Wealthy and Wise ® by InsMark Technology Based Stress-Testing of Wealth Transfer Strategies

69

Wealthy and Wise ® by InsMark Technology Based Stress- Testing of Wealth Transfer Strategies

-

Upload

bryson-rasey -

Category

Documents

-

view

219 -

download

0

Transcript of Wealthy and Wise ® by InsMark Technology Based Stress-Testing of Wealth Transfer Strategies

Wealthy and Wise®

byInsMark

Technology Based Stress-Testing of Wealth Transfer Strategies

Examples and case studies are for illustration purposes. Actual results may vary. Legal and tax information is for general use only and may not be applicable to specific circumstances. Clients should consult their own legal, tax and accounting advisors to assist in the evaluation of any potential transaction or strategy.

Circular 230 Disclosure: To ensure compliance with requirements imposed by the IRS under Circular 230, any U.S. Federal tax advice or information contained in this communication, unless otherwise specifically stated, is not intended or written to be used, and cannot be used, for the purpose of (1) avoiding penalties under the Internal Revenue Code or (2) promoting, marketing or recommending to another party any matters addressed herein.

Important Notice

An effective wealth planning program must address the following core subject:

Real wealth involves sustainable Cash Flow, and most people are more concerned with running out of money than any other financial issue.

Focus of This Presentation

An effective wealth planning program must:

Focus of This Presentation

A. Include the financial impact of a client’s required after tax Cash Flow in the analysis (including a factor for inflation);

B. Calculate the most efficient distribution from liquid assets to produce the required Cash Flow;

C. Convert illiquid assets to liquid assets at any time a shortfall of required Cash Flow exists;

D. Calculate Net Worth using realistic asset-by-asset client assumptions;

An effective wealth planning program must also:

Focus of This Presentation

E. Provide a client-approved comfort zone of residual Net Worth in all years;

F. Illustrate revisions to the assets to improve Cash Flow and maximize Net Worth;

G. Integrate life insurance solutions and illustrate comparisons with no life insurance;

H. Maximize Wealth to Heirs coordinated with the most efficient pre-death Net Worth;

An effective wealth planning program must also:

Focus of This Presentation

I. Illustrate varying levels of death taxes due to the unstable nature of federal taxes;

J. Analyze all planning variations in “do-it vs. don’t-do- it” graphical comparisons;

K. Provide year-by-year numerical backup for every aspect of the analysis so that professional advisers can easily audit any aspect of it.

Each of the Case Studies in this presentation includes a life insurance component utilizing these wealth planning features.

Focus of This Presentation

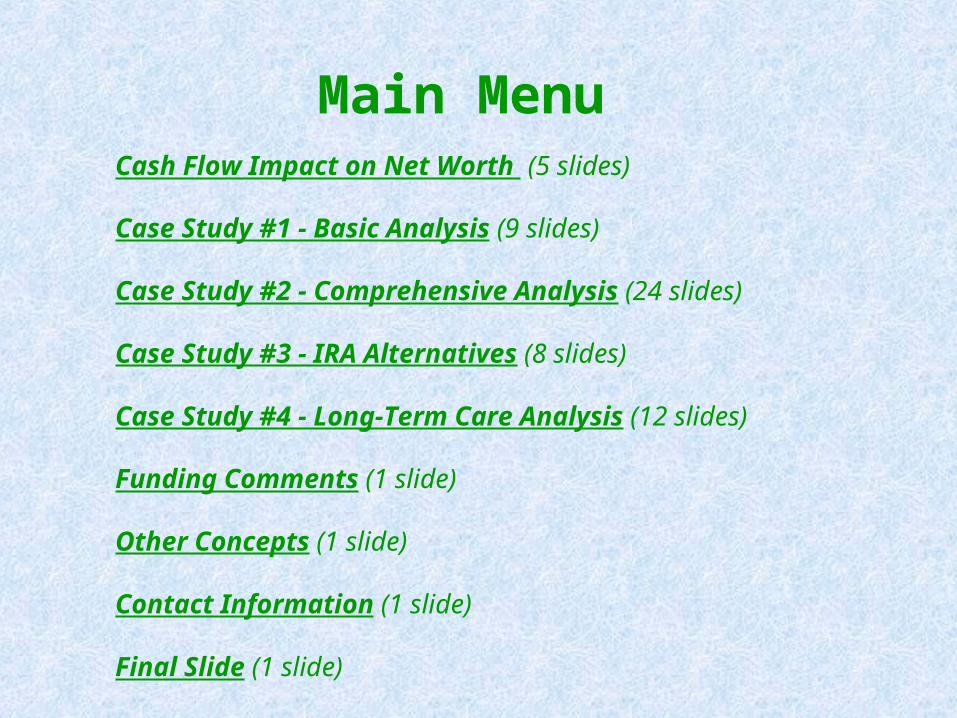

Cash Flow Impact on Net Worth (5 slides)

Main Menu

Case Study #1 - Basic Analysis (9 slides)

Case Study #2 - Comprehensive Analysis (24 slides)

Case Study #3 - IRA Alternatives (8 slides)

Case Study #4 - Long-Term Care Analysis (12 slides)

Funding Comments (1 slide)

Contact Information (1 slide)

Final Slide (1 slide)

Other Concepts (1 slide)

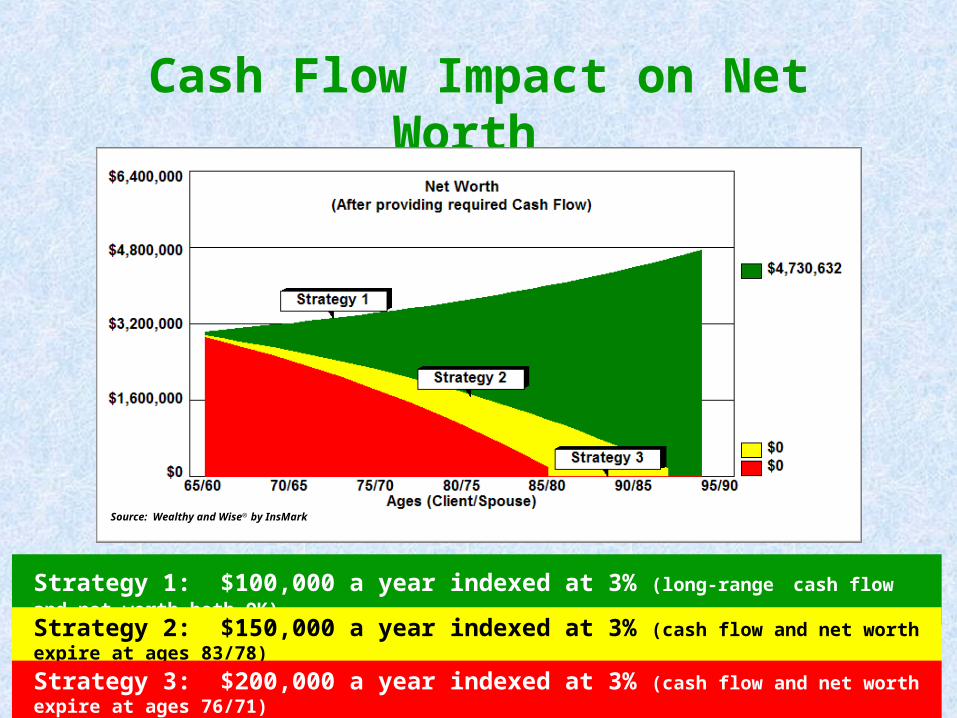

• Liquid assets available to provide retirement income: $3,000,000.

• Desired retirement income:– Strategy 1: $100,000 a year indexed at 3%;– Strategy 2: $150,000 a year indexed at 3%;– Strategy 3: $200,000 a year indexed at 3%.

• Couple, ages 65 and 60.

Cash Flow Impact on Net Worth

Strategy 1: $100,000 a year indexed at 3% (long-range cash flow and net worth both OK)

Strategy 2: $150,000 a year indexed at 3% (cash flow and net worth expire at ages 83/78)

Strategy 3: $200,000 a year indexed at 3% (cash flow and net worth expire at ages 76/71)

Cash Flow Impact on Net Worth

Source: Wealthy and Wise by InsMark

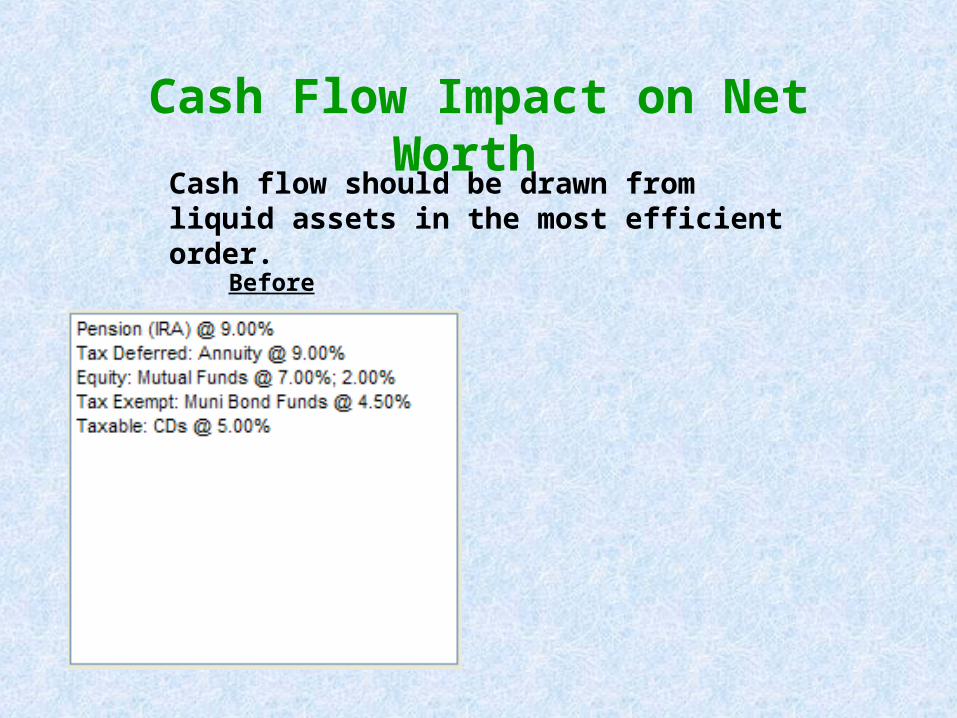

Cash flow should be drawn from liquid assets in the most efficient order.

Before

Cash Flow Impact on Net Worth

Liquid Assets should be set to produce the highest possible long-range Net Worth.

Liquid Assets should be set to produce the highest possible long-range Net Worth.

Before After

Source: Wealthy and Wise by InsMark

Cash flow should be drawn from liquid assets in the most efficient order.

Cash Flow Impact on Net Worth

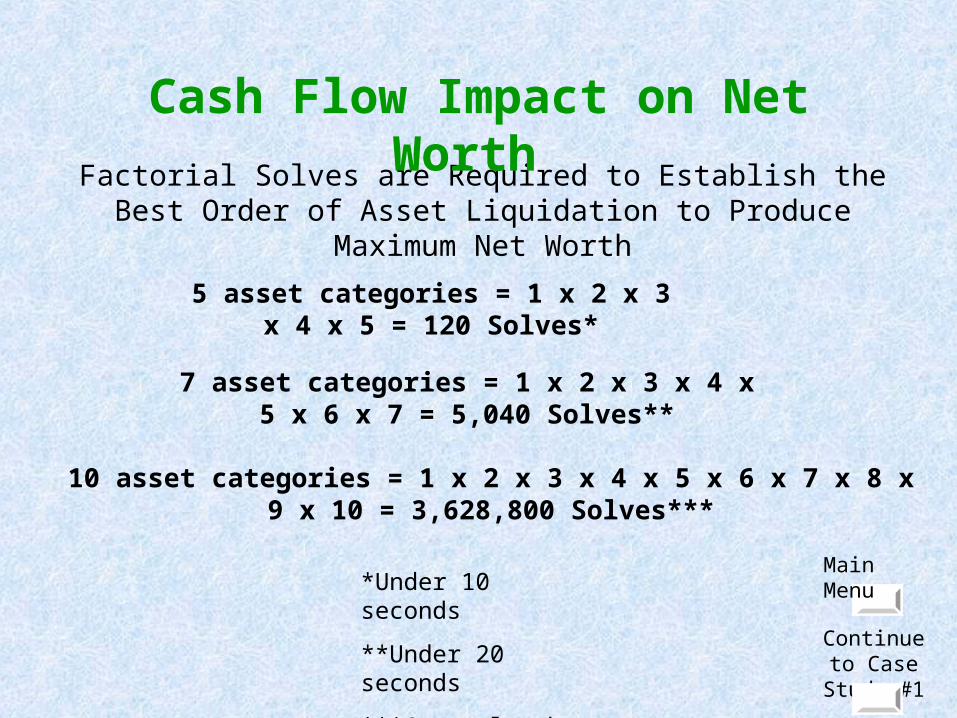

7 asset categories = 1 x 2 x 3 x 4 x 5 x 6 x 7 = 5,040 Solves**

5 asset categories = 1 x 2 x 3 x 4 x 5 = 120 Solves*

10 asset categories = 1 x 2 x 3 x 4 x 5 x 6 x 7 x 8 x 9 x 10 = 3,628,800 Solves***

*Under 10 seconds

**Under 20 seconds

***Go to lunch

Factorial Solves are Required to Establish the Best Order of Asset Liquidation to Produce Maximum Net Worth

Main Menu

Continue to Case Study #1

Cash Flow Impact on Net Worth

Their current estate is valued at close to $5.7 million.

They are both retired.

Their current financial plan has been designed to provide them with $100,000 a year in after tax retirement cash flow -- increasing by 3% a year as an inflation offset.

Richard and Elaine Masters are ages 65 and 60 -- with two grown children.

Case Study #1

Richard and Elaine are considering gifting $25,000 a year in trust to each of their two children (total $50,000).

Case Study #1

However, they are concerned about the impact of such a gift on their retirement income and residual net worth, i.e., their “comfort zone” of retained assets.

They also want to determine what would be the most effective use of the gift – an equity account or life insurance.

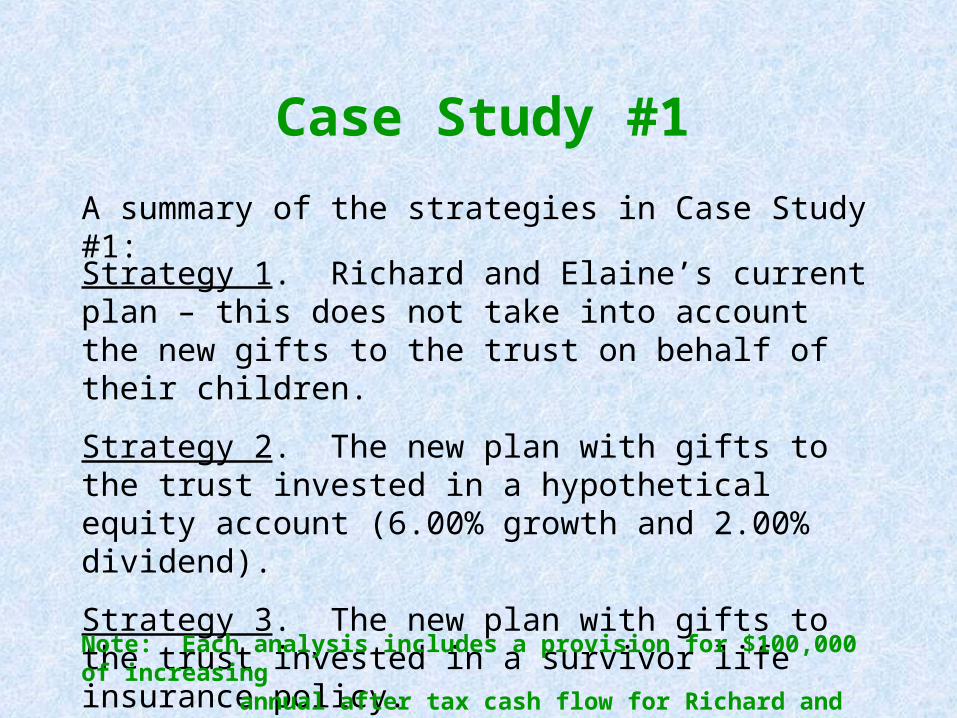

A summary of the strategies in Case Study #1:

Case Study #1

Strategy 1. Richard and Elaine’s current plan – this does not take into account the new gifts to the trust on behalf of their children.

Strategy 2. The new plan with gifts to the trust invested in a hypothetical equity account (6.00% growth and 2.00% dividend).

Strategy 3. The new plan with gifts to the trust invested in a survivor life insurance policy.

Note: Each analysis includes a provision for $100,000 of increasing annual after tax cash flow for Richard and Elaine’s retirement.

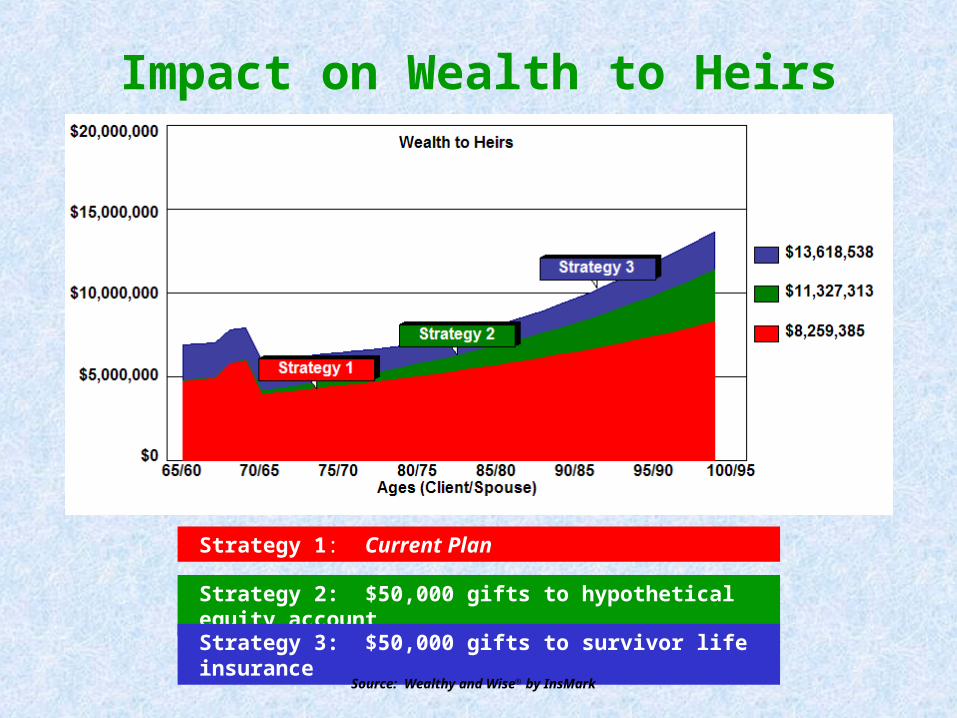

Impact on Net Worth

Strategy 1: Current Plan

Strategy 2: $50,000 gifts to hypothetical equity account

Strategy 3: $50,000 gifts to survivor life insurance

Source: Wealthy and Wise by InsMark

Strategy 1: Current Plan

Strategy 2: $50,000 gifts to hypothetical equity account

Strategy 3: $50,000 gifts to survivor life insurance

Impact on Wealth to Heirs

Source: Wealthy and Wise by InsMark

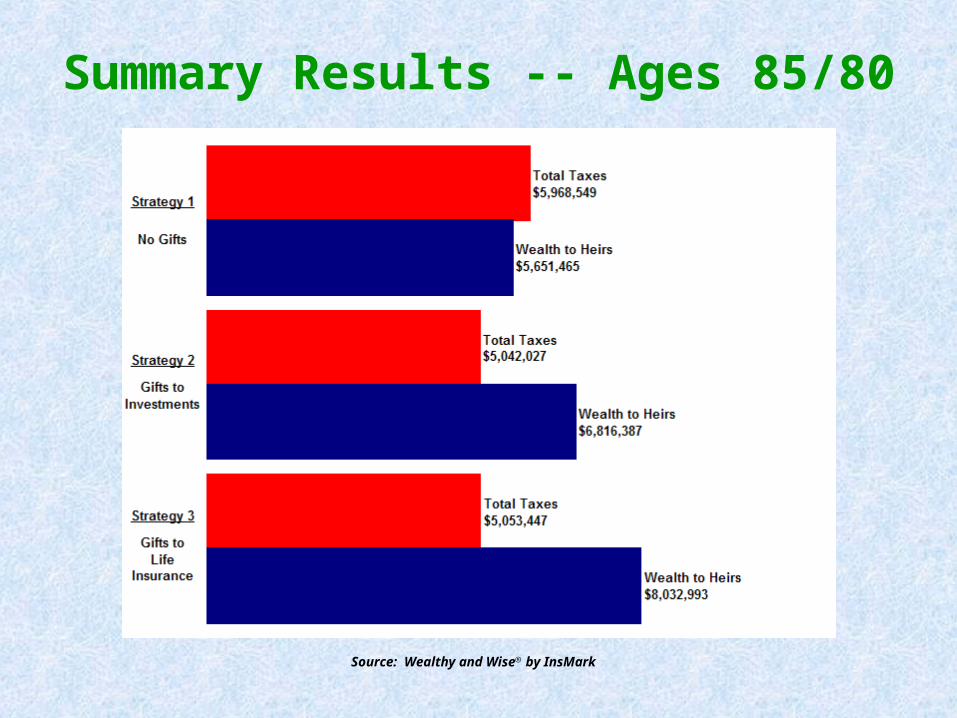

Summary Results -- Ages 85/80

Source: Wealthy and Wise by InsMark

Summary Results -- Ages 100/95

Source: Wealthy and Wise by InsMark

Case Study #1Conclusion

Since the source of the funding for the $50,000 annual gift is their capital not their income, Richard and Elaine’s retirement income cash flow is unaffected by the transaction.

Consequently, it is likely that they will consider the long-range decrease in net worth well worth the significant increase in wealth to heirs -- and the life insurance policy appears to be the preferred funding instrument.

Main Menu

Continue to Case Study #2

Case Study #2 illustrates a wealth preservation strategy that includes a charitable component.

Case Study #2

Their current estate is valued at close to $4.3 million.

They plan to retire in five years.

Their current financial plan has been designed to provide them with $150,000 a year in after tax retirement cash flow -- increasing by 3% a year as an inflation offset.

Ken and Jennifer Hudson are in their mid-fifties with three grown children.

Case Study #2

IRS

There are three possible beneficiaries of an estate:

With proper planning, you get to pick two!

Family Charity

IRS

If given the choice . . .

Family Charity

With proper planning, you get to pick two!

Let’s examine this in context . . .

Family IRS

Most people decide this way . . .

Charity

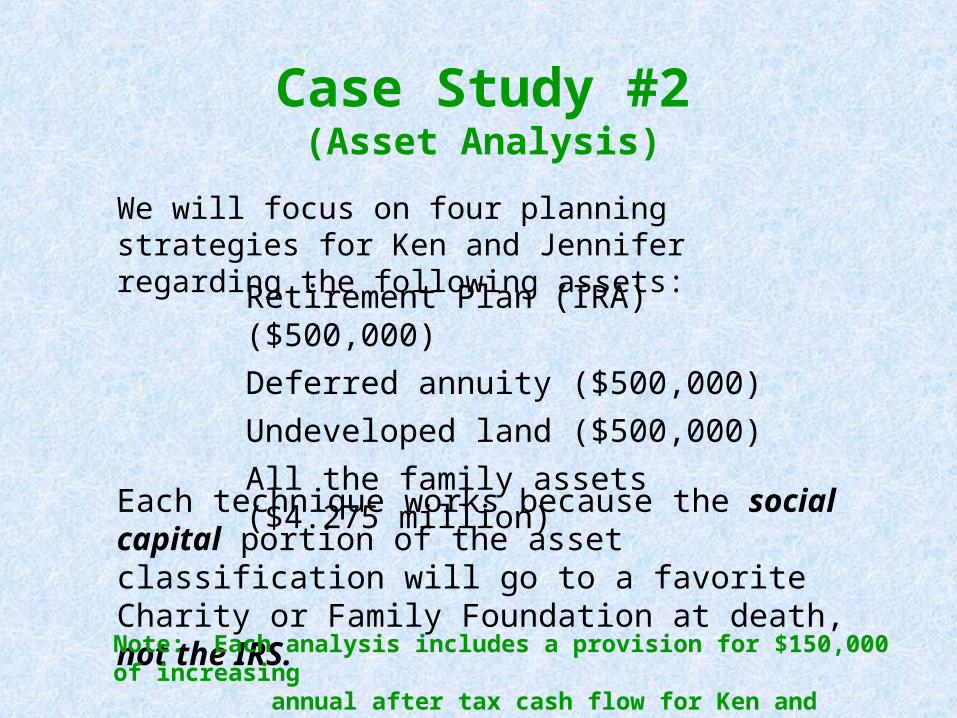

Retirement Plan (IRA) ($500,000)

Deferred annuity ($500,000)

Undeveloped land ($500,000)

All the family assets ($4.275 million)

We will focus on four planning strategies for Ken and Jennifer regarding the following assets:

Each technique works because the social capital portion of the asset classification will go to a favorite Charity or Family Foundation at death, not the IRS.

Case Study #2(Asset Analysis)

Note: Each analysis includes a provision for $150,000 of increasing annual after tax cash flow for Ken and Jennifer’s retirement.

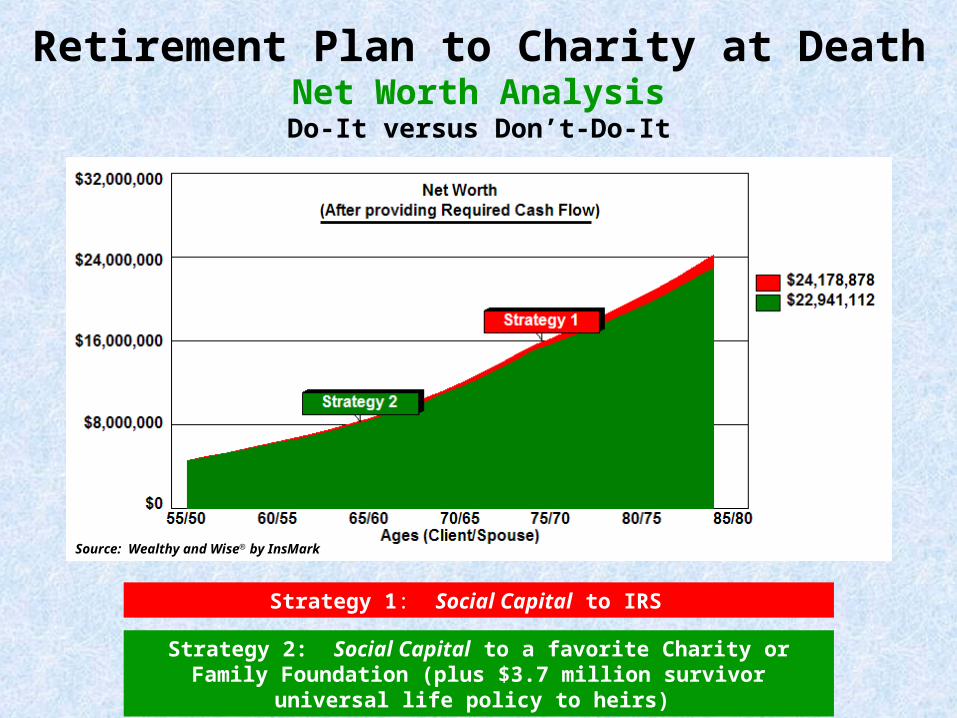

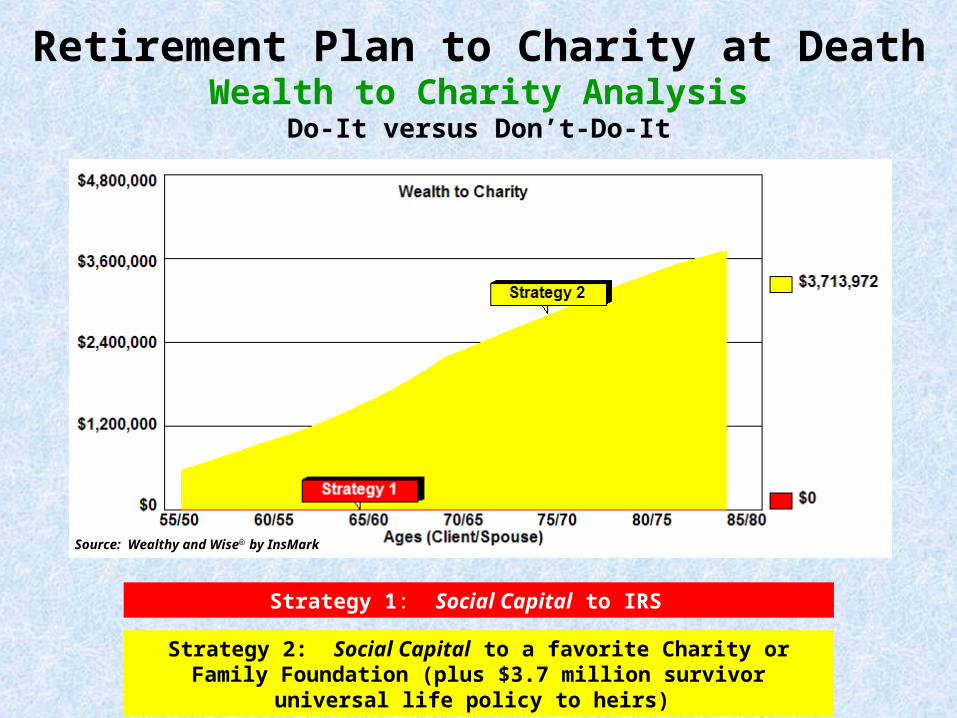

Strategy 1: Social Capital to IRS

Strategy 2: Social Capital to a favorite Charity or Family Foundation (plus $3.7 million survivor universal life policy to heirs)

Retirement Plan to Charity at DeathNet Worth AnalysisDo-It versus Don’t-Do-It

Source: Wealthy and Wise by InsMark

Strategy 1: Social Capital to IRS

Strategy 2: Social Capital to a favorite Charity or Family Foundation (plus $3.7 million survivor universal life policy to heirs)

Retirement Plan to Charity at DeathWealth to Heirs Analysis

Do-It versus Don’t-Do-It

Source: Wealthy and Wise by InsMark

Strategy 1: Social Capital to IRS

Strategy 2: Social Capital to a favorite Charity or Family Foundation (plus $3.7 million survivor universal life policy to heirs)

Retirement Plan to Charity at DeathWealth to Charity Analysis

Do-It versus Don’t-Do-It

Source: Wealthy and Wise by InsMark

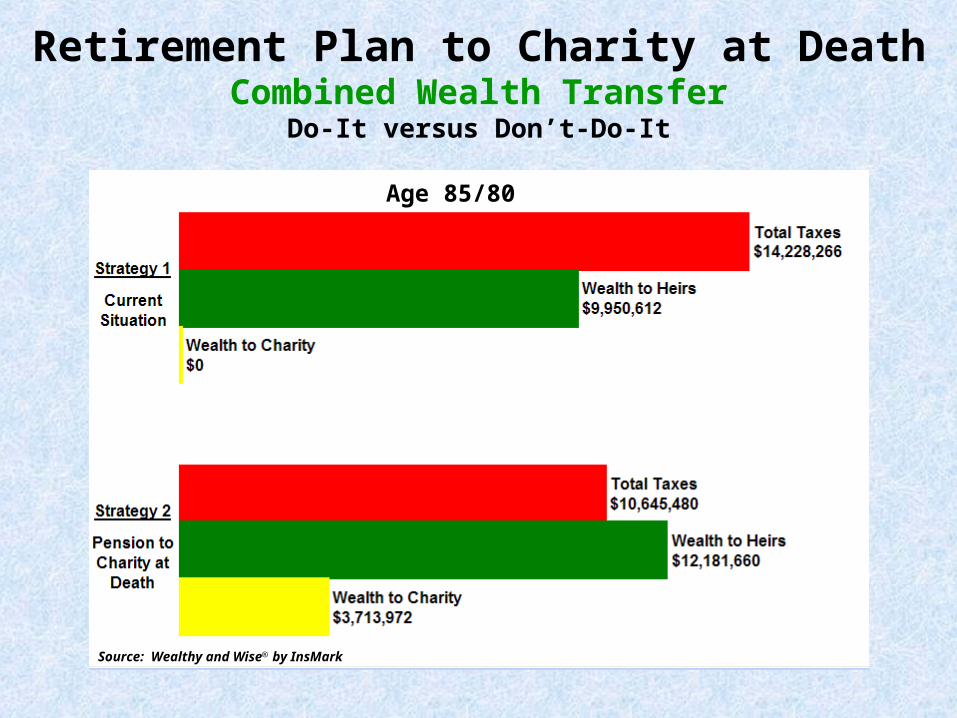

Retirement Plan to Charity at DeathCombined Wealth Transfer

Do-It versus Don’t-Do-It

Source: Wealthy and Wise by InsMark

Age 85/80

Strategy 1: Social Capital to IRS

Strategy 3: Social Capital to a favorite Charity or Family Foundation (plus $5.2 million survivor universal life policy to heirs)

Deferred Annuity to Charity at DeathNet Worth AnalysisDo-It versus Don’t-Do-It

Source: Wealthy and Wise by InsMark

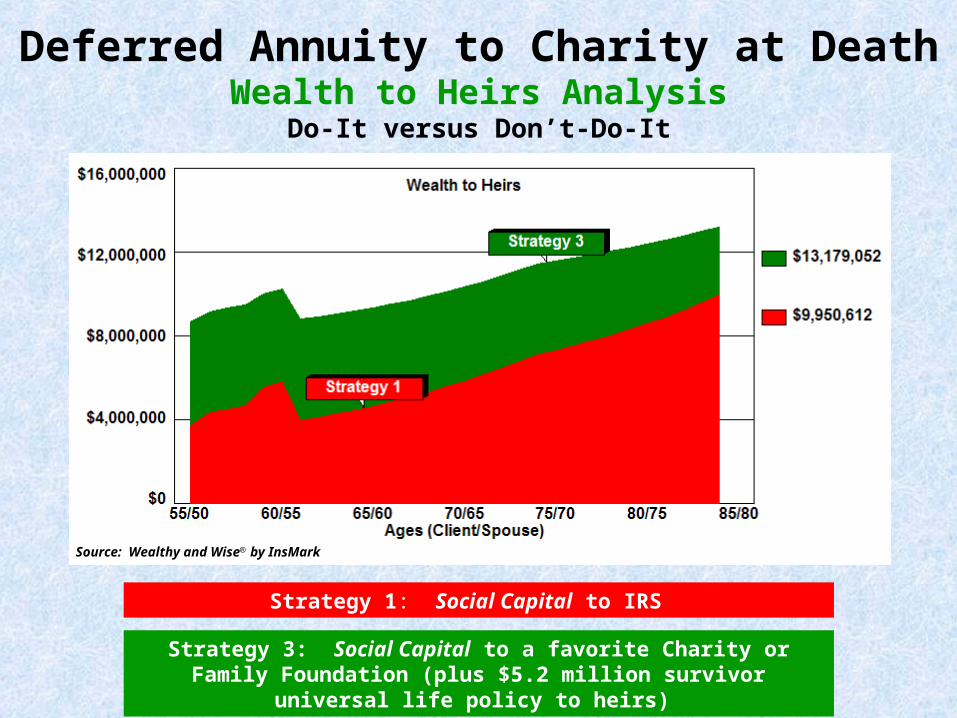

Strategy 1: Social Capital to IRS

Strategy 3: Social Capital to a favorite Charity or Family Foundation (plus $5.2 million survivor universal life policy to heirs)

Source: Wealthy and Wise by InsMark

Deferred Annuity to Charity at DeathWealth to Heirs Analysis

Do-It versus Don’t-Do-It

Strategy 1: Social Capital to IRS

Strategy 3: Social Capital to a favorite Charity or Family Foundation (plus $5.2 million survivor universal life policy to heirs)

Source: Wealthy and Wise by InsMark

Deferred Annuity to Charity at DeathWealth to Charity Analysis

Do-It versus Don’t-Do-It

Deferred Annuity to Charity at DeathCombined Wealth Transfer

Do-It versus Don’t-Do-It

Source: Wealthy and Wise by InsMark

Age 85/80

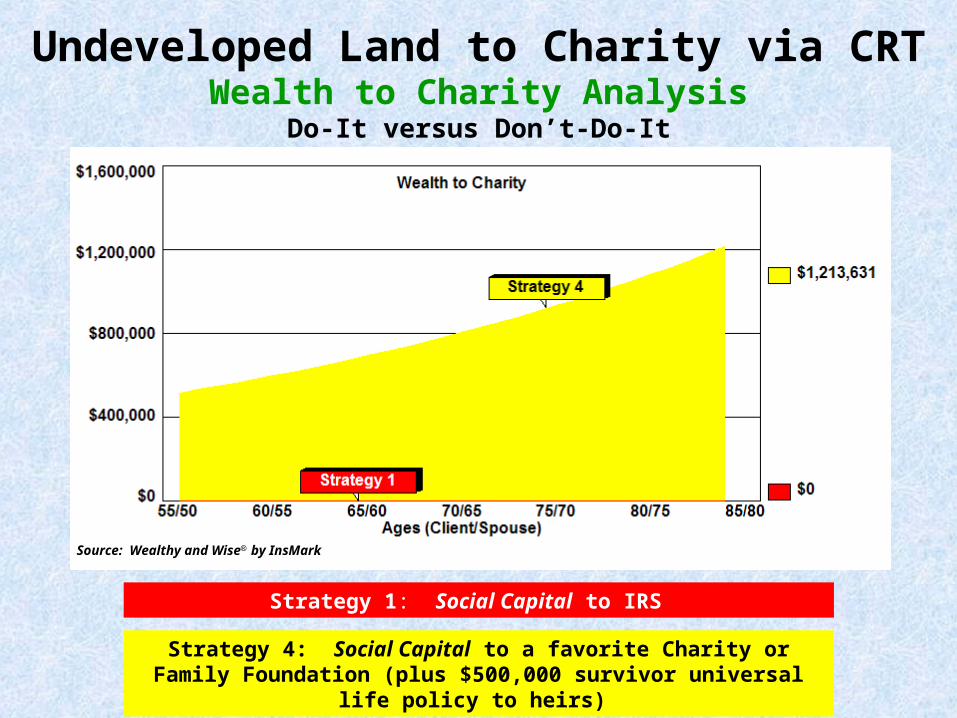

Strategy 1: Social Capital to IRS

Strategy 4: Social Capital to a favorite Charity or Family Foundation (plus $500,000 survivor universal life policy to heirs)

Undeveloped Land to Charity via CRTNet Worth AnalysisDo-It versus Don’t-Do-It

Source: Wealthy and Wise by InsMark

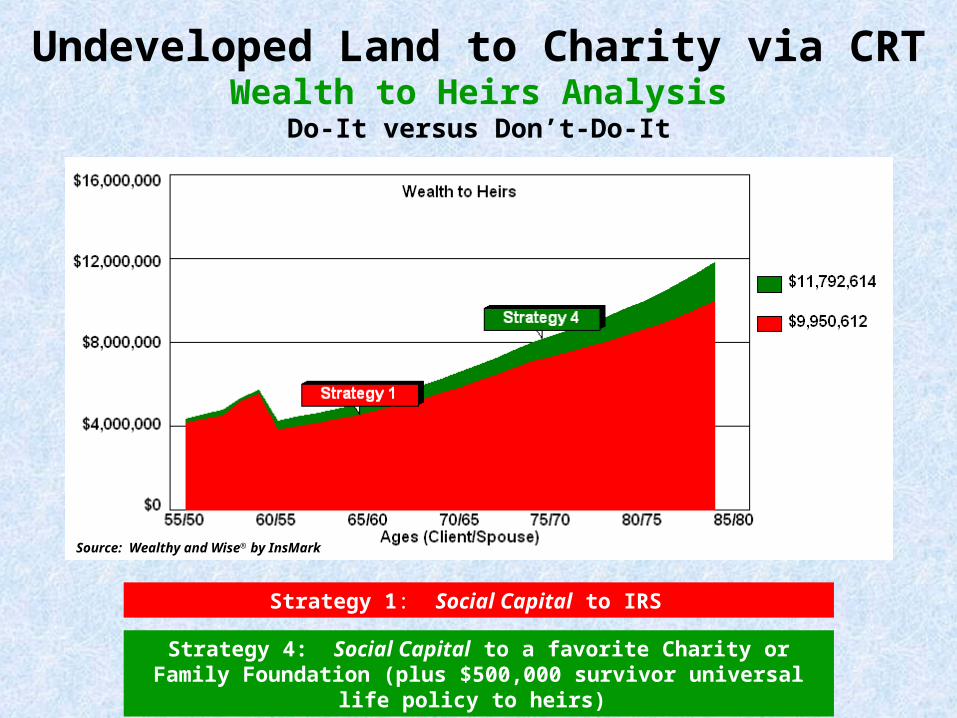

Strategy 1: Social Capital to IRS

Strategy 4: Social Capital to a favorite Charity or Family Foundation (plus $500,000 survivor universal life policy to heirs)

Undeveloped Land to Charity via CRTWealth to Heirs Analysis

Do-It versus Don’t-Do-It

Source: Wealthy and Wise by InsMark

Strategy 1: Social Capital to IRS

Strategy 4: Social Capital to a favorite Charity or Family Foundation (plus $500,000 survivor universal life policy to heirs)

Source: Wealthy and Wise by InsMark

Undeveloped Land to Charity via CRTWealth to Charity Analysis

Do-It versus Don’t-Do-It

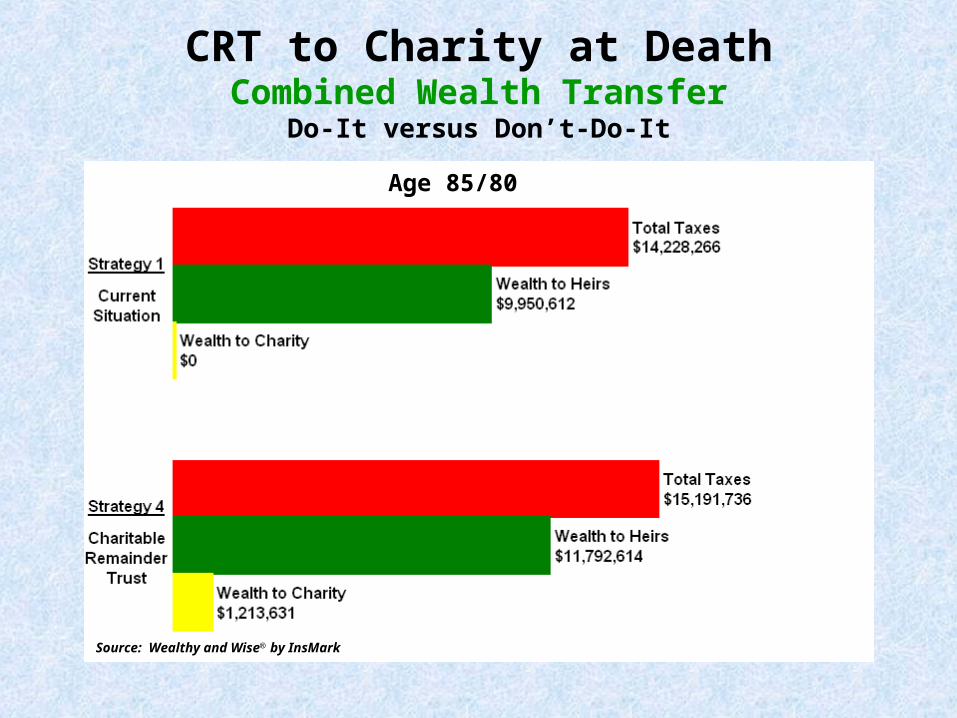

CRT to Charity at DeathCombined Wealth Transfer

Do-It versus Don’t-Do-It

Source: Wealthy and Wise by InsMark

Age 85/80

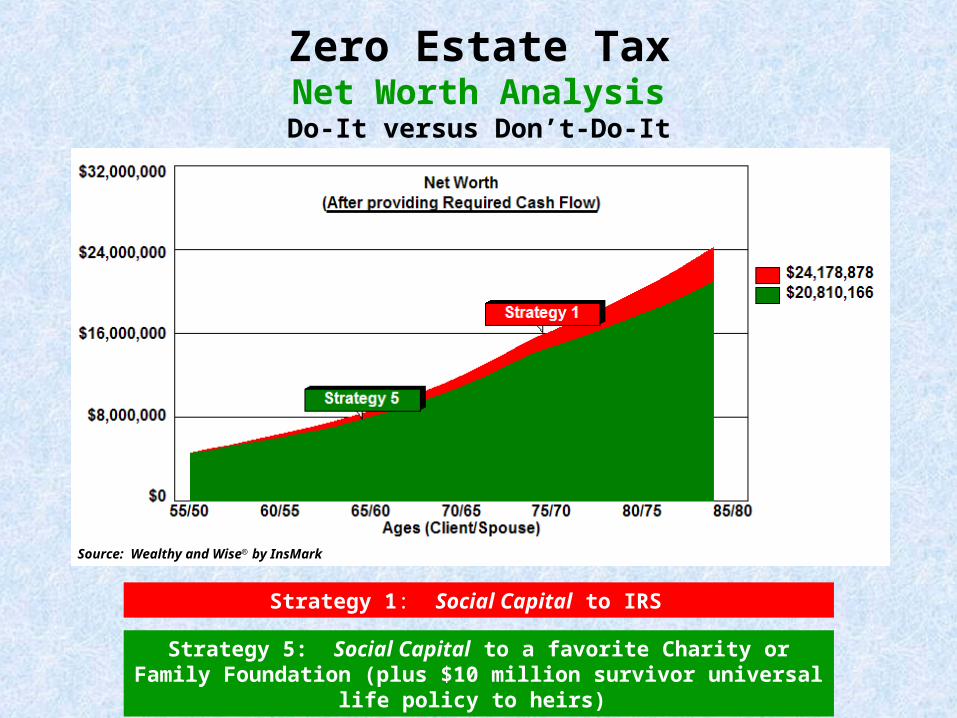

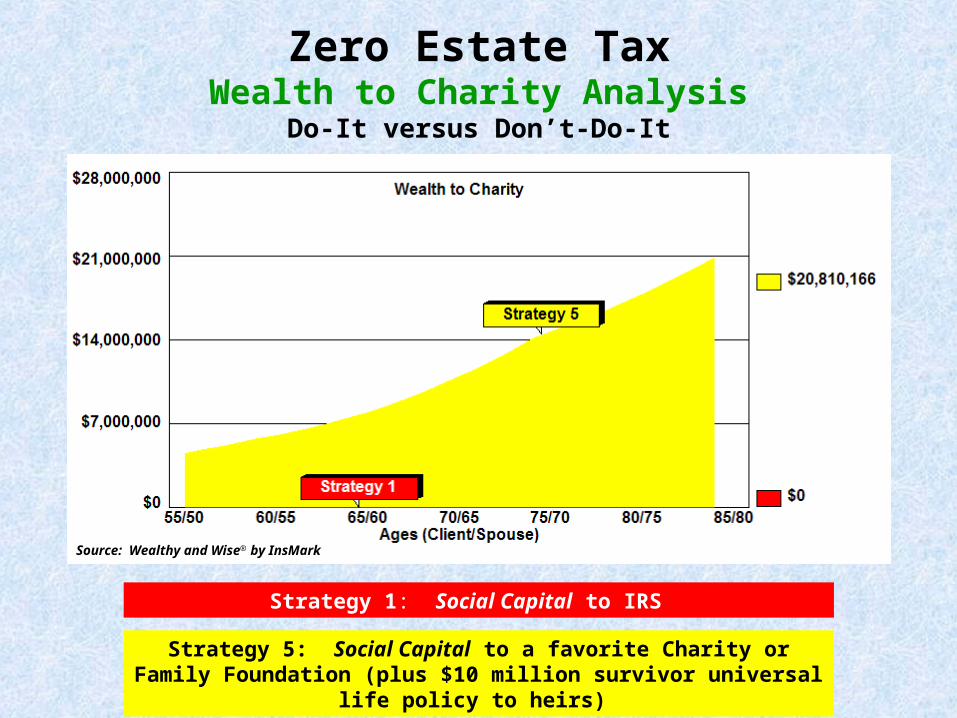

Strategy 1: Social Capital to IRS

Strategy 5: Social Capital to a favorite Charity or Family Foundation (plus $10 million survivor universal life policy to heirs)

Zero Estate TaxNet Worth AnalysisDo-It versus Don’t-Do-It

Source: Wealthy and Wise by InsMark

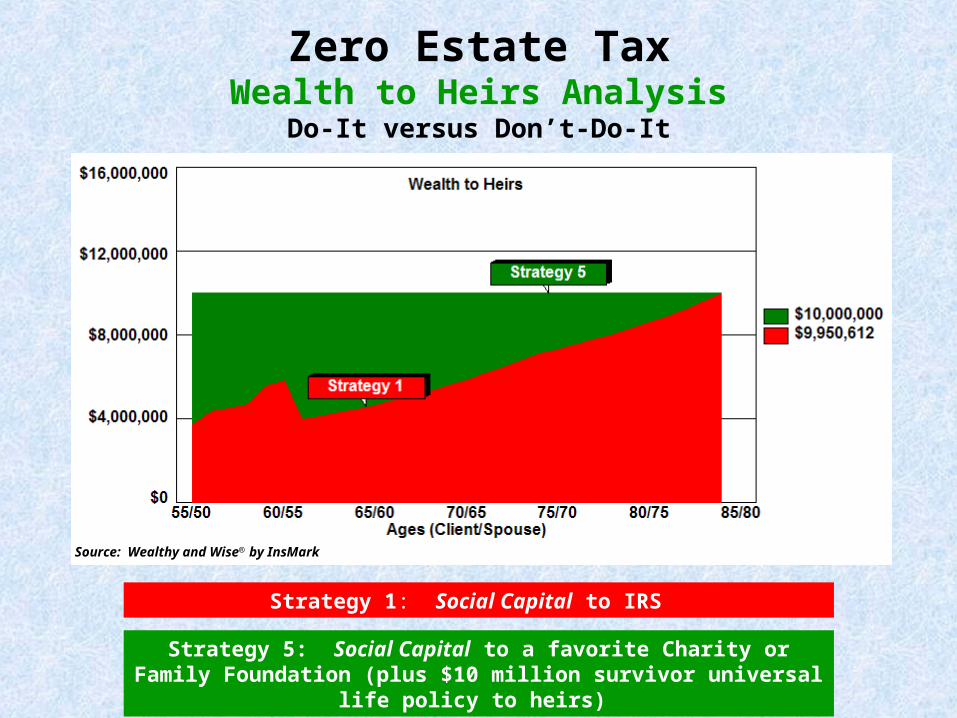

Strategy 1: Social Capital to IRS

Strategy 5: Social Capital to a favorite Charity or Family Foundation (plus $10 million survivor universal life policy to heirs)

Source: Wealthy and Wise by InsMark

Zero Estate TaxWealth to Heirs Analysis

Do-It versus Don’t-Do-It

Strategy 1: Social Capital to IRS

Strategy 5: Social Capital to a favorite Charity or Family Foundation (plus $10 million survivor universal life policy to heirs)

Source: Wealthy and Wise by InsMark

Zero Estate TaxWealth to Charity Analysis

Do-It versus Don’t-Do-It

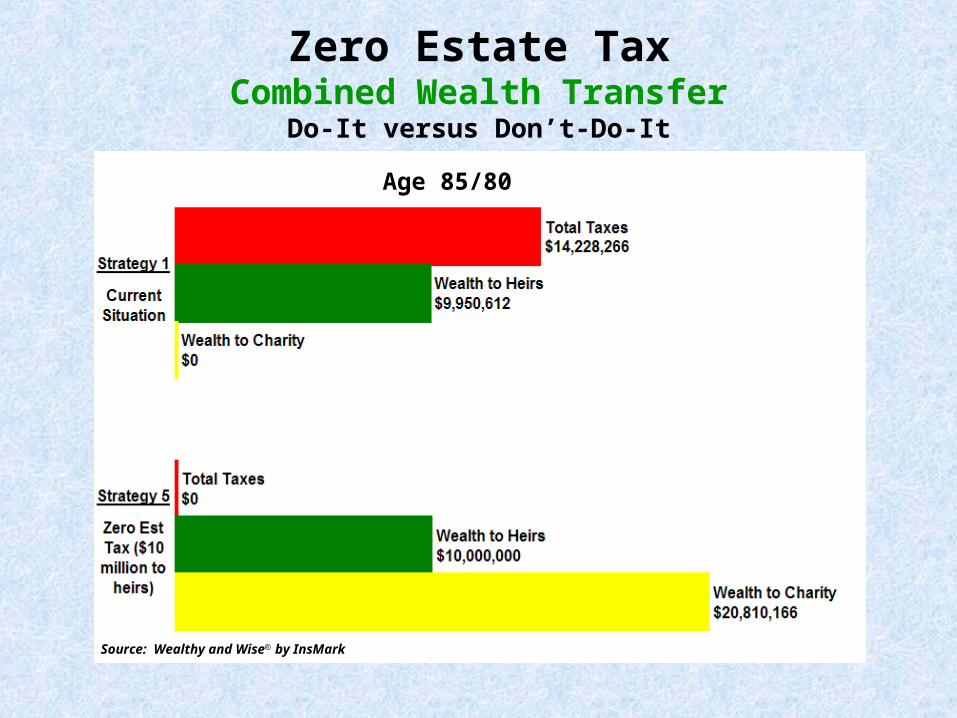

Zero Estate TaxCombined Wealth Transfer

Do-It versus Don’t-Do-It

Source: Wealthy and Wise by InsMark

Age 85/80

*If enacted, the Charitable Remainder Trust is a “done deal”.

All money to charity from the retirement plan, annuity, and zero estate tax strategies is via a revocable charitable beneficiary designation or a testamentary bequest.*

Flexibility

Therefore, these assets remain an active part of Net Worth until death -- and are freely available to Ken and Jennifer during their lifetimes.

Should Ken and Jennifer wish to change their minds, they may do so at any time.

To give you a thorough understanding of all the details available in the individual reports from a Wealthy and Wise analysis, click here to review the 52 pages associated with Strategy 1 (Current Situation) versus Strategy 5 (Zero Estate Tax Plan).

Illustration Resource

Case Study #3What About a Stretch-Out IRA?

Which hand do you want to play?

Stretch-Out IRACharitable IRA

Good as the stretch-out approach is, it is second best to the charitable strategy.

Very few people know this -- but those who do have a very significant planning edge.

Using Ken Hudson’s $500,000 IRA as an example, let’s review a wealth preservation analysis that compares a stretch-out IRA to a charitable IRA.

Case Study #3What About a Stretch-Out IRA?

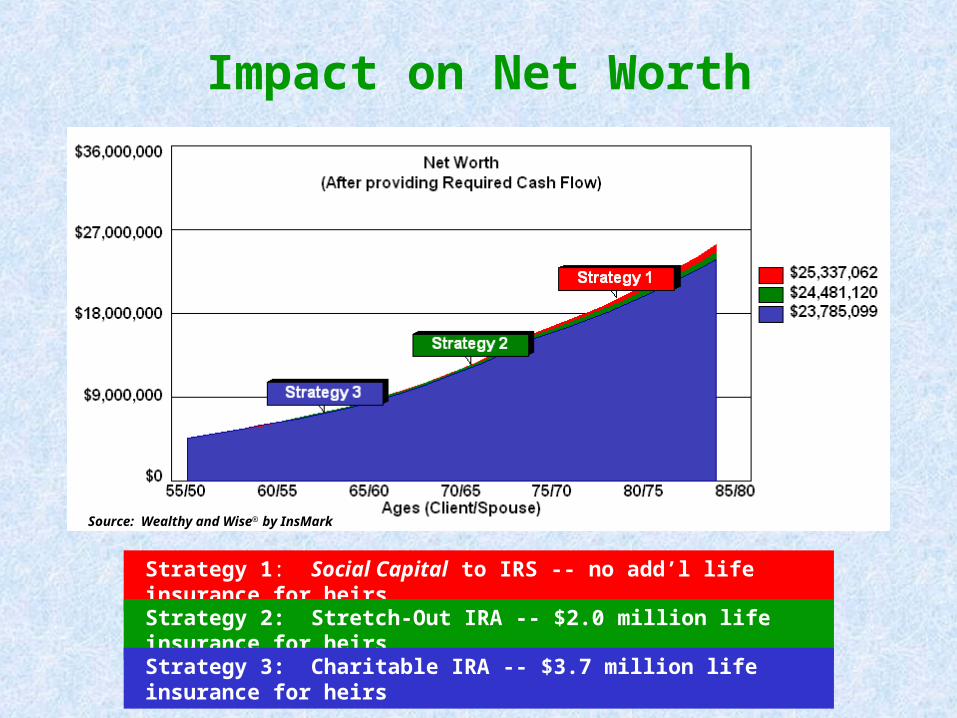

Impact on Net Worth

Source: Wealthy and Wise by InsMark

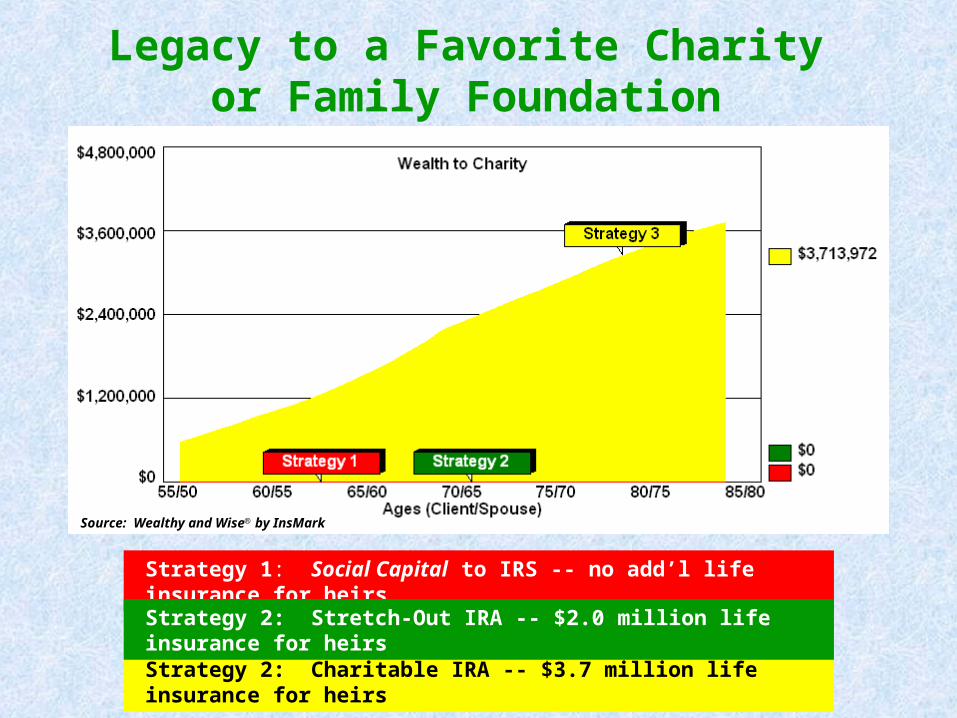

Strategy 1: Social Capital to IRS -- no add’l life insurance for heirs

Strategy 2: Stretch-Out IRA -- $2.0 million life insurance for heirs

Strategy 3: Charitable IRA -- $3.7 million life insurance for heirs

Source: Wealthy and Wise by InsMark

Impact on Wealth to Heirs

Strategy 1: Social Capital to IRS -- no add’l life insurance for heirs

Strategy 2: Stretch-Out IRA -- $2.0 million life insurance for heirs

Strategy 3: Charitable IRA -- $3.7 million life insurance for heirs

Legacy to a Favorite Charity or Family Foundation

Source: Wealthy and Wise by InsMark

Strategy 2: Charitable IRA -- $3.7 million life insurance for heirs

Strategy 1: Social Capital to IRS -- no add’l life insurance for heirs

Strategy 2: Stretch-Out IRA -- $2.0 million life insurance for heirs

The major difference between charitable and stretch-out is the quality of the inherited capital.

*

Source: Wealthy and Wise by InsMark

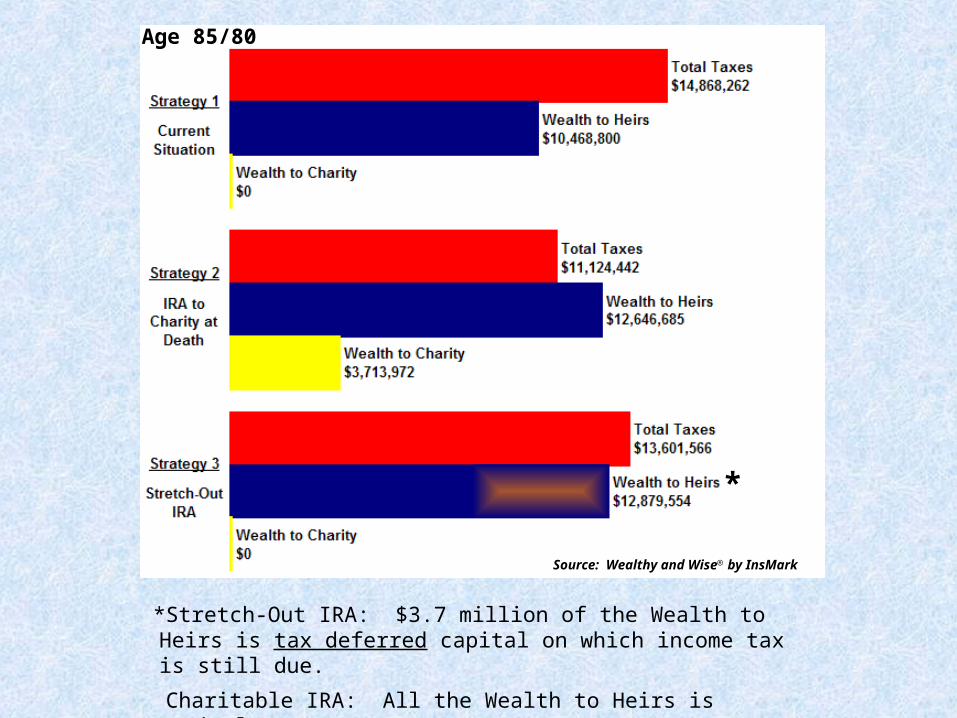

Age 85/80

*Stretch-Out IRA: $3.7 million of the Wealth to Heirs is tax deferred capital on which income tax is still due.

Charitable IRA: All the Wealth to Heirs is capital.

Case Study #3Conclusion

The edge clearly goes to the charitable IRA approach (backed up by the life insurance).

Main Menu

Continue to Case Study #4

They have a current Net Worth of $3.5 million and question whether it is better to self-insure this risk – should it occur.

John and Fran Sandor are ages 65 and 60.

The Sandors’ financial adviser has recommended they acquire a Long-Term Care policy.

Case Study #4Long-Term Care – Insure or Self-Insure

Should the Sandors purchase the Long-Term Care policy or is their Net Worth sufficient to self-insure the potential risk?

Let’s examine the mathematics . . .

Case Study #4Long-Term Care – Insure or Self-Insure

• Assume a claim occurs in 8 years that lasts for 6 years.

Analysis

• Assume the total daily benefits for the claim on a monthly basis will be $6,000 in today’s dollars -- and medical inflation averages 5% a year.

• Assume the annual premium for a Long-Term Care policy covering both John and Fran is $8,600 -- reducing to $4,300 during the claim period.

• Assume an inflation rider increases total monthly benefits by 5% (compounded) a year.

• Assume retirement cash flow needs decline by 25% during the claim period.

An evaluation of alternatives follows . . .

• Retirement cash flow must be unaffected by the transaction.

A Cash Flow Neutral Analysis

• This means the source of the Long-Term Care claims or premiums must be John and Fran’s asset base, not a reduction in their spendable income.

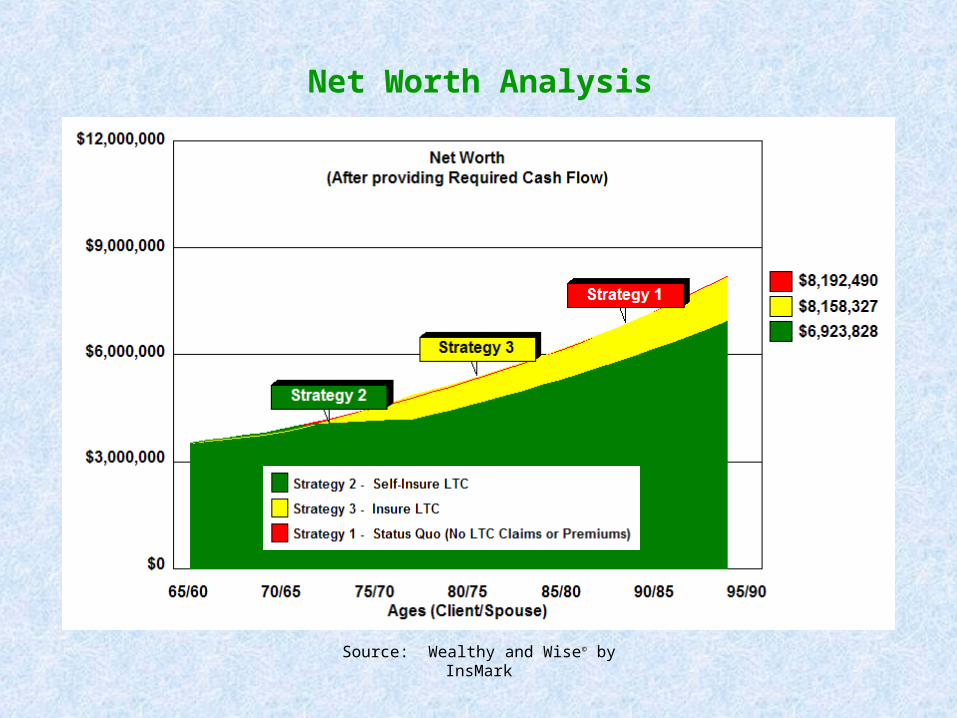

Net Worth Analysis

Source: Wealthy and Wise© by InsMark

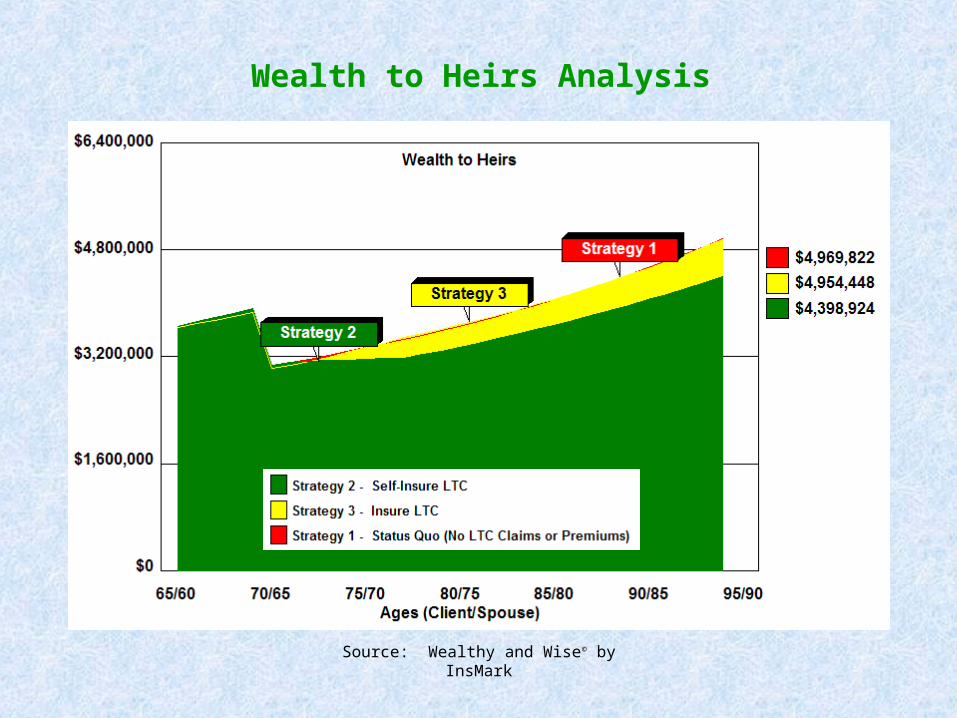

Wealth to Heirs Analysis

Source: Wealthy and Wise© by InsMark

Given the assumptions, John and Fran should seriously consider acquiring the Long-Term Care policy as it is not worth assuming the risk inherent in self-insuring.

Case Study #4Conclusion #1

Is there a way to improve further the wealth transferred to heirs?

Let’s include a Wealth Replacement Trust funded with $2,500,000 of survivorship life insurance ($25,000 annual premium).

Case Study #4Query

Strategy 1: Status Quo (no Long-Term Care claims or premiums)

Strategy 3: Insure LTC

Strategy 4: Insure LTC + $2,500,000 life insurance in a Wealth Replacement Trust

The self-insured approach (Strategy 2) is not a desirable option, so our comparison will evaluate the following three alternatives:

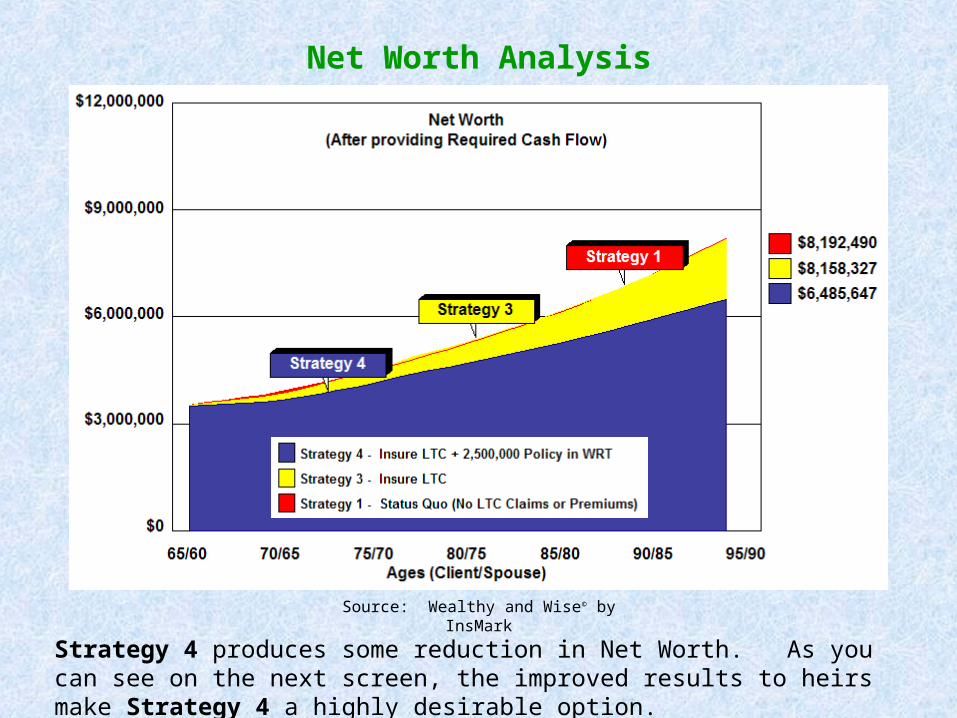

Strategy 4 produces some reduction in Net Worth. As you can see on the next screen, the improved results to heirs make Strategy 4 a highly desirable option.

Net Worth Analysis

Source: Wealthy and Wise© by InsMark

Strategy 4 produces superior results in Wealth to Heirs.

Wealth to Heirs

Source: Wealthy and Wise© by InsMark

Given the assumptions, John and Fran should seriously consider acquiring the both the Long-Term Care policy and the Wealth Replacement Trust funded with life insurance.

Case Study #4Conclusion #2

Main Menu

Continue to Funding Comments

All the graphics for Net Worth and Wealth to Heirs and/or Charity reflect assets after the funding has been accounted for, and spendable cash flow for retirement income is calculated to be the same whether or not the participants take advantage of any of the protection strategies suggested.

One of the conditions for each of the evaluations in this presentation requires that spendable cash flow for planned retirement income should be unaffected by the transactions, and this has been confirmed during each step of each analysis.

Funding Comments

Main Menu

Continue to Other Concepts

Just A Few of the Many Other Concepts That Can Be Illustrated in Wealthy and Wise Using “Do it” vs. “Don’t do it”

ComparisonsPension Rescue (in or out of the estate)

Arbitrage Uses of Single Premium Immediate Annuities

Downsize or Upsize Home (or Refinance)

Family Limited Partnership

Additional Insurance Inside the Estate (the LEAP approach)

The Overall Economics of Gifts to Heirs

Private Ltd. Collateral Assignment Split Dollar

Loan-Based Private Split Dollar

Annuity Rescue (in or out of the estate)

Continue to Contact Information

Main Menu

Other Concepts

Institutional inquiries: David A. Grant, Senior Vice President, Sales.925-543-0513 or [email protected].

Individual Inquiries: 1-888-InsMark (467-6275) or [email protected].

Or visit our website at www.insmark.com.

Contact Information

Continue to Final Slide

Main Menu

Copyright 2006, InsMark, Inc. All Rights Reserved

“Wealthy and Wise” and “InsMark” are registered trademarks of InsMark, Inc. InsMark, Inc. owns the copyright to the leverage logo. It is not licensed for re-use without the express written permission of InsMark, Inc.

Wealthy and Wiseby

InsMark

End PresentationMain Menu