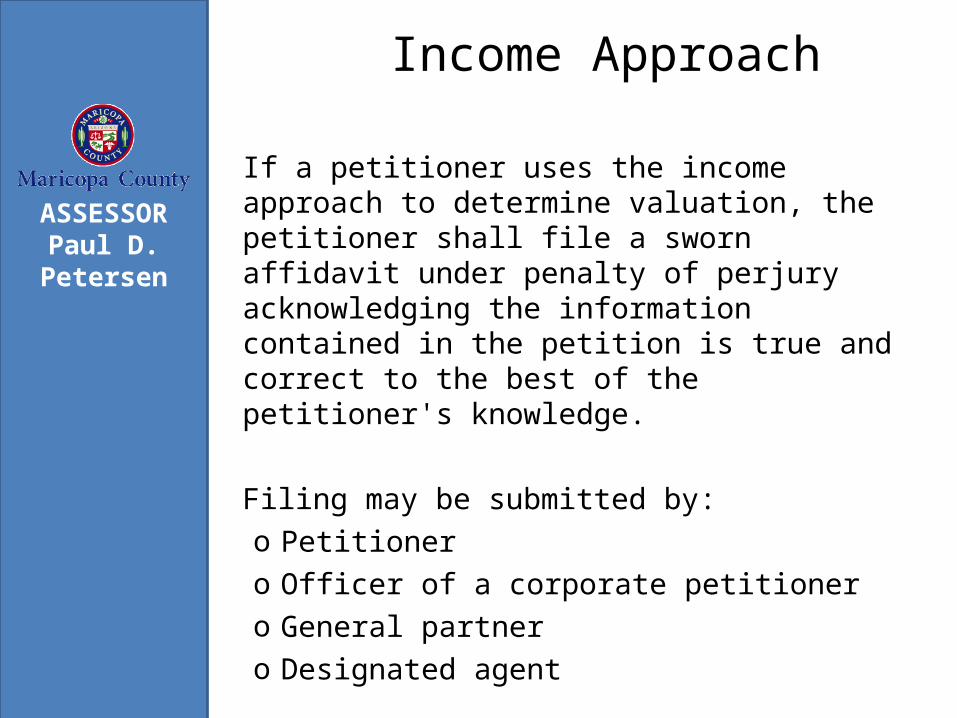

If a petitioner uses the income approach to determine valuation, the petitioner shall file a sworn affidavit under penalty of perjury acknowledging the information contained in the petition is true and correct to the best of the petitioner's knowledge.

Filing may be submitted by:o Petitionero Officer of a corporate petitionero General partner o Designated agent

ASSESSORPaul D.

Petersen

Income Approach

The petition may include more than one parcel of property if:

o Part of the same economic unit according to department guidelines

o Owned by the same ownero Have the same useo Appealed on the same basiso Located in the same geographic

area o Submitted on a form prescribed by

the Department

ASSESSORPaul D.

Petersen

Multiple Parcel Appeals

Different types of property must be filed

separately:

oResidentialoCommercialo LandoAgriculturalo Exemptions

ASSESSORPaul D.

Petersen

Multiple Parcel Appeals

Depot Building (501 W Jackson):o Residentialo Exemptiono Mobile Home

Administration Building (301 W Jefferson, Suite A210)o Commercialo Agricultural/Land

ASSESSORPaul D.

Petersen

Meeting Room Assignments

• The duties of the Assessor’s office have not changed.

• The focus will be on canvassing the county to clean property component characteristics.

• The 2016 assessment ratios changed.– Class 2 is at 15%– Class 1 is at 18%

ASSESSORPaul D.

Petersen

Conclusion

Paul Petersen, Assessor• [email protected]• 602-506-3877

David “Beau” Boisvert, Chief Appraiser• [email protected]• 602-372-1629

Frankie Woodard, Appeals Coordinator• [email protected]• 602-506-3080

ASSESSORPaul D.

Petersen

Contacts

Questions

• Questions asked and emailed will be available on the website:

mcassessor.maricopa.gov/category/news

ASSESSORPaul D.

Petersen

ASSESSORPaul D.

PetersenMaricopa County Assessor’s Office

Tax Year 2016 Valuation Overview

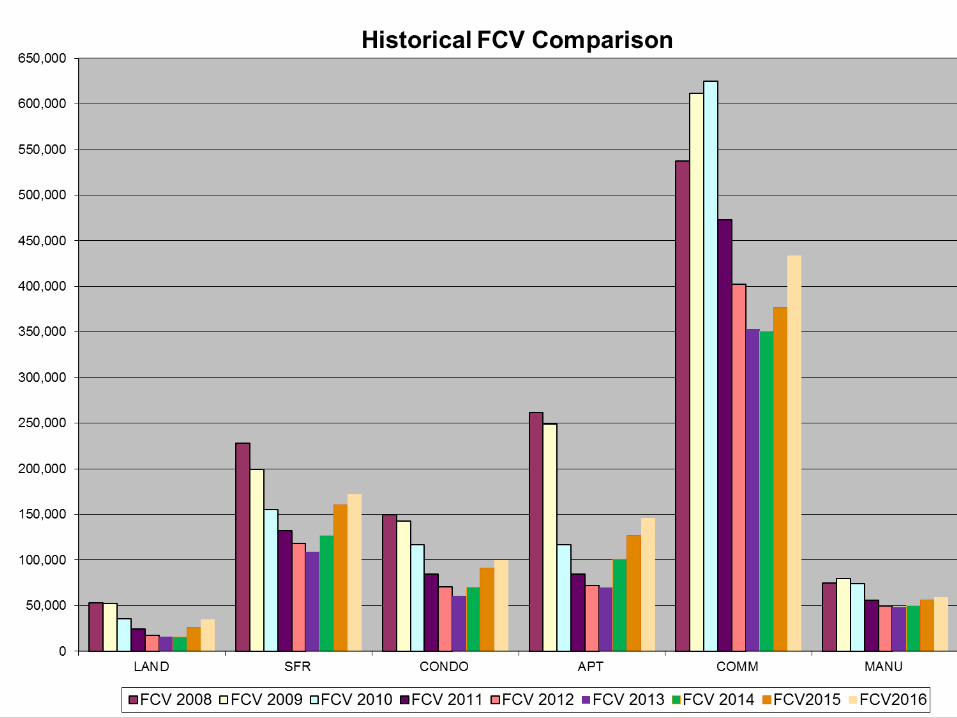

Maricopa County Property Types

17

ASSESSORPaul D.

Petersen

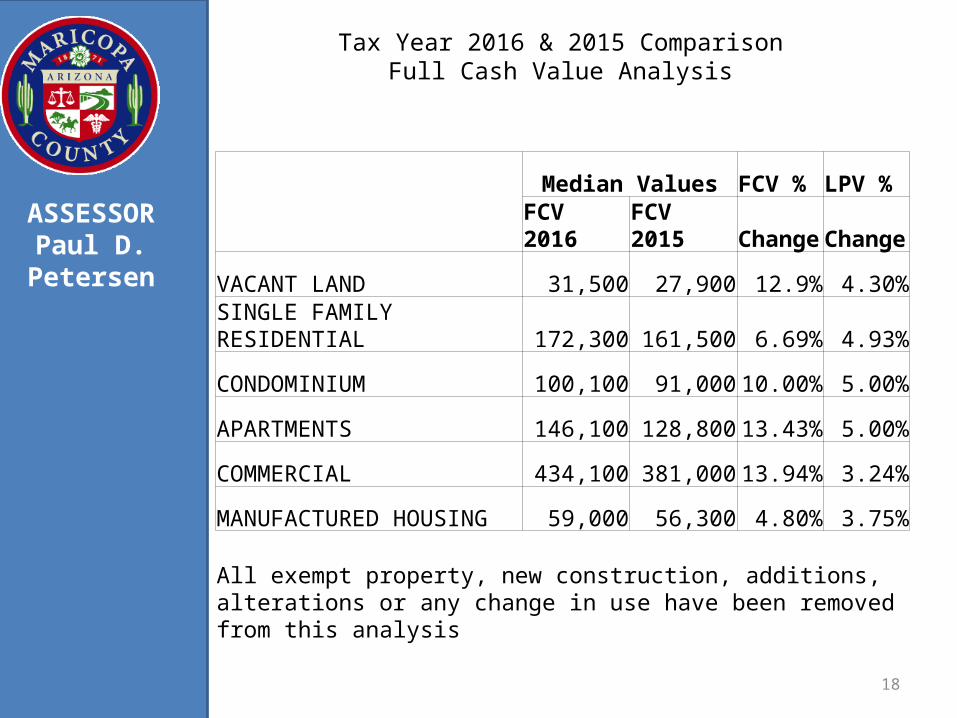

18

ASSESSORPaul D.

Petersen

Median Values FCV % LPV %

FCV 2016 FCV 2015 Change Change

VACANT LAND 31,500 27,900 12.9% 4.30%

SINGLE FAMILY RESIDENTIAL 172,300 161,500 6.69% 4.93%

CONDOMINIUM 100,100 91,000 10.00% 5.00%

APARTMENTS 146,100 128,800 13.43% 5.00%

COMMERCIAL 434,100 381,000 13.94% 3.24%

MANUFACTURED HOUSING 59,000 56,300 4.80% 3.75%

All exempt property, new construction, additions, alterations or any change in use have been removed from this analysis

Tax Year 2016 & 2015 ComparisonFull Cash Value Analysis

20

Vacant Land

21

Vacant Land

3% of the 2013 Sales are REO

22

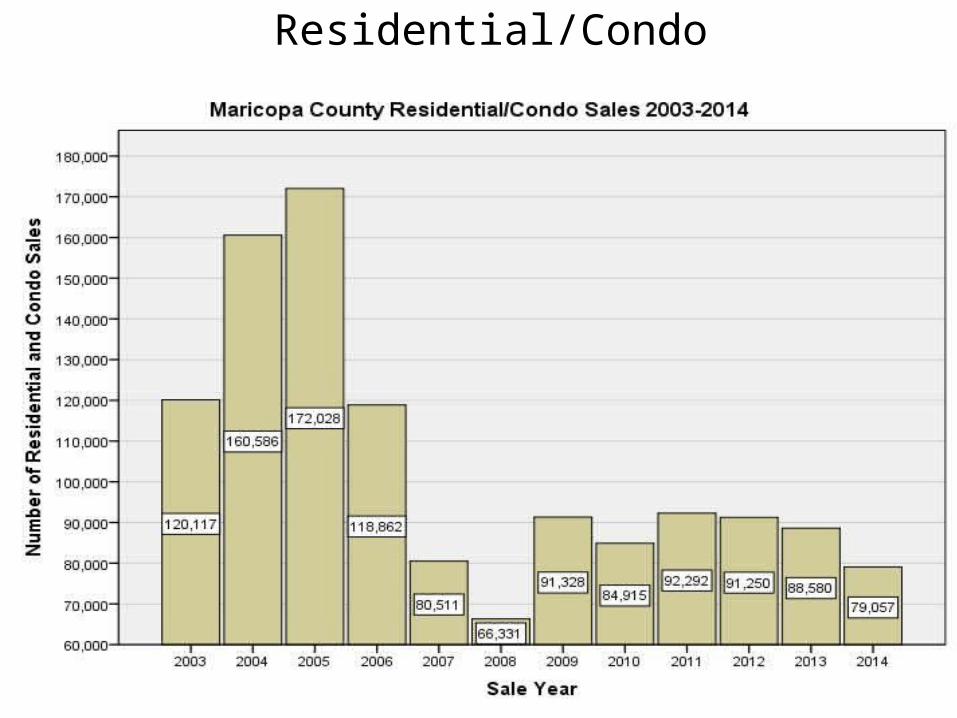

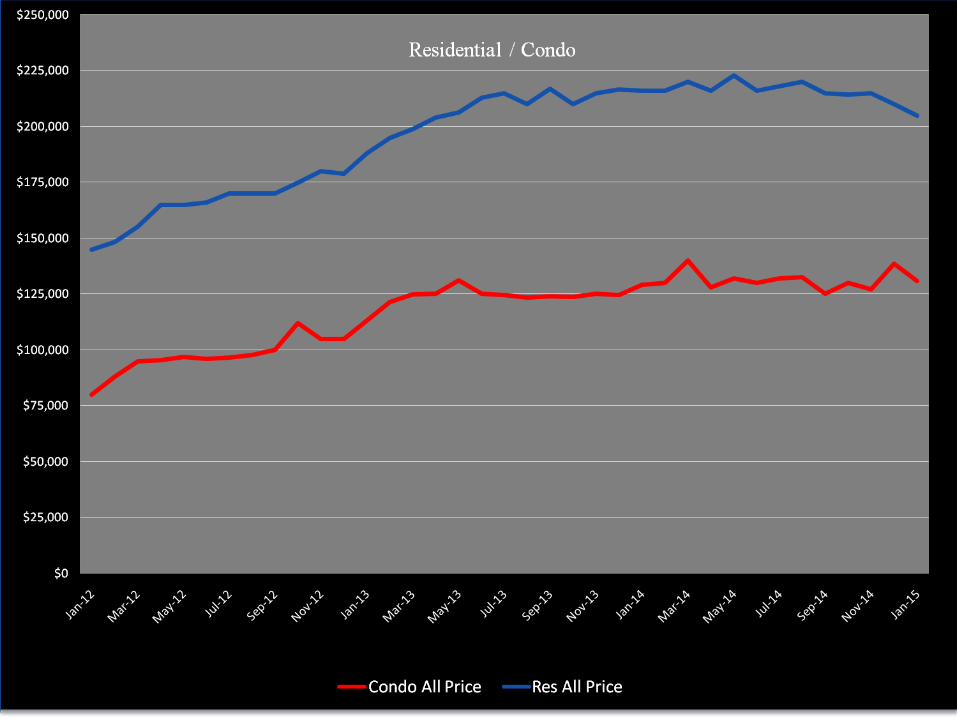

Residential/Condo

23

Residential/Condo

24

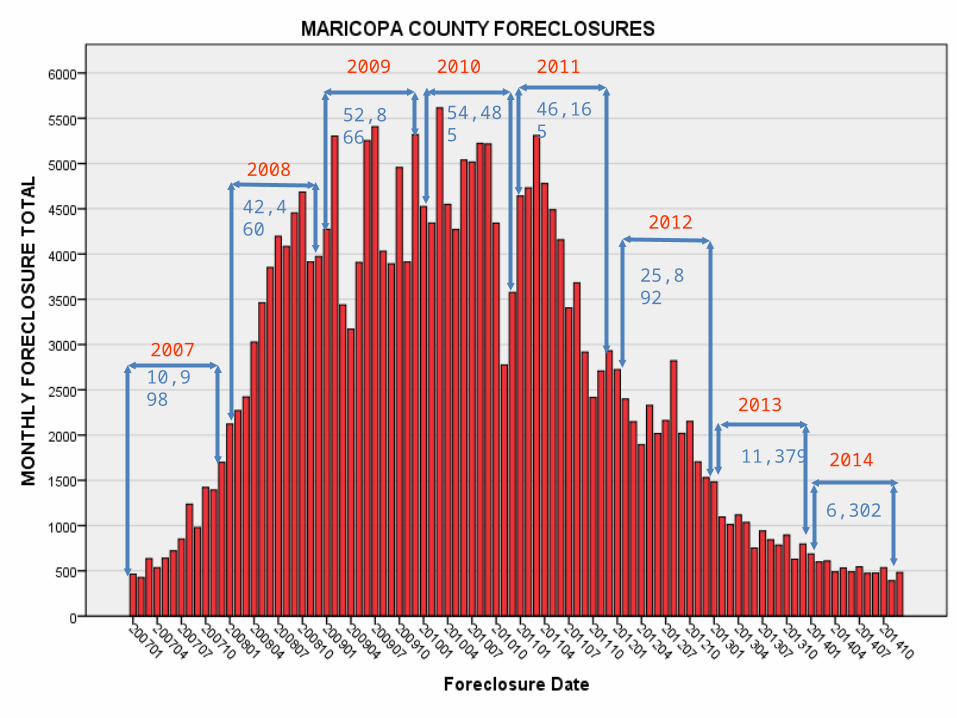

42,460

52,866

42,460

25,892

11,379

10,998

42,460

52,866 54,485 46,165

25,892

11,379

6,302

2007

2008

2009 2010 2011

2012

2013

2014

25

Residential/Condo

97.2% 2.8%

63.5% 36.5%

49.6% 50.4%

60.4% 39.6%

60.9% 39.1%

86.7% 13.3%

95.4% 4.6%

96.4% 3.6%

SYEAR2007

2008

2009

2010

2011

2012

2013

2014

No Yes

Reo

26

27

Commercial

28

Commercial

29

Commercial

9% of the 2009 Sales are REO

ASSESSORPaul D.

Petersen

Commercial % change by type

31

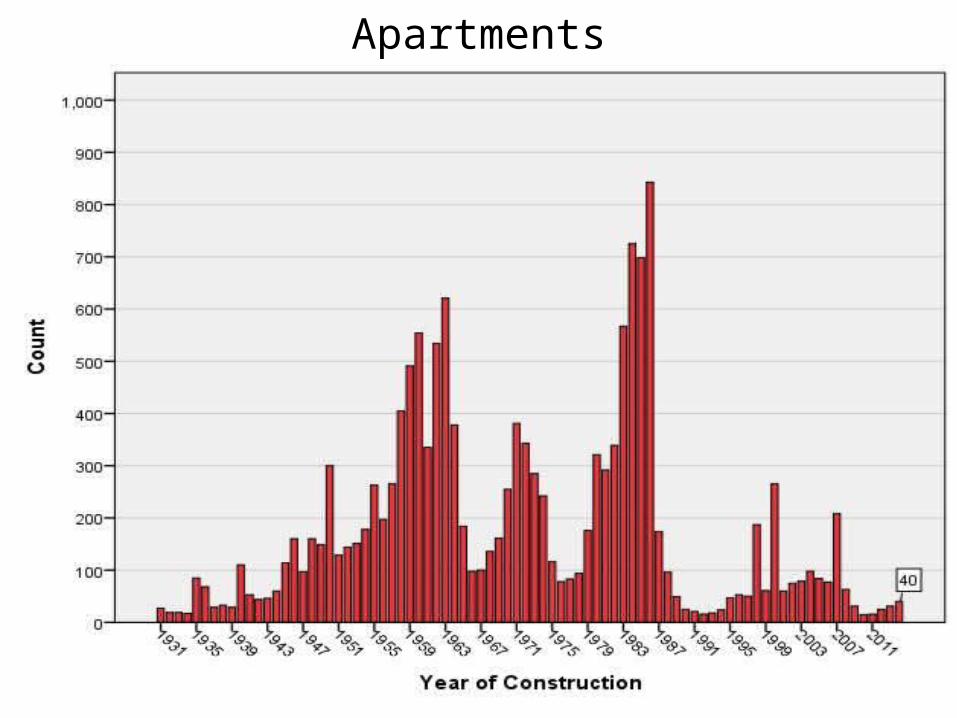

Apartments

32

Apartments

33

Apartments

34

Apartments

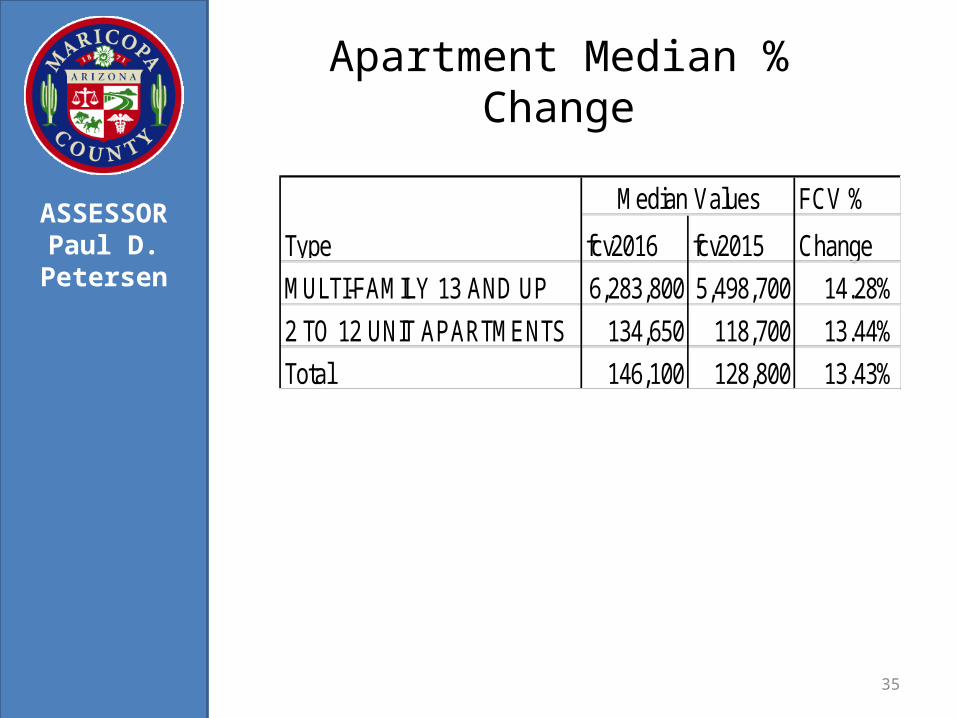

Apartment Median % Change

35

ASSESSORPaul D.

Petersen

FCV %

fcv2016 fcv2015 Change

MULTI-FAMILY 13 AND UP 6,283,800 5,498,700 14.28%

2 TO 12 UNIT APARTMENTS 134,650 118,700 13.44%

Total 146,100 128,800 13.43%

Median Values

Type

CAMA Model Overview

36

All remaining property types are valued using the Cost Approach.

ASSESSORPaul D.

Petersen

PROPERTY TYPE MODEL TYPE

Residential Market

Condo Market

Vacant Land Market

2-12 Unit Apartments Market

13 + Unit Apartments Income

Hotels/Resorts > 200 Rooms Income

Commercial Condo Market

Warehouse/Industrial Market

Offices < 22,000 SF Market

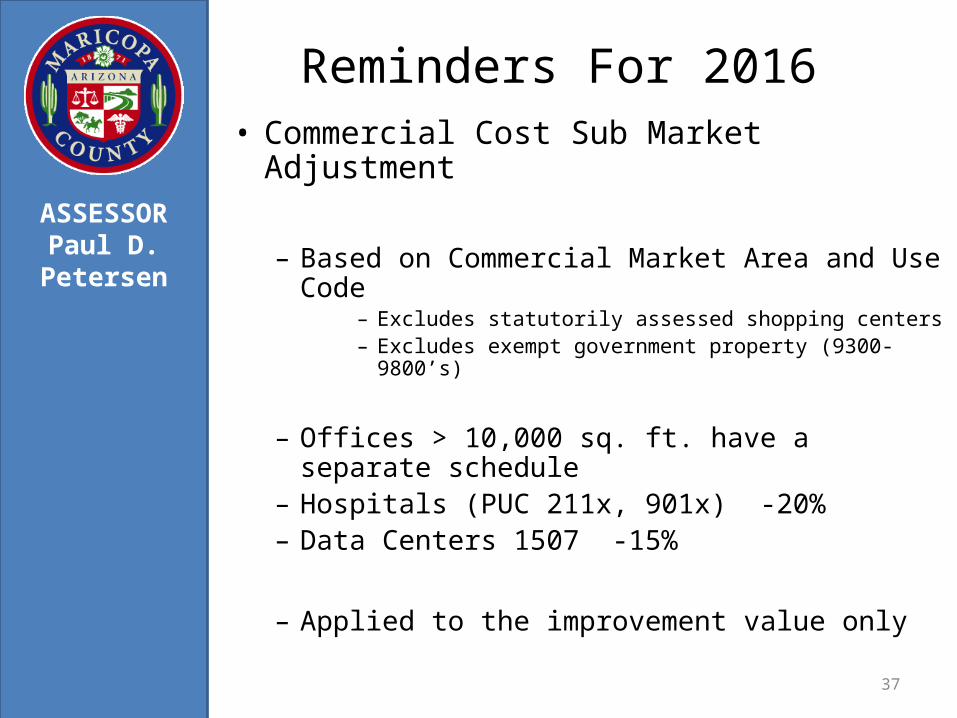

Reminders For 2016• Commercial Cost Sub Market Adjustment

– Based on Commercial Market Area and Use Code

– Excludes statutorily assessed shopping centers– Excludes exempt government property (9300-9800’s)

– Offices > 10,000 sq. ft. have a separate schedule– Hospitals (PUC 211x, 901x) -20%– Data Centers 1507 -15%

– Applied to the improvement value only

37

ASSESSORPaul D.

Petersen

2016 Sub Market Adjustments

38

ASSESSORPaul D.

Petersen

Type Market Sub Mkt AdjustmentRetail All -10%Medical All -35%Offi ce All -40%Remaining Cost All -30%

Questions

• Questions asked and emailed will be available on the website:

mcassessor.maricopa.gov/category/news

Thank you.

ASSESSORPaul D.

Petersen